Embed Size (px)

Citation preview

PEMODELAN DAN PERAMALAN DATA

PEMBUKAAN IHSG MENGGUNAKAN

MODEL ARIMA

OLEH :OLEH :

1. Triyono ( M0107086 )2. Nariswari S ( M0108022 )3. Ayunita C ( M0180034 )4. Ibnuhardi F.Ihsan ( M0108045 )5. Marvina P ( M0108056 )

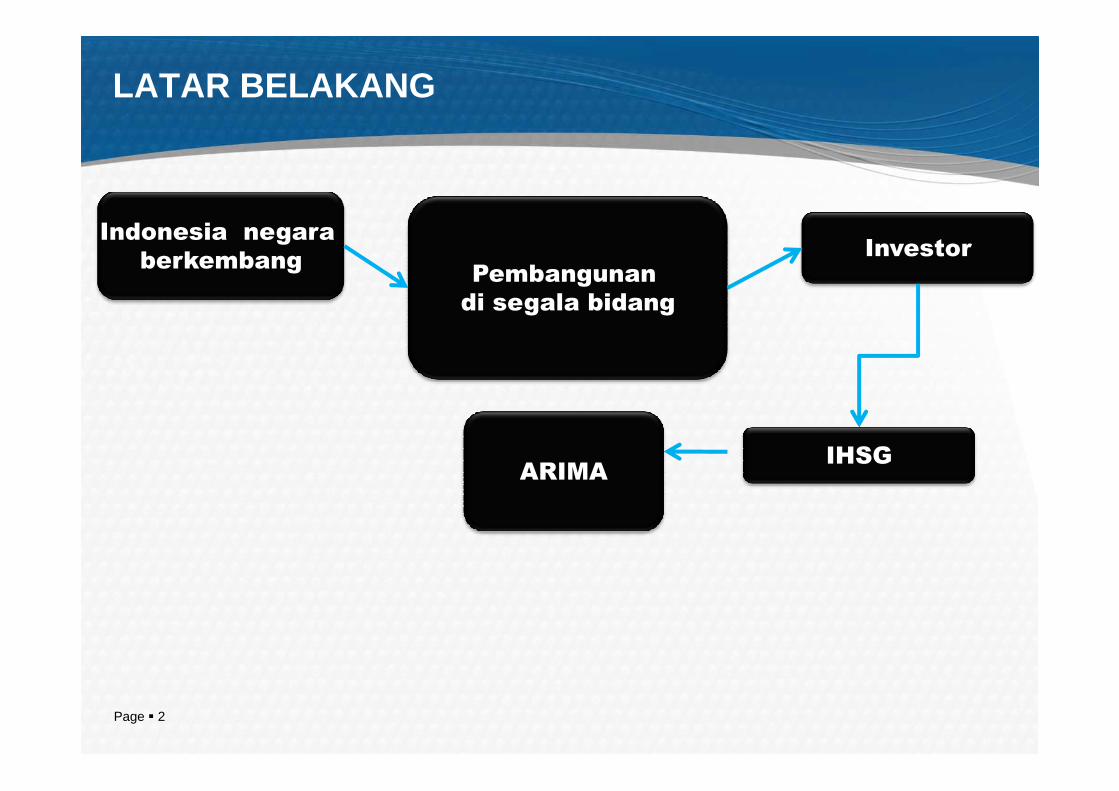

LATAR BELAKANG

Pembangunan

di segala bidang

InvestorIndonesia negara

berkembang

Page � 2

IHSGARIMA

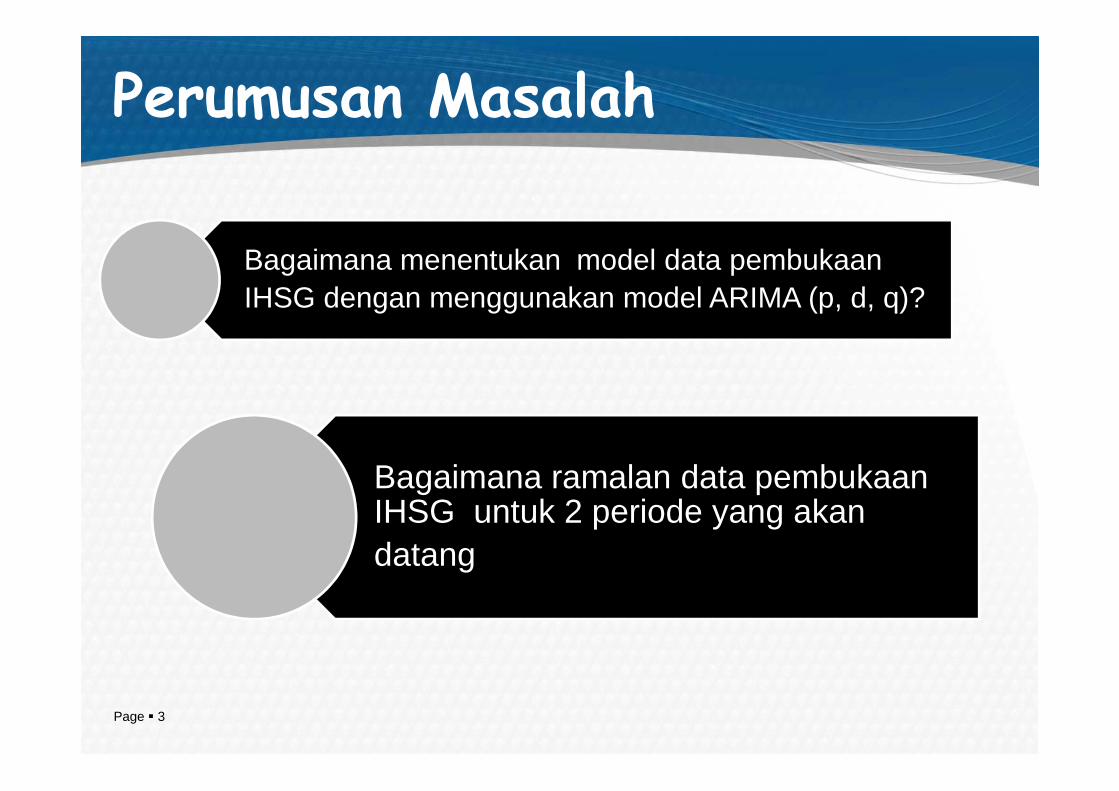

Perumusan Masalah

Bagaimana menentukan model data pembukaan IHSG dengan menggunakan model ARIMA (p, d, q)?

