Embed Size (px)

Citation preview

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Parameter-free Machine Learning through Coin Betting

Francesco Orabona

Boston UniversityBoston, MA USA

Geometric Analysis Approach to AI Workshop

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Motivation of my Recent Work: Parameter-free Algorithms

Most of the algorithms we know/use in machine learning have parameters

E.g. regularization parameter in LASSO, k in k -Nearest Neighbourhood,topology of the networks in deep learning

Most of the time, a large enough validation set can be used to tune theparameters

But, at what computational price? Are they really necessary?

Are you ignoring some computational/sample complexities?

When is the last time you needed to tune the learning rate to sort a vector?Or to invert a matrix?

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Motivation of my Recent Work: Parameter-free Algorithms

Most of the algorithms we know/use in machine learning have parametersE.g. regularization parameter in LASSO, k in k -Nearest Neighbourhood,topology of the networks in deep learning

Most of the time, a large enough validation set can be used to tune theparameters

But, at what computational price? Are they really necessary?

Are you ignoring some computational/sample complexities?

When is the last time you needed to tune the learning rate to sort a vector?Or to invert a matrix?

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Motivation of my Recent Work: Parameter-free Algorithms

Most of the algorithms we know/use in machine learning have parametersE.g. regularization parameter in LASSO, k in k -Nearest Neighbourhood,topology of the networks in deep learning

Most of the time, a large enough validation set can be used to tune theparameters

But, at what computational price? Are they really necessary?

Are you ignoring some computational/sample complexities?

When is the last time you needed to tune the learning rate to sort a vector?Or to invert a matrix?

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Motivation of my Recent Work: Parameter-free Algorithms

Most of the algorithms we know/use in machine learning have parametersE.g. regularization parameter in LASSO, k in k -Nearest Neighbourhood,topology of the networks in deep learning

Most of the time, a large enough validation set can be used to tune theparameters

But, at what computational price? Are they really necessary?

Are you ignoring some computational/sample complexities?

When is the last time you needed to tune the learning rate to sort a vector?Or to invert a matrix?

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Motivation of my Recent Work: Parameter-free Algorithms

Most of the algorithms we know/use in machine learning have parametersE.g. regularization parameter in LASSO, k in k -Nearest Neighbourhood,topology of the networks in deep learning

Most of the time, a large enough validation set can be used to tune theparameters

But, at what computational price? Are they really necessary?

Are you ignoring some computational/sample complexities?

When is the last time you needed to tune the learning rate to sort a vector?Or to invert a matrix?

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Motivation of my Recent Work: Parameter-free Algorithms

Most of the algorithms we know/use in machine learning have parametersE.g. regularization parameter in LASSO, k in k -Nearest Neighbourhood,topology of the networks in deep learning

Most of the time, a large enough validation set can be used to tune theparameters

But, at what computational price? Are they really necessary?

Are you ignoring some computational/sample complexities?

When is the last time you needed to tune the learning rate to sort a vector?Or to invert a matrix?

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

My Dream: Truly Automatic Machine Learning

No parameters to tune

No humans in the loop

Some guarantees

Sometimes this is possible

This talk is about a method to achieve this dream in many interesting cases

Not the only way nor the only parameter-free method I proposed

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

My Dream: Truly Automatic Machine Learning

No parameters to tune

No humans in the loop

Some guarantees

Sometimes this is possible

This talk is about a method to achieve this dream in many interesting cases

Not the only way nor the only parameter-free method I proposed

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Outline

1 Optimization of Non-smooth Convex Functions

2 Coin BettingBetting on a CoinFrom Betting to OptimizationCOCOB

3 Experiments

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Outline

1 Optimization of Non-smooth Convex Functions

2 Coin BettingBetting on a CoinFrom Betting to OptimizationCOCOB

3 Experiments

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

How Subgradient Descent Work in Machine Learning?

w

F (w)

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

How Subgradient Descent Work in Machine Learning?

w

F (w)

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

How Subgradient Descent Work in Machine Learning?

w

F (w)

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

What About “Adaptive” Algorithms?

In the stochastic setting is even more challenging: the function at eachround is always the same only in expectation

What about AdaGrad?

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

What About “Adaptive” Algorithms?

In the stochastic setting is even more challenging: the function at eachround is always the same only in expectation

What about AdaGrad?

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

AdaGrad

w

F (w)

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

What the Theory Says?

