Embed Size (px)

Citation preview

1Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

OESA AUTOMOTIVE SUPPLIER BAROMETERQ4 2019

HR & TALENT

2Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

Executive Summary

Supplier Barometer Index (SBI)

SBI Score = 37;

unchanged from Q3

The barometer reading remained

deep in pessimistic territory this

quarter on trade concerns, volume

declines and the United Auto

Workers (UAW) strike at General

Motors. The Q4 2019 index marks

the sixth straight quarter of net

pessimism and is two points lower

than a year ago

Trade policy continues to be identified as the greatest industry threat

The threat level surrounding trade policy on a 10-point scale (1=greatest

threat) remains pronounced, falling 0.2 points from Q3 2019 to 3.2.

Poor sales of vehicles in programs supplied and weakness in the U.S.

economy fell drastically, down 0.8 points each from Q3 to 3.4 and 3.8

respectively. Two Federal Reserve rate cuts prior to the sampling period

lowered the threat of higher interest rates substantially.

Automotive suppliers remain diversified

Median non-automotive revenue estimates are essentially unchanged

from last year.

A much greater number of non-automotive industries were named

specifically in comparison to Q4 2018 as suppliers search for alternative

revenue streams.

Regardless of revenue size, supplier executive responses maintain

high levels of pessimism as with the prior quarter

The largest companies by revenue, over $500 mils. in revenue, were the

most pessimistic. 75% of firms with revenue between $501 mils. and $1.0

bils. became more pessimistic and 66% of firms with revenue over $1.0

bils. became more pessimistic.

Medium sized suppliers by revenue ($151-500 mils.) had the most

improved outlook compared to Q3, however the cohort remains

pessimistic on net with a few suppliers reporting a more optimistic outlook.

3Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

Executive SummarySkills and company cultural gaps

persist but suppliers are more than

willing to embrace change

Executive responses indicate that nearly

60% of suppliers have moderate to wide

gaps between their current roles and

responsibilities versus skills, yet 93% of

executives were willing to embrace

change needed to reduce skills gaps.

Furthermore, 60% of responses indicate

that suppliers face moderate to wide

gaps between current and expected

company culture, while 88% are willing to

take steps to close cultural gaps.

Firms are focusing on increasing internal

skill development and reorganizing to

offset skills gaps, while re-evaluating

current policies and increasing flexibility

to close cultural gaps.

Technical skills remain scarce in

North America

The vast majority of suppliers indicate

that technical positions, both white and

blue-collar, are the most difficult to fill.

Engineering positions are the most

challenging to fill in the U.S.

Suppliers also indicated that

mechanical and software engineers are

the most difficult to hire.

Regional voluntary turnover rates are

extremely high throughout North

America

25% of suppliers report their turnover

rates in the U.S. at above 7.5% for

salaried workers while 46% of suppliers

estimate their turnover rates for hourly

workers at above 7.5%.

Canada and Mexico are not immune to

competitive labor markets with high

turnover rates in both salaried and

hourly positions.

Developing employees internally

through training, mentorship and

cross-functional job rotation,

through a structured development

plan are the key themes for career

path and succession planning

On net, employment growth is not

anticipated to keep up with sales growth

in the U.S., Canada, Europe, China, the

Rest of Asia and South America

The industry continues to adapt to

the desires of the younger workforce

with most suppliers implementing or

planning to implement programs to

attract and retain younger workers

HSA accounts and incentivizing a

healthy lifestyle are the most

common healthcare cost cutting

measures, while high deductible

plans and healthy living are the most

effective at reducing costs for the

company

Organizational leadership,

communication and empowerment

are the top HR priorities going into

2020, followed closely by training

and employee development

4Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SUPPLIER OUTLOOK

5Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

37

20

30

40

50

60

70

80

Jan-2

009

Jan-2

010

Jan-2

011

Jan-2

012

Jan-2

013

Jan-2

014

Jan-2

015

Jan-2

016

Jan-2

017

Jan-2

018

Jan-2

019

Euro

Crisis

Begins

Japan

Tsunami/

Grexit Crisis

US

Fiscal

Cliff

Lehman

Collapse

0%

20%

40%

60%

Sig

nific

antly m

ore

op

tim

istic

Som

ew

ha

t m

ore

op

tim

istic

Un

ch

ang

ed

Som

ew

ha

t m

ore

pe

ssim

istic

Sig

nific

antly m

ore

pe

ssim

istic

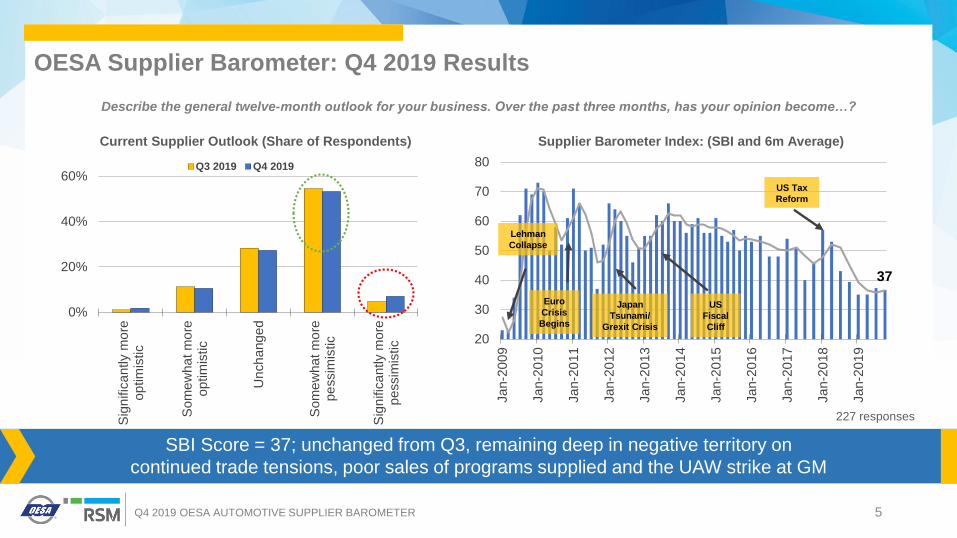

Q3 2019 Q4 2019

227 responses

Describe the general twelve-month outlook for your business. Over the past three months, has your opinion become…?

Current Supplier Outlook (Share of Respondents) Supplier Barometer Index: (SBI and 6m Average)

SBI Score = 37; unchanged from Q3, remaining deep in negative territory on

continued trade tensions, poor sales of programs supplied and the UAW strike at GM

OESA Supplier Barometer: Q4 2019 Results

US Tax

Reform

6Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

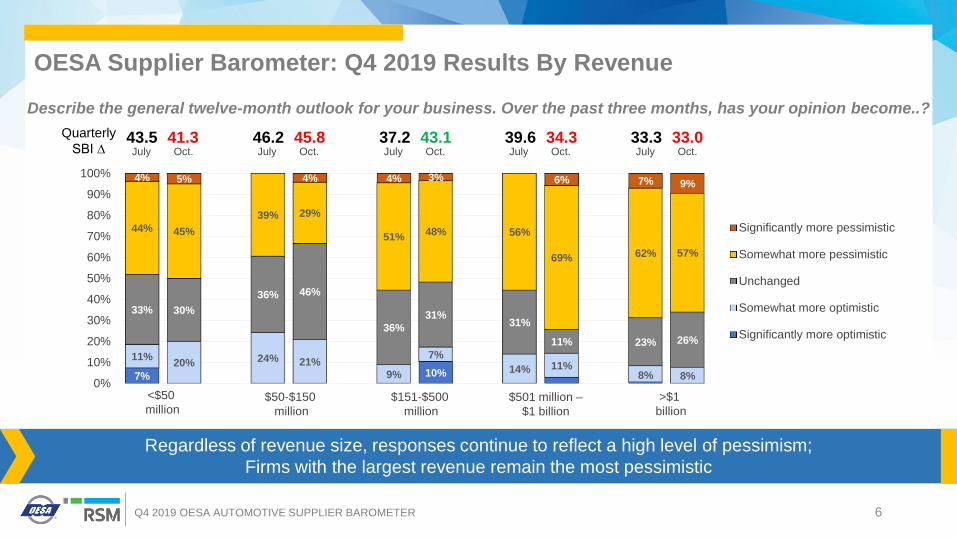

July Oct.

