Embed Size (px)

Citation preview

Prepayment Risk- andOption-Adjusted Valuation of MBSopportunities for arbitrai^e.

Alexander Levin and Andrew Davidson

ALEXANDER LEVIN is head

ot Valuation i^cvclopment atAndrew Davidson &: Co.,Inc., in New York [email protected]

ANDREW DAVIDSON IS the

president and founder ofAndrew Davidson & Co., [email protected]

SUMMKR 2005

Option-adjusted spread (OAS), while a muchbetter measure than yield or static spread,still tails short in explaining the dynamics ofmortgage pricing. The standard OAS typ-

ically varies across instruments {pass-throughs, collater-alized mortgage obligations, interest-only securities,principal-only securities), coupons, prepayment optionmoneyness, and pool seasoning stages.

Premium and discount MBS are often priced atwider OAS than the current-coupon issues. PremiumMBS and lOs stripped oft premium pools are consideredhazardous, and their higher OAS reflect concerns ofunderstated refinancing. Naturally, the respective POslook rich. In the discount sector, higher OAS reflects therisk associated with possible overstatement of the hous-ing turnover rate.

Clearly, these market phenomena defeat the verypurpose ofa constant OAS approach. Rich-cheap judg-ments become inconclusive, and rate shock analysis canproduce inaccurate hedge ratios.'

Like Cheyette [1996] and Cohler, Feldman, andLancaster [1997], we attribute the OAS and its variabil-ity to the prepayment risk premium, i.e., possible non-diversifiable deviations of actual future prepayments fix)ma best guess prepay model's forecast.

It is the market's fear of systematic bias in prepay-ment forecasts that leads to a risk premium. If prepaymentswere perfectly predictable, then an exact, even inefficient,option exercise model should produce a zero OAS to anappropriate option-trf e benchmark, just as options and

THE JOURNAL OF PORTFOHO MANAGEMENT 7 3

embedded option instruments with known algorithms ofexercise such as swaptions, callable agency debt, and cor-porate bonds are all priced flat to their respective option-free rate curves.

While OAS varies widely among instruments, ournew spread measure, called prepayment risk- and option-adjusted spread (prOAS, pronounced pro-A-S), accounts forboth option and prepayment risk. We posit that, on aprOAS basis, all liquid agency MBS should he priced flatto agency debentures, eliminating the variability found intraditional OAS measures. Our method has its roots in thecapital asset pricing model (CAPM) and its extension, arbi-trage pricing theory (APT), where return compensationfor risk and the concept of equivalent risk-neutrality playkey roles.

For unstructured pass-throughs, we propose a prOASvaluation model that is armed with the power of back-ward induction and allows for endogenously finding riskmeasures and prices reflecting embedded prepay uncer-tainty^—in the form of return spread compensation—computed for each investment period and level of inter-est rates. All the required prices and risk spreads can befound concurrently in the course of valuation performedbackward on a probability tree or a fmite-difference grid.

A price obtained in this manner will reflect the dif-ferences in prepayment uncertainty without the need tovary OAS across instruments. Values of IOs, POs, andmortgage servicing rights (MSR) can be objectivelyderived without knowing the OAS level for each instru-ment; if necessary, traditional OAS can later be calculatedfrom the resulting prices.

We prove that this process of explicit endogenous pre-pay risk accounting is mathematically equivalent to risk-neu-tral prepayment modeling. Such a model retains the structureand the features of a physical prepay model, but operates withrisk factors stressed to their undesired directions (wherevalue deteriorates). A risk-neutral prepay model easily solvesthe issue of CMO valuation under price of prepay riskimplicitly, without reliance on a non-feasible backward val-uation. Tbat is, we could refine the handling of CMOs hyreplacing the time-consuming prepayment stress testsdescribed in Cohler, Feldman, and Lancaster [1997] witbrisk-neutral forecasts.

We find that two prepayment risk factors are essen-tial: the risk of refmancing understatement, and tbe riskof turnover overstatement. Having calibrated prices ofthese two prepayment risks to a set of widely tradedMBS, we can then produce prices for all other instrumentsexposed to the same risks. Without two independent risk

factors, it would be impossible to explain why botb dis-counts and premiums of nearly all MBS collateral typesare traded at higher OAS tban non-MBS instruments. Thisparadox bas apparently puzzled some authors; see Kupiecand Kah [1999] and Gabaix, Krishnamurtby and Vigneron[2004]. A single-dimensional risk analysis would allow forhedging prepayment risk by combining premium MBSand discount MBS, a strategy any experienced traderknows would fail.

PRICING FDE FOROPTION-ADJUSTED VALUATION

We start with a hypothetical dynamic asset (mortgage)whose market price P(r, .v) depends on time f and one mar-ket factor .\'. We treat x{t) as a randotn process with a (gen-erally variable) drift rate /i and a volatility CT, disturbed bya standard Brownian motion z{t):

dx ^ + adz (1)

We assume further that tbe asset pays tbe continu-ous coupon rate c{t, x), and its balance B is amortized attbe A(f, .v) rate, so that (dB/dt) = ~XB. Then, one canprove that tbe price function P{t, x) should solve the par-tial diflx'rential equation (PDE):

r -+ OAS = — - + (c + A) - A +

dP

2Pdx- (2)

A derivation of this PDE can be found in Levin[1998], but it goes back at least to Fabozzi and Fong[1994[. If our amortizing asset is an interest-only strip (IO),the pricing equation is modified by excluding the X/Pterm in the time return expression.

A notable feature of the PDE (2) is tbe absence oftbe balance variable, JB. Tbe entire effect of possibly ran-dom prepayments is represented by the amortization ratefunction, X{t. x). Although the total cash flow observed foreach accrtial period does depend on tbe beginning-periodbalance, construction of a backward induction scheme willrequire the knowledge of A(r, x), not the balance.

Pricing PDE (2) can be solved on a probability treeor a fmite-difference grid tbat has as many dimensions asthe total number of factors or state variables r, c, and A,

74 PREi'AYMENT RiSK- AND Ol'TION-AnjUSTEH VALUATION OF MBS SUMMER 2005

or by Monte Carlo simulation. If the coupon rate is fixed,and the amorrization rate A depends only on current time{loan age) and the immediate market factor x, the entirevaluation problem can he solved backward on a two-dimensional {x, l) lattice (the lattice will require moredimension if the market factor .v is a vector).

To implement this method, we would start the val-uation process trom maturity 7'when wt* surely know thatthe price is par, P{T. x) — 1 (zero for an IO), whateverthe value of factor x. Working backward, we deduceprices at age f - 1 from prices found at age t. In doing so,we replace derivatives in PDE (2) by finite-differenceapproximations, or weigh branches of the lattice by explic-itly computed probabilities.

Even for a simple fixed-rate mortgage pass-through,though, total amortization speed A usually cannot bemodeled as a function of time and the immediate mar-ket. Prepayment burnout is a strong source of path-depen-dence because tuture refinancing activity is afiected by thepast incentives. One can think ofa mortgage pool as a het-erogeneous population of participants with different refi-nancing propensities. Some mortgagors have higher ratesor better credit or larger loans, or perhaps they face lowerregional transaction costs. Once they leave the pool,future prepayment activity gradually declines. Hence, Adepends on historical market rates, making the valuationproblem path-dependent.

