Embed Size (px)

Citation preview

✓ There are rising concerns in the country that the negotiation over the EFF program will not

be reopened for discussion during the spring, after the Article IV mission is done by the IMF.

✓ The immunization process has still not started in B&H, while none of the authorities, cannot

confirm when and how many doses of vaccine will arrive from the COVAX program and

paid 1.23 mn vaccines doses for B&H.

✓ The final month of Q4 brought slightly stronger than expected rebound of the key real

sector heavy-weight indicators such are - exports of goods and industrial production

finally breaking out to positive territory. Positive outlook remains for Q1 and overall 2021.

✓ Total loans by the CBBH report as of December 2020 confirmed further deterioration with

-2% yoy decline which is the value not seen since the GFC. The decline was driven by both

segments Corporate and Retail (PI).

✓ We have adjusted the pace of recovery in 2021 GDP down to 3% yoy in real terms, under the

assumption that the distribution and vaccination process in the Western Balkan and B&H

will improve from its current slow pace, along with current quite high level of people

already recover from the COVID-19, we hope to see some level of “herd immunity” and no

further hard lock-down measures in Q3 and Q4 in B&H in 2021.

No.33

2

Highlights

Source: Central Bank of B&H, Raiffeisen BANK dd BiH

✓ The entity level Budgets for 2021 were planned and adopted with the

EFF funds planned from the IMF, but with current firms stand from RS

authorities, there are rising concerns in the country that the

arrangement will not be reopened for discussion during the spring,

after the Article IV mission is done by the IMF.

✓ At the time when the world has started with more massive vaccination

while vaccinated number of people in the SEE region is also moving

ahead (especially in Serbia with 13% vaccinated population being

second the best in Europe), the immunization process has still not

started in B&H. none of the authorities, starting from the state to entity

levels, cannot confirm when and how many doses of vaccine will arrive

or from which manufacturer to the country.

✓ The final month of Q4 brought slightly stronger than expected rebound

of the key real sector heavy-weight indicators such are - exports of

goods and industrial production of B&H, which finally have break out to

positive territory and reported positive yoy growth rates in December-

20 (manufacturing finally reported growth strong in positive territory of

+6% yoy in Dec-20). Therefore, we expect growth of industrial

production to be at minimum in range of 4.5-5% yoy in 2021.

✓ Consumer sentiment has slightly improved based on the Retail sales

data over in Q4, while December brought slight upside surprise.

Consequently, Retail sales index contracted by -6.3% yoy in the last

month of the year, marking the 10th straight month of decline in 2020.

However, it is obvious that the holiday season sales at least brought up

some retail sales turnover and dynamics in the last two months of the

year (FY retail sales index was down by -8.3% yoy).

✓ December's data published by CBBH for total loans confirmed further

deterioration ending the year with -2% yoy decline which is the value

not seen since 2009-2010, or the GFC. The decline was driven by both

segment Corporate and retail (PI).

✓ We have adjusted the pace of recovery in 2021 GDP down to 3% yoy in

real terms, under the assumption that the distribution and vaccination

process in the Western Balkan countries will improve from its current

slow pace, and along with current quite high level of people recovered

from the COVID-19, we hope to see some level of “herd immunity” and

no further hard lock-down measures in Q3 and Q4 in 2021.

Credit rating of B&H

Analysts:

Ivona Zametica, Asja Grđo

Tel.: +387 33 287 784

e-mail:

Published by:

Raiffeisen BANK dd Bosnia and

Herzegovina

Investment Banking

Research and Advisory

Highlights

Source: Agency for Statistics of B&H, Central Bank of B&H, Raiffeisen BANK dd BiH

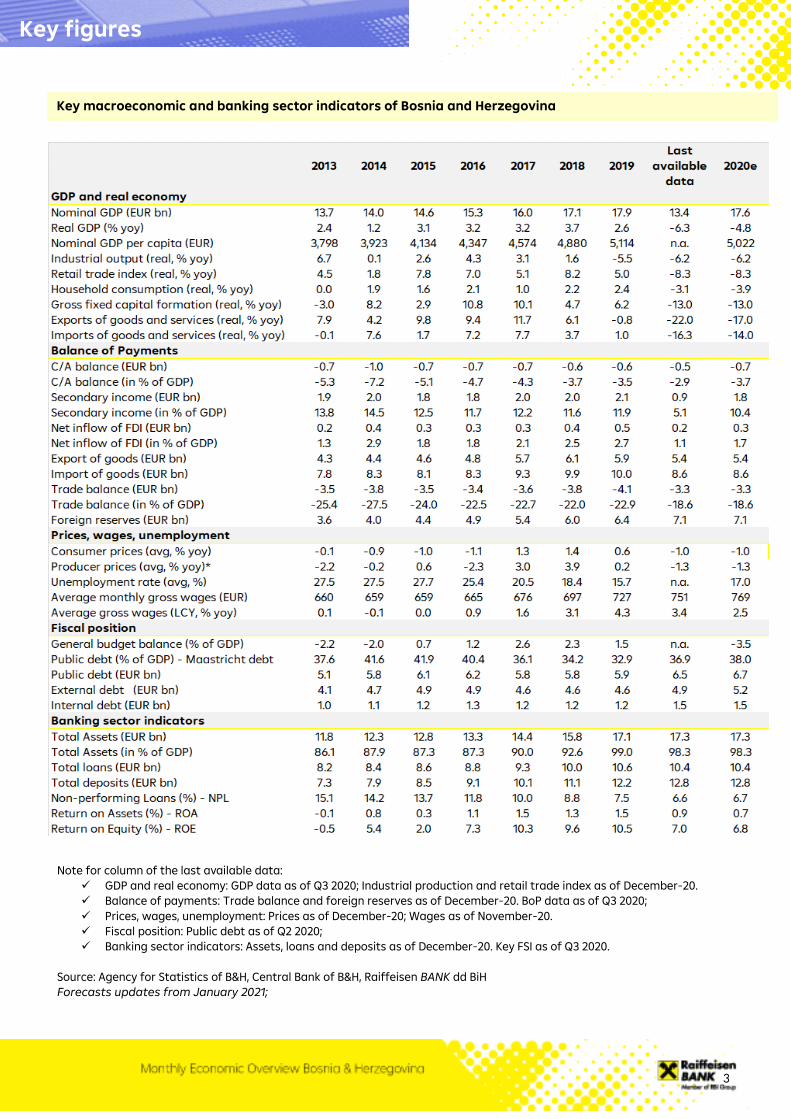

Key macroeconomic figures of Bosnia and Herzegovina

3

Note for column of the last available data:

✓ GDP and real economy: GDP data as of Q3 2020; Industrial production and retail trade index as of December-20.