Only strategy known: use a decreasing step size, O(η√

t

)Convergence after T iterations is O

(1√T

(‖w∗‖2

η+ η))

w∗ is the best solution

The optimal learning rate is with η = ‖w∗‖ that would give a rate ofO(

1√T‖w∗‖

)...but you don’t know w∗...

Why we cannot have an optimization algorithm that self-tunes its learning rate?

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

What the Theory Says?

Only strategy known: use a decreasing step size, O(η√

t

)Convergence after T iterations is O

(1√T

(‖w∗‖2

η+ η))

w∗ is the best solution

The optimal learning rate is with η = ‖w∗‖ that would give a rate ofO(

1√T‖w∗‖

)

...but you don’t know w∗...

Why we cannot have an optimization algorithm that self-tunes its learning rate?

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

What the Theory Says?

Only strategy known: use a decreasing step size, O(η√

t

)Convergence after T iterations is O

(1√T

(‖w∗‖2

η+ η))

w∗ is the best solution

The optimal learning rate is with η = ‖w∗‖ that would give a rate ofO(

1√T‖w∗‖

)...but you don’t know w∗...

Why we cannot have an optimization algorithm that self-tunes its learning rate?

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

What the Theory Says?

Only strategy known: use a decreasing step size, O(η√

t

)Convergence after T iterations is O

(1√T

(‖w∗‖2

η+ η))

w∗ is the best solution

The optimal learning rate is with η = ‖w∗‖ that would give a rate ofO(

1√T‖w∗‖

)...but you don’t know w∗...

Why we cannot have an optimization algorithm that self-tunes its learning rate?

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Parameter-free Optimization

[McMahan&Streeter, NIPS’12][McMahan&Abernethy, NIPS’13] suboptimal bound,1D

[Orabona, NIPS’13] suboptimal bound, Hilbert spaces

[McMahan&Orabona, COLT’14] optimal bound, Hilbert space

[Orabona, NIPS’14] data-dependent bound, analysis in RKHS, algorithm in VW

[Cutkosky&Boahen, NIPS’16, COLT’17] unbounded gradients

[van Erven&Koolen, NIPS’16] run multiple learning rates in parallel & aggregate

[Orabona&Pal, NIPS’16] coin-betting view

[Orabona&Tommasi, NIPS’17] coin-betting for deep learning

[Kotlowski, ALT’17] scale-free bound

[Foster et al., NIPS’17] run multiple learning rates in parallel & aggregate, works inBanach spaces

[Cutkosky&Orabona, COLT’18] coin-betting for Banach spaces

[Foster et al., COLT’18] parameter-free in Banach spaces, not data-dependent

Also, Learning with Experts algorithms: NormalHedge [Chaudhuri et al. NIPS’09],AdaNormalHedge [Luo&Schapire, NIPS’14, COLT’15], Squint [Koolen&Erven, COLT’15],etc.

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Parameter-free Optimization

[McMahan&Streeter, NIPS’12][McMahan&Abernethy, NIPS’13] suboptimal bound,1D

[Orabona, NIPS’13] suboptimal bound, Hilbert spaces

[McMahan&Orabona, COLT’14] optimal bound, Hilbert space

[Orabona, NIPS’14] data-dependent bound, analysis in RKHS, algorithm in VW

[Cutkosky&Boahen, NIPS’16, COLT’17] unbounded gradients

[van Erven&Koolen, NIPS’16] run multiple learning rates in parallel & aggregate

[Orabona&Pal, NIPS’16] coin-betting view

[Orabona&Tommasi, NIPS’17] coin-betting for deep learning

[Kotlowski, ALT’17] scale-free bound

[Foster et al., NIPS’17] run multiple learning rates in parallel & aggregate, works inBanach spaces

[Cutkosky&Orabona, COLT’18] coin-betting for Banach spaces

[Foster et al., COLT’18] parameter-free in Banach spaces, not data-dependent

Also, Learning with Experts algorithms: NormalHedge [Chaudhuri et al. NIPS’09],AdaNormalHedge [Luo&Schapire, NIPS’14, COLT’15], Squint [Koolen&Erven, COLT’15],etc.

