Embed Size (px)

Citation preview

February, 2017

Key growth areas ahead

Overview of opportunities for new and

existing aftermarket companies in the KSA

Table of Contents

1

2

3

4

5

6

Macroeconomic Background and Outlook

New Vehicle Market Dynamics

Vehicles In Operation Analysis

Aftermarket Analysis

Global Trends and Local Perspective

About Frost & Sullivan

3

5

8

11

14

19

2

Macroeconomic Background and Outlook

3

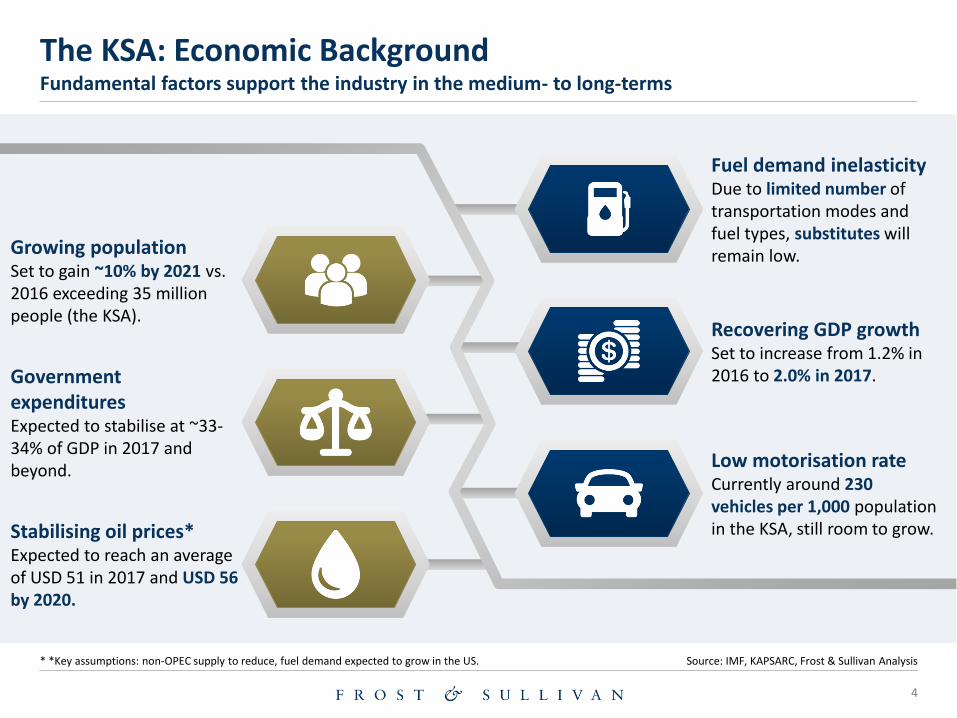

The KSA: Economic Background Fundamental factors support the industry in the medium- to long-terms

* *Key assumptions: non-OPEC supply to reduce, fuel demand expected to grow in the US. Source: IMF, KAPSARC, Frost & Sullivan Analysis

Fuel demand inelasticity Due to limited number of transportation modes and fuel types, substitutes will remain low.

Recovering GDP growth Set to increase from 1.2% in 2016 to 2.0% in 2017.

Low motorisation rate Currently around 230 vehicles per 1,000 population in the KSA, still room to grow.

Growing population Set to gain ~10% by 2021 vs. 2016 exceeding 35 million people (the KSA).

Government expenditures Expected to stabilise at ~33-34% of GDP in 2017 and beyond.

Stabilising oil prices* Expected to reach an average of USD 51 in 2017 and USD 56 by 2020.

4

New Vehicle Market Dynamics

5

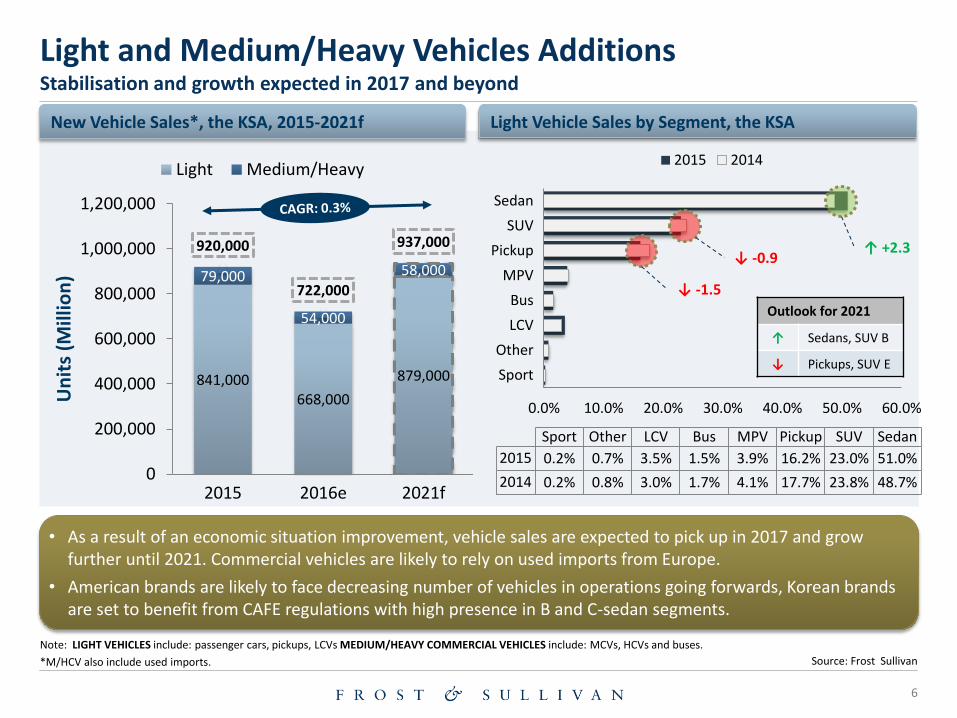

Light and Medium/Heavy Vehicles Additions Stabilisation and growth expected in 2017 and beyond

Note: LIGHT VEHICLES include: passenger cars, pickups, LCVs MEDIUM/HEAVY COMMERCIAL VEHICLES include: MCVs, HCVs and buses.

