Embed Size (px)

Citation preview

0

Occupational Certificate Tax Professional Knowledge (Syllabus Specificated) Curriculum Guide 2020

1

I. Background Pursuant to the mandate of the Quality Council for Trades and Occupations, the Tax Professional programme requires three components for passage. These components consist of: (i) a knowledge component, (ii) a practical component, and (iii) a workplace / work training component. The purpose of this document is to provide the full spectrum of learning required for the knowledge component. This knowledge requires an understanding of legislative acts and authoritative interpretations as listed below (include SARS guides which are not officially viewed as dispositive). The curriculum outline also includes recommended study materials (in this case, “South African Income Tax” by Silke). Trainees (and Skills Development Providers) are free to utilise other study materials that cover the same learning coverage.

II. Learning Objectives Tax Professionals have multiple skills. Tax professionals can handle tax compliance, tax controversy and tax advisory. Tax professionals may work in a range of knowledge areas or may be specialised to a select few. The core knowledge areas of tax directly or indirectly pertain to company income tax (IT14 company returns), value-added tax (VAT 201 returns), personal income taxes (IT12 personal returns) and employer payroll taxes (EMP 501 employer returns). Some of these knowledge areas include cross-border (international) considerations. Tax Professionals deal with a range of clients, mostly businesses and high net-worth individuals / families. Most businesses are of a medium-to-large nature (typically exceeding R20-to-25 million in revenue and possibly including listed companies). Tax Professionals must have analytical skills. They need to be able to assess risk, especially in terms of their advisory capabilities. Tax Professionals need to be able to develop and organise arguments with credibility, both in terms of tax controversy and advisory. Understanding compliance is key, including audit review. The primary role of a Tax Technician is compliance. Compliance involves more than just preparation but assurance that the numbers and statements satisfy the full standards of law and due diligence regarding the facts provided.

2

III. Overall Knowledge Modules Unlike the syllabus of many tax programmes, the syllabus for the Tax Professional programme has been specifically arranged in a logical / transaction order. Tax law needs to be understood in a practical and transactional setting. Most of the coverage relates to income tax with a secondary emphasis on value-added tax and other secondary taxes. In terms of specific categories, the Tax Professional Programme falls into ten knowledge modules, as follows:

Fundamentals 1. General Tax Fundamentals 2. Advanced Tax Fundamentals 3. Accounting for Tax Fundamentals 4. International Tax Fundamentals

Core Subspecialties 5. Corporate / Shareholder Transactional Taxation 6. Indirect Taxation 7. Personal Taxation 8. Employment Payroll Taxation 9. Wealth Succession Planning (Lifetime and Death Transfers)

Tax Controversy and Practice

10. Tax Administration and Practice Management

III. Detailed Coverage

Fundamentals – Overall note: The purpose of the first four modules is to cover the essential basics associated with income taxation. This analytical framework is expected of every tax trainee in the Tax Professional programme.

1. General Tax Fundamentals Trainees are expected to have an in-depth understanding of the basic conceptual framework associated with income tax. This segment represents the core basics at both an academic level and for practical application.

Fundamental Conceptual Pillar I: Overall Income Tax Calculation Trainees must understand the core formula associated with the income tax calculation to determine taxable income as applied to a specific taxpayer at a specified tax rate. This formula essentially acts as the “spinal cord” for the income tax system. More specifically, this pillar

3

mainly covers the net profit (i.e. taxable income) formula, tax rates, identification of key taxpayer types, and the nature of annual tax periods.

Fundamental Conceptual Pillar II: General Inflows & Outflows This pillar covers general revenue flows and outflowing expenditures. These flows include items, such as services, general rentals and related operational expenses. At issue in a tax sense is whether and when to account for these items as well as the calculation of amounts. Part A: Gross Income / Exempt Income: The income tax formula begins with the

calculation of receipts and accruals. These receipts and accruals are taken into account during one or more years of assessments under the general “gross income” formula definition (before paragraph (a)). Special additional inclusions of gross income exist to override the potential treatment of certain receipts and accruals as capital in nature and further special inclusions can be found elsewhere in the income tax act (via paragraph (n) of the section 1 “gross income” definition). In a limited number of cases, certain exemptions exist (under section 10). These exemptions can be in regards to a whole entity (e.g. a sphere of government) or in regards to particular categories of receipts and accruals (e.g. dividends).

Part B: Deductions and Assessed Losses: The income tax formula then allows

deductions to be subtracted so as to determine “taxable income”. Deductions are initially found in section 11(a) under the general deduction formula associated with trading activities. Special deductions also exist in other paragraphs of section 11 or are derived from other sections of the income tax act (with section 11(x), thereby bringing these other sections technically into operation). Deductions may stem from expenditures incurred during the current year of assessment or as excess deductions from prior years (known as assessed losses).

Fundamental Conceptual Pillar III: General Property Disposals

The disposal of property operates differently in a tax sense from the general flow of revenue and expense outlined in Pillar II. Properties of this nature fall into three practical groups: immovable property, movable property and intellectual property. Part A: Character Determination of Overall Disposal: In terms of income tax, each of

these property groups will typically be classified as trading stock, capital assets and allowance assets for tax purposes. The question of classification is generally based on facts-and-circumstance (e.g. ordinary versus capital) and must be determined upfront because each classified group has its own system of determining gain or loss (as well as the impact on tax rates).

Part B: Disposals of an ordinary nature: The disposal of assets giving rise or ordinary

gain and loss is generally referred to as trading stock. Trading stock largely consists of business inventory but may also consist of others assets held largely for disposal (as opposed to assets held for use or long-term investment).

4

Part C: Disposals of a capital nature: The disposal of capital assets fall entirely under

the capital gain system of the 8th Schedule. These extensive rules have their own system of deemed disposals, value determinations, anti-loss rules and exclusions.

Part D: Impairing Allowance / Depreciable Assets and Subsequent Disposals: Allowance

assets fall under a mix of ordinary revenue / loss and capital gain / loss. In the main, allowances assets are capital assets that can be depreciated / amortized over the life of the asset, thereby generating a stream of ordinary deductions. This system of depreciation / amortization is roughly akin to the financial accounting system of impairment. The disposal of these assets give rise to a mix of ordinary and capital consequences.

Fundamental Conceptual Pillar IV: Tax Reporting and Payments

Tax practice is not just a theoretical exercise. Once the core calculations are complete, the information must be properly submitted to SARS. Taxpayers must make payment or claim refunds. Income tax payments are not just a year-end event, but must also be preceded by interim payments (known as provisional taxes). 2. Advanced Tax Fundamentals The tax law contains many subsystems in addition to the core conceptual systems outlined above. Each of these subsystems is self-contained – some defer or accelerate gains and losses while others ensuring appropriate matching principles. The purpose of this core pillar is to introduce a staple array of unique subsystems that commonly apply to local business activities (e.g. as a company operation or as a sole proprietorship). Part A: Capital and allowance asset rollovers and deferrals: The tax system contains

various rollover / deferral regimes. In these regimes, gain or loss is disregarded upon disposal when certain conditions apply. These conditions typically require a reinvestment in comparable assets or a transfer within the same economic unit. The deferred gain / loss will only be triggered upon a subsequent disposal. This part also serves as an important entry to other more advanced rollover regimes in specialised areas (e.g. particularly corporate formations and reorganisations).

Part B: Leases: Commercial leases are a frequent method of business occupation.

Under this subsystem, there is a dual impact – a deduction for the rent paid by the commercial lessee (i.e. tenant) and gross income for the commercial lessor (i.e. a landlord). Other dual systems are required in the case of lease premiums and lessee improvements on lessor land.

Part C: Debt / Loans (Initial Funding and Repayments): The most common form of

business financing is via borrowing (e.g. from a bank or other source). Lending has two elements – the underlying capital loan and the interest charge. This part covers the initial lending and repayment (Note: Failure to repay creates

5

another set of rules for creditors who may be eligible to claim a capital /ordinary loss and for debtors who may have resultant capital gain / ordinary revenue).

Part D: Foreign currency: South African businesses regularly utilise foreign currency in

the case of imports and exports as part of everyday operations. Taxation of foreign currency is very unique among asset classes in that foreign currency gains and losses are generally taken into account annually even if not disposed of (i.e. still held at annual year-end).

Part E: Government grants: Grants may be exempt, but the use of government funds

can hardly be viewed as a taxpayer expenditure incurred. This subsystem ensures that the direct or indirect receipt of government funds is not reduced in value by the burden of tax. However, taxpayers cannot claim a deduction to the extent expenses are subsidised by government grants nor can assets purchased with subsidised funds be considered a taxpayer cost.

Part F: Business incentives: Government frequently utilises the tax system to

incentivise certain activities. This part focuses on a few frequently used incentives with either a business focus or an employment focus. While incentives may differ, the overall structure contains recurring similarities. For purposes of this qualification, the knowledge level is required to be at a diagnostic level only.

Part G: Small and Micro Business Relief: Like most countries, South Africa provides

special measures of relief for small and micro-business to ease the tax burden and reduce compliance. In the case of tax professionals, the core focus will be on small business relief (as opposed to the micro-business turnover tax, which is infrequently used).

Part H: Specialised Industries (Farming and Mining): Certain businesses operate

uniquely, requiring their own set of special tax rules. In South Africa, the most notable regimes are for farming and mining (i.e. primary sector). Farming may have a crop focus or a livestock focus. Mining typically encounters large capital intensity and timing challenges in terms of price volatility. For purposes of this qualification, the knowledge level is required to be at a diagnostic level only.

This module closes with the concept of tax avoidance, which tends to be a permeating issue throughout the tax system. Although the tax law has a strong preference for hard objective rules over (subjective (e.g. intention-based) rules, concerns have grown that clever tax planners can misuse those rule so that the technical wording works against the underlying intention. Trainees must accordingly focus on the judicial doctrine of substance-over-form, the general anti-avoidance rule and other longstanding subjective anti-avoidance rules that are recurrent concern for planning, compliance a controversy purposes. 3. Accounting for Tax Fundamentals Accounting information is often the key facts relied upon as evidence for tax return calculations. Compliance requires a continuous connection between accounting and tax. Tax

6

planning must synchronise both the tax and the accounting so that the substance of the plan can be fully understood and justified. Tax controversy can often turn on the accounting because the accounting may be the best demonstration of the underlying business substance. Students must accordingly have a solid awareness of accounting and how the accounting numbers translate into tax numbers (with appropriate adjustments). Given that most (if not all) trainees are assumed to have an accounting background based on their university or other experiences, no additional knowledge criteria is specifically listed for this module. Students will integrate their accounting and tax knowledge mainly via simulations (i.e. practical knowledge component) and work training. At a more detailed level, tax professional trainees must:

• Be familiar with the terms and concepts contained within core accounting statements regarding profit and loss (e.g. the statement of profit and loss and other comprehensive statement of income);

• Be familiar with terms and concepts regarding balance sheet assets and liabilities (e.g. the statement of financial position); and

• Be familiar with the general concepts associated with trial balances and general ledgers. These concepts include the distinction between current and non-current assets / liabilities, the basics of equity (e.g. share capital versus debt), impairments and similar financial basics. Tax professionals must additionally be familiar with commonplace terminology and processes (e.g. the meaning of a deferred tax account and the general role of IFRS). In terms of reading, tax professionals should be able to rely on their books used in university relating to financial accounting. 4. International Tax Fundamentals

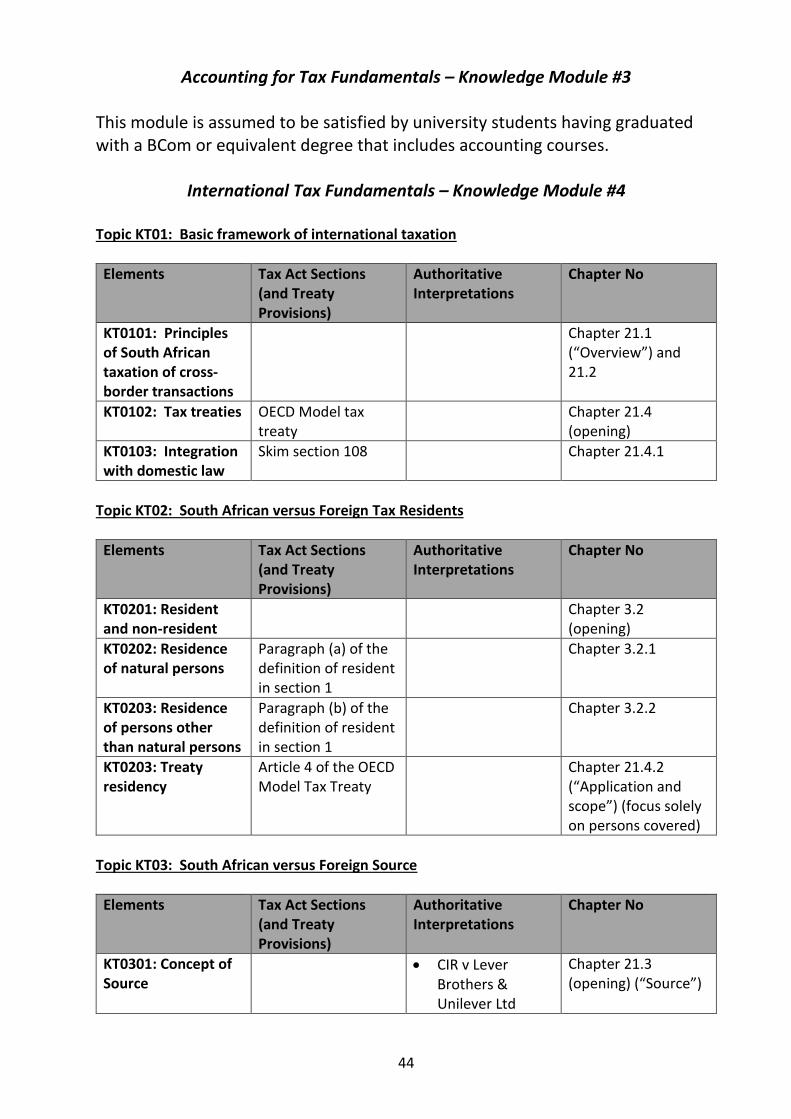

A. Overview

Most of the programme is focused on transactions between domestic taxpayers in terms of domestic activities. However, tax professionals must understand the basics of cross-border taxation. The basic framework entails two sets of considerations:

• South African residents versus foreign tax residents; and

• South African activities versus foreign activities. South African tax can apply only when South Africa has taxing jurisdiction (i.e. a nexus) to the person or the underlying activities. Like most modern countries, South Africa taxes its (e.g. individual and corporate) tax residents on a worldwide basis. South Africa also taxes foreign tax residents on their South African tax residents. South Africa also has an extensive network of tax treaties. These treaties allocate taxing rights between countries so as to eliminate double taxation (and also to promote cross-border reporting and enforcement). The first portion of this module covers the overall framework for this allocation, including the basic role of tax treaties. Key aspects of this portion focus on the rules that distinguish

7

domestic tax residents from foreign tax residents (including tax treaty adjustments where dual country tax residence is otherwise claimed). This portion also focuses on distinguishing activities that have a South African source versus a foreign source.

