Embed Size (px)

DESCRIPTION

Overcapacity in the steel industry

Citation preview

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

Steel Industry Responses to

Overcapacity

OECD Steel Committee

June 5, 2014

By Philip Tomlinson

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

0

200

400

600

800

1000

1200

1400

1600

1800

1951 1956 1961 1966 1971 1976 1981 1986 1991 1996 2001 2006 2011

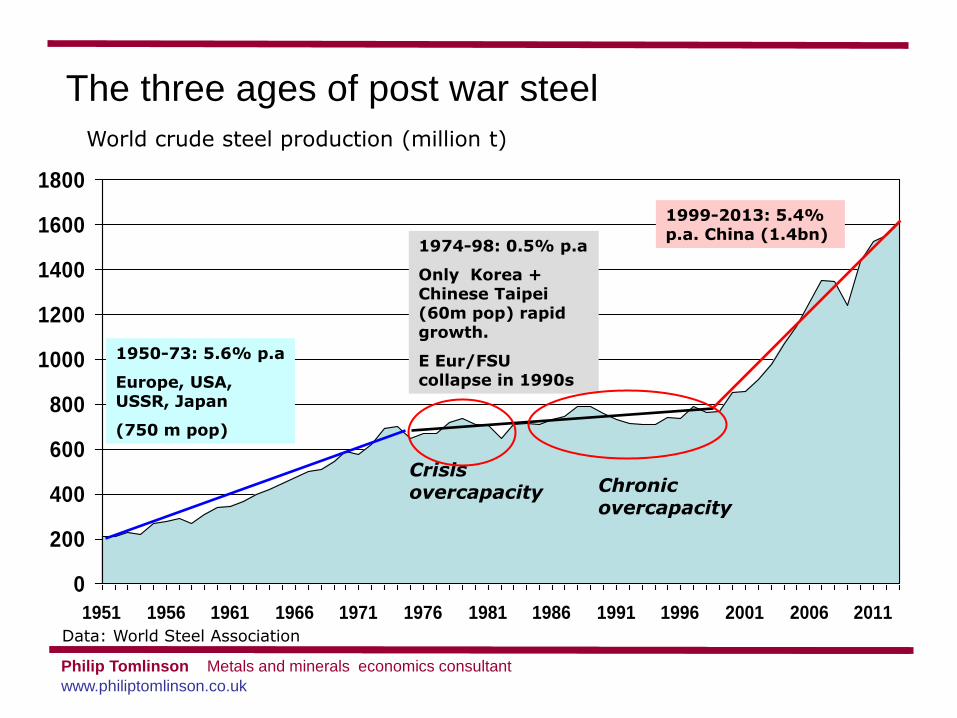

World crude steel production (million t)

Data: World Steel Association

The three ages of post war steel

1950-73: 5.6% p.a

Europe, USA, USSR, Japan

(750 m pop)

1974-98: 0.5% p.a

Only Korea + Chinese Taipei (60m pop) rapid growth.

E Eur/FSU collapse in 1990s

1999-2013: 5.4% p.a. China (1.4bn)

Crisis overcapacity

Chronic overcapacity

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

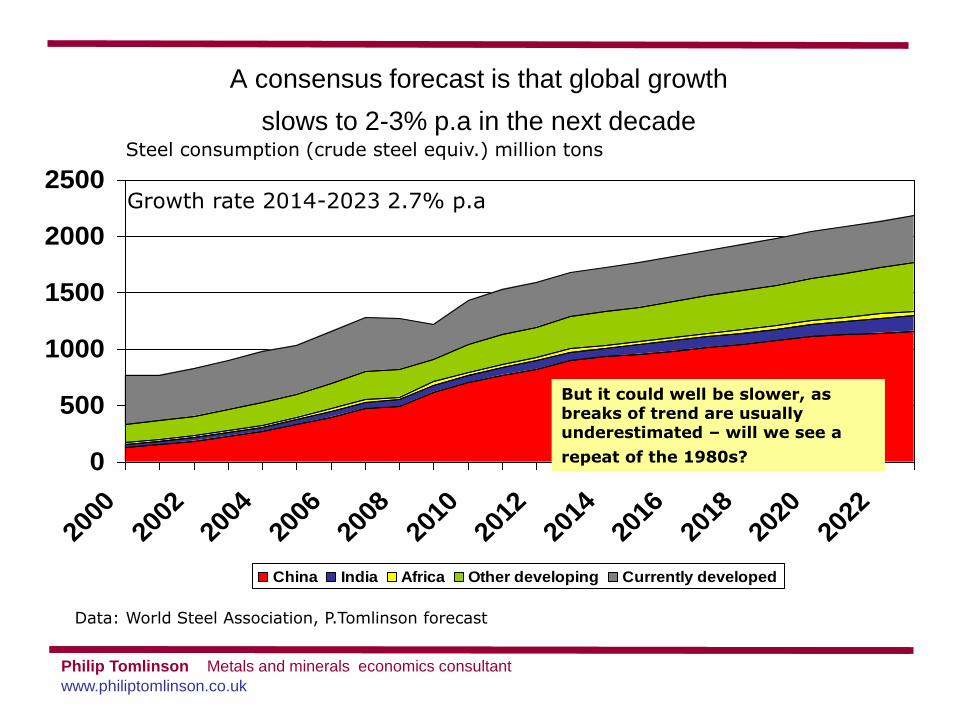

A consensus forecast is that global growth

slows to 2-3% p.a in the next decade

0

500

1000

1500

2000

2500

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

China India Africa Other developing Currently developed

Growth rate 2014-2023 2.7% p.a

Steel consumption (crude steel equiv.) million tons

Data: World Steel Association, P.Tomlinson forecast

But it could well be slower, as breaks of trend are usually underestimated – will we see a

repeat of the 1980s?

