Embed Size (px)

Citation preview

National Newspaper Association

127th Annual Convention & Trade Show

September 13, 2013

The Health Insurance Marketplace 101

• Community Resource

• California-Based

– Arizona, California, Hawaii, Nevada, and the U.S. Affiliated Pacific Islands

• Educate the public on the benefits of healthcare reform

-- Healthcare.gov

-- CuidadodeSalud.gov (Spanish)

Office of the Regional Director

2

The Problem

• At least 51 million Americans without coverage • Fast rising health care costs, partially due to

uninsured

• Premiums had more than doubled over the last decade, while insurance company profits continued to rise

• Economic hardship for families, small businesses and the U.S. Economy

In March 2010, President Obama signed into law the

Affordable Care Act.

Affordable Care Act

4

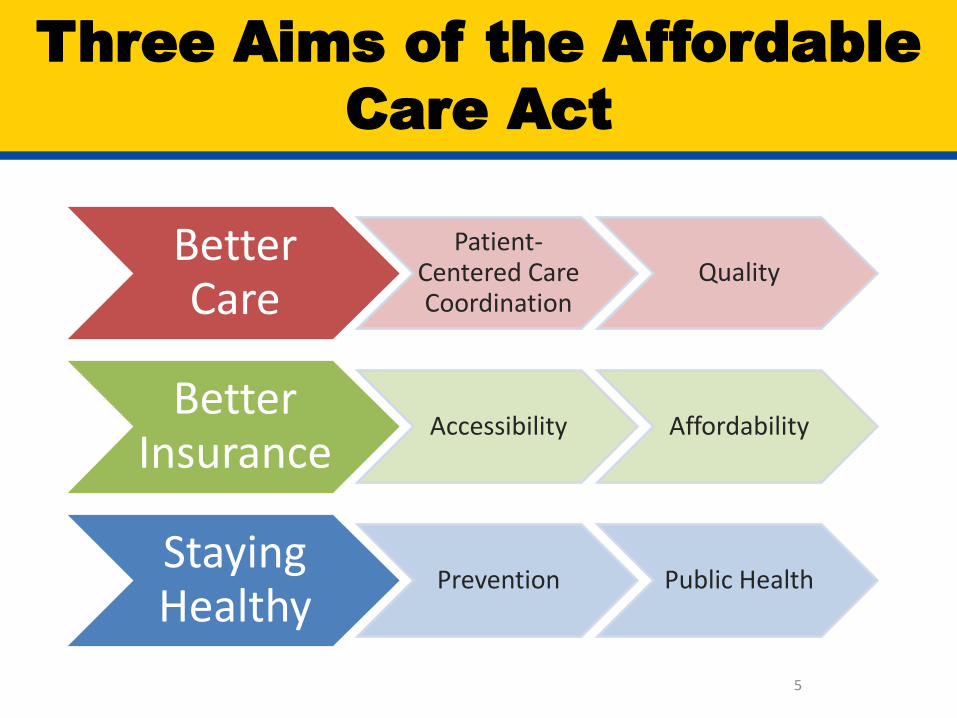

Three Aims of the Affordable

Care Act

5

Better Care

Patient-Centered Care Coordination

Quality

Better Insurance

Accessibility Affordability

Staying Healthy