>$1

billion

7% 10%

11%20% 24% 21%

9%

7%

14% 11%8% 8%

33% 30%

36% 46%

36%

31%31%

11% 23% 26%

44% 45%

39% 29%

51%48% 56%

69% 62% 57%

4% 5% 4% 4% 3% 6% 7% 9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Significantly more pessimistic

Somewhat more pessimistic

Unchanged

Somewhat more optimistic

Significantly more optimistic

43.5 41.3 46.2 45.8 37.2 43.1 39.6 34.3 33.3 33.0

<$50

million$50-$150

million

$501 million –

$1 billion

Quarterly

SBI ∆

$151-$500

million

Regardless of revenue size, responses continue to reflect a high level of pessimism;

Firms with the largest revenue remain the most pessimistic

OESA Supplier Barometer: Q4 2019 Results By Revenue

Describe the general twelve-month outlook for your business. Over the past three months, has your opinion become..?

July Oct. July Oct. July Oct. July Oct.

7Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

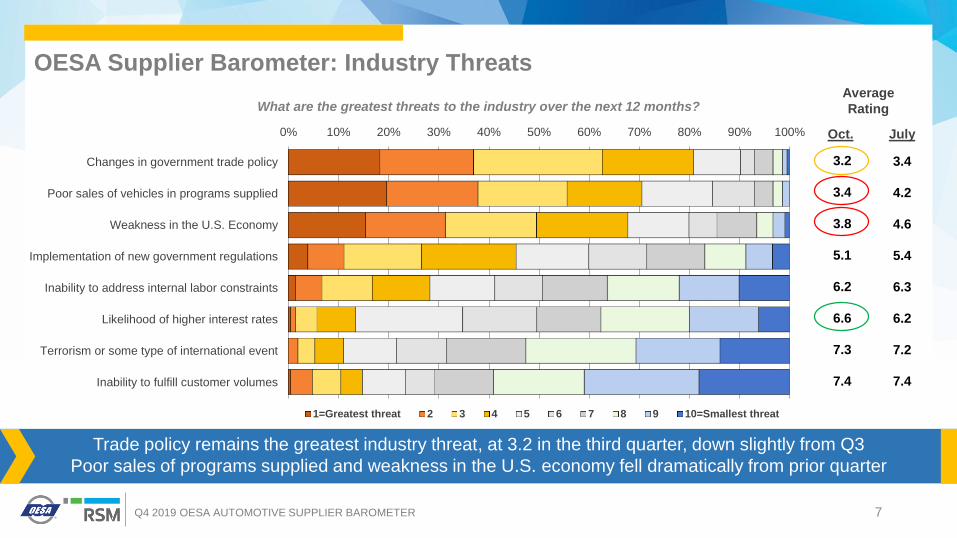

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Changes in government trade policy

Poor sales of vehicles in programs supplied

Weakness in the U.S. Economy

Implementation of new government regulations

Inability to address internal labor constraints

Likelihood of higher interest rates

Terrorism or some type of international event

Inability to fulfill customer volumes

1=Greatest threat 2 3 4 5 6 7 8 9 10=Smallest threat

Average

Rating

3.2

3.4

3.8

5.1

6.2

6.6

7.3

7.4

3.4

4.2

4.6

5.4

6.3

6.2

7.2

7.4

JulyOct.

Trade policy remains the greatest industry threat, at 3.2 in the third quarter, down slightly from Q3

Poor sales of programs supplied and weakness in the U.S. economy fell dramatically from prior quarter

OESA Supplier Barometer: Industry Threats

What are the greatest threats to the industry over the next 12 months?

8Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

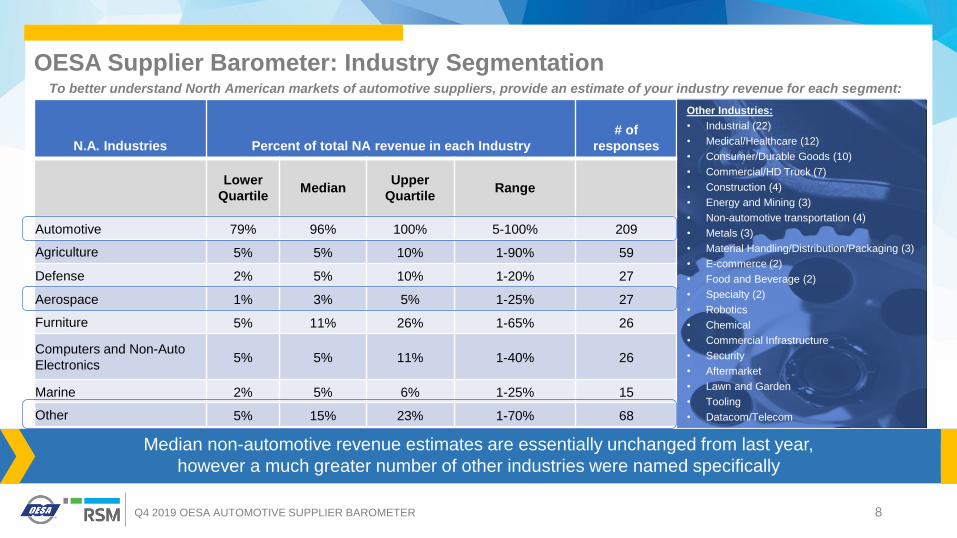

OESA Supplier Barometer: Industry Segmentation

N.A. Industries Percent of total NA revenue in each Industry

# of

responses

Lower

Quartile Median

Upper

QuartileRange

Automotive 79% 96% 100% 5-100% 209

Agriculture 5% 5% 10% 1-90% 59

Defense 2% 5% 10% 1-20% 27

Aerospace 1% 3% 5% 1-25% 27

Furniture 5% 11% 26% 1-65% 26

Computers and Non-Auto

Electronics5% 5% 11% 1-40% 26

Marine 2% 5% 6% 1-25% 15

Other 5% 15% 23% 1-70% 68

To better understand North American markets of automotive suppliers, provide an estimate of your industry revenue for each segment:

Other Industries:

• Industrial (22)

• Medical/Healthcare (12)

• Consumer/Durable Goods (10)

• Commercial/HD Truck (7)

• Construction (4)

• Energy and Mining (3)

• Non-automotive transportation (4)

• Metals (3)

• Material Handling/Distribution/Packaging (3)

• E-commerce (2)

• Food and Beverage (2)

• Specialty (2)

