Embed Size (px)

Citation preview

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 1 Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 1

Overview Category Management &

Shopper Marketing

Germany

Perspectives of a common journey with

retailers and shoppers

Moscow, 25th October 2011

Markus Hoffmann

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 3 27.10.2011 | 3

Shopper Marketing: a brand new topic ! - ?

Originally Category Management and Shopper Marketing is what the

Mom&Pop stores still knew. Do you know why ?

Mom knew her clients personally. We do NOT.

She knew their wishes and needs.

We do NOT.

She took them very serious.

We do - ?

…and she did her best to satisfy them

We - ??

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 4 27.10.2011 | 4

• During the last 40 years the shops have been growing constantly in two aspects :

1) Single retailers suddenly turned up with many stores.

2) The stores themselves increased and suddenly got many shoppers.

• The single shopper and his needs were no longer such important – main topic was the

multitude.

• The shopper had to accept what he was offered by the retailers and manufacturers.

• The shopper became anonymous.

• Mom vanished – and together with her unfortunately the origin of category

management and shopper marketing.

Shopper Marketing in former times –

and nowadays

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 5 27.10.2011 | 5

• In about 1989 Mom and her principles were

"recovered", mainly in the United states, and

later on also in Europe.

• Her name was now„Category Management“,

her main principle

Efficient Consumer Response

• Retailers and manufacturers got aware of the fact that it is worth

caring for the shopper – for his wishes and needs.

• Shopper marketing was born again

Shopper Marketing in former times –

and nowadays

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 6 27.10.2011 | 6

Milestones during the development of

Category Management

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 7 27.10.2011 | 7

• The driver of the total FMCG-Business is the Shopper. For this, we are

dealing not only with Category Managment but with Shopper Marketing

• The Shopper is in the center of all our efforts, analysis, decisions and

messages to the retailer. In all we do HE must be in our focus.

• We want to understand the complete FMCG-Business for a better

understanding of all categories – and to be able to help the retailer with our

categories and our brands

• Many shoppers, many shopping trips and a high purchase frequency is the

common target of both retailers and FERRERO

Ferrero Category Management and Shopper

Marketing

Our main principles

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 8 27.10.2011 | 8

Learning more about the

shopper

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 9 27.10.2011 | 9

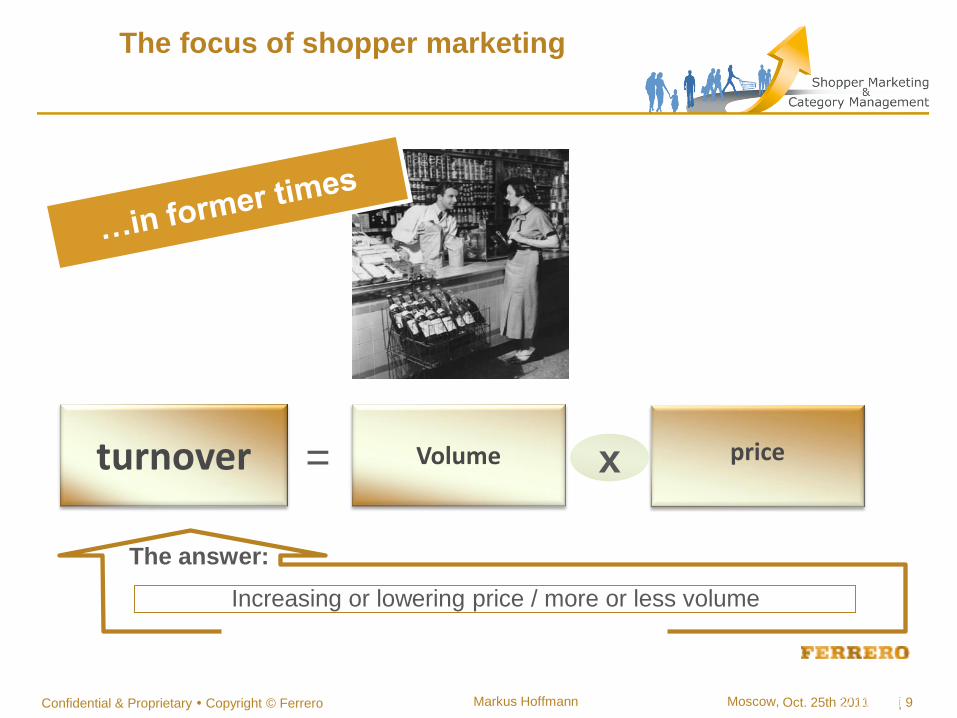

turnover = Volume price x

The focus of shopper marketing

Increasing or lowering price / more or less volume

The answer:

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 10 27.10.2011 | 10

FMCG- turnover =

More or less clients – more or less purchase frequency – small or big basket / valuable shopper

The changed focus within Shopper

Marketing…

shopper Purchase frequency x

Value FMCG- basket

x

…is based on the shoppers and their behaviour

The answer:

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 11 Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 11

Is the shopper focus really such

important ?

• Soaring usage of the expression “Shopper Marketing” in both

science and business community over the last 3 to 5 years

• Explosion of number of congresses, seminars etc. dealing

with “Shopper Marketing” e. g.:

ECR Europe conference Brussels 2011: The consumer and

shopper journey

• GS1 initiative: Launch of a workgroup with representatives of

biggest FMCG companies and retailers in Germany to define

„Shopper Marketing“

• New basic studies about “Shopper Marketing” conducted

recently by Market Research/Consulting companies (e.g. Frey,

plan+impulse,…)

Observations during the last years:

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 12 Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 12

Actual study about the current status of “Shopper

Marketing” in Germany

Quelle: Survey Shopper Marketing / plan + impuls 2011

• Objective: Assess understanding of Shopper Marketing in GER

• Design: Online survey (N = 193) suppliers (157) retailers (36)

• Field phase: March 2011

• Publication: July 2011

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 14 Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 14

1

6

33

61

6 5

47 47

0

10

20

30

40

50

60

70

No, never heard of it Heard of it, but don't knowwhat it means

Yes. I have a rough ideaof what it probably means

Yes, I know exactly what itmeans

58 % 36 % 2 % 5 %

Total Manufacturers Retailers

(n=193) (n=157) (n=36)

42% of respondents have no

or only a rough idea about

the meaning of „Shopper

Marketing“

Does the term “Shopper Marketing” mean anything to you?

More than half of respondents (58%) stated, they knew exactly what was meant by the phrase Shopper Marketing; another 36% had a rough idea of what was meant.

Quelle: Survey Shopper Marketing / plan + impuls 2011

The phrase „Shopper Marketing“ is well known by

German manufactures and retailers

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 15 Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 15

“To know the needs shoppers have while shopping”

“Increasing knowledge about shoppers (behaviors, decision making and search patterns)”

Focus: Understanding

Shoppers (43%)

For me it’s a question of really understanding consumers”

Quelle: Survey Shopper Marketing / plan + impuls 2011 / Original quotations

However, understanding of the exact meaning

of Shopper Marketing differs broadly

“Actions based on analysis of shopper behaviors”

Why and when does a customer purchase a product in a store?”

“It focuses on the entire shopping process, from the first idea to buy a product to the moment when the product is picked up off the shelf”

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 16 Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 16