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

Outline

1 Optimization of Non-smooth Convex Functions

2 Coin BettingBetting on a CoinFrom Betting to OptimizationCOCOB

3 Experiments

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

Betting on a Coin

Start with $1Bet wt money on head (wt > 0) or tails (wt < 0)

Cannot borrow money

Win or lose depending on the outcome of the coingt ∈ {−1, 1}Wealtht = Wealtht−1 + wtgt

Aim: Maximize gain on all sequences where the number of tails and head aredifferent

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

Optimal Betting Strategy for a Stochastic Coin: Kelly Betting (1956)

Known problem in economics

Bet a fraction of your money equal to2p − 1 = E[gt ] on tail at each round

E.g. p = 0.51⇒ bet 2%

Expected log wealth is linear in time200 400 600 800

Number of betting rounds

0

500

1000

1500

2000

2500

Mo

ne

y

Kelly Betting

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

Non-Stochastic setting, but Knowing the Future

Non-stochastic setting, T rounds

Assume to bet a fixed fraction of money at each round

What is the optimal fraction?

The optimal signed fraction at each time step t is∑T

i=1 giT

Hence you bet∑T

i=1 giT ·Wealtht−1

Winnings are exponential

Winnings > exp

((∑T

t=1 gt)2

2T

)

[McMahan&Abernethy, NIPS’13; Orabona&Pal, NIPS’16]

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

Non-Stochastic setting, but Knowing the Future

Non-stochastic setting, T rounds

Assume to bet a fixed fraction of money at each round

What is the optimal fraction?

The optimal signed fraction at each time step t is∑T

i=1 giT

Hence you bet∑T

i=1 giT ·Wealtht−1

Winnings are exponential

Winnings > exp

((∑T

t=1 gt)2

2T

)

[McMahan&Abernethy, NIPS’13; Orabona&Pal, NIPS’16]

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

Worst case Optimal Betting Strategy: Krichevsky-Trofimov Bettor

What if we don’t know the future?

Estimate probability of head with Krichevsky-Trofimov (KT) estimator:12 +# of heads in t rounds

t+1

No stochastic assumptions: KT has optimal regret w.r.t. the log loss

Hence, on round t bet a fraction of your money equal to |∑t−1

i=1 gi |t , on the

side that appeared more often

Still exponential

Winnings of KT Bettor ≥ Winnings knowing the future2√

T

Not the only possible strategy, but the simplest one

Coin betting is solvable with a parameter-free optimal strategy, but what is theconnection with SGD?

[Orabona&Pal, NIPS’16]

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

Worst case Optimal Betting Strategy: Krichevsky-Trofimov Bettor

What if we don’t know the future?Estimate probability of head with Krichevsky-Trofimov (KT) estimator:12 +# of heads in t rounds

t+1

No stochastic assumptions: KT has optimal regret w.r.t. the log loss

Hence, on round t bet a fraction of your money equal to |∑t−1

i=1 gi |t , on the

side that appeared more often

Still exponential

Winnings of KT Bettor ≥ Winnings knowing the future2√

T

Not the only possible strategy, but the simplest one

Coin betting is solvable with a parameter-free optimal strategy, but what is theconnection with SGD?

[Orabona&Pal, NIPS’16]

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

Worst case Optimal Betting Strategy: Krichevsky-Trofimov Bettor

What if we don’t know the future?Estimate probability of head with Krichevsky-Trofimov (KT) estimator:12 +# of heads in t rounds

t+1

No stochastic assumptions: KT has optimal regret w.r.t. the log loss

Hence, on round t bet a fraction of your money equal to |∑t−1

i=1 gi |t , on the

side that appeared more often

Still exponential

Winnings of KT Bettor ≥ Winnings knowing the future2√

T

Not the only possible strategy, but the simplest one

Coin betting is solvable with a parameter-free optimal strategy, but what is theconnection with SGD?

[Orabona&Pal, NIPS’16]

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

Worst case Optimal Betting Strategy: Krichevsky-Trofimov Bettor

What if we don’t know the future?Estimate probability of head with Krichevsky-Trofimov (KT) estimator:12 +# of heads in t rounds

t+1

No stochastic assumptions: KT has optimal regret w.r.t. the log loss

Hence, on round t bet a fraction of your money equal to |∑t−1

i=1 gi |t , on the

side that appeared more often

Still exponential

Winnings of KT Bettor ≥ Winnings knowing the future2√

T

Not the only possible strategy, but the simplest one

Coin betting is solvable with a parameter-free optimal strategy, but what is theconnection with SGD?

[Orabona&Pal, NIPS’16]

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

Worst case Optimal Betting Strategy: Krichevsky-Trofimov Bettor

What if we don’t know the future?Estimate probability of head with Krichevsky-Trofimov (KT) estimator:12 +# of heads in t rounds

t+1

No stochastic assumptions: KT has optimal regret w.r.t. the log loss

Hence, on round t bet a fraction of your money equal to |∑t−1

i=1 gi |t , on the

side that appeared more often

Still exponential

Winnings of KT Bettor ≥ Winnings knowing the future2√

T

Not the only possible strategy, but the simplest one

Coin betting is solvable with a parameter-free optimal strategy, but what is theconnection with SGD?