Instead of considering pricing PDE (2) for the entirecollateral. Levin [2001, 2004] proposes decomposing it intotwo components, active and passive, differing in refi-nanceability. Under the active-passive decomposition(APD) model, mortgage path-dependent collateral canbe deemed a simple portfolio of two path-independentinstruments if;

• Active and passive components prepay differently,but follow immediate market rates and loan age.

• Any migration between components is prohibited.

Alternatives and variations of this modeling struc-ture include decomposition into several groups, as well asstratifying the entire pool explicitly by available loan char-acteristics (see Davidson [1987], Davidson, Herskovitz,aiidVan Drimen[1988|, Hayre |1994, 2()0{)], and Kalotay,Yang, and Fabozzi [2004]). With a decomposed collateral,it is possible to value mortgage-backed securities usingbackward induction and, as we show further, explicitlyaccount for prepayment risk.

VALUATION WITH PREPAYMENT RISK:BASIC CONCEPTS

Mortgage practitioners use the term prcpayntctu riskloosely. Most often they simply mean prepayment vari-ability, but this is not what we attempt to capture. Indeed,a large portion of prepayment uncertainty is associatedwith interest rates and is thus explained by the prepaymentmodels that are inherent in modern option-adjusted spreadanalytical systetns.

If prepayments were perfectly explained by a model,there would not be any prepayment risk premium. Anoption model coupled with an exact prepayment formulashould be ahle to deliver the right price for an agency-backed (default-protected) MBS operating with OAS =0. MBS would be valued flat to a known benchmarkcurve—similarly to swaptions or callable notes, except witha more complex exercise rule.

Savvy market participants realize that a model cantell only part of the prepayment story. Because a modelcannot predict prepayments exactly, we have unexplaineddeviations of prepayment speeds above or below the mod-el's forecast, often called prepayment surprises or prepay-ment errors. Not all prepayment surprise should requiremarket compensation. Random oscillations of actual pre-payments around the model are diversifiable over time.Prepayment errors typically seen in small pools are diver-sifiable in large pools.

We associate the notion of prepayment risk with mm-diuersifiabU' niia-nainty. common for the MBS market, sys-tematic in trend and unexplained by an otherwise best-guess prepay model. The varying level of OAS on differ-ent instruments represents compensation for this risk.

Al! the terms in pricing Equation (2) represent dif-ferent sources of return, but none of them explicitlyquantifies prepayment risk. The entire compensation forbearing this risk is hidden in the OAS term.

How would we price prepayment risk? Supposethat the prepayment rate A (r, x, i ), depends on oneuncertain variable or uncertain parameter, ^, independentof the interest rate market. For the first conceptual illus-tration, we assume ^(r) is a Wiener process with zerodrift and volatility of <7c, i.e., d^= G^dz^, and known ini-tial value, < (()). According to the CAPM/APT, the riskyreturn should be proportional to the price volatility dueto the risky factor ^. A comnion multiplier, Tie, called priceof risk, should apply to every asset exposed to the samerisk factor ^.

Using this notation, we therefore state that, for every

SUMMER 2(III5 THE JOURNAL OF PORTFOHO MANAGEMENT 7 5

investment period, the expected return, r + OAS on theleft-hand side of PDE (2), should be adjusted tor risk as:

Single-Period Expected Return —

prOAS+idP

(3)

prepay nsk ipread

where the prepay risk- and option-adjusted spread (prOAS)is a "risk-free" OAS; in the absence of any other risk fac-tors, it should be zero for a properly selected pricingbenchmark.

For example, we may assume that all agency MBSshould be valued flat to the same agency yield curve, onthis prepay risk-adjusted basis (prOAS = 0). For non-agency MBS, this should certainly account for an addi-tional risk associated with imperfect credit, and thusbecomes equal to the pure credit spread that can bederived from the S&P or Moody's rankings for a non-agency pass-through or a particular C M O tranche.

The risky spread term, unlike the traditional OAS.is not constant—it varies with interest rates and loan age.It is also directional—it can be both positive and nega-tive —depending on the sign ot price exposLire to the fac-tor < . Since the market provides a return premium torbearing the risk, it must make hedge instruments rich sothat a properly constructed i^-neutral portfolio of an assetand its hedge will earn nothing but risk-free OAS, i.e.,prOAS. This is a traditional arbitrage argument that pre-vents construction of a risk-free portfolio earning anyexcess above the risk-free return (see Hull |2000]).

VALUATION METHOD 1:ENDOGENOUS ASSESSMENT OF RISK

Factor volatility (Te and price of risk constant K^ aredefined outside the pricing model; they are common torall instruments exposed to prepay tactor ^. Let us show-how price P(/, x\ ^) and its partial derivative taken withrespect to the risk factor, dP/d^, denoted trom now onas Pc, can be estimated internally and simultaneously inthe course of backward valuation.

Suppose we have a path-independent instrument inhand that is subject to pricing Equation (2), and theamortization rate X depends on risk factor ^. Let us firstmultiply both sides of pricing Equation (2) by price P andreplace the traditional expected return. r+ OAS, with therisk-adjusted version from (3):

p(r + prOAS)P - —

at

price of iTik (4)

Second, we take the first derivative of both sides ofEquation (4) with respect to t :

(r -f prOAS)P. ^dP

(1 - P)-

1

term (o oniit or approximate (5)

where for now we disregard the last term.We have here a system of two linear partial differ-

ential Equations (4) and (5) with two unknown func-tions, P((, A") and PM, x). It can be simultaneously solvedbackward starting from the terminal (maturity 7) conditions:P{T, x) - 1, PA.T, x) - 0. This backward induction is car-ried out on a usual {t, A")-grid or probability tree, for one valueof ( = ^(0), and separately for the active and passive part.

Omission or approxinaation of the prepayment con-vexity term, proportional to P==, avoids expanding thepricing grid to the (^-dimension. If we want to accountfor the convexity term, we can do so by adding \Pif<yl tothe PDE, and then differentiate both parts twfce whileneglecting (or approximating) the third derivative. Wewould end up with a system of three PDEs, to be solvedon the same ((, A:)-grid for three unknown functions, P[i,.v), P-(f, x). and P..(^ A")—see Levin [2004] for details.

VALUATION METHOD 2:EQUIVALENT RISK-NEUTRAL PREPAY MODEL

Pricing Equation (4) allows for an important finan-cial interpretation. Suppose we still work w ith the tradi-tional PDE (2), ignoring the price of risk but insteadletting the risk tiictor B, drift with a negative Kg. (7= rate peryear:

dt= a.dz. - Tt.G.dt (6)

It is easy to see that such a drift contributes a sys-tematic return that is mathematically identical to the abovemarked price of risk. Indeed, the full-time derivative term,dP/dt on the right-hand side ot Equation (2), will now becomposed of a dP/dt term measured due to a simple pas-

76 PREPAYMENT RrsK- AND O[>TioN-AiiiusTEi.i VALUATION OF MBS SUMMER 20U5

sage of time {i.e., with unchanged ^ minus a TT^ CTc Pc termthat comes fix)m the Ito lemma applied to price P as a flinc-tioii of random variable ^ defined by Equation (6). Thisleads directly to the pricing Equation (4) with risk.