*M/HCV also include used imports. Source: Frost Sullivan

841,000 668,000

879,000

79,000

54,000

58,000

920,000

722,000

937,000

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

2015 2016e 2021f

Un

its

(Mill

ion

)

Light Medium/Heavy

• As a result of an economic situation improvement, vehicle sales are expected to pick up in 2017 and grow further until 2021. Commercial vehicles are likely to rely on used imports from Europe.

• American brands are likely to face decreasing number of vehicles in operations going forwards, Korean brands are set to benefit from CAFE regulations with high presence in B and C-sedan segments.

New Vehicle Sales*, the KSA, 2015-2021f

6

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0%

Sport

Other

LCV

Bus

MPV

Pickup

SUV

Sedan

Sport Other LCV Bus MPV Pickup SUV Sedan

2015 0.2% 0.7% 3.5% 1.5% 3.9% 16.2% 23.0% 51.0%

2014 0.2% 0.8% 3.0% 1.7% 4.1% 17.7% 23.8% 48.7%

2015 2014

↑ +2.3

↓ -1.5

↓ -0.9

Light Vehicle Sales by Segment, the KSA

Outlook for 2021

↑ Sedans, SUV B

↓ Pickups, SUV E

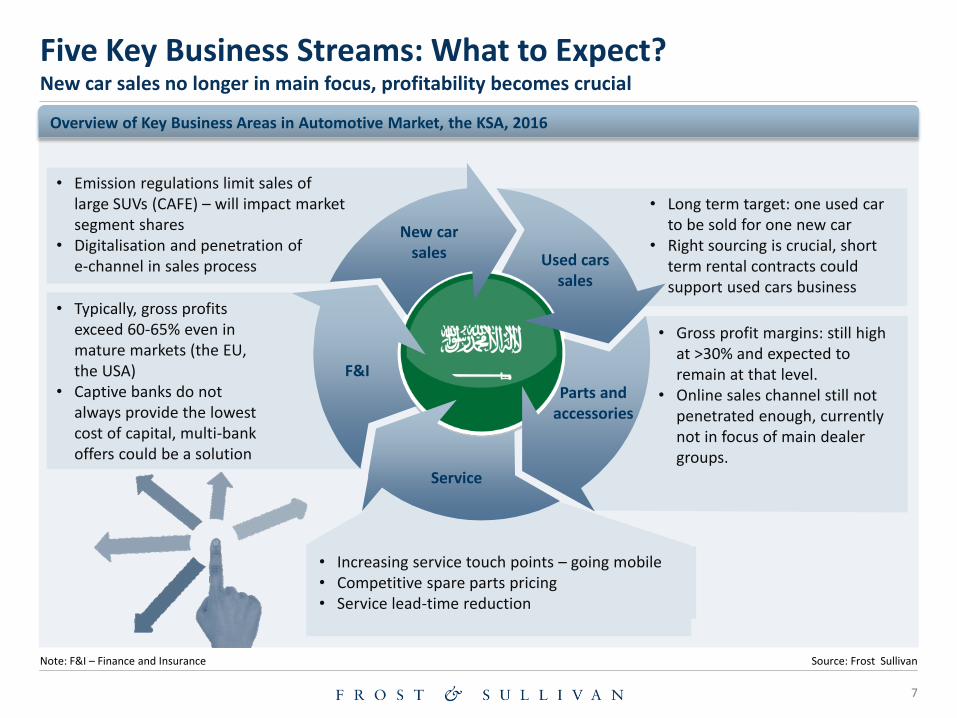

• Long term target: one used car to be sold for one new car

• Right sourcing is crucial, short term rental contracts could support used cars business

• Gross profit margins: still high at >30% and expected to remain at that level.

• Online sales channel still not penetrated enough, currently not in focus of main dealer groups.

• Typically, gross profits exceed 60-65% even in mature markets (the EU, the USA)

• Captive banks do not always provide the lowest cost of capital, multi-bank offers could be a solution

• Emission regulations limit sales of large SUVs (CAFE) – will impact market segment shares

• Digitalisation and penetration of e-channel in sales process

• Increasing service touch points – going mobile • Competitive spare parts pricing • Service lead-time reduction

Five Key Business Streams: What to Expect? New car sales no longer in main focus, profitability becomes crucial