✓ Balance of payments: Trade balance and foreign reserves as of December-20. BoP data as of Q3 2020;

✓ Prices, wages, unemployment: Prices as of December-20; Wages as of November-20.

✓ Fiscal position: Public debt as of Q2 2020;

✓ Banking sector indicators: Assets, loans and deposits as of December-20. Key FSI as of Q3 2020.

Source: Agency for Statistics of B&H, Central Bank of B&H, Raiffeisen BANK dd BiH

Forecasts updates from January 2021;

Key figures

Key macroeconomic and banking sector indicators of Bosnia and Herzegovina

4

Politics

Source: Raiffeisen RESEARCH

Torn between no progress in the IMF negotiations

and delays in vaccination process

Bosnia and Herzegovina have been the second poorest country in Europe after

Albania with GDP per capita in PPPs of only 32% of the EU average for several

years. The country has been in a very difficult economic and social position for

years now, due to constant political turmoil, instability and lack of continuous

and credible reform processes, outlined to the authorities by the European

Commission (EC) and the international financial institutions (the IMF and the

WB,). One of the new signs of such fragile political and institutional strength

and credibility is also the fact that B&H has entered a new year with the IMF

negotiations being “on hold” since December 2020, over a EUR 750 mn EFF

arrangement (cca. 4% GDP) offered to the country as COVID-19 follow up

financial package. The negotiations have been halted due to a strong

opposition from Republic of Srpska (RS) authorities, over the condition

from the Letter of Intent (LOI) for making the State Registry of Banking

Accounts (all personal and legal entities accounts) within the Central Bank of

B&H (CBBH). This was defined as “transfer of responsibilities from entity to

state level authorities” by RS authorities. Although the entity level Budgets

for 2021 were planned and adopted with the EFF funds from the IMF, with

current firms stand from RS authorities, there are rising concerns in the

country that the arrangement will not be reopened for discussion during

the spring, after the Article IV mission is done by the IMF. Hence, the entity

and lower levels of government will have to find other options and sources of

financing in local and international debt markets for 2021 budgets,

colored by declining tax revenues and rising needs of economy and private

sector after the COVID-19 hit. We expect amending budgets in late spring –

early summer by the entity levels governments and lower authority

levels.

Mostar Elections were the most expected political event in the country

and event closely followed by international community due to its overall

importance for B&H’s political stability. The first voting round which was

publicly done for the Mostar’s Mayor, was suspended by the Office of the High

Representative (OHR) due to stipulations of the City’s Statue. After the second

repeated session of the elections in the City’s Council the outcome was much

clearer. Despite high hopes of civil opposition voters, the opposition B&H Block

failed to agree over a common candidate for the Mostar elections providing

majority for the ruling right-hand oriented parties (HDZ and SDA) who remain

the majority in the City Council. Hence, Mr. Mario Kordic (HDZ BiH) and Mr. Zlatko

Guzin (SDA) candidate of the “Coalition for Mostar”, entered the second round.

In the end, Mr. Kordić (HDZ BiH) I was elected as the new Mayor of Mostar

who was elected in the first City’s elections after 12 years with only one

vote ahead of SDA’s candidate. Therefore, although highly awaited the

Mostar’s Elections in the end were large disappointment for B&H and civil

oriented oppositions voters over the “the most divided city”, as the major right-

hand oriented parties who are leading the Federal government continue to

have the majority in the City Council.

At the time when the world has started with more massive vaccination

while vaccinated number of people in the SEE region is also moving

ahead (especially in Serbia with 13% vaccinated population being second

the best in Europe), the immunization process has still not started in B&H.

The country is still waiting for the first delivery of vaccines from the

COVAX WHO program, which were committed to be delivered by end of

February 2021 the latest. The country was promised to be delivered with 180K

vaccines (23.5K Pfizer and 156.5K from Astra Zeneca) out of 1.2 mn paid by the

country through the COVAX. It was on January 24, 2021 after the meeting of the

Entity Prime ministers and the Chairman of the Council of Ministers when B&H

decided to start the direct procurement and negotiation with vaccines

producers. Although discussed to order directly 202K doses of Russian

Sputnik V, none of the authorities, starting from the state to entity levels,

cannot confirm when and how many doses of vaccine will arrive or from

which manufacturer to the country (above-mentioned doses of these two

distributors would be sufficient to vaccinate 10.9% of people with one dose).

Is the IMF EFF program in question?

side

Mostar elections: new, but the

same..

Vaccination in B&H still has not

started

5

Source: BHAS, Raiffeisen BANK dd BiH

Source CBBH, Raiffeisen BANK dd BiH

Source: BHAS, Raiffeisen BANK dd BiH

Source: BHAS, Raiffeisen BANK dd BiH

B&H industry and exports of goods, finally break

out to positive territory in Dec-20

The final month of Q4 brought slightly stronger than expected

rebound of the key real sector heavy-weight indicators such are -

exports of goods and industrial production of B&H, which finally

have break out to positive territory and reported positive yoy

growth rates in December-20. Despite very strong Wave 2 of COVID-19

infections, seen in Q3 and Q4, which hit all European countries and B&H,

the industry and exports of goods proved to be quite resilient and

continued with further rebound in Q4 which was started in Q3 2020.

Real economy, driven by manufacturing and other segments of

industrial production continue to work uninterrupted in Q4 in

Europe and B&H as well, driving a further bounce back after the full

lock-down and plunge of economy in Q2 and quite pale recovery in

Q3 in case of B&H (+3.9% qoq GDP growth in Q3). Foreign demand is

strongly rebounding and driving the manufacturing lines across the

Europe, bringing also export-driven B&H manufacturing finally to

strong positive territory of +6% yoy in December 2020. However,

second largest industry category - Production and distribution of

electricity was still strongly below 2019 (-6.6% yoy) along with quite low

rebound in Mining (+0.8% yoy) which held overall Industrial production

still at moderate +2.8% yoy in Dec-2020. Therefore, overall industrial

production volume in Q4 2020 was at almost same level and

amount compared to the same period of 2019, as industrial

production was reporting almost flat reading (-0.1% yoy) in Q4-20.

Hence, we expect continuation of positive dynamics in Q1 2021 in

industrial production and manufacturing in B&H, after more than

two years of a deep recession in B&H industry which started back in

Dec-2018. The rebound is expected to be driven by strong rebound of

external demand visible on one hand but also strong “base-effect” from

very low base from after recessionary trends reported for two years in

Manufacturing. Therefore, we expect growth of industrial production to

be at minimum in range of 4.5-5% yoy in 2021.

