Embed Size (px)

Citation preview

Perspectives from the Americas Recent Experiences with IFRS

Bruce MescherAugust 30, 2011

Agenda

Overview of IFRS in the Americas

Case Study: IFRS Convergence in Brazil

Best Practices & Lessons Learned

Looking Forward

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 2

Overview of IFRS in the Americas

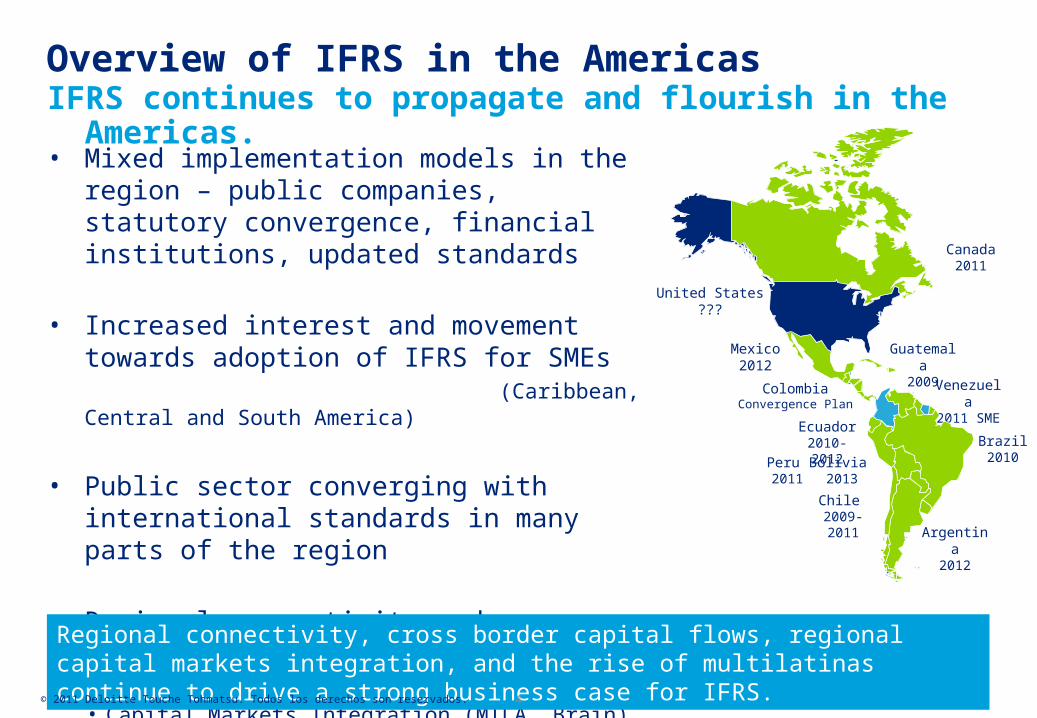

Overview of IFRS in the AmericasIFRS continues to propagate and flourish in the Americas.

• Mixed implementation models in the region – public companies, statutory convergence, financial institutions, updated standards

• Increased interest and movement towards adoption of IFRS for SMEs (Caribbean, Central and South America)

• Public sector converging with international standards in many parts of the region

• Regional connectivity and collaboration• Standard Setting – GLASS• Capital Markets Integration (MILA, Brain)

Regional connectivity, cross border capital flows, regional capital markets integration, and the rise of multilatinas continue to drive a strong business case for IFRS.

Brazil2010

Argentina2012

Chile 2009-2011

Mexico2012

Canada2011

Peru 2011

Ecuador2010-2012

ColombiaConvergence Plan

United States???

Venezuela2011 SME

Bolivia 2013

Guatemala2009

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 4

Case Study:IFRS Convergence in Brazil

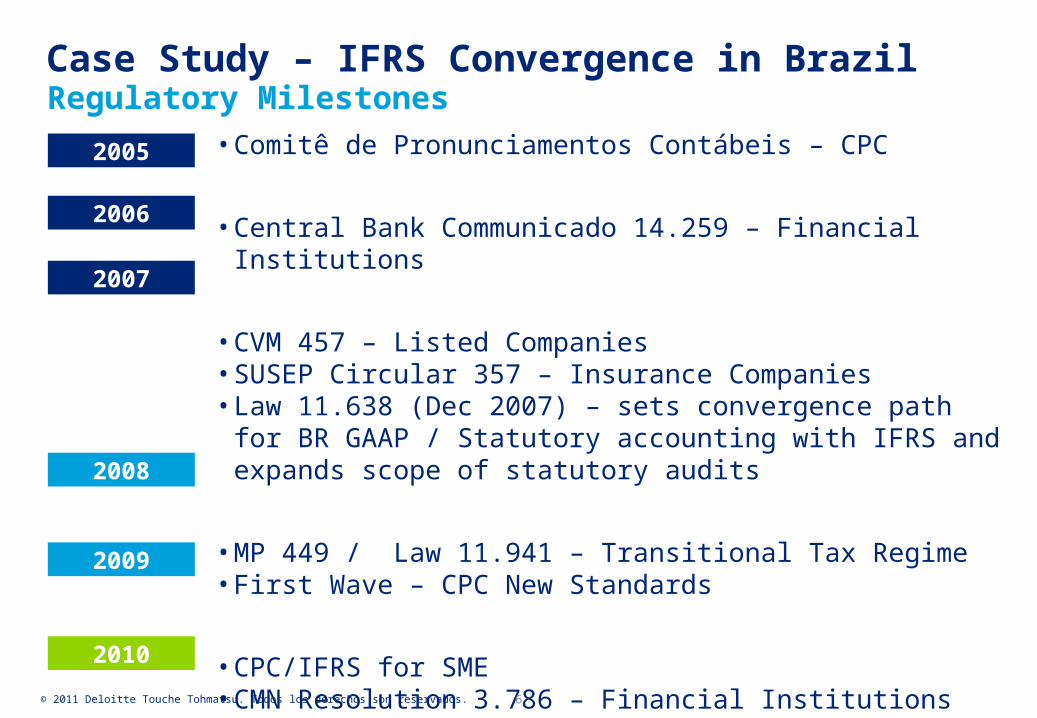

Case Study – IFRS Convergence in Brazil Regulatory Milestones

2005 • Comitê de Pronunciamentos Contábeis – CPC

• Central Bank Communicado 14.259 – Financial Institutions

• CVM 457 – Listed Companies• SUSEP Circular 357 – Insurance Companies• Law 11.638 (Dec 2007) – sets convergence path for BR GAAP /