[Orabona&Pal, NIPS’16]

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

Worst case Optimal Betting Strategy: Krichevsky-Trofimov Bettor

What if we don’t know the future?Estimate probability of head with Krichevsky-Trofimov (KT) estimator:12 +# of heads in t rounds

t+1

No stochastic assumptions: KT has optimal regret w.r.t. the log loss

Hence, on round t bet a fraction of your money equal to |∑t−1

i=1 gi |t , on the

side that appeared more often

Still exponential

Winnings of KT Bettor ≥ Winnings knowing the future2√

T

Not the only possible strategy, but the simplest one

Coin betting is solvable with a parameter-free optimal strategy, but what is theconnection with SGD?

[Orabona&Pal, NIPS’16]

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

1D Optimization through Betting

Assume that there exists a function H(·) such that our betting strategy willguarantee that the wealth after T rounds will be at least H(

∑Tt=1 gt) for any

arbitrary sequence g1, · · · , gT

For KT H(∑T

t=1 gt ) = C exp((∑T

t=1 gt )2/T )/

√T )

We want to minimize F (w) = |w − 10|Let’s set a betting game: bet wt dollars on gt = −∂F (wt) ∈ {−1,+1}Claim: the average of the bets will converge to the minimum of F (w) at arate that depends on how good is our betting strategy!

F

(1T

T∑t=1

wt

)− F (w∗)

Jensen≤ 1

T

T∑t=1

F (wt)− F (w∗)Convexity≤ 1

T

(T∑

t=1

gtw∗ −T∑

t=1

gtwt

)Def. H≤ 1

T

(T∑

t=1

gtw∗ − H

(T∑

t=1

gt

))Max≤ 1

T maxv

vw∗ − H(v) Def H∗= H∗(w∗)

T

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

1D Optimization through Betting

Assume that there exists a function H(·) such that our betting strategy willguarantee that the wealth after T rounds will be at least H(

∑Tt=1 gt) for any

arbitrary sequence g1, · · · , gT

For KT H(∑T

t=1 gt ) = C exp((∑T

t=1 gt )2/T )/

√T )

We want to minimize F (w) = |w − 10|Let’s set a betting game: bet wt dollars on gt = −∂F (wt) ∈ {−1,+1}Claim: the average of the bets will converge to the minimum of F (w) at arate that depends on how good is our betting strategy!

F

(1T

T∑t=1

wt

)− F (w∗)

Jensen≤ 1

T

T∑t=1

F (wt)− F (w∗)Convexity≤ 1

T

(T∑

t=1

gtw∗ −T∑

t=1

gtwt

)Def. H≤ 1

T

(T∑

t=1

gtw∗ − H

(T∑

t=1

gt

))Max≤ 1

T maxv

vw∗ − H(v) Def H∗= H∗(w∗)

T

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

1D Optimization through Betting

Assume that there exists a function H(·) such that our betting strategy willguarantee that the wealth after T rounds will be at least H(

∑Tt=1 gt) for any

arbitrary sequence g1, · · · , gT

For KT H(∑T

t=1 gt ) = C exp((∑T

t=1 gt )2/T )/

√T )

We want to minimize F (w) = |w − 10|

Let’s set a betting game: bet wt dollars on gt = −∂F (wt) ∈ {−1,+1}Claim: the average of the bets will converge to the minimum of F (w) at arate that depends on how good is our betting strategy!

F

(1T

T∑t=1

wt

)− F (w∗)

Jensen≤ 1

T

T∑t=1

F (wt)− F (w∗)Convexity≤ 1

T

(T∑

t=1

gtw∗ −T∑

t=1

gtwt

)Def. H≤ 1

T

(T∑

t=1

gtw∗ − H

(T∑

t=1

gt

))Max≤ 1

T maxv

vw∗ − H(v) Def H∗= H∗(w∗)

T

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

1D Optimization through Betting

Assume that there exists a function H(·) such that our betting strategy willguarantee that the wealth after T rounds will be at least H(

∑Tt=1 gt) for any

arbitrary sequence g1, · · · , gT

For KT H(∑T

t=1 gt ) = C exp((∑T

t=1 gt )2/T )/

√T )

We want to minimize F (w) = |w − 10|Let’s set a betting game: bet wt dollars on gt = −∂F (wt) ∈ {−1,+1}

Claim: the average of the bets will converge to the minimum of F (w) at arate that depends on how good is our betting strategy!