• Robotics

• Chemical

• Commercial Infrastructure

• Security

• Aftermarket

• Lawn and Garden

• Tooling

• Datacom/Telecom

Median non-automotive revenue estimates are essentially unchanged from last year,

however a much greater number of other industries were named specifically

9Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

Human Resources and Talent

10Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

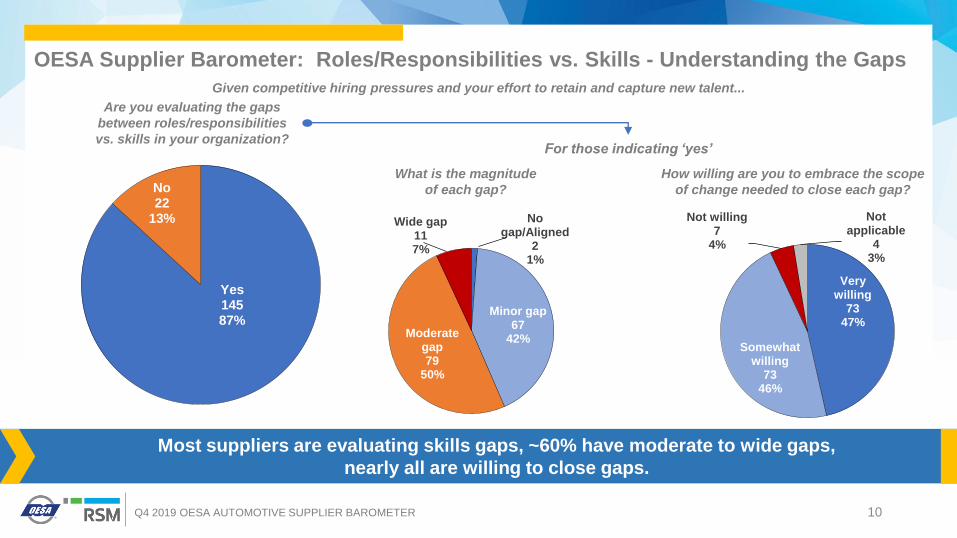

Yes14587%

No22

13% No gap/Aligned

21%

Minor gap 67

42%Moderate gap 79

50%

Wide gap 117%

Very willing

7347%

Somewhat willing

7346%

Not willing 7

4%

Not applicable

43%

For those indicating ‘yes’

Given competitive hiring pressures and your effort to retain and capture new talent...

How willing are you to embrace the scope

of change needed to close each gap?

What is the magnitude

of each gap?

Are you evaluating the gaps

between roles/responsibilities

vs. skills in your organization?

OESA Supplier Barometer: Roles/Responsibilities vs. Skills - Understanding the Gaps

Most suppliers are evaluating skills gaps, ~60% have moderate to wide gaps,

nearly all are willing to close gaps.

11Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

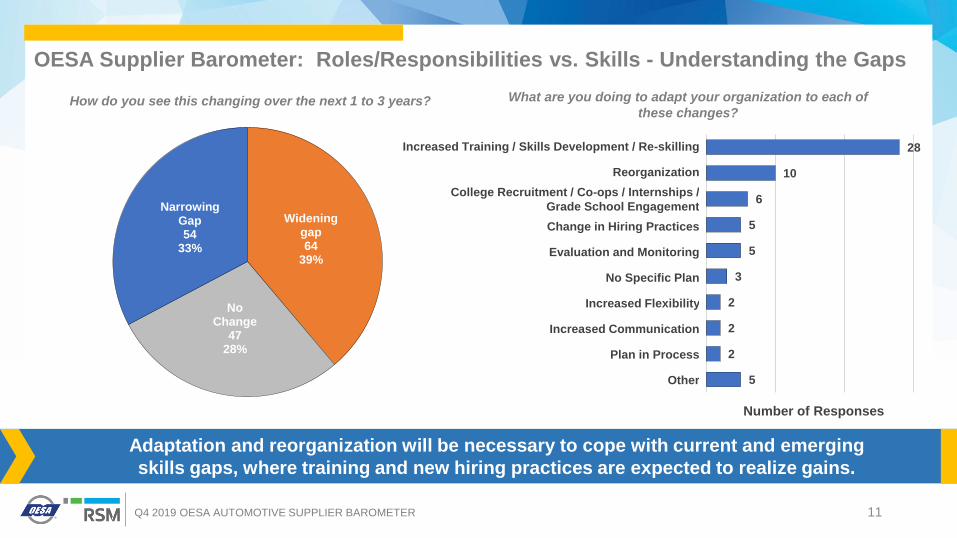

How do you see this changing over the next 1 to 3 years? What are you doing to adapt your organization to each of

these changes?

OESA Supplier Barometer: Roles/Responsibilities vs. Skills - Understanding the Gaps

Widening gap64

39%

No Change

4728%

Narrowing Gap54

33%

28

10

6

5

5

3

2

2

2

5

Increased Training / Skills Development / Re-skilling

Reorganization

College Recruitment / Co-ops / Internships /

Grade School Engagement

Change in Hiring Practices

Evaluation and Monitoring

No Specific Plan

Increased Flexibility

Increased Communication

Plan in Process

Other

Number of Responses

Adaptation and reorganization will be necessary to cope with current and emerging

skills gaps, where training and new hiring practices are expected to realize gains.

12Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

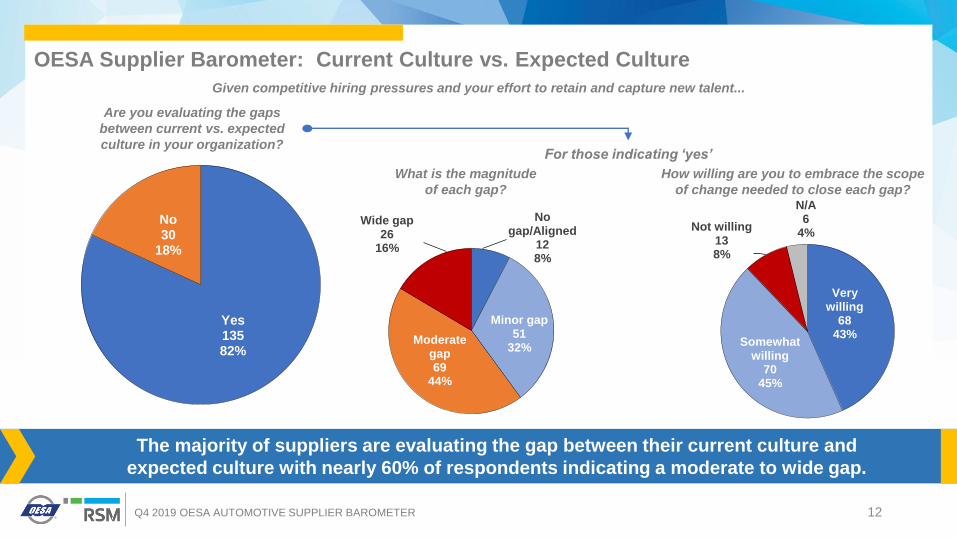

Yes13582%

No30

18%

No gap/Aligned

128%

Minor gap 51

32%Moderate

gap 69

44%

Wide gap 26

16%

Very willing

6843%

Somewhat willing

7045%

Not willing 138%

N/A6

4%

For those indicating ‘yes’

Given competitive hiring pressures and your effort to retain and capture new talent...

How willing are you to embrace the scope

of change needed to close each gap?

What is the magnitude

of each gap?

Are you evaluating the gaps

between current vs. expected

culture in your organization?

OESA Supplier Barometer: Current Culture vs. Expected Culture

The majority of suppliers are evaluating the gap between their current culture and

expected culture with nearly 60% of respondents indicating a moderate to wide gap.

13Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

How do you see this changing over the next 1 to 3 years? What are you doing to adapt your organization to each of

these changes?

