Embed Size (px)

Citation preview

Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Copyright © 2011 Standard & Poor’s Financial Services LLC, a subsidiary of The McGraw-Hill Companies, Inc. All rights reserved.

Next Generation:

Public Private Partnerships

October 2, 2012

CACUBO Presentation

2.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Presenters

• Illinois State University

– Dan Layzell, Vice President for Finance and Planning

• RBC Capital Markets

– Sara Russell, Vice President

• Standard and Poor’s

– Jessica Lukas, Associate Director, Higher Education Group

3.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Illinois State University

Dan Layzell

Vice President for Finance and Planning

4.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

University Overview

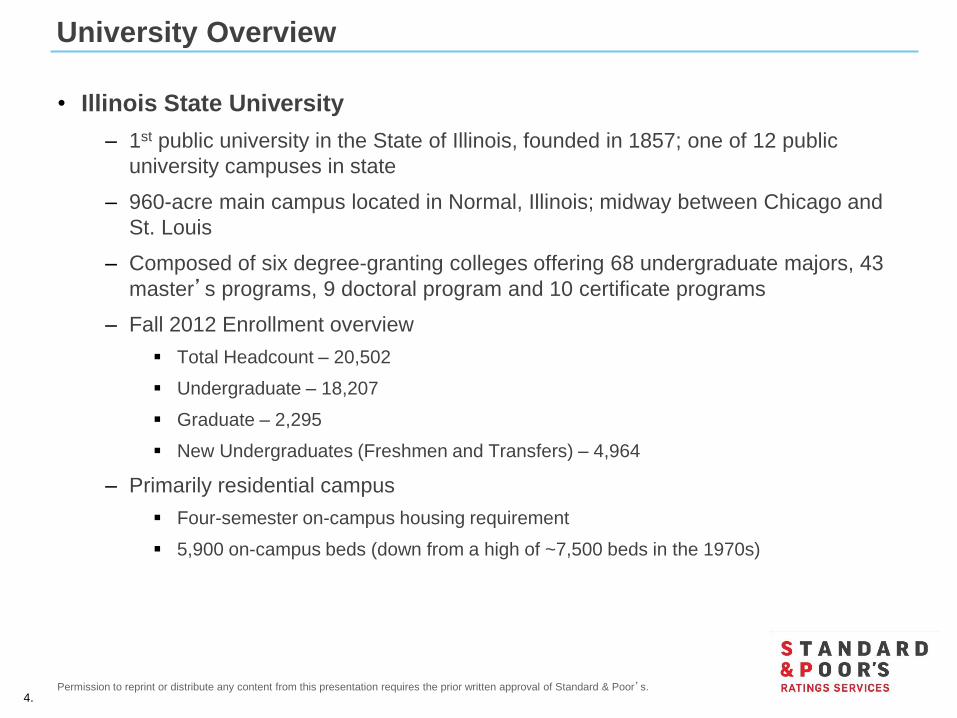

• Illinois State University

– 1st public university in the State of Illinois, founded in 1857; one of 12 public

university campuses in state

– 960-acre main campus located in Normal, Illinois; midway between Chicago and

St. Louis

– Composed of six degree-granting colleges offering 68 undergraduate majors, 43

master’s programs, 9 doctoral program and 10 certificate programs

– Fall 2012 Enrollment overview

Total Headcount – 20,502

Undergraduate – 18,207

Graduate – 2,295

New Undergraduates (Freshmen and Transfers) – 4,964

– Primarily residential campus

Four-semester on-campus housing requirement

5,900 on-campus beds (down from a high of ~7,500 beds in the 1970s)

