Embed Size (px)

Citation preview

Mikhail Reider-Gordon, Managing Director, Capstone Advisory Group LLC

Alan Granwell, Partner, International Tax, DLA Piper

Bruce Zagaris, Partner, Berliner, Corcoran + Rowe LLP

James Dowling, President/Managing Director, Dowling Advisory GroupJanuary 27, 2011

WEBINARUNDERSTANDING OFFSHORE TAX HAVENS

Presented by:

If you cannot hear us speaking, please make sure you have called the teleconference number on your invitation.Toll Free: +1 800.735.5968

Toll: +1 212.231.2920The audio portion is available via conference call. It is not broadcast through your computer.

JUST WHAT DO THEY KNOW?EXCHANGE OF INFORMATION BETWEEN TAX AUTHORITIES

January 27, 2011

Alan Winston Granwell

This power point presentation is offered for informational purposes only and

and the content should not be construed as legal advice on any matter.

January 27, 2011 3

Tax Transparency and Exchange of Information – Introduction

� Industrialized and developing countries have heightened their scrutiny of offshore financial centers and the use of offshore accounts in efforts to recoup tax revenues from taxpayers improperly using offshore financial centers.

� 2009-2010 saw a dramatic expansion of exchange of information agreements, particularly with offshore jurisdictions.

� Administrations are moving beyond standard forms of exchange of information (automatic, on request, spontaneous) to other types of sharing of information.

January 27, 2011 4

Why Now?

� Today’s increasingly borderless world.

� Growth in international transactions.

� Increased complexity of transactions and tax laws.

� Recent international tax evasion scandals put the spotlight on improving international compliance.

� Economic crisis: ensuring compliance by all taxpayers and collecting all tax legally due.

January 27, 2011 5

2009-2010 Revolution in Tax Cooperation

� Tax transparency was a key feature of the G20 Summit. In London, the G20 leaders stated that:“We agree to take action against non-cooperative jurisdictions, including tax havens. We stand ready to deploy sanctions to protect our public finances and financial systems. The era of bank secrecy is over. We note that the OECD has today published a list of countries assessed by the Global Forum against the international standard for exchange of information.”

� In Pittsburg (September 2009), the G20 Leaders underscored the need for quick progress, stating that they “stand ready to use countermeasures”against jurisdictions that do not adopt the OECD Standard.

� In 2009, more progress toward full effective exchange of information was made than in the past decade.

� In the run up to the G20 summit held in London on 2 April 2009, the standards on transparency and exchange of information developed by the OECD (the OECD Standard) were endorsed by all key players, including jurisdictions that had so far been opposed to exchange of information.

January 27, 2011 6

2009-2010 Revolution in Tax Cooperation

� The OECD Standard has been universally endorsed.

� All OECD countries accept the OECD Standard, with the withdrawalof opposition to the reservation by Austria, Belgium, Luxembourg and Switzerland.

� Andorra, Liechtenstein and Monaco, the three non-cooperative tax havens, that previously refused to endorse the standard now agree to the OECD Standard.

� Costa Rica, Malaysia, Philippines and Uruguay, the four Global Form Jurisdictions that had not previously committed to implement theOECD Standard, have now committed to the standard.

� All non-OECD countries that previously expressed a reservation to the OECD Standard have withdrawn their reservation, including Brazil, Chile and Thailand.

January 27, 2011 7

2009-2010 Revolution in Tax Cooperation

� The UN has endorsed the standard.

� To date, well over 500 agreements have been signed by jurisdictions which were identified by the OECD as not substantially implementing the standard in the progress report published on 2 April in conjunction of the G20. Signing agreements is a necessary step towards full implementation of the standard.

� Austria, Andorra, The Bahamas, Chile, Costa Rica, Guatemala, Hong Kong, Liechtenstein, Macao, Malaysia, Panama, the Philippines, San Marino and Singapore have adopted (or are in the process of adopting) legislation to allow them to meet the OECD Standard.

� Brazil and Indonesia, have since joined the Global Forum and have provided detailed information on their treaty networks. Both jurisdictions have demonstrated that they have substantially implemented the OECD Standard.

January 27, 2011 8

2009 Revolution in Tax Cooperation

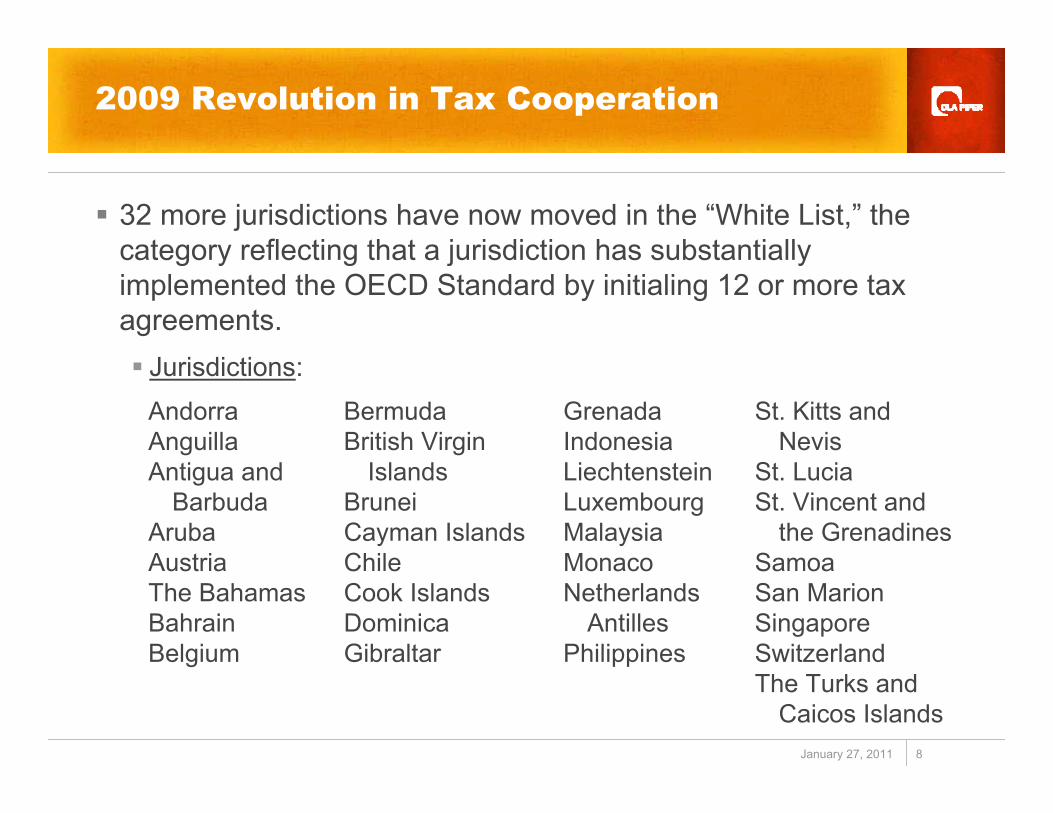

� 32 more jurisdictions have now moved in the “White List,” the category reflecting that a jurisdiction has substantially implemented the OECD Standard by initialing 12 or more tax agreements.� Jurisdictions:

AndorraAnguillaAntigua and

BarbudaArubaAustriaThe BahamasBahrainBelgium

BermudaBritish Virgin

IslandsBruneiCayman IslandsChileCook IslandsDominicaGibraltar

GrenadaIndonesiaLiechtensteinLuxembourgMalaysiaMonacoNetherlands

AntillesPhilippines

St. Kitts and Nevis

St. LuciaSt. Vincent and

the GrenadinesSamoaSan MarionSingaporeSwitzerlandThe Turks and

Caicos Islands

January 27, 2011 9

2009–2010 YEARS OF THE G20:IMPACT ON IMPLEMENTATION

January 27, 2011 10

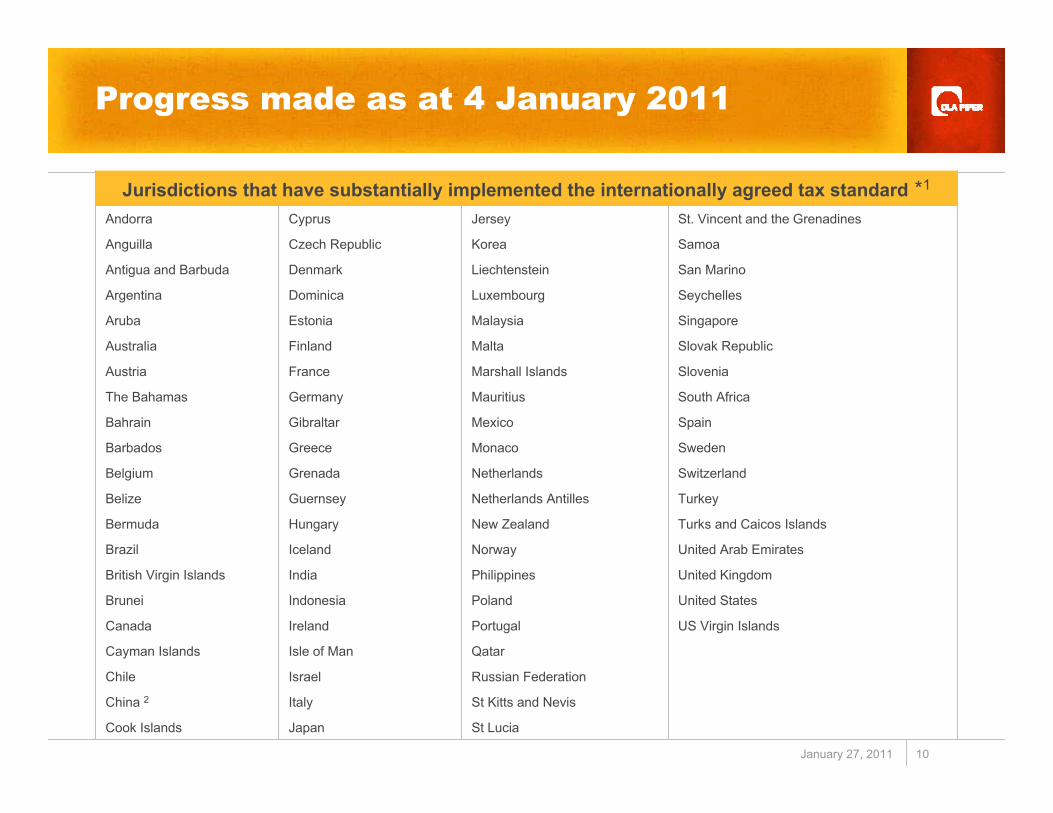

Progress made as at 4 January 2011

St LuciaJapanCook Islands

St Kitts and NevisItalyChina 2Russian FederationIsraelChile

QatarIsle of ManCayman Islands

US Virgin IslandsPortugalIrelandCanada

United StatesPolandIndonesiaBrunei

United KingdomPhilippinesIndiaBritish Virgin Islands

United Arab EmiratesNorwayIcelandBrazil

Turks and Caicos IslandsNew ZealandHungaryBermuda

TurkeyNetherlands AntillesGuernseyBelize

SwitzerlandNetherlandsGrenadaBelgium

Barbados

Bahrain

The Bahamas

Austria

Australia

Aruba

Argentina

Antigua and Barbuda

Anguilla

Andorra

SwedenMonacoGreece

SpainMexicoGibraltar

South AfricaMauritiusGermany

SloveniaMarshall IslandsFrance

Slovak RepublicMaltaFinland

SingaporeMalaysiaEstonia

SeychellesLuxembourgDominica

San MarinoLiechtensteinDenmark

SamoaKoreaCzech Republic

St. Vincent and the GrenadinesJerseyCyprus

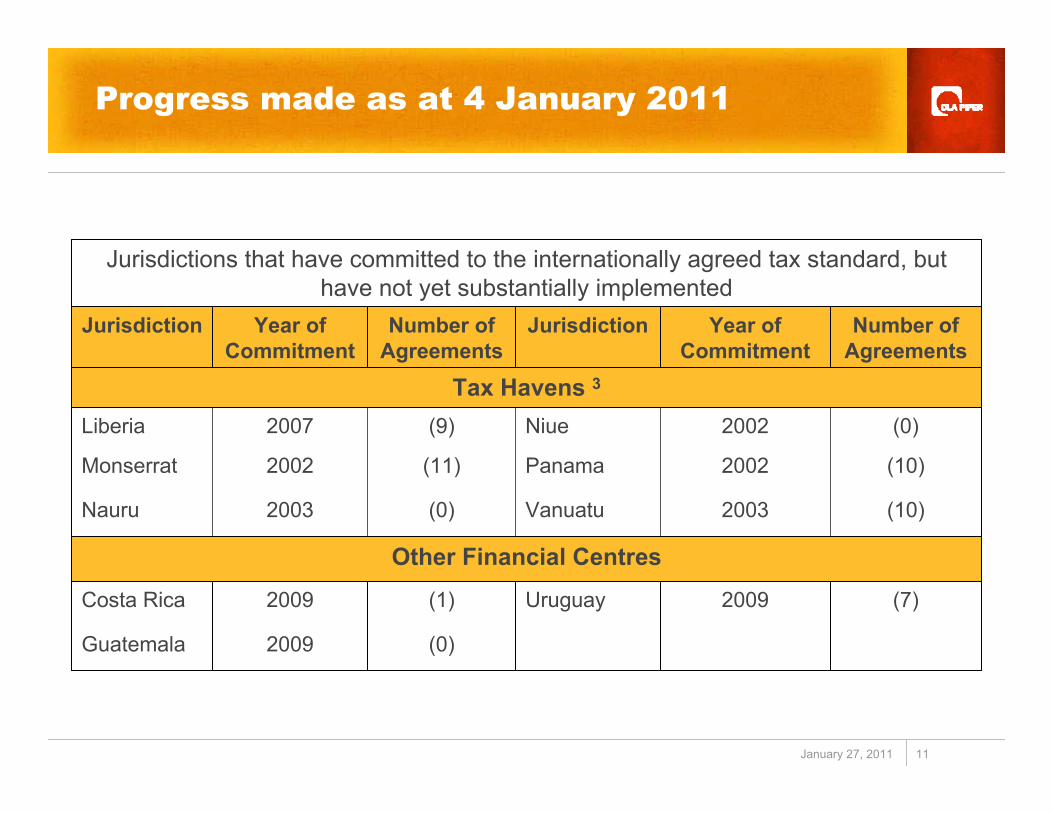

Jurisdictions that have substantially implemented the internationally agreed tax standard *1

January 27, 2011 11

Progress made as at 4 January 2011

(0)2009Guatemala

(7)2009Uruguay(1)2009Costa Rica

Other Financial Centres

(10)2003Vanuatu(0)2003Nauru

(10)2002Panama(11)2002Monserrat

(0)2002Niue(9)2007Liberia

Tax Havens 3

Number of Agreements

Year of Commitment

JurisdictionNumber of Agreements

Year of Commitment

Jurisdiction

Jurisdictions that have committed to the internationally agreed tax standard, but have not yet substantially implemented

January 27, 2011 12

The Global Forum

� The Global Forum brings together jurisdictions, both OECD and non-OECD, that have made commitments to transparency and exchange of information and have worked together to develop the OECD Standard in tax matters.

� The Global Forum was established in 2000 to provide a global andinclusive forum for cooperation on issues of transparency and information exchange and currently has 95 members. New participants are being invited to join, from both the developed and the developing world.

� Since 2006, the Global Forum has published annual assessments ofthe legal and administrative framework for transparency and exchange of information in over 80 countries.

� The Global Forum survey covers OECD countries, countries that participate in the OECD’s Committee on Fiscal Affairs as “Observer”countries (Argentina, China, Russia, South Africa), jurisdictions that meet the tax haven criteria and other financial centers.

January 27, 2011 13

The Global Forum

� The principle that has guided the Global Forum’s work is that all jurisdictions, regardless of their tax systems, should meet the OECD Standard so that competition takes place on the basis of legitimate commercial considerations rather than the basis of lack of transparency or lack of effective exchange of information for tax purposes.

� Political attention to the Global Forum’s work, and the urgency of ensuring that high standards of transparency and exchange of information are in place around the work made it imperative to review the Global Forum’s structure and mandate.

January 27, 2011 14

Global Forum Mandate

� An initial 3-year mandate to create a strengthened Global Forum to promote rapid and consistent implementation of the standards through a robust and comprehensive peer review process.

� Peer-based two-phase reviews. � Phase 1 is a review of each jurisdiction’s legal and regulatory framework

for transparency and the exchange of information for tax purposes.

� Phase 2 involves a survey of the practical implementation of the standards.

� In-depth ongoing monitoring of legal instruments which allow for exchange of information. This is necessary to monitor that agreements enter into force and are effectively implemented.

� Review process to be overseen by a Peer Review Group, made up of30 Global Forum members.

