Embed Size (px)

Citation preview

Financial Results Q2 FY 2020

September 2019

MUTHOOT FINANCE LIMITED

SAFE HARBOUR STATEMENT

This presentation may include statements, which may constitute forward-looking statements. All statements that address

expectations or projections about the future, including, but not limited to, statements about the strategy for growth, business

development, market position, expenditures, and financial results, are forward looking statements. Forward-looking statements

are based on certain assumptions and expectations of future events. The company cannot guarantee that these assumptions

and expectations are accurate or will be realised. The actual results, performance or achievements, could thus differ materially

from those projected in any such forward-looking statements.

The company assumes no responsibility to publicly amend, modify or revise any forward-looking statements, on the basis of

any subsequent developments, information or events, or otherwise. While every effort is made to ensure that this presentation

conforms with all applicable legal requirements, the company does not warrant that it is complete, comprehensive or accurate,

or commit to its being updated. No part of the information provided herein is to be construed as a solicitation to make any

financial investment and is provided for information only.

Any person/ party intending to provide finance / invest in the shares/businesses of the Company shall do so after seeking their

own professional advice and after carrying out their own due diligence procedure to ensure that they are making an informed

decision. In no event shall the company be liable for any damages whatsoever, whether direct, incidental, indirect,

consequential or special damages of any kind or including, without limitation, those resulting from loss of profit, loss of

contracts, goodwill, data, information, income, expected savings or business relationships arising out of or in connection with

the use of this presentation.

1

Primary BusinessShareholding of holding

company (%)

Muthoot Finance Ltd Gold Loans Holding Company

Muthoot Homefin (India) Ltd Affordable Housing Finance 100.00

Belstar Microfinance Private Limited Microfinance 70.01

Muthoot Money Limited Vehicle Finance 100.00

Asia Asset Finance PLC Listed Diversified NBFC in Sri Lanka 72.92

Muthoot Insurance Brokers Private Limited Insurance Broking 100.00

Muthoot Asset Management Private Limited - 100.00

Muthoot Trustee Private Limited - 100.00

2

THE GROUP

Diversified business of the Group

H1 FY 2020 H1 FY 2019 Q1 FY 2020 FY 2019 YoY(%)

Group Branch Network (Nos) 5190 4765 5,092 5,020 9

Consolidated Gross Loan Assets* of the Group (` in million) 403,903 358,353 402,263 383,036 13

Consolidated Profit of the Group (` in million) 14,719 10,326 5,633 21,030 43

Contribution in the Consolidated Gross Loan Assets* of the

Group

Muthoot Finance (%) 87 90 88 88 (3)

Subsidiaries (%) 13 10 12 12 30

Contribution in the Consolidated Profit of the Group

Muthoot Finance (%) 94 95 94 94 (1)

Subsidiaries (%) 6 5 6 6 20

3

THE GROUP

Snapshot of performance

*Principal amount of Loan assets

H1 FY 2020 H1 FY 2019 Q1 FY 2020 FY 2019 YoY (%)

Muthoot Finance Ltd 357,305 323,186 358,159 342,461 11

Muthoot Homefin (India) Ltd 20,975 17,753 19,875 19,075 18

Belstar Microfinance Private Limited 21,074 13,806 19,385 18,419 53

Muthoot Money Limited 4,263 658 3,927 3,107 548

Asia Asset Finance PLC 5,086 4,813 5,030 4,974 6

Less: Intra-Group Loan Assets 4,800 1,863 4,100 5,000 158

Total 403,903 358,353 402,276 383,036 13

4

THE GROUP

Gross Loan Assets* of the Group (` in millions)

*Principal amount of Loan assets

H1 FY 2020 H1 FY 2019 Q2 FY 2020 Q2 FY 2019 Q1 FY 2020 FY 2019

Muthoot Finance Ltd 13,880 9,754 8,579 4,838 5,300 19,721

Muthoot Homefin (India) Ltd 202 210 139 105 62 363

Muthoot Insurance Brokers Private Limited 65 61 39 37 27 150

Belstar Microfinance Private Limited 509 286 281 161 229 729

Muthoot Money Limited 32 (19) 32 (15) (0.40) 3

Asia Asset Finance PLC 21 16 11 9 10 41

Muthoot Asset Management Private Limited23 - 17 - 6 2

Muthoot Trustee Private Limited 0.01 - 0.18 - (0.20) -

5

THE GROUP

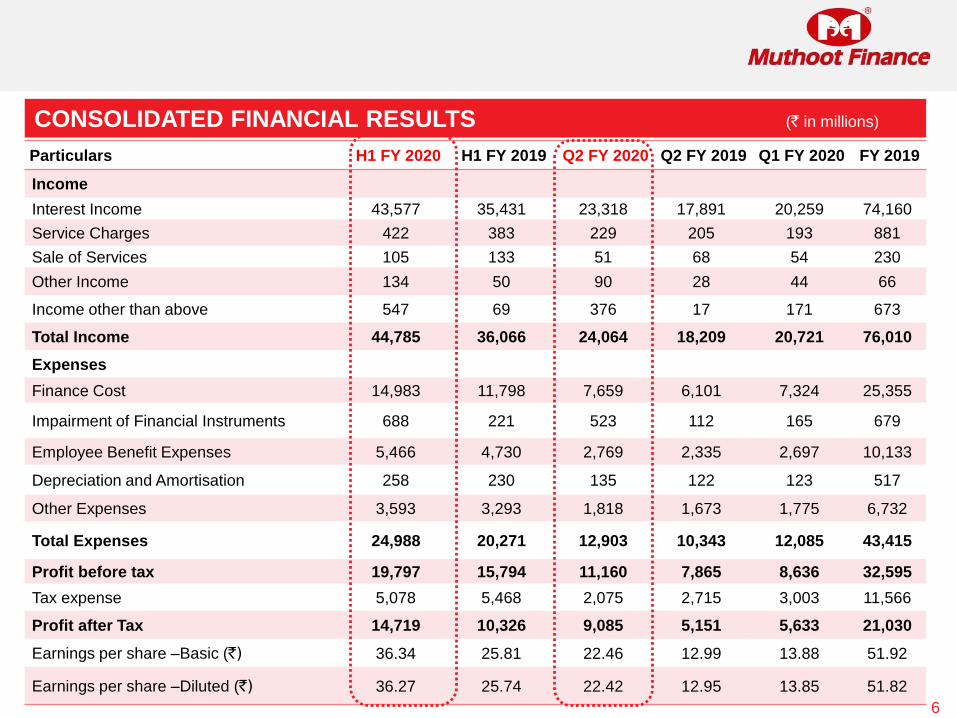

Standalone Profit of Group Companies (` in millions)

Particulars H1 FY 2020 H1 FY 2019 Q2 FY 2020 Q2 FY 2019 Q1 FY 2020 FY 2019

Income

Interest Income 43,577 35,431 23,318 17,891 20,259 74,160

Service Charges 422 383 229 205 193 881

Sale of Services 105 133 51 68 54 230

Other Income 134 50 90 28 44 66

Income other than above 547 69 376 17 171 673

Total Income 44,785 36,066 24,064 18,209 20,721 76,010

Expenses

Finance Cost 14,983 11,798 7,659 6,101 7,324 25,355

Impairment of Financial Instruments 688 221 523 112 165 679

Employee Benefit Expenses 5,466 4,730 2,769 2,335 2,697 10,133

Depreciation and Amortisation 258 230 135 122 123 517

Other Expenses 3,593 3,293 1,818 1,673 1,775 6,732

Total Expenses 24,988 20,271 12,903 10,343 12,085 43,415

Profit before tax 19,797 15,794 11,160 7,865 8,636 32,595

Tax expense 5,078 5,468 2,075 2,715 3,003 11,566

Profit after Tax 14,719 10,326 9,085 5,151 5,633 21,030

Earnings per share –Basic (`) 36.34 25.81 22.46 12.99 13.88 51.92

Earnings per share –Diluted (`) 36.27 25.74 22.42 12.95 13.85 51.82

6

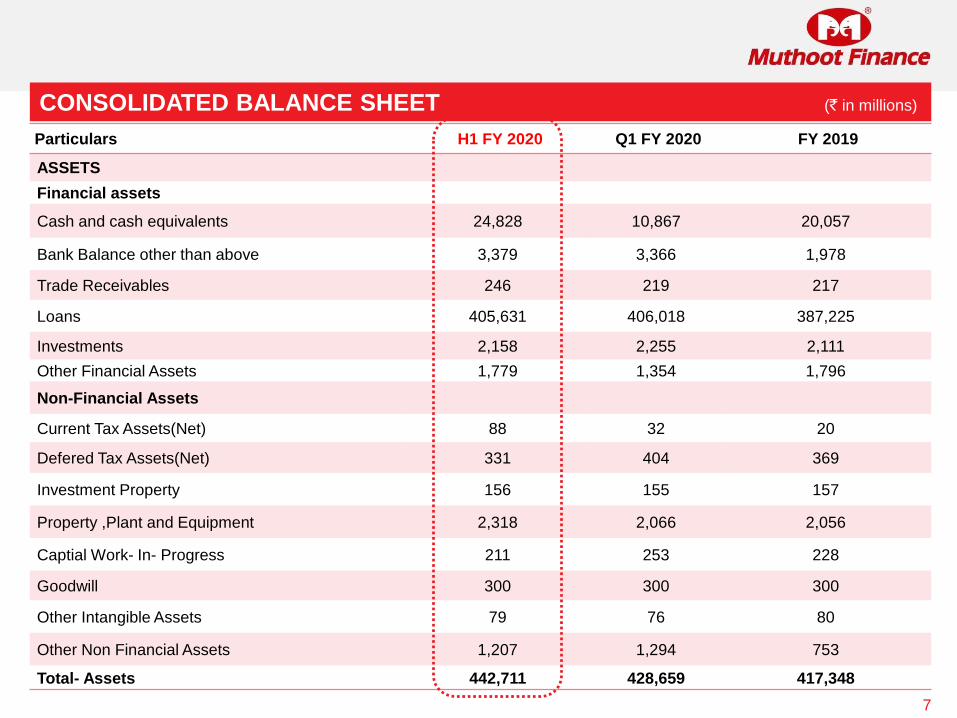

CONSOLIDATED FINANCIAL RESULTS (` in millions)

Particulars H1 FY 2020 Q1 FY 2020 FY 2019

ASSETS

Financial assets

Cash and cash equivalents 24,828 10,867 20,057

Bank Balance other than above 3,379 3,366 1,978

Trade Receivables 246 219 217

Loans 405,631 406,018 387,225

Investments 2,158 2,255 2,111

Other Financial Assets 1,779 1,354 1,796

Non-Financial Assets

Current Tax Assets(Net) 88 32 20

Defered Tax Assets(Net) 331 404 369

Investment Property 156 155 157

Property ,Plant and Equipment 2,318 2,066 2,056

Captial Work- In- Progress 211 253 228

Goodwill 300 300 300

Other Intangible Assets 79 76 80

Other Non Financial Assets 1,207 1,294 753

Total- Assets 442,711 428,659 417,348

7

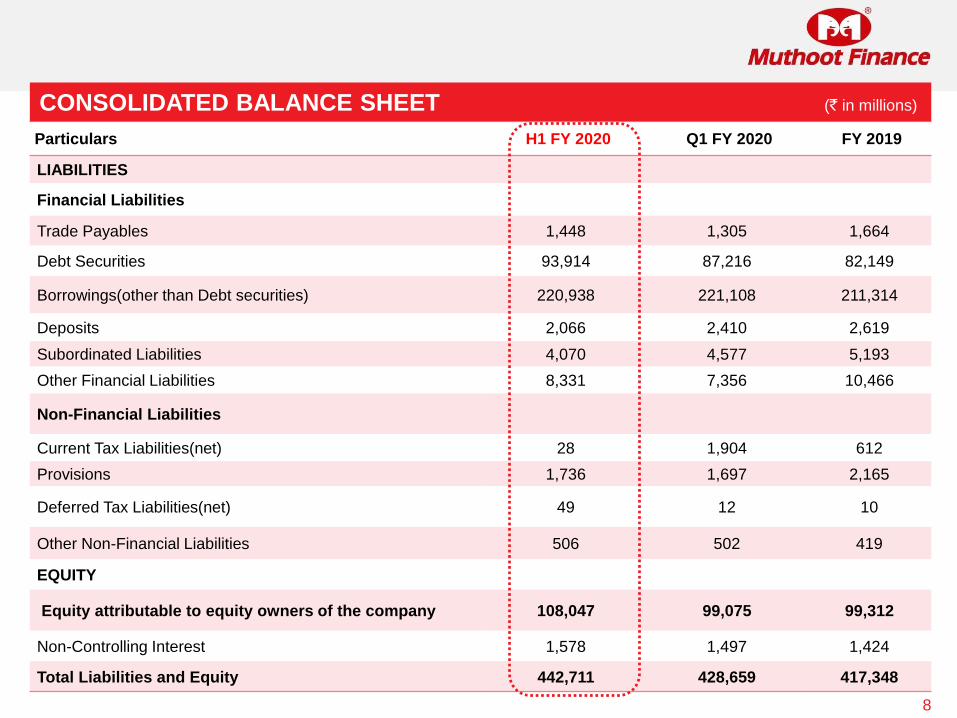

CONSOLIDATED BALANCE SHEET (` in millions)

Particulars H1 FY 2020 Q1 FY 2020 FY 2019

LIABILITIES

Financial Liabilities

Trade Payables 1,448 1,305 1,664

Debt Securities 93,914 87,216 82,149

Borrowings(other than Debt securities) 220,938 221,108 211,314

Deposits 2,066 2,410 2,619

Subordinated Liabilities 4,070 4,577 5,193

Other Financial Liabilities 8,331 7,356 10,466

Non-Financial Liabilities

Current Tax Liabilities(net) 28 1,904 612

Provisions 1,736 1,697 2,165

Deferred Tax Liabilities(net) 49 12 10

Other Non-Financial Liabilities 506 502 419

EQUITY

Equity attributable to equity owners of the company 108,047 99,075 99,312

Non-Controlling Interest 1,578 1,497 1,424

Total Liabilities and Equity 442,711 428,659 417,348

8

CONSOLIDATED BALANCE SHEET (` in millions)

MUTHOOT FINANCE: DRIVING INCLUSIVE GROWTH

9

o India’s largest gold financing company (by loan portfolio)

o Trusted pan-India brand in the gold loans sector; revolutionised India’s gold banking

o Our intervention has empowered millions of people across the social pyramid

Gold Loans Money Transfer Services

White Label ATM

National Pension Scheme

CORE

SERVICE

OTHER

SERVICES

Collection Services

Wind Mill Power Generation

Multiple service offerings

Personal Loans

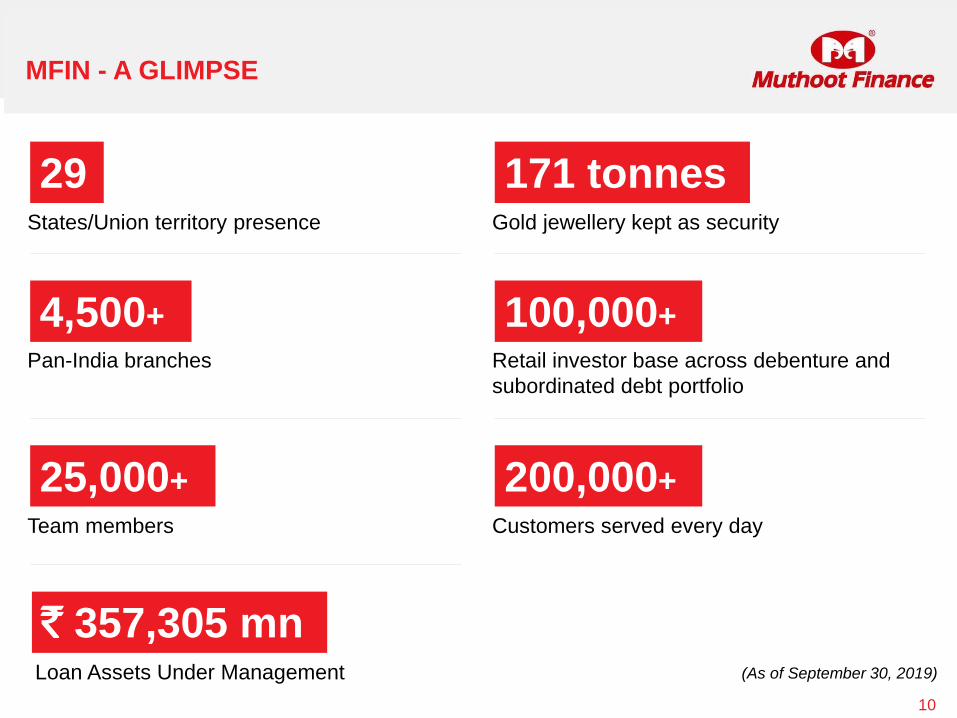

MFIN - A GLIMPSE

10

29States/Union territory presence

4,500+

Pan-India branches

25,000+

Team members

171 tonnesGold jewellery kept as security

100,000+

Retail investor base across debenture and

subordinated debt portfolio

200,000+

Customers served every day

` 357,305 mnLoan Assets Under Management (As of September 30, 2019)

SHAREHOLDING PATTERN

11

NSE Ticker

MUTHOOTFIN

BSE Ticker

533398

Market Capitalisation (as on September 30, 2019)

` 270,855 million

Strong promoter interest in business with 74% stake

(%) Shareholding as on

September 30, 2019

73.65

23.293.06

Promoters & Relatives

FII, FC, MF & Others

Public

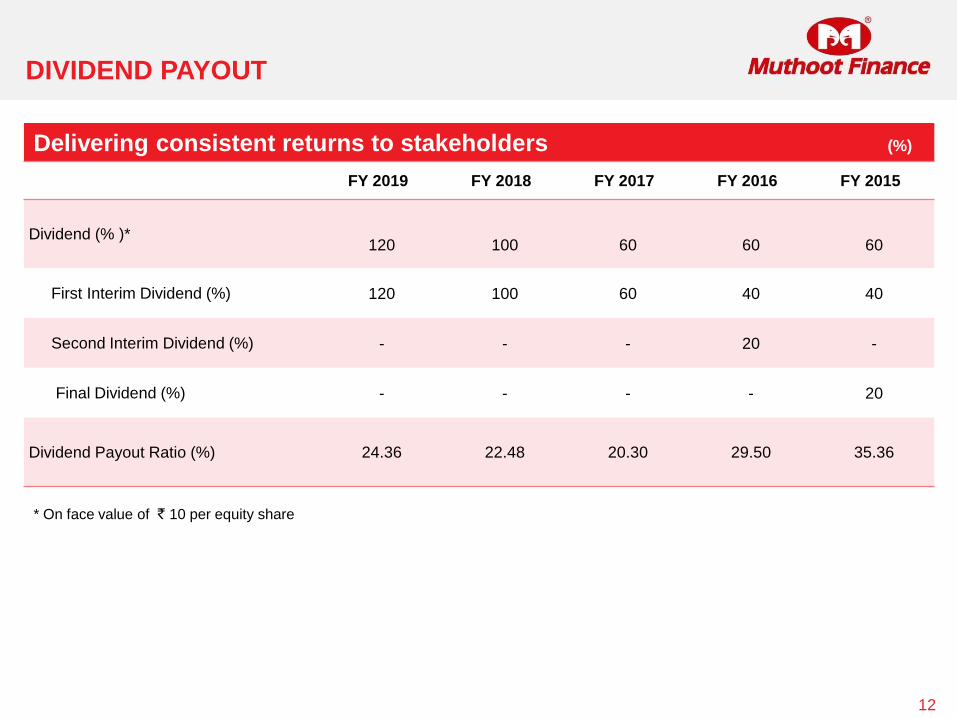

DIVIDEND PAYOUT

12

Delivering consistent returns to stakeholders (%)

