Embed Size (px)

Citation preview

OPPORTUNITIES FOR CHEMICALS AND MATERIALS IN PVTechnical Seminar 3 Market TrendsDecember 6, 2011PV Japan 2011

Michael CorbettManaging Partner

Linx [email protected]

Outline

1. Overview of Linx Consulting

2. Understanding Solar Drivers

3. Opportunities for Chemicals and Materials in PV

4. Conclusions

LINX CONSULTING 2SEE BEYOND THE HORIZON

Overview of Linx Consulting

LINX CONSULTING 3SEE BEYOND THE HORIZON

LINX CONSULTING SEE BEYOND THE HORIZON 4

The Value We Bring To Clients

1. We create knowledge and develop unique insights at the intersection of advanced thin film processes and the chemicals and materials industry

2. We help our clients to succeed through our:• Experience in global electronics / semiconductor and advanced materials

and thin film processing industries:

• Experience in the global chemicals industry• Experience at Device Producers• Experience at OEMs• Global network and capabilities• Advanced modeling capabilities

– Semi– LCD

– Packaging– PV

– HBLED– Electrochemical

LINX CONSULTING SEE BEYOND THE HORIZON 5

We Provide High Confidence Decision Support Services – Single Client

PLANNINGBusiness Analysis

M&A / Due DiligenceDiversification / Expansion

Planning

IDEAS TO MARKETIP Development

Value Chain AnalysisTechnology Assessment and

Commercialization

OPERATIONSCost Benchmarking

Competitive IntelligenceCOO Models and Assessment

Process Technology Assessment

MARKETING & SALESMarket Analysis/Monitoring

Market Forecasting and ModelingCompetitive IntelligenceCustomer Perceptions

SINGLE CLIENT SERVICES

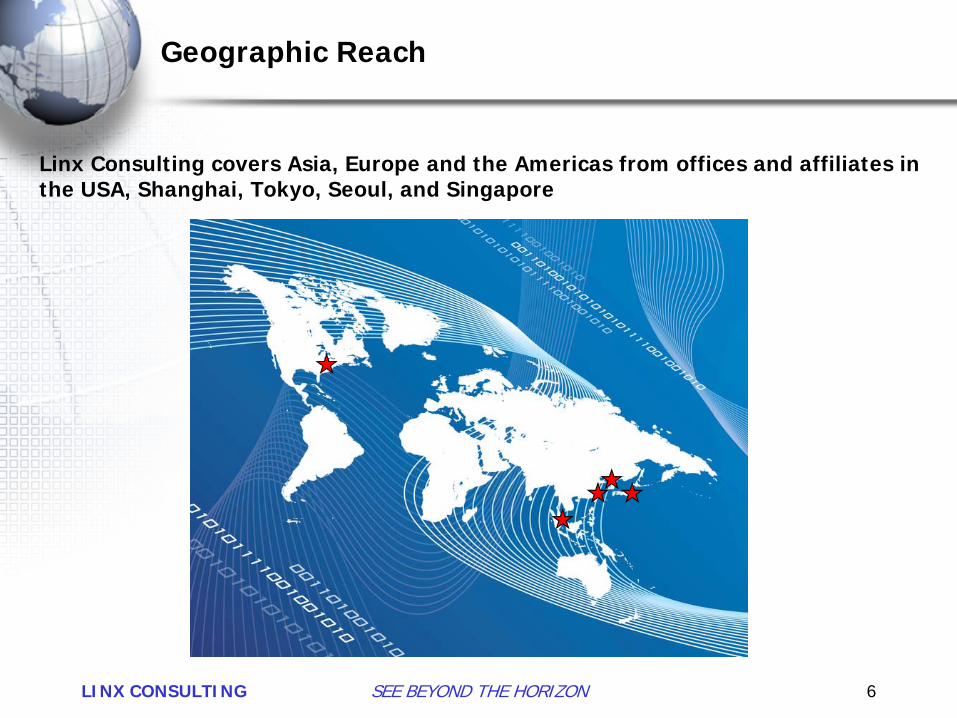

Geographic Reach

Linx Consulting covers Asia, Europe and the Americas from offices and affiliates in the USA, Shanghai, Tokyo, Seoul, and Singapore

LINX CONSULTING SEE BEYOND THE HORIZON 6

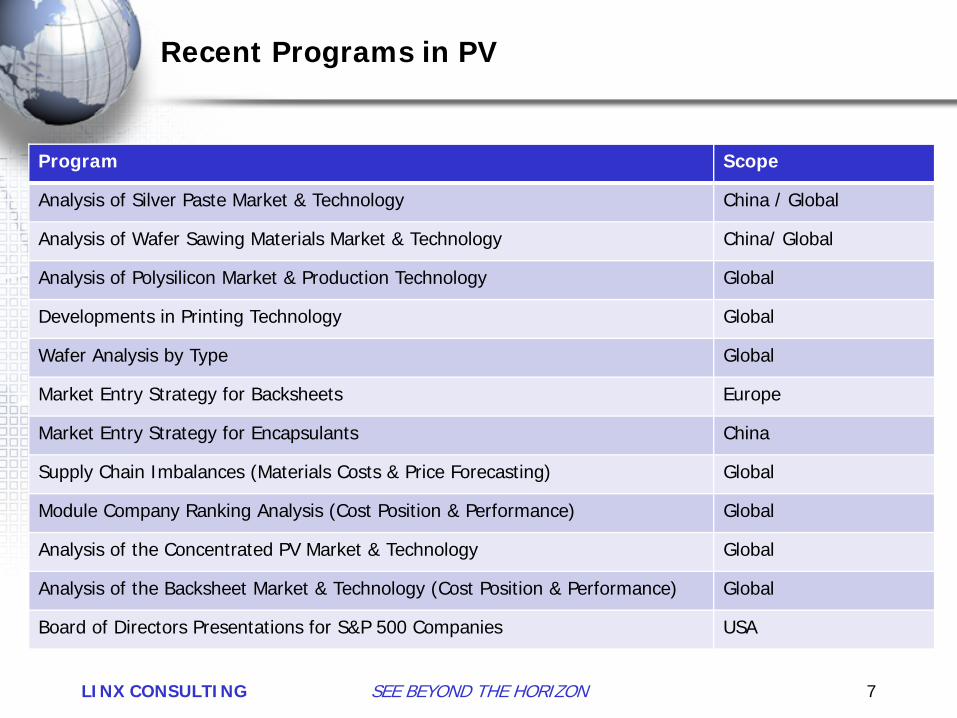

Recent Programs in PV

Program Scope

Analysis of Silver Paste Market & Technology China / Global

Analysis of Wafer Sawing Materials Market & Technology China/ Global

Analysis of Polysilicon Market & Production Technology Global

Developments in Printing Technology Global

Wafer Analysis by Type Global

Market Entry Strategy for Backsheets Europe

Market Entry Strategy for Encapsulants China

Supply Chain Imbalances (Materials Costs & Price Forecasting) Global

Module Company Ranking Analysis (Cost Position & Performance) Global

Analysis of the Concentrated PV Market & Technology Global

Analysis of the Backsheet Market & Technology (Cost Position & Performance) Global

