Embed Size (px)

Citation preview

1

Taklimat Laporan Tahunan 2009 dan Laporan Kestabilan Kewangan & Sistem Pembayaran 2009

Gabenor Bank Negara Malaysia24 Mac 2010

Embargo

Not for publication or broadcast before 1800 hours on Wednesday, 24 March 2010

2 Please check against delivery

Uneven global economic recovery in 2010

•

The global economy is on a recovery path:–

The advanced economies to record modest growth, supported by stimulus measures

– The emerging economies, particularly Asia, to lead the global growth

•

Global financial conditions have stabilised–

But lending activity in the advanced economies remains constrained

3 Please check against delivery

•

Modest growth in the advanced economies due to:

−

Persistent high unemployment

−

Restricted access to credit

−

Sluggish housing market

−

Continued de-leveraging by the private sector

−

Fiscal consolidation plans

Global Growth Projection for 2010

•

Better growth prospects in the emerging economies:

−

Stronger domestic demand

−

Robust financial sector

−

Growing intra-regional trade

Emerging economies leading the recovery

Source: IMF World Economic Outlook (WEO) (January 2010 Update), National

authorities, BNM estimates

2008 2009e 2010f

Annual change (%)

World GDP 3.0 -0.8 3.9

World Trade 2.8 -12.3 5.8

US 0.4 -2.4 2.7

Euro area 0.6 -4.1 1.0

Japan -1.2 -5.2 1.7

East Asia 6.9 5.1 7.7~7.9

Asian NIEs 1.7 -0.9 4.6~4.9

China 9.6 8.7 10.0

ASEAN-4 4.6 1.1 4.4~5.2

India 7.4 6.5 7.7

4 Please check against delivery

Financial conditions have improved but lending activities in the advanced economies yet to resume

-10

-5

0

5

10

15

20

25

Mar

-07

Jun-

07

Sep

-07

Dec

-07

Mar

-08

Jun-

08

Sep

-08

Dec

-08

Mar

-09

Jun-

09

Sep

-09

Dec

-09

yoy, %

Source: National authorities & Haver

1

Lending to non-financial corporations

Credit growth to private sector

UK1

Euro area

US0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

Jan-

2007

Apr

-200

7

Jul-2

007

Oct

-200

7

Jan-

2008

Apr

-200

8

Jul-2

008

Oct

-200

8

Jan-

2009

Apr

-200

9

Jul-2

009

Oct

-200

9

Jan-

2010

LIBOR-OISTED spread

basis points

Source: Bloomberg

Interbank market spreads

Spreads have narrowed But credit growth remains negative

5 Please check against delivery

0

300

600

900

1200

1500

Prior 3Q07

4Q07

1Q08

2Q08

3Q08

4Q08

1Q09

2Q09

3Q09

4Q09

USD bn

0

50

100

150

200

250

300

350

400

450USD bn

Advanced economies losses

Advanced economies capital

Advanced economies cumulative losses (LHS)

Advanced economies cumulative capital (LHS)

Slow progress in financial sector resolution

•

Cumulative bank losses for

advanced economies expected to

reach USD2.6 trillion1

•

As at end-2009, realised

losses have reached USD1.7 trillion2

(65% of expected losses)

•

Continued deleveraging

process

•

Banks remain cautious in view of the ongoing financial reforms

Advanced economies refer to US and EuropeSource: Bloomberg and BNM calculations

1

Based on IMF estimate (October 2009 GFSR)2

BNM calculations based on Bloomberg data

Cumulative bank losses exceeding capital raised

6 Please check against delivery

Source: IMF and national authorities

•

Unprecedented stimulus measures during the crisis have led to rising fiscal deficit in many countries

•

Growing sovereign debt problems and fiscal consolidation may affect strength of growth

Fiscal balance as % of GDP

Large fiscal deficits and rising public debt levels in several advanced economies

-15

-13

-11

-9

-7

-5

-3

-1

Gre

ece

US

Irela

nd

UK

Spai

n

Japa

n

Por

tuga

l

2008 2009e

7 Please check against delivery

3Q 09 4Q 09 2009 2010f

Annual change (%)

Region1 5.5 8.6 5.1 7.7 ~ 7.9PR China 9.1 10.7 8.7 10.0

India 7.9 6.0 6.5 7.7

Indonesia 4.2 5.4 4.5 5.5 ~ 6.0

Singapore 0.6 4.0 -2.0 4.5 ~ 6.5Malaysia -1.2 4.5 -1.7 4.5 ~ 5.5Chinese Taipei -1.0 9.2 -1.9 4.7Korea 0.9 6.0 0.2 4.6