5.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

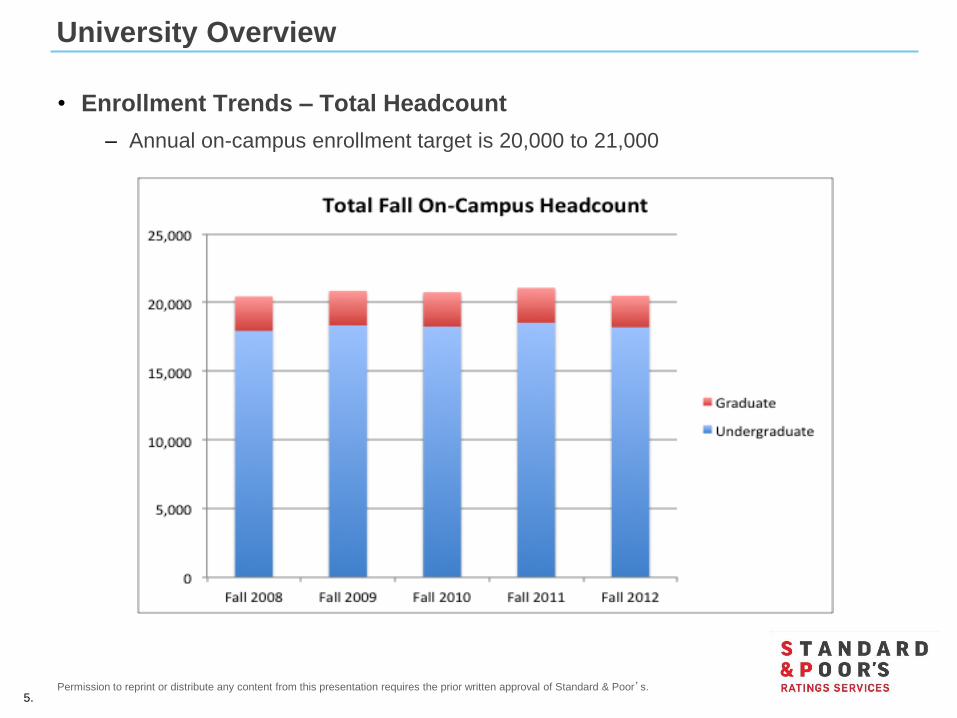

University Overview

• Enrollment Trends – Total Headcount

– Annual on-campus enrollment target is 20,000 to 21,000

6.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

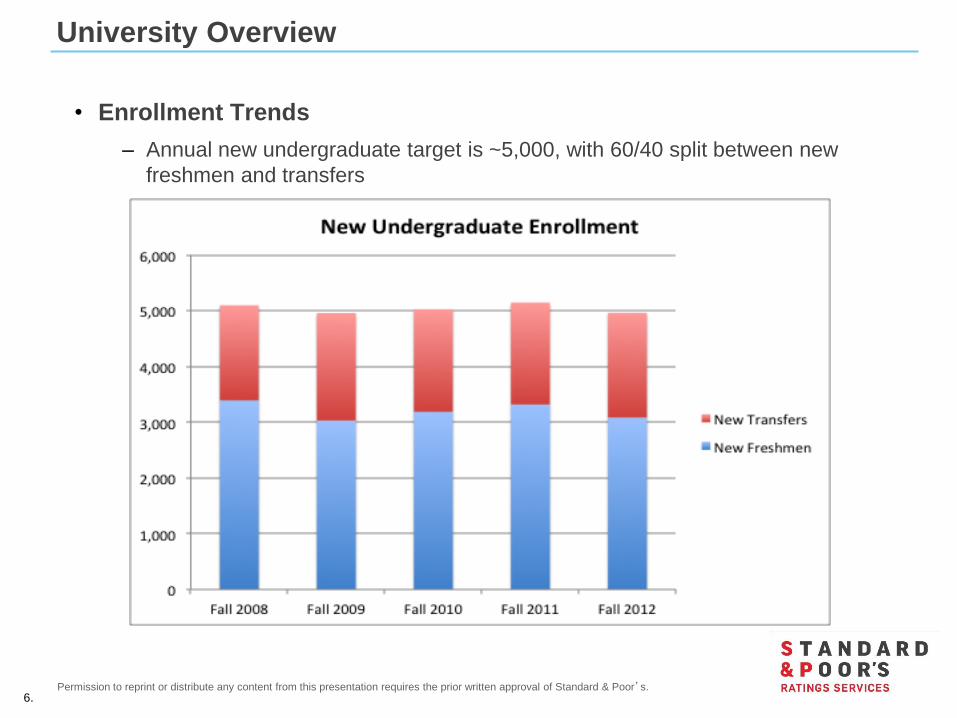

University Overview

• Enrollment Trends

– Annual new undergraduate target is ~5,000, with 60/40 split between new

freshmen and transfers

7.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

University Overview

Long Range Housing and Dining Plan

• Initiated in 2004

– Upgrade University housing and dining facilities

– Strategically right size campus housing and dining capacity to

accommodate future enrollment targets

– Planned decommissioning of selected facilities

– Rotated 400-800 beds offline each year

– Project completed in 2012

• Financing

– Total cost – $96M

– Equity financed with cash reserves - $48M

– Debt financed - $48M

8.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

University Overview

• Occupancy rates & capacity

– On-campus beds were reduced from 6,600 in 2009-10 to 5,900 in Fall 2012

(including 900 in new Cardinal Court complex)

Note: Includes ~ 300 supplemental lounge spaces each year. Cardinal Court Fall 2012 occupancy – 99.3%.

9.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

The On-Campus Housing Challenge and Decision Process

• On-Campus Housing Status

– Long-range Housing and Dining Plan completed in 2012

– Four-semester on-campus housing requirement

– State law requiring sprinklers in all residence halls effective January 2013

– Decision NOT to renovate South Campus Complex (~1,600 beds)

• Considerations

– Cost and other University debt-issuance needs

– No apartment-style housing on campus for undergraduates

– Land availability and options

– Time constraints

• Options

– Eliminate four-semester on-campus housing requirement

– Re-densify existing residence halls

– Build new residence hall

– Explore public-private partnership (P3) to address housing needs

10.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

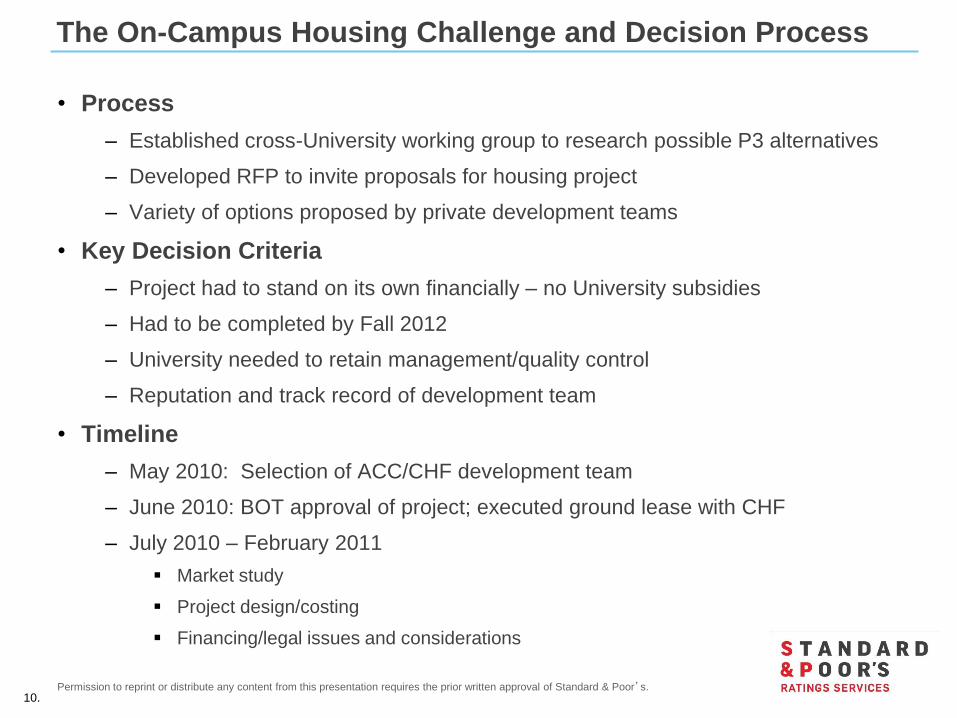

The On-Campus Housing Challenge and Decision Process

• Process

– Established cross-University working group to research possible P3 alternatives

– Developed RFP to invite proposals for housing project

– Variety of options proposed by private development teams

• Key Decision Criteria

– Project had to stand on its own financially – no University subsidies

– Had to be completed by Fall 2012

– University needed to retain management/quality control

– Reputation and track record of development team

• Timeline

– May 2010: Selection of ACC/CHF development team

– June 2010: BOT approval of project; executed ground lease with CHF

– July 2010 – February 2011

Market study

Project design/costing

Financing/legal issues and considerations

11.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

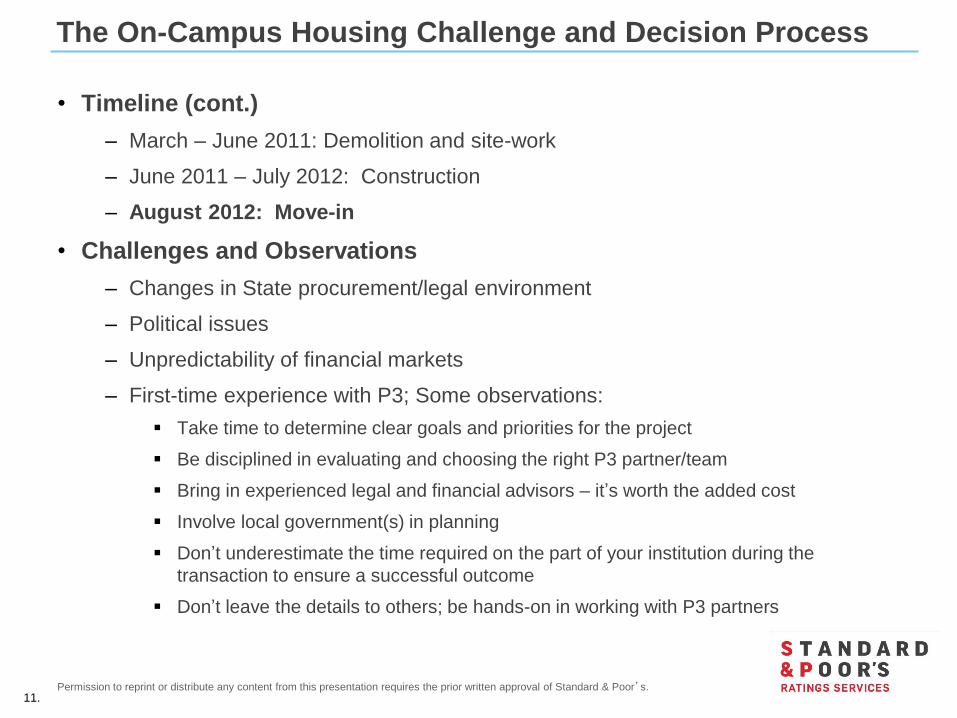

The On-Campus Housing Challenge and Decision Process

• Timeline (cont.)