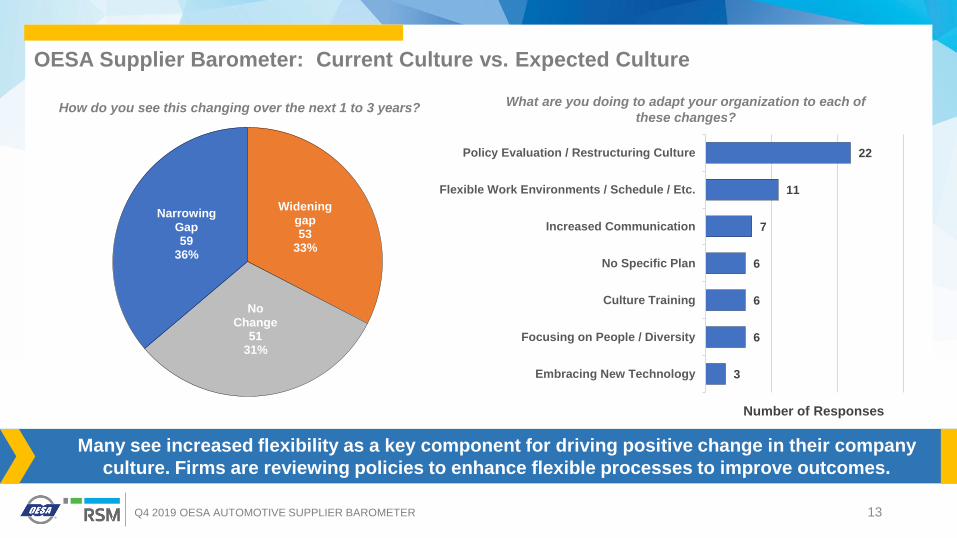

Many see increased flexibility as a key component for driving positive change in their company

culture. Firms are reviewing policies to enhance flexible processes to improve outcomes.

OESA Supplier Barometer: Current Culture vs. Expected Culture

Widening gap53

33%

No Change

5131%

Narrowing Gap59

36%

22

11

7

6

6

6

3

Policy Evaluation / Restructuring Culture

Flexible Work Environments / Schedule / Etc.

Increased Communication

No Specific Plan

Culture Training

Focusing on People / Diversity

Embracing New Technology

Number of Responses

14Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

How do you see this changing over the next 1 to 3 years? What are you doing to adapt your organization to each of

these changes?

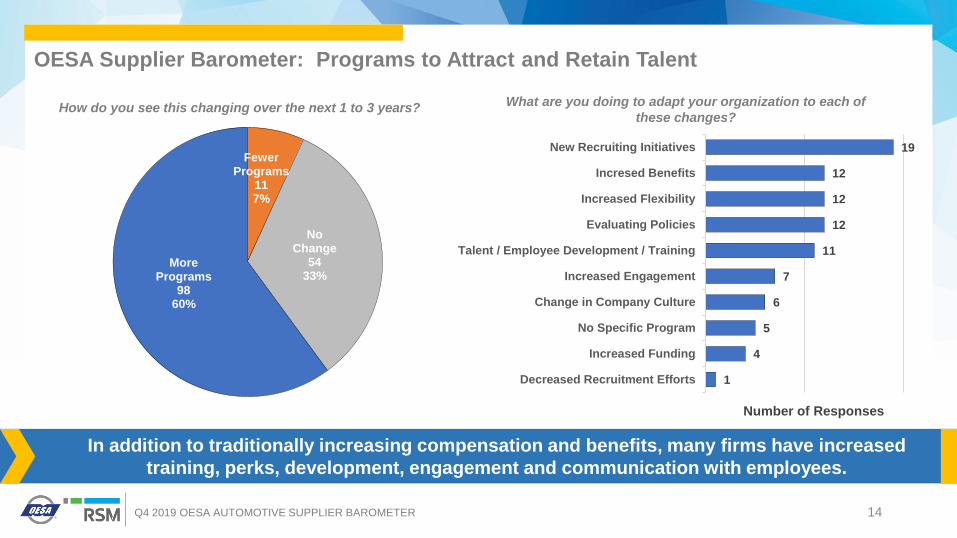

In addition to traditionally increasing compensation and benefits, many firms have increased

training, perks, development, engagement and communication with employees.

OESA Supplier Barometer: Programs to Attract and Retain Talent

Fewer Programs

117%

No Change

5433%

More Programs

9860%

19

12

12

12

11

7

6

5

4

1

New Recruiting Initiatives

Incresed Benefits

Increased Flexibility

Evaluating Policies

Talent / Employee Development / Training

Increased Engagement

Change in Company Culture

No Specific Program

Increased Funding

Decreased Recruitment Efforts

Number of Responses

15Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

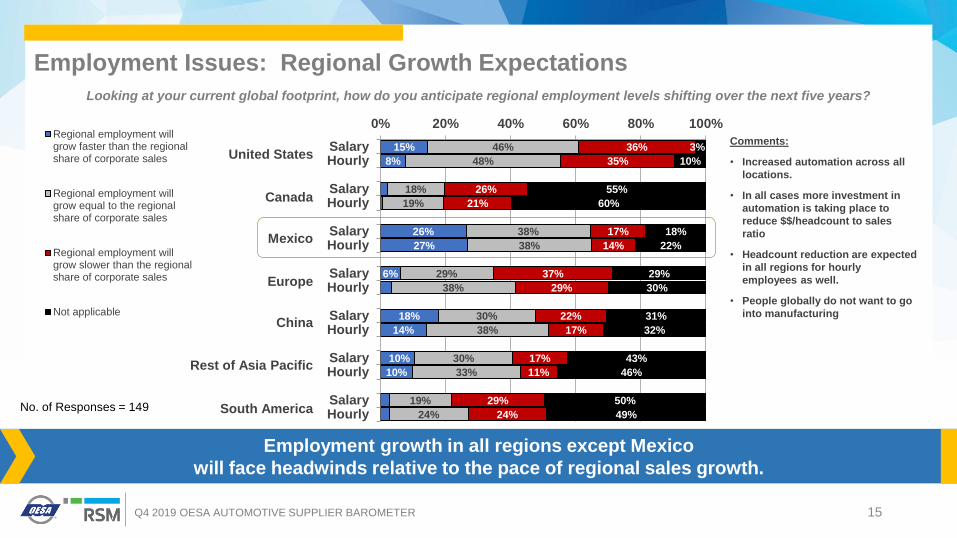

No. of Responses = 149

15%

8%

26%

27%

6%

18%

14%

10%

10%

46%

48%

18%

19%

38%

38%

29%

38%

30%

38%

30%

33%

19%

24%

36%

35%

26%

21%

17%

14%

37%

29%

22%

17%

17%

11%

29%

24%

3%

10%

55%

60%

18%

22%

29%

30%

31%

32%

43%

46%

50%

49%

0% 20% 40% 60% 80% 100%

SalaryHourly

SalaryHourly

SalaryHourly

SalaryHourly

SalaryHourly

SalaryHourly

SalaryHourly

Regional employment willgrow faster than the regionalshare of corporate sales

Regional employment willgrow equal to the regionalshare of corporate sales

Regional employment willgrow slower than the regionalshare of corporate sales

Not applicable

United States

Canada

Mexico

Europe

China

South America

Looking at your current global footprint, how do you anticipate regional employment levels shifting over the next five years?

Employment growth in all regions except Mexico

will face headwinds relative to the pace of regional sales growth.

Employment Issues: Regional Growth Expectations

Rest of Asia Pacific

Comments:

• Increased automation across all

locations.

• In all cases more investment in

automation is taking place to

reduce $$/headcount to sales

ratio

• Headcount reduction are expected

in all regions for hourly

employees as well.