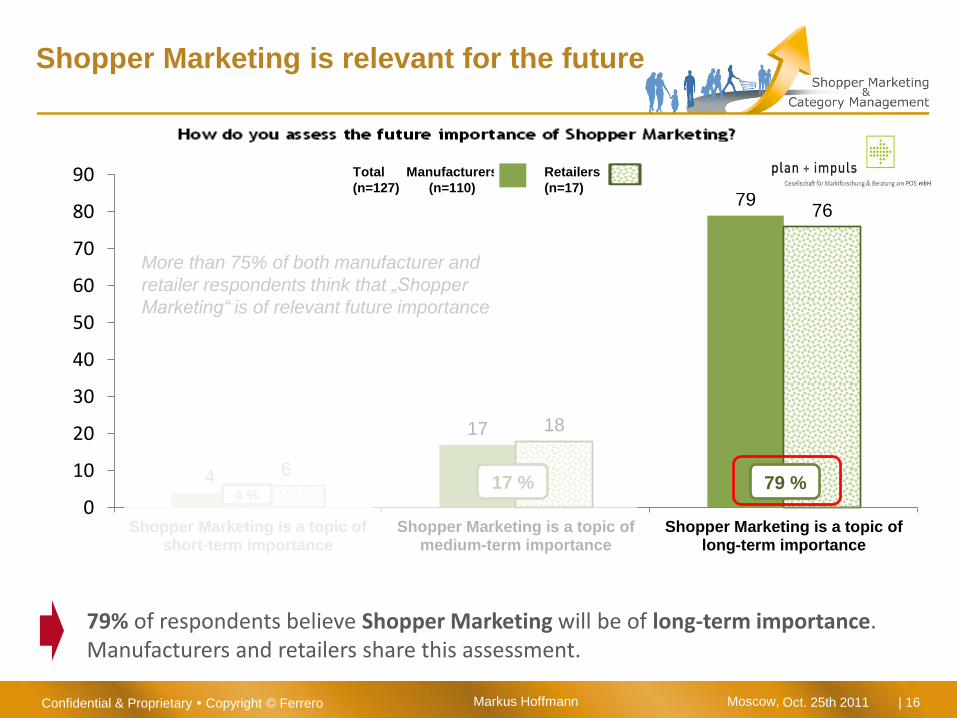

Shopper Marketing is relevant for the future

79% of respondents believe Shopper Marketing will be of long-term importance. Manufacturers and retailers share this assessment.

4

17

79

6

18

76

0

10

20

30

40

50

60

70

80

90

Shopper Marketing is a topic ofshort-term importance

Shopper Marketing is a topic ofmedium-term importance

Shopper Marketing is a topic oflong-term importance

79 % 17 % 4 %

Total Manufacturers Retailers

(n=127) (n=110) (n=17)

More than 75% of both manufacturer and

retailer respondents think that „Shopper

Marketing“ is of relevant future importance

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 18 Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 18

Which company is the pioneer in the area of

Shopper Marketing in Germany ?

With regard to being a pioneer in shopper marketing, Ferrero was most frequently cited by both manufacturers (25%) and retailers (16%).

74

5

5

16

45

1

1

1

1

1

1

5

5

15

25

0 10 20 30 40 50 60 70 80

Don't know

Maggi

Henkel

Danone

Colgate Palmolive

Coca Cola

Avery Dennison

Unilever

Nestlé

Procter & Gamble

FERRERO

1 %

1 %

1 %

1 %

1 %

1 %

50 %

5 %

5 %

14 %

23 %

Quelle: Survey Shopper Marketing / plan + impuls 2011

Total Manufacturers Retailers

(n=129) (n=110) (n=19)