Note: F&I – Finance and Insurance Source: Frost Sullivan

Overview of Key Business Areas in Automotive Market, the KSA, 2016

New car sales Used cars

sales

Parts and accessories

Service

F&I

7

Vehicles In Operation Analysis

8

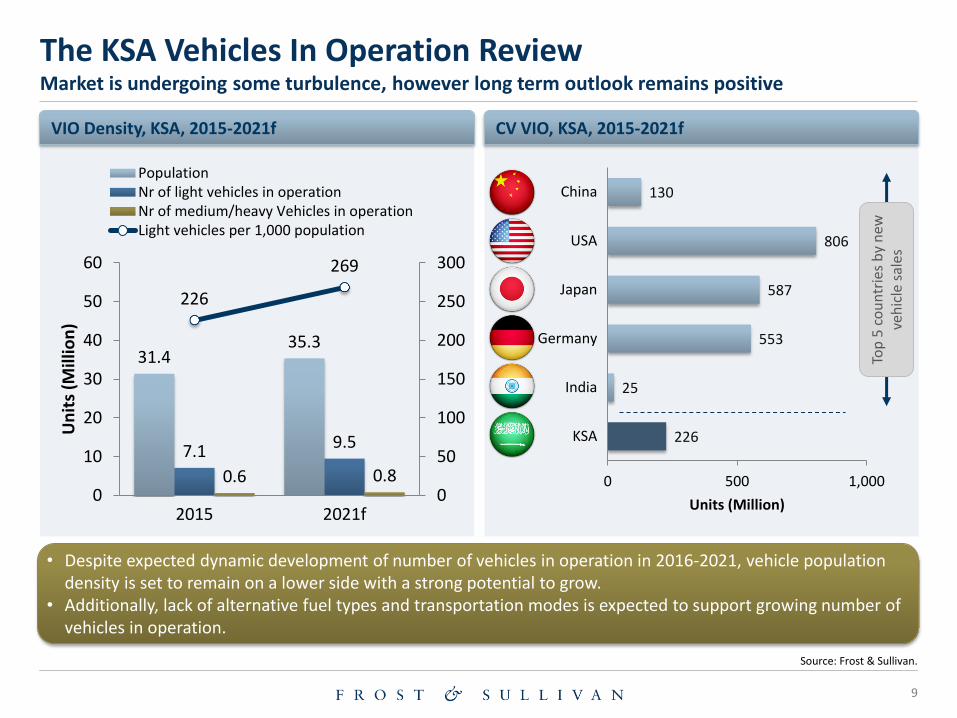

The KSA Vehicles In Operation Review Market is undergoing some turbulence, however long term outlook remains positive

Source: Frost & Sullivan.

31.4 35.3

7.1 9.5

0.6 0.8

226

269

0

50

100

150

200

250

300

0

10

20

30

40

50

60

2015 2021f

Un

its

(Mill

ion

)

PopulationNr of light vehicles in operationNr of medium/heavy Vehicles in operationLight vehicles per 1,000 population

• Despite expected dynamic development of number of vehicles in operation in 2016-2021, vehicle population density is set to remain on a lower side with a strong potential to grow.

• Additionally, lack of alternative fuel types and transportation modes is expected to support growing number of vehicles in operation.

CV VIO, KSA, 2015-2021f VIO Density, KSA, 2015-2021f

9

226

25

553

587

806

130

0 500 1,000

KSA

India

Germany

Japan

USA

China

Units (Million)

Top

5 c

ou

ntr

ies

by

new

ve

hic

le s

ales

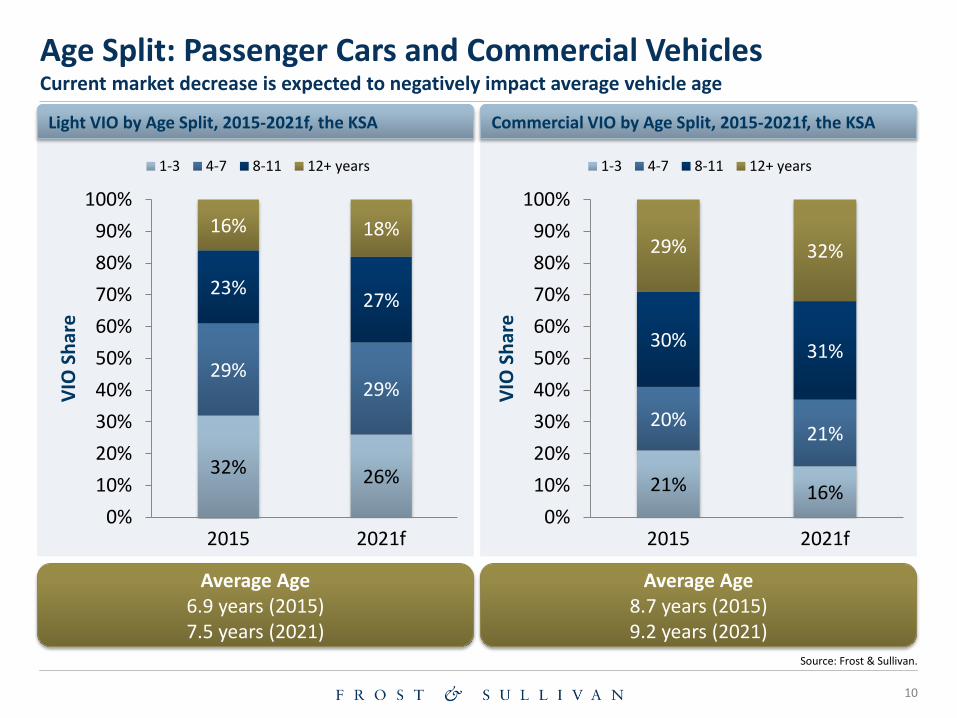

Age Split: Passenger Cars and Commercial Vehicles Current market decrease is expected to negatively impact average vehicle age

Source: Frost & Sullivan.

32% 26%

29% 29%

23% 27%

16% 18%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2021f

VIO

Sh

are

1-3 4-7 8-11 12+ years

21% 16%

20% 21%

30% 31%

29% 32%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2021f

VIO

Sh

are

1-3 4-7 8-11 12+ years

Average Age 6.9 years (2015) 7.5 years (2021)

Average Age 8.7 years (2015) 9.2 years (2021)

Light VIO by Age Split, 2015-2021f, the KSA Commercial VIO by Age Split, 2015-2021f, the KSA