Hong Kong SAR -2.2 2.3 -2.7 4.0 ~ 5.0

Thailand -2.7 5.8 -2.3 3.5 ~ 4.5

Philippines 0.4 1.8 0.9 2.6 ~ 3.6f

forecast 1 excluding IndiaSource: National authorities, IMF

Regional economies to lead global growth Asian Region: Growth Outlook for 2010

8 Please check against delivery

Modest inflation in 2010

-6

-4

-2

0

2

4

6

8

10

Jan-

09

Feb-

09

Mar

-09

Apr

-09

May

-09

Jun-

09

Jul-0

9

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Indonesia Thailand PhilippinesSingapore Malaysia China

yoy,%

Regional inflation rates rising moderately •

Global inflation is expected to rise, albeit moderately in 2010 :

– Improving demand conditions

– Upward trend in commodity prices

•

But, underlying inflation is expected to remain contained

9 Please check against delivery

Uneven recovery to lead to differences in thrust of policy

0

2

4

6

8

10

2008 2009 2010

China

Thailand

Indonesia

Korea

%

Philippines

Malaysia

0

1

2

3

4

5

6

2008 2009 2010

%

US

Euro area

UKJapan

Regional economies: Stronger growth expected

Advanced economies: Recovery and improving financial conditions

Key interest rates, % Key interest rates, %

10 Please check against delivery

The Malaysian economy is projected to grow by 4.5% to 5.5% in 2010

•

Growth will be underpinned by strengthening domestic demand and an improving external environment

•

The underlying strong fundamentals will provide support to a private sector-led recovery

•

Continued access to financing key in supporting private sector-led growth

-2

-1

0

1

2

3

4

5

6

7

2001

2002

2003

2004

2005

2006

2007

2008

2009

p/

2010

f/

Annual change (%)

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

4.5%

5.5%

11 Please check against delivery

Strengthening domestic demand to drive growth, reinforced by external demand

2009p 2010f 2009p 2010f

Annual change (%) Contribution to growth (p.p)