We essentially arrive at a powerful risk-neutralityconcept for prepayment risk: IVicing with risk consider-ation can be replaced with pricing without it, but with theprepay risk factor ^ drifting in the undesired direction. Therate ot this drift is proportional to volatility <Tc, and the coef-ficient of this proportionality is the price of risk, Kp. ThisIS the same concept we use in constructing term structuremodels and pricing financial derivatives wbilc taking for-ward rates and prices into consideration.

A prepayment model with the factor ^ set to driftat the risk-adjusted rate can be logically called a risk-ncu-trat prepayment model, like all other financial models thatexploit this concept. It is therefore meaningless to won-der how well such a model fits actual prepayments—it issimply not meant to do this job.

The risk-neutral drift for factor ^ can also be partlycaused by a model's systematic bias. For example, themarket may expect tbe refinancing process to becomemore efficient going forward than it has been. Mathe-matically this bias cannot be distinguished from the priceof risk; it too results in a drift cbange for ^. Using tbe risk-neutral prepay model and the prOAS should lead to thesame valuation results as using an empirical prepaymentmodel witb the traditional OAS.

Mortgage market participants are accustomed to see-ing ditferences in broker and analyst forecasts of prepaymentsand reports of OAS numbers for the same instruments andmarket conditions. The transition 6x)m an objective model,which often Lises historical prepayments, to a risk-neutralone that targets known prices for known instruments mayexplain the disparities. Hence, risk-neutral prepay speedsshould differ less across firms. Since Black and Scholes,risk-neutral modeling has been known for its abihty toreduce bias from systematic model-induced errors.

Although we have shown that a risk-neutral prepaymodel is theoretically equivalent to the explicit risk assess-ment performed for each investment period, from a finan-cial engineer's point of view there is a fundamentaldifference between the two techniques. The exphcit riskassessment method computes the partial derivative P-directly tor each investment period and rate level. This taskis feasible if the entire valuation is performed backward,and the MBS price and its derivatives with respect to riskyfactor ( can be found tor every node of the pricing grid.

For example, unstructured MBS can be priced this

way using the burnout-curing active-passive decomposi-tion idea. CMOs, though, are heavily path-dependentbeyond burnout, and are therefore not subject to backwardvaluation. For CMOs, the risk-neutral prepay modelwould be an ideal method as it does not require comput-ing Pp directly. Letting the risk factor ^ drift in the unde-sired direction naturally explores the price's dependenceon ( , without measuring P^ explicitly.

We have so far assumeci for simplicity that the risk fac-tor follows a simple Wiener process. In general, the behav-ior of prepayment factors is more complex. For example,prepayments cannot grow more uncertain over time with-out bounds, suggesting that the dynamics of risk factorsare mean-reverting. Yet purely diffusive behavior cannotcapture uncertainty in tbe starting values, i.e., risk presentat time zero. For example, the price ot risk constant modelconsiders risky prepayment parameters where values areconstant but drawn from some distribution (see Cohler,Feldman, and Lancaster [1997|).

In general, we may extend the stochastic model forfactor ^(r) to:

(7)VarBiO) - a;

where d- is the mean reversion parameter, and ^ is thelong-term equilibrium. The starting value is now con-sidered uncertain and drawn from N]^^^, (7^J. This mean-reverting pattern will add more terms in pricing PDEs.Also, tbe very last {time zero) step in backward valuationwill become a special one—to account for the time zerorisk and convexity.

Transforming model {7) into a risk-neutral form, weagain add a -K^CT,: drift rate, and shift the initial condi-tion by -;rc(T^:

G.dz

{7-RN)

These are the generalized dynamics of the risk fac-tor ^{t) in a risk-neutral prepayment model. We see thatrisk-neutrality lowers both the starting value and {in thepresence of mean reversion) the long-term equilibriumfor ^{/).

2(105 THE JOURNAL OF POUTFOLII) MANAGEMENT 7 7

A PROAS P R I C I N G MODEL WITHREFINANCING AND TURNOVER RISK

We have noted that both premium and discount MBSare often traded at somewhat elevated option-adjustedspreads. IOs stripped fixjm premium collateral are priced pro-gressively cheaper, on an OAS basis, than IOs taken fi omdiscount or current-coupon collateral. We conjecture thattwo major prepayment sources, the refinancing process(driving the premiums) and the turnover process (vital forunderstanding the discounts), are perceived as risky by themortgage market. To put this into simple practical terms,there are two distinct market fears—refinancing under-statement, and turnover overstatement. Hence, the modelof risk should be at least two-dimensional, which is a rathersimple extension ot what we have considered so far. Allow-ing the refinancing and the turnover processes to be ran-domly scaled, we can model the total prepayment speed as:

SMM - pRefiSMM + iTurnoverSMM (K)

where the prepay multipliers, p and T, are considereduncertain but centered on 1, and mutually independent.Thus, instead of one hypothetical prepay risk factor i , webave now two, p and T.

If we use the active-passive (or other) collateraldecomposition, we apply the additive rule in Equation (8)to each constituent piece. Every risk premium and con-vexity cost found in pricing equations now becomes a sim-ple sum of two terms associated with the refinancing riskand the turnover risk. We assume known volatihties, (7and (T of two Wiener processes, p{l) and r(f), as well astwo prices of risk, 71 and 71^

The conceptual risk-adjusted return formula inEquation (3) now becomes

Single-Period Expected Return =

P, P.r -\- prOAS ^ p f p

prepay risk spread

where P and P stand tor partial derivatives. Note thenegative sign for the refinancing risk. Since premiumtixed-rate MBS typically have P < 0, we can reward themby either assuming a negative price of risk constant, 71 ,or using the negative sign in the spread formula. Discountfixed-rate MBS have P^ > 0, so the positive sign in (9)produces positive return compensation for bearingturnover risk.

