Embed Size (px)

Citation preview

The scope of cover

Motor Insurance Policies

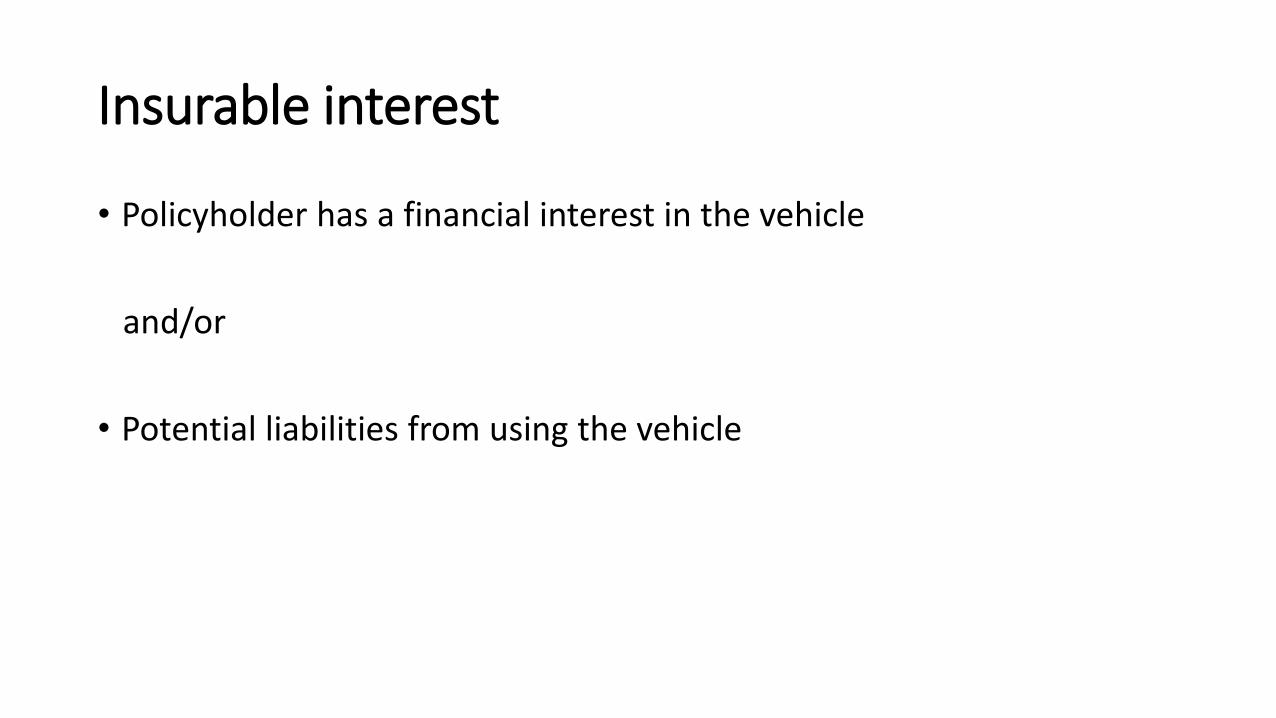

Insurable interest

• Policyholder has a financial interest in the vehicle

and/or

• Potential liabilities from using the vehicle

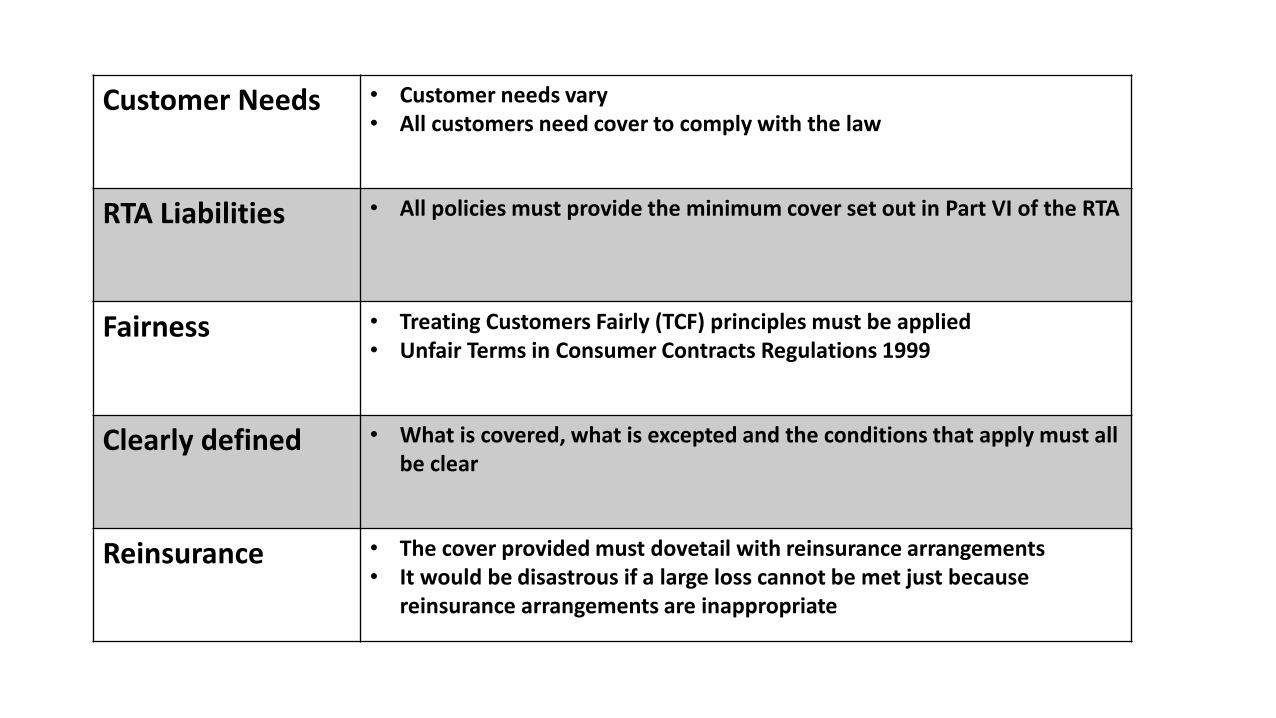

Customer Needs • Customer needs vary• All customers need cover to comply with the law

RTA Liabilities • All policies must provide the minimum cover set out in Part VI of the RTA

Fairness • Treating Customers Fairly (TCF) principles must be applied• Unfair Terms in Consumer Contracts Regulations 1999

Clearly defined • What is covered, what is excepted and the conditions that apply must all be clear

Reinsurance • The cover provided must dovetail with reinsurance arrangements• It would be disastrous if a large loss cannot be met just because