F

(1T

T∑t=1

wt

)− F (w∗)

Jensen≤ 1

T

T∑t=1

F (wt)− F (w∗)Convexity≤ 1

T

(T∑

t=1

gtw∗ −T∑

t=1

gtwt

)Def. H≤ 1

T

(T∑

t=1

gtw∗ − H

(T∑

t=1

gt

))Max≤ 1

T maxv

vw∗ − H(v) Def H∗= H∗(w∗)

T

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

1D Optimization through Betting

Assume that there exists a function H(·) such that our betting strategy willguarantee that the wealth after T rounds will be at least H(

∑Tt=1 gt) for any

arbitrary sequence g1, · · · , gT

For KT H(∑T

t=1 gt ) = C exp((∑T

t=1 gt )2/T )/

√T )

We want to minimize F (w) = |w − 10|Let’s set a betting game: bet wt dollars on gt = −∂F (wt) ∈ {−1,+1}Claim: the average of the bets will converge to the minimum of F (w) at arate that depends on how good is our betting strategy!

F

(1T

T∑t=1

wt

)− F (w∗)

Jensen≤ 1

T

T∑t=1

F (wt)− F (w∗)Convexity≤ 1

T

(T∑

t=1

gtw∗ −T∑

t=1

gtwt

)Def. H≤ 1

T

(T∑

t=1

gtw∗ − H

(T∑

t=1

gt

))Max≤ 1

T maxv

vw∗ − H(v) Def H∗= H∗(w∗)

T

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

1D Optimization through Betting

Assume that there exists a function H(·) such that our betting strategy willguarantee that the wealth after T rounds will be at least H(

∑Tt=1 gt) for any

arbitrary sequence g1, · · · , gT

For KT H(∑T

t=1 gt ) = C exp((∑T

t=1 gt )2/T )/

√T )

We want to minimize F (w) = |w − 10|Let’s set a betting game: bet wt dollars on gt = −∂F (wt) ∈ {−1,+1}Claim: the average of the bets will converge to the minimum of F (w) at arate that depends on how good is our betting strategy!

F

(1T

T∑t=1

wt

)− F (w∗)

Jensen≤ 1

T

T∑t=1

F (wt)− F (w∗)

Convexity≤ 1

T

(T∑

t=1

gtw∗ −T∑

t=1

gtwt

)Def. H≤ 1

T

(T∑

t=1

gtw∗ − H

(T∑

t=1

gt

))Max≤ 1

T maxv

vw∗ − H(v) Def H∗= H∗(w∗)

T

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

1D Optimization through Betting

Assume that there exists a function H(·) such that our betting strategy willguarantee that the wealth after T rounds will be at least H(

∑Tt=1 gt) for any

arbitrary sequence g1, · · · , gT

For KT H(∑T

t=1 gt ) = C exp((∑T

t=1 gt )2/T )/

√T )

We want to minimize F (w) = |w − 10|Let’s set a betting game: bet wt dollars on gt = −∂F (wt) ∈ {−1,+1}Claim: the average of the bets will converge to the minimum of F (w) at arate that depends on how good is our betting strategy!

F

(1T

T∑t=1

wt

)− F (w∗)

Jensen≤ 1

T

T∑t=1

F (wt)− F (w∗)Convexity≤ 1

T

(T∑

t=1

gtw∗ −T∑

t=1

gtwt

)

Def. H≤ 1

T

(T∑

t=1

gtw∗ − H

(T∑

t=1

gt

))Max≤ 1

T maxv

vw∗ − H(v) Def H∗= H∗(w∗)

T

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

1D Optimization through Betting

Assume that there exists a function H(·) such that our betting strategy willguarantee that the wealth after T rounds will be at least H(

∑Tt=1 gt) for any

arbitrary sequence g1, · · · , gT

For KT H(∑T

t=1 gt ) = C exp((∑T

t=1 gt )2/T )/

√T )

We want to minimize F (w) = |w − 10|Let’s set a betting game: bet wt dollars on gt = −∂F (wt) ∈ {−1,+1}Claim: the average of the bets will converge to the minimum of F (w) at arate that depends on how good is our betting strategy!