Page � 3

Bagaimana ramalan data pembukaan IHSG untuk 2 periode yang akandatang

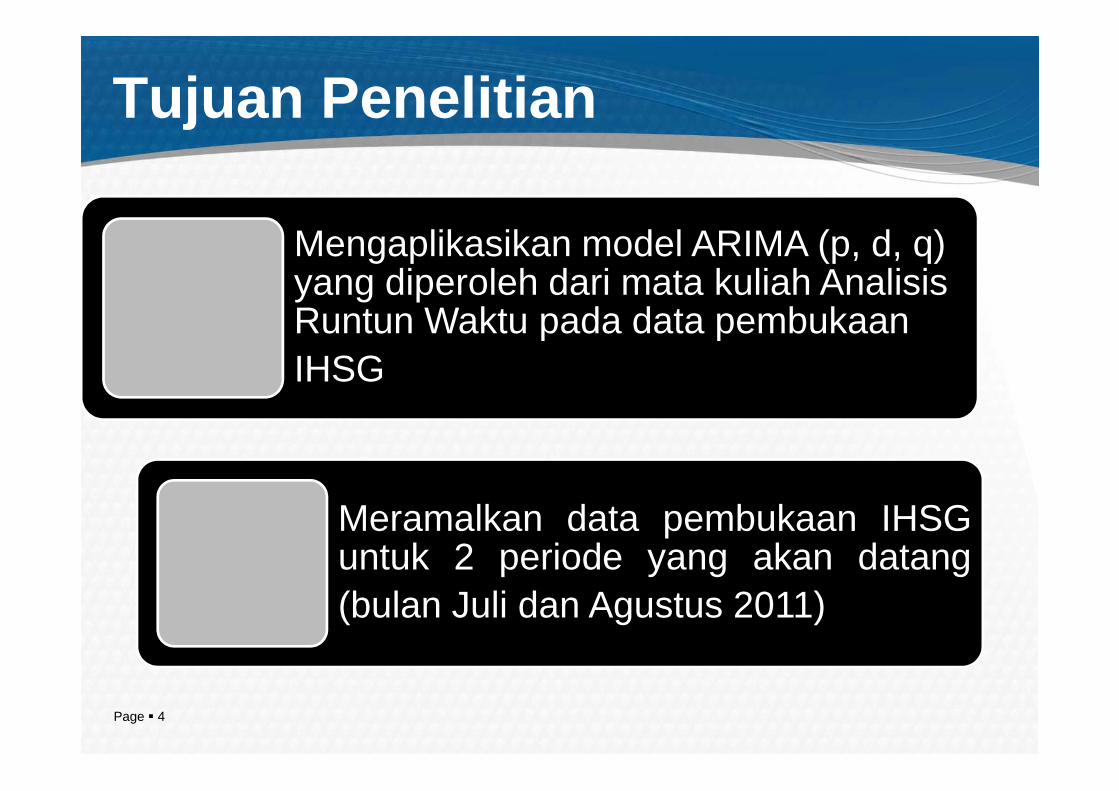

Tujuan Penelitian

Mengaplikasikan model ARIMA (p, d, q) yang diperoleh dari mata kuliah AnalisisRuntun Waktu pada data pembukaan IHSG

Page � 4

Meramalkan data pembukaan IHSGuntuk 2 periode yang akan datang(bulan Juli dan Agustus 2011)

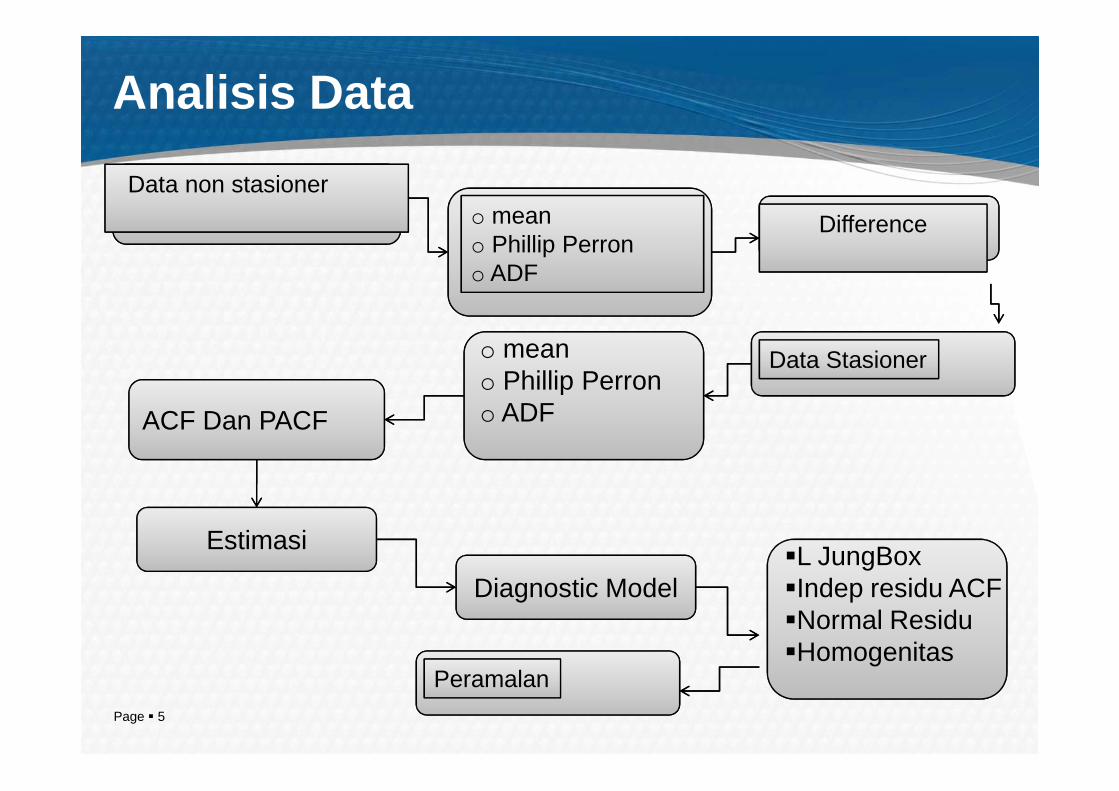

Analisis Data

o meano Phillip Perron

Data non stasionero meano Phillip Perrono ADF

Difference

Data Stasioner

Page � 5

oo ADFACF Dan PACF

Diagnostic Model�L JungBox�Indep residu ACF�Normal Residu�Homogenitas

Estimasi

Peramalan

4000

3500

3000MA PE 17

A ccu racy M easu res

A ctual

F its

Var iab le

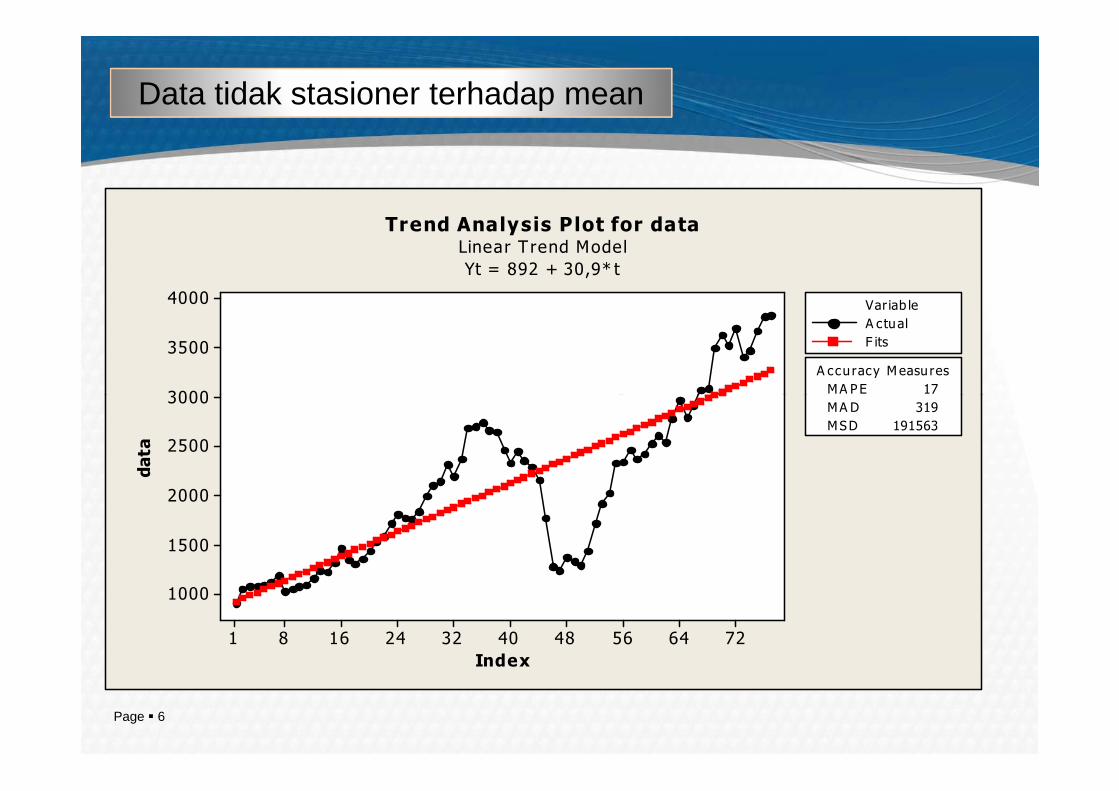

Trend Analysis Plot for dataLinear T rend Model

Yt = 892 + 30,9* t

Data tidak stasioner terhadap mean

Page � 6

726456484032241681

3000

2500

2000

1500

1000

Index

data

MA PE 17

MA D 319

MSD 191563

1,0

0,8

0,6

0,4

0,2

tion

Autocorrelation Function for data(with 5% significance limits for the autocorrelations)

