Embed Size (px)

Citation preview

1

POSITIONED FOR GROWTHBNSF Railway

John Miller Group Vice President Agricultural Products BNSF Railway

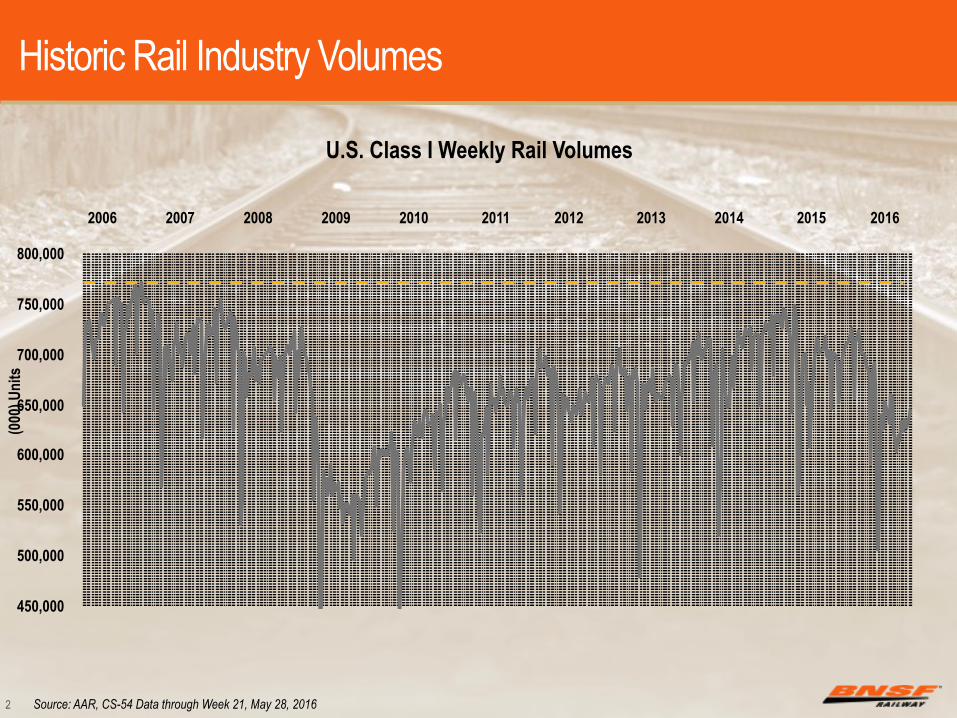

450,000

500,000

550,000

600,000

650,000

700,000

750,000

800,000

(000

) Uni

ts

Historic Rail Industry Volumes

2

U.S. Class I Weekly Rail Volumes

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Source: AAR, CS-54 Data through Week 21, May 28, 2016

Recent Volume Trends Across the U.S. Rail Industry

3

Year-over-Year Percent Change Four-Week Rolling Average Volume

U.S. Class I Rail Industry

-14%

10%

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 3 6 9 12 15 18 21

2015 2016

-7.3% year-over-year

Last 4 weeks through Week 21

Source: Association of American Railroads (AAR) through week 21; May 28, 2016

Weeks

BNSF Weekly Volume Trends

4

145

160

175

190

205

220

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52

219K215K

2006 Peak2015 Peak

2016

BNSF Railway Units Weekly Railroad Traffic Actuals Through Week 21

2007 2015

Source: Association of American Railroads (AAR) through May 28, 2016

Units

Economic ConditionsThe Good, The Bad, and The Ugly

5

ALL OTHER

WASTE AND SCRAP

FOOD AND KINDRED

CHEMICALS

LUMBER AND WOOD

GRAIN

GRAIN MILL PRODUCTS

PULP AND PAPER

CRUSHED STONE

METALLIC ORES

TRAILERS

-40% 30%-32.7%

-26.3%-20.6%-20.4%

-13.7%-7.1%-6.8%-6.6%-6.4%-6.3%-6.0%

-2.6%-1.3%

0.2%0.5%0.8%0.9%1.2%

7.6%9.8%

18.0%22.5%

U.S. Railroads (CS54 Groups, % Change in Units Handled) 2016 YTD, Most Recent 21 Weeks 2016 vs. 2015 (through May 28, 2016)