reinsurance arrangements are inappropriate

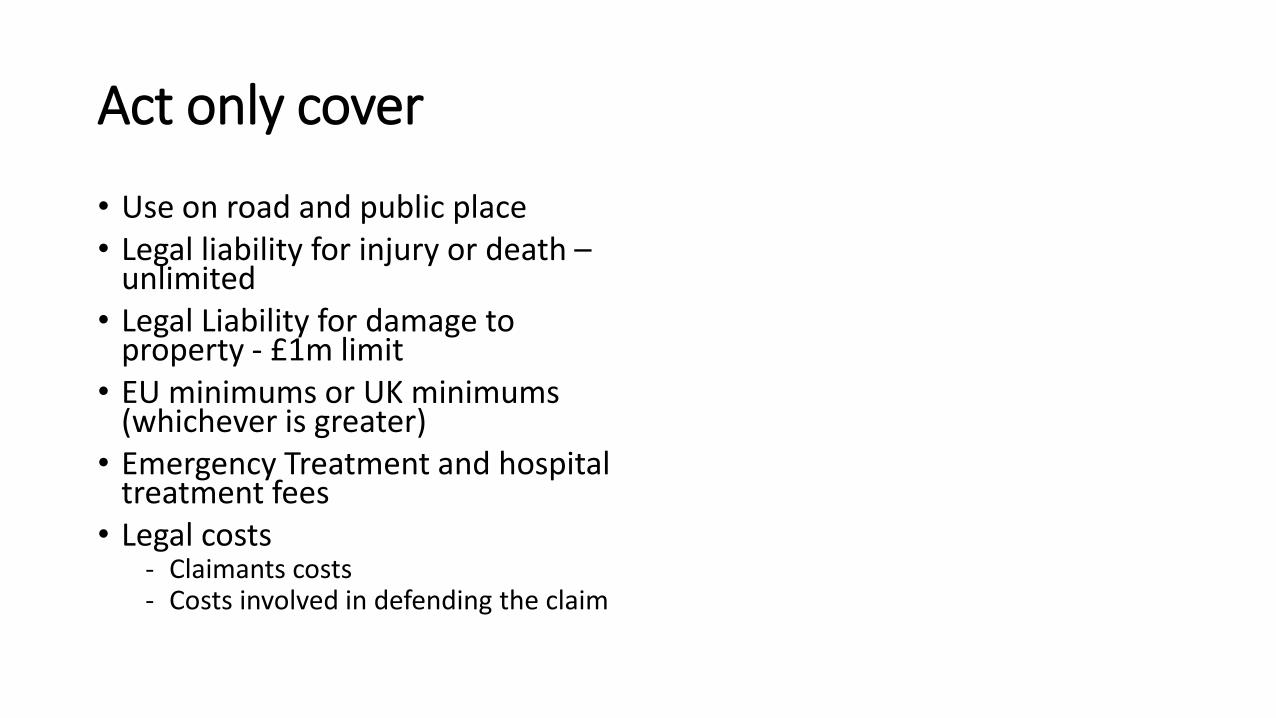

Act only cover

• Use on road and public place• Legal liability for injury or death –

unlimited• Legal Liability for damage to

property - £1m limit• EU minimums or UK minimums

(whichever is greater)• Emergency Treatment and hospital

treatment fees• Legal costs

- Claimants costs- Costs involved in defending the claim

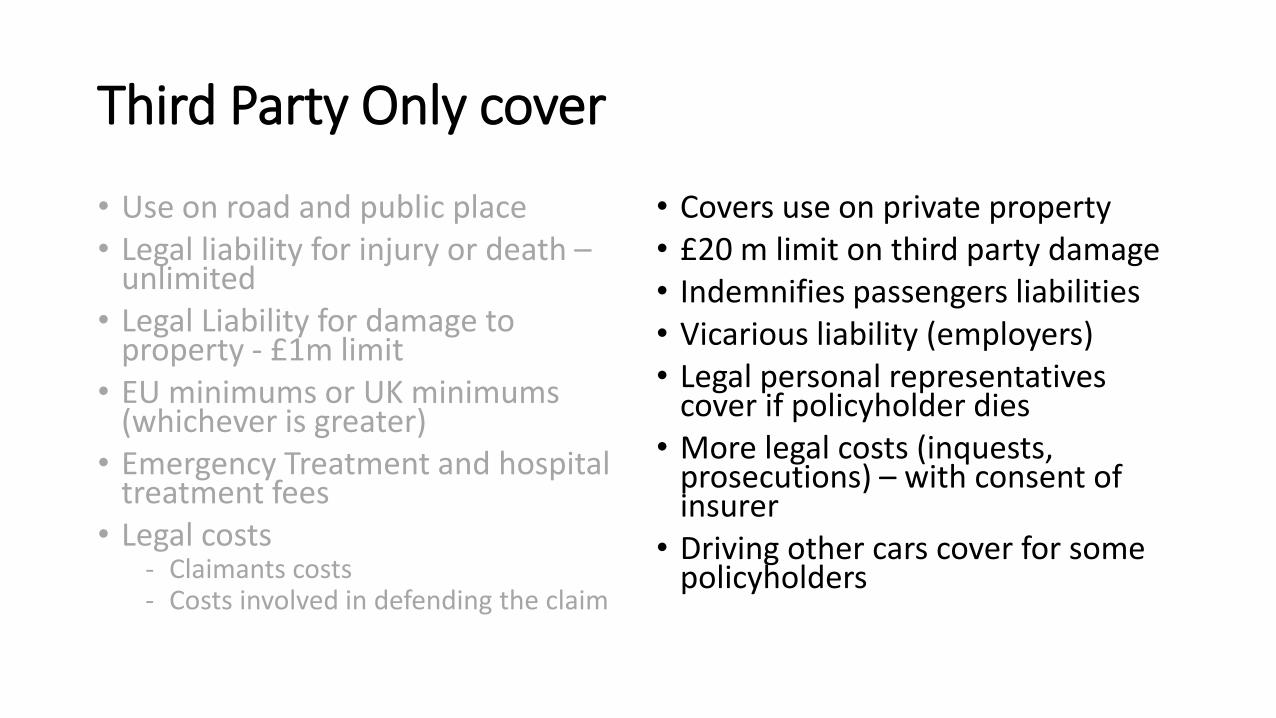

Third Party Only cover

• Use on road and public place• Legal liability for injury or death –

unlimited• Legal Liability for damage to

property - £1m limit• EU minimums or UK minimums

(whichever is greater)• Emergency Treatment and hospital

treatment fees• Legal costs

- Claimants costs- Costs involved in defending the claim

• Covers use on private property• £20 m limit on third party damage• Indemnifies passengers liabilities• Vicarious liability (employers)• Legal personal representatives

cover if policyholder dies• More legal costs (inquests,

prosecutions) – with consent of insurer

• Driving other cars cover for some policyholders

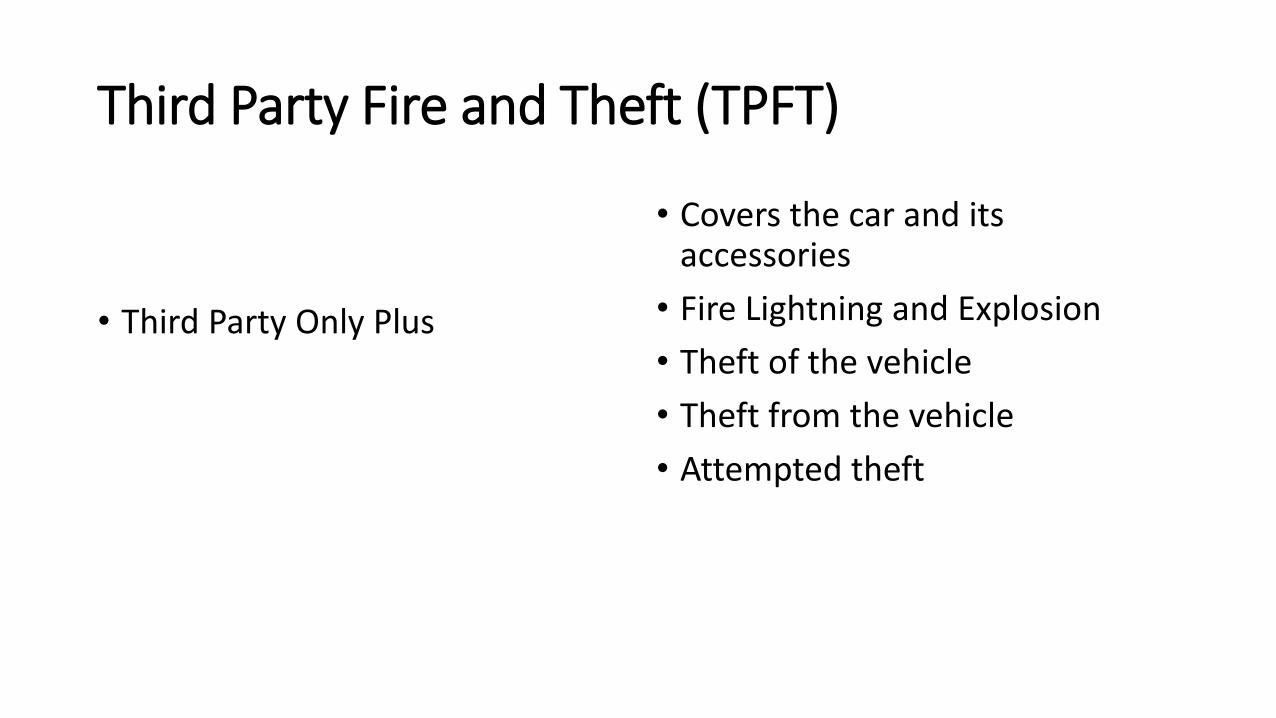

Third Party Fire and Theft (TPFT)