January 27, 2011 15

Global Forum Peer Reviews

� Peer reviews commenced in March 2010. All jurisdictions will undergo Phase 1 reviews before June 2012 and all Phase 2 reviews should be completed before June 2014.

� A schedule of reviews has been published and the outcome of the reviews will be published once they are adopted by the Global Forum.

� A system of on-going monitoring has been put in place to ensure that developments that occur after a review is complete are acknowledged, and to ensure that the most complete and up-to-date information about all the jurisdictions covered by the Global Forum’s work is available to the public, and also to include a database of information concerning transparency and exchange of information on the Global Forum website.

January 27, 2011 16

The OECD Standard

� The OECD Standard was developed in 2002 by the OECD in co-operation with non-OECD countries, and was endorsed by G20 Finance Ministers at their Berlin Meeting in 2004, by the UN Committee of Experts on International Cooperation in Tax Matters at its October 2008 Meeting and by all members of the Global Forum.

� The OECD Standard imposes an obligation to exchange all types ofinformation foreseeably relevant to the administration and enforcement of the requesting country's domestic tax laws, including information on companies, trusts and their owners and beneficiaries.

� The OECD Standard can be implemented through:� Bilateral tax treaties;� Tax Information Exchange Agreements (TIEAs);� Multilateral Agreements; or� Domestic legislation allowing for the provision of information on a

unilateral basis.

January 27, 2011 17

OECD StandardElements

� The OECD Standard requires:� Exchange of information on request where “foreseeably relevant”

to administration or enforcement of all tax matters of the treaty partner.

� Without regard to a domestic tax interest, bank secrecy, or dualcriminality.

� Availability of reliable information and powers to obtain it.

� Respect of taxpayer’s rights.

� Strict confidentiality of information exchanged.

January 27, 2011 18

OECD StandardKey Principles

� Existence of mechanisms for exchange of information upon request.

� Exchange of information in both criminal and civil matters.

� No restrictions of information exchange caused by application of dual criminality principle or domestic tax interest requirement.

� Respect for safeguards and limitations.

� Strict confidentiality rules for information exchanges.

� Availability of reliable information (in particular, bank, ownership identity and accounting information) and powers to obtain and provide such information in response to a specific request.

January 27, 2011 19

International Cooperation

� OECD Forum on Tax Administration (FTA).

� Joint International Tax Shelter Information Center (JITSIC).

� OECD Aggressive Tax Planning Directory.

� Joint Audits.

January 27, 2011 20

OECD’s Forum on Tax Administration (FTA)

� The FTA was established by the OECD’s Committee on Fiscal Affairs in 2002, and brings together tax commissioners from over 40 countries to promote cooperation between revenue bodies and to develop good tax administration practices.

� The FTA will assist cooperation by tax authorities to identify tax evasion and tax avoidance schemes by focusing on:� Offshore compliance.

� Financial institutions.

� High net worth individuals.

� IRS Commissioner Shulman is the current chair of the FTA.

January 27, 2011 21

JITSIC

� JITSIC established in 2004 by Australia, Canada, UK and US to supplement ongoing work of tax administrations in identifying and curbing abusive tax avoidance transactions, arrangements and schemes. Japan joined in 2007.

� Purpose of JITSIC is to � provide support to the parties through identification and understanding of

abusive tax schemes and those who promote them;

� share expertise, best practices and experience in tax administration to combat abusive tax schemes;

� exchange information on abusive tax schemes, their promoters and investors consistent with the provisions of bilateral tax conventions; and

� enable the parties to better address abusive tax schemes promoted by firms and individuals who operate without regard to national borders.

January 27, 2011 22

Joint Audits

� Forum Tax Administration study

� Bilateral or multilateral treaties (e.g., Convention on Mutual Administrative Assistance in Tax Matters) provide legal framework for such audits. � The Global Forum updated this agreement, which is a powerful

tool to counter offshore non-compliance open to all countries.

January 27, 2011 23

Data Stolen from Private Banks and Use of that Data

� There have been at least three well-publicized incidents where a bank employee stole data and sold it to tax authorities; one involving Liechtenstein and the other two in Switzerland.

January 27, 2011 24

Whistleblower Disclosure

� On January 17, 2011, The WikiLeaks announcement today that it plans to release information on more than 2,000 international bank accounts threatens to provide the IRS and other tax authorities with the names of persons with undeclared foreign accounts.

� The data was provided by a former chief operating officer who managed the Caribbean operations of a prominent Swiss private bank.

� This data to significant ramifications for undeclared account holders whose names will soon become public.

January 27, 2011 25

United StatesEfforts to Combat Global Tax Evasion

� 2009 was a turning point in efforts to curb global tax evasion.

� Global tax evasion continues to be high on the political agenda, and is a priority for the Internal Revenue Service (IRS)and the US Department of Justice (DOJ).

� The United States was extremely active in the area of international tax enforcement this past year.

� The Commissioner of the IRS has testified that international tax issues are a major priority and that the IRS needs additional resources, information (from foreign countries and financial institutions) and regulatory and legislative changes (all of which are in process or have been implemented).

January 27, 2011 26

Efforts of the IRS and DOJ to Combat Global Tax Evasion

� The IRS currently uses multiple methods to detect non-compliant taxpayers using offshore accounts or tax haven entities. These include: � International collaboration through the exchange of information

provisions of bilateral tax agreements and cooperative information agreements that the US has entered into with over 70 countries;

� The qualified intermediary ("QI") program that the IRS has with foreign financial institutions that agree to become QIs;

� Criminal investigations in collaboration with the DOJ;

� The "whistleblower" program through which the IRS receives many tips; and

� The "John Doe" summons authority, which the IRS uses when it strongly suspects U.S. taxpayers are using offshore bank accounts to avoid paying taxes, but does not know their identities.

January 27, 2011 27

2009-2011 Changes in the Enforcement Landscape

� Deferred Prosecution Agreement and John Doe Summons with Respect to a Well Known Swiss Financial Institution.

� Criminal Prosecution of Bankers, Account Holders and Others.

� Voluntary Disclosure Initiatives/Focus on Foreign Bank Account Reports (a new initiative may be proposed soon).

� Enhanced Whistleblower Incentives.

� Increased Cooperation by G-20 & Others (noted above).

� New IRS Offices Offshore.

� Additional Dedicated Resources.

� Proposed Regulations on Reporting of Bank Interest by US Banks.

� Foreign Account Tax Compliance Act.

January 27, 2011 28

Dedicated Resources Added

� The Criminal Investigation Division (CID) has offices in 11 countries.

� The IRS has opened new CID Offices in Beijing, Panama City and Sydney.

� CID employs 4,200 workers worldwide, of whom 2,700 are special agents with police authority.

� The President's budget would provide funds to add nearly 800 new IRS employees to combat offshore tax evasion and improve US tax compliance.

� CID Agents specially dedicated to international compliance.

January 27, 2011 29

Dedicated Resources Added

� International Agents on West Coast to Focus on Pacific Rim Activities.

� IRS Global High Wealth Industry Group� Will centralize and focus IRS compliance expertise involving high wealth

individuals and their related entities. � The purpose of the group is to build new risk assessment techniques to

identify high wealth individuals and their related enterprises that should be reviewed holistically.

� The IRS has started to hire revenue agents, flow-through specialists and international examiners to conduct reviews to "get the entire picture.“� Currently, the group has 100 staff members; examining 250 enterprises, with 40

under audit.

� DOJ to Lead Inter-Agency Team to Review SARS Regarding Foreign Activity.

� Hiring of New Prosecutors.

January 27, 2011 30

Introduction

� Section 501 of the HIRE Act (new Chapter 4 of the Code) is sometimes described as the “centerpiece” of the FATCA provisions of the Act.

� FATCA provides for a new withholding regime aimed at expanding reporting on foreign accounts owned by certain U.S. persons and disclosure of U.S. owners of certain foreign entities.

January 27, 2011 31

Reasons for Legislation

� The legislation is a direct result of the focus by the United States on combating offshore tax evasion and recouping much needed tax revenues.

� The legislation (and earlier versions) was proposed to remedy perceived deficiencies in the current methods used by the IRS and the U.S. Department of Justice (“DOJ”) to identify U.S. persons who utilize foreign financial accounts or foreign entities and thereby provide more information to the IRS to enforce compliance.

January 27, 2011 32

Chapter 4 of the Code

� Chapter 4 of the Internal Revenue Code imposes new compliance burdens on foreign financial institutions and other foreign entities, requiring them to identify and disclose U.S. account holders and investors or be subject to a new 30 percent U.S. withholding tax under a new U.S. withholding tax regime on any payment of U.S. source investment income and proceeds from the sale of equity or debt instruments of U.S. issuers (“New U.S. Withholding Tax Regime”).

January 27, 2011 33

Ultimate Objective

� The ultimate goal of Chapter 4 is for the United States to obtain information with respect to offshore accounts and investments beneficially owned by U.S. taxpayers, in an efficient and timely manner, rather than have the New U.S. Withholding Tax regime imposed.

January 27, 2011 34

Effective Date

� Payments made after December 31, 2012.

� Grandfathered Treatment of Outstanding Obligations.� Any payment under any obligation outstanding on date which is

two years after date of enactment of the Act (March 18, 2010) orgross proceeds from disposition of such obligation.

January 27, 2011 35

IRS Authority toPromulgate Regulations

� During this interim period, the IRS, pursuant to a wide grant ofregulatory authority, will draft regulations to implement the new provisions.

� In drafting its guidance, it is understood that the IRS will endeavor: � To construct a workable information reporting and withholding system that

can be effectively implemented and utilized by foreign reporting entities;� To obtain information consistent with the purposes of the legislation; and� In a manner that will not discourage or disrupt foreign investment in U.S.

capital markets.

� In Announcement 2010-22, the IRS has requested comments on future guidance concerning the interpretation and implementation of the new law.

� In Notice 2010-60, the IRS provided preliminary guidance on selected issues.

January 27, 2011 36

Withholdable Payments toForeign Financial Institutions

� Entities Covered. Section 1471 applies to foreign financial institutions (FFIs) (except as otherwise provided by the Secretary; a financial institution organized under the laws of aU.S. possession is not an FFI).

� Except as otherwise provided by the Secretary, an FFI is any entity that is not a United States person and: � Accepts deposits in the ordinary course of a banking or similar

business;

� As a substantial portion of its business, holds financial assets for the account of others; or

� Is engaged (or holds itself out to be engaged) primarily in the business of investing, reinvesting or trading in securities, partnership interests, commodities or other interests, includingderivatives (Foreign Investment Vehicle).

January 27, 2011 37

Withholdable Payments toForeign Financial Institutions

� Accounts Subject to Reporting Requirements. In order for an account to be subject to these rules, it must constitute a financial account that is held by one or more specified U.S. persons or U.S. owned foreign entities (a “U.S. Account”). � Financial Account. This term, except as otherwise provided by the

Secretary, means with respect to an FFI: � Any depository account maintained by the FFI;� Any custodial account maintained by the FFI; and� Any debt or equity interest in an FFI that is not regularly traded on an

established securities market.� Specified U.S. Person. Generally a U.S. non-exempt recipient

(individual, trust, partnership or estate) and a privately held U.S. corporation.

� U.S. Owned Foreign Entity. A foreign entity that has Substantial U.S. Owners:� Corporation, partnership or trust where specified U.S. person owns a greater

than 10-percent interest, directly or indirectly.� Foreign investment vehicles. 10 percent is reduced to 0 percent.

January 27, 2011 38

Withholdable Payments toForeign Financial Institutions

� Withholdable Payment. A Withholdable Payment, except as otherwise provided by the Secretary, means:� Any payment of interest (including any original issue discount), dividends,

rents, salaries, wages, premiums, annuities, compensation, remunerations, emoluments and other fixed or determinable annual or periodical gains, profits and income from sources within the United States;

� Interest paid on deposits by foreign branches of domestic banks (861(a)(1)(B) does not apply for this purpose); and

� Gross proceeds from the sale or other disposition of property which can produce U.S. source dividends or interest.

� Rate of Withholding: 30 percent.� Exceptions:

� Effectively connected income.� To the extent provided in regulations, certain payments made with respect

to short-term debt or short-term deposits (including gross proceeds), may be excluded.

January 27, 2011 39

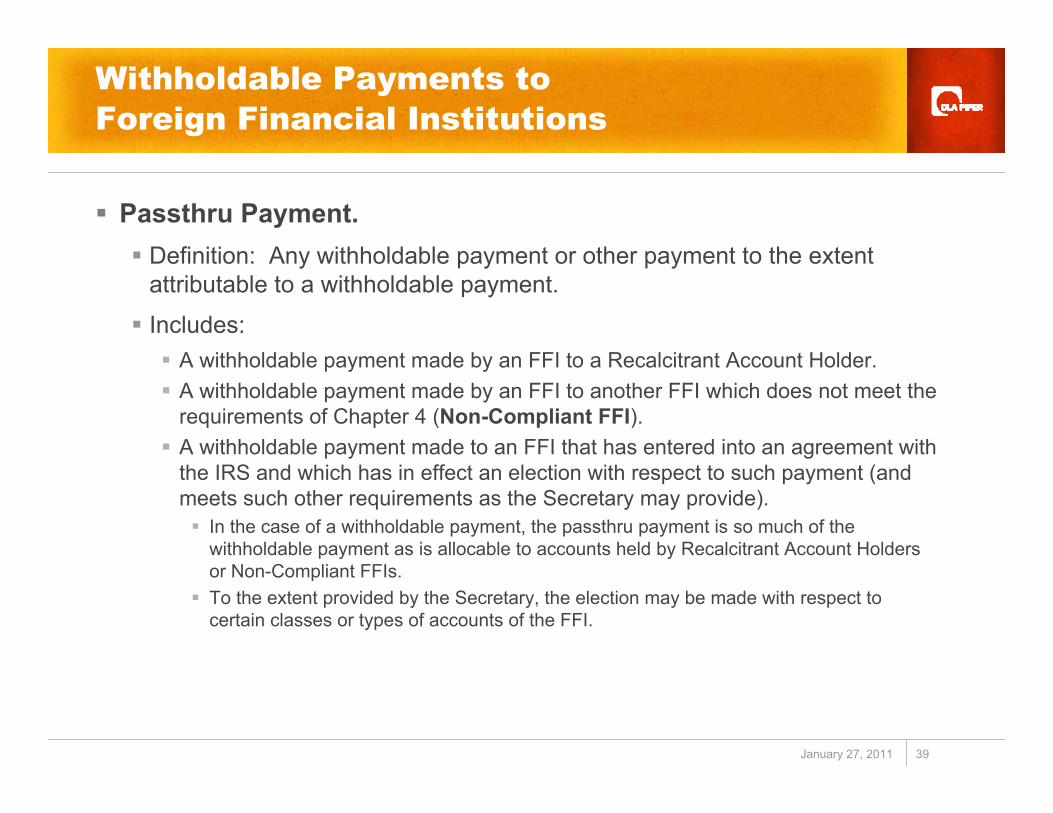

Withholdable Payments toForeign Financial Institutions

� Passthru Payment.� Definition: Any withholdable payment or other payment to the extent

attributable to a withholdable payment.

� Includes:� A withholdable payment made by an FFI to a Recalcitrant Account Holder.� A withholdable payment made by an FFI to another FFI which does not meet the

requirements of Chapter 4 (Non-Compliant FFI).� A withholdable payment made to an FFI that has entered into an agreement with

the IRS and which has in effect an election with respect to such payment (and meets such other requirements as the Secretary may provide).� In the case of a withholdable payment, the passthru payment is so much of the

withholdable payment as is allocable to accounts held by Recalcitrant Account Holders or Non-Compliant FFIs.

� To the extent provided by the Secretary, the election may be made with respect to certain classes or types of accounts of the FFI.

January 27, 2011 40

Withholdable Payments toForeign Financial Institutions

� Recalcitrant Account Holders and Non-Compliant FFIs.� To deal with situations where an FFI has a Recalcitrant Account

Holder or an FFI that does not meet the IRS agreement requirements, the statute provides certain rules: � Recalcitrant Account Holder. An account holder that fails to comply

with reasonable requests for information pursuant to IRS mandated verification, and due diligence procedures to identify U.S. Accounts, to provide a name, address and TIN or fails to provide a bank secrecy waiver upon request.

� Under the general rule, an FFI that makes a payment to a Recalcitrant Account Holder or a Non-Compliant FFI, is required to withhold 30 percent of the gross amount of such payment.