10

Aftermarket Analysis

11

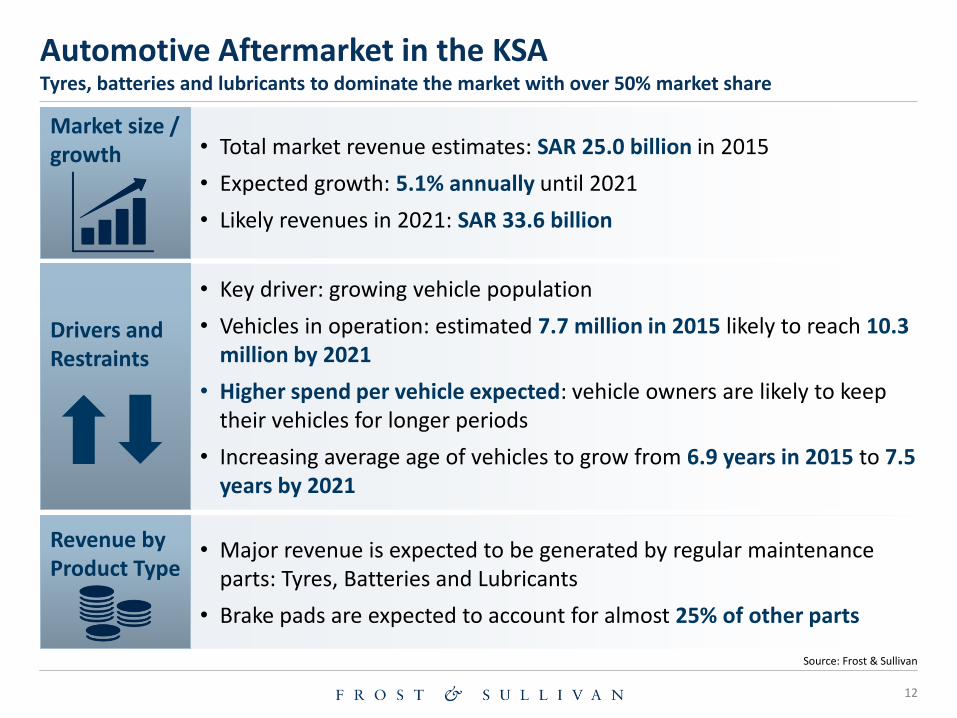

Automotive Aftermarket in the KSA Tyres, batteries and lubricants to dominate the market with over 50% market share

Source: Frost & Sullivan

• Total market revenue estimates: SAR 25.0 billion in 2015

• Expected growth: 5.1% annually until 2021

• Likely revenues in 2021: SAR 33.6 billion

• Key driver: growing vehicle population

• Vehicles in operation: estimated 7.7 million in 2015 likely to reach 10.3 million by 2021

• Higher spend per vehicle expected: vehicle owners are likely to keep their vehicles for longer periods

• Increasing average age of vehicles to grow from 6.9 years in 2015 to 7.5 years by 2021

• Major revenue is expected to be generated by regular maintenance parts: Tyres, Batteries and Lubricants

• Brake pads are expected to account for almost 25% of other parts

Market size / growth

Drivers and Restraints

Revenue by Product Type

12

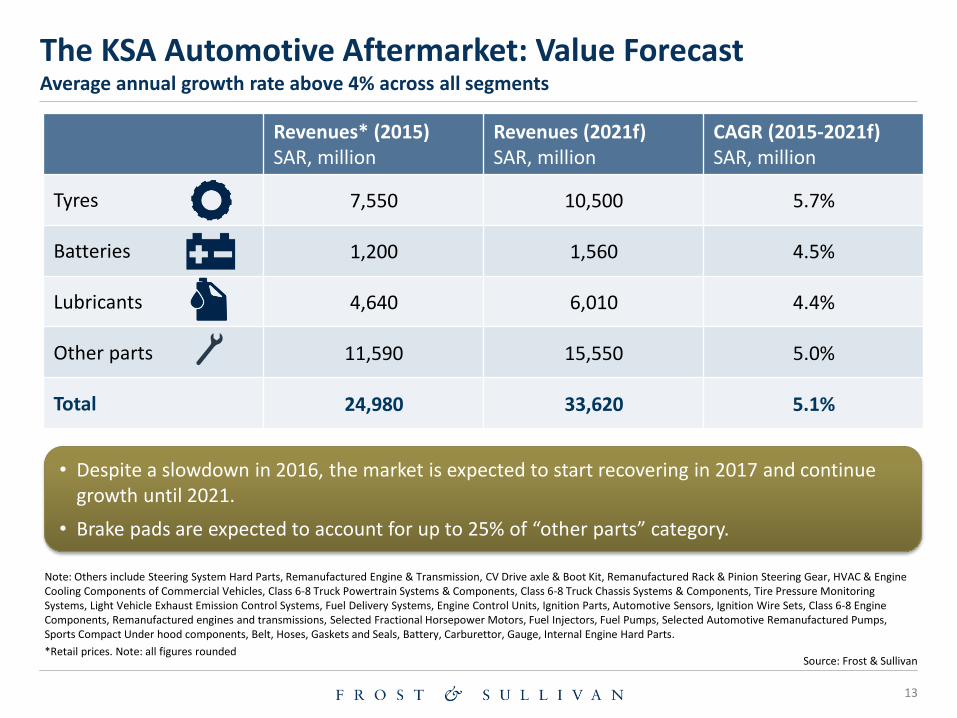

The KSA Automotive Aftermarket: Value Forecast Average annual growth rate above 4% across all segments

Note: Others include Steering System Hard Parts, Remanufactured Engine & Transmission, CV Drive axle & Boot Kit, Remanufactured Rack & Pinion Steering Gear, HVAC & Engine Cooling Components of Commercial Vehicles, Class 6-8 Truck Powertrain Systems & Components, Class 6-8 Truck Chassis Systems & Components, Tire Pressure Monitoring Systems, Light Vehicle Exhaust Emission Control Systems, Fuel Delivery Systems, Engine Control Units, Ignition Parts, Automotive Sensors, Ignition Wire Sets, Class 6-8 Engine Components, Remanufactured engines and transmissions, Selected Fractional Horsepower Motors, Fuel Injectors, Fuel Pumps, Selected Automotive Remanufactured Pumps, Sports Compact Under hood components, Belt, Hoses, Gaskets and Seals, Battery, Carburettor, Gauge, Internal Engine Hard Parts.