Statutory accounting with IFRS and expands scope of statutory audits

• MP 449 / Law 11.941 – Transitional Tax Regime• First Wave – CPC New Standards

• CPC/IFRS for SME• CMN Resolution 3.786 – Financial Institutions

• First Year Full IFRS Reporting

2006

2007

2008

2009

2010

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 6

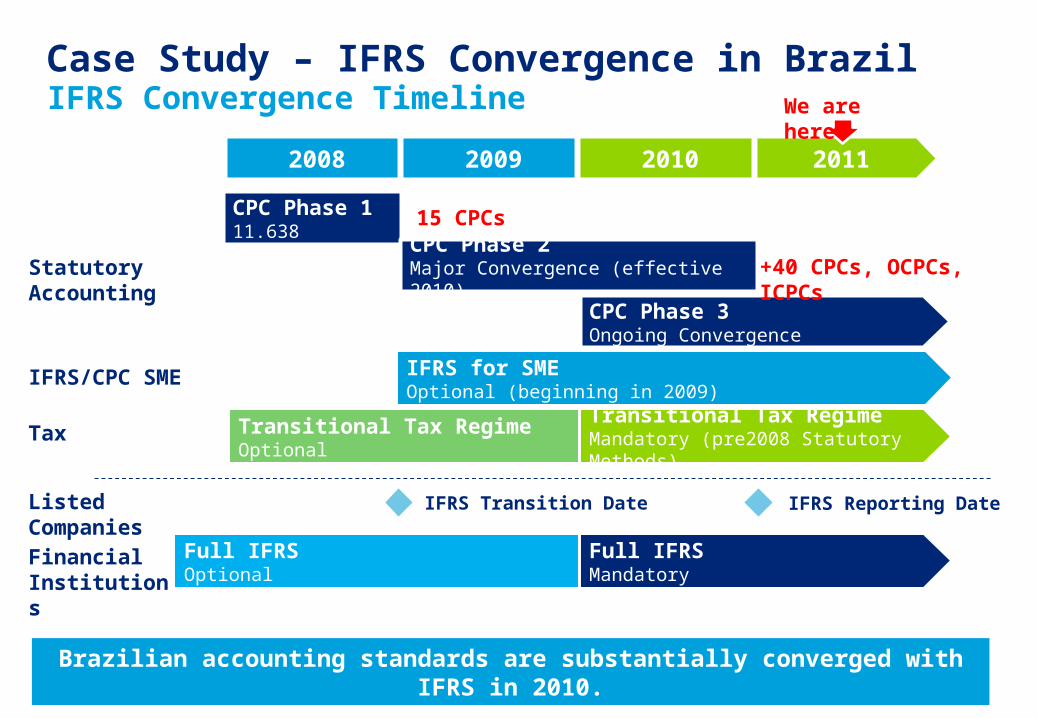

Case Study – IFRS Convergence in Brazil IFRS Convergence Timeline

2008 2009 2010 2011

CPC Phase 1 11.638

CPC Phase 2Major Convergence (effective 2010)

CPC Phase 3Ongoing Convergence

Transitional Tax RegimeOptional

Transitional Tax Regime Mandatory (pre2008 Statutory Methods)

Statutory Accounting

Tax

Listed Companies

Financial Institutions

Full IFRSOptional

Full IFRSMandatory

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 7

IFRS/CPC SME IFRS for SME Optional (beginning in 2009)

15 CPCs

+40 CPCs, OCPCs, ICPCs

We are here.

IFRS Transition Date IFRS Reporting Date

Brazilian accounting standards are substantially converged with IFRS in 2010.

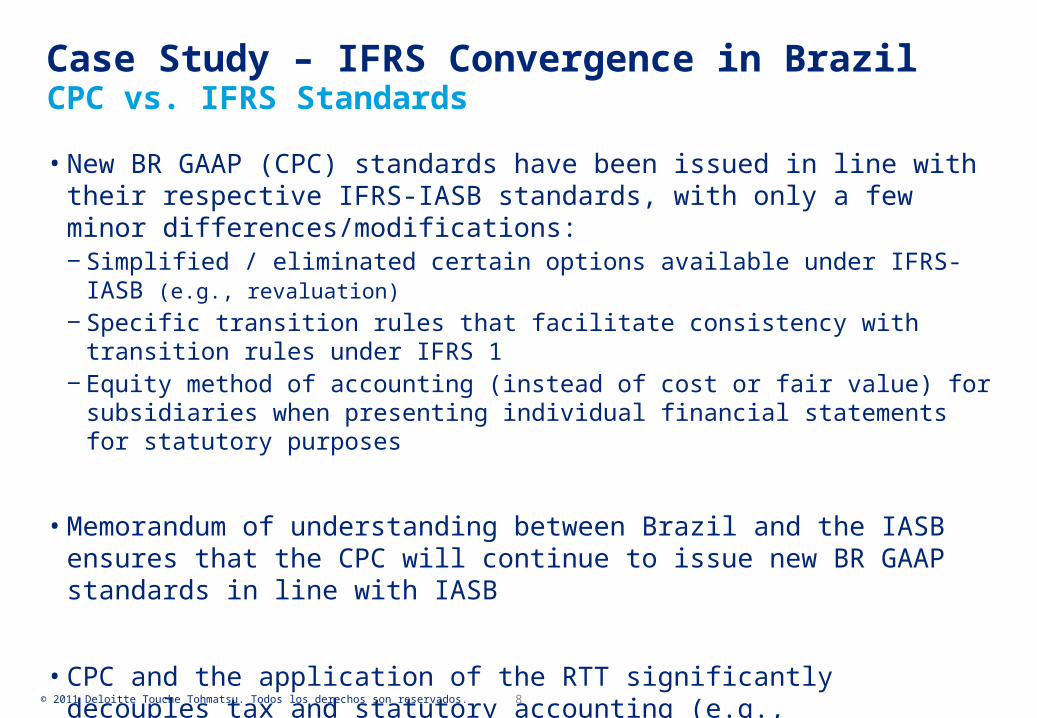

Case Study – IFRS Convergence in Brazil CPC vs. IFRS Standards

• New BR GAAP (CPC) standards have been issued in line with their respective IFRS-IASB standards, with only a few minor differences/modifications:‒ Simplified / eliminated certain options available under IFRS-IASB (e.g., revaluation)

‒ Specific transition rules that facilitate consistency with transition rules under IFRS 1 ‒ Equity method of accounting (instead of cost or fair value) for subsidiaries when

presenting individual financial statements for statutory purposes

• Memorandum of understanding between Brazil and the IASB ensures that the CPC will continue to issue new BR GAAP standards in line with IASB

• CPC and the application of the RTT significantly decouples tax and statutory accounting (e.g., depreciation methods)

• CPC serves as official accounting records applicable to most organizations(electronic tax filings, distributable reserves and dividends, thin capitalization rules, transfer pricing)

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 8

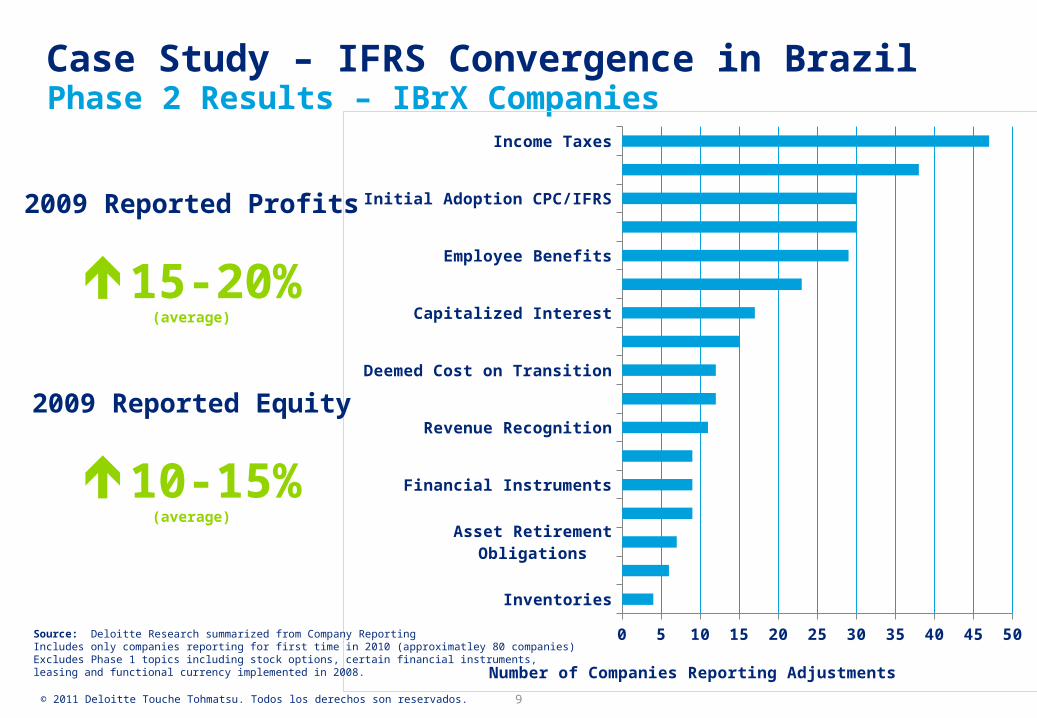

Case Study – IFRS Convergence in Brazil Phase 2 Results – IBrX Companies

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 9

Inventories

Provisions / Contingencies

Asset Retirement Obligations

Biological Assets

Financial Instruments

Service Concessions

Revenue Recognition

Fixed Assets

Deemed Cost on Transition

Consolidation/ Investments Associates / JVs

Capitalized Interest

Dividends

Employee Benefits

Financial Statement Presentation

Initial Adoption CPC/IFRS

Business Combinations

Income Taxes

0 5 10 15 20 25 30 35 40 45 50

Number of Companies Reporting Adjustments

Source: Deloitte Research summarized from Company ReportingIncludes only companies reporting for first time in 2010 (approximatley 80 companies)Excludes Phase 1 topics including stock options, certain financial instruments, leasing and functional currency implemented in 2008.

