Embed Size (px)

Citation preview

1

New Supervisory Expectations for Interest Rate Risk Management

On July 7, 2011, the Office of the Comptroller of the Currency (OCC), Board of Governors of the Federal Reserve System (FRB), the Federal Deposit Insurance Corporation (FDIC), and the Office of Thrift Supervision (OTS), published a final notice in the Federal Register to notify OTS-supervised institutions of the conversion from filing the Thrift Financial Report (TFR) to filing the Call Report beginning with the reporting period ending March 31, 2012.

OCC regulated thrifts will also be expected to comply with assessment, measurement and management processes for interest rate risk that have been applied to national banks for years. The relevant supervisory documents that thrifts may refer to include:

• Interagency Interest Rate Risk (IRR) Advisory issued by the FFIEC, January 2010 • OCC Bulletin 2010-1, IRR: Interagency Advisory on IRR Management • OTS CEO Memo #334, January 7, 2010 • OCC Bulletin 2011-12, Sound Practices for Model Risk Management • OCC Bulletin 2004-29, Embedded Options and Long-Term IRR • 1996 Interagency Policy Statement on Interest Rate Risk issued by the OCC, FDIC and

FRB

This document will discuss some of the key changes thrifts will be required to implement and will hopefully serve as a guide for savings associations as they make the transition to the OCC guidelines.

Key Differences between OTS and OCC IRR Supervision

The banking regulators’ approach to interest rate risk management requires greater management participation in the process than that of the thrift supervisors. Perhaps the most significant change is the abolition of the IRR measurement service by the OTS for thrifts under $ 1 billion in assets. Beginning March 31, 2012, all thrifts must have resources to measure their own interest rate sensitivity. The OTS asset and liability price tables will no longer be published after December 31, 2011 since most of the information is available through model vendors and public websites. Assumptions used in IRR modeling are expected to be documented, monitored for relevancy over time, back-tested for appropriateness and regularly updated.

Earnings at Risk

Another key difference between the OCC and OTS approach is the requirement to evaluate the impact of interest rate changes on economic capital and earnings. What the OCC refers to as long term and short term views, respectively. A minimum simulation period of 2 years is noted in the January 2010 Interagency IRR Advisory; 5 years is desirable. In addition, the