Plot Fungsi Autokorelasi

Page � 7

757065605550454035302520151051

0,2

0,0

-0,2

-0,4

-0,6

-0,8

-1,0

Lag

Autocorrelat

1,0

0,8

0,6

0,4

0,2relation

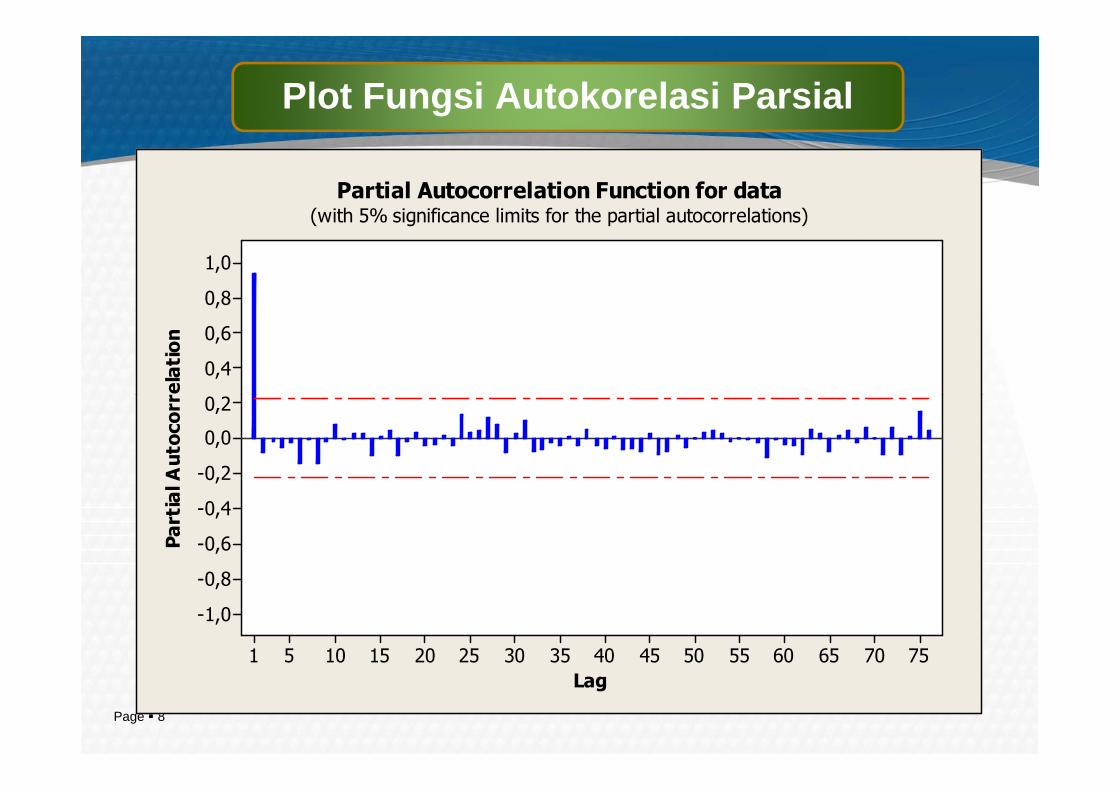

Partial Autocorrelation Function for data(with 5% significance limits for the partial autocorrelations)