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 20 27.10.2011 | 20

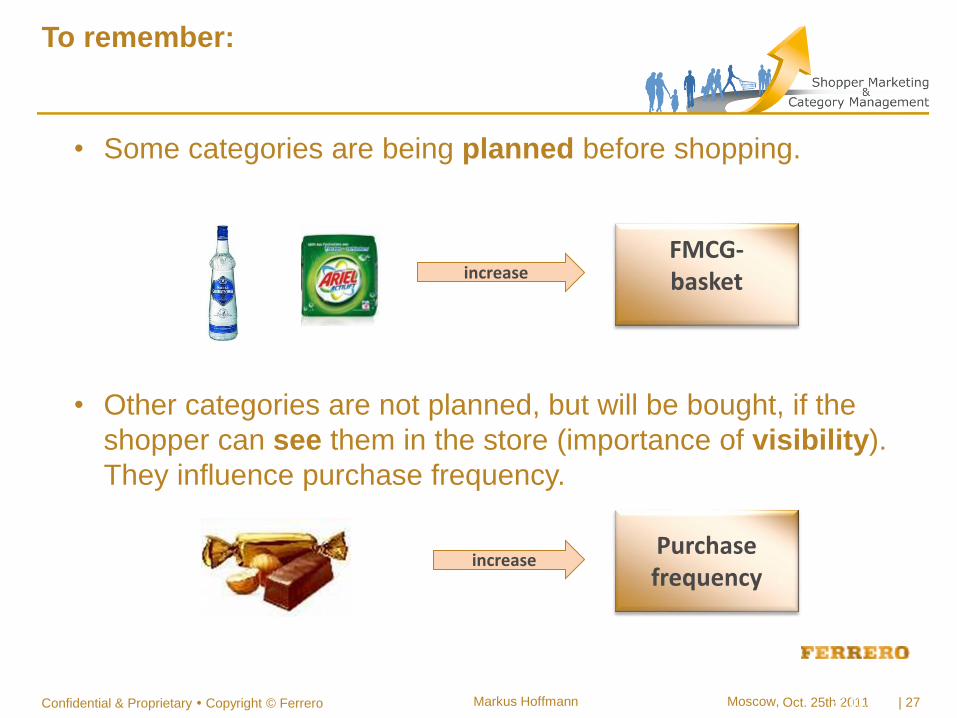

• Some categories are being planned before shopping.

Several of their products will increase the value of the FMCG

basket

FMCG- basket

increase

FMCG- turnover = shopper

Purchase frequency x

FMCG- basket

x

Back to the Shopper facts – what can we

learn about them, and how to use them ?

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 21 27.10.2011 | 21

Learning more about the Shopper facts and

their influence on categories

• Other categories are not planned, but will be bought, if the

shopper can see them in the store (importance of visibility).

They influence purchase frequency.

• Confectionery is one of the categories which is typical for

this phenomenon

Purchase frequency

increase

FMCG- turnover = shopper

Purchase frequency x

FMCG- basket

x

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 22 Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 22

FMCG- turnover = shopper

Purchase frequency x

FMCG- basket

x

1. Products with many

shoppers

2. Products with high

purchase frequency

Shopper traffic ( number of checkout

receipts)

=

What is Shoppertraffic ?

So - what generates Shoppertraffic ?

Learning more about the Shopper facts and

their influence on categories

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 23 Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 23

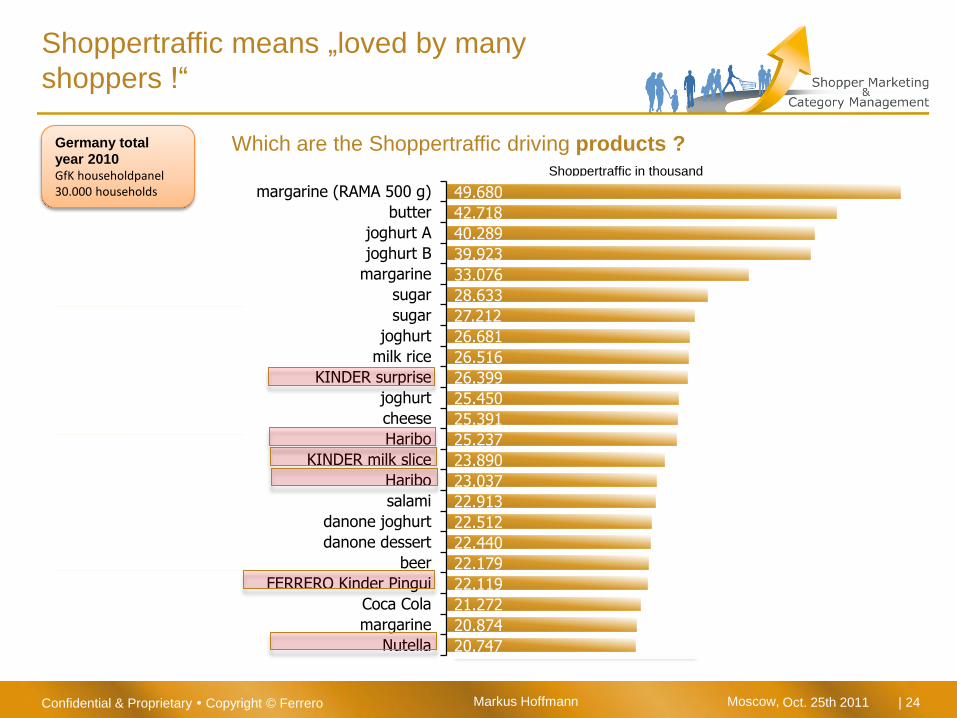

Shoppertraffic means „loved by many

shoppers !“

Which are the Shoppertraffic driving categories ?