Domestic demand -0.4 3.2 -0.3 2.8Private sector -3.4 3.3 -2.2 2.1

Consumption 0.8 3.8 0.4 2.0Investment -21.8 0.7 -2.6 0.1

Public sector 7.7 2.7 1.9 0.7Consumption 3.7 -2.7 0.5 -0.4

Investment 12.9 9.3 1.3 1.1Net exports 8.4 -18.6 1.1 -2.7

Exports of G&S -10.1 7.7 -12.0 8.3Imports of G&S -12.5 11.7 -13.1 11.0

Real GDP -1.7 4.5 ~ 5.5 -1.7 4.5 ~ 5.5

12 Please check against delivery

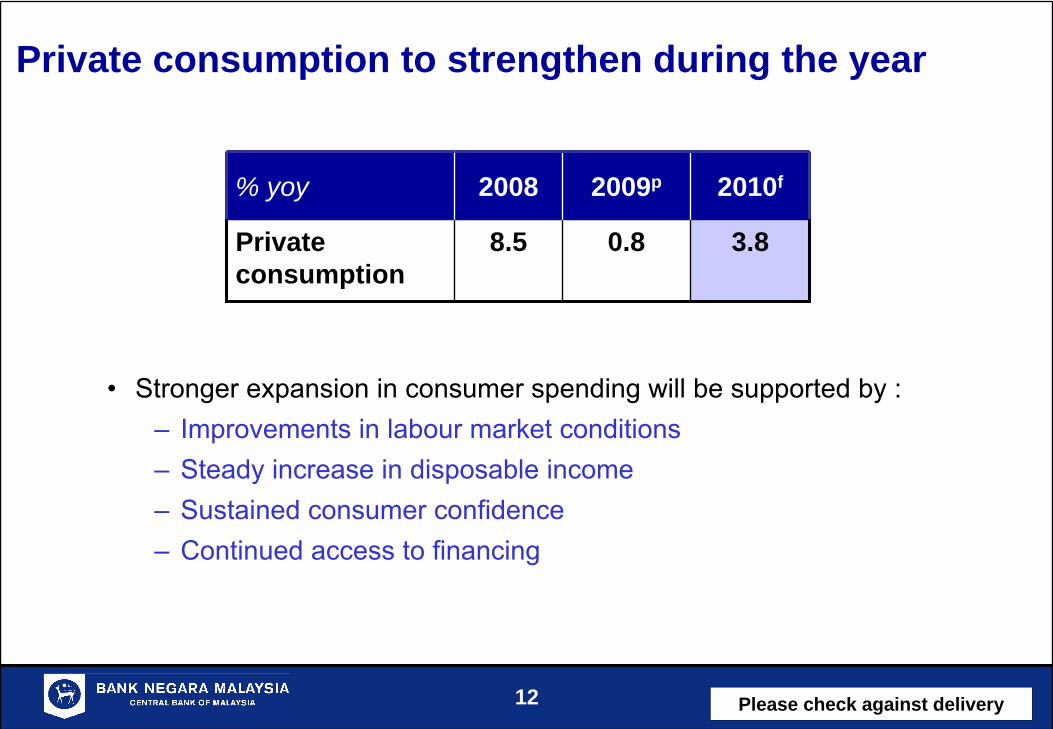

Private consumption to strengthen during the year

% yoy 2008 2009p 2010f

Private consumption

8.5 0.8 3.8

•

Stronger expansion in consumer spending will be supported by :–

Improvements in labour market conditions

– Steady increase in disposable income

– Sustained consumer confidence

– Continued access to financing

13 Please check against delivery

Improving labour market conditions in 2010

2.4

3.1

3.43.6

3.6

3.3

3.7

1.5

2.0

2.5

3.0

3.5

4.019

97

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

e

2010

f

Unemployment rate (as % of labour force)

-4

-2

0

2

4

6

8

10

annual change (%)

Employment (RHS) Labour force(RHS) Unemployment rate (LHS)

Lower unemployment rate in 2010

e Estimatef Forecast

Source: Economic Planning Unit

14 Please check against delivery

Private investment to recover gradually

% yoy 2008 2009p 2010f

Real private investment 0.8 -21.8 0.7

•

Capital spending is forecast to

recover

with the

strengthening of domestic and external demand

•

Improved business optimism and resumption of projects that have been deferred

Nominal Private Investment

0102030405060708090

2006 2007 2008 2009p/ 2010f/

RM billion

Agriculture Mining ManufacturingConstruction Services

Source: Department of Statistics, Malaysia and BNM

62.1

77.0 80.6

62.565.4

15 Please check against delivery

Gross FDI inflows sustained in 2010

• Gross inflows of FDI at RM32.4 billion in 2010

• Inflows into the manufacturing, services, and oil and gas sectors

Gross FDI inflows into Malaysia

32.4

25.4 27.1

37.3

46.2

31.6

49.0

0

10

20

30

40

50

2004 2005 2006 2007 2008 2009p 2010f

RM billion

p/ preliminary; f/ forecast

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

16 Please check against delivery

Public sector to continue to support domestic demand in 2010

2009p 2010f

Annual change (%)

Public sector 7.7 2.7

Consumption 3.7 -2.7

Investment 12.9 9.3

Contribution to growth (p.p)

Public sector 1.9 0.7

17 Please check against delivery

External trade to expand in 2010Broad-based expansion in external trade

-30

-20

-10

0

10

20

30

2005 2006 2007 2008 2009e/ 2010f/

yoy (%)

-200

-100

0

100

200

RMb

Trade balance (RHS)Exports (LHS)Imports (LHS)

2009e 2010f

Annual change (%)

Gross exports -16.6 11.2

ManufacturedE&E

Non E&ECommodities

AgricultureMinerals

-12.5-11.0-14.5-27.6-21.6-32.2

10.110.010.316.312.819.4

Source: Department of Statistics, Malaysia and Bank Negara Malaysiae/ estimate f/ forecast

-16.6%

11.2%14.6%

-16.6%

RM116.7b

•

Export expansion to be more broad-based:

– Stronger external demand, particularly from the region

– Higher commodity prices

•

Imports to expand faster than exports:

– expansion in manufactured exports

– higher imports of consumption & capital goods

18 Please check against delivery

Source: Department Statistics, Malaysia and Bank Negara Malaysiap/ preliminary f/ forecast

Current account surplus to narrow but remains significant

•

Trade surplus to narrow as imports expand faster than exports

•

Recovery in external trade and outbound tourism will result in a marginal services deficit

•

Income deficit to widen due mainly to repatriation of profits and dividends by MNCs operating in Malaysia