2009 Reported Profits

15-20%(average)

2009 Reported Equity

10-15%(average)

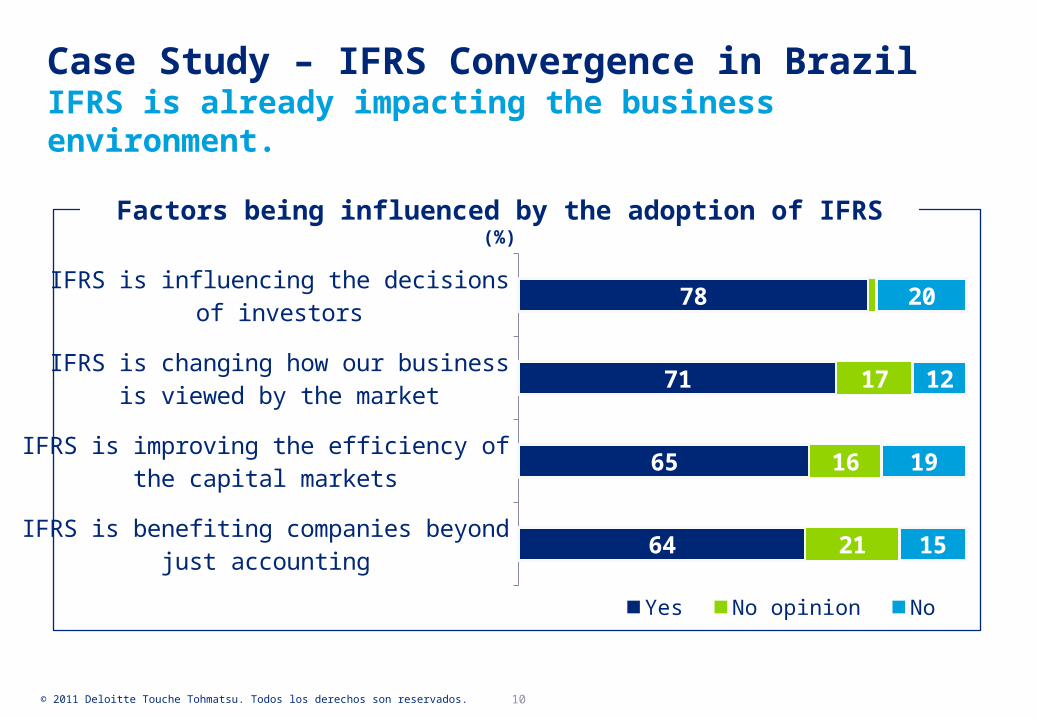

IFRS is benefiting companies beyond just accounting

IFRS is improving the efficiency of the capital markets

IFRS is changing how our business is viewed by the market

IFRS is influencing the decisions of investors

64

65

71

78

21

16

17

15

19

12

20

Yes No opinion No

IFRS is already impacting the business environment.Case Study – IFRS Convergence in Brazil

Factors being influenced by the adoption of IFRS(%)

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 10

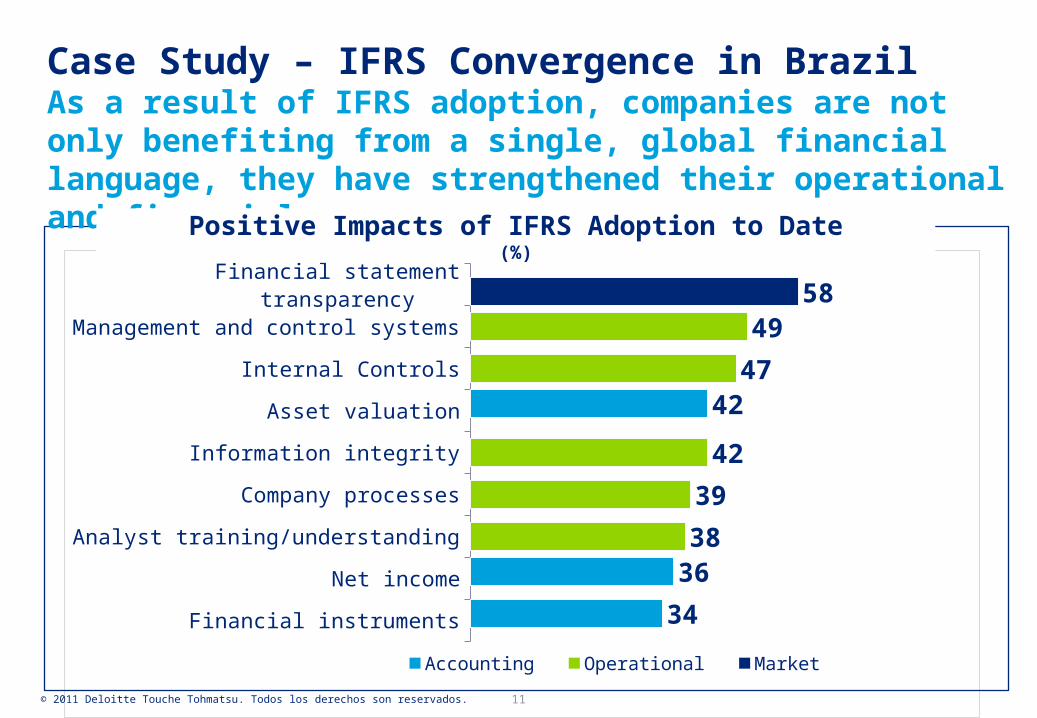

Financial instruments

Net income

Analyst training/understanding

Company processes

Information integrity

Asset valuation

Internal Controls

Management and control systems

Financial statement transparency

34

36

42

38

39

42

47

4958

Accounting Operational Market

As a result of IFRS adoption, companies are not only benefiting from a single, global financial language, they have strengthened their operational and financial processes.

Case Study – IFRS Convergence in Brazil

Positive Impacts of IFRS Adoption to Date(%)

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 11

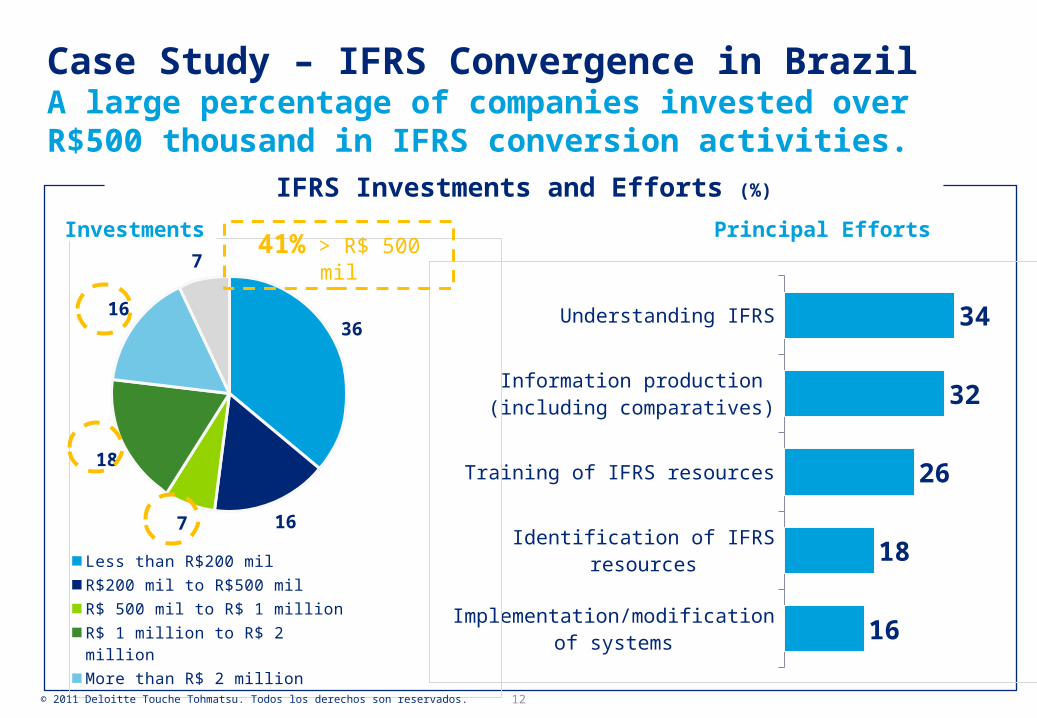

Case Study – IFRS Convergence in Brazil

IFRS Investments and Efforts (%)

