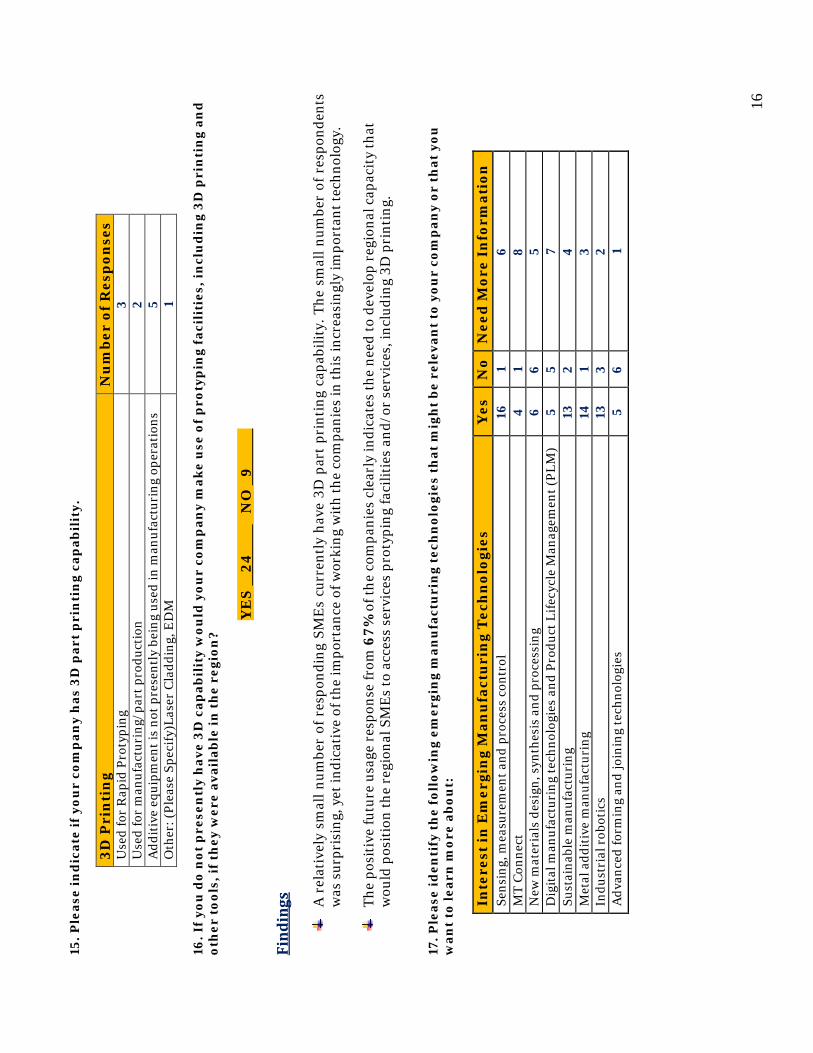

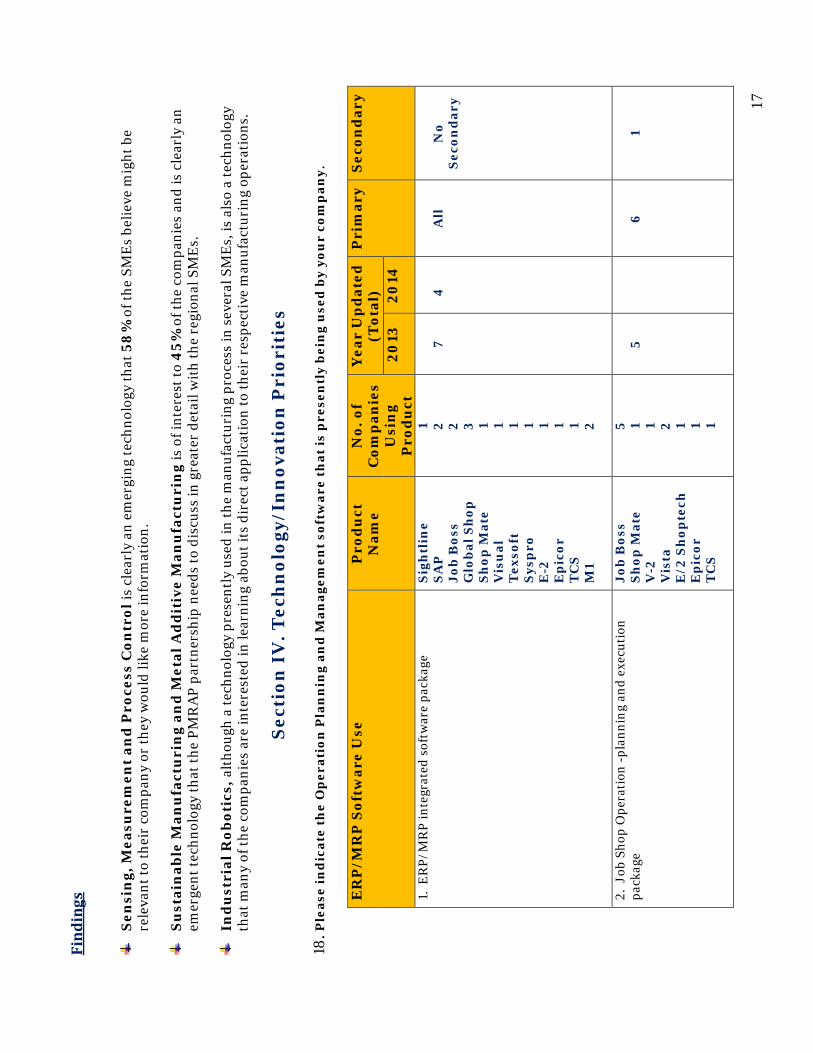

Embed Size (px)

Citation preview

Precision Manufacturing RegionalAlliance Project (PMRAP)

Workforce Development And

Technology Adoption Report

Findings and Recommendations

The Precision Manufacturing Regional Alliance Project (PMRAP) is funded by the Massachusetts Executive Office of Housing and Economic Development (EOHED). PMRAP’s early stage capacity and partnership building work was funded by the Innovation Institute at the Massachusetts Technology Collaborative. Matching cash and in-kind contributions were provided by the lead agency, the Regional Employment Board of Hampden County, Inc. (REB) and the Western Massachusetts Chapter of the National Tooling and Machining Association (WMNTMA). In-kind contributions were also provided by other PMRAP project partners.

On the Cover Cover photos courtesy of advanced manufacturing companies that are members of the Western Massachusetts Chapter of the National Tooling and Machining Association (WMNTMA).

Precision Manufacturing Regional Alliance Project (PMRAP)

Workforce Development

And

Technology Adoption Report

Findings and Recommendations

June 2014

Table of Contents

Introduction Overview Executive Summary Section I- Principal Markets 1 Section II- Workforce Needs 2 Section III- Manufacturing Operations 14 Section IV- Technology/Innovation Priorities 17 Section V- Education Initiatives 23 Appendix

INTRODUCTION

Technology enabled advanced manufacturing is a critical industry in the Pioneer Valley Region and in Massachusetts. The advanced manufacturing companies are small and medium sized enterprises (SMEs) and are part of a supply chain primarily engaged in producing precision mechanical parts, components, and sub-assemblies utilizing high technology equipment, lean manufacturing, and world class technology development.

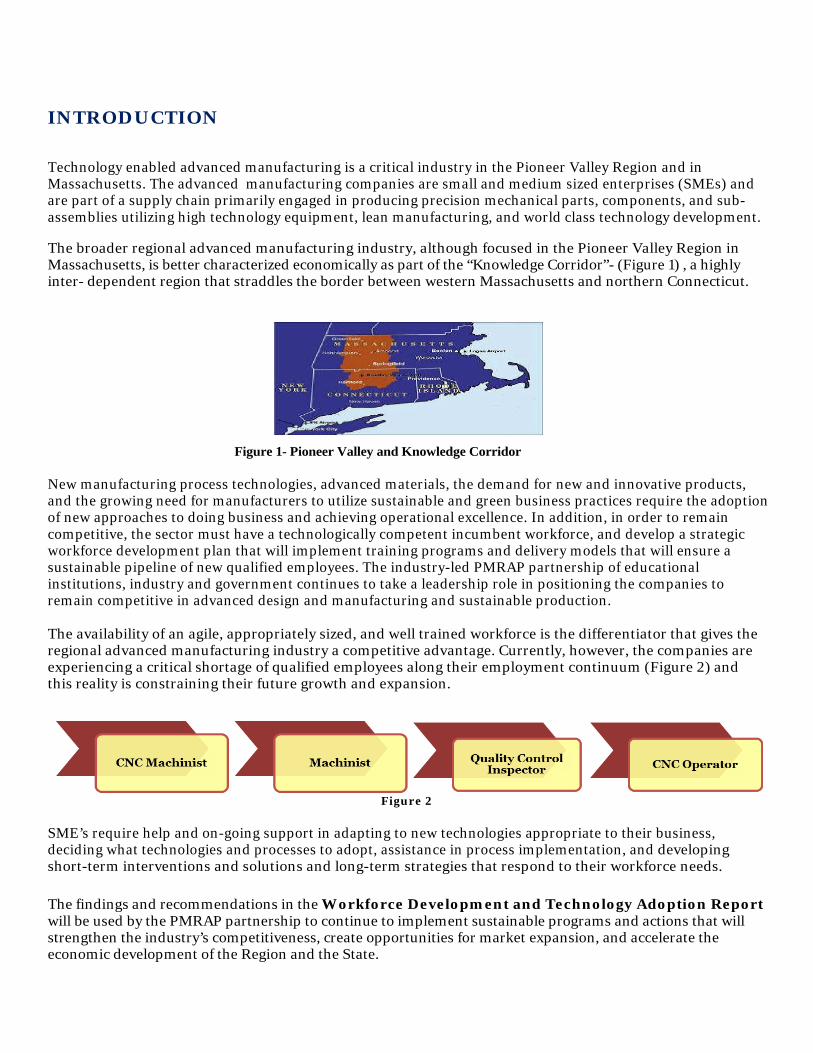

The broader regional advanced manufacturing industry, although focused in the Pioneer Valley Region in Massachusetts, is better characterized economically as part of the “Knowledge Corridor”- (Figure 1) , a highly inter- dependent region that straddles the border between western Massachusetts and northern Connecticut.

Figure 1- Pioneer Valley and Knowledge Corridor

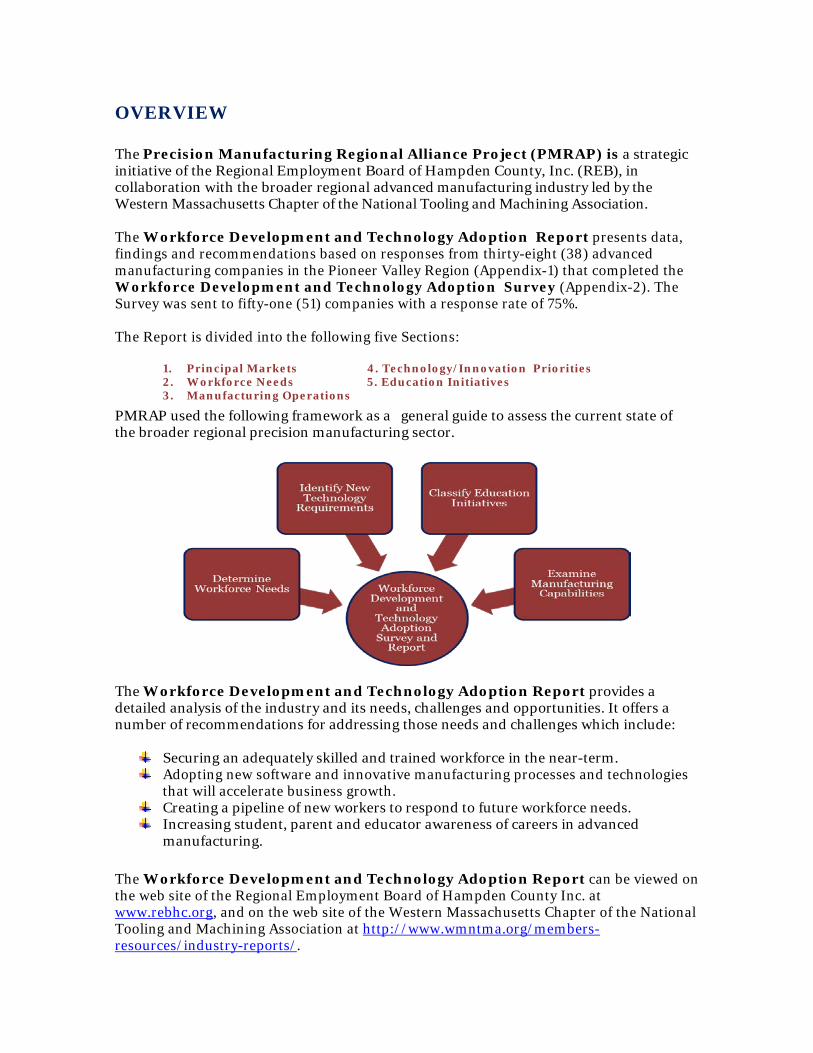

New manufacturing process technologies, advanced materials, the demand for new and innovative products, and the growing need for manufacturers to utilize sustainable and green business practices require the adoption of new approaches to doing business and achieving operational excellence. In addition, in order to remain competitive, the sector must have a technologically competent incumbent workforce, and develop a strategic workforce development plan that will implement training programs and delivery models that will ensure a sustainable pipeline of new qualified employees. The industry-led PMRAP partnership of educational institutions, industry and government continues to take a leadership role in positioning the companies to remain competitive in advanced design and manufacturing and sustainable production. The availability of an agile, appropriately sized, and well trained workforce is the differentiator that gives the regional advanced manufacturing industry a competitive advantage. Currently, however, the companies are experiencing a critical shortage of qualified employees along their employment continuum (Figure 2) and this reality is constraining their future growth and expansion.

Figure 2 SME’s require help and on-going support in adapting to new technologies appropriate to their business, deciding what technologies and processes to adopt, assistance in process implementation, and developing short-term interventions and solutions and long-term strategies that respond to their workforce needs. The findings and recommendations in the Workforce Development and Technology Adoption Report will be used by the PMRAP partnership to continue to implement sustainable programs and actions that will strengthen the industry’s competitiveness, create opportunities for market expansion, and accelerate the economic development of the Region and the State.