Even more impressive was the final month, of challenging 2020, for

B&H exporters who reported overall growth in Dec-2020 by +14.8%

yoy bringing overall exports also to positive area in Q4 (+4.5% yoy)

after five consecutive quarters of negative growth from Q3 2019-

Q3 2020. Therefore, total exports of goods reached at the end total

value of BAM 10.5 bn (30.5% of GDP) which is -8.5% yoy compared to

record value of exports from 2019 and in line with our expectation for FY

2020. We expect further increase of exports of goods in 2021 with

expected growth rate in range of 6-7% yoy.

By analyzing the sector structure of exporters, we see that the exports of

Prepared food staff and beverages reported record value of

exports ever, reporting even strong positive FY 2020 performance of

+6.9% yoy or total value of exports of BAM 328 mn. Even more, out of the

most important Exports of goods categories - Furniture exports

managed also to report positive FY 2020 yoy growth rate of 1.1% yoy

or total value of BAM 1.13 bn. Also, impressive and quite resilient proved

to be exports of Plastics and rubber products and Wood and pulp

products, followed by almost equal amount of exports of Machinery

and Mechanical appliances who remain flat in 2020 vs. 2019 (-0.4%

yoy).

GDP performance (qoq)

Structure of industry

Industrial production

Real sector developments

6

Source: CBBH, Raiffeisen BANK dd BiH

Source: CBBH, Raiffeisen BANK dd BiH

Source: Agency for Statistics of B&H,

Source: CBBH, Raiffeisen BANK dd BiH

Revival of domestic demand and private

consumption in Q4 2020

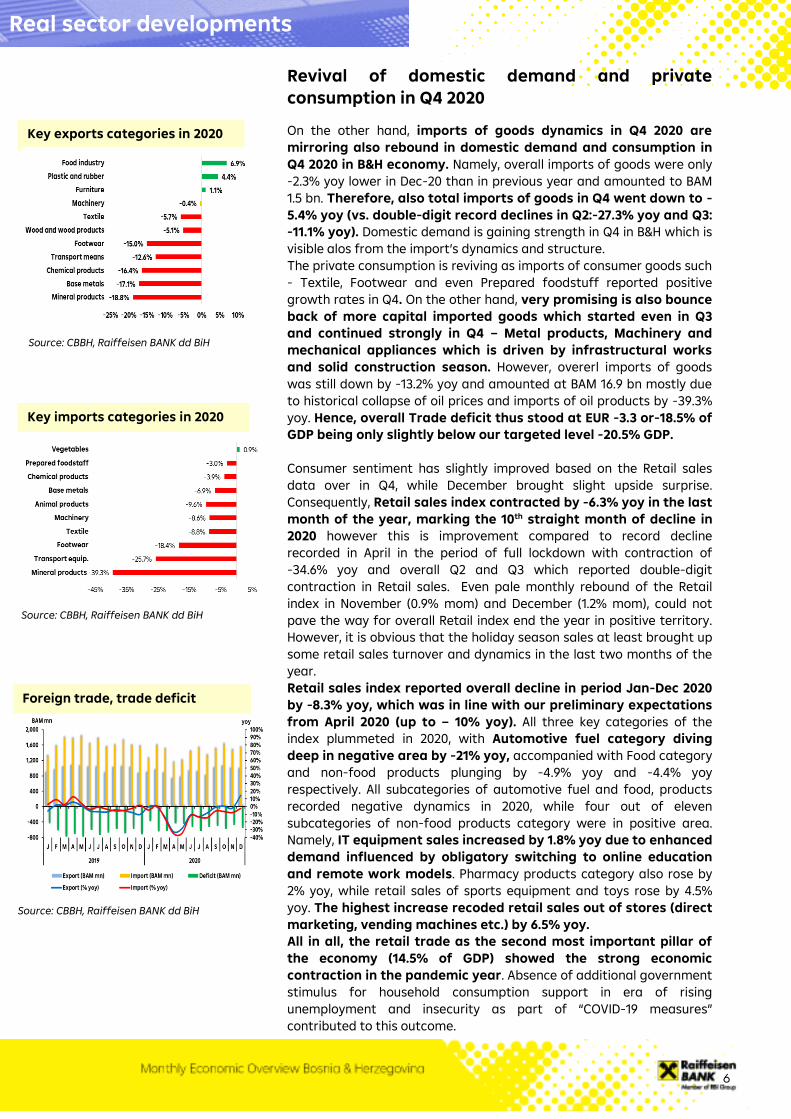

On the other hand, imports of goods dynamics in Q4 2020 are

mirroring also rebound in domestic demand and consumption in

Q4 2020 in B&H economy. Namely, overall imports of goods were only

-2.3% yoy lower in Dec-20 than in previous year and amounted to BAM

1.5 bn. Therefore, also total imports of goods in Q4 went down to -

5.4% yoy (vs. double-digit record declines in Q2:-27.3% yoy and Q3:

-11.1% yoy). Domestic demand is gaining strength in Q4 in B&H which is

visible alos from the import’s dynamics and structure.

The private consumption is reviving as imports of consumer goods such

- Textile, Footwear and even Prepared foodstuff reported positive

growth rates in Q4. On the other hand, very promising is also bounce

back of more capital imported goods which started even in Q3

and continued strongly in Q4 – Metal products, Machinery and

mechanical appliances which is driven by infrastructural works

and solid construction season. However, overerl imports of goods

was still down by -13.2% yoy and amounted at BAM 16.9 bn mostly due

to historical collapse of oil prices and imports of oil products by -39.3%

yoy. Hence, overall Trade deficit thus stood at EUR -3.3 or-18.5% of

GDP being only slightly below our targeted level -20.5% GDP.

Consumer sentiment has slightly improved based on the Retail sales

data over in Q4, while December brought slight upside surprise.

Consequently, Retail sales index contracted by -6.3% yoy in the last

month of the year, marking the 10th straight month of decline in

2020 however this is improvement compared to record decline

recorded in April in the period of full lockdown with contraction of

-34.6% yoy and overall Q2 and Q3 which reported double-digit

contraction in Retail sales. Even pale monthly rebound of the Retail

index in November (0.9% mom) and December (1.2% mom), could not

pave the way for overall Retail index end the year in positive territory.

However, it is obvious that the holiday season sales at least brought up

some retail sales turnover and dynamics in the last two months of the

year.

Retail sales index reported overall decline in period Jan-Dec 2020

by -8.3% yoy, which was in line with our preliminary expectations

from April 2020 (up to – 10% yoy). All three key categories of the

index plummeted in 2020, with Automotive fuel category diving

deep in negative area by -21% yoy, accompanied with Food category

and non-food products plunging by -4.9% yoy and -4.4% yoy

respectively. All subcategories of automotive fuel and food, products

recorded negative dynamics in 2020, while four out of eleven

subcategories of non-food products category were in positive area.