• People globally do not want to go

into manufacturing

16Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

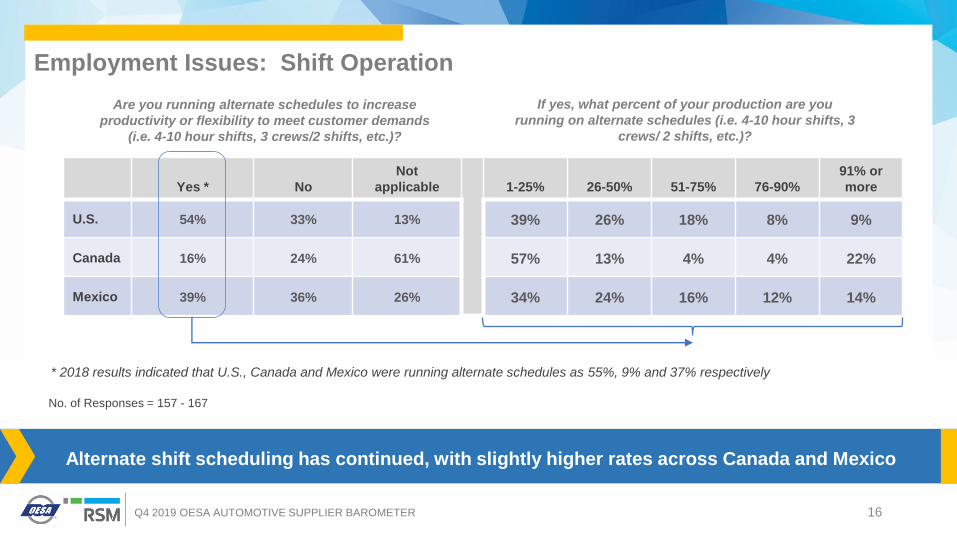

Yes * No

Not

applicable 1-25% 26-50% 51-75% 76-90%

91% or

more

U.S. 54% 33% 13% 39% 26% 18% 8% 9%

Canada 16% 24% 61% 57% 13% 4% 4% 22%

Mexico 39% 36% 26% 34% 24% 16% 12% 14%

* 2018 results indicated that U.S., Canada and Mexico were running alternate schedules as 55%, 9% and 37% respectively

No. of Responses = 157 - 167

Are you running alternate schedules to increase

productivity or flexibility to meet customer demands

(i.e. 4-10 hour shifts, 3 crews/2 shifts, etc.)?

If yes, what percent of your production are you

running on alternate schedules (i.e. 4-10 hour shifts, 3

crews/ 2 shifts, etc.)?

Alternate shift scheduling has continued, with slightly higher rates across Canada and Mexico

Employment Issues: Shift Operation

17Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

28%

19%20%

15%

7%

5%6%

44%

18%

14%

4%

1%18%

23%

30%22%

10%

10%

4% 1%

Less than 2.5%

2.5 - 5%

5 - 7.5%

7.5 - 10%

10 - 15%

15 - 20%

More than 20%

16%

15%

20%16%

11%

6%

16%

Salaried Workers

Hourly Workers

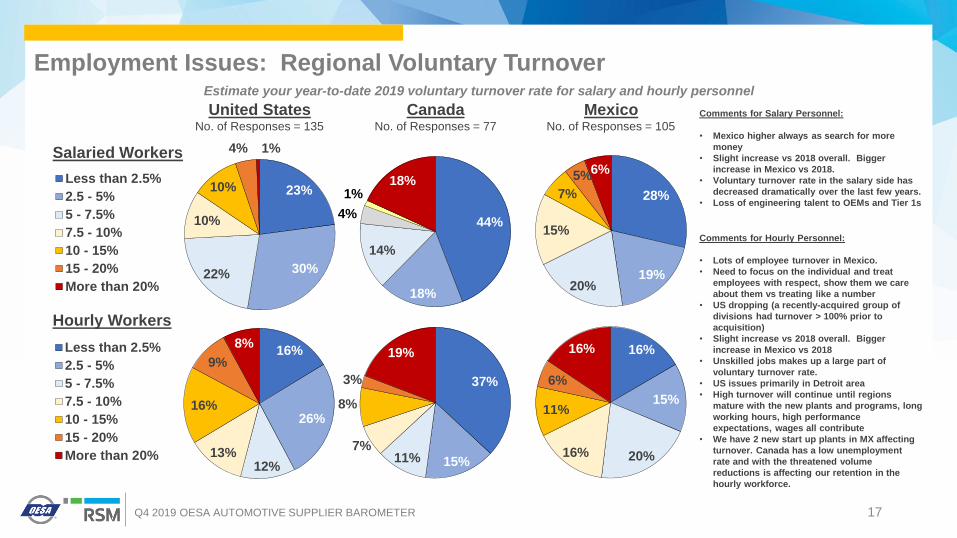

United States Canada MexicoNo. of Responses = 135 No. of Responses = 77 No. of Responses = 105

Estimate your year-to-date 2019 voluntary turnover rate for salary and hourly personnel

16%

26%

12%13%

16%

9%

8%Less than 2.5%

2.5 - 5%

5 - 7.5%

7.5 - 10%

10 - 15%

15 - 20%

More than 20%

Employment Issues: Regional Voluntary Turnover

37%

15%11%7%

8%

3%

19%

Comments for Salary Personnel:

• Mexico higher always as search for more

money

• Slight increase vs 2018 overall. Bigger

increase in Mexico vs 2018.

• Voluntary turnover rate in the salary side has

decreased dramatically over the last few years.

• Loss of engineering talent to OEMs and Tier 1s

Comments for Hourly Personnel:

• Lots of employee turnover in Mexico.

• Need to focus on the individual and treat

employees with respect, show them we care

about them vs treating like a number

• US dropping (a recently-acquired group of

divisions had turnover > 100% prior to

acquisition)

• Slight increase vs 2018 overall. Bigger

increase in Mexico vs 2018

• Unskilled jobs makes up a large part of

voluntary turnover rate.

• US issues primarily in Detroit area

• High turnover will continue until regions

mature with the new plants and programs, long

working hours, high performance

expectations, wages all contribute

• We have 2 new start up plants in MX affecting

turnover. Canada has a low unemployment

rate and with the threatened volume

reductions is affecting our retention in the

hourly workforce.

18Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

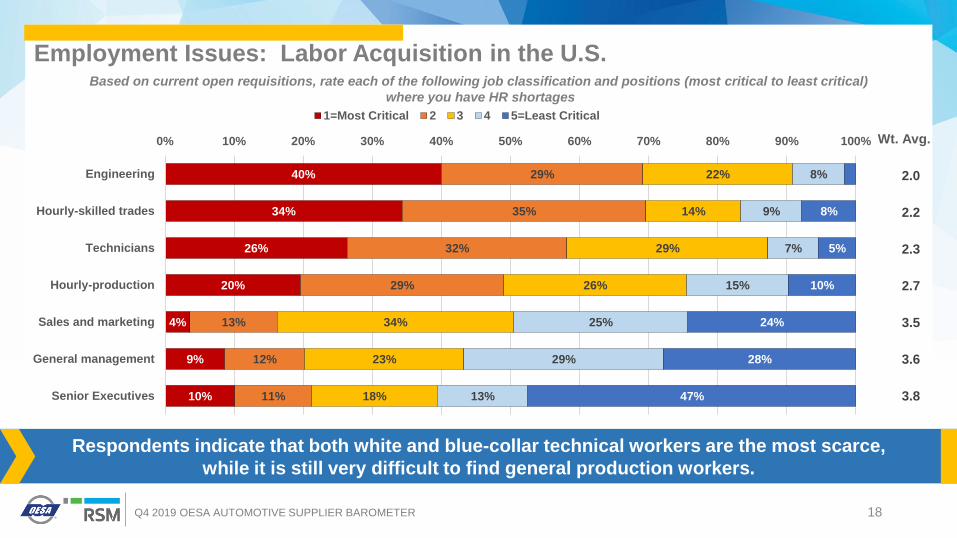

Respondents indicate that both white and blue-collar technical workers are the most scarce,

while it is still very difficult to find general production workers.

Wt. Avg.