F

(1T

T∑t=1

wt

)− F (w∗)

Jensen≤ 1

T

T∑t=1

F (wt)− F (w∗)Convexity≤ 1

T

(T∑

t=1

gtw∗ −T∑

t=1

gtwt

)Def. H≤ 1

T

(T∑

t=1

gtw∗ − H

(T∑

t=1

gt

))

Max≤ 1

T maxv

vw∗ − H(v) Def H∗= H∗(w∗)

T

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

1D Optimization through Betting

Assume that there exists a function H(·) such that our betting strategy willguarantee that the wealth after T rounds will be at least H(

∑Tt=1 gt) for any

arbitrary sequence g1, · · · , gT

For KT H(∑T

t=1 gt ) = C exp((∑T

t=1 gt )2/T )/

√T )

We want to minimize F (w) = |w − 10|Let’s set a betting game: bet wt dollars on gt = −∂F (wt) ∈ {−1,+1}Claim: the average of the bets will converge to the minimum of F (w) at arate that depends on how good is our betting strategy!

F

(1T

T∑t=1

wt

)− F (w∗)

Jensen≤ 1

T

T∑t=1

F (wt)− F (w∗)Convexity≤ 1

T

(T∑

t=1

gtw∗ −T∑

t=1

gtwt

)Def. H≤ 1

T

(T∑

t=1

gtw∗ − H

(T∑

t=1

gt

))Max≤ 1

T maxv

vw∗ − H(v)

Def H∗= H∗(w∗)

T

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

1D Optimization through Betting

Assume that there exists a function H(·) such that our betting strategy willguarantee that the wealth after T rounds will be at least H(

∑Tt=1 gt) for any

arbitrary sequence g1, · · · , gT

For KT H(∑T

t=1 gt ) = C exp((∑T

t=1 gt )2/T )/

√T )

We want to minimize F (w) = |w − 10|Let’s set a betting game: bet wt dollars on gt = −∂F (wt) ∈ {−1,+1}Claim: the average of the bets will converge to the minimum of F (w) at arate that depends on how good is our betting strategy!

F

(1T

T∑t=1

wt

)− F (w∗)

Jensen≤ 1

T

T∑t=1

F (wt)− F (w∗)Convexity≤ 1

T

(T∑

t=1

gtw∗ −T∑

t=1

gtwt

)Def. H≤ 1

T

(T∑

t=1

gtw∗ − H

(T∑

t=1

gt

))Max≤ 1

T maxv

vw∗ − H(v) Def H∗= H∗(w∗)

T

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

KT as an Optimization Algorithm

Assume ∂F (wt) ∈ {−1,+1}

wt =−

∑t−1i=1 ∂F (wi )

t Wealtht−1 =−

∑t−1i=1 ∂F (wi )

t (1−∑t−1

i=1 ∂F (wi) · wi)

Theorem (Informal)

KT betting in 1-d guarantees

F

(1T

T∑t=1

wt

)− F (w∗) ≤ C

|w∗|√

log(T )√T

[Orabona&Pal, NIPS’16]

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

KT as an Optimization Algorithm

Assume the function 1-Lipschitz

w t =−

∑t−1i=1 ∂F (w i )

t Wealtht−1 =−

∑t−1i=1 ∂F (w i )

t (1−∑t−1

i=1 〈∂F (w i),w i〉)

Theorem (Informal)

KT betting in Hilbert spaces guarantees

F

(1T

T∑t=1

w t

)− F (w∗) ≤ C

‖w∗‖√

log(T )√T

Proof idea:

“Worst” direction for gradient at time t is parallel to∑t−1

i=1 g i

“Worst” gradient have ‖gt‖ = 1

[Orabona&Pal, NIPS’16]

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

KT as an Optimization Algorithm

Assume the function 1-Lipschitz

w t =−

∑t−1i=1 ∂F (w i )

t Wealtht−1 =−

∑t−1i=1 ∂F (w i )

t (1−∑t−1

i=1 〈∂F (w i),w i〉)

Theorem (Informal)

KT betting in Hilbert spaces guarantees

F

(1T

T∑t=1

w t

)− F (w∗) ≤ min

ηC

(‖w∗‖2

η+ η)√

log(T )√

T

Compare it to Gradient Descent guarantee with learning rate η√t

F

(1T

T∑t=1

w t

)− F (w∗) ≤ C′

‖w∗‖2

η+ η

√T

[Orabona&Pal, NIPS’16]

