Embed Size (px)

Citation preview

Neuberger Berman Multi-Asset Class Growth FundJuly 2018

For Professional Client Use Only

FIRM OVERVIEW

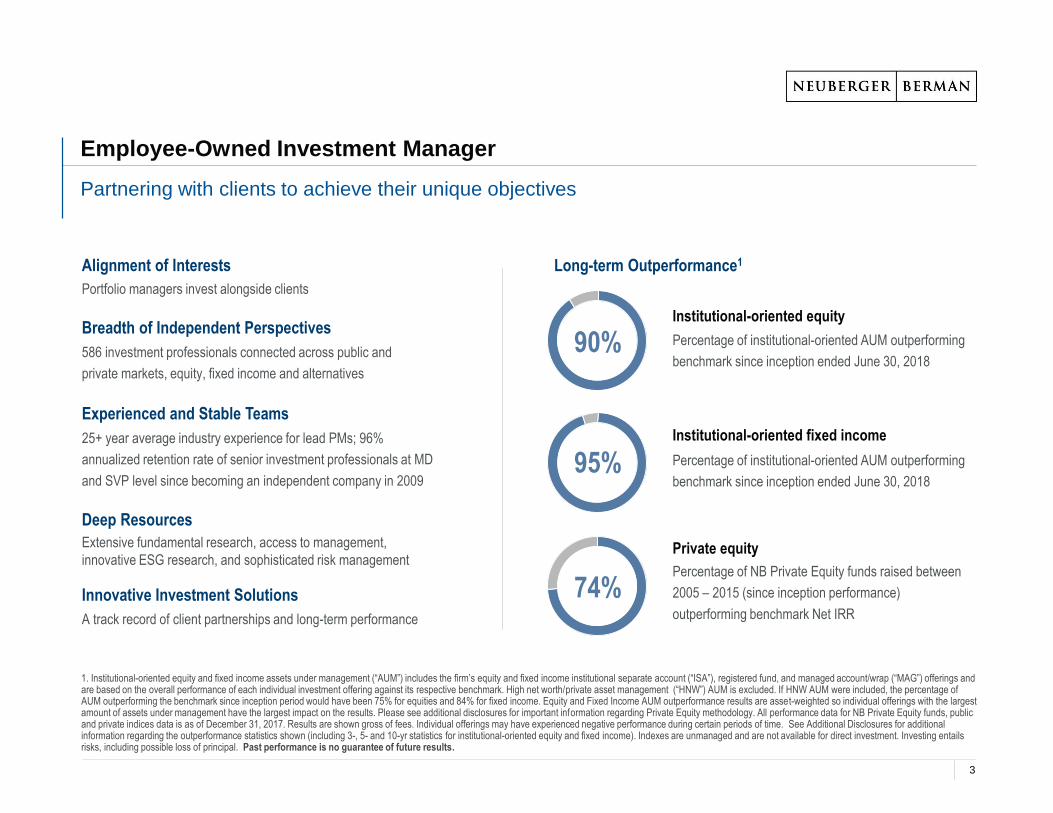

Employee-Owned Investment Manager

Partnering with clients to achieve their unique objectives

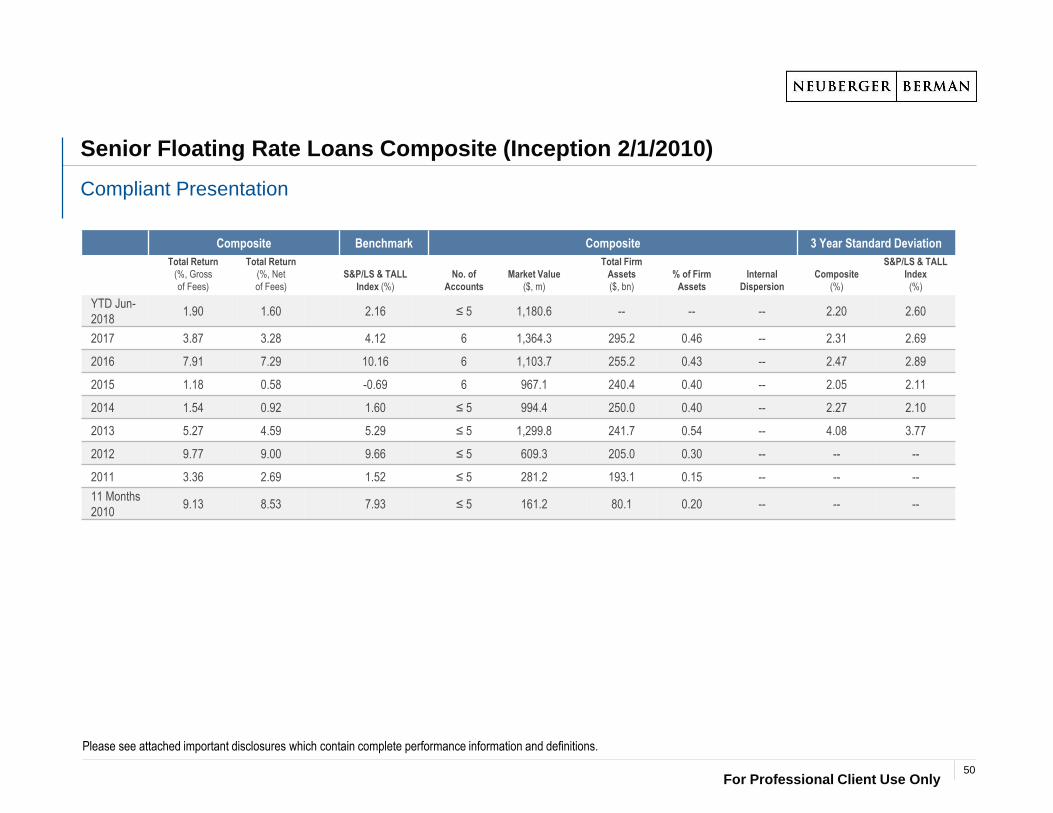

1. Institutional-oriented equity and fixed income assets under management (“AUM”) includes the firm’s equity and fixed income institutional separate account (“ISA”), registered fund, and managed account/wrap (“MAG”) offerings and are based on the overall performance of each individual investment offering against its respective benchmark. High net worth/private asset management (“HNW”) AUM is excluded. If HNW AUM were included, the percentage of AUM outperforming the benchmark since inception period would have been 75% for equities and 84% for fixed income. Equity and Fixed Income AUM outperformance results are asset-weighted so individual offerings with the largest amount of assets under management have the largest impact on the results. Please see additional disclosures for important information regarding Private Equity methodology. All performance data for NB Private Equity funds, public and private indices data is as of December 31, 2017. Results are shown gross of fees. Individual offerings may have experienced negative performance during certain periods of time. See Additional Disclosures for additional information regarding the outperformance statistics shown (including 3-, 5- and 10-yr statistics for institutional-oriented equity and fixed income). Indexes are unmanaged and are not available for direct investment. Investing entails risks, including possible loss of principal. Past performance is no guarantee of future results.

Long-term Outperformance1Alignment of Interests

Portfolio managers invest alongside clients

Breadth of Independent Perspectives

586 investment professionals connected across public and

private markets, equity, fixed income and alternatives

Experienced and Stable Teams

25+ year average industry experience for lead PMs; 96%

annualized retention rate of senior investment professionals at MD

and SVP level since becoming an independent company in 2009

Innovative Investment Solutions

A track record of client partnerships and long-term performance

90%Institutional-oriented equity

Percentage of institutional-oriented AUM outperforming

benchmark since inception ended June 30, 2018

95%Institutional-oriented fixed income

Percentage of institutional-oriented AUM outperforming

benchmark since inception ended June 30, 2018

74%

Private equity

Percentage of NB Private Equity funds raised between

2005 – 2015 (since inception performance)

outperforming benchmark Net IRR

Deep Resources

Extensive fundamental research, access to management,

innovative ESG research, and sophisticated risk management

3

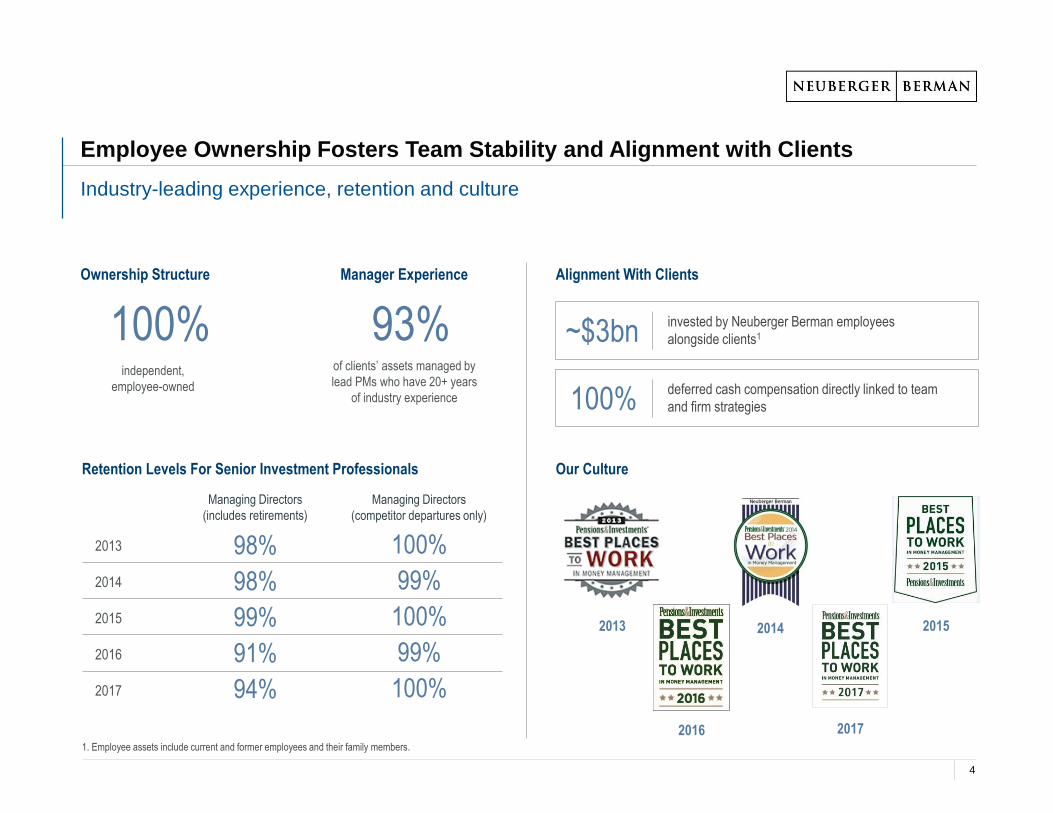

Employee Ownership Fosters Team Stability and Alignment with Clients

Industry-leading experience, retention and culture

1. Employee assets include current and former employees and their family members.

of clients’ assets managed by

lead PMs who have 20+ years

of industry experience

Manager Experience

Retention Levels For Senior Investment Professionals

Managing Directors

(includes retirements)

Managing Directors

(competitor departures only)

98%

98%

99%

91%

94%

100%

99%

100%

99%

100%

2013

2014

2015

2016

2017

93%

Alignment With Clients

invested by Neuberger Berman employees

alongside clients1~$3bn100%independent,

employee-owned

Ownership Structure

deferred cash compensation directly linked to team

and firm strategies100%

Our Culture

2013 2014 2015

2016 2017

4

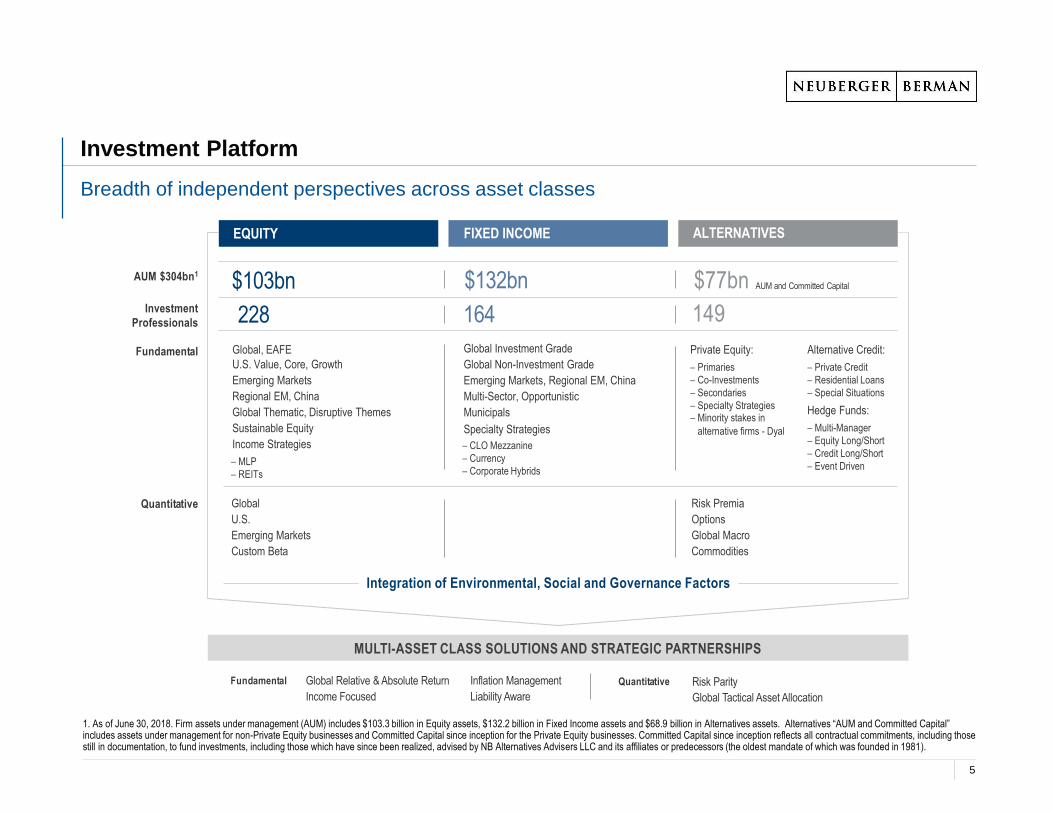

Investment Platform

Breadth of independent perspectives across asset classes

1. As of June 30, 2018. Firm assets under management (AUM) includes $103.3 billion in Equity assets, $132.2 billion in Fixed Income assets and $68.9 billion in Alternatives assets. Alternatives “AUM and Committed Capital” includes assets under management for non-Private Equity businesses and Committed Capital since inception for the Private Equity businesses. Committed Capital since inception reflects all contractual commitments, including those still in documentation, to fund investments, including those which have since been realized, advised by NB Alternatives Advisers LLC and its affiliates or predecessors (the oldest mandate of which was founded in 1981).

EQUITY FIXED INCOME ALTERNATIVES

AUM $304bn1

Investment

Professionals

$103bn

228

$132bn

164

Risk Parity

Global Tactical Asset Allocation

Global Relative & Absolute Return

Income Focused

Inflation Management

Liability Aware

$77bn AUM and Committed Capital

149

Quantitative Global

U.S.

Emerging Markets

Custom Beta

Risk Premia

Options

Global Macro

Commodities

Fundamental Global, EAFE

U.S. Value, Core, Growth

Emerging Markets

Regional EM, China

Global Thematic, Disruptive Themes

Sustainable Equity

Income Strategies

– MLP

– REITs

Global Investment Grade

Global Non-Investment Grade

Emerging Markets, Regional EM, China

Multi-Sector, Opportunistic

Municipals

Specialty Strategies

– CLO Mezzanine

– Currency

– Corporate Hybrids

Private Equity:

– Primaries

– Co-Investments

– Secondaries

– Specialty Strategies– Minority stakes in

alternative firms - Dyal

Alternative Credit:

– Private Credit

– Residential Loans

– Special Situations

Hedge Funds:

– Multi-Manager

– Equity Long/Short

– Credit Long/Short

– Event Driven

QuantitativeFundamental

MULTI-ASSET CLASS SOLUTIONS AND STRATEGIC PARTNERSHIPS

Integration of Environmental, Social and Governance Factors

5

NEUBERGER BERMAN MULTI-ASSET CLASS GROWTH FUND

For Professional Client Use Only

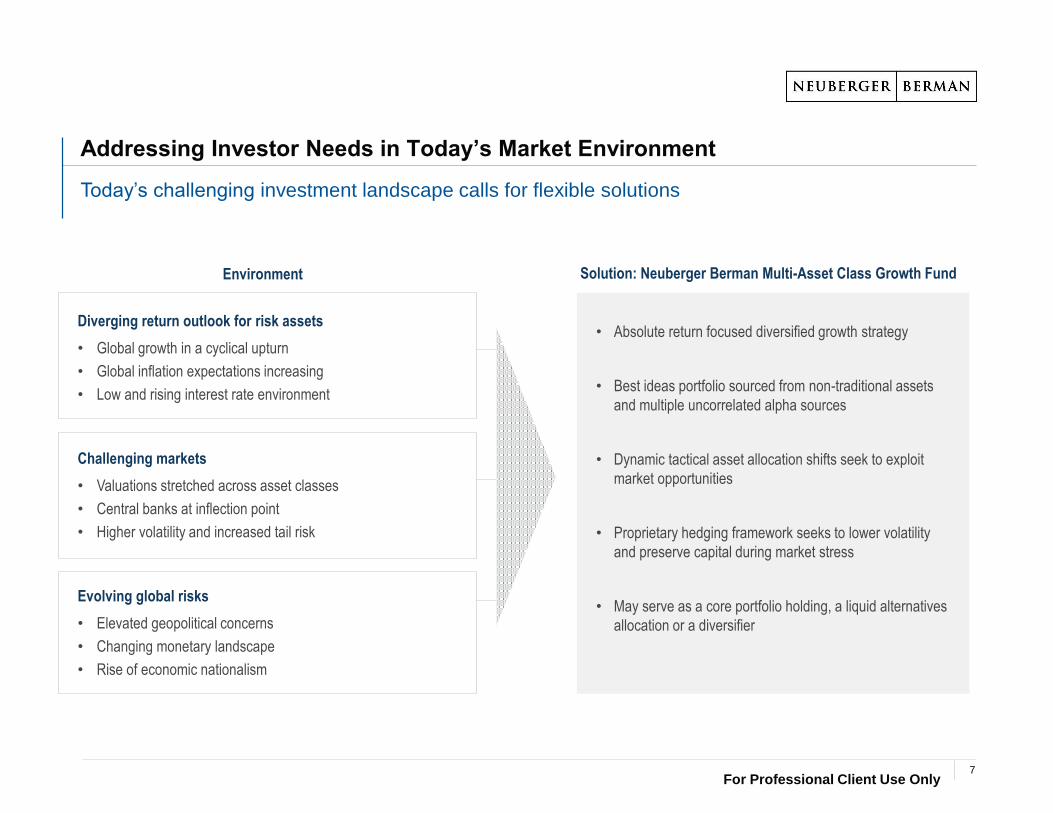

Addressing Investor Needs in Today’s Market Environment

Today’s challenging investment landscape calls for flexible solutions

Solution: Neuberger Berman Multi-Asset Class Growth FundEnvironment

Diverging return outlook for risk assets

• Global growth in a cyclical upturn

• Global inflation expectations increasing

• Low and rising interest rate environment

Challenging markets

• Valuations stretched across asset classes

• Central banks at inflection point

• Higher volatility and increased tail risk

Evolving global risks

• Elevated geopolitical concerns

• Changing monetary landscape

• Rise of economic nationalism

• Absolute return focused diversified growth strategy

• Best ideas portfolio sourced from non-traditional assets

and multiple uncorrelated alpha sources

• Dynamic tactical asset allocation shifts seek to exploit

market opportunities

• Proprietary hedging framework seeks to lower volatility

and preserve capital during market stress

• May serve as a core portfolio holding, a liquid alternatives

allocation or a diversifier

7

For Professional Client Use Only

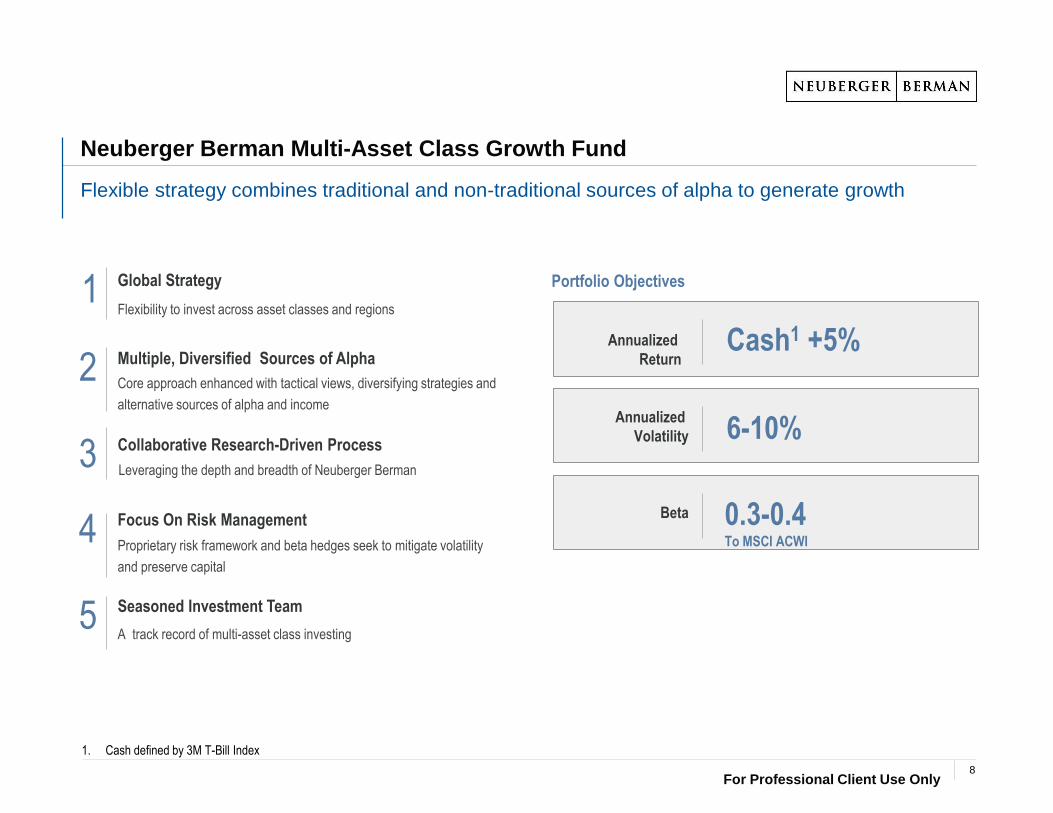

Neuberger Berman Multi-Asset Class Growth Fund

Flexible strategy combines traditional and non-traditional sources of alpha to generate growth

Portfolio Objectives

Cash1 +5%

Annualized

Volatility

Leveraging the depth and breadth of Neuberger Berman

Flexibility to invest across asset classes and regions

Core approach enhanced with tactical views, diversifying strategies and

alternative sources of alpha and income

Proprietary risk framework and beta hedges seek to mitigate volatility

and preserve capital

Global Strategy

Multiple, Diversified Sources of Alpha

Collaborative Research-Driven Process

Focus On Risk Management

A track record of multi-asset class investing

Seasoned Investment Team

1

2

3

4

5

Annualized

Return

6-10%

Beta 0.3-0.4To MSCI ACWI

1. Cash defined by 3M T-Bill Index

8

For Professional Client Use Only

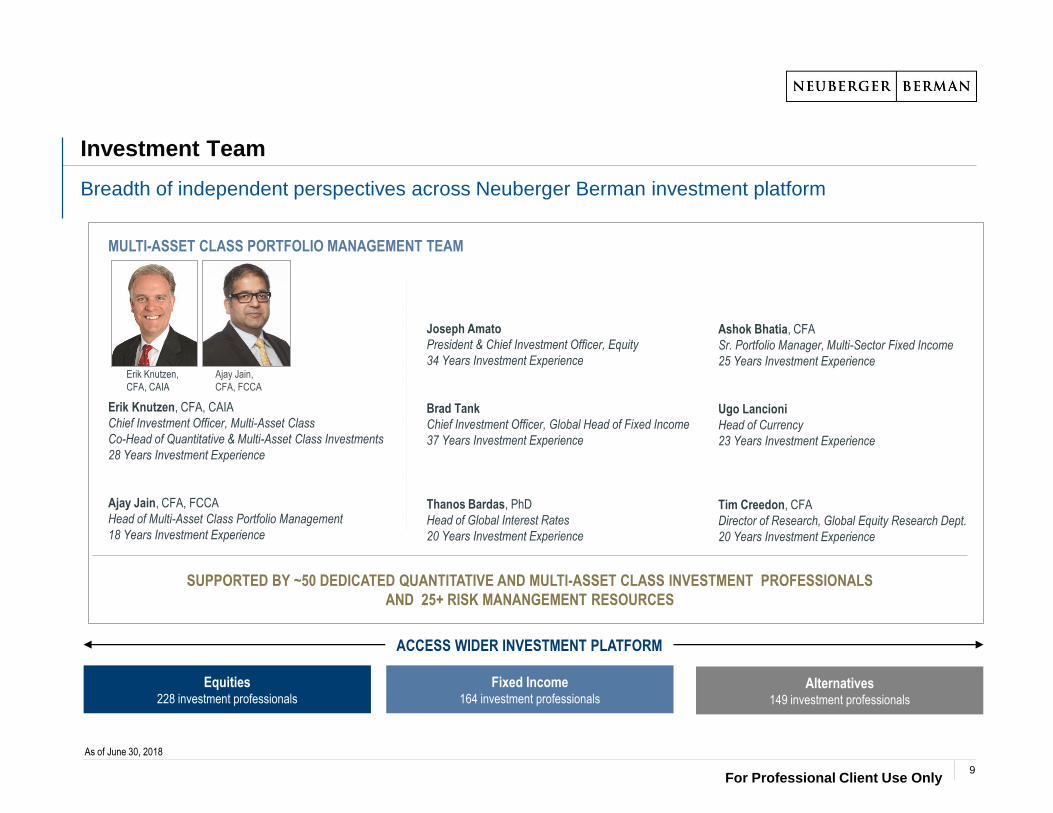

MULTI-ASSET CLASS PORTFOLIO MANAGEMENT TEAM

Erik Knutzen, CFA, CAIA

Chief Investment Officer, Multi-Asset Class

Co-Head of Quantitative & Multi-Asset Class Investments

28 Years Investment Experience

Ajay Jain, CFA, FCCA

Head of Multi-Asset Class Portfolio Management

18 Years Investment Experience

Investment Team

Breadth of independent perspectives across Neuberger Berman investment platform

As of June 30, 2018

Equities228 investment professionals

Fixed Income164 investment professionals

Erik Knutzen,

CFA, CAIA

Ajay Jain,

CFA, FCCA

Joseph Amato

President & Chief Investment Officer, Equity

34 Years Investment Experience

Brad Tank

Chief Investment Officer, Global Head of Fixed Income

37 Years Investment Experience

Thanos Bardas, PhD

Head of Global Interest Rates

20 Years Investment Experience

Ashok Bhatia, CFA

Sr. Portfolio Manager, Multi-Sector Fixed Income

25 Years Investment Experience

Ugo Lancioni

Head of Currency

23 Years Investment Experience

Tim Creedon, CFA

Director of Research, Global Equity Research Dept.

20 Years Investment Experience

SUPPORTED BY ~50 DEDICATED QUANTITATIVE AND MULTI-ASSET CLASS INVESTMENT PROFESSIONALS

AND 25+ RISK MANANGEMENT RESOURCES

ACCESS WIDER INVESTMENT PLATFORM

For Professional Client Use Only

Alternatives149 investment professionals

9

For Professional Client Use Only

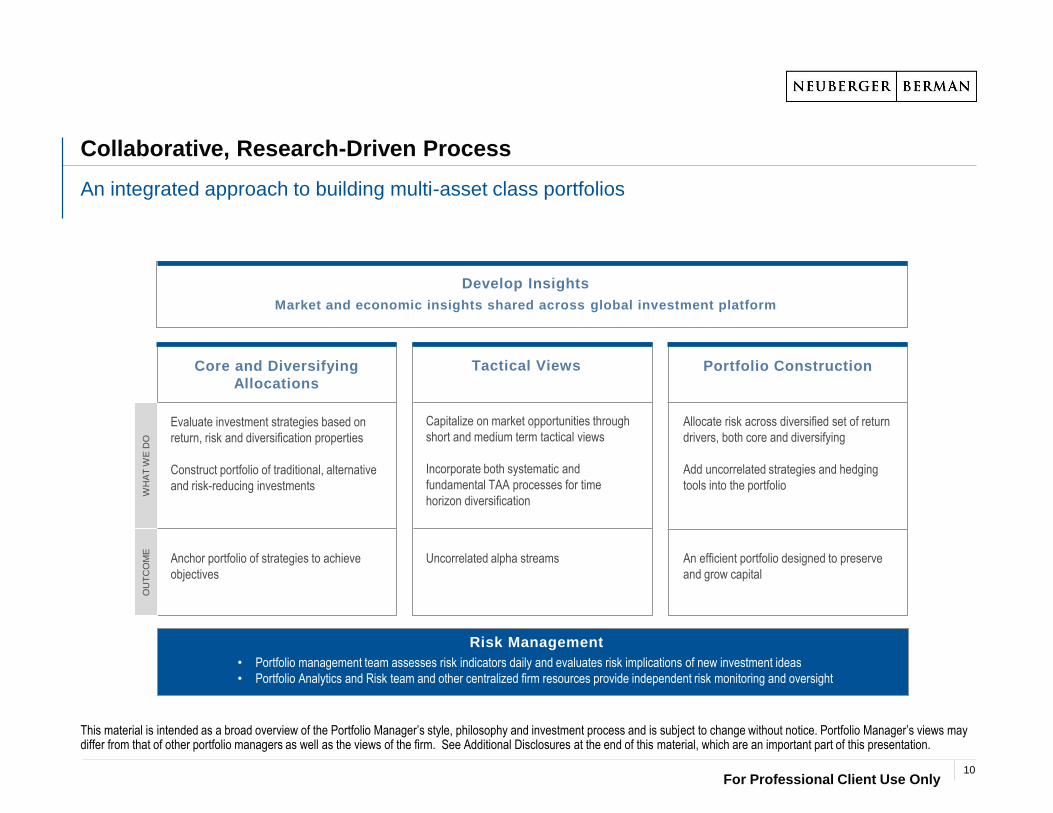

Collaborative, Research-Driven Process

Develop Insights

Risk Management

• Portfolio management team assesses risk indicators daily and evaluates risk implications of new investment ideas

• Portfolio Analytics and Risk team and other centralized firm resources provide independent risk monitoring and oversight

Market and economic insights shared across global investment platform

OU

TC

OM

EW

HA

T W

E D

O

Core and Diversifying

Allocations

Evaluate investment strategies based on

return, risk and diversification properties

Construct portfolio of traditional, alternative

and risk-reducing investments

Anchor portfolio of strategies to achieve

objectives

Tactical Views

Capitalize on market opportunities through

short and medium term tactical views

Incorporate both systematic and

fundamental TAA processes for time

horizon diversification

Uncorrelated alpha streams

Portfolio Construction

Allocate risk across diversified set of return

drivers, both core and diversifying

Add uncorrelated strategies and hedging

tools into the portfolio

An efficient portfolio designed to preserve

and grow capital

An integrated approach to building multi-asset class portfolios

This material is intended as a broad overview of the Portfolio Manager’s style, philosophy and investment process and is subject to change without notice. Portfolio Manager’s views may differ from that of other portfolio managers as well as the views of the firm. See Additional Disclosures at the end of this material, which are an important part of this presentation.

10

For Professional Client Use Only

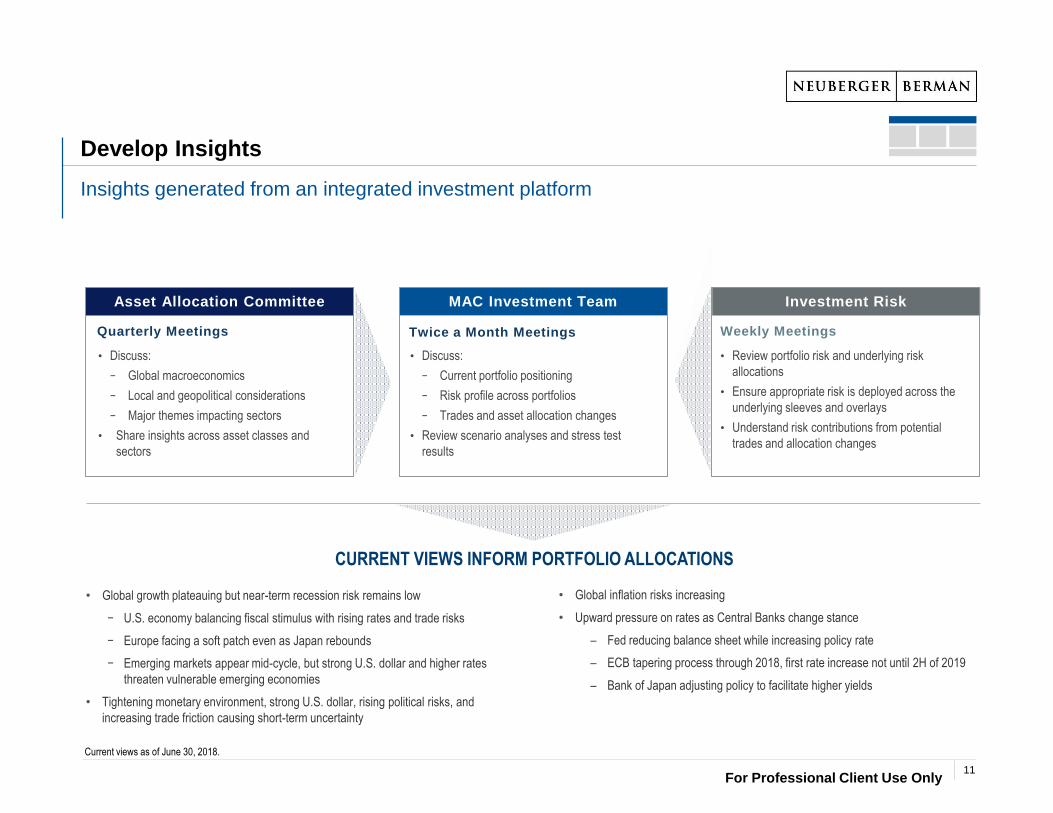

Develop Insights

Insights generated from an integrated investment platform

• Review portfolio risk and underlying risk

allocations

• Ensure appropriate risk is deployed across the

underlying sleeves and overlays

• Understand risk contributions from potential

trades and allocation changes

Weekly Meetings

Investment Risk

• Discuss:

− Global macroeconomics

− Local and geopolitical considerations

− Major themes impacting sectors

• Share insights across asset classes and

sectors

Quarterly Meetings

Asset Allocation Committee MAC Investment Team

• Discuss:

− Current portfolio positioning

− Risk profile across portfolios

− Trades and asset allocation changes

• Review scenario analyses and stress test

results

Twice a Month Meetings

CURRENT VIEWS INFORM PORTFOLIO ALLOCATIONS

Current views as of June 30, 2018.

For Professional Client Use Only

• Global growth plateauing but near-term recession risk remains low

− U.S. economy balancing fiscal stimulus with rising rates and trade risks

− Europe facing a soft patch even as Japan rebounds

− Emerging markets appear mid-cycle, but strong U.S. dollar and higher rates

threaten vulnerable emerging economies

• Tightening monetary environment, strong U.S. dollar, rising political risks, and

increasing trade friction causing short-term uncertainty

• Global inflation risks increasing

• Upward pressure on rates as Central Banks change stance

– Fed reducing balance sheet while increasing policy rate

– ECB tapering process through 2018, first rate increase not until 2H of 2019

– Bank of Japan adjusting policy to facilitate higher yields

11

For Professional Client Use Only

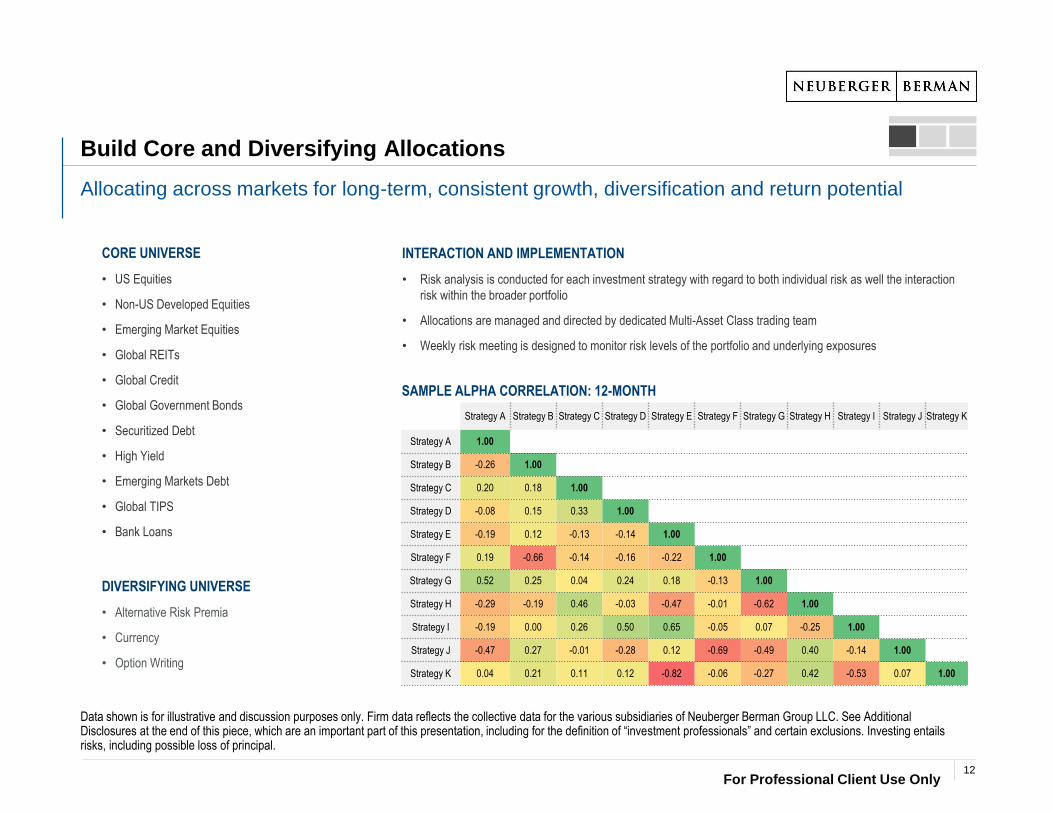

Build Core and Diversifying Allocations

Allocating across markets for long-term, consistent growth, diversification and return potential

Data shown is for illustrative and discussion purposes only. Firm data reflects the collective data for the various subsidiaries of Neuberger Berman Group LLC. See Additional Disclosures at the end of this piece, which are an important part of this presentation, including for the definition of “investment professionals” and certain exclusions. Investing entails risks, including possible loss of principal.