Implementation/modification of systems

Identification of IFRS resources

Training of IFRS resources

Information production (including comparatives)

Understanding IFRS

16

18

26

32

3436

167

18

16

7

Less than R$200 mil

R$200 mil to R$500 mil

R$ 500 mil to R$ 1 million

R$ 1 million to R$ 2 million

More than R$ 2 million

Don´t know / no response

Investments Principal Efforts

A large percentage of companies invested over R$500 thousand in IFRS conversion activities.

41% > R$ 500 mil

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 12

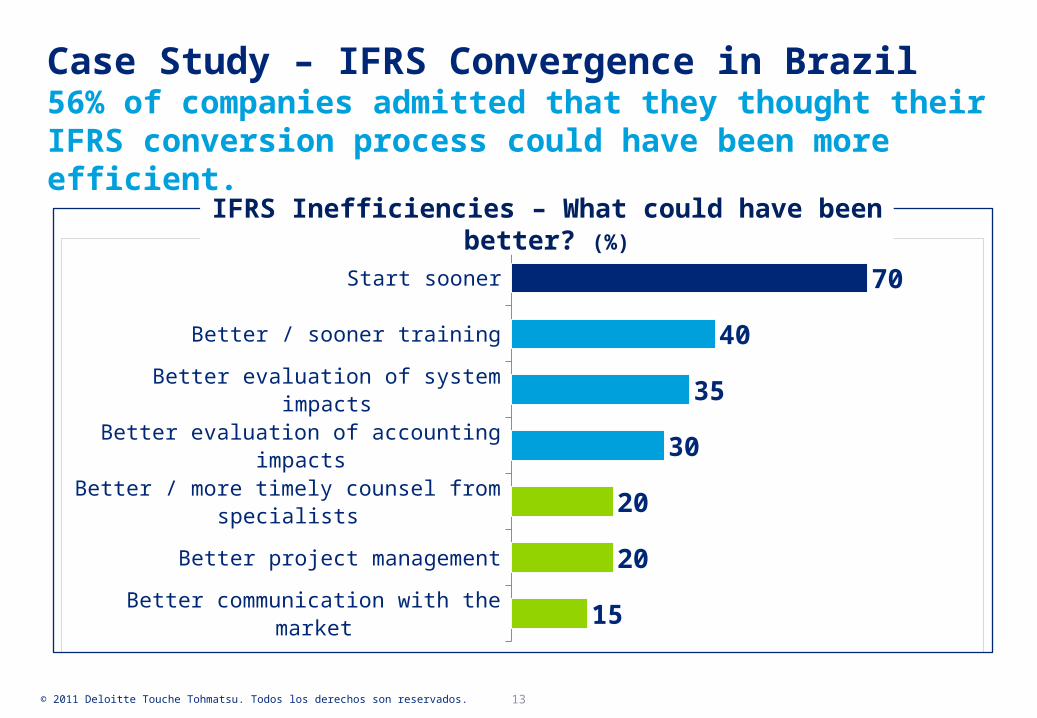

56% of companies admitted that they thought their IFRS conversion process could have been more efficient.

Case Study – IFRS Convergence in Brazil

Better communication with the market

Better project management

Better / more timely counsel from specialists

Better evaluation of accounting impacts

Better evaluation of system impacts

Better / sooner training

Start sooner

15

20

20

30

35

40

70

IFRS Inefficiencies – What could have been better? (%)

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 13

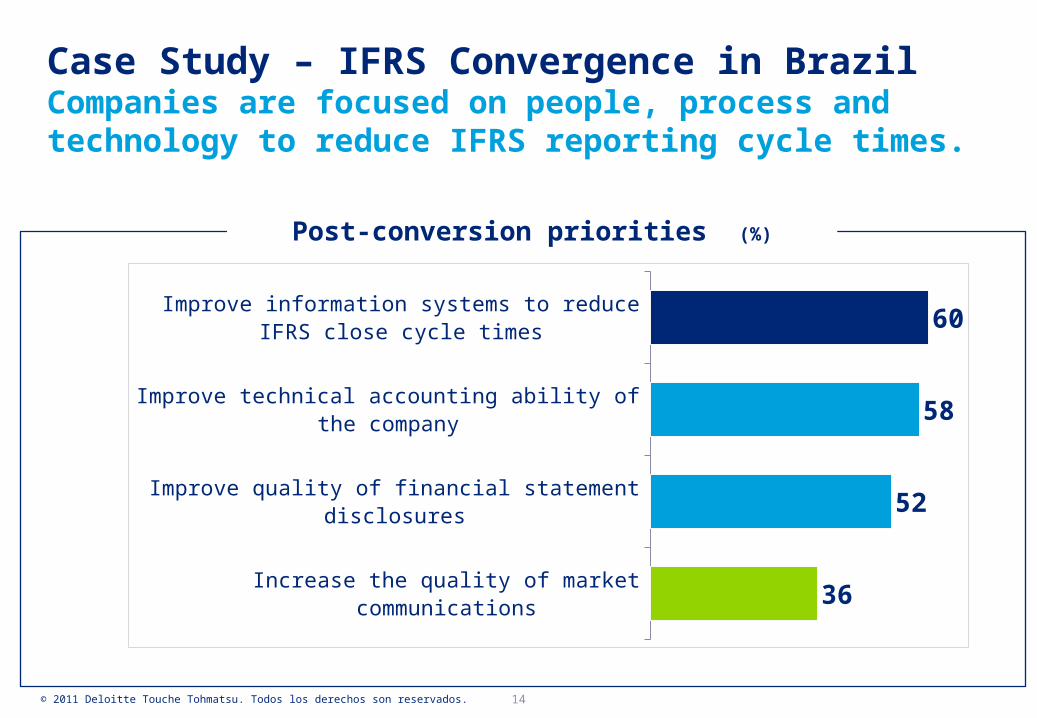

Companies are focused on people, process and technology to reduce IFRS reporting cycle times.

Case Study – IFRS Convergence in Brazil

Post-conversion priorities (%)

Increase the quality of market communications

Improve quality of financial statement disclosures

Improve technical accounting ability of the company

Improve information systems to reduce IFRS close cycle times

36

52

58

60

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 14

Case Study – IFRS Convergence in Brazil Perspectives – Key Success Factors

• Decision and commitment – “IFRS for All”

• Stakeholder support, participation and input

• Central role of the CPC - composition, charter and communication

• Tax “neutrality”

• IFRS part of broader financial reporting and corporate governance changes‒ New public company listing and annual reporting requirements‒ New statutory audit requirements‒ Migration to international auditing standards

• Favorable economic “moment” – providing additional incentives‒ International interest and global investment in Brazil‒ Solid financial system in the wake of the financial crisis‒ Capital markets in expansion

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 15

Case Study – IFRS Convergence in Brazil Perspectives - Macro Challenges

• Application of IFRS in the local legal/regulatory environment‒ Coordination between regulators‒ Tax neutrality – application and future uncertainty

• Consistency in the application of standards‒ Principles vs. rules – significant cultural and operational change‒ Industry-specific issues and interpretations (e.g., real estate, concessions)

• Transition – upgrading people, processes and systems

• Quality of financial statement disclosures and alignment with other reporting requirements/initiatives – regulatory scrutiny

• Dissemination of IFRS for SMEs

• Continued and proactive participation in global IFRS “ecosystem”