Prevention Public Health

• Protection from the worst insurance company

abuses

• Makes health care more affordable

• Better access to care

• Stronger Medicare

Affordable Care Act

6

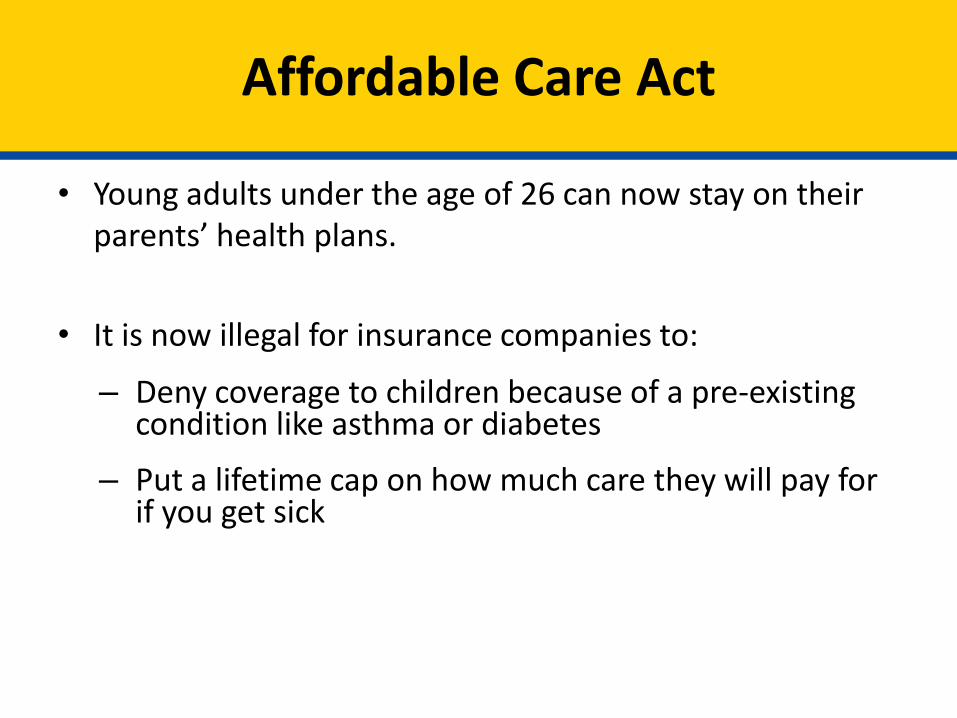

Affordable Care Act

• Young adults under the age of 26 can now stay on their parents’ health plans.

• It is now illegal for insurance companies to:

– Deny coverage to children because of a pre-existing condition like asthma or diabetes

– Put a lifetime cap on how much care they will pay for if you get sick

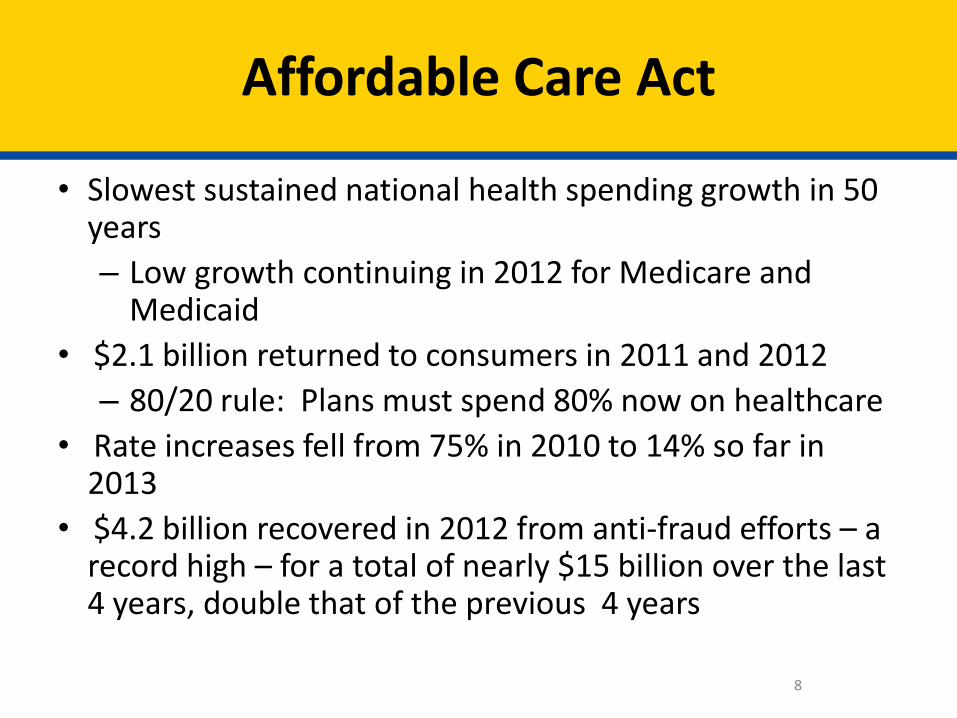

• Slowest sustained national health spending growth in 50 years

– Low growth continuing in 2012 for Medicare and Medicaid

• $2.1 billion returned to consumers in 2011 and 2012

– 80/20 rule: Plans must spend 80% now on healthcare

• Rate increases fell from 75% in 2010 to 14% so far in 2013

• $4.2 billion recovered in 2012 from anti-fraud efforts – a record high – for a total of nearly $15 billion over the last 4 years, double that of the previous 4 years