Namely, IT equipment sales increased by 1.8% yoy due to enhanced

demand influenced by obligatory switching to online education

and remote work models. Pharmacy products category also rose by

2% yoy, while retail sales of sports equipment and toys rose by 4.5%

yoy. The highest increase recoded retail sales out of stores (direct

marketing, vending machines etc.) by 6.5% yoy.

All in all, the retail trade as the second most important pillar of

the economy (14.5% of GDP) showed the strong economic

contraction in the pandemic year. Absence of additional government

stimulus for household consumption support in era of rising

unemployment and insecurity as part of “COVID-19 measures”

contributed to this outcome.

Foreign trade, trade deficit

Key imports categories in 2020

(% yoy)

Key exports categories in 2020

(% yoy)BAM)

Real sector developments

7

Source: Agency for Statistics of B&H,

Raiffeisen BANK dd BiH

Source: Agency for Statistics of B&H,

Raiffeisen BANK dd BiH

Source: Agency for Statistics of B&H,

Raiffeisen BANK dd BiH

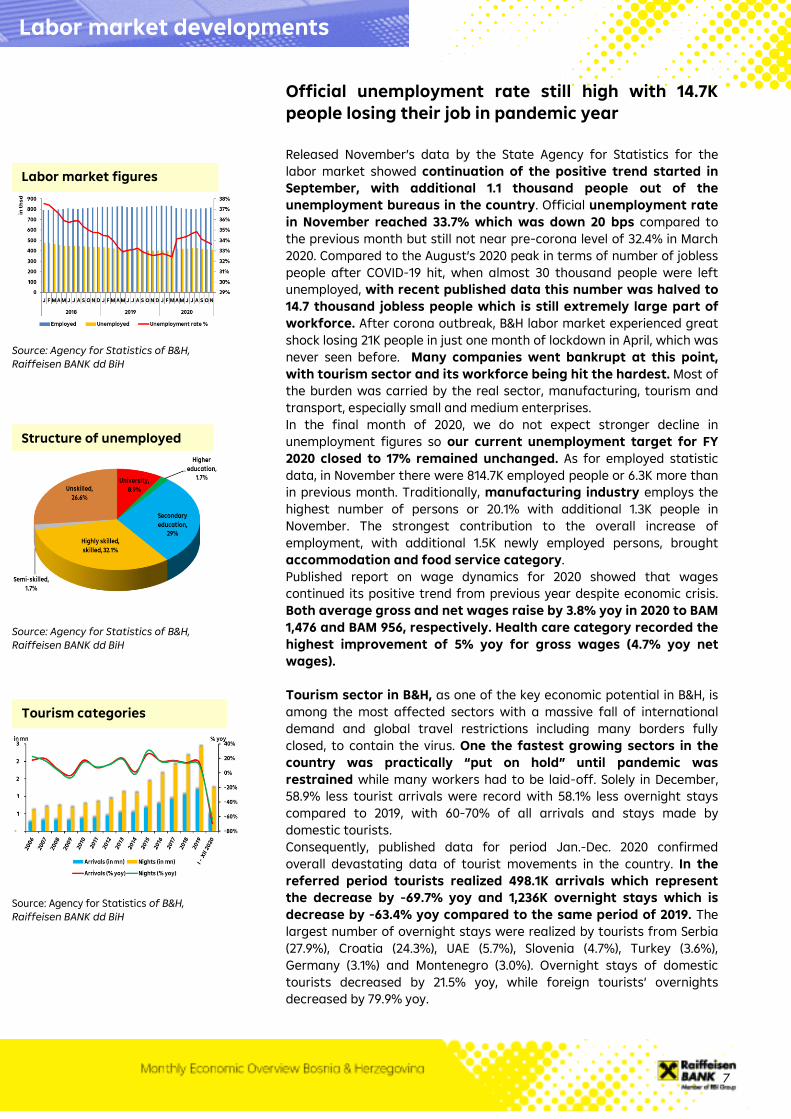

Official unemployment rate still high with 14.7K

people losing their job in pandemic year

Released November’s data by the State Agency for Statistics for the

labor market showed continuation of the positive trend started in

September, with additional 1.1 thousand people out of the

unemployment bureaus in the country. Official unemployment rate

in November reached 33.7% which was down 20 bps compared to

the previous month but still not near pre-corona level of 32.4% in March

2020. Compared to the August’s 2020 peak in terms of number of jobless

people after COVID-19 hit, when almost 30 thousand people were left

unemployed, with recent published data this number was halved to

14.7 thousand jobless people which is still extremely large part of

workforce. After corona outbreak, B&H labor market experienced great

shock losing 21K people in just one month of lockdown in April, which was

never seen before. Many companies went bankrupt at this point,

with tourism sector and its workforce being hit the hardest. Most of

the burden was carried by the real sector, manufacturing, tourism and

transport, especially small and medium enterprises.

In the final month of 2020, we do not expect stronger decline in

unemployment figures so our current unemployment target for FY

2020 closed to 17% remained unchanged. As for employed statistic

data, in November there were 814.7K employed people or 6.3K more than

in previous month. Traditionally, manufacturing industry employs the

highest number of persons or 20.1% with additional 1.3K people in

November. The strongest contribution to the overall increase of

employment, with additional 1.5K newly employed persons, brought

accommodation and food service category.

Published report on wage dynamics for 2020 showed that wages

continued its positive trend from previous year despite economic crisis.

Both average gross and net wages raise by 3.8% yoy in 2020 to BAM

1,476 and BAM 956, respectively. Health care category recorded the

highest improvement of 5% yoy for gross wages (4.7% yoy net

wages).

Tourism sector in B&H, as one of the key economic potential in B&H, is

among the most affected sectors with a massive fall of international

demand and global travel restrictions including many borders fully

closed, to contain the virus. One the fastest growing sectors in the

country was practically “put on hold” until pandemic was

restrained while many workers had to be laid-off. Solely in December,

58.9% less tourist arrivals were record with 58.1% less overnight stays

compared to 2019, with 60-70% of all arrivals and stays made by

domestic tourists.

Consequently, published data for period Jan.-Dec. 2020 confirmed

overall devastating data of tourist movements in the country. In the

referred period tourists realized 498.1K arrivals which represent

the decrease by -69.7% yoy and 1,236K overnight stays which is

decrease by -63.4% yoy compared to the same period of 2019. The

largest number of overnight stays were realized by tourists from Serbia

(27.9%), Croatia (24.3%), UAE (5.7%), Slovenia (4.7%), Turkey (3.6%),

Germany (3.1%) and Montenegro (3.0%). Overnight stays of domestic

tourists decreased by 21.5% yoy, while foreign tourists’ overnights

decreased by 79.9% yoy.