Extension ot the single risk factor is rather simple.In the fundamental pricing PDE (2), we now replace theexpected return, r + OAS, with Equation (9). Thus mod-ified risk-adjusted PDE will apparently include unknownderivatives Pj.and P . The next step is to differentiate thisequation with respect to each risk factor, p and r, therebyadding two more equations and closing mathematicalconstruct. The total number of pricing PDEs to solve willbe either three with prepay convexity cost disregarded (forP, P , and P ), or six with prepay convexity cost included(for P, P , P^ the second derivatives, P , P and themixed derivative P^^)-'

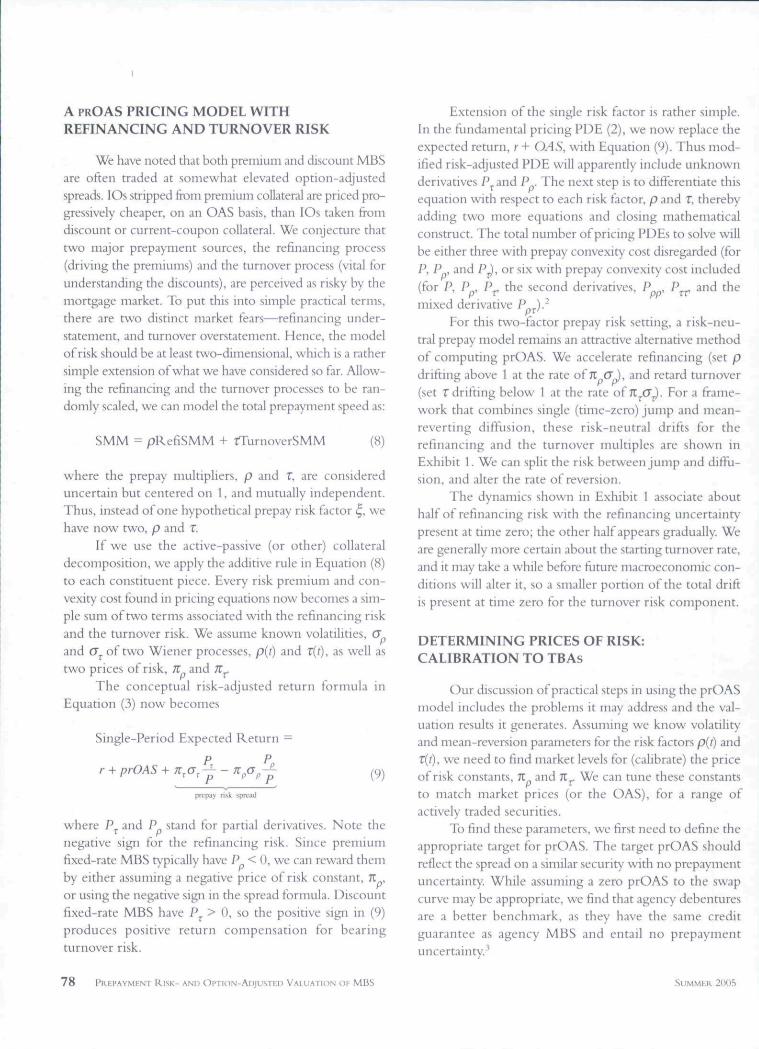

For this two-factor prepay risk setting, a risk-neu-tral prepay model remains an attractive alternative methodof computing prOAS. We accelerate refinancing (set pdrifting above 1 at the rate ofu <JX and retard turnover(set T drifting below t at the rate of JCCTj}. For a frame-work that combines single (time-zero) jump and mean-reverting diffusion, these risk-neutral drifts tor therefmancing and the turnover multiples are shown inExhibit 1. We can split the risk between jump and diffu-sion, and alter the rate of reversion.

The dynamics shown in Exhibit 1 associate abouthalf ot refinancing risk with the refinancing uncertaintypresent at time zero; the other half appears gradually. Weare generally more certain about the starting turnover rate,and it may take a while before future macroeconomic con-ditions will alter it. so a smaller portion of the total driftis present at time zero for the turnover risk component.

DETERMINING PRICES OE RISK:CALIBRATION TO TBAs

Our discussion of practical steps m using the prOASmodel includes the problems it may address and the val-uation results it generates. Assuming we know volatilityand mean-reversion parameters for the risk factors p{t) andr(f), we need to find market levels for (calibrate) the priceof risk constants, K and 71 . We can tune these constantsto match market prices (or the OAS), for a range ofactively traded securities.

To find these parameters, we first need to define theappropriate target for prOAS. The target prOAS shouldreflect the spread on a similar securit\' with no prepaymentuncertainty. While assuming a zero prOAS to the swapcurve may be appropriate, we fmd that agency debenturesare a better benchmark, as they have the same creditguarantee as agency MBS and entail no prepaymentuncertainty.'

78 PKEI'AYMENT RISK- AND OPTION-ADJUSTEP VALUATION OF MBS SUMMER 21H)5

E X H I B I T 1Risk-Neutral Prepay Multiples

prepayment multiple1.5

0.7

refinancing, p (t)

time-zero jumps recognizinguncertainty in starting vaiues

physicai equilibrium

turnover, T (f )

5 6 7years forward, t

10 11 12

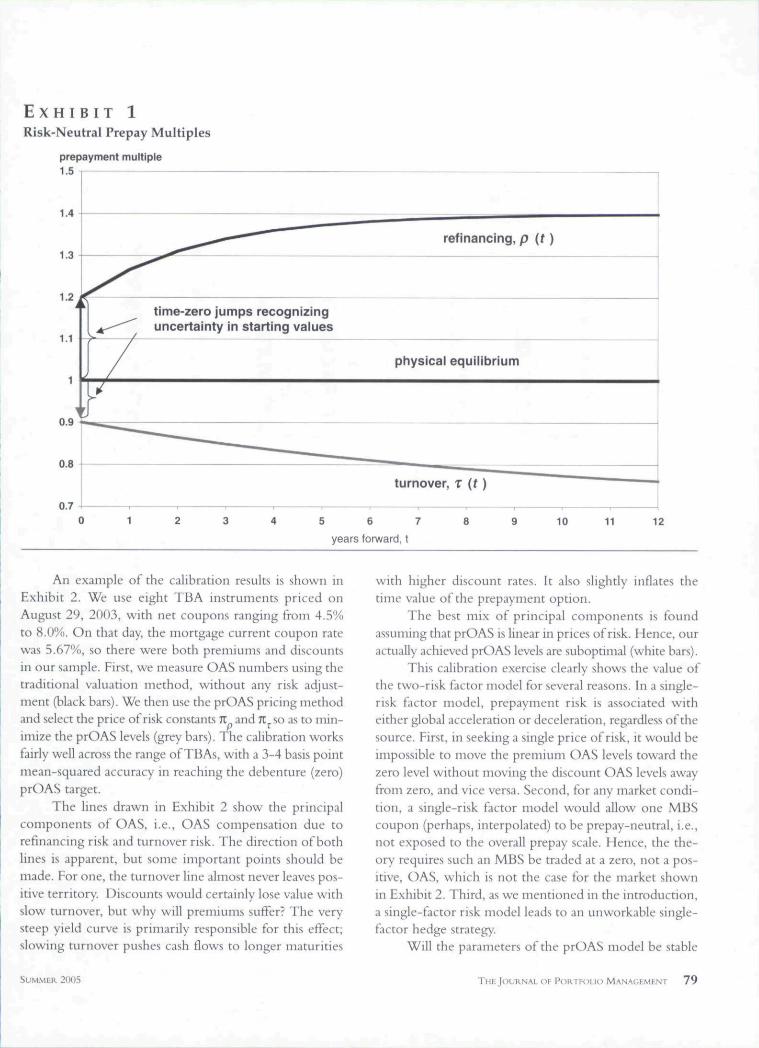

An example of the calibration results is shown inExhibit 2. We use eight TBA instruments priced onAugust 29, 2003, with net coupons ranging from 4.5%to 8.0%. On that day, the mortgage current coupon ratewas 5.67%, so there were both premiums and discountsin our sample. First, we measure OAS numbers using thetraditional valuation method, without any risk adjust-ment (black bars). We then use the prOAS pricing methodand select the price of risk constants 71 and 71 so as to min-imize the prOAS levels (grey bars). The calibration worksfairly well across the range of TBAs, with a 3-4 basis pointmean-squared accuracy in reaching the debenture (zero)prOAS target.