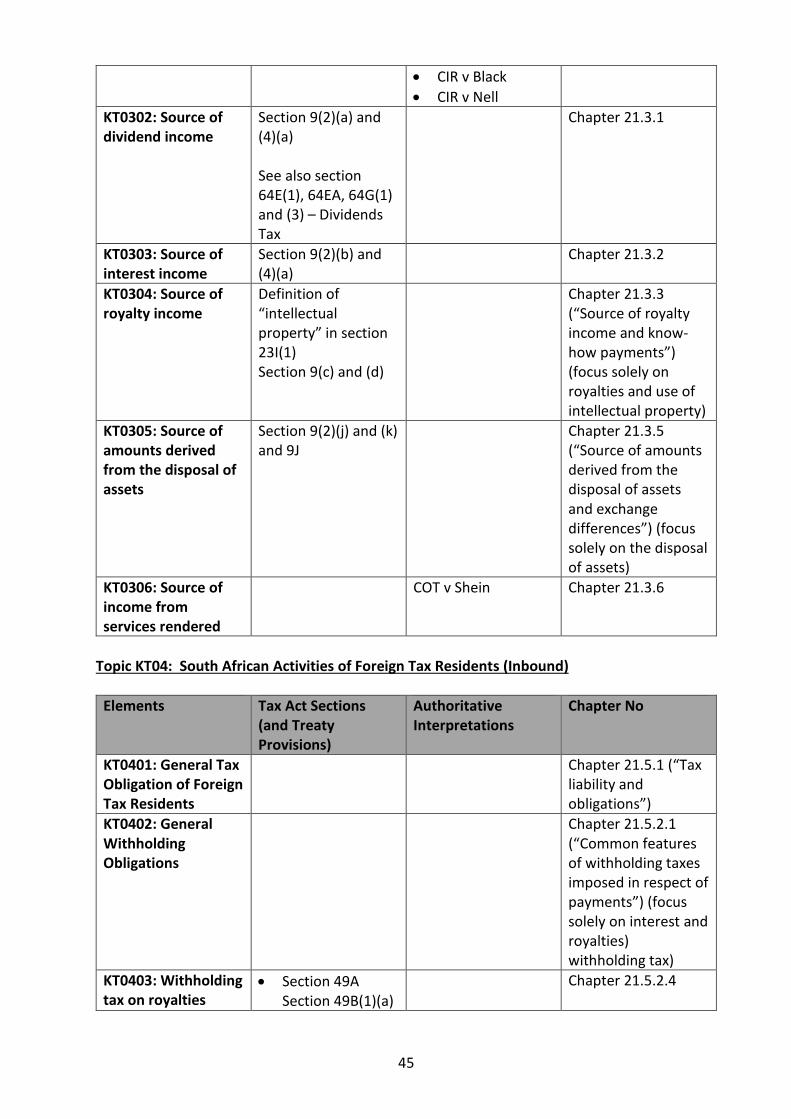

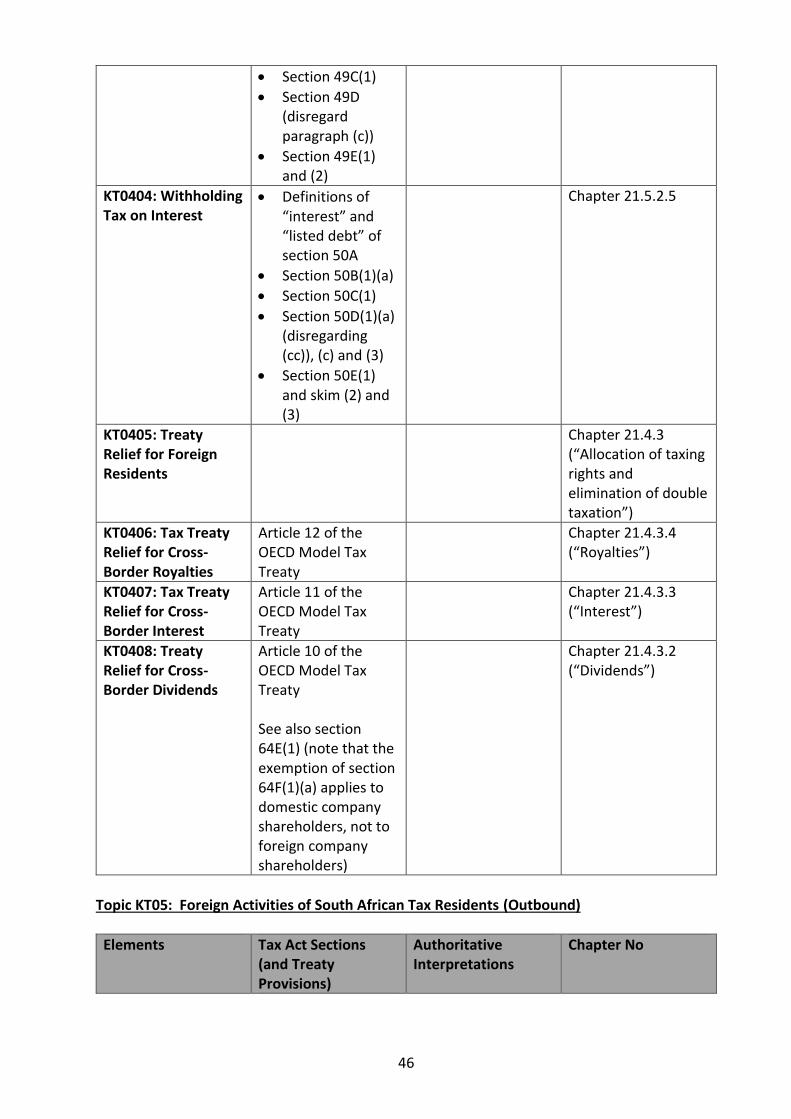

B. South African Activities of Foreign Tax Residents (Inbound) Special rules apply when foreign persons operate within South Africa. Foreign persons are either subject to direct taxation or South African persons must withhold tax when making payments to foreign persons. This portion focuses on both tax mechanisms with the main focus being on cross-border withholding. Three main forms of cross-border payments are at play – royalties, interest and dividends. South African taxation of these items can also be eliminated or reduced via tax treaty.

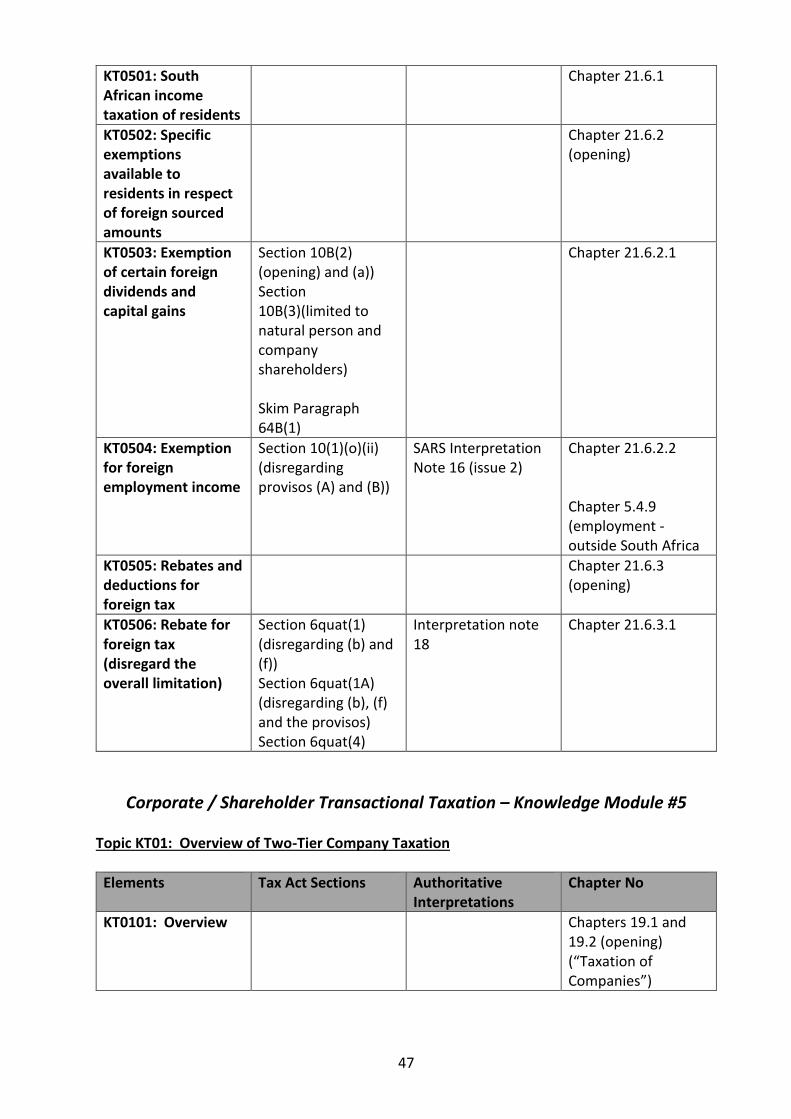

C. Foreign Activities of South Tax Residents (Outbound) This portion of the module focuses on South Africans with foreign activities. As stated above, South Africans are subject to worldwide taxation so all foreign income must be included as income on a South African taxpayer’s tax return. However, this worldwide tax system is subject to key adjustments:

• South African taxpayers receive section 6quat rebates (i.e. tax credits) for taxes “proved to be payable”. The purpose of this rebate is to eliminate double taxation (with South Africa yielding in favour of the other country because the activities arise in that foreign country).

• The South African tax system also contains a number of limited exemptions. This module focuses on the most common foreign exemptions: (i) the exemption for foreign-earned salaries and the exemption for foreign dividends, (ii) as well as capital gains for the disposal of foreign shares.

5. Core Subspecialties (Modules 5 through 9) In addition to the fundamentals above, trainees should have a broader understanding of certain specialty areas that are expected of most mid-level tax professional trainees. While most trainees may find that only certain of these specialities are of use on a daily basis, a basic understanding of these areas is intermittently required for peripheral use and engagement with other tax experts. The introductory specialities outlined below form the basis of the expertise that is the main object of most tax professionals. These specialties are as follows: 1. Corporate / Shareholder Transactional Taxation 2. Indirect (e.g. Value-Added) Tax 3. Personal Taxation 4. Employment Payroll Taxation 5. Family and Wealth Taxation

A. Specialty I – Corporate / Shareholder Transaction Taxation: Most profit-making business in South Africa operate as a company. Companies are separate taxpayers whose operations are taxed accordingly. One unique aspect of companies is the relationship between the company and its owners (i.e. shareholders). It is these transactions

8

between the company and its shareholders that forms the basis of the work undertaken by many company tax specialists.

➢ Company formations: The first stage of the shareholder / company relationship entails

the company’s formation. This stage entails the transfer of cash and assets to a newly formed company in exchange for newly issued shares. This formation can be taxable or tax-free (i.e. tax-deferred via the reorganisation rollover rules). This area also includes some basics about the securities transfer tax.

➢ Taxation of company distributions to its shareholders: One of the primary functions of a company is to produce profits for its shareholders that can be distributed as dividends. Alternatively, distributions can be made that represent a return of capital (i.e. the initial investment). In tax, the shareholders can freely choose whether they want the profits first or a return on the initial investment. Dividends are taxed at a flat 20 per cent rate. Return of capital distributions reduce the base cost in shares and / or trigger capital gains tax. A variation on this theme are other forms of distributions, such as share buybacks and liquidations.

➢ Taxable Company Acquisitions: There comes a point when the owner of the company may seek to sell his or her shares in a company. This is a common event for practitioner advise. In most cases, these sales are taxable events. The main issue is whether the owner directly sells the shares or the underlying company sells the business. The purpose of this portion of the module is to unpack both forms of sale.

➢ Debt Corpus: Besides equity investments, the second major source of funding for

companies is debt borrowed from banks and other sources. The advanced tax fundamental module addresses simply debt creation and repayment. In this subspecialty, the focus is mainly on the impact of concessions of compromises of underlying debt.

B. Indirect Tax

1. VAT Overview and initial formalities Trainees are expected to understand the basic mechanics of “output and input” calculations required for VAT 201 returns. They must also understand the underlying purpose of the VAT system. This understanding must include a solid foundation of the basic concepts of standard rated, zero rated and exempt supplies. Trainees must additionally understand the initial formalities associated with VAT. These initial formalities include:

• Registration: Trainees must understand how clients can register for VAT to become a VAT vendor – including “who may” / “who must” register for VAT and when registration must occur. This understanding requires a basic knowledge of the definition of “enterprise” for general private sector activities as well as the rules relating to taxable turnover that form part of the “enterprise” calculation.

9

• Tax periods: VAT vendors are required to submit VAT 201 returns periodically throughout the year. Most VAT vendors must submit returns every two months or every month.

2. Basic VAT compliance in terms of taxable supplies

Basic VAT 201 return calculations as well as the time periods for filing returns (e.g. monthly and bi-monthly) are core to a fundamental understanding of VAT. Trainees are expected to have the knowledge to service small or medium size companies as well as individual businesses in terms of making these calculations. Trainees must further understand the input and output calculations required for goods (both trading stock and capital) as well as for services in respect of purchaser / clients. These input / output calculations will include the basics associated with imports and exports.

3. Common VAT Zero Rated and Exempt Supplies Trainees must be familiar with recurring zero-rated and exempt supplies that often arise in the small and medium business sector. In terms of zero-rated goods, trainees must be aware of the list of zero rated goods (e.g. for food and fuel) and the zero-rated claims for direct exports. Trainees must additionally know the basics associated with exempt supplies, especially the supply of transport, education, residential rentals and straight-forward financial services (e.g. credit / debt, shares and currency). Of further importance is how to account for (i.e. exclude) direct inputs associated with exempt outputs.

4. Frequently Recurring Special Circumstances Beyond the core concepts outlined above, VAT (like the Income Tax) contains a number of special rules and subsystems. These subsystems are designed to extend the VAT into unique circumstances. Recurring circumstances of this kind include second-hand goods, employee motor cars (and other employee fringe benefits), irrecoverable debts and fixed property rentals. Some basic general awareness of the VAT as applied to farming is also expected (similar to the diagnostic awareness of income tax as applied to farming).