Source: Association of American Railroads (AAR) through May 28, 2016

U.S. Economic Outlook Trend 2016

6

GDP IPI Less Tech

Source: IHS Economics, May 2016

y/y percent change

2016 Annual Forecast Changes Over Time

The Rail Industry Sees Cyclical Movements Similar to GDP

7

-17%

12%

19971998

19992000

20012002

20032004

20052006

20072008

20092010 2011

20122013

20142015

U.S. Rail Volumes U.S. GDP

Percent Change Year-over-Year

Exchange RatesWall Street Journal U.S. Dollar Index

8 Source: Wall Street Journal, BUXX; June 3, 2016

64

73

82

91

100

01/01/2013 03/19/2013 06/04/2013 08/20/2013 11/05/2013 01/21/2014 04/08/2014 06/24/2014 09/09/2014 11/25/2014 02/06/2015 04/24/2015 07/10/2015 09/25/2015 12/11/2015 02/26/2016 05/13/2016

June 3, 2016 86.15

-0.7% y/y

-5% YTD

+19% vs. Jul '14

U.S. Dollar Index

BNSF is a Leading U.S. Railroad

9

• A Berkshire Hathaway company

• 32,500 route miles in 28 states and operates in three Canadian provinces

• Approximately 8,199 locomotives

• 13,000 bridges and 88 tunnels

• Moves one-fourth of the nation’s rail freight

• Operates about 1,200 freight trains per day

• Serves more than 40 ports and 25 intermodal facilities

• Leads rail industry in technological innovation

• Unlike other forms of transportation, BNSF trains operate on an infrastructure financed almost entirely by the railroad

2015 BNSFDensity Flow

10

What BNSF Carried in 2015

(thousands of units)

INDUSTRIAL PRODUCTS

1,873Y/Y CHANGE -5.9%

COAL

2,286Y/Y CHANGE +0.7%

AGRICULTURAL PRODUCTS

1,044Y/Y CHANGE +7.2%

(000) Units

CONSUMER PRODUCTS

5,066Y/Y CHANGE +0.5%

Consumer Products Commodity Breakdown

11

Domestic International Automotive

BNSF Network – Consumer Products

12

2015 BNSF Consumer ProductsDensity Flow

Consumer Products

13

The long-term outlook for Domestic intermodal is strong given the demand for Highway-to-Rail conversions

International intermodal will grow with the economy and Trans-Pacific Trade

Regulatory pressure on Truck Industry – Hours of Service, Electronic Logging Device, Drug and Alcohol Database, Speed Limiters

Consumer Products Market Drivers

14 Source: IHS Economics, FTR

GDP GROWTH VS. INTERMODAL GROWTH

37

38.8571

40.7143

42.5714

44.4286

46.2857

48.1429

50

Jan-0

8Ju

l-08

Jan-0

9Ju

l-09

Jan-1

0Ju

l-10

Jan-1

1Ju

l-11

Jan-1

2Ju

l-12

Jan-1

3Ju

l-13

Jan-1

4Ju

l-14

Jan-1

5Ju

l-15

Jan-1

6Ju

l-16

Jan-1

7Ju

l-17

Jan-1

8Ju

l-18

Jan-1

9Ju

l-19

Jan-2

0

RETAILERS INVENTORIES

0.0%

4.0%

2015Q1 2015Q2

2015Q3 2015Q4

2016Q1 2016Q2

2016Q3 2016Q4

2017Q1 2017Q2

2017Q3 2017Q4

Real GDP Less-Tech Mfg.REAL GDP VS. "LESS-TECH" MANUFACTURING OUTPUT

-15%

-7%

1%

8%

16%

20002001

20022003

20042005

20062007

20082009

20102011 2012

20132014

2015

U.S. GDP NA Intermodal

Driver Shortage (-) / Surplus (+)