Tourism categories

Structure of unemployed

Labor market figures

Labor market developments

8

Source: Agency for Statistics of B&H,

Raiffeisen BANK dd BiH

Source: Agency for Statistics of B&H,

Raiffeisen BANK dd BiH

Source: Agency for Statistics of B&H,

Raiffeisen BANK dd BiH

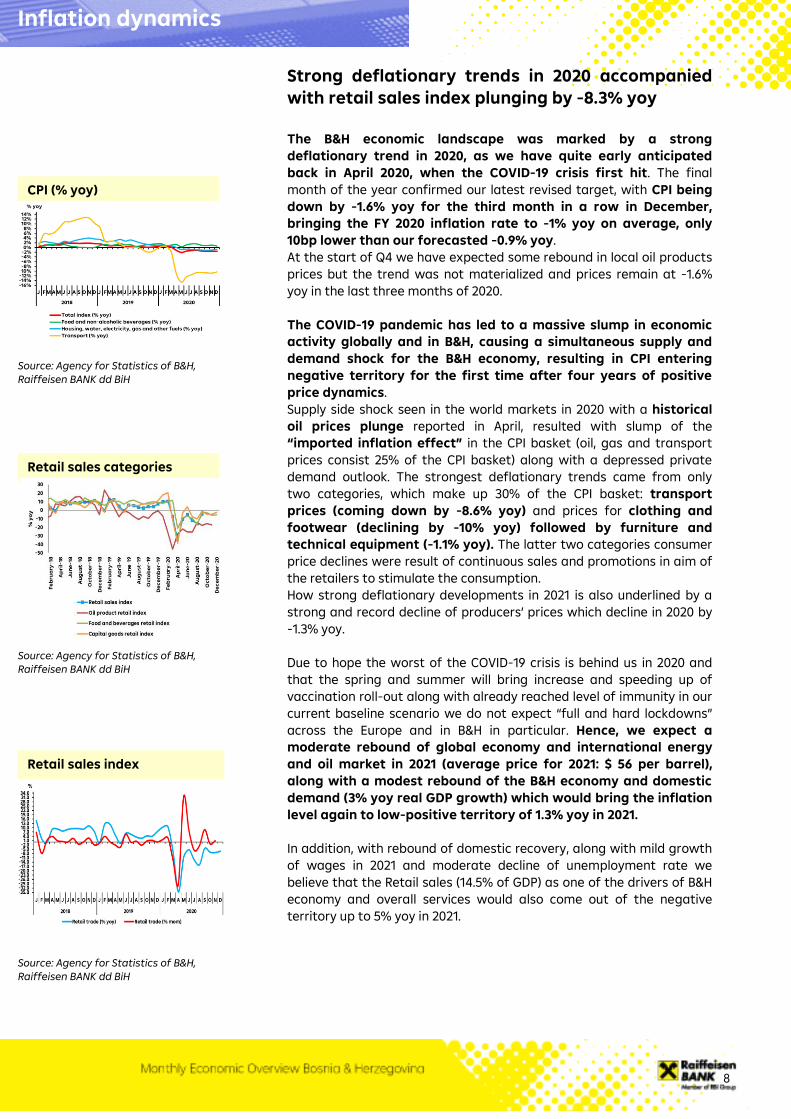

Strong deflationary trends in 2020 accompanied

with retail sales index plunging by -8.3% yoy

The B&H economic landscape was marked by a strong

deflationary trend in 2020, as we have quite early anticipated

back in April 2020, when the COVID-19 crisis first hit. The final

month of the year confirmed our latest revised target, with CPI being

down by -1.6% yoy for the third month in a row in December,

bringing the FY 2020 inflation rate to -1% yoy on average, only

10bp lower than our forecasted -0.9% yoy.

At the start of Q4 we have expected some rebound in local oil products

prices but the trend was not materialized and prices remain at -1.6%

yoy in the last three months of 2020.

The COVID-19 pandemic has led to a massive slump in economic

activity globally and in B&H, causing a simultaneous supply and

demand shock for the B&H economy, resulting in CPI entering

negative territory for the first time after four years of positive

price dynamics.

Supply side shock seen in the world markets in 2020 with a historical

oil prices plunge reported in April, resulted with slump of the

“imported inflation effect” in the CPI basket (oil, gas and transport

prices consist 25% of the CPI basket) along with a depressed private

demand outlook. The strongest deflationary trends came from only

two categories, which make up 30% of the CPI basket: transport

prices (coming down by -8.6% yoy) and prices for clothing and

footwear (declining by -10% yoy) followed by furniture and

technical equipment (-1.1% yoy). The latter two categories consumer

price declines were result of continuous sales and promotions in aim of

the retailers to stimulate the consumption.

How strong deflationary developments in 2021 is also underlined by a

strong and record decline of producers’ prices which decline in 2020 by

-1.3% yoy.

Due to hope the worst of the COVID-19 crisis is behind us in 2020 and

that the spring and summer will bring increase and speeding up of

vaccination roll-out along with already reached level of immunity in our

current baseline scenario we do not expect “full and hard lockdowns”

across the Europe and in B&H in particular. Hence, we expect a

moderate rebound of global economy and international energy

and oil market in 2021 (average price for 2021: $ 56 per barrel),

along with a modest rebound of the B&H economy and domestic

demand (3% yoy real GDP growth) which would bring the inflation

level again to low-positive territory of 1.3% yoy in 2021.

In addition, with rebound of domestic recovery, along with mild growth

of wages in 2021 and moderate decline of unemployment rate we

believe that the Retail sales (14.5% of GDP) as one of the drivers of B&H

economy and overall services would also come out of the negative

territory up to 5% yoy in 2021.