59.583

427.823

493.603

601.884

623.880

702.462

816.048

826.501

957.660

1.042.121

1.429.691

1.677.645

2.094.992

2.345.343

2.347.173

2.681.679

2.810.478

3.260.580

baby food

pet food & articles

other Near Food

Wasch-Putz-Reinigs.mittel

tissues & other stationeries

fresh food rest (eggs, fish)

Beauty-Home-Care

alcoholic drinks

hot beverages

frozen food / ice cream

non alcoholic drinks

cheese

confectionery

bread

dairy food

meat/sausages/poultry

fruit and vegetables

FOOD generic

Shoppertraffic in thousand

Germany total year 2010 GfK householdpanel 30.000 households

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 24 Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 24

Which are the Shoppertraffic driving products ?

Shoppertraffic means „loved by many

shoppers !“

FERRERO KINDER PINGUI STD.240 GR

OETTINGEROETTINGER500 ML

DANONE DANY SAHNE460 GR

DANONE ACTIVIA CLASSIC FJ460 GR

WILTMANN SALAMI80 GR

HARIBO COLOR RADO300 GR

FERRERO MILCHSCHNITTE 280 GR

HARIBO GOLDBAEREN300 GR

GERAMONT REST FR WK200 GR

MUELLER MDE SCHLEMMER FJ150 GR

KINDER UEBERRASCHUNG 20 GR

MUELLER MILCHREIS ORIGINAL200 GR

MUELLER FROOP FJ150 GR

Zucker DIAMANTDIAMANT1000 GR

SUEDZUCKER1000 GR

LAETTA500 GR

MUELLER Mit Der Ecke KNUSPER FJ150 GR

EHRMANN ALMIGHURT FJ150 GR

KERRYGOLD ORIG. IRISCHE BUTTER250 GR

RAMA STANDARD500 GR

COCA-COLA REGULAR1000 ML

RAMA CREMEFINE ZUM KOCHEN250 ML

FERRERO NUTELLA400 GR

Shoppertraffic in thousand

49.680

42.718

40.289

39.923

33.076

28.633

27.212

26.681

26.516

26.399

25.450

25.391

25.237

23.890

23.037

22.913

22.512

22.440

22.179

22.119

21.272

20.874

20.747

margarine (RAMA 500 g)

butter

joghurt A

joghurt B

margarine

sugar

sugar

joghurt

milk rice

KINDER surprise

joghurt

cheese

Haribo

KINDER milk slice

Haribo

salami

danone joghurt

danone dessert

beer

FERRERO Kinder Pingui

Coca Cola

margarine

Nutella

Germany total year 2010 GfK householdpanel 30.000 households

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 25 Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 25 Quelle: GAT; GfK CS 30.000, CY 2010

Shoppertraffic is the initial point of all our

analyses, activities and strategies

1. brands which have a lot of fans, are important brands

2. Most of our FERRERO brands are ranked among them

3. Each retailer who focuses on the shopper will do his best to take

HIS wishes and needs into aspect

4. To understand better what this implies for us and the retailers, we are

working hard.

And we share our knowledge with the retailers.

What we have learned:

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 26 27.10.2011 | 26

More buyers

assortment

Placement/

visibility

Media & price

assortment-

management

Leaflet-

management

Visibility &

placement

management

Purchase frequency

The category management Marketing MIX

targets

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 27 27.10.2011 | 27

To remember:

• Other categories are not planned, but will be bought, if the

shopper can see them in the store (importance of visibility).

They influence purchase frequency.

Purchase frequency

increase

• Some categories are being planned before shopping.

FMCG- basket

increase

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 28 27.10.2011 | 28

Where to place which

categories

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 29 Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 29

Placement of impulse categories

?