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

-2

0

2

4

6

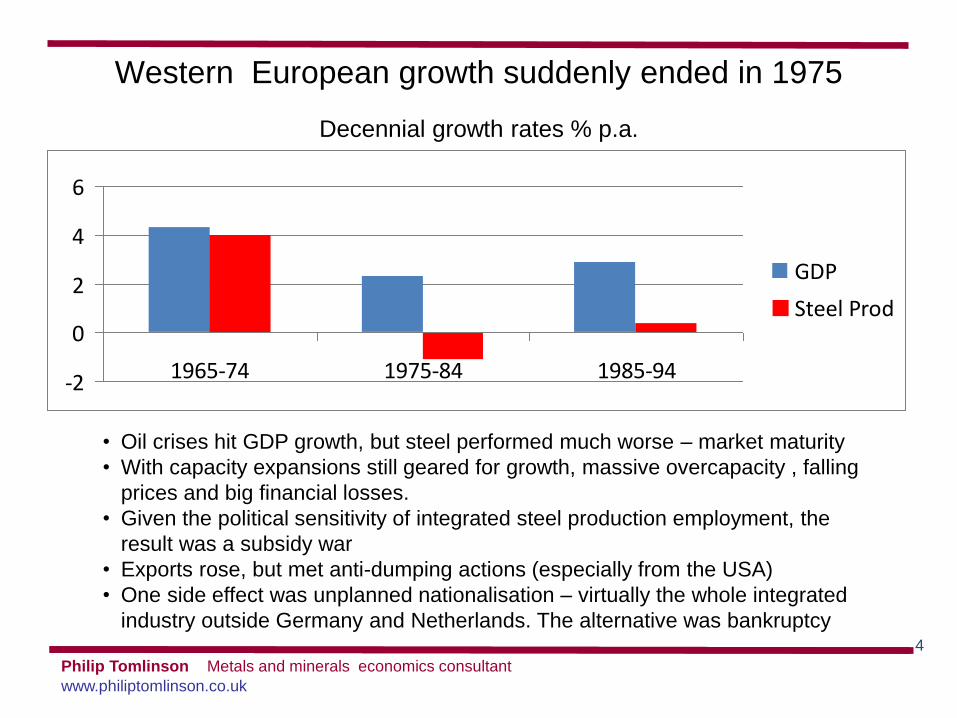

1965-74 1975-84 1985-94

GDP

Steel Prod

4

Western European growth suddenly ended in 1975

Decennial growth rates % p.a.

• Oil crises hit GDP growth, but steel performed much worse – market maturity

• With capacity expansions still geared for growth, massive overcapacity , falling

prices and big financial losses.

• Given the political sensitivity of integrated steel production employment, the

result was a subsidy war

• Exports rose, but met anti-dumping actions (especially from the USA)

• One side effect was unplanned nationalisation – virtually the whole integrated

industry outside Germany and Netherlands. The alternative was bankruptcy

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

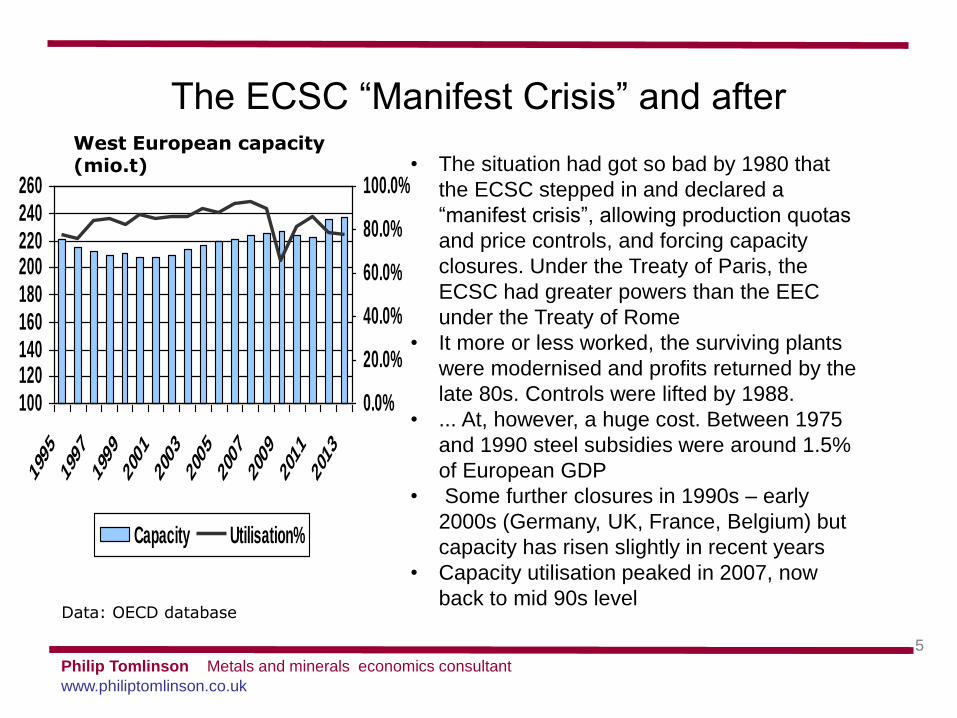

The ECSC “Manifest Crisis” and after

5

• The situation had got so bad by 1980 that

the ECSC stepped in and declared a

“manifest crisis”, allowing production quotas

and price controls, and forcing capacity

closures. Under the Treaty of Paris, the

ECSC had greater powers than the EEC

under the Treaty of Rome

• It more or less worked, the surviving plants

were modernised and profits returned by the

late 80s. Controls were lifted by 1988.

• ... At, however, a huge cost. Between 1975

and 1990 steel subsidies were around 1.5%

of European GDP

• Some further closures in 1990s – early

2000s (Germany, UK, France, Belgium) but

capacity has risen slightly in recent years

• Capacity utilisation peaked in 2007, now

back to mid 90s level

100120140160180200220240260

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Capacity Utilisation%

West European capacity (mio.t)