'(300) '(225) '(150)

'(75) '- 75

150 225 300

2007.12008.1

2009.12010.1

2011.12012.1

2013.12014.1

2015.12016.1

2017.12018.1

15

What BNSF Carried in 2015

(thousands of units)

CONSUMER PRODUCTS

5,066Y/Y CHANGE +0.5%

INDUSTRIAL PRODUCTS

1,873Y/Y CHANGE -5.9%

AGRICULTURAL PRODUCTS

1,044Y/Y CHANGE +7.2%

(000) Units

COAL

2,286Y/Y CHANGE +0.7%

BNSF Network - Coal

16

2015 BNSF CoalDensity Flow

Coal

17

Decreased electricity generation due to record mild winter and low natural gas prices has resulted in all-time high coal inventory levels

Unfavorable export market driven by worldwide supply and strong dollar

Increased Federal regulation leads to more renewable capacity and coal plant closures in the long-term

Coal Energy MarketsLow natural gas prices and softening utility generation

18

PRB INVENTORIES

30

51

73

94

115

Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

Days of Burn Normal Days of Burn

PRB COAL BURN

16

23

31

38

45

Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

NATURAL GAS PRICE

$0

$2

$3

$5

$6

Jan-14Jul-14

Jan-15Jul-15

Jan-16Jul-16

Jan-17Jul-17

Jan-18Jul-18

Jan-19Jul-19

Jan-20Jul-20

Source: Nymex; Energy Ventures Analysis; EEI

Days

Days

WEEKLY U.S. POWER GENERATION

60,000

145,000

230,000

315,000

400,000

Jan May Jun Jul Nov Dec

2015 5 YR MIN 5 YR Range 20165 YR AVG

kWh

19

What BNSF Carried in 2015

(thousands of units)

COAL

2,286Y/Y CHANGE +0.7%

AGRICULTURAL PRODUCTS

1,044Y/Y CHANGE +7.2%

(000) Units

CONSUMER PRODUCTS

5,066Y/Y CHANGE +0.5%

INDUSTRIAL PRODUCTS

1,873Y/Y CHANGE -5.9%

Industrial Products Commodity Breakdown

20

Building ProductsPaper, Pulp, Lumber, Panel,

Rail Equipment, Transformers, Generators, Roofing Materials, Waste

Construction ProductsPipe, Sheet, Structural,

Scrap, Taconite, Aluminum, Sand, Salt, Clays, Crushed Stone, Cement, Lime, Gypsum

Petroleum ProductsCrude OilLPGAsphaltAlcohols & Solvents

Food & BeverageBeer & WineCanned GoodsPerishablesVegetables

Chemicals & PlasticsAcids, Intermediates,Caustic Soda, PVC,

Polypropylene, Polystyrene, Polyethylene

BNSF Network – Industrial Products

21

2015 BNSF Industrial ProductsDensity Flow

Industrial Products

Dramatically lower oil prices have driven down demand for petroleum and its associated products (such as frac sand and steel pipe)

Demand for residential and commercial construction materials (aggregates, cement and lumber) remains solid

22

The strong U.S. Dollar is limiting steel exports, as well as steel inputs such as taconite

Active Oil Rig Counts Bottoming OutCurrent rig count supported by improved supply-demand and pricing environment

23 Source: Baker Hughes, BTU Analytics, EIA.gov

U.S. OIL RIG COUNT

Rig

Coun

t

0

450

900

1,350

1,800

1/2/098/14/09

3/26/1011/5/10

6/17/111/27/12

9/7/124/19/13

11/27/137/11/14

2/20/1510/2/15

5/13/16

WEEKLY WTI SPOT PRICE 2009-CURRENT

$/bbl

0

30

60

90

120

Jan-09Jun-09

Dec-09Jun-10

Dec-10Jun-11

Nov-11May-12

Nov-12May-13

Nov-13May-14

Oct-14Apr-15

Oct-15Apr-16

CRUDE OIL PRODUCTION (Lower 48 States-Onshore)