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 16

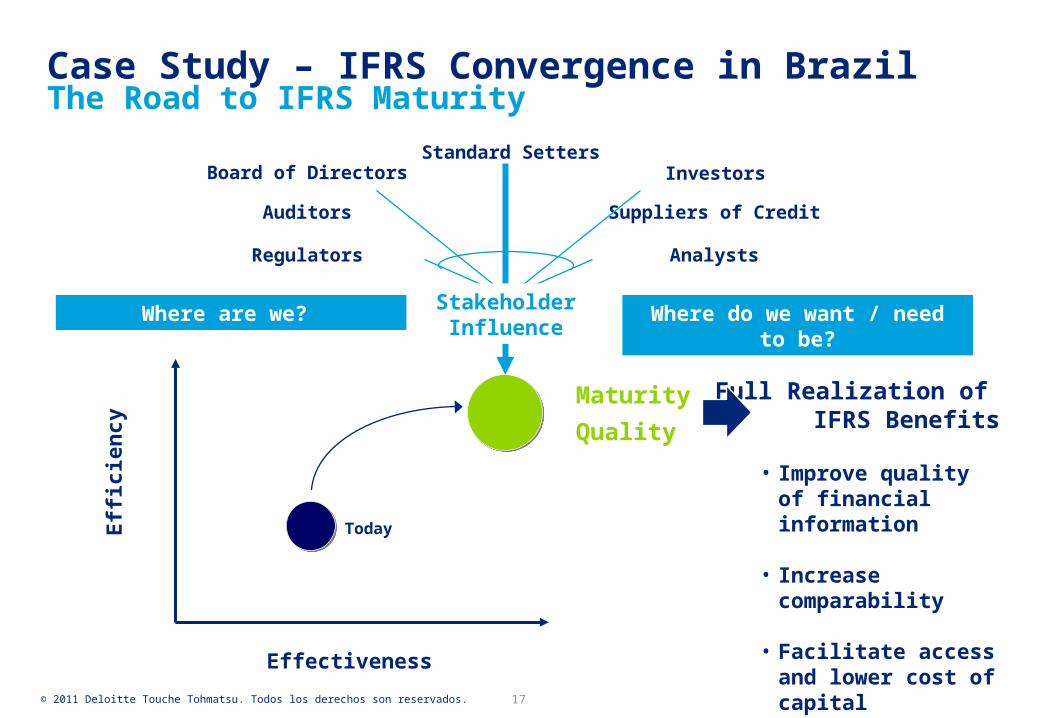

The Road to IFRS MaturityCase Study – IFRS Convergence in Brazil

Maturity

Quality

Effectiveness

Eff

icie

ncy

Today

Investors

Regulators

Standard Setters

Analysts

Suppliers of Credit

Board of Directors

Auditors

Stakeholder Influence

Full Realization of IFRS Benefits

Where are we? Where do we want / need to be?

• Improve quality of financial information

• Increase comparability

• Facilitate access and lower cost of capital

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 17

Best Practices & Lessons Learned

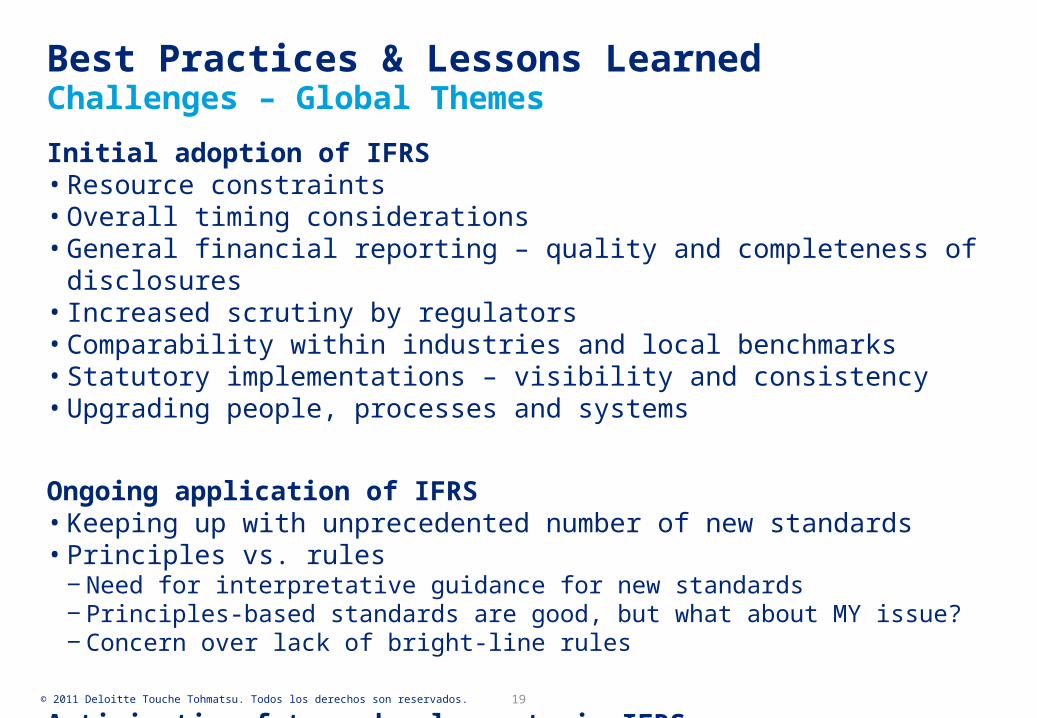

Best Practices & Lessons LearnedChallenges – Global Themes

Initial adoption of IFRS• Resource constraints• Overall timing considerations• General financial reporting – quality and completeness of disclosures• Increased scrutiny by regulators• Comparability within industries and local benchmarks• Statutory implementations – visibility and consistency• Upgrading people, processes and systems

Ongoing application of IFRS• Keeping up with unprecedented number of new standards• Principles vs. rules

‒ Need for interpretative guidance for new standards‒ Principles-based standards are good, but what about MY issue?‒ Concern over lack of bright-line rules

Anticipating future developments in IFRS

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 19

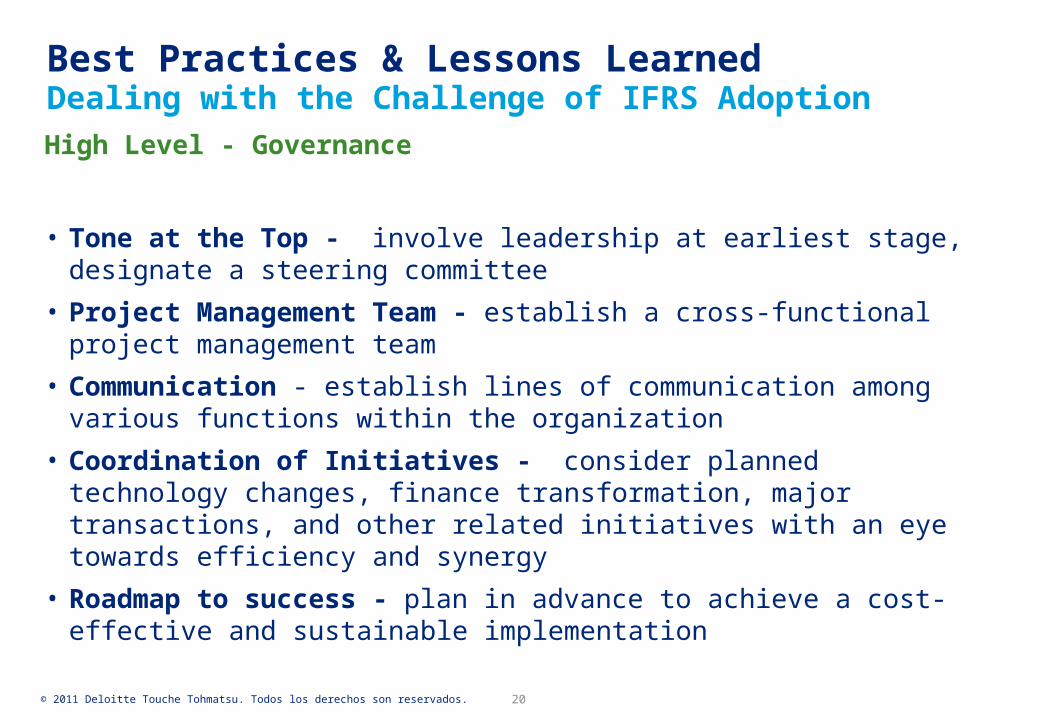

Best Practices & Lessons LearnedDealing with the Challenge of IFRS Adoption

High Level - Governance

• Tone at the Top - involve leadership at earliest stage, designate a steering committee