Retail sales index

Retail sales categories

CPI (% yoy)

Inflation dynamics

9

Source: Central Bank of B&H,

Raiffeisen BANK dd BiH

Source: Central Bank of B&H,

Raiffeisen BANK dd BiH

Source: Central Bank of B&H,

Raiffeisen BANK dd BiH

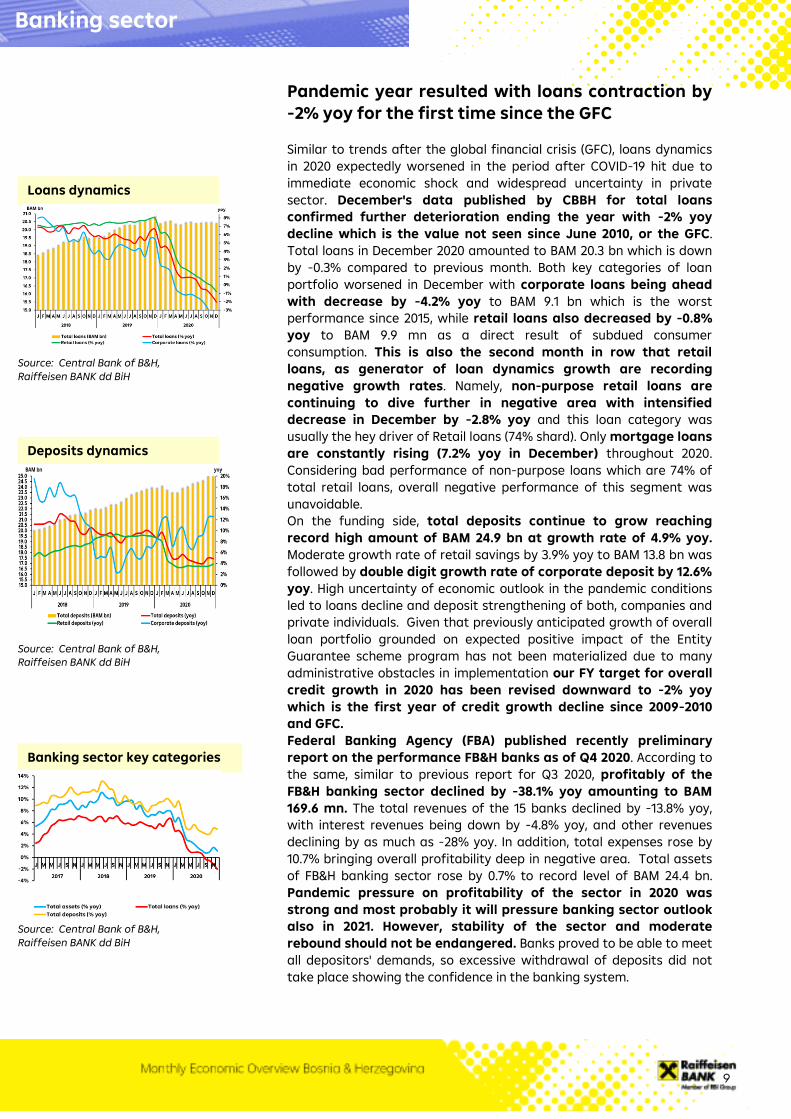

Pandemic year resulted with loans contraction by

-2% yoy for the first time since the GFC

Similar to trends after the global financial crisis (GFC), loans dynamics

in 2020 expectedly worsened in the period after COVID-19 hit due to

immediate economic shock and widespread uncertainty in private

sector. December's data published by CBBH for total loans

confirmed further deterioration ending the year with -2% yoy

decline which is the value not seen since June 2010, or the GFC.

Total loans in December 2020 amounted to BAM 20.3 bn which is down

by -0.3% compared to previous month. Both key categories of loan

portfolio worsened in December with corporate loans being ahead

with decrease by -4.2% yoy to BAM 9.1 bn which is the worst

performance since 2015, while retail loans also decreased by -0.8%

yoy to BAM 9.9 mn as a direct result of subdued consumer

consumption. This is also the second month in row that retail

loans, as generator of loan dynamics growth are recording

negative growth rates. Namely, non-purpose retail loans are

continuing to dive further in negative area with intensified

decrease in December by -2.8% yoy and this loan category was

usually the hey driver of Retail loans (74% shard). Only mortgage loans

are constantly rising (7.2% yoy in December) throughout 2020.

Considering bad performance of non-purpose loans which are 74% of

total retail loans, overall negative performance of this segment was

unavoidable.

On the funding side, total deposits continue to grow reaching

record high amount of BAM 24.9 bn at growth rate of 4.9% yoy.

Moderate growth rate of retail savings by 3.9% yoy to BAM 13.8 bn was

followed by double digit growth rate of corporate deposit by 12.6%

yoy. High uncertainty of economic outlook in the pandemic conditions

led to loans decline and deposit strengthening of both, companies and

private individuals. Given that previously anticipated growth of overall

loan portfolio grounded on expected positive impact of the Entity

Guarantee scheme program has not been materialized due to many

administrative obstacles in implementation our FY target for overall

credit growth in 2020 has been revised downward to -2% yoy

which is the first year of credit growth decline since 2009-2010

and GFC.

Federal Banking Agency (FBA) published recently preliminary

report on the performance FB&H banks as of Q4 2020. According to

the same, similar to previous report for Q3 2020, profitably of the

FB&H banking sector declined by -38.1% yoy amounting to BAM

169.6 mn. The total revenues of the 15 banks declined by -13.8% yoy,

with interest revenues being down by -4.8% yoy, and other revenues

declining by as much as -28% yoy. In addition, total expenses rose by

10.7% bringing overall profitability deep in negative area. Total assets

of FB&H banking sector rose by 0.7% to record level of BAM 24.4 bn.

Pandemic pressure on profitability of the sector in 2020 was

strong and most probably it will pressure banking sector outlook

also in 2021. However, stability of the sector and moderate

rebound should not be endangered. Banks proved to be able to meet

all depositors' demands, so excessive withdrawal of deposits did not

take place showing the confidence in the banking system.