Plot Fungsi Autokorelasi Parsial

Page � 8

757065605550454035302520151051

0,2

0,0

-0,2

-0,4

-0,6

-0,8

-1,0

Lag

Partial Autocorr

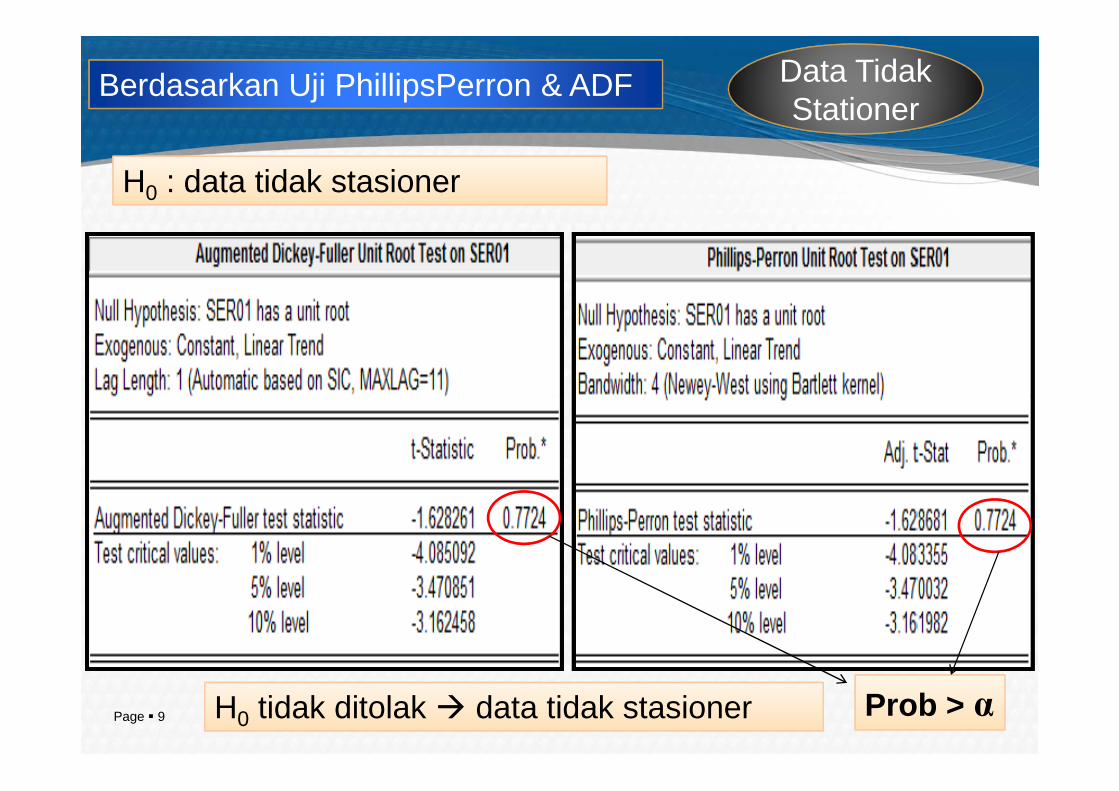

Data TidakStationer

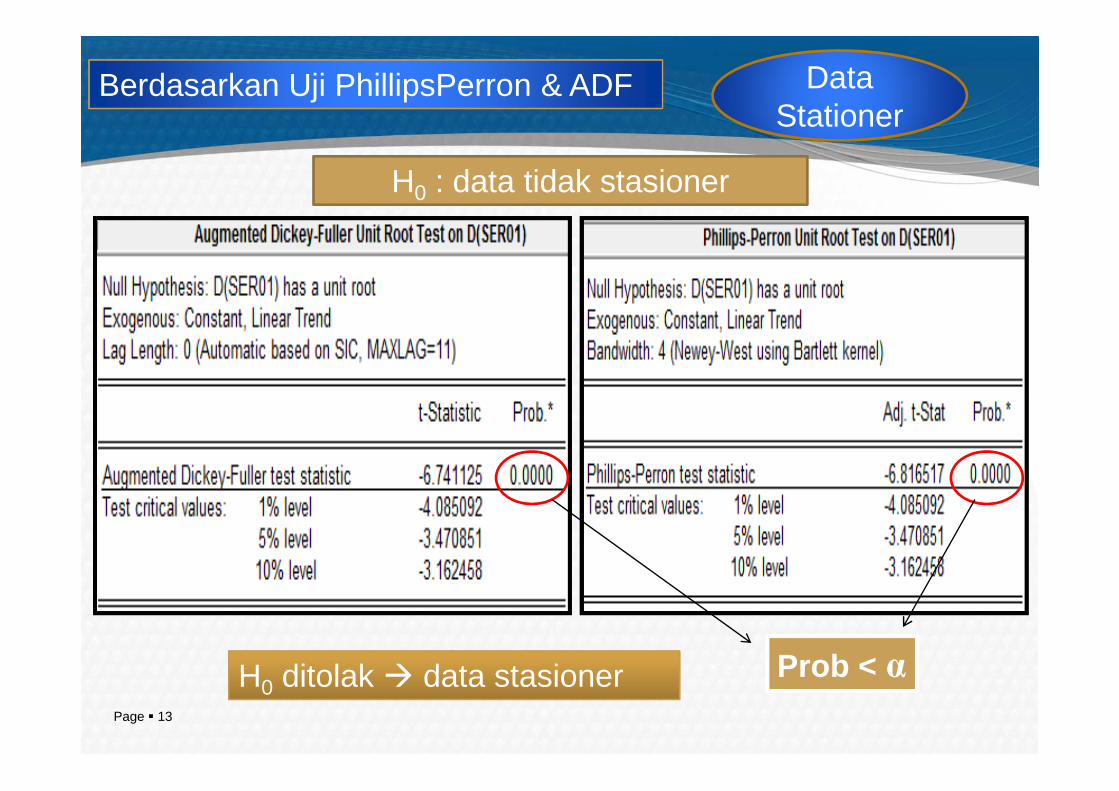

H0 : data tidak stasioner

Berdasarkan Uji PhillipsPerron & ADF

Page � 9 Prob > αH0 tidak ditolak � data tidak stasioner

Data Stationer

500

250MA PE 113,4

A ccu racy Measu res

A c tual

F its

Var iab le

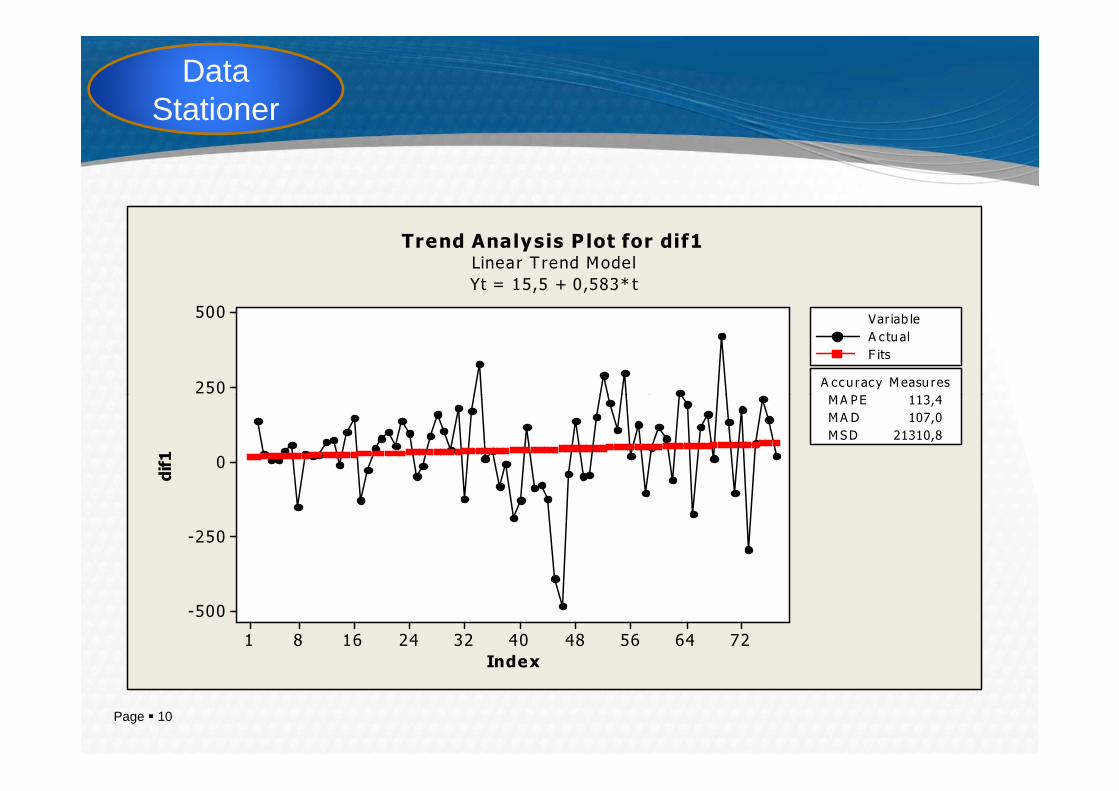

Trend Analysis P lot for dif1Linear T rend Model

Yt = 15,5 + 0,583* t

Page � 10

726456484032241681

250

0

-250

-500

Index

dif1

MA PE 113,4

MA D 107,0

MSD 21310,8

1,0

0,8

0,6

0,4

0,2

ion

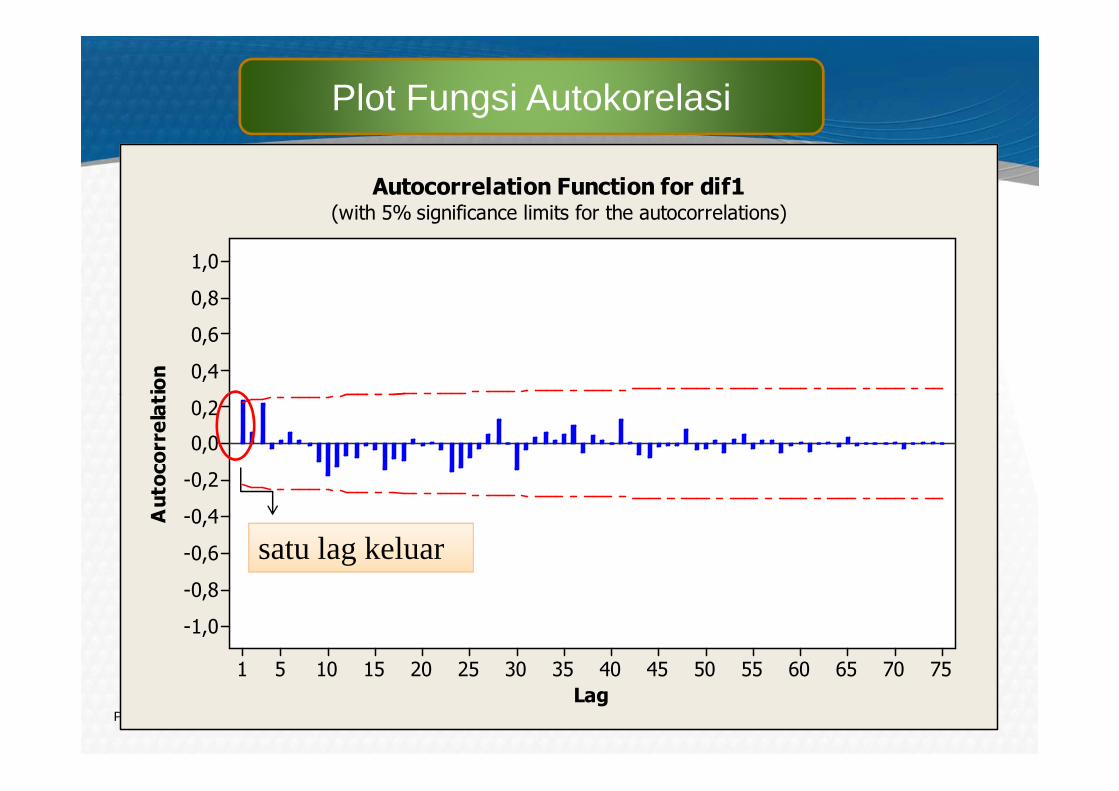

Autocorrelation Function for dif1(with 5% significance limits for the autocorrelations)