– March – June 2011: Demolition and site-work

– June 2011 – July 2012: Construction

– August 2012: Move-in

• Challenges and Observations

– Changes in State procurement/legal environment

– Political issues

– Unpredictability of financial markets

– First-time experience with P3; Some observations:

Take time to determine clear goals and priorities for the project

Be disciplined in evaluating and choosing the right P3 partner/team

Bring in experienced legal and financial advisors – it’s worth the added cost

Involve local government(s) in planning

Don’t underestimate the time required on the part of your institution during the

transaction to ensure a successful outcome

Don’t leave the details to others; be hands-on in working with P3 partners

12.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

RBC Capital Markets

Sara Russell, Vice President

13.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Project Location

The Project is situated on the previous Cardinal Court Apartment site located on the main campus of the

University, an approximately 10 - 15 minute walk from the academic quad.

Project Site

Wilkins Hall

Wright Hall

Watterson Towers

Whitten Hall Hamilton Hall

Atkins HallColby Hall

Haynie Hall

Manchester Hall

Hewett Hall

Quad

Student Rec Center

Bone Student Center

Project Site

Wilkins Hall

Wright Hall

Watterson Towers

Whitten Hall Hamilton Hall

Atkins HallColby Hall

Haynie Hall

Manchester Hall

Hewett Hall

Quad

Student Rec Center

Bone Student Center

Existing residence halls are labeled in blue.

14.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Project Description & Amenities

• The project provides replacement housing and enables ISU to

“right-size” campus housing options.

• The community provides both private and semi-private bedroom and

bathroom accommodations for students.

• A 15,000 square foot community center provides for student

recreation, food service, residence life programming and outdoor

amenities.

• Resident amenities also include on-site parking, bicycle racks and a

campus shuttle bus stop.

1,053

989

989

924

1,223

720

Sq FtPer Unit

$605

$575

$605

$575

$641

$806

2012-13 Monthly

Rent

$3,6309648

Unit D | 3 Bedroom / 2 Bath (Single Occupancy)

2012-13 Semester

Rent# of Beds

# of UnitsUnit Type

896228Total

$3,63038496Unit E | 4 Bedroom / 2 Bath (Single Occupancy)

$3,450963 Bedroom / 2 Bath (Double Occupancy)

$3,4504812Unit C | 2 Bedroom / 2 Bath (Double Occupancy)

$3,84625664Unit B | 4 Bedroom / 4 Bath (Single Occupancy)

$4,836168Unit A | 2 Bedroom / 2 Bath (Single Occupancy)

1,053

989

989

924

1,223

720

Sq FtPer Unit

$605

$575

$605

$575

$641

$806

2012-13 Monthly

Rent

$3,6309648

Unit D | 3 Bedroom / 2 Bath (Single Occupancy)

2012-13 Semester

Rent# of Beds

# of UnitsUnit Type

896228Total

$3,63038496Unit E | 4 Bedroom / 2 Bath (Single Occupancy)

$3,450963 Bedroom / 2 Bath (Double Occupancy)

$3,4504812Unit C | 2 Bedroom / 2 Bath (Double Occupancy)

$3,84625664Unit B | 4 Bedroom / 4 Bath (Single Occupancy)

$4,836168Unit A | 2 Bedroom / 2 Bath (Single Occupancy)

15.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

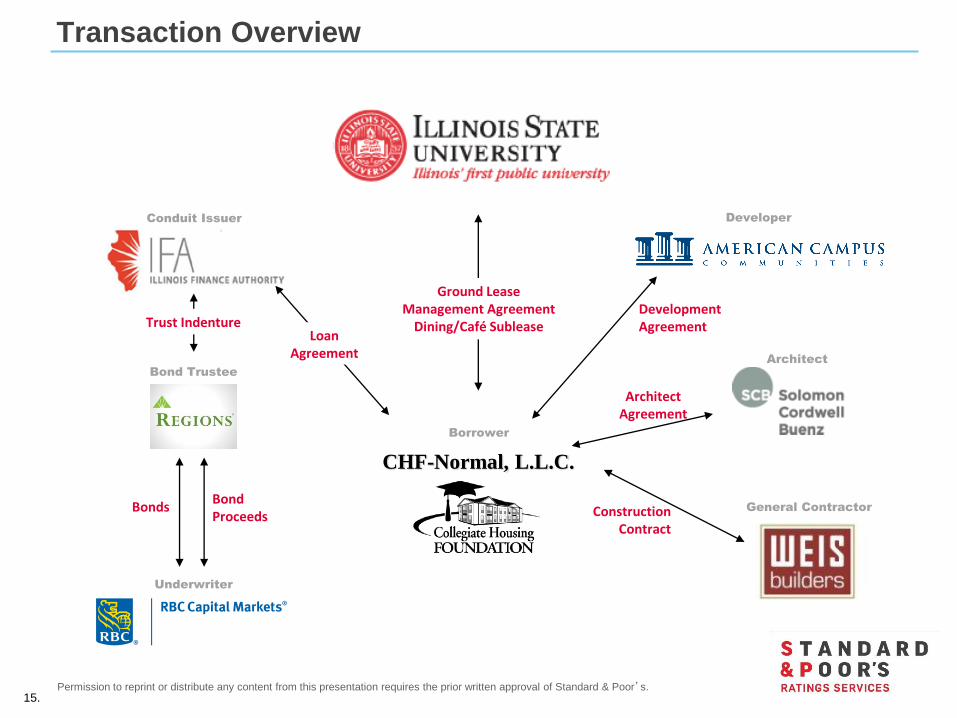

Transaction Overview

BondsBondProceeds

DevelopmentAgreement

ArchitectAgreement

Construction Contract

Conduit Issuer

Bond Trustee

Underwriter

Developer

Architect

General Contractor

Trust Indenture

Ground Lease Management Agreement

Dining/Café Sublease

Borrower

CHF-Normal, L.L.C.

Loan Agreement

16.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Structural Finance Considerations – Market Study

• August 2010 - CHF engaged CDS Market Research to conduct an independent

market feasibility study to evaluate the overall need for additional housing at ISU

– Survey and analysis - evaluation of existing housing facilities both on and off campus, the

demand for additional housing, and the type of units and pricing that would best fulfill

students needs

• The market contains approximately 8,000 rental units in approximately 1,000 buildings

– The complexes most immediately adjacent to campus are approximately 97% - 100%

occupied, though renters pay a premium price for the proximity to campus as compared to

some of the larger garden style units available further away.