Board of Directors Presentations for S&P 500 Companies USA

LINX CONSULTING SEE BEYOND THE HORIZON 7

Understanding Solar Drivers

LINX CONSULTING 8SEE BEYOND THE HORIZON

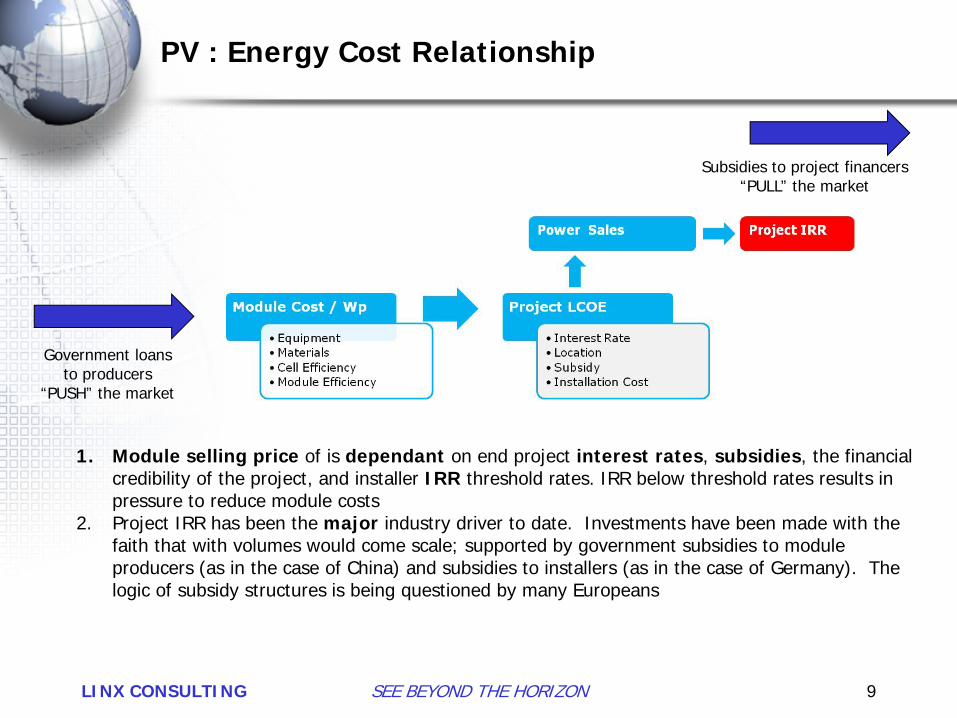

PV : Energy Cost Relationship

1. Module selling price of is dependant on end project interest rates, subsidies, the financial credibility of the project, and installer IRR threshold rates. IRR below threshold rates results in pressure to reduce module costs

2. Project IRR has been the major industry driver to date. Investments have been made with the faith that with volumes would come scale; supported by government subsidies to module producers (as in the case of China) and subsidies to installers (as in the case of Germany). The logic of subsidy structures is being questioned by many Europeans

LINX CONSULTING SEE BEYOND THE HORIZON 9

Subsidies to project financers “PULL” the market

Government loans to producers

“PUSH” the market

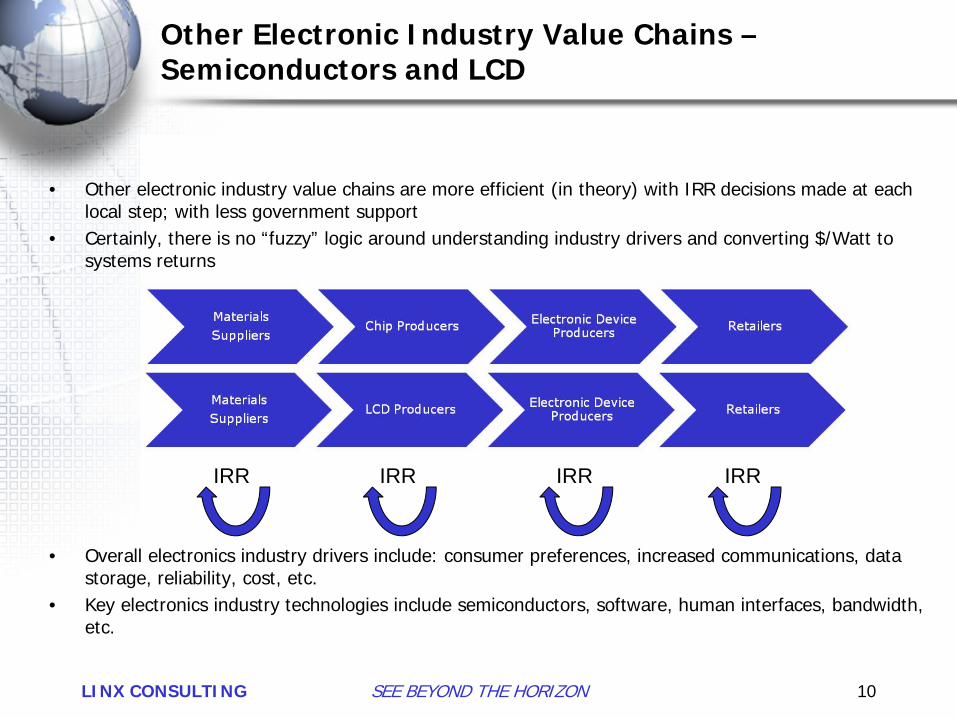

Other Electronic Industry Value Chains –Semiconductors and LCD

LINX CONSULTING SEE BEYOND THE HORIZON 10

• Other electronic industry value chains are more efficient (in theory) with IRR decisions made at each local step; with less government support

• Certainly, there is no “fuzzy” logic around understanding industry drivers and converting $/Watt to systems returns

• Overall electronics industry drivers include: consumer preferences, increased communications, data storage, reliability, cost, etc.

• Key electronics industry technologies include semiconductors, software, human interfaces, bandwidth, etc.

IRR IRRIRR IRR

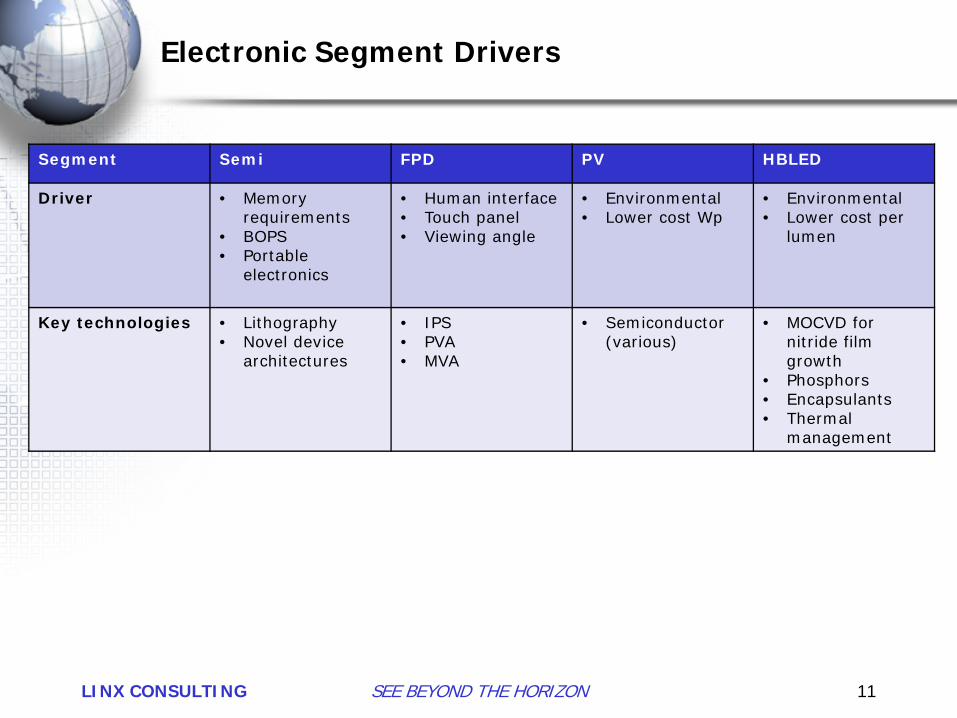

Electronic Segment Drivers

Segment Semi FPD PV HBLED

Driver • Memory requirements

• BOPS• Portable

electronics

• Human interface• Touch panel• Viewing angle

• Environmental• Lower cost Wp

• Environmental• Lower cost per

lumen

Key technologies • Lithography• Novel device

architectures

• IPS• PVA• MVA

• Semiconductor (various)