January 27, 2011 41

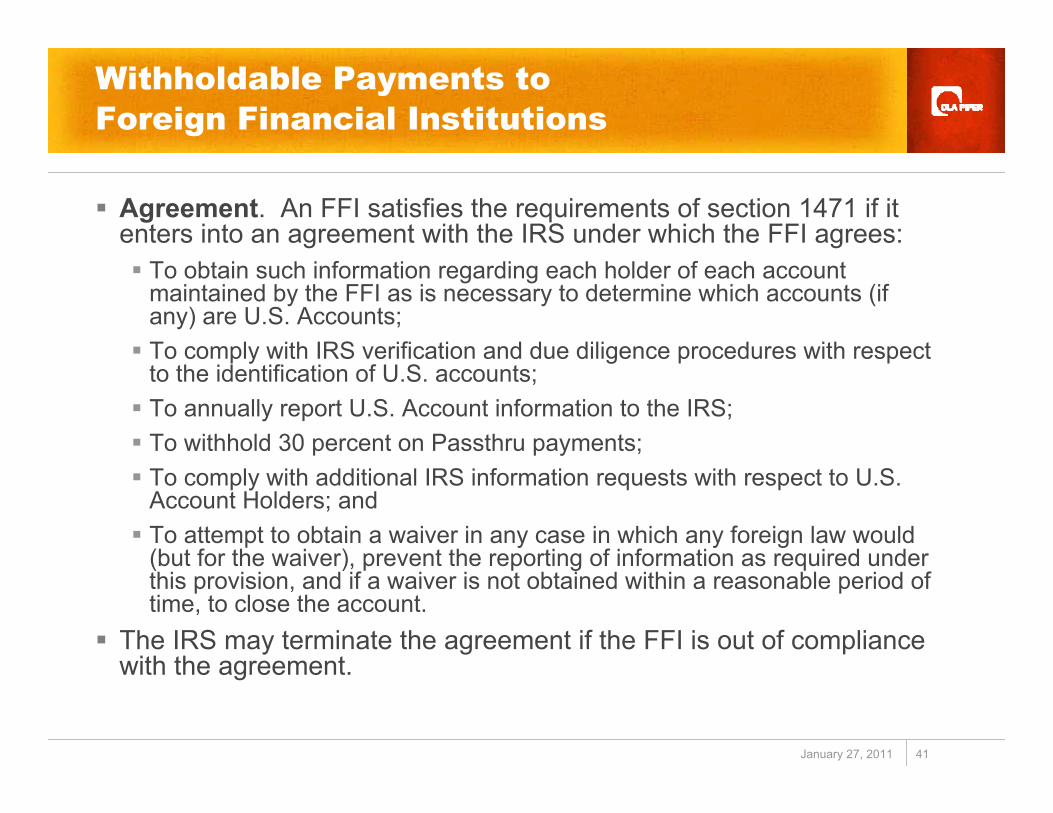

Withholdable Payments toForeign Financial Institutions

� Agreement. An FFI satisfies the requirements of section 1471 if it enters into an agreement with the IRS under which the FFI agrees: � To obtain such information regarding each holder of each account

maintained by the FFI as is necessary to determine which accounts (if any) are U.S. Accounts;

� To comply with IRS verification and due diligence procedures with respect to the identification of U.S. accounts;

� To annually report U.S. Account information to the IRS; � To withhold 30 percent on Passthru payments; � To comply with additional IRS information requests with respect to U.S.

Account Holders; and � To attempt to obtain a waiver in any case in which any foreign law would

(but for the waiver), prevent the reporting of information as required under this provision, and if a waiver is not obtained within a reasonable period of time, to close the account.

� The IRS may terminate the agreement if the FFI is out of compliance with the agreement.

January 27, 2011 42

Withholdable Payments toForeign Financial Institutions

� Certain FFIs Deemed to Meet Reporting Requirements.� The statute provides two procedures for FFIs to avoid having to

enter into an IRS agreement because, for example, the FFI may not have U.S. Accounts:� The first way is if the FFI complies with such procedures as the IRS

may prescribe, to ensure that the FFI does not maintain U.S. Accounts, and the FFI meets such other requirements as the IRS may prescribe, with respect to accounts of other FFIs maintained by the first FFI.

� The second way is if the FFI is a member of a class of institutions with respect to which the IRS has determined that the application of the agreement/withholding provisions is not necessary.

January 27, 2011 43

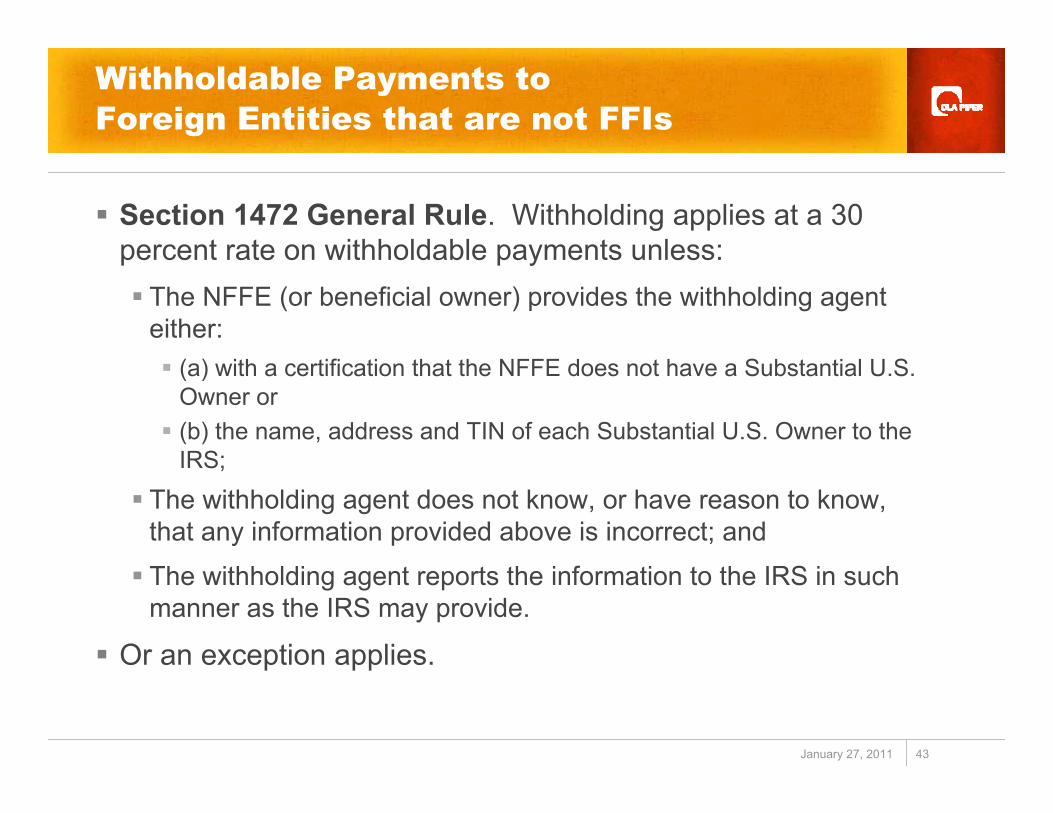

Withholdable Payments toForeign Entities that are not FFIs

� Section 1472 General Rule. Withholding applies at a 30 percent rate on withholdable payments unless:� The NFFE (or beneficial owner) provides the withholding agent

either:� (a) with a certification that the NFFE does not have a Substantial U.S.

Owner or � (b) the name, address and TIN of each Substantial U.S. Owner to the

IRS;

� The withholding agent does not know, or have reason to know, that any information provided above is incorrect; and

� The withholding agent reports the information to the IRS in suchmanner as the IRS may provide.

� Or an exception applies.

January 27, 2011 44

Alan Winston Granwell

Alan Granwell has practiced in the area of international taxation for 40 years. He represents US multinational groups and US high-net worth individuals investing or conducting business abroad, and foreign multinational groups and foreign high net-worth individuals investing or conducting business in the United States.

From 1981 through 1984, Mr. Granwell was the International Tax Counsel and Director, Office of International Tax Affairs atthe US Department of the Treasury. In that capacity, Mr. Granwell was the senior international tax advisor at the Treasury Department and was responsible for advising the Assistant Secretary for Tax Policy on legislation, regulations, and administrative matters involving international taxation and directing the US tax treaty program.

T. +1 202.378.0344E. [email protected]

January 27, 2011 45

Circular 230 Notice

In compliance with U.S. Treasury Regulations, please be advised that any tax advice given herein (or in any attachment) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax penalties or (ii) promoting, marketing or recommending to another person any transaction or matter addressed herein.

January�27,�2011 46

OFFSHORE�TAX�HAVEN�WEBCAST

TAX�HAVENS:�THE�INTERPLAY�BETWEEN�TAX�AND�MONEY�

LAUNDERING

46

Association�of�Certified�Anti�Money�Laundering�SpecialistsWebcast�on�Off�Shore�Tax�Havens

January�27,�2011

Bruce�Zagaris © 2011Berliner,�Corcoran�&�Rowe,�LLP1101�17th St.�NW�Suite�1100Washington�DC,�20036(202)�293�2371bzagaris@bcr�dc.com© 2011

This�presentation�is�a�reprint�from�the�ALI�ABA�International�Trust�and�Estate�Planning�

Course�of�StudyAugust�19,2010

The information in these slides reflects the views of the presenter and do not reflect the views of DLA Piper.

January�27,�2011 47

I.�Overview�of�Slides*

• Limits�on�Bank�Secrecy

• Implementation�of�Gatekeeper�Standards

• US�Legislative�Initiatives

• Other�US�Legislative�Initiatives

• Initiatives�of�Int’l�Organizations

• Extradition

• Analysis�and�the�Way�Forward

47

January�27,�2011 48

II.�Limits�on�Bank�Secrecy

• Limits�from�Soft�Law�(FATF &�OECD)

• International�Enforcement�Conventions

• SOX�and�QI Regime• June�10,�2010–Swiss�

Parliament�Approves�US�Swiss�Agreement�on�UBS

• Whistleblowers�&�Wikileaks

• Governments�Encourage�Whistleblowing

48

January�27,�2011 49

II.�Limits�on�Bank�Secrecy�(2)

• The�US�Panama�TIEA illustrates�the�limits�to�bank�and�financial�confidentiality.

• To�a�large�extent�the�Panama�financial�services�sector�has�attracted�investors�through�offering�them�confidentiality,�including�the�use�of�bearer�shares.

• Even�the�US�Panama�MLAT was�limited�in�terms�of�the�scope�of�assistance.

49

January�27,�2011 50

II.�Limits�on�Bank�Secrecy�(3)

• On�November�30,�2010,�the�United�States�and�Panama�signed�a�new�tax�information�exchange�agreement�(TIEA)�that�would�allow�for�access�to�information�about�Panamanian�bank�accounts�and�information�on�bearer�shares�for�the�first�time.�

• The�TIEA has�enormous�significance�because�Panama�is�the�most�important�entry�point�for�capital�from�Latin�America�into�the�U.S.�and�Panama�has�long�resisted�signing�a�TIEA due�to�its�strong�international�financial�sector,�which�has�been�based�in�part�on�strong�bank�and�financial�confidentiality.

50

January�27,�2011 51

II.�Limits�on�Bank�Secrecy�(4)

• The�agreement�allows�the�United�States�and�Panama�to�seek�information�from�each�other�on�all�types�of�national�taxes�in�both�civil�and�criminal�matters�for�tax�years�beginning�on�or�after�November�30,�2007.

• According�to�a�joint�declaration�between�the�two�countries,�the�TIEA will�take�effect�“as�soon�as�practicable” after�Panama�passes�implementing�legislation.

51

January�27,�2011 52

II.�Limits�on�Bank�Secrecy�(5)

• The�diplomatic�note�to�the�convention�states�that�Panama�expectsto�enact�implementing�legislation�before�the�end�of�2011.

• According�to�the�diplomatic�note�Panama�intends�that�the�legislation�would�require�the�identification�of�bearer�shares.

• Resident�agents�acting�for�Panamanian�entities�would�have�to�obtain�and�retain�in�their�records�sufficient�information�to�identify�those�entities,�including,�where�the�owner�is�a�legal�person,�information�sufficient�to�identify�substantial�owners�of�that�legal�person.��

• However,�a�resident�agent�will�not�be�required�to�obtain�and�maintain�information�sufficient�to�identify�substantial�owners�of�legal�persons�in�cases�where�the�resident�agent�acts�for�a�professional�client�that�is�part�of�an�organization�that�is�required�to�maintain�information�on�such�entities�and�that�has�agreed�to�make�such�information�available�to�the�resident�agent�when�requested.

52

January�27,�2011 53

II.�Limits�on�Bank�Secrecy�(6)

• Under�the�contemplated�legislation,�agents�will�have�to�produce�ownership�and�client�identity�information�in�response�to�a�proper�request�under�the�TIEA,�regardless�of�whether�the�entity�is�newly�formed�or�already�existing�at�the�time�the�legislation�is�enacted,�the�declaration�said.�

• The�agents�must�produce�ownership�and�client�identity�information�in�their�possession�in�response�to�a�proper�request�under�the�Agreement,�whether�with�respect�to�newly�formed�entities�or�entities�in�existence�at�the�time�the�legislation�is�enacted

53

January�27,�2011 54

II.�Limits�on�Bank�Secrecy�(7)

• With�respect�to�already�existing�entities,�ownership�information�would�have�to�be�obtained�within�a�five�year�period�from�the�date�of�enactment.

• The�TIEA itself�provides�for�the�exchange�of�information,�through�competent�authorities,�“that�may�be�relevant�to�the�administration�and�enforcement�of�the�domestic�laws�of�the�parties�concerning�the�taxes�covered�by�this�agreement.”

• This�includes�information�relevant�to�determining,�assessing,�enforcing,�or�collecting�tax,�as�well�as�to�the�investigation�or�prosecution�of�criminal�tax�matters.

54

January�27,�2011 55

II.�Limits�on�Bank�Secrecy�(8)

• The�TIEA applies�to�all�U.S.�federal�taxes,�including�income�taxes,�taxes�related�to�employment,�estate�and�gift�taxes�and�excise�taxes.�

• The�TIEA does�not�apply�to�taxes�imposed�by�states,�municipalities,�or�other�political�subdivisions,�or�possessions�of�a�party.��

• For�Panama�the�TIEA applies�to�income�tax,�real�estate�tax,�vessels�tax,�stamp�tax,�notice�of�operations�tax,�tax�on�banks,�financial�and�currency�exchange�companies,�insurance�tax,�tax�on�the�consumption�of�fuel�and�oil�derivatives,�tax�on�the�transfer�of�movable�goods�and�the�provision�of�services

55

January�27,�2011 56

II.�Limits�on�Bank�Secrecy�(9)

• The�agreement�requires�that�requests�for�information�can�only�be�made�when�the�requesting�Party�is�not�able�to�obtain�the�requested�information�by�other�means,�“except�where�recourse�to�such�means�would�give�rise�to�disproportionate�difficulty.”

• Privileges�under�the�laws�and�practices�of�the�requesting�Party�will�not�apply�in�the�execution�of�a�request�by�the�requested�Party�and�these�matters�must�be�reserved�for�resolution�of�the�requesting�Party.

56

January�27,�2011 57

II.�Limits�on�Bank�Secrecy�(10)

• Any�request�for�information�must�be�made�with�the�greatest�degree�of�specificity�as�possible,�and�in�all�cases�must�specify,�in�writing,�the�taxpayer's�identity,�the�period�of�time�for�which�information�is�requested,�the�nature�of�the�information�requested�and�the�form�in�which�the�requesting�party�would�prefer�to�receive�it,�and�reasons�for�believing�the�information�requested�(1)�is�relevant�to�tax�administration�or�enforcement,�and�(2)�is�present�or�in�the�possession�or�control�of�a�person�in�the�other�country.��

57

January�27,�2011 58

II.�Limits�on�Bank�Secrecy�(11)

• In�addition,�requests�must�provide�• the�grounds�for�believing�the�information�requested�is�

present�in�the�requested�Part�or�is�in�the�possession�or�control�of�a�person�within�the�jurisdiction�of�the�requested�Party;�

• a�statement�as�to�whether�the�requesting�Party�would�be�able�to�obtain�and�provide�the�requested�information�if�a�similar�request�were�made�by�the�requested�Party;�and�

• a�statement�that�the�requesting�Party�has�pursued�all�reasonable�means�available�in�its�own�territory�to�obtain�the�information,�except�where�that�would�give�rise�to�disproportionate�difficulty

58

January�27,�2011 59

II.�Limits�on�Bank�Secrecy�(12)

• However,�under�the�TIEA,�the�parties�are�not�obligated�to�obtain�or�provide�ownership�information�with�respect�to�publicly�traded�companies�or�public�collective�investment�funds�or�schemes,�“unless�such�information�can�be�obtained�without�giving�rise�to�disproportionate�difficulties.”