Employment Issues: Labor Acquisition in the U.S.Based on current open requisitions, rate each of the following job classification and positions (most critical to least critical)

where you have HR shortages

40%

34%

26%

20%

4%

9%

10%

29%

35%

32%

29%

13%

12%

11%

22%

14%

29%

26%

34%

23%

18%

8%

9%

7%

15%

25%

29%

13%

8%

5%

10%

24%

28%

47%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Engineering

Hourly-skilled trades

Technicians

Hourly-production

Sales and marketing

General management

Senior Executives

1=Most Critical 2 3 4 5=Least Critical

2.0

2.2

2.3

2.7

3.5

3.6

3.8

19Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

Based on current open requisitions, rate each of the following job classification and positions (most critical to least critical)

where you have HR shortages

Employment Issues: Labor Acquisition in Canada

Technical knowledge shortages are spread throughout Canada as well,

but more so on the shop floor.

Wt. Avg.

23%

29%

24%

17%

11%

45%

25%

28%

17%

7%

15%

9%

19%

29%

31%

38%

18%

30%

17%

6%

11%

10%

21%

25%

19%

4%

6%

7%

7%

7%

39%

37%

70%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Technicians

Hourly-skilled Trades

Engineering

Hourly-production

General Management

Sales and Marketing

Senior Executives

1=Most Critical 2 3 4 5=Least Critical

2.3

2.4

2.5

2.8

3.8

3.8

4.3

20Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

Based on current open requisitions, rate each of the following job classification and positions (most critical to least critical)

where you have HR shortages

Employment Issues: Labor Acquisition in Mexico

Technical knowledge shortages are abundant in Mexico as are shortages of hourly production

workers, yet the supply imbalance for general office personnel is not as acute.

Wt. Avg.

38%

26%

29%

21%

4%

5%

3%

26%

37%

25%

34%

23%

9%

12%

17%

25%

21%

29%

14%

22%

19%

13%

4%

18%

7%

27%

28%

17%

5%

8%

7%

10%

31%

37%

49%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Hourly-skilled Trades

Technicians

Hourly-production

Engineering

General Management

Sales and Marketing

Senior Executives

1=Most Critical 2 3 4 5=Least Critical

2.2

2.3

2.5

2.5

3.6

3.8

4.0

21Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

22%

37%

28%

21%

16%

42%

23%

35%

26%

27%

10%

19%

17%

14%

27%

22%

30%

10%

10%

13%

18%

14%

20%

7%

13%

10%

9%

22%

40%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Mechanical Engineer

Software Engineer/Computer Scientist

Electrical Engineer

Industrial Engineer

Chemical Engineer

Aerospace Engineer

1=Most critical 2 3 4 5=Least critical

2.4

2.4

2.4

2.7

3.0

3.9

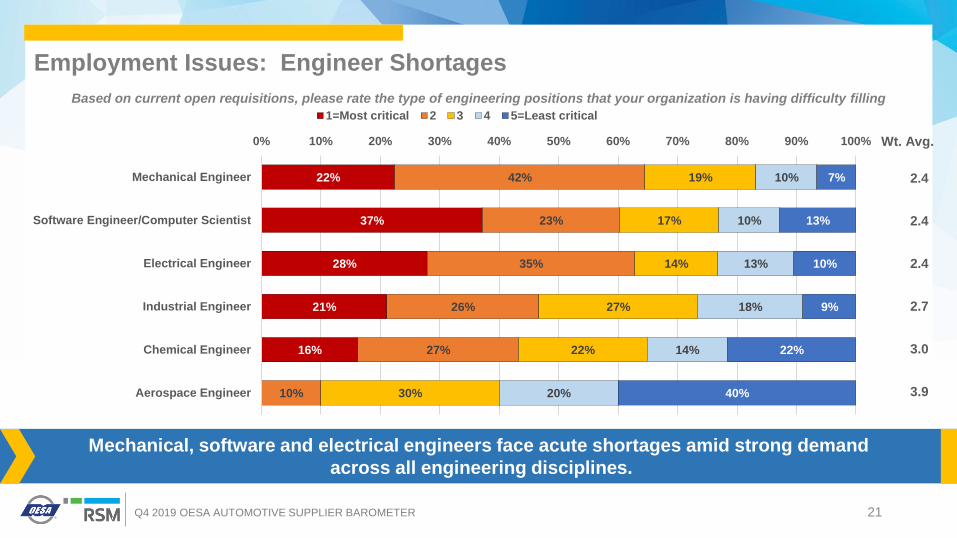

Based on current open requisitions, please rate the type of engineering positions that your organization is having difficulty filling

Mechanical, software and electrical engineers face acute shortages amid strong demand

across all engineering disciplines.

Wt. Avg.

Employment Issues: Engineer Shortages

22Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

64%

35%

24%

26%

8%

13%

27%

9%

28%

51%

49%

65%

0% 20% 40% 60% 80% 100%

Flexible Schedule

Flexible Work Space

Cross-functional Job Rotation

Increased Paid or Unpaid Time-off Allowances

Implemented Planning to implement Neither

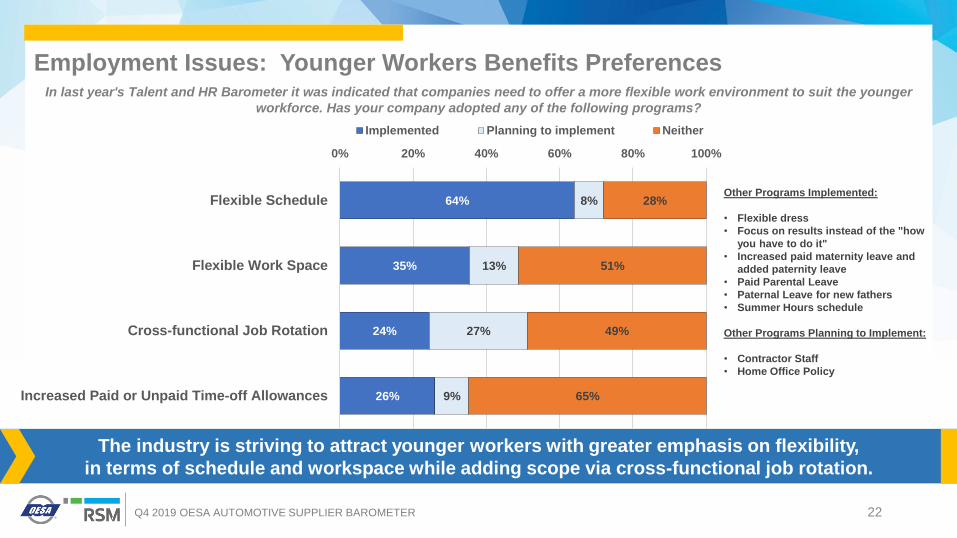

In last year's Talent and HR Barometer it was indicated that companies need to offer a more flexible work environment to suit the younger

workforce. Has your company adopted any of the following programs?

The industry is striving to attract younger workers with greater emphasis on flexibility,

in terms of schedule and workspace while adding scope via cross-functional job rotation.

Employment Issues: Younger Workers Benefits Preferences

Other Programs Implemented:

• Flexible dress

• Focus on results instead of the "how

you have to do it"

• Increased paid maternity leave and

added paternity leave

• Paid Parental Leave

• Paternal Leave for new fathers

• Summer Hours schedule

Other Programs Planning to Implement:

• Contractor Staff

• Home Office Policy

23Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

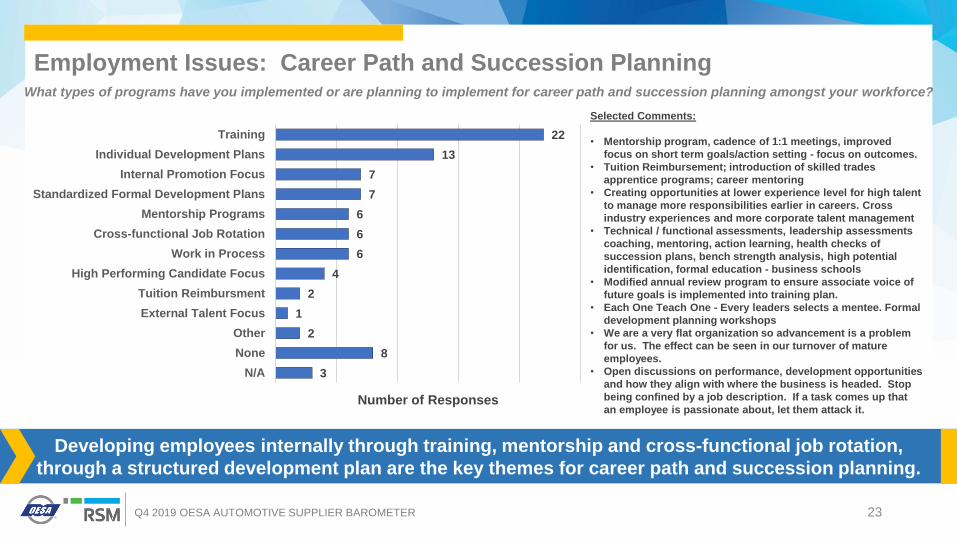

What types of programs have you implemented or are planning to implement for career path and succession planning amongst your workforce?