CORE UNIVERSE

• US Equities

• Non-US Developed Equities

• Emerging Market Equities

• Global REITs

• Global Credit

• Global Government Bonds

• Securitized Debt

• High Yield

• Emerging Markets Debt

• Global TIPS

• Bank Loans

DIVERSIFYING UNIVERSE

• Alternative Risk Premia

• Currency

• Option Writing

SAMPLE ALPHA CORRELATION: 12-MONTH

INTERACTION AND IMPLEMENTATION

• Risk analysis is conducted for each investment strategy with regard to both individual risk as well the interaction

risk within the broader portfolio

• Allocations are managed and directed by dedicated Multi-Asset Class trading team

• Weekly risk meeting is designed to monitor risk levels of the portfolio and underlying exposures

Strategy A Strategy B Strategy C Strategy D Strategy E Strategy F Strategy G Strategy H Strategy I Strategy J Strategy K

Strategy A 1.00

Strategy B -0.26 1.00

Strategy C 0.20 0.18 1.00

Strategy D -0.08 0.15 0.33 1.00

Strategy E -0.19 0.12 -0.13 -0.14 1.00

Strategy F 0.19 -0.66 -0.14 -0.16 -0.22 1.00

Strategy G 0.52 0.25 0.04 0.24 0.18 -0.13 1.00

Strategy H -0.29 -0.19 0.46 -0.03 -0.47 -0.01 -0.62 1.00

Strategy I -0.19 0.00 0.26 0.50 0.65 -0.05 0.07 -0.25 1.00

Strategy J -0.47 0.27 -0.01 -0.28 0.12 -0.69 -0.49 0.40 -0.14 1.00

Strategy K 0.04 0.21 0.11 0.12 -0.82 -0.06 -0.27 0.42 -0.53 0.07 1.00

12

For Professional Client Use Only

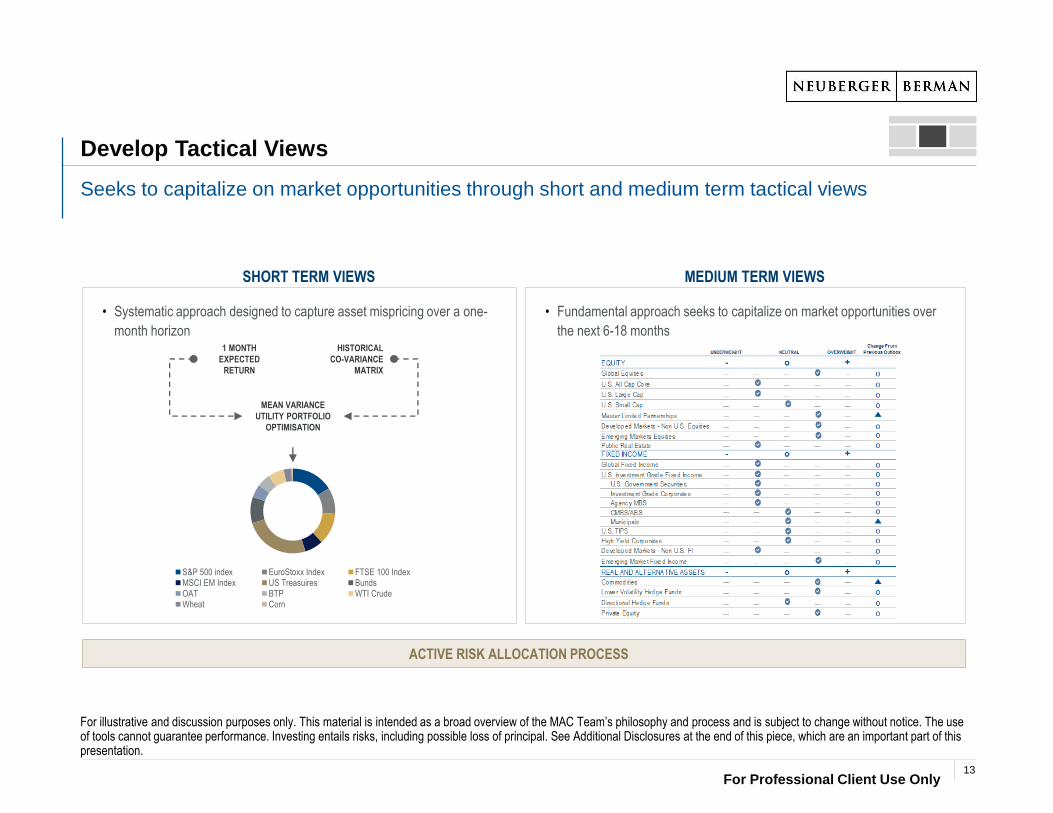

Develop Tactical Views

Seeks to capitalize on market opportunities through short and medium term tactical views

• Fundamental approach seeks to capitalize on market opportunities over

the next 6-18 months

SHORT TERM VIEWS MEDIUM TERM VIEWS

• Systematic approach designed to capture asset mispricing over a one-

month horizon

MEAN VARIANCE

UTILITY PORTFOLIO

OPTIMISATION

1 MONTH

EXPECTED

RETURN

HISTORICAL

CO-VARIANCE

MATRIX

S&P 500 index EuroStoxx Index FTSE 100 IndexMSCI EM Index US Treasuires BundsOAT BTP WTI CrudeWheat Corn

For illustrative and discussion purposes only. This material is intended as a broad overview of the MAC Team’s philosophy and process and is subject to change without notice. The use of tools cannot guarantee performance. Investing entails risks, including possible loss of principal. See Additional Disclosures at the end of this piece, which are an important part of this presentation.

ACTIVE RISK ALLOCATION PROCESS

13

For Professional Client Use Only

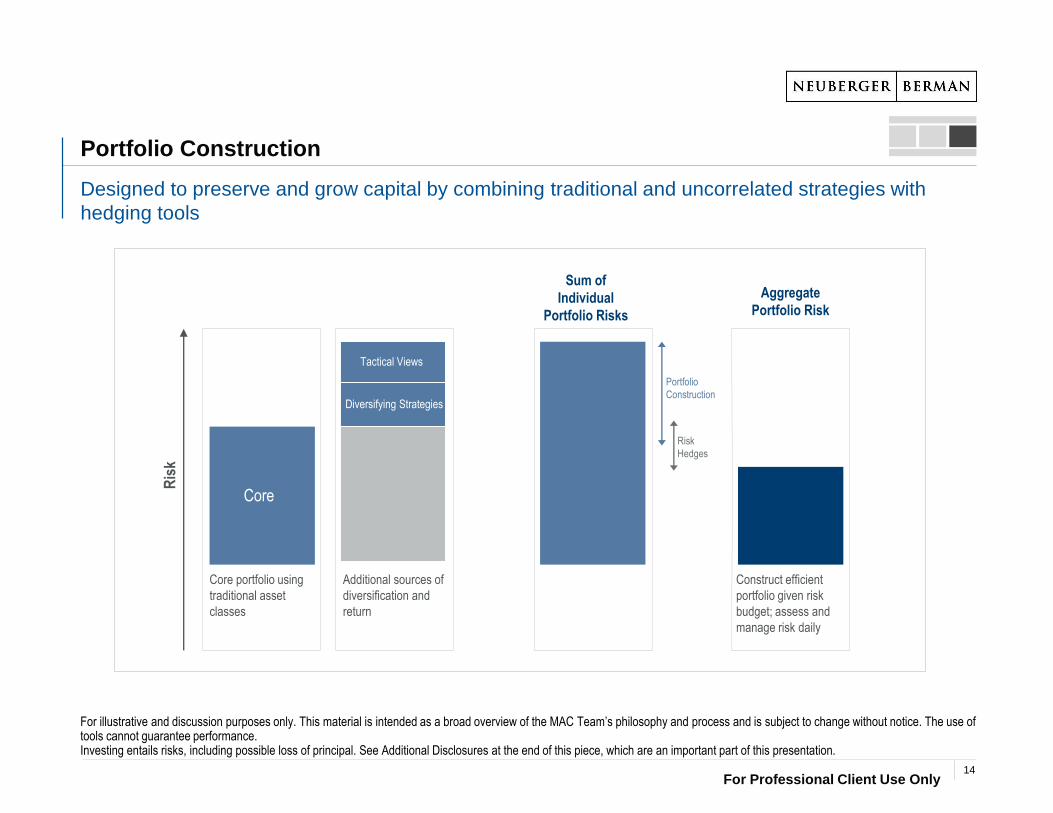

Portfolio Construction

Designed to preserve and grow capital by combining traditional and uncorrelated strategies with

hedging tools

For illustrative and discussion purposes only. This material is intended as a broad overview of the MAC Team’s philosophy and process and is subject to change without notice. The use of tools cannot guarantee performance. Investing entails risks, including possible loss of principal. See Additional Disclosures at the end of this piece, which are an important part of this presentation.

Core portfolio using

traditional asset

classes

Sum of

Individual

Portfolio Risks

Ris

k

Core

Additional sources of

diversification and

return

Construct efficient

portfolio given risk

budget; assess and

manage risk daily

Aggregate

Portfolio Risk

Tactical Views

Diversifying Strategies

Portfolio

Construction

Risk

Hedges

14

For Professional Client Use Only

Risk Management: Portfolio Risk Monitoring & New Investments

PORTFOLIO RISK MONITORING

On an ongoing basis, the MAC Investment team will:

The MAC Investment team rigorously and continuously reviews portfolio risk considerations and new

investment ideas

NEW INVESTMENT RISK ASSESSMENT

Prior to implementing a new investment idea or discretionary trade,

the MAC investment team will:

Monitor portfolio exposures and risks daily

Run stress tests on packaged and custom scenarios

Discuss portfolio risk at weekly MAC Risk meeting

Ensure appropriate risk is deployed across underlying

sleeves and overlays

Utilize proprietary framework to assess and manage

equity and credit market risk

Analyze historical performance and risk metrics

Conduct forward-looking scenario analysis and stress testing

Assess trade weights, instruments and operational

considerations

Evaluate risk contributions from potential trades

Engage Portfolio Analytics and Risk (PAR) team for an

independent assessment

ONGOING

RISK

MONITORING

15

For Professional Client Use Only

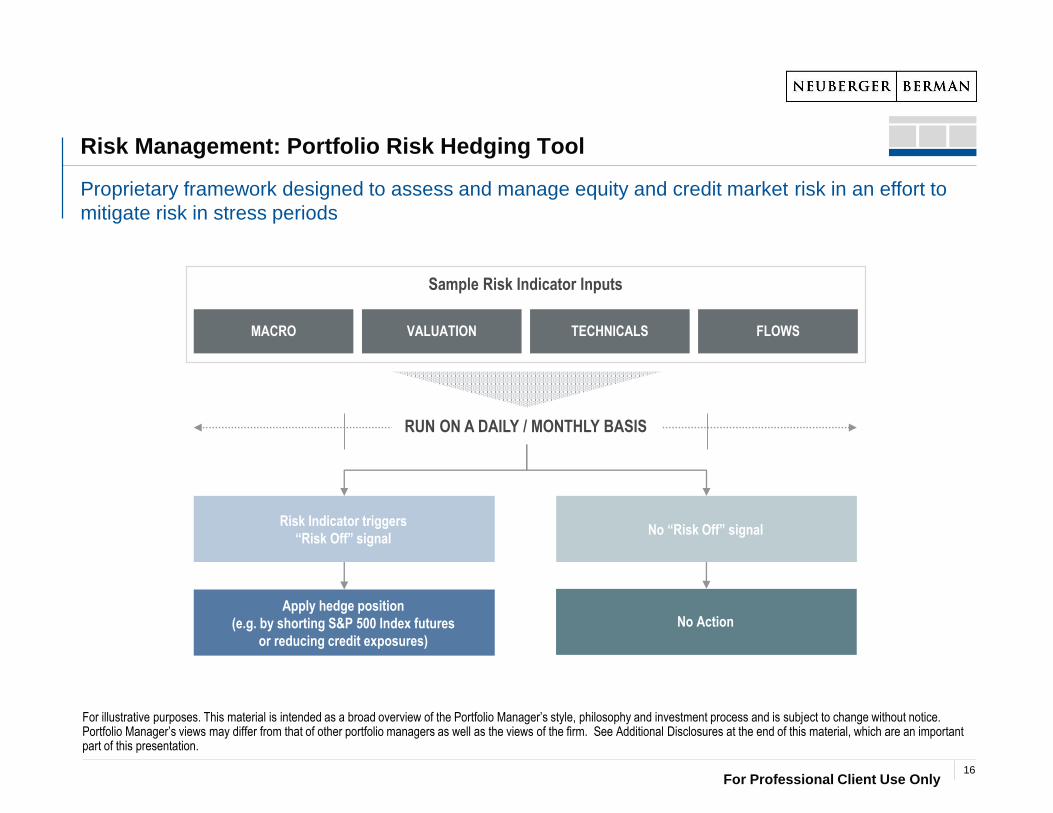

Risk Management: Portfolio Risk Hedging Tool

For illustrative purposes. This material is intended as a broad overview of the Portfolio Manager’s style, philosophy and investment process and is subject to change without notice. Portfolio Manager’s views may differ from that of other portfolio managers as well as the views of the firm. See Additional Disclosures at the end of this material, which are an important part of this presentation.

Proprietary framework designed to assess and manage equity and credit market risk in an effort to

mitigate risk in stress periods

Sample Risk Indicator Inputs

MACRO VALUATION TECHNICALS FLOWS

RUN ON A DAILY / MONTHLY BASIS

Apply hedge position

(e.g. by shorting S&P 500 Index futures

or reducing credit exposures)

Risk Indicator triggers

“Risk Off” signalNo “Risk Off” signal

No Action

16

For Professional Client Use Only

For illustrative and discussion purposes only. This material is intended as a broad overview of the MAC Team’s philosophy and process and is subject to change without notice. The use of tools cannot guarantee performance. Investing entails risks, including possible loss of principal. See Additional Disclosures at the end of this piece, which are an important part of this presentation.

Risk oversight at the security, portfolio and firm levels

Risk Management: Firm Oversight

PORTFOLIO LEVEL

• Portfolio management team utilizes

Aladdin system for overall portfolio

risk management

• Daily monitoring of risk exposures by

portfolio managers

UNDERLYING STRATEGY

• Underlying active portfolio

management teams implement

risk management by monitoring

exposures and company fundamentals

RISK & OPERATIONS

• Portfolio Analysis and Risk (PAR)

provides independent risk

oversight

• Operational Risk Committee

reviews operating processes

COMPLIANCE

• Asset Management Guideline

Oversight (AMGO) team monitors

compliance with fund investment

guidelines daily

MULTI-ASSET

CLASS GROWTH

PORTFOLIO

INVESTMENT TEAM LEVEL

FIRM LEVEL

17

PORTFOLIO CHARACTERISTICS AND PERFORMANCE

For Professional Client Use Only

-30% -20% -10% 0% 10% 20% 30%

Low Vol Global Equity

Global Equity

Investment Grade Corporate

Securitized Credit

Inflation Linked

High Yield

Emerging Markets Debt

Global Sovereign Bonds

Tactical Asset Allocation

Absolute Return Options

Alternative Risk Premia

Currency

Cash & Equivalents

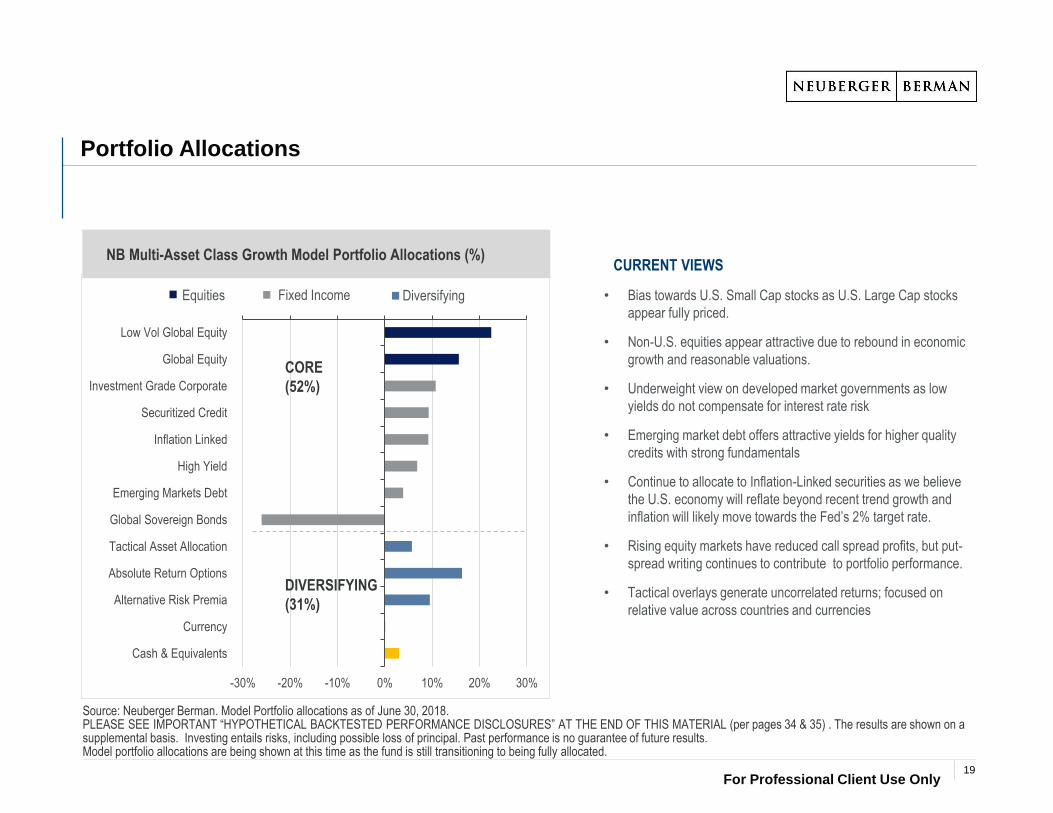

Portfolio Allocations

Source: Neuberger Berman. Model Portfolio allocations as of June 30, 2018. PLEASE SEE IMPORTANT “HYPOTHETICAL BACKTESTED PERFORMANCE DISCLOSURES” AT THE END OF THIS MATERIAL (per pages 34 & 35) . The results are shown on a supplemental basis. Investing entails risks, including possible loss of principal. Past performance is no guarantee of future results.Model portfolio allocations are being shown at this time as the fund is still transitioning to being fully allocated.