2

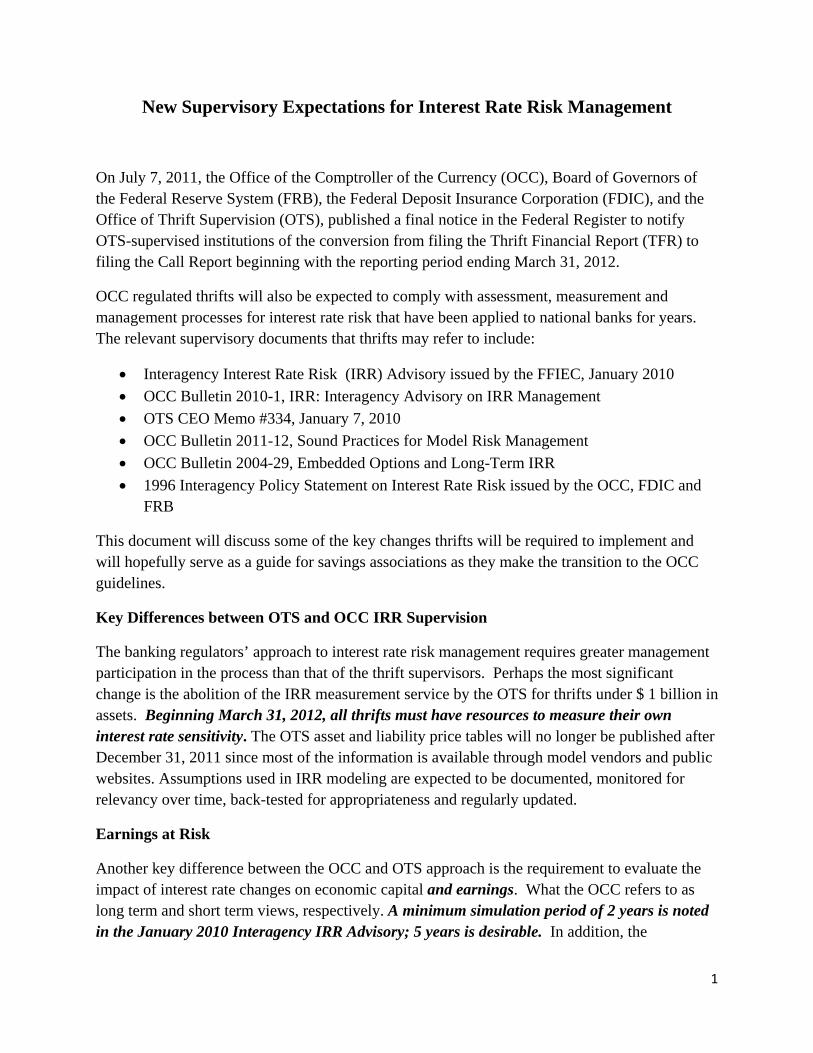

simulation of non-parallel yield curves, or yield curve twists, and the affect on a thrift’s income and net present value, is now required. The OTS CEO Memo #334 specifically states, “due to data collection limitations, in some cases the NPV model may give an incomplete picture of thrift’s IRR profile. Specifically, it does not capture the potential impact of non-parallel shifts in the yield curve and the extent to which changes in interest rates affect short-term earnings. Well managed institutions should be able to quantify these specific risks.” A sample analysis from Sterne Agee’s Bank Earnings Report (SABER) is pictured below.

Threshold limits for earnings at risk should also be established and approved by the Board of Directors of the institutions. A summary of the approval process in Board minutes are an effective way to document this action for future reference.

Measuring Risk of Complex Securities

In Thrift Bulletin 13a (TB 13a), OTS required smaller thrifts to independently measure the risk of a security deemed “complex” only when the holdings exceeded 5 percent of total assets. OCC regulated thrifts will be required to perform price sensitivity analyses for all complex securities prior to purchase, regardless of the size of the institution or its holdings.

Measuring the Impact of Transactions on IRR

3

In previous thrift guidance, institutions with more than $1 billion in assets were required to conduct analysis to show the impact on NPV for transactions that my increase the thrift’s IRR sensitivity by more than 25 basis points. The OCC expects all institutions, regardless of size, to evaluate the potential impact on earnings and economic value resulting from any new financial products or business plans.

Stress Testing

Stress testing of model assumptions, earnings and economic value are all essential parts of IRR management. The stress testing should include both scenario and sensitivity analysis such as rate changes of up and down 300 and 400 basis points. Institutions with sizable amounts of embedded options or structured products on the balance sheet (mortgage loans or securities, callable bonds, convertible wholesale funding) are expected to perform option adjusted spread (OAS) analysis to measure the interest rate risk of the instruments.

Qualitative Measures

OCC interest rate risk guidance places equal weight on qualitative measures and quantitative measures to determine an overall level of risk in the institution. Thrifts that have historically relied on the OTS NPV model for risk assessment must now incorporate qualitative risk measures such as risk limit structures for earnings and economic value; automated processes compared with manual input; staff knowledge of IRR management techniques.

Model Validation

Lastly, model validation is required for both in-house and vendor models to ensure the integrity of the overall IRR management process. In-house models should be independently reviewed for soundness of the algorithms and of the modeling process. Institutions should conduct at least an annual review of the IRR model to determine if it is working as intended and if the existing validation activities are sufficient. Institutions that use third party models are not required to test the algorithms of the model, but request an independent validation from the vendor. A review of the processes by which IRR is measured, monitored and managed is still required.

Use of Third Party Models

OCC regulated institutions have used third party vendor models for many years. According to officials from the OCC, “model capabilities have increased tremendously over the last decade, and the improved ability to control your risk positions and ensure consistent earnings and capital support, will bring immediate and hopefully lasting benefits. ….. Technological advances have made third party models a cost effective alternative for institutions of all sizes

4

and levels of complexity.”1 As with any third party system employed by banks, institutions are expected to understand the assumptions and methodologies employed by the vendor. The model calculations and methodologies should be transparent to the user and we encourage banks to request written documentation of the risk measures, assumptions and scenarios used by the model. Assumptions should be flexible to allow for the user to choose alternative rate scenarios and other key drivers of the model results. Vendors ought to provide ongoing support to the users and training if required.

Suggestions for Interest Rate Risk Management

Sterne Agee believes that the model is just the beginning of the interest rate risk management process. The recent volatility in interest rates requires a sound measurement of the impact of interest rate changes on earnings and economic value to afford management the most accurate data from which to make decisions that may enhance profitability without imposing undue risk. Institutions with balance sheets that have few embedded options or other complex structures, may not require option adjusted spread analyses or other option pricing methodologies in their IRR model. Size is not always an appropriate measure of complexity as this previous banking crises has shown; therefore, it is important that when choosing a model, institutions find one that is capable of measuring the cash flow and valuation sensitivity to changing interest rates of the instruments on the balance sheet.