Developing employees internally through training, mentorship and cross-functional job rotation,

through a structured development plan are the key themes for career path and succession planning.

Employment Issues: Career Path and Succession Planning

22

13

7

7

6

6

6

4

2

1

2

8

3

Training

Individual Development Plans

Internal Promotion Focus

Standardized Formal Development Plans

Mentorship Programs

Cross-functional Job Rotation

Work in Process

High Performing Candidate Focus

Tuition Reimbursment

External Talent Focus

Other

None

N/A

Number of Responses

Selected Comments:

• Mentorship program, cadence of 1:1 meetings, improved

focus on short term goals/action setting - focus on outcomes.

• Tuition Reimbursement; introduction of skilled trades

apprentice programs; career mentoring

• Creating opportunities at lower experience level for high talent

to manage more responsibilities earlier in careers. Cross

industry experiences and more corporate talent management

• Technical / functional assessments, leadership assessments

coaching, mentoring, action learning, health checks of

succession plans, bench strength analysis, high potential

identification, formal education - business schools

• Modified annual review program to ensure associate voice of

future goals is implemented into training plan.

• Each One Teach One - Every leaders selects a mentee. Formal

development planning workshops

• We are a very flat organization so advancement is a problem

for us. The effect can be seen in our turnover of mature

employees.

• Open discussions on performance, development opportunities

and how they align with where the business is headed. Stop

being confined by a job description. If a task comes up that

an employee is passionate about, let them attack it.

24Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

36%

34%

18%

13%

9%

14%

9%

4%

4%

38%

35%

25%

25%

28%

20%

23%

24%

10%

15%

13%

20%

23%

26%

20%

26%

21%

18%

8%

13%

18%

22%

21%

21%

18%

15%

22%

4%

6%

18%

17%

16%

24%

24%

36%

46%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

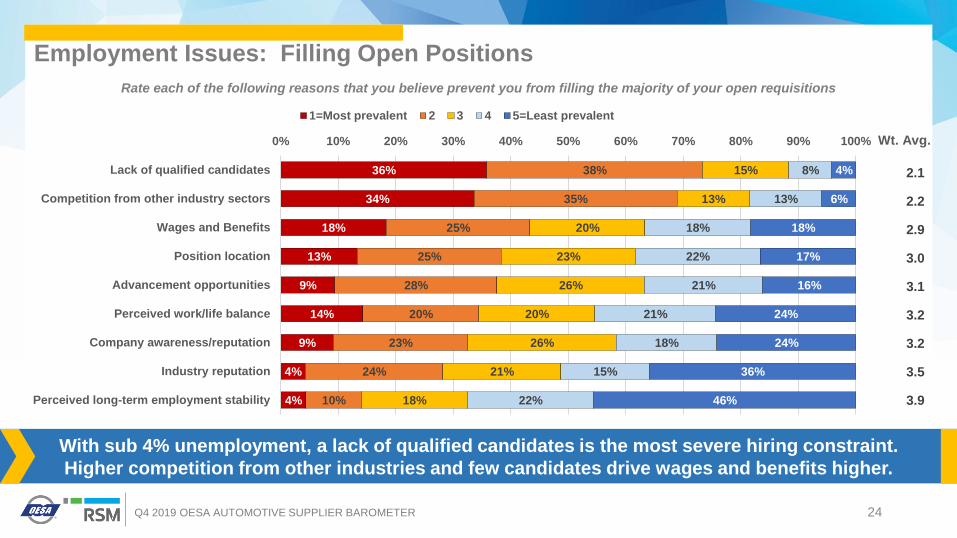

Lack of qualified candidates

Competition from other industry sectors

Wages and Benefits

Position location

Advancement opportunities

Perceived work/life balance

Company awareness/reputation

Industry reputation

Perceived long-term employment stability

1=Most prevalent 2 3 4 5=Least prevalent

Rate each of the following reasons that you believe prevent you from filling the majority of your open requisitions

2.1

2.2

2.9

3.0

3.1

3.2

3.2

3.5

3.9

Wt. Avg.

Employment Issues: Filling Open Positions

With sub 4% unemployment, a lack of qualified candidates is the most severe hiring constraint.

Higher competition from other industries and few candidates drive wages and benefits higher.

25Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

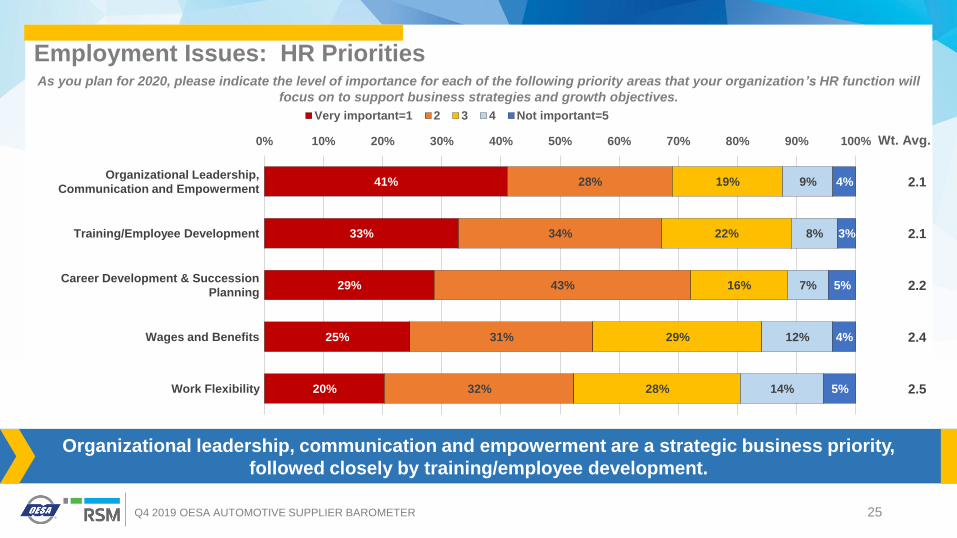

As you plan for 2020, please indicate the level of importance for each of the following priority areas that your organization’s HR function will

focus on to support business strategies and growth objectives.

Wt. Avg.

Employment Issues: HR Priorities

Organizational leadership, communication and empowerment are a strategic business priority,

followed closely by training/employee development.