59

January�27,�2011 60

II.�Limits�on�Bank�Secrecy�(13)

• Competent�authorities�can�decline�requests�where:�the�request�does�not�conform�to�the�agreement;�the�requesting�party�has�not�pursued�“all�reasonable�means” available�in�its�own�territory�to�obtain�the�information,�except where�recourse�to�such�means�would�cause�disproportionate�difficulty;�and��where�the�disclosure�of�the�information�would�be�contrary�to�the�public�policy�of�the�requested�party

60

January�27,�2011 61

II.�Limits�on�Bank�Secrecy�(14)

• The�Agreement�must�not�impose�on�a�Party�any�obligation:�to�provide�information�that�under�the�laws�of�the�requested�Party�is�subject�to�legal�privilege�or�contains�any�trade,�business,�industrial,�commercial�or�professional�secret�or�trade�process.�

• The�Agreement�does�not�require�a�Party�to�carry�out�administrative�measures�at�variance�with�its�laws�and�administrative�practices.

61

January�27,�2011 62

II.�Limits�on�Bank�Secrecy�(15)

• The�requested�Party�need�to�obtain�and�provide�information�which�the�requesting�Party�would�be�unable�to�obtain�in�similar�circumstances�under�its�own�laws�for�the�purpose�of�the�administration/enforcement�of�its�own�tax�laws�or�in�response�to�a�valid�request�from�the�requested�Party�under�the�Agreement.

62

January�27,�2011 63

II.�Limits�on�Bank�Secrecy�(16)

• The�statute�of�limitations�of�the�requesting�Party�pertaining�to�the�taxes�described�in�the�Agreement�will�govern�a�request�for�information.

• Once�the�TIEA enters�into�force,�it�will�have�effect�for�requests�made�or�after�the�date�of�entry�into�force,�with�regard�to�taxable�periods�beginning�on�or�after�three�years�prior�to�the�signature�of�the�Agreement,�to�which�the�matter�relates.

63

January�27,�2011 64

II.�Limits�on�Bank�Secrecy�(17)

• One�of�the�main�incentives�for�Panama�to�sign�a�TIEA with�the�U.S.�was�its�desire�to�obtain�ratification�by�the�U.S.�of�the�free�trade�agreement,�which�was�blocked�by�the�U.S.�government’s�demand�for�Panama�to�conclude�a�TIEA.��

• This�condition�was�reflected�by�the�remarks�of�the�leaders�of�the�House�Ways�&�Means�Committee�subsequent�to�the�signing�of�the�TIEA.

64

January�27,�2011 65

II.�Limits�on�Bank�Secrecy�(18)

• The�fact�that�the�ratification�of�the�Panama�US�TIEA has�been�delayed�for�three�years�and�the�signing�of�a�TIEA imposed�as�a�condition�to�the�U.S.�ratification�raises�the�question�of�whether�the�U.S.�and�other�countries�(EU�and�its�members)�may�impose�the�condition�of�a�TIEA as�a�prerequisite�to�other�future�trade�and�investment�agreements.

65

January�27,�2011 66

III.�Gatekeeper�Standards

• 2003�Revised�FATF Recommendations

• 2006�– FATF Finds�US�Non�Compliant�with�Gatekeeper�Requirements

• GAO�Report�on�Company�Formations

• FATF Risk�Based�Guidance�for�Lawyers�and�other�Gatekeepers

• ABA�RB Guidance

66

January�27,�2011 67

III.�Gatekeeper�Standards�(2)

• The�U.S.�private�sector�is�caught�between�the�U.S.�leadership�in�the�OECD,�G�20,�and�FATFand�the�pressure�those�orgs/groups�are�exerting�on�the�tax�havens.

• Because�of�the�agreement�in�the�OECD�and�G�20�of�the�need�for�a�level�playing�field,�the�U.S.�needs�to�take�the�same�medicine�it�is�prescribing�for�tax�havens.

67

January�27,�2011 68

III.�Gatekeeper�Standards�(3)

• Some�OECD�members,�such�as�Luxembourg�and�Switzerland,�and�many�members�of�the�OECD’s�Global�Forum,�such�as�the�Channel�Islands,�as�well�as�some�civil�society�groups�and�media,�have�pointed�out�that,�notwithstanding�the�non�compliant�marks�received�by�the�US�from�FATF in�2006�on�the�gatekeeper�standards,�the�U.S.�has�not�acted�satisfactorily�on�the�non�compliant�marks.

68

January�27,�2011 69

III.�Gatekeeper�Standards�(4)

• Interested�members�of�the�US�Congress�and�international�organizations/foreign�governments�are�pressing�the�U.S.�(and�hence�the�ABA)�to�effectively�implement�the�voluntary�guidance��and�show�that�they�are�really�binding.

• It�seems�that�the�next�step�is�for�the�ABA�to�insert�the�guidance�into�the�model�rules�for�professional�conduct,�meaning�that�the�states�will�be�expected�to�adopt�them�and�use�them�to�potentially�discipline�attorneys�violating�them.

69

January�27,�2011 7070

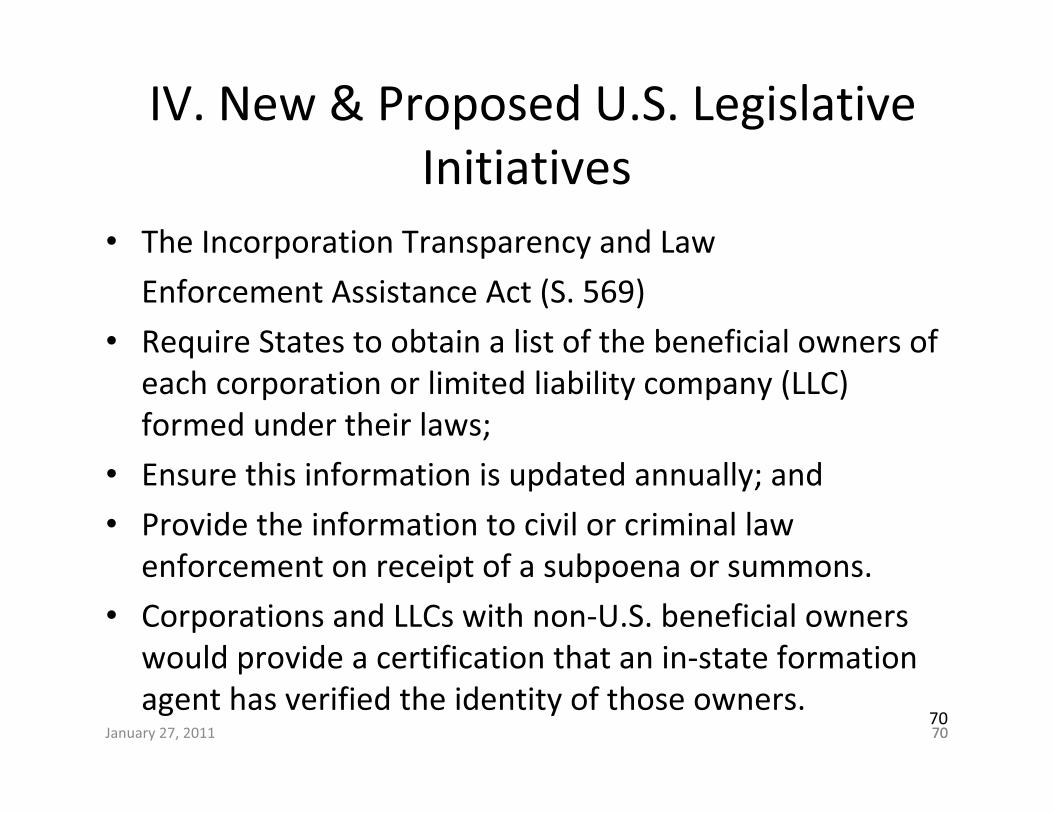

IV.�New�&�Proposed�U.S.�Legislative�Initiatives�

• The�Incorporation�Transparency�and�Law

Enforcement�Assistance�Act�(S.�569)

• Require�States�to�obtain�a�list�of�the�beneficial�owners�of�each�corporation�or�limited�liability�company�(LLC)�formed�under�their�laws;

• Ensure�this�information�is�updated�annually;�and

• Provide�the�information�to�civil�or�criminal�law�enforcement�on�receipt�of�a�subpoena�or�summons.

• Corporations�and�LLCs with�non�U.S.�beneficial�owners�would�provide�a�certification�that�an�in�state�formation�agent�has�verified�the�identity�of�those�owners.

70

January�27,�2011 71

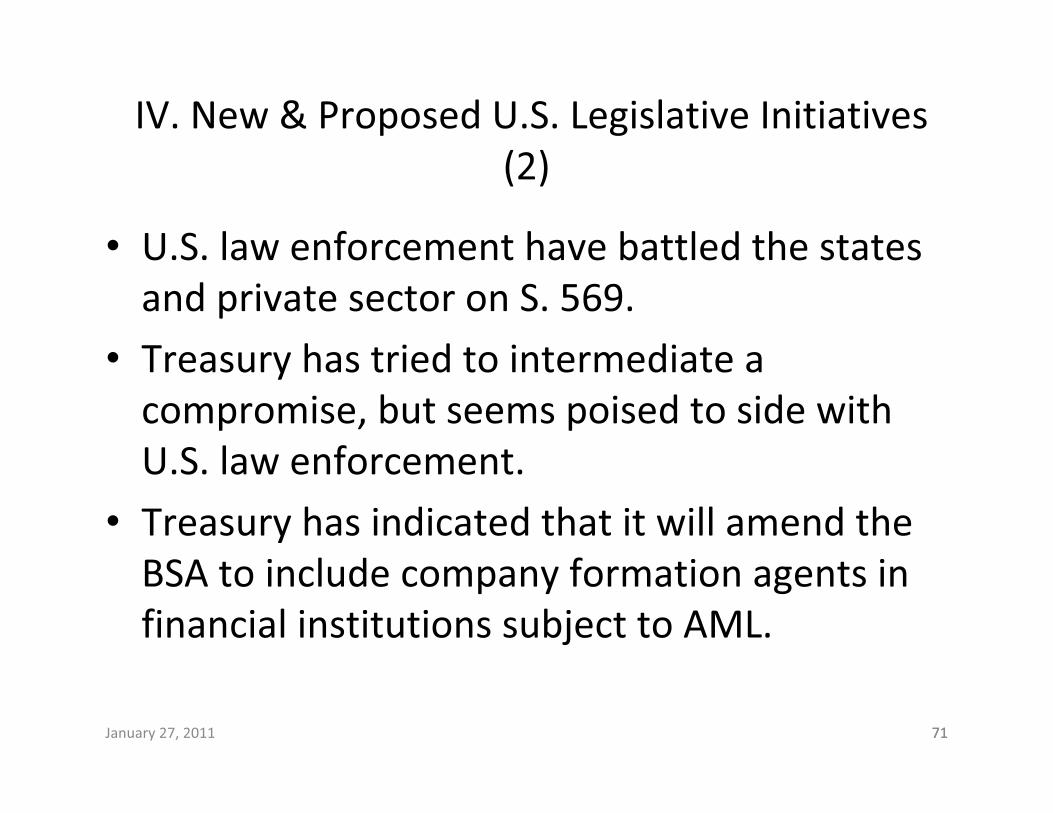

IV.�New�&�Proposed�U.S.�Legislative�Initiatives�(2)

• U.S.�law�enforcement�have�battled�the�states�and�private�sector�on�S.�569.

• Treasury�has�tried�to�intermediate�a�compromise,�but�seems�poised�to�side�with�U.S.�law�enforcement.

• Treasury�has�indicated�that�it�will�amend�the�BSA to�include�company�formation�agents�in�financial�institutions�subject�to�AML.

71

January�27,�2011 72

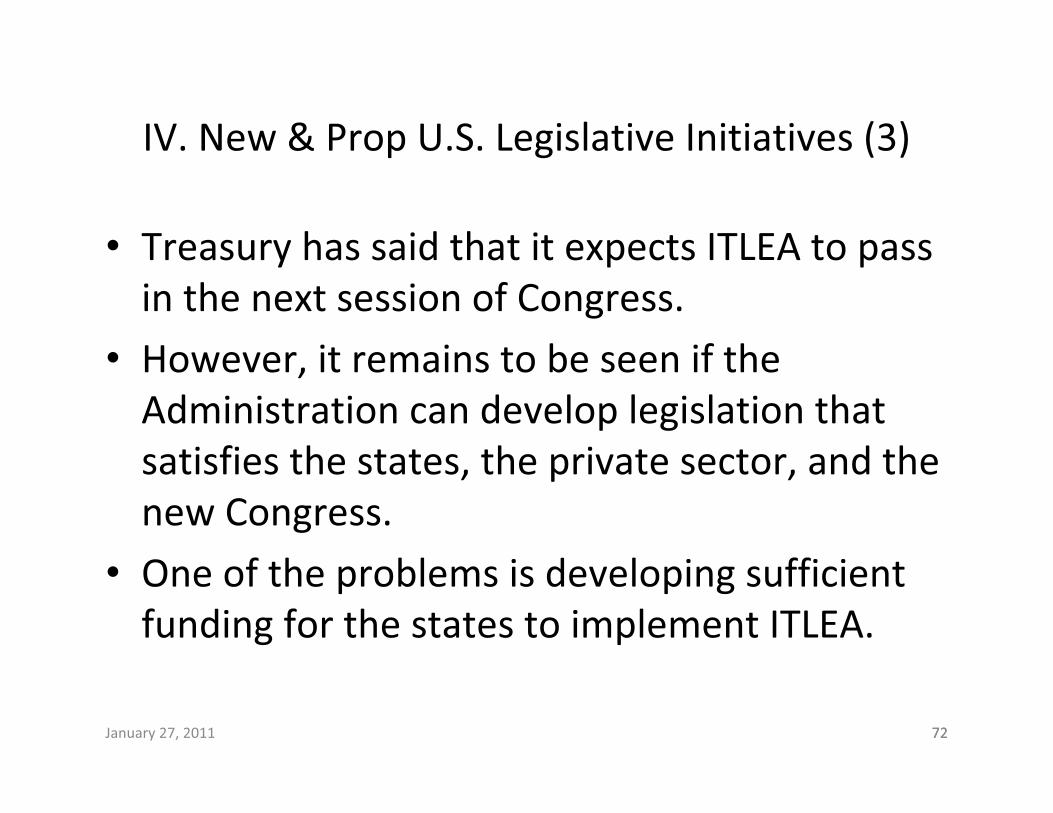

IV.�New�&�Prop�U.S.�Legislative�Initiatives�(3)

• Treasury�has�said�that�it�expects�ITLEA to�pass�in�the�next�session�of�Congress.

• However,�it�remains�to�be�seen�if�the�Administration�can�develop�legislation�that�satisfies�the�states,�the�private�sector,�and�the�new�Congress.��

• One�of�the�problems�is�developing�sufficient�funding�for�the�states�to�implement�ITLEA.

72

January�27,�2011 73

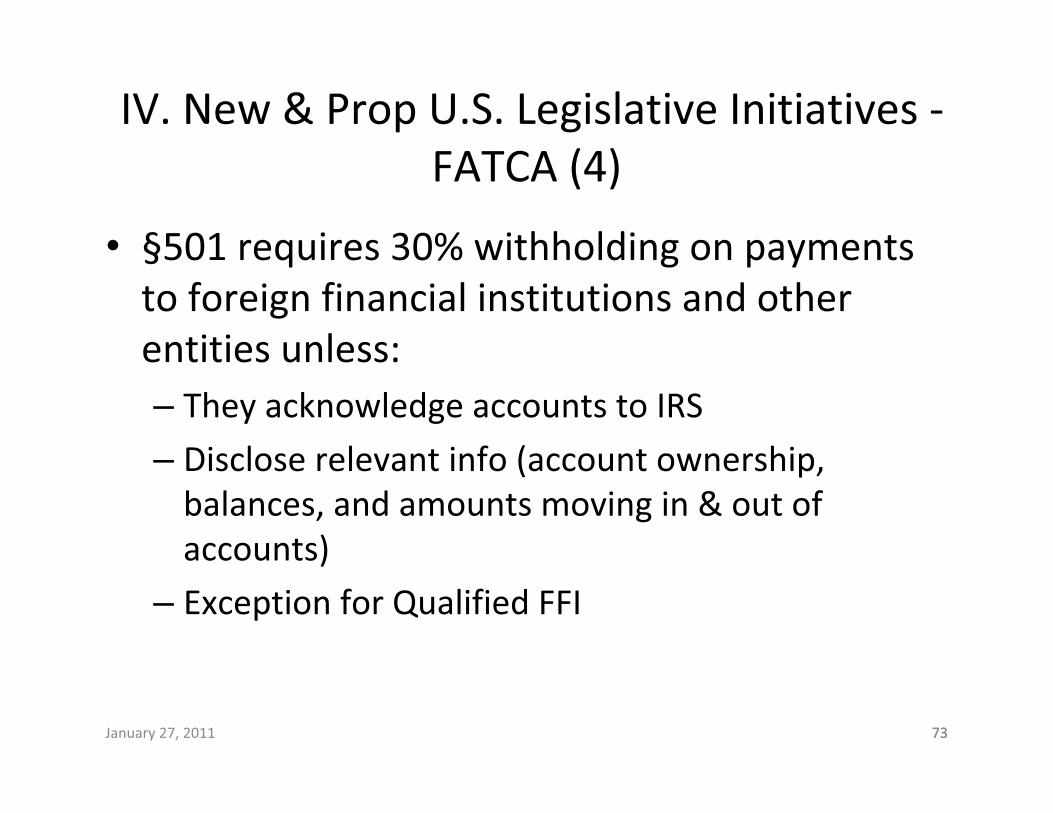

IV.�New�&�Prop�U.S.�Legislative�Initiatives��FATCA (4)

• §501�requires�30%�withholding�on�payments�to�foreign�financial�institutions�and�other�entities�unless:– They�acknowledge�accounts�to�IRS

– Disclose�relevant�info�(account�ownership,�balances,�and�amounts�moving�in�&�out�of�accounts)

– Exception�for�Qualified�FFI

73

January�27,�2011 74

IV.�New�&�Proposed�U.S.�Legislative�Initiatives�� FATCA (5)

– Withhold�30%�from�any�“pass�thru�payment” that�is�made�to:�(1)�a�“recalcitrant” account�holder,�(ii)�a�non�QFFI,�or�(iii)�a�QFFI that�has�elected�to�be�withheld�upon�with�respect�to�the�part�of�the�payment�allocable�to�a�recalcitrant�account�holder�or�to�a�non�QFFI;�and

– Try�to�obtain�a�waiver�in�any�case�in�which�any�foreign�law�would�(but�for�the�waiver)�prevent�the�reporting�of�the�required�information�required�with�respect�to�any�US�owned�account�maintained�by�the�FFI;�if�a�waiver�is�not�obtained,�the�QFFI is�required�to�close�the�account.