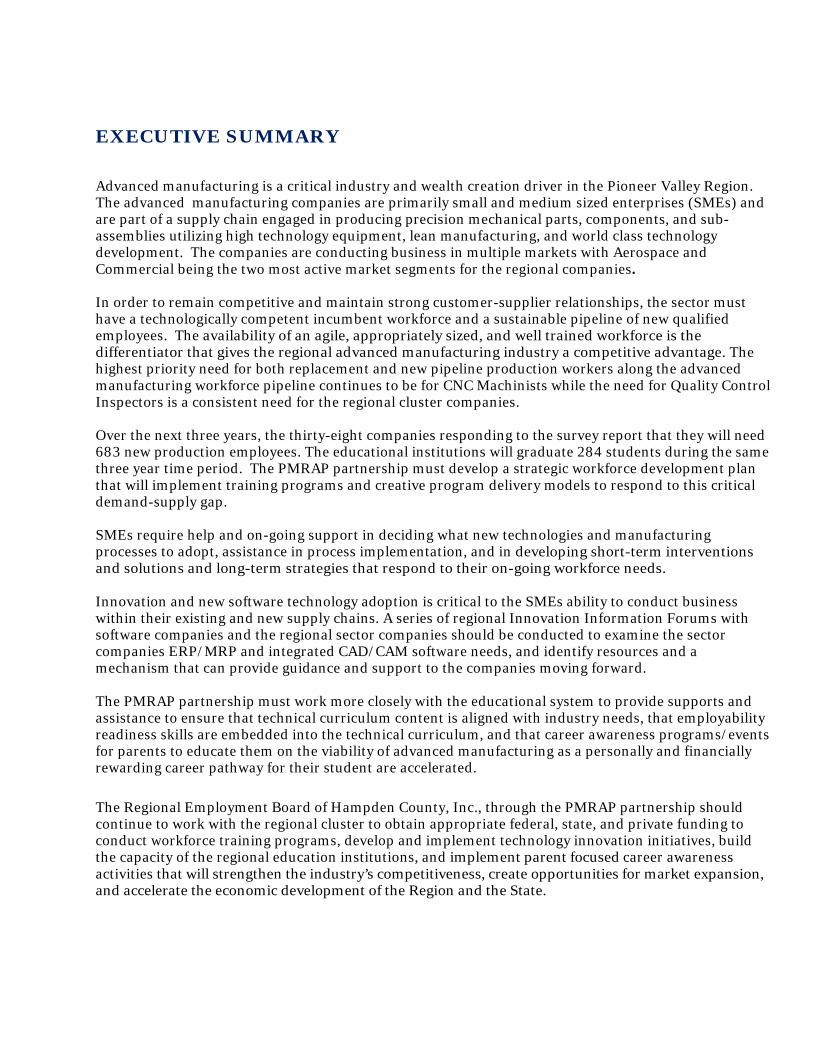

OVERVIEW The Precision Manufacturing Regional Alliance Project (PMRAP) is a strategic initiative of the Regional Employment Board of Hampden County, Inc. (REB), in collaboration with the broader regional advanced manufacturing industry led by the Western Massachusetts Chapter of the National Tooling and Machining Association. The Workforce Development and Technology Adoption Report presents data, findings and recommendations based on responses from thirty-eight (38) advanced manufacturing companies in the Pioneer Valley Region (Appendix-1) that completed the Workforce Development and Technology Adoption Survey (Appendix-2). The Survey was sent to fifty-one (51) companies with a response rate of 75%. The Report is divided into the following five Sections:

1. Principal Markets 4. Technology/Innovation Priorities 2. Workforce Needs 5. Education Initiatives 3. Manufacturing Operations

PMRAP used the following framework as a general guide to assess the current state of the broader regional precision manufacturing sector.

The Workforce Development and Technology Adoption Report provides a detailed analysis of the industry and its needs, challenges and opportunities. It offers a number of recommendations for addressing those needs and challenges which include:

Securing an adequately skilled and trained workforce in the near-term. Adopting new software and innovative manufacturing processes and technologies

that will accelerate business growth. Creating a pipeline of new workers to respond to future workforce needs. Increasing student, parent and educator awareness of careers in advanced

manufacturing. The Workforce Development and Technology Adoption Report can be viewed on the web site of the Regional Employment Board of Hampden County Inc. at www.rebhc.org, and on the web site of the Western Massachusetts Chapter of the National Tooling and Machining Association at http://www.wmntma.org/members-resources/industry-reports/.

EXECUTIVE SUMMARY

Advanced manufacturing is a critical industry and wealth creation driver in the Pioneer Valley Region. The advanced manufacturing companies are primarily small and medium sized enterprises (SMEs) and are part of a supply chain engaged in producing precision mechanical parts, components, and sub-assemblies utilizing high technology equipment, lean manufacturing, and world class technology development. The companies are conducting business in multiple markets with Aerospace and Commercial being the two most active market segments for the regional companies.

In order to remain competitive and maintain strong customer-supplier relationships, the sector must have a technologically competent incumbent workforce and a sustainable pipeline of new qualified employees. The availability of an agile, appropriately sized, and well trained workforce is the differentiator that gives the regional advanced manufacturing industry a competitive advantage. The highest priority need for both replacement and new pipeline production workers along the advanced manufacturing workforce pipeline continues to be for CNC Machinists while the need for Quality Control Inspectors is a consistent need for the regional cluster companies. Over the next three years, the thirty-eight companies responding to the survey report that they will need 683 new production employees. The educational institutions will graduate 284 students during the same three year time period. The PMRAP partnership must develop a strategic workforce development plan that will implement training programs and creative program delivery models to respond to this critical demand-supply gap. SMEs require help and on-going support in deciding what new technologies and manufacturing processes to adopt, assistance in process implementation, and in developing short-term interventions and solutions and long-term strategies that respond to their on-going workforce needs. Innovation and new software technology adoption is critical to the SMEs ability to conduct business within their existing and new supply chains. A series of regional Innovation Information Forums with software companies and the regional sector companies should be conducted to examine the sector companies ERP/MRP and integrated CAD/CAM software needs, and identify resources and a mechanism that can provide guidance and support to the companies moving forward. The PMRAP partnership must work more closely with the educational system to provide supports and assistance to ensure that technical curriculum content is aligned with industry needs, that employability readiness skills are embedded into the technical curriculum, and that career awareness programs/events for parents to educate them on the viability of advanced manufacturing as a personally and financially rewarding career pathway for their student are accelerated. The Regional Employment Board of Hampden County, Inc., through the PMRAP partnership should continue to work with the regional cluster to obtain appropriate federal, state, and private funding to conduct workforce training programs, develop and implement technology innovation initiatives, build the capacity of the regional education institutions, and implement parent focused career awareness activities that will strengthen the industry’s competitiveness, create opportunities for market expansion, and accelerate the economic development of the Region and the State.

P

reci

sion

Man

ufa

ctu

rin

g R

egio

nal

All

ian

ce P

roje

ct (

PM

RA

P)

W

orkf

orce

Dev

elop

men

t an

d T

ech

nol

ogy

Ad

opti

on R

epor

t

N=

38

Com

pan

ies

Sec

tion

I- P

rin

cip

al M

arke

ts

1.

P

leas

e in

dic

ate

the

pri

nci

pal

mar

kets

in w

hic

h y

ou c

ond

uct

yo

ur

man

ufa

ctu

rin

g b

usi

nes

s.

50%

66

%

42%

66

%

21%

13

%

42%

39

%

21%

21

%

10%

Mar

ket

Con

cen

trat

ion

Mar

kets

N

um

ber

of

Res

pon

ses

Mar

ket

Ran

kin

g

Mar

kets

Nu

mbe

r of

R

esp

onse

s M

arke

t R

anki

ng

2014

20

12

2014

20

12

Def

ense

19

3

3

Fir

earm

s 16

5

10

Aer

osp

ace

25

1 1

P

ower

G

ener

atio

n

15

6

5

Med

ical

Dev

ice

16

4

4

Au

tom

otiv

e 8

8

-

Com

mer

cial

25

1

2

Oil

/Gas

Fie

ld

8

9

- E

lect

ron

ics

8

7

6

P

acka

gin

g 4

11

7

Mat

eria

l Han

dli

ng

5

10

9

R

enew

able

E

ner

gy

N/A

- 8

1

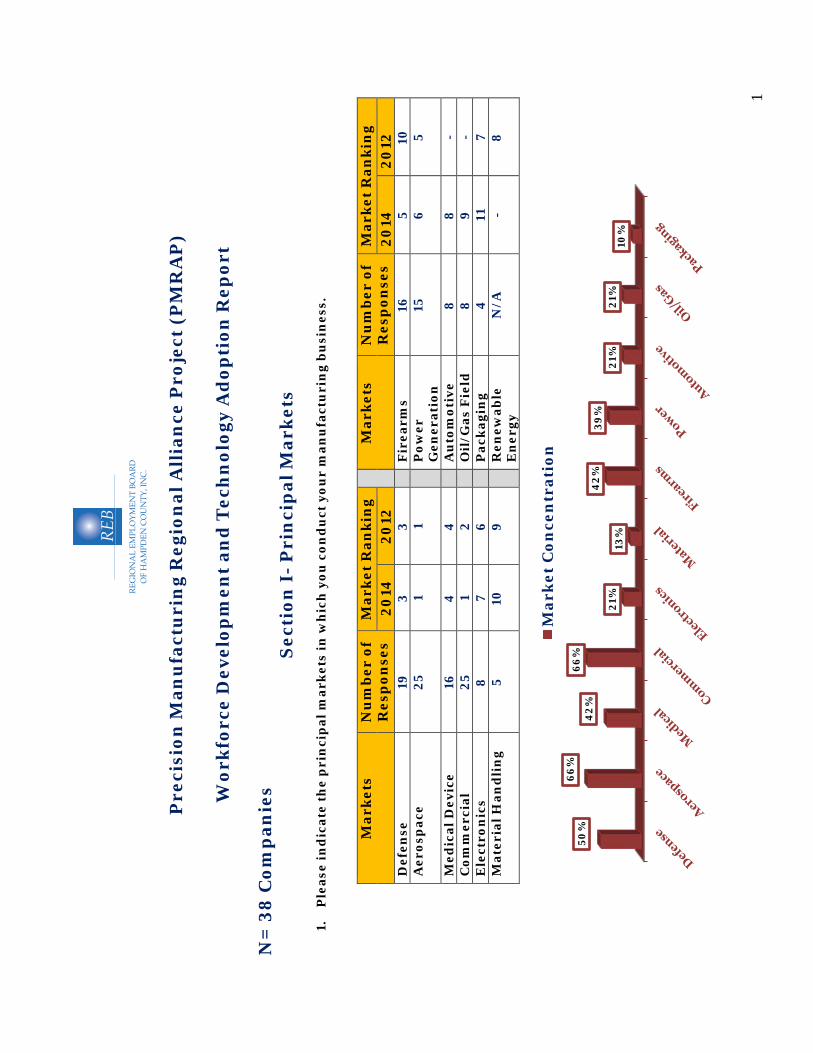

Find

ings

Th

e re

gion

al p

reci

sion

man

ufac

turi

ng c

ompa

nies

are

con

duct

ing

busi

ness

in m

ulti

ple

mar

kets

wit

h A

eros

pac

e (6

6%

) an

d C

omm

erci

al (

66%

) be

ing

the

two

mos

t act

ive

mar

ket s

egm

ents

for

the

regi

onal

com

pani

es.

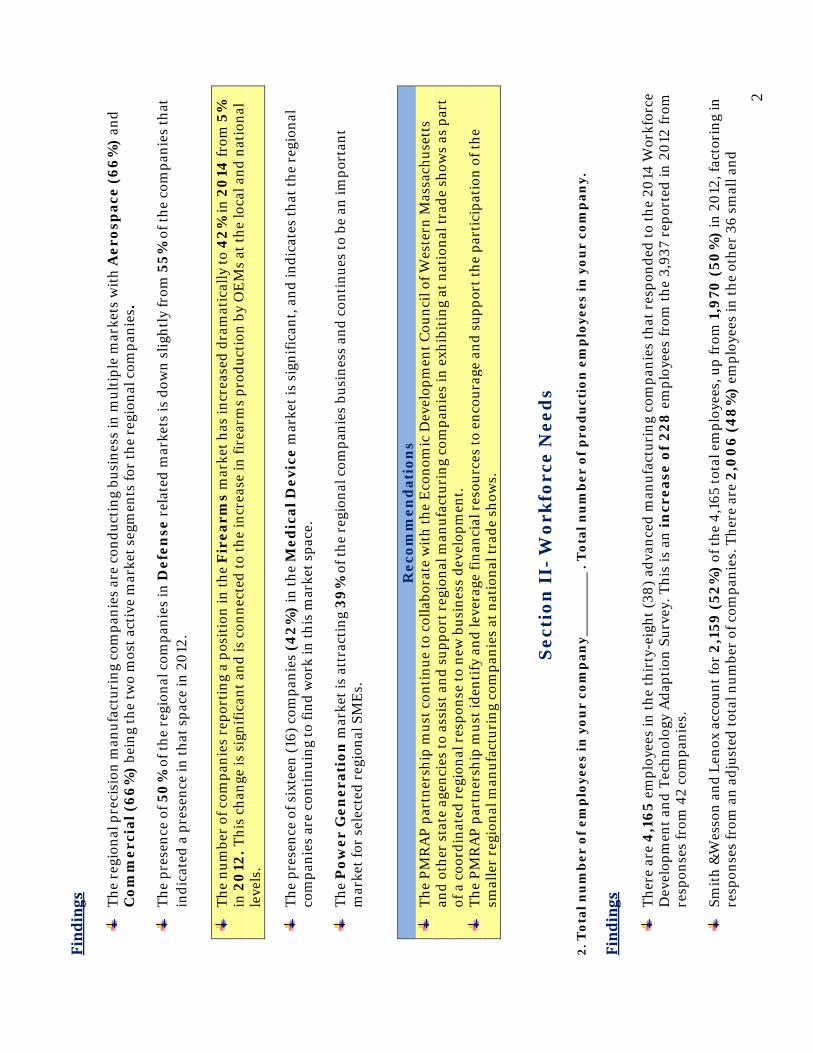

The

pres

ence

of 5

0%

of t

he r

egio

nal c

ompa

nies

in D

efen

se r

elat

ed m

arke

ts is

dow

n sl

ight

ly fr

om 5

5% o

f the

com

pani

es th

at

indi

cate

d a

pres

ence

in th

at s

pace

in 2

012.

Th

e nu

mbe

r of

com

pani

es r

epor

ting

a p

osit

ion

in th

e F

irea

rms

mar

ket h

as in

crea

sed

dram

atic

ally

to 4

2% in

20

14 fr

om 5

%

in 2

012

. Thi

s ch

ange

is s

igni

fican

t and

is c

onne

cted

to th

e in

crea

se in

fire

arm

s pr

oduc

tion

by

OE

Ms

at th

e lo

cal a

nd n

atio

nal

leve

ls.

The

pres

ence

of s

ixte

en (1

6) c

ompa

nies

(42

%)

in th

e M

edic

al D

evic

e m

arke

t is

sign

ifica

nt, a

nd in

dica

tes

that

the

regi

onal

co

mpa

nies

are

con

tinu

ing

to fi

nd w

ork

in th

is m

arke

t spa

ce.

