Embed Size (px)

Citation preview

Networks of counterparties in the centrally cleared EU-wideinterest rate derivatives market1

Pawe l Fiedor∗ Sarah Lapschies∗ Lucia Orszaghova∗,†,‡

∗European Systemic Risk Board Secretariat

†Narodna banka Slovenska

‡University of Economics in Bratislava

1The views expressed are not necessarily the views of the ESRB, or the ESCB.

Overview of the presentation

Dataset

Results

Conclusions

What data do we use?

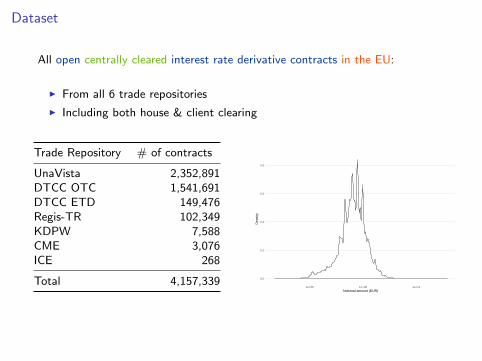

Dataset

All open centrally cleared interest rate derivative contracts in the EU:

I From all 6 trade repositories

I Including both house & client clearing

Trade Repository # of contracts

UnaVista 2,352,891DTCC OTC 1,541,691DTCC ETD 149,476Regis-TR 102,349KDPW 7,588CME 3,076ICE 268

Total 4,157,339 0.0

0.2

0.4

0.6

0.8

1e+05 1e+08 1e+11Notional amount (EUR)

Den

sity

Dataset

All open centrally cleared interest rate derivative contracts in the EU:

I From all 6 trade repositories

I Including both house & client clearing

Trade Repository # of contracts

UnaVista 2,352,891DTCC OTC 1,541,691DTCC ETD 149,476Regis-TR 102,349KDPW 7,588CME 3,076ICE 268

Total 4,157,339 0.0

0.2

0.4

0.6

0.8

1e+05 1e+08 1e+11Notional amount (EUR)

Den

sity

Dataset

All open centrally cleared interest rate derivative contracts in the EU:

I From all 6 trade repositories

I Including both house & client clearing

Trade Repository # of contracts

UnaVista 2,352,891DTCC OTC 1,541,691DTCC ETD 149,476Regis-TR 102,349KDPW 7,588CME 3,076ICE 268

Total 4,157,339 0.0

0.2

0.4

0.6

0.8

1e+05 1e+08 1e+11Notional amount (EUR)

Den

sity

Dataset

All open centrally cleared interest rate derivative contracts in the EU:

I From all 6 trade repositories

I Including both house & client clearing

Trade Repository # of contracts

UnaVista 2,352,891DTCC OTC 1,541,691DTCC ETD 149,476Regis-TR 102,349KDPW 7,588CME 3,076ICE 268

Total 4,157,339 0.0

0.2

0.4

0.6

0.8

1e+05 1e+08 1e+11Notional amount (EUR)

Den

sity

Dataset

All open centrally cleared interest rate derivative contracts in the EU:

I From all 6 trade repositories

I Including both house & client clearing

Trade Repository # of contracts

UnaVista 2,352,891DTCC OTC 1,541,691DTCC ETD 149,476Regis-TR 102,349KDPW 7,588CME 3,076ICE 268

Total 4,157,339 0.0

0.2

0.4

0.6

0.8

1e+05 1e+08 1e+11Notional amount (EUR)

Den

sity

Dataset

All open centrally cleared interest rate derivative contracts in the EU:

I From all 6 trade repositories

I Including both house & client clearing

Trade Repository # of contracts

UnaVista 2,352,891DTCC OTC 1,541,691DTCC ETD 149,476Regis-TR 102,349KDPW 7,588CME 3,076ICE 268

Total 4,157,339 0.0

0.2

0.4

0.6

0.8

1e+05 1e+08 1e+11Notional amount (EUR)

Den

sity

Dataset

All open centrally cleared interest rate derivative contracts in the EU:

I From all 6 trade repositories

I Including both house & client clearing

Trade Repository # of contracts

UnaVista 2,352,891DTCC OTC 1,541,691DTCC ETD 149,476Regis-TR 102,349KDPW 7,588CME 3,076ICE 268

Total 4,157,339

0.0

0.2

0.4

0.6

0.8

1e+05 1e+08 1e+11Notional amount (EUR)

Den

sity

Dataset

All open centrally cleared interest rate derivative contracts in the EU:

I From all 6 trade repositories

I Including both house & client clearing

Trade Repository # of contracts

UnaVista 2,352,891DTCC OTC 1,541,691DTCC ETD 149,476Regis-TR 102,349KDPW 7,588CME 3,076ICE 268

Total 4,157,339 0.0

0.2

0.4

0.6

0.8

1e+05 1e+08 1e+11Notional amount (EUR)

Den

sity

What kind of companies are in the network?

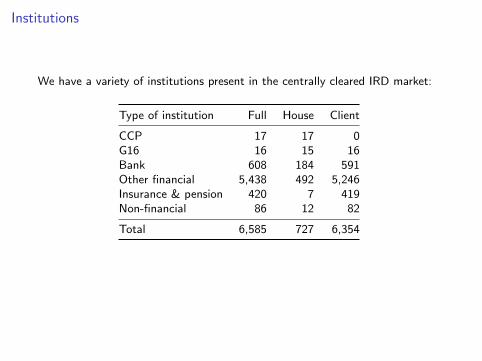

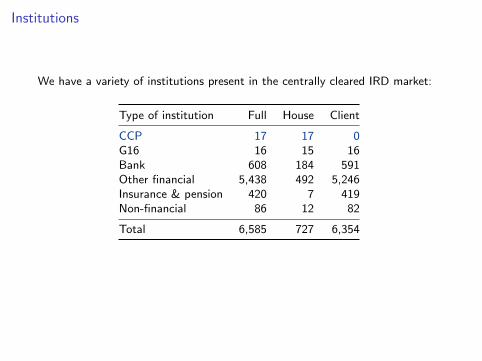

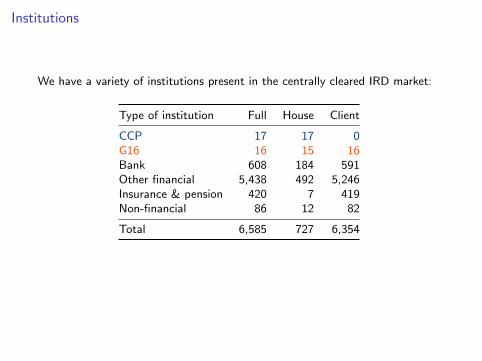

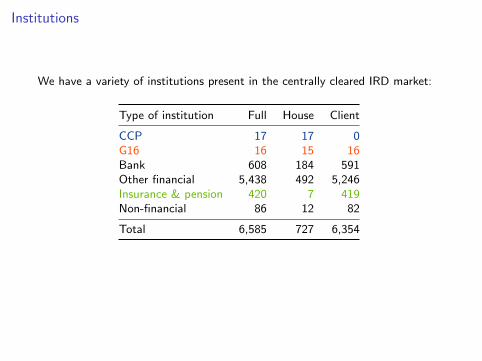

Institutions

We have a variety of institutions present in the centrally cleared IRD market:

Type of institution Full House Client

CCP 17 17 0G16 16 15 16Bank 608 184 591Other financial 5,438 492 5,246Insurance & pension 420 7 419Non-financial 86 12 82

Total 6,585 727 6,354

Institutions

We have a variety of institutions present in the centrally cleared IRD market:

Type of institution Full House Client

CCP 17 17 0G16 16 15 16Bank 608 184 591Other financial 5,438 492 5,246Insurance & pension 420 7 419Non-financial 86 12 82

Total 6,585 727 6,354

Institutions

We have a variety of institutions present in the centrally cleared IRD market:

Type of institution Full House Client

CCP 17 17 0G16 16 15 16Bank 608 184 591Other financial 5,438 492 5,246Insurance & pension 420 7 419Non-financial 86 12 82

Total 6,585 727 6,354

Institutions

We have a variety of institutions present in the centrally cleared IRD market:

Type of institution Full House Client

CCP 17 17 0G16 16 15 16Bank 608 184 591Other financial 5,438 492 5,246Insurance & pension 420 7 419Non-financial 86 12 82

Total 6,585 727 6,354

Institutions

We have a variety of institutions present in the centrally cleared IRD market:

Type of institution Full House Client

CCP 17 17 0G16 16 15 16Bank 608 184 591Other financial 5,438 492 5,246Insurance & pension 420 7 419Non-financial 86 12 82

Total 6,585 727 6,354

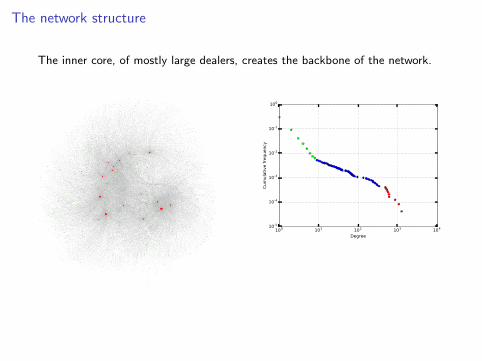

What does the network look like?

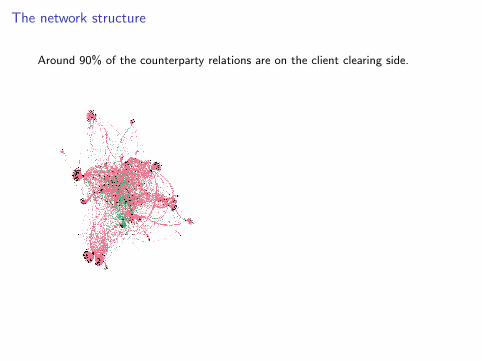

The network structure

Around 90% of the counterparty relations are on the client clearing side.

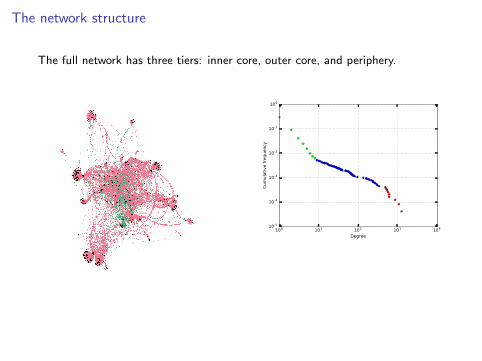

The network structure

The full network has three tiers: inner core, outer core, and periphery.

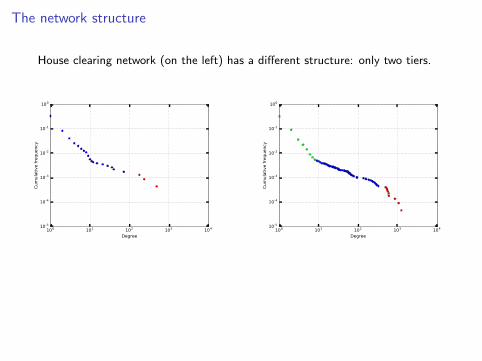

The network structure

House clearing network (on the left) has a different structure: only two tiers.

The network structure

The inner core, of mostly large dealers, creates the backbone of the network.

Is the network stable over time?

Persistence across time

The network is relatively stable between Q3 & Q4 of 2016, including thecounterparty relations.

Persistence across time

The network is relatively stable between Q3 & Q4 of 2016, including thecounterparty relations.