• Project Management Team - establish a cross-functional project management team

• Communication - establish lines of communication among various functions within the organization

• Coordination of Initiatives - consider planned technology changes, finance transformation, major transactions, and other related initiatives with an eye towards efficiency and synergy

• Roadmap to success - plan in advance to achieve a cost-effective and sustainable implementation

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 20

Best Practices & Lessons LearnedDealing with the Challenge of IFRS Adoption

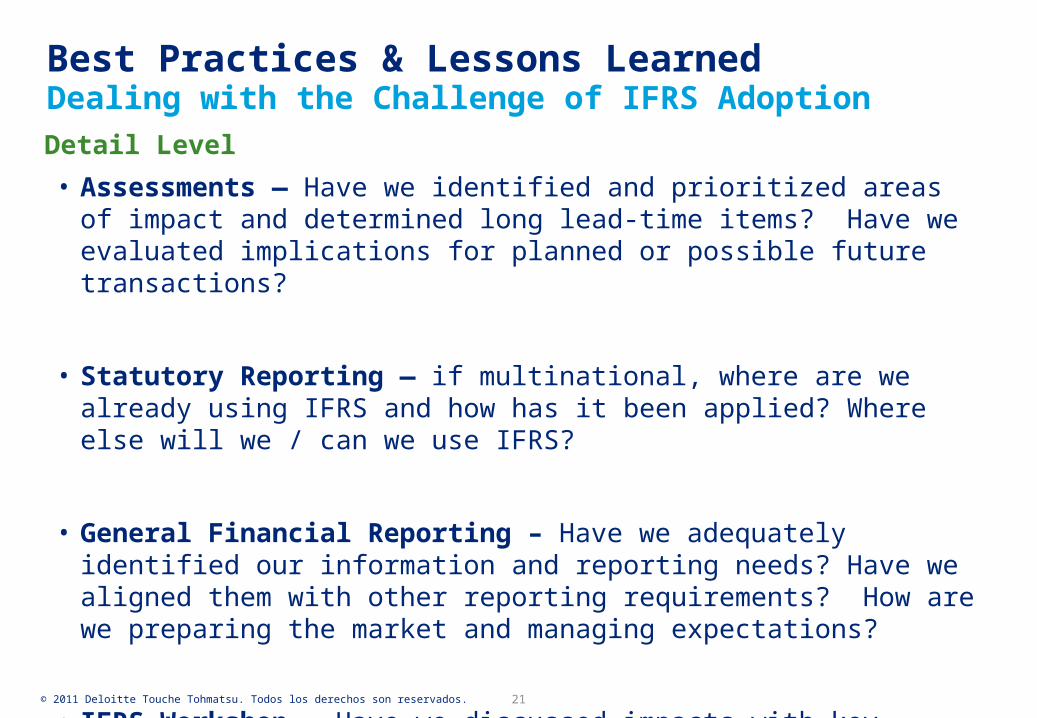

Detail Level

• Assessments — Have we identified and prioritized areas of impact and determined long lead-time items? Have we evaluated implications for planned or possible future transactions?

• Statutory Reporting — if multinational, where are we already using IFRS and how has it been applied? Where else will we / can we use IFRS?

• General Financial Reporting – Have we adequately identified our information and reporting needs? Have we aligned them with other reporting requirements? How are we preparing the market and managing expectations?

• IFRS Workshop — Have we discussed impacts with key members of Management? The Board? The Audit Committee?

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 21

Best Practices & Lessons LearnedDealing with the Challenge of IFRS Adoption

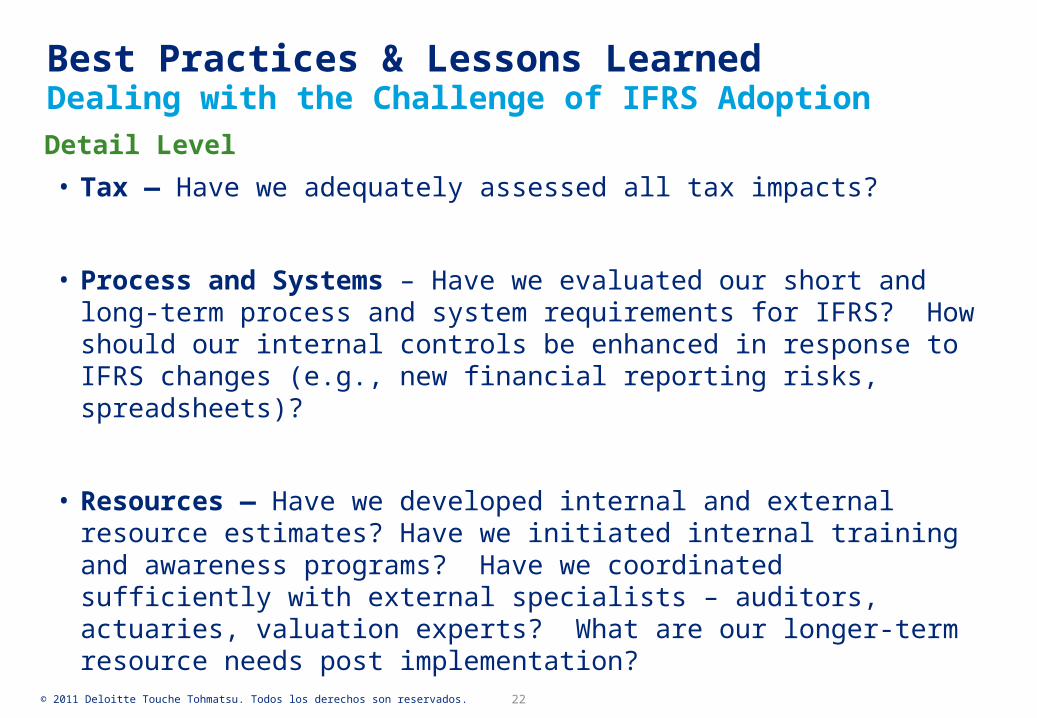

Detail Level

• Tax — Have we adequately assessed all tax impacts?

• Process and Systems – Have we evaluated our short and long-term process and system requirements for IFRS? How should our internal controls be enhanced in response to IFRS changes (e.g., new financial reporting risks, spreadsheets)?

• Resources — Have we developed internal and external resource estimates? Have we initiated internal training and awareness programs? Have we coordinated sufficiently with external specialists – auditors, actuaries, valuation experts? What are our longer-term resource needs post implementation?

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 22

Looking Forward and Final Thoughts

Deloitte se refiere a una o más de las firmas miembros de Deloitte Touche Tohmatsu Limited, una compañía privada del Reino Unido limitada por garantía, y su red de firmas miembros, cada una como una entidad única e independiente y legalmente separada. Una descripción detallada de la estructura legal de Deloitte Touche Tohmatsu Limited y sus firmas miembros puede verse en el sitio web www.deloitte.com/about. Deloitte presta servicios de auditoría, impuestos, consultoría y asesoramiento financiero a organizaciones públicas y privadas de diversas industrias. Con una red global de firmas miembros en más de 150 países, Deloitte brinda sus capacidades de clase mundial y su profunda experiencia local para ayudar a sus clientes a tener éxito donde sea que operen. Aproximadamente 170.000 profesionales de Deloitte se han comprometido a convertirse en estándar de excelencia.