FY 2019 FY 2018 FY 2017 FY 2016 FY 2015

Dividend (% )*120 100 60 60 60

First Interim Dividend (%) 120 100 60 40 40

Second Interim Dividend (%) - - - 20 -

Final Dividend (%) - - - - 20

Dividend Payout Ratio (%) 24.36 22.48 20.30 29.50 35.36

* On face value of ` 10 per equity share

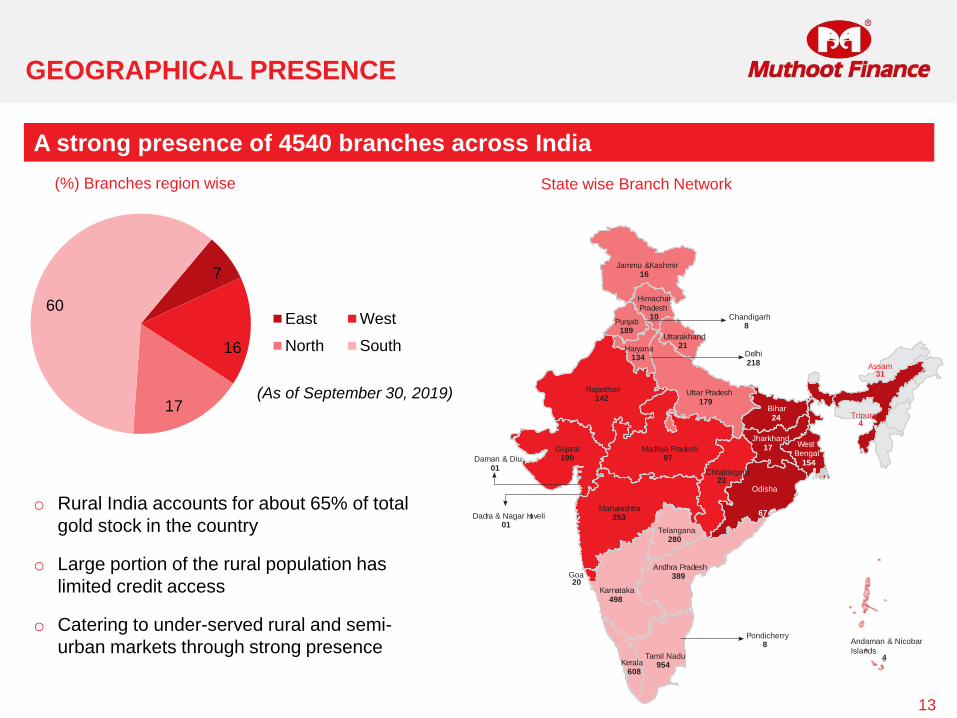

GEOGRAPHICAL PRESENCE

13

A strong presence of 4540 branches across India

(%) Branches region wise State wise Branch Network

7

16

17

60East West

North South

(As of September 30, 2019)

o Rural India accounts for about 65% of total

gold stock in the country

o Large portion of the rural population has

limited credit access

o Catering to under-served rural and semi-

urban markets through strong presence

Jammu &Kashmir16

HimachalPradesh

10Punjab

189

Chandigarh8

Delhi218

Rajasthan142

Gujarat190Daman & Diu

01

Dadra & Nagar Haveli01

Madhya Pradesh97

Uttar Pradesh179

Bihar24

Uttarakhand21Haryana

134

Maharashtra253

Karnataka498

Goa20

Tamil Nadu954

Pondicherry8

Andhra Pradesh389

Telangana280

Chhattisgarh23

Odisha

67

Jharkhand17 West

Bengal

154

Kerala608

Assam31

Tripura4

4

Andaman & Nicobar

Islands

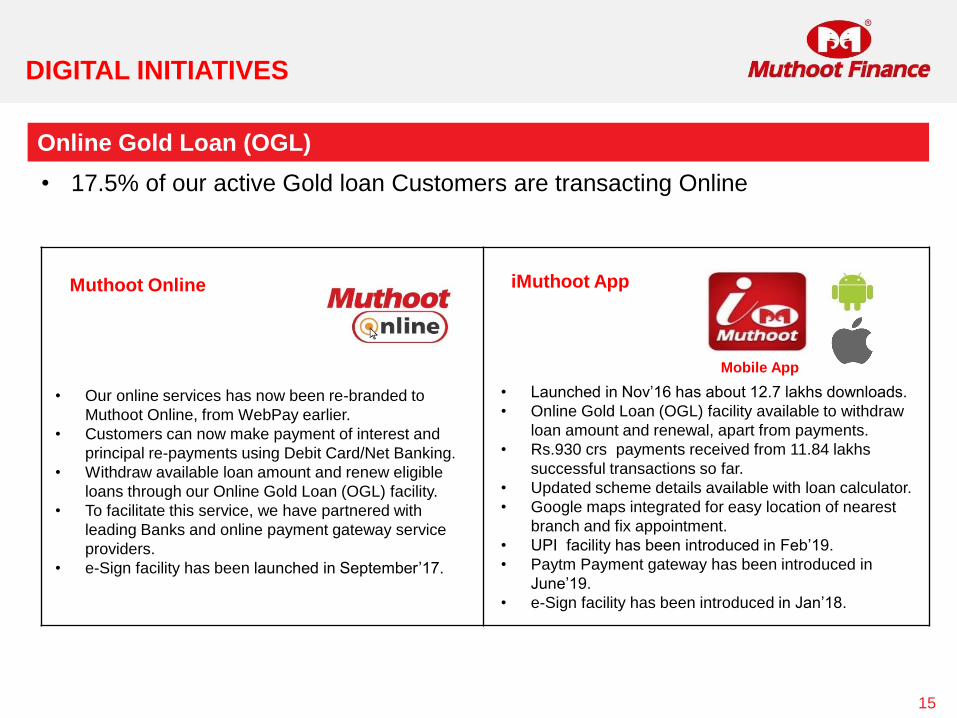

DIGITAL INITIATIVES

14

Digital convenience for new gen & Millennium Customer acquisition

Direct Credit Facility

• Loan proceeds credited to bank

account

• NEFT/RTGS/IMPS mode of bank

transfer

• Less cash handling at branch

• Instant credit to customer bank

account

Gold Cash Card (GCC) - DCB VISA

• Gold Loan amount loaded in card

• Use in ATMs & Shopping (online & offline)

• Accepted at all VISA enabled PoS

• Bank account not required for issuance

• Only Gold Loan NBFC to provide this

service

PoS Terminals

• Enables swiping of Debit

cards issued by banks

• Swiping charges for

Interest payments

waived off

DIGITAL INITIATIVES

15

Online Gold Loan (OGL)

• 17.5% of our active Gold loan Customers are transacting Online

Muthoot Online iMuthoot App

Mobile App

• Our online services has now been re-branded to

Muthoot Online, from WebPay earlier.

• Customers can now make payment of interest and

principal re-payments using Debit Card/Net Banking.

• Withdraw available loan amount and renew eligible

loans through our Online Gold Loan (OGL) facility.

• To facilitate this service, we have partnered with

leading Banks and online payment gateway service

providers.

• e-Sign facility has been launched in September’17.

• Launched in Nov’16 has about 12.7 lakhs downloads.

• Online Gold Loan (OGL) facility available to withdraw

loan amount and renewal, apart from payments.

• Rs.930 crs payments received from 11.84 lakhs

successful transactions so far.

• Updated scheme details available with loan calculator.

• Google maps integrated for easy location of nearest

branch and fix appointment.

• UPI facility has been introduced in Feb’19.

• Paytm Payment gateway has been introduced in

June’19.

• e-Sign facility has been introduced in Jan’18.

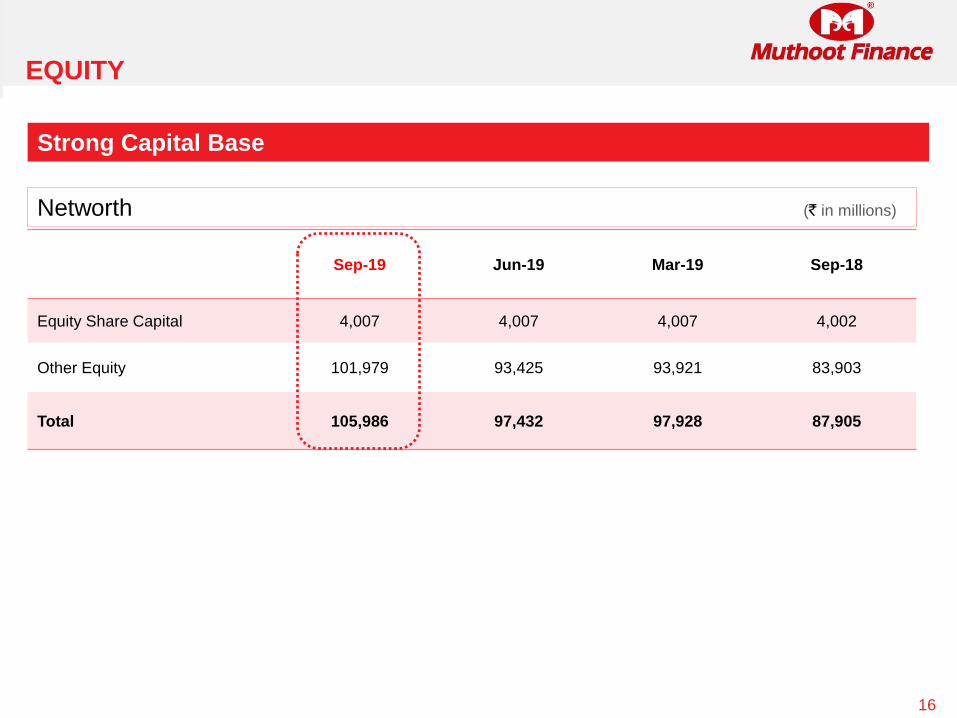

EQUITY

16

Sep-19 Jun-19 Mar-19 Sep-18

Equity Share Capital 4,007 4,007 4,007 4,002

Other Equity 101,979 93,425 93,921 83,903

Total 105,986 97,432 97,928 87,905

Networth (` in millions)

Strong Capital Base

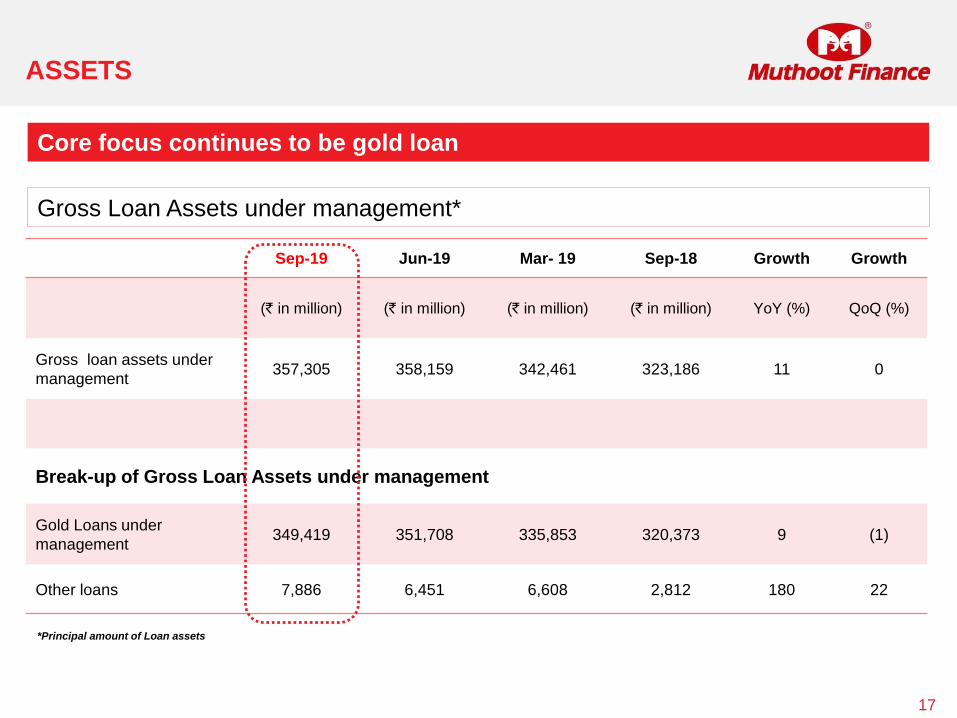

ASSETS

17

Gross Loan Assets under management*

Core focus continues to be gold loan

*Principal amount of Loan assets

Sep-19 Jun-19 Mar- 19 Sep-18 Growth Growth

(` in million) (` in million) (` in million) (` in million) YoY (%) QoQ (%)

Gross loan assets under

management 357,305 358,159 342,461 323,186 11 0

Break-up of Gross Loan Assets under management

Gold Loans under

management 349,419 351,708 335,853 320,373 9 (1)

Other loans 7,886 6,451 6,608 2,812 180 22

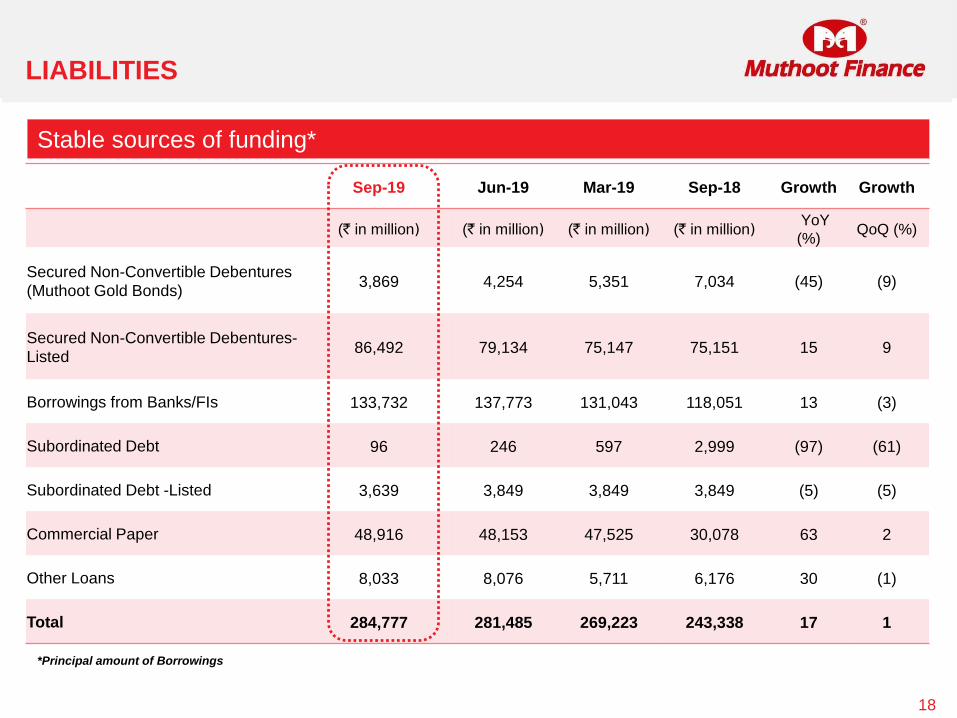

LIABILITIES

Sep-19 Jun-19 Mar-19 Sep-18 Growth Growth

(` in million) (` in million) (` in million) (` in million)YoY

(%)QoQ (%)

Secured Non-Convertible Debentures

(Muthoot Gold Bonds)3,869 4,254 5,351 7,034 (45) (9)

Secured Non-Convertible Debentures-

Listed86,492 79,134 75,147 75,151 15 9

Borrowings from Banks/FIs 133,732 137,773 131,043 118,051 13 (3)

Subordinated Debt 96 246 597 2,999 (97) (61)

Subordinated Debt -Listed 3,639 3,849 3,849 3,849 (5) (5)

Commercial Paper 48,916 48,153 47,525 30,078 63 2

Other Loans 8,033 8,076 5,711 6,176 30 (1)

Total 284,777 281,485 269,223 243,338 17 1

Stable sources of funding*

18

*Principal amount of Borrowings

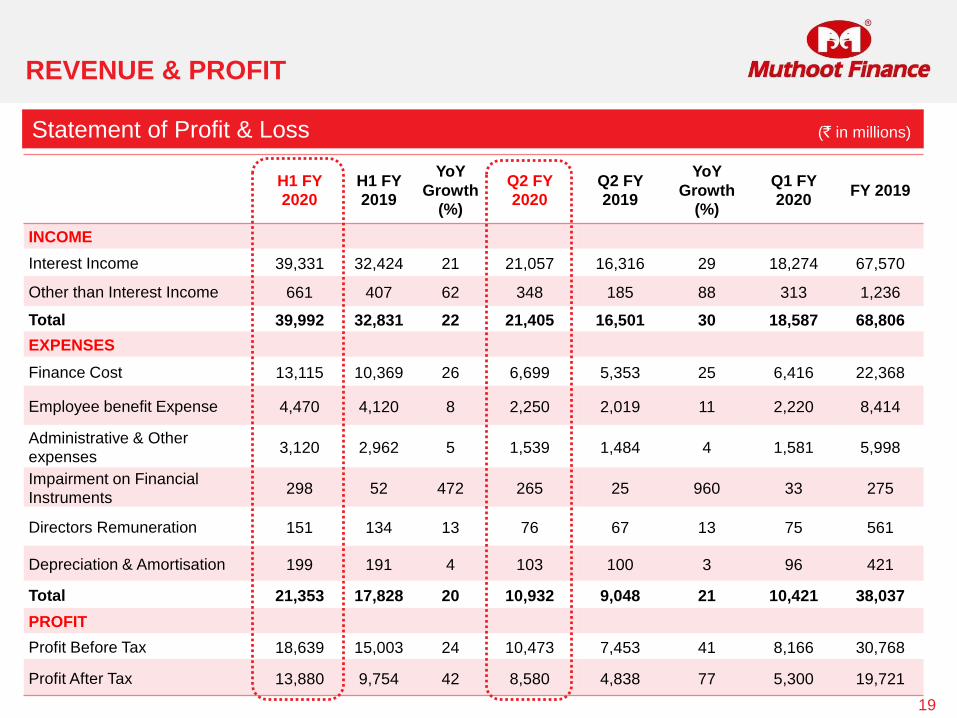

REVENUE & PROFIT

19

H1 FY

2020

H1 FY

2019

YoY

Growth

(%)