• MOCVD for nitride film growth

• Phosphors• Encapsulants• Thermal

management

LINX CONSULTING SEE BEYOND THE HORIZON 11

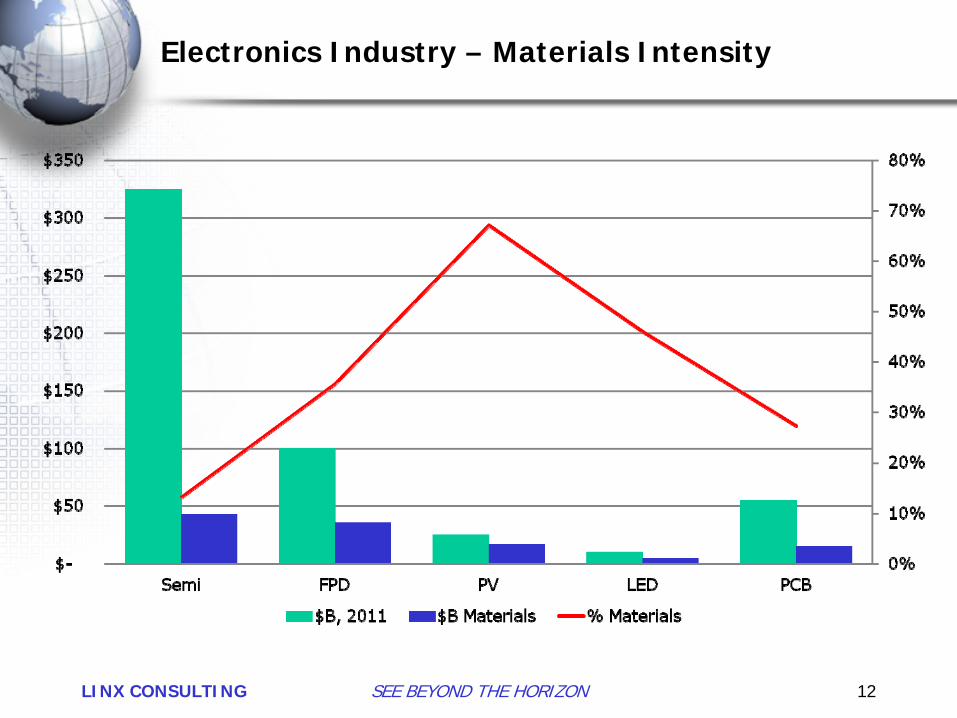

Electronics Industry – Materials Intensity

LINX CONSULTING SEE BEYOND THE HORIZON 12

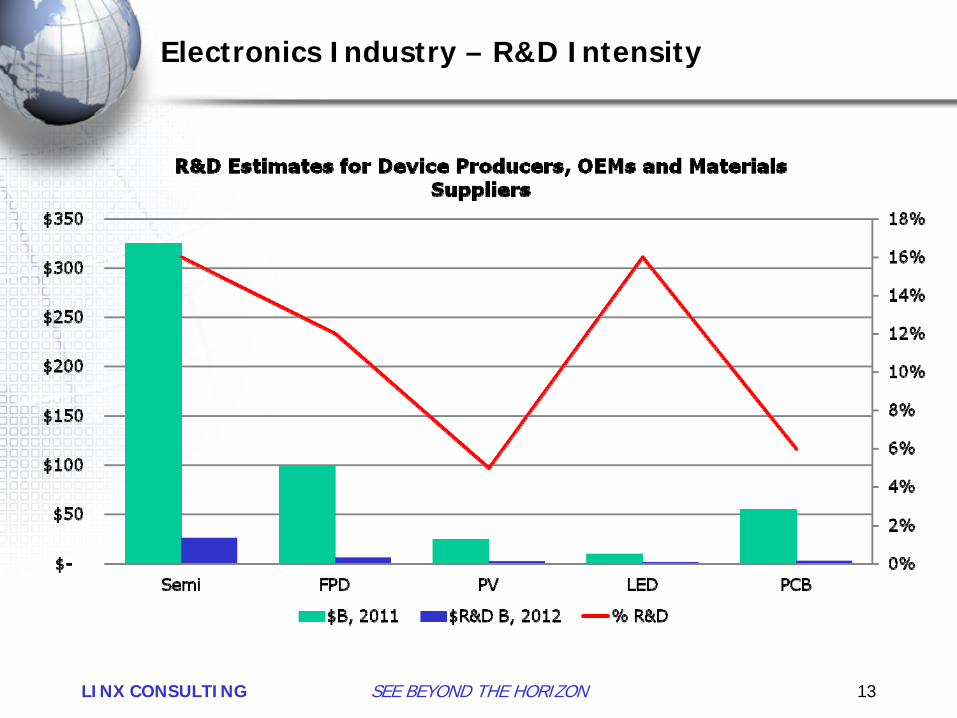

Electronics Industry – R&D Intensity

LINX CONSULTING SEE BEYOND THE HORIZON 13

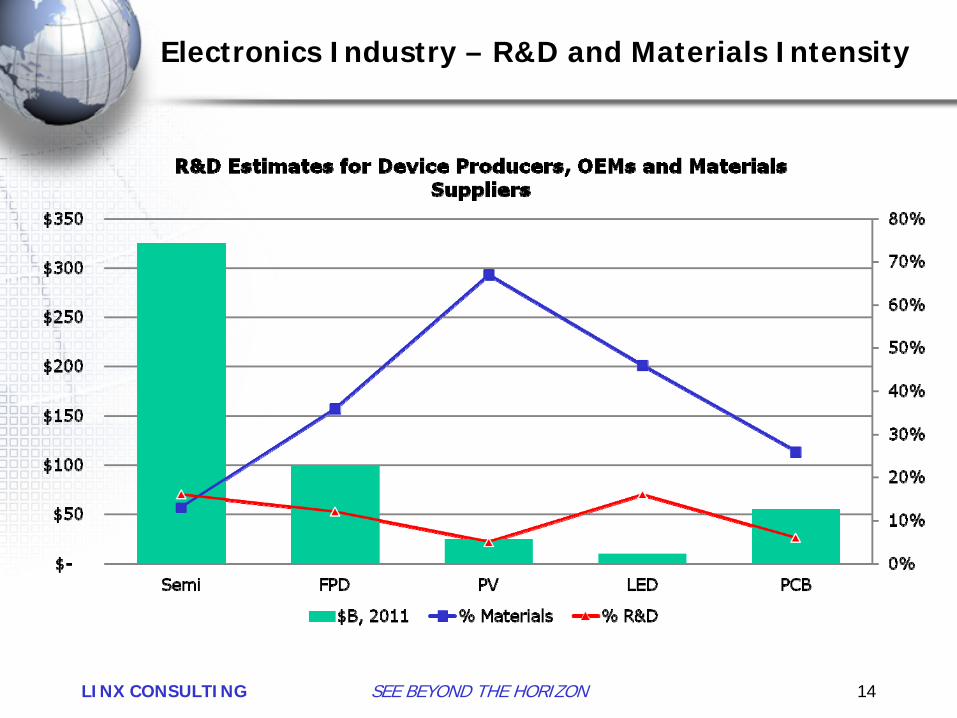

Electronics Industry – R&D and Materials Intensity

LINX CONSULTING SEE BEYOND THE HORIZON 14

Opportunities for Chemicals and Materials in PV

LINX CONSULTING 15SEE BEYOND THE HORIZON

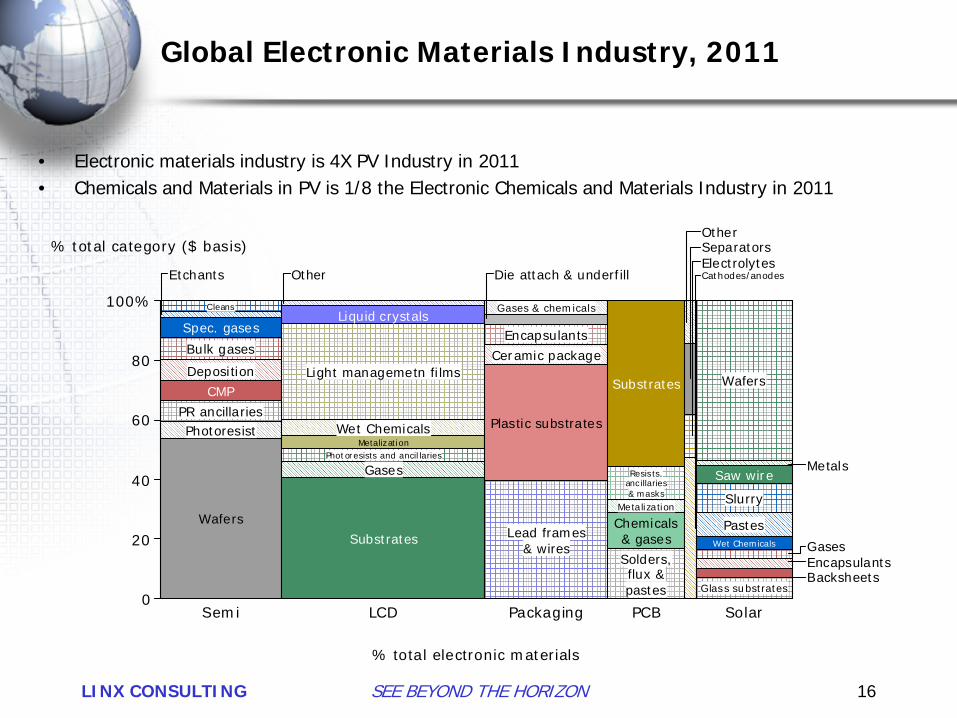

Global Electronic Materials Industry, 2011

• Electronic materials industry is 4X PV Industry in 2011• Chemicals and Materials in PV is 1/8 the Electronic Chemicals and Materials Industry in 2011