5. Special Rules for VAT Administration

VAT contains its own rules pertaining to administration. Tax periods are more recurring (generally bi-monthly or monthly). Most notably, the key to any VAT system are refunds to ensure that the VAT does not effectively apply to business-to-business transactions. Another key feature of VAT is the required accuracy of VAT invoices, especially in terms of claiming input credits.

6. Basics of Customs Duty

Another key indirect tax is Customs, which is largely a specialty on its own (often seen as a separate form of revenue from other nationally imposed taxes). Trainees are expected to have a general diagnostic awareness of customs and its core essentials. Customs Duty applies to the import of goods, and these imports must be coo-ordinated with the VAT. Customs is based on

10

three concepts – origin, classification and valuation. When calculating duties, these calculations may contain rebates, drawbacks ad refunds. In some cases, anti-dumping and countervailing duties may apply in order to ensure fair trade.

C. Personal Taxation Tax preparation for individual tax returns (IT12s) is a specific line of activity for many practitioners. Tax returns for most individuals differ significantly from business returns. – many deductions are denied to prevent private / personal consumption while also containing special relief measures and incentives to assist middle and lower-income families save or cover core needs. Many tax practitioners provide this service for individual shareholders as part of their service for the underlying business. ➢ Special net calculations: Individual tax returns contain a number of special automatic relief

measures designed to mitigate taxation of middle and lower-income workers. These include the primary rebate and the annual exclusion.

➢ Special deduction limitations, medical credits, retirement and capital gain adjustments: Individuals cannot deduct private expenses or expenses that can easily masquerade as private expenses. On the other hand, government provides relief for medical aid contributions or the sale of the home and other personal effects.

➢ Retirement funds: Government has created a whole array of retirement fund rules in order

to facilitate long-term savings so that individuals have savings upon retirement. Under this system, contributions are generally deductible, the growth is tax-free while in a fund and tax occurs on pay-out. This deferred tax effectively arises only upon retirement consumption.

➢ General savings: Individuals have an array of savings products to choose from them – each

of which offer a tax outcome. For most middle and upper-income earners, these savings products entail institutional savings products, such as bank interest, collective investment schemes, insurance products and investment units in real estate investment trusts.

➢ Basics of Transfer Duty: A common issue for many individuals is the purchase of a home.

This purchase typically triggers Transfer Duty, which may be substantial. Although this area is typically dealt with by conveyancers and real estate attorneys, tax practitioners are expected to have a general awareness of this area given that this area may be the subject of a general discussion with clients.

D. Employment Payroll Taxation The taxation of individual salary earners are effectively split into two as a practical matter. Individual taxpayers must file their own independent tax returns (IT12s) at year-end as outlined above. In addition, individual employee salaries must be taxed on a monthly basis. This monthly tax obligation falls on the employer with certain tax specialists solely dedicated to payroll and the related monthly-related payment of the tax imposed on payroll.

11

➢ Employees’ Tax (Pay-As-You-Earn Withholding): Employers must withholding tax on salaries on a monthly basis to be paid over seven days after every month. Most withholding is fairly straight-forward. However, special concerns do arise, such as employment versus independent contractor status, part-time and occasional employees and irregular payments.

➢ Fringe benefits: Salary comes in many forms. Salary can come as a bonus, accrued and sick leave, exit payments and often disguised as an allowance (e.g. travel, entertainment and subsistence). Salary can also be in the form of cash or in-kind – all of which has a value. The purpose of the tax rules is largely to value these fringe benefits in a simplified manner with special relief mechanisms for certain government preferred priorities (e.g. bursaries).

E. Wealth Succession Planning (Lifetime and Death Transfers)

Wealth planning is a combination of estate preservation, investment growth and tax minimisation. Tax practitioners can be specifically dedicated to wealth preservation while others find themselves assisting their small and entrepreneurial clientele with preservations as the businesses reach maturity.

➢ Family Income Taxation: The starting point for the tax system is to treat each individual as

a wholly independent taxpayer even if those individuals are part of the same family economic unit. While this principle eases administration, the tax law contains certain attribution rules to prevent the artificial shifting of income from high-income earners to low-income earners merely to mitigate tax. In other cases, special allocations of income are required to represent the various forms of marriage (community of property, ANC with accrual and without accrual).

➢ Taxation of donations: Donations trigger both an income tax consequence and a Donations

Tax consequence. In terms of income tax, the donation of an asset generally triggers capital gain based on the fair value of the asset less the tax cost. In terms of the Donations Tax, the charge generally triggers a 20 per cent charge (less the R100 000 annual exemption).

➢ Taxation at death: Death has a similar dual consequence to donations. In terms of the

Income Tax, the death of an individual generally triggers gain or loss on all assets held immediately before death (triggering capital gains or ordinary revenue). Death also triggers the Estate Duty at 20 per cent. This 20 per cent charge largely falls on the net value (gross assets less debts owed) of the estate.

➢ Trusts: One core feature of estate planning is a trust. Trusts can preserve wealth for

multiple generations and remove growth from a person’s estate before death. Many small and medium South African companies are held by domestic trusts established by a founding business owner or entrepreneur. Trusts can be in the simple form of a bewind or vesting trust, both of which automatically give rise to income allocated to the beneficiaries. Most trusts, however, come as a discretionary trust. Discretionary trusts are a flexible vehicle in terms of income / capital gain allocations with income/ gains being allocable to various beneficiaries and the trust itself.

12

6. Tax Administration and Practice Management A. Tax Administration Expertise in tax administration has become of increasing importance in the tax field. SARS audit and dispute has become an increasing part of everyday tax practice. Tax returns are no longer simply submitted. SARS increasingly verifies, queries or audits returns. Tax professionals are expected to understand this part of practice in order to properly engage. This form of practice must also be understand when dealing with basic compliance and advisory. ➢ Preliminary Concepts: Tax practitioners must have a basic understanding of the Tax

Administration Act and related acts (such as the Promotion of Administrative Justice Act). Also of importance is an understanding of the roles and responsibility of the basic actors (e.g. SARS, the Tax Ombud and the tax practitioners themselves).

➢ Ancillary Return Administration: There are a number of ancillary aspects to every tax return. Tax returns will be assessed and adjusted (e.g. additional and reduced assessments). Understatements result in interest and penalties. Post-return adjustments may leave taxpayers seeking a reduction or seeking to pay extra without penalty (e.g. via the Voluntary Disclosure Programme). Other common issues pertain to tax clearance certificates, which are often needed by taxpayers to conduct certain forms of business.

➢ Dispute and Settlement: There comes a point when the process becomes increasingly

confrontational, and tax practitioners need to understand the early stages of dispute as issues and amounts in dispute coalesce. These early stages entail a fair amount of information gathering and disclosure. SARS may issue an additional assessment, which may be followed by a formal taxpayer objection. Tax practitioners must be very familiar with these aspects of the process as well as settlement alternatives and payment options. Lastly, tax practitioner must have general familiarity with the role of Tax Board, Tax Court and other judicial processes (most of which will be handled by lawyers and other legal specialists).

B. Practice Management

Tax practitioners must be able to properly manage the affairs of the client, including the practitioner-client relationship. These aspects of tax practice are best learned through simulations and job training. Hence, no specific modules are generally required in terms of these issues. However, one formal part of practice management is a Code of Professional ethics. Trainees are therefore required to review the SAIT Code of Conduct in Relation to Taxation and the South African Tax Standards. Both of these items can be found on the SAIT website.

13

General Tax Fundamentals – Knowledge Module #1

Topic KT01: Range of Tax Instruments

Elements

Specific Authorities Study Guide

KT0101: Tax Types General awareness of the multiplicity of South African tax acts, including:

• Income Tax Act

• Value-Added Tax Act

• Transfer Duty Act

• Estate Duty Act

• Securities Transfer Tax Act

• Customs and Excise Duties

• Unemployment Insurance Contributions Act

• Skills Development Levy Act

Table 2.1 of Chapter 2.2.3

KT0102: Charges within the Income Tax Act

General awareness of:

• The Normal Tax

• Cross-Border Withholding

• Turnover Tax

• Dividends Tax

• Donations Tax

Chapters 2.2.3.1 through 2.2.3.5

KT0103: Direct versus Indirect Tax

“Direct versus Indirect Tax: Top 6 Differences You Must Know”, by Wallstreet Mojo (Website)

KT0104: Tax base versus tax rate

Chapter 1.2 and 1.3

KT0105: Annual Tax Legislative Changes

General awareness of the Rates and Monetary Amounts Amendment Act

Chapter 2.2.2

Topic KT02: Overall Income Tax Construction

Elements

Specific Authorities Study Guide

KT0201: Core Components of the Normal Tax (within the Income Tax Act)

Income Tax Act: Section 5(1) and (2) Income Tax Act: Section 1(1) the definitions of:

Chapter 2.5 (“Illustrating the components of normal tax and the interpretation of tax law in South Africa” other than 2.5.1), 2.6

14

• “normal tax”

• “taxable income”

• “income”

• “tax” Capital Gains Tax:

• Section 26A

• Eighth Schedule (skim)

(“Comprehensive example”) and 19.2.2 (“Taxation of company profits”) See also Silke Chapter 17.1 (CGT Overview)

KT0202: Tax rates and monetary thresholds

Rates and Monetary Amounts Amendment Act (latest year):

• Paragraph 1

• Paragraph 2

• Paragraph 3 (Up through (a))

Appendices A and B (“Tax monetary thresholds”)

KT0203: Key recurring definitions

Taxable Entities: Income Tax Act: Section 1(1) the definitions of: “company” (paragraphs (a) and (f)) “person” “trust” Income Tax Act:

• Section 1(1) the definitions of: “financial year”, “return” and “year of assessment”

• Section 66(13) (without regard to the provisos)

Income Tax Act: Section 1(1) the definitions of:

• “connected person”

• “relative”

• “spouse” SARS interpretation: Interpretation Note 67 (issue 3)

Chapter 2.5.1 (“The incidence of normal tax”), 3.5 (“Year or period of assessment”) and 13.2.1 (“Connected persons”)

Topic KT03: General Trading Inflows: Single Stream Receipts and Accruals

Element KT0301: General Gross Income Definition General concept: Ordinary receipts and accruals Income Tax Act:

15

Section 1 “gross income definition” (opening paragraph before (a) but disregarding (ii) dealing with non-residents)

Sub-Elements Specific Authorities Study Guide

The definition of ‘gross income’

Chapter 3.1 (“Overview”)

Amount in cash or otherwise

CSARS v Brummeria Renaissance (Pty) Ltd; : CIR v Butcher Brothers (Pty) Ltd; Lategan v CIR

Chapter 3.3

Received by or accrued to Chapter 3.4 (opening)

Meaning of ‘received by’ Geldenhuys v CIR; MP Finance Group CC v CSARS; Pyott Ltd v CIR; CIR V Delagoa Bay Connect Co Ltd CSARS v Cape Consumers (Pty) Ltd

Chapter 3.4.1

Meaning of ‘accrued to’ Cactus Investments (Pty) Ltd; CIR v People's Stores (Walvis Bay) (Pty) Ltd Mooi v SIR Gud Holdings (Pty) Limited v CSARS; CIR v Witwatersrand Racing Clubs

Chapter 3.4.2

Valuation of receipt or accrual

CSARS v KWJ Investment (142/2017) [2018] ZASCA 81 (31 May 2018) South Atlantic Jazz Festival (Pty) Ltd v CSARS

Chapter 3.4.3

Disposal of income after receipt or accrual

CIR v Witwatersrand Association of Racing Clubs SIR v Silverglen Investments (Pty) Ltd CSARS v KWJ Investment (142/2017) [2018] ZASCA 81 (31 May 2018)

See also section 7(1) and 7(7)

Chapter 3.4.7

Time of accrual of interest payable by SARS

Section 7E Chapter 3.4.8

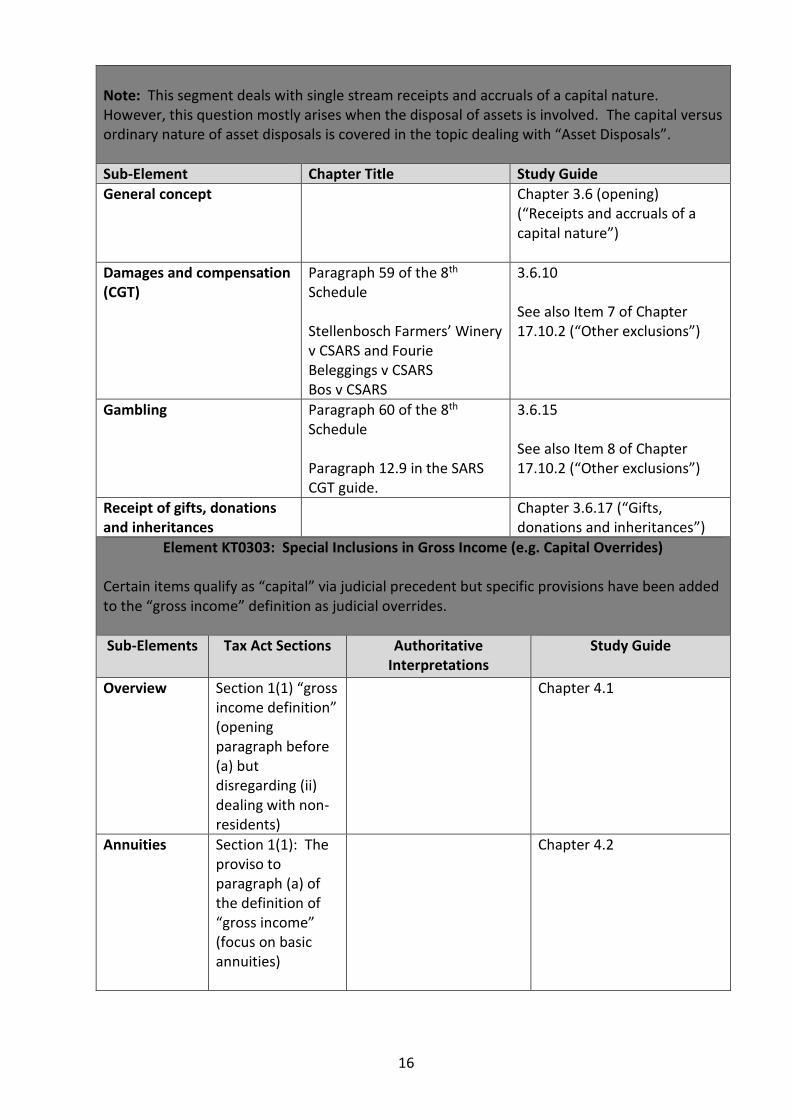

Element KT0302: Exclusion for Receipts and Accruals of a Capital Nature General concept: Receipts and accruals of a capital nature are excluded from the gross income definition but may fall under the Capital Gains Tax. Income Tax Act: Section 1 “gross income definition” (opening paragraph before (a) but disregarding (ii) dealing with non-residents)

16

Note: This segment deals with single stream receipts and accruals of a capital nature. However, this question mostly arises when the disposal of assets is involved. The capital versus ordinary nature of asset disposals is covered in the topic dealing with “Asset Disposals”.