The

Pow

er G

ener

atio

n m

arke

t is

attr

acti

ng 3

9% o

f the

reg

iona

l com

pani

es b

usin

ess

and

cont

inue

s to

be

an im

port

ant

mar

ket f

or s

elec

ted

regi

onal

SM

Es.

Rec

omm

end

atio

ns

Th

e PM

RA

P pa

rtne

rshi

p m

ust c

onti

nue

to c

olla

bora

te w

ith

the

Eco

nom

ic D

evel

opm

ent C

ounc

il of

Wes

tern

Mas

sach

uset

ts

and

othe

r st

ate

agen

cies

to a

ssis

t and

sup

port

reg

iona

l man

ufac

turi

ng c

ompa

nies

in e

xhib

itin

g at

nat

iona

l tra

de s

how

s as

par

t of

a c

oord

inat

ed r

egio

nal r

espo

nse

to n

ew b

usin

ess

deve

lopm

ent.

The

PMR

AP

part

ners

hip

mus

t ide

ntify

and

leve

rage

fina

ncia

l res

ourc

es to

enc

oura

ge a

nd s

uppo

rt th

e pa

rtic

ipat

ion

of th

e sm

alle

r re

gion

al m

anuf

actu

ring

com

pani

es a

t nat

iona

l tra

de s

how

s.

Sec

tion

II-

Wor

kfor

ce N

eed

s 2.

Tot

al n

um

ber

of

emp

loye

es in

you

r co

mp

any

.

Tot

al n

um

ber

of

pro

du

ctio

n e

mp

loye

es in

yo

ur

com

pan

y.

Find

ings

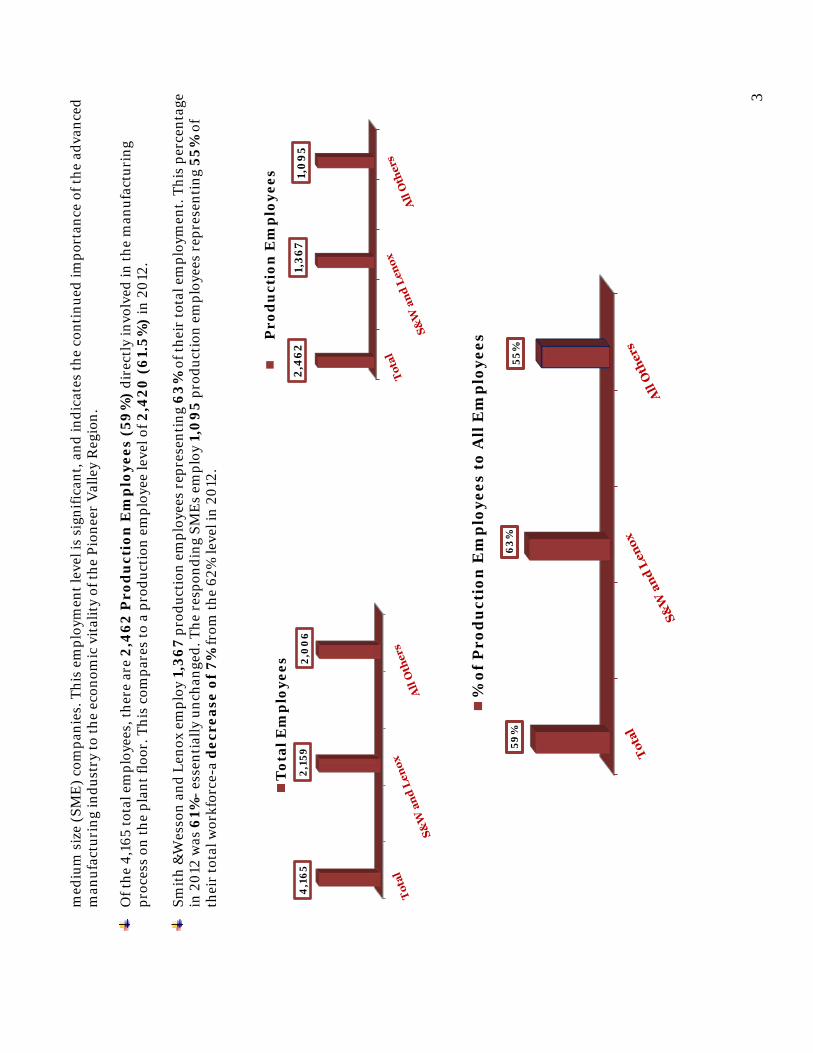

Th

ere

are

4,1

65

empl

oyee

s in

the

thir

ty-e

ight

(38)

adv

ance

d m

anuf

actu

ring

com

pani

es th

at r

espo

nded

to th

e 20

14 W

orkf

orce

D

evel

opm

ent a

nd T

echn

olog

y A

dapt

ion

Surv

ey. T

his

is a

n in

crea

se o

f 22

8 e

mpl

oyee

s fr

om th

e 3,

937

repo

rted

in 2

012

from

re

spon

ses

from

42

com

pani

es.

Smit

h &

Wes

son

and

Leno

x ac

coun

t for

2,1

59 (

52%

) of

the

4,16

5 to

tal e

mpl

oyee

s, u

p fr

om 1

,970

(50

%)

in 2

012,

fact

orin

g in

re

spon

ses

from

an

adju

sted

tota

l num

ber

of c

ompa

nies

. The

re a

re 2

,00

6 (

48

%)

empl

oyee

s in

the

othe

r 36

sm

all a

nd

2

med

ium

siz

e (S

ME

) com

pani

es. T

his

empl

oym

ent l

evel

is s

igni

fican

t, an

d in

dica

tes

the

cont

inue

d im

port

ance

of t

he a

dvan

ced

man

ufac

turi

ng in

dust

ry to

the

econ

omic

vit

alit

y of

the

Pion

eer

Val

ley

Reg

ion.

O

f the

4,1

65 to

tal e

mpl

oyee

s, th

ere

are

2,46

2 P

rod

uct

ion

Em

plo

yees

(59

%)

dire

ctly

invo

lved

in th

e m

anuf

actu

ring

pr

oces

s on

the

plan

t flo

or. T

his

com

pare

s to

a p

rodu

ctio

n em

ploy

ee le

vel o

f 2,4

20 (

61.

5%)

in 2

012.

Sm

ith

&W

esso

n an

d Le

nox

empl

oy 1

,36

7 pr

oduc

tion

em

ploy

ees

repr

esen

ting

63%

of t

heir

tota

l em

ploy

men

t. Th

is p

erce

ntag

e in

201

2 w

as 6

1%- e

ssen

tial

ly u

ncha

nged

. The

res

pond

ing

SME

s em

ploy

1,0

95

prod

ucti

on e

mpl

oyee

s re

pres

enti

ng 5

5% o

f th

eir

tota

l wor

kfor

ce-a

dec

reas

e of

7%

from

the

62%

leve

l in

2012

.

4,1

65

2,15

9 2,

00

6

Tot

al E

mp

loye

es2,

462

1,36

7 1,

095

P

rod

uct

ion

Em

plo

yees

59%

63

%

55%

% o

f P

rod

uct

ion

Em

plo

yees

to

All

Em

plo

yees

3

3. N

um

ber

of

pro

du

ctio

n e

mp

loye

es w

ho

wil

l be

reti

rin

g in

th

e n

ext

thre

e (3

) ye

ars

wh

ose

pos

itio

ns

wil

l nee

d t

o b

e re

pla

ced

.

Find

ings

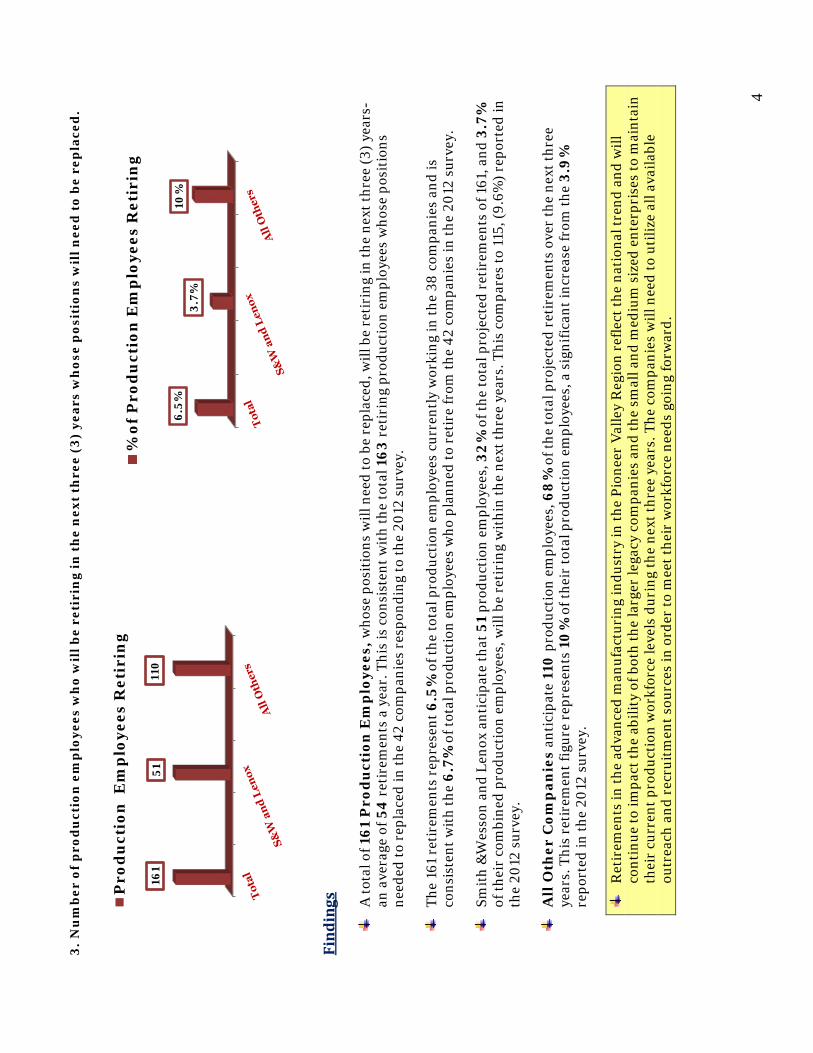

A

tota

l of 1

61 P

rod

uct

ion

Em

plo

yees

, who

se p

osit

ions

will

nee

d to

be

repl

aced

, will

be

reti

ring

in th

e ne

xt th

ree

(3) y

ears

- an

ave

rage

of 5

4 r

etir

emen

ts a

yea

r. T

his

is c

onsi

sten

t wit

h th

e to

tal 1

63

reti

ring

pro

duct

ion

empl

oyee

s w

hose

pos

itio

ns

need

ed to

rep

lace

d in

the

42 c

ompa

nies

res

pond

ing

to th

e 20

12 s

urve

y.

The

161

reti

rem

ents

rep

rese

nt 6

.5%

of t

he to

tal p

rodu

ctio

n em

ploy

ees

curr

entl

y w

orki

ng in

the

38 c

ompa

nies

and

is

cons

iste

nt w

ith

the

6.7

% o

f tot

al p

rodu

ctio

n em

ploy

ees

who

pla

nned

to r

etir

e fr

om th

e 42

com

pani

es in

the

2012

sur

vey.

Sm

ith

&W

esso

n an

d Le

nox

anti

cipa

te th

at 5

1 pr

oduc

tion

em

ploy

ees,

32%

of t

he to

tal p

roje

cted

ret

irem

ents

of 1

61, a

nd 3

.7%

of

thei

r co

mbi

ned

prod

ucti

on e

mpl

oyee

s, w

ill b

e re

tiri

ng w

ithi

n th

e ne

xt th

ree

year

s. T

his

com

pare

s to

115

, (9.

6%) r

epor

ted

in

the

2012

sur

vey.

A

ll O

ther

Com

pan

ies

anti

cipa

te 1

10 p

rodu

ctio

n em

ploy

ees,

68

% o

f the

tota

l pro

ject

ed r

etir

emen

ts o

ver

the

next

thre

e ye

ars.

Thi

s re

tire

men

t fig

ure

repr

esen

ts 1

0%

of t

heir

tota

l pro

duct

ion

empl

oyee

s, a

sig

nific

ant i

ncre

ase

from

the

3.9

%

repo

rted

in th

e 20

12 s

urve

y.

Ret

irem

ents

in th

e ad

vanc

ed m

anuf

actu

ring

indu

stry

in th

e Pi

onee

r V

alle

y R

egio

n re

flect

the

nati

onal

tren

d an

d w

ill

cont

inue

to im

pact

the

abili

ty o

f bot

h th

e la

rger

lega

cy c

ompa

nies

and

the

smal

l and

med

ium

siz

ed e

nter

pris

es to

mai

ntai

n th

eir

curr

ent p

rodu

ctio

n w

orkf

orce

leve

ls d

urin

g th

e ne

xt th

ree

year

s. T

he c

ompa

nies

will

nee

d to

uti

lize

all a

vaila

ble

outr

each

and

rec

ruit

men

t sou

rces

in o

rder

to m

eet t

heir

wor

kfor

ce n

eeds

goi

ng fo

rwar

d.

161

51

110

Pro

du

ctio

n E

mp

loye

es R

etir

ing

6.5%

3.

7%

10%

% o

f P

rod

uct

ion

Em

plo

yees

Ret

irin

g

4

4. N

um

ber

of

new

pip

elin

e p

rod

uct

ion

em

plo

yees

you

pro

ject

hir

ing

over

th

e n

ext

thre

e (3

) ye

ars.