NB Multi-Asset Class Growth Model Portfolio Allocations (%)

Equities DiversifyingFixed Income

CURRENT VIEWS

CORE

(52%)

DIVERSIFYING

(31%)

• Bias towards U.S. Small Cap stocks as U.S. Large Cap stocks

appear fully priced.

• Non-U.S. equities appear attractive due to rebound in economic

growth and reasonable valuations.

• Underweight view on developed market governments as low

yields do not compensate for interest rate risk

• Emerging market debt offers attractive yields for higher quality

credits with strong fundamentals

• Continue to allocate to Inflation-Linked securities as we believe

the U.S. economy will reflate beyond recent trend growth and

inflation will likely move towards the Fed’s 2% target rate.

• Rising equity markets have reduced call spread profits, but put-

spread writing continues to contribute to portfolio performance.

• Tactical overlays generate uncorrelated returns; focused on

relative value across countries and currencies

19

For Professional Client Use Only

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

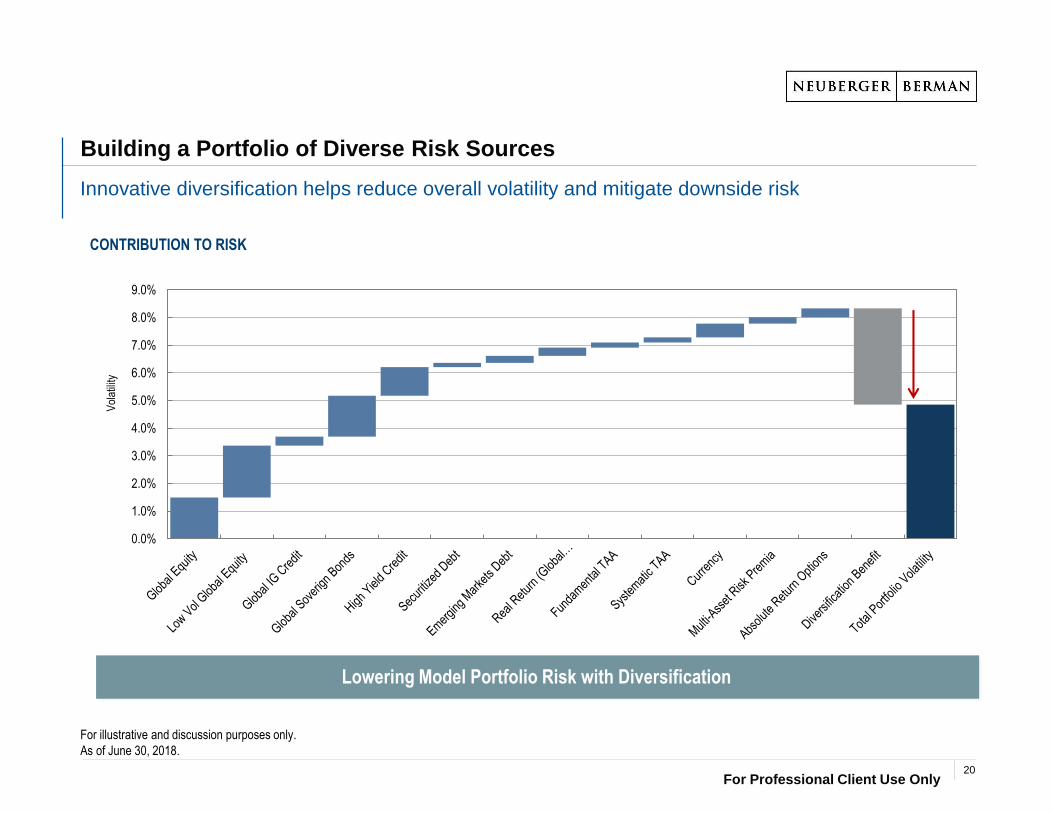

Building a Portfolio of Diverse Risk Sources

For illustrative and discussion purposes only.

As of June 30, 2018.

Lowering Model Portfolio Risk with Diversification

Innovative diversification helps reduce overall volatility and mitigate downside risk

CONTRIBUTION TO RISK

Vol

atili

ty

20

For Professional Client Use Only

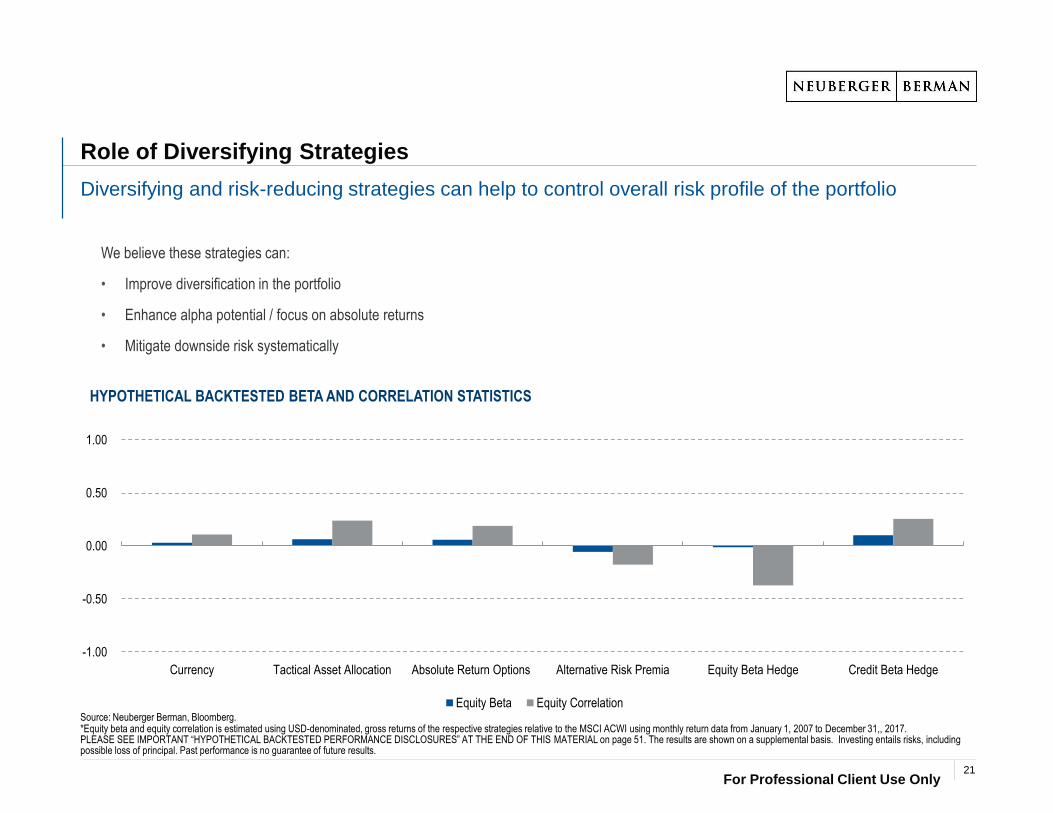

Role of Diversifying Strategies

Diversifying and risk-reducing strategies can help to control overall risk profile of the portfolio

We believe these strategies can:

• Improve diversification in the portfolio

• Enhance alpha potential / focus on absolute returns

• Mitigate downside risk systematically

HYPOTHETICAL BACKTESTED BETA AND CORRELATION STATISTICS

Source: Neuberger Berman, Bloomberg.*Equity beta and equity correlation is estimated using USD-denominated, gross returns of the respective strategies relative to the MSCI ACWI using monthly return data from January 1, 2007 to December 31,, 2017.PLEASE SEE IMPORTANT “HYPOTHETICAL BACKTESTED PERFORMANCE DISCLOSURES” AT THE END OF THIS MATERIAL on page 51. The results are shown on a supplemental basis. Investing entails risks, including possible loss of principal. Past performance is no guarantee of future results.

-1.00

-0.50

0.00

0.50

1.00

Currency Tactical Asset Allocation Absolute Return Options Alternative Risk Premia Equity Beta Hedge Credit Beta Hedge

Equity Beta Equity Correlation

21

For Professional Client Use Only

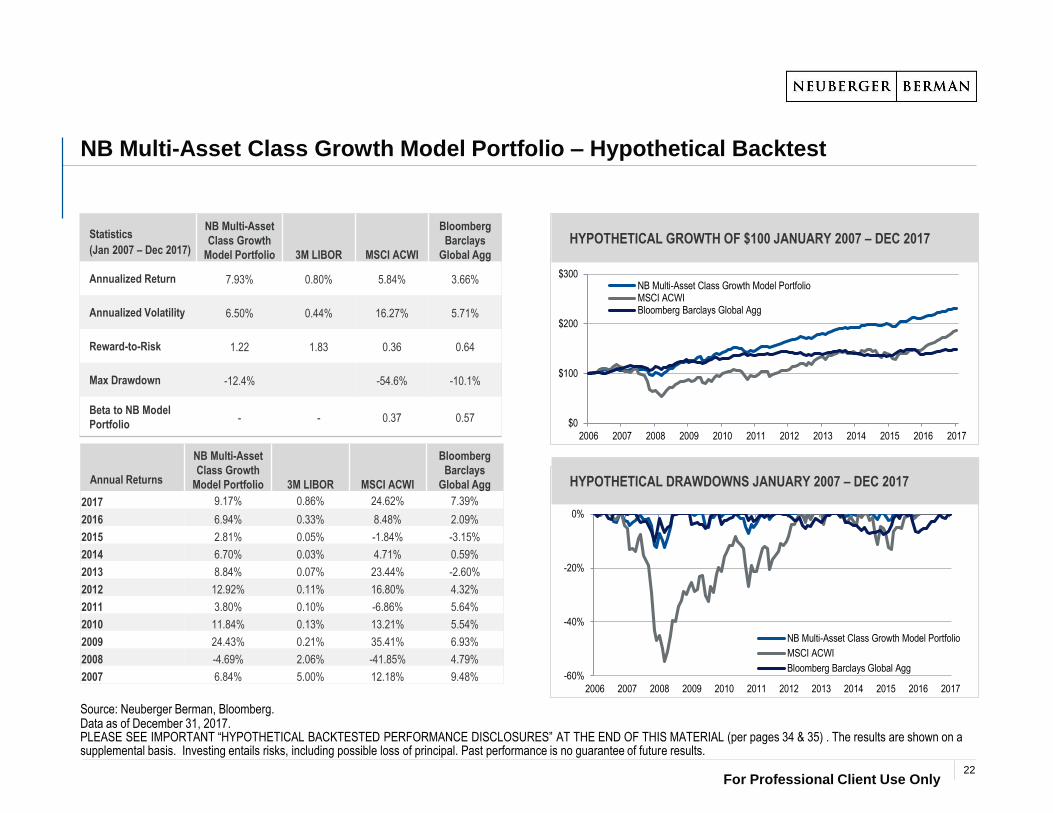

NB Multi-Asset Class Growth Model Portfolio – Hypothetical Backtest

HYPOTHETICAL DRAWDOWNS JANUARY 2007 – DEC 2017

Source: Neuberger Berman, Bloomberg.Data as of December 31, 2017.PLEASE SEE IMPORTANT “HYPOTHETICAL BACKTESTED PERFORMANCE DISCLOSURES” AT THE END OF THIS MATERIAL (per pages 34 & 35) . The results are shown on a supplemental basis. Investing entails risks, including possible loss of principal. Past performance is no guarantee of future results.

HYPOTHETICAL GROWTH OF $100 JANUARY 2007 – DEC 2017Statistics

(Jan 2007 – Dec 2017)

NB Multi-Asset

Class Growth

Model Portfolio 3M LIBOR MSCI ACWI

Bloomberg

Barclays

Global Agg

Annualized Return 7.93% 0.80% 5.84% 3.66%

Annualized Volatility 6.50% 0.44% 16.27% 5.71%

Reward-to-Risk 1.22 1.83 0.36 0.64

Max Drawdown -12.4% -54.6% -10.1%

Beta to NB Model

Portfolio- - 0.37 0.57 $0

$100

$200

$300

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

NB Multi-Asset Class Growth Model PortfolioMSCI ACWIBloomberg Barclays Global Agg

Annual Returns

NB Multi-Asset

Class Growth

Model Portfolio 3M LIBOR MSCI ACWI

Bloomberg

Barclays

Global Agg

2017 9.17% 0.86% 24.62% 7.39%

2016 6.94% 0.33% 8.48% 2.09%

2015 2.81% 0.05% -1.84% -3.15%

2014 6.70% 0.03% 4.71% 0.59%

2013 8.84% 0.07% 23.44% -2.60%

2012 12.92% 0.11% 16.80% 4.32%

2011 3.80% 0.10% -6.86% 5.64%

2010 11.84% 0.13% 13.21% 5.54%

2009 24.43% 0.21% 35.41% 6.93%

2008 -4.69% 2.06% -41.85% 4.79%

2007 6.84% 5.00% 12.18% 9.48% -60%

-40%

-20%

0%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

NB Multi-Asset Class Growth Model Portfolio

MSCI ACWI

Bloomberg Barclays Global Agg

22

For Professional Client Use Only

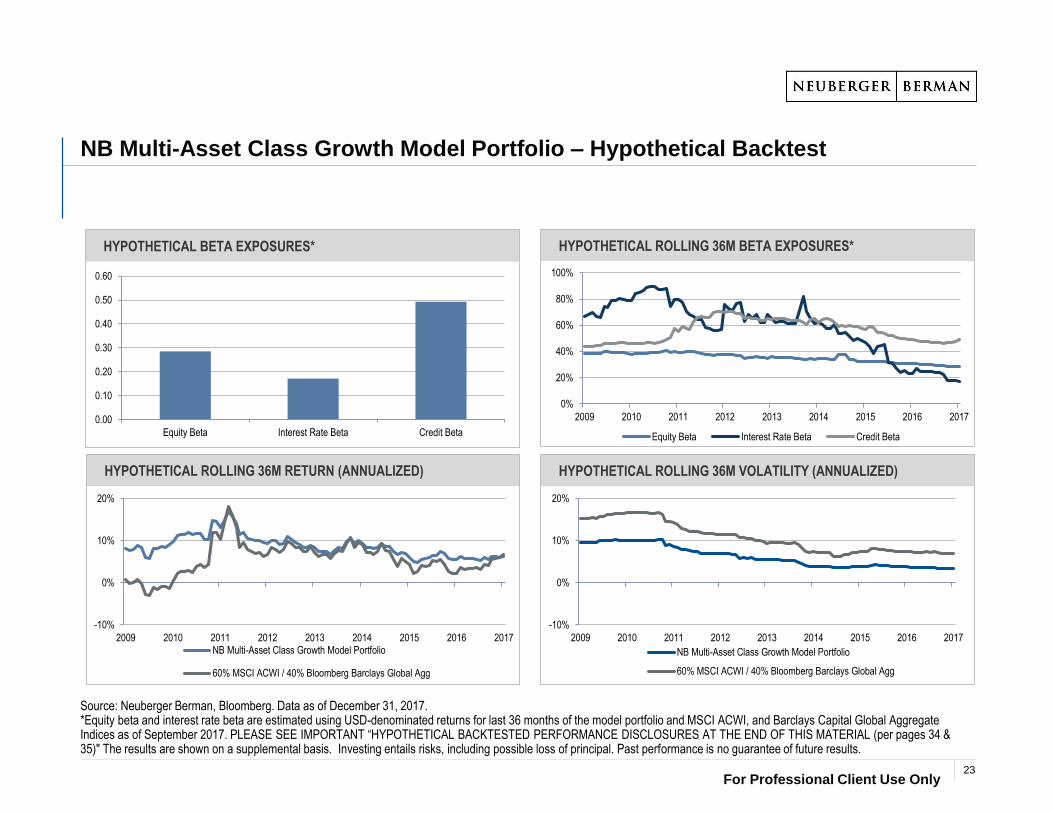

NB Multi-Asset Class Growth Model Portfolio – Hypothetical Backtest

HYPOTHETICAL BETA EXPOSURES* HYPOTHETICAL ROLLING 36M BETA EXPOSURES*

HYPOTHETICAL ROLLING 36M RETURN (ANNUALIZED) HYPOTHETICAL ROLLING 36M VOLATILITY (ANNUALIZED)

Source: Neuberger Berman, Bloomberg. Data as of December 31, 2017.*Equity beta and interest rate beta are estimated using USD-denominated returns for last 36 months of the model portfolio and MSCI ACWI, and Barclays Capital Global Aggregate Indices as of September 2017. PLEASE SEE IMPORTANT “HYPOTHETICAL BACKTESTED PERFORMANCE DISCLOSURES AT THE END OF THIS MATERIAL (per pages 34 & 35)" The results are shown on a supplemental basis. Investing entails risks, including possible loss of principal. Past performance is no guarantee of future results.

0.00

0.10

0.20

0.30

0.40

0.50

0.60

Equity Beta Interest Rate Beta Credit Beta

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 2013 2014 2015 2016 2017

Equity Beta Interest Rate Beta Credit Beta

-10%

0%

10%

20%

2009 2010 2011 2012 2013 2014 2015 2016 2017NB Multi-Asset Class Growth Model Portfolio

60% MSCI ACWI / 40% Bloomberg Barclays Global Agg

-10%

0%

10%

20%

2009 2010 2011 2012 2013 2014 2015 2016 2017

NB Multi-Asset Class Growth Model Portfolio

60% MSCI ACWI / 40% Bloomberg Barclays Global Agg

23

SOURCES OF RETURN & DIVERSIFICATION

For Professional Client Use Only

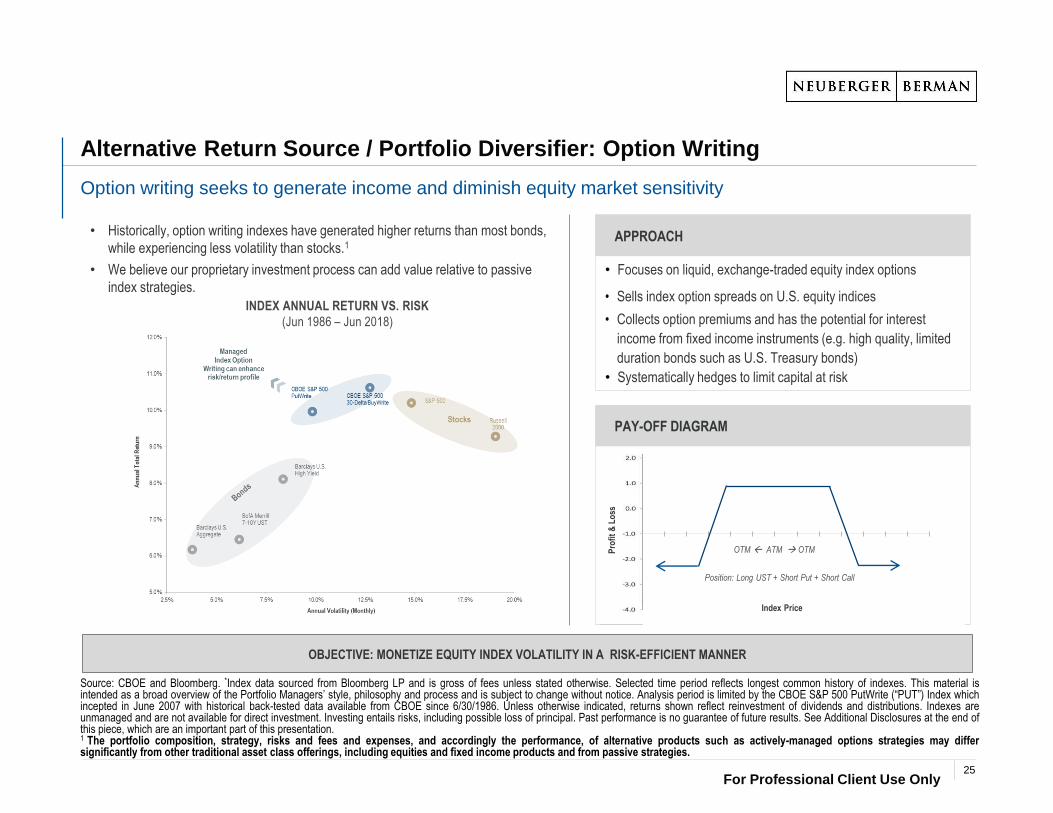

• Historically, option writing indexes have generated higher returns than most bonds,

while experiencing less volatility than stocks.1

• We believe our proprietary investment process can add value relative to passive

index strategies.