Q2 FY

2020

Q2 FY

2019

YoY

Growth

(%)

Q1 FY

2020FY 2019

INCOME

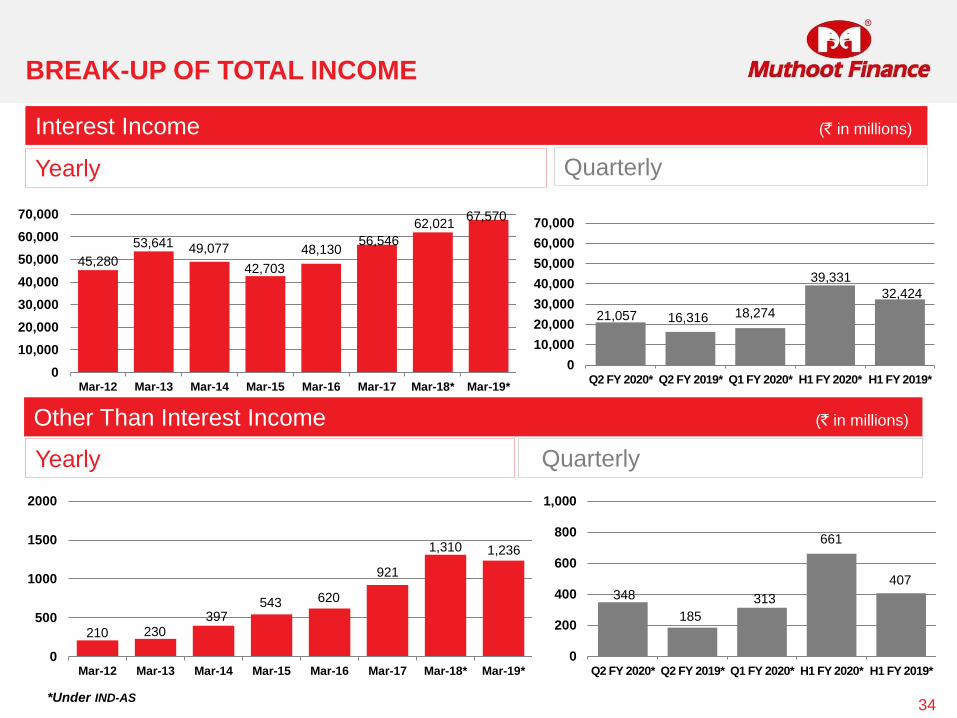

Interest Income 39,331 32,424 21 21,057 16,316 29 18,274 67,570

Other than Interest Income 661 407 62 348 185 88 313 1,236

Total 39,992 32,831 22 21,405 16,501 30 18,587 68,806

EXPENSES

Finance Cost 13,115 10,369 26 6,699 5,353 25 6,416 22,368

Employee benefit Expense 4,470 4,120 8 2,250 2,019 11 2,220 8,414

Administrative & Other

expenses3,120 2,962 5 1,539 1,484 4 1,581 5,998

Impairment on Financial

Instruments298 52 472 265 25 960 33 275

Directors Remuneration 151 134 13 76 67 13 75 561

Depreciation & Amortisation 199 191 4 103 100 3 96 421

Total 21,353 17,828 20 10,932 9,048 21 10,421 38,037

PROFIT

Profit Before Tax 18,639 15,003 24 10,473 7,453 41 8,166 30,768

Profit After Tax 13,880 9,754 42 8,580 4,838 77 5,300 19,721

Statement of Profit & Loss (` in millions)

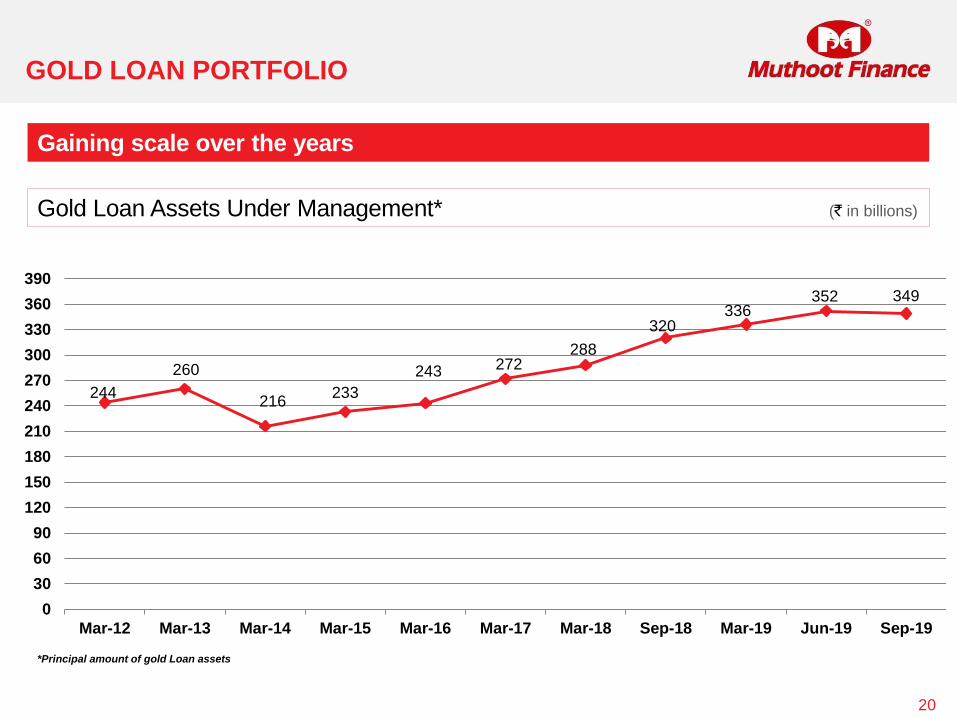

Gold Loan Assets Under Management* (` in billions)

GOLD LOAN PORTFOLIO

20

Gaining scale over the years

244

260

216233

243 272288

320336

352 349

0

30

60

90

120

150

180

210

240

270

300

330

360

390

Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18 Sep-18 Mar-19 Jun-19 Sep-19

*Principal amount of gold Loan assets

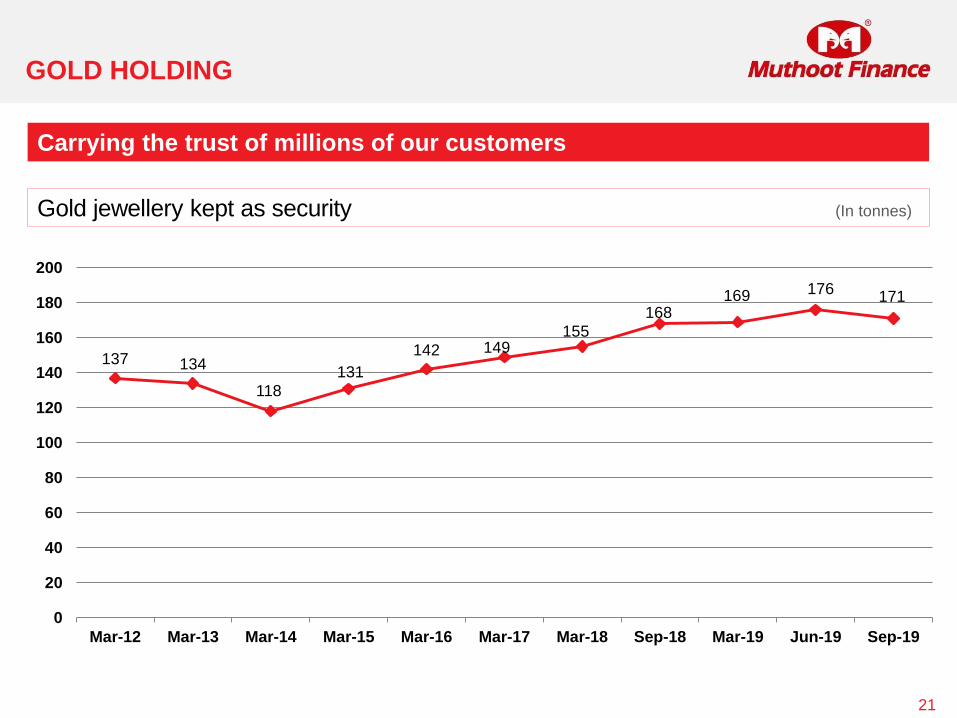

GOLD HOLDING

21

Carrying the trust of millions of our customers

Gold jewellery kept as security (In tonnes)

137 134

118

131

142 149155

168169 176

171

0

20

40

60

80

100

120

140

160

180

200

Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18 Sep-18 Mar-19 Jun-19 Sep-19

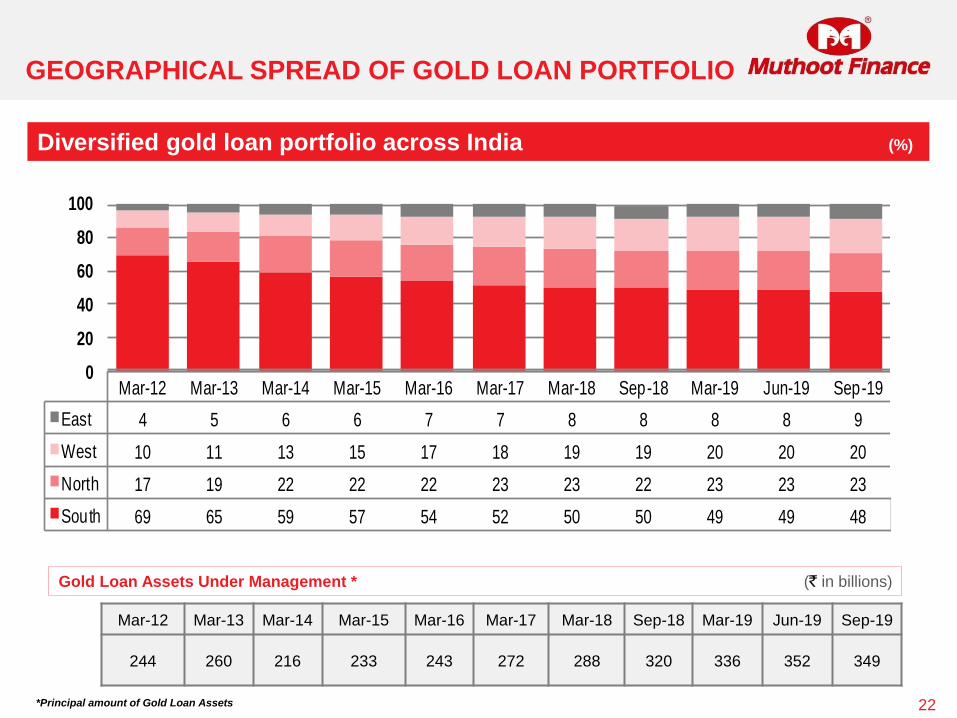

Diversified gold loan portfolio across India (%)

GEOGRAPHICAL SPREAD OF GOLD LOAN PORTFOLIO

22

Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18 Sep-18 Mar-19 Jun-19 Sep-19

244 260 216 233 243 272 288 320 336 352 349

Gold Loan Assets Under Management * (` in billions)

Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18 Sep-18 Mar-19 Jun-19 Sep-19

East 4 5 6 6 7 7 8 8 8 8 9

West 10 11 13 15 17 18 19 19 20 20 20

North 17 19 22 22 22 23 23 22 23 23 23

South 69 65 59 57 54 52 50 50 49 49 48

0

20

40

60

80

100

*Principal amount of Gold Loan Assets

PRODUCTIVITY

23

Average Gold Loan Per Branch * (` in millions)

66.39

63.69

50.6355.01

56.93

63.20

66.70

73.31 74.9778.12 76.96

15

25

35

45

55

65

75

85

Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18 Sep-18 Mar-19 Jun-19 Sep-19

Widening presence with increasing gold loan business per branch

*Principal amount of Gold Loan Assets

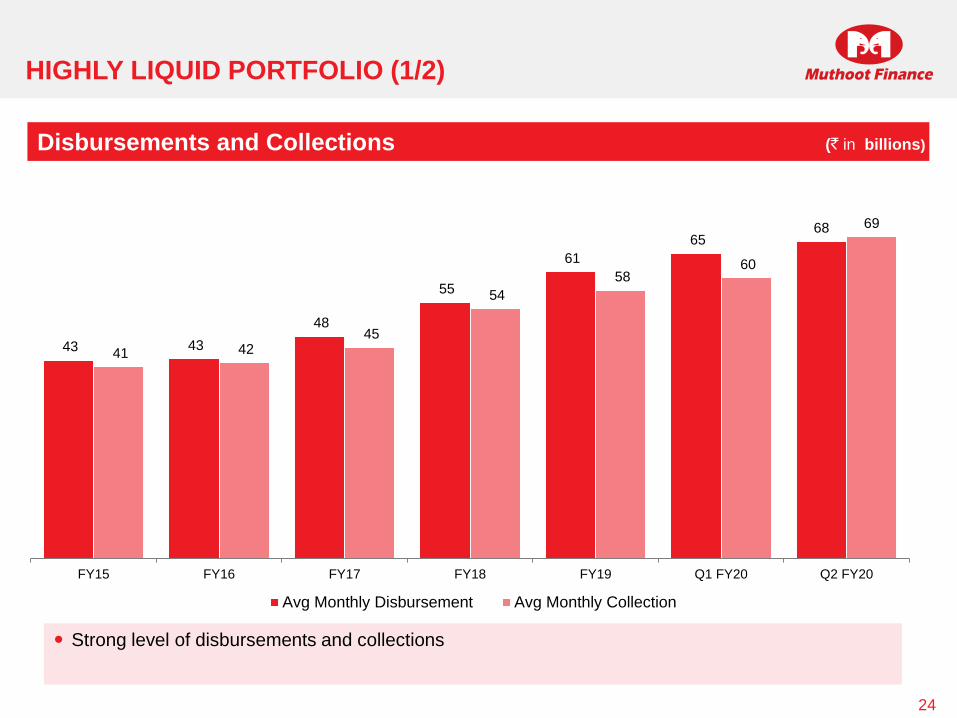

Disbursements and Collections

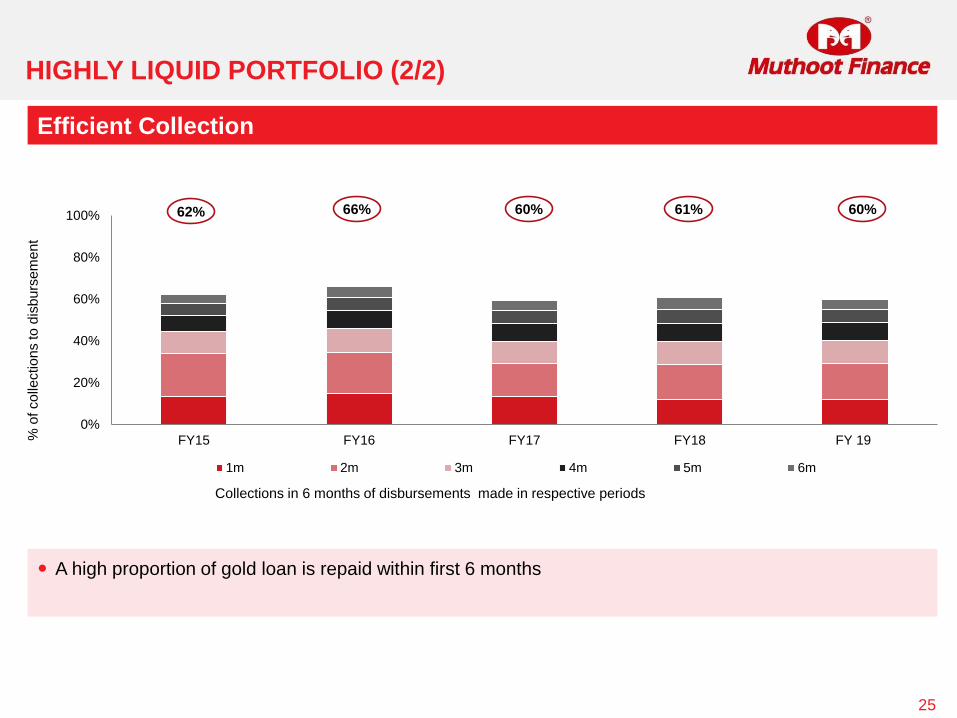

HIGHLY LIQUID PORTFOLIO (1/2)

24

(` in billions)

43 43

48

55

61

65 68

41 42 45

54

58 60

69

FY15 FY16 FY17 FY18 FY19 Q1 FY20 Q2 FY20

Avg Monthly Disbursement Avg Monthly Collection

Strong level of disbursements and collections

HIGHLY LIQUID PORTFOLIO (2/2)