74

January�27,�2011 75

IV.�New�&�Proposed�U.S.�Legislative�Initiatives�� FATCA (6)

• §522�authorizes�Treasury�to�require�financial�institutions�to�electronically�file�information�reports�about�withholding�on�transfers�to�foreign�accts��to�enable�the�IRS�to�better�match�reports�to�tax�returns.

• §§ 531�5�strengthens�rules�&�penalties�re�foreign�trusts,�including�rules�to�determine�whether�distributions�from�foreign�trusts�are�going�to�US�beneficiaries�&�reporting�requirements�on�US�transfers�to�foreign�trusts.

75

January�27,�2011 76

IV.�New�&�Propose�Legislative�Initiatives�� FATCA (7)

• §541�clarifies�that�U.S.�dividend�payments�received�by�foreign�persons�are�treated�as�dividends�even�when�couched�as�another�type�of�distribution�in�an�effort�to�avoid�U.S.�taxes.

• An�unknown�will�be�whether�FFIs without�a�large�U.S.�client�base�will�decide�it�is�cost�effective�to��participate�in�the�regime�or�will�decide�to�avoid�U.S.�clients.

76

January�27,�2011 77

V.�International�Organizations�and�Related�Initiatives

• The�OECD,�FATF,�G�20,�and�IMF/World�Bank�Group�have�taken�some�important�and�dynamic�action�with�respect�to�tax�enforcement�and�money�laundering.��

• See�Alan�Granwell’s presentation�for�these�developments.

77

January�27,�2011 7878

V.�International�Organizations�and�Related�Initiatives�(2)�

– Third�EU�Directive�on�Money�Laundering:• Adopted�by�most�member�states

• Belgium,�Ireland,�Spain,�and�Sweden�not�implemented

• Finland,�France,�Poland,�partially�implemented

– EU�Savings�Directive:• Subject�interest�payments�made�to�an�account�held�by�an�EU�

citizen�in�a�country�other�than�that�of�his/her�residence�to�taxation�in�country�of�residence

• EU�members�receiving�inward�investments�have�the�choice�to�withhold�tax�and�share�in�the�withholding�or�exchange�information�with�country�of�residence�of�the�depositor

78

January�27,�2011 7979

V. International�Organizations�and�Related�Initiatives�(3)

• Three�initiatives�that�the�European�Commission�is�currently�pursuing:

• The�review�of�the�savings�tax�directive,��to�close�certain�loopholes;

• The�proposed�directive�on�mutual�assistance�between�the�member�states�to�help�EU�members�assess�the�tax�positions�of�their�residents�in�other�countries�and�to�collect�the�tax�that�is�due.

• Communication�on�good�governance�in�the�area�of�taxation,�which�would�cover�exchange�of�information,�transparency,�and�fair�tax�competition,�"the�three�pillars�of�good�governance�in�the�tax�area”.

79

January�27,�2011 80

V. International�Organizations�and�Related�Initiatives�(4)

• On�December�7,�2010,�the�Council�of�the�European�Union�at�a�meeting�of�the�Economic�and�Financial�Affairs�Council�reached�political�agreement�on�a�draft�directive�aimed�at�strengthening�administrative�cooperation�in�the�field�of�direct�taxation�in�order�to�enable�the�EN�Members�to�better�combat�tax�evasion�and�tax�fraud.

80

January�27,�2011 81

V. International�Organizations�and�Related�Initiatives�(5)

• The�draft�directive�has�the�goal�of�fulfilling�the�EU�members’ growing�need�for�mutual�assistance,�especially�through�the�exchange�of�information,�in�order�to�enable�them�to�better�assess�taxes�due,�in�the�context�of�greater�taxpayer�mobility,�globalization,�and�a�growing�number�of�cross�border�transactions.

• Among�other�activities,�the�directive�will�overhaul�directive�77/799/99/EEC,�on�which�administrative�cooperation�in�the�field�of�taxation�has�been�based�since�1977.

81

January�27,�2011 82

V. International�Organizations�and�Related�Initiatives�(6)

• The�directive�will�ensure�that�the�OECD�standard�for�the�exchange�of�information�on�request�is�implemented�in�the�EU�as�regards�the�exchange�of�information�on�request.�

• It�will�prevent�an�EU�member�from�refusing�to�furnish�information�concerning�a�taxpayer�of�another�EU�Member�on�the�sole�ground�that�the�information�is�held�by�a�bank�or�other�financial�institution.

82

January�27,�2011 83

V. International�Organizations�and�Related�Initiatives�(7)

• The�directive�will�extend�cooperation�between�EU�members�to�cover�taxes�of�any�kind.��It�will�establish�time�limits�for�the�provision�of�information�on�request�and�other�administrative�enquiries.��

• The�directive�will�introduce�provisions�on�the�automatic exchange�of�information.

• Under�the�directive�officials�of�one�EU�member�can�participate�in�administrative�enquires�on�the�territory�of�another�EU�member.

83

January�27,�2011 84

V. International�Organizations�and�Related�Initiatives�(8)

• With�respect�to�automatic�exchange�of�information�the�Council�agreed�on�a�step�by�step�approach�aimed�at�eventually�ensuring�unconditional�exchange�of�information�for�eight�categories�of�income�and�capital.��

• Those�categories�are:�income�from�employment,�directors’ fees,�dividends,�capital�gains,�royalties,�certain�life�insurance�products,�pensions,�and�ownership�of�and�income�from�immovable�property.��From�2015,�EU�members�will�communicate�automatically�information�for�a�maximum�of�five�categories,�provided�that�such�information�is�readily�available.

84

January�27,�2011 85

V. International�Organizations�and�Related�Initiatives�(9)

• By�July�1,�2017,�the�Commission�will�provide�a�report�and,�if�required,�a�proposal.��When�examining�that�proposal,�the�Council�will�examine�the�possibilities�for�removing�the�condition�of�availability�and�extending�the�number�of�categories�from�five�to�eight.

85

January�27,�2011 86

V. International�Organizations�and�Related�Initiatives�(10)

• The�European�Commission�proposed�the�legislation�calling�for�automatic�information�exchange�almost�two�years�ago,�stating�the�legislative�proposal�included�a�transition�to�automatic�information�exchange�that�was�already�agreed�in�the�EU�cross�border�savings�directive.�However,�Luxembourg�and�Austria�disputed�that�claim�and�cited�the�original�terms�of�the�EU�cross�border�savings�tax�directive�agreed�in�2000�that�permitted�them�to�preserve�bank�secrecy�laws�as�long�as�Switzerland�and�other�independent�territories�such�as�the�Channel�Islands,�Monaco�and�others�kept�them.

86

January�27,�2011 87

V. International�Organizations�and�Related�Initiatives�(11)

• In�2009,�Luxembourg�and�Austria�softened�their�positions�as�part�of�the�G�20�agreement�in�London,�which�targeted�tax�havens�where�tax�evaders�have�been�hiding�trillions�of�dollars.�In�order�to�avoid�the�OECD�gray�list�backed�by�the�G�20,�both�Luxembourg�and�Austria�� as�well�as�Switzerland�� agreed�to�the�OECD�Tax�Model�convention�that�requires�them�to�exchange�info�on�request.

87

January�27,�2011 88

V. International�Organizations�and�Related�Initiatives�(12)

• Because�the�EU�coordinates�tax�and�foreign�policy�and�has�key�policymaking�positions�in�groups,�such�as�the�G�20�and�international�organizations,�such�as�the�OECD�and�the�IMF/World�Bank�Group,�the�draft�directive�has�implications�well�beyond�the�EU.

88

January�27,�2011 8989

VI.�Analysis�&�the�Way�Forward�� Clear�Domestic�and�Global�Impetus�to�Crackdown�on�Tax�

Havens

• President�Obama�supportive�of�STHAA,�FATCA,�and�other�international�tax�enforcement�initiatives.

• Increasing�convergence�and�prosecution�of:

– Money�laundering

– Bribery/foreign�corruption�(FCPA)

– Tax�evasion

• Pressure�on�a�macro�level�on�offshore�centers�and�large�international�banks�as�well�as�micro�level�facilitators�(lawyers,�accountants,�financial�advisers,�etc.)

• Get�to�know�your�clients�better!89

January�27,�2011 9090

VI.�Analysis�&�the�Way�Forward�(2)

• The�current�crackdown�on�tax�havens�may�lead�to�increased�movement�of�assets�globally.

• The�current�increased�regulatory�and�enforcement�environment�has�practice�implications�for�all�the�players,�including�banks,�financial�institutions,�professionals,�such�as�lawyers�and�other�gatekeepers,�and�governments.

• Financial�institutions�and�gatekeepers�will�increasingly�take�AML�due�diligence�action�for�tax�reasons�(e.g.,�UK�Code�of�Conduct�in�Tax�for�Banks).��

90

January�27,�2011 9191

VI.�Analysis�&�the�Way�Forward�(3)

• The�level�playing�field,�whereby�OECD�countries�must�have�and�enforce�the�same�AML,�tax�and�entity�transparency,�as�the�small�financial�centers,�will�exert�significant�pressure�for�meeting�international�standards�in�onshore�jurisdictions,�such�as�the�U.S.

• On�Aug�10,�2010,�the�ABA�House�of�Delegates�approved�AML�good�practice�standards�to�ensure�lawyers�meet�Know�Your�Customer�anddue�diligence�standards�when�they�conduct�financial�transactions.��Emphasis�will�turn�to�integrating�the�standards�into�state�ethical�codes.

• Increasingly,�transnational�enforcement�cases�will�be�initiated�outside�the�U.S.,�requesting�assistance�from�and�asserting�jurisdiction�over�U.S.�transactions�and�professionals.

91

January�27,�2011 92

VI.�Analysis�&�the�Way�Forward�(4)

• A�continuing�trend�is�the�use�of�unilateral�extraterritorial�measures�to�obtain�evidence,�such�as�John�Doe�summons.

• Another�trend�is�the�investigation�of�foreign�financial�institutions�for�potential�prosecution�(e.g.,�HSBC),�as�well�as�foreign�professionals.

• Other�countries�will�emulate�US�tax�enforcement�actions.

92

January�27,�2011 93

VI.�Analysis�&�the�Way�Forward�(5)

• Stakeholders�must�construct�a�better�architecture�that�affords�transparency,�due�process,�and�a�meaningful�opportunity�to�participate.

• Stakeholders�should�ascertain�that�the�decisions�made�by�informal�groups�(e.g.,�G20,�FATF,�G8)�and�int’l�orgs�were�done,�after�proper�due�process�and�debate.

93

January�27,�2011 94

VI.�Analysis�&�the�Way�Forward�(6)

• Without�better�and�fair�process�the�decisions�will�not�be�sustainable.

• Hence,�when�FATF or�G20�issue�revised�standards�and�has�difficulty�engaging�some�of�the�gatekeepers�and/or�jurisdictions�on�implementing�the�standards,�FATF learns�that�the�gatekeepers�believe�that�some�standards�are�fundamentally�flawed�because�they

94

January�27,�2011 95

VI.�Analysis�&�the�Way�Forward�(7)

violate�fundamental�national�law�and�that�some�of�the�polices�were�not�democratically�or�fairly�adopted.

• Trying�to�assess�the�future�scope�and�substance�of�international�financial�regulation�is�difficult�because�the�world�is�still�at�the�very�start�of�developing�transnational�networks�in�the�area�of�international�financial�regulation.

95

January�27,�2011 96

ADDENDUM�TO�FATCAReprint�from�B.�Zagaris,�FATCA and�Bank�Secrecy:�A�View�from�Abroad

Florida�International�Bankers�Assoc.�webinar,�Dec.�17,�2010

96

January�27,�2011 97

I.��Overview�of�Foreign�Views

� A.�Some�critics�complain�that�FATCA extends�the�QI whereby�US�obtains�automatic�exchange�of�information�w/o�reciprocity:��it�permits�non�US�persons�to�invest�in�the�US�thru�a�QI in�a�foreign�jurisdiction�w/o�the�identity�of�these�foreign�persons�being�disclosed�to�the�U.S.�payors of�income�of�the�USG,�thereby�precluding�US�to�exchange�the�relevant�info�with�the�respect�foreign�government�where�foreign�investor�resides.

97

January�27,�2011 98

I.�Overview�of�Foreign�Views�(2)� B.�If�you�can�beat�them,�join�them:��foreign�

governments�emulate�the�U.S.�and�more• E.g.,�EU�Savings�Directive.• E.g.,�Proposal�for�a�Directive�on�Alternative�

Investment�Fund�Managers� C.�Another�response�is�a�practical�one:�small�and�

medium�size�and�indigenous�foreign�financial�institutions�(FFIs)�whose�clients�are�not�predominantly�U.S.�taxpayers�must�make�a�cost�benefit�decision:��are�the�costs�and�administrative�burdens�worthwhile?

98

January�27,�2011 99

I.�Overview�of�Foreign�Views(3)

• In�this�regard,�already�some�FFIs,�such�as�Lloyds�and�Sarasin,�have�decided�to�avoid�U.S.�taxpayers�as�clients�because�the�administrative�burdens�and�costs�of�due�diligence,�plus�the�costs�(reputational�risk,�penalties,�and�prof.�fees)�of�penalties�outweigh�the�benefits�of�having�U.S.�clients.

99

January�27,�2011 100

I.�Overview�of�Foreign�Views(4)

• Other�responses�are�to�Notice�2010�60.��They�call�for�exclusions,�clarification,�simplification,�and�more�practical�rules.�

• In�particular,�they�call�for�redesigned�W�8�forms�and�self�certifications.

100

January�27,�2011 101

II.�Issues�Impacting�USFIs

A. Identification�of�Payees�by�USFIs

• A�USFI making�withholdable payments�must�determine�whether�the�recipient�is�a�US�person,�an�FFI,�an�entity�described�in�sec.�1471(f),�or�a�Non�Foreign�Financial�Institution�(NFFE).

• If�an�entity�is�determined�to�be�an�FFI,�the�USFImust�then�determine�whether�it�should�be�treated�as�a�participating�FFI (pFFI),�deemed�compliant�FFI(dcFF)�or�non� participating�FFI (npFFI).

101

January�27,�2011 102

II.�Issues�Impacting�USFIs (2)

• If�an�entity�is�determined�to�be�an�NFFE,�the�USFI must�determine�if�it�should�be�treated�as�an�excepted�NFFE or�“other” NFFE.

• To�comply�with�FATCA,�USFIs will�need�clear�and�workable�rules.

102

January�27,�2011 103

II.�Issues�Impacting�USFIs (3)

• 1.�New�Form�W�8�Commentators�have�suggested�new�(redesigned)�W�8�to�identify�new�foreign�entity�payees.

• Separate�Forms�W�8�for�individuals�and�entities�would�facilitate�the�work�of�USFIs.

• An�entity�checking�the�box�that�it�is�an�NFFEshould�have�to�attach�a�schedule�with�the�name,�address�and�TIN�of�each�of�its�substantial�U.S.�owners.