The lines drawn in Exhibit 2 show the principalcomponents of OAS, i.e., OAS compensation due torefinancing risk and turnover risk. The direction of bothlines is apparent, but some important points should bemade. For one, the turnover line almost never leaves pos-itive territory. Discounts would certainly lose value withslow turnover, but why will premiums suffer? The verysteep yield curve is primarily responsible for this effect;slowing turnover pushes cash flows to longer maturities

with higher discount rates. It also slightly inflates thetime value of the prepayment option.

The best mix of principal components is foundassuming that prOAS is linear in prices of risk. Hence, ouractually achieved prOAS levels are suboptimal (white bars).

This calibration exercise clearly shows the value ofthe two-risk factor model for several reasons. In a single-risk factor model, prepayment risk is associated witheither global acceleration or deceleration, regardless of thesource. First, in seeking a single price of risk, it would beimpossible to move the premium OAS levels toward thezero level without moving the discount OAS levels awayfrom zero, and vice versa. Second, for any market condi-tion, a single-risk factor model would allow one MBScoupon {perhaps, interpolated) to be prepay-neutral, i.e.,not exposed to the overall prepay scale. Hence, the the-ory requires such an MBS be traded at a zero, not a pos-itive, OAS, which is not the case for the market shownin Exhibit 2. Third, as we mentioned in the introduction,a single-factor risk model leads to an unworkable single-factor hedge strategy.

Will the parameters of the prOAS model be stable

SUMMEU 2005 THE JOURNAL OF PORTFOLIO MANAGEMENT 7 9

E X H I B I T 2Prices of Risk Calibrated to FNCL TBAs as of August 29, 2003

Agency OAS/prOAS, bp

60usual OAS

PCA-optimized prOAS (RMSE = 2.9 bp)

actually achieved prOAS (RMSE = 3.6 bp)

refinancing principal component

turnover principal component

FNCL4.5 FNCLS.O FNCL5.5 FNCL6.0 FNCL6.5 FNCL7.0 FNCL7.5 FNCLS.O

over time, or do we need to calibrate them on a daily basis?Wbile one goal of physical models is to stay steady, theconcept of risk-neutrality is linked to changing marketprices for benchmark instruments, which reflect thedynamics of market preferences for risk. If the marketprices for TBAs exhibit OAS tightening or wideningover time, they are sending us a message ot changingperceptions of prepayment risk.

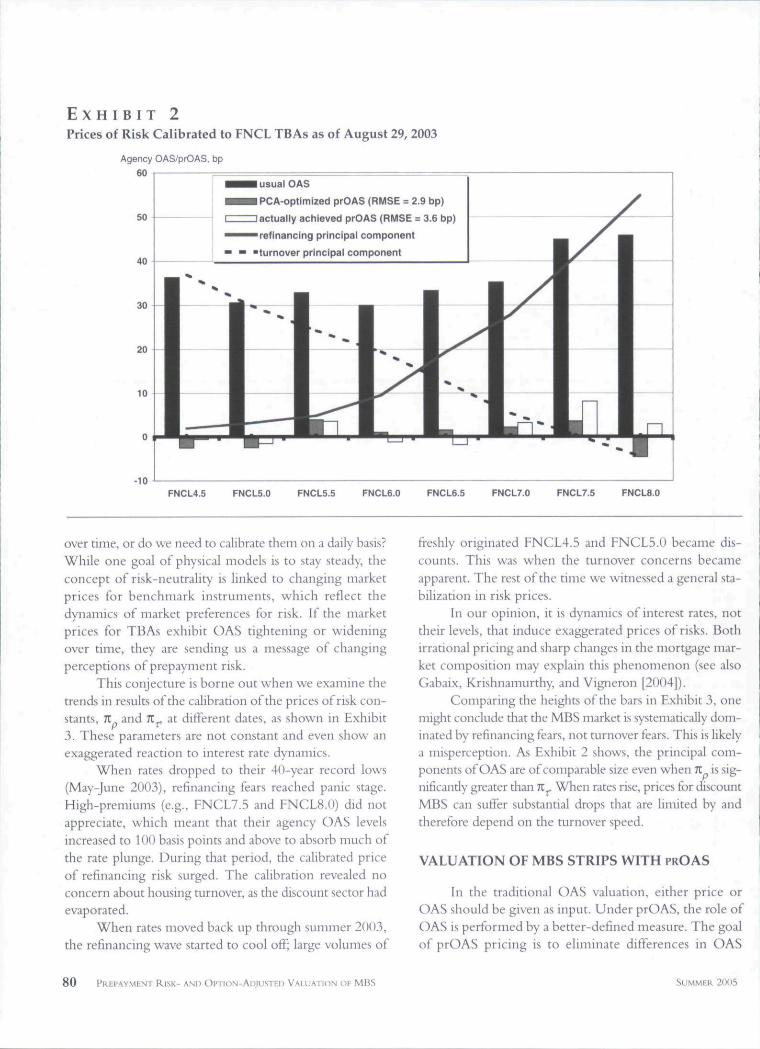

This conjecture is borne out when we examine thetrends in results of the calibration of tbe prices of risk con-stants, 71 and Jlj at different dates, as shown in Exhibit3. These parameters are not constant and even show anexaggerated reaction to interest rate dynamics.

When rates dropped to tbeir 4(.)-year record lows(May-June 2003), refinancing fears reached panic stage.High-premiums (e.g., FNCL7.5 and FNCLS.O) did notappreciate, which meant that their agency OAS levelsincreased to 100 basis points and above to absorb much ofthe rate plunge. During that period, the calibrated priceof refinancing risk surged. The calibration revealed noconcern about housing turnover, as the discount sector hadevaporated.

When rates moved back up through summer 2003,the refinancing wave started to cool off; large volumes of

freshly originated FNCL4.5 and FNCL5.0 became dis-counts. This was when the turnover concerns becameapparent. The rest of the time we witnessed a general sta-bihzation in risk prices.

In our opinion, it is dynamics of interest rates, nottheir levels, that induce exaggerated prices of risks. Bothirrational pricing and sharp changes in the mortgage mar-ket composition may explain this phenomenon (see alsoGabaix, Krishnamurthy, and Vigneron [2004]).

Comparing the heights of the bars in Exhibit 3, onemight conclude that the MBS market is systematically dom-inated by refinancing fears, not turnover fears. This is likelya misperception. As Exhibit 2 shows, tbe principal com-ponents of OAS are of comparable size even when K is sig-nificantly greater tban K^ When rates rise, prices for discountMBS can suffer substantial drops that are limited by andtherefore depend on the turnover speed.