Fin

ding

s

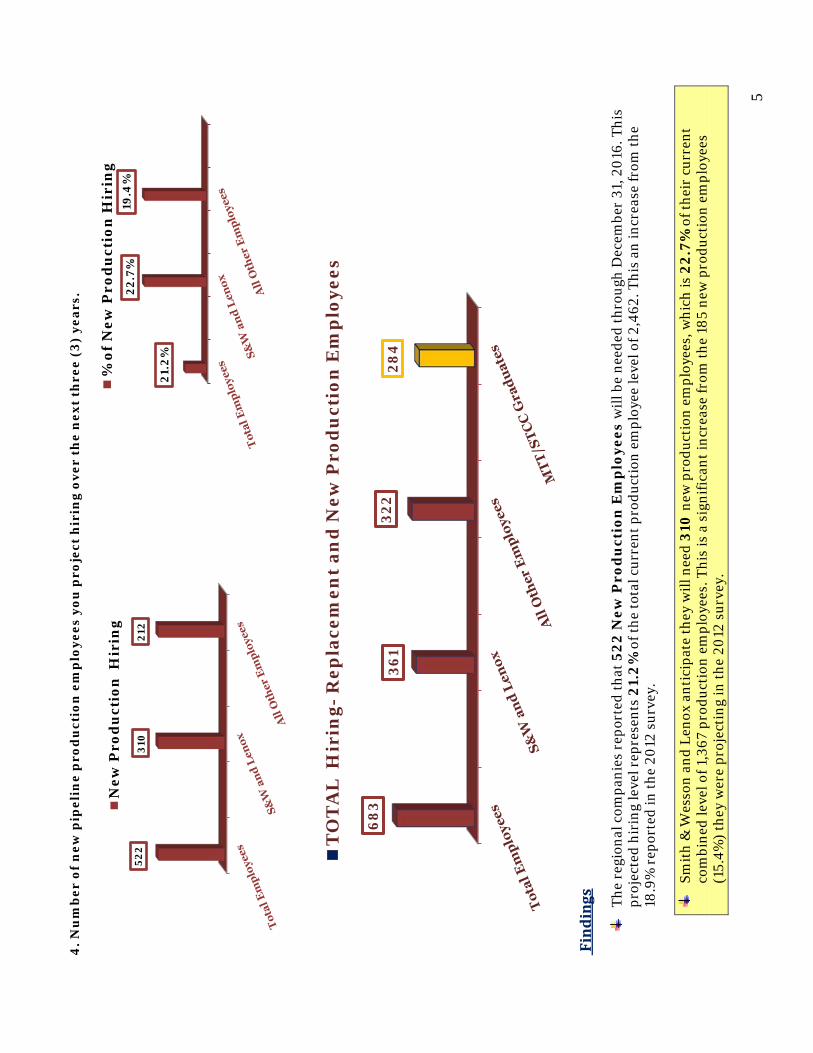

Th

e re

gion

al c

ompa

nies

rep

orte

d th

at 5

22 N

ew P

rod

uct

ion

Em

plo

yees

will

be

need

ed th

roug

h D

ecem

ber

31, 2

016.

Thi

s pr

ojec

ted

hiri

ng le

vel r

epre

sent

s 21

.2%

of t

he to

tal c

urre

nt p

rodu

ctio

n em

ploy

ee le

vel o

f 2,4

62. T

his

an in

crea

se fr

om th

e 18

.9%

rep

orte

d in

the

2012

sur

vey.

Sm

ith

& W

esso

n an

d Le

nox

anti

cipa

te th

ey w

ill n

eed

310

new

pro

duct

ion

empl

oyee

s, w

hich

is 2

2.7%

of t

heir

cur

rent

co

mbi

ned

leve

l of 1

,367

pro

duct

ion

empl

oyee

s. T

his

is a

sig

nific

ant i

ncre

ase

from

the

185

new

pro

duct

ion

empl

oyee

s (1

5.4%

) the

y w

ere

proj

ecti

ng in

the

2012

sur

vey.

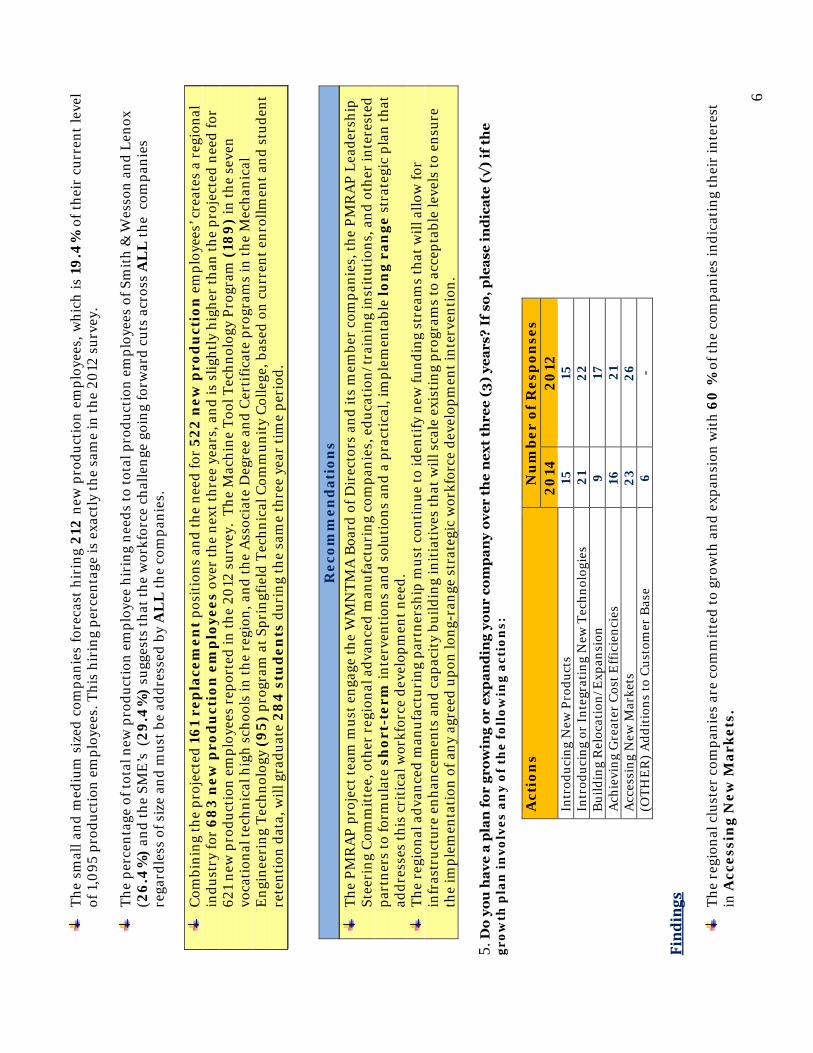

522

310

21

2

New

Pro

du

ctio

n H

irin

g

21.2

%

22.7

%

19.4

%

% o

f N

ew P

rod

uct

ion

Hir

ing

68

3 36

1 32

2 28

4

TO

TA

L H

irin

g- R

epla

cem

ent

and

New

Pro

du

ctio

n E

mp

loye

es

5

Th

e sm

all a

nd m

ediu

m s

ized

com

pani

es fo

reca

st h

irin

g 21

2 ne

w p

rodu

ctio

n em

ploy

ees,

whi

ch is

19

.4%

of t

heir

cur

rent

leve

l of

1,0

95 p

rodu

ctio

n em

ploy

ees.

Thi

s hi

ring

per

cent

age

is e

xact

ly th

e sa

me

in th

e 20

12 s

urve

y.

The

perc

enta

ge o

f tot

al n

ew p

rodu

ctio

n em

ploy

ee h

irin

g ne

eds

to to

tal p

rodu

ctio

n em

ploy

ees

of S

mit

h &

Wes

son

and

Leno

x (2

6.4

%)

and

the

SME

’s (

29.4

%)

sugg

ests

that

the

wor

kfor

ce c

halle

nge

goin

g fo

rwar

d cu

ts a

cros

s A

LL

the

com

pani

es

rega

rdle

ss o

f siz

e an

d m

ust b

e ad

dres

sed

by A

LL

the

com

pani

es.

Com

bini

ng th

e pr

ojec

ted

161

rep

lace

men

t pos

ition

s an

d th

e ne

ed fo

r 52

2 n

ew p

rod

uct

ion

em

ploy

ees’

cre

ates

a r

egio

nal

indu

stry

for

68

3 n

ew p

rod

uct

ion

em

plo

yees

ove

r th

e ne

xt th

ree

year

s, a

nd is

slig

htly

hig

her

than

the

proj

ecte

d ne

ed fo

r 62

1 ne

w p

rodu

ctio

n em

ploy

ees

repo

rted

in th

e 20

12 s

urve

y. T

he M

achi

ne T

ool T

echn

olog

y Pr

ogra

m (

189

) in

the

seve

n vo

cati

onal

tech

nica

l hig

h sc

hool

s in

the

regi

on, a

nd th

e A

ssoc

iate

Deg

ree

and

Cer

tific

ate

prog

ram

s in

the

Mec

hani

cal

Eng

inee

ring

Tec

hnol

ogy

(95)

pro

gram

at S

prin

gfie

ld T

echn

ical

Com

mun

ity

Col

lege

, bas

ed o

n cu

rren

t enr

ollm

ent a

nd s

tude

nt

rete

ntio

n da

ta, w

ill g

radu

ate

284

stu

den

ts d

urin

g th

e sa

me

thre

e ye

ar ti

me

peri

od.

R

ecom

men

dat

ion

s

The

PMR

AP

proj

ect t

eam

mus

t eng

age

the

WM

NTM

A B

oard

of D

irec

tors

and

its

mem

ber

com

pani

es, t

he P

MR

AP

Lead

ersh

ip

Stee

ring

Com

mit

tee,

oth

er r

egio

nal a

dvan

ced

man

ufac

turi

ng c

ompa

nies

, edu

cati

on/t

rain

ing

inst

itut

ions

, and

oth

er in

tere

sted

pa

rtne

rs to

form

ulat

e sh

ort-

term

inte

rven

tion

s an

d so

luti

ons

and

a pr

acti

cal,

impl

emen

tabl

e lo

ng

ran

ge s

trat

egic

pla

n th

at

addr

esse

s th

is c

riti

cal w

orkf

orce

dev

elop

men

t nee

d.

Th

e re

gion

al a

dvan

ced

man

ufac

turi

ng p

artn

ersh

ip m

ust c

onti

nue

to id

enti

fy n

ew fu

ndin

g st

ream

s th

at w

ill a

llow

for

infr

astr

uctu

re e

nhan

cem

ents

and

cap

acit

y bu

ildin

g in

itia

tive

s th

at w

ill s

cale

exi

stin

g pr

ogra

ms

to a

ccep

tabl

e le

vels

to e

nsur

e th

e im

plem

enta

tion

of a

ny a

gree

d up

on lo

ng-r

ange

str

ateg

ic w

orkf

orce

dev

elop

men

t int

erve

ntio

n.

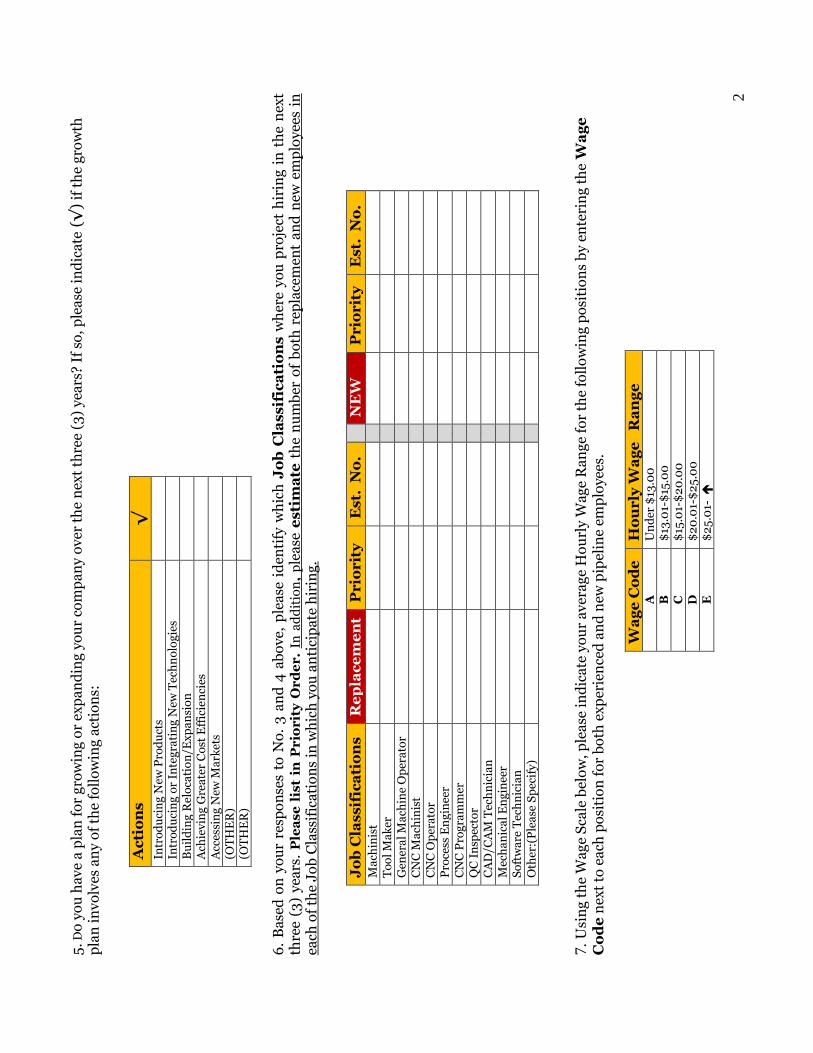

5.

Do

you

hav

e a

pla

n f

or

grow

ing

or e

xpan

din

g yo

ur

com

pan

y ov

er t

he

nex

t th

ree

(3)

year

s? I

f so

, ple

ase

ind

icat

e (√

) if

th

e gr

owth

pla

n in

volv

es a

ny

of t

he

foll

owin

g ac

tio

ns:

Act

ion

s N

um

ber

of R

esp

onse

s 20

14

2012

In

trod

ucin

g N

ew P

rodu

cts

15

15

Intr

oduc

ing

or I

nteg

rati

ng N

ew T

echn

olog

ies

21

22

Bui

ldin

g R

eloc

atio

n/E

xpan

sion

9

17

A

chie

ving

Gre

ater

Cos

t Eff

icie

ncie

s 16

21

A

cces

sing

New

Mar

kets

23

26

(O

THE

R) A

ddit

ions

to C

usto

mer

Bas

e 6

-

Find

ings

Th

e re

gion

al c

lust

er c

ompa

nies

are

com

mit

ted

to g

row

th a

nd e

xpan

sion

wit

h 60

% o

f the

com

pani

es in

dica

ting

thei

r in

tere

st

in A

cces

sin

g N

ew M

arke

ts.