*Retail prices. Note: all figures rounded Source: Frost & Sullivan

Revenues* (2015) SAR, million

Revenues (2021f) SAR, million

CAGR (2015-2021f) SAR, million

Tyres 7,550 10,500 5.7%

Batteries 1,200 1,560 4.5%

Lubricants 4,640 6,010 4.4%

Other parts 11,590 15,550 5.0%

Total 24,980 33,620 5.1%

• Despite a slowdown in 2016, the market is expected to start recovering in 2017 and continue growth until 2021.

• Brake pads are expected to account for up to 25% of “other parts” category.

13

Global Trends and Local Perspective

14

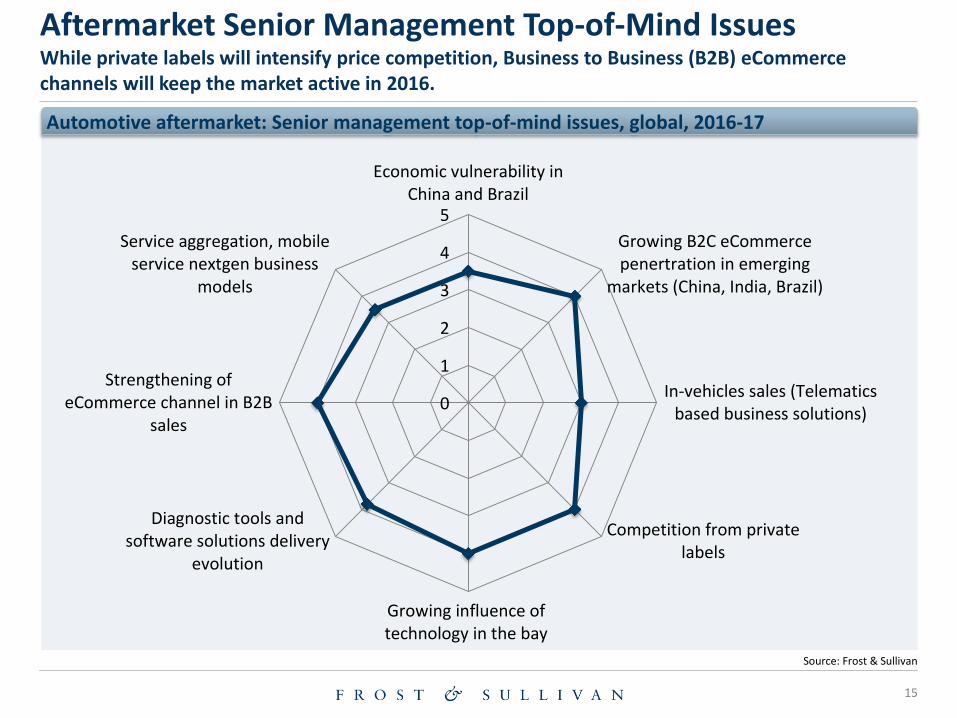

Aftermarket Senior Management Top-of-Mind Issues While private labels will intensify price competition, Business to Business (B2B) eCommerce channels will keep the market active in 2016.

Source: Frost & Sullivan

Automotive aftermarket: Senior management top-of-mind issues, global, 2016-17

0

1

2

3

4

5

Economic vulnerability inChina and Brazil

Growing B2C eCommercepenertration in emerging

markets (China, India, Brazil)

In-vehicles sales (Telematicsbased business solutions)

Competition from privatelabels

Growing influence oftechnology in the bay

Diagnostic tools andsoftware solutions delivery

evolution

Strengthening ofeCommerce channel in B2B

sales

Service aggregation, mobileservice nextgen business

models

15

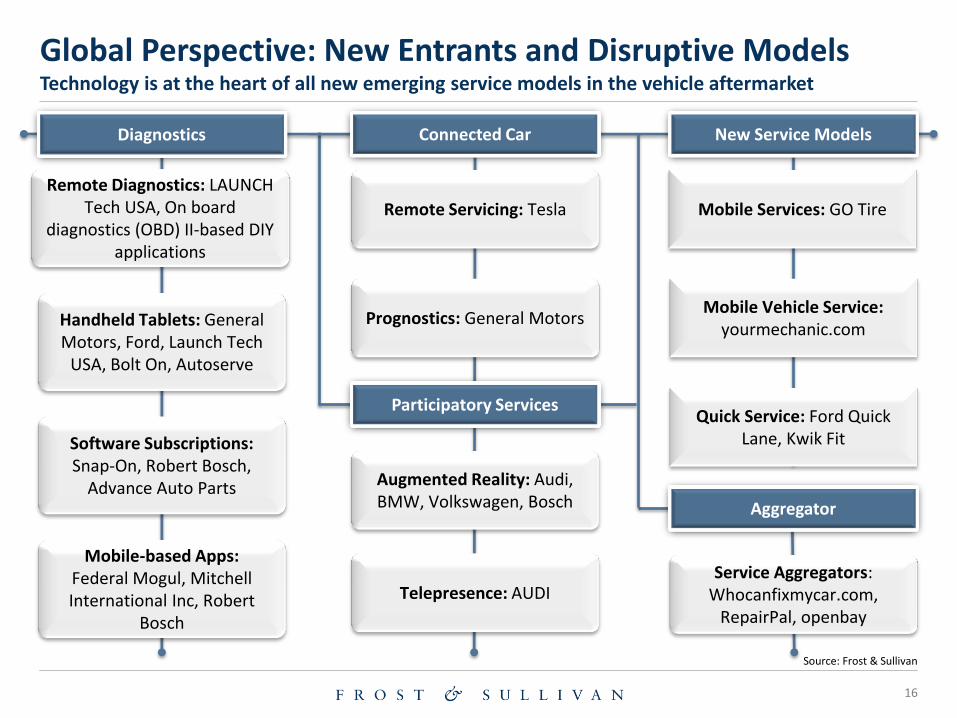

Global Perspective: New Entrants and Disruptive Models Technology is at the heart of all new emerging service models in the vehicle aftermarket