LINX CONSULTING SEE BEYOND THE HORIZON 16

Cleans

Etchants

Spec. gasesBulk gases

DepositionCMP

PR ancillariesPhotoresist

Wafers

Other

Liquid crystals

Light managemetn films

Wet ChemicalsMetalization

Photoresists and ancillaries

Gases

Substrates

Gases & chemicals

Die attach & underfill

EncapsulantsCeramic package

Plastic substrates

Lead frames& wires

Substrates

Resists,ancillaries& masks

Metalization

Chemicals& gasesSolders,flux &pastes

OtherSeparatorsElectrolytesCathodes/anodes

Wafers

MetalsSaw wire

Slurry

PastesWet Chemicals Gases

EncapsulantsBacksheets

Glass substrates

Semi LCD Packaging PCB Solar

Total =110.9

0

20

40

60

80

100%

% total category ($ basis)

% total electronic materials

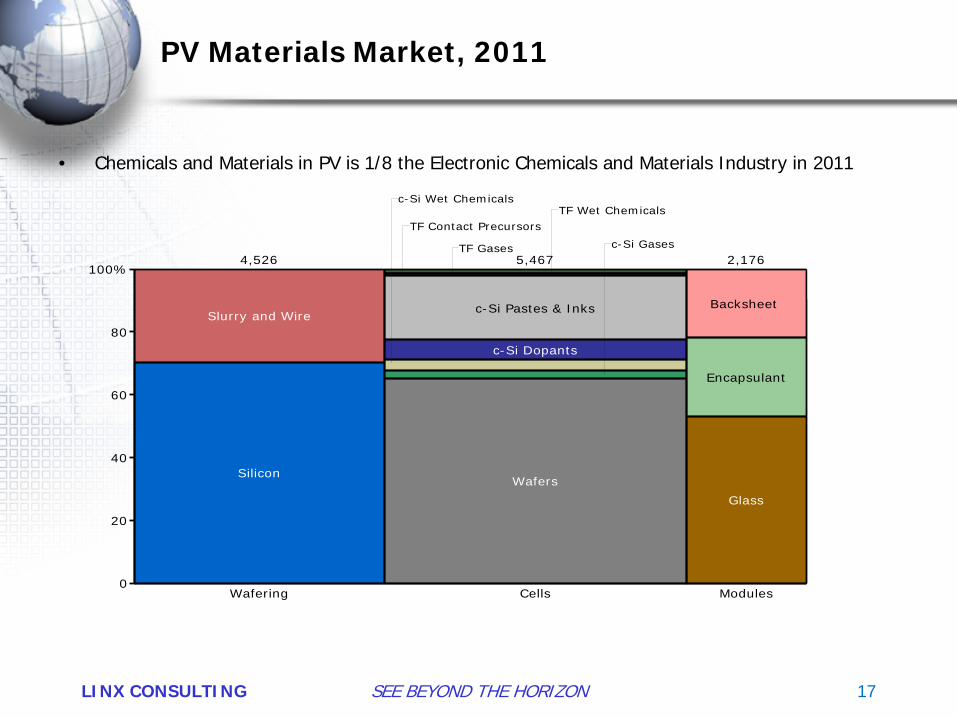

PV Materials Market, 2011

LINX CONSULTING SEE BEYOND THE HORIZON 17

• Chemicals and Materials in PV is 1/8 the Electronic Chemicals and Materials Industry in 2011

0

20

40

60

80

100%

Wafering

Slurry and Wire

Silicon

4,526

Cells

c-Si Pastes & Inks

c-Si Dopants

Wafers

5,467

Modules

Backsheet

Encapsulant

Glass

2,176 Total = 12,169.7

TF Contact PrecursorsTF Wet Chemicals

TF Gases

c-Si Wet Chemicals

c-Si Gases

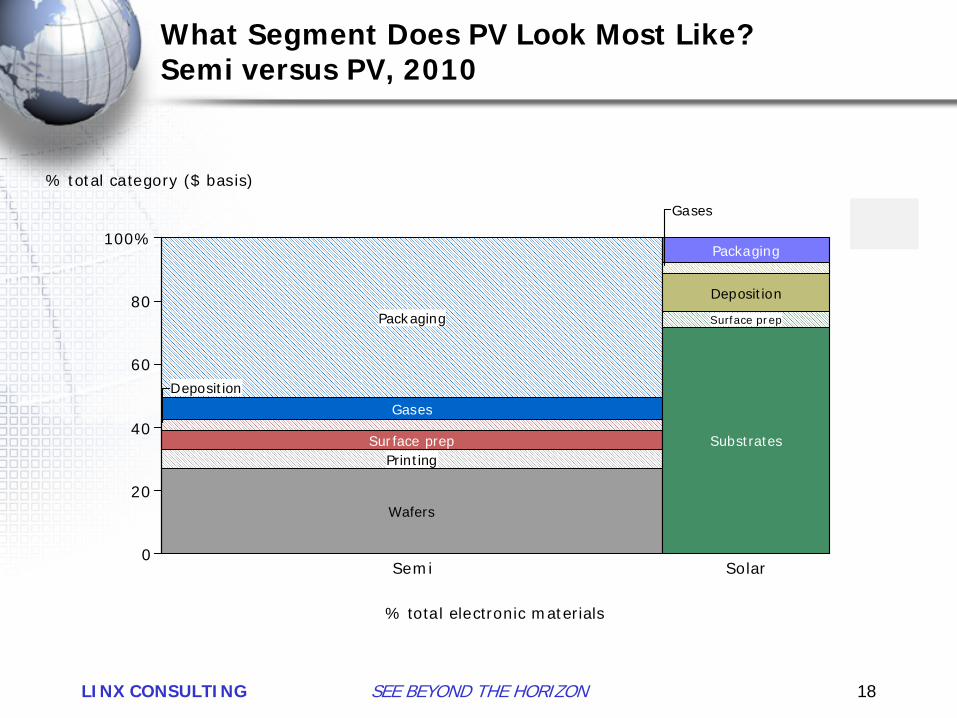

What Segment Does PV Look Most Like?Semi versus PV, 2010

LINX CONSULTING SEE BEYOND THE HORIZON 18

Packaging

GasesDeposition

Surface prepPrinting

Wafers

Packaging

Gases

Deposition

Surface prep

Substrates

Semi Solar

Total =56.9

0

20

40

60

80

100%

% total category ($ basis)