Data: OECD database

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

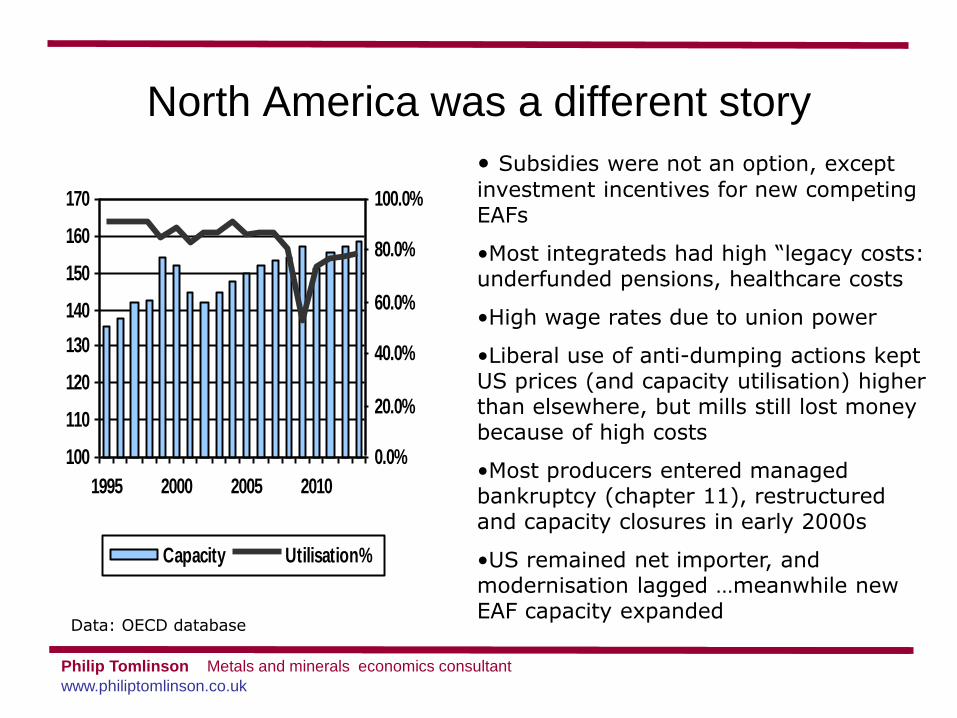

North America was a different story

100

110

120

130

140

150

160

170

1995 2000 2005 2010

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Capacity Utilisation%

• Subsidies were not an option, except

investment incentives for new competing EAFs

•Most integrateds had high “legacy costs: underfunded pensions, healthcare costs

•High wage rates due to union power

•Liberal use of anti-dumping actions kept US prices (and capacity utilisation) higher than elsewhere, but mills still lost money because of high costs

•Most producers entered managed bankruptcy (chapter 11), restructured and capacity closures in early 2000s

•US remained net importer, and modernisation lagged …meanwhile new EAF capacity expanded

Data: OECD database

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

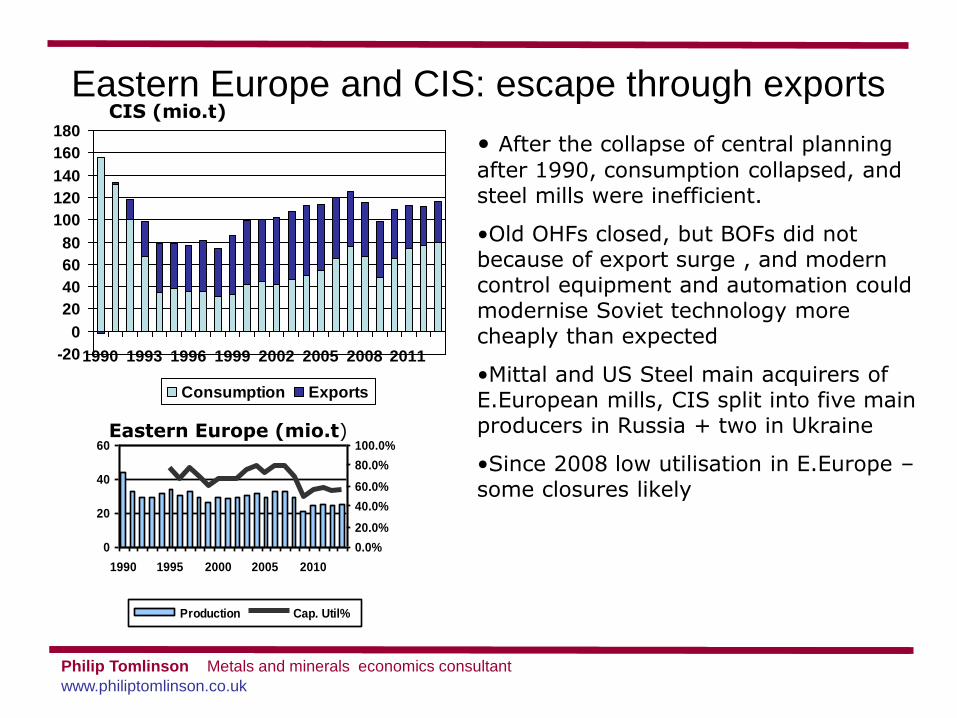

Eastern Europe and CIS: escape through exports

0

20

40

60

1990 1995 2000 2005 2010

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Production Cap. Util%

• After the collapse of central planning

after 1990, consumption collapsed, and steel mills were inefficient.

•Old OHFs closed, but BOFs did not because of export surge , and modern control equipment and automation could modernise Soviet technology more cheaply than expected

•Mittal and US Steel main acquirers of E.European mills, CIS split into five main producers in Russia + two in Ukraine

•Since 2008 low utilisation in E.Europe – some closures likely

Eastern Europe (mio.t)

-20

0

20

40

60

80

100

120

140

160

180

1990 1993 1996 1999 2002 2005 2008 2011

Consumption Exports

CIS (mio.t)