• After project completion and the decommissioning of existing housing units, ISU’s total

housing stock will be approximately 6,000 beds (approximately 5,000 residence hall

beds and 1,000 apartment beds)

17.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

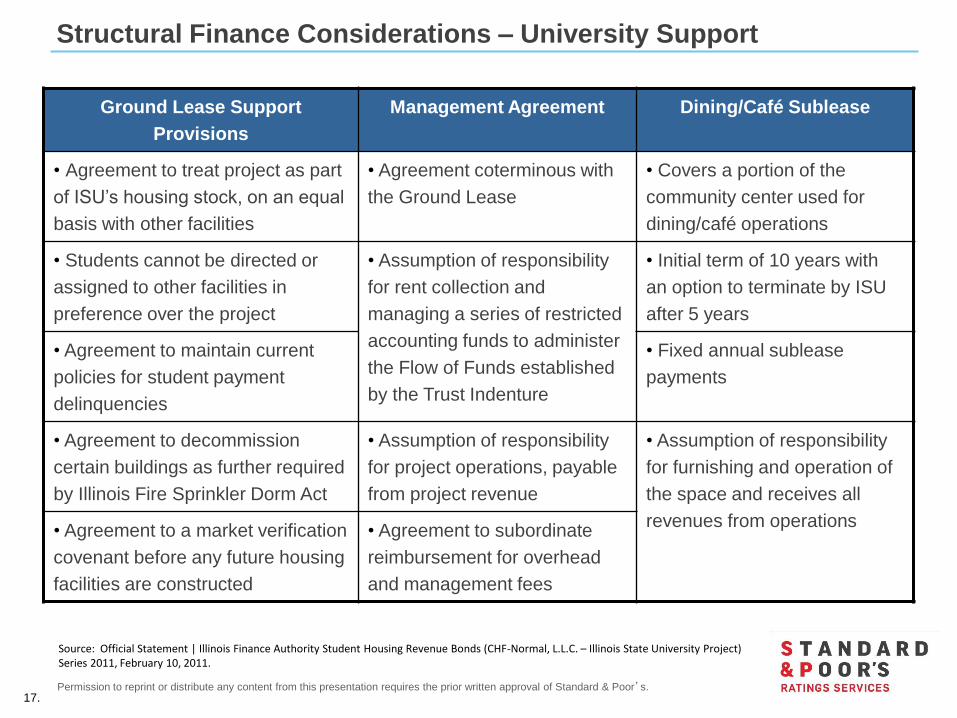

Structural Finance Considerations – University Support

Ground Lease Support

Provisions

Management Agreement Dining/Café Sublease

• Agreement to treat project as part

of ISU’s housing stock, on an equal

basis with other facilities

• Agreement coterminous with

the Ground Lease

• Covers a portion of the

community center used for

dining/café operations

• Students cannot be directed or

assigned to other facilities in

preference over the project

• Assumption of responsibility

for rent collection and

managing a series of restricted

accounting funds to administer

the Flow of Funds established

by the Trust Indenture

• Initial term of 10 years with

an option to terminate by ISU

after 5 years

• Agreement to maintain current

policies for student payment

delinquencies

• Fixed annual sublease

payments

• Agreement to decommission

certain buildings as further required

by Illinois Fire Sprinkler Dorm Act

• Assumption of responsibility

for project operations, payable

from project revenue

• Assumption of responsibility

for furnishing and operation of

the space and receives all

revenues from operations• Agreement to a market verification

covenant before any future housing

facilities are constructed

• Agreement to subordinate

reimbursement for overhead

and management fees

Source: Official Statement | Illinois Finance Authority Student Housing Revenue Bonds (CHF-Normal, L.L.C. – Illinois State University Project) Series 2011, February 10, 2011.

18.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

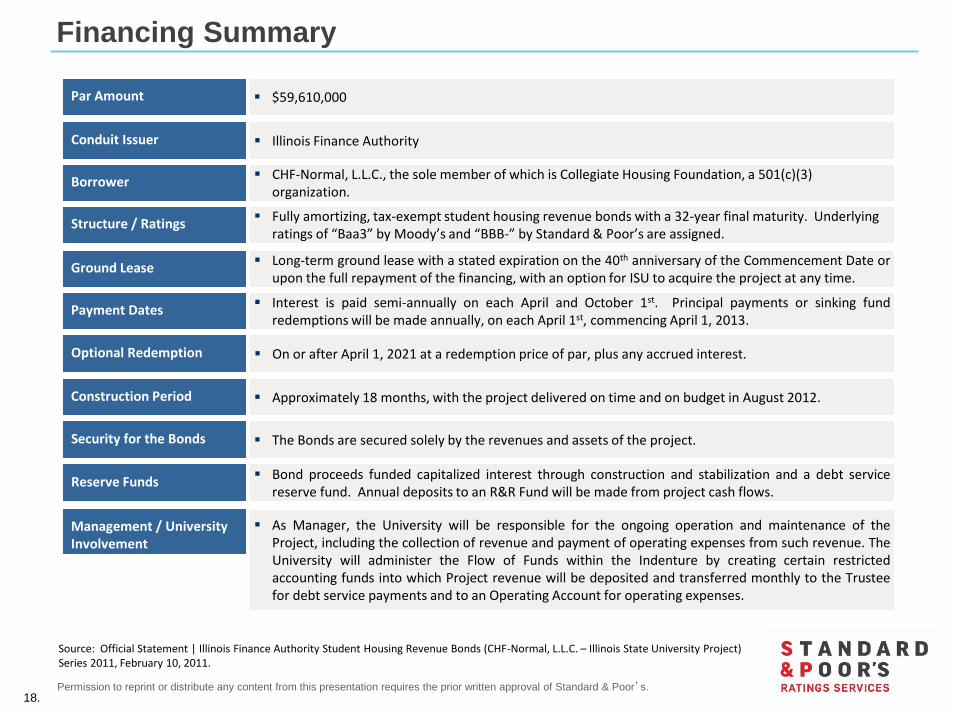

Financing Summary

$59,610,000Par Amount

Fully amortizing, tax-exempt student housing revenue bonds with a 32-year final maturity. Underlying ratings of “Baa3” by Moody’s and “BBB-” by Standard & Poor’s are assigned.

Structure / Ratings

Interest is paid semi-annually on each April and October 1st. Principal payments or sinking fundredemptions will be made annually, on each April 1st, commencing April 1, 2013.

Payment Dates

On or after April 1, 2021 at a redemption price of par, plus any accrued interest.Optional Redemption

Approximately 18 months, with the project delivered on time and on budget in August 2012.Construction Period

The Bonds are secured solely by the revenues and assets of the project.Security for the Bonds

Bond proceeds funded capitalized interest through construction and stabilization and a debt servicereserve fund. Annual deposits to an R&R Fund will be made from project cash flows.

Reserve Funds

The University will enter into an absolute net, bond type lease, which will be sufficient to cover debt service on the bonds and related expenses.

Management / University Involvement

As Manager, the University will be responsible for the ongoing operation and maintenance of theProject, including the collection of revenue and payment of operating expenses from such revenue. TheUniversity will administer the Flow of Funds within the Indenture by creating certain restrictedaccounting funds into which Project revenue will be deposited and transferred monthly to the Trusteefor debt service payments and to an Operating Account for operating expenses.