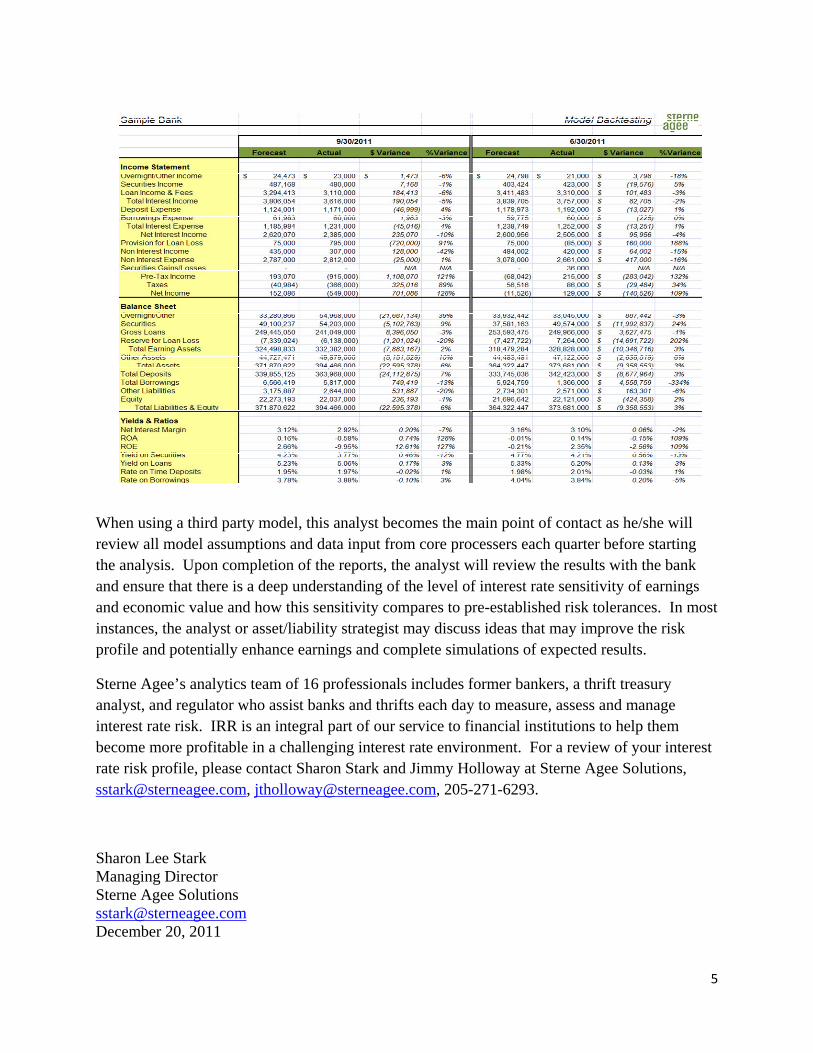

We suggest banks request a dedicated analyst for your bank from the vendor to ensure that the institution’s risk profile is accurately represented and results are monitored and managed in an ongoing manner. This includes the quarterly review of assumptions and back-testing of actual results and implementation of adjustments if needed. An example of back-testing is illustrated below.

1 OCC Transcript “Supervisory Expectations for Interest Rate Risk Management,” November 7, 2011, page 12 of 36. OCC PowerPoint presentation, “Supervisory Expectations for Interest Rate Risk Management,” November 7, 2011, page 30.

5

When using a third party model, this analyst becomes the main point of contact as he/she will review all model assumptions and data input from core processers each quarter before starting the analysis. Upon completion of the reports, the analyst will review the results with the bank and ensure that there is a deep understanding of the level of interest rate sensitivity of earnings and economic value and how this sensitivity compares to pre-established risk tolerances. In most instances, the analyst or asset/liability strategist may discuss ideas that may improve the risk profile and potentially enhance earnings and complete simulations of expected results.

Sterne Agee’s analytics team of 16 professionals includes former bankers, a thrift treasury analyst, and regulator who assist banks and thrifts each day to measure, assess and manage interest rate risk. IRR is an integral part of our service to financial institutions to help them become more profitable in a challenging interest rate environment. For a review of your interest rate risk profile, please contact Sharon Stark and Jimmy Holloway at Sterne Agee Solutions, [email protected], [email protected], 205-271-6293.

Sharon Lee Stark Managing Director Sterne Agee Solutions [email protected] December 20, 2011