Affordable Care Act

8

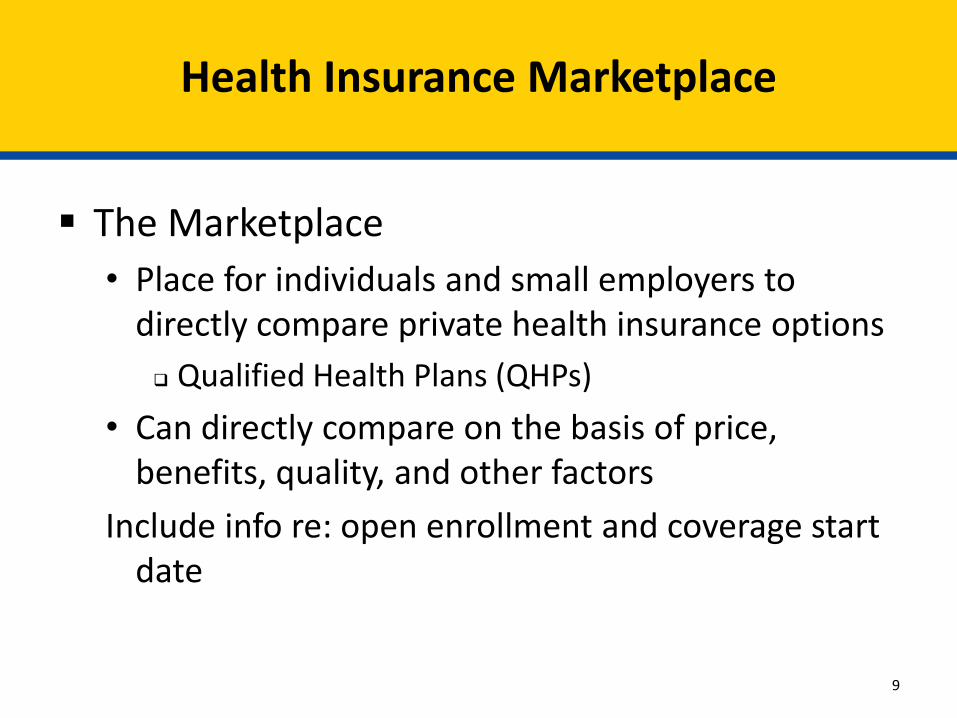

The Marketplace

• Place for individuals and small employers to directly compare private health insurance options

Qualified Health Plans (QHPs)

• Can directly compare on the basis of price, benefits, quality, and other factors