% total electronic materials

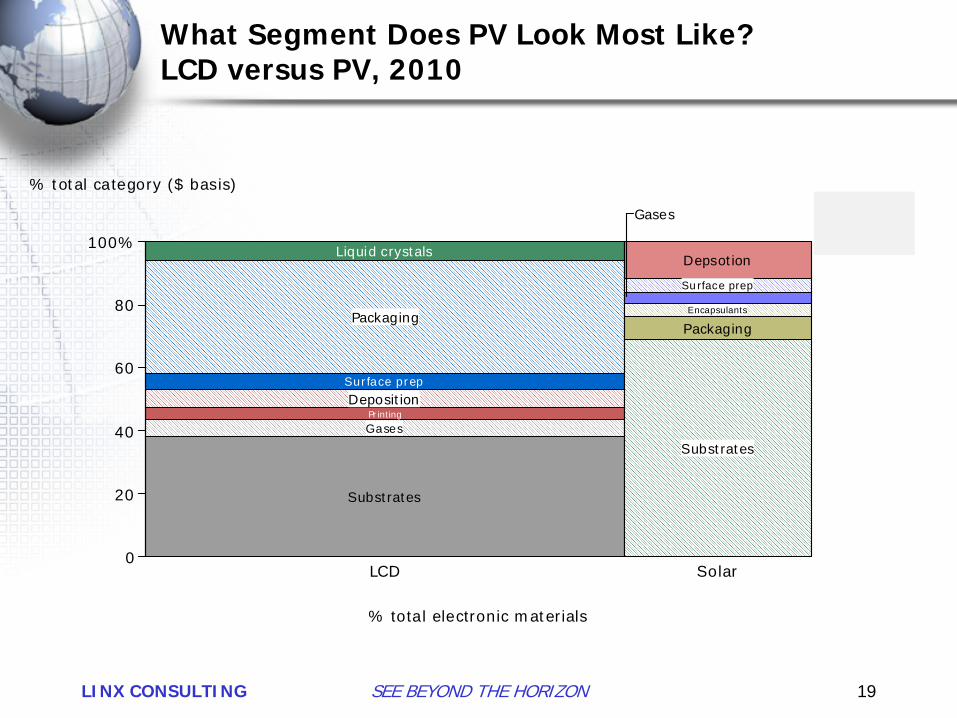

What Segment Does PV Look Most Like?LCD versus PV, 2010

LINX CONSULTING SEE BEYOND THE HORIZON 19

Liquid crystals

Packaging

Surface prepDeposition

PrintingGases

Substrates

Depsotion

Surface prep

Gases

Encapsulants

Packaging

Substrates

LCD Solar

Total =52.7

0

20

40

60

80

100%

% total category ($ basis)

% total electronic materials

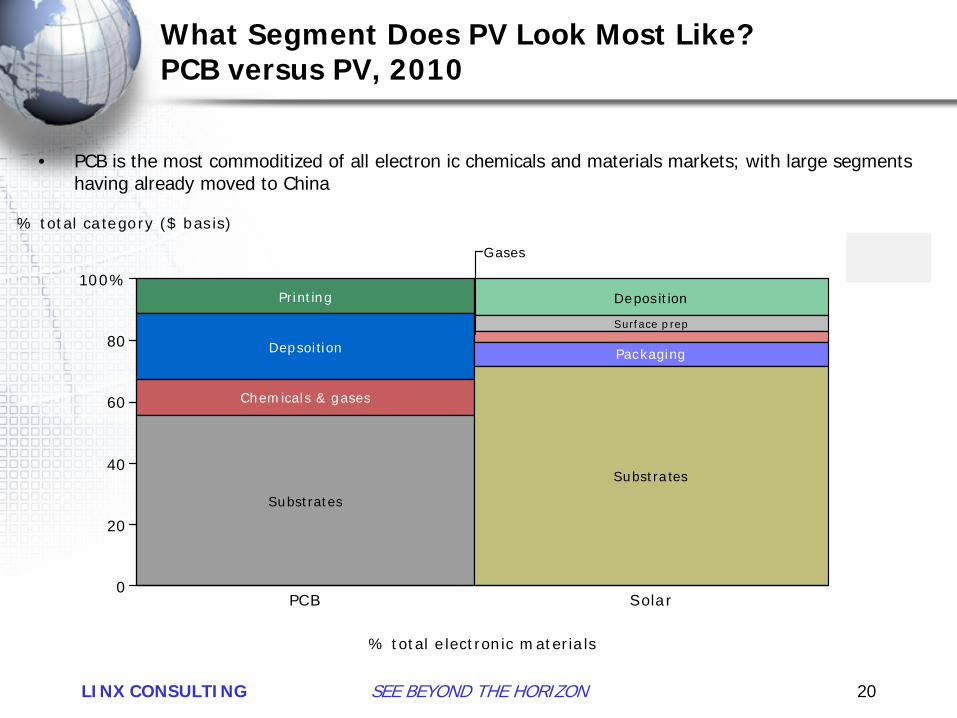

What Segment Does PV Look Most Like?PCB versus PV, 2010

• PCB is the most commoditized of all electron ic chemicals and materials markets; with large segments having already moved to China

LINX CONSULTING SEE BEYOND THE HORIZON 20

Printing

Depsoition

Chemicals & gases

Substrates

Deposition

Surface prep

Gases

Packaging

Substrates

PCB Solar

Total =27.7

0

20

40

60

80

100%

% total category ($ basis)

% total electronic materials

Conclusions

LINX CONSULTING 21SEE BEYOND THE HORIZON

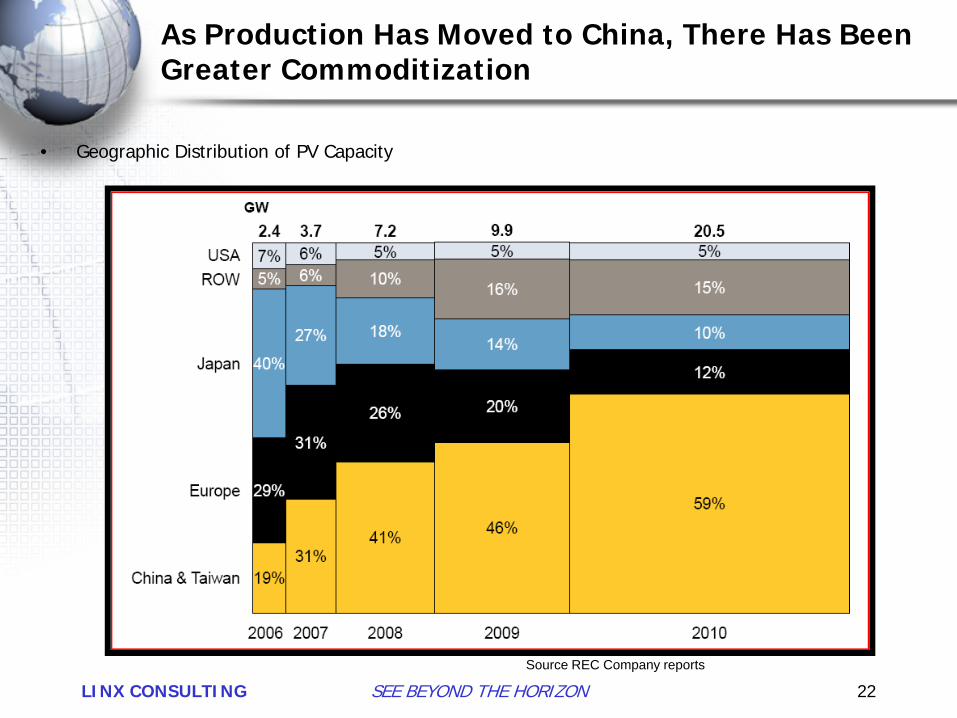

As Production Has Moved to China, There Has Been Greater Commoditization

• Geographic Distribution of PV Capacity

LINX CONSULTING SEE BEYOND THE HORIZON 22

Source REC Company reports

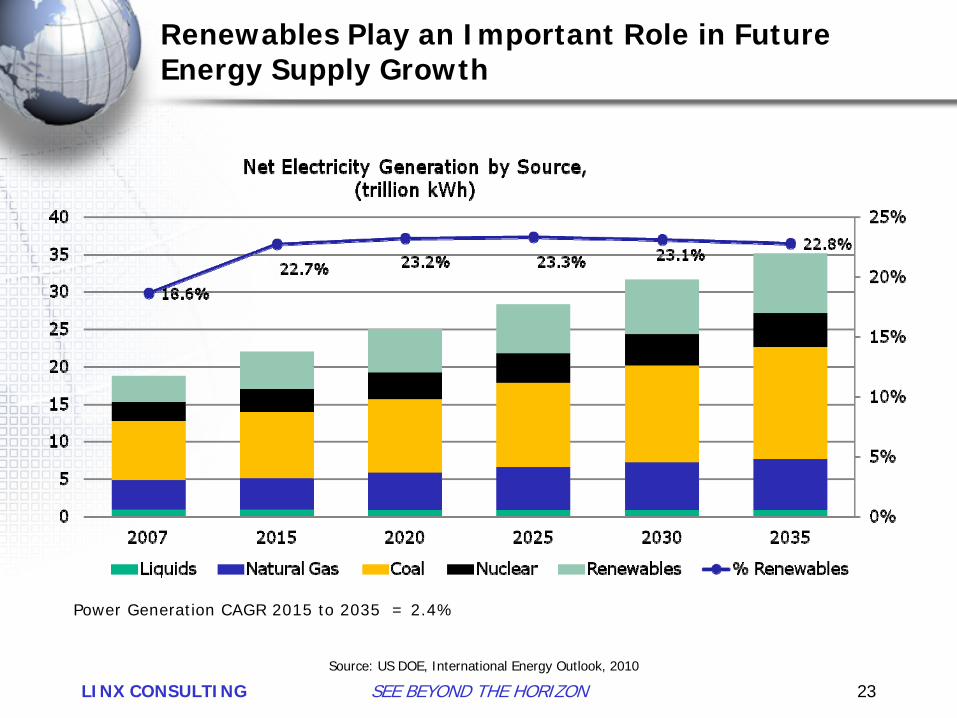

Renewables Play an Important Role in Future Energy Supply Growth

LINX CONSULTING SEE BEYOND THE HORIZON 23Source: US DOE, International Energy Outlook, 2010