VALUATION OF MBS STRIPS WITH P R O A S

In the traditional OAS valuation, either price orOAS should be given as input. Under prOAS, the role ofOAS is performed by a better-defined measure. The goalof prOAS pricing is to eliminate differences in OAS

80 PREPAYMENT RISK- AND OpnoN-AoiusTEn VALUATION OF MBS SUMMER 2005

E X H I B I T 3Historical Prices of Refinancing and Turnover Risk

Price of Risk

4.5

refinancing scare turnover concerns stabilization

^m Refl Risk

t- . I Turnover Risk

MTGEFNCL

Rats,

- 6

0.5

-0.5

5.S

5.6

5.4

4.6

4.4

4.2Apr-03 May-03 Jun-03 Jul-03 Aug-03 Sep-03 Oct-03 Nov-03 Dec-03 Jan-04 Feb-04 Mar-04

among instruments that are exposed to prepayment risk.As we asserted earlier, the prOAS measure should

value agency MBS flat to agency debentures. Therefore,once the risk factors are given their stochastic specifica-tions (jump sizes, diffusive volatility, and mean reversion)and the prices of risk constants are determined, we canvalue any agency MBS or its IO and PO strips much likeswaptions, i.e., hy looking at the benchmark rate andvolatility structure, but without any knowledge of the tra-ditional OAS.

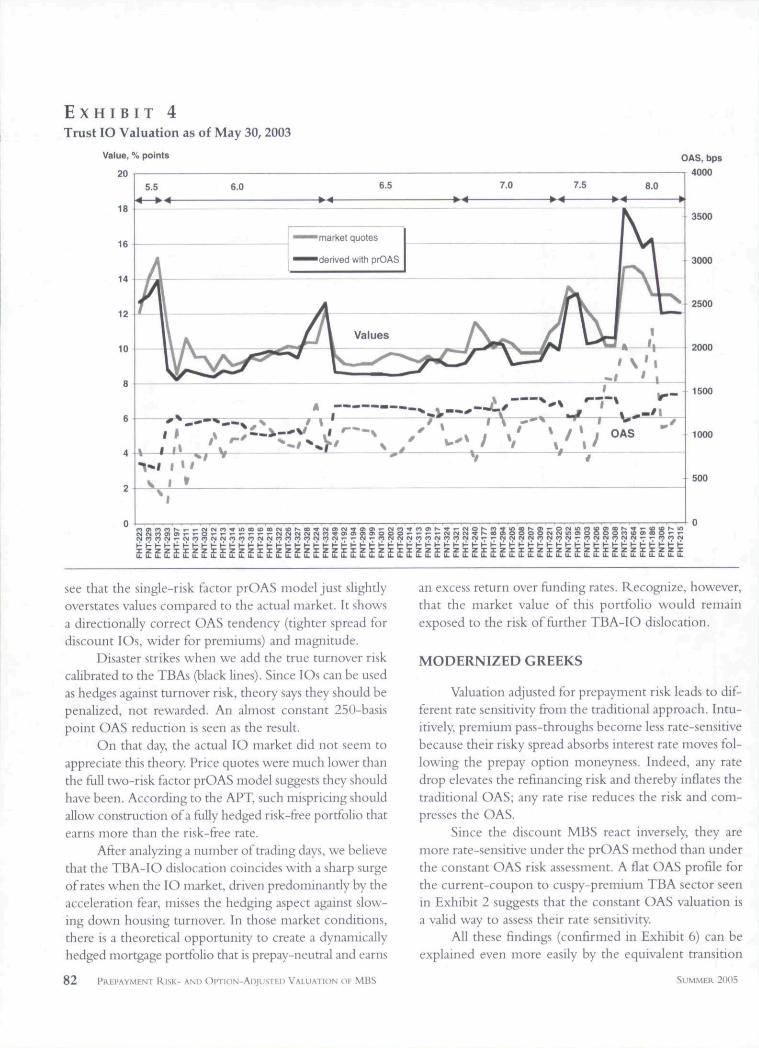

Exhibit 4 shows valuation results for agency trust IOsusing prices of risk constants, a high TT , and a near-zero7Cj., obtained from the cahbration to Fannie Mae TBAs onMay 30, 2003. Application of the prOAS method firstleads to values that are then converted into conventionalOAS measures. The prOAS model explains IO cheap-ness (and therefore PO richness) naturally, and correctlypredicts an OAS level of (and above) 1,000 basis points.

As POs stripped off premium pools should be lookedat as hedges against refinancing risk, they have to betraded rich according to arbitrage pricing theory. OurprOAS model successfully confirms this in that virtuallyall OAS for trust POs are deep in negative territory (notshown in Exhibit 4). Results in Exhibit 4 also provide

some degree of confidence for managers of mortgageservicing rights (MSR) portfolios (not actively traded orfrequently quoted)—they can use the prOAS measure tobetter assess the risk of their portfolios.

Exhibit 3 sbows in a historical risk chart that on May30, 2003, the entire risk perception was evolving out ofa refinancing scare. Exhibit 4 shows that both the TBAmarket and the trust IO market agree with one anotherin incorporating this risk into pricing.

In the summer months of 2003, rates rose sharply,pushing lower-coupon MBS (4.5s and 5.0s) into discountterritory. Exhibit 2 confirms that by the end of that sum-mer the refinancing fear had dissipated, making room forturnover concerns (slower-than-modeled turnover resultsin a loss for a discount MBS holder). It is not surprisingthat the price for turnover risk, virtually non-existent inMay 2003, grew considerably (Exhibit 3).