Include info re: open enrollment and coverage start date

Health Insurance Marketplace

9

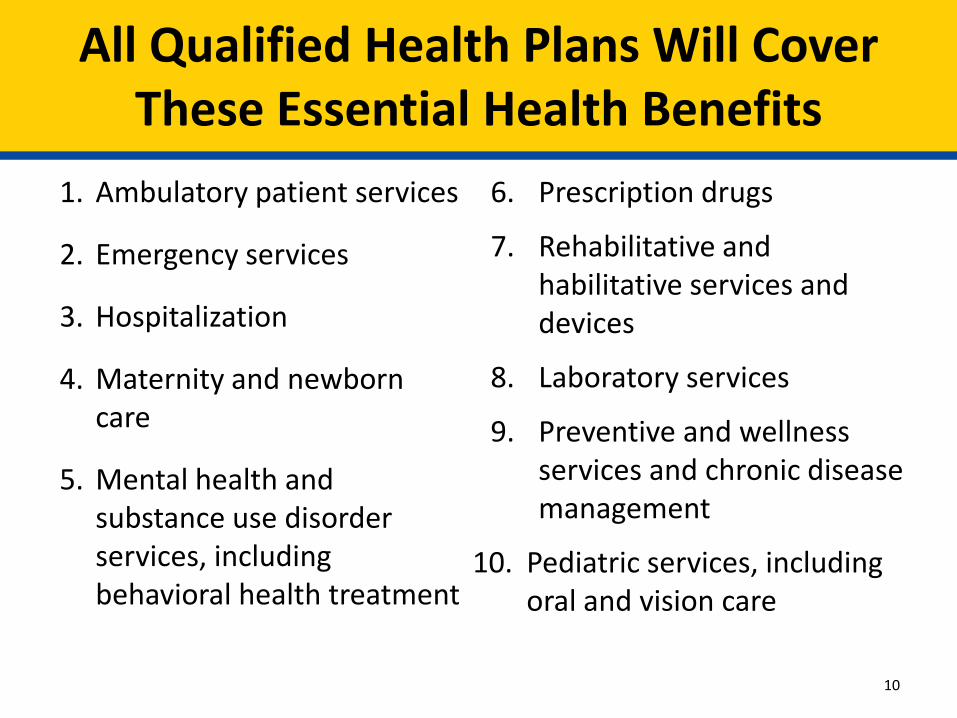

6. Prescription drugs

7. Rehabilitative and habilitative services and devices

8. Laboratory services

9. Preventive and wellness services and chronic disease management

10. Pediatric services, including oral and vision care

1. Ambulatory patient services

2. Emergency services

3. Hospitalization

4. Maternity and newborn care

5. Mental health and substance use disorder services, including behavioral health treatment

All Qualified Health Plans Will Cover These Essential Health Benefits

10

A new way to get health insurance

• Enrollment starts October 1, 2013

• Coverage begins January 2014

About 25 million Americans will have access to quality health insurance

• Up to 20 million may qualify for help to make it more affordable

• Working families can get help through the Marketplace

The Health Insurance Marketplace

11

Health Insurance Marketplaces:

12

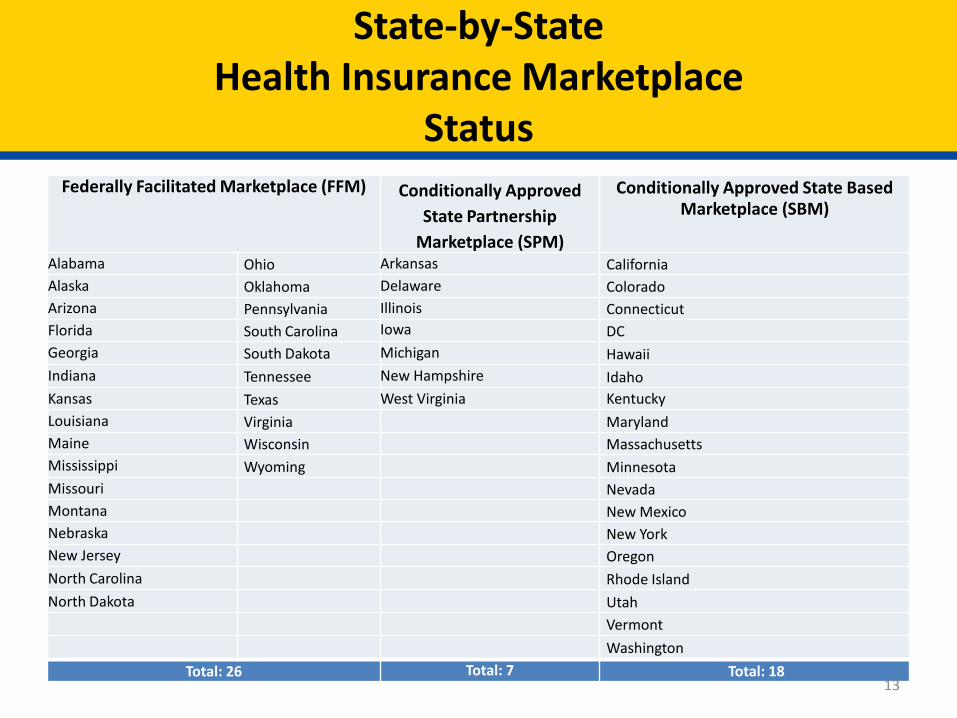

Health Insurance Marketplaces will be established in every state:

1) Federally Facilitated Marketplace (FFM)

2) State Partnership Marketplace (SPM)

3) State Based Marketplace (SBM)

Federally Facilitated Marketplace (FFM) Conditionally Approved

State Partnership

Marketplace (SPM)

Conditionally Approved State Based Marketplace (SBM)

Alabama Ohio Arkansas California

Alaska Oklahoma Delaware Colorado

Arizona Pennsylvania Illinois Connecticut

Florida South Carolina Iowa DC

Georgia South Dakota Michigan Hawaii

Indiana Tennessee New Hampshire Idaho

Kansas Texas West Virginia Kentucky

Louisiana Virginia Maryland

Maine Wisconsin Massachusetts

Mississippi Wyoming Minnesota

Missouri Nevada

Montana New Mexico

Nebraska New York

New Jersey Oregon

North Carolina Rhode Island

North Dakota Utah

Vermont

Washington

Total: 26 Total: 7 Total: 18

State-by-State Health Insurance Marketplace

Status

13

1. It’s an easier way to shop for health insurance • Simplifies the search for health insurance

• All options in one place

• One application, one time, and an individual or family can explore every qualified insurance plan in the area