Narrowing current account surplus

-50

-20

10

40

70

100

130

160

190

220

2006 2007 2008 2009p/ 2010f/

RMb

-5

0

5

10

15

20% GNI

Goods ServicesIncome Current transfersCurrent Account, % GNI (RHS)

14.3%17%

RM112.7b RM103.8b

19 Please check against delivery

Annual change (%) 2009p 2010f

Agriculture 0.4 3.1

Mining -3.8 2.5

Manufacturing -9.3 6.5

Construction 5.7 3.7

Services 2.6 4.9

Real GDP -1.7 4.5 ~ 5.5

Broad-based growth across all sectors

20 Please check against delivery

Services sector to be a key contributor to growth

Sub-sector2009p 2010f

Annual change (%)

Total Services 2.6 4.9

Finance & insurance 4.4 5.2

Real estate & business services 2.1 7.0

Wholesale & retail trade 1.2 4.4

Accommodation & restaurant 2.7 4.8

Transport & storage -2.8 4.8

Communication 6.0 6.5

Utilities 0.4 5.0

Other services 4.4 5.1

Government services 3.0 3.0

•

Higher demand for consumption-related services

•

Continued lending and financial intermediation activities

•

Recovery in trade and manufacturing-related services

21 Please check against delivery

Strong recovery in the manufacturing sector

•

Broad-based expansion across all clusters, reflecting:

Improved external demand

Strengthening of domestic demand

Value-added growth (% yoy)

2009p 2010f

Total Manufacturing -9.3 6.5

Export-oriented -11.7 6.7

E&E -18.7 9.6

Primary-related (e.g. chemicals, petroleum, rubber,

wood)-5.1 4.3

Domestic-oriented -4.5 6.2

Construction-related(e.g. iron & steel, cement)

-2.6 6.5

Consumer-related(e.g. food & beverages,transport equipment)

-9.4 5.4

22

Better performance in the agriculture and mining sectors

% yoy 2009p 2010f

Agriculture 0.4 3.1

Palm oil -1.0 1.1

Rubber -20.2 20.3

Mining -3.8 2.5

Crude Oil -4.4 1.8

Natural gas -4.0 2.5

Agriculture•

Production of palm oil and rubber are expected to increase to meet higher demand

Mining•

Higher crude oil production with the recovery in demand

•

Higher gas output partly reflecting LNG exports to China

23 Please check against delivery

Construction sector to maintain growth momentum

•

Growth supported by the second stimulus package, benefiting the civil engineering and non- residential sub-sectors, and the remaining projects under the Ninth Malaysia Plan

•

Continued growth in residential

sub-sector due to stronger demand

2.1

5.7

3.7

4.7

0

1

2

3

4

5

6

2007 2008 2009p/ 2010f/

% yoy

Growth in the Construction Sector

24 Please check against delivery

Headline inflation to remain modest at 2.0 – 2.5% in 2010

0

1

2

3

4

5

6

2005 2006 2007 2008 2009 2010/f

Annual change

(%)

Inflation Forecast for 2010

2.0 – 2.5%

• Price increase in 2010 modest reflecting :

– Improving demand conditions

– Potential adjustments to administered prices

25 Please check against delivery

OPR

2.0%

3.5%

2.25%

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep

-08

Nov

-08

Jan-

09

Mar

-09

May

-09

Jul-0

9

Sep

-09

Nov

-09

Jan-

10

Mar

-10

%

Monetary policy remains supportive of economic growth

The OPR was raised by 25 bps in March •

OPR was reduced to a historic low in early 2009 under extraordinary conditions

•

Given improved economic outlook, the OPR was adjusted in March 2010 to:

o

normalise monetary conditions

o

prevent the risk of financial imbalances that could undermine the economic recovery process

•

Monetary policy continues to remain accommodative to provide support to domestic economic activity

26 Please check against delivery

Continued access to financing is a key support to economic recovery

Net financing through banking system loans and PDS

Feb-109.9%

56789

1011121314

Jan-

09

Feb-

09

Mar

-09

Apr

-09

May

-09

Jun-

09

Jul-0

9

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Feb-

10

yoy, %

Q3 09: 7.2%

Q4 09: 8.5%

•

Financing to businesses and households increasing, supported by :–

continued access to financing

– ample liquidity

– low interest rate environment

•

Expansion in other sources of financing

Domestic Sources of Financing for the Private Sector as at end 2009

PDS19%

DFIs6%

Other financial intermediaries

9%

Equities13%

Banking system loans53%

27 Please check against delivery

Commercial Banks' Lending Rates

4.85%

Average Lending Rate

5.76%

Base Lending Rate

4

6

8

10

12

14

Jan

95

Mar

96

May

97

Jul 9

8

Sep

99

Nov

00

Jan

02

Mar

03

May

04

Jul 0

5

Sep

06

Nov

07

Jan

09

Mar

10

%

15 M

ar 1

0p

Cost of financing remains low

• BLR responded to OPR adjustments

• Lending rates remained near historical lows :