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

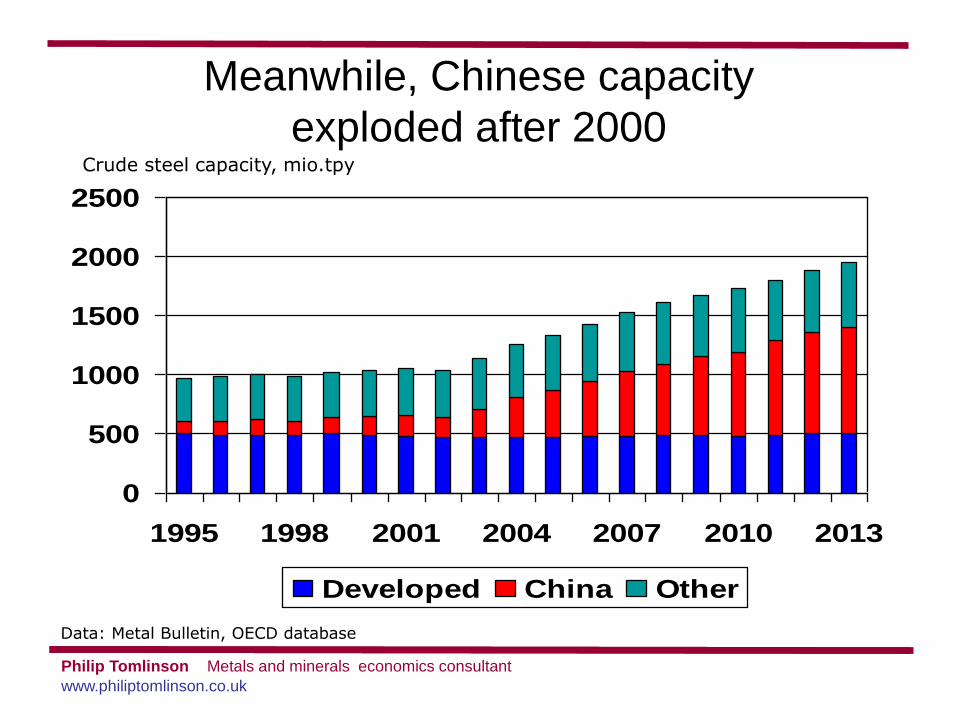

Meanwhile, Chinese capacity

exploded after 2000

0

500

1000

1500

2000

2500

1995 1998 2001 2004 2007 2010 2013

Developed China Other

Data: Metal Bulletin, OECD database

Crude steel capacity, mio.tpy

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

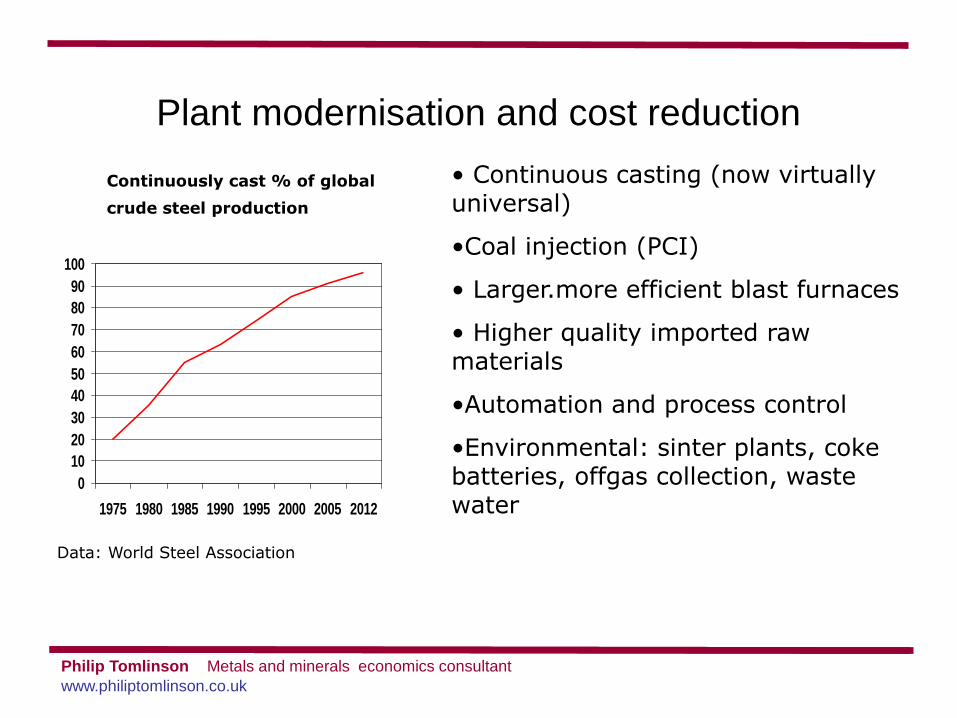

Plant modernisation and cost reduction

0

10

20

30

40

50

60

70

80

90

100

1975 1980 1985 1990 1995 2000 2005 2012

Continuously cast % of global

crude steel production

• Continuous casting (now virtually universal)

•Coal injection (PCI)

• Larger.more efficient blast furnaces

• Higher quality imported raw materials

•Automation and process control

•Environmental: sinter plants, coke batteries, offgas collection, waste water

Data: World Steel Association

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

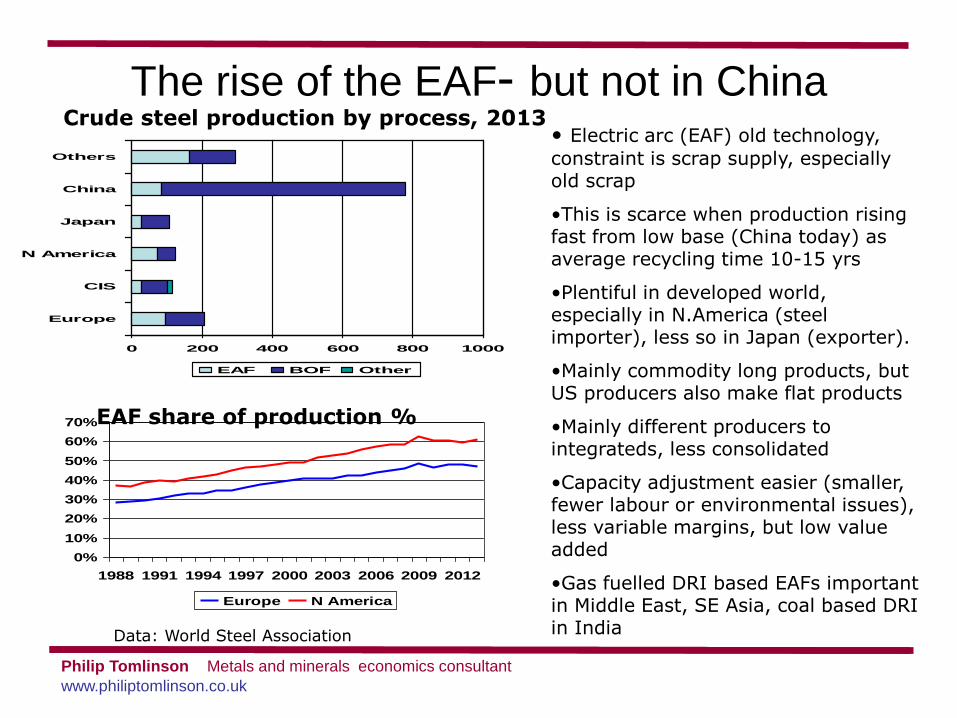

The rise of the EAF- but not in China

0 200 400 600 800 1000

Europe

CIS

N America

Japan

China

Others

EAF BOF Other

0%

10%

20%

30%

40%

50%

60%

70%

1988 1991 1994 1997 2000 2003 2006 2009 2012

Europe N America

Crude steel production by process, 2013

EAF share of production %

• Electric arc (EAF) old technology,

constraint is scrap supply, especially old scrap

•This is scarce when production rising fast from low base (China today) as average recycling time 10-15 yrs

•Plentiful in developed world, especially in N.America (steel importer), less so in Japan (exporter).