2. Most people will be able to get a break on costs • 90% of people who are currently uninsured will qualify for

discounted or free health insurance

3. Clear options with apples-to-apples comparisons • All health insurance plans present their price and benefit

information in plain language

Health Insurance Marketplace: Top-line

Messages

14

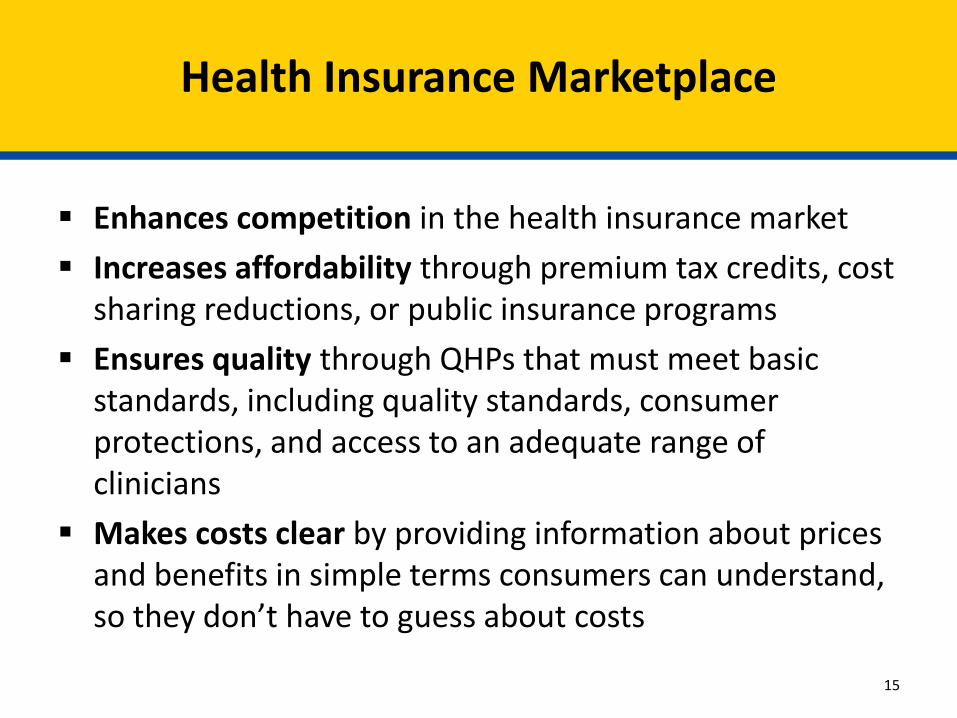

Enhances competition in the health insurance market

Increases affordability through premium tax credits, cost sharing reductions, or public insurance programs

Ensures quality through QHPs that must meet basic standards, including quality standards, consumer protections, and access to an adequate range of clinicians

Makes costs clear by providing information about prices and benefits in simple terms consumers can understand, so they don’t have to guess about costs