CHF-Normal, L.L.C., the sole member of which is Collegiate Housing Foundation, a 501(c)(3) organization.

Borrower

Illinois Finance AuthorityConduit Issuer

Long-term ground lease with a stated expiration on the 40th anniversary of the Commencement Date orupon the full repayment of the financing, with an option for ISU to acquire the project at any time.

Ground Lease

Source: Official Statement | Illinois Finance Authority Student Housing Revenue Bonds (CHF-Normal, L.L.C. – Illinois State University Project) Series 2011, February 10, 2011.

19.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

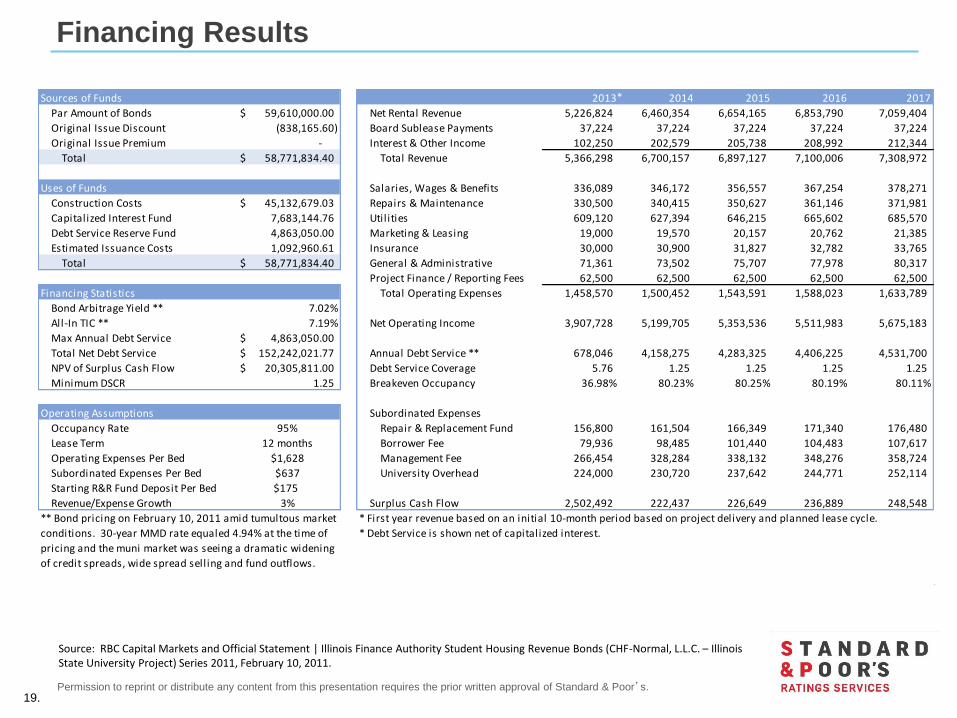

Financing Results

Sources of Funds 2013 2014 2015 2016 2017

Par Amount of Bonds 59,610,000.00$ Net Rental Revenue 5,226,824 6,460,354 6,654,165 6,853,790 7,059,404

Original Issue Discount (838,165.60) Board Sublease Payments 37,224 37,224 37,224 37,224 37,224

Original Issue Premium - Interest & Other Income 102,250 202,579 205,738 208,992 212,344

Total 58,771,834.40$ Total Revenue 5,366,298 6,700,157 6,897,127 7,100,006 7,308,972

Uses of Funds Salaries, Wages & Benefits 336,089 346,172 356,557 367,254 378,271

Construction Costs 45,132,679.03$ Repairs & Maintenance 330,500 340,415 350,627 361,146 371,981

Capitalized Interest Fund 7,683,144.76 Util ities 609,120 627,394 646,215 665,602 685,570

Debt Service Reserve Fund 4,863,050.00 Marketing & Leasing 19,000 19,570 20,157 20,762 21,385

Estimated Issuance Costs 1,092,960.61 Insurance 30,000 30,900 31,827 32,782 33,765

Total 58,771,834.40$ General & Administrative 71,361 73,502 75,707 77,978 80,317

Project Finance / Reporting Fees 62,500 62,500 62,500 62,500 62,500

Financing Statistics Total Operating Expenses 1,458,570 1,500,452 1,543,591 1,588,023 1,633,789

Bond Arbitrage Yield ** 7.02%

All-In TIC ** 7.19% Net Operating Income 3,907,728 5,199,705 5,353,536 5,511,983 5,675,183

Max Annual Debt Service 4,863,050.00$

Total Net Debt Service 152,242,021.77$ Annual Debt Service ** 678,046 4,158,275 4,283,325 4,406,225 4,531,700

NPV of Surplus Cash Flow 20,305,811.00$ Debt Service Coverage 5.76 1.25 1.25 1.25 1.25

Minimum DSCR 1.25 Breakeven Occupancy 36.98% 80.23% 80.25% 80.19% 80.11%

Operating Assumptions Subordinated Expenses

Occupancy Rate 95% Repair & Replacement Fund 156,800 161,504 166,349 171,340 176,480

Lease Term 12 months Borrower Fee 79,936 98,485 101,440 104,483 107,617

Operating Expenses Per Bed $1,628 Management Fee 266,454 328,284 338,132 348,276 358,724

Subordinated Expenses Per Bed $637 University Overhead 224,000 230,720 237,642 244,771 252,114

Starting R&R Fund Deposit Per Bed $175

Revenue/Expense Growth 3% Surplus Cash Flow 2,502,492 222,437 226,649 236,889 248,548

** Bond pricing on February 10, 2011 amid tumultous market * First year revenue based on an initial 10-month period based on project delivery and planned lease cycle.

conditions. 30-year MMD rate equaled 4.94% at the time of * Debt Service is shown net of capitalized interest.

pricing and the muni market was seeing a dramatic widening

of credit spreads, wide spread selling and fund outflows.

*

Source: RBC Capital Markets and Official Statement | Illinois Finance Authority Student Housing Revenue Bonds (CHF-Normal, L.L.C. – Illinois State University Project) Series 2011, February 10, 2011.