– Base lending rate: 5.76% (15 March 2010)

– Average lending rate: 4.85% (end-Feb 2010)

P

Preliminary

28 Please check against delivery

Deposit rates have increased

Term Structure of FD rates

2.052.042.032.00

2.50

2.35

2.32.25

2.35

2.66

1.9

2.0

2.1

2.2

2.3

2.4

2.5

2.6

2.7

1 3 6 9 12

mths

% p.a.

Post OPR hike(15 Mar '10p)

Pre-OPR hike(Feb '10)

P

Preliminary

•

FD rates raised by 16-30 bps following increase in OPR

29 Please check against delivery

Domestic equity market recovered on improving economic conditions

KLCI and Bursa Malaysia sectoral indices

30

40

50

60

70

80

90

100

110

120

Jan-

08M

ar-0

8M

ay-0

8Ju

l-08

Sep

-08

Nov

-08

Jan-

09M

ar-0

9M

ay-0

9Ju

l-09

Sep

-09

Nov

-09

Jan-

10M

ar-1

0

Finance

KLCIIndustrial

Construction

Plantations

Index(Jan 2008=100)

Performance of Major Indices (% growth)

-50.6

-46.0

-49.2

-47.6

-48.3

-48.3

-40.7

-39.3

-38.5

-31.3

-42.1

87.0

78.3

64.5

63.2

63.0

52.0

49.7

45.2

23.5

22.1

19.0

-60 -40 -20 0 20 40 60 80 100

Indon

Taiwan

Spore

Thai

Phil

HK

Korea

Msia

US

UK

Jpn

%

2008 2009

30 Please check against delivery

Ringgit performance driven by external developments and improving domestic fundamentals

•

Ringgit was on a broad appreciating trend, in tandem with regional currencies

•

Generally, orderly ringgit adjustment

Regional: CNY, IDR, KRW, PHP, SGD, TWD, THBMajor: AUD, JPY, EUR, GBP

Movement of Currencies against USD (31 Dec 2008 - 23 Mar 2010)

90

95

100

105

110

115

Dec

-08

Jan-

09

Feb-

09

Mar

-09

Apr

-09

May

-09

Jun-

09

Jul-0

9

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Index 31 Dec 08 =100

Appreciation against USD

RegionalMajor

Ringgit

31 Please check against delivery

For Malaysia, policies will focus on strengthening private sector led growth

•

Strategies being put in place to transition Malaysia to ahigh value-added, high income economy

•

Measures to promote private investment –

incentives for high growth sectors

–

liberalisation of the economy–

privatisation of Government-owned corporations

•

Monetary policy to remain supportive of growth

•

Ensure continued access to financing

32

Bank Negara Malaysia Annual Accounts 2009

33 Please check against delivery

•

Total assets of BNM increased by RM18.5 billion to RM363 billion with international reserves of RM331.3 billion (USD96.7 billion)

•

Net profit of RM7.7 billion

•

Dividend paid amounted to RM2 billion

Financial position of the Bank remained strong in 2009

34

FINANCIAL STABILITY AND PAYMENT SYSTEMS REPORT 2009

35

Financial system stability was preserved, supported by a well- functioning financial intermediation process and orderly financial markets

36 Please check against delivery

High degree of financial system resilienceBanking sector (%) Dec 08 Jan 10Risk-weighted capital ratio 12.6 14.8

Core capital ratio 10.6 13.3Capital buffer (RM billion) 38.7 60.3Insurance sector (%) Dec 08 Dec 09Capital adequacy ratio 187.6 230.0