Source: Frost & Sullivan

16

Diagnostics

Remote Diagnostics: LAUNCH Tech USA, On board

diagnostics (OBD) II-based DIY applications

Connected Car

Remote Servicing: Tesla

Prognostics: General Motors

New Service Models

Mobile Services: GO Tire

Mobile Vehicle Service: yourmechanic.com

Quick Service: Ford Quick Lane, Kwik Fit

Aggregator

Handheld Tablets: General Motors, Ford, Launch Tech

USA, Bolt On, Autoserve

Service Aggregators: Whocanfixmycar.com,

RepairPal, openbay

Software Subscriptions: Snap-On, Robert Bosch,

Advance Auto Parts

Participatory Services

Augmented Reality: Audi, BMW, Volkswagen, Bosch

Telepresence: AUDI

Mobile-based Apps: Federal Mogul, Mitchell International Inc, Robert

Bosch

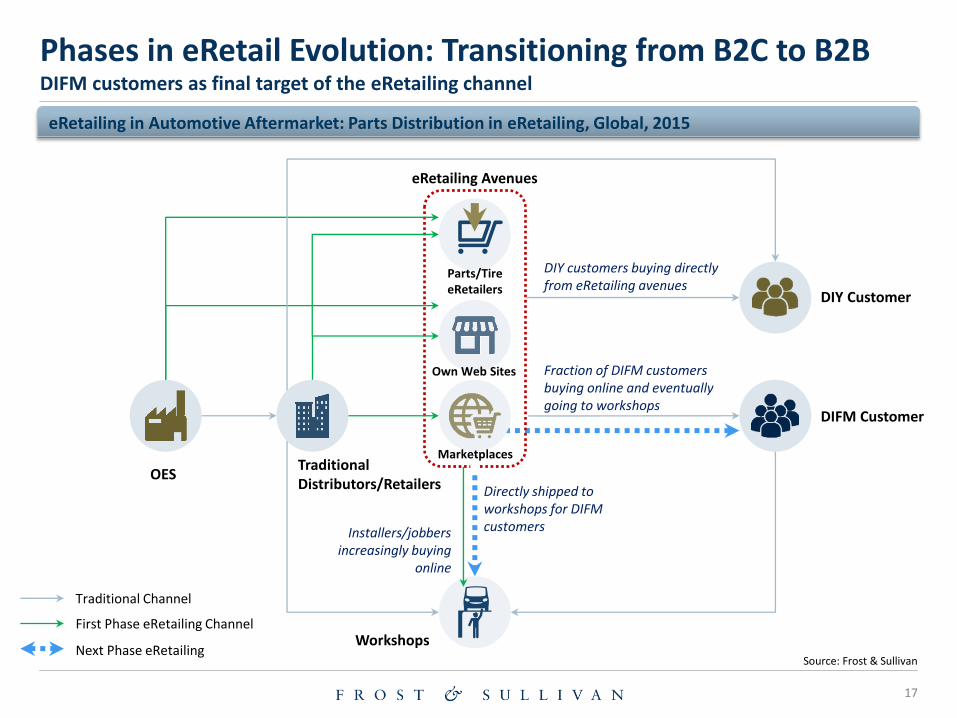

Phases in eRetail Evolution: Transitioning from B2C to B2B DIFM customers as final target of the eRetailing channel

Source: Frost & Sullivan

eRetailing in Automotive Aftermarket: Parts Distribution in eRetailing, Global, 2015

17

OES Traditional Distributors/Retailers

Workshops

Parts/Tire eRetailers

Own Web Sites

DIFM Customer

DIY Customer

Directly shipped to workshops for DIFM customers

DIY customers buying directly from eRetailing avenues

Fraction of DIFM customers buying online and eventually going to workshops

Installers/jobbers increasingly buying

online

eRetailing Avenues

Traditional Channel

First Phase eRetailing Channel

Marketplaces

Next Phase eRetailing

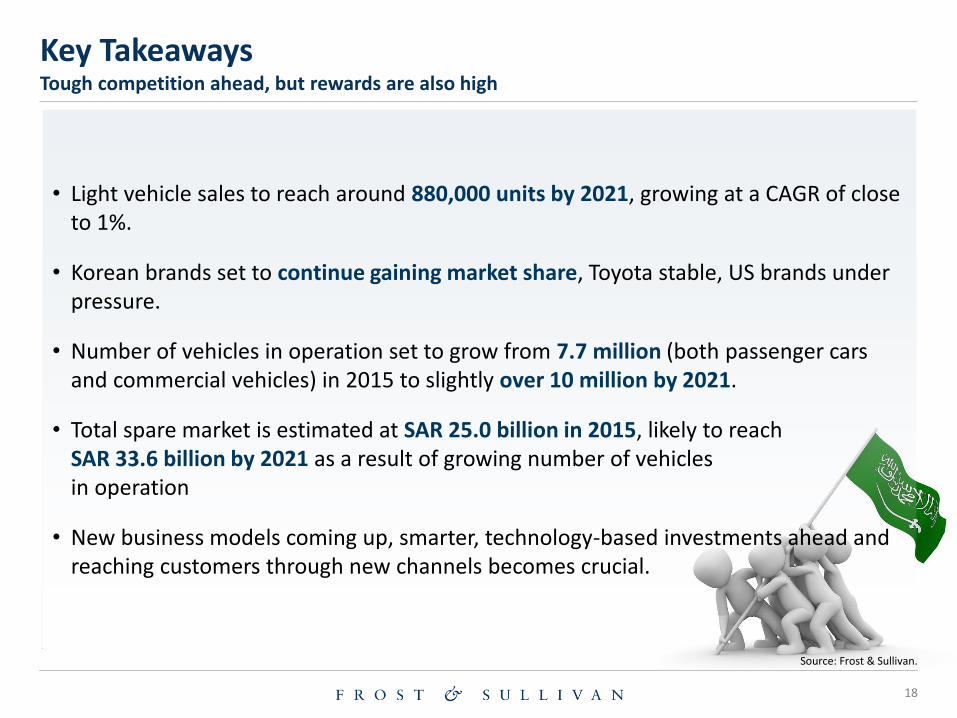

Key Takeaways Tough competition ahead, but rewards are also high

Source: Frost & Sullivan.