25

0%

20%

40%

60%

80%

100%

FY15 FY16 FY17 FY18 FY 19

1m 2m 3m 4m 5m 6m

62% 66% 60% 61% 60%

A high proportion of gold loan is repaid within first 6 months

Efficient Collection

Collections in 6 months of disbursements made in respective periods

% o

f co

llectio

ns to

dis

bu

rse

me

nt

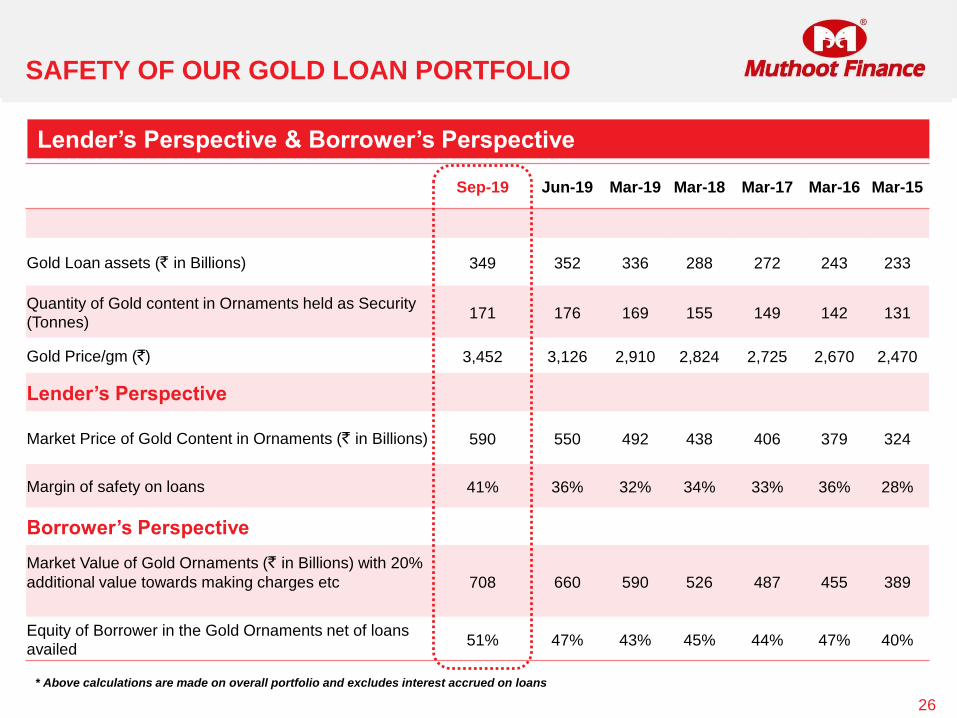

SAFETY OF OUR GOLD LOAN PORTFOLIO

Sep-19 Jun-19 Mar-19 Mar-18 Mar-17 Mar-16 Mar-15

Gold Loan assets (` in Billions) 349 352 336 288 272 243 233

Quantity of Gold content in Ornaments held as Security

(Tonnes)171 176 169 155 149 142 131

Gold Price/gm (`) 3,452 3,126 2,910 2,824 2,725 2,670 2,470

Lender’s Perspective

Market Price of Gold Content in Ornaments (` in Billions) 590 550 492 438 406 379 324

Margin of safety on loans 41% 36% 32% 34% 33% 36% 28%

Borrower’s Perspective

Market Value of Gold Ornaments (` in Billions) with 20%

additional value towards making charges etc 708 660 590 526 487 455 389

Equity of Borrower in the Gold Ornaments net of loans

availed 51% 47% 43% 45% 44% 47% 40%

Lender’s Perspective & Borrower’s Perspective

26

* Above calculations are made on overall portfolio and excludes interest accrued on loans

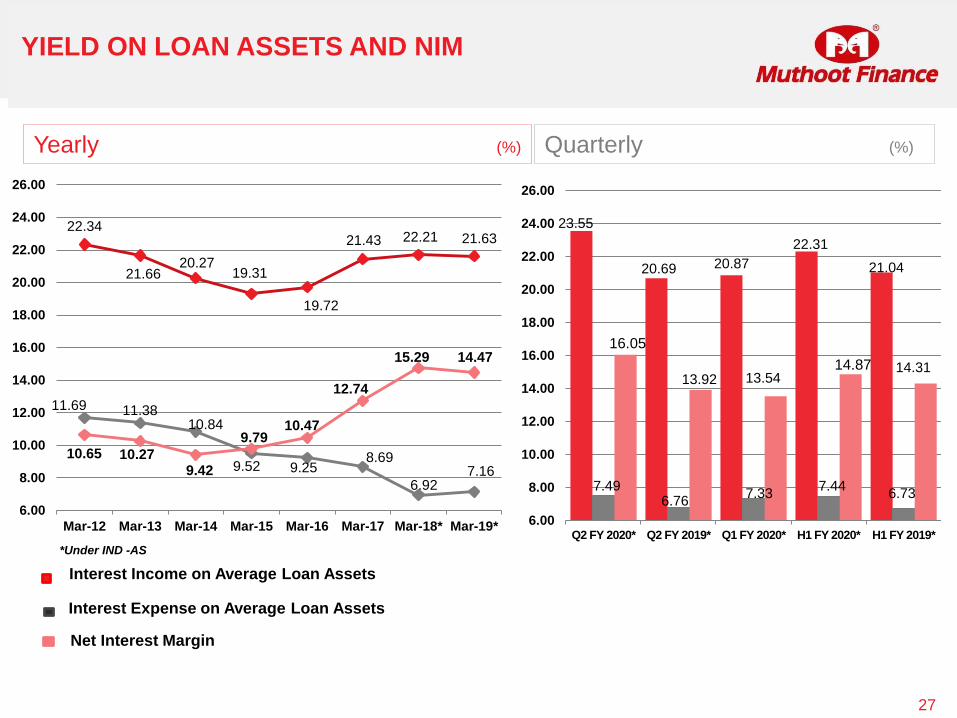

YIELD ON LOAN ASSETS AND NIM

27

22.34

21.6620.27

19.31

19.72

21.43 22.21 21.63

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

22.00

24.00

26.00

Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18* Mar-19*

10.65

15.29

9.79

9.42

10.47

11.69

9.25

11.38

9.52

10.84

10.27 8.69

12.74

7.16

14.47

6.92

23.55

20.69 20.87

22.31

21.04

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

22.00

24.00

26.00

Q2 FY 2020* Q2 FY 2019* Q1 FY 2020* H1 FY 2020* H1 FY 2019*

7.447.49

13.9214.87

16.05

6.767.33

13.54

6.73

14.31

Yearly (%) Quarterly (%)

Interest Income on Average Loan Assets

Interest Expense on Average Loan Assets

Net Interest Margin

*Under IND -AS

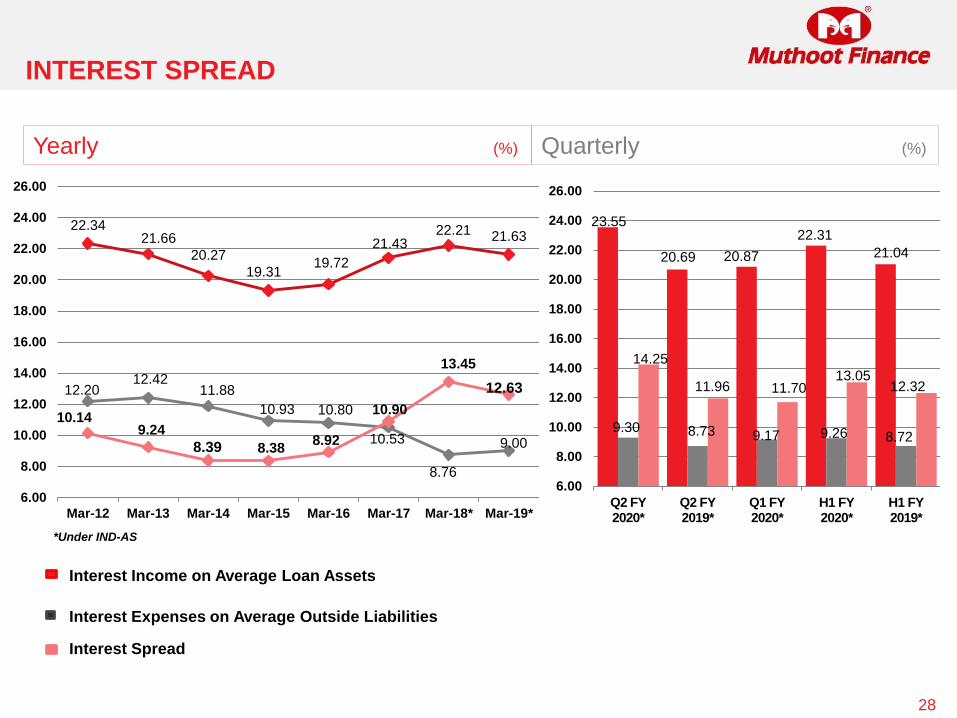

INTEREST SPREAD

28

22.3421.66

20.27

19.3119.72

21.4322.21 21.63

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

22.00

24.00

26.00

Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18* Mar-19*

13.45

10.149.24

8.39 9.00

8.76

12.2012.42

11.88

10.80

8.92 10.53

10.90

12.63

23.55

20.69 20.87

22.31

21.04

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

22.00

24.00

26.00

Q2 FY 2020*

Q2 FY 2019*

Q1 FY 2020*

H1 FY 2020*

H1 FY 2019*

9.30

14.25

8.728.73

11.96

9.17

11.7013.05

12.32

Yearly (%) Quarterly (%)

Interest Income on Average Loan Assets

Interest Expenses on Average Outside Liabilities

Interest Spread

8.38

10.93

*Under IND-AS

9.26

RETURN ON AVERAGE LOAN ASSETS

29

Yearly (%) Quarterly (%)

Attractive returns over the years

4.404.05

3.223.03 3.32

4.47

6.36

6.31

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18* Mar-19*

9.59

6.11 6.05

7.87

6.33

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

Q2 FY2020*

Q2 FY2019*

Q1 FY2020*

H1 FY2020*

H1 FY2019*

*Under IND-AS

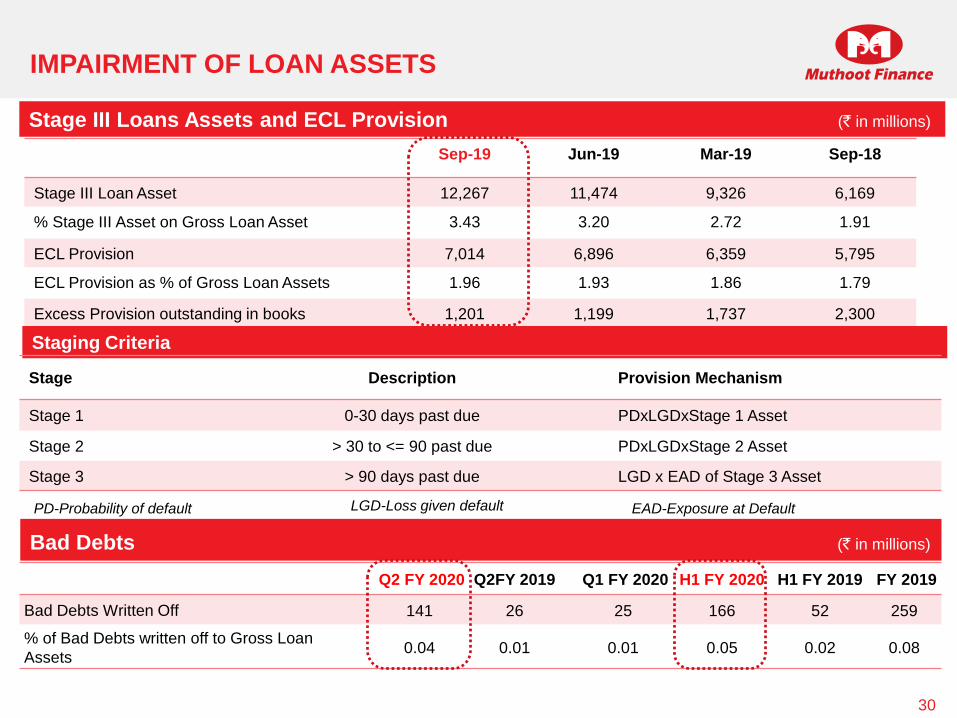

IMPAIRMENT OF LOAN ASSETS

30

Sep-19 Jun-19 Mar-19 Sep-18

Stage III Loan Asset 12,267 11,474 9,326 6,169

% Stage III Asset on Gross Loan Asset 3.43 3.20 2.72 1.91

ECL Provision 7,014 6,896 6,359 5,795

ECL Provision as % of Gross Loan Assets 1.96 1.93 1.86 1.79

Excess Provision outstanding in books 1,201 1,199 1,737 2,300

Stage III Loans Assets and ECL Provision (` in millions)

Staging Criteria

Stage Description Provision Mechanism

Stage 1 0-30 days past due PDxLGDxStage 1 Asset

Stage 2 > 30 to <= 90 past due PDxLGDxStage 2 Asset

Stage 3 > 90 days past due LGD x EAD of Stage 3 Asset

PD-Probability of default LGD-Loss given default EAD-Exposure at Default

Bad Debts (` in millions)

Q2 FY 2020 Q2FY 2019 Q1 FY 2020 H1 FY 2020 H1 FY 2019 FY 2019

Bad Debts Written Off 141 26 25 166 52 259

% of Bad Debts written off to Gross Loan

Assets0.04 0.01 0.01 0.05 0.02 0.08

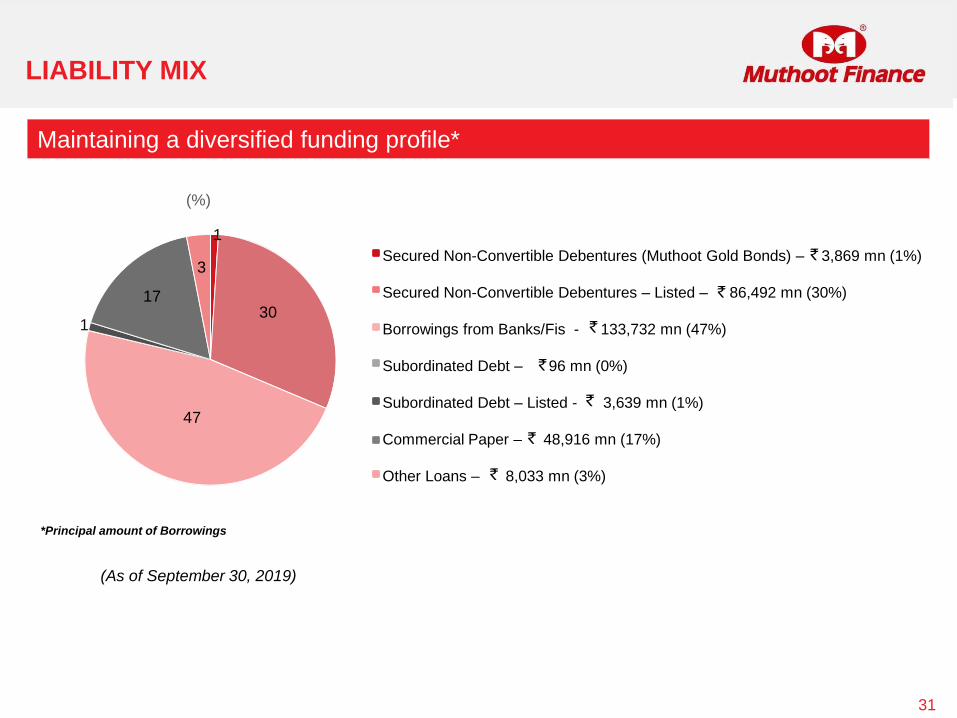

LIABILITY MIX

31

Maintaining a diversified funding profile*

(%)

(As of September 30, 2019)

30

1

Secured Non-Convertible Debentures (Muthoot Gold Bonds) – 3,869 mn (1%)

Secured Non-Convertible Debentures – Listed – 86,492 mn (30%)

Borrowings from Banks/Fis - 133,732 mn (47%)

Subordinated Debt – 96 mn (0%)

Subordinated Debt – Listed - 3,639 mn (1%)

Commercial Paper – 48,916 mn (17%)

Other Loans – 8,033 mn (3%)

47

3

1

`

`

`

`

`

`

`

17

*Principal amount of Borrowings

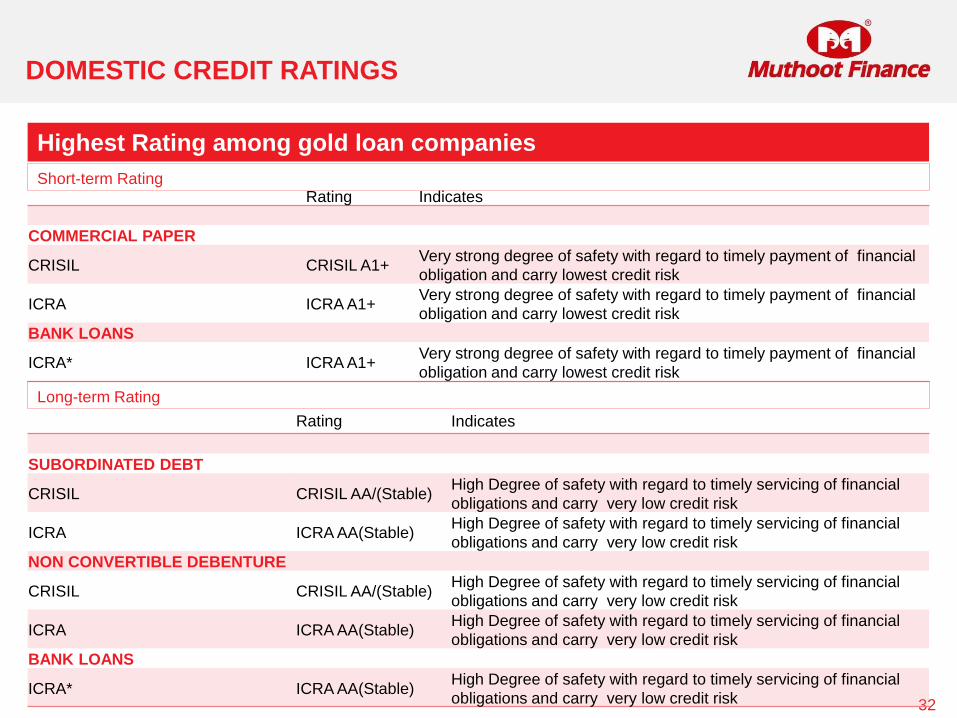

DOMESTIC CREDIT RATINGS

32

Rating Indicates

COMMERCIAL PAPER

CRISIL CRISIL A1+Very strong degree of safety with regard to timely payment of financial

obligation and carry lowest credit risk

ICRA ICRA A1+Very strong degree of safety with regard to timely payment of financial

obligation and carry lowest credit risk

BANK LOANS

ICRA* ICRA A1+Very strong degree of safety with regard to timely payment of financial

obligation and carry lowest credit risk

Long-term Rating

Rating Indicates

SUBORDINATED DEBT

CRISIL CRISIL AA/(Stable)High Degree of safety with regard to timely servicing of financial

obligations and carry very low credit risk

ICRA ICRA AA(Stable)High Degree of safety with regard to timely servicing of financial

obligations and carry very low credit risk

NON CONVERTIBLE DEBENTURE

CRISIL CRISIL AA/(Stable)High Degree of safety with regard to timely servicing of financial

obligations and carry very low credit risk

ICRA ICRA AA(Stable)High Degree of safety with regard to timely servicing of financial

obligations and carry very low credit risk

BANK LOANS

ICRA* ICRA AA(Stable)High Degree of safety with regard to timely servicing of financial

obligations and carry very low credit risk

Short-term Rating

Highest Rating among gold loan companies

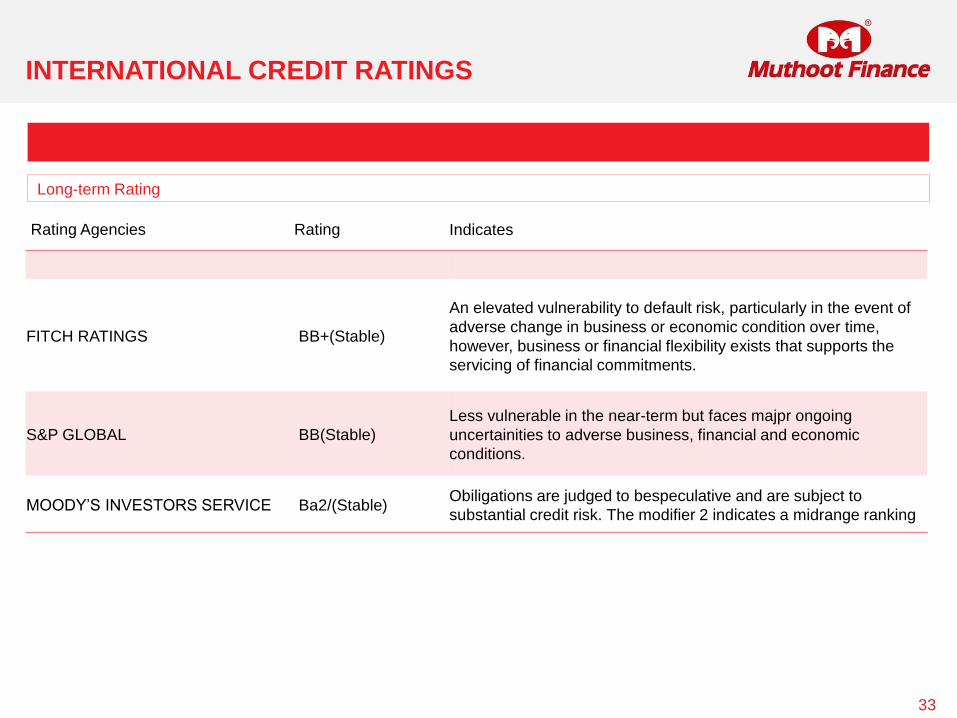

INTERNATIONAL CREDIT RATINGS

33

Long-term Rating

Rating Agencies Rating Indicates

FITCH RATINGS BB+(Stable)

An elevated vulnerability to default risk, particularly in the event of

adverse change in business or economic condition over time,

however, business or financial flexibility exists that supports the

servicing of financial commitments.