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 30 Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 30

Visibility Management

Strategic focus: Off Shelf Placement

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 31 27.10.2011 | 31

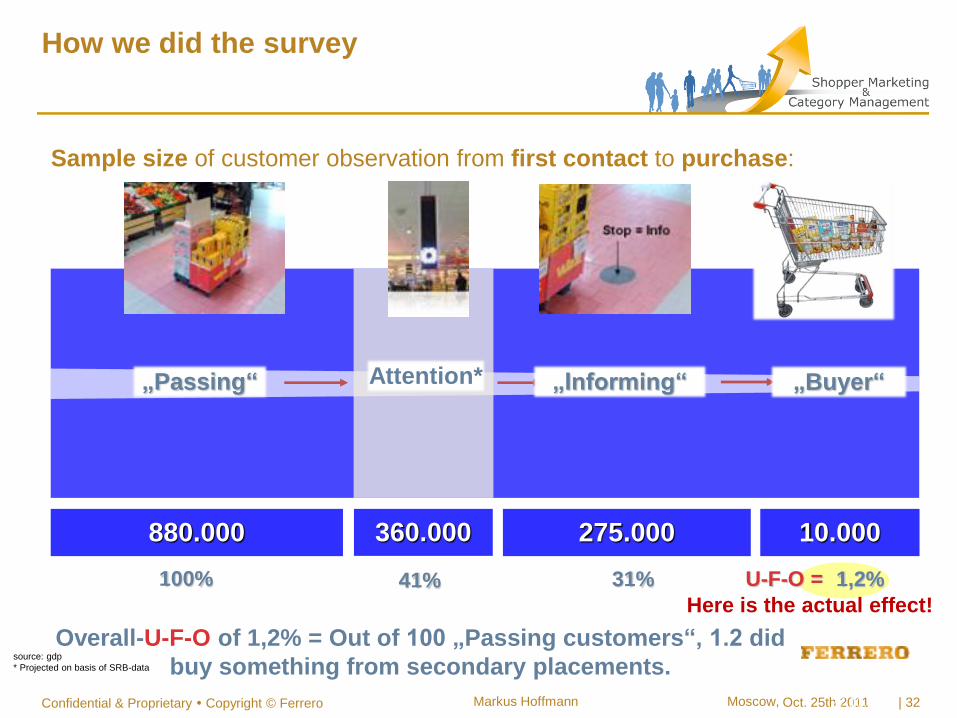

• After this, more than 60 different products from different categories have been analized

sample

The survey: 880,000 customer contacts

were evaluated within a period of 16 weeks

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 32 27.10.2011 | 32

100%

880.000

Sample size of customer observation from first contact to purchase:

source: gdp

* Projected on basis of SRB-data

„Passing“ „Buyer“

Here is the actual effect!

U-F-O =

Overall-U-F-O of 1,2% = Out of 100 „Passing customers“, 1.2 did

buy something from secondary placements.

Attention* „Informing“

How we did the survey

360.000

41%

275.000

31%

10.000

1,2%

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 33 27.10.2011 | 33

0,30,3

0,6

0,8

1,11,11,21,2

1,3

1,51,5

2,2

Feinko

st

Alkoh

ol

Bio

+Kons

erve

rn

Milc

hdrin

ksAFG

Kon

serv

en

Fertigg

ericht

e

Sal

zgebä

ck

Get

ränk

e*

Näh

rmitt

el

Frühs

tück

Süß

ware

n**

Result: Confectionary is no.1 converter of frequency

source: gdp, manual census by market and week and Shopperbox Data

Reading example: Per 100 „Passing customers“, 2.2 bought products out of

secondary placement concerning confectionary.

per 100 „passing customers“ did buy in secondary placement without advertising and without reduction in price…

Ø 1,2

* Beverages = averages of 2 special placement, ** confectionary = averages of 3 special placements

Confectionary**

Breakfast Processed

Food

Drinks* Salty snacks

Instant meals

Cans Non alcoholic

beverages

Milk drinks Bio Alcohol Delica-

tessen

Category overview based on conversion of

frequency

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 34 27.10.2011 | 34

153

142

104 98

94 88

74

60

38 35 29

21

High frequency

Ø 81

Result: Confectionary benefits from higher frequency

Sales [pieces] per market and week

In high frequency zones, 153 articles per week and market were sold from

second placement confectionary. Breakfast without Nutella is only 45 pieces on

average.