• Light vehicle sales to reach around 880,000 units by 2021, growing at a CAGR of close to 1%.

• Korean brands set to continue gaining market share, Toyota stable, US brands under pressure.

• Number of vehicles in operation set to grow from 7.7 million (both passenger cars and commercial vehicles) in 2015 to slightly over 10 million by 2021.

• Total spare market is estimated at SAR 25.0 billion in 2015, likely to reach SAR 33.6 billion by 2021 as a result of growing number of vehicles in operation

• New business models coming up, smarter, technology-based investments ahead and reaching customers through new channels becomes crucial.

18

About Frost & Sullivan

19

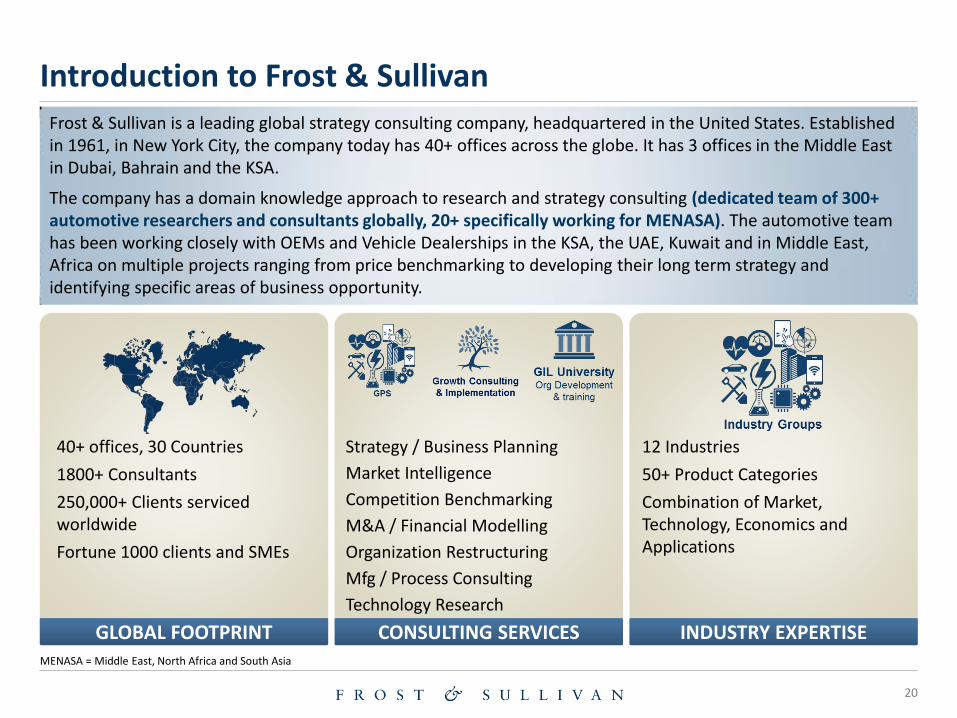

Introduction to Frost & Sullivan

MENASA = Middle East, North Africa and South Asia

Frost & Sullivan is a leading global strategy consulting company, headquartered in the United States. Established in 1961, in New York City, the company today has 40+ offices across the globe. It has 3 offices in the Middle East in Dubai, Bahrain and the KSA.

The company has a domain knowledge approach to research and strategy consulting (dedicated team of 300+ automotive researchers and consultants globally, 20+ specifically working for MENASA). The automotive team has been working closely with OEMs and Vehicle Dealerships in the KSA, the UAE, Kuwait and in Middle East, Africa on multiple projects ranging from price benchmarking to developing their long term strategy and identifying specific areas of business opportunity.