Power Generation CAGR 2015 to 2035 = 2.4%

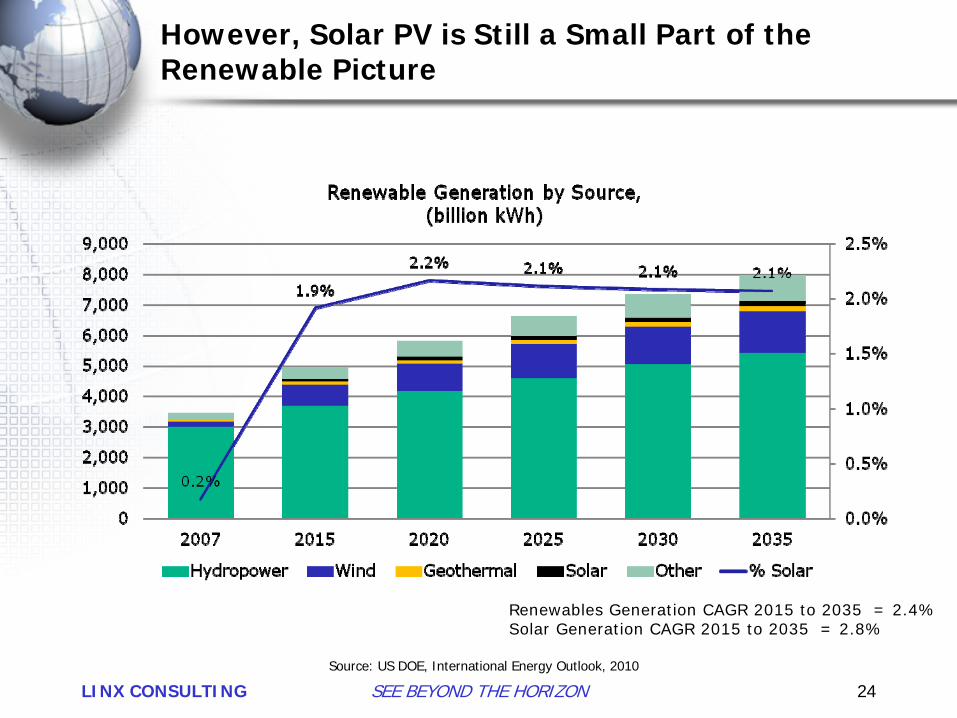

However, Solar PV is Still a Small Part of the Renewable Picture

LINX CONSULTING SEE BEYOND THE HORIZON 24Source: US DOE, International Energy Outlook, 2010

Renewables Generation CAGR 2015 to 2035 = 2.4%Solar Generation CAGR 2015 to 2035 = 2.8%

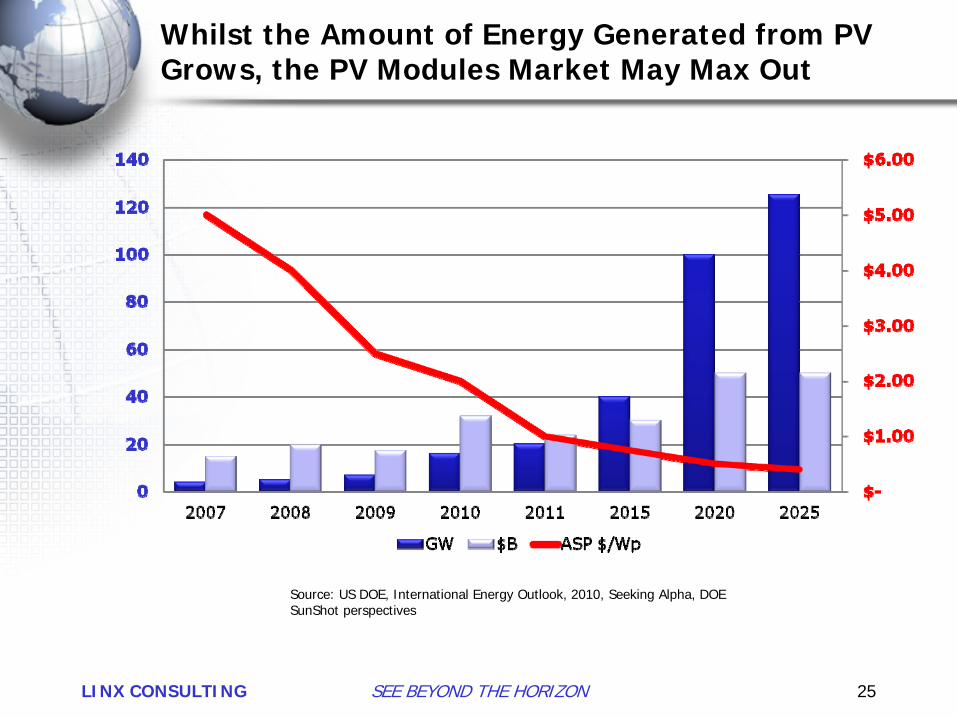

Whilst the Amount of Energy Generated from PV Grows, the PV Modules Market May Max Out

LINX CONSULTING SEE BEYOND THE HORIZON 25

Source: US DOE, International Energy Outlook, 2010, Seeking Alpha, DOE SunShot perspectives