Health Insurance Marketplace

15

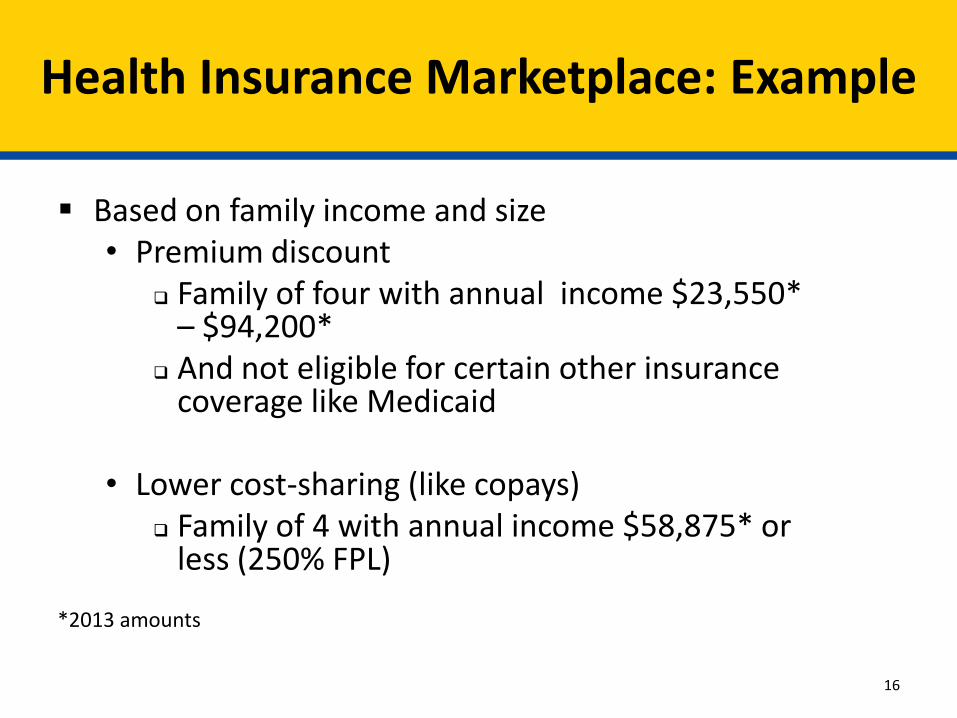

Based on family income and size • Premium discount

Family of four with annual income $23,550* – $94,200*

And not eligible for certain other insurance coverage like Medicaid

• Lower cost-sharing (like copays)

Family of 4 with annual income $58,875* or less (250% FPL)

*2013 amounts

Health Insurance Marketplace: Example

16

Starting in 2014, you’ll have more choice and control over your health insurance spending through the Small Business Health Options Program (SHOP), a new program that simplifies the process of buying health coverage for your small business.

Small Business Health Options Plan (SHOP)

17

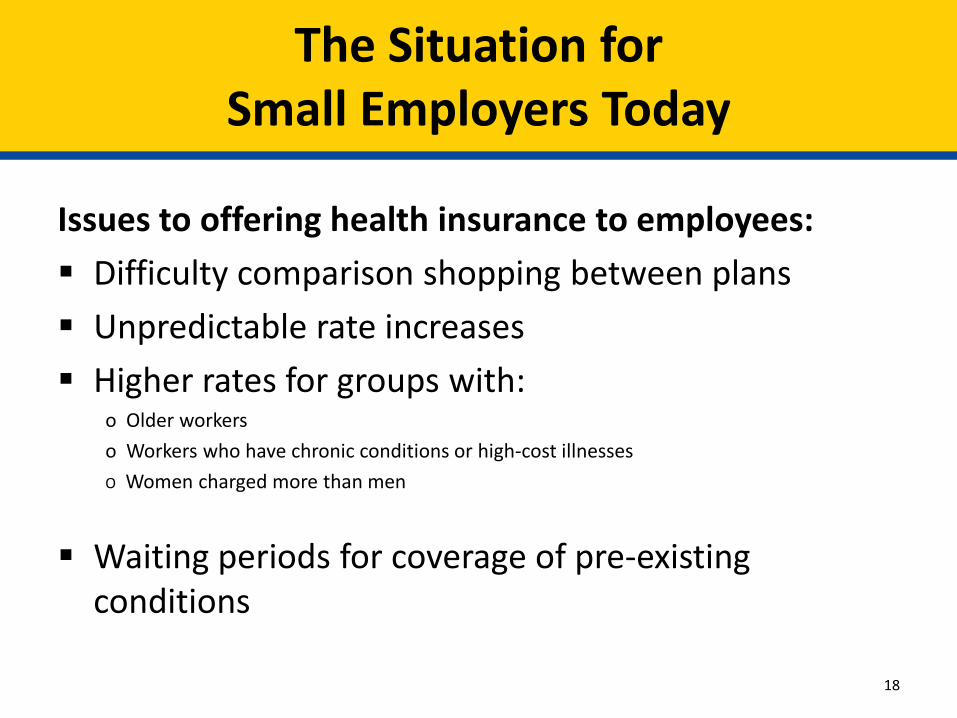

Issues to offering health insurance to employees:

Difficulty comparison shopping between plans

Unpredictable rate increases

Higher rates for groups with: o Older workers

o Workers who have chronic conditions or high‐cost illnesses

O Women charged more than men

Waiting periods for coverage of pre‐existing conditions

The Situation for Small Employers Today

18

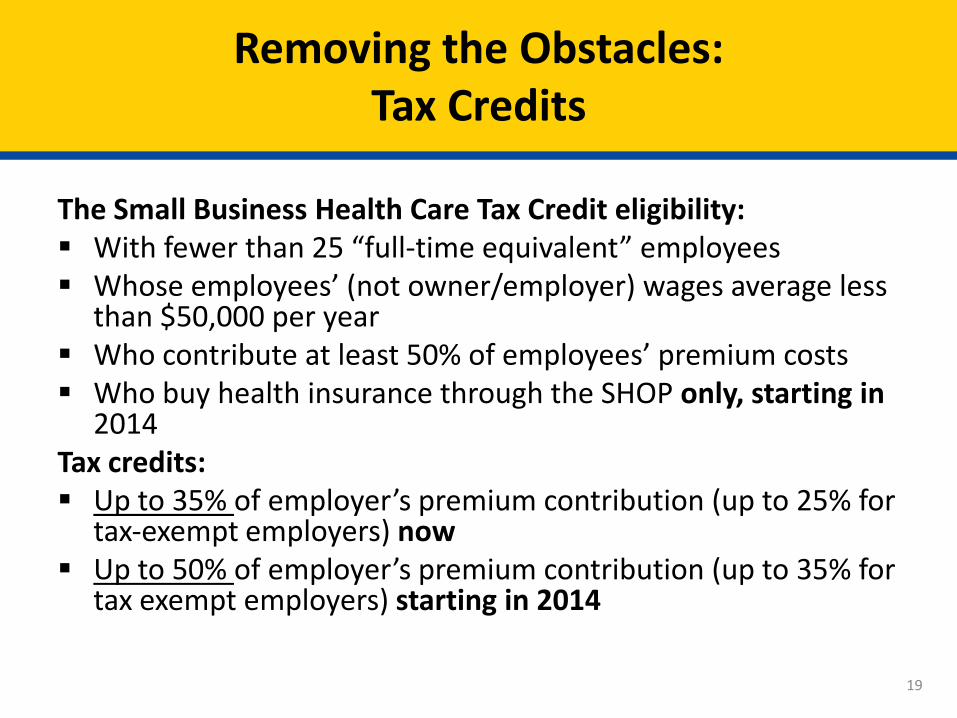

The Small Business Health Care Tax Credit eligibility: With fewer than 25 “full‐time equivalent” employees Whose employees’ (not owner/employer) wages average less

than $50,000 per year Who contribute at least 50% of employees’ premium costs Who buy health insurance through the SHOP only, starting in

2014 Tax credits: Up to 35% of employer’s premium contribution (up to 25% for

tax‐exempt employers) now Up to 50% of employer’s premium contribution (up to 35% for

tax exempt employers) starting in 2014

Removing the Obstacles: Tax Credits

19

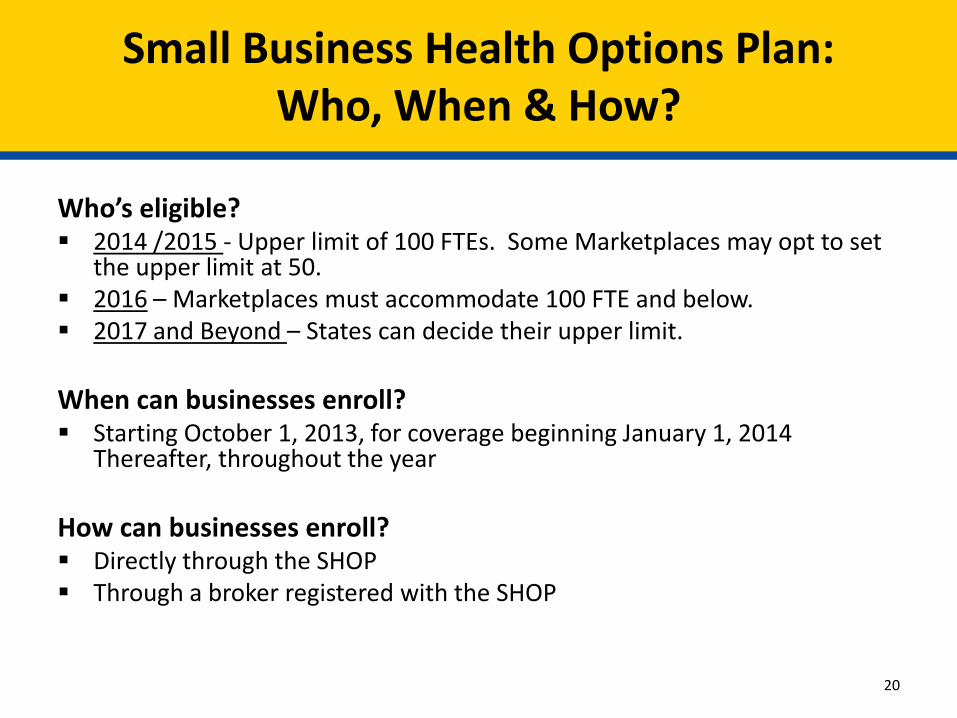

Who’s eligible? 2014 /2015 - Upper limit of 100 FTEs. Some Marketplaces may opt to set