S&P GLOBAL BB(Stable)

Less vulnerable in the near-term but faces majpr ongoing

uncertainities to adverse business, financial and economic

conditions.

MOODY’S INVESTORS SERVICE Ba2/(Stable)Obiligations are judged to bespeculative and are subject to

substantial credit risk. The modifier 2 indicates a midrange ranking

Interest Income (` in millions)

BREAK-UP OF TOTAL INCOME

34

Other Than Interest Income (` in millions)

21,057 16,316 18,274

39,331

32,424

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Q2 FY 2020* Q2 FY 2019* Q1 FY 2020* H1 FY 2020* H1 FY 2019*

45,280

53,641 49,077

42,703

48,13056,546

62,02167,570

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18* Mar-19*

210 230397

543 620

921

1,310 1,236

0

500

1000

1500

2000

Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18* Mar-19*

348

185

313

661

407

0

200

400

600

800

1,000

Q2 FY 2020* Q2 FY 2019* Q1 FY 2020* H1 FY 2020* H1 FY 2019*

Yearly Quarterly

Yearly Quarterly

*Under IND-AS

OPERATING EXPENSES TO AVERAGE LOAN ASSETS

35

4.024.08

4.46

5.01 5.10

5.635.43

4.89

2.50

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

7.00

7.50

8.00

Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18* Mar-19*

4.64 4.55 4.47 4.57 4.72

2.50

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

7.00

7.50

8.00

Q2 FY 2020*Q2 FY 2019*Q1 FY 2020*H1 FY 2020*H1 FY 2019*

Operational efficiency over the years

Yearly (%) Quarterly (%)

*Under IND AS

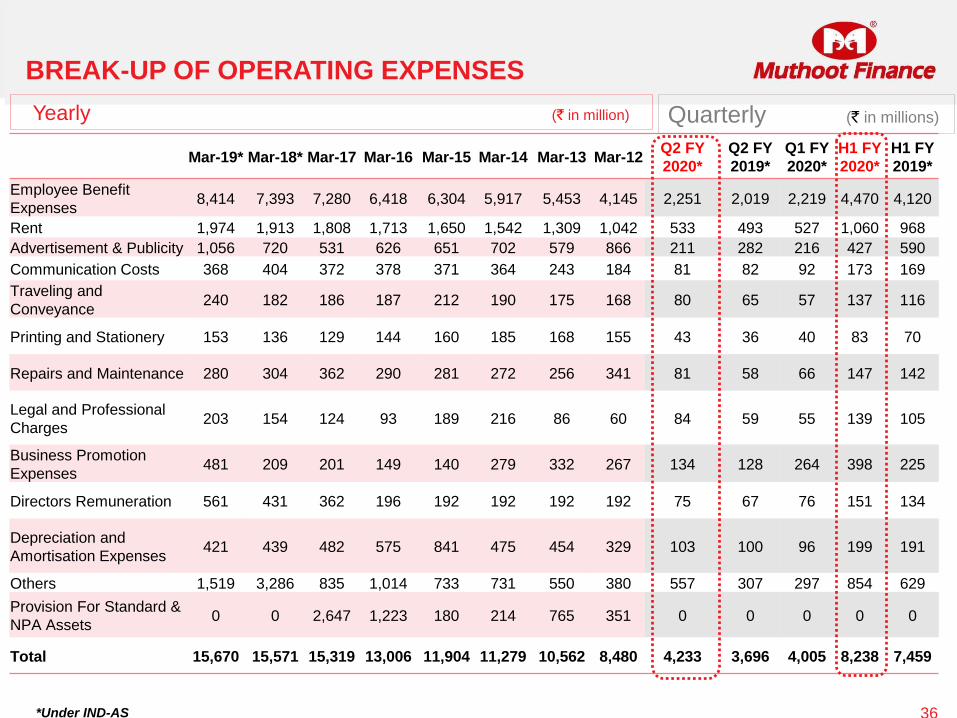

BREAK-UP OF OPERATING EXPENSES

Mar-19* Mar-18* Mar-17 Mar-16 Mar-15 Mar-14 Mar-13 Mar-12Q2 FY

2020*

Q2 FY

2019*

Q1 FY

2020*

H1 FY

2020*

H1 FY

2019*

Employee Benefit

Expenses8,414 7,393 7,280 6,418 6,304 5,917 5,453 4,145 2,251 2,019 2,219 4,470 4,120

Rent 1,974 1,913 1,808 1,713 1,650 1,542 1,309 1,042 533 493 527 1,060 968

Advertisement & Publicity 1,056 720 531 626 651 702 579 866 211 282 216 427 590

Communication Costs 368 404 372 378 371 364 243 184 81 82 92 173 169

Traveling and

Conveyance240 182 186 187 212 190 175 168 80 65 57 137 116

Printing and Stationery 153 136 129 144 160 185 168 155 43 36 40 83 70

Repairs and Maintenance 280 304 362 290 281 272 256 341 81 58 66 147 142

Legal and Professional

Charges203 154 124 93 189 216 86 60 84 59 55 139 105

Business Promotion

Expenses481 209 201 149 140 279 332 267 134 128 264 398 225

Directors Remuneration 561 431 362 196 192 192 192 192 75 67 76 151 134

Depreciation and

Amortisation Expenses421 439 482 575 841 475 454 329 103 100 96 199 191

Others 1,519 3,286 835 1,014 733 731 550 380 557 307 297 854 629

Provision For Standard &

NPA Assets0 0 2,647 1,223 180 214 765 351 0 0 0 0 0

Total 15,670 15,571 15,319 13,006 11,904 11,279 10,562 8,480 4,233 3,696 4,005 8,238 7,459

Yearly (` in million) Quarterly (` in millions)

36*Under IND-AS

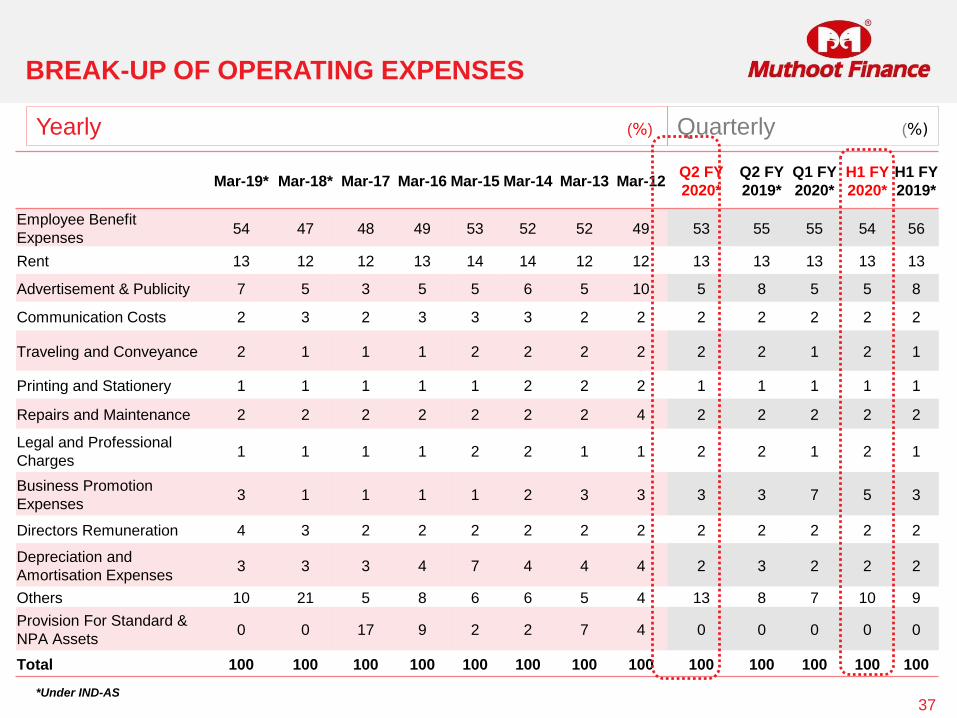

BREAK-UP OF OPERATING EXPENSES

Mar-19* Mar-18* Mar-17 Mar-16 Mar-15 Mar-14 Mar-13 Mar-12Q2 FY

2020*

Q2 FY

2019*

Q1 FY

2020*

H1 FY

2020*

H1 FY

2019*

Employee Benefit

Expenses54 47 48 49 53 52 52 49 53 55 55 54 56

Rent 13 12 12 13 14 14 12 12 13 13 13 13 13

Advertisement & Publicity 7 5 3 5 5 6 5 10 5 8 5 5 8

Communication Costs 2 3 2 3 3 3 2 2 2 2 2 2 2

Traveling and Conveyance 2 1 1 1 2 2 2 2 2 2 1 2 1

Printing and Stationery 1 1 1 1 1 2 2 2 1 1 1 1 1

Repairs and Maintenance 2 2 2 2 2 2 2 4 2 2 2 2 2

Legal and Professional

Charges1 1 1 1 2 2 1 1 2 2 1 2 1

Business Promotion

Expenses3 1 1 1 1 2 3 3 3 3 7 5 3

Directors Remuneration 4 3 2 2 2 2 2 2 2 2 2 2 2

Depreciation and

Amortisation Expenses3 3 3 4 7 4 4 4 2 3 2 2 2

Others 10 21 5 8 6 6 5 4 13 8 7 10 9

Provision For Standard &

NPA Assets0 0 17 9 2 2 7 4 0 0 0 0 0

Total 100 100 100 100 100 100 100 100 100 100 100 100 100

Yearly (%) Quarterly (%)

37*Under IND-AS

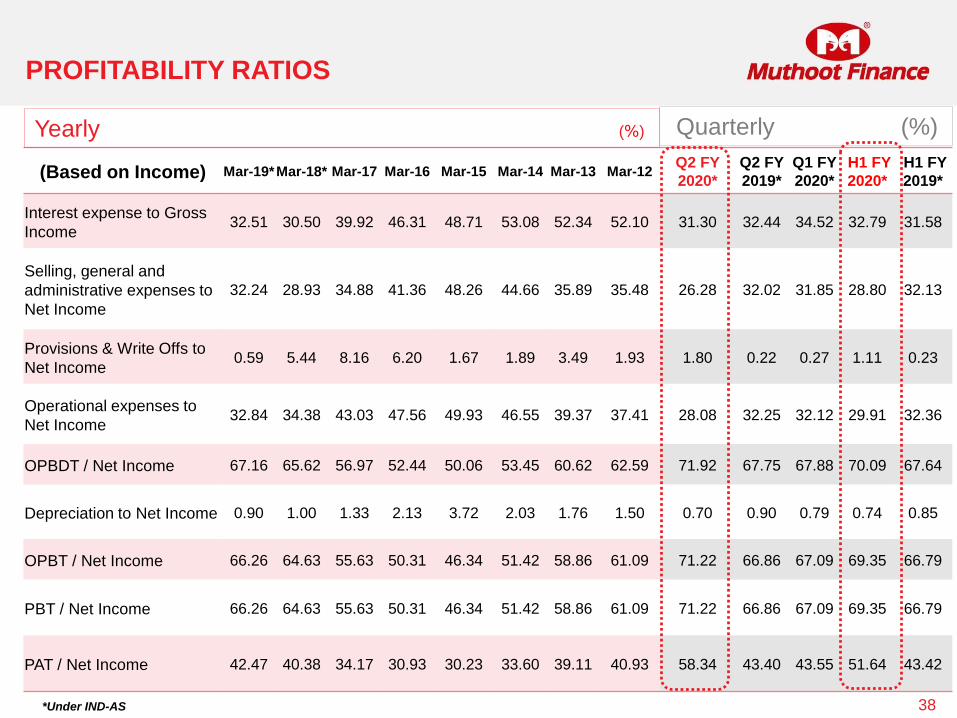

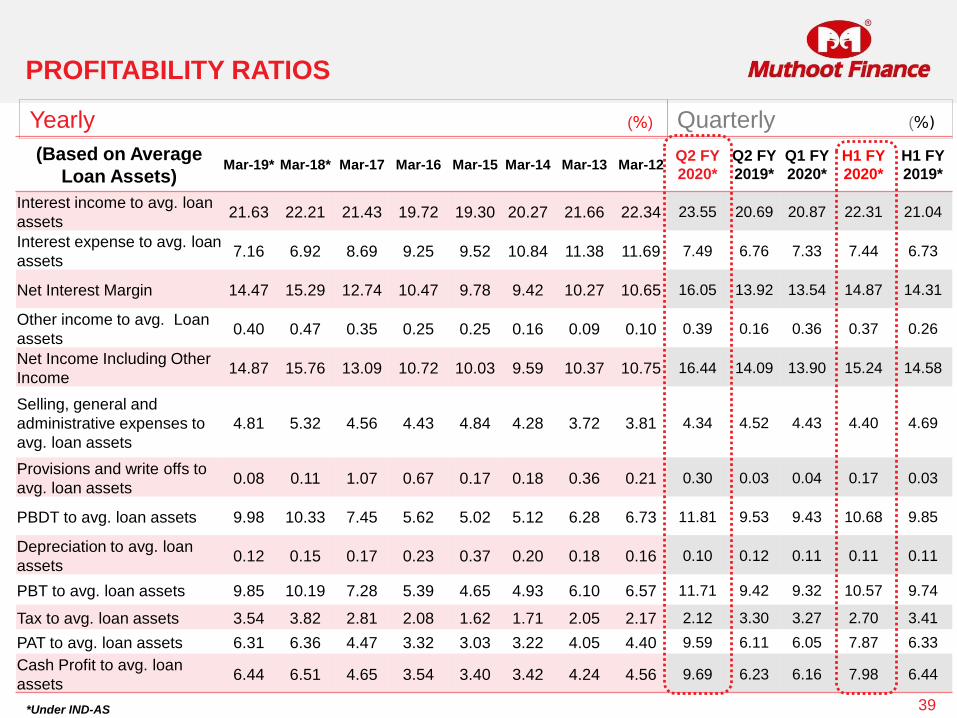

PROFITABILITY RATIOS

(Based on Income) Mar-19*Mar-18* Mar-17 Mar-16 Mar-15 Mar-14 Mar-13 Mar-12Q2 FY

2020*

Q2 FY

2019*

Q1 FY

2020*

H1 FY

2020*

H1 FY

2019*

Interest expense to Gross

Income32.51 30.50 39.92 46.31 48.71 53.08 52.34 52.10 31.30 32.44 34.52 32.79 31.58

Selling, general and

administrative expenses to

Net Income

32.24 28.93 34.88 41.36 48.26 44.66 35.89 35.48 26.28 32.02 31.85 28.80 32.13

Provisions & Write Offs to

Net Income0.59 5.44 8.16 6.20 1.67 1.89 3.49 1.93 1.80 0.22 0.27 1.11 0.23

Operational expenses to

Net Income32.84 34.38 43.03 47.56 49.93 46.55 39.37 37.41 28.08 32.25 32.12 29.91 32.36

OPBDT / Net Income 67.16 65.62 56.97 52.44 50.06 53.45 60.62 62.59 71.92 67.75 67.88 70.09 67.64

Depreciation to Net Income 0.90 1.00 1.33 2.13 3.72 2.03 1.76 1.50 0.70 0.90 0.79 0.74 0.85

OPBT / Net Income 66.26 64.63 55.63 50.31 46.34 51.42 58.86 61.09 71.22 66.86 67.09 69.35 66.79

PBT / Net Income 66.26 64.63 55.63 50.31 46.34 51.42 58.86 61.09 71.22 66.86 67.09 69.35 66.79

PAT / Net Income 42.47 40.38 34.17 30.93 30.23 33.60 39.11 40.93 58.34 43.40 43.55 51.64 43.42

Yearly (%) Quarterly (%)

38*Under IND-AS

(Based on Average

Loan Assets)Mar-19* Mar-18* Mar-17 Mar-16 Mar-15 Mar-14 Mar-13 Mar-12

Q2 FY

2020*

Q2 FY

2019*

Q1 FY

2020*

H1 FY

2020*

H1 FY

2019*

Interest income to avg. loan

assets21.63 22.21 21.43 19.72 19.30 20.27 21.66 22.34 23.55 20.69 20.87 22.31 21.04

Interest expense to avg. loan

assets7.16 6.92 8.69 9.25 9.52 10.84 11.38 11.69 7.49 6.76 7.33 7.44 6.73

Net Interest Margin 14.47 15.29 12.74 10.47 9.78 9.42 10.27 10.65 16.05 13.92 13.54 14.87 14.31