CC

P−C

MC

M−C

lientFU

LL

AUD BRL CAD CHF CLP CZK DKK EUR GBP HKD HUF JPY MXN NOK NZD PLN SEK SGD USD ZAR

0.00

0.25

0.50

0.75

1.00

0.00

0.25

0.50

0.75

1.00

0.00

0.25

0.50

0.75

1.00

Currency

% o

f edg

es

common only in one period

CC

P−C

MC

M−C

lientFU

LL

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

2050

2051

2052

2053

2054

2055

2056

2057

2058

2059

2060

2061

2062

2063

2064

2065

2066

0.00

0.25

0.50

0.75

1.00

0.00

0.25

0.50

0.75

1.00

0.00

0.25

0.50

0.75

1.00

Maturity year

% o

f edg

es

common only in one period

What can we find in the networks?

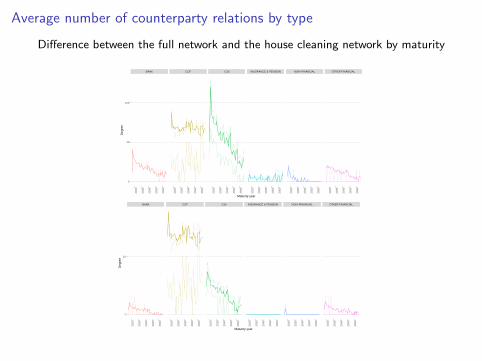

Average number of counterparty relations by type

Difference between the full network and the house cleaning network by maturity

BANK CCP G16 INSURANCE & PENSION NON−FINANCIAL OTHER FINANCIAL

2020

2030

2040

2050

2060

2020

2030

2040

2050

2060

2020

2030

2040

2050

2060

2020

2030

2040

2050

2060

2020

2030

2040

2050

2060

2020

2030

2040

2050

2060

1

10

100

Maturity year

Deg

ree

BANK CCP G16 INSURANCE & PENSION NON−FINANCIAL OTHER FINANCIAL

2020

2030

2040

2050

2060

2020

2030

2040

2050

2060

2020

2030

2040

2050

2060

2020

2030

2040

2050

2060

2020

2030

2040

2050

2060

2020

2030

2040

2050

2060

1

10

Maturity year

Deg

ree

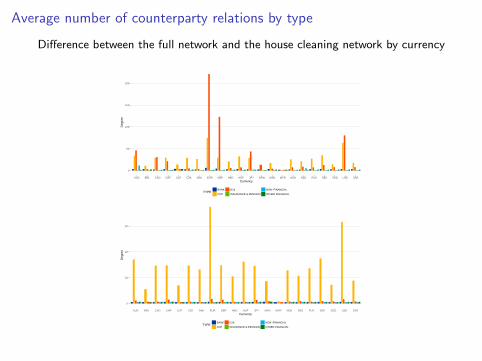

Average number of counterparty relations by type

Difference between the full network and the house cleaning network by currency

0

50

100

150

200

AUD BRL CAD CHF CLP CZK DKK EUR GBP HKD HUF JPY KRW MXN MYR NOK NZD PLN SEK SGD USD ZARCurrency

Deg

ree

TYPEBANK

CCP

G16

INSURANCE & PENSION

NON−FINANCIAL

OTHER FINANCIAL

0

20

40

60

AUD BRL CAD CHF CLP CZK DKK EUR GBP HKD HUF JPY MXN MYR NOK NZD PLN SEK SGD USD ZARCurrency

Deg

ree

TYPEBANK

CCP

G16

INSURANCE & PENSION

NON−FINANCIAL

OTHER FINANCIAL

Are the networks stable if we remove counterparties?

Random removal of counterparties by type

We remove a number of institution at random and see how many additionalones are disconnected with the main component.

Random removal of counterparties by type

For the full network G16 dealers have the most effect, followed by banks, andonly then CCPs.

Random removal of counterparties by type

For the house clearing network this information is lost, while it’s useful forfinancial stability, e.g. question of the suspension of clearing obligation.