Confect- ionary**

Breakfast Nutri- ments

Drinks* Salty snacks

Instant meals

Cans Non-alcoholi

beverages

Milk drinks Bio Alcohol Delicatessen

45

Breakfast w/o Nutella

Placement on the right place Which category benefits most from higher

frequency ?

source: gdp, manual census by market and week and Shopperbox Data

* Beverages = averages of 2 special placement, ** confectionary = averages of 3 special placements

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 35 27.10.2011 | 35

Pictures of best practice

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 36 Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 36

Example from Supermarket

Clear shelf structure:

Anchor brand conception at the POS

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 37 Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 37

EXAMPLE:

„Genusswelt“ in the 1st third of the market

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 38 Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 38

EXAMPLE:

„Genusswelt“ in a very special presentation

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 39 Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 39

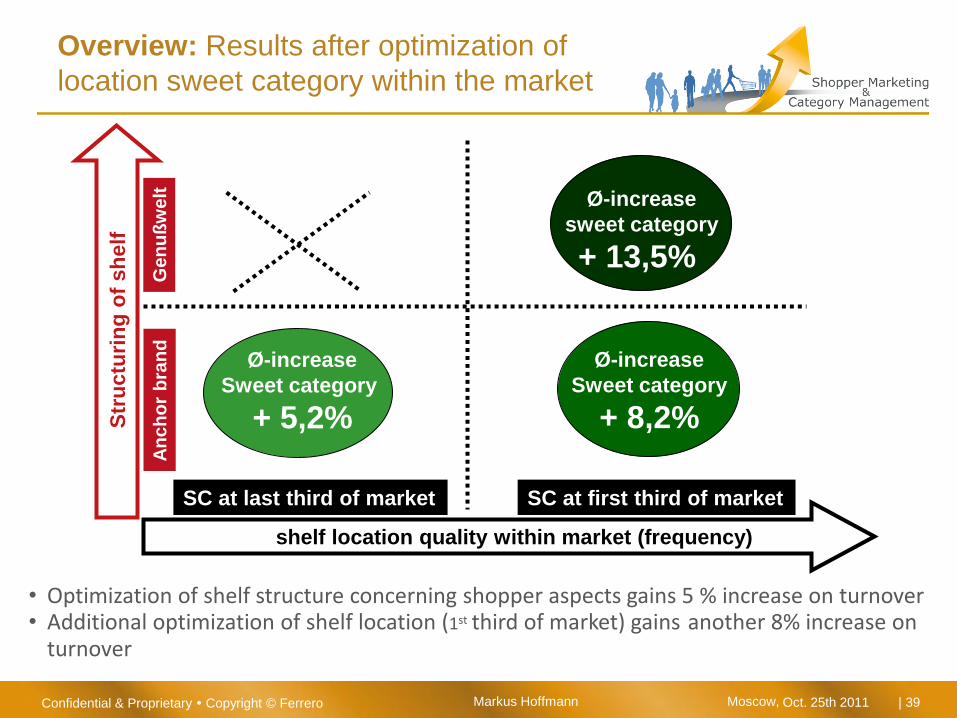

shelf location quality within market (frequency)

Str

uc

turi

ng

of

sh

elf

SC at last third of market

An

ch

or

bra

nd

G

en

uß

we

lt

SC at first third of market

Ø-increase

sweet category

+ 13,5%

Ø-increase

Sweet category

+ 8,2%

Ø-increase

Sweet category

+ 5,2%

Overview: Results after optimization of

location sweet category within the market

• Optimization of shelf structure concerning shopper aspects gains 5 % increase on turnover • Additional optimization of shelf location (1st third of market) gains another 8% increase on

turnover

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 40 Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 40

+

Shoppertraffic is the initial point of all our

analyses, activities and strategies

1. brands which have a lot of fans, are important brands

2. Categories and products with a high impact on impulse have to be

placed in high-frequent zones

3. Categories and products with a high impact on impulse have to be

placed in the first 3rd of the market, since:

4. They have high conversion rates from frequency into output

5. In the end the whole category is winning.

What we learned:

Win for

retailer Win for

customer + Win for

manufacturer

Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 41 Markus Hoffmann Moscow, Confidential & Proprietary Copyright © Ferrero Oct. 25th 2011 | 41

Thank you !