•Mainly commodity long products, but US producers also make flat products

•Mainly different producers to integrateds, less consolidated

•Capacity adjustment easier (smaller, fewer labour or environmental issues), less variable margins, but low value added

•Gas fuelled DRI based EAFs important in Middle East, SE Asia, coal based DRI in India Data: World Steel Association

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

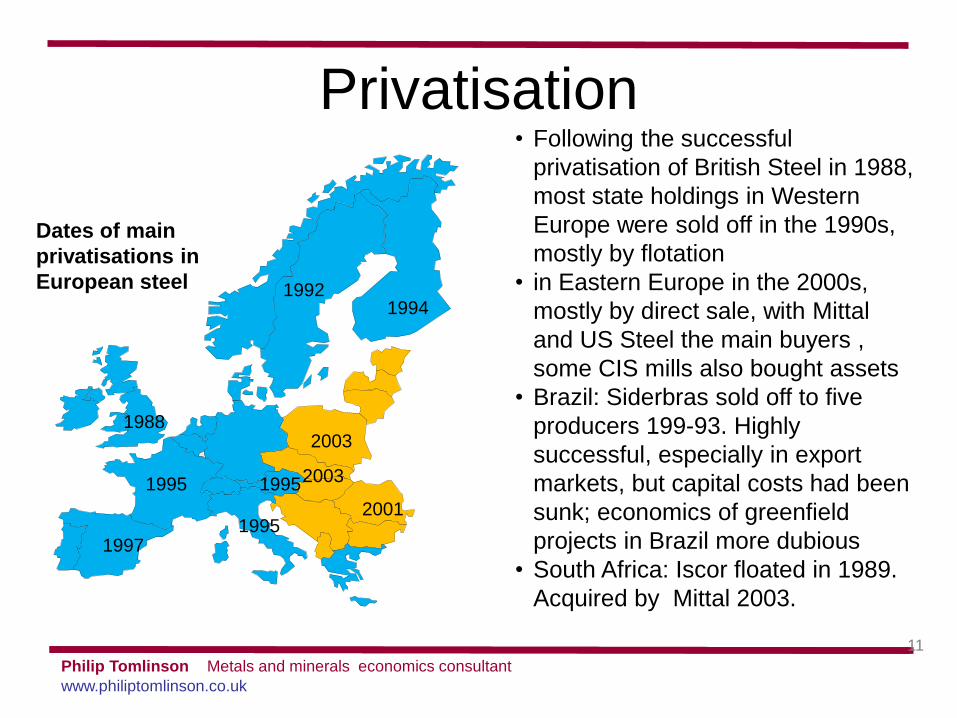

Privatisation

11

1988

1992

1995

1995

1995

1997

2003

2003

1994

2001

Dates of main

privatisations in

European steel

• Following the successful

privatisation of British Steel in 1988,

most state holdings in Western

Europe were sold off in the 1990s,

mostly by flotation

• in Eastern Europe in the 2000s,

mostly by direct sale, with Mittal

and US Steel the main buyers ,

some CIS mills also bought assets

• Brazil: Siderbras sold off to five

producers 199-93. Highly

successful, especially in export

markets, but capital costs had been

sunk; economics of greenfield

projects in Brazil more dubious

• South Africa: Iscor floated in 1989.

Acquired by Mittal 2003.

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

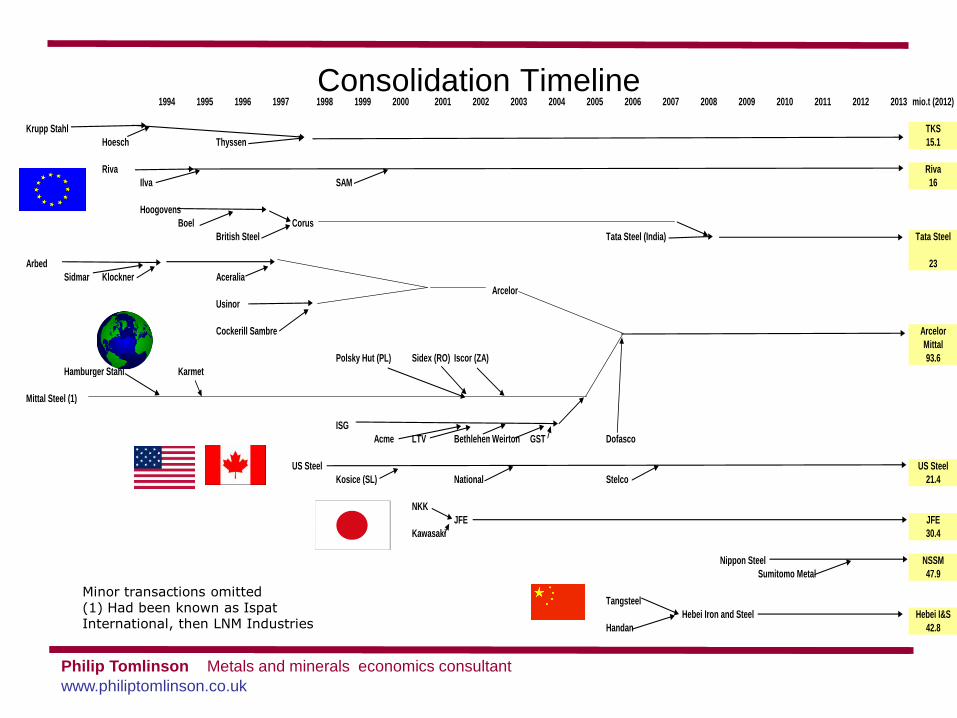

Consolidation Timeline 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 mio.t (2012)

Krupp Stahl TKS

Hoesch Thyssen 15.1

Riva Riva

Ilva SAM 16

Hoogovens

Boel Corus

British Steel Tata Steel (India) Tata Steel

Arbed 23

Sidmar Klockner Aceralia

Arcelor

Usinor

Cockerill Sambre Arcelor

Mittal

Polsky Hut (PL) Sidex (RO) Iscor (ZA) 93.6

Hamburger Stahl Karmet

Mittal Steel (1)

ISG

Acme LTV BethlehemWeirton GST Dofasco

US Steel US Steel

Kosice (SL) National Stelco 21.4

NKK

JFE JFE

Kawasaki 30.4

Nippon Steel NSSM

Sumitomo Metal 47.9

Tangsteel

Hebei Iron and Steel Hebei I&S

Handan 42.8

Minor transactions omitted (1) Had been known as Ispat International, then LNM Industries