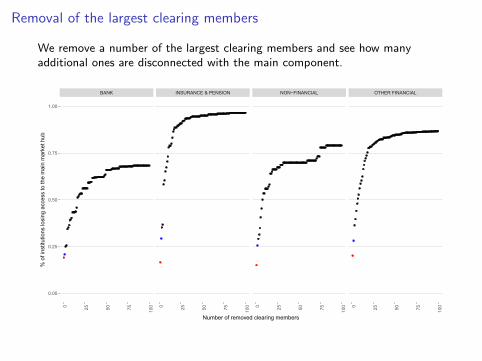

Removal of the largest clearing members

We remove a number of the largest clearing members and see how manyadditional ones are disconnected with the main component.

BANK INSURANCE & PENSION NON−FINANCIAL OTHER FINANCIAL

0 25 50 75 100 0 25 50 75 100 0 25 50 75 100 0 25 50 75 100

0.00

0.25

0.50

0.75

1.00

Number of removed clearing members

% o

f ins

titut

ions

losi

ng a

cces

s to

the

mai

n m

arke

t hub

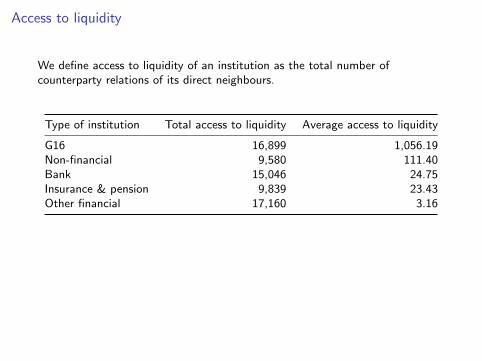

Access to liquidity

We define access to liquidity of an institution as the total number ofcounterparty relations of its direct neighbours.

Type of institution Total access to liquidity Average access to liquidity

G16 16,899 1,056.19Non-financial 9,580 111.40Bank 15,046 24.75Insurance & pension 9,839 23.43Other financial 17,160 3.16

When we remove clearing members at random the loss of access to liquidity isproportional to the starting access to liquidity, irrespective of the type of theinstitution.

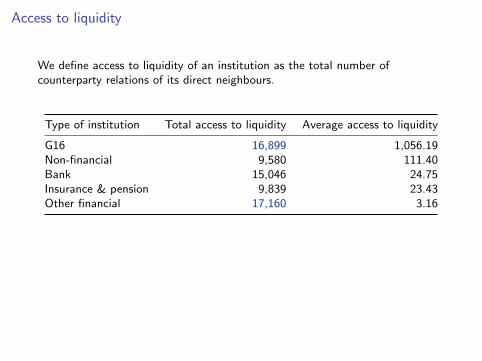

Access to liquidity

We define access to liquidity of an institution as the total number ofcounterparty relations of its direct neighbours.

Type of institution Total access to liquidity Average access to liquidity

G16 16,899 1,056.19Non-financial 9,580 111.40Bank 15,046 24.75Insurance & pension 9,839 23.43Other financial 17,160 3.16

When we remove clearing members at random the loss of access to liquidity isproportional to the starting access to liquidity, irrespective of the type of theinstitution.

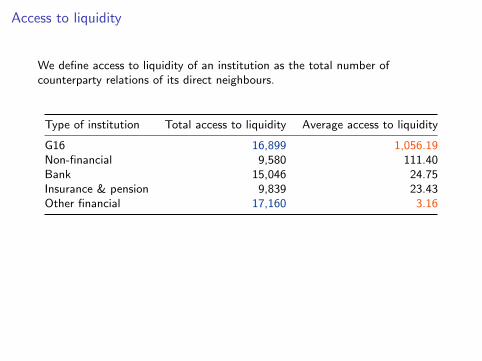

Access to liquidity

We define access to liquidity of an institution as the total number ofcounterparty relations of its direct neighbours.

Type of institution Total access to liquidity Average access to liquidity

G16 16,899 1,056.19Non-financial 9,580 111.40Bank 15,046 24.75Insurance & pension 9,839 23.43Other financial 17,160 3.16

When we remove clearing members at random the loss of access to liquidity isproportional to the starting access to liquidity, irrespective of the type of theinstitution.