Plot Fungsi Autokorelasi

Page � 11

757065605550454035302520151051

0,2

0,0

-0,2

-0,4

-0,6

-0,8

-1,0

Lag

Autocorrelat

satu lag keluar

1,0

0,8

0,6

0,4

elation

Partial Autocorrelation Function for dif1(with 5% significance limits for the partial autocorrelations)

Plot Fungsi Autokorelasi Parsial

Page � 12

757065605550454035302520151051

0,2

0,0

-0,2

-0,4

-0,6

-0,8

-1,0

Lag

Partial Autocorre

satu lag keluar

Data Stationer

Berdasarkan Uji PhillipsPerron & ADF

H0 : data tidak stasioner

Page � 13

Prob < αH0 ditolak � data stasioner

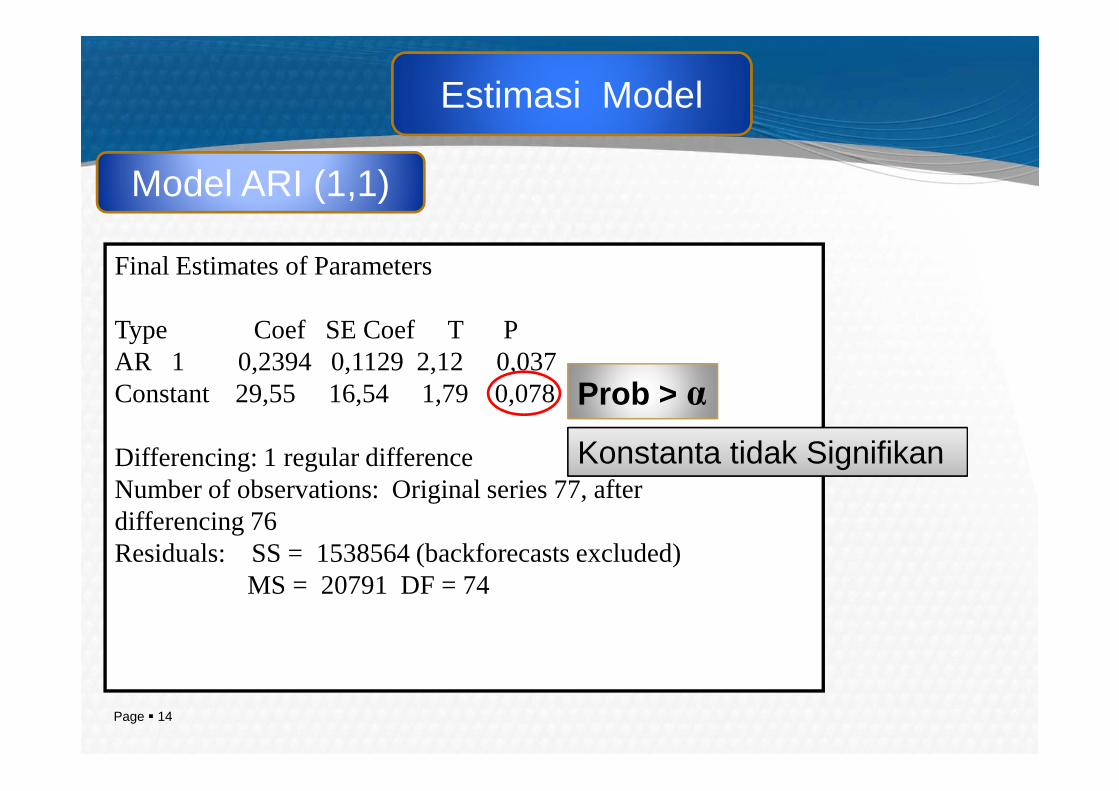

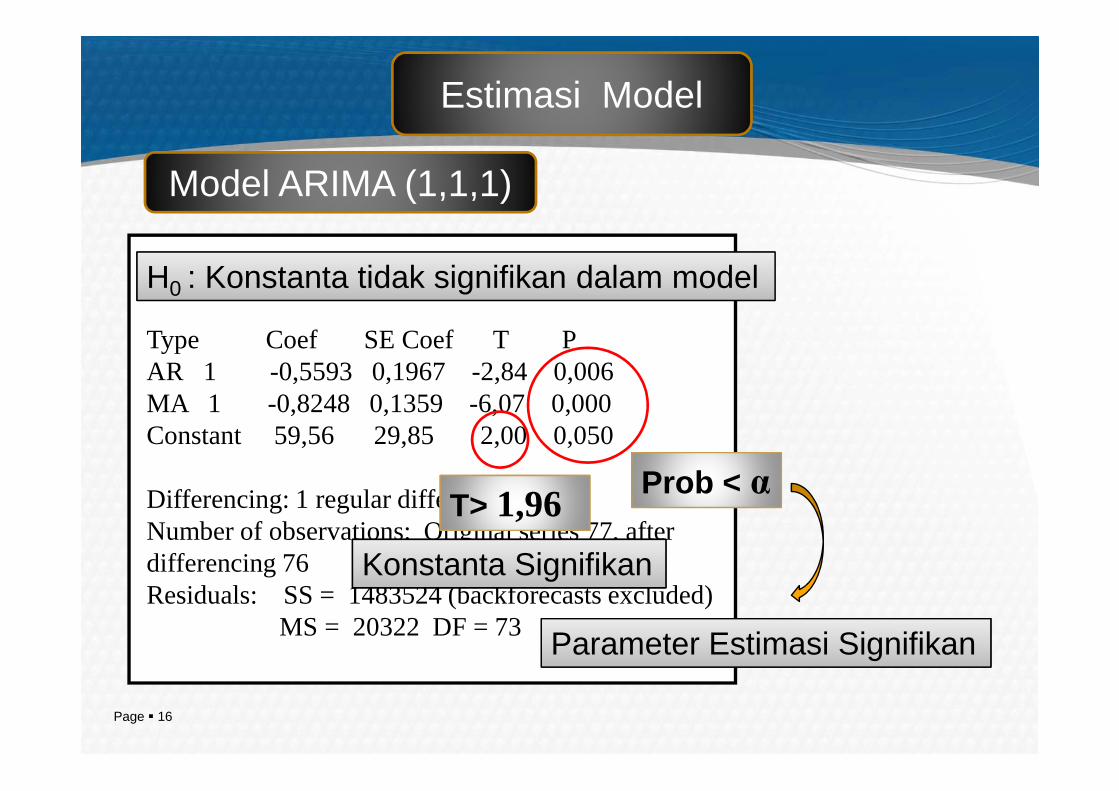

Estimasi Model

Final Estimates of Parameters

Type Coef SE Coef T PAR 1 0,2394 0,1129 2,12 0,037Constant 29,55 16,54 1,79 0,078

Model ARI (1,1)

Prob > α

Page � 14

Constant 29,55 16,54 1,79 0,078

Differencing: 1 regular differenceNumber of observations: Original series 77, after differencing 76Residuals: SS = 1538564 (backforecasts excluded)

MS = 20791 DF = 74

Prob > α

Konstanta tidak Signifikan

Type Coef SE Coef T PMA 1 -0,2766 0,1118 -2,47 0,016Constant 38,75 21,06 1,84 0,070

Estimasi Model

Model IMA (1,1)

Final Estimates of Parameters

Prob > α

Page � 15

Constant 38,75 21,06 1,84 0,070

Differencing: 1 regular differenceNumber of observations: Original series 77, after differencing 76Residuals: SS = 1531747 (backforecasts excluded)

MS = 20699 DF = 74

Prob > α

Konstanta tidak Signifikan

Final Estimates of Parameters

Type Coef SE Coef T PAR 1 -0,5593 0,1967 -2,84 0,006MA 1 -0,8248 0,1359 -6,07 0,000