Banking sector key categories

Deposits dynamics

Loans dynamics

Banking sector

10

Source: RBI/Raiffeisen RESEARCH

Raiffeisen BANK dd BiH

Source: RBI/Raiffeisen RESEARCH

Raiffeisen BANK dd BiH

Source: RBI/Raiffeisen RESEARCH

Raiffeisen BANK dd BiH

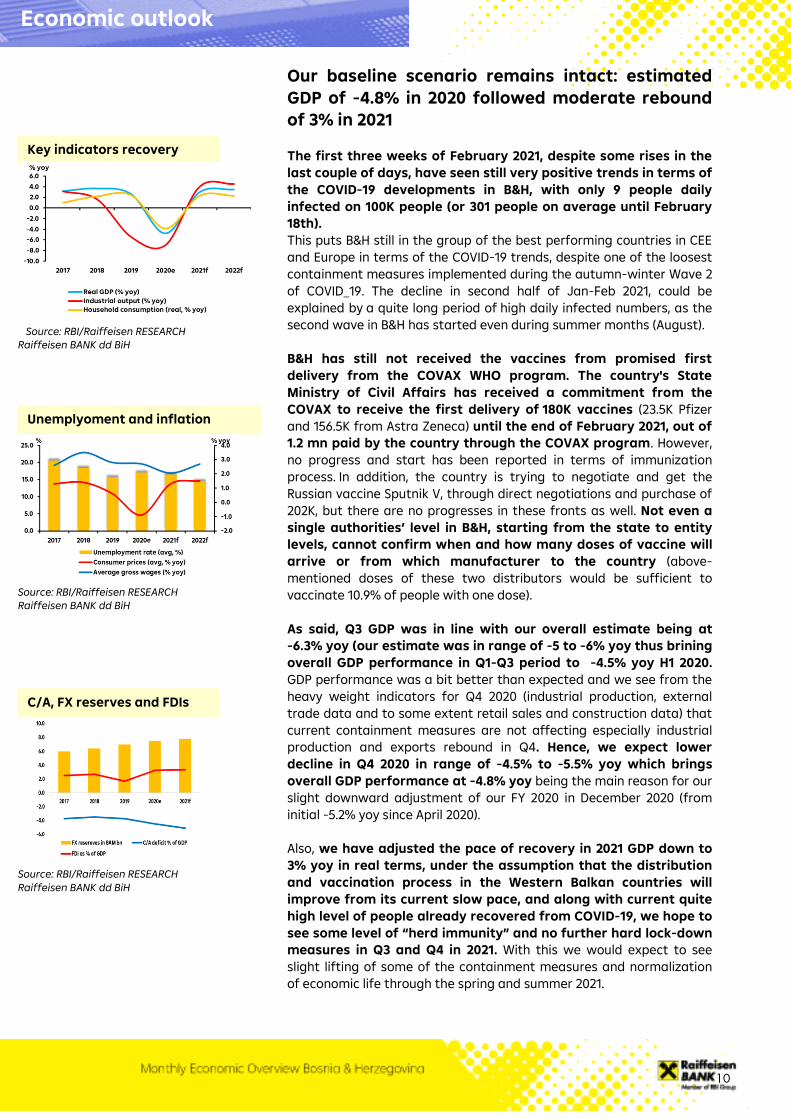

Our baseline scenario remains intact: estimated

GDP of -4.8% in 2020 followed moderate rebound

of 3% in 2021

The first three weeks of February 2021, despite some rises in the

last couple of days, have seen still very positive trends in terms of

the COVID-19 developments in B&H, with only 9 people daily

infected on 100K people (or 301 people on average until February

18th).

This puts B&H still in the group of the best performing countries in CEE

and Europe in terms of the COVID-19 trends, despite one of the loosest

containment measures implemented during the autumn-winter Wave 2

of COVID_19. The decline in second half of Jan-Feb 2021, could be

explained by a quite long period of high daily infected numbers, as the

second wave in B&H has started even during summer months (August).

B&H has still not received the vaccines from promised first

delivery from the COVAX WHO program. The country's State

Ministry of Civil Affairs has received a commitment from the

COVAX to receive the first delivery of 180K vaccines (23.5K Pfizer

and 156.5K from Astra Zeneca) until the end of February 2021, out of

1.2 mn paid by the country through the COVAX program. However,

no progress and start has been reported in terms of immunization

process. In addition, the country is trying to negotiate and get the

Russian vaccine Sputnik V, through direct negotiations and purchase of

202K, but there are no progresses in these fronts as well. Not even a

single authorities’ level in B&H, starting from the state to entity

levels, cannot confirm when and how many doses of vaccine will

arrive or from which manufacturer to the country (above-

mentioned doses of these two distributors would be sufficient to

vaccinate 10.9% of people with one dose).

As said, Q3 GDP was in line with our overall estimate being at

-6.3% yoy (our estimate was in range of -5 to -6% yoy thus brining

overall GDP performance in Q1-Q3 period to -4.5% yoy H1 2020.

GDP performance was a bit better than expected and we see from the

heavy weight indicators for Q4 2020 (industrial production, external

trade data and to some extent retail sales and construction data) that

current containment measures are not affecting especially industrial

production and exports rebound in Q4. Hence, we expect lower

decline in Q4 2020 in range of -4.5% to -5.5% yoy which brings

overall GDP performance at -4.8% yoy being the main reason for our

slight downward adjustment of our FY 2020 in December 2020 (from

initial -5.2% yoy since April 2020).

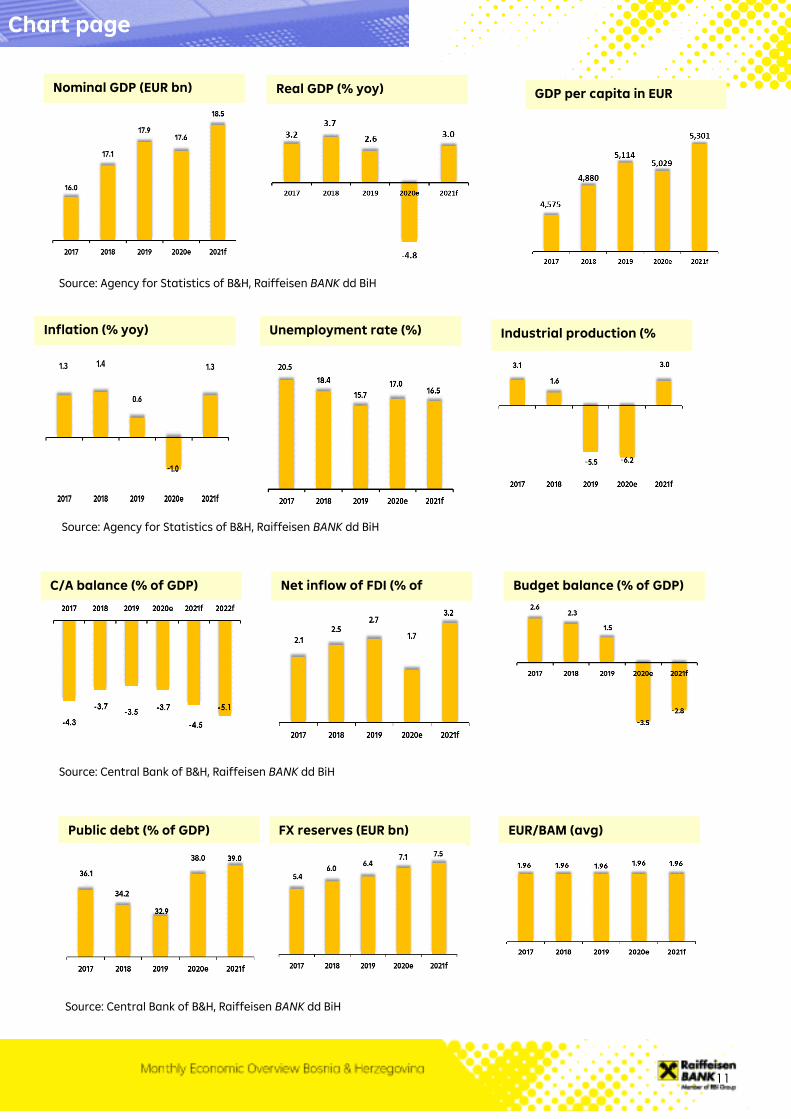

Also, we have adjusted the pace of recovery in 2021 GDP down to

3% yoy in real terms, under the assumption that the distribution

and vaccination process in the Western Balkan countries will

improve from its current slow pace, and along with current quite

high level of people already recovered from COVID-19, we hope to

see some level of “herd immunity” and no further hard lock-down

measures in Q3 and Q4 in 2021. With this we would expect to see

slight lifting of some of the containment measures and normalization

of economic life through the spring and summer 2021.