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

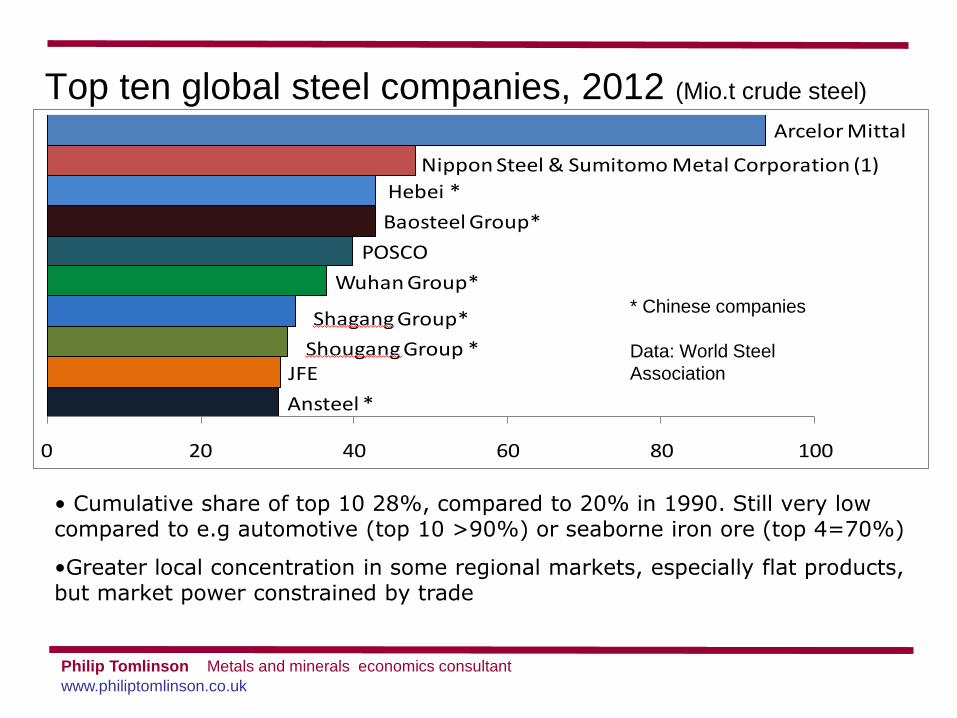

Ansteel *

JFE

Wuhan Group*

POSCO

Baosteel Group*

Hebei *

Arcelor Mittal

0 20 40 60 80 100

Nippon Steel & Sumitomo Metal Corporation (1)

Shagang Group*

Shougang Group *

Top ten global steel companies, 2012 (Mio.t crude steel)

Data: World Steel Association

* Chinese companies

Data: World Steel

Association

• Cumulative share of top 10 28%, compared to 20% in 1990. Still very low compared to e.g automotive (top 10 >90%) or seaborne iron ore (top 4=70%)

•Greater local concentration in some regional markets, especially flat products, but market power constrained by trade

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

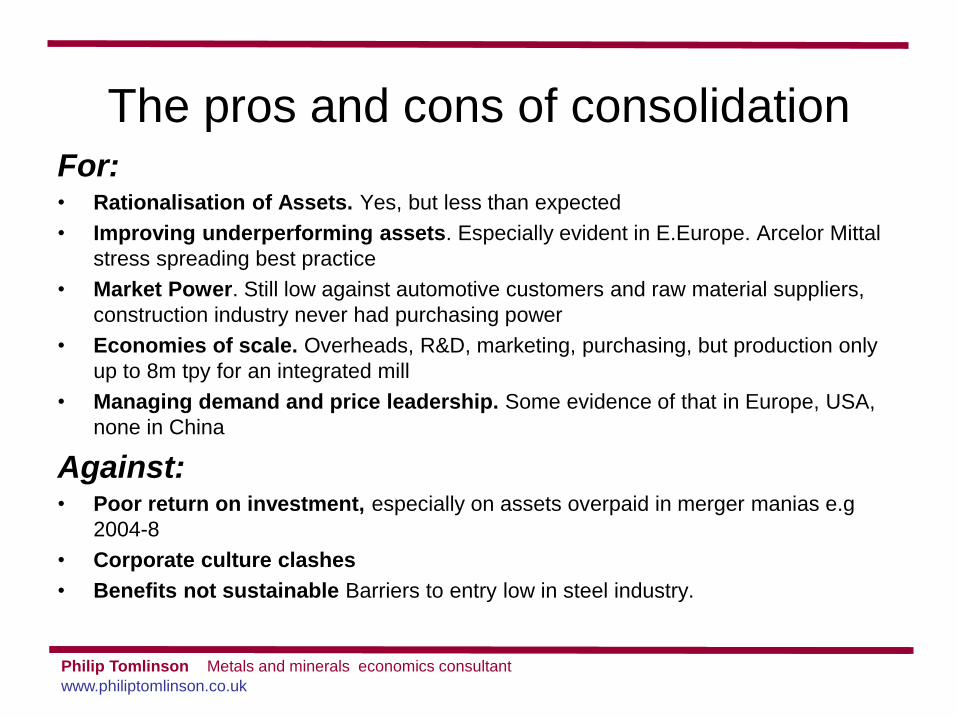

The pros and cons of consolidation For: • Rationalisation of Assets. Yes, but less than expected

• Improving underperforming assets. Especially evident in E.Europe. Arcelor Mittal

stress spreading best practice

• Market Power. Still low against automotive customers and raw material suppliers,

construction industry never had purchasing power

• Economies of scale. Overheads, R&D, marketing, purchasing, but production only

up to 8m tpy for an integrated mill

• Managing demand and price leadership. Some evidence of that in Europe, USA,

none in China

Against: • Poor return on investment, especially on assets overpaid in merger manias e.g

2004-8

• Corporate culture clashes

• Benefits not sustainable Barriers to entry low in steel industry.