Sub-Element Chapter Title Study Guide

General concept Chapter 3.6 (opening) (“Receipts and accruals of a capital nature”)

Damages and compensation (CGT)

Paragraph 59 of the 8th Schedule Stellenbosch Farmers’ Winery v CSARS and Fourie Beleggings v CSARS Bos v CSARS

3.6.10 See also Item 7 of Chapter 17.10.2 (“Other exclusions”)

Gambling

Paragraph 60 of the 8th Schedule Paragraph 12.9 in the SARS CGT guide.

3.6.15 See also Item 8 of Chapter 17.10.2 (“Other exclusions”)

Receipt of gifts, donations and inheritances

Chapter 3.6.17 (“Gifts, donations and inheritances”)

Element KT0303: Special Inclusions in Gross Income (e.g. Capital Overrides) Certain items qualify as “capital” via judicial precedent but specific provisions have been added to the “gross income” definition as judicial overrides.

Sub-Elements Tax Act Sections Authoritative Interpretations

Study Guide

Overview Section 1(1) “gross income definition” (opening paragraph before (a) but disregarding (ii) dealing with non-residents)

Chapter 4.1

Annuities Section 1(1): The proviso to paragraph (a) of the definition of “gross income” (focus on basic annuities)

Chapter 4.2

17

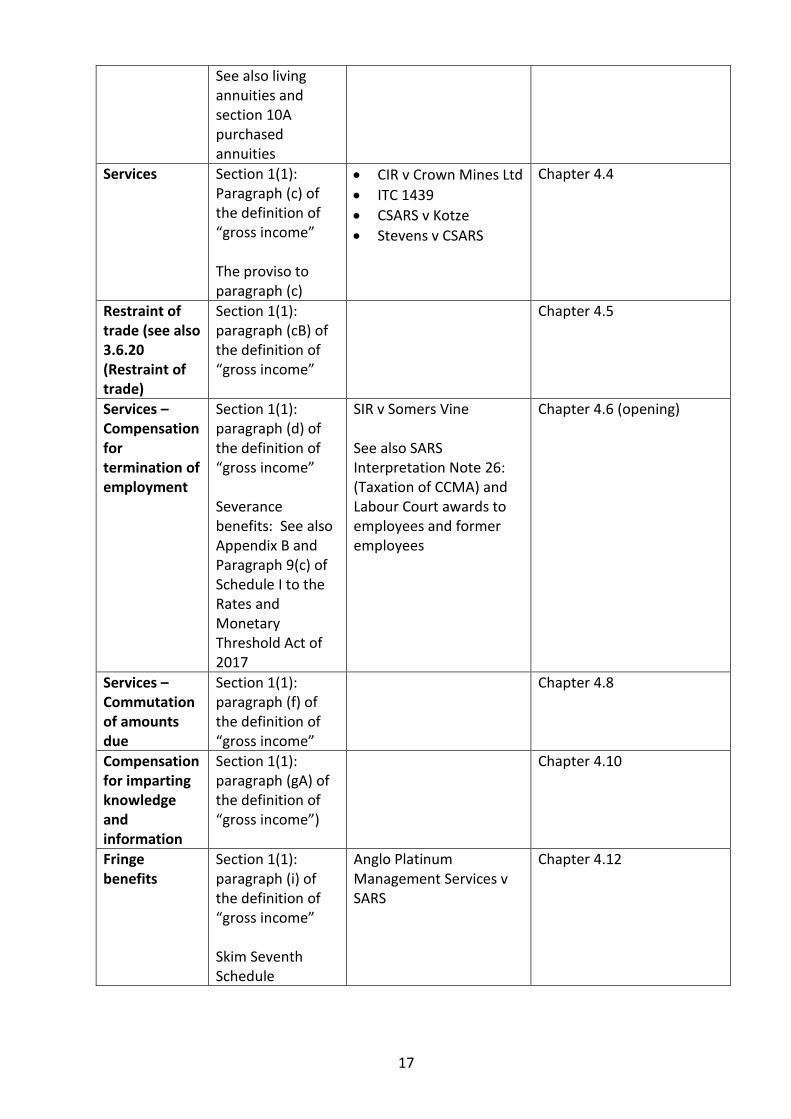

See also living annuities and section 10A purchased annuities

Services

Section 1(1): Paragraph (c) of the definition of “gross income” The proviso to paragraph (c)

• CIR v Crown Mines Ltd

• ITC 1439

• CSARS v Kotze

• Stevens v CSARS

Chapter 4.4

Restraint of trade (see also 3.6.20 (Restraint of trade)

Section 1(1): paragraph (cB) of the definition of “gross income”

Chapter 4.5

Services – Compensation for termination of employment

Section 1(1): paragraph (d) of the definition of “gross income” Severance benefits: See also Appendix B and Paragraph 9(c) of Schedule I to the Rates and Monetary Threshold Act of 2017

SIR v Somers Vine See also SARS Interpretation Note 26: (Taxation of CCMA) and Labour Court awards to employees and former employees

Chapter 4.6 (opening)

Services – Commutation of amounts due

Section 1(1): paragraph (f) of the definition of “gross income”

Chapter 4.8

Compensation for imparting knowledge and information

Section 1(1): paragraph (gA) of the definition of “gross income”)

Chapter 4.10

Fringe benefits

Section 1(1): paragraph (i) of the definition of “gross income” Skim Seventh Schedule

Anglo Platinum Management Services v SARS

Chapter 4.12

18

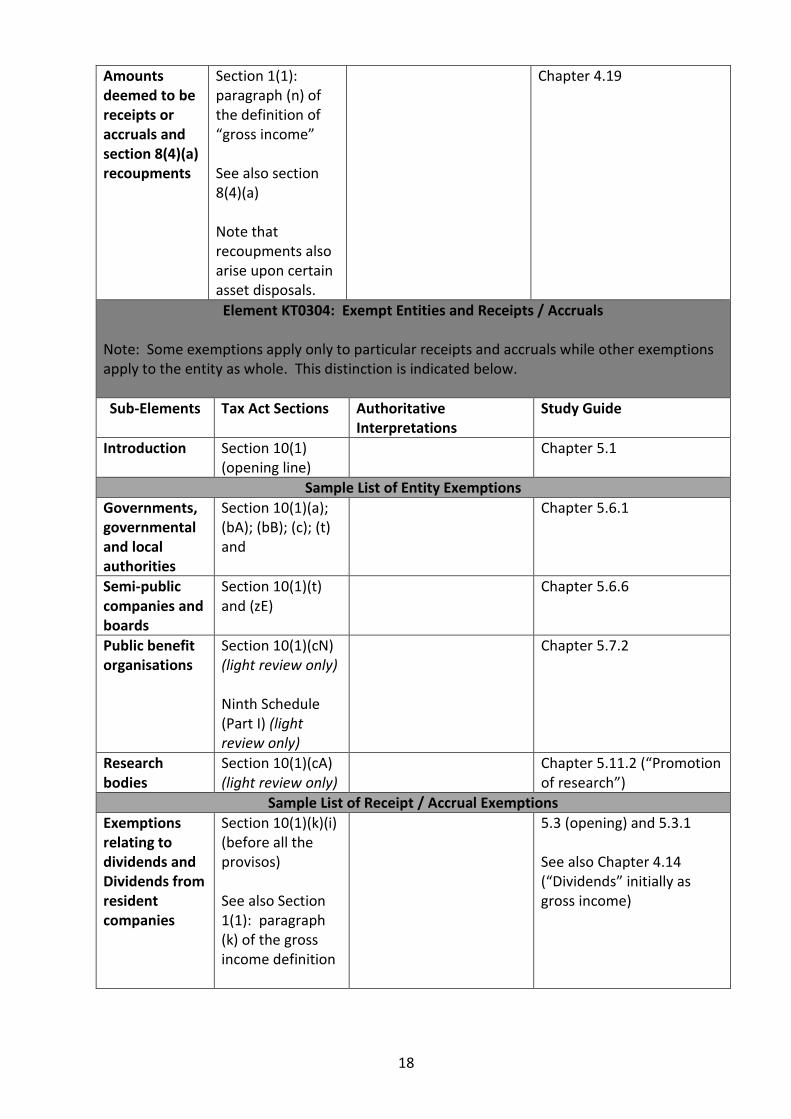

Amounts deemed to be receipts or accruals and section 8(4)(a) recoupments

Section 1(1): paragraph (n) of the definition of “gross income” See also section 8(4)(a) Note that recoupments also arise upon certain asset disposals.

Chapter 4.19

Element KT0304: Exempt Entities and Receipts / Accruals

Note: Some exemptions apply only to particular receipts and accruals while other exemptions apply to the entity as whole. This distinction is indicated below.

Sub-Elements Tax Act Sections Authoritative Interpretations

Study Guide

Introduction Section 10(1) (opening line)

Chapter 5.1

Sample List of Entity Exemptions

Governments, governmental and local authorities

Section 10(1)(a); (bA); (bB); (c); (t) and

Chapter 5.6.1

Semi-public companies and boards

Section 10(1)(t) and (zE)

Chapter 5.6.6

Public benefit organisations

Section 10(1)(cN) (light review only) Ninth Schedule (Part I) (light review only)

Chapter 5.7.2

Research bodies

Section 10(1)(cA) (light review only)

Chapter 5.11.2 (“Promotion of research”)

Sample List of Receipt / Accrual Exemptions

Exemptions relating to dividends and Dividends from resident companies

Section 10(1)(k)(i) (before all the provisos) See also Section 1(1): paragraph (k) of the gross income definition

5.3 (opening) and 5.3.1 See also Chapter 4.14 (“Dividends” initially as gross income)

19

Note: Many of these dividends may instead be subject to the dividends withholding tax (see Part VIII of the Income Tax Act)

Unemployment insurance benefits

Section 10(1)(mB) 5.4.2

Bursaries and scholarships (but only in respect of non-employees)

Section 10(1)(q) (before the proviso) and (qB) (before the proviso)

5.5.1

War pensions and awards for diseases and injuries (but only disability and compensation)

Section 10(1)(g): war pension; Section 10(1)(gA): disability pension; and (gB)(i): Compensation for Occupational Injuries and Diseases Act; (gB)(iii): compensation where death arose out of and in the course of employment; and (gB)(iv): Road Accident Fund

5.11.4 (lightly review)

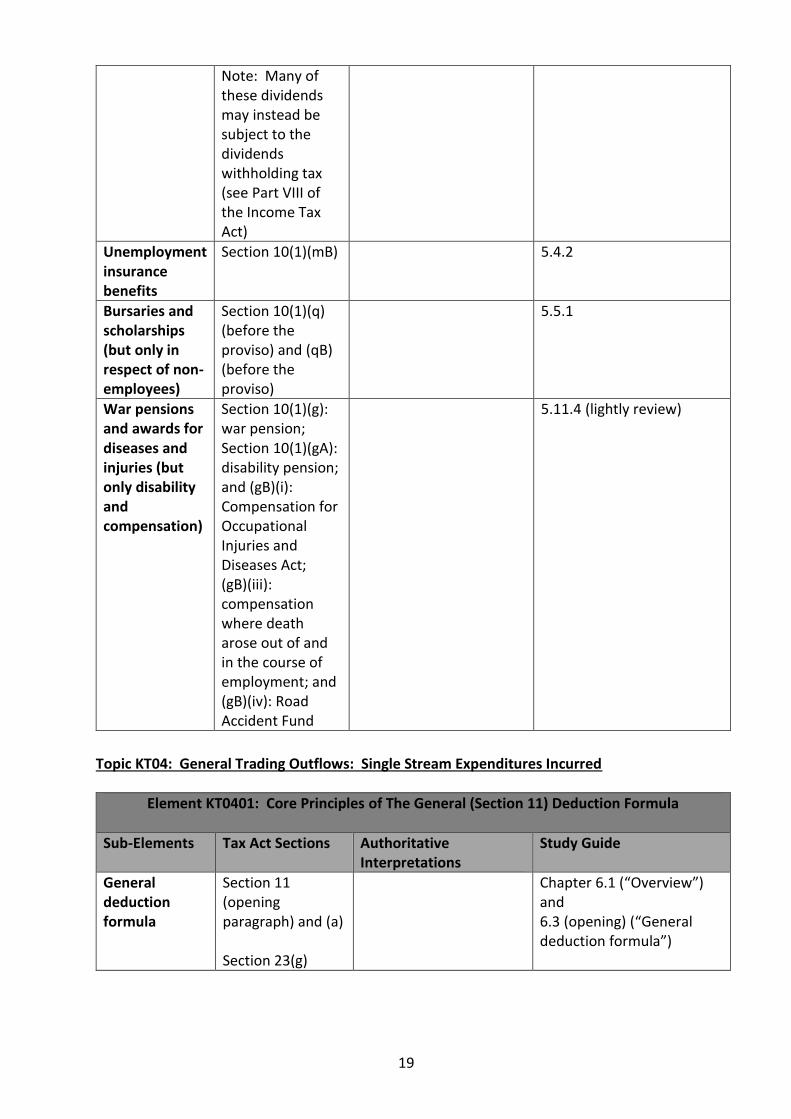

Topic KT04: General Trading Outflows: Single Stream Expenditures Incurred

Element KT0401: Core Principles of The General (Section 11) Deduction Formula

Sub-Elements Tax Act Sections Authoritative Interpretations

Study Guide

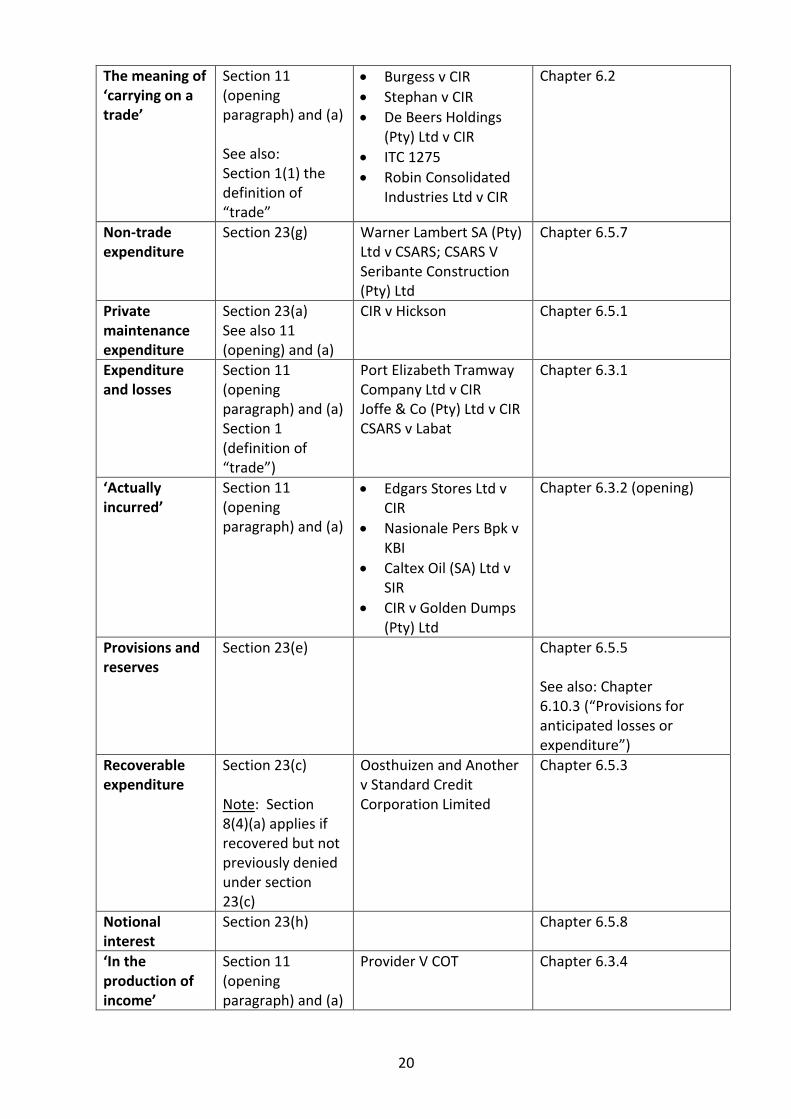

General deduction formula

Section 11 (opening paragraph) and (a) Section 23(g)