40+ offices, 30 Countries

1800+ Consultants

250,000+ Clients serviced worldwide

Fortune 1000 clients and SMEs

Strategy / Business Planning

Market Intelligence

Competition Benchmarking

M&A / Financial Modelling

Organization Restructuring

Mfg / Process Consulting

Technology Research

12 Industries

50+ Product Categories

Combination of Market, Technology, Economics and Applications

GLOBAL FOOTPRINT CONSULTING SERVICES INDUSTRY EXPERTISE

20

Core Functions

• Growth Strategy

• Geographic Expansion

• Partner Identification

• Mergers and Acquisitions

• Techno Economic Feasibility Studies

• Vendor / Supplier Identification

• Vendor Satisfaction

• Regulatory Analysis

• Technology Assessment

• Product clinic

• Technical Insights

• Market Entry Strategy

• Econometric Analysis

• Dashboard – Market Information

• Dealer Development

• Spare Part Pricing

• Dealer Benchmarking

• Dealer Training

• Usage and Attitude

• Brand Equity

• Cost of Ownership

• Product Clinic

• Customer Satisfaction

• Mobility Tracking

• Manufacturing Excellence

Support functions

CEOs office Vendor Sourcing R&D Technology

Manufacturing Sales and Marketing

Channel Management

Customers

Finance Administration Human

Resources Information Technology

Quality Assurance

Corporate Communication

Legal Compliance

Logistics

Fund Raising Company Due Diligence

Salary Benchmarking Management Systems

Awards Brand Protection

Infrastructure Assessment

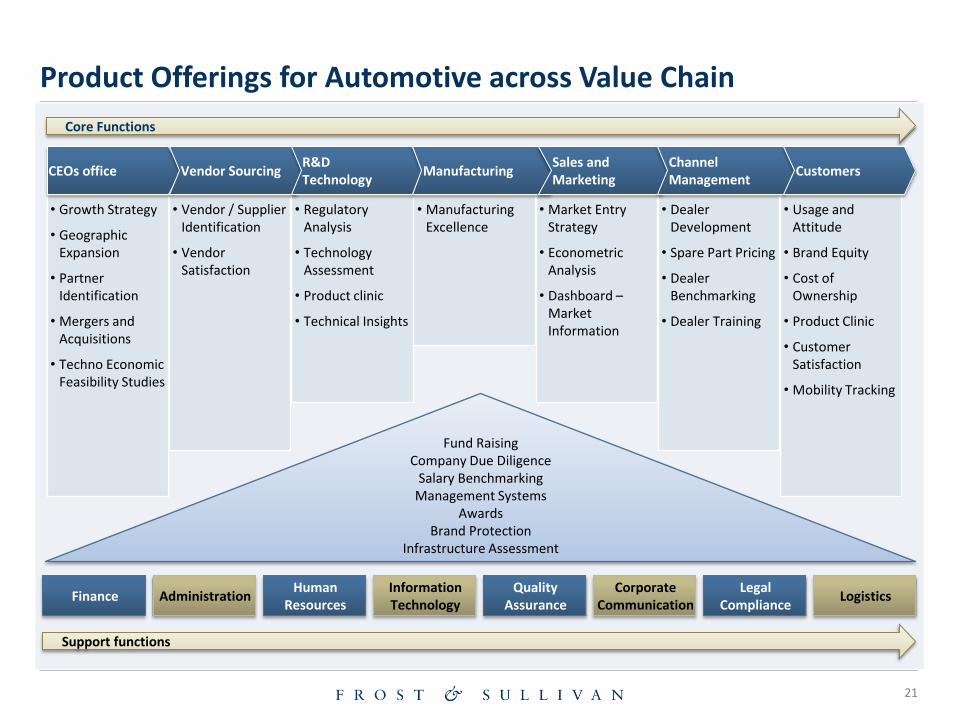

Product Offerings for Automotive across Value Chain

21

Frost & Sullivan’s Automotive Practice offers 6 levels of Consulting and Advisory Services

6 L

eve

ls o

f En

gage

me

nt

Customised Databases and information provide all necessary inputs for Operational Planning

Decision Support Databases

1

Knowledge Centre Reports and Industry Updates on Market and Competition provide Tactical Information Support

Syndicated Research Reports

2

Customised Market Research Projects to Analyse and Evaluate Customer Requirements, Competition Business, Industry Trends and New Growth areas

Customised Market Research

3

Long term Engagements on Identifying Growth Options, Market Entry Strategy, Business Portfolio Assessment and Consulting Projects 4

Working on Inorganic Growth: Mergers and Acquisitions, Joint Ventures, Partner Identification to Due Diligence, Structuring and Post Deal Integration

Partner Identification and Research

5

Strategy Workshops with Boards and Senior Teams on Business and Strategic Planning, Growth Roadmaps, Solving Critical Business Issues

Strategy Workshops and Advisory

6

Support Advisory Services

Supply Chain Engineering Financial Advisory Manufacturing Advisory

1. Operational Improvement 2. Growth 3. Shareholder Value

Key Organisational Challenges

22

Disclaimer and Copyright Notice

This White Paper prepared by Frost & Sullivan is based on analysis of primary, secondary information and knowledge available in the public domain. While Frost & Sullivan has made all efforts to check the validity of the information presented, it is not liable for errors in information whose accuracy cannot be guaranteed by Frost & Sullivan. Information herein should be used more as indicators and trends rather than representation of factual information. The White Paper is intended to set the tone of discussions at the conference in which it was presented. It contains forward-looking statements, particularly those concerning growth, consumption, policy support for water supply. Forward looking statements involve risks and uncertainties because they relate to events, and depend on circumstances, that will or may occur in the future. Actual results may differ depending on a variety of factors, including product supply, demand and pricing; political stability; general economic conditions; legal and regulatory developments; availability of new technologies; natural disasters and adverse weather conditions and hence should not be construed to be facts.

The contents of these pages are copyright © Frost & Sullivan. All rights reserved. Except with the prior written permission of Frost & Sullivan, you may not (whether directly or indirectly) create a database in an electronic or other form by downloading and storing all or any part of the content of this document. No part of this document may be copied or otherwise incorporated into, transmitted to, or stored in any other website, electronic retrieval system, publication or other work in any form (whether hard copy, electronic or otherwise) without the prior written permission of Frost & Sullivan.

Disclaimer

Copyright notice

23

State your need, we would be happy to serve you…

Contact

Vitali Bielski Senior Consultant– MENA, Automotive Practice

E-mail : [email protected]

Bahrain Mobile : +973-344-27416

Landline : +973-17387666

Frost & Sullivan Consulting Bahrain WLL Unit 121 & 122, 9th Floor, Unisono Tower, Building 614, Road 1011, Block 410, Sanabis, PO Box 65172, Kingdom of Bahrain

Contact

E-mail : [email protected]

UAE Mobile : +971-56-7686450

Frost & Sullivan International Inc. 22601, Swiss Tower, Cluster Y, Jumeirah Lake Towers, P O Box 33372 Dubai, United Arab Emirates

Subhash Joshi Regional Head – MENA, Automotive Practice

Contact Information

24