Alternative Return Source / Portfolio Diversifier: Option Writing

Option writing seeks to generate income and diminish equity market sensitivity

Source: CBOE and Bloomberg. *Index data sourced from Bloomberg LP and is gross of fees unless stated otherwise. Selected time period reflects longest common history of indexes. This material isintended as a broad overview of the Portfolio Managers’ style, philosophy and process and is subject to change without notice. Analysis period is limited by the CBOE S&P 500 PutWrite (“PUT”) Index whichincepted in June 2007 with historical back-tested data available from CBOE since 6/30/1986. Unless otherwise indicated, returns shown reflect reinvestment of dividends and distributions. Indexes areunmanaged and are not available for direct investment. Investing entails risks, including possible loss of principal. Past performance is no guarantee of future results. See Additional Disclosures at the end ofthis piece, which are an important part of this presentation.1 The portfolio composition, strategy, risks and fees and expenses, and accordingly the performance, of alternative products such as actively-managed options strategies may differsignificantly from other traditional asset class offerings, including equities and fixed income products and from passive strategies.

APPROACH

• Focuses on liquid, exchange-traded equity index options

• Sells index option spreads on U.S. equity indices

• Collects option premiums and has the potential for interest

income from fixed income instruments (e.g. high quality, limited

duration bonds such as U.S. Treasury bonds)

• Systematically hedges to limit capital at risk

PAY-OFF DIAGRAM

OTM ATM OTM

Position: Long UST + Short Put + Short Call

Index PriceP

rofi

t &

Lo

ss

INDEX ANNUAL RETURN VS. RISK

(Jun 1986 – Jun 2018)

OBJECTIVE: MONETIZE EQUITY INDEX VOLATILITY IN A RISK-EFFICIENT MANNER

25

For Professional Client Use Only

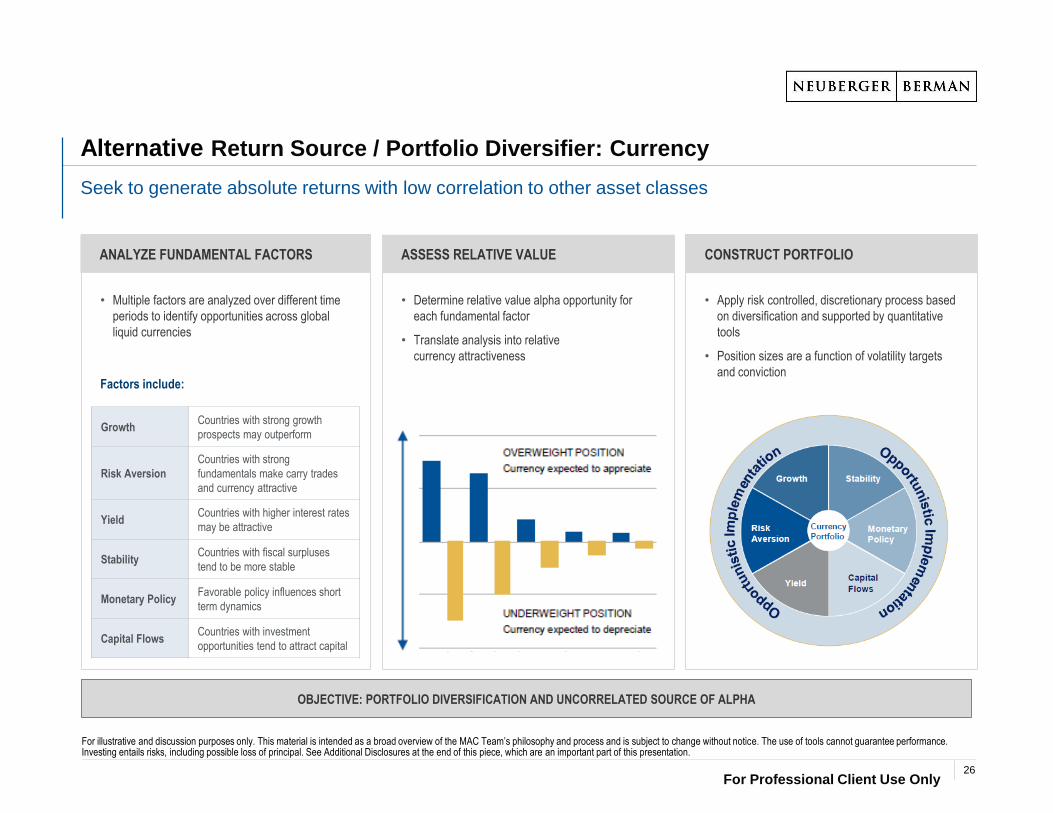

Alternative Return Source / Portfolio Diversifier: Currency

Seek to generate absolute returns with low correlation to other asset classes

For illustrative and discussion purposes only. This material is intended as a broad overview of the MAC Team’s philosophy and process and is subject to change without notice. The use of tools cannot guarantee performance. Investing entails risks, including possible loss of principal. See Additional Disclosures at the end of this piece, which are an important part of this presentation.

• Determine relative value alpha opportunity for

each fundamental factor

• Translate analysis into relative

currency attractiveness

• Multiple factors are analyzed over different time

periods to identify opportunities across global

liquid currencies

• Apply risk controlled, discretionary process based

on diversification and supported by quantitative

tools

• Position sizes are a function of volatility targets

and conviction

GrowthCountries with strong growth

prospects may outperform

Risk Aversion

Countries with strong

fundamentals make carry trades

and currency attractive

YieldCountries with higher interest rates

may be attractive

StabilityCountries with fiscal surpluses

tend to be more stable

Monetary PolicyFavorable policy influences short

term dynamics

Capital FlowsCountries with investment

opportunities tend to attract capital

CONSTRUCT PORTFOLIO ANALYZE FUNDAMENTAL FACTORS ASSESS RELATIVE VALUE

Factors include:

OBJECTIVE: PORTFOLIO DIVERSIFICATION AND UNCORRELATED SOURCE OF ALPHA

26

For Professional Client Use Only

0%

5%

10%

15%

20%E

q-V

al

FI-

Val

FX

-Val

Eq-

…

FI-

Mom FX

-…

Com

-…

Eq-

Car

FI-

Car

FX

-Car

Com

-…

Eq-

Liq

Com

-…

Value

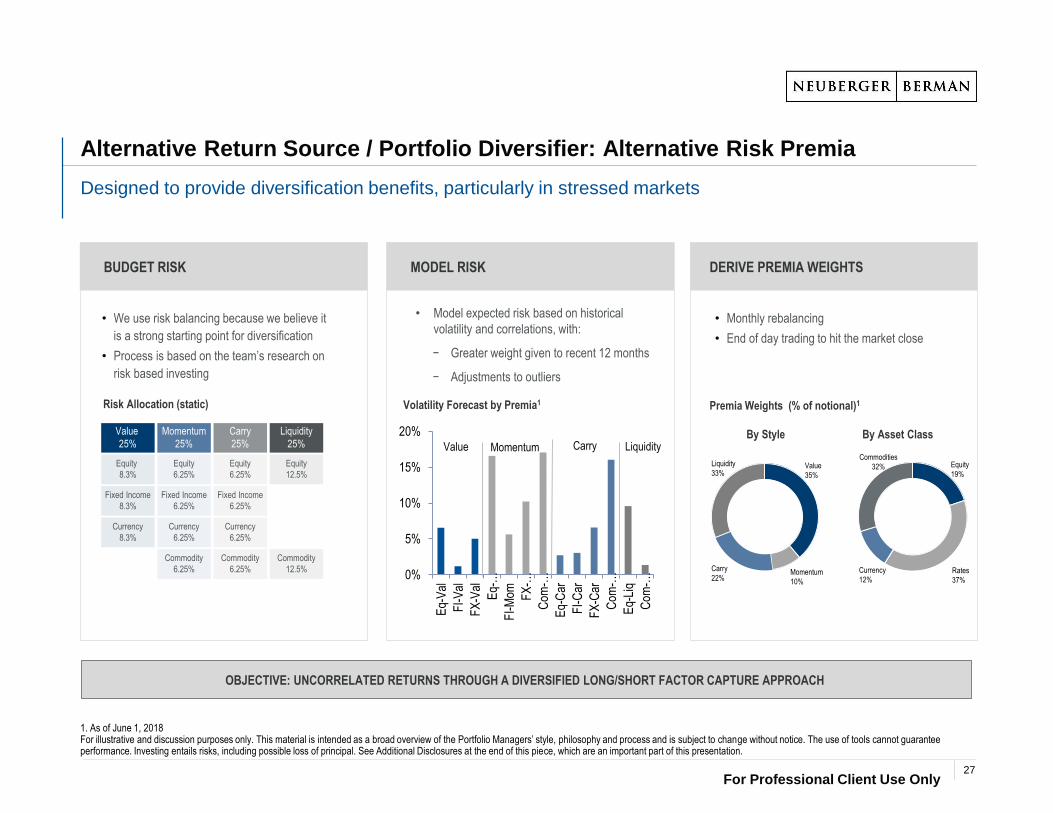

Alternative Return Source / Portfolio Diversifier: Alternative Risk Premia

Designed to provide diversification benefits, particularly in stressed markets

1. As of June 1, 2018For illustrative and discussion purposes only. This material is intended as a broad overview of the Portfolio Managers’ style, philosophy and process and is subject to change without notice. The use of tools cannot guarantee performance. Investing entails risks, including possible loss of principal. See Additional Disclosures at the end of this piece, which are an important part of this presentation.

BUDGET RISK MODEL RISK DERIVE PREMIA WEIGHTS

• Monthly rebalancing

• End of day trading to hit the market close

• We use risk balancing because we believe it

is a strong starting point for diversification

• Process is based on the team’s research on

risk based investing

Value

25%

Momentum

25%

Carry

25%

Liquidity

25%

Equity

8.3%

Equity

6.25%

Equity

6.25%

Equity

12.5%

Fixed Income

8.3%

Fixed Income

6.25%

Fixed Income

6.25%

Currency

8.3%

Currency

6.25%

Currency

6.25%

Commodity

6.25%

Commodity

6.25%

Commodity

12.5%

• Model expected risk based on historical

volatility and correlations, with:

− Greater weight given to recent 12 months

− Adjustments to outliers

LiquidityMomentum Carry

Volatility Forecast by Premia1Risk Allocation (static) Premia Weights (% of notional)1

By Style By Asset Class

Liquidity

33%Value

35%

Carry

22%Momentum

10%

Equity

19%

Currency

12%Rates

37%

Commodities

32%

OBJECTIVE: UNCORRELATED RETURNS THROUGH A DIVERSIFIED LONG/SHORT FACTOR CAPTURE APPROACH

27

SUMMARY AND TERMS

For Professional Client Use Only

Why Neuberger Berman Multi-Asset Class Growth Fund?

Flexible strategy combines traditional and non-traditional sources of alpha to generate growth

Portfolio Objectives

Cash1 +5%

Annualized

Volatility

Leveraging the depth and breadth of Neuberger Berman

Flexibility to invest across asset classes and regions

Core approach enhanced with tactical views, diversifying strategies and

alternative sources of alpha and income

Proprietary risk framework and beta hedges seek to mitigate volatility

and preserve capital

Global Strategy

Multiple, Diversified Sources of Alpha

Collaborative Research-Driven Process

Focus On Risk Management

A track record of multi-asset class investing

Seasoned Investment Team

1

2

3

4

5

Annualized

Return

6-10%

Beta 0.3-0.4To MSCI ACWI

1. Cash defined by 3M T-Bill Index

29

For Professional Client Use OnlyFor Professional Client Use Only

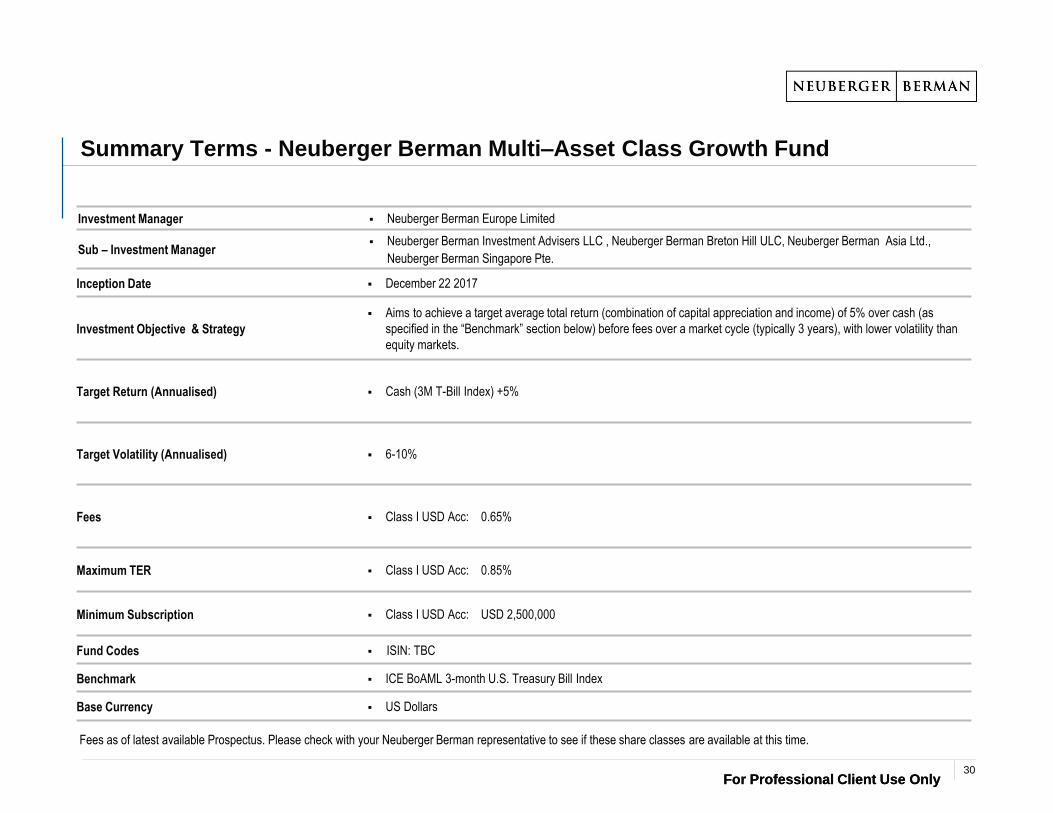

Summary Terms - Neuberger Berman Multi–Asset Class Growth Fund

Investment Manager Neuberger Berman Europe Limited

Sub – Investment Manager Neuberger Berman Investment Advisers LLC , Neuberger Berman Breton Hill ULC, Neuberger Berman Asia Ltd.,

Neuberger Berman Singapore Pte.

Inception Date December 22 2017

Investment Objective & Strategy

Aims to achieve a target average total return (combination of capital appreciation and income) of 5% over cash (as

specified in the “Benchmark” section below) before fees over a market cycle (typically 3 years), with lower volatility than

equity markets.

Target Return (Annualised) Cash (3M T-Bill Index) +5%

Target Volatility (Annualised) 6-10%

Fees Class I USD Acc: 0.65%

Maximum TER Class I USD Acc: 0.85%

Minimum Subscription Class I USD Acc: USD 2,500,000

Fund Codes ISIN: TBC

Benchmark ICE BoAML 3-month U.S. Treasury Bill Index

Base Currency US Dollars

Fees as of latest available Prospectus. Please check with your Neuberger Berman representative to see if these share classes are available at this time.