Model ARIMA (1,1,1)

Estimasi Model

H0 : Konstanta tidak signifikan dalam model

Page � 16

MA 1 -0,8248 0,1359 -6,07 0,000Constant 59,56 29,85 2,00 0,050

Differencing: 1 regular differenceNumber of observations: Original series 77, after differencing 76Residuals: SS = 1483524 (backforecasts excluded)

MS = 20322 DF = 73

Prob < α

Parameter Estimasi Signifikan

T> 1,96

Konstanta Signifikan

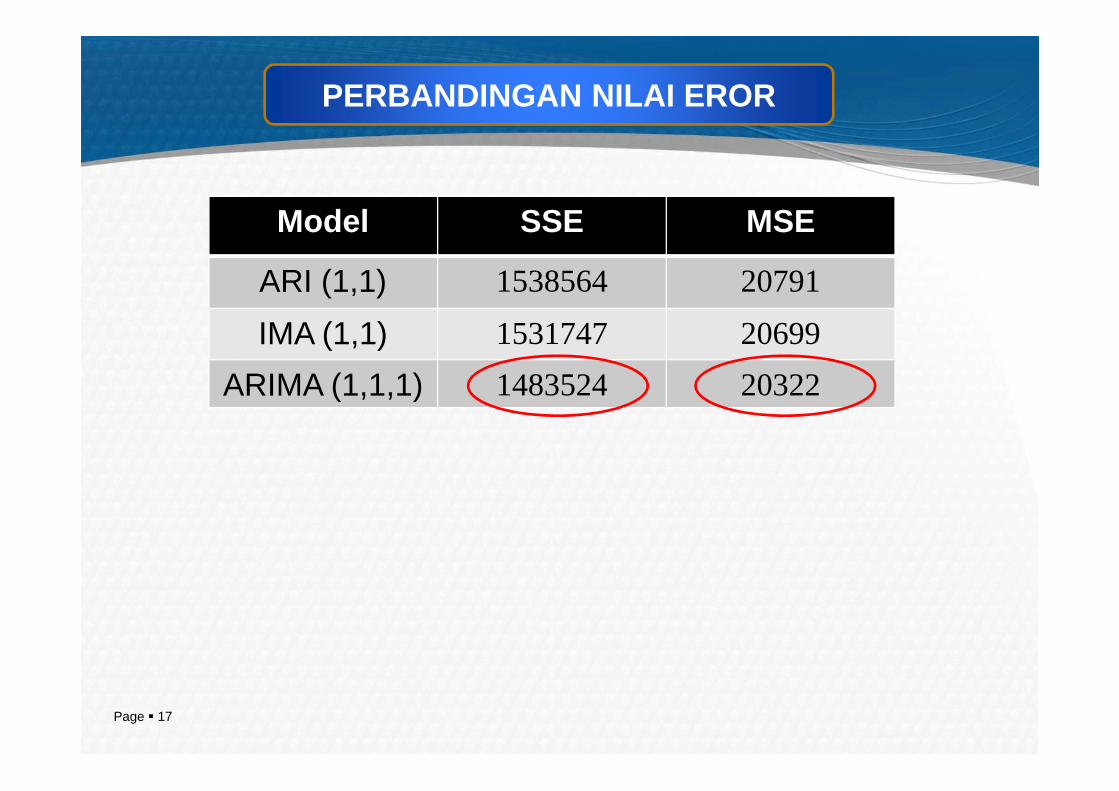

PERBANDINGAN NILAI EROR

Model SSE MSE

ARI (1,1) 1538564 20791

IMA (1,1) 1531747 20699

ARIMA (1,1,1) 1483524 20322

Page � 17

ARIMA (1,1,1) 1483524 20322

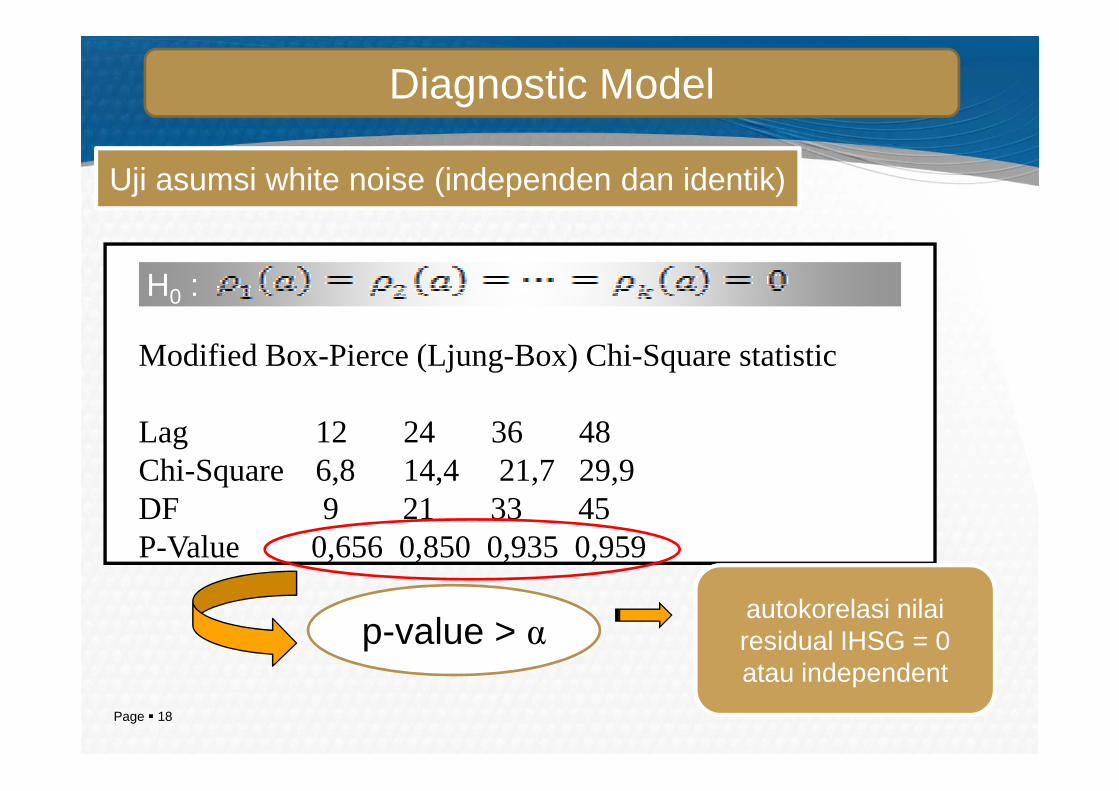

Diagnostic Model

Uji asumsi white noise (independen dan identik)

Modified Box-Pierce (Ljung-Box) Chi-Square statistic

H0 :