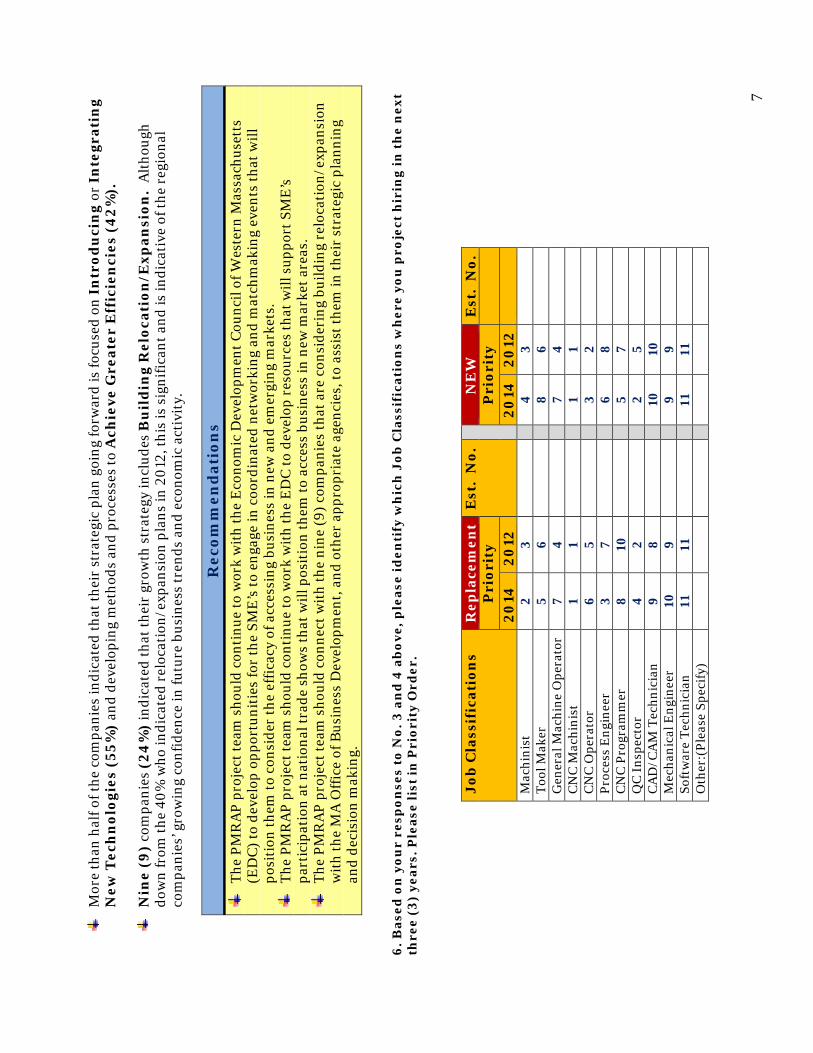

6

Mor

e th

an h

alf o

f the

com

pani

es in

dica

ted

that

thei

r st

rate

gic

plan

goi

ng fo

rwar

d is

focu

sed

on I

ntr

odu

cin

g or

In

tegr

atin

g N

ew T

ech

nol

ogie

s (5

5%)

and

deve

lopi

ng m

etho

ds a

nd p

roce

sses

to A

chie

ve G

reat

er E

ffic

ien

cies

(42

%).

N

ine

(9)

com

pani

es (

24%

) in

dica

ted

that

thei

r gr

owth

str

ateg

y in

clud

es B

uil

din

g R

eloc

atio

n/E

xpan

sion

. A

lthou

gh

dow

n fr

om th

e 40

% w

ho in

dica

ted

relo

cati

on/e

xpan

sion

pla

ns in

201

2, th

is is

sig

nific

ant a

nd is

indi

cati

ve o

f the

reg

iona

l co

mpa

nies

’ gro

win

g co

nfid

ence

in fu

ture

bus

ines

s tr

ends

and

eco

nom

ic a

ctiv

ity.

Rec

omm

end

atio

ns

The

PM

RA

P pr

ojec

t tea

m s

houl

d co

ntin

ue to

wor

k w

ith

the

Eco

nom

ic D

evel

opm

ent C

ounc

il of

Wes

tern

Mas

sach

uset

ts

(ED

C) t

o de

velo

p op

port

unit

ies

for

the

SME

’s to

eng

age

in c

oord

inat

ed n

etw

orki

ng a

nd m

atch

mak

ing

even

ts th

at w

ill

posi

tion

them

to c

onsi

der

the

effic

acy

of a

cces

sing

bus

ines

s in

new

and

em

ergi

ng m

arke

ts.

T

he P

MR

AP

proj

ect t

eam

sho

uld

cont

inue

to w

ork

wit

h th

e E

DC

to d

evel

op r

esou

rces

that

will

sup

port

SM

E’s

pa

rtic

ipat

ion

at n

atio

nal t

rade

sho

ws

that

will

pos

itio

n th

em to

acc

ess

busi

ness

in n

ew m

arke

t are

as.

T

he P

MR

AP

proj

ect t

eam

sho

uld

conn

ect w

ith

the

nine

(9) c

ompa

nies

that

are

con

side

ring

bui

ldin

g re

loca

tion

/exp

ansi

on

wit

h th

e M

A O

ffic

e of

Bus

ines

s D

evel

opm

ent,

and

othe

r ap

prop

riat

e ag

enci

es, t

o as

sist

them

in th

eir

stra

tegi

c pl

anni

ng

and

deci

sion

mak

ing.

6

. Bas

ed o

n y

our

resp

on

ses

to N

o. 3

an

d 4

ab

ove

, ple

ase

iden

tify

wh

ich

Job

Cla

ssif

icat

ion

s w

her

e yo

u p

roje

ct h

irin

g in

th

e n

ext

thre

e (3

) ye

ars.

Ple

ase

list

in P

rior

ity

Ord

er.

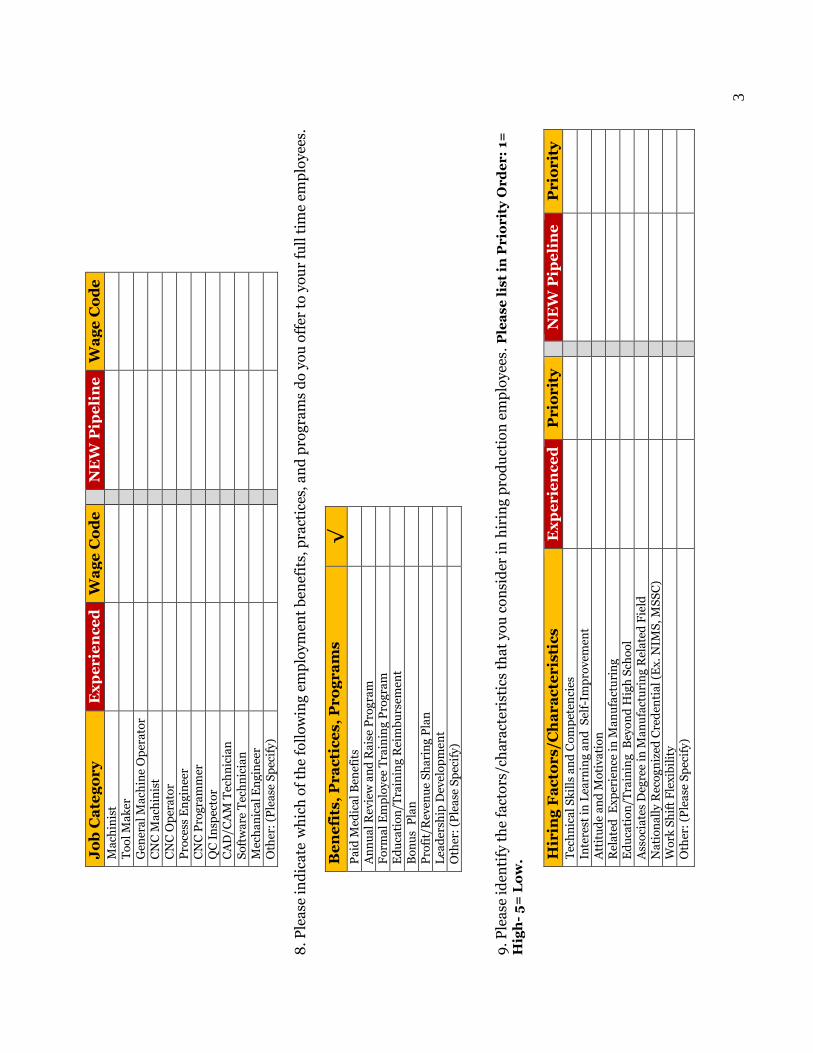

Job

Cla

ssif

icat

ion

s R

epla

cem

ent

Est

. N

o.

N

EW

E

st.

No.

P

rior

ity

Pri

orit

y

2014

20

12

2014

20

12

M

achi

nist

2

3

4

3

Tool

Mak

er

5 6

8 6

G

ener

al M

achi

ne O

pera

tor

7 4

7 4

C

NC

Mac

hini

st

1 1

1 1

C

NC

Ope

rato

r 6

5

3

2

Proc

ess

Eng

inee

r 3

7

6

8

CN

C P

rogr

amm

er

8 10

5

7

QC

Insp

ecto

r 4

2

2

5

CA

D/C

AM

Tec

hnic

ian

9 8

10

10

M

echa

nica

l Eng

inee

r 10

9

9 9

So

ftw

are

Tech

nici

an

11

11

11

11

O

ther

:(Pl

ease

Spe

cify

)

7

Th

e hi

ghes

t pri

orit

y ne

ed fo

r bo

th r

epla

cem

ent a

nd n

ew p

ipel

ine

prod

ucti

on w

orke

rs a

long

the

adva

nced

man

ufac

turi

ng

wor

kfor

ce p

ipel

ine

cont

inue

s to

be

for

CN

C M

ach

inis

ts. T

his

need

has

not

cha

nged

from

the

2012

sur

vey

and

indi

cate

s th

at

iden

tify

ing

qual

ified

app

lican

ts w

ith

the

requ

isit

e sk

ills

to fi

ll th

is jo

b cl

assi

ficat

ion

cont

inue

to b

e a

chal

leng

e.

The

need

for

Mac

hin

ists

rem

ains

a c

onsi

sten

t and

hig

h pr

iori

ty b

oth

for

repl

acem

ent a

s w

ell a

s fo

r ne

w p

ipel

ine

prod

ucti

on

wor

kers

. Sim

ilar

to C

NC

Mac

hini

sts,

iden

tify

ing

qual

ified

app

lican

ts w

ith

the

requ

isit

e sk

ills

and

expe

rien

ce to

fill

this

job

clas

sific

atio

n w

ill c

onti

nue

to b

e di

ffic

ult.

Fi

ndin

g qu

alifi

ed Q

ual

ity

Con

trol

In

spec

tors

rem

ains

a c

onsi

sten

t nee

d fo

r th

e re

gion

al c

lust

er c

ompa

nies

, and

ref

lect

s th

e va

lue-

adde

d w

ork

that

SM

Es

are

bei

ng r

equi

red

to p

erfo

rm b

y th

e O

EM

’s a

nd s

yste

m in

tegr

ator

s. T

his

is a

str

ong

prio

rity

am

ong

the

regi

onal

com

pani

es, a

nd d

evel

op p

rogr

ams

that

res

pond

to th

is n

eed

is c

riti

cal.

T

he n

eed

for

repl

acem

ent P

roce

ss E

ngi

nee

rs h

as in

crea

sed

dram

atic

ally

from

the

2012

sur

vey

findi

ngs

and

appe

ars

to b

e tr

endi

ng u

pwar

d.

Rec

omm

end

atio

ns

C

ompa

nies

will

nee

d to

dev

elop

a c

ompr

ehen

sive

str

ateg

y th

at in

clud

es u

pgra

ding

the

tech

nica

l com

pete

ncie

s of

thei

r in

cum

bent

w

orke

rs b

y im

plem

enti

ng i

nter

nal

cros

s-tr

aini

ng p

rogr

ams

and

wor

king

wit

h th

e PM

RA

P pr

ojec

t te

am t

o im

plem

ent

colle

ge

cred

it a

nd “

shor

t cou

rses

” th

at w

ill p

rovi

de e

mpl

oyee

s w

ith

very

pre

scri

ptiv

e te

chni

cal c

ompe

tenc

ies.

Fund

ing

mus

t con

tinu

e to

be

acce

ssib

le th

at w

ill a

llow

for

a st

ruct

ured

, seq

uent

ial r

espo

nse

to p

repa

ring

the

incu

mbe

nt w

orkf

orce

w

ith

the

skill

s re

quir

ed to

fill

thes

e cr

itic

al, h

ard

to fi

ll po

siti

ons.

7.

Usi

ng

the

Wag

e S

cale

bel

ow, p

leas

e in

dic

ate

you

r av

erag

e H

ou

rly

Wag

e R

ange

for

th

e fo

llow

ing

pos

itio

ns

by

ente

rin

g th

e W

age

Cod

e n

ext

to e

ach

pos

itio

n f

or b

oth

exp

erie

nce

d a

nd

new

pip

elin

e em

plo

yees

.