C/A, FX reserves and FDIs

Unemplyoment and inflation

Key indicators recovery

Economic outlook

11

EUR/BAM (avg) FX reserves (EUR bn)

C/A balance (% of GDP) Budget balance (% of GDP) Net inflow of FDI (% of

GDP)

Industrial production (%

yoy)

Unemployment rate (%) Inflation (% yoy)

Source: Agency for Statistics of B&H, Raiffeisen BANK dd BiH

Source: Agency for Statistics of B&H, Raiffeisen BANK dd BiH

Source: Central Bank of B&H, Raiffeisen BANK dd BiH

Source: Central Bank of B&H, Raiffeisen BANK dd BiH

Public debt (% of GDP)

Nominal GDP (EUR bn)

Chart page

Real GDP (% yoy) GDP per capita in EUR

12

Raiffeisen BANK d.d. Bosna i Hercegovina

Investment Banking

Sanja Korene, Head of Investment Banking; Phone: + 387 33 28 71 22, e-mail:

Ivona Zametica, Chief Economist/Head of Research and Advisory; Phone: + 387 33 28 77 84, e-

mail: [email protected]

Asja Grđo, Senior Capital Market Specialist; Phone: +387 33 287 762; e-mail:

Nadira Čenanović, Head of Brokerage Business; Phone: +387 33 28 76 47, e-mail:

Raiffeisen CAPITAL a.d. Banja Luka

Vedrana Đukić, Director; Phone: + 387 51 23 14 90, e-mail:

Editor: Ivona Zametica, Chief Economist

Publisher:

Raiffeisen BANK d.d. Bosna i Hercegovina

Zmaja od Bosne bb, 71000 Sarajevo

www.raiffeisenbank.ba

Raiffeisen direct info: +387 33 75 50 10 • Fax: +387 33 21 38 51

The cut-off date for the data used in the publication February 19th, 2021

This publication was completed on February 24th, 2021

The publication was published on February 24th, 2021.

Impressum

13

Disclaimer Financial Analysis

Publisher: Raiffeisen BANK dd Bosna i Hercegovina (abbreviated as “RBBH”)

RBBH is a credit institution with the registered office Zmaja od Bosne bb, 71000 Sarajevo Bosnia and Herzegovina

Raiffeisen RESEARCH is an organisational unit of Raiffeisen Bank dd Bosna i Hercegovina

Supervisory authority: The Banking Agency of the FBiH, Zmaja od Bosne 47, 71000 Sarajevo, Bosnia and Herzegovina and The

Central Bank of Bosnia and Herzegovina, 25 Maršala Tita Street, 71 000, Sarajevo, Bosnia and Herzegovina. Unless set out herein

explicitly otherwise, references to legal norms refer to norms enacted by the Bosnia and Herzegovina.

This document is for information purposes and may not be reproduced or distributed to other persons without RBBH’s

permission. This document constitutes neither a solicitation of an offer nor a prospectus in the sense of the Law on Capital

Market or the Stock Exchange rules or any other comparable foreign law. An investment decision in respect of a security,

financial product or investment must be made on the basis of an approved, published prospectus or the complete

documentation for the security, financial product or investment in question, and not on the basis of this document.

This document does not constitute a personal recommendation to buy or sell financial instruments in the sense Law on Capital

Markets. Neither this document nor any of its components shall form the basis for any kind of contract or commitment

whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a security, investment or

other financial product. In respect of the sale or purchase of securities, investments or financial products, your banking advisor

can provide individualised advice which is suitable for investments and financial products.

This analysis is fundamentally based on generally available information and not on confidential information which the party

preparing the analysis has obtained exclusively on the basis of his/her client relationship with a person.

Unless otherwise expressly stated in this publication, RBBH deems all of the information to be reliable, but does not make any

assurances regarding its accuracy and completeness.

In emerging markets, there may be higher settlement and custody risk as compared to markets with established

infrastructure. The liquidity of stocks/financial instruments can be influenced by the number of market makers. Both of these

circumstances can result in elevated risk in relation to the safety of investments made on the basis of the information

contained in this document.

The information in this publication is current, up to the creation date of the document. It may be outdated by future

developments, without the publication being changed.

The analysts employed by Raiffeisen BANK dd Bosna i Hercegovina are not compensated for specific investment banking

transactions. Compensation of the author or authors of this report is based (amongst other things) on the overall profitability

of RBBH, which includes, inter alia, earnings from investment banking and other transactions of RBBH. In general, RBBH forbids

its analysts and persons reporting to the analysts from acquiring securities or other financial instruments of any enterprise

which is covered by the analysts, unless such acquisition is authorised in advance by RBBH’s Compliance Department.

RBBH has put in place the following organisational and administrative agreements, including information barriers, to impede

or prevent conflicts of interest in relation to recommendations: RBBH has designated fundamentally binding confidentiality

zones. Confidentiality zones are typically units within credit institutions, which are isolated from other units by organisational

measures governing the exchange of information, because compliance-relevant information is continuously or temporarily

handled in these zones. Compliance-relevant information may fundamentally not leave a confidentiality zone and is to be

treated as strictly confidential in internal business operations, including interaction with other units. This does not apply to the

transfer of information necessary for usual business operations. Such transfer of information is limited, however, to what is

absolutely necessary (need-to-know principle). The exchange of compliance-relevant information between two confidentiality

zones may only occur with the involvement of the Compliance Officer.

If any term of this Disclaimer is found to be illegal, invalid or unenforceable under any applicable law, such term shall, insofar

as it is severable from the remaining terms, be deemed omitted from this Disclaimer; it shall in no way affect the legality,

validity or enforceability of the remaining terms.

Disclaimer