Page � 18

Lag 12 24 36 48Chi-Square 6,8 14,4 21,7 29,9DF 9 21 33 45P-Value 0,656 0,850 0,935 0,959

p-value > αautokorelasi nilairesidual IHSG = 0 atau independent

1 ,0

0 ,8

0 ,6

0 ,4

on

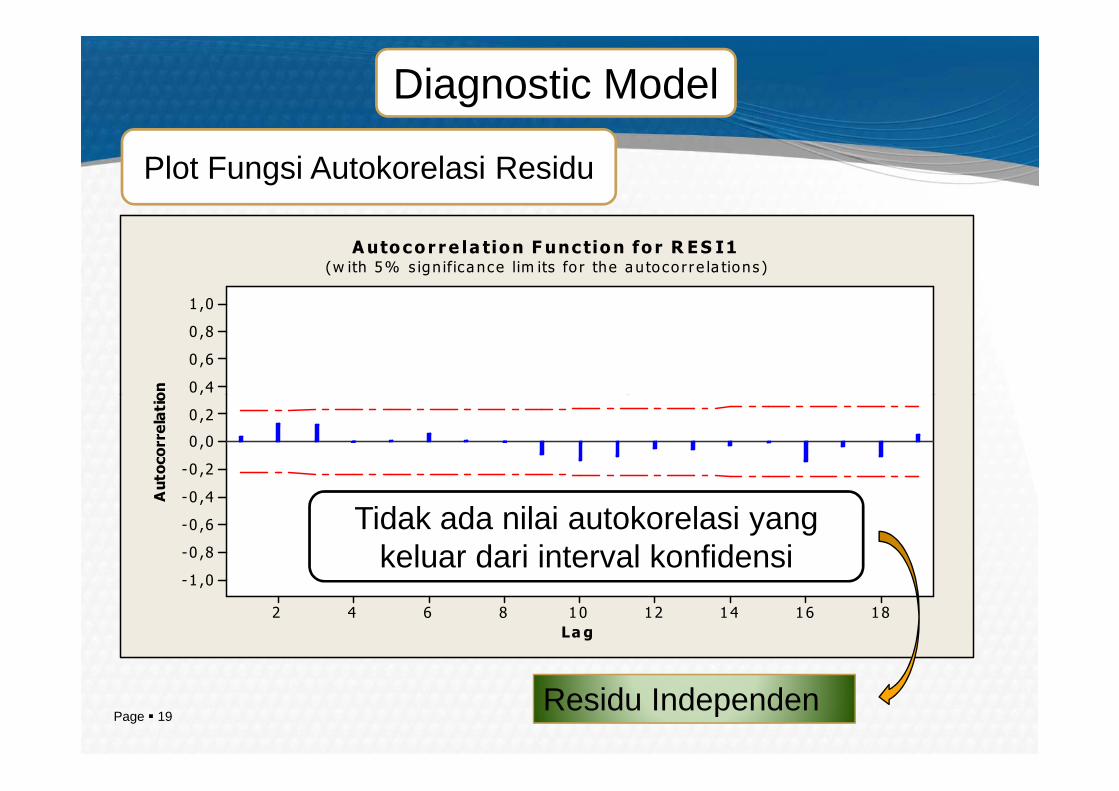

Autoco r r e la tion F unc tion fo r R ES I1(w ith 5% s ign ifica nce lim its fo r the a u to co r r e la tions )

Diagnostic Model

Plot Fungsi Autokorelasi Residu

Page � 19

18161412108642

0 ,2

0 ,0

-0 ,2

-0 ,4

-0 ,6

-0 ,8

-1 ,0

La g

Autocorrelatio

Tidak ada nilai autokorelasi yang keluar dari interval konfidensi

Residu Independen

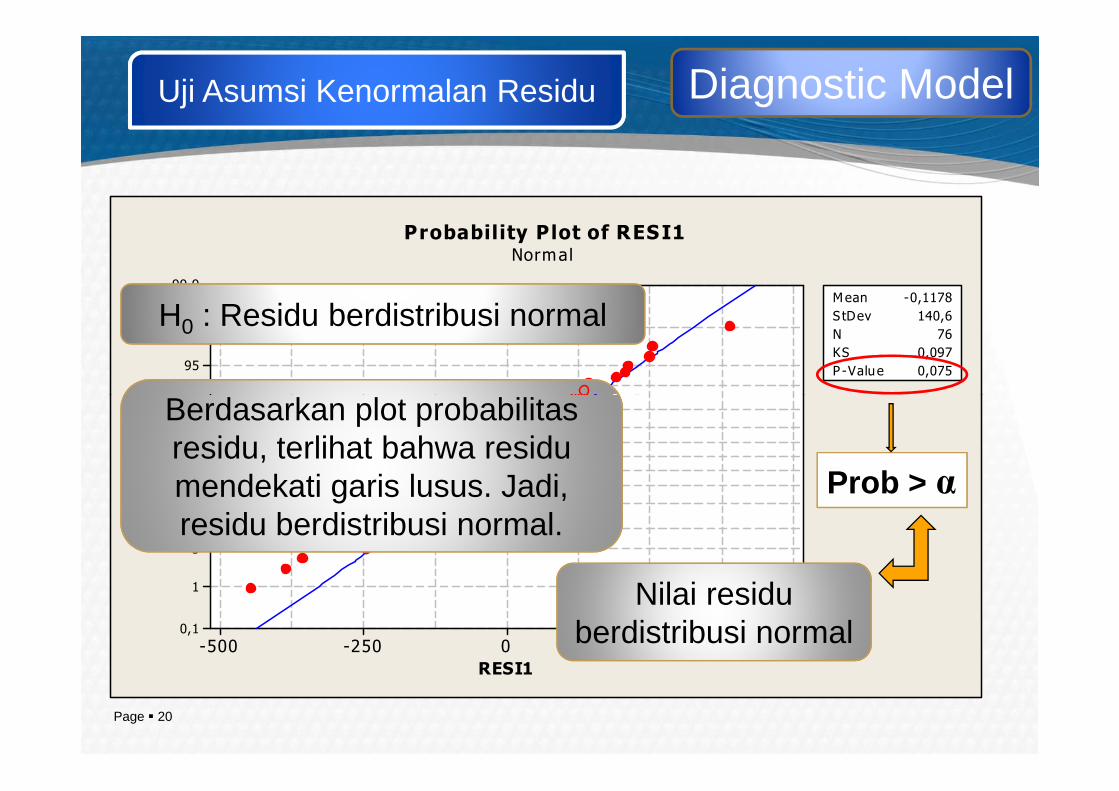

99,9

99

95

90

Mean -0,1178

S tDev 140,6

N 76

KS 0,097

P -Value 0,075

Probability Plot of RESI1Normal

Diagnostic ModelUji Asumsi Kenormalan Residu

Berdasarkan plot probabilitas

H0 : Residu berdistribusi normal

Page � 20

5002500-250-500

80

7060504030

20

10

5

1

0,1

RESI1

Percent

Berdasarkan plot probabilitasresidu, terlihat bahwa residumendekati garis lusus. Jadi, residu berdistribusi normal.

Prob > α

Nilai residuberdistribusi normal

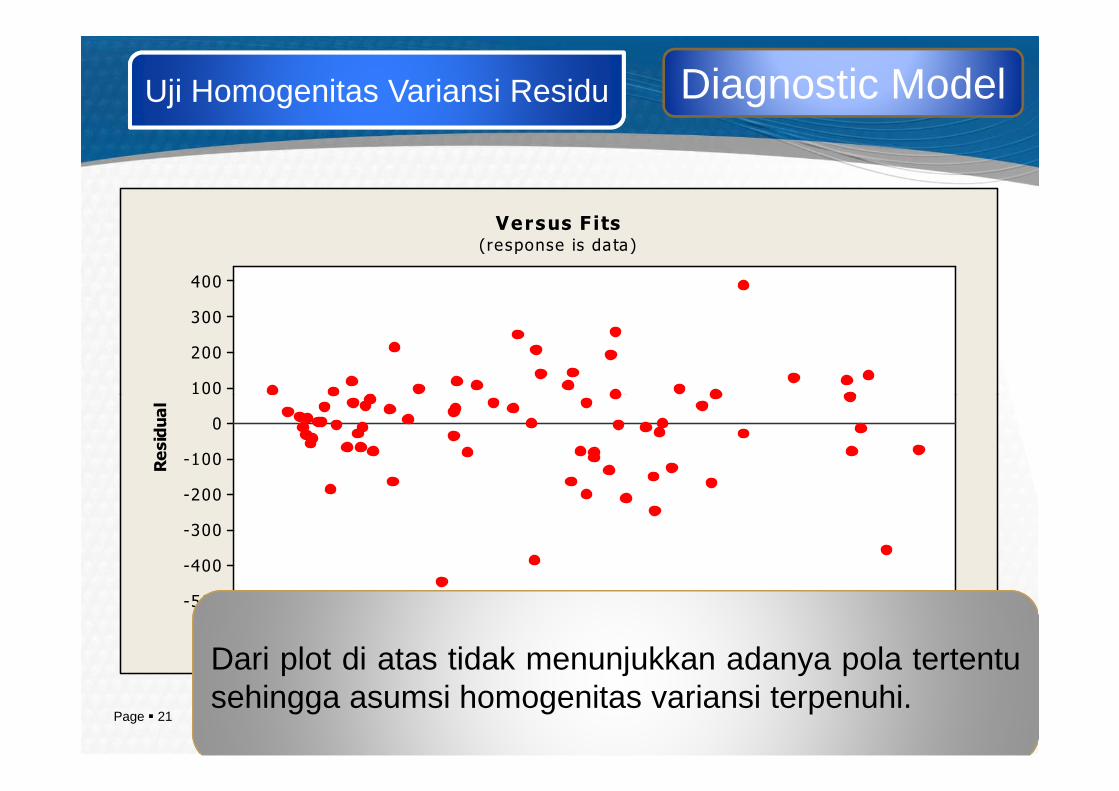

400

300

200

100

Versus F its(response is da ta)