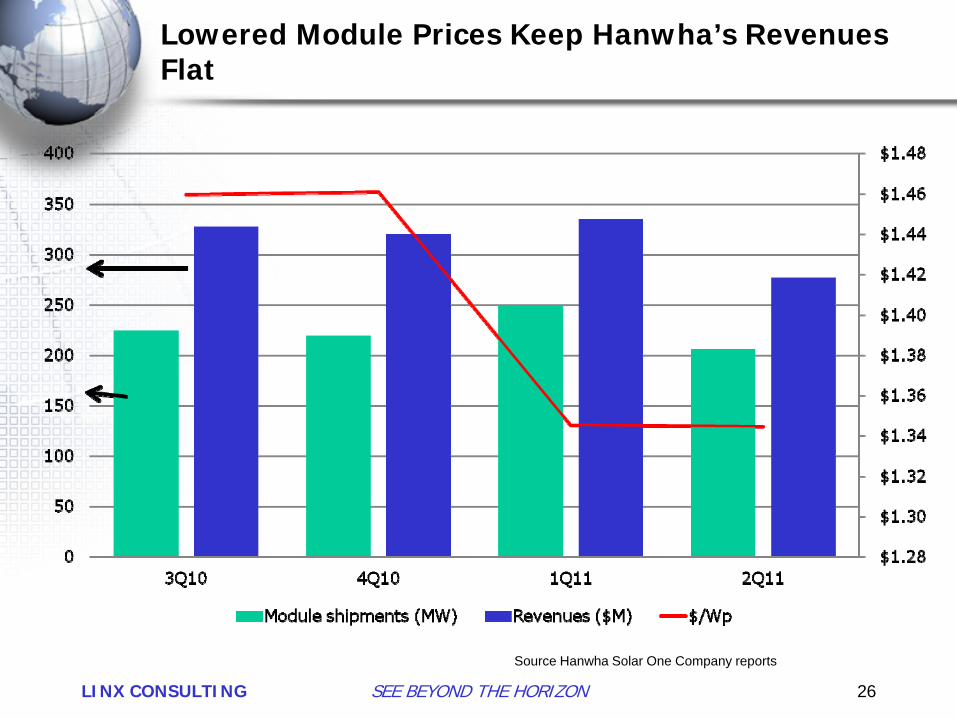

Lowered Module Prices Keep Hanwha’s Revenues Flat

LINX CONSULTING SEE BEYOND THE HORIZON 26

Source Hanwha Solar One Company reports

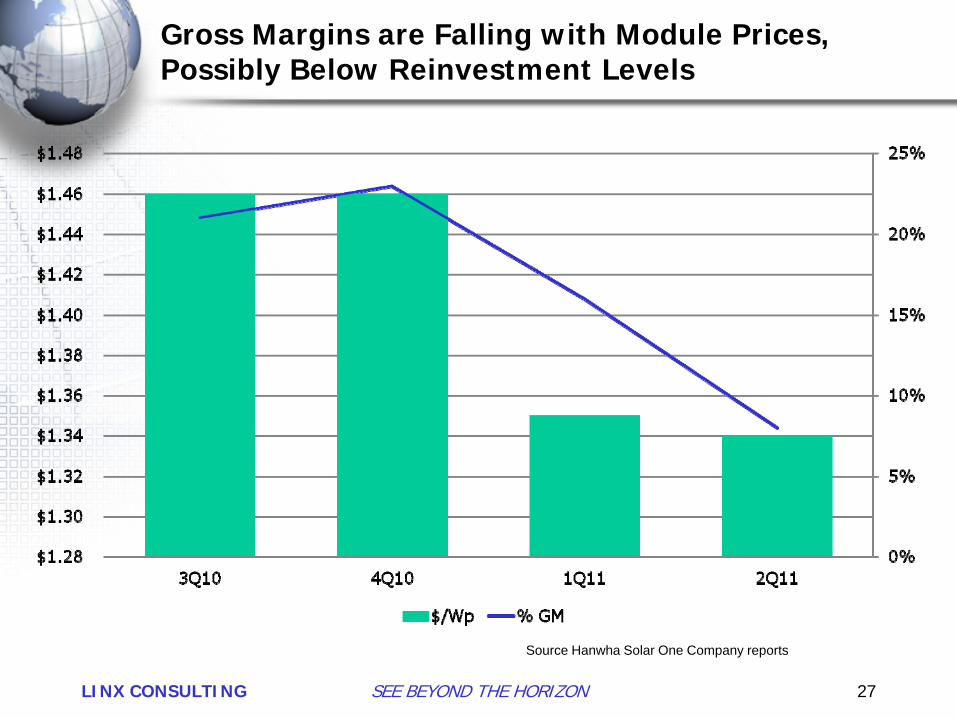

Gross Margins are Falling with Module Prices, Possibly Below Reinvestment Levels

LINX CONSULTING SEE BEYOND THE HORIZON 27

Source Hanwha Solar One Company reports

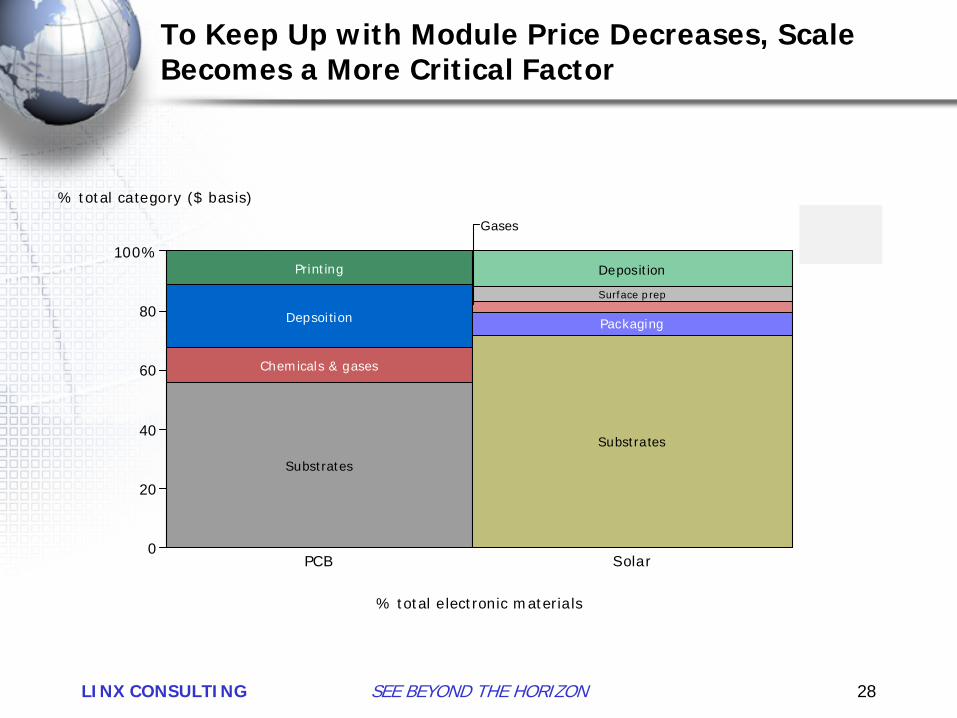

To Keep Up with Module Price Decreases, Scale Becomes a More Critical Factor

LINX CONSULTING SEE BEYOND THE HORIZON 28

Printing

Depsoition

Chemicals & gases

Substrates

Deposition

Surface prep

Gases

Packaging

Substrates

PCB Solar

Total =27.7

0

20

40

60

80

100%

% total category ($ basis)

% total electronic materials

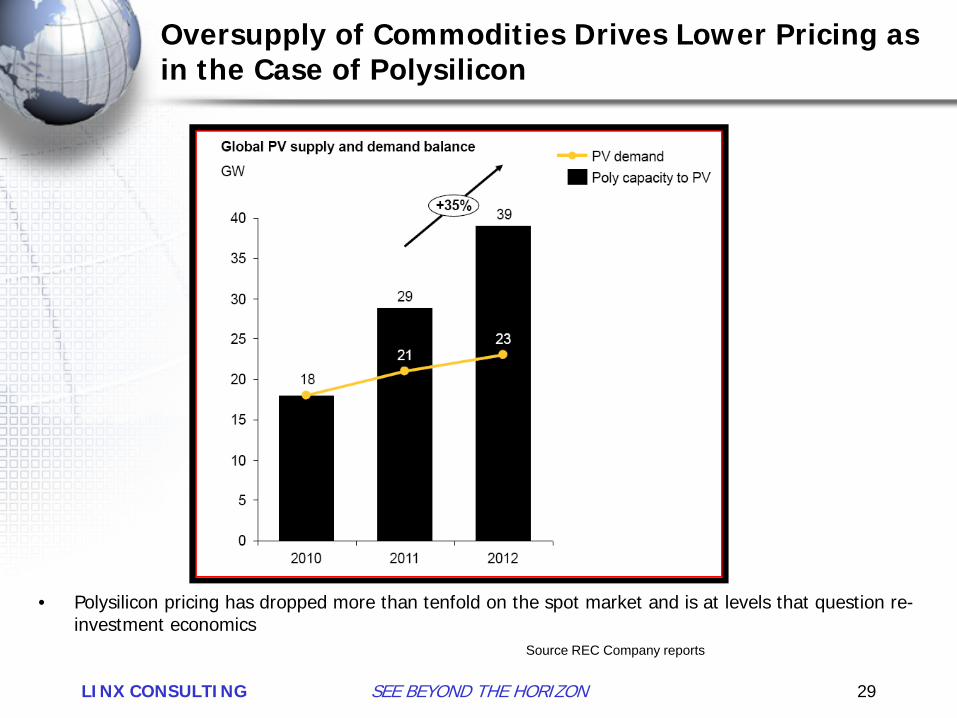

Oversupply of Commodities Drives Lower Pricing as in the Case of Polysilicon

• Polysilicon pricing has dropped more than tenfold on the spot market and is at levels that question re-investment economics