Other income to avg. Loan

assets0.40 0.47 0.35 0.25 0.25 0.16 0.09 0.10 0.39 0.16 0.36 0.37 0.26

Net Income Including Other

Income14.87 15.76 13.09 10.72 10.03 9.59 10.37 10.75 16.44 14.09 13.90 15.24 14.58

Selling, general and

administrative expenses to

avg. loan assets

4.81 5.32 4.56 4.43 4.84 4.28 3.72 3.81 4.34 4.52 4.43 4.40 4.69

Provisions and write offs to

avg. loan assets0.08 0.11 1.07 0.67 0.17 0.18 0.36 0.21 0.30 0.03 0.04 0.17 0.03

PBDT to avg. loan assets 9.98 10.33 7.45 5.62 5.02 5.12 6.28 6.73 11.81 9.53 9.43 10.68 9.85

Depreciation to avg. loan

assets0.12 0.15 0.17 0.23 0.37 0.20 0.18 0.16 0.10 0.12 0.11 0.11 0.11

PBT to avg. loan assets 9.85 10.19 7.28 5.39 4.65 4.93 6.10 6.57 11.71 9.42 9.32 10.57 9.74

Tax to avg. loan assets 3.54 3.82 2.81 2.08 1.62 1.71 2.05 2.17 2.12 3.30 3.27 2.70 3.41

PAT to avg. loan assets 6.31 6.36 4.47 3.32 3.03 3.22 4.05 4.40 9.59 6.11 6.05 7.87 6.33

Cash Profit to avg. loan

assets6.44 6.51 4.65 3.54 3.40 3.42 4.24 4.56 9.69 6.23 6.16 7.98 6.44

Yearly (%) Quarterly (%)

39

PROFITABILITY RATIOS

*Under IND-AS

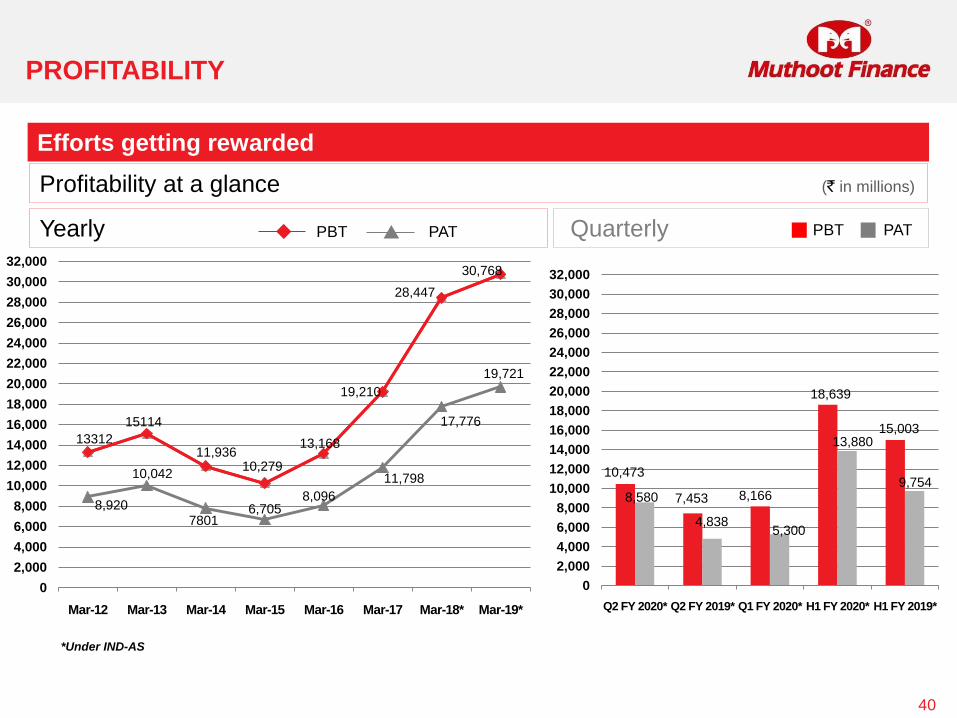

PROFITABILITY

40

Profitability at a glance (` in millions)

Efforts getting rewarded

13312

15114

11,936

28,447

13,168

10,279

8,920

10,042

78016,705

8,096

11,798

17,776

19,721

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

26,000

28,000

30,000

32,000

Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18* Mar-19*

19,210

30,768

10,473

7,453 8,166

18,639

9,7548,580

4,8385,300

13,88015,003

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

26,000

28,000

30,000

32,000

Q2 FY 2020* Q2 FY 2019* Q1 FY 2020* H1 FY 2020* H1 FY 2019*

Yearly QuarterlyPBT PAT PATPBT

*Under IND-AS

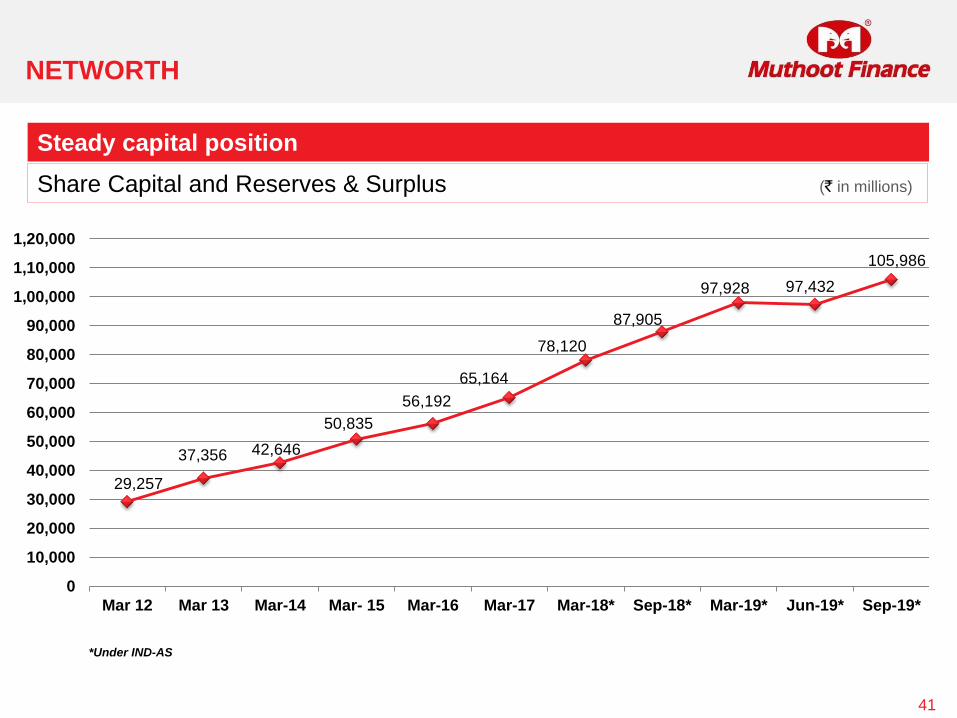

NETWORTH

41

Share Capital and Reserves & Surplus (` in millions)

Steady capital position

29,257

37,356 42,646

50,835

56,192

65,164

78,120

87,905

97,928 97,432

105,986

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

1,00,000

1,10,000

1,20,000

Mar 12 Mar 13 Mar-14 Mar- 15 Mar-16 Mar-17 Mar-18* Sep-18* Mar-19* Jun-19* Sep-19*

*Under IND-AS

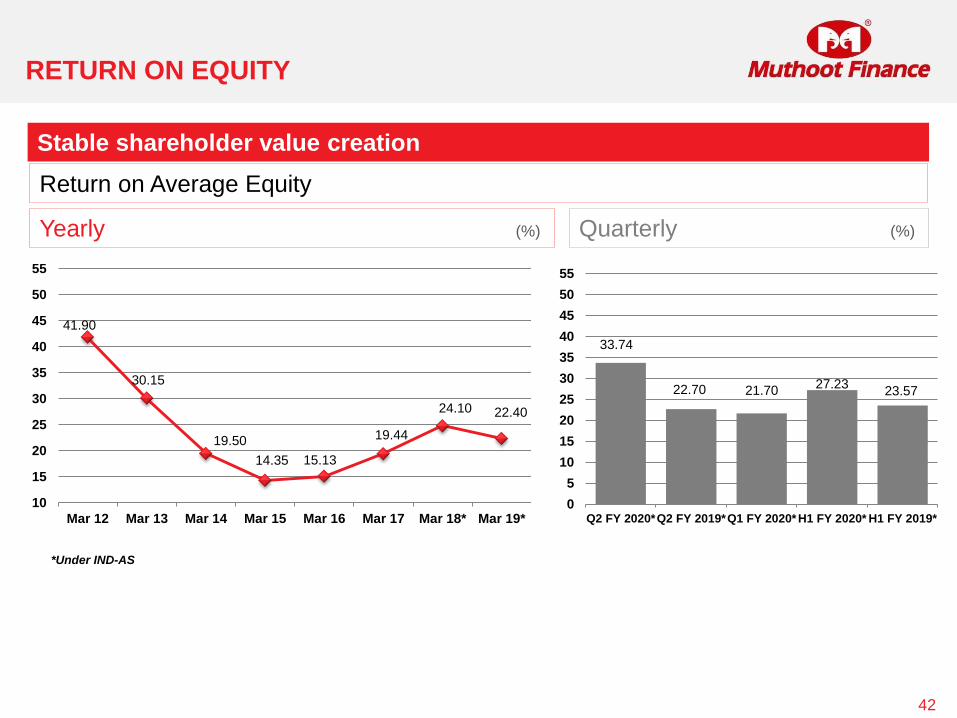

RETURN ON EQUITY

42

Return on Average Equity

Stable shareholder value creation

41.90

30.15

19.50

14.35 15.13

19.44

24.10 22.40

10

15

20

25

30

35

40

45

50

55

Mar 12 Mar 13 Mar 14 Mar 15 Mar 16 Mar 17 Mar 18* Mar 19*

33.74

22.70 21.7027.23

23.57

0

5

10

15

20

25

30

35

40

45

50

55

Q2 FY 2020*Q2 FY 2019*Q1 FY 2020* H1 FY 2020* H1 FY 2019*

Yearly (%) Quarterly (%)

*Under IND-AS

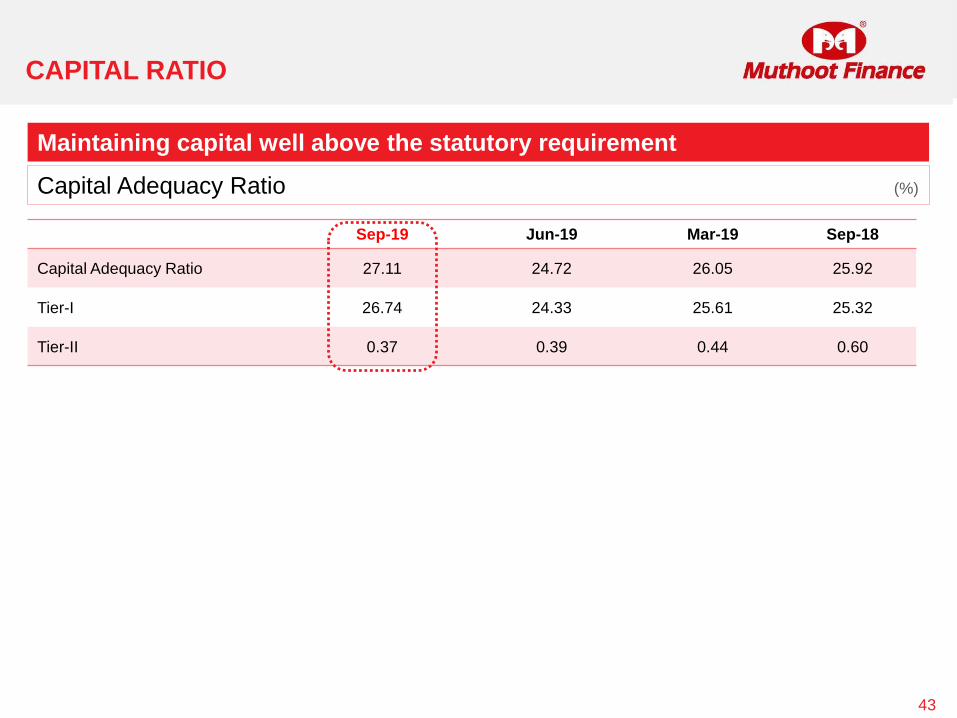

CAPITAL RATIO

43

Sep-19 Jun-19 Mar-19 Sep-18

Capital Adequacy Ratio 27.11 24.72 26.05 25.92

Tier-I 26.74 24.33 25.61 25.32

Tier-II 0.37 0.39 0.44 0.60

Maintaining capital well above the statutory requirement

Capital Adequacy Ratio (%)

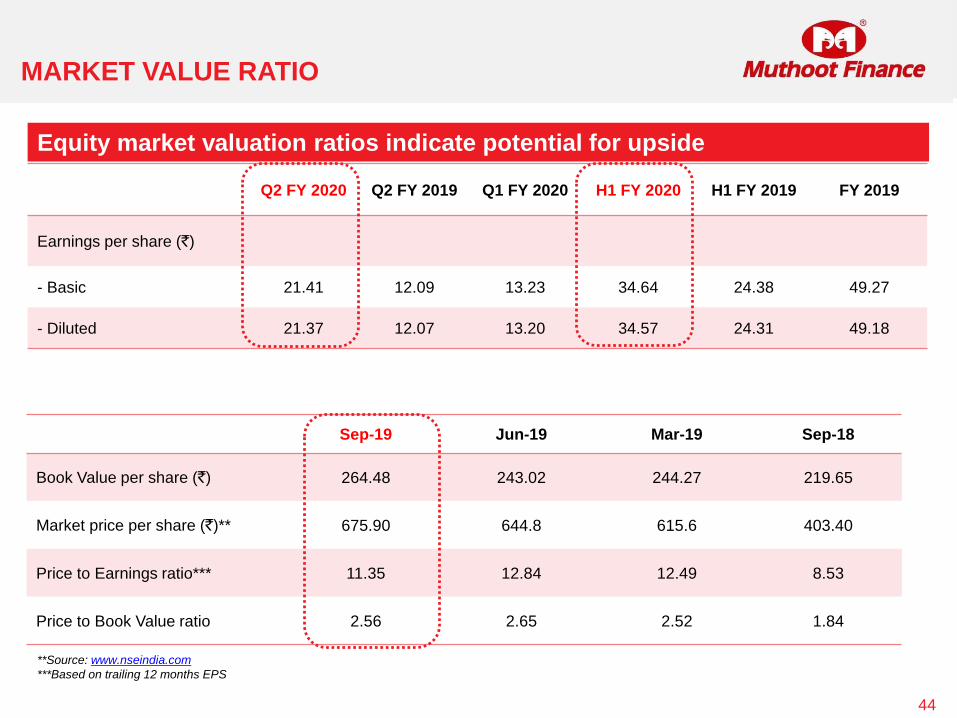

MARKET VALUE RATIO

44

Q2 FY 2020 Q2 FY 2019 Q1 FY 2020 H1 FY 2020 H1 FY 2019 FY 2019

Earnings per share (`)

- Basic 21.41 12.09 13.23 34.64 24.38 49.27

- Diluted 21.37 12.07 13.20 34.57 24.31 49.18

**Source: www.nseindia.com

***Based on trailing 12 months EPS

Equity market valuation ratios indicate potential for upside

Sep-19 Jun-19 Mar-19 Sep-18

Book Value per share (`) 264.48 243.02 244.27 219.65

Market price per share (`)** 675.90 644.8 615.6 403.40

Price to Earnings ratio*** 11.35 12.84 12.49 8.53

Price to Book Value ratio 2.56 2.65 2.52 1.84

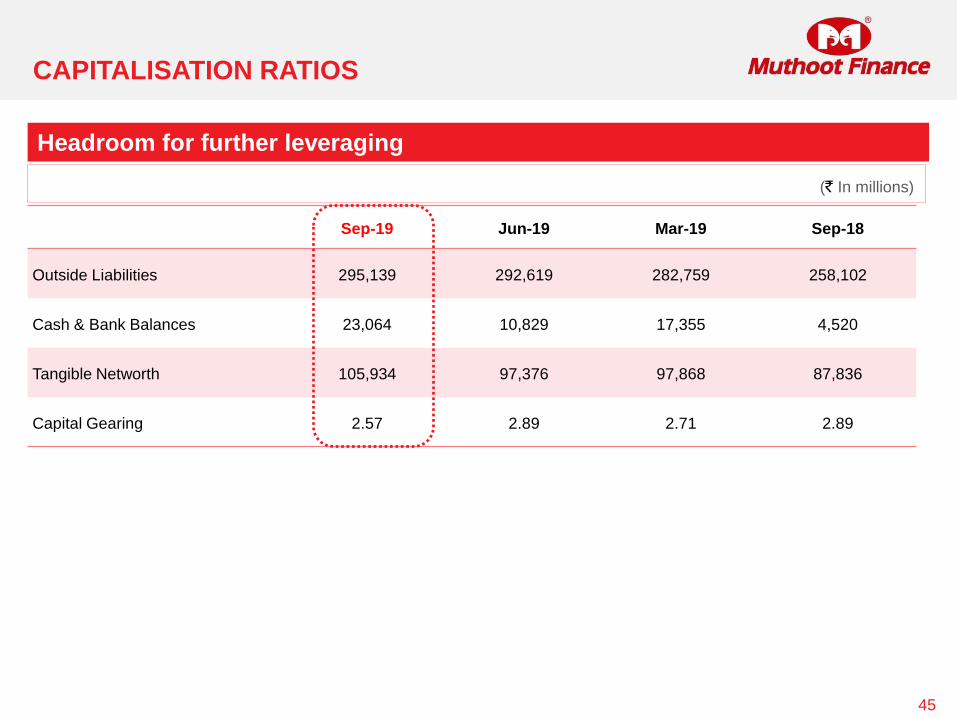

CAPITALISATION RATIOS

45

Sep-19 Jun-19 Mar-19 Sep-18

Outside Liabilities 295,139 292,619 282,759 258,102

Cash & Bank Balances 23,064 10,829 17,355 4,520

Tangible Networth 105,934 97,376 97,868 87,836

Capital Gearing 2.57 2.89 2.71 2.89

(` In millions)