• Third Party Only Plus

• Covers the car and its accessories

• Fire Lightning and Explosion

• Theft of the vehicle

• Theft from the vehicle

• Attempted theft

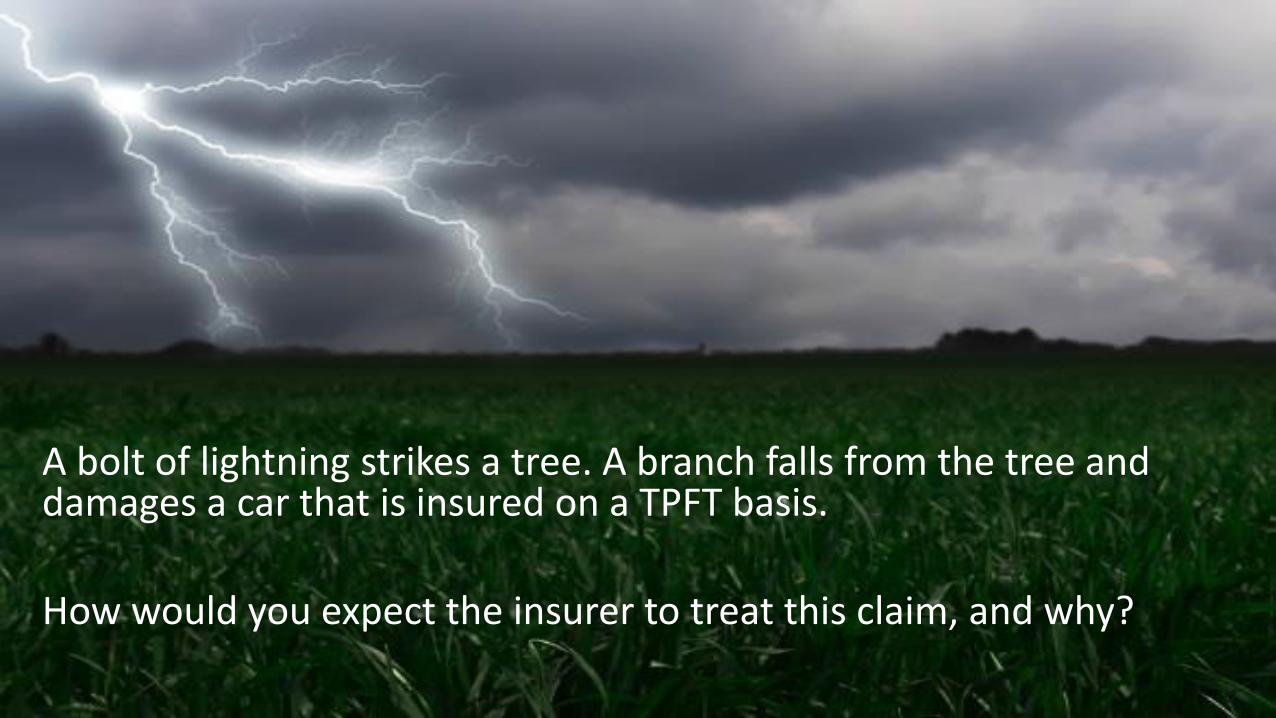

Lightning Strike

A bolt of lightning strikes a tree. A branch falls from the tree and damages a car that is insured on a TPFT basis.

How would you expect the insurer to treat this claim, and why?

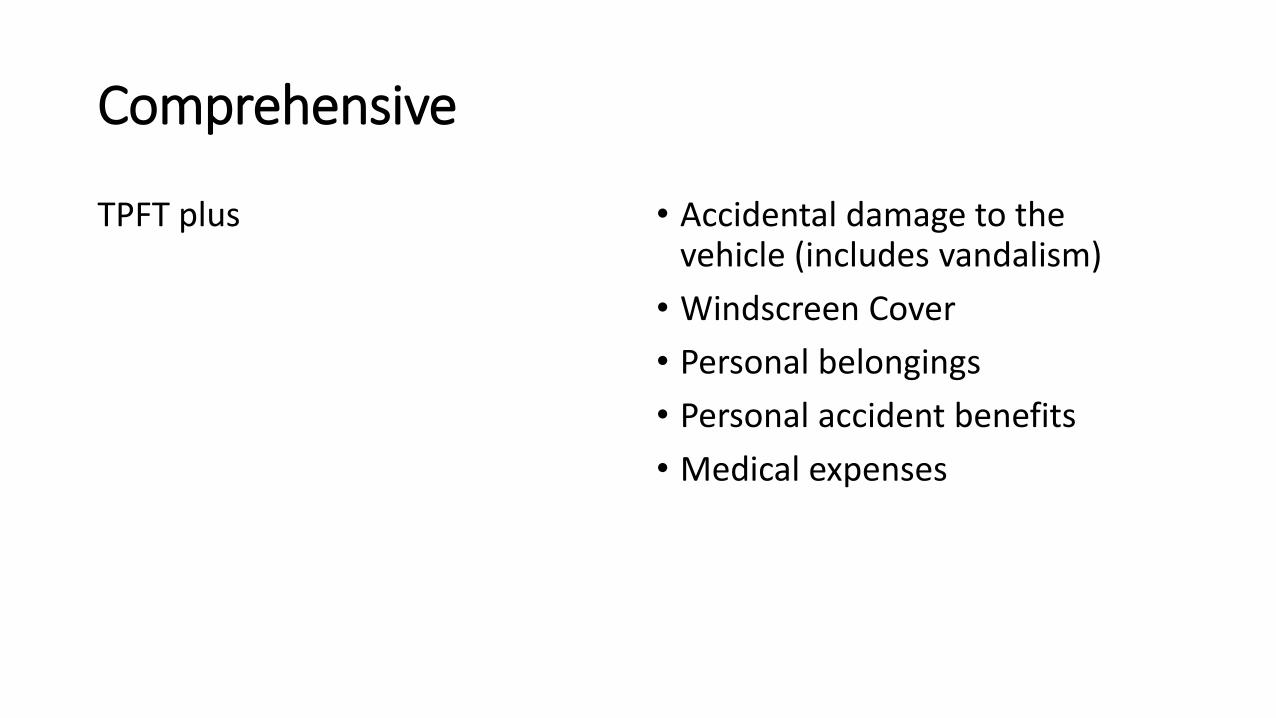

Comprehensive

TPFT plus • Accidental damage to the vehicle (includes vandalism)

• Windscreen Cover

• Personal belongings

• Personal accident benefits

• Medical expenses

Comprehensive:

including or dealing with all or nearly all elements or aspects of something

Fully

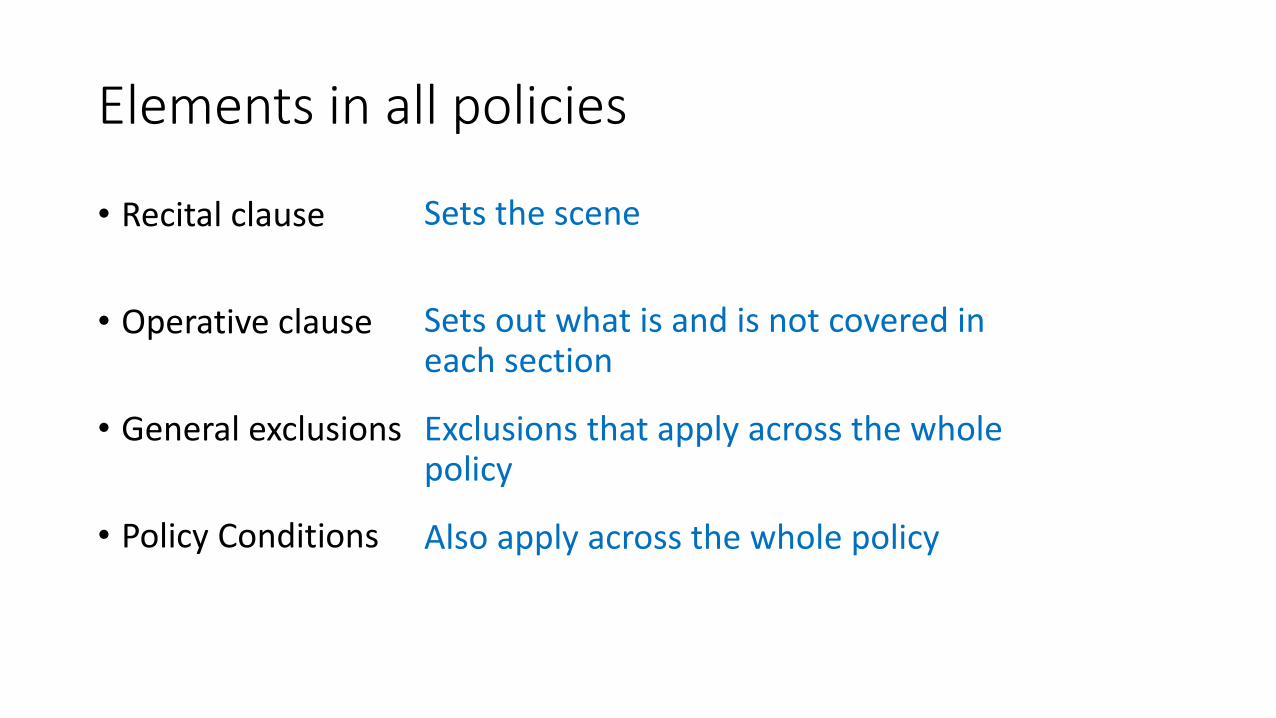

Elements in all policies

• Recital clause

• Operative clause

• General exclusions

• Policy Conditions

Sets the scene

Sets out what is and is not covered in each section

Exclusions that apply across the whole policy

Also apply across the whole policy

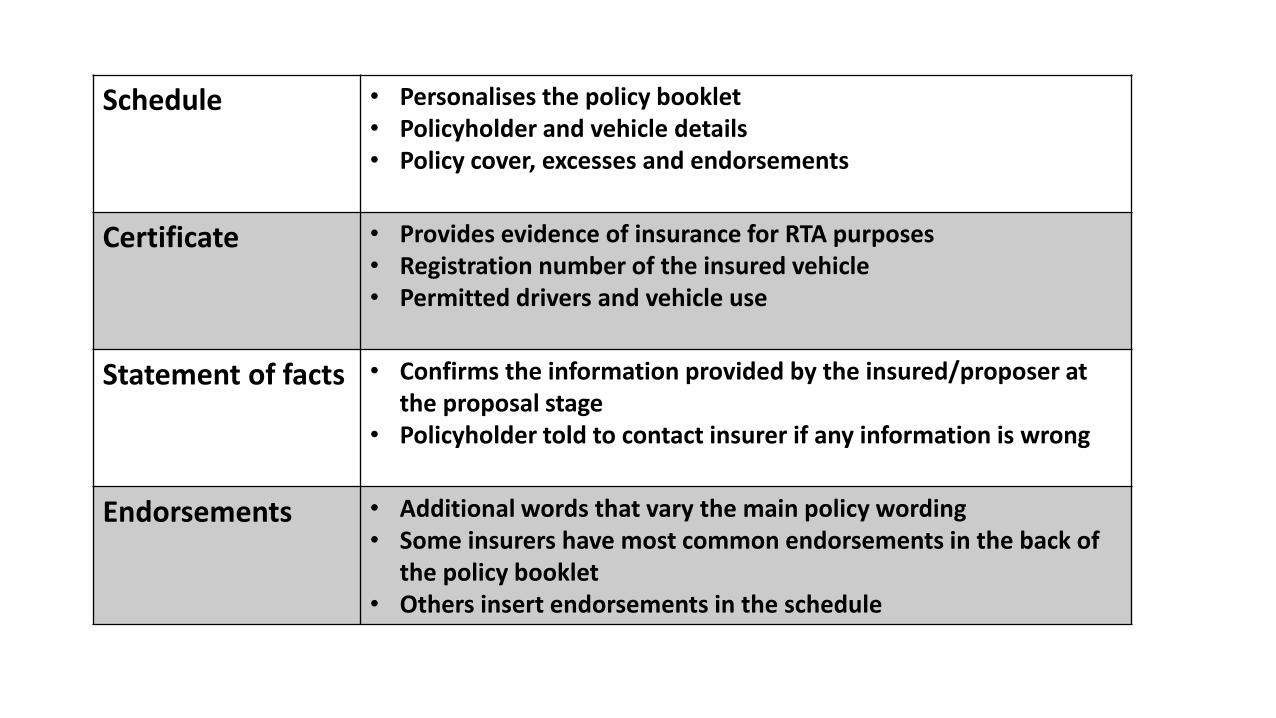

Schedule • Personalises the policy booklet• Policyholder and vehicle details• Policy cover, excesses and endorsements

Certificate • Provides evidence of insurance for RTA purposes• Registration number of the insured vehicle• Permitted drivers and vehicle use

Statement of facts • Confirms the information provided by the insured/proposer at the proposal stage

• Policyholder told to contact insurer if any information is wrong

Endorsements • Additional words that vary the main policy wording• Some insurers have most common endorsements in the back of

the policy booklet• Others insert endorsements in the schedule

Recital Clause

• Privity of contract despite Contracts (Rights of Third Parties)Act 1999

• Policyholder agrees to pay the premium

• Insurer agrees to provide cover

• The law applicable

• Ensures that contractual disputes are dealt with in the courts of the UK Channel Islands or Isle of Man

Case Law

• Laurence v Davis 1972

• Dodson v Dodson 2001

• A van was deemed to be a ‘motor car’

• Policy does not come to an end when the specifically insured vehicle disposed of

• This overturned Tatersall v Drysdale 1935

• Led to a change in the DOC wording

Legal Fees

• Covers coroner’s inquest, fatal accident enquiry, defence costs in criminal courts

• Subject to the prior agreement of the insurer

• Only applies in cases where the proceedings result from an accident covered by the policy

• Some policies cover full defence of manslaughter or causing death by dangerous or careless driving

• If so, other defence costs covered in a court of summary jurisdiction (e.g. magistrates courts)

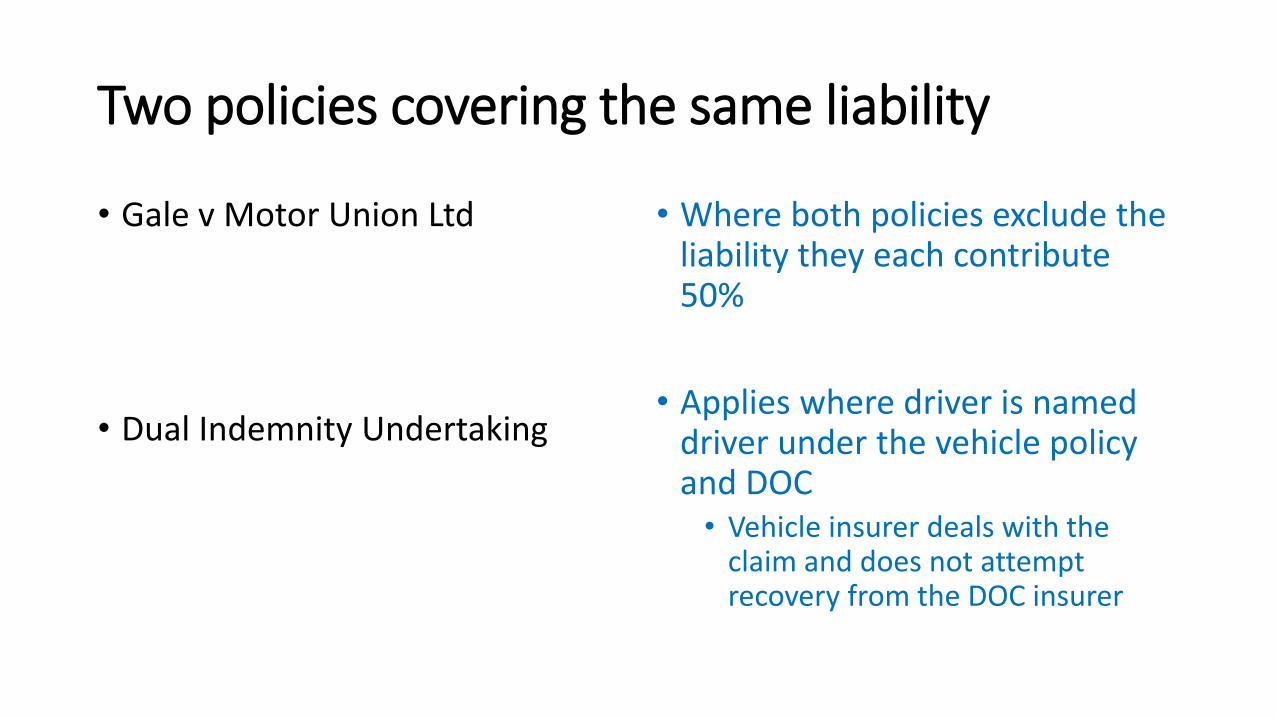

Two policies covering the same liability

• Gale v Motor Union Ltd

• Dual Indemnity Undertaking

• Where both policies exclude the liability they each contribute 50%

• Applies where driver is named driver under the vehicle policy and DOC• Vehicle insurer deals with the

claim and does not attempt recovery from the DOC insurer

Which one would you buy?

• Price £8000• Very good condition• One careful owner• 12,000 miles on the clock

• Price £8000• Very good condition• One careful owner• 11,000 miles on the clock• Previous accident damage - £5000