30

APPENDIX

CONFIDENTIAL

For Professional Client Use Only

Confidential Presentation

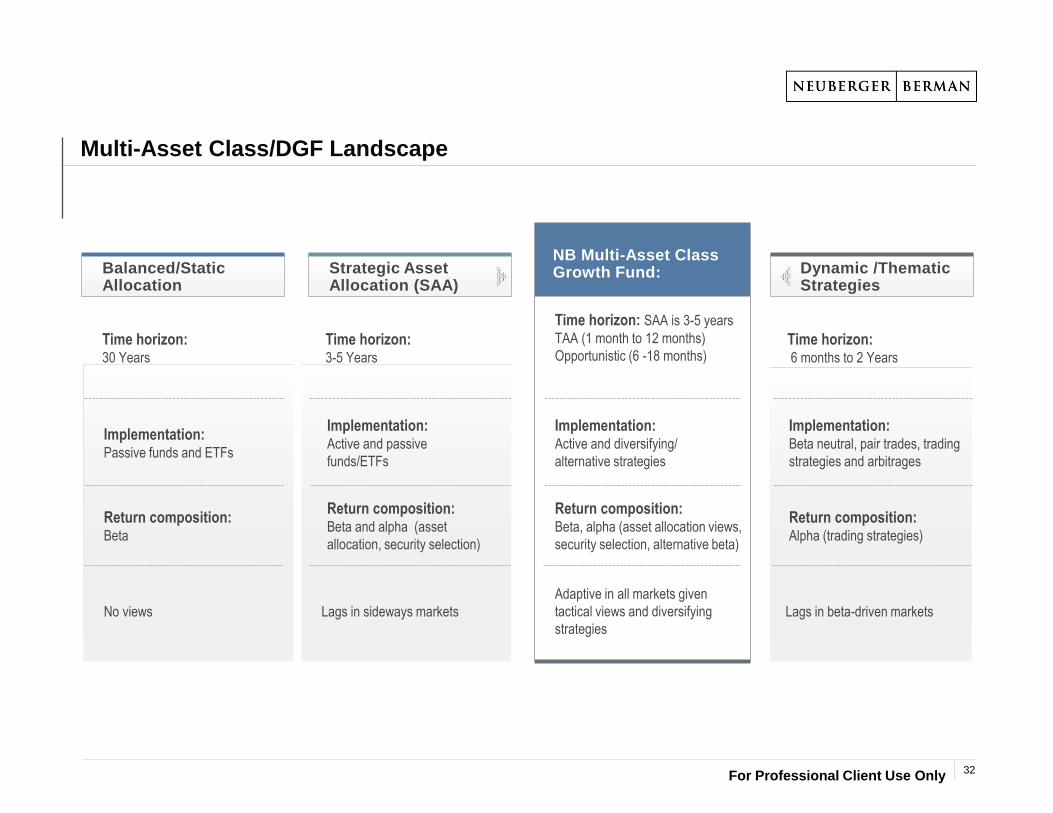

Multi-Asset Class/DGF Landscape

Balanced/Static Allocation

AssessmentStrategic Asset Allocation (SAA)

AssessmentDynamic /Thematic Strategies

Return composition: Beta, alpha (asset allocation views,

security selection, alternative beta)

Time horizon:30 Years

Implementation: Passive funds and ETFs

Implementation: Active and passive

funds/ETFs

Implementation: Active and diversifying/

alternative strategies

Implementation: Beta neutral, pair trades, trading

strategies and arbitrages

Return composition: Beta

Return composition: Beta and alpha (asset

allocation, security selection)

Return composition: Alpha (trading strategies)

Time horizon: SAA is 3-5 years

TAA (1 month to 12 months)

Opportunistic (6 -18 months)

Lags in beta-driven markets

Time horizon: 3-5 Years

Time horizon: 6 months to 2 Years

No views Lags in sideways markets

Adaptive in all markets given

tactical views and diversifying

strategies

NB Multi-Asset Class Growth Fund:

For Professional Client Use Only32

For Professional Client Use Only

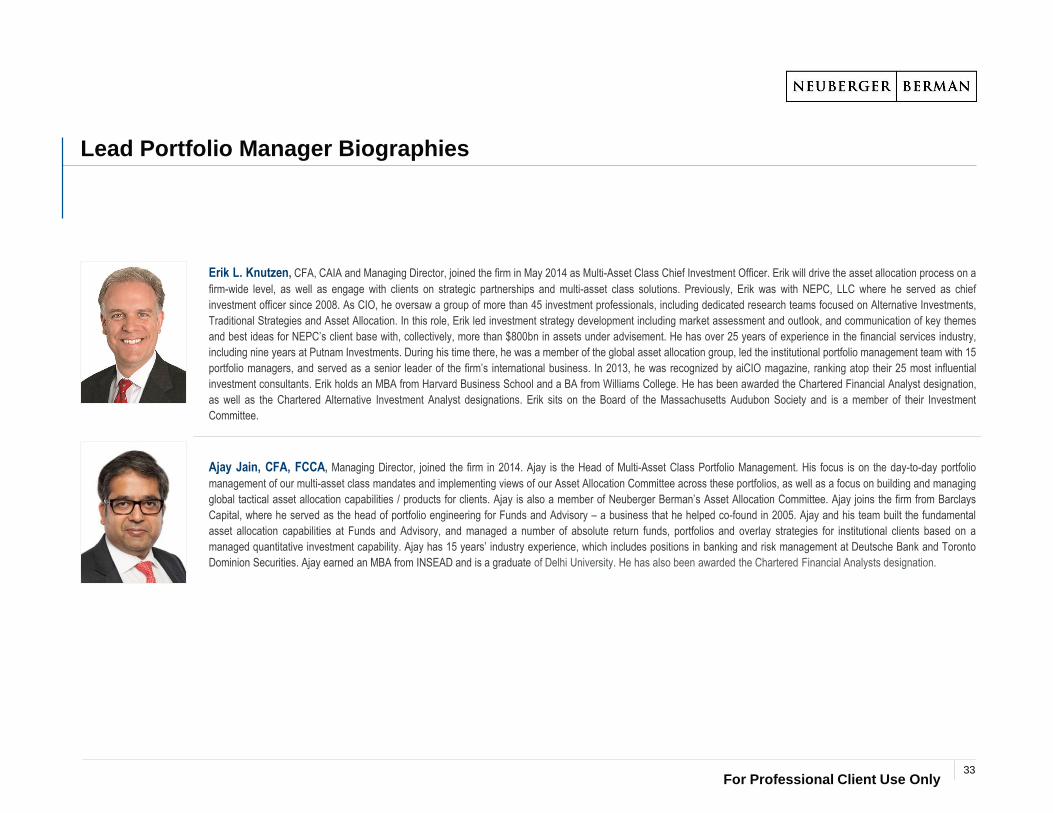

Lead Portfolio Manager Biographies

Erik L. Knutzen, CFA, CAIA and Managing Director, joined the firm in May 2014 as Multi-Asset Class Chief Investment Officer. Erik will drive the asset allocation process on a

firm-wide level, as well as engage with clients on strategic partnerships and multi-asset class solutions. Previously, Erik was with NEPC, LLC where he served as chief

investment officer since 2008. As CIO, he oversaw a group of more than 45 investment professionals, including dedicated research teams focused on Alternative Investments,

Traditional Strategies and Asset Allocation. In this role, Erik led investment strategy development including market assessment and outlook, and communication of key themes

and best ideas for NEPC’s client base with, collectively, more than $800bn in assets under advisement. He has over 25 years of experience in the financial services industry,

including nine years at Putnam Investments. During his time there, he was a member of the global asset allocation group, led the institutional portfolio management team with 15

portfolio managers, and served as a senior leader of the firm’s international business. In 2013, he was recognized by aiCIO magazine, ranking atop their 25 most influential

investment consultants. Erik holds an MBA from Harvard Business School and a BA from Williams College. He has been awarded the Chartered Financial Analyst designation,

as well as the Chartered Alternative Investment Analyst designations. Erik sits on the Board of the Massachusetts Audubon Society and is a member of their Investment

Committee.

Ajay Jain, CFA, FCCA, Managing Director, joined the firm in 2014. Ajay is the Head of Multi-Asset Class Portfolio Management. His focus is on the day-to-day portfolio

management of our multi-asset class mandates and implementing views of our Asset Allocation Committee across these portfolios, as well as a focus on building and managing

global tactical asset allocation capabilities / products for clients. Ajay is also a member of Neuberger Berman’s Asset Allocation Committee. Ajay joins the firm from Barclays

Capital, where he served as the head of portfolio engineering for Funds and Advisory – a business that he helped co-found in 2005. Ajay and his team built the fundamental

asset allocation capabilities at Funds and Advisory, and managed a number of absolute return funds, portfolios and overlay strategies for institutional clients based on a

managed quantitative investment capability. Ajay has 15 years’ industry experience, which includes positions in banking and risk management at Deutsche Bank and Toronto

Dominion Securities. Ajay earned an MBA from INSEAD and is a graduate of Delhi University. He has also been awarded the Chartered Financial Analysts designation.

33

For Professional Client Use Only

Risk Considerations

Market Risk: The risk of a change in the value of a position as a result of underlying market factors, including among other things, the overall performance of companies

and the market perception of the global economy.

Liquidity Risk: The risk that the Fund may be unable to sell an investment readily at its fair market value. In extreme market conditions this can affect the Fund’s ability

to meet redemption requests upon demand.

Derivatives Risk: The Fund is permitted to use certain types of financial derivative instruments (including certain complex instruments). This may increase the Fund’s

leverage significantly which may cause large variations in the value of your share. [(Investors should note that the Fund may achieve its investment objective by

investing principally in Financial Derivative Instruments (FDI). There are certain investment risks that apply in relation to the use of FDI.)]

Interest Rate Risk: The risk of interest rate movements affecting the value of fixed-rate bonds.

Credit Risk: The risk that bond issuers may fail to meet their interest repayments, or repay debt, resulting in temporary or permanent losses to the Fund.

Model Risk: The investment strategy of a Portfolio using a quantitative investment approach is rules based and model-driven. Therefore, it would not necessarily result

in a security being sold because that security’s issuer was in financial trouble or defaulted, or had its credit rating downgraded, unless such indicators are tracked by the

investment strategy of that Portfolio. There is no guarantee that the investment strategy of such a Portfolio will meet the purpose for which it was designed.

Counterparty Risk: The risk that a counterparty will not fulfil its payment obligation for a trade, contract or other transaction, on the due date.

Operational Risk: The risk of direct or indirect loss resulting from inadequate or failed processes, people and systems including those relating to the safekeeping of

assets or from external events.

Currency Risk: Investors who subscribe in a currency other than the base currency of the Fund are exposed to currency risk. Fluctuations in exchange rates may affect

the return on investment. The past performance shown is based on the share class to which this presentation relates. If the currency of this share class is different from

your local currency, then you should be aware that due to exchange rate fluctuations the performance shown may increase or decrease if converted into your local

currency.

34

For Professional Client Use Only

Hypothetical Backtested Performance Disclosures

The hypothetical performance results included in this material are for a back-tested model portfolio and are shown for illustrative purposes only. Neuberger Berman calculated the hypothetical results by

running a variety of model portfolios on a back-tested basis using the methodology described herein. The results are shown on a supplemental basis and do not represent the performance of any Neuberger

Berman managed account or product and do not reflect the fees and expenses associated with managing a portfolio.

Model NB Multi-Asset Class Growth Portfolio:

Model Presented: Model NB Multi-Asset Class Growth

Period: January 1, 2007 – December 31, 2017

Data Sources: Bloomberg; Neuberger Berman

Hypothetical Backtest Methodology:

The back-tested returns presented reflect hypothetical performance an investor would have obtained had it invested in the manner shown and does not represents returns that any investor actually attained.

Certain of the assumptions have been made for modeling purposes and are unlikely to be realized. No representation or warranty is made as to the reasonableness of the assumptions made or that all

assumptions used in achieving the returns have been stated or fully considered. Changes in the assumptions may have a material impact on the hypothetical returns presented.

The information presented is based upon the following hypothetical assumptions: Returns are gross of taxes and fees. Where live track records have been presented, returns are net of transaction costs;

where index data has been used, returns exclude the impact of transaction costs. The presented hypothetical returns have been simulated by creating a blend of strategies, rebalanced monthly (see next

page for the back-tested constituents and time periods).

There may be material differences between the hypothetical back-tested performance results and actual results achieved by actual accounts. Back-tested model performance is hypothetical and does not

represent the performance of actual accounts. Hypothetical performance has certain inherent limitations. Unlike actual investment performance, hypothetical results do not represent actual trading and

accordingly the performance results may have under- or over-compensated for the impact, if any, that certain economic or other market factors, such as lack of liquidity or price fluctuations, might have had

on the investment decision-making process or results if assets were actually being managed. Hypothetical performance may also not accurately reflect the impact, if any, of other material economic and

market factors, or the impact of financial risk and the ability to withstand losses. Hypothetical performance results are also subject to the fact that they are generally designed with the benefit of hindsight. As a

result, the back-tested models theoretically may be changed from time to time to obtain more favorable performance results. In addition, the results are based, in part, on hypothetical assumptions. Certain of

the assumptions have been made for modeling purposes and may not have been realized in the actual management of accounts. No representation or warranty is made as to the reasonableness of the

assumptions made or that all assumptions used in achieving the hypothetical results have been stated or fully considered. Changes in the model assumptions may have a material impact on the hypothetical

returns presented. There are frequently material differences between hypothetical performance results and actual results achieved by any investment strategy. Neuberger Berman did not manage any

accounts in this manner reflected in the models during the backtested time periods shown.

Unless otherwise indicated, results shown reflect reinvestment of any dividends and distributions. The hypothetical performance figures are shown gross of fees, which do not reflect the deduction of

investment advisory fees and other expense. If such fees and expense were reflected, returns referenced would be lower. Advisory fees are described in Part 2 of Neuberger Berman’s Form ADV. A client's

return will be reduced by the advisory fees and any other expenses it may incur in the management of its account. The deduction of fees has a compounding effect on performance results. For example,

assume Neuberger Berman achieves a 10% annual return prior to the deduction of fees each year for a period of ten years. If a fee of 1% of assets under management were charged and deducted from the

returns, the resulting compounded annual return would be reduced to 8.91%. Please note that there is no comparable reduction from the indices for the fees.

Model NB Multi-Asset Class Growth Portfolio

35

For Professional Client Use Only

Hypothetical Backtested Performance Disclosures

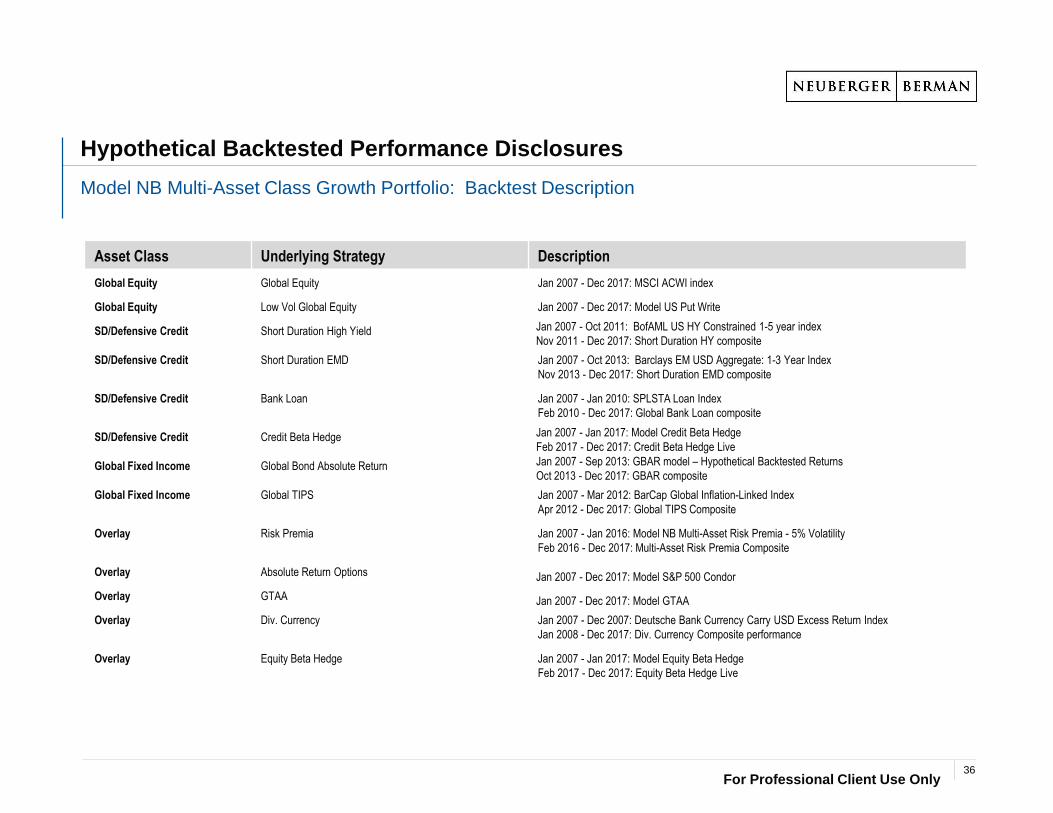

Model NB Multi-Asset Class Growth Portfolio: Backtest Description

Asset Class Underlying Strategy Description

Global Equity Global Equity Jan 2007 - Dec 2017: MSCI ACWI index

Global Equity Low Vol Global Equity Jan 2007 - Dec 2017: Model US Put Write

SD/Defensive Credit Short Duration High Yield Jan 2007 - Oct 2011: BofAML US HY Constrained 1-5 year index

Nov 2011 - Dec 2017: Short Duration HY composite

SD/Defensive Credit Short Duration EMD Jan 2007 - Oct 2013: Barclays EM USD Aggregate: 1-3 Year Index

Nov 2013 - Dec 2017: Short Duration EMD composite

SD/Defensive Credit Bank Loan Jan 2007 - Jan 2010: SPLSTA Loan Index

Feb 2010 - Dec 2017: Global Bank Loan composite

SD/Defensive Credit Credit Beta Hedge Jan 2007 - Jan 2017: Model Credit Beta Hedge

Feb 2017 - Dec 2017: Credit Beta Hedge Live

Global Fixed Income Global Bond Absolute Return Jan 2007 - Sep 2013: GBAR model – Hypothetical Backtested Returns

Oct 2013 - Dec 2017: GBAR composite

Global Fixed Income Global TIPS Jan 2007 - Mar 2012: BarCap Global Inflation-Linked Index

Apr 2012 - Dec 2017: Global TIPS Composite

Overlay Risk Premia Jan 2007 - Jan 2016: Model NB Multi-Asset Risk Premia - 5% Volatility

Feb 2016 - Dec 2017: Multi-Asset Risk Premia Composite

Overlay Absolute Return Options Jan 2007 - Dec 2017: Model S&P 500 Condor

Overlay GTAA Jan 2007 - Dec 2017: Model GTAA

Overlay Div. Currency Jan 2007 - Dec 2007: Deutsche Bank Currency Carry USD Excess Return Index

Jan 2008 - Dec 2017: Div. Currency Composite performance

Overlay Equity Beta Hedge Jan 2007 - Jan 2017: Model Equity Beta Hedge

Feb 2017 - Dec 2017: Equity Beta Hedge Live

36

For Professional Client Use Only

The hypothetical performance results included in this material are backtested model portfolios and are shown for illustrative purposes only. Neuberger Berman calculated the hypothetical results by running a variety ofmodel portfolios on a backtested basis using the methodology described herein. The results are shown on a supplemental basis and do not represent the performance of any Neuberger Berman managed account orproduct and do not reflect the fees and expenses associated with managing a portfolio.

Models Presented:

Model Iron Condor: Reflects a hypothetical backed tested model portfolio based on the performance of selling put and call option spreads on the S&P 500.

Time Periods: January 1, 2007 – December 31, 2017 for Model S&P 500 Iron Condor.

Hypothetical Backtest Methodology:The option strategy back-testing platform is designed to estimate historical performance of portfolios that implement systematic option writing strategies. Models support a multitude of variables including option strategy,e.g., put writing or call writing, underlying exposure (index or stock), tenor, moneyness, risk management parameters and collateral investments. While models incorporate different parameter sets, they adhere to aconsistent structure across all back-tested model scenarios and our model architecture is such that returns are estimated independent of account size.

All models rely on a Black-Scholes pricing to estimate option prices based on historical implied volatility surfaces. We compile daily implied volatility surfaces from exchange listed option price and/or option impliedvolatility data available from external data providers including the Chicago Board of Options Exchange (“CBOE”) and Bloomberg LP. Additional inputs for option pricing (dividends, risk-free rate, etc.) are sourced fromBloomberg LP.

Daily implied volatility surfaces allow models to price weekly expiration dates even though weekly option expirations may not have been actively traded on an exchange over the full history of a model back-test. Modelsmethodically allocate options across weekly expirations to promote diversification across expiration dates and are assumed to settle on each Friday consistent with current option market practices.

Exposures are rebalanced on a daily basis at the close of each trading day. Daily model rebalancing adjusts portfolio exposures and rolls (covers and writes) option positions consistent with specified risk managementtargets. Options are rolled in a manner that seeks to preserve exposures across multiple expiration dates, and risk management targets, e.g., option delta and or moneyness, are set at the inception of a back-test andapplied over its full history. All trading is assumed to be transacted at market closing prices derived from closing implied volatility levels and includes estimates for transaction costs. Option strike prices follow standardoption market conventions unique to the underlying index/security. Models may round up, down or to the nearest strike price when selecting option to write.