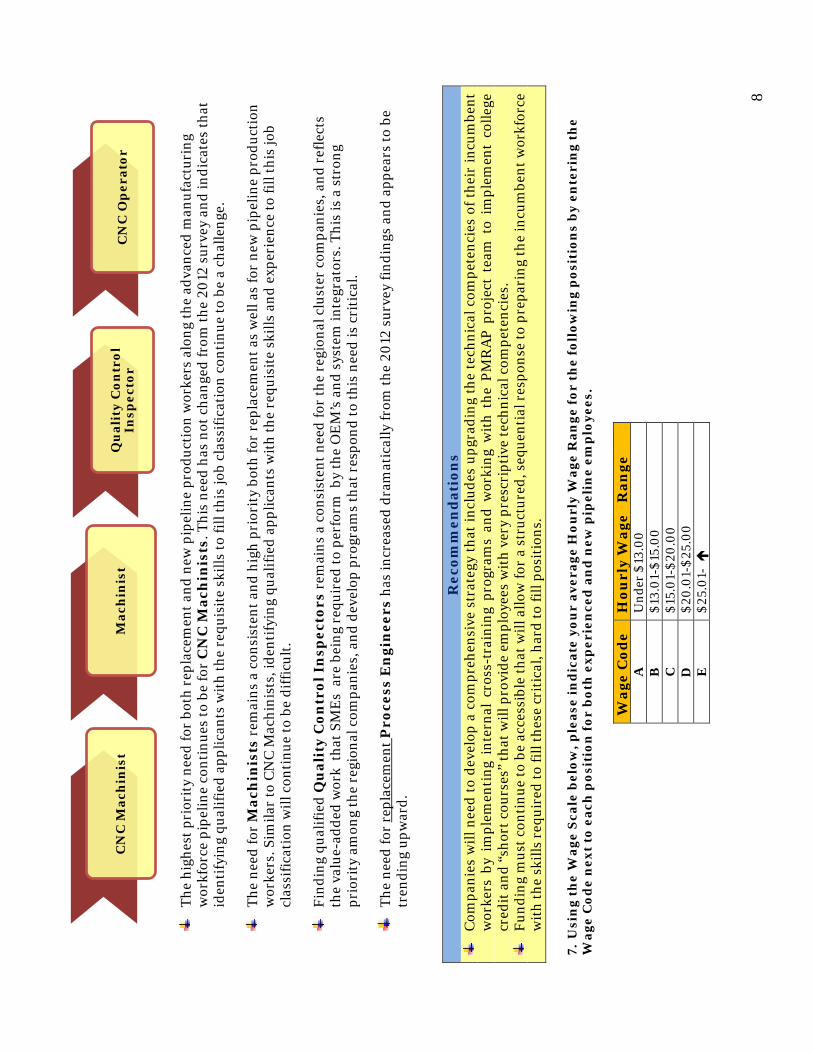

Wag

e C

ode

Hou

rly

Wag

e R

ange

A

Und

er $

13.0

0

B

$1

3.01

-$15

.00

C

$1

5.01

-$20

.00

D

$2

0.01

-$25

.00

E

$2

5.01

-

CN

C M

ach

inis

t M

ach

inis

t Q

ual

ity

Con

trol

In

spec

tor

CN

C O

per

ator

8

Jo

b C

ateg

ory

Exp

erie

nce

d

Wag

e C

ode

N

EW

Pip

elin

e W

age

Cod

e M

achi

nist

D

C

Tool

Mak

er

D

C

G

ener

al M

achi

ne O

pera

tor

C

B

C

NC

Mac

hini

st

D

C

C

NC

Ope

rato

r

C

C

Proc

ess

Eng

inee

r

E

D

CN

C P

rogr

amm

er

E

D

Q

C In

spec

tor

D

C

C

AD

/CA

M T

echn

icia

n

D

C

Soft

war

e Te

chni

cian

E

B

Mec

hani

cal E

ngin

eer

E

D

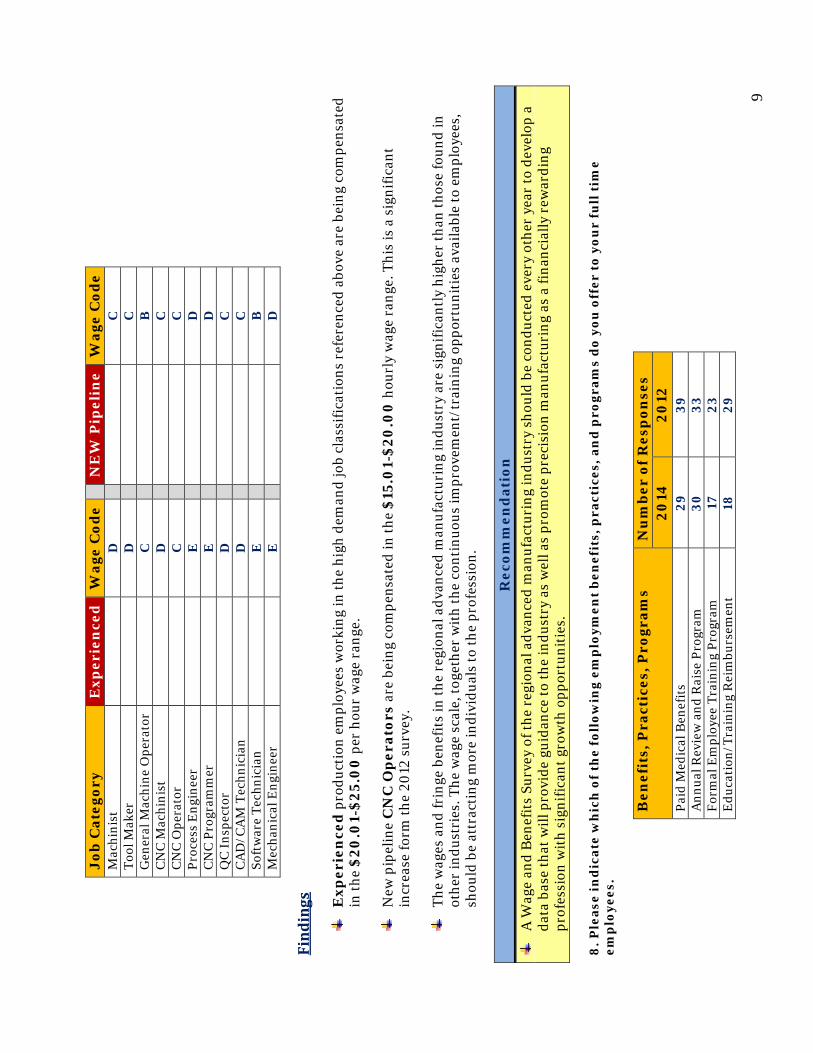

Find

ings

E

xper

ien

ced

pro

duct

ion

empl

oyee

s w

orki

ng in

the

high

dem

and

job

clas

sific

atio

ns r

efer

ence

d ab

ove

are

bein

g co

mpe

nsat

ed

in th

e $2

0.0

1-$2

5.0

0 p

er h

our

wag

e ra

nge.

N

ew p

ipel

ine

CN

C O

per

ator

s ar

e be

ing

com

pens

ated

in th

e $1

5.0

1-$2

0.0

0 h

ourl

y w

age

rang

e. T

his

is a

sig

nific

ant

incr

ease

form

the

2012

sur

vey.

Th

e w

ages

and

frin

ge b

enef

its

in th

e re

gion

al a

dvan

ced

man

ufac

turi

ng in

dust

ry a

re s

igni

fican

tly

high

er th

an th

ose

foun

d in

ot

her

indu

stri

es. T

he w

age

scal

e, to

geth

er w

ith

the

cont

inuo

us im

prov

emen

t/tr

aini

ng o

ppor

tuni

ties

ava

ilabl

e to

em

ploy

ees,

sh

ould

be

attr

acti

ng m

ore

indi

vidu

als

to th

e pr

ofes

sion

.

Rec

omm

end

atio

n

A

Wag

e an

d B

enef

its

Surv

ey o

f the

reg

iona

l adv

ance

d m

anuf

actu

ring

indu

stry

sho

uld

be c

ondu

cted

eve

ry o

ther

yea

r to

dev

elop

a

data

bas

e th

at w

ill p

rovi

de g

uida

nce

to th

e in

dust

ry a

s w

ell a

s pr

omot

e pr

ecis

ion

man

ufac

turi

ng a

s a

finan

cial

ly r

ewar

ding

pr

ofes

sion

wit

h si

gnifi

cant

gro

wth

opp

ortu

niti

es.

8. P

leas

e in

dic

ate

wh

ich

of

the

foll

owin

g em

plo

ymen

t b

enef

its,

pra

ctic

es, a

nd

pro

gram

s d

o yo

u o

ffer

to

you

r fu

ll t

ime

emp

loye

es.

B

enef

its,

Pra

ctic

es, P

rogr

ams

N

um

ber

of R

esp

onse

s 20

14

2012

Pa

id M

edic

al B

enef

its

29

39

Ann

ual R

evie

w a

nd R

aise

Pro

gram

30

33

Fo

rmal

Em

ploy

ee T

rain

ing

Prog

ram

17

23

E

duca

tion

/Tra

inin

g R

eim

burs

emen

t 18

29

9

Ben

efit

s, P

ract

ices

, Pro

gram

s

Nu

mbe

r of

Res

pon

ses

2014

20

12

Bon

us P

lan

20

22

Prof

it/R

even

ue S

hari

ng P

lan

15

17

Lead

ersh

ip D

evel

opm

ent

14

19

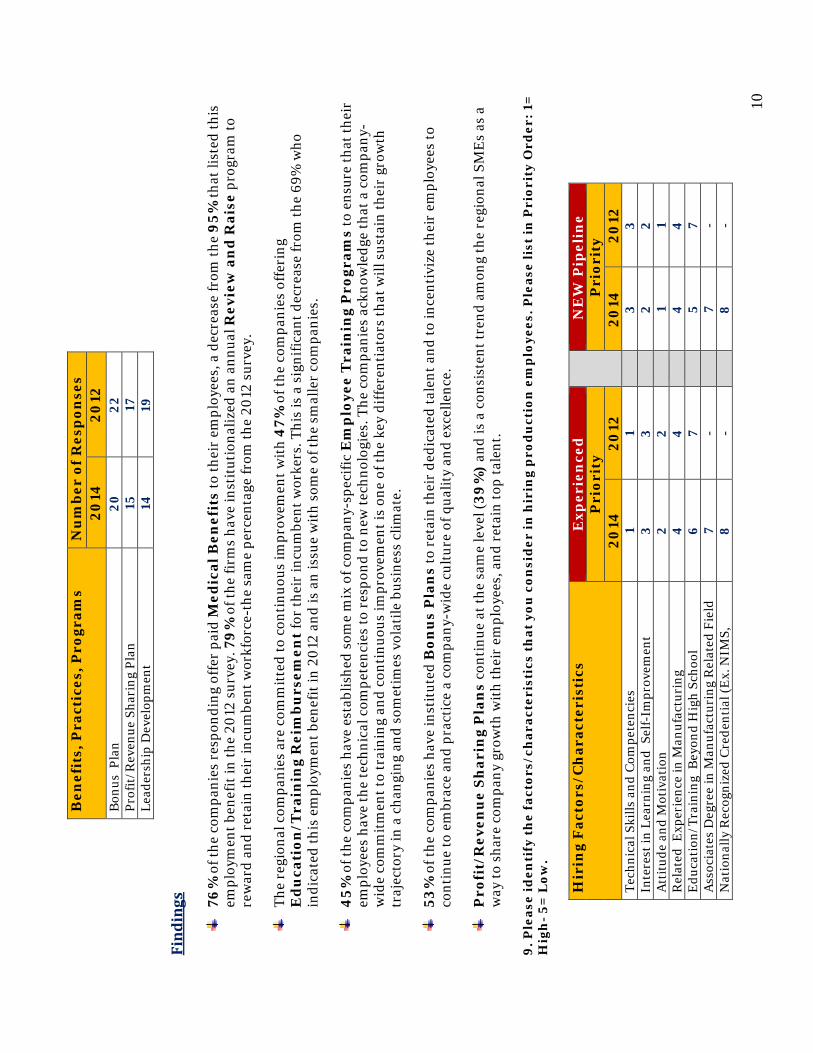

Find

ings

76

% o

f the

com

pani

es r

espo

ndin

g of

fer

paid

Med

ical

Ben

efit

s to

thei

r em

ploy

ees,

a d

ecre

ase

from

the

95%

that

list

ed th

is

empl

oym

ent b

enef

it in

the

2012

sur

vey.

79%

of t

he fi

rms

have

inst

itut

iona

lized

an

annu

al R

evie

w a

nd

Rai

se p

rogr

am to

re

war

d an

d re

tain

thei

r in

cum

bent

wor

kfor

ce-t

he s

ame

perc

enta

ge fr

om th

e 20

12 s

urve

y.

The

regi

onal

com

pani

es a

re c

omm

itte

d to

con

tinu

ous

impr

ovem

ent w

ith

47%

of t

he c

ompa

nies

off

erin

g E

du

cati

on/T

rain

ing

Rei

mbu

rsem

ent

for

thei

r in

cum

bent

wor

kers

. Thi

s is

a s

igni

fican

t dec

reas

e fr

om th

e 69

% w

ho

indi

cate

d th

is e

mpl

oym

ent b

enef

it in

201

2 an

d is

an

issu

e w

ith

som

e of

the

smal

ler

com

pani

es.

45%

of t

he c

ompa

nies

hav

e es

tabl

ishe

d so

me

mix

of c

ompa

ny-s

peci

fic E

mp

loye

e T

rain

ing

Pro

gram

s to

ens

ure

that

thei

r em

ploy

ees

have

the

tech

nica

l com

pete

ncie

s to

res

pond

to n

ew te

chno

logi

es. T

he c

ompa

nies

ack

now

ledg

e th

at a

com

pany

-w

ide

com

mit

men

t to

trai

ning

and

con

tinu

ous

impr

ovem

ent i

s on

e of

the

key

diff

eren

tiat

ors

that

will

sus

tain

thei

r gr

owth

tr

ajec

tory

in a

cha

ngin

g an

d so

met

imes

vol

atile

bus

ines

s cl

imat

e.

53%

of t

he c

ompa

nies

hav

e in

stit

uted

Bon

us

Pla

ns

to r

etai

n th

eir

dedi

cate

d ta

lent

and

to in

cent

iviz

e th

eir

empl

oyee

s to

co

ntin

ue to

em

brac

e an

d pr

acti

ce a

com

pany

-wid

e cu

ltur

e of

qua

lity

and

exce

llenc

e.

Pro

fit/

Rev

enu

e Sh

arin

g P

lan

s co

ntin

ue a

t the

sam

e le

vel (

39%

) an

d is

a c

onsi

sten

t tre

nd a

mon

g th

e re

gion

al S

ME

s as

a

way

to s

hare

com

pany

gro

wth

wit

h th

eir

empl

oyee

s, a

nd r

etai

n to

p ta

lent

.

9. P

leas

e id

enti

fy t

he

fact

ors/

char

acte

rist

ics

that

you

con

sid

er in

hir

ing

pro

du

ctio

n e

mp

loye

es. P

leas

e li

st in

Pri

orit

y O

rder

: 1=

H

igh

- 5=

Low

.

Hir

ing

Fac

tors

/Ch

arac

teri

stic

s E

xper

ien

ced

NE

W P

ipel

ine

Pri

orit

y P

rior

ity

2014

20

12

2014

20

12

Tech

nica

l Ski

lls a

nd C

ompe

tenc

ies

1 1

3

3 In

tere

st in

Lea

rnin

g an

d S

elf-

Impr

ovem

ent

3 3

2

2 A

ttit

ude

and

Mot

ivat

ion

2

2

1 1

Rel

ated

Exp

erie

nce

in M

anuf

actu

ring

4

4

4

4

Edu

cati

on/T

rain

ing

Bey

ond

Hig

h Sc

hool

6

7

5

7 A

ssoc

iate

s D

egre

e in

Man

ufac

turi

ng R

elat

ed F

ield

7

-

7 -

Nat

iona

lly R

ecog

nize

d C

rede

ntia

l (E

x. N

IMS,

8

-

8

-

10

Hir

ing

Fac

tors

/Ch

arac

teri

stic

s E

xper

ien

ced

NE

W P

ipel

ine

Pri

orit

y P

rior

ity

2014

20

12

2014

20

12

MSS

C)

Wor

k Sh

ift F

lexi

bilit

y 5

5

6

6

Pote

ntia

l for

Car

eer

mob

ility

Wit

hin

Com

pany

-

6

-

5 O

ther

: (Pl

ease

Spe

cify

)

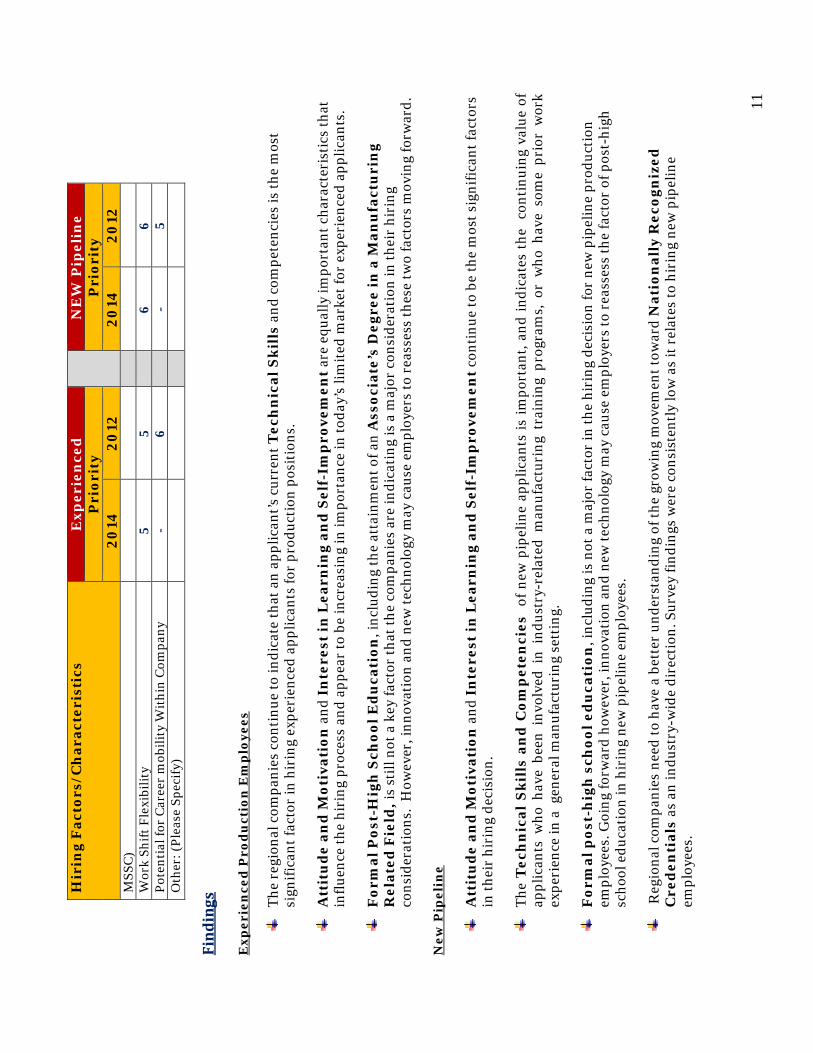

Find

ings

E

xper

ien

ced

Pro

du

ctio

n E

mp

loye

es

The

regi

onal

com

pani

es c

onti

nue

to in

dica

te th

at a

n ap

plic

ant’s

cur

rent

Tec

hn

ical

Ski

lls

and

com

pete

ncie

s is

the

mos

t si

gnifi

cant

fact

or in

hir

ing

expe

rien

ced

appl

ican

ts fo

r pr

oduc

tion

pos

itio

ns.