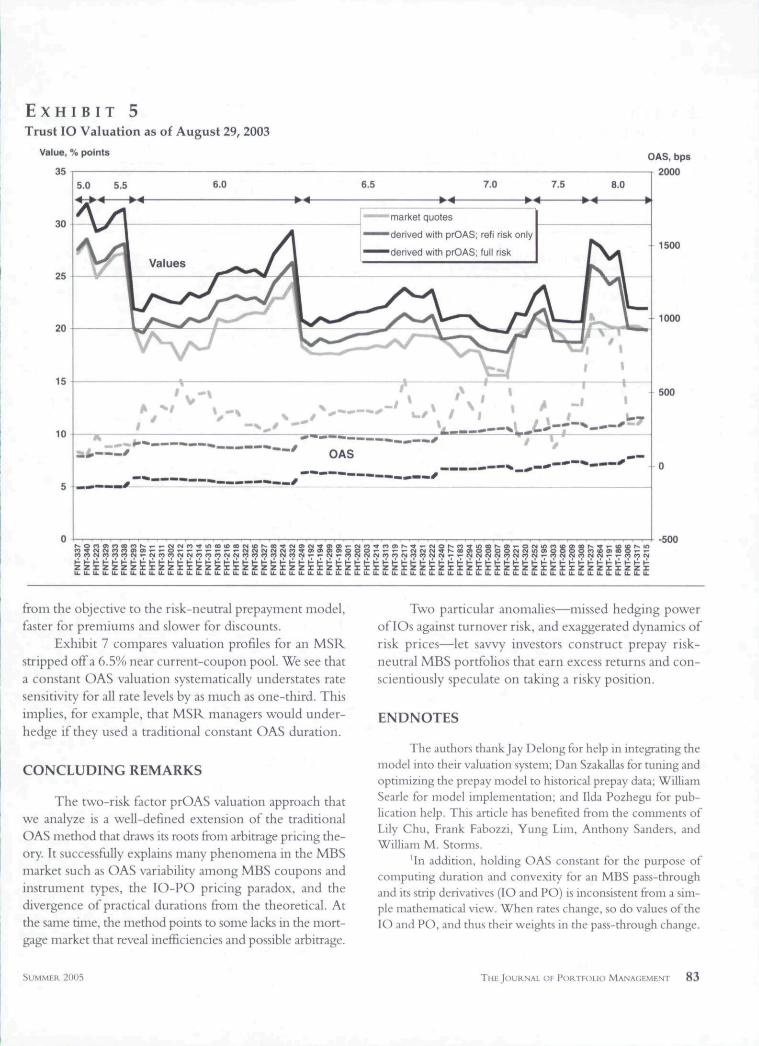

What if we apply prices of risk calibrated to theAugust 29, 2003, TBA market to value trust IOs? Exhibit5 shows two stages in application of the prOAS model,valuation with refinancing risk only, and with total risk.

Comparing the market prices and related OAS (lightgrey lines) with the valuation results under the prOASmodel with refinancing risk only {darker grey hnes), we

SUMMER 2005 THEJOURNAI OF PORTFOLIO MANAC;F.MI;NT 8 1

E X H I B I T 4

Trust IO Valuation as of May 30, 2003

Value, % points

20

18

16

14

12

10

5.5

h

\\

1\ 1

^*l 1V 1

^ '

A

*

6.0 6.5

^ ^ market quotes

^^^derived with prOAS

AU \ Values

^ V ^

7.0

idr

7.5

ftC

s

1

OAS

8.0

1

l\.-/I

OAS, bps

4000

3500

3000

2500

2000

_ 1500

1000

500

izzzrizzxrzzzrizzzzrzzriziziiizzrzziziizriizizzi

see that the single-risk factor prOAS model just slightlyoverstates values compared to the actual market. It showsa directionally correct OAS tendency (tighter spread fordiscount IOs, wider for premiums) and magnitude.

Disaster strikes when we add the true turnover riskcalibrated to the TBAs (black lines). Since IOs can be usedas hedges against turnover risk, theory says they should bepenalized, not rewarded. An almost constant 250-basispoint OAS reduction is seen as the result.

On that day the actual IO market did not seem toappreciate this theory. Price quotes were much lower thanthe full two-risk factor prOAS model suggests they shouldhave been. According to the APT, such mispricing shouldallow construction of a flilly hedged risk-free portfolio thatearns more than the risk-tree rate.

After analyzing a number of trading days, we believethat the TBA-IO dislocation coincides with a sharp surgeof rates when the IO market, driven predominandy by theacceleration fear, misses the hedging aspect against slow-ing down housing turnover. In those market conditions,there is a theoretical opportunity to create a dynamicallyhedged mortgage portfolio that is prepay-neutral and earns

an excess return over funding rates. Recognize, however,that the market value of this portfolio would remainexposed to the risk of further TBA-IO dislocation.

MODERNIZED GREEKS

Valuation adjusted for prepayment risk leads to dif-ferent rate sensitivity from the traditional approach. Intu-itively, premium pass-throughs become less rate-sensitivebecause their risky spread absorbs interest rate moves fol-lowing the prepay option moneyness. Indeed, any ratedrop elevates the refmancing risk and thereby inflates thetraditional OAS; any rate rise reduces the risk and com-presses the OAS.

Smce the discount MBS react inversely, they aremore rate-sensitive under the prOAS method than underthe constant OAS risk assessment. A flat OAS profile forthe current-coupon to cuspy-premium TBA sector seenin Exhibit 2 suggests that the constant OAS valuation isa valid way to assess their rate sensitivity.

All these findings (confirmed in Exhibit 6) can beexplained even more easily by the equivalent transition

8 2 I'uhi'AVMENT RISK- AND OI'TION-ADJUSTKD VALUATION of- MBS SUMMEK 20(15

E X H I B I T 5Trust IO Valuation as of August 29, 2003

Value, % points OAS, bps

6.0 6.5 7.0 7.5 S.O

market quotes

•derived with prOAS; refi risk only

'derived with prOAS; full risk

XZZZZZrZZTTZXZXXZZZZZZXZZXZXXXZXZZXZXZ

2000

1500

1000

500

-500

z z r z z z z x r z z x

from the objective to the risk-neutral prepayment model,faster for premiums and slower for discounts.

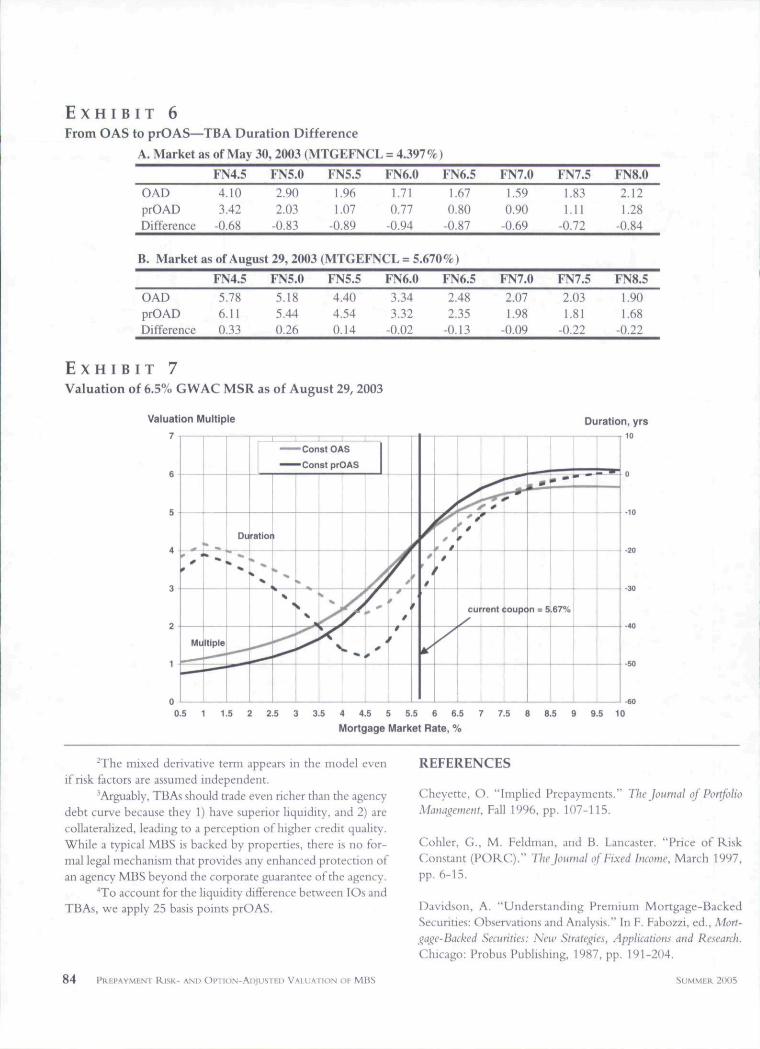

Exhibit 7 compares valuation profiles for an MSRstripped off a 6.5% near current-coupon pool. We see thata constant OAS valuation systematically understates ratesensitivity for all rate levels by as much as one-third. Thisimplies, for example, that MSR managers would under-hedge if they used a traditional constant OAS duration.