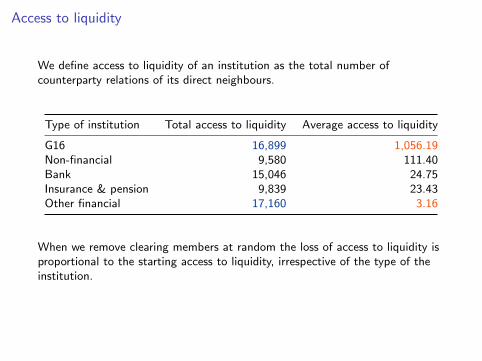

Access to liquidity

We define access to liquidity of an institution as the total number ofcounterparty relations of its direct neighbours.

Type of institution Total access to liquidity Average access to liquidity

G16 16,899 1,056.19Non-financial 9,580 111.40Bank 15,046 24.75Insurance & pension 9,839 23.43Other financial 17,160 3.16

When we remove clearing members at random the loss of access to liquidity isproportional to the starting access to liquidity, irrespective of the type of theinstitution.

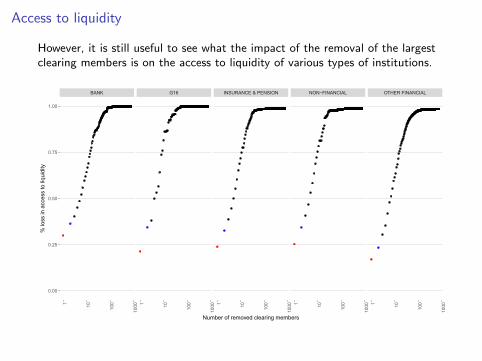

Access to liquidity

However, it is still useful to see what the impact of the removal of the largestclearing members is on the access to liquidity of various types of institutions.

BANK G16 INSURANCE & PENSION NON−FINANCIAL OTHER FINANCIAL

1 10 100

1000 1 10 10

0

1000 1 10 100

1000 1 10 10

0

1000 1 10 10

0

1000

0.00

0.25

0.50

0.75

1.00

Number of removed clearing members

% lo

ss in

acc

ess

to li

quid

ity

Conclusions

Main findings:

I Client clearing is important and changes the perception of the centrallycleared interest rate derivatives market dramatically:

I In particular, the insurance sector is only visible via client clearing;I Importance of various types of institutions changes dramatically;

I CCPs are not systemic in isolation, and should be analysed in conjunctionwith G16 dealers – also for policy issues (e.g. R&R).

Conclusions

Main findings:

I Client clearing is important and changes the perception of the centrallycleared interest rate derivatives market dramatically:

I In particular, the insurance sector is only visible via client clearing;I Importance of various types of institutions changes dramatically;

I CCPs are not systemic in isolation, and should be analysed in conjunctionwith G16 dealers – also for policy issues (e.g. R&R).

Conclusions

Main findings:

I Client clearing is important and changes the perception of the centrallycleared interest rate derivatives market dramatically:

I In particular, the insurance sector is only visible via client clearing;

I Importance of various types of institutions changes dramatically;

I CCPs are not systemic in isolation, and should be analysed in conjunctionwith G16 dealers – also for policy issues (e.g. R&R).

Conclusions

Main findings:

I Client clearing is important and changes the perception of the centrallycleared interest rate derivatives market dramatically:

I In particular, the insurance sector is only visible via client clearing;I Importance of various types of institutions changes dramatically;

I CCPs are not systemic in isolation, and should be analysed in conjunctionwith G16 dealers – also for policy issues (e.g. R&R).

Conclusions

Main findings:

I Client clearing is important and changes the perception of the centrallycleared interest rate derivatives market dramatically:

I In particular, the insurance sector is only visible via client clearing;I Importance of various types of institutions changes dramatically;

I CCPs are not systemic in isolation, and should be analysed in conjunctionwith G16 dealers – also for policy issues (e.g. R&R).

Thank you