Millio

n bb

ls/da

y

2

3.5

5

6.5

8

May-16Nov-15

May-15Nov-14

May-14Nov-13

May-13Nov-12

May-12Nov-11

May-11Nov-10

May-10Nov-09

May-09

NEW WELL OIL PRODUCTION PER RIG

'-

250

500

750

1,000

Jan-09Jul-09

Jan-10Jul-10

Jan-11 Jul-11 Jan-12Jul-12

Jan-13Jul-13

Jan-14Jul-14

Jan-15Jul-15

Jan-16

Bakken Eagleford Niobrara Permian

BBLS

/day

Successful Leadership – Successful Business

24

What BNSF Carried in 2015

(thousands of units)

INDUSTRIAL PRODUCTS

1,873Y/Y CHANGE -5.9%

COAL

2,286Y/Y CHANGE +0.7%

(000) Units

CONSUMER PRODUCTS

5,066Y/Y CHANGE +0.5%

AGRICULTURAL PRODUCTS

1,044Y/Y CHANGE +7.2%

Agricultural Products Commodity Breakdown

25

GrainWheat Barley Corn Soybeans Milo

Bulk FoodsSweeteners Syrups Animal Products Starch

Other Grain ProductsOils Feeds Flour Specialty Grains Oilseeds & Meals Malt

EthanolFertilizer

BNSF Network – Agricultural Products

26

2015 BNSF Agricultural ProductsDensity Flow

Agricultural Products

27

U.S. grain supplies are at their highest levels in almost 30 years after three consecutive large crops, incenting farmers to store grain

Grain exports remain challenged due to the strong U.S. dollar and high domestic/global supplies

Global demand continues to outpace supply

Agricultural Products Market Drivers

28 Source: USDA.gov; www.investing.com

60,000

65,000

70,000

75,000

80,000

2011/122012/13

2013/142014/15

2015/16

Supply DemandWORLD GRAIN SUPPLY OUTPACING DEMAND

'-

750

1,500

2,250

3,000

2011/122012/13

2013/142014/15

2015/16

CHINESE SOYBEAN IMPORTS

$70

$80

$90

$100

$110

$3

$5

$6

$8

$9

Jan-10Jul-10

Jan-11Aug-11

Feb-12Sept-12

Mar-13Oct-13

Apr-14Nov-14

May-15Nov-15

Corn Price U.S. Dollar Index

'-

875

1,750

2,625

3,500

2011/122012/13

2013/142014/15

2015/16

Corn WheatSoybeans

U.S. RECORD ENDING GRAIN STOCKS STRONG DOLLAR VS. CORN PRICE

Corn

Pric

e

Millio

n Bu

shels

Millio

n Bu

shels

Millio

n Bu

shels

19501960197019801990200020102015

Northern Migration of Crop Production –1950 -2015

29

U.S. Farm Income Decreases

30 Source: USDA (http://ers.usda.gov) – U.S. and State-Level Farm Statistics February, 2016

USDA forecasting a 40% decrease in U.S. Farm INCOME in 2016 v. 2014

Total U.S. Farm DEBT will RISE $9B year over year –

totaling $373B in 2016

Total U.S. Farm EQUITY expected to decrease by 2% in 2016

Rail Industry Capital Spend Over the Years

31

$10.0

$15.5

$21.0

$26.5

$32.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Capital Spend

Record Railroad Spending on Infrastructure & Equipment*

Source: AAR

* Capital spending + maintenance expenses. Data are for Class I railroads

$ Billions

BNSF’s Capital Investments

32

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016F

Replacement Capital Expansion PTC Locomotive Equipment

$5.8

$ Billions

2016 Capital Investments

8%12%

14%66%

Core Network and Related AssetsLocomotive, Freight Car, and Other EquipExpansion and EfficiencyPTC

2016 Capital Commitment $4.2B

$2.8 billion

Core Network & Related Assets

$600 million

Loco, Freight Car, & Other Equip

$500 million

Expansion & Efficiency

$300 million

Positive Train Control

33

34