Att

itu

de

and

Mot

ivat

ion

and

In

tere

st in

Lea

rnin

g an

d S

elf-

Imp

rove

men

t are

equ

ally

impo

rtan

t cha

ract

eris

tics

that

in

fluen

ce th

e hi

ring

pro

cess

and

app

ear

to b

e in

crea

sing

in im

port

ance

in to

day’

s lim

ited

mar

ket f

or e

xper

ienc

ed a

pplic

ants

.

F

orm

al P

ost-

Hig

h S

choo

l Ed

uca

tion

, inc

ludi

ng th

e at

tain

men

t of a

n A

ssoc

iate

’s D

egre

e in

a M

anu

fact

uri

ng

Rel

ated

Fie

ld, i

s st

ill n

ot a

key

fact

or th

at th

e co

mpa

nies

are

indi

cati

ng is

a m

ajor

con

side

rati

on in

thei

r hi

ring

co

nsid

erat

ions

. H

owev

er, i

nnov

atio

n an

d ne

w te

chno

logy

may

cau

se e

mpl

oyer

s to

rea

sses

s th

ese

two

fact

ors

mov

ing

forw

ard.

New

Pip

elin

e

A

ttit

ud

e an

d M

otiv

atio

n a

nd I

nte

rest

in L

earn

ing

and

Sel

f-Im

pro

vem

ent c

onti

nue

to b

e th

e m

ost s

igni

fican

t fac

tors

in

thei

r hi

ring

dec

isio

n.

The

Tec

hn

ical

Ski

lls

and

Com

pet

enci

es o

f new

pip

elin

e ap

plic

ants

is im

port

ant,

and

indi

cate

s th

e c

onti

nuin

g va

lue

of

appl

ican

ts w

ho h

ave

been

inv

olve

d in

ind

ustr

y-re

late

d m

anuf

actu

ring

tra

inin

g pr

ogra

ms,

or

who

hav

e so

me

prio

r w

ork

expe

rien

ce in

a g

ener

al m

anuf

actu

ring

set

ting

.

F

orm

al p

ost-

hig

h s

choo

l ed

uca

tion

, inc

ludi

ng is

not

a m

ajor

fact

or in

the

hiri

ng d

ecis

ion

for

new

pip

elin

e pr

oduc

tion

em

ploy

ees.

Goi

ng fo

rwar

d ho

wev

er, i

nnov

atio

n an

d ne

w te

chno

logy

may

cau

se e

mpl

oyer

s to

rea

sses

s th

e fa

ctor

of p

ost-

high

sc

hool

edu

cati

on in

hir

ing

new

pip

elin

e em

ploy

ees.

R

egio

nal c

ompa

nies

nee

d to

hav

e a

bett

er u

nder

stan

ding

of t

he g

row

ing

mov

emen

t tow

ard

Nat

ion

ally

Rec

ogn

ized

C

red

enti

als

as a

n in

dust

ry-w

ide

dire

ctio

n. S

urve

y fin

ding

s w

ere

cons

iste

ntly

low

as

it r

elat

es to

hir

ing

new

pip

elin

e em

ploy

ees.

11

10. W

hic

h o

f th

e fo

llow

ing

com

pet

enci

es/a

ttri

bu

tes

wou

ld y

ou li

ke n

ew p

ipel

ine

emp

loye

es t

o p

osse

ss?

Ple

ase

list

Top

3

Com

pet

enci

es/A

ttri

bu

tes

in P

rior

ity

Ord

er.

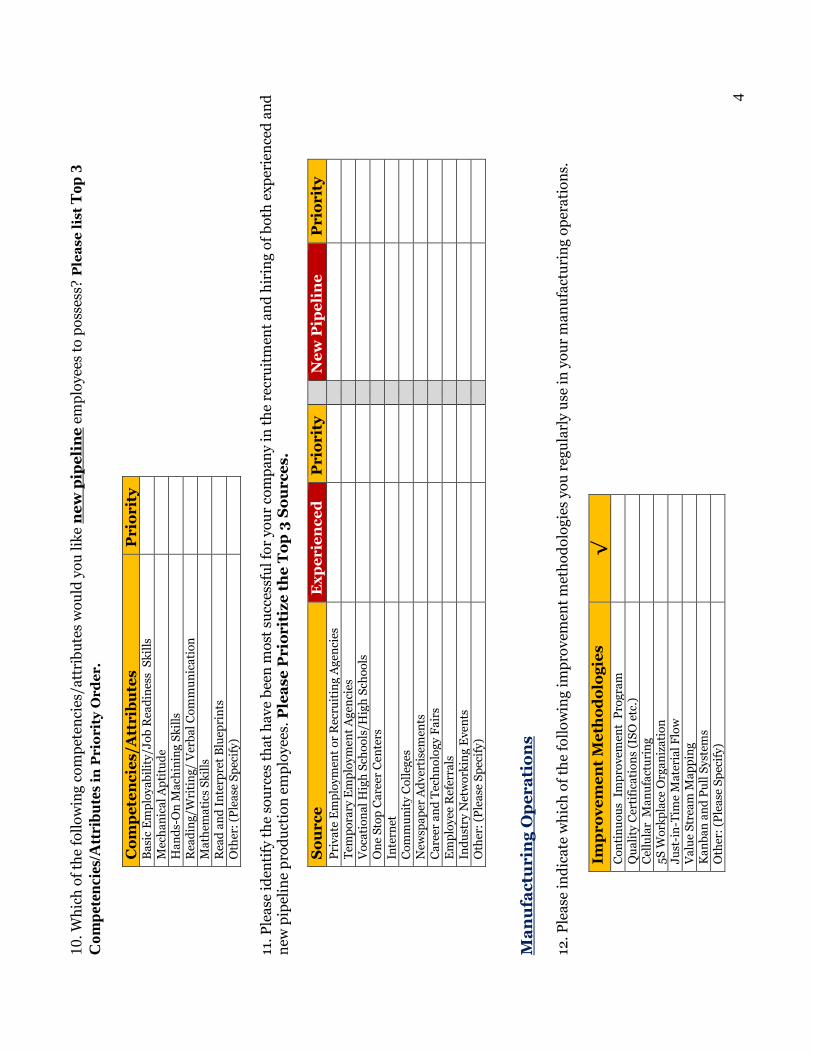

C

omp

eten

cies

/Att

ribu

tes

Pri

orit

y 20

14

2012

B

asic

Em

ploy

abili

ty/J

ob R

eadi

ness

Ski

lls

1 1

Mec

hani

cal A

ptit

ude

2

2 H

ands

-On

Mac

hini

ng S

kills

3

3 R

eadi

ng/W

riti

ng/

Ver

bal C

omm

unic

atio

n

M

athe

mat

ics

Skill

s

R

ead

and

Inte

rpre

t Blu

epri

nts

Oth

er: (

Plea

se S

peci

fy)

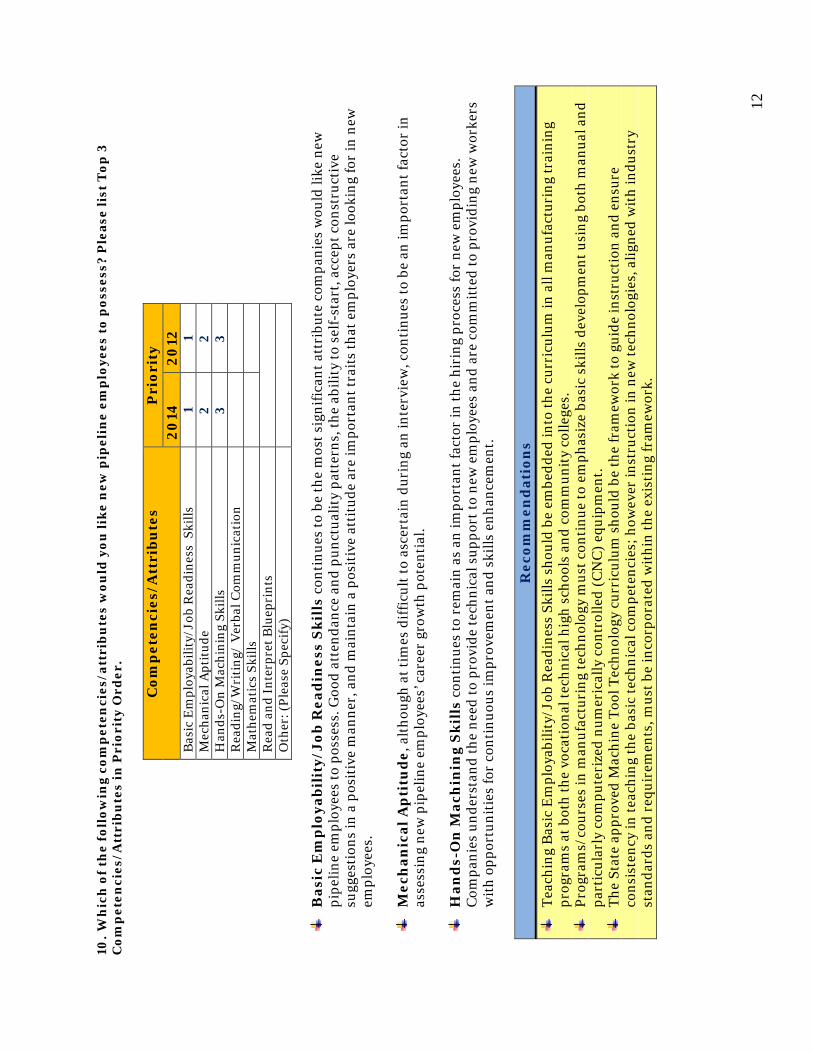

B

asic

Em

plo

yabi

lity

/Job

Rea

din

ess

Ski

lls

cont

inue

s to

be

the

mos

t sig

nific

ant a

ttri

bute

com

pani

es w

ould

like

new

pi

pelin

e em

ploy

ees

to p

osse

ss. G

ood

atte

ndan

ce a

nd p

unct

ualit

y pa

tter

ns, t

he a

bilit

y to

sel

f-st

art,

acce

pt c

onst

ruct

ive

su

gges

tion

s in

a p

osit

ive

man

ner,

and

mai

ntai

n a

posi

tive

att

itud

e ar

e im

port

ant t

rait

s th

at e

mpl

oyer

s ar

e lo

okin

g fo

r in

new

em

ploy

ees.

M

ech

anic

al A

pti

tud

e, a

ltho

ugh

at ti

mes

diff

icul

t to

asce

rtai

n du

ring

an

inte

rvie

w, c

onti

nues

to b

e an

impo

rtan

t fac

tor

in

asse

ssin

g ne

w p

ipel

ine

empl

oyee

s’ c

aree

r gr

owth

pot

enti

al.

Han

ds-

On

Mac

hin

ing

Ski

lls

cont

inue

s to

rem

ain

as a

n im

port

ant f

acto

r in

the

hiri

ng p

roce

ss fo

r ne

w e

mpl

oyee

s.

Com

pani

es u

nder

stan

d th

e ne

ed to

pro

vide

tech

nica

l sup

port

to n

ew e

mpl

oyee

s an

d ar

e co

mm

itte

d to

pro

vidi

ng n

ew w

orke

rs

wit

h op

port

unit

ies

for

cont

inuo

us im

prov

emen

t and

ski

lls e

nhan

cem

ent.

Rec

omm

end

atio

ns

Te

achi

ng B

asic

Em

ploy

abili

ty/J

ob R

eadi

ness

Ski

lls s

houl

d be

em

bedd

ed in

to th

e cu

rric

ulum

in a

ll m

anuf

actu

ring

trai

ning

pr

ogra

ms

at b

oth

the

voca

tion

al te

chni

cal h

igh

scho

ols

and

com

mun

ity

colle

ges.

Prog

ram

s/co

urse

s in

man

ufac

turi

ng te

chno

logy

mus

t con

tinu

e to

em

phas

ize

basi

c sk

ills

deve

lopm

ent u

sing

bot

h m

anua

l and

pa

rtic

ular

ly c

ompu

teri

zed

num

eric

ally

con

trol

led

(CN

C) e

quip

men

t.

Th

e St

ate

appr

oved

Mac

hine

Too

l Tec

hnol

ogy

curr

icul

um s

houl

d be

the

fram

ewor

k to

gui

de in

stru

ctio

n an

d en

sure

co

nsis

tenc

y in

teac

hing

the

basi

c te

chni

cal c

ompe

tenc

ies;

how

ever

inst

ruct

ion

in n

ew te

chno

logi

es, a

ligne

d w

ith

indu

stry

st

anda

rds

and

requ

irem

ents

, mus

t be

inco

rpor

ated

wit

hin

the

exis

ting

fram

ewor

k.