41%

33%

29%

25%

20%

28%

34%

43%

31%

32%

19%

22%

16%

29%

28%

9%

8%

7%

12%

14%

4%

3%

5%

4%

5%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Very important=1 2 3 4 Not important=5

Organizational Leadership,

Communication and Empowerment

Training/Employee Development

Career Development & Succession

Planning

Wages and Benefits

Work Flexibility

2.1

2.1

2.2

2.4

2.5

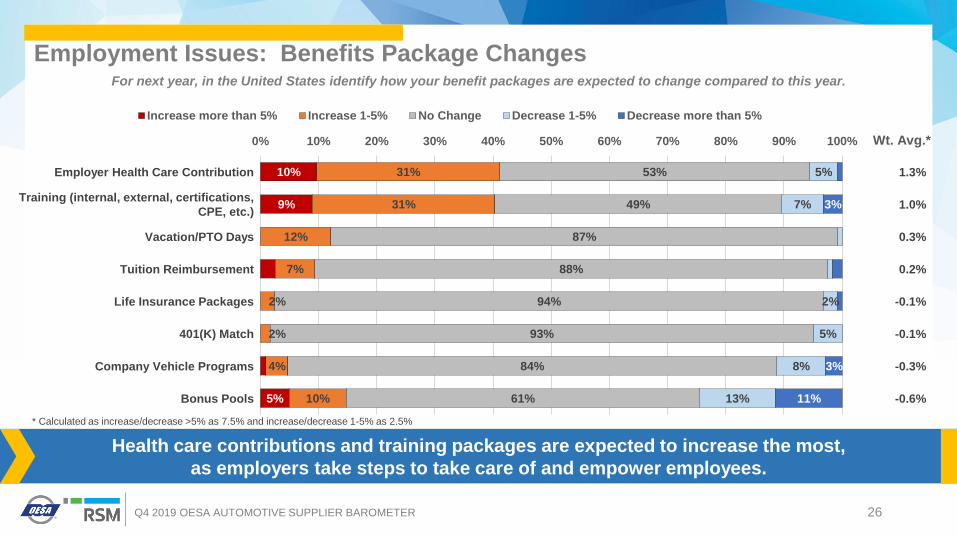

26Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

1.3%

1.0%

0.3%

0.2%

-0.1%

-0.1%

-0.3%

-0.6%

10%

9%

5%

31%

31%

12%

7%

2%

2%

4%

10%

53%

49%

87%

88%

94%

93%

84%

61%

5%

7%

2%

5%

8%

13%

3%

3%

11%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Increase more than 5% Increase 1-5% No Change Decrease 1-5% Decrease more than 5%

Employer Health Care Contribution

Training (internal, external, certifications,

CPE, etc.)

Vacation/PTO Days

Tuition Reimbursement

Life Insurance Packages

401(K) Match

Company Vehicle Programs

Bonus Pools

For next year, in the United States identify how your benefit packages are expected to change compared to this year.

Health care contributions and training packages are expected to increase the most,

as employers take steps to take care of and empower employees.

Employment Issues: Benefits Package Changes

Wt. Avg.*

* Calculated as increase/decrease >5% as 7.5% and increase/decrease 1-5% as 2.5%

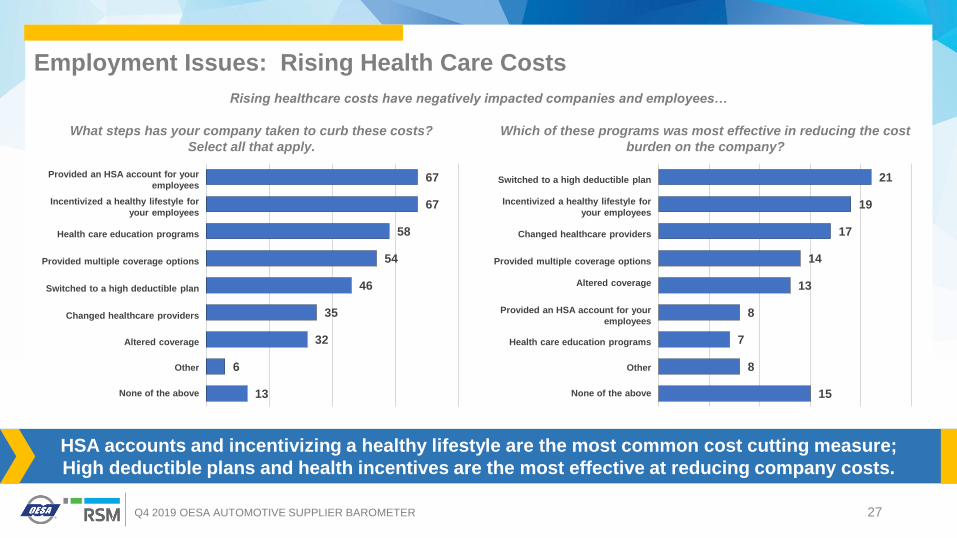

27Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

SBI Score = 53; drops 4 points from the Q1 level of 57

Tax reform supports optimism while trade and declining sales drive pessimism

Rising healthcare costs have negatively impacted companies and employees…

HSA accounts and incentivizing a healthy lifestyle are the most common cost cutting measure;

High deductible plans and health incentives are the most effective at reducing company costs.

Employment Issues: Rising Health Care Costs

What steps has your company taken to curb these costs?

Select all that apply.

Which of these programs was most effective in reducing the cost

burden on the company?

67

67

58

54

46

35

32

6

13

21

19

17

14

13

8

7

8

15

Provided an HSA account for your

employees

Incentivized a healthy lifestyle for

your employees

Health care education programs

Provided multiple coverage options

Switched to a high deductible plan

Changed healthcare providers

Altered coverage

Other

None of the above

Switched to a high deductible plan

Incentivized a healthy lifestyle for

your employees

Changed healthcare providers

Provided multiple coverage options

Altered coverage

Provided an HSA account for your

employees

Health care education programs

Other

None of the above

28Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

OESA Human Resources Council meetings focus on Talent, Success Planning and

other topics included in this quarter’s barometer.

If you are interested in learning more about the council, please contact:

Ginger Juncker, Executive Director, Councils and Member Programs

[email protected] / 248.430.5953

Karen Bohannon, Manager Administration and On-site Facilities

[email protected] / 248.430.5965

OESA Human Resources Council

29Q4 2019 OESA AUTOMOTIVE SUPPLIER BAROMETER

The information and opinions contained in this report are for general information purposes. Comments are edited only for

spelling and may contain grammatical errors due to their verbatim nature. Responses to this survey are confidential.

Therefore, only aggregated results will be reported and individual responses will not be released or shared.

Antitrust Statement:

Respondents/participants should not contact competitors to discuss responses, or to discuss the issues dealt with in the

survey. It is an absolute imperative to consult legal counsel about any contacts with competitors. All pricing and other terms

of sale decisions and negotiating strategies should be handled on an individual company basis.

OESA Automotive Supplier Barometer is a survey of the top

executives of OESA regular member companies. The OESA

Automotive Supplier Barometer takes the pulse of the suppliers'

twelve month business sentiment. In addition, it provides a snapshot

of the industry commercial issues, business environment and

business strategies that influence the supplier industry.

www.oesa.org.

Survey Methodology

• Data collected October 15 – October 26 via invitation to online survey.

• Executives of OESA supplier companies.

• 145 complete survey responses were received, with 227 responses total.

Contacts

Mike Jackson

Executive Director

Strategy and Research

248.430.5954

Joe Zaciek

Manager

Research and Industry Analysis

248.430.5960

Larry Keyler

RSM Detroit Office Managing Partner

317.805.6205

Original Equipment Suppliers Association

25925 Telegraph Road

Suite 350

Southfield, Michigan 48033

RSM US LLP is the leading provider of audit, tax and consulting

services focused on the middle market, with nearly 10,000

professionals nationwide. It is a licensed CPA firm and the U.S.

member of RSM International, a global network of independent audit,

tax and consulting firms with more than 41,000 people in 116

countries. RSM uses its deep understanding of the needs and

aspirations of clients to help them succeed. For more information, visit

rsmus.com, like us on Facebook at RSM US LLP, follow us on Twitter

@RSMUSLLP or connect with us on LinkedIn.