to repair

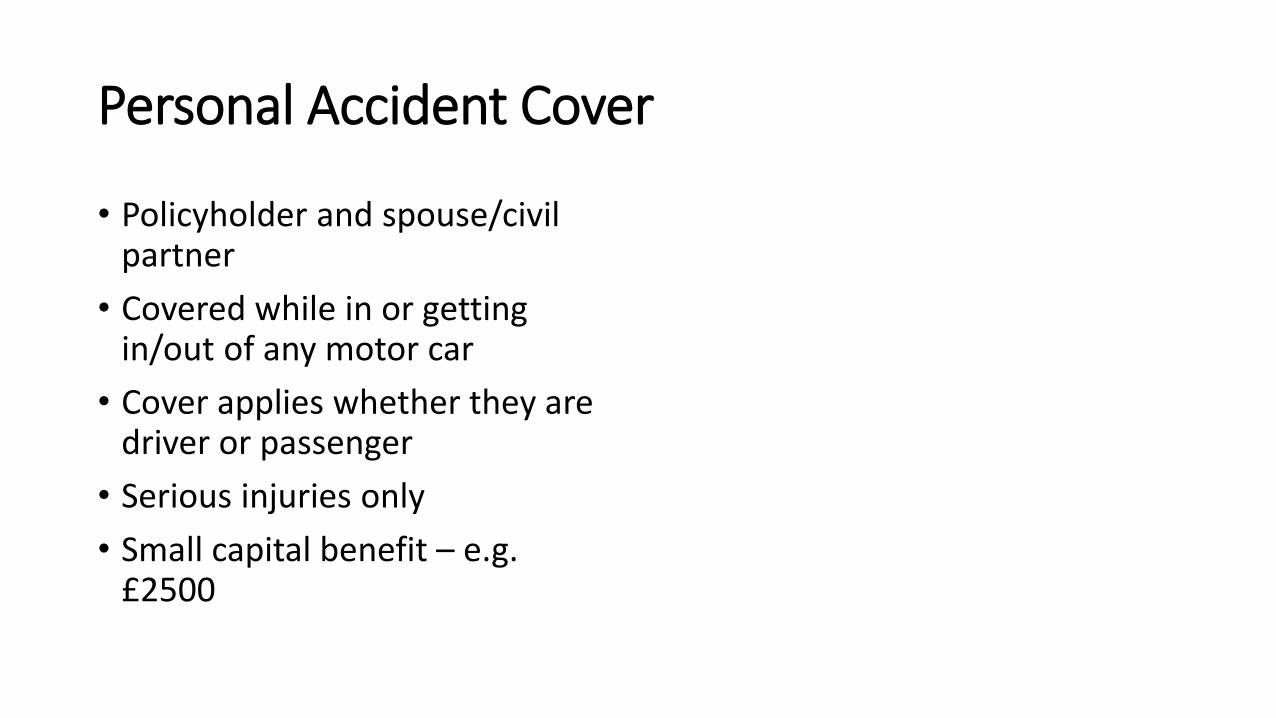

Personal Accident Cover

• Policyholder and spouse/civil partner

• Covered while in or getting in/out of any motor car

• Cover applies whether they are driver or passenger

• Serious injuries only

• Small capital benefit – e.g. £2500

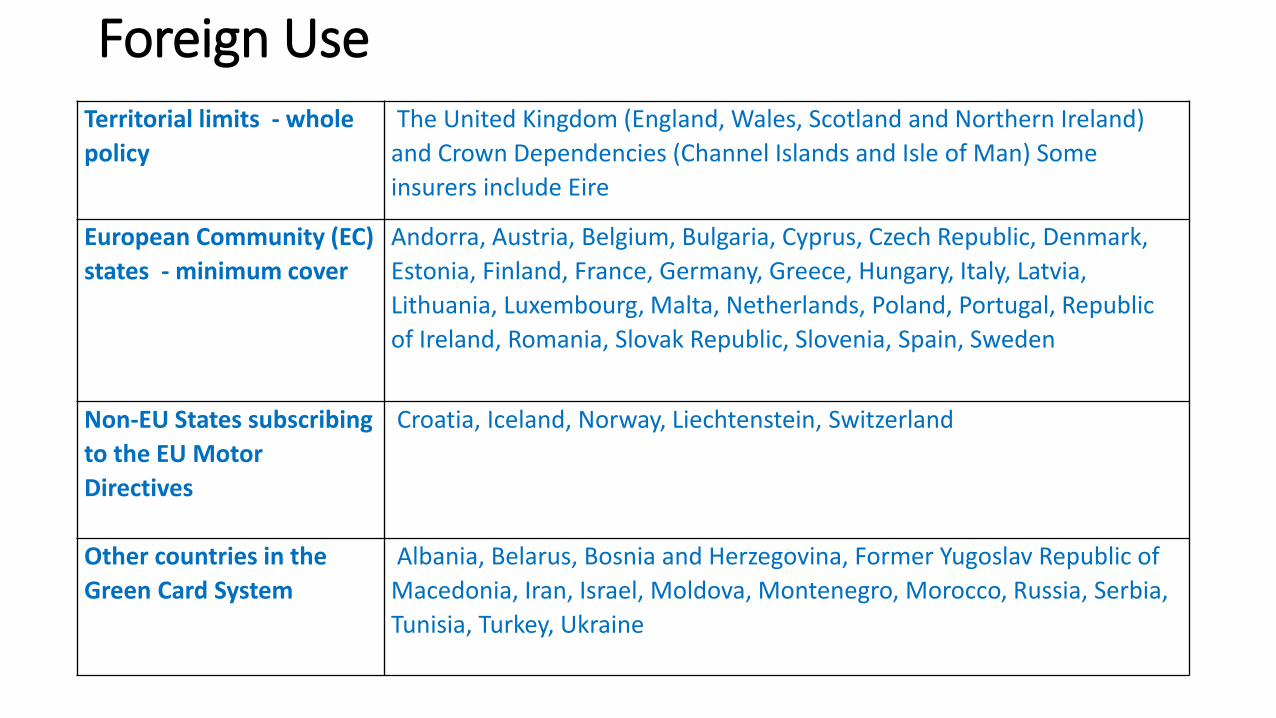

Foreign UseTerritorial limits - whole

policy

The United Kingdom (England, Wales, Scotland and Northern Ireland)

and Crown Dependencies (Channel Islands and Isle of Man) Some

insurers include Eire

European Community (EC)

states - minimum cover

Andorra, Austria, Belgium, Bulgaria, Cyprus, Czech Republic, Denmark,

Estonia, Finland, France, Germany, Greece, Hungary, Italy, Latvia,

Lithuania, Luxembourg, Malta, Netherlands, Poland, Portugal, Republic

of Ireland, Romania, Slovak Republic, Slovenia, Spain, Sweden

Non-EU States subscribing

to the EU Motor

Directives

Croatia, Iceland, Norway, Liechtenstein, Switzerland

Other countries in the

Green Card System

Albania, Belarus, Bosnia and Herzegovina, Former Yugoslav Republic of

Macedonia, Iran, Israel, Moldova, Montenegro, Morocco, Russia, Serbia,

Tunisia, Turkey, Ukraine

General Average/Salvage Contributions

Motor Cycle Insurances - differences• DOMC

• Not always available• Engine size limit is usual

• Accessories and spare parts• Must be on the vehicle• Helmets and protective clothing may

be available for extra premium

• Not normally available• Personal Accident• Personal belongings• Medical expenses

Goods carrying

vehicles

• May be used to carry own goods or those of others

• Haulage risks categories

• Local

• Medium Distance

• Long Distance

Agricultural and

forestry vehiclesIncludes vehicles used for farming, sport ground maintenance and vehicles used on

private estates

Passenger carrying

vehiclesHire or reward use

Includes taxis, self drive hire, buses and coaches

Vehicles of special

constructionVehicles used for various trades. Examples include excavators, dump trucks, ice cream

vans, mobile shops, mobile libraries etc.

Legal Fees - Commercial Vehicles

• Same as Private Car plus:

• Health and Safety enquiries

• Criminal proceedings for breach of:

• Health and Safety at Work Act 1974and/or

• Corporate Manslaughter and Corporate Homicide Act 2007

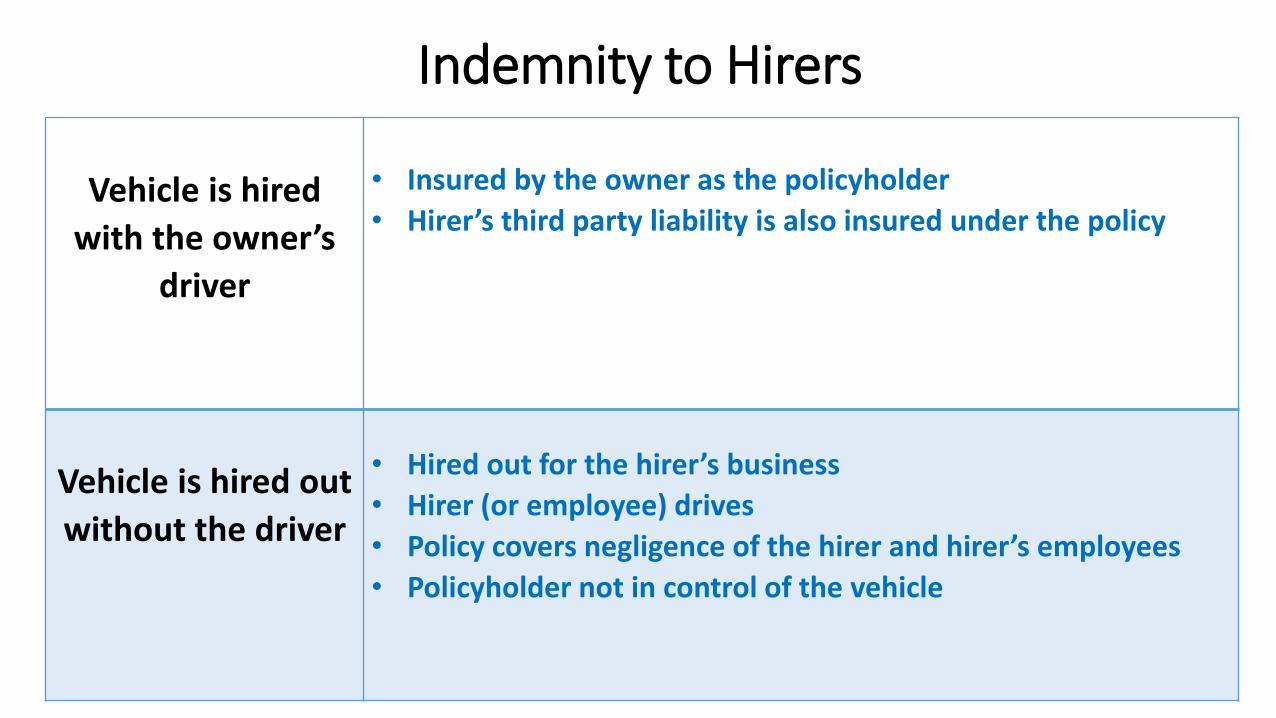

Indemnity to Hirers

Vehicle is hired

with the owner’s

driver

• Insured by the owner as the policyholder

• Hirer’s third party liability is also insured under the policy

Vehicle is hired out

without the driver

• Hired out for the hirer’s business

• Hirer (or employee) drives

• Policy covers negligence of the hirer and hirer’s employees

• Policyholder not in control of the vehicle

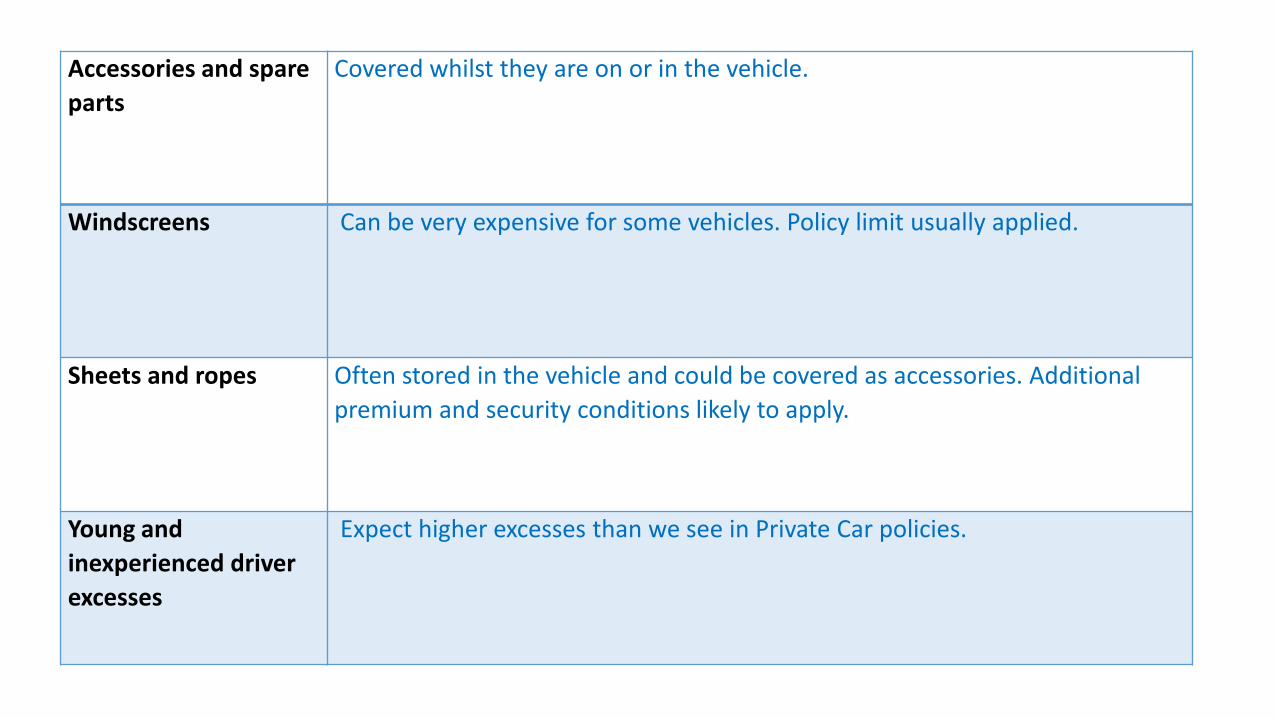

Accessories and spare

parts

Covered whilst they are on or in the vehicle.

Windscreens Can be very expensive for some vehicles. Policy limit usually applied.

Sheets and ropes Often stored in the vehicle and could be covered as accessories. Additional

premium and security conditions likely to apply.

Young and

inexperienced driver

excesses

Expect higher excesses than we see in Private Car policies.

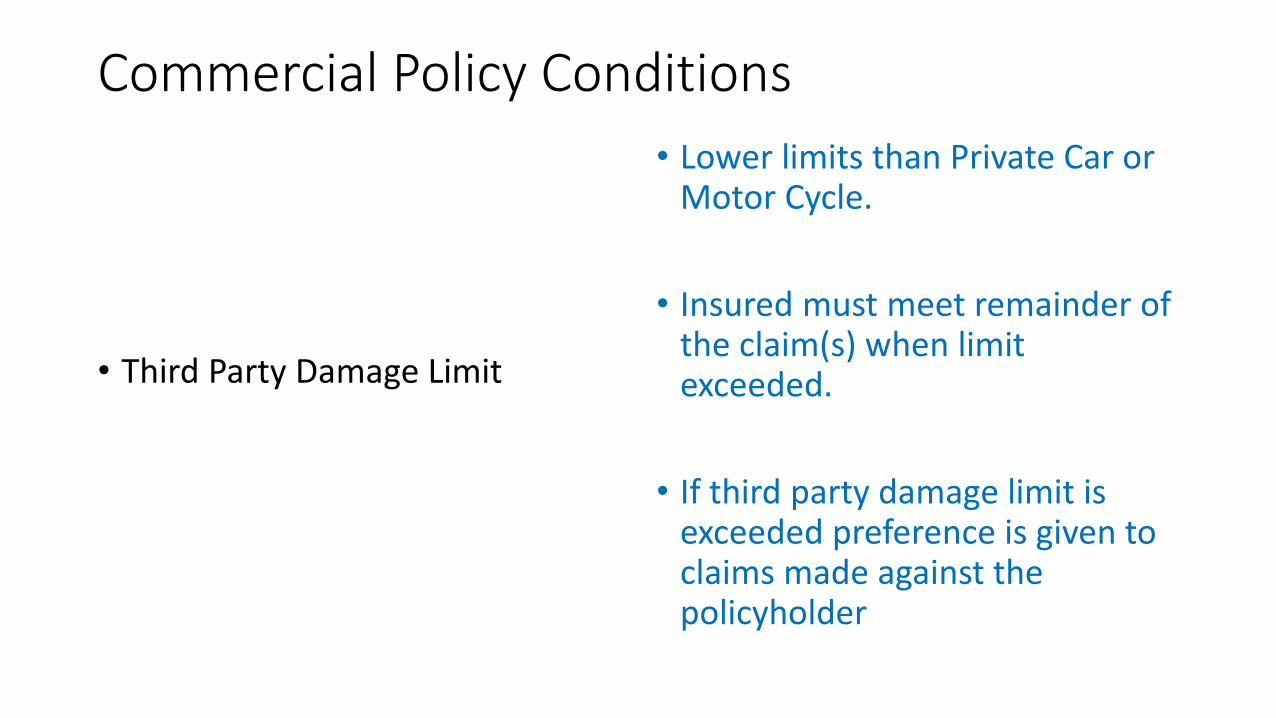

Commercial Policy Conditions

• Third Party Damage Limit

• Lower limits than Private Car or Motor Cycle.

• Insured must meet remainder of the claim(s) when limit exceeded.

• If third party damage limit is exceeded preference is given to claims made against the policyholder

Special Types Policies

• Some insurers adapt their commercial vehicle policy wordings

• Some Insurers issue a ‘special types’ policy

• Third party working risks normally covered under a public liability policy

• Some insurers will extend the motor policy to include third party working risks

Special Types – Hire or Reward options

• Restricted to policyholder’s own business

or

• Hire covered whilst being driven by policyholder’s drivers

and/or

• Hire covered whilst being driven by hirer’s drivers

Agricultural vehicles

• Any tractor or self propelled vehicle used solely for agricultural or forestry work, including the haulage of agricultural produce or articles required for agriculture

• Any other vehicle used solely for agricultural or forestry purposes for which a road fund licence is not required or under a licence exemption from duty under the Vehicles (Excise) Act

• Cover may be for own use or hire to another (e.g. local authorities) for defined purposes

• Standard exclusion is liabilities arising form crop spraying –unless it is a RTA liability

Agricultural Trailers

• Third party towing risks covered

• Can be extended to include third party risks while detached

• Some insurers automatically provide comprehensive cover for trailers – practice varies