Chapter 6.1 (“Overview”) and 6.3 (opening) (“General deduction formula”)

20

The meaning of ‘carrying on a trade’

Section 11 (opening paragraph) and (a) See also: Section 1(1) the definition of “trade”

• Burgess v CIR

• Stephan v CIR

• De Beers Holdings (Pty) Ltd v CIR

• ITC 1275

• Robin Consolidated Industries Ltd v CIR

Chapter 6.2

Non-trade expenditure

Section 23(g) Warner Lambert SA (Pty) Ltd v CSARS; CSARS V Seribante Construction (Pty) Ltd

Chapter 6.5.7

Private maintenance expenditure

Section 23(a) See also 11 (opening) and (a)

CIR v Hickson Chapter 6.5.1

Expenditure and losses

Section 11 (opening paragraph) and (a) Section 1 (definition of “trade”)

Port Elizabeth Tramway Company Ltd v CIR Joffe & Co (Pty) Ltd v CIR CSARS v Labat

Chapter 6.3.1

‘Actually incurred’

Section 11 (opening paragraph) and (a)

• Edgars Stores Ltd v CIR

• Nasionale Pers Bpk v KBI

• Caltex Oil (SA) Ltd v SIR

• CIR v Golden Dumps (Pty) Ltd

Chapter 6.3.2 (opening)

Provisions and reserves

Section 23(e) Chapter 6.5.5 See also: Chapter 6.10.3 (“Provisions for anticipated losses or expenditure”)

Recoverable expenditure

Section 23(c) Note: Section 8(4)(a) applies if recovered but not previously denied under section 23(c)

Oosthuizen and Another v Standard Credit Corporation Limited

Chapter 6.5.3

Notional interest

Section 23(h) Chapter 6.5.8

‘In the production of income’

Section 11 (opening paragraph) and (a)

Provider V COT Chapter 6.3.4

21

CSARS v Mobile Telephone Networks Holdings (Pty) Ltd Port Elizabeth Electric Tramway Co Ltd v CIR

Expenditure incurred to produce exempt income

Section 23(f) See also section 10(1)(k)(i)(before all provisos)

Sub-Nigel Ltd v CIR CIR V Nemojim

Chapter 6.5.6

‘Not of a capital nature’

Section 11(opening paragraph) and (a) Note: Incurrals of a capital nature may be added to the cost / base cost of assets (see Pillar III)

• BP Southern Africa (Pty) Ltd v CSARS

• SIR v Guardian Assurance Holdings (SA) Ltd

• Rand Mines (Minding and Services) Ltd v CIR

• New State Areas Ltd v CIR

• ITC 1036

Chapter 6.3.5

‘During the year of assessment’

Section 11 (opening paragraph) and (a)

• Concentra (Pty) Ltd v CIR

Chapter 6.3.3

Element KT0402: The General (Section 11) Deduction Formula: Ancillary Principles

Sub-Elements Tax Act Sections Authoritative Interpretations

Study Guide

Prepaid expenditure

Section 23H(1) (other than provisos (cc)) and (3)

Chapter 6.4

Interest penalties and taxes

Section 23(d) Chapter 6.5.4

Fines Section 11 (opening paragraph) and (a) Section 23(o)

SARS Interpretation Note 54 (Issue 2) (Deductions: Corrupt activities, fines and penalties)

Chapter 6.10.6

Prohibition against double deductions

Section 23B(1) through (3)

Chapter 6.6

Excessive expenditure

Section 11 (opening paragraph) and (a) and 23(g)

• ITC 792

• ITC 1518

• ITC 575

Chapter 6.8

Cost of assets and VAT

Section 23C(1) (before the proviso)

Chapter 6.9

Variable remuneration

Section 7B

Paragraph 1.4 Explanatory

Chapter 12.2.7

22

Employees’ tax (focus on variable remuneration)

See also Employees’ Tax Withholding

Memorandum on the Taxation Laws Amendment Bill, 2012 10 December 2012

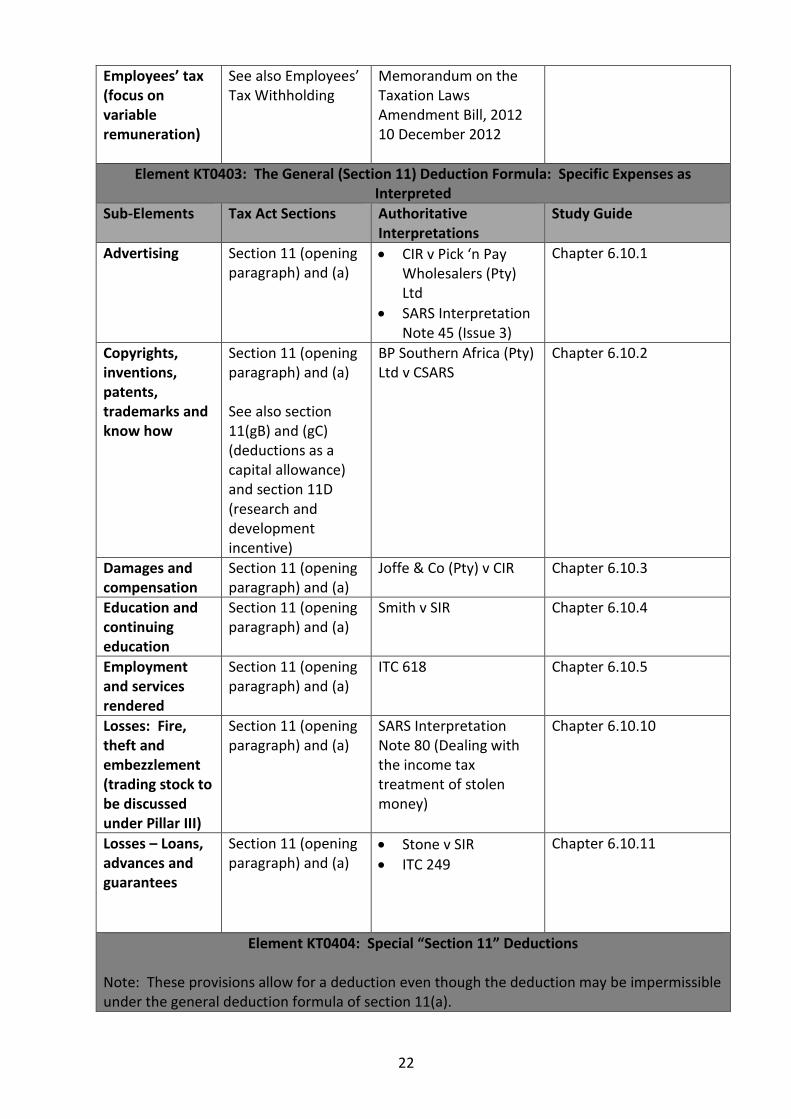

Element KT0403: The General (Section 11) Deduction Formula: Specific Expenses as Interpreted

Sub-Elements Tax Act Sections Authoritative Interpretations

Study Guide

Advertising Section 11 (opening paragraph) and (a)

• CIR v Pick ‘n Pay Wholesalers (Pty) Ltd

• SARS Interpretation Note 45 (Issue 3)

Chapter 6.10.1

Copyrights, inventions, patents, trademarks and know how

Section 11 (opening paragraph) and (a) See also section 11(gB) and (gC) (deductions as a capital allowance) and section 11D (research and development incentive)

BP Southern Africa (Pty) Ltd v CSARS

Chapter 6.10.2

Damages and compensation

Section 11 (opening paragraph) and (a)

Joffe & Co (Pty) v CIR Chapter 6.10.3

Education and continuing education

Section 11 (opening paragraph) and (a)

Smith v SIR

Chapter 6.10.4

Employment and services rendered

Section 11 (opening paragraph) and (a)

ITC 618 Chapter 6.10.5

Losses: Fire, theft and embezzlement (trading stock to be discussed under Pillar III)

Section 11 (opening paragraph) and (a)

SARS Interpretation Note 80 (Dealing with the income tax treatment of stolen money)

Chapter 6.10.10

Losses – Loans, advances and guarantees

Section 11 (opening paragraph) and (a)

• Stone v SIR

• ITC 249

Chapter 6.10.11

Element KT0404: Special “Section 11” Deductions

Note: These provisions allow for a deduction even though the deduction may be impermissible under the general deduction formula of section 11(a).

23

Sub-Elements Tax Act Sections Authoritative Interpretations

Study Guide

Restraint of trade payments

Sections 11(cA) and 23(l)

SARS Interpretation Note 7 (Restraint of trade payments)

Chapter 12.2.1 See also Chapters 3.6.20 (“Restraint of trade”) and 6.5.11 (“Restraint of trade”)

Annuities to former employees (disregard partners and dependants)

Section 11(m)(i) Chapter 12.2.5

Legal expenses

Section 11(c) • ITC 1310

• ITC 1154

• ITC 1241

• ITC 1598

Chapter 12.3 See also Chapters 6.10.8 (“Legal expenditure”) and 6.10.9 (“Legal expenditure: Of a capital nature”)

Repairs Section 11(d) Note: Repairs can alternatively be viewed as improvements that add to cost – mainly base cost for Capital Gains Tax purposes (see “Disposal of Assets” module)

• CSARS v Pinestone Properties CC

• ITC 491

• Rhodesia Railways Ltd v Collector of Income Tax, Bechuanaland

• Flemming v KBI

• CIR v African Products Manufacturing Co Ltd

• ITC 915

Chapter 12.4

Bad debt Section 11(i) – one sided concession Note: Reverses prior unpaid accrual or invoices

SIR v Kempton Furnishers (Pty) Ltd

Chapter 12.5

Doubtful debt Section 11(j) Note: Reverses prior unpaid accrual

Chapter 12.6

Allowance for outstanding debt: Credit

Section 24 Chapter12.10

24

agreements and debtor’ allowance

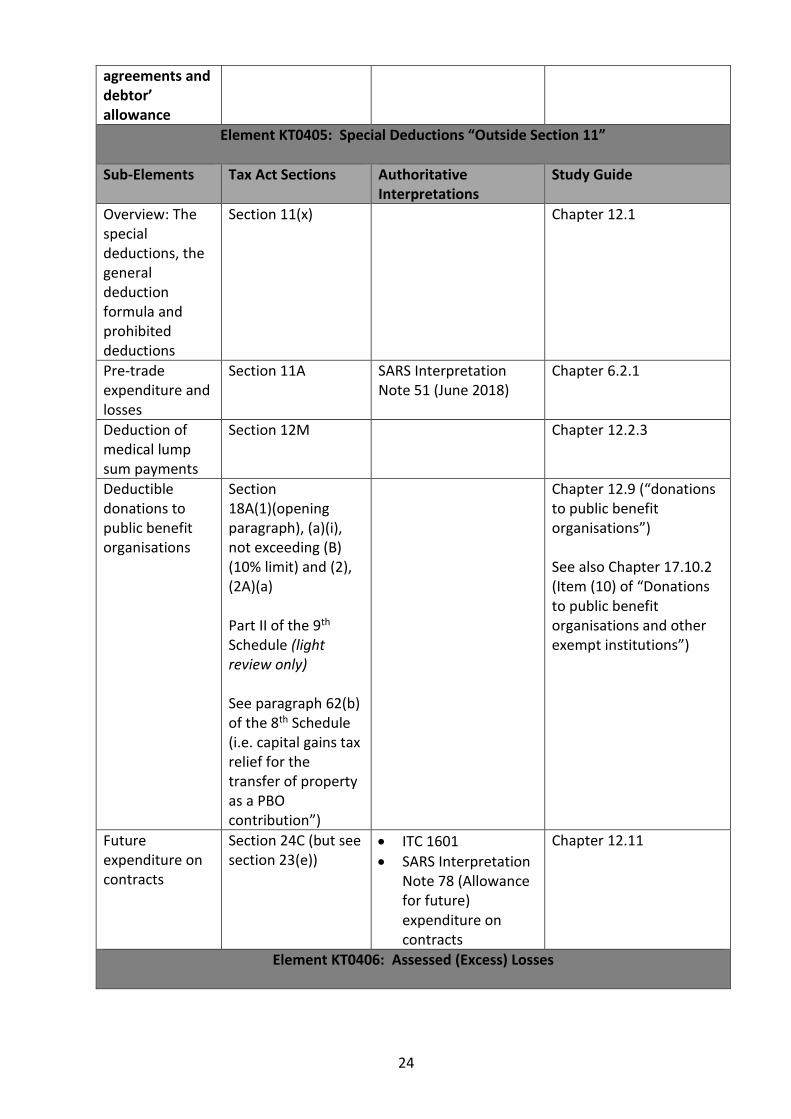

Element KT0405: Special Deductions “Outside Section 11”