103

January�27,�2011 104

II.�Issues�Impacting�USFIs (4)

• The�USFI will�use�this�information�to�prepare

• its�annual�IRS�information�reporting�with�respect�to�the�NFFE’s substantial�US�owners

• 2.�Standards�to�Determine�Pre�Existing�Payee���Status

• Instead�of�requiring�USFIs to�“prove�the�negative�(i.e.,�that�an�entity�is�non�US),�the�IRS�should�provide�presumption�rules�to�allow

104

January�27,�2011 105

II.�Issues�Impacting�USFIs (5)

• USFIs to�rely�on�the�IRS�Reg.�1.6049�4�“eyeball�tests” as�proof�that�an�entity�is�foreign.

B.��USFI Verification�of�FFI Status�as

“Participating” or�“Non�Participating”

• USFFIs have�recommended�that�the�IRS�provide�simple�and�clear�rules�for�the�due�diligence�to�verify�the�certifications�by�foreign�payees�of�their�pFFI status�andcertifications by�NFFEs with�substantial�US�owners.

105

January�27,�2011 106

II.�Issues�Impacting�USFIs (6)

• The�IRS�should�develop�an�FFI validation�program�similar�to�the�current�IRS�TIN�matching�program.

• The�program�would�require�a�USFI to�submit�a�list�of�pFFI names/TINs to�the�IRS�for�validation.

• The�IRS�would�notify�the�requesting�USFI of�FFIson�the�submitted�list�that�are�in�fact�pFFIs and�those�that�have�not�been�validated�as�pFFIs.

106

January�27,�2011 107

II.�Issues�Impacting�USFIs (7)

C.�Exclusion�of�Certain�Payments�from�the�Definition�of�Withholdable Payment

• FATCA exempts�certain�types�of�payments�from�the�definition�of�withholdable payments.

• The�IRS�has�broad�authority�to�exclude�other�types�of�payment.�Commentators�are�asking�the�IRS�to�use�the�authority�to�exclude�payments�that�have�a�very�low�risk�of�US�tax�

107

January�27,�2011 108

II.�Issues�Impacting�USFIs (8)

evasion,�such�as�certain�investment�type�income�(i.e.,�interest�payments�on�short�term�debt�and�bank�deposits,�as�well�as�payments�to�vendors�for�services�and�license�fees).

108

January�27,�2011 109

II.�Issues�Impacting�USFIs (9)

D.��Presumption�Rules�w/�Respect�to�CFCs,�US������

Branches�of�FFIs,�&�Foreign�Branches�of�USFIs

• Some�recommend�the�IRS�reconsider�its�position�w�respect�to�prior�requests�that�certain�entities�be�treated�as�dcFFIs because�these�entities�are�already�subject�to�various�information�reporting�and�withholding�requirements.

109

January�27,�2011 110

III.�Issues�Affecting�FFIsA.�Members�of�the�Same�Expanded�Affiliated�Group

• IRS�should�clarify�that�an�FFI belonging�to�an�expanded�affiliated�group�need�not�certify�that�no�other�member�of�the�same�expanded�knows,�or�has�reason�to�know,�that�any�information�provided��to�the�FFI by�a�customer�is�incorrect.

• Processing�systems�usually�do�not�permit�members�of�the�same�expanded�affiliated�group�to�share�certain�information�about�each�other.

110

January�27,�2011 111

III.�Issues�Affecting�FFIs (2)B.�Carve�Out�Provisions• 1.�Carve�Out�Provision�for�Certain�FFIs

Carve�outs�have�been�recommended�for:• a)�FFIs owned�by�US�parents�or�US�holding�cos.

• b)�FFIs located�in�jurisdictions�where�they�are�already�required�to�provide�comprehensive�reports�on�their�clients�and

• c)�FFIs located�in�jurisdictions�that�have�TIEAs or�tax�treaties�with�the�US.

111

January�27,�2011 112

III.�Issues�Affecting�FFIs (3)

• 2.�Carve�Out�Provision�for�Certain�FFEs

• Including�NFFEs located�in�a�country�that�a)has a�DTA or�TIEA;�and

• b)�is�regarded�by�the�US�as�actively�complying�with�the�same.

112

January�27,�2011 113

III.�Issues�Affecting�FFIs (4)• 3.�Carve�Out�Provision�for�Certain�Beneficial

Owners• Some�comments�are�that�the�IRS�should�clarify�that�

investors�such�as�foreign�insurance�companies,�foreign�pension�funds,�pension�fund�pooling�vehicles�and�other�pooled�investment�vehicles�utilized�by�charities,�other�entities�exempt�from�US�withholding�under�tax�treaties�and�publicly�traded�companies�are�included�in�the�beneficial�owner�exceptions�for�Foreign�Financial�institutions�or�NFFEs.

113

January�27,�2011 114

III.�Issues�Affecting�FFIs (5)

• 4.�FFI Determination�of�“Specified�US�Person”

• IRS�should�develop�practical�rules�with�examples�since�most�FFIs and�NFFEs are�unfamiliar�with�US�tax�laws�and�are�likely�to�have�difficulty�determining�the�classification�of�entities�for�US�tax�purposes.

114

January�27,�2011 115

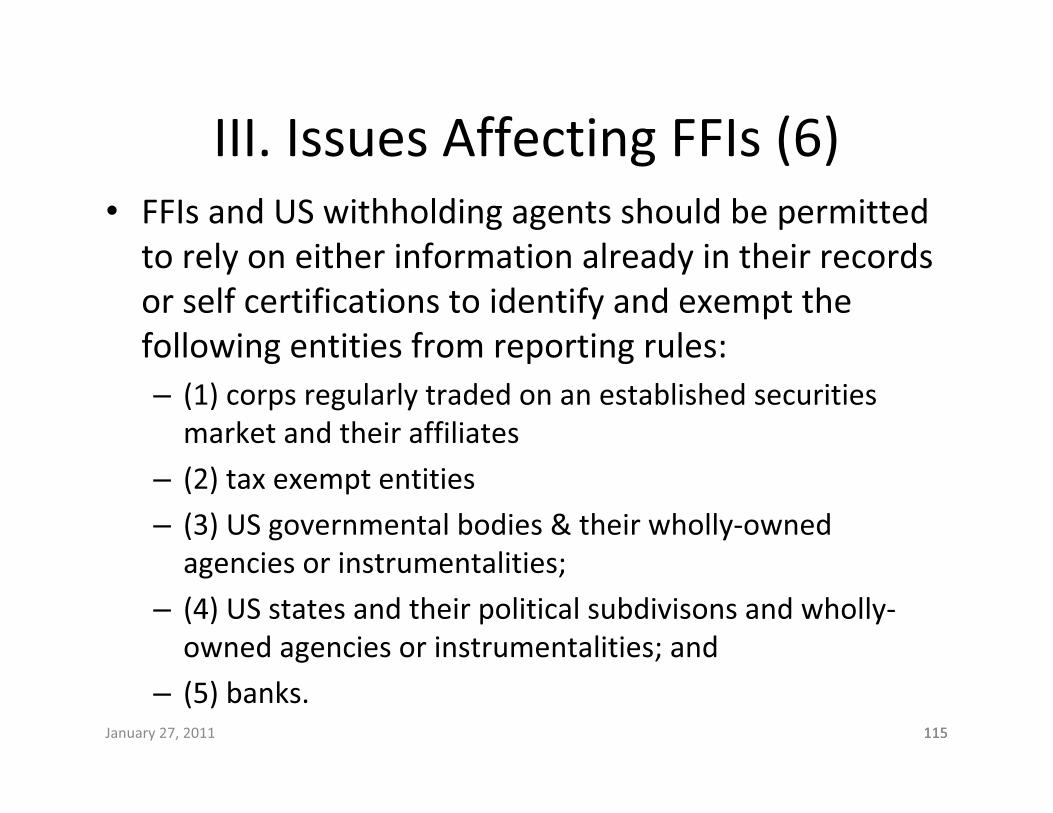

III.�Issues�Affecting�FFIs (6)• FFIs and�US�withholding�agents�should�be�permitted�

to�rely�on�either�information�already�in�their�records�or�self�certifications�to�identify�and�exempt�the�following�entities�from�reporting�rules:– (1)�corps�regularly�traded�on�an�established�securities�

market�and�their�affiliates

– (2)�tax�exempt�entities

– (3)�US�governmental�bodies�&�their�wholly�owned�agencies�or�instrumentalities;

– (4)�US�states�and�their�political�subdivisons and�wholly�owned�agencies�or�instrumentalities;�and

– (5)�banks.115

January�27,�2011 116

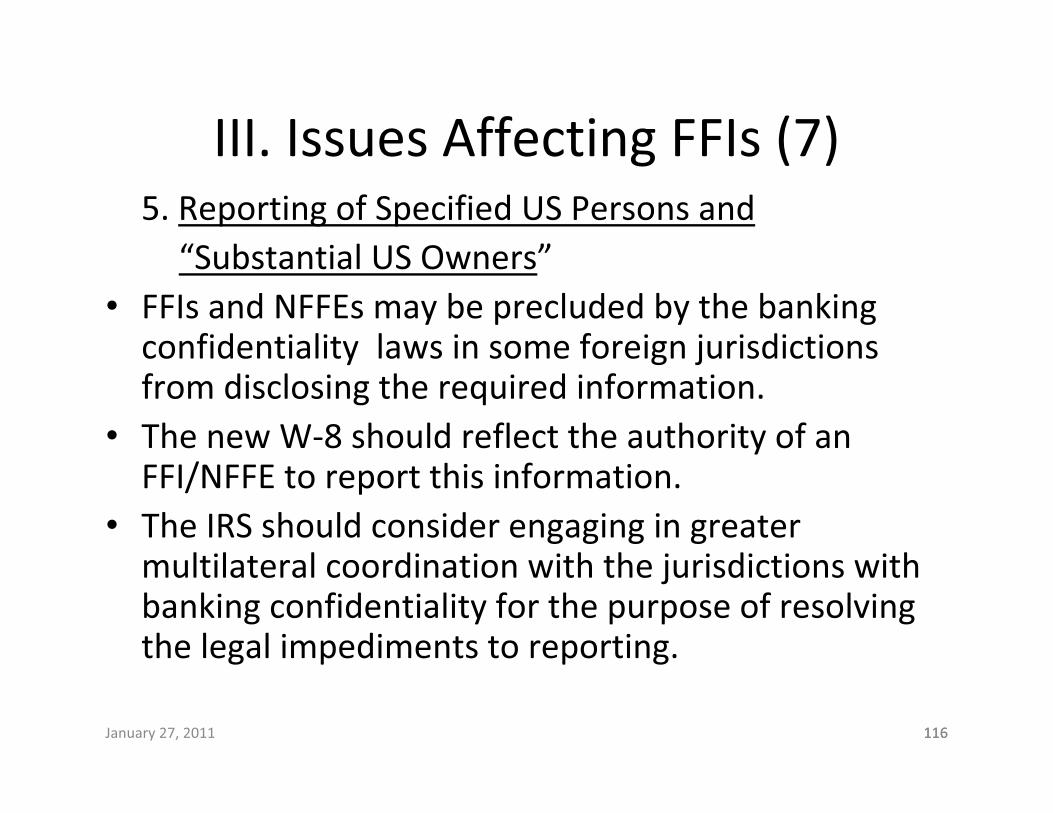

III.�Issues�Affecting�FFIs (7)5.�Reporting�of�Specified�US�Persons�and����

“Substantial�US�Owners”• FFIs and�NFFEs may�be�precluded�by�the�banking�

confidentiality��laws�in�some�foreign�jurisdictions�from�disclosing�the�required�information.

• The�new�W�8�should�reflect�the�authority�of�an�FFI/NFFE to�report�this�information.

• The�IRS�should�consider�engaging�in�greater�multilateral�coordination�with�the�jurisdictions�with�banking�confidentiality�for�the�purpose�of�resolving�the�legal�impediments�to�reporting.

116

January�27,�2011 117

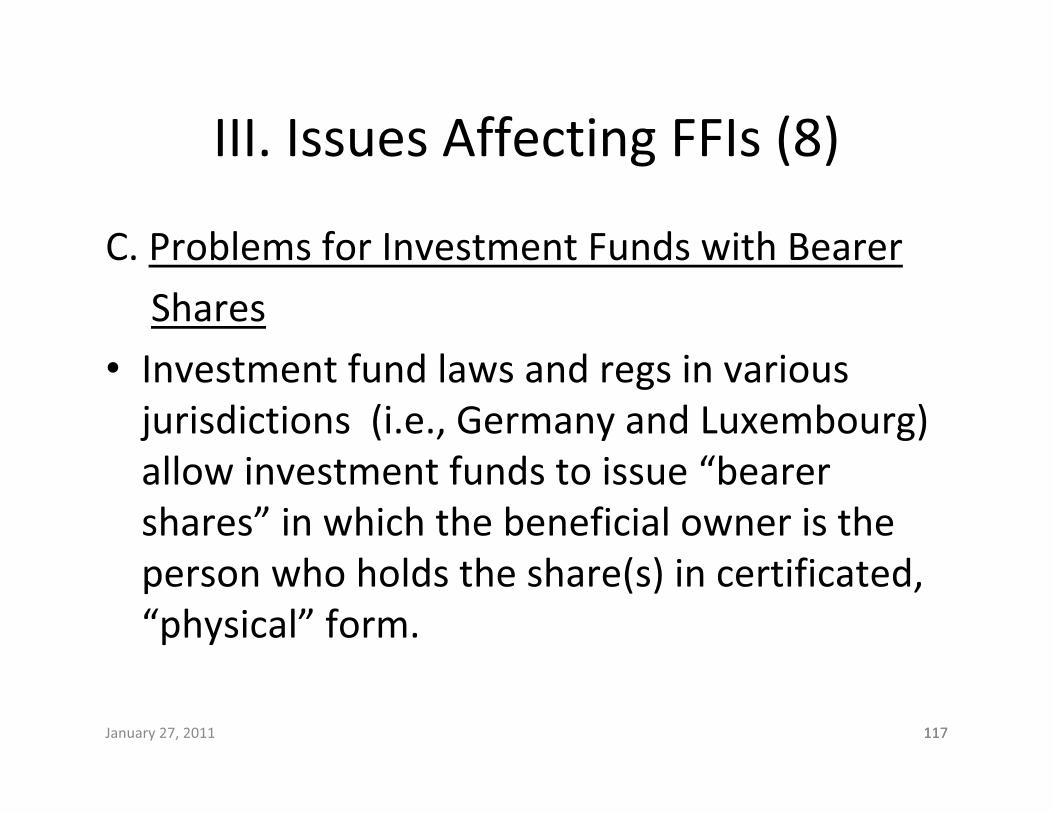

III.�Issues�Affecting�FFIs (8)

C.�Problems�for�Investment�Funds�with�Bearer�

Shares

• Investment�fund�laws�and�regs in�various�jurisdictions��(i.e.,�Germany�and�Luxembourg)�allow�investment�funds�to�issue�“bearer�shares” in�which�the�beneficial�owner�is�the�person�who�holds�the�share(s)�in�certificated,�“physical” form.

117

January�27,�2011 118

III.�Issues�Affecting�FFIs (9)

• Although�FATCA rules,�as�presently�drafted,��give�an�incentive�for�FFIs to�identify�their�US�account�holders�on�an�annual�basis,�they�cannot�establish�the�beneficial�owners�of�bearer�shares�at�a�given�point�in�time.