the upper limit at 50. 2016 – Marketplaces must accommodate 100 FTE and below. 2017 and Beyond – States can decide their upper limit.

When can businesses enroll? Starting October 1, 2013, for coverage beginning January 1, 2014

Thereafter, throughout the year

How can businesses enroll? Directly through the SHOP Through a broker registered with the SHOP

Small Business Health Options Plan: Who, When & How?

20

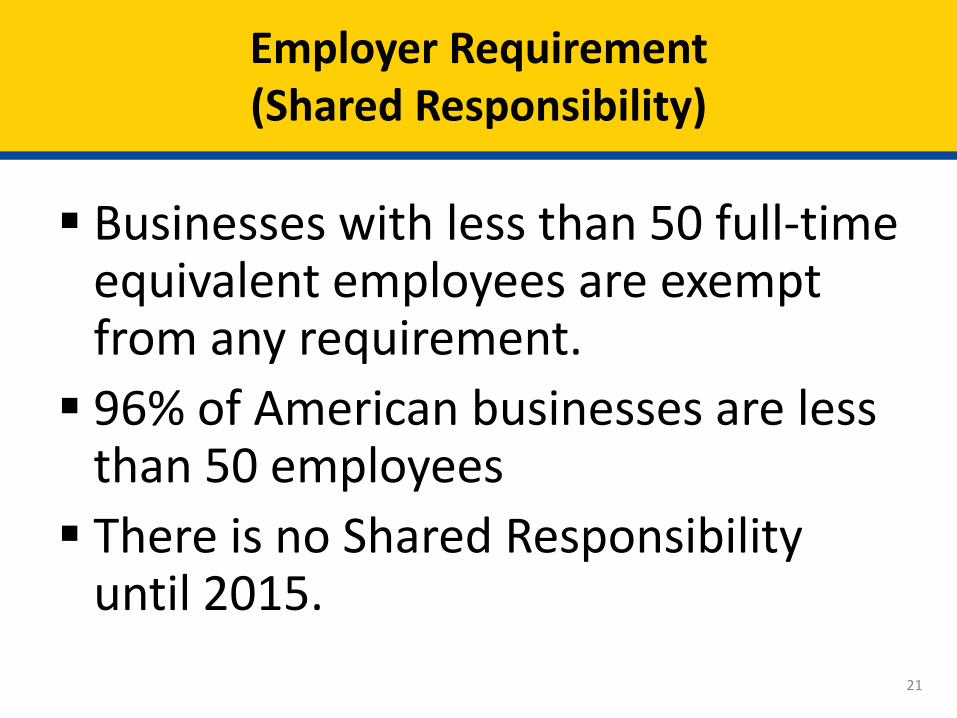

Businesses with less than 50 full-time equivalent employees are exempt from any requirement.

96% of American businesses are less than 50 employees

There is no Shared Responsibility until 2015.

Employer Requirement (Shared Responsibility)

21

The Health Insurance Marketplace is a new way to find and buy health insurance

Individuals and small businesses can shop for health insurance that fits their budget

There is financial help for working families and other people with limited income to obtain health insurance

There is assistance available to help consumers get the best coverage for their needs

Summary

22

Marketplace Call Center (Consumers) - 24/7 – English and Spanish and 150 Languages

1-800-318-2596, 1-855-889-4325 (TTY)

SHOP Marketplace for Businesses

1-800-706-7893, 1-800-706-7915 (TTY)

Stay Connected

• Go to www.healthcare.gov / www.cuidadodesalud.gov

• Updates and resources for partner organizations are available at www.Marketplace.cms.gov

• Twitter@HealthCareGov

• facebook.com/Healthcare.gov

Want more information about the Marketplace?

23

Steven Wiener

Regional Outreach Specialist, Region IX

(415) 437-8500 – Main Number

(415) 437-8518 – Direct Number

HHS Website: www.hhs.gov

Thank you!

24