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

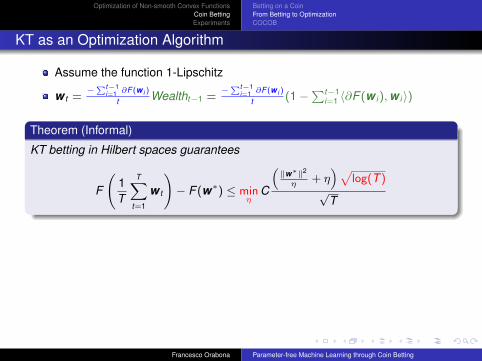

Betting on a CoinFrom Betting to OptimizationCOCOB

KT as an Optimization Algorithm

Assume the function 1-Lipschitz

w t =−

∑t−1i=1 ∂F (w i )

t Wealtht−1 =−

∑t−1i=1 ∂F (w i )

t (1−∑t−1

i=1 〈∂F (w i),w i〉)

Theorem (Informal)

KT betting in Hilbert spaces guarantees

F

(1T

T∑t=1

w t

)− F (w∗) ≤ min

ηC

(‖w∗‖2

η+ η)√

log(T )√

T

Compare it to Gradient Descent guarantee with learning rate η√t

F

(1T

T∑t=1

w t

)− F (w∗) ≤ C′

‖w∗‖2

η+ η

√T

[Orabona&Pal, NIPS’16]

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

How the Betting Approach Work?

w

f (w)

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

Effective Learning Rate

0 50 100 150 200

Iterations

0

1

2

3

4

5

6

Eff

ective

Le

arn

ing

Ra

te

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

Improving KT: Continuous Coin Betting (COCOB)

We want per-coordinate learning rates

One coin for each coordinate

We want faster convergence with sparse gradients

KT strategy: w t =−

∑t−1i=1 ∂F (w i )

t Wealtht−1

COCOB strategy: w t = σ

(−

∑t−1i=1 ∂F (w i )

L(L+∑t−1

i=1 |∂F (w i )|)

)Wealtht−1

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

Improving KT: Continuous Coin Betting (COCOB)

We want per-coordinate learning ratesOne coin for each coordinate

We want faster convergence with sparse gradients

KT strategy: w t =−

∑t−1i=1 ∂F (w i )

t Wealtht−1

COCOB strategy: w t = σ

(−

∑t−1i=1 ∂F (w i )

L(L+∑t−1

i=1 |∂F (w i )|)

)Wealtht−1

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

Improving KT: Continuous Coin Betting (COCOB)

We want per-coordinate learning ratesOne coin for each coordinate

We want faster convergence with sparse gradients

KT strategy: w t =−

∑t−1i=1 ∂F (w i )

t Wealtht−1

COCOB strategy: w t = σ

(−

∑t−1i=1 ∂F (w i )

L(L+∑t−1

i=1 |∂F (w i )|)

)Wealtht−1

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

Improving KT: Continuous Coin Betting (COCOB)

We want per-coordinate learning ratesOne coin for each coordinate

We want faster convergence with sparse gradients

KT strategy: w t =−

∑t−1i=1 ∂F (w i )

t Wealtht−1

COCOB strategy: w t = σ

(−

∑t−1i=1 ∂F (w i )

L(L+∑t−1

i=1 |∂F (w i )|)

)Wealtht−1

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

COCOB for Deep Learning

wt,i = σ

(−∑t−1

j=1 gj,i

Li(Li +∑t−1

j=1 |gj,i |)

)Wealtht−1,i

Estimate Li over time

Assures that the Wealth remains positive

Remove the sigmoid

Make sure first steps are small

Lt,i = max(Lt−1,i , |gt,i |)Wealtht−1,i = min(Wealtht−1,i , Lt,i)

wt,i =−∑t−1

j=1 gj,i

Lt,i max(Lt,i +∑t−1

j=1 |gj,i |, 100Lt,i)Wealtht−1,i

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

COCOB for Deep Learning

wt,i = σ

(−∑t−1

j=1 gj,i

Li(Li +∑t−1

j=1 |gj,i |)

)Wealtht−1,i

Estimate Li over time

Assures that the Wealth remains positive

Remove the sigmoid

Make sure first steps are small

Lt,i = max(Lt−1,i , |gt,i |)Wealtht−1,i = min(Wealtht−1,i , Lt,i)

wt,i =−∑t−1

j=1 gj,i

Lt,i max(Lt,i +∑t−1

j=1 |gj,i |, 100Lt,i)Wealtht−1,i

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

COCOB for Deep Learning

wt,i = σ

(−∑t−1

j=1 gj,i

Li(Li +∑t−1

j=1 |gj,i |)