AppendixIFRS Case Study

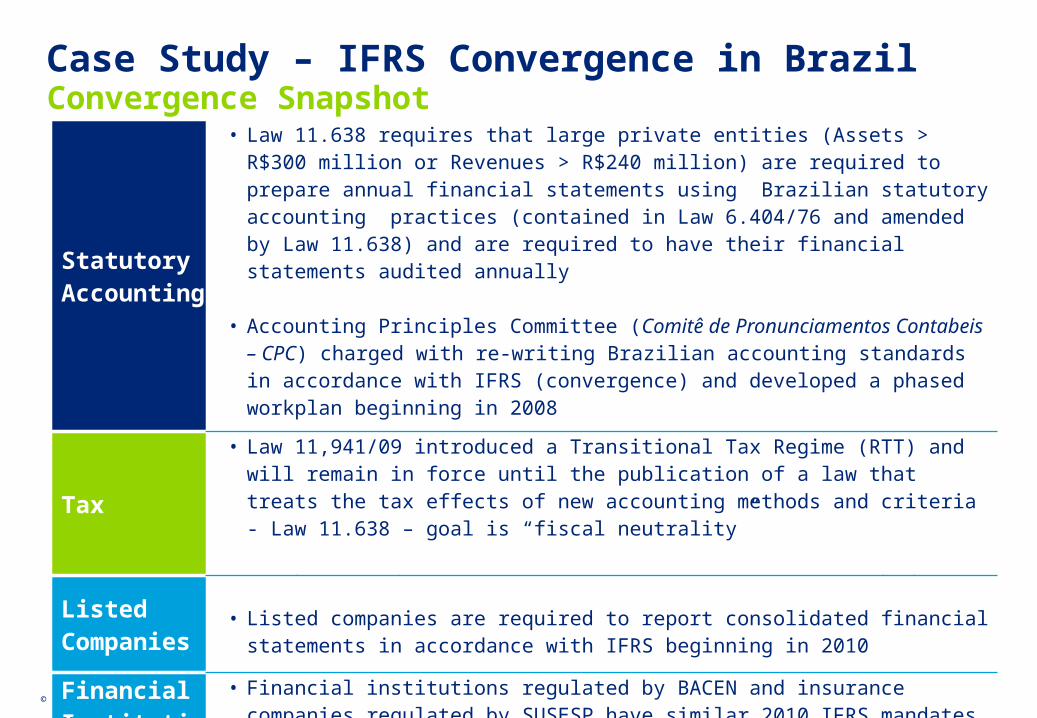

Case Study – IFRS Convergence in Brazil Convergence Snapshot

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 26

Statutory Accounting

• Law 11.638 requires that large private entities (Assets > R$300 million or Revenues > R$240 million) are required to prepare annual financial statements using Brazilian statutory accounting practices (contained in Law 6.404/76 and amended by Law 11.638) and are required to have their financial statements audited annually

• Accounting Principles Committee (Comitê de Pronunciamentos Contabeis – CPC) charged with re-writing Brazilian accounting standards in accordance with IFRS (convergence) and developed a phased workplan beginning in 2008

• CPC version of IFRS for SME´s issued and effective for 2009

Tax

• Law 11,941/09 introduced a Transitional Tax Regime (RTT) and will remain in force until the publication of a law that treats the tax effects of new accounting methods and criteria - Law 11.638 – goal is “fiscal neutrality”

• Tax bases under RTT use 2007 statutory accounting methods

Listed Companies

• Listed companies are required to report consolidated financial statements in accordance with IFRS beginning in 2010

Financial Institutions

• Financial institutions regulated by BACEN and insurance companies regulated by SUSESP have similar 2010 IFRS mandates for their consolidated financial statement requirements – however some exceptions (e.g., comparability)

Case Study – IFRS Convergence in Brazil CPC vs. IFRS Standards

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 27

CPC Phase I (2008) CPC Phase 2 – Major Convergence (2009/2010)

Topic CPC IFRS Topic CPC IFRS Topic CPC IFRS

Structural FrameworkStructural Framework - Complement

Agriculture CPC 29 IAS 41

Impairment of Assets CPC 01 IAS 36 Business Combinations CPC 15 IFRS 3 Revenue CPC 30 IAS 18

Effects of Changes in Foreign Exchange Rates

CPC 02 IAS 21 Inventory CPC 16 IAS 2Non-current Assets held for Sale and Discontinued Operations

CPC 31 IFRS 5

Cash Flow Statements CPC 03 IAS 7 Construction Contracts CPC 17 IAS 11 Income Taxes CPC 32 IAS 12

Intangible Assets CPC 04 IAS 38 Investments in Associates CPC 18 IAS 28 Employee Benefits CPC 33 IAS 19

Related Party Disclosures CPC 05 IAS 24 Interests in Joint Ventures CPC 19 IAS 31Exploration for and Evaluation of Mineral Assets

CPC 34 IFRS 6

Leasing CPC 06 IAS 17 Borrowing Costs CPC 20 IAS 23Consolidated and Separate Financial Statements

CPC 35/36 IAS 27

Government Grants CPC 07 IAS 20 Interim Financial Statements CPC 21 IAS 34First Time Adoption of IFRS (2010) and CPC Phase 2

CPC 37/43 IFRS 1

Transaction Premium and Costs Associated with the Issuance of Debt/Shares

CPC 08 IAS 39 Segment Reporting CPC 22 IFRS 8 Financial Instruments - Phase II CPC 38/39/40

IAS 32/39 IFRS 7

Statement of Value Added CPC 09 N/AAccounting policies, changes, corrections of errors

CPC 23 IAS 8 Earnings per Share (2010) CPC 41 IAS 33

Share-based Payments CPC 10 IFRS 2 Subsequent events CPC 24 IAS 10Financial Reporting in Hyperinflationary Economies (N/A)

CPC 42 IAS 29

Insurance Contracts CPC 11 IFRS 4Provisions, Contingent Liabilities and Contingent Assets

CPC 25 IAS 37 Interpretations (15) ICPC IFRIC

Present Value Measurements CPC 12 N/APresentation of Financial Statements

CPC 26 IAS 1 Orientations (5) OCPC N/A

Initial Application of Law 11,638 Accounting Changes

CPC 13 N/A Fixed Assets CPC 27 IAS 16 Updates/Corrections CPC XX(R) N/A

Financial Instruments - Phase I CPC 14 IAS 32/39 Investment Property CPC 28 IAS 40

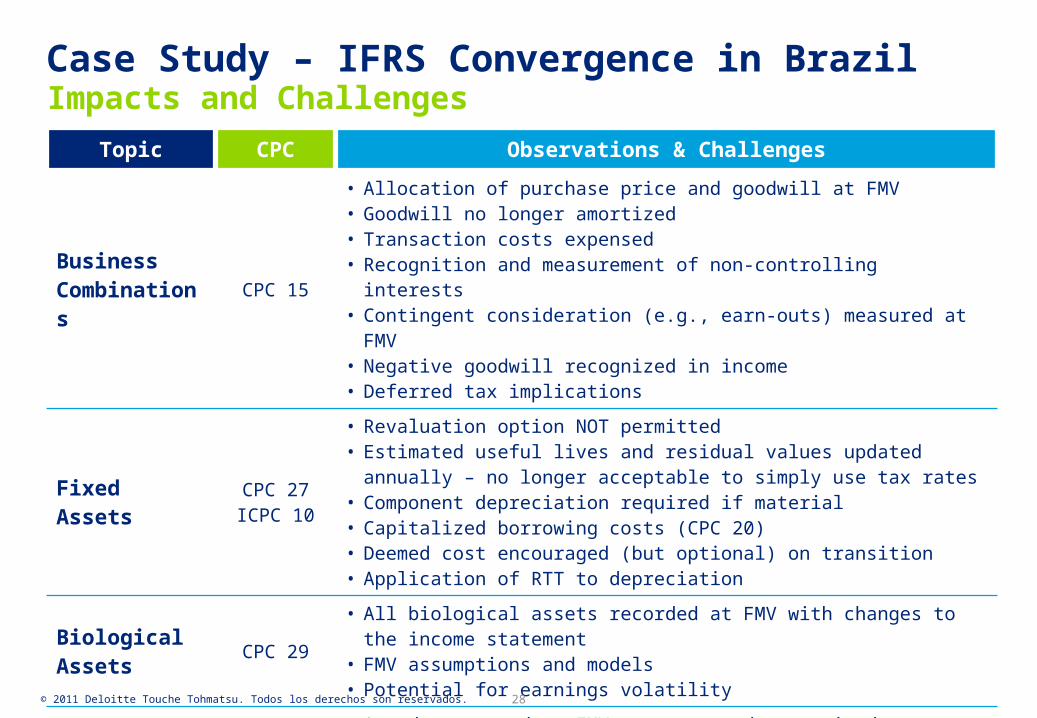

Case Study – IFRS Convergence in Brazil Impacts and Challenges

Topic CPC Observations & Challenges

Business Combinations

CPC 15

• Allocation of purchase price and goodwill at FMV• Goodwill no longer amortized• Transaction costs expensed• Recognition and measurement of non-controlling interests• Contingent consideration (e.g., earn-outs) measured at FMV• Negative goodwill recognized in income • Deferred tax implications