20.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

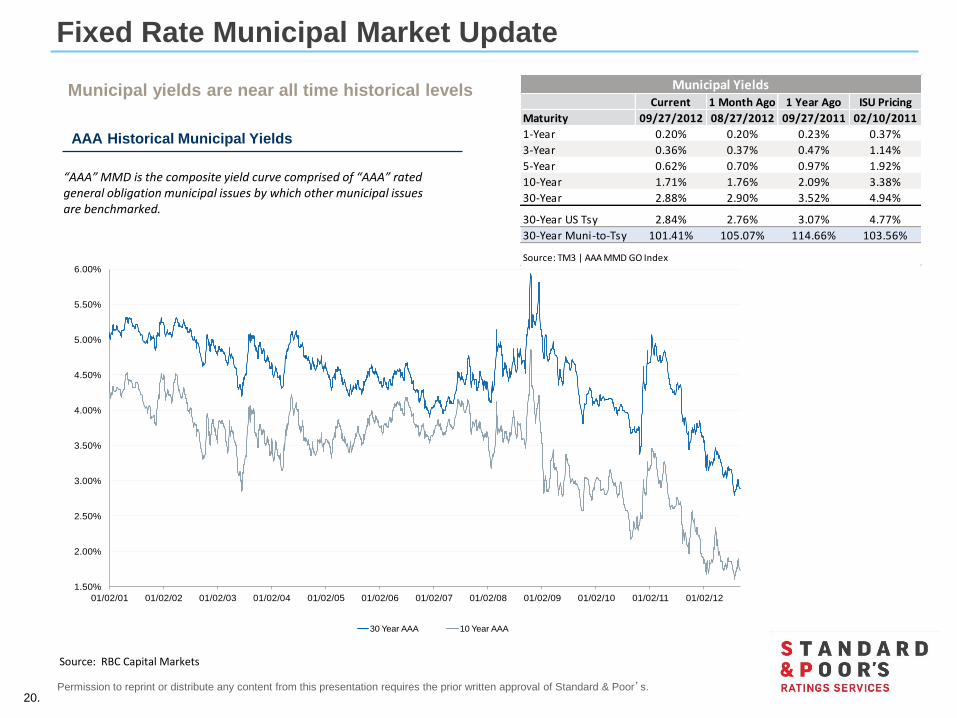

Fixed Rate Municipal Market Update

Municipal yields are near all time historical levels

AAA Historical Municipal Yields

“AAA” MMD is the composite yield curve comprised of “AAA” rated general obligation municipal issues by which other municipal issues are benchmarked.

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

5.50%

6.00%

01/02/01 01/02/02 01/02/03 01/02/04 01/02/05 01/02/06 01/02/07 01/02/08 01/02/09 01/02/10 01/02/11 01/02/12

30 Year AAA 10 Year AAA

Source: RBC Capital Markets

Current 1 Month Ago 1 Year Ago ISU Pricing

Maturity 09/27/2012 08/27/2012 09/27/2011 02/10/2011

1-Year 0.20% 0.20% 0.23% 0.37%

3-Year 0.36% 0.37% 0.47% 1.14%

5-Year 0.62% 0.70% 0.97% 1.92%

10-Year 1.71% 1.76% 2.09% 3.38%

30-Year 2.88% 2.90% 3.52% 4.94%

30-Year US Tsy 2.84% 2.76% 3.07% 4.77%

30-Year Muni-to-Tsy 101.41% 105.07% 114.66% 103.56%

Source: TM3 | AAA MMD GO Index

Municipal Yields

21.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

A Rating Agency Perspective Jessica Lukas, Associate Director

Standard and Poor’s

22.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Current Debt Trends

Median Debt per FTE By Rating Category 2011-2007

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

AAA AA A BBB

2011 2010 2009 2008 2007

Median Debt per FTE By Rating Category 2011-2007

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

AAA AA A BBB

2011 2010 2009 2008 2007

Public University

Private University

• General Characteristics

• Debt Issuance Increasing

• Deferred maint. growing

• Issuers remain conservative

• Types of Debt and Structure

• No major trend changes in

security types

• Direct purchase bonds

• Century bonds

• Off-balance sheet bonds*

23.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Traditional vs. Private Housing

• Difference between traditional housing and private housing

– Connectivity: university management, ownership or oversight

– Location: on-campus/ off-campus

• Credit Risk Relationship Model

– University’s long term viability and credit rating

– Economic interest and control

– Demand for housing

– Linkage to university

– Stand alone or housing system

24.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

S&P Criteria

• Criteria that Standard and Poor’s follows:

– Location

– Management

– Rate covenants and bond test

Cash flows

– Reserves and insurance

– Occupancy rates and breakeven levels

– Construction risk

– Debt structure

– Long term rating of institution

WICHE = Western Interstate Commission for Higher Education.

25.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

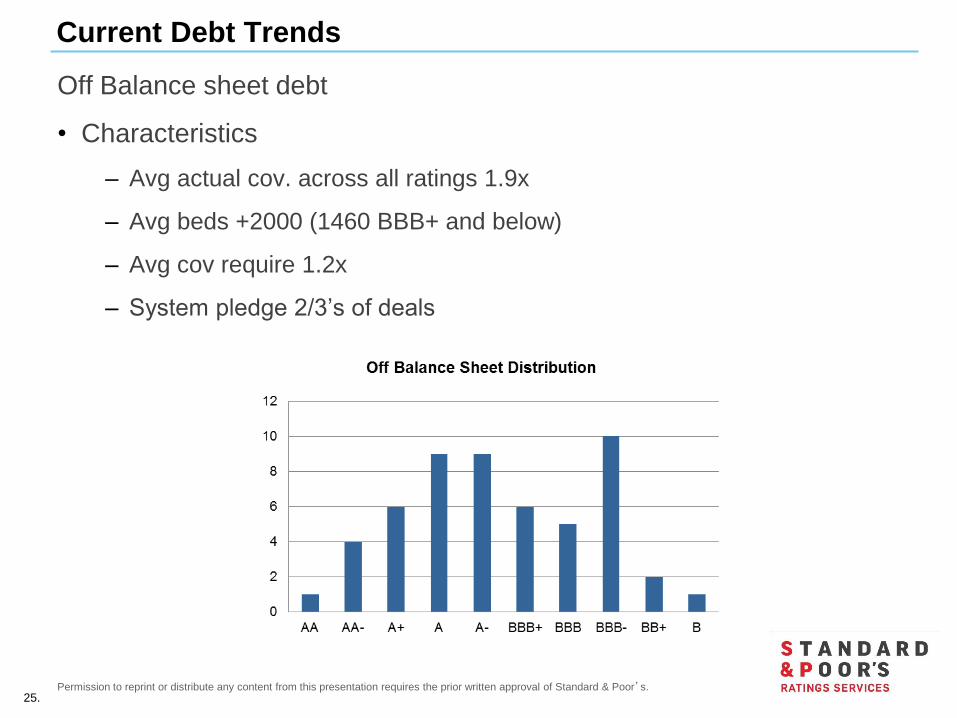

Current Debt Trends

Off Balance sheet debt

• Characteristics

– Avg actual cov. across all ratings 1.9x

– Avg beds +2000 (1460 BBB+ and below)

– Avg cov require 1.2x

– System pledge 2/3’s of deals

26.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

CHF-Normal, LLC – Rating Strengths

Overview of OBS Rating (from Standard and Poor’s Perspective)

• ISU's (A+/ Stable) solid demand for university-owned housing, which operates at over

96% of capacity

• New project beds are substantially replacement stock

• The bonds' adequate security features

• High connectivity between ISU and the project, as demonstrated by the project's on-

campus location, ISU's management, oversight, and active role in marketing the new

housing as part of its own housing stock, and eventual ownership of the project once

the bonds are repaid

• The project's assumed break-even (1.0x) occupancy levels of 83.6%, which we

consider manageable

• ISU's stable enrollment and demand trends - with fall 2011's enrollment of 21,080,

71% freshman selectivity, and 36% matriculation rate.