Hypothetical option models are fully collateralized such that model portfolios are assumed to hold fixed income securities whose aggregate market values are greater than or equal to the aggregate notional exposure ofthe options. Collateral is assumed to be invested in a widely followed index(s) that approximates the performance of short-term U.S. Treasuries. Models may vary from actual strategy performance due to assignmentrisk for American style options, exchanged traded option contract availability, intra-day trading and differences in transaction costs (implicit and explicit).

There may be material differences between the hypothetical back-tested performance results and actual results achieved by actual accounts. Back-tested model performance is hypothetical and does not represent theperformance of actual accounts. Hypothetical performance has certain inherent limitations. Unlike actual investment performance, hypothetical results do not represent actual trading and accordingly the performanceresults may have under- or over-compensated for the impact, if any, that certain economic or other market factors, such as lack of liquidity or price fluctuations, might have had on the investment decision-makingprocess or results if assets were actually being managed. Hypothetical performance may also not accurately reflect the impact, if any, of other material economic and market factors, or the impact of financial risk andthe ability to withstand losses. Hypothetical performance results are also subject to the fact that they are generally designed with the benefit of hindsight. As a result, the back-tested models theoretically may bechanged from time to time to obtain more favorable performance results. In addition, the results are based, in part, on hypothetical assumptions. Certain of the assumptions have been made for modeling purposes andmay not have been realized in the actual management of accounts. No representation or warranty is made as to the reasonableness of the assumptions made or that all assumptions used in achieving the hypotheticalresults have been stated or fully considered. Changes in the model assumptions may have a material impact on the hypothetical returns presented. There are frequently material differences between hypotheticalperformance results and actual results achieved by any investment strategy. Neuberger Berman did not manage any accounts in this manner reflected in the models during the backtested time periods shown.

Unless otherwise indicated, results shown reflect reinvestment of any dividends and distributions. Unless otherwise indicated, the hypothetical performance figures are shown gross of fees, which do not reflect thededuction of investment advisory fees, transaction costs and other expenses. If such fees and expense were reflected, returns referenced would be lower. Advisory fees are described in Part 2 of Neuberger Berman’sForm ADV. A client's return will be reduced by the advisory fees and any other expenses it may incur in the management of its account. The deduction of fees has a compounding effect on performance results. Forexample, assume Neuberger Berman achieves a 10% annual return prior to the deduction of fees each year for a period of ten years. If a fee of 1% of assets under management were charged and deducted from thereturns, the resulting compounded annual return would be reduced to 8.91%. Please note that there is no comparable reduction from the indices for the fees.

Hypothetical Backtested Performance Disclosures

Model S&P 500 Iron Condor

37

For Professional Client Use Only

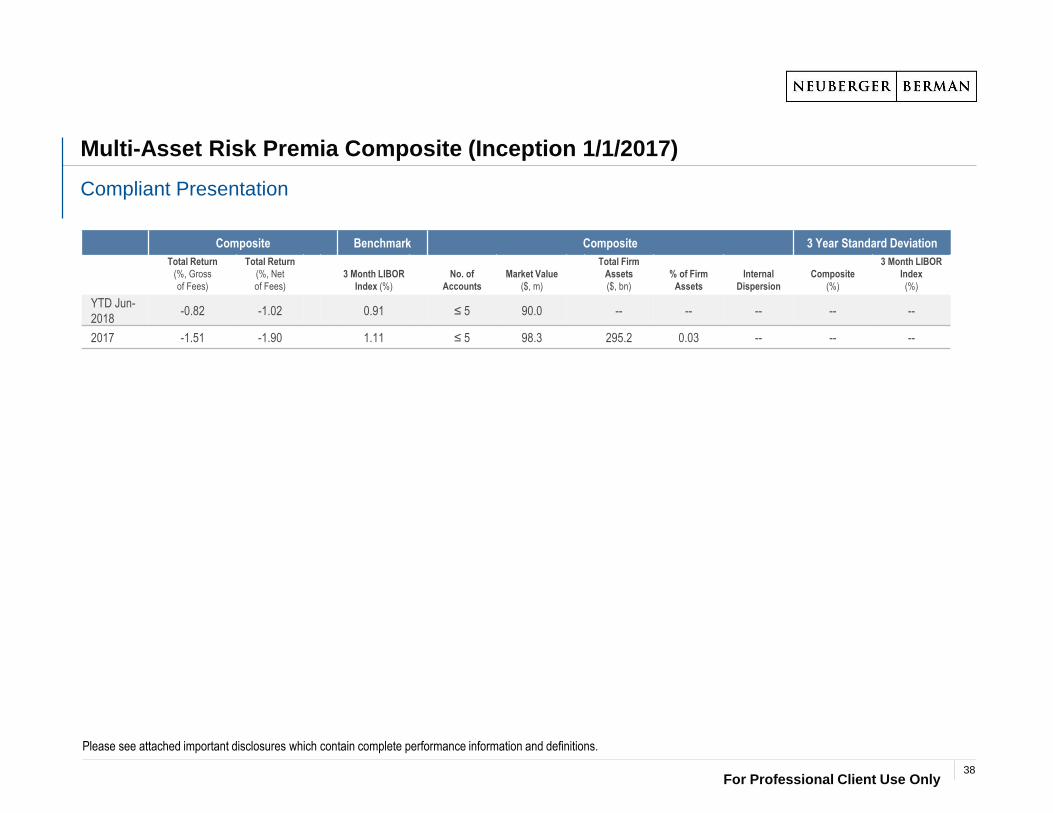

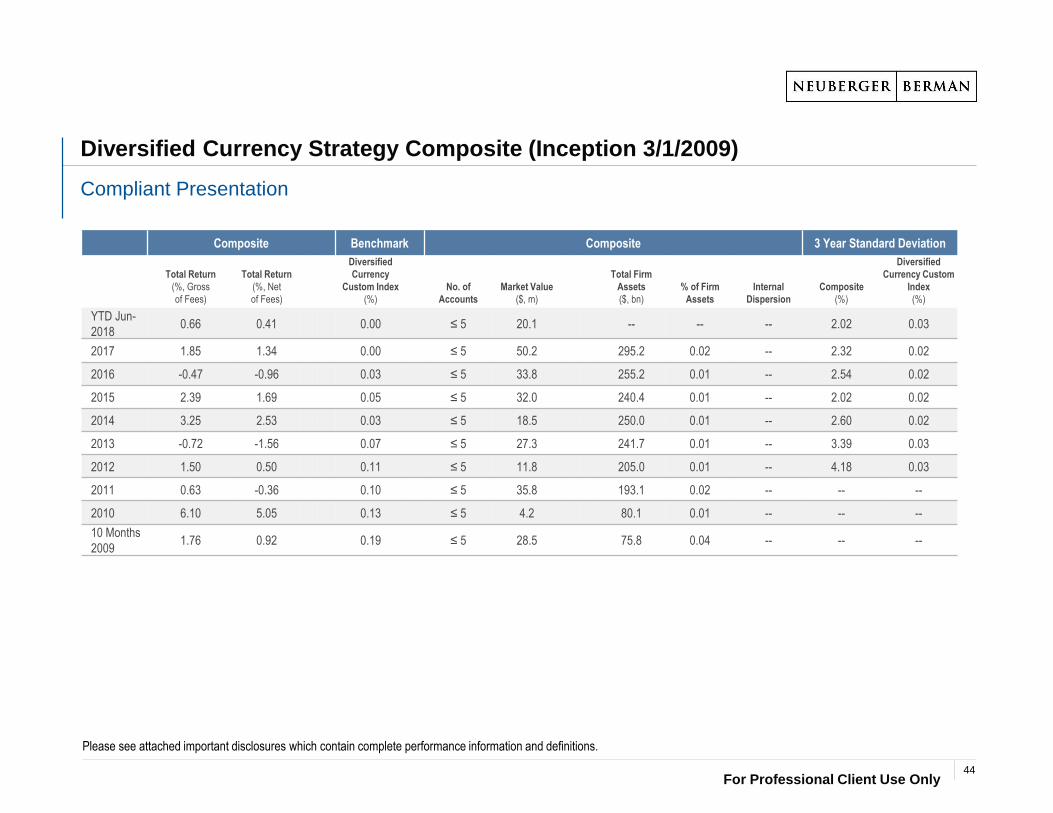

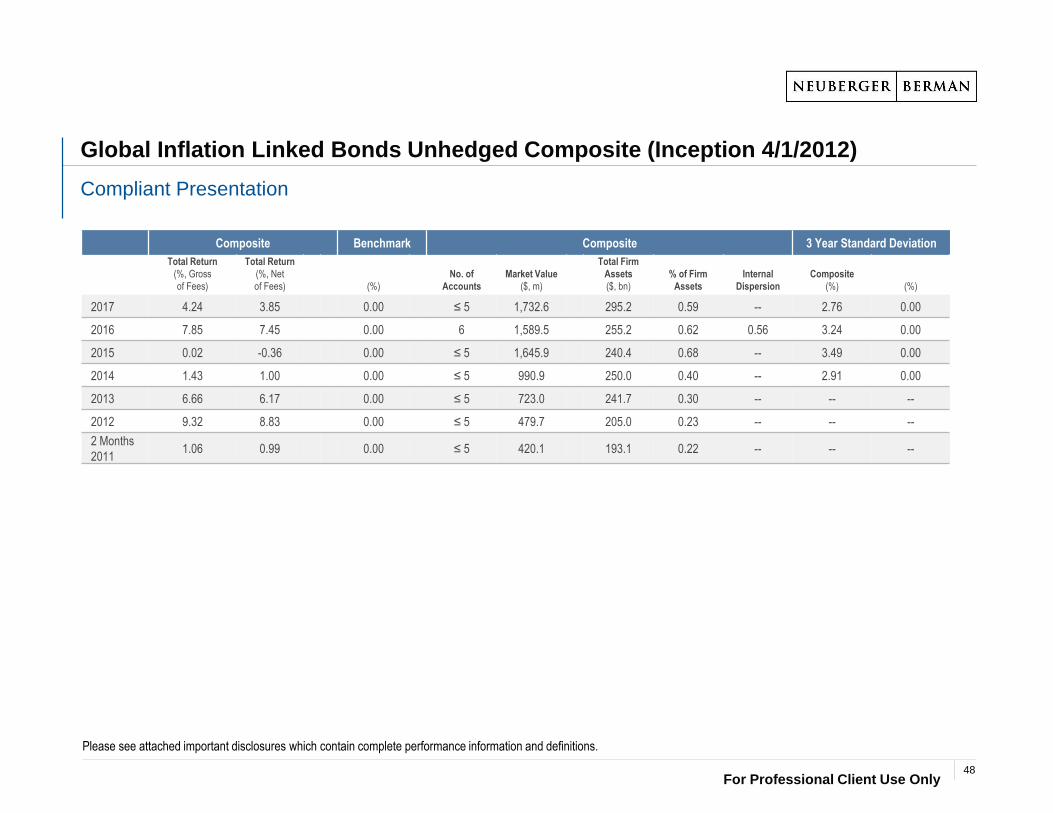

Multi-Asset Risk Premia Composite (Inception 1/1/2017)

Compliant Presentation

Please see attached important disclosures which contain complete performance information and definitions.

Composite Benchmark Composite 3 Year Standard Deviation

Total Return

(%, Gross

of Fees)

Total Return

(%, Net

of Fees)

3 Month LIBOR

Index (%)

No. of

Accounts

Market Value

($, m)

Total Firm

Assets

($, bn)

% of Firm

Assets

Internal

Dispersion

Composite

(%)

3 Month LIBOR

Index

(%)

YTD Jun-

2018-0.82 -1.02 0.91 ≤ 5 90.0 -- -- -- -- --

2017 -1.51 -1.90 1.11 ≤ 5 98.3 295.2 0.03 -- -- --

38

For Professional Client Use Only

Multi-Asset Risk Premia Composite

Investment Performance Disclosure Statement

Compliance Statement• Neuberger Berman Group LLC ("NB", "Neuberger Berman" or the "Firm") claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in

compliance with the GIPS® standards. Neuberger Berman was independently verified for the period January 1, 2011 to December 31, 2016. The GIPS® firm definition was redefined effective January 1,2011. For prior periods there were two separate firms for GIPS® firm definition purposes and such firms were independently verified for the periods January 1, 1997 to December 31, 2010 and January1, 1996 to December 31, 2010, respectively. Verification assesses whether (1) the firm has complied with all the composite construction requirements of the GIPS® standards on a firm-wide basis and(2) the firm's policies and procedures are designed to calculate and present performance in compliance with the GIPS® standards. Verification does not ensure the accuracy of any specific compositepresentation. The verification reports are available upon request.

Definition of the Firm• The firm is currently defined for GIPS® purposes as Neuberger Berman Group LLC, ("NB", "Neuberger Berman" or the "Firm"), and includes the following subsidiaries: Neuberger Berman Investment

Advisers LLC, Neuberger Berman Europe Ltd., Neuberger Berman Asia Ltd., Neuberger Berman East Asia Ltd., Neuberger Berman Singapore Pte. Ltd., Neuberger Berman Taiwan Ltd, NeubergerBerman Australia Pty. Ltd., Neuberger Berman Trust Company N.A., Neuberger Berman Trust Company of Delaware N.A. and NB Alternatives Advisers LLC.

Policies• Policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request.Composite Description• The Multi-Asset Class Risk Premia Composite (the "Composite") represents the performance of all fee-paying Multi-Asset Class Risk Premia portfolios managed on a fully discretionary basis by the

Quant and Multi-Asset Class team.The Multi-Asset Risk Premia strategy offers exposure to a multi-asset, long/short portfolio of risk premia spanning four styles (Value, Momentum, Carry, and Liquidity) and four asset classes (Equity, Fixed Income, Currencies, Commodities. The strategy targets total volatility of 5% and given the long/short construction of many of the risk premia, as well as the diversification among them, the strategy has the potential to deliver attractive absolute returns across a variety of market environments, with low to even negative correlation to traditional asset classes.The Composite creation and performance inception date is January 2017. A complete list of Neuberger Berman's composites is available upon request.

Primary Benchmark Description

Reporting Currency• Valuations are computed and performance is reported in U.S. Dollars.Fees• Portfolios in the Composite use an all - inclusive fee schedule which includes investment advisory fees, trading expenses, custody fees, and other administrative fees.• Composite Gross of Fee returns are the return on investments reduced by any trading expenses incurred during the period. Composite Net of Fee returns are the Gross of Fee returns reduced by

investment advisory fees (including Performance Based Fees and Carried Interest).Fee Schedule• The annual investment advisory fee, generally payable quarterly, is as follows: 0.40%. Internal Dispersion• Internal dispersion is calculated using the asset-weighted standard deviation of annual gross returns of those portfolios that were in the composite for the entire year. Internal dispersion is not calculated if

the composite does not contain at least 6 portfolios for the entire year.Annualized Standard Deviation• The three-year annualized standard deviation measures the variability of the composite and the benchmark returns over the preceding 36-month period. The standard deviation is not required for periods

prior to 2011.

39

For Professional Client Use Only

Hypothetical Backtested Performance DisclosuresThe hypothetical performance results included in this material are backtested model portfolios and are shown for illustrative purposes only. Neuberger Berman calculated the hypothetical results by running a variety of model portfolios on a backtested basis using the methodology described herein. The results are shown on a supplemental basis and do not reflect the fees and expenses associated with managing a portfolio. The models assume a minimum $25 million investment with no cash allocations and monthly rebalancing.

Models Presented:

Model NB Multi-Asset Risk Premia - 5% Volatility (“Model NB MARP”): Reflects a hypothetical backed tested model portfolio that blends the performance of the individual risk premia that comprise the Model

NB MARP with a risk-balancing weighting assigned to each of the 13 alternative risk premia.

Model Equally-Weighted Alternative Risk Premia (“Model Equal Weight”): Reflects a hypothetical backed tested model portfolio that blends the performance of the individual risk premia that comprise the

Model NB MARP with a weighting assigned to each of the 13 alternative risk premia. The returns are then scaled by a constant so that the annualized volatility of the return series is equal to that of the Model NB

MARP.

Model Individual Risk Premia: 13 Individual Risk Premia Models from the categories of value, momentum, carry and liquidity. Reflects 13 individual hypothetical backed tested model portfolios using a rules-based

methodology that are subsequently combined to develop the Model NB MARP and Model Equal Weight portfolios.

Time Periods: January 1, 2005 – April 30, 2018 for Model NB MARP and Model Equal Weight. January 1, 2000 – April 30, 2018 for Model Individual Risk Premia.

Hypothetical Backtest Methodology:The simulated portfolios were constructed by determining a risk budget for the underlying assets and then applying a risk-balanced framework to determine portfolio weights. The risk budget was determined by identifying common risk premia from multiple assets, then bundling “similar” strategies into respective risk premia buckets. Risk budgeting was then applied at both the risk premia level as well as within each bucket, at the strategy level. The risk of each constituent asset was defined using historical data with more weight assigned to recent data (i.e. exponentially weighted with 1 year half life). To calculate the covariance matrix, we use an expanding data set with at least 5 years of data. Some shrinkage methods are also applied at this stage. The correlation matrix is a combination of 1) a standard correlation matrix and 2) a correlation matrix that averages correlations both within the asset classes and also across asset classes. The portfolio weights were derived by allocating equal risk to each asset class and to each asset within the asset class, and subsequently determining the portfolio weights to each asset that would provide for such a distribution of risk budget. After forming the portfolio, the next period’s asset returns obtained from Bloomberg are multiplied by the respective portfolio weights to get the next period's portfolio return. For certain period of time the backtested data reflects the returns of one or more Credit Suisse Index or Index Premia obtained from Bloomberg. The Credit Suisse Index/Premia is based upon the substantial similar methodology as utilized for the NB Model backtests. There may be differences between the NB Model backtests and Credit Suisse Index/Premia data as a result of the differences between the models and indexes/index premia, including the treatment of cash and timing of execution prices (NB Models use intra day execution prices whereas Credit Suisse Index/Premia data is based upon end of day pricing) . For purposes of clarification, regardless of the data source used for the hypothetical backtested models, all data is hypothetical backtested.

There may be material differences between the hypothetical back-tested performance results and actual results achieved by actual accounts. Back-tested model performance is hypothetical and does not represent the performance of actual accounts. Hypothetical performance has certain inherent limitations. Unlike actual investment performance, hypothetical results do not represent actual trading and accordingly the performance results may have under- or over-compensated for the impact, if any, that certain economic or other market factors, such as lack of liquidity or price fluctuations, might have had on the investment decision-making process or results if assets were actually being managed. Hypothetical performance may also not accurately reflect the impact, if any, of other material economic and market factors, or the impact of financial risk and the ability to withstand losses. Hypothetical performance results are also subject to the fact that they are generally designed with the benefit of hindsight. As a result, the back-tested models theoretically may be changed from time to time to obtain more favorable performance results. In addition, the results are based, in part, on hypothetical assumptions. Certain of the assumptions have been made for modeling purposes and may not have been realized in the actual management of accounts. No representation or warranty is made as to the reasonableness of the assumptions made or that all assumptions used in achieving the hypothetical results have been stated or fully considered. Changes in the model assumptions may have a material impact on the hypothetical returns presented. There are frequently material differences between hypothetical performance results and actual results achieved by any investment strategy. Neuberger Berman did not manage any accounts in this manner reflected in the models during the backtested time periods shown.