Sub-Elements Tax Act Sections Authoritative Interpretations

Study Guide

Overview: The special deductions, the general deduction formula and prohibited deductions

Section 11(x) Chapter 12.1

Pre-trade expenditure and losses

Section 11A SARS Interpretation Note 51 (June 2018)

Chapter 6.2.1

Deduction of medical lump sum payments

Section 12M Chapter 12.2.3

Deductible donations to public benefit organisations

Section 18A(1)(opening paragraph), (a)(i), not exceeding (B) (10% limit) and (2), (2A)(a) Part II of the 9th Schedule (light review only) See paragraph 62(b) of the 8th Schedule (i.e. capital gains tax relief for the transfer of property as a PBO contribution”)

Chapter 12.9 (“donations to public benefit organisations”) See also Chapter 17.10.2 (Item (10) of “Donations to public benefit organisations and other exempt institutions”)

Future expenditure on contracts

Section 24C (but see section 23(e))

• ITC 1601

• SARS Interpretation Note 78 (Allowance for future) expenditure on contracts

Chapter 12.11

Element KT0406: Assessed (Excess) Losses

25

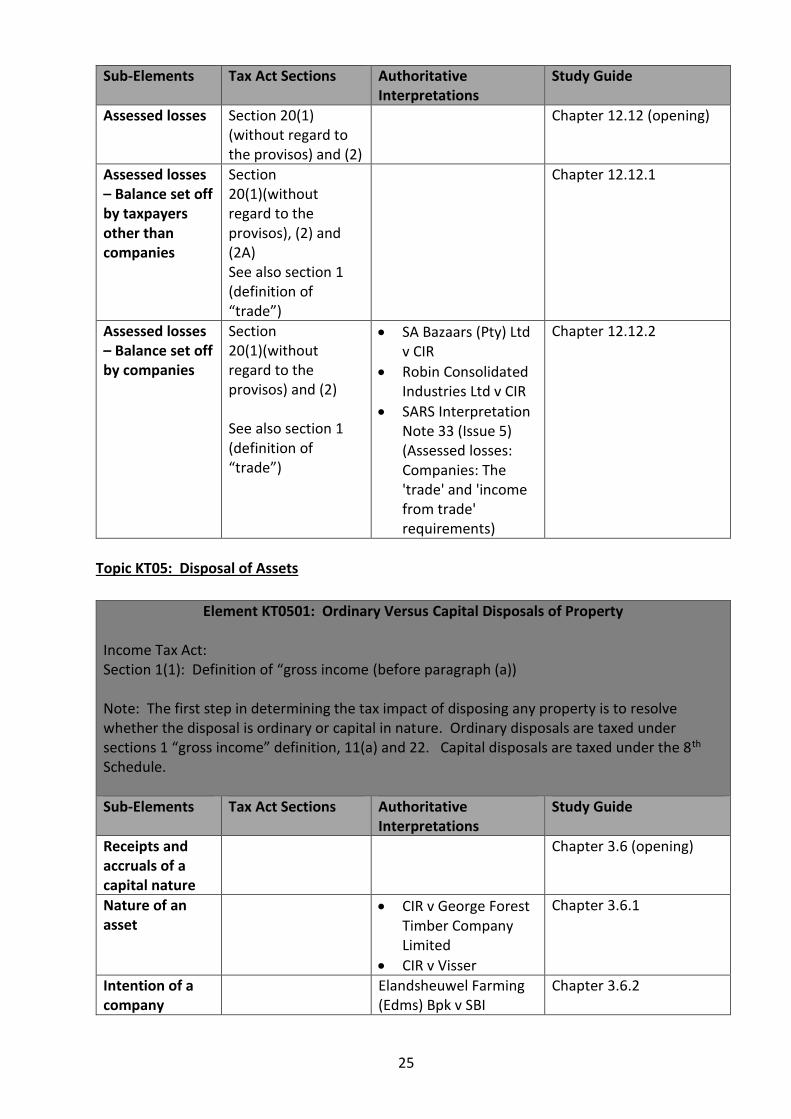

Sub-Elements Tax Act Sections Authoritative Interpretations

Study Guide

Assessed losses Section 20(1) (without regard to the provisos) and (2)

Chapter 12.12 (opening)

Assessed losses – Balance set off by taxpayers other than companies

Section 20(1)(without regard to the provisos), (2) and (2A) See also section 1 (definition of “trade”)

Chapter 12.12.1

Assessed losses – Balance set off by companies

Section 20(1)(without regard to the provisos) and (2) See also section 1 (definition of “trade”)

• SA Bazaars (Pty) Ltd v CIR

• Robin Consolidated Industries Ltd v CIR

• SARS Interpretation Note 33 (Issue 5) (Assessed losses: Companies: The 'trade' and 'income from trade' requirements)

Chapter 12.12.2

Topic KT05: Disposal of Assets

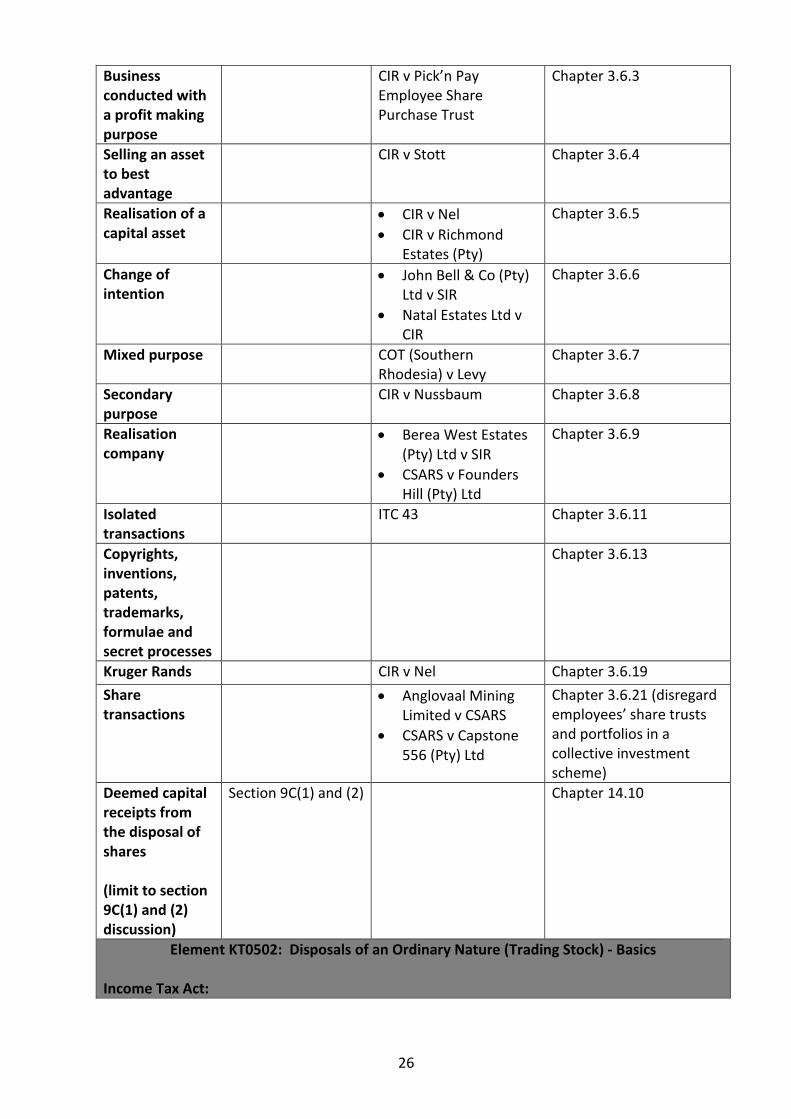

Element KT0501: Ordinary Versus Capital Disposals of Property

Income Tax Act: Section 1(1): Definition of “gross income (before paragraph (a)) Note: The first step in determining the tax impact of disposing any property is to resolve whether the disposal is ordinary or capital in nature. Ordinary disposals are taxed under sections 1 “gross income” definition, 11(a) and 22. Capital disposals are taxed under the 8th Schedule.

Sub-Elements Tax Act Sections Authoritative Interpretations

Study Guide

Receipts and accruals of a capital nature

Chapter 3.6 (opening)

Nature of an asset

• CIR v George Forest Timber Company Limited

• CIR v Visser

Chapter 3.6.1

Intention of a company

Elandsheuwel Farming (Edms) Bpk v SBI

Chapter 3.6.2

26

Business conducted with a profit making purpose

CIR v Pick’n Pay Employee Share Purchase Trust

Chapter 3.6.3

Selling an asset to best advantage

CIR v Stott Chapter 3.6.4

Realisation of a capital asset

• CIR v Nel

• CIR v Richmond Estates (Pty)

Chapter 3.6.5

Change of intention

• John Bell & Co (Pty) Ltd v SIR

• Natal Estates Ltd v CIR

Chapter 3.6.6

Mixed purpose COT (Southern Rhodesia) v Levy

Chapter 3.6.7

Secondary purpose

CIR v Nussbaum Chapter 3.6.8

Realisation company

• Berea West Estates (Pty) Ltd v SIR

• CSARS v Founders Hill (Pty) Ltd

Chapter 3.6.9

Isolated transactions

ITC 43 Chapter 3.6.11

Copyrights, inventions, patents, trademarks, formulae and secret processes

Chapter 3.6.13

Kruger Rands CIR v Nel Chapter 3.6.19

Share transactions

• Anglovaal Mining Limited v CSARS

• CSARS v Capstone 556 (Pty) Ltd

Chapter 3.6.21 (disregard employees’ share trusts and portfolios in a collective investment scheme)

Deemed capital receipts from the disposal of shares (limit to section 9C(1) and (2) discussion)

Section 9C(1) and (2) Chapter 14.10

Element KT0502: Disposals of an Ordinary Nature (Trading Stock) - Basics Income Tax Act:

27

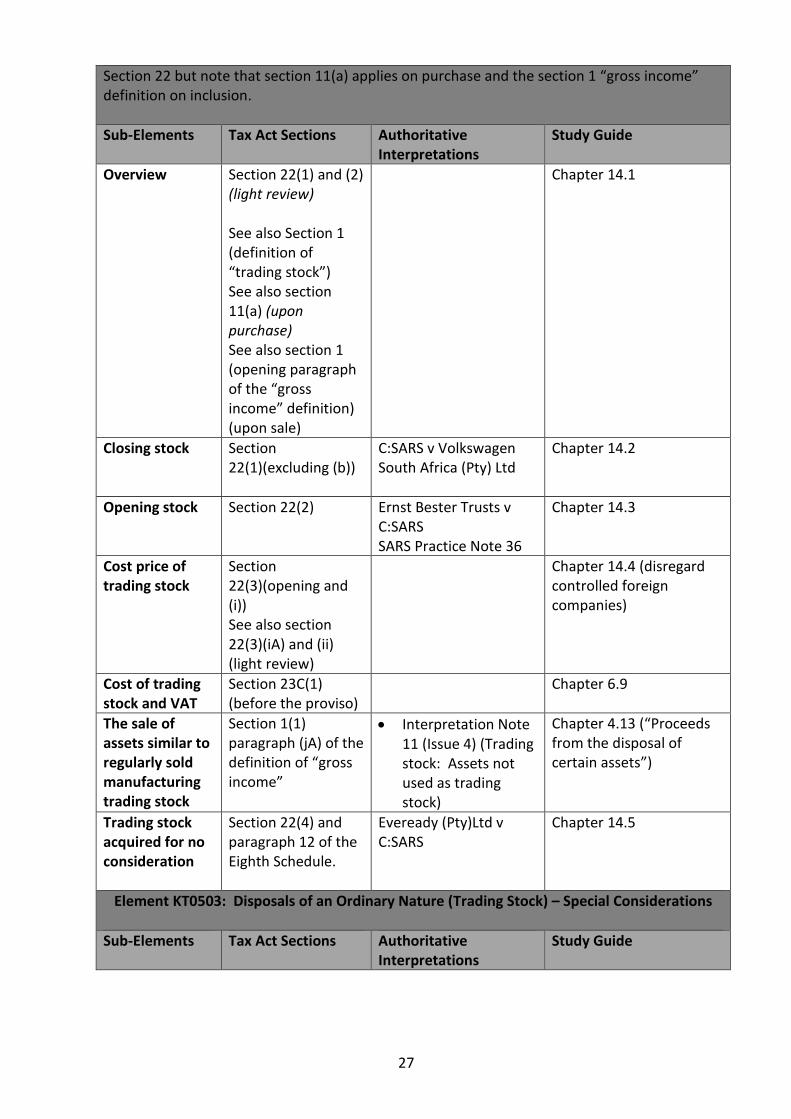

Section 22 but note that section 11(a) applies on purchase and the section 1 “gross income” definition on inclusion.

Sub-Elements Tax Act Sections Authoritative Interpretations

Study Guide

Overview Section 22(1) and (2) (light review) See also Section 1 (definition of “trading stock”) See also section 11(a) (upon purchase) See also section 1 (opening paragraph of the “gross income” definition) (upon sale)

Chapter 14.1

Closing stock Section 22(1)(excluding (b))

C:SARS v Volkswagen South Africa (Pty) Ltd

Chapter 14.2

Opening stock Section 22(2) Ernst Bester Trusts v C:SARS SARS Practice Note 36

Chapter 14.3

Cost price of trading stock

Section 22(3)(opening and (i)) See also section 22(3)(iA) and (ii) (light review)

Chapter 14.4 (disregard controlled foreign companies)

Cost of trading stock and VAT

Section 23C(1) (before the proviso)

Chapter 6.9

The sale of assets similar to regularly sold manufacturing trading stock

Section 1(1) paragraph (jA) of the definition of “gross income”

• Interpretation Note 11 (Issue 4) (Trading stock: Assets not used as trading stock)

Chapter 4.13 (“Proceeds from the disposal of certain assets”)

Trading stock acquired for no consideration

Section 22(4) and paragraph 12 of the Eighth Schedule.