Fixed Assets CPC 27ICPC 10

• Revaluation option NOT permitted• Estimated useful lives and residual values updated annually – no longer

acceptable to simply use tax rates• Component depreciation required if material• Capitalized borrowing costs (CPC 20)• Deemed cost encouraged (but optional) on transition • Application of RTT to depreciation

Biological Assets

CPC 29

• All biological assets recorded at FMV with changes to the income statement

• FMV assumptions and models• Potential for earnings volatility

Share-Based Awards

CPC 10

• Awards measured at FMV at grant and recognized to expense (either immediately or over vesting period)

• FMV considerations for complex awards• Recognition (push-down) of parent awards

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 28

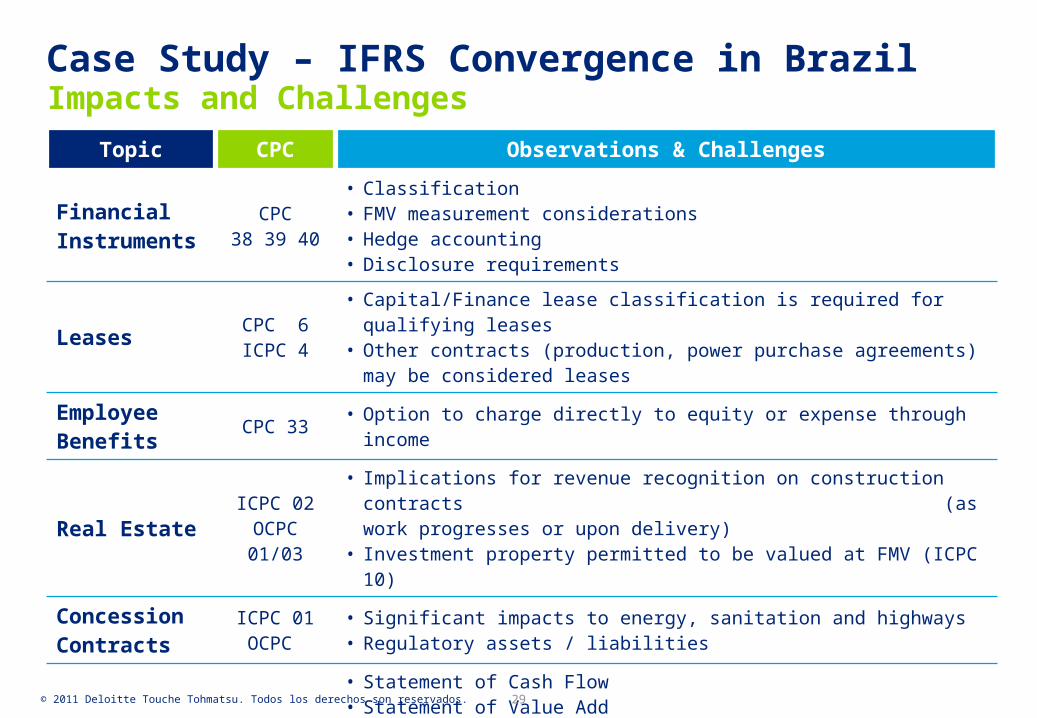

Case Study – IFRS Convergence in Brazil Impacts and Challenges

Topic CPC Observations & Challenges

Financial Instruments

CPC38 39 40

• Classification• FMV measurement considerations• Hedge accounting• Disclosure requirements

Leases CPC 6ICPC 4

• Capital/Finance lease classification is required for qualifying leases• Other contracts (production, power purchase agreements) may be

considered leases

Employee Benefits

CPC 33 • Option to charge directly to equity or expense through income

Real EstateICPC 02OCPC 01/03

• Implications for revenue recognition on construction contracts (as work progresses or upon delivery)

• Investment property permitted to be valued at FMV (ICPC 10)

Concession Contracts

ICPC 01OCPC

• Significant impacts to energy, sanitation and highways• Regulatory assets / liabilities

General Financial Reporting

Public Companies

• Statement of Cash Flow• Statement of Value Add • Presentation - classification• First-time adoption – reconciliations / restatements• Segment Reporting• Alignment with new public company annual reporting requirements

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 29

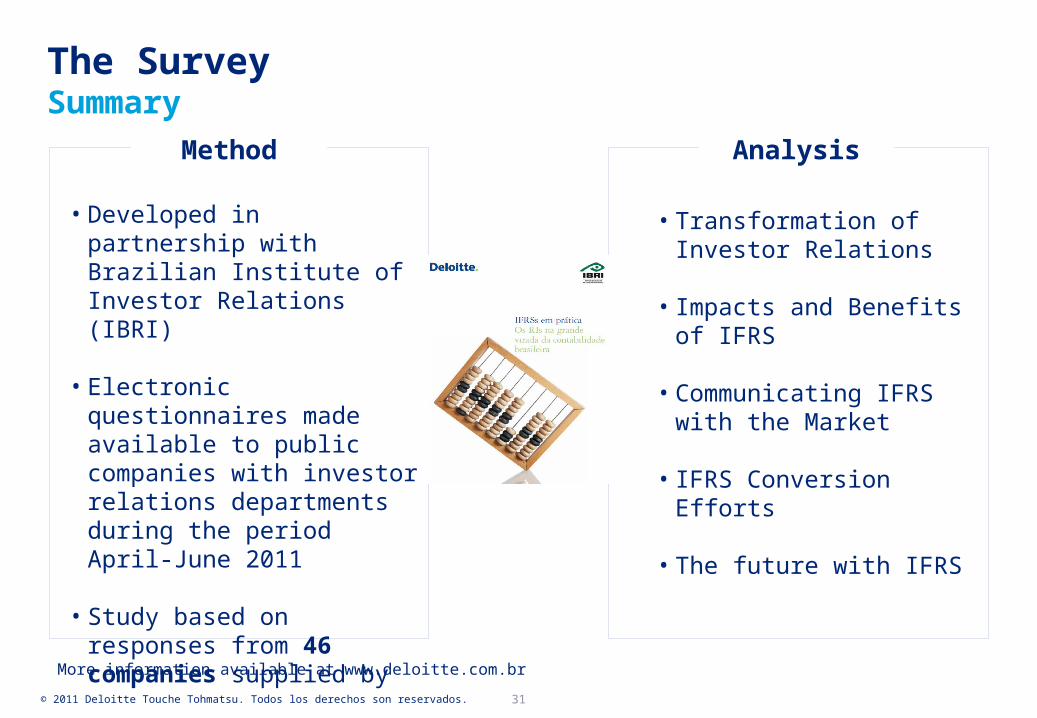

AppendixIFRS Impact Study

• Developed in partnership with Brazilian Institute of Investor Relations (IBRI)

• Electronic questionnaires made available to public companies with investor relations departments during the period April-June 2011

• Study based on responses from 46 companies supplied by representatives of Investor Relations

SummaryThe Survey

• Transformation of Investor Relations

• Impacts and Benefits of IFRS

• Communicating IFRS with the Market

• IFRS Conversion Efforts

• The future with IFRS

Method Analysis

More information available at www.deloitte.com.br

© 2011 Deloitte Touche Tohmatsu. Todos los derechos son reservados. 31