Capital buffer (RM billion) 12.3 18.6

•

Strong solvency position–

Forward looking capital management since 2008

–

High quality of capital

•

Loan quality intact–

Improved underwriting standards

–

Pro-active management of debts

–

Historical high provisions

•

Profitability sustained–

RoE

of 13.9% and RoA

of 1.2%0

2

4

6

8

10

12

2001 2002 2003 2004 2005 2006 2007 2008 2009 Jan'10

%Net NPL ratio

1.7%1.8%2.2%3.2%

37 Please check against delivery

0

2

4

6

8

10

12

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

RM billionPDS issued

Loans approved - Large Businesses

2009

0

5

10

15

20

25

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

RM billionLoans approved - HouseholdsLoans approved - SMEs

2009

Access to financing supported early recovery

38 Please check against delivery

Improving quality of loan portfolio

0

10

20

30

40

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

RM billion

0

1

2

3

4

5%

2- <3 month1- <2 month2- <3 month (% of total loans)1- <2 month (% of total loans)

2007 2008 20090

2

4

6

8

10

12

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

%

Large businesses SMEs Households2007 2008 2009

Stable loans-in-arrearsNPL ratio on steady decreasing trend

39 Please check against delivery

Financial stability supported by supervisory vigilance and robust prudential framework•

Early and prompt detection and management of emerging risks–

Enhanced surveillance and stress testing –

Strengthening of home-host supervisory engagementto support consolidated supervision

•

Improved risk management and governance practices–

Implementation of more sophisticated approaches to assessments of capital adequacy under Basel II and Risk-Based Capital Framework

–

Continued strengthening of capital buffers to withstand potential shocks–

Enhanced liquidity framework to address market disruptions and foreign currency exposures

–

Continued improvements in governance practices–

Strengthened oversight capability of boards of financial institutions

40 Please check against delivery

Policy measures to enhance access to financing

•

Special funds–

SME Assistance Guarantee Scheme (RM 2 billion)

–

Working Capital Guarantee Scheme (RM 7 billion)–

Industry Restructuring Guarantee Scheme (RM 3 billion)

•

Avenues for debt restructuring–

Large corporations: Corporate Debt Restructuring Committee (CDRC)

–

SMEs

: Small Debt Resolution Scheme (SDRS)–

Individuals

: Agensi

Kaunseling

dan

Pengurusan

Kredit

(AKPK)

•

Avenues for complaints and financial advice–

BNM Integrated Contact Centre

–

ABMConnect

•

Introduction of credit enhancement agency in 2009–

Danajamin

Nasional

Berhad

41 Please check against delivery

Developmental strategies continued to be pursued - In addition to institutional arrangements, mechanisms and schemes for access to financing

• Enhance interlinkages with international economies

–

Liberalisation

plan for financial sector–

MoUs

to strengthen bilateral and multilateral cooperation–

Reinforce international dimension of Islamic finance

• Promote financial inclusion

–

Raise level of financial literacy –

Operational flexibilities for new branches and bancassurance

arrangements for insurance companies and takaful

operators

• Continuous priority on human capital development

–

Asian Institute of Finance (AIF) fully operationalised

to coordinate human capital development initiatives

–

Continuous enhancement to FSTEP programme

design and delivery–

Enhance FIDE programme

for boards of financial institutions

42 Please check against delivery

Outlook for domestic financial stability

•

Malaysian financial system has adequate buffers to withstand external risks and domestic challenges–

Banking system capitalisation expected to remain >10% under most

challenging stress test scenario

•

Downside risks mainly stem from external environment–

Sustainability of global economic recovery

–

Orderly exit from unconventional support measures

–

Reforms in global prudential regulations and regulatory structure

–

Destabilising capital flows

43 Please check against delivery

Supported by strengthened financial stability framework under Central Bank of Malaysia Act 2009

•

Greater clarity in mandates, functions and power

•

Captures core elements of macroprudential stability–

Ex-ante surveillance powers for timely risks identification

– Pre-emptive powers to avert or mitigate systemic risks

– Ex-post powers for resolution to reduce impact of instability

•

Complemented by strengthened framework for governance, transparency and accountability

•

Positions the Bank to effectively address current and future challenges

44 Please check against delivery

Areas of focus for financial sector in 2010•

Blueprint for financial sector development–

Develop a strong and stable financial sector that best serves Malaysia

–

Competitive, dynamic and inclusive financial system

•

Comprehensive review of existing legislations to ensure an effective and efficient legislative framework to: –

Align legislation with more principle-based and differentiated supervisory approaches

–

Enhance appropriate enforcement and resolution framework –

Achieve more consistent legal framework across different financial sectors

–

Strengthen market conduct regulation and supervision

•

Transition to enhanced deposit guarantee scheme

•

Greater internationalisation of sukuk

market

45 Please check against delivery

Thank you