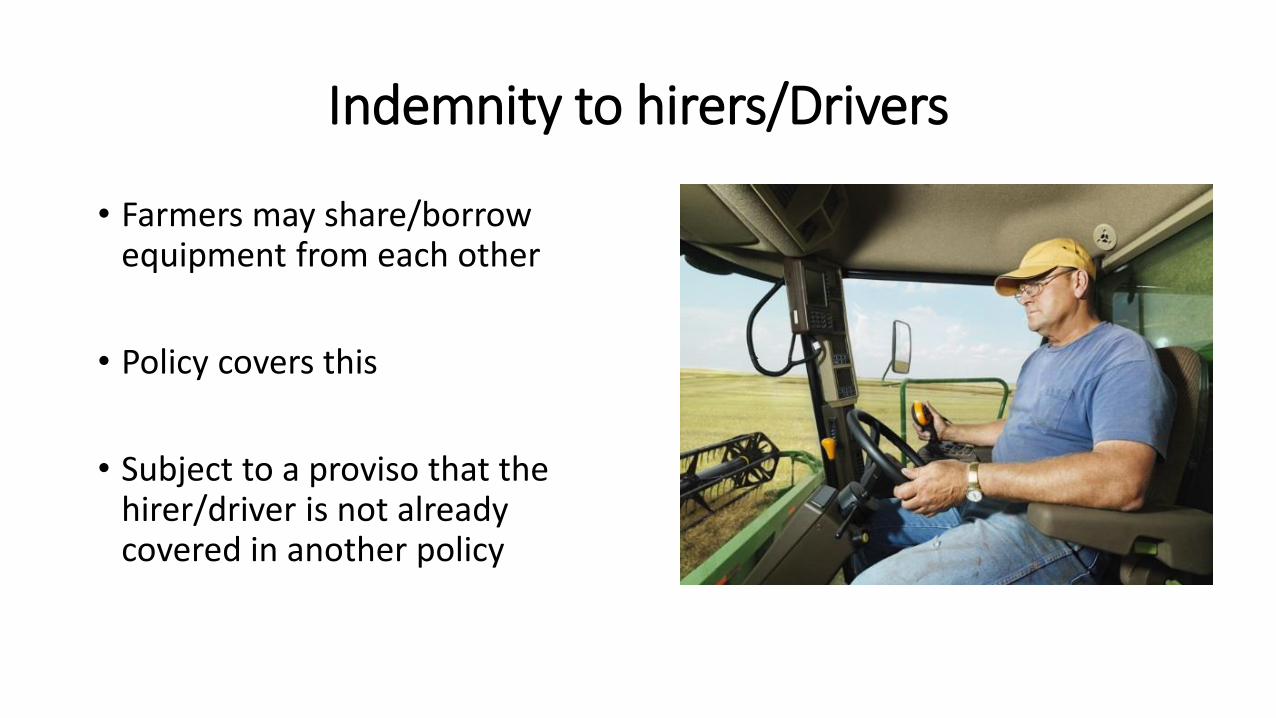

Indemnity to hirers/Drivers

• Farmers may share/borrow equipment from each other

• Policy covers this

• Subject to a proviso that the hirer/driver is not already covered in another policy

Self Drive Hire

• Hired without a driver

• Insured on the basis of individual hiring's

• Hirer and/or named drivers complete an application form

• Subject to limitations on acceptable risks (e.g. age, driving record)

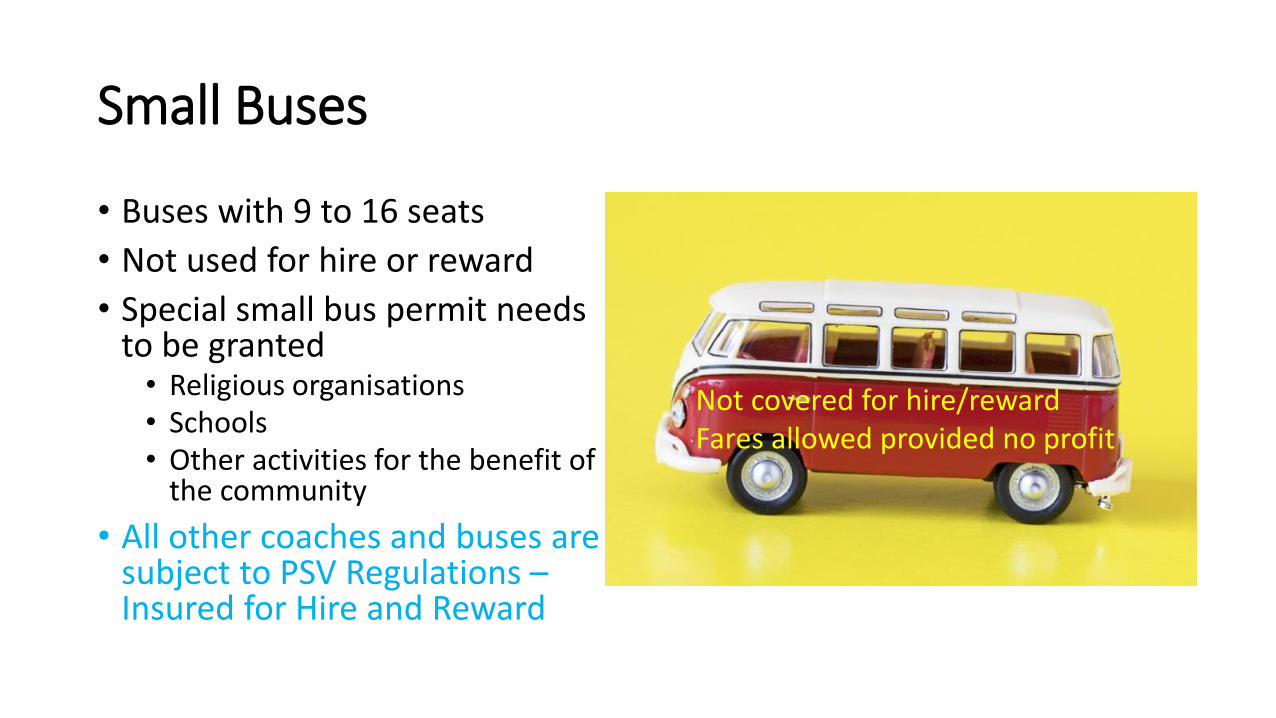

Small Buses

• Buses with 9 to 16 seats

• Not used for hire or reward

• Special small bus permit needs to be granted• Religious organisations• Schools• Other activities for the benefit of

the community

• All other coaches and buses are subject to PSV Regulations –Insured for Hire and Reward