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

-2.0%0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%

Arcelo

r*

Corus

TKS

Rautaru

ukki

Salzg

itter

SSAB

voest

alpin

e

1997-2006 1997-2011

n/a

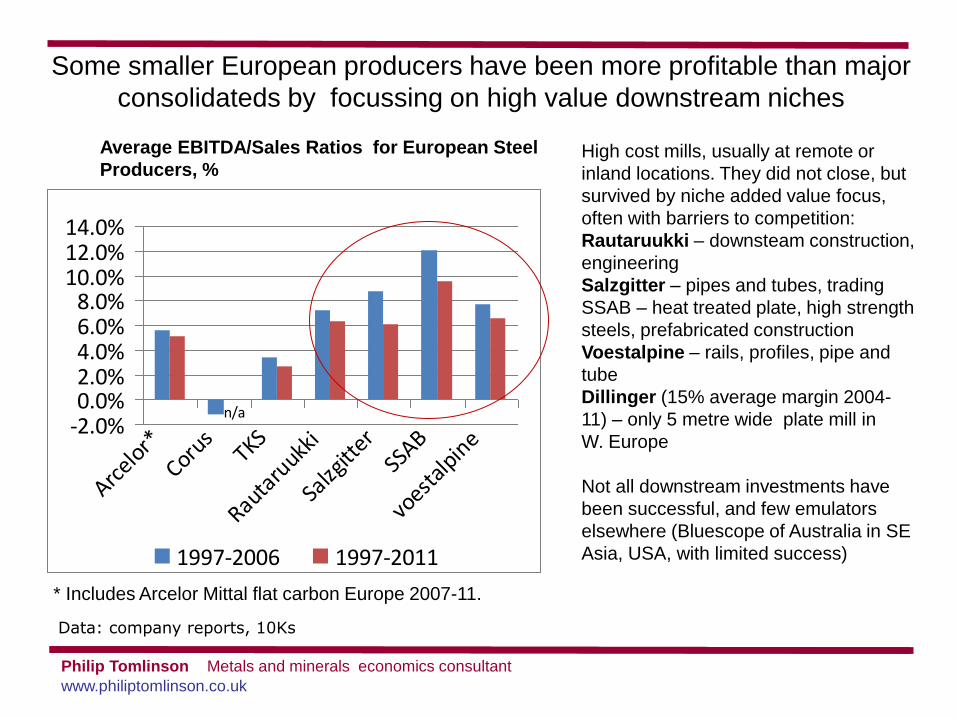

Some smaller European producers have been more profitable than major

consolidateds by focussing on high value downstream niches

Data: company reports

and websites

* Includes Arcelor Mittal flat carbon Europe 2007-11.

Average EBITDA/Sales Ratios for European Steel

Producers, % High cost mills, usually at remote or

inland locations. They did not close, but

survived by niche added value focus,

often with barriers to competition:

Rautaruukki – downsteam construction,

engineering

Salzgitter – pipes and tubes, trading

SSAB – heat treated plate, high strength

steels, prefabricated construction

Voestalpine – rails, profiles, pipe and

tube

Dillinger (15% average margin 2004-

11) – only 5 metre wide plate mill in

W. Europe

Not all downstream investments have

been successful, and few emulators

elsewhere (Bluescope of Australia in SE

Asia, USA, with limited success)

Data: company reports, 10Ks

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

Low level of upstream integration

into raw materials

• Global average only ~15% for iron ore, The only significant integrated regions are:

– Russia and the Ukraine, where all the major producers own iron ore mines, except MMK;

– North America, especially Arcelor Mittal and AHMSA (Mexico)

– Brazil, where CSN, Usiminas and Gerdau own mines, but only CSN is currently self sufficient (indeed a major ore exporter)

– India (SAIL and Tata)

• Even less for coal (only USA, Russia)

• Steel mills sold mines before 2003 when iron ore cheap

• Arcelor Mittal have ambitious plan to raise self sufficiency to 75%

• Constraints on investment: cost, quality of available assets, lead times, expertise, timing (downturn possible)

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

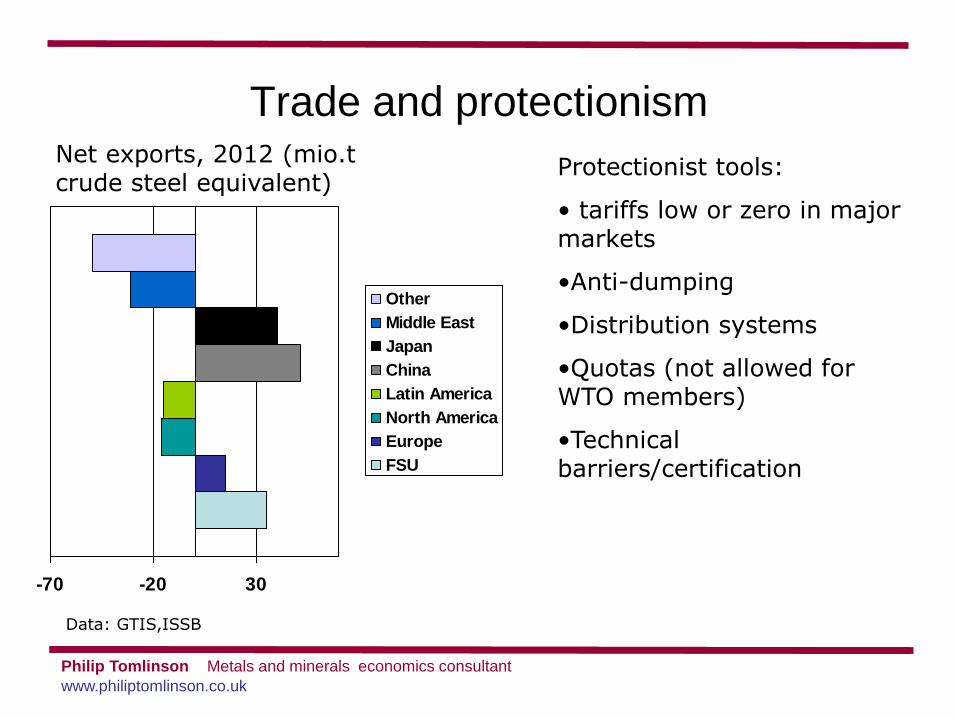

Trade and protectionism

-70 -20 30

Other

Middle East

Japan

China

Latin America

North America

Europe

FSU

Net exports, 2012 (mio.t crude steel equivalent)

Data: GTIS,ISSB

Protectionist tools:

• tariffs low or zero in major markets

•Anti-dumping

•Distribution systems

•Quotas (not allowed for WTO members)