Eveready (Pty)Ltd v C:SARS

Chapter 14.5

Element KT0503: Disposals of an Ordinary Nature (Trading Stock) – Special Considerations

Sub-Elements Tax Act Sections Authoritative Interpretations

Study Guide

28

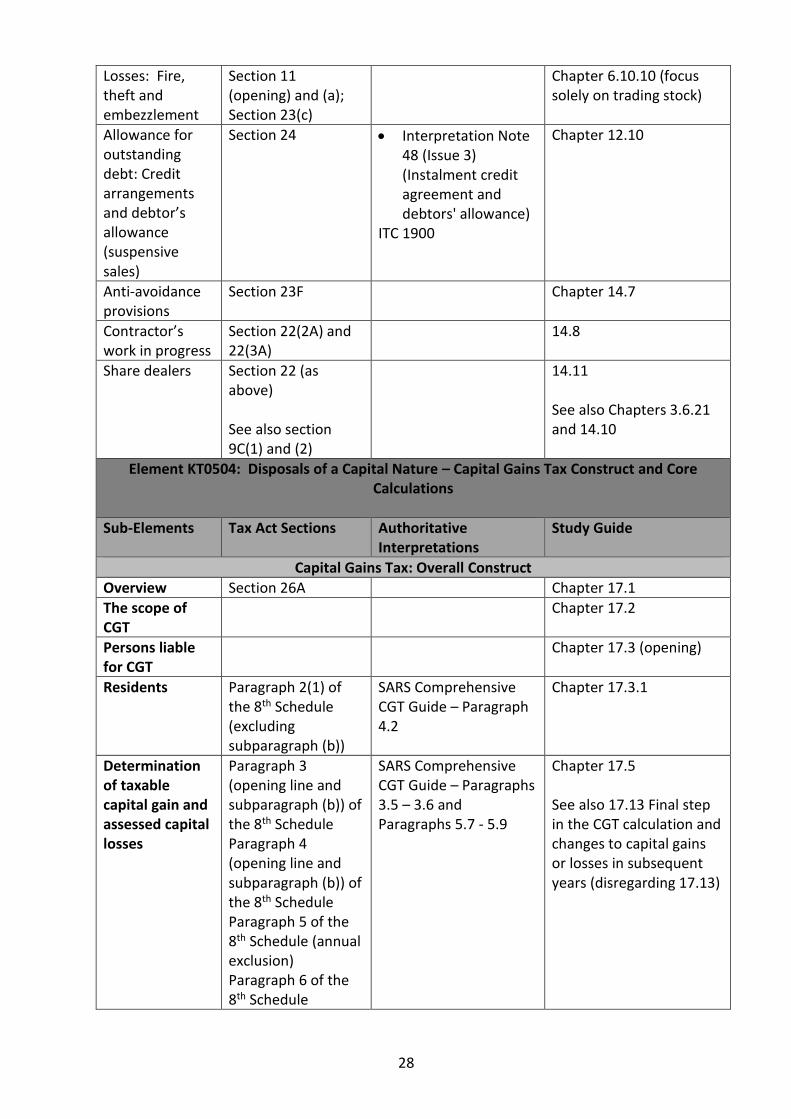

Losses: Fire, theft and embezzlement

Section 11 (opening) and (a); Section 23(c)

Chapter 6.10.10 (focus solely on trading stock)

Allowance for outstanding debt: Credit arrangements and debtor’s allowance (suspensive sales)

Section 24 • Interpretation Note 48 (Issue 3) (Instalment credit agreement and debtors' allowance)

ITC 1900

Chapter 12.10

Anti-avoidance provisions

Section 23F Chapter 14.7

Contractor’s work in progress

Section 22(2A) and 22(3A)

14.8

Share dealers Section 22 (as above) See also section 9C(1) and (2)

14.11 See also Chapters 3.6.21 and 14.10

Element KT0504: Disposals of a Capital Nature – Capital Gains Tax Construct and Core Calculations

Sub-Elements Tax Act Sections Authoritative Interpretations

Study Guide

Capital Gains Tax: Overall Construct

Overview Section 26A Chapter 17.1

The scope of CGT

Chapter 17.2

Persons liable for CGT

Chapter 17.3 (opening)

Residents Paragraph 2(1) of the 8th Schedule (excluding subparagraph (b))

SARS Comprehensive CGT Guide – Paragraph 4.2

Chapter 17.3.1

Determination of taxable capital gain and assessed capital losses

Paragraph 3 (opening line and subparagraph (b)) of the 8th Schedule Paragraph 4 (opening line and subparagraph (b)) of the 8th Schedule Paragraph 5 of the 8th Schedule (annual exclusion) Paragraph 6 of the 8th Schedule

SARS Comprehensive CGT Guide – Paragraphs 3.5 – 3.6 and Paragraphs 5.7 - 5.9

Chapter 17.5 See also 17.13 Final step in the CGT calculation and changes to capital gains or losses in subsequent years (disregarding 17.13)

29

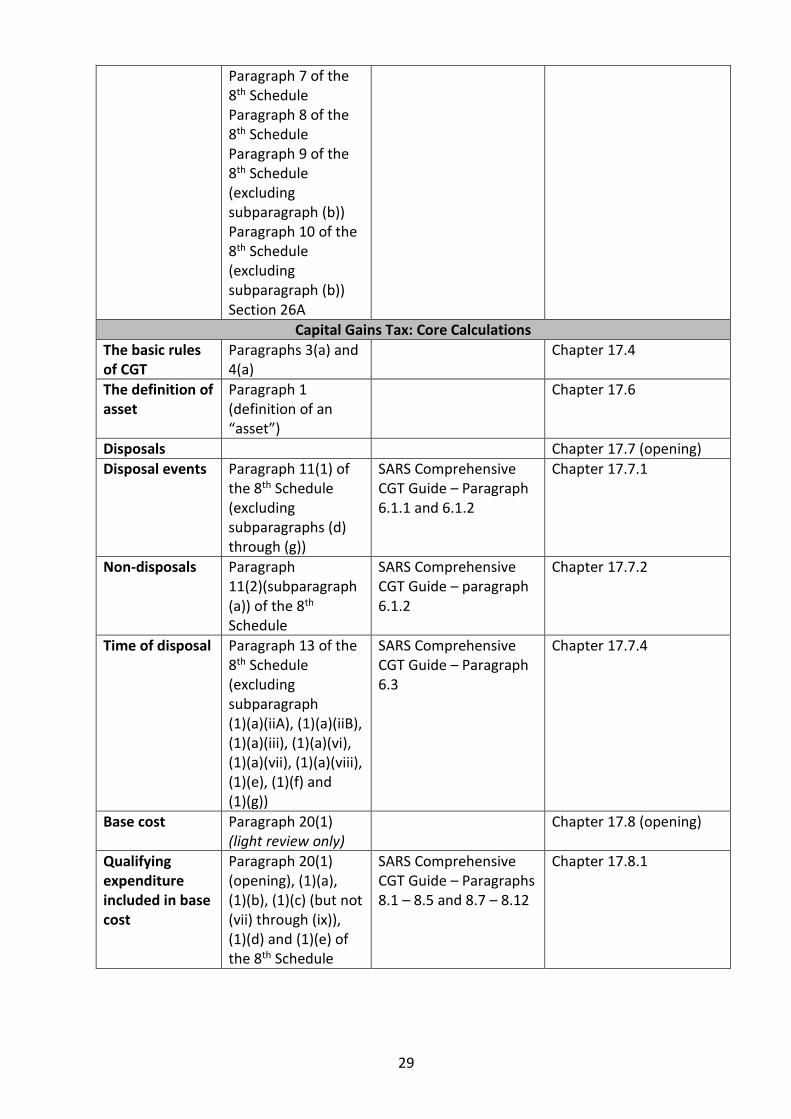

Paragraph 7 of the 8th Schedule Paragraph 8 of the 8th Schedule Paragraph 9 of the 8th Schedule (excluding subparagraph (b)) Paragraph 10 of the 8th Schedule (excluding subparagraph (b)) Section 26A

Capital Gains Tax: Core Calculations

The basic rules of CGT

Paragraphs 3(a) and 4(a)

Chapter 17.4

The definition of asset

Paragraph 1 (definition of an “asset”)

Chapter 17.6

Disposals Chapter 17.7 (opening)

Disposal events

Paragraph 11(1) of the 8th Schedule (excluding subparagraphs (d) through (g))

SARS Comprehensive CGT Guide – Paragraph 6.1.1 and 6.1.2

Chapter 17.7.1

Non-disposals Paragraph 11(2)(subparagraph (a)) of the 8th Schedule

SARS Comprehensive CGT Guide – paragraph 6.1.2

Chapter 17.7.2

Time of disposal Paragraph 13 of the 8th Schedule (excluding subparagraph (1)(a)(iiA), (1)(a)(iiB), (1)(a)(iii), (1)(a)(vi), (1)(a)(vii), (1)(a)(viii), (1)(e), (1)(f) and (1)(g))

SARS Comprehensive CGT Guide – Paragraph 6.3

Chapter 17.7.4

Base cost Paragraph 20(1) (light review only)

Chapter 17.8 (opening)

Qualifying expenditure included in base cost

Paragraph 20(1) (opening), (1)(a), (1)(b), (1)(c) (but not (vii) through (ix)), (1)(d) and (1)(e) of the 8th Schedule

SARS Comprehensive CGT Guide – Paragraphs 8.1 – 8.5 and 8.7 – 8.12

Chapter 17.8.1

30

Qualifying expenditure excluded from base cost

Paragraph 20(2) of the 8th Schedule (excluding (c)) See also section 23C (VAT adjustment)

SARS Comprehensive CGT Guide – Paragraph 8.16

Chapter 17.8.2

Reduction of base cost

Paragraph 20(3) of the 8th Schedule (excluding subparagraphs (a)(ii), (b)(ii), (b)(iii) and (c))

SARS Comprehensive CGT Guide – Paragraphs 8.17, 8.18 and 8.19

Chapter 17.8.3

Cancellation of contracts

Paragraphs 11(2)(o) and 20(4) of the 8th Schedule

SARS Comprehensive CGT Guide – Paragraph 8.20

Chapter 17.8.5

Limitation of expenditure

Paragraph 21 of the 8th Schedule

SARS Comprehensive CGT Guide – Paragraph 8.23

Chapter 17.8.6

Identical assets Paragraph 32(1), (4)(b) and (6) Note: Only apply these rules in respect of shares (not any other assets)

Chapter 17.8.14

Part-disposals Paragraph 33 (disregarding any pre-2001 effective date assets and (3)(c))

SARS Comprehensive CGT guide – paragraph 8.37

Chapter 17.8.15

Proceeds (opening)

Paragraph 35(1) and (4)

Chapter 17.9 (opening)

Amounts excluded from the definition of ‘proceeds’

Paragraph 35(3) of the 8th Schedule

SARS Comprehensive CGT Guide – Paragraphs 9.1.3 and 9.1.4

Chapter 17.9.1

Element KT0505: Capital Gains Tax: Special Rules

Sub-Elements Tax Act Sections Authoritative Interpretations

Study Guide

Deeming Disposals, Values and Trapped Losses

Deemed disposals

Paragraph 12(2)(c) and (3) of the 8th Schedule See also section 22(8) (skim)

SARS Comprehensive CGT guide – paragraph 6.2.2

Chapter 17.7.3 (but only with reference to switches between trading stock, a capital-use asset and a personal use asset

31

(i.e. items (8), (9), (10) and (11)) See also Chapter 14.6 (i.e. trading stock applied for another purpose)

Disposals and donations not at arm’s length or to a connected person

Paragraph 38(1) of the 8th Schedule See also paragraph 11(1)(a) of the 8th Schedule See also section 22(8) (skim)

SARS Comprehensive CGT guide – Paragraphs 9.4.1 – 9.4.3

Chapter 17.9.5 See also Chapter 14.6 (i.e. donated trading stock)

Exclusions

Exclusion for personal compensation

Paragraph 59 of the 8th Schedule

Chapter 17.10.2 (Other exclusions) (focus only on compensation for personal injury, illness of defamation)

Exclusion for gambling

Paragraph 60 of the 8th Schedule

Chapter 17.10.2 (Other exclusions) (focus only on gambling, games and competitions)

Exclusion for donations to public benefit organisations

Paragraph 62 (opening) and (b) of the 8th Schedule See also section 18A(3) and (3A)

SARS Comprehensive CGT guide – Paragraph 12.11

Chapter 17.10.2 (Other exclusions) (focus only on donations to public benefit organisations) See also Chapter 7.4.2 (Other exclusions) (limited solely to donations in kind)

Exclusions for exempt persons

Paragraph 63 of the 8th Schedule

SARS Comprehensive CGT guide – Paragraph 12.12

Chapter 17.10.2 (Other exclusions) (focus only on exempt persons)

Exclusions for assets producing exempt income

Paragraph 64 of the 8th Schedule (disregarding (b))

Chapter 17.10.2 (Other exclusions) (focus only on assets used to produce exempt income)

Topic KT06: Allowance / Depreciable Assets: Impairments

Elements Tax Act Sections Authoritative Interpretations

Study Guide

KT0601: General depreciation concepts

32

Overview Chapter 13.1 (Overview) and 13.2 (Core Concepts)

Connected person (anti-avoidance rules)

Section 1 “connected person definition Sections and 11(e) and 12C(1) (light review) Section 12C(1) (light review) Paragraph 1 “depreciable asset

SIR v Safrenmark (Pty) Ltd

Chapter 13.2.1 Chapter 13.2.2 Chapter 13.2.3 Chapter 13.2.4

Repairs Section 11(d) SARS Interpretation Note 74 (Issue 2)

Chapter 12.4 (see also – Element KT0404)

Qualifying expenditure included in base cost

See also paragraph 20(1)(e) of the 8th Schedule

Chapter 17.8.1

KT0602: Depreciation of movable assets

Wear-and-tear allowance

Section 11(e) (excluding subparagraph (iA) and (iiiA))

SARS Interpretation Note 47 (also Binding General Ruling 7)

Chapter 13.3.1 Appendix E (Write-off periods acceptable to SARS)

Movable assets used by manufacturers, for research and development or by hotelkeepers, and ships, aircraft and assets used for the storage and packing of agricultural products

Section 12C(1)(but not (1)(bA), (c), (d) through (g)) taking into account only assets acquired on or after 1 January 2017 Section 12C(2), (4A) and (6)

SARS Practice Note (also Binding General Ruling 7)

Chapter 13.3.3 (focus only on plant or machinery used by the taxpayer, excluding leased assets and reductions for periods in which trade was not included in income)

KT0603: Depreciation of immovable assets

Allowances on immovable assets

SARS guide to building allowances

Chapter 13.4

Buildings and improvements: Annual allowance

Section 13(1) (opening), (a), (d), (dA), (f) and (proviso (b)), (9)(definition of “improvements”)

Chapter 13.4.1

33

Commercial buildings

Section 13quin(1) and (7)

Chapter 13.4.5

Residential units Section 1 (definition of “residential unit”) Section 13sex(1) (excluding the proviso) and (8)

Chapter 13.4.3

KT0604: Amortisation of intangible property

Intellectual property

Sections 11(gB) and (gC)