27.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Connectivity – University support for the project

• The new housing facility represents a small portion of total on-campus beds

(approximately 15%) at ISU

• Replacement Housing - as the new housing becomes available, the university plans

to take approximately 1,774 beds offline

• Ground lease - contains provisions outlining the university's support for the project,

which includes the decommissioning of the aforementioned existing housing facilities

• The new apartment complex will be located on campus; a natural pathway will

connect the facilities with the main campus.

28.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

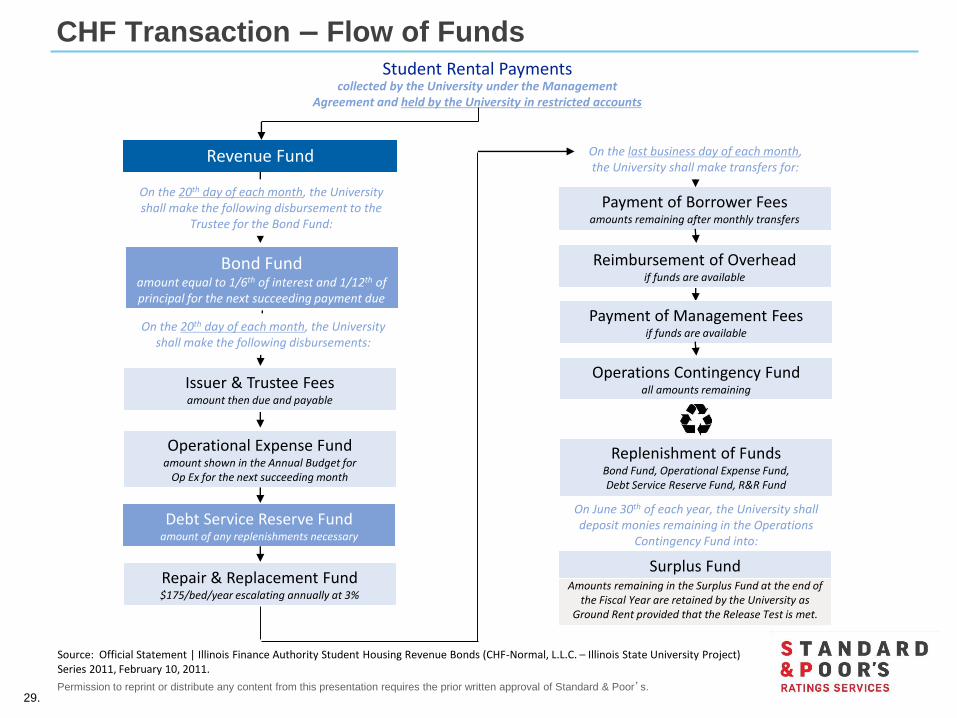

Management & Flow of Funds

Why is this important?

• Who will manage the housing units?

• Who will market the housing units?

• Will the housing units be connected to the campus computer system?

• Will they have the benefits of university campus parking and police services?

• What type of housing contract will be used? And, will it enforce the same terms and

conditions as other university housing?

• Who will collect monthly all housing rental payments and who will transmit revenues to

the trustee to provide for the funding of debt service payments and other financing

related expenses?

• What will happen to any surplus funds, after debt service coverage has been met?

29.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

CHF Transaction – Flow of Funds

3

Student Rental Payments

Revenue Fund

collected by the University under the Management Agreement and held by the University in restricted accounts

Issuer & Trustee Feesamount then due and payable

Operational Expense Fundamount shown in the Annual Budget for

Op Ex for the next succeeding month

Debt Service Reserve Fundamount of any replenishments necessary

Payment of Borrower Feesamounts remaining after monthly transfers

Replenishment of FundsBond Fund, Operational Expense Fund, Debt Service Reserve Fund, R&R Fund

On the 20th day of each month, the University shall make the following disbursement to the

Trustee for the Bond Fund:

Operations Contingency Fundall amounts remaining

On June 30th of each year, the University shall deposit monies remaining in the Operations

Contingency Fund into:

Repair & Replacement Fund$175/bed/year escalating annually at 3%

Bond Fundamount equal to 1/6th of interest and 1/12th of principal for the next succeeding payment due

On the 20th day of each month, the University shall make the following disbursements:

On the last business day of each month, the University shall make transfers for:

Reimbursement of Overheadif funds are available

Payment of Management Feesif funds are available

Amounts remaining in the Surplus Fund at the end of the Fiscal Year are retained by the University as

Ground Rent provided that the Release Test is met.

Surplus Fund

Source: Official Statement | Illinois Finance Authority Student Housing Revenue Bonds (CHF-Normal, L.L.C. – Illinois State University Project) Series 2011, February 10, 2011.

30.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

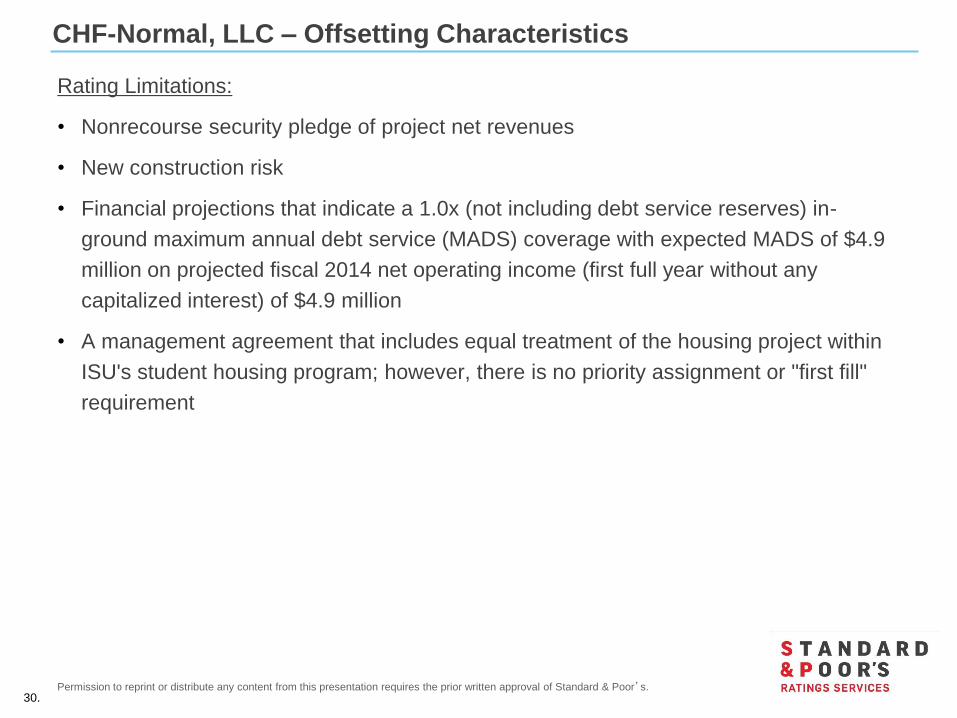

CHF-Normal, LLC – Offsetting Characteristics

Rating Limitations:

• Nonrecourse security pledge of project net revenues

• New construction risk

• Financial projections that indicate a 1.0x (not including debt service reserves) in-

ground maximum annual debt service (MADS) coverage with expected MADS of $4.9

million on projected fiscal 2014 net operating income (first full year without any

capitalized interest) of $4.9 million

• A management agreement that includes equal treatment of the housing project within