Diagnostic ModelUji Homogenitas Variansi Residu

Page � 21

4000350030002500200015001000

100

0

-100

-200

-300

-400

-500

Fit ted Va lue

Residual

Dari plot di atas tidak menunjukkan adanya pola tertentusehingga asumsi homogenitas variansi terpenuhi.

PERAMALANPERAMALANPERAMALANPERAMALAN

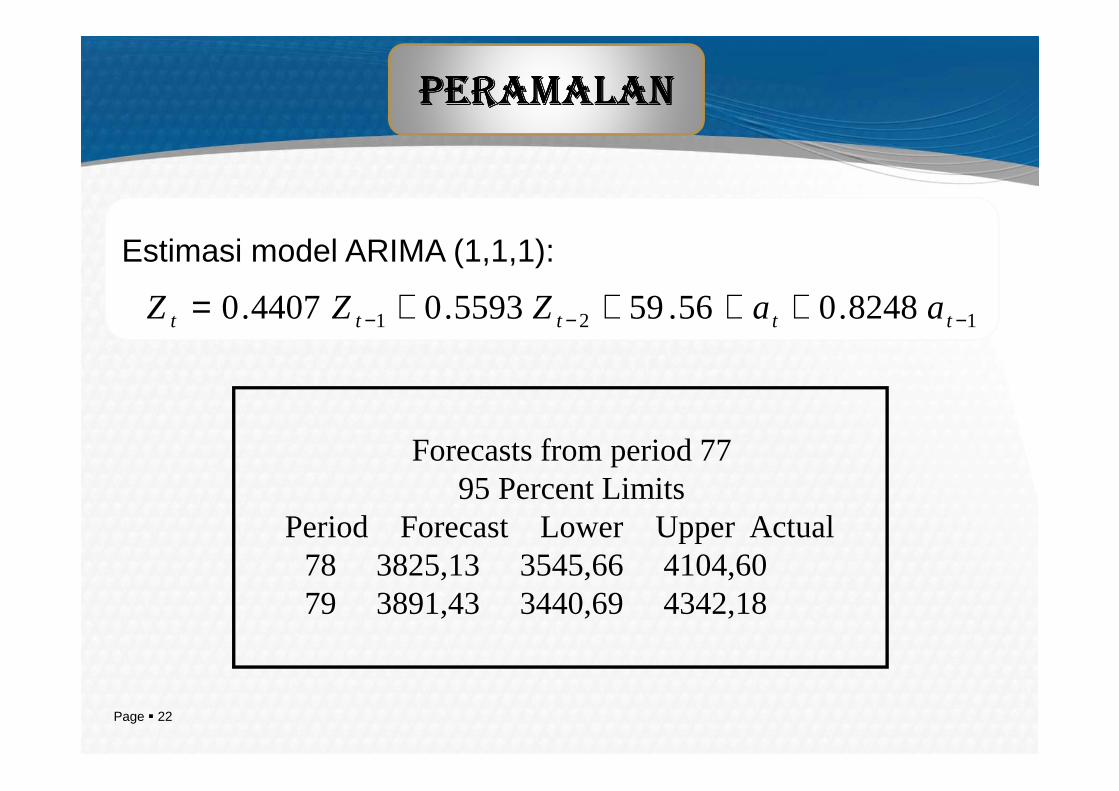

Estimasi model ARIMA (1,1,1):

121 8248.056.595593.04407.0 −−− ++++= ttttt aaZZZ

Page � 22

Forecasts from period 7795 Percent Limits

Period Forecast Lower Upper Actual78 3825,13 3545,66 4104,6079 3891,43 3440,69 4342,18

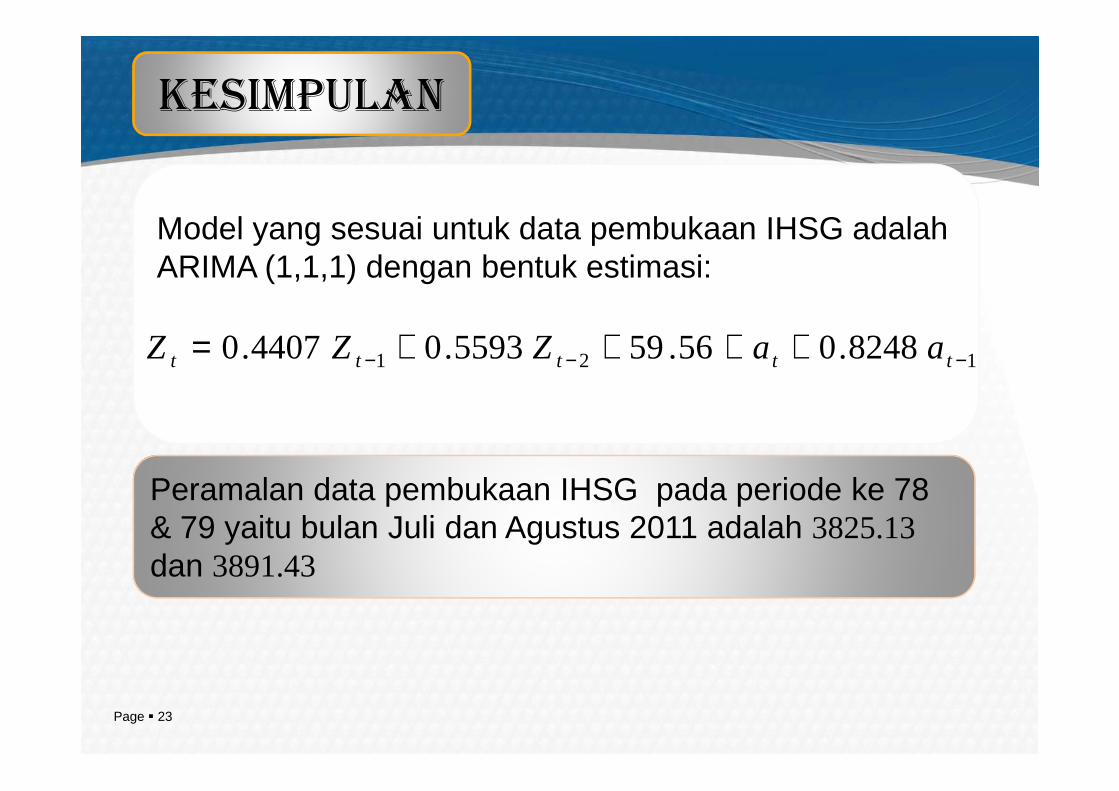

KESIMPULAN

Model yang sesuai untuk data pembukaan IHSG adalahARIMA (1,1,1) dengan bentuk estimasi:

121 8248.056.595593.04407.0 −−− ++++= ttttt aaZZZ

Page � 23

Peramalan data pembukaan IHSG pada periode ke 78 & 79 yaitu bulan Juli dan Agustus 2011 adalah 3825.13 dan 3891.43

Company LOGO

TERIMA KASIH

www.company.com