CONCLUDING REMARKS

The two-risk tactor prOAS valuation approach thatwe analyze is a well-defined extension oi the traditionalOAS method that draws its roots from arbitrage pricing the-ory. It successfully explains many phenomena in the MBSmarket such as OAS variability among MBS coupons andinstrument types, the IO-PO pricing paradox, and thedivergence of practical durations from the theoretical. Atthe satne time, the method points to some lacks in the mort-gage market that reveal inefficiencies and possible arbitrage.

Two particular anomalies—missed hedging pow^erof IOs against turnover risk, and exaggerated dynamics ofrisk prices—let savvy investors construct prepay risk-neutral MBS portfohos that earn excess returns and con-scientiously speculate on taking a risky position.

ENDNOTES

The authors thank Jay Delong for help in integrating themodel into their valuation system; Dan Szakallas for tuning andoptimizing the prepay model to historical prepay data; WilliamSearle for model implementation; and Ilda Pozhegu for pub-lication help. This article has benefited from the comments ofLily Chu, Frank Fabozzi, Yung Lini, Anthony Sanders, andWilliam M. Storms.

'In addition, holding OAS constant for the purpose ofcomputing duration and convexity for au MBS pass-throughand its strip derivatives (IO and PO) is inconsistent from a sim-ple mathematical view. When rates change, so do values of theIO and PO, and thus their weights in the pass-through change.

SUMMER 2O(J5 THt JOURNAL <.>F PORTFOLIO MANAGEMENT 83

E X H I B I T 6

From OAS lo prOAS—TBA Duration Difference

A. Market as of May 30,2003 (MTGEFNCL = 4.397%)

OADprOADDifference

FN4.54.103.42

-0.68

FN5.02.902.03

-0.83

B. Market as ofAugust 29, 2003

OADprOADDifference

FN4.55.786.110.33

FN5.05.185.440.26

FN5.51.961.07

-0.89

FN6.01.710.77

-0.94

(MTGEFNCL = 5

FN5.54.404.540.14

FN6.03.343.32

-0.02

FN6.51.670.80

-0.87

.670%)

FN6.52.482.35

-0.13

FN7.01.590.90

-0.69

FN7.02.071.98

-0.09

FN7.51.83l.ll

-0.72

FN'7.5

2.031.81

-0.22

FN8.02.121.28

-0.84

FN8.51.901.68

-0.22

E X H I B I T 7

Valuation of 6.5% GWAC MSR as of August 29, 2003

Valuation Multiple Duration, yrs10

Mi

——

b

Itipie- — -

DL

—i—-

— Const OAS

——Const prOAS

ratior

k

k

1

f

/

01

( f

f

cu rent :oupc

""*f '

n = 567%

^ ^ ^ ^

h

0.5 1 1.5 2 2.5 3 3.5 4 4.5 5 5.5 6 6.5Mortgage Market Rate, %

7.5 8 B.5 9.5 10

-Tbe mixed derivative term appears m the model evenif risk factors arc assumed independent.

'Arguably, TBAs should trade even ncber than the agencydebt curve because tbcy 1) have superior liquidity, and 2) arecollateralized, leading to a perception of higber credit quality.Wbile a typical MBS is backed by properties, tbere is no for-mal legal mechanism tbat provides any enhanced protection ofan agency MBS beyond the corporate guarantee of tbe agency.

""To account for the liquidity difference between IOs andTBAs, we apply 25 basis points prOAS.

REFERENCES

Cheyette, O. "Implied Prepayments." Tlic JournaJ of PortfolioManagement, Fall 1996, pp. 107-115.

Cohler, G., M. Feldman, and B. Lancaster. "Price of RiskConstant (PORC)." The Journal of Fixed Income, March 1997,pp. 6-15.

Davidson, A. "Understanding Prciniuin Mortgage-BackedSecurities: Observations and Analysis." In F. Fabozzi, ed., Morr-gaj^e-Backed Securities: New Strate_i>ies, Applications and Research.

Chicago: Probus Publishing, 1987. pp. 191-204.

84 PllEHAYMENT RiSK- ftNl) Of I"H)N-Al)JUS"rEI) VALUAI'ION Oh MBS SUMMER 2005

Davidson, A., M. Herskovitz, and L. Van Drunen. "The Refi-nancing Threshold Model: An Economic Approach to Valu-ing MBS." Journal of Real Estate Finance and Econoinics, 1 (June1988), pp. 117-130.

Fabozzi, F., and G. Fong. Advanced Fixed Income Portfolio Man-

a<iemait. Burr Ridge, IL: Irwin Professional Publishing, 1994.

Gahaix, X., A. Krisbnamurthy, and O. Vigneron. "Limit ofArbitrage: Theory and Evidence from the Mortgage-BackedSecurities Market." Working paper, 2004.

Hayre, L. "Anatomy of Prepayments." Ttie Joumai of Fixed!ncome,]une 2000, pp. 19-49.

. "A Simple Statistical Framework for Modehng Bumoutand Refinancing Behavior.*' Tliejoutfialof Fixed Income, Decem-ber 1994, pp. 69-74.

Hull, J. Options, Futures, and Other Deriuatii>es, 4th ed. UpperSaddle River, NJ: Prentice-Hall, 2000.

Kalotay, A., D. Yang, and F. Fabozzi. "An Option-TheoreticPrepayment Model for Mortgages and Mortgage-Backed Secu-rities." Intemational journal of Theoretical and Applied Finance,Vol. 7, No. 8 (2004), pp. 1-29.

Kupiec, P., and A. Kah. "On the Origin and Interpretation ofOAS." Tiie journal of Fixed Income, December 1999, pp. 82-92.

Levin, A. "Active-Passive Decomposition in Burnout Model-ing." Tlxc journal of Fixed Income, March 2001, pp. 27-40.

. "Deriving Closed-Form Solutions for Gaussian PricingModels: A Systematic Time-Domain Approach." Internationaljournal of Theoretical and Applied Finance, 1(3) (1998), pp. 348-376.

. "Divide and Conquer: Exploring New OAS Horizons."Andrew Davidson & Co., 2004.

To order reprints of this article, please contact Ajani Malik at

anialik(^iijournab.com or 212-224-3205.

SUMMtK 2( THEJOUKNAI OF l-*oRTFoir(i MANAGEMENT 85

![[Bank of America] Hybrid ARM MBS - Valuation and Risk Measures](https://img.dokumen.tips/doc/110x75/55205dca4979590a3f8b4684/bank-of-america-hybrid-arm-mbs-valuation-and-risk-measures.jpg)