ISU's student housing program; however, there is no priority assignment or "first fill"

requirement

31.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

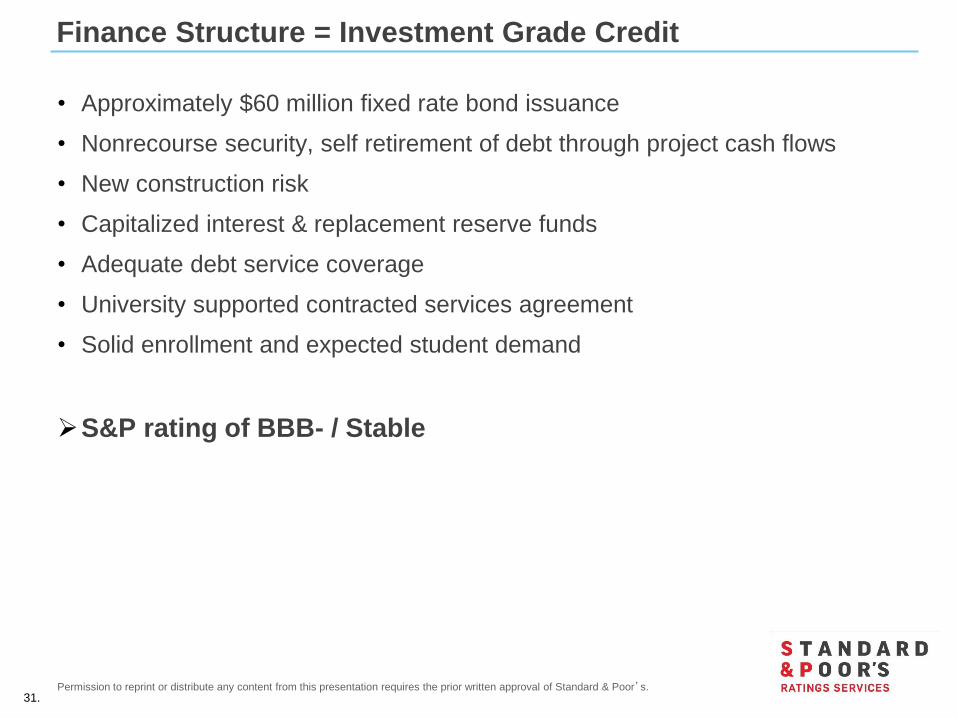

Finance Structure = Investment Grade Credit

• Approximately $60 million fixed rate bond issuance

• Nonrecourse security, self retirement of debt through project cash flows

• New construction risk

• Capitalized interest & replacement reserve funds

• Adequate debt service coverage

• University supported contracted services agreement

• Solid enrollment and expected student demand

S&P rating of BBB- / Stable

32.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Cardinal Court

• Project construction commenced in March 2011 and was completed by August 2012

• Construction was on time and on budget

• Student demand for the property is strong, with fall 2012 occupancy of 99%

Before….

After….

33.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Question & Answer Session

34.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Contact Information

Jessica Lukas

(312) 233-7004

Dan Layzell

(309) 438-2775

Sara Russell

(410) 625-6119

35.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Copyright © 2011 by Standard & Poor’s Financial Services LLC. All rights reserved.

No content (including ratings, credit-related analyses and data, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse engineered, reproduced or

distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of Standard & Poor’s Financial Services LLC or its affiliates (collectively, S&P). The

Content shall not be used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or agents (collectively S&P Parties) do not

guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results

obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content is provided on an “as is” basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR

IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS,

SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT’S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE

CONFIGURATION. In no event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees,

or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised of the possibility of such

damages.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact. S&P’s opinions, analyses and rating

acknowledgment decisions (described below) are not recommendations to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security.. S&P

assumes no obligation to update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its

management, employees, advisors and/or clients when making investment and other business decisions.. S&P does not act as a fiduciary or an investment advisor except where registered as such. While

S&P has obtained information from sources it believes to be reliable, S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain regulatory purposes, S&P reserves the right to assign,

withdraw or suspend such acknowledgement at any time and in its sole discretion. S&P Parties disclaim any duty whatsoever arising out of the assignment, withdrawal or suspension of an acknowledgment as

well as any liability for any damage alleged to have been suffered on account thereof.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business units of S&P may

have information that is not available to other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain non-public information received in connection with each

analytical process.

S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the right to disseminate its opinions and analyses. S&P's

public ratings and analyses are made available on its Web sites, www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription), and may be

distributed through other means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available at www.standardandpoors.com/usratingsfees.

STANDARD & POOR’S, S&P, GLOBAL CREDIT PORTAL and RATINGSDIRECT are registered trademarks of Standard & Poor’s Financial Services LLC.

www.standardandpoors.com

36.Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Disclaimer

RBC Capital Markets, LLC (“RBC CM”) is providing the information contained in this document for discussion purposes only and not in

connection with RBC CM serving as Underwriter, Investment Banker, municipal advisor, financial advisor or fiduciary to a financial transaction

participant or any other person or entity. RBC CM will not have any duties or liability to any person or entity in connection with the information

being provided herein. The information provided is not intended to be and should not be construed as “advice” within the meaning of Section

15B of the Securities Exchange Act of 1934. The financial transaction participants should consult with its own legal, accounting, tax, financial

and other advisors, as applicable, to the extent it deems appropriate.

This presentation was prepared exclusively for the benefit of and internal use by the recipient for the purpose of considering the transaction or

transactions contemplated herein. This presentation is confidential and proprietary to RBC Capital Markets, LLC (“RBC CM”) and may not be

disclosed, reproduced, distributed or used for any other purpose by the recipient without RBCCM’s express written consent.

By acceptance of these materials, and notwithstanding any other express or implied agreement, arrangement, or understanding to the contrary,

RBC CM, its affiliates and the recipient agree that the recipient (and its employees, representatives, and other agents) may disclose to any and

all persons, without limitation of any kind from the commencement of discussions, the tax treatment, structure or strategy of the transaction

and any fact that may be relevant to understanding such treatment, structure or strategy, and all materials of any kind (including opinions or

other tax analyses) that are provided to the recipient relating to such tax treatment, structure, or strategy.

The information and any analyses contained in this presentation are taken from, or based upon, information obtained from the recipient or from

publicly available sources, the completeness and accuracy of which has not been independently verified, and cannot be assured by RBC CM.

The information and any analyses in these materials reflect prevailing conditions and RBC CM’s views as of this date, all of which are subject

to change.

To the extent projections and financial analyses are set forth herein, they may be based on estimated financial performance prepared by or in

consultation with the recipient and are intended only to suggest reasonable ranges of results. The printed presentation is incomplete without

reference to the oral presentation or other written materials that supplement it.

IRS Circular 230 Disclosure: RBC CM and its affiliates do not provide tax advice and nothing contained herein should be construed as tax

advice. Any discussion of U.S. tax matters contained herein (including any attachments) (i) was not intended or written to be used, and cannot

be used, by you for the purpose of avoiding tax penalties; and (ii) was written in connection with the promotion or marketing of the matters

addressed herein. Accordingly, you should seek advice based upon your particular circumstances from an independent tax advisor.