Headroom for further leveraging

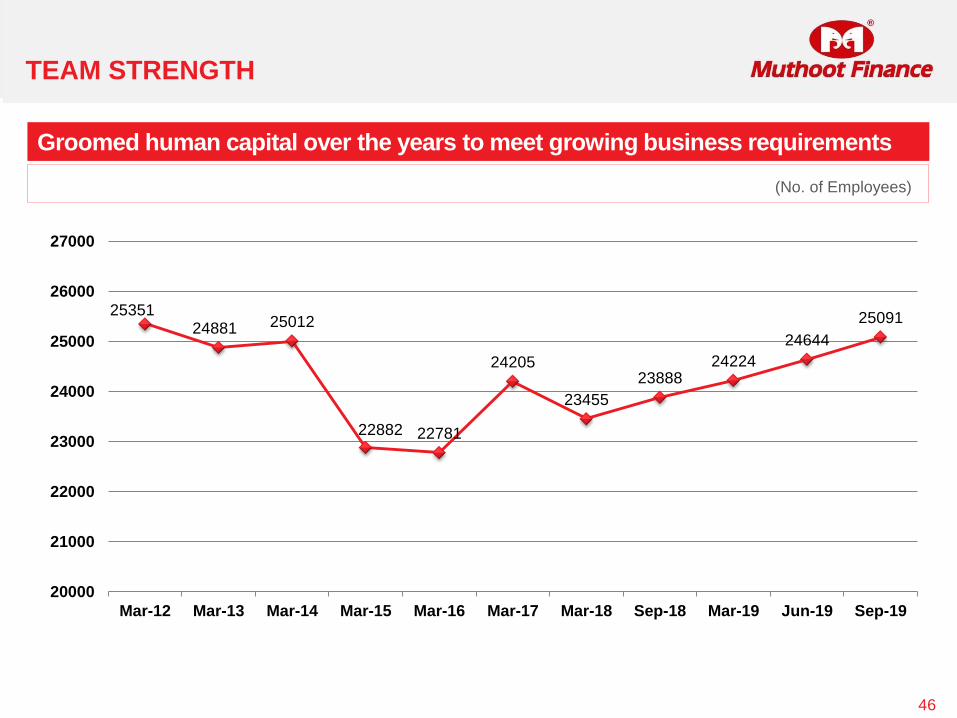

TEAM STRENGTH

46

2535124881 25012

22882 22781

24205

23455

2388824224

24644

25091

20000

21000

22000

23000

24000

25000

26000

27000

Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18 Sep-18 Mar-19 Jun-19 Sep-19

Groomed human capital over the years to meet growing business requirements

(No. of Employees)

OUR SUBSIDIARY

47

ASIA ASSET FINANCE PLC – AN OVERVIEW

48

Asia Asset Finance PLC, (AAF) Colombo, Sri Lanka became a foreign subsidiary of Muthoot Finance on

December 31, 2014 . As on September 30, 2019, total holding in AAF stood at 90 million equity shares

representing 72.92% of their total capital. The loan portfolio stands at LKR 13,143 million as on September 30,

2019

AAF is a Registered Financial Company based in Sri Lanka a fully licensed, deposit-taking institution

registered with the Central Bank of Sri Lanka and listed in the Colombo Stock Exchange

AAF is in lending business since 1970. At present the company is involved in Retail Finance, Hire Purchase

& Business Loans and has 25 branches across Sri Lanka.

The company formerly known as Finance and Land Sales has been in operation for over 48 years, evolving

to serve the growing needs of people of Sri Lanka.

PRODUCTS

49

o Fixed Deposits

o Leasing

o Business Loan

o Personal Loan

o Group Personal Loan

o Corporate Loans

o Mortgage Loans

o Factoring

o Short Term Loans

o Micro Finance

o Loan against Gold Jewellery

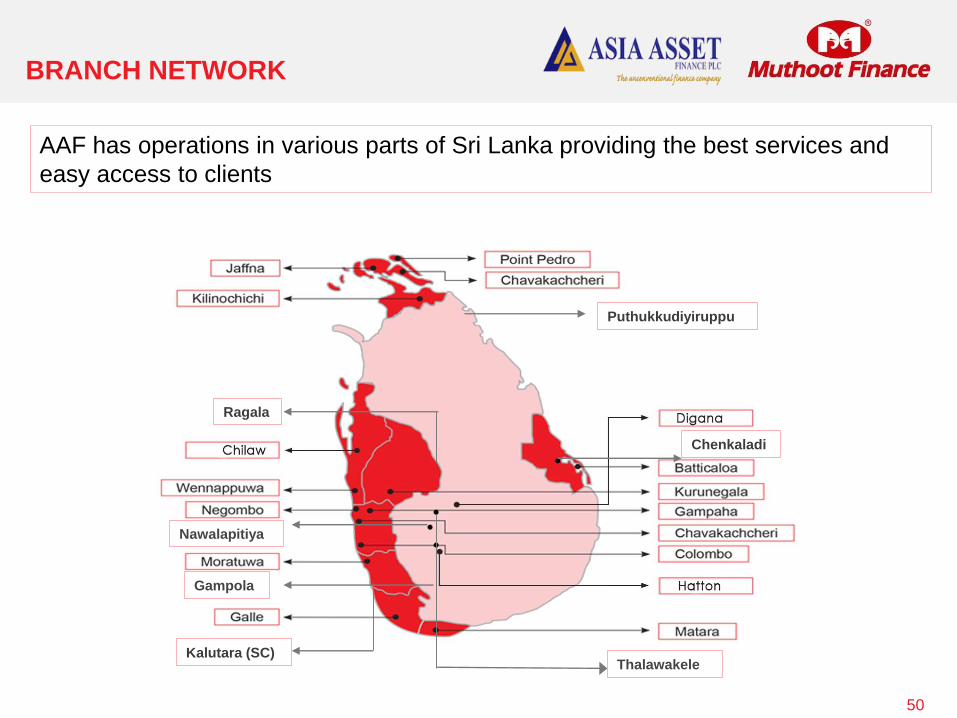

BRANCH NETWORK

50

AAF has operations in various parts of Sri Lanka providing the best services and

easy access to clients

Chenkaladi

Thalawakele

Nawalapitiya

Gampola

Puthukkudiyiruppu

Kalutara (SC)

Ragala

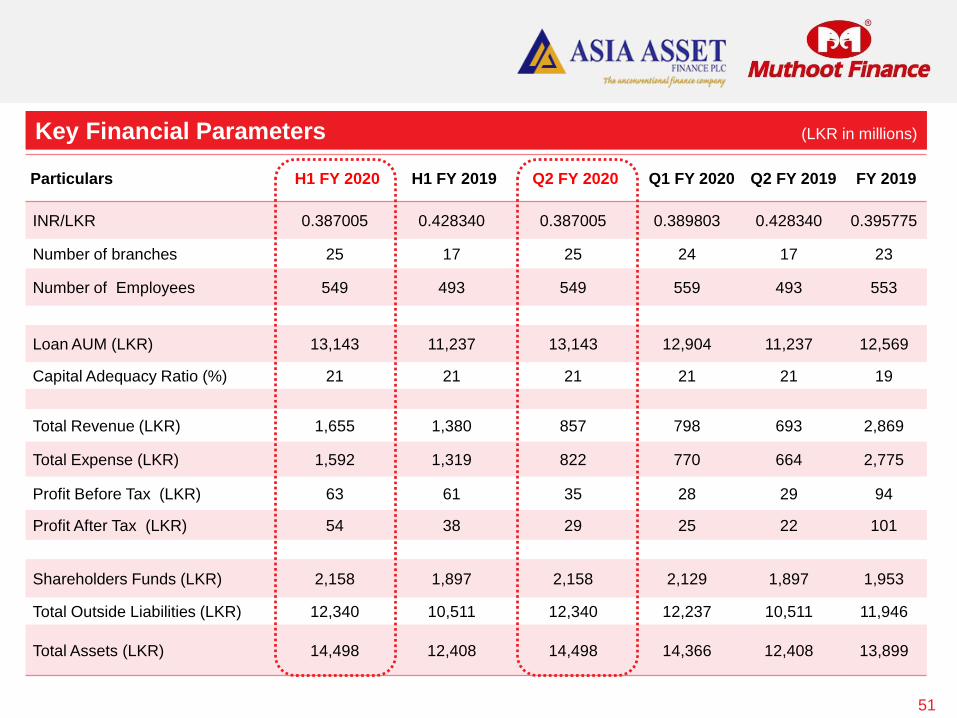

Particulars H1 FY 2020 H1 FY 2019 Q2 FY 2020 Q1 FY 2020 Q2 FY 2019 FY 2019

INR/LKR 0.387005 0.428340 0.387005 0.389803 0.428340 0.395775

Number of branches 25 17 25 24 17 23

Number of Employees 549 493 549 559 493 553

Loan AUM (LKR) 13,143 11,237 13,143 12,904 11,237 12,569

Capital Adequacy Ratio (%) 21 21 21 21 21 19

Total Revenue (LKR) 1,655 1,380 857 798 693 2,869

Total Expense (LKR) 1,592 1,319 822 770 664 2,775

Profit Before Tax (LKR) 63 61 35 28 29 94

Profit After Tax (LKR) 54 38 29 25 22 101

Shareholders Funds (LKR) 2,158 1,897 2,158 2,129 1,897 1,953

Total Outside Liabilities (LKR) 12,340 10,511 12,340 12,237 10,511 11,946

Total Assets (LKR) 14,498 12,408 14,498 14,366 12,408 13,899

51

Key Financial Parameters (LKR in millions)

OUR SUBSIDIARY

52

MUTHOOT HOMEFIN – AN OVERVIEW

Muthoot Homefin (India) Limited is a Housing Finance Company registered with The National Housing Bank

(NHB). It became a wholly owned subsidiary of Muthoot Finance Ltd in Aug’17.

MHIL focuses on extending affordable housing finance and targets customers in Economically Weaker

Sections (EWS) and Lower Income Groups (LIG) in Tier II & Tier III locations.

It operates on a ‘Hub and Spoke’ model, with the centralised processing at Corporate Office at Mumbai. MHIL

has operations in Kerala, Maharashtra, Gujarat, Rajasthan, Madhya Pradesh, Chandigarh, Andhra Pradesh,

Telangana, Karnataka, Uttar Pradesh, Haryana, Punjab, Delhi, Tamil Nadu, Chattisgarh and Pondicherry.

As on September 30, 2019, it has a loan portfolio of Rs.20,975 million.

53

ICRA assigned Long Term Debt Rating of ICRA AA-(Stable) for its Bank limits and Short Term Debt Rating

of ICRA A1+ for its Commercial Paper. CRISIL Upgraded long term rating from AA-(Stable) to AA (Stable).

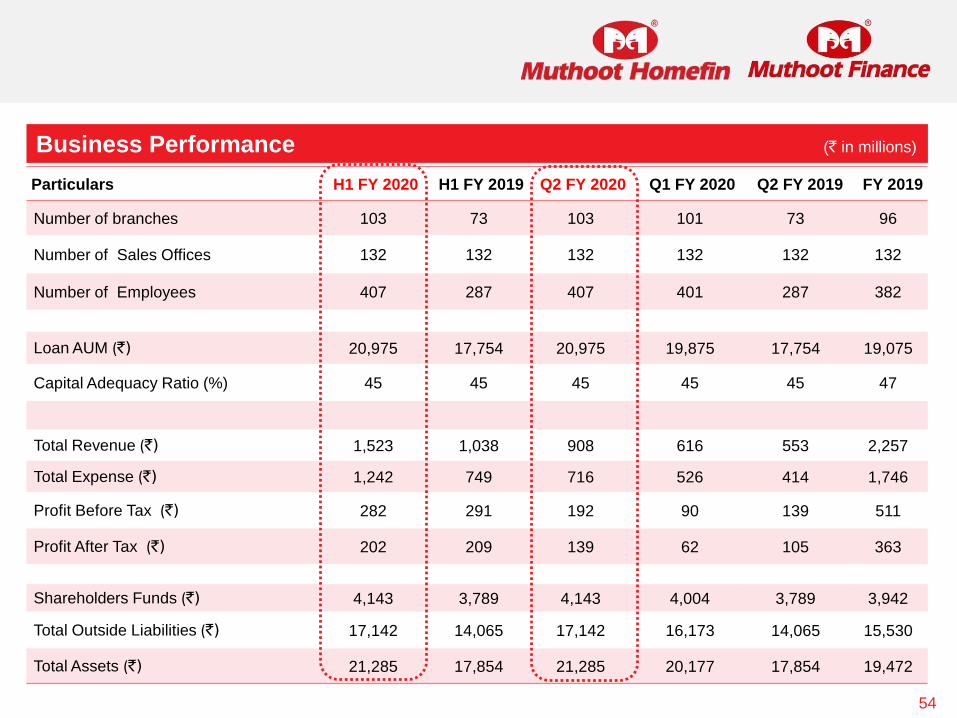

Particulars H1 FY 2020 H1 FY 2019 Q2 FY 2020 Q1 FY 2020 Q2 FY 2019 FY 2019

Number of branches 103 73 103 101 73 96

Number of Sales Offices 132 132 132 132 132 132

Number of Employees 407 287 407 401 287 382

Loan AUM (`) 20,975 17,754 20,975 19,875 17,754 19,075

Capital Adequacy Ratio (%) 45 45 45 45 45 47

Total Revenue (`) 1,523 1,038 908 616 553 2,257

Total Expense (`) 1,242 749 716 526 414 1,746

Profit Before Tax (`) 282 291 192 90 139 511

Profit After Tax (`) 202 209 139 62 105 363

Shareholders Funds (`) 4,143 3,789 4,143 4,004 3,789 3,942

Total Outside Liabilities (`) 17,142 14,065 17,142 16,173 14,065 15,530

Total Assets (`) 21,285 17,854 21,285 20,177 17,854 19,472

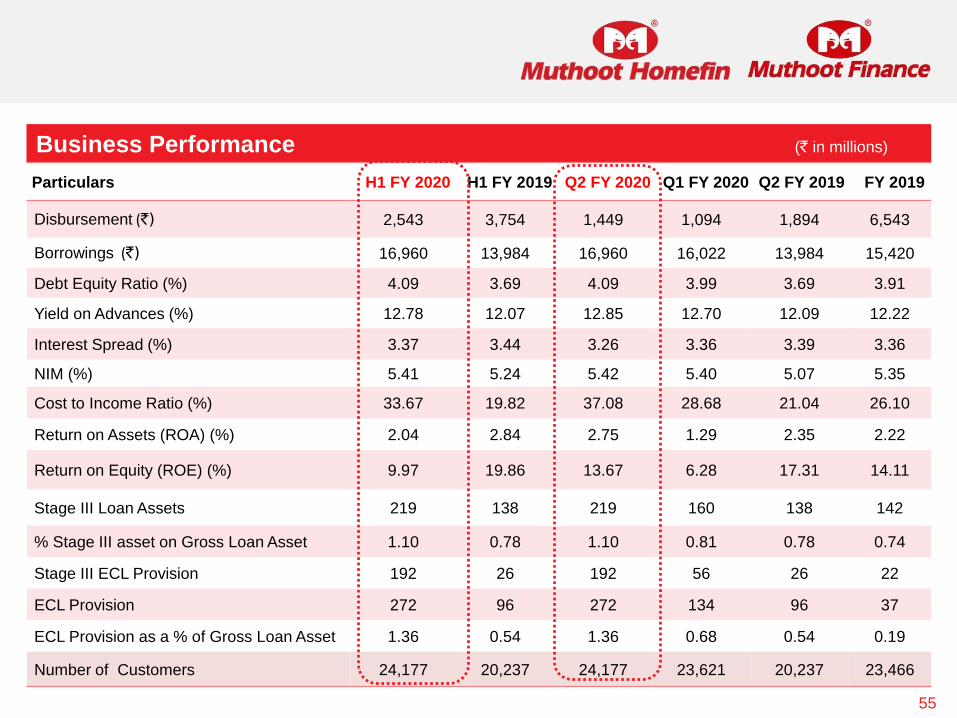

Business Performance (` in millions)

54

Business Performance (` in millions)

Particulars H1 FY 2020 H1 FY 2019 Q2 FY 2020 Q1 FY 2020 Q2 FY 2019 FY 2019

Disbursement (`) 2,543 3,754 1,449 1,094 1,894 6,543

Borrowings (`) 16,960 13,984 16,960 16,022 13,984 15,420

Debt Equity Ratio (%) 4.09 3.69 4.09 3.99 3.69 3.91

Yield on Advances (%) 12.78 12.07 12.85 12.70 12.09 12.22

Interest Spread (%) 3.37 3.44 3.26 3.36 3.39 3.36

NIM (%) 5.41 5.24 5.42 5.40 5.07 5.35

Cost to Income Ratio (%) 33.67 19.82 37.08 28.68 21.04 26.10

Return on Assets (ROA) (%) 2.04 2.84 2.75 1.29 2.35 2.22

Return on Equity (ROE) (%) 9.97 19.86 13.67 6.28 17.31 14.11

Stage III Loan Assets 219 138 219 160 138 142

% Stage III asset on Gross Loan Asset 1.10 0.78 1.10 0.81 0.78 0.74

Stage III ECL Provision 192 26 192 56 26 22

ECL Provision 272 96 272 134 96 37

ECL Provision as a % of Gross Loan Asset 1.36 0.54 1.36 0.68 0.54 0.19

Number of Customers 24,177 20,237 24,177 23,621 20,237 23,466

55

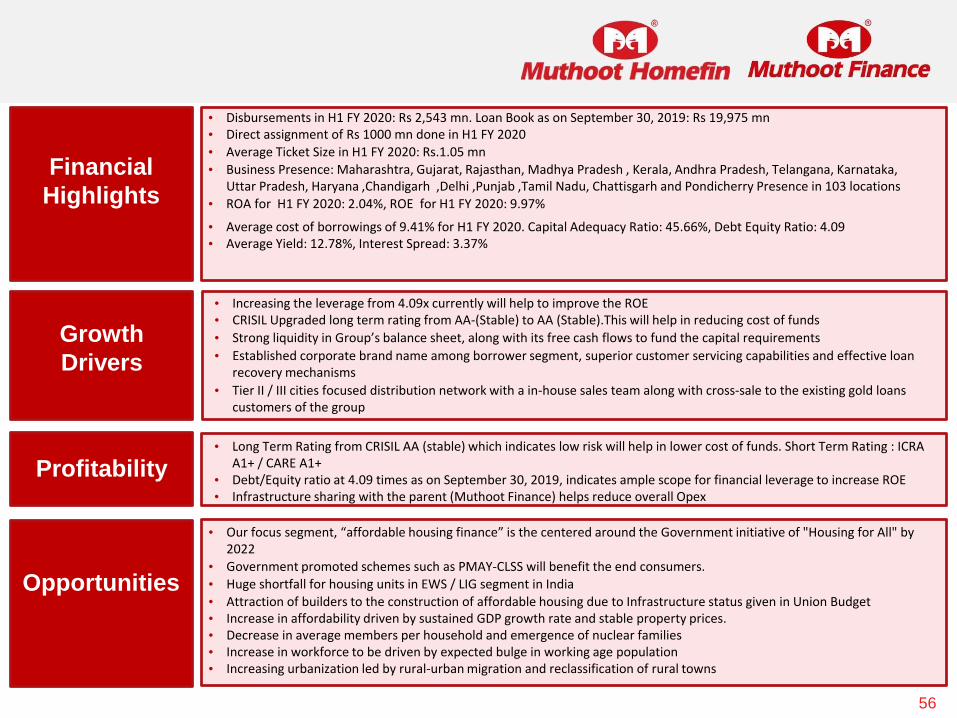

Financial

Highlights

Growth

Drivers

Profitability

Opportunities

• Disbursements in H1 FY 2020: Rs 2,543 mn. Loan Book as on September 30, 2019: Rs 19,975 mn• Direct assignment of Rs 1000 mn done in H1 FY 2020

• Average Ticket Size in H1 FY 2020: Rs.1.05 mn

• Business Presence: Maharashtra, Gujarat, Rajasthan, Madhya Pradesh , Kerala, Andhra Pradesh, Telangana, Karnataka, Uttar Pradesh, Haryana ,Chandigarh ,Delhi ,Punjab ,Tamil Nadu, Chattisgarh and Pondicherry Presence in 103 locations

• ROA for H1 FY 2020: 2.04%, ROE for H1 FY 2020: 9.97%

• Average cost of borrowings of 9.41% for H1 FY 2020. Capital Adequacy Ratio: 45.66%, Debt Equity Ratio: 4.09• Average Yield: 12.78%, Interest Spread: 3.37%

• Increasing the leverage from 4.09x currently will help to improve the ROE• CRISIL Upgraded long term rating from AA-(Stable) to AA (Stable).This will help in reducing cost of funds

• Strong liquidity in Group’s balance sheet, along with its free cash flows to fund the capital requirements

• Established corporate brand name among borrower segment, superior customer servicing capabilities and effective loan recovery mechanisms

• Tier II / III cities focused distribution network with a in-house sales team along with cross-sale to the existing gold loans customers of the group

• Long Term Rating from CRISIL AA (stable) which indicates low risk will help in lower cost of funds. Short Term Rating : ICRA A1+ / CARE A1+

• Debt/Equity ratio at 4.09 times as on September 30, 2019, indicates ample scope for financial leverage to increase ROE• Infrastructure sharing with the parent (Muthoot Finance) helps reduce overall Opex

• Our focus segment, “affordable housing finance” is the centered around the Government initiative of "Housing for All" by 2022

• Government promoted schemes such as PMAY-CLSS will benefit the end consumers.