)Wealtht−1,i

Estimate Li over time

Assures that the Wealth remains positive

Remove the sigmoid

Make sure first steps are small

Lt,i = max(Lt−1,i , |gt,i |)Wealtht−1,i = min(Wealtht−1,i , Lt,i)

wt,i =−∑t−1

j=1 gj,i

Lt,i max(Lt,i +∑t−1

j=1 |gj,i |, 100Lt,i)Wealtht−1,i

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

COCOB-Backprop: Coin-betting for Deep Learning

Require: w1 ∈ Rd (initial weights)Initialize: L0,i ← 0, G0,i ← 0, Reward0,i ← 0, θ0,i ← 0, i = 1, · · · , drepeat

Get a stochastic subgradient gtfor each i-th weight in the network do

Rewardt,i ← max(Rewardt−1,i − (wt,i − w1,i )gt,i , 0)Lt,i ← max(Lt−1,i , |gt,i |)Gt,i ← Gt−1,i + |gt,i |θt,i ← θt−1,i + gt,i

wt+1,i ← w1,i −θt,i

Lt,i max(Gt,i+Lt,i ,100Lt,i )

(Lt,i + Rewardt,i

)end for

until Stopping condition is met

Theorem (Informal)

Up to√

log T terms, the performance guarantee is the same one obtained byAdaGrad tuning the learning rate for each single weight.

[Tommasi&Orabona, NIPS’17; Cutkosky&Orabona, COLT’18]

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Betting on a CoinFrom Betting to OptimizationCOCOB

And More!

All the results presented holds in the strict more difficult setting ofadversarial online learning

Learning in RKHS without regularization nor learning rates [Orabona,NIPS’14]

Learning With Expert Advice [Orabona&Pal, NIPS’16]

Sleeping Experts [Jun et al., AISTATS’17]

Online Learning with changing environments [Jun et al., AISTATS’17]

Coin-betting in Banach spaces, i.e. any norm [Cutkosky&Orabona,COLT’18]

Adaptation to the curvature: faster rates for strongly convex functions[Cutkosky&Orabona, COLT’18]

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Outline

1 Optimization of Non-smooth Convex Functions

2 Coin BettingBetting on a CoinFrom Betting to OptimizationCOCOB

3 Experiments

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Deep Learning: MNIST, fully connected

Training cost (cross-entropy) (left) and testing error rate (0/1 loss) (right) vs. thenumber epochs

TensorFlow COCOB code: http://github.com/bremen79/cocob

[Orabona&Tommasi, NIPS’17]

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Deep Learning: MNIST, CNN

Training cost (cross-entropy) (left) and testing error rate (0/1 loss) (right) vs. thenumber epochs

TensorFlow COCOB code: http://github.com/bremen79/cocob

[Orabona&Tommasi, NIPS’17]

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Deep Learning: PTB, word-level

0 10 20 30 40Epochs

0

100

200

300

400

500

600

Per

plex

ity

Word Prediction on PTB - Training Cost

AdaGrad 0.25RMSprop 0.001Adadelta 2.5Adam 0.00075COCOB

0 10 20 30 40Epochs

50

100

150

200

250

300

350

400

Per

plex

ity

Word Prediction on PTB - Test Cost

AdaGrad 0.25RMSprop 0.001Adadelta 2.5Adam 0.00075COCOB

Training cost (left) and test cost (right) measured as average per-word perplexityvs. the number epochs

TensorFlow COCOB code: http://github.com/bremen79/cocob

[Orabona&Tommasi, NIPS’17]

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Conclusions

Learning rates in SGD for quasi-convex Lipschitz functions areunnecessary

SGD, Learning with Experts, SVMs, etc. can be reduced to betting on acoin

Betting algorithms are easy to design, parameter-free, and (most of thetime) optimal

Future Work:

Beyond quasi-convex functions: convergence to critical point

Coin betting and Newton algorithms?

Francesco Orabona Parameter-free Machine Learning through Coin Betting

Optimization of Non-smooth Convex FunctionsCoin BettingExperiments

Thanks for your attention

http://francesco.orabona.com

Thanks to my collaborators: Ashok Cutkosky, Kwang-Sung Jun, David Pal,Brendan McMahan, Tatiana Tommasi, Rebecca Willett, Stephen Wright

Thanks to the support of Google and NSF

Francesco Orabona Parameter-free Machine Learning through Coin Betting