LINX CONSULTING SEE BEYOND THE HORIZON 29

Source REC Company reports

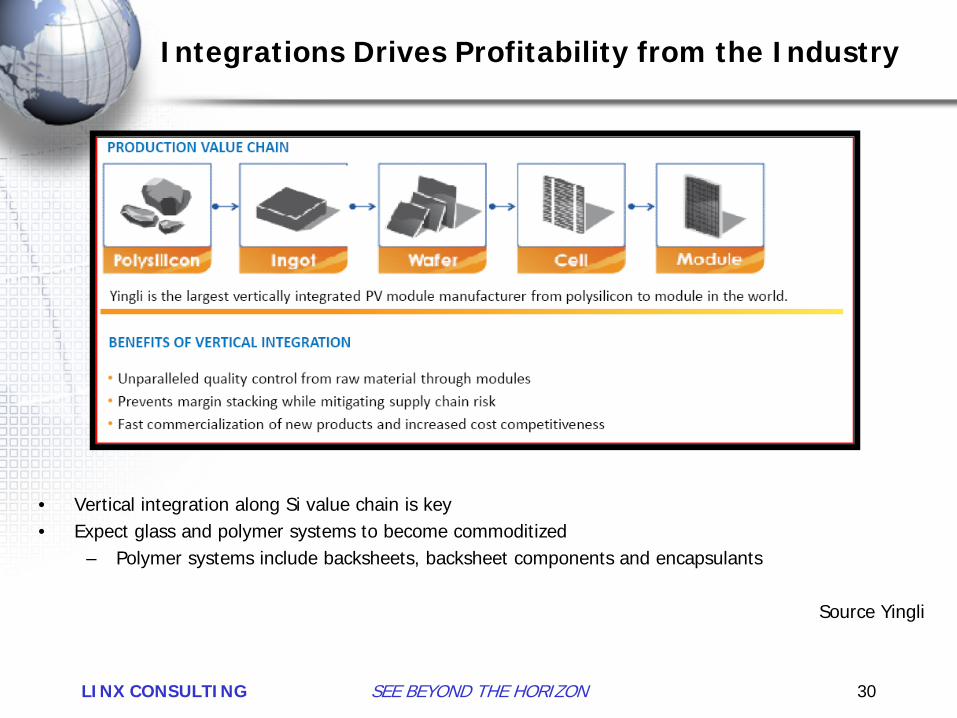

Integrations Drives Profitability from the Industry

• Vertical integration along Si value chain is key• Expect glass and polymer systems to become commoditized

– Polymer systems include backsheets, backsheet components and encapsulants

Source Yingli

LINX CONSULTING SEE BEYOND THE HORIZON 30

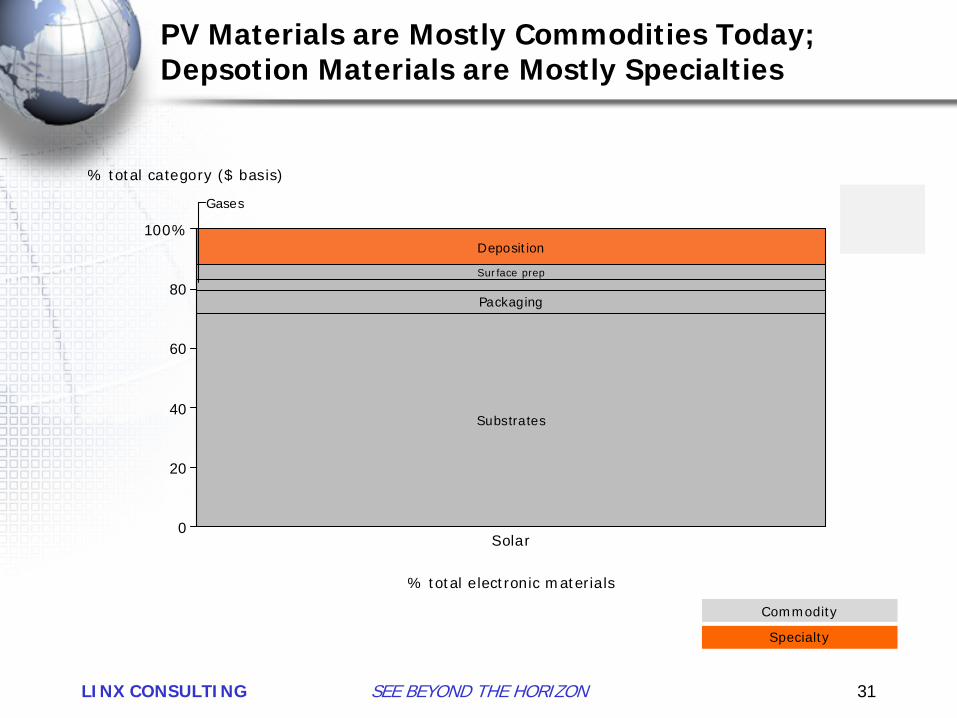

PV Materials are Mostly Commodities Today; Depsotion Materials are Mostly Specialties

Commodity

Specialty

LINX CONSULTING SEE BEYOND THE HORIZON 31

Deposition

Surface prep

Gases

Packaging

Substrates

Solar

Total =14.2

0

20

40

60

80

100%

% total category ($ basis)

% total electronic materials

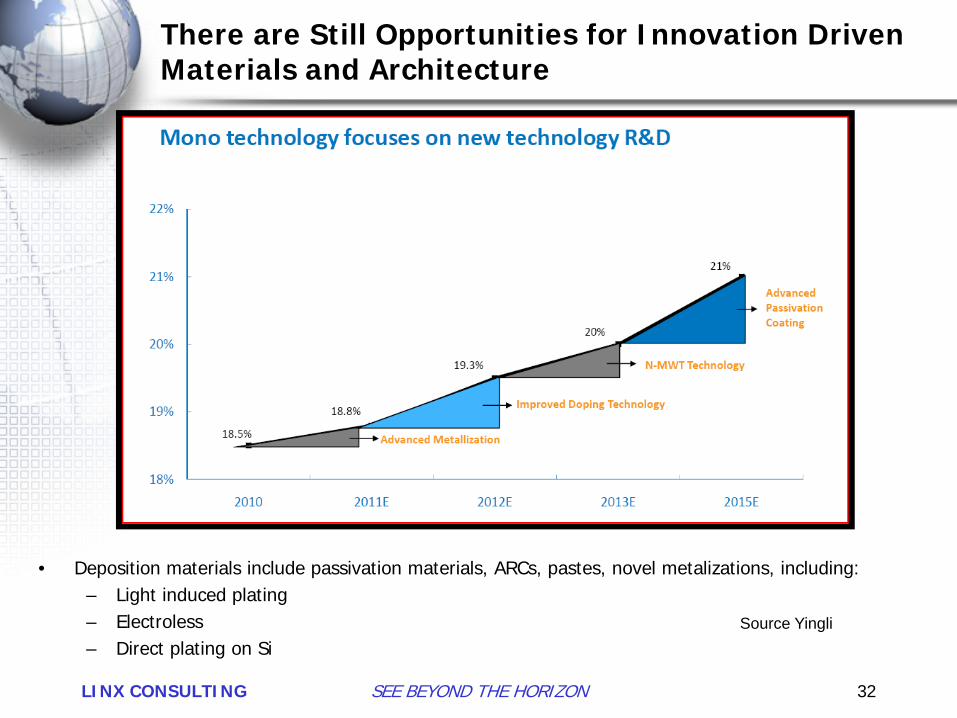

There are Still Opportunities for Innovation Driven Materials and Architecture

• Deposition materials include passivation materials, ARCs, pastes, novel metalizations, including:– Light induced plating– Electroless– Direct plating on Si

LINX CONSULTING SEE BEYOND THE HORIZON 32

Source Yingli

Conclusions: PV Model is Under Pressure

• Many chemicals and materials segments in PV are becoming / have become commoditized– Volume as a strategy is difficult as module prices still have to continue coming down

• Opportunities for new materials are difficult as it takes time to implement them due to module life concerns

• It is unrealistic for PV manufacturers’ to expect that their materials and equipment suppliers will drive their R&D for an extended period of time; due to current margin situation

– However, there is still room for chemicals and materials suppliers as well as OEMs to pay for more of the R&D in larger segments such as LCD and semiconductors

• The operating margins of many value chain participants are below that required for reinvestment

• Chemical and materials suppliers need to chose their shots and development activities very carefully

LINX CONSULTING SEE BEYOND THE HORIZON 33