• FFIs issuing�bearer�shares�with�a�term�greater�than�one�year�will�not�be�able�to�verify�ownership�on�annual�basis.��

118

January�27,�2011 119

III.�Issues�Affecting�FFIs (10)

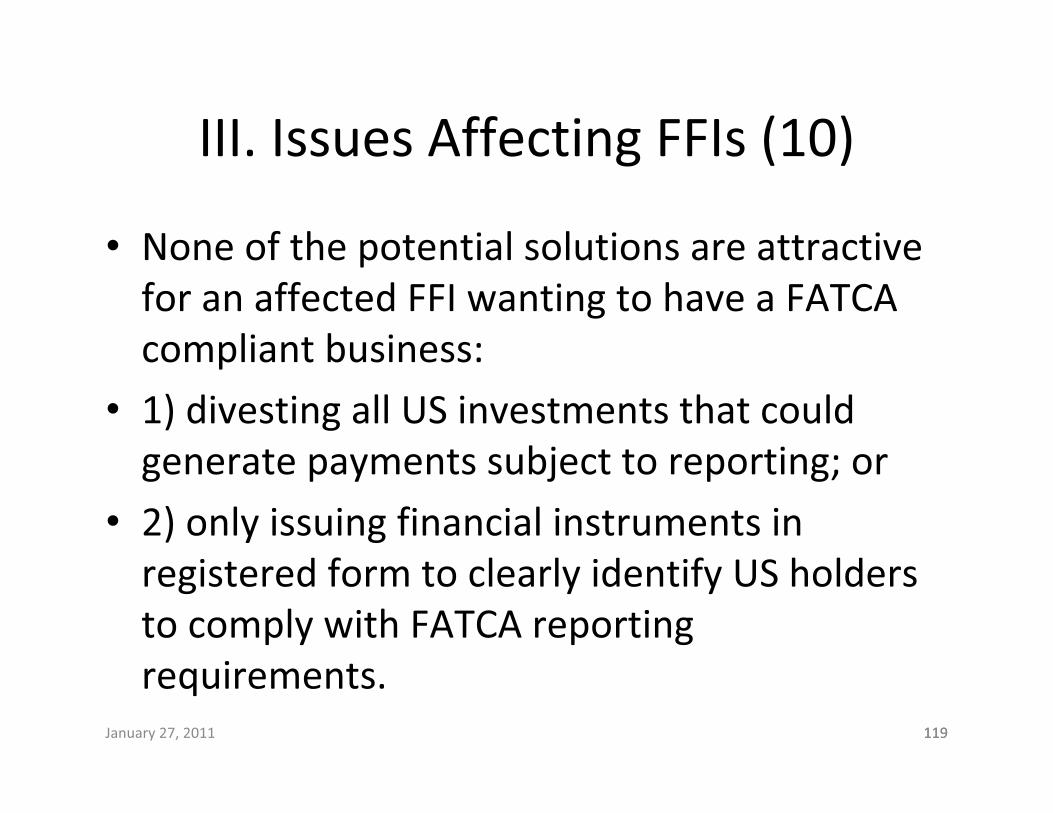

• None�of�the�potential�solutions�are�attractive�for�an�affected�FFI wanting�to�have�a�FATCAcompliant�business:

• 1)�divesting�all�US�investments�that�could�generate�payments�subject�to�reporting;�or

• 2)�only�issuing�financial�instruments�in�registered�form�to�clearly�identify�US�holders�to�comply�with�FATCA reporting�requirements.

119

January�27,�2011 120

IV.�Problems�of�Foreign�Law

A. Sec.�511�Identification�and�Reporting���

Requirements�Will�Override�Foreign�Law

• § 511�imposes�subject�to�the�Chapter�4�withholding�tax�a�30�percent�tax�withholding�on�payments�either�to�foreign�banks�and�trusts�that�fail�to�identify�U.S.�accounts�and�their�owners�and�assets�to�the�IRS,�or�to�foreign�corporations�that�do�not�furnish�the�name,�address,�and�tax�identification�number�of�any�U.S.�individual�with:�

120

January�27,�2011 121

IV.�Problems�of�Foreign�Law�(2)

• (1)�at�least�10�percent�ownership�by�vote�or�value�of�a�foreign�corporation,�

• (2)�interest�in�a�partnership,�or�• (3)�is�treated�as�a�grantor�of�a�foreign�trust�or,�

(4)�holds�more�than�10%�of�the�beneficial�interest�in�a�foreign�trust.��This�will�take�effect�for�payments�made�after�December�31,�2010,�with�some�exceptions�for�grandfathered�agreements.��

121

January�27,�2011 122

IV.�Problems�of�Foreign�Law�(3)

• The�foreign�institution�must�agree�to�annually�report�on�the�account�balance,�gross�receipts,�and�gross�withdrawals/payments�from�such�account.��

• Foreign�financial�institutions�must�also�agree�to�disclose�and�report�foreign�entities�that�have�substantial�U.S.�owners.

122

January�27,�2011 123

IV.�Problems�of�Foreign�Law�(4)

• The�ability�to�avoid��a�withholding�tax�requires�foreign�financial�institutions�(FFIs)�and�non�financial�foreign�entities�to�identify�and�report�information�with�respect�to�U.S.�account�holders�and�U.S.�investors.��

• Treasury�and�the�IRS�should�be�careful�and�sensitive�to�concerns�that�the�reporting�requirements�be�implemented�in�a�way�that�does�not�violate�the�local�laws�to�which�FFIs and�NFFEsare�subject.��

123

January�27,�2011 124

IV.�Problems�of�Foreign�Law�(5)

• Local�laws�on�regulatory,�privacy,�information�disclosure�and�other�matters,�some�of�which�may�impose�criminal�sanctions�for�the�disclosure�of�information�relating�to�persons�that�are�investing�in�or�doing�business�with�the�reporting�entity,�may�prevent�FFIs and�NFFEs from�identifying�and�reporting�U.S.�account�holders�and�U.S.�investors.

124

January�27,�2011 125

IV.�Problems�of�Foreign�Law�(6)

• Hence,�FFIs or�NFFEs,�even�if�part�of�the�same�expanded�affiliate�group,�may�be�subject�to�differing�legal�restrictions�and�requirements.

125

January�27,�2011 126

IV.�Problems�of�Foreign�Law�(7)

B.��Sec.�511�Reporting�May�Be�Duplicative�

• The�bank�asked�IRS�to�exclude,�from�the�definition�of�a�U.S.�account�that�must�be�disclosed,�depository�accounts�held�in�foreign�jurisdictions�that�already�must�report�to�local�tax�authorities�and�that�routinely�exchange�the�information�with�the�United�States.�

126

January�27,�2011 127

IV.�Problems�of�Foreign�Law�(8)

• It�pointed�out�that�under�the�new�law,�accounts�are�excluded�if�they�already�are�subject�to�reporting�requirements�that�the�U.S.�treasury�secretary�determines�are�“duplicative.”

• TD�Bank�explained�that�in�Canada,�banks�are�required�to�file�Forms�NR4�reflecting�amounts�paid�or�credited�to�nonresidents�subject�to�Canadian�withholding�tax�on�Form�NR4.�

127

January�27,�2011 128

IV.�Problems�of�Foreign�Law�(9)

• The�information�that�goes�to�the�Canadian�tax�authority�is�similar�to�that�required�to�be�reported�by�foreign�financial�institutions�on�the�Form�1099,�the�bank�said.

128

January�27,�2011 129

V.�Emulating�FATCA

• An�example�of�foreign�countries�emulating�FATCA is�the�European�Union’s�proposed�Alternative�Investment�Fund�Managers�Directive�(AIFM),�first�published�by�the�European�Commission�in�April�2009.

• It�seeks�to�establish�a�harmonized�framework�for�monitoring�and�supervising�the�risks�posed�by�alternative�investment�funds,�such�as�hedge�funds�and�private�equity.

129

January�27,�2011 130

V.�Emulating�FATCA (2)

• One�of�the�two�competing�drafts,�from�the�European�Parliament,�proposes�that�third�country�funds�may�be�marketed�exclusively�to�professional�investors�in�the�EU�provided�a�number�of�key�conditions�are�fulfilled:

• 1)�an�agreement�between�the�supervisor�of�the�fund�and�the�EU�Member�in�which�it�wishes�to�market,�agreeing�to�exchange�information;

130

January�27,�2011 131

V.�Emulating�FATCA (3)

• 2)�the�third�country�from�which�the�manager�operates�must�be�“approved” by�the�Commission,�subject�to�its�compliance�with�FATF’s 40+9�recommendations;

• 3)�an�agreement�between�the�third�country�and�the�EU�Member,�in�which�the�manager�wants�to�market,�granting�authorization�subject�to�compliance�with�the�OECD�Model�Tax�Convention�and�an�agreement�to�

131

January�27,�2011 132

V.�Emulating�FATCA (4)

the�Commission’s�decision�that�confirms�EU�managers�will�have�marketing�opportunities�in�that�third�country�equal�to�the�market�access�received�by�the�non�EU�manager�in�Europe.�

• On�Nov.�11,�2010,�the�European�Parliament�approved�the�Directive.�Once�approved�by�the�Council,�the�European�Securities��&�Marketing�Authority�will�lead�in�the�drafting�and�negotiation�of�detailed�“Level�2” regulations.��

132

January�27,�2011 133

V.�Emulating�FATCA (5)

� Although�Treasury�Secretary�Geithner has�lobbied�against�the�adoption�of�the�AIFM,�the�EU�has�responded�that�the�AIFM is�precisely�in�response�to�the�G20’s�initiative�to�improve�gaps�in�int’l�securities�regulation�to�protect�against�some�of�the�foreign�(e.g.,�U.S.)�products�that�resulted�in�the�financial�crisis.�

133

January�27,�2011 134

VI.�FATCA is�Unilateral�&�w/o�Reciprocity

• Critics�charge�that�FATCA extends�the�qualified�intermediary�(QI)�provisions,�requiring�each�foreign�financial�institution�(FFI)�that�is�a�QI to�provide�information�automatically�to�the�U.S.�government�about�U.S.�persons�investing�in�the�U.S.�through�the�QI.

134

January�27,�2011 135

VI.�FATCA is�Unilateral�&�w/o�Reciprocity�(2)

• Neither�the�QI program�nor�FATCA allows�non�U.S.�persons�to�invest�in�the�U.S.�without�disclosing�the�identity�of�such�persons�to�the�U.S.�payors of�income�or�to�the�U.S.�government.

• As�a�result,�the�U.S.�cannot�exchange�the�information�with�foreign�governments�where�the�foreign�investor�resides.

135

January�27,�2011 136

VII.�Practical�Issues

• Some�FFIs may�decide�not�to�implement�FATCA because�their�U.S.�business�may�not�be�large�enough�make�it�worthwhile�to�invest�in�the�new�resources�it�will�take�to�implement�FATCA.

• Developing�countries�will�have�trouble�implementing�FATCA because�they�do�not�have�the�technical�and�resource�capacity.

136

January�27,�2011 137

VII.�Practical�Issues�(2)

• Already�indigenous�financial�institutions�in�small�jurisdictions�lost�access�to�the�U.S.�when�they�had�difficulty�implementing�the��anti�money�laundering�requirements�of�the�PATRIOT�Act.

• The�more�FFIs that�decide�it�is�not�worthwhile�to�implement�FATCA,�the�more�opportunity�for�U.S.�investors�to�put�their�money�outside�of�the�QI and�FATCA.��

137

January�27,�2011 138

VII.�Practical�Issues�(3)

• The�more�FFIs that�decide�not�to�implement�FACTA means�loss�of�U.S.�market�to�foreign�capital�at�the�very�time�when�the�U.S.�needs�continued�access�to�foreign�capital�to�finance�the�U.S.�deficit.

138

January�27,�2011 www.DowlingAdvisoryGroup.com 139

““Understanding�offshore�tax�havens�and�the�Understanding�offshore�tax�havens�and�the�impact�of�the�new�tax�transparency�lawsimpact�of�the�new�tax�transparency�laws””

Who�Is�Involved�and�What�Financial�Institutions�Need�To�Look�For

www.DowlingAdvisoryGroup.com139

Jim�DowlingManaging�DirectorDowling�Advisory�Group

The information in these slides reflects the views of the presenter and do not reflect the views of DLA Piper.

January�27,�2011 www.DowlingAdvisoryGroup.com 140

Who�Is�Involved

There�are�two�groups�of�individuals�involved�in�“illegal” offshore�tax�havens:

1.Those�who�start�with�illegal�proceeds�(narcotics,�organized�crime,�financial�fraud,�etc.)

2.High�net�worth�individuals�looking�to�hide�money�to�evade�taxes�or�to�hide�from�spouse�or�business�associates.

140www.DowlingAdvisoryGroup.com

January�27,�2011 www.DowlingAdvisoryGroup.com 141

The�Government’s�Approach

Traditionally�the�government�has�only�pursued�individuals�who�placed�“illegal�proceeds”offshore�because�they�could.

Most�countries�have�MLAT (Mutual�Legal�Assistance�Treaties)�with�the�U.S.�Government�for�sharing�information�on�those�involved�in�the�sale�of�narcotics�and�other�“illegal” activities.��Many�countries�do�not�recognize�“tax�evasion” as�a�crime�rising�to�the�level�of�mutual�assistance.

141www.DowlingAdvisoryGroup.com

January�27,�2011 www.DowlingAdvisoryGroup.com 142

UBS:�The�Game�Changer

• Cooperating�witnesses�and�undercover�tapes– U.S.�government�got�an�“inside” view�of�foreign�

financial�institution’s�involvement�in�assisting�U.S.�citizens�in�committing�tax�evasion

• “John�Doe�Summons” served�on�UBS�in�the�U.S.,�requiring�the�names�and�account�numbers�of�U.S.�citizens.

142www.DowlingAdvisoryGroup.com

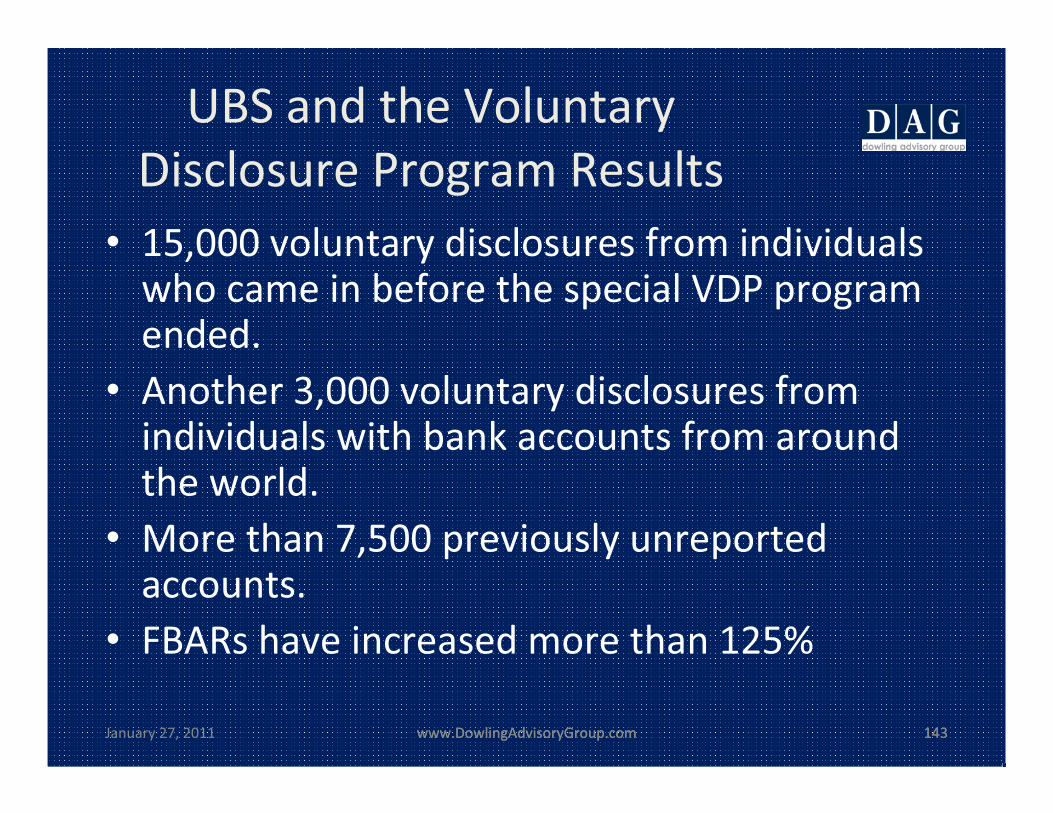

January�27,�2011 www.DowlingAdvisoryGroup.com 143

UBS�and�the�Voluntary�Disclosure�Program�Results

• 15,000�voluntary�disclosures�from�individuals�who�came�in�before�the�special�VDP program�ended.�

• Another�3,000�voluntary�disclosures�from�individuals�with�bank�accounts�from�around�the�world.

• More�than�7,500�previously�unreported�accounts.