•Technical barriers/certification

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

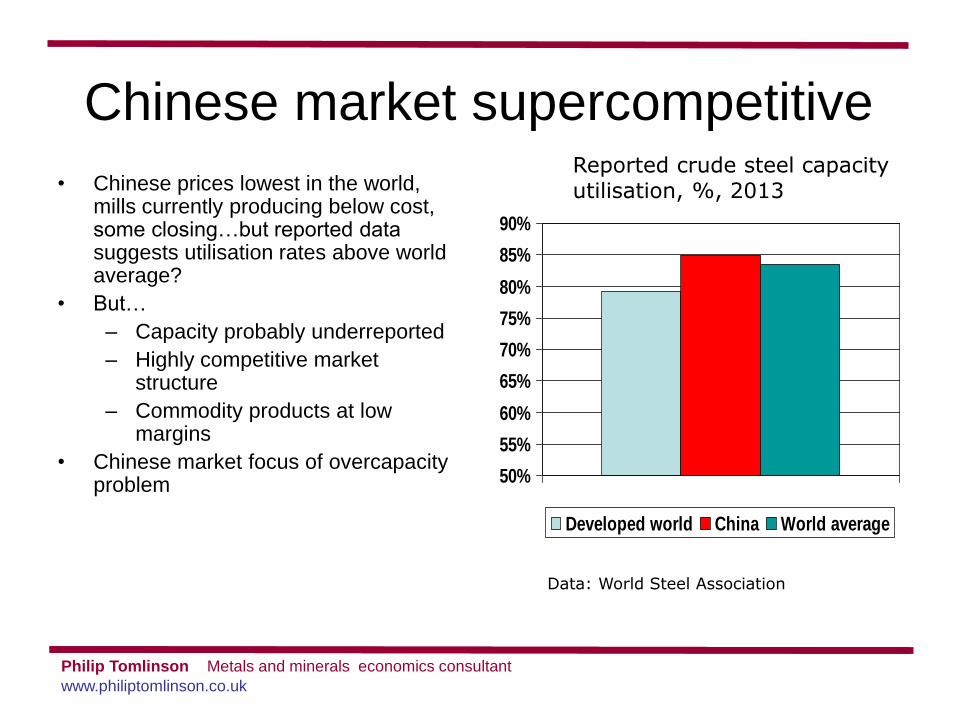

Chinese market supercompetitive

• Chinese prices lowest in the world, mills currently producing below cost, some closing…but reported data suggests utilisation rates above world average?

• But…

– Capacity probably underreported

– Highly competitive market structure

– Commodity products at low margins

• Chinese market focus of overcapacity problem

50%

55%

60%

65%

70%

75%

80%

85%

90%

Developed world China World average

Reported crude steel capacity utilisation, %, 2013

Data: World Steel Association

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

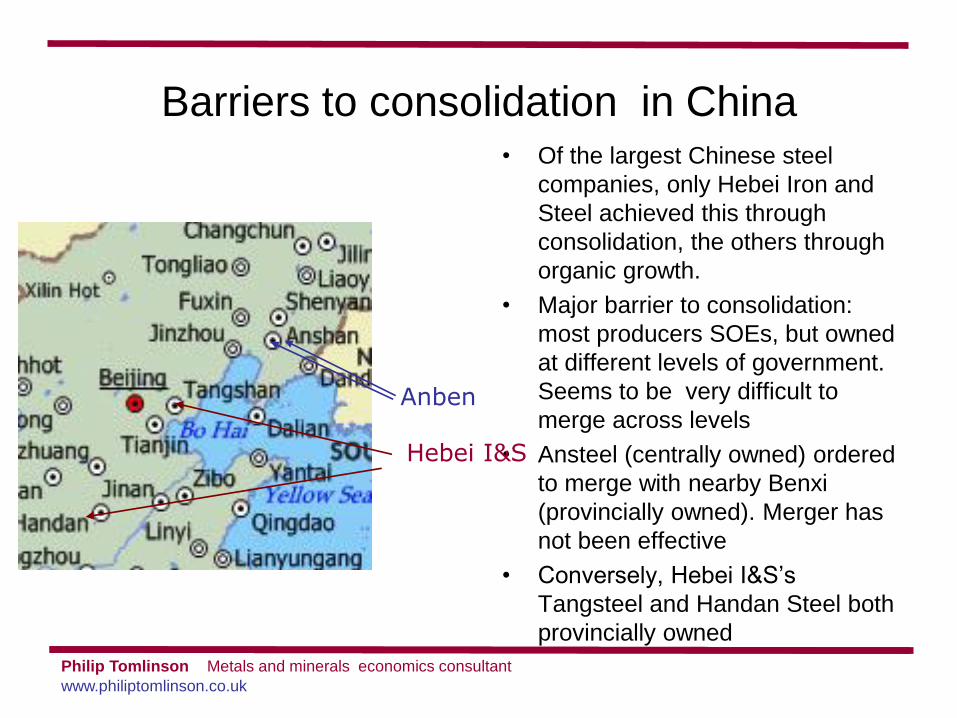

Barriers to consolidation in China • Of the largest Chinese steel

companies, only Hebei Iron and

Steel achieved this through

consolidation, the others through

organic growth.

• Major barrier to consolidation:

most producers SOEs, but owned

at different levels of government.

Seems to be very difficult to

merge across levels

• Ansteel (centrally owned) ordered

to merge with nearby Benxi

(provincially owned). Merger has

not been effective

• Conversely, Hebei I&S’s

Tangsteel and Handan Steel both

provincially owned

Anben

Hebei I&S

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

Europe after 1975 v China Today

Similarities

• The largest competitive market in the world, private and state producers, imported raw materials .

• In theory central power (EEC Commission or Chinese central government) has strong powers, in practice local powers important

• Because of importance of integrated mill employment, local subsidies as growth declined

• Market forces alone would lead to closures being focussed on weaker regions, politically unacceptable

Differences

• EEC industry invested in new cost reducing technologies (e.g concast), most Chinese industry new and modern – but environmental enforcement is lax

• No significant EAF sector

Philip Tomlinson Metals and minerals economics consultant www.philiptomlinson.co.uk

Some ideas for China

• Accurate production and capacity data

• Encourage/assist weaker regions to

create alternative consumer-focused

employment (as in France, UK after

1975) not fight steel closures to the last

(as in Belgium, Italy)

• Exports not a solution

• Enforce environmental regulations,

starting with centrally owned mills

• Privatisation? (may not be ideologically

acceptable)

• Focus on value added

Consett steelworks, UK, closed

1980

Consett’s largest employer

today

Seek to avoid the wasteful subsidies that happened in Europe!