• Huge shortfall for housing units in EWS / LIG segment in India

• Attraction of builders to the construction of affordable housing due to Infrastructure status given in Union Budget• Increase in affordability driven by sustained GDP growth rate and stable property prices.• Decrease in average members per household and emergence of nuclear families• Increase in workforce to be driven by expected bulge in working age population• Increasing urbanization led by rural-urban migration and reclassification of rural towns

56

OUR SUBSIDIARY

57

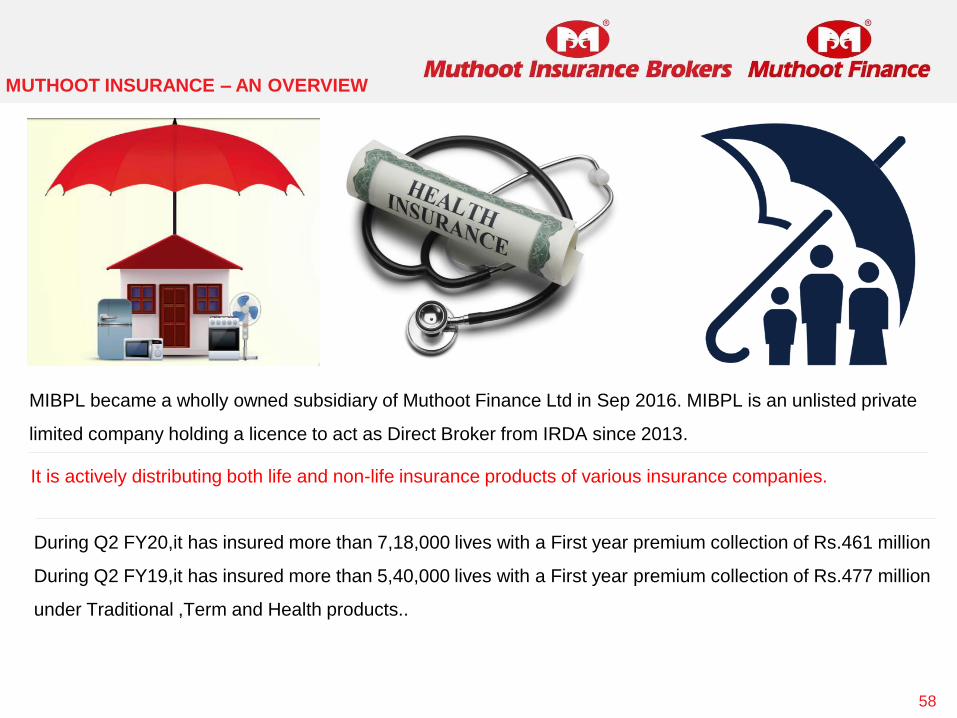

MUTHOOT INSURANCE – AN OVERVIEW

MIBPL became a wholly owned subsidiary of Muthoot Finance Ltd in Sep 2016. MIBPL is an unlisted private

limited company holding a licence to act as Direct Broker from IRDA since 2013.

It is actively distributing both life and non-life insurance products of various insurance companies.

During Q2 FY20,it has insured more than 7,18,000 lives with a First year premium collection of Rs.461 million

During Q2 FY19,it has insured more than 5,40,000 lives with a First year premium collection of Rs.477 million

under Traditional ,Term and Health products..

58

59

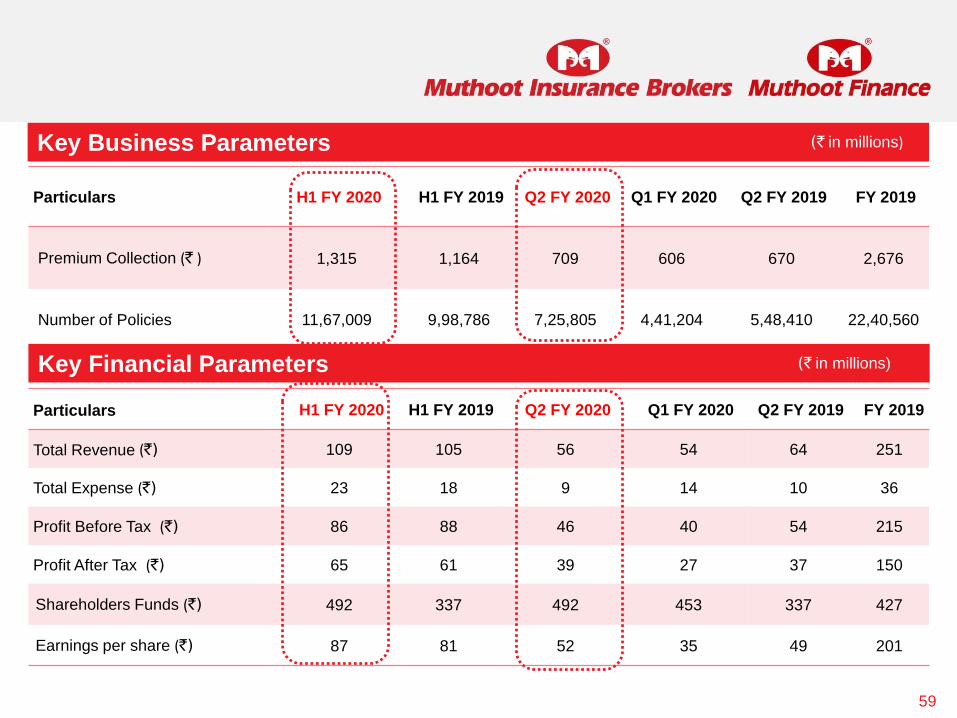

Particulars H1 FY 2020 H1 FY 2019 Q2 FY 2020 Q1 FY 2020 Q2 FY 2019 FY 2019

Premium Collection (` ) 1,315 1,164 709 606 670 2,676

Number of Policies 11,67,009 9,98,786 7,25,805 4,41,204 5,48,410 22,40,560

Key Business Parameters (` in millions)

Particulars H1 FY 2020 H1 FY 2019 Q2 FY 2020 Q1 FY 2020 Q2 FY 2019 FY 2019

Total Revenue (`) 109 105 56 54 64 251

Total Expense (`) 23 18 9 14 10 36

Profit Before Tax (`) 86 88 46 40 54 215

Profit After Tax (`) 65 61 39 27 37 150

Shareholders Funds (`) 492 337 492 453 337 427

Earnings per share (`) 87 81 52 35 49 201

Key Financial Parameters (` in millions)

OUR SUBSIDIARY

60

BELSTAR MICROFINANCE – AN OVERVIEW

As of September 2019 , Muthoot Finance holds 70.01% in BMPL . BMPL was incorporated on January 1988 at Bangalore and the

Company was registered with the RBI in March 2001 as a Non- Banking Finance Company. The Company was reclassified as “NBFC-

MFI” by RBI effective from 11th December 2013.

BMPL was acquired by the ‘Hand in Hand’ group in September 2008 to provide scalable microfinance services to entrepreneurs nurtured

by ‘Hand in Hand’s’ Self Help Group (SHG) program. The Company commenced its first lending operations at Haveri District of Karnataka

in March 2009 to 3 SHGs, 22 members for INR 0.20 mn.

In the last ten years of its operations, BMPL primarily relied on taking over the existing groups formed by Hand in Hand India . BMPL

predominantly follows the SHG model of lending. Effective January 2015, BMPL started working in JLG model of lending in Pune district,

Maharashtra.

As of September 30, 2019, BMPL operations are spread over 11 states and 1 UT (Tamil Nadu, Karnataka, Madhya Pradesh, Maharashtra,

Kerala, Odisha ,Pondicherry ,Chattisgarh, Gujarat, Rajasthan, Bihar and Uttar Pradesh. It has 498 branches, with 99 controlling regional

offices and employs 3837 staffs. Its gross loan portfolio has grown from INR 0.20 mn in March 2009 to INR 21,074 mn in September 2019

61

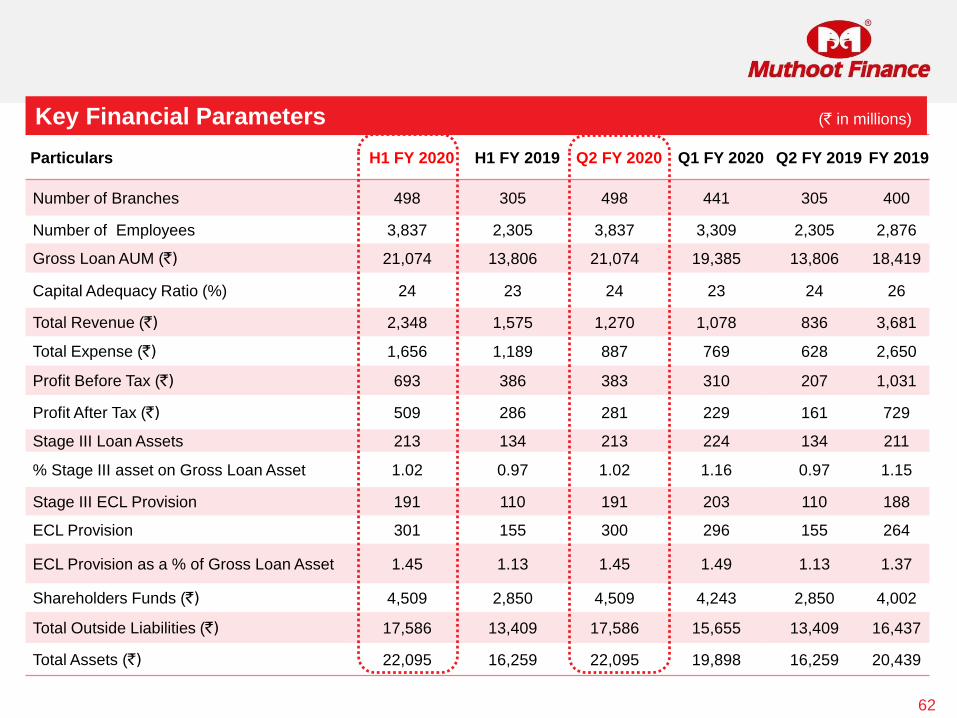

Particulars H1 FY 2020 H1 FY 2019 Q2 FY 2020 Q1 FY 2020 Q2 FY 2019 FY 2019

Number of Branches 498 305 498 441 305 400

Number of Employees 3,837 2,305 3,837 3,309 2,305 2,876

Gross Loan AUM (`) 21,074 13,806 21,074 19,385 13,806 18,419

Capital Adequacy Ratio (%) 24 23 24 23 24 26

Total Revenue (`) 2,348 1,575 1,270 1,078 836 3,681

Total Expense (`) 1,656 1,189 887 769 628 2,650

Profit Before Tax (`) 693 386 383 310 207 1,031

Profit After Tax (`) 509 286 281 229 161 729

Stage III Loan Assets 213 134 213 224 134 211

% Stage III asset on Gross Loan Asset 1.02 0.97 1.02 1.16 0.97 1.15

Stage III ECL Provision 191 110 191 203 110 188

ECL Provision 301 155 300 296 155 264

ECL Provision as a % of Gross Loan Asset 1.45 1.13 1.45 1.49 1.13 1.37

Shareholders Funds (`) 4,509 2,850 4,509 4,243 2,850 4,002

Total Outside Liabilities (`) 17,586 13,409 17,586 15,655 13,409 16,437

Total Assets (`) 22,095 16,259 22,095 19,898 16,259 20,439

62

Key Financial Parameters (` in millions)

OUR SUBSIDIARY

63

OUR SUBSIDIARY

45

Muthoot Money Ltd (MML), became a wholly owned subsidiary of Muthoot Finance Ltd in October 2018. MML is

a RBI registered Non- Banking Finance Company engaged mainly in extending loans for vehicles.

The operations are now centered in Hyderabad. Recently , Company has started extending loans for

Commercial Vehicles and Equipments.

As on 30th September, 2019 it has a total loan portfolio of Rs.4,263 million.

MUTHOOT MONEY– AN OVERVIEW

64

OUR SUBSIDIARY

45

Key Financial Parameters (` in millions)

Particulars H1 FY 2020 Q2 FY 2020 Q1 FY 2020 FY 2019

Number of branches 24 24 24 21

Number of Employees 277 277 245 247

Gross Loan AUM (`) 4,263 4,263 3,927 3,107

Capital Adequacy Ratio(%) 24 24 26 32

Total Revenue (`) 311 169 142 156

Total Expense (`) 258 126 132 149

Profit Before Tax (`) 54 43 9 7

Profit After Tax (`) 32 32 (0.40) 3

Stage III Loan Assets 38 38 12 -

% Stage III asset on Gross Loan Asset 0.90 0.90 0.30 -

Stage III ECL Provision 9.57 9.57 12 -

ECL Provision 51.66 51.66 48 15

ECL Provision as a % of Gross Loan Asset 1.21 1.21 1.24 0.47

Shareholders Funds (`) 1,067 1,067 1,035 1,035

Total Outside Liabilities (`) 3,455 3,455 3,116 2,317

Total Assets (`) 4,522 4,522 4,151 3,35265

66

OTHER SUBSIDIARIES

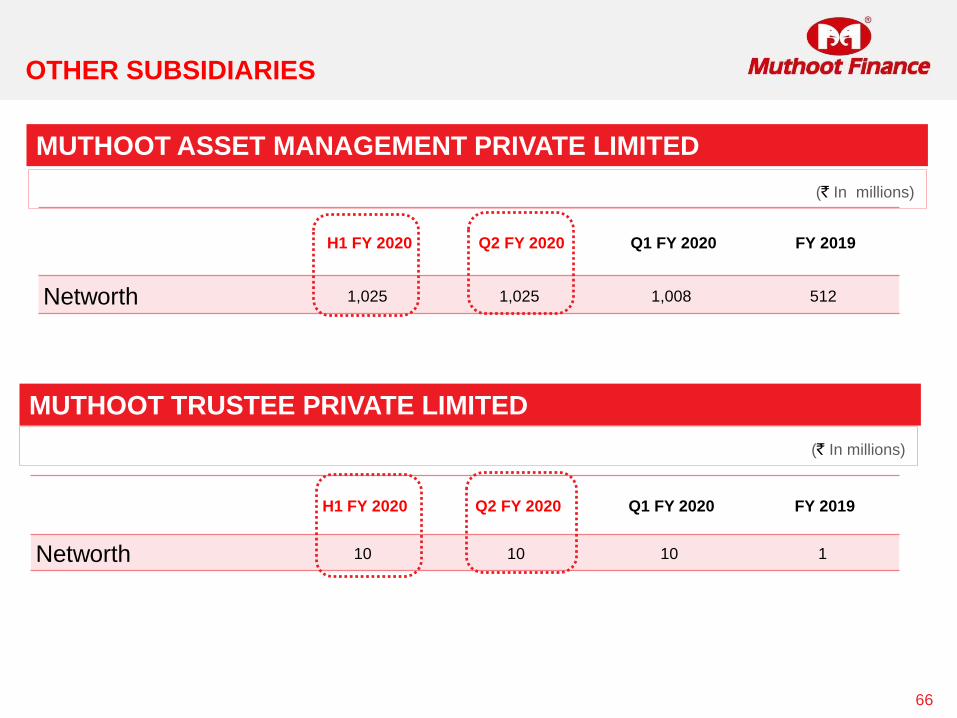

MUTHOOT ASSET MANAGEMENT PRIVATE LIMITED

(` In millions)

H1 FY 2020 Q2 FY 2020 Q1 FY 2020 FY 2019

Networth 1,025 1,025 1,008 512

MUTHOOT TRUSTEE PRIVATE LIMITED

(` In millions)

H1 FY 2020 Q2 FY 2020 Q1 FY 2020 FY 2019

Networth 10 10 10 1

(Individual & Corporate Investors)

(Institutional Investors)

REGISTERED OFFICE

2nd Floor, Muthoot Chambers

Opposite Saritha Theatre Complex

Banerji Road, Kochi

Kerala – 682 018. India

Tel: (91484) 2394712

Fax: (91484) 2396506

www.muthootfinance.com

CIN: L65910KL1997PLC011300

RBI Reg No: N 16.00167