• FBARs have�increased�more�than�125%

143www.DowlingAdvisoryGroup.com

January�27,�2011 www.DowlingAdvisoryGroup.com 144

Offshore�InvestigationsOffshore�Investigations

January�27,�2011 www.DowlingAdvisoryGroup.com 145145www.DowlingAdvisoryGroup.com

January�27,�2011 www.DowlingAdvisoryGroup.com 146146www.DowlingAdvisoryGroup.com

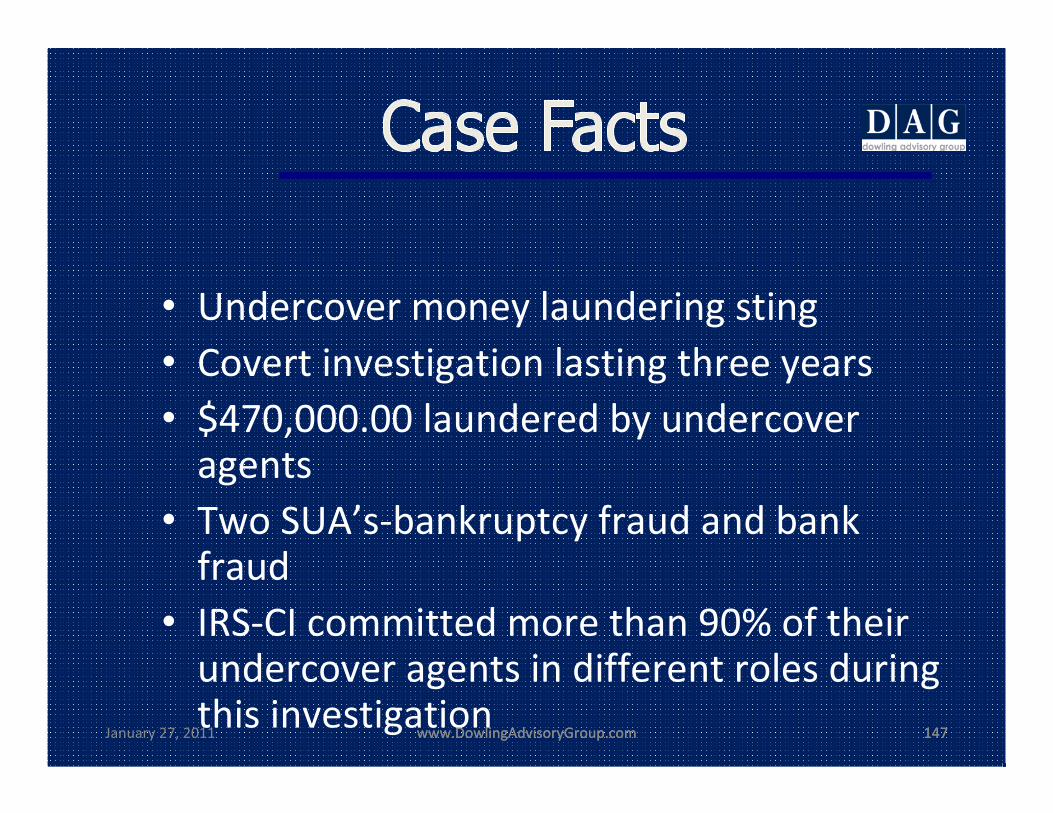

January�27,�2011 www.DowlingAdvisoryGroup.com 147

• Undercover�money�laundering�sting• Covert�investigation�lasting�three�years• $470,000.00�laundered�by�undercover�

agents• Two�SUA’s�bankruptcy�fraud�and�bank�

fraud• IRS�CI�committed�more�than�90%�of�their�

undercover�agents�in�different�roles�during�this�investigation

147www.DowlingAdvisoryGroup.com

January�27,�2011 www.DowlingAdvisoryGroup.com 148148www.DowlingAdvisoryGroup.com

January�27,�2011 www.DowlingAdvisoryGroup.com 149149www.DowlingAdvisoryGroup.com

January�27,�2011 www.DowlingAdvisoryGroup.com 150150www.DowlingAdvisoryGroup.com

January�27,�2011 www.DowlingAdvisoryGroup.com 151

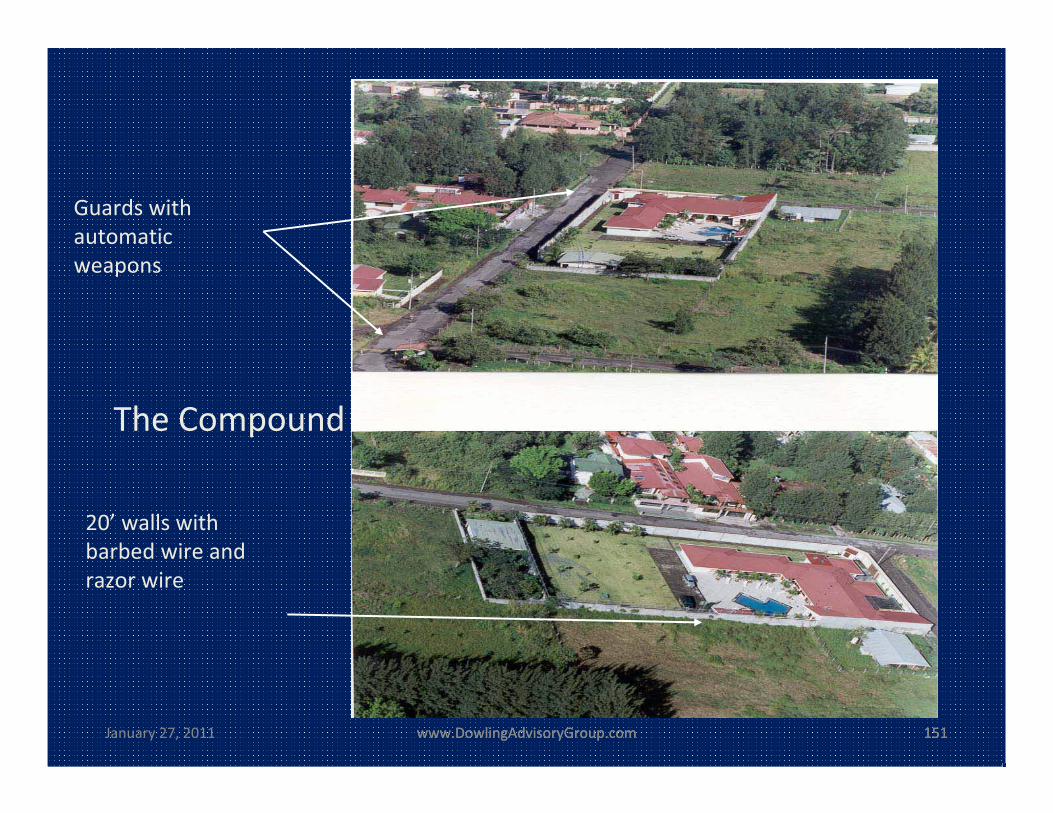

The�Compound

Guards�withautomatic�weapons

20’ walls�withbarbed�wire�and�razor�wire

151www.DowlingAdvisoryGroup.com

January�27,�2011 www.DowlingAdvisoryGroup.com 152152www.DowlingAdvisoryGroup.com

January�27,�2011 www.DowlingAdvisoryGroup.com 153

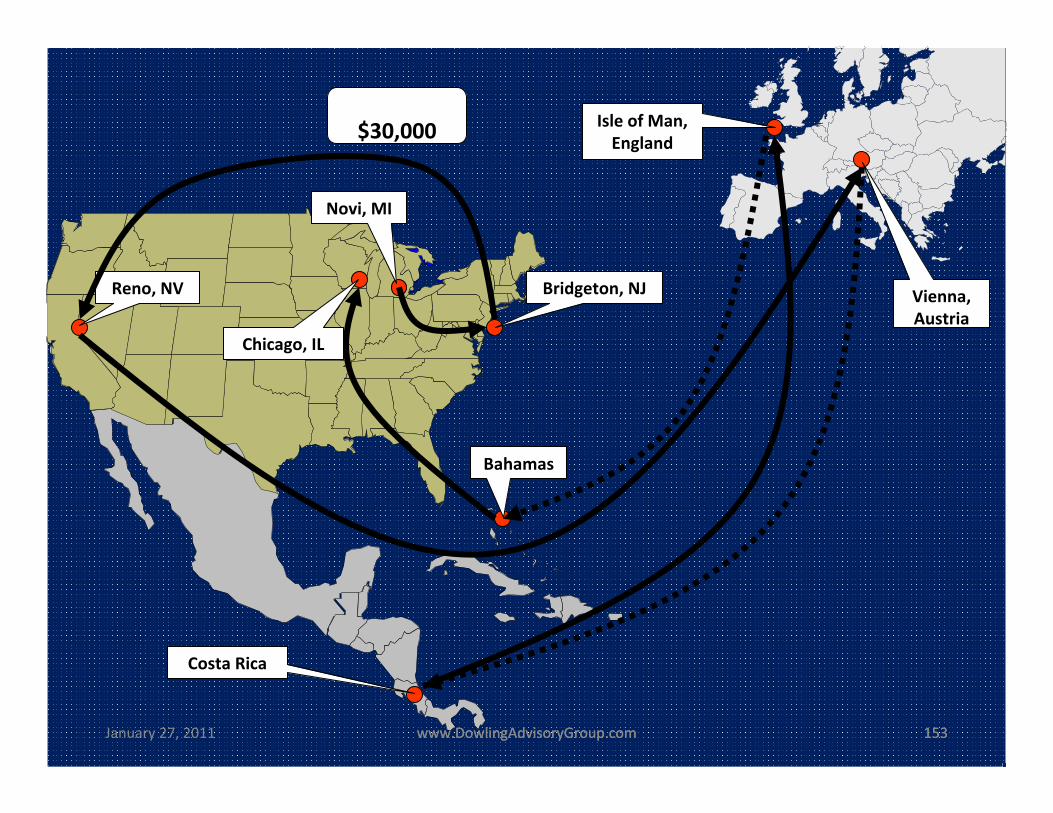

Isle�of�Man,England

Vienna,Austria

$30,000

Reno,�NV

Costa�Rica

Chicago,�IL

Novi,�MI

Bridgeton,�NJ

Bahamas

153www.DowlingAdvisoryGroup.com

January�27,�2011 www.DowlingAdvisoryGroup.com 154

Fresno,�CA

Costa�Rica

Boston,�MA

$100,000

154www.DowlingAdvisoryGroup.com

January�27,�2011 www.DowlingAdvisoryGroup.com 155155www.DowlingAdvisoryGroup.com

January�27,�2011 www.DowlingAdvisoryGroup.com 156

What�Areas�is�the�Government�Looking�At?

Foreign�trustsForeign�corporationsForeign�(offshore)�partnerships,�LLCs and�LLPsInternational�Business�Companies�(IBCs)Offshore�private�annuitiesPrivate�banking�(U.S.�and�offshore)Personal�investment�companiesCaptive�insurance�companiesOffshore�bank�accounts�and�credit�cards

156www.DowlingAdvisoryGroup.com

January�27,�2011 www.DowlingAdvisoryGroup.com 157

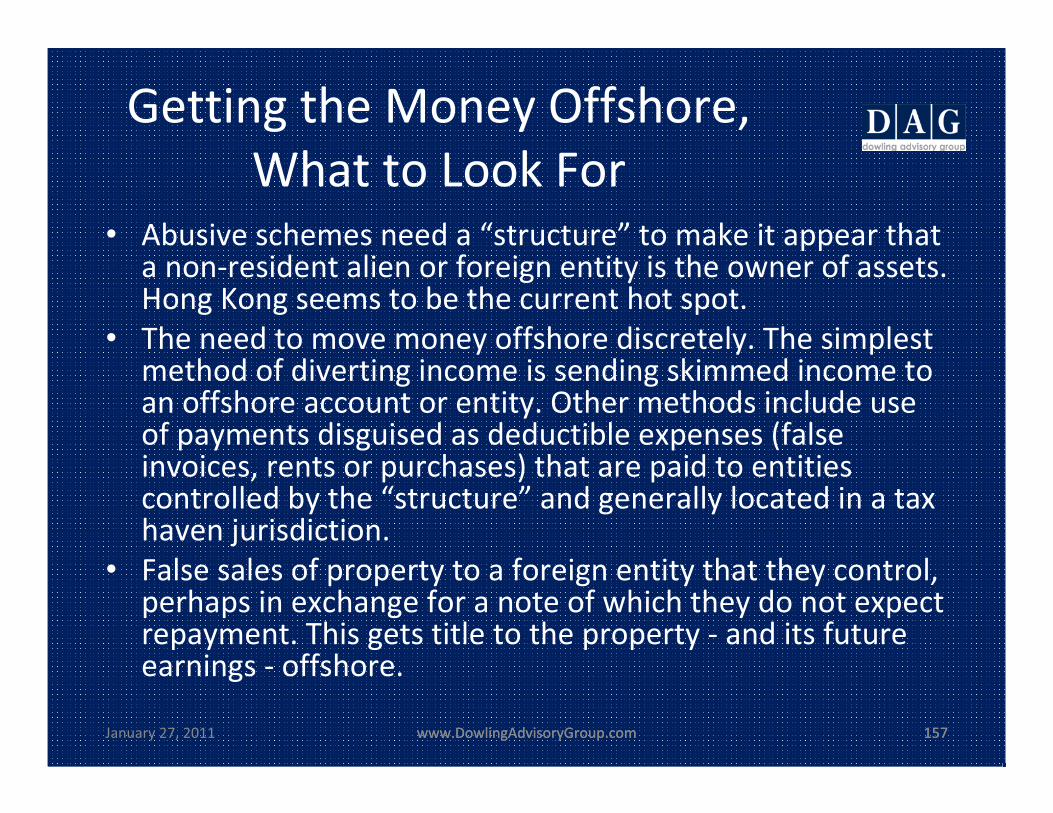

Getting�the�Money�Offshore,�What�to�Look�For

• Abusive�schemes�need�a�“structure” to�make�it�appear�that�a�non�resident�alien�or�foreign�entity�is�the�owner�of�assets.��Hong�Kong�seems�to�be�the�current�hot�spot.�

• The�need�to�move�money�offshore�discretely.�The�simplest�method�of�diverting�income�is�sending�skimmed�income�to�an�offshore�account�or�entity.�Other�methods�include�use�of�payments�disguised�as�deductible�expenses�(false�invoices,�rents�or�purchases)�that�are�paid�to�entities�controlled�by�the�“structure” and�generally�located�in�a�tax�haven�jurisdiction.�

• False�sales�of�property�to�a�foreign�entity�that�they�control,�perhaps�in�exchange�for�a�note�of�which�they�do�not�expect�repayment.�This�gets�title�to�the�property�� and�its�future�earnings�� offshore.�

157www.DowlingAdvisoryGroup.com

January�27,�2011 www.DowlingAdvisoryGroup.com 158

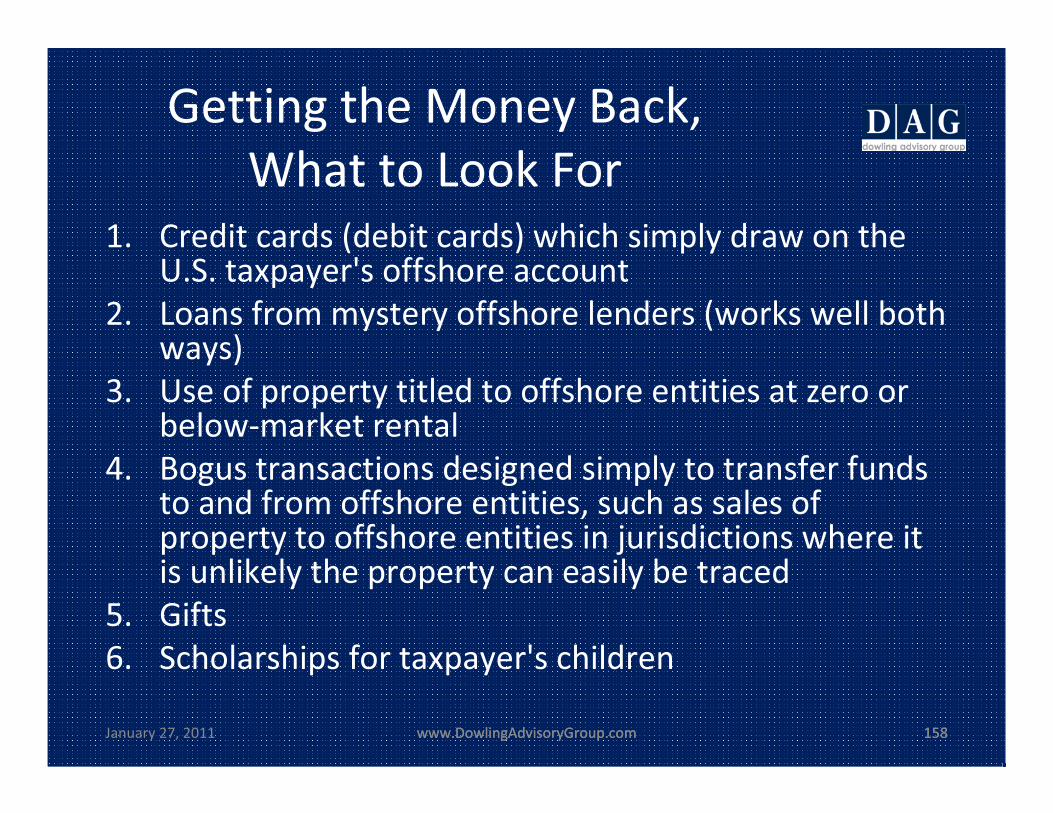

Getting�the�Money�Back,�What�to�Look�For

1. Credit�cards�(debit�cards)�which�simply�draw�on�the�U.S.�taxpayer's�offshore�account

2. Loans�from�mystery�offshore�lenders�(works�well�both�ways)

3. Use�of�property�titled�to�offshore�entities�at�zero�or�below�market�rental

4. Bogus�transactions�designed�simply�to�transfer�funds�to�and�from�offshore�entities,�such�as�sales�of�property�to�offshore�entities�in�jurisdictions�where�it�is�unlikely�the�property�can�easily�be�traced

5. Gifts6. Scholarships�for�taxpayer's�children

158www.DowlingAdvisoryGroup.com