Chapter 13.8 (disregard research and development)

Topic KT0507: Allowance / Depreciable Assets: Recoupments

Elements Tax Act Sections Authoritative Interpretations

Study Guide

KT0701: Recoupments (General recoupment provision)

NT Section 8(4)(a) Omnia Fertilizer Limited v CSARS CSARS v Pinestone Properties CC

Chapter 13.10.1 (focus solely on section 8(4)(a) on disposal of section 11(e), 12C, 13 13quin and 13sex assets)

KT0702: Alienation, loss or destruction allowance

Section 11(o)

SARS Interpretation Note 60 (Issue 2)

Chapter 13.11

Topic KT08: Tax Reporting and Payments

Elements Tax Act Sections Authoritative Interpretations

Chapter No

KT0801: Conceptual

overview of income

tax registration

Section 22(1) and (2) of the Tax Administration Act; Section 23 of the Tax Administration Act Section 216 of the Tax Administration Act

Chapter 33.3.1 (“Registration and changes in particulars”)

KT0802: Submission of

final annual income

tax returns and

payments

Sections 25 ad 27 of the Tax Administration Act

Chapter 33.3.2.1 (“Form and timing of returns”)

KT0803: Record

retention Sections 29, 30(1), 31 and 32 of the Tax Administration Act

Chapter 33.3.3 (opening) (“Returns and Records”), 33.3.3.1 (“Retention

34

period”), 33.3.3.2 (“Form of records kept or retained”), 33.3.3.3 (“Access to records”) and 33.3.4 (“Positions taken when preparing returns”)

KT0804: Refunds Section 190(1) through (4) and (6) of the Tax Administration Act Section 191(1) and (3) of the Tax Administration Act

Chapter 33.3.7.5

Element KT0805: Provisional Taxpayers

Sub-Elements Tax Act Sections Authoritative Interpretations

Chapter No

Overview Chapter 11.1 See also Chapter 11.12 (“Summary of provisional tax”)

Important definitions The definition of provisional taxpayer (disregarding all the exclusions other than (dd)(B)) in paragraph 1 of the 4th Schedule

Chapter 11.2

Registering for provisional tax

• Section 22 of the Tax Administration Act

• Skim section 234 of the Tax Administration Act

Chapter 11.3

Element KT0806: First, Second and Top-Up Provisional Payments

35

Sub-Elements Tax Act Sections Authoritative Interpretations

Chapter No

Estimate of taxable income

Paragraphs 19(1), (2), (3), (5) and (6) of the 4th Schedule Skim paragraphs 24 and 25 of the 4th Schedule

SARS Interpretation Note 1

Chapter 11.5

Normal tax rate used to calculate provisional tax payments

Paragraph 17 of the 4th Schedule (review lightly)

Chapter 11.6

Provisional tax payments for persons other than companies

Paragraph 21 of the 4th Schedule

Chapter 11.7

Provisional tax payments for companies

Paragraph 23 of the 4th Schedule

Chapter 11.8

Element KT0807: Provisional tax penalties and interest

Sub-Elements Tax Act Sections Authoritative Interpretations

Chapter No

Late payment penalty

Paragraph 27 of the 4th Schedule

Chapter 11.9.1

Underpayment penalty

Paragraph 20(1) and (2) of the 4th Schedule See also sections 213 and 214 of the Tax Administration Act

Chapter 11.9.2

Interest in respect of the late payment of provisional tax

Section 89bis (interest on overdue 4th schedule taxes)

Chapter 11.10.1

Interest on the underpayment and overpayment of provisional tax

Section 89quat

Chapter 11.10.2

Additional provisional tax payments

Paragraph 23A(1) of the 4th Schedule

11.10.3

Advanced Tax Fundamentals – Knowledge Module #2

36

Topic KT01: Capital and Allowance Asset Rollovers and Deferrals

Elements Tax Act Sections Authoritative Interpretations

Chapter No

KT0101: Conceptual Overview

Chapters 17.10 (opening) (“Exclusions, roll-overs and attributions”) and 17.10.3 (opening) (“Roll-overs”)

KT0102: Transfer of assets between spouses

Paragraph 67 of the 8th Schedule

Chapter 17.10.3.3

KT0103: Involuntary Disposals

Paragraph 65 of the 8th Schedule

SARS CGT guide – Paragraph 13.1

Chapter 17.10.3.1

KT0104: Reinvestment in replacement assets

Paragraph 66 of the 8th Schedule

SARS CGT guide – Paragraph 13.2

Chapter 17.10.3.2

KT0105: Recoupment rollovers for involuntary disposals and reinvestment replacement

Section 8(4)(e), (eA) – (eE) Note: Recoupment analogue for paragraphs 65 and 66 of the 8th Schedule

Chapter 13.10.3 (“Recoupments: Deferred recoupment of allowances”)

KT0106: Reacquired financial instruments

Paragraph 42(1) of the 8th Schedule

Chapter 17.12.2

Topic KT02: Leases

Elements Tax Act Sections Authoritative Interpretations

Chapter No

KT0201: General lease income and expense

Section 1 “gross income” definition and section 11(a)

KT0202: Lease premiums (lessor income)

Paragraph (f) of the definition of gross income in section 1(1). See also section 1: Gross income definition before paragraph (a)

Chapter 4.9

37

KT0203: Lease premiums (lessee deductions)

Section 11(f)

Chapter 13.7.1

KT0204: Leasehold improvements (lessor income)

Paragraph (h) of the section 1 “gross income” definition

Chapter 4.11

KT0205: Leasehold improvements (lessee deductions)

Section 11(g) Chapter 13.7.2

KT0206: Relief for lessor (lessor’s special allowance)

Section 11(h) Chapter 13.7.3

KT0207: Leasehold improvements as a non-disposable event

Paragraphs 13(1)(b) and 33(3)(c)

Chapter 17.12.4 (Leasehold improvements)

KT0208: Recoupments: Acquisition of hired assets

Rent paid that is subsequently applied to reduce purchase price. Section 8(5) (a) and (b) Lessor acquires the asset after termination of the lease. Section 8(5)(bB)

Chapter 13.10.6

KT0209: Deductions in respect of improvements not owned by the taxpayer

Section 12N(1) (light review)

Chapter 13.7.4

Topic KT03: Debt / Loans (Initial Funding and Repayment)

Elements Tax Act Sections Authoritative Interpretations

Chapter No

KT0301: Debt instruments (Initial loan and full repayment)

Genn & Co. (Pty) Ltd v. CIR

Chapter 16.2 (overview)

KT0302: Common principles that apply

Chapter 16.2.1 (opening)

38

to lenders and borrowers

KT0303: Application of section 24J

Section 24J(1) (paragraphs (c) and (d) in terms of the definition of instrument) Section 24J(12); see also section 1 (gross income definition) and section 11(a)

Chapter 16.2.1.1

KT0304: Meaning of interest

Section 24J(1) (definition of interest (disregarding (c))

Chapter 16.2.1.2

KT0305:Timing provisions of section 24J: Yield to maturity method

Section 24J(1) (definitions of “term”, “accrual period”, “accrual amount”, “initial amount and adjusted initial amount”, “yield to maturity”

16.2.1.3 Chapter 16.2.1.3

KT0306: Lender perspective: Taxability of interest received or accrued

Section 24J(3) (disregarding (b))

Chapter 16.2.2

KT0307: Borrower perspective: Deductibility of interest incurred

Section 24J(2) (disregarding (b))

Chapter 16.2.3 (disregarding 16.2.3.4 interest incurred on loans to acquire shares in a controlled company)

KT0308: Timing provisions of section 24J: Alternative methods

Sections 24J(2)(b) and 24J(3)(b) Section 24J(1) (alternative method definition)

Chapter 16.2.1.4

Topic KT04: Foreign Currency

Elements Tax Act Sections Authoritative Interpretations

Chapter No

KT0401: Conceptual Overview

Chapter 15.1

KT0402: Translation of foreign currency amounts

Chapter 15.2 (opening)

39

KT0403: Definitions Section 1: Definitions of “average exchange rate” and “spot rate”

SARS Interpretation Note 101

Chapter 15.2.1

KT0404: General translation rule

Section 25D(1) and (3)

4.12.1 Determination of taxable income in foreign currency

Chapter 15.2.2 (focus solely on section 25D(1) and (3) and Note 1)

KT0405: Specific translation rule: Exchange differences on exchange items

Charging provision: Section 24(2) Calculation: Section 24I(3) Subsection (1) definitions: Definitions of “exchange item” (Step 1), “ruling exchange rate” (step 2) “exchange difference” (step 3)

Comprehensive Guide to Capital Gains Tax (Issue 6): Paragraph 19.1, 19.3, 19.4 and 19.5 of the SARS Interpretation Note 101: Paragraph 4.12.2 (Assets disposed of or acquired in foreign currency)

Chapter 15.3 (Opening) (Focus only on foreign cash and foreign denominated loans)

KT0406: Potential application of the foreign currency mark-to-market rules

Chapter 15.3.1 (Step 1: Identify the exchange item and determine if section 24I applies)

KT0407: Timing rules for the foreign currency mark-to-market rules

Chapter 15.3.2 (Step 2: Determine the ruling exchange rate) See also Chapter 15.6.3 (“Commencement or cessation of application of provisions of section 24I”)

KT0408: Ordinary gain or loss calculation for the foreign currency mark-to-market rules

Chapter 15.3.3 (Step 3: Calculate the foreign exchange differences (ignore bad debts))

KT0409: The acquisition and

Paragraph 43(1), (1A) and (7) of the 8th Schedule

Chapter 15.7 (Specific transaction

40

disposal of assets in foreign currency

Note: Foreign currency itself is not an “asset” (see the “asset” definition in paragraph 1 of the 8th Schedule)

rule: Disposal and acquisition of assets)

Topic KT05: Government Grants

Elements Tax Act Sections Authoritative

Interpretations Chapter No

KT0501: Subsidies Section 1: Before paragraph (a) of the gross income definition

Chapter 3.6.22

KT0502: Government grants

Section 1: Paragraph (lC) of the gross income definition

Chapter 4.17

KT0503: Amounts received in respect of government grants

Section 12P (but not (2)(b), (2A) and (6)(b)) See also section 10(1)(y)

Chapter 5.8.3

Topic KT06: Basic Overview of Business Incentives (Diagnostic Awareness Only) Note: Trainees are expected to have an awareness of the taxation of farming and mining operations but are not expected to perform detailed calculations.

Elements Tax Act Sections (Light Review Only)

Chapter

KT0601: Intellectual property and research and development

Section 11D Chapter 13.8

KT0602: Urban development zones

Section 13quat Chapter 13.4.2

KT0603: Industrial policy project allowance

Section 12I Chapter 13.9.2

KT0604: Companies operating in special economic zones

Sections 12R and 12S Chapter 19.5.5

KT0605: Learnership agreements

Section 12H Chapter 12.2.8

41

KT0606: Employment Tax Incentive (Payroll Credits)

The Employment Tax Incentive Act, 2013

Chapter 10.12 (The Employment Tax Incentive Act, 2013)

Topic KT07: Small and Micro Business Relief

KT0701: Small Business Relief

Sub-Elements Tax Act Sections Authoritative Interpretations

Chapter No

Small business corporations and Appendix B (Rates of Tax and Other Information)

Section 12E(4)(excluding (ii)(bb) through (ii)(gg) and (iv) of the “small business corporation” definition) Paragraph 5 of the Rates and Monetary Amounts Amendment Bill (Act No. 14 of 2017 for the 2018 Assessment Year)

SARS Interpretation Note 9 (Issue 7) (Small business corporations)

Chapter 19.5.4

Small business corporations

Section 12E(1) and (1A)

SARS Interpretation Note 9 (Issue 7) (Small business corporations)

Chapter 13.3.4

Interaction of the 6th Schedule with other taxes

Skim sections 10(1)(zJ) and 64F(h) Skim paragraph 57A of the 8th Schedule

Chapter 23.9

KT0702: Micro Business Relief (Diagnostic Awareness Only)

Sub-Elements Tax Act Sections Authoritative Interpretations

Chapter No

Overview Sections 48A and 48B Chapter 23.1

Qualifying Turnover Paragraphs 1 through 4 of the 6th Schedule

Chapter 23.2

Micro Business Paragraphs 5 through 7 of the 6th Schedule

Chapter 23.3

Taxable turnover Chapter 23.4

Levying of turnover tax

Paragraph 8 of the Rates and Monetary Amounts and Amendment

Chapter 23.6

42

Revenue Laws Act (latest year)

Topic KT08: Basics of Farming and Mining Operations (Diagnostic Awareness Only) Note: Trainees are expected to have an awareness of the taxation of farming and mining operations but are not expected to perform detailed calculations.

Elements Tax Act Sections Authoritative Interpretations

Chapter No

KT0801: Conceptual Overview

Second and Final Report on Hard Rock Mining by the Davis Tax Committee (Chapter 2.2.1)

Chapter

KT0802: Gold Formula

• Skim section 1 definition of “mining for gold”

• Skim Paragraph 3(b) of the Rates and Monetary Amounts Amendment Act (latest year)

Second and Final Report on Hard Rock Mining by the Davis Tax Committee (Chapter 2.2.2)

Chapter

KT0803: Operating expenses and CAPEX depreciation

Skim sections 15 and 36

Second and Final Report on Hard Rock Mining by the Davis Tax Committee (Chapters 2.3.1 through 2.3.4)

Chapter

KT0804: Recoupment of assets

Skim paragraph (j) of the “gross income” definition and section 37

Second and Final Report on Hard Rock Mining by the Davis Tax Committee (Chapter 2.3.5)

Chapter

KT0805: Nature of Farming Income

Section 26 Chapters 22.1 (“Overview”), 22.2 (“Framework for the calculation of taxable income of a farmer”) and 22.3 (“Meaning of ‘farming operations’”)

KT0806: Basics of livestock and produce

Skim paragraphs 2 through 9 of the 1st Schedule

Chapter 22.5 (“Livestock and produce”)

43

KT0807: Basics of plantation farming

Skim paragraph 12(1)(g), 14, 15 and 16 of the 1st Schedule

Chapter 22.16 (“Plantation farmers”)

KT0808: Game Farming

SARS Interpretation Note 69

Chapter 22.12 (“Game farmers”)

Topic KT09: Tax Avoidance

KT0901: Main Concepts

Sub-Elements Tax Act Sections Authoritative Interpretations

Chapter No

Overview: Distinction between tax evasion and avoidance

Chapter 32.1

Impermissible tax avoidance arrangements

Section 80A, 80B and 80L (disregard sections 80C through 80K) (light review only)

Chapter 32.2