12

11. P

leas

e id

enti

fy t

he

sou

rces

th

at h

ave

bee

n m

ost

succ

essf

ul f

or y

our

com

pan

y in

th

e re

cru

itm

ent

and

hir

ing

of b

oth

ex

per

ien

ced

an

d n

ew p

ipel

ine

pro

du

ctio

n e

mp

loye

es. P

leas

e P

rior

itiz

e th

e T

op 3

Sou

rces

. Fi

ndin

gs

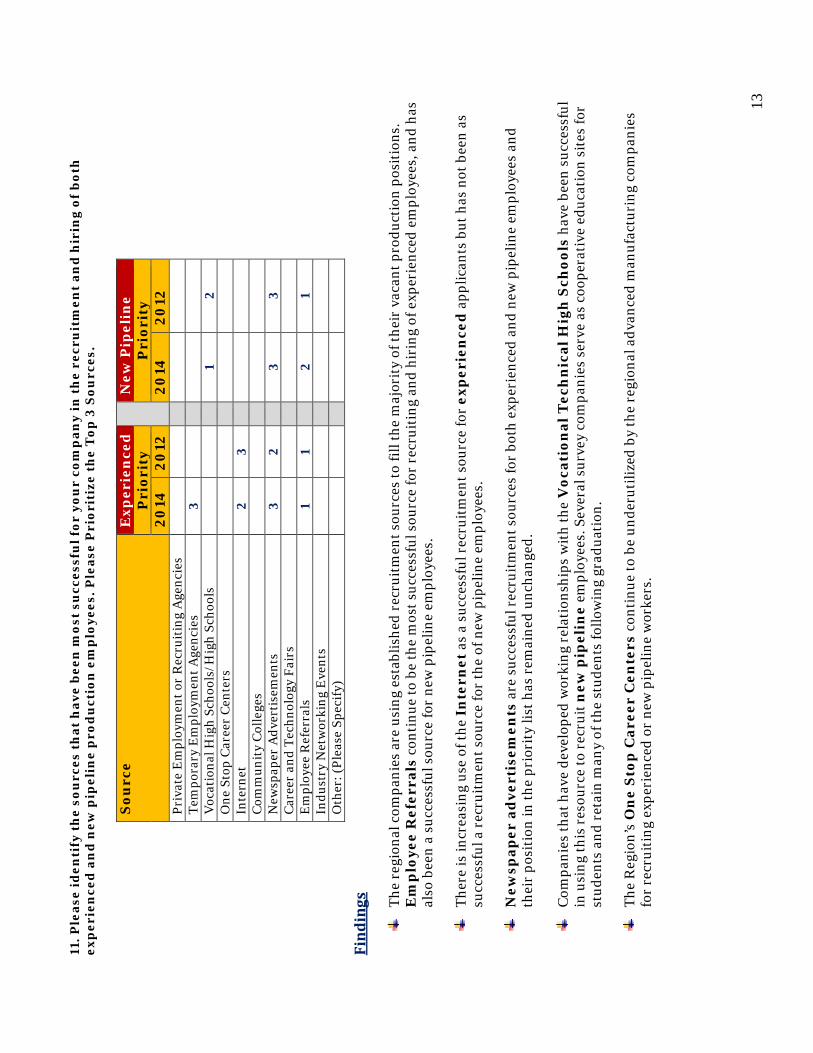

The

regi

onal

com

pani

es a

re u

sing

est

ablis

hed

recr

uitm

ent s

ourc

es to

fill

the

maj

orit

y of

thei

r va

cant

pro

duct

ion

posi

tion

s.

Em

plo

yee

Ref

erra

ls c

onti

nue

to b

e th

e m

ost s

ucce

ssfu

l sou

rce

for

recr

uiti

ng a

nd h

irin

g of

exp

erie

nced

em

ploy

ees,

and

has

al

so b

een

a su

cces

sful

sou

rce

for

new

pip

elin

e em

ploy

ees.

Th

ere

is in

crea

sing

use

of t

he I

nte

rnet

as

a su

cces

sful

rec

ruit

men

t sou

rce

for

exp

erie

nce

d a

pplic

ants

but

has

not

bee

n as

su

cces

sful

a r

ecru

itm

ent s

ourc

e fo

r th

e of

new

pip

elin

e em

ploy

ees.

N

ewsp

aper

ad

vert

isem

ents

are

suc

cess

ful r

ecru

itm

ent s

ourc

es fo

r bo

th e

xper

ienc

ed a

nd n

ew p

ipel

ine

empl

oyee

s an

d th

eir

posi

tion

in th

e pr

iori

ty li

st h

as r

emai

ned

unch

ange

d.

Com

pani

es th

at h

ave

deve

lope

d w

orki

ng r

elat

ions

hips

wit

h th

e V

ocat

ion

al T

ech

nic

al H

igh

Sch

ools

hav

e be

en s

ucce

ssfu

l in

usi

ng th

is r

esou

rce

to r

ecru

it n

ew p

ipel

ine

empl

oyee

s. S

ever

al s

urve

y co

mpa

nies

ser

ve a

s co

oper

ativ

e ed

ucat

ion

site

s fo

r st

uden

ts a

nd r

etai

n m

any

of th

e st

uden

ts fo

llow

ing

grad

uati

on.

The

Reg

ion’

s O

ne

Stop

Car

eer

Cen

ters

con

tinu

e to

be

unde

ruti

lized

by

the

regi

onal

adv

ance

d m

anuf

actu

ring

com

pani

es

for

recr

uiti

ng e

xper

ienc

ed o

r ne

w p

ipel

ine

wor

kers

.

Sou

rce

Exp

erie

nce

d

N

ew P

ipel

ine

Pri

orit

y P

rior

ity

2014

20

12

2014

20

12

Priv

ate

Em

ploy

men

t or

Rec

ruit

ing

Age

ncie

s

Tem

pora

ry E

mpl

oym

ent A

genc

ies

3

V

ocat

iona

l Hig

h Sc

hool

s/H

igh

Scho

ols

1

2 O

ne S

top

Car

eer

Cen

ters

Inte

rnet

2

3

Com

mun

ity

Col

lege

s

New

spap

er A

dver

tise

men

ts

3 2

3

3 C

aree

r an

d Te

chno

logy

Fai

rs

E

mpl

oyee

Ref

erra

ls

1 1

2

1 In

dust

ry N

etw

orki

ng E

vent

s

Oth

er: (

Plea

se S

peci

fy)

13

R

ecom

men

dat

ion

s

The

PMR

AP

proj

ect t

eam

sho

uld

faci

litat

e a

mee

ting

bet

wee

n re

pres

enta

tive

s fr

om s

elec

ted

regi

onal

com

pani

es a

nd th

e O

ne S

top

Car

eer

Cen

ters

to d

iscu

ss w

ays

to in

clud

e th

e C

ente

rs a

s a

mor

e in

tegr

al p

artn

er in

the

recr

uitm

ent p

roce

ss.

R

egio

nal c

ompa

nies

mus

t acc

eler

ate

thei

r in

volv

emen

t in

the

Coo

pera

tive

Edu

cati

on p

rogr

am a

s a

prov

en r

ecru

itm

ent m

etho

d fo

r id

enti

fyin

g ne

w p

ipel

ine

tale

nt.

S

ecti

on I

II. M

anu

fact

uri

ng

Op

erat

ion

s 12

. Ple

ase

ind

icat

e w

hic

h o

f th

e fo

llow

ing

imp

rove

men

t m

eth

odol

ogie

s yo

u r

egu

larl

y u

se in

you

r m

anu

fact

uri

ng

oper

atio

ns.

Imp

rove

men

t M

eth

odol

ogie

s N

um

ber

of R

esp

onse

s 20

14

2012

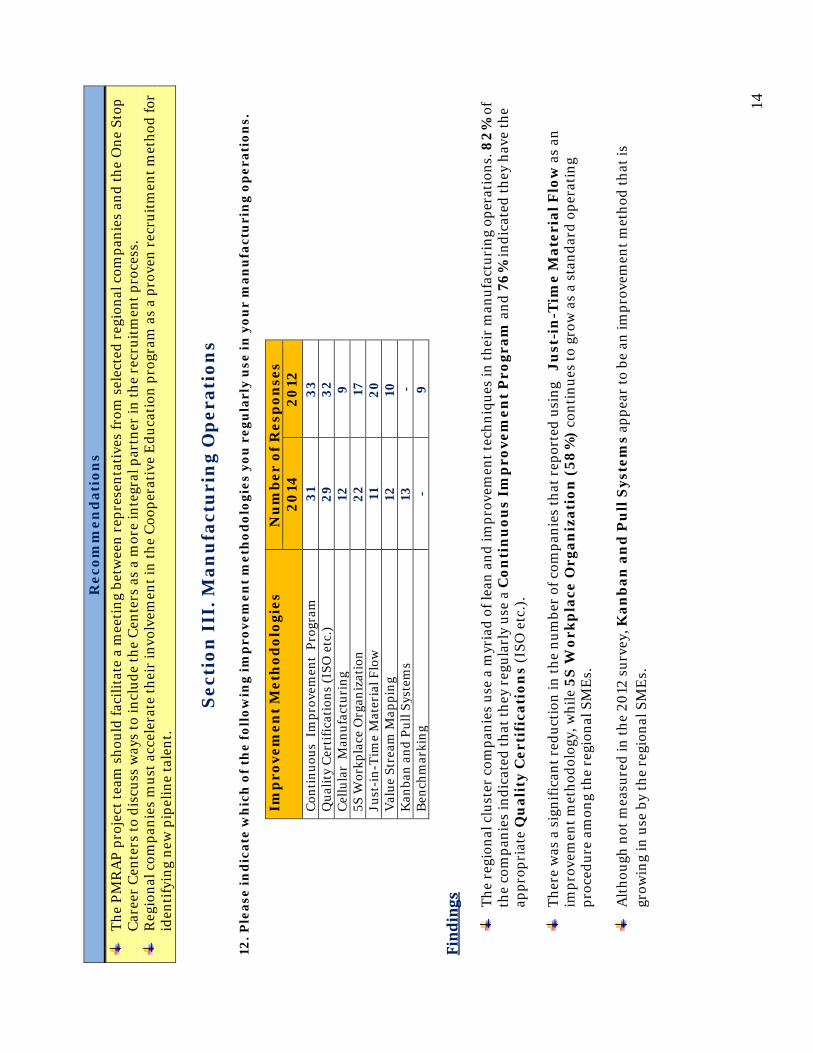

C

onti

nuou

s I

mpr

ovem

ent

Prog

ram

31

33

Q

ualit

y C

erti

ficat

ions

(IS

O e

tc.)

29

32

C

ellu

lar

Man

ufac

turi

ng

12

9

5S W

orkp

lace

Org

aniz

atio

n 22

17

Ju

st-i

n-Ti

me

Mat

eria

l Flo

w

11

20

Val

ue S

trea

m M

appi

ng

12

10

Kan

ban

and

Pull

Syst

ems

13

- B

ench

mar

king

-

9

Find

ings

Th

e re

gion

al c

lust

er c

ompa

nies

use

a m

yria

d of

lean

and

impr

ovem

ent t

echn

ique

s in

thei

r m

anuf

actu

ring

ope

rati

ons.

82%

of

the

com

pani

es in

dica

ted

that

they

reg

ular

ly u

se a

Con

tin

uou

s Im

pro

vem

ent

Pro

gram

and

76%

indi

cate

d th

ey h

ave

the

appr

opri

ate

Qu

alit

y C

erti

fica

tion

s (I

SO e

tc.)

.

Th

ere

was

a s

igni

fican

t red

ucti

on in

the

num

ber

of c

ompa

nies

that

rep

orte

d us

ing

Ju

st-i

n-T

ime

Mat

eria

l Flo

w a

s an

im

prov

emen

t met

hodo

logy

, whi

le 5

S W

orkp

lace

Org

aniz

atio

n (

58%

) co

ntin

ues

to g

row

as

a st

anda

rd o

pera

ting

pr

oced

ure

amon

g th

e re

gion

al S

ME

s.

Alt

houg

h no

t mea

sure

d in

the

2012

sur

vey,

Kan

ban

an

d P

ull

Sys

tem

s ap

pear

to b

e an

impr

ovem

ent m

etho

d th

at is

gr

owin

g in

use

by

the

regi

onal

SM

Es.

14

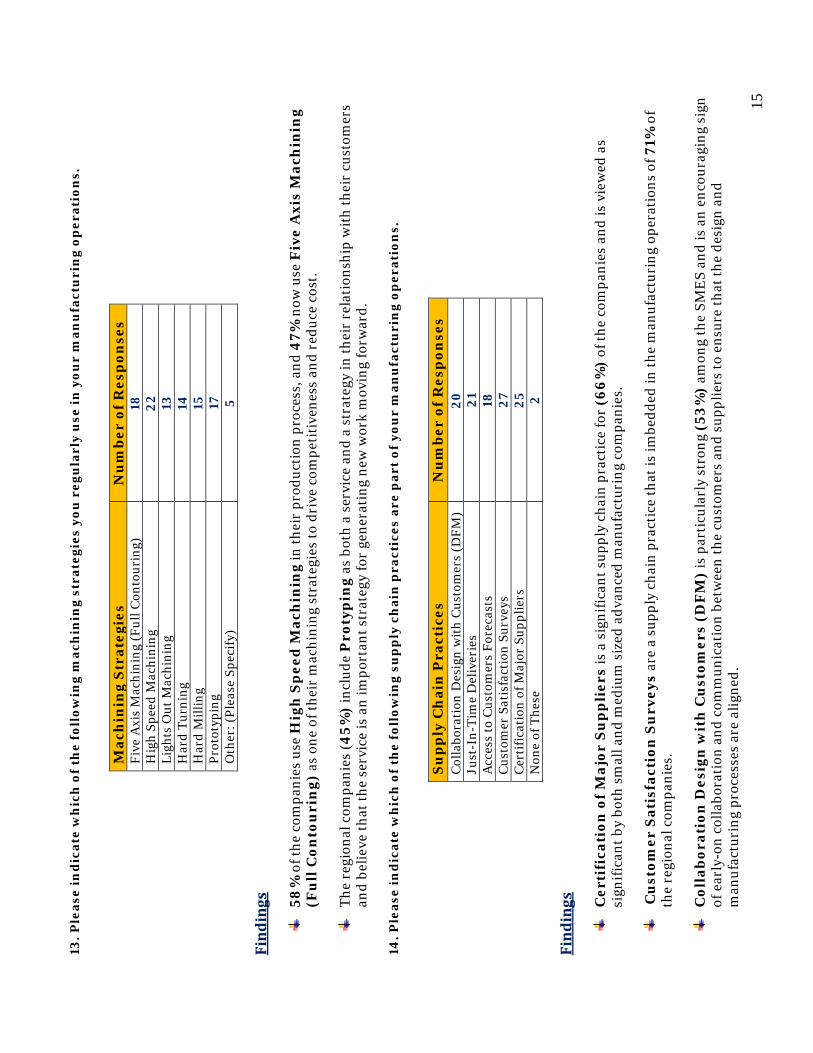

13. P

leas

e in

dic

ate

wh

ich

of

the

foll

owin

g m

ach

inin

g st

rate

gies

you

reg

ula

rly

use

in y

our

man

ufa

ctu

rin

g op