Unless otherwise indicated, results shown reflect reinvestment of any dividends and distributions. Unless otherwise indicated, the hypothetical performance figures are shown gross of fees, which do not reflect the deduction of investment advisory fees, transaction costs and other expenses. If such fees and expense were reflected, returns referenced would be lower. Advisory fees are described in Part 2 of Neuberger Berman’s Form ADV. A client's return will be reduced by the advisory fees and any other expenses it may incur in the management of its account. The deduction of fees has a compounding effect on performance results. For example, assume Neuberger Berman achieves a 10% annual return prior to the deduction of fees each year for a period of ten years. If a fee of 1% of assets under management were charged and deducted from the returns, the resulting compounded annual return would be reduced to 8.91%. Please note that there is no comparable reduction from the indices for the fees.

40

For Professional Client Use Only

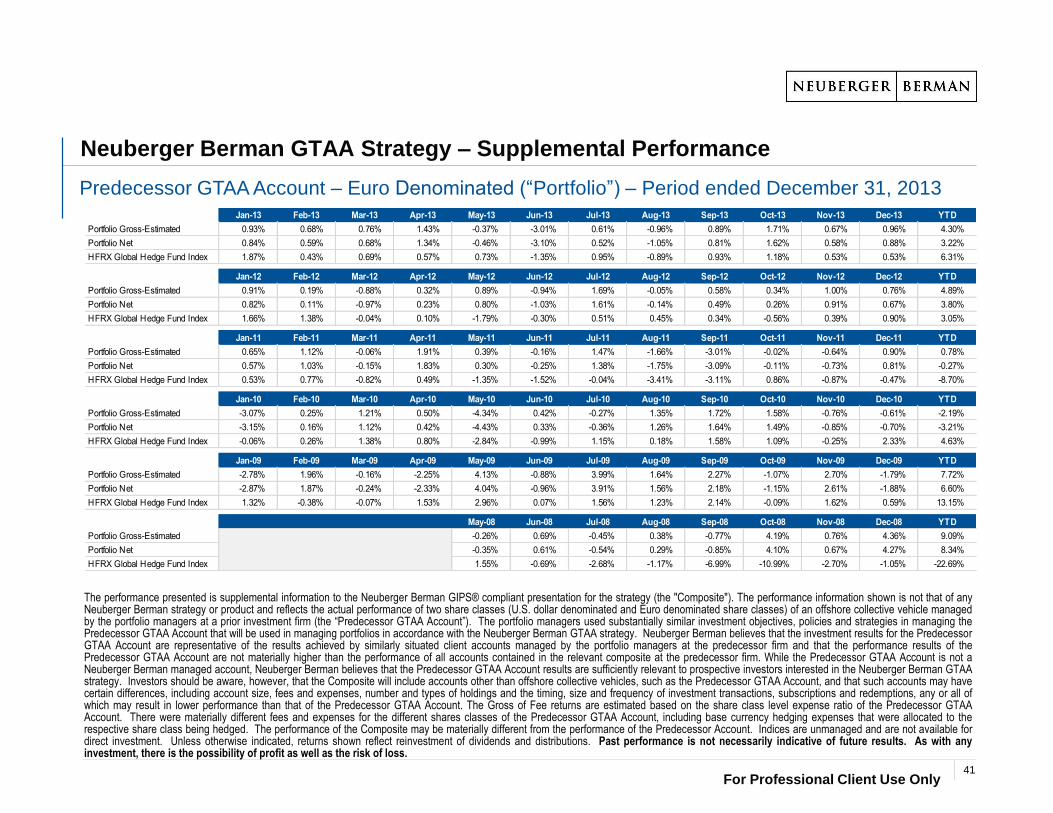

The performance presented is supplemental information to the Neuberger Berman GIPS® compliant presentation for the strategy (the "Composite"). The performance information shown is not that of anyNeuberger Berman strategy or product and reflects the actual performance of two share classes (U.S. dollar denominated and Euro denominated share classes) of an offshore collective vehicle managedby the portfolio managers at a prior investment firm (the “Predecessor GTAA Account”). The portfolio managers used substantially similar investment objectives, policies and strategies in managing thePredecessor GTAA Account that will be used in managing portfolios in accordance with the Neuberger Berman GTAA strategy. Neuberger Berman believes that the investment results for the PredecessorGTAA Account are representative of the results achieved by similarly situated client accounts managed by the portfolio managers at the predecessor firm and that the performance results of thePredecessor GTAA Account are not materially higher than the performance of all accounts contained in the relevant composite at the predecessor firm. While the Predecessor GTAA Account is not aNeuberger Berman managed account, Neuberger Berman believes that the Predecessor GTAA Account results are sufficiently relevant to prospective investors interested in the Neuberger Berman GTAAstrategy. Investors should be aware, however, that the Composite will include accounts other than offshore collective vehicles, such as the Predecessor GTAA Account, and that such accounts may havecertain differences, including account size, fees and expenses, number and types of holdings and the timing, size and frequency of investment transactions, subscriptions and redemptions, any or all ofwhich may result in lower performance than that of the Predecessor GTAA Account. The Gross of Fee returns are estimated based on the share class level expense ratio of the Predecessor GTAAAccount. There were materially different fees and expenses for the different shares classes of the Predecessor GTAA Account, including base currency hedging expenses that were allocated to therespective share class being hedged. The performance of the Composite may be materially different from the performance of the Predecessor Account. Indices are unmanaged and are not available fordirect investment. Unless otherwise indicated, returns shown reflect reinvestment of dividends and distributions. Past performance is not necessarily indicative of future results. As with anyinvestment, there is the possibility of profit as well as the risk of loss.

Predecessor GTAA Account – Euro Denominated (“Portfolio”) – Period ended December 31, 2013

Neuberger Berman GTAA Strategy – Supplemental Performance

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 YTD

Portfolio Gross-Estimated 0.93% 0.68% 0.76% 1.43% -0.37% -3.01% 0.61% -0.96% 0.89% 1.71% 0.67% 0.96% 4.30%

Portfolio Net 0.84% 0.59% 0.68% 1.34% -0.46% -3.10% 0.52% -1.05% 0.81% 1.62% 0.58% 0.88% 3.22%

HFRX Global Hedge Fund Index 1.87% 0.43% 0.69% 0.57% 0.73% -1.35% 0.95% -0.89% 0.93% 1.18% 0.53% 0.53% 6.31%

Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 YTD

Portfolio Gross-Estimated 0.91% 0.19% -0.88% 0.32% 0.89% -0.94% 1.69% -0.05% 0.58% 0.34% 1.00% 0.76% 4.89%

Portfolio Net 0.82% 0.11% -0.97% 0.23% 0.80% -1.03% 1.61% -0.14% 0.49% 0.26% 0.91% 0.67% 3.80%

HFRX Global Hedge Fund Index 1.66% 1.38% -0.04% 0.10% -1.79% -0.30% 0.51% 0.45% 0.34% -0.56% 0.39% 0.90% 3.05%

Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 YTD

Portfolio Gross-Estimated 0.65% 1.12% -0.06% 1.91% 0.39% -0.16% 1.47% -1.66% -3.01% -0.02% -0.64% 0.90% 0.78%

Portfolio Net 0.57% 1.03% -0.15% 1.83% 0.30% -0.25% 1.38% -1.75% -3.09% -0.11% -0.73% 0.81% -0.27%

HFRX Global Hedge Fund Index 0.53% 0.77% -0.82% 0.49% -1.35% -1.52% -0.04% -3.41% -3.11% 0.86% -0.87% -0.47% -8.70%

Jan-10 Feb-10 Mar-10 Apr-10 May-10 Jun-10 Jul-10 Aug-10 Sep-10 Oct-10 Nov-10 Dec-10 YTD

Portfolio Gross-Estimated -3.07% 0.25% 1.21% 0.50% -4.34% 0.42% -0.27% 1.35% 1.72% 1.58% -0.76% -0.61% -2.19%

Portfolio Net -3.15% 0.16% 1.12% 0.42% -4.43% 0.33% -0.36% 1.26% 1.64% 1.49% -0.85% -0.70% -3.21%

HFRX Global Hedge Fund Index -0.06% 0.26% 1.38% 0.80% -2.84% -0.99% 1.15% 0.18% 1.58% 1.09% -0.25% 2.33% 4.63%

Jan-09 Feb-09 Mar-09 Apr-09 May-09 Jun-09 Jul-09 Aug-09 Sep-09 Oct-09 Nov-09 Dec-09 YTD

Portfolio Gross-Estimated -2.78% 1.96% -0.16% -2.25% 4.13% -0.88% 3.99% 1.64% 2.27% -1.07% 2.70% -1.79% 7.72%

Portfolio Net -2.87% 1.87% -0.24% -2.33% 4.04% -0.96% 3.91% 1.56% 2.18% -1.15% 2.61% -1.88% 6.60%

HFRX Global Hedge Fund Index 1.32% -0.38% -0.07% 1.53% 2.96% 0.07% 1.56% 1.23% 2.14% -0.09% 1.62% 0.59% 13.15%

May-08 Jun-08 Jul-08 Aug-08 Sep-08 Oct-08 Nov-08 Dec-08 YTD

Portfolio Gross-Estimated -0.26% 0.69% -0.45% 0.38% -0.77% 4.19% 0.76% 4.36% 9.09%

Portfolio Net -0.35% 0.61% -0.54% 0.29% -0.85% 4.10% 0.67% 4.27% 8.34%

HFRX Global Hedge Fund Index 1.55% -0.69% -2.68% -1.17% -6.99% -10.99% -2.70% -1.05% -22.69%

41

For Professional Client Use Only

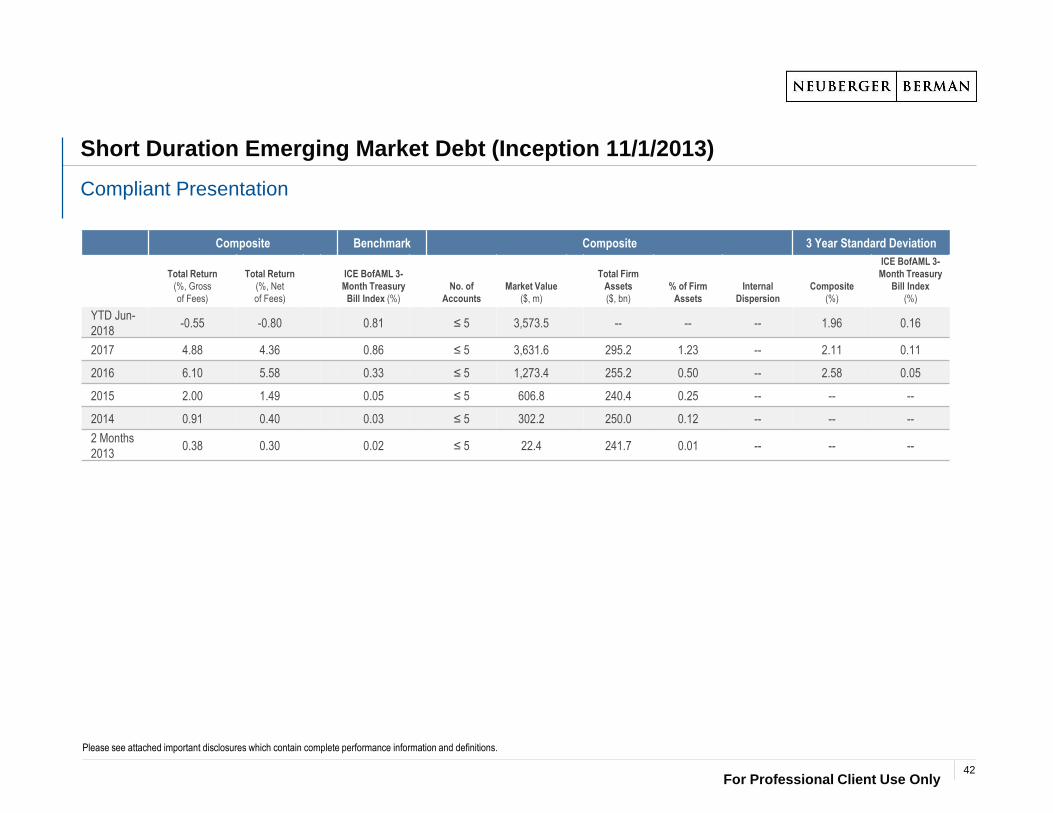

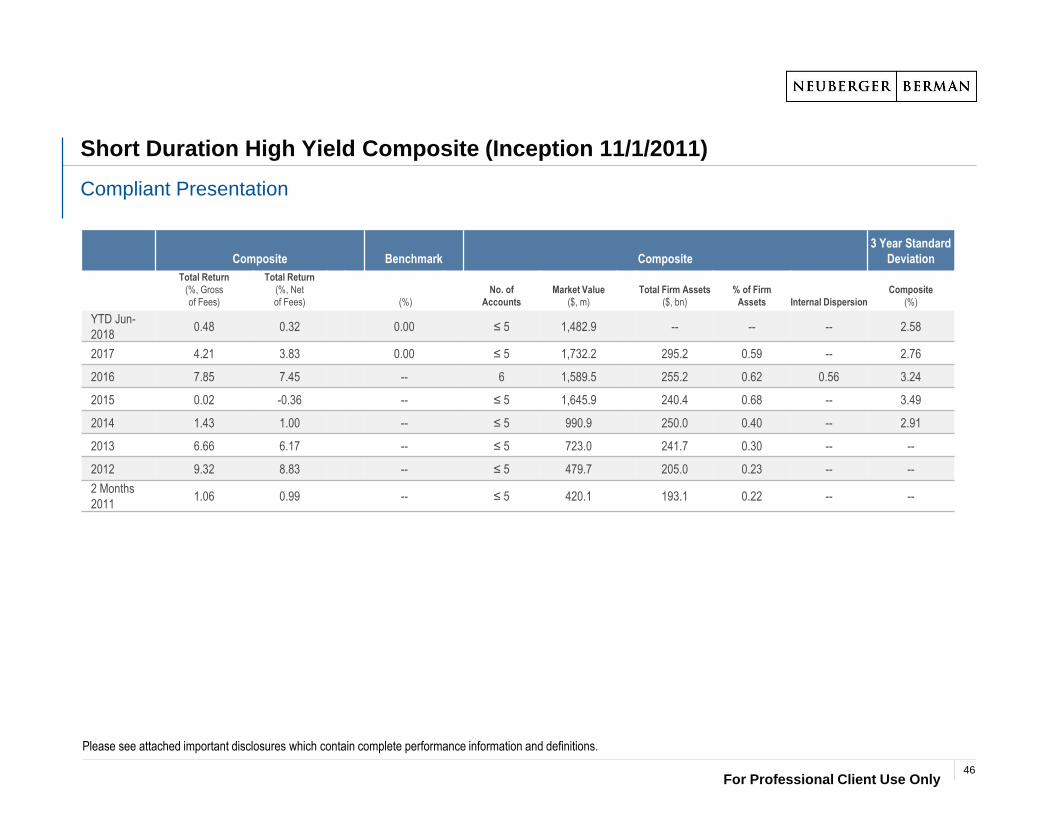

Short Duration Emerging Market Debt (Inception 11/1/2013)

Compliant Presentation

Please see attached important disclosures which contain complete performance information and definitions.

Composite Benchmark Composite 3 Year Standard Deviation

Total Return

(%, Gross

of Fees)

Total Return

(%, Net

of Fees)

ICE BofAML 3-

Month Treasury

Bill Index (%)

No. of

Accounts

Market Value

($, m)

Total Firm

Assets

($, bn)

% of Firm

Assets

Internal

Dispersion

Composite

(%)

ICE BofAML 3-

Month Treasury

Bill Index

(%)

YTD Jun-

2018-0.55 -0.80 0.81 ≤ 5 3,573.5 -- -- -- 1.96 0.16

2017 4.88 4.36 0.86 ≤ 5 3,631.6 295.2 1.23 -- 2.11 0.11

2016 6.10 5.58 0.33 ≤ 5 1,273.4 255.2 0.50 -- 2.58 0.05

2015 2.00 1.49 0.05 ≤ 5 606.8 240.4 0.25 -- -- --

2014 0.91 0.40 0.03 ≤ 5 302.2 250.0 0.12 -- -- --

2 Months

20130.38 0.30 0.02 ≤ 5 22.4 241.7 0.01 -- -- --

42

For Professional Client Use Only

Short Duration Emerging Market Debt

Investment Performance Disclosure Statement

Compliance Statement• Neuberger Berman Group LLC ("NB", "Neuberger Berman" or the "Firm") claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in

compliance with the GIPS® standards. Neuberger Berman was independently verified for the period January 1, 2011 to December 31, 2016. The GIPS® firm definition was redefined effective January 1,2011. For prior periods there were two separate firms for GIPS® firm definition purposes and such firms were independently verified for the periods January 1, 1997 to December 31, 2010 and January1, 1996 to December 31, 2010, respectively. Verification assesses whether (1) the firm has complied with all the composite construction requirements of the GIPS® standards on a firm-wide basis and(2) the firm's policies and procedures are designed to calculate and present performance in compliance with the GIPS® standards. Verification does not ensure the accuracy of any specific compositepresentation. The verification reports are available upon request.

Definition of the Firm• The firm is currently defined for GIPS® purposes as Neuberger Berman Group LLC, ("NB", "Neuberger Berman" or the "Firm"), and includes the following subsidiaries: Neuberger Berman Investment

Advisers LLC, Neuberger Berman Europe Ltd., Neuberger Berman Asia Ltd., Neuberger Berman East Asia Ltd., Neuberger Berman Singapore Pte. Ltd., Neuberger Berman Taiwan Ltd, NeubergerBerman Australia Pty. Ltd., Neuberger Berman Trust Company N.A., Neuberger Berman Trust Company of Delaware N.A. and NB Alternatives Advisers LLC.

Policies• Policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request.Composite Description• The Short Duration Emerging Market Debt Composite (the ""Composite"") represents the performance of all fee-paying Short Duration Emerging Market Debt portfolios with a minimum of $100,000,000

managed on a fully discretionary basis by the Short Duration Emerging Market Debt Fixed Income team.The Short Duration Emerging Market Debt Strategy seeks to achieve a positive total return by investing in short duration emerging market sovereign securities denominated in hard currencies and short duration emerging market corporate debt securities denominated in USD. The strategy focuses primarily on issuers from developing countries located in Latin America, Asia, Central and Eastern Europe, Middle East and Africa.The Short Duration Emerging Market Debt composite ("Composite") represents the performance of all fee-paying, discretionary accounts, managed according to the Short Duration Emerging Market Debt Strategy. The Composite creation and performance inception date is November 2013. A complete list and description of the NB composites and performance results is available upon request.

Primary Benchmark Description• The benchmark is the BofA Merrill Lynch 3-Month Treasury Bill Index. The index is comprised of a single issue purchased at the beginning of the month and held for a full month. At the end of the month

that issue is sold and rolled into a newly selected issue. The issue selected at each month-end rebalancing is the outstanding Treasury Bill that matures closest to, but not beyond, three months from the rebalancing date. To qualify for selection, an issue must have settled on or before the month-end rebalancing date.