Not covered for hire/rewardFares allowed provided no profit

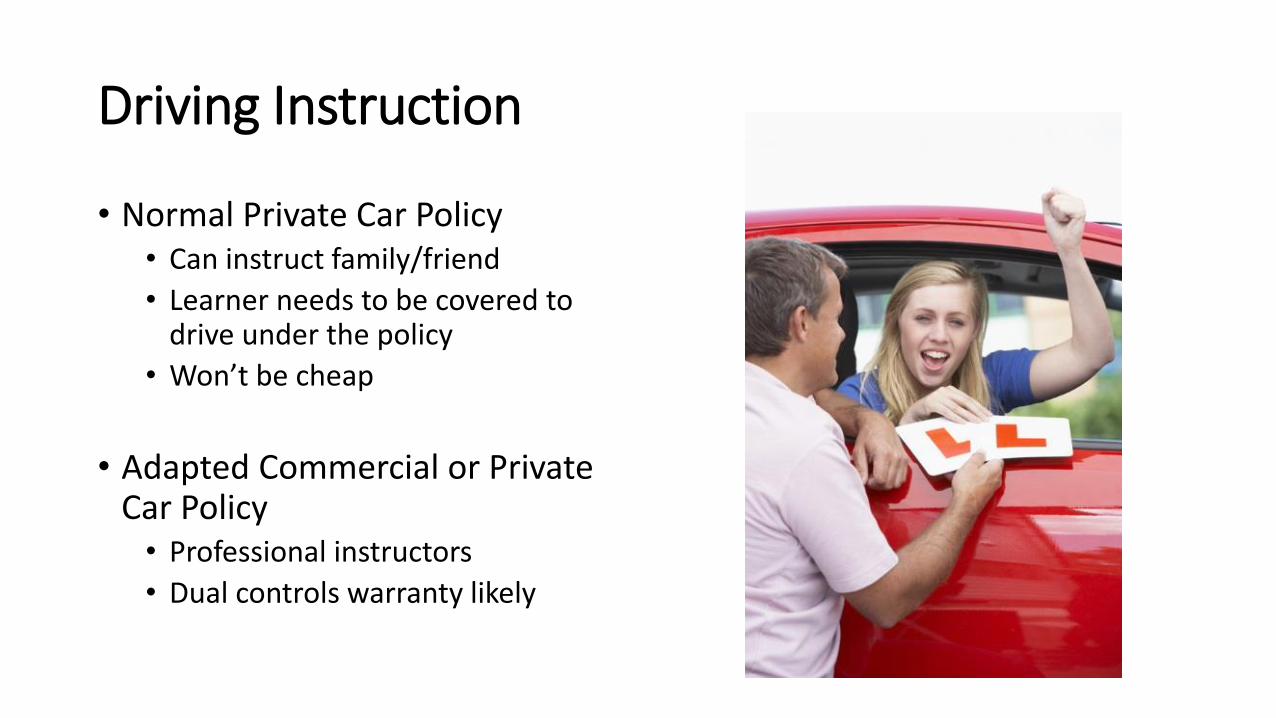

Driving Instruction

• Normal Private Car Policy• Can instruct family/friend

• Learner needs to be covered to drive under the policy

• Won’t be cheap

• Adapted Commercial or Private Car Policy• Professional instructors

• Dual controls warranty likely

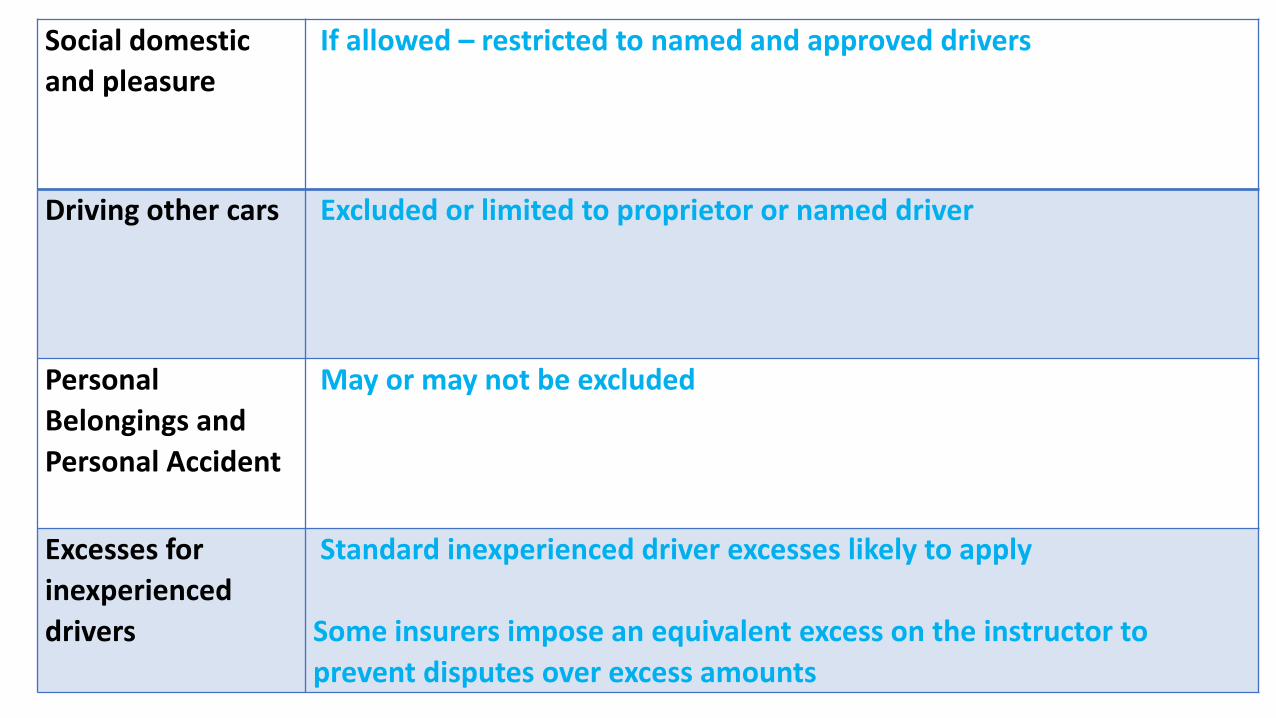

Social domestic

and pleasure

If allowed – restricted to named and approved drivers

Driving other cars Excluded or limited to proprietor or named driver

Personal

Belongings and

Personal Accident

May or may not be excluded

Excesses for

inexperienced

drivers

Standard inexperienced driver excesses likely to apply

Some insurers impose an equivalent excess on the instructor to

prevent disputes over excess amounts

Contingent Liability

• Applies when somebody else uses own car on ‘your’ business

• Contingent liability covers situations where that ‘somebody else’ is not properly insured

• Third party cover only

• Excludes and vehicles owned or being driven by the policyholder

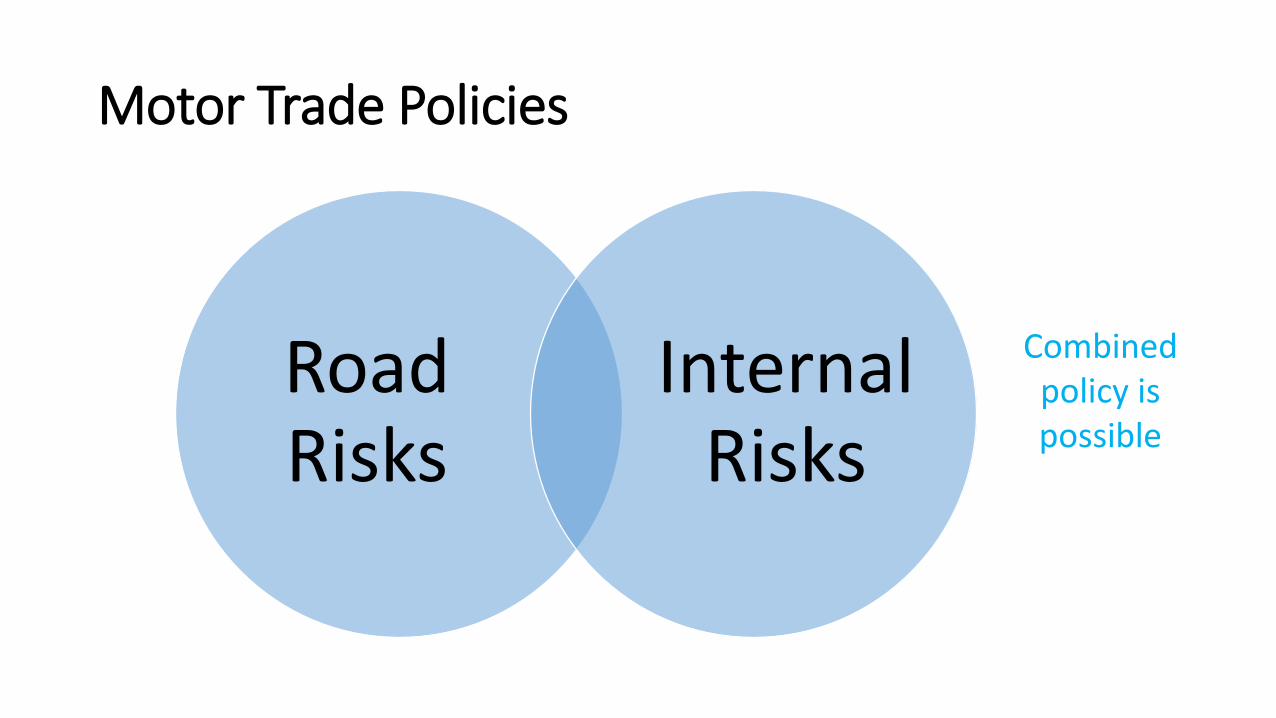

Motor Trade Policies

Road Risks

Internal Risks

Combined policy is possible

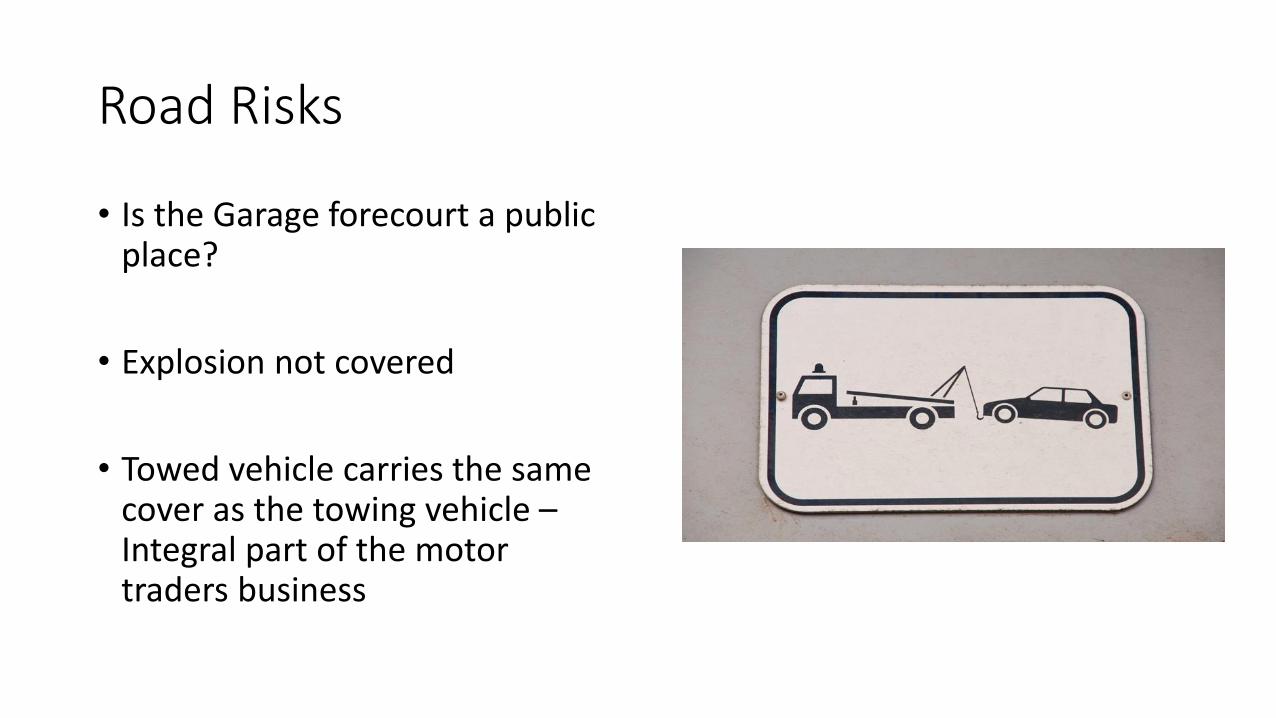

Road Risks

• Is the Garage forecourt a public place?

• Explosion not covered

• Towed vehicle carries the same cover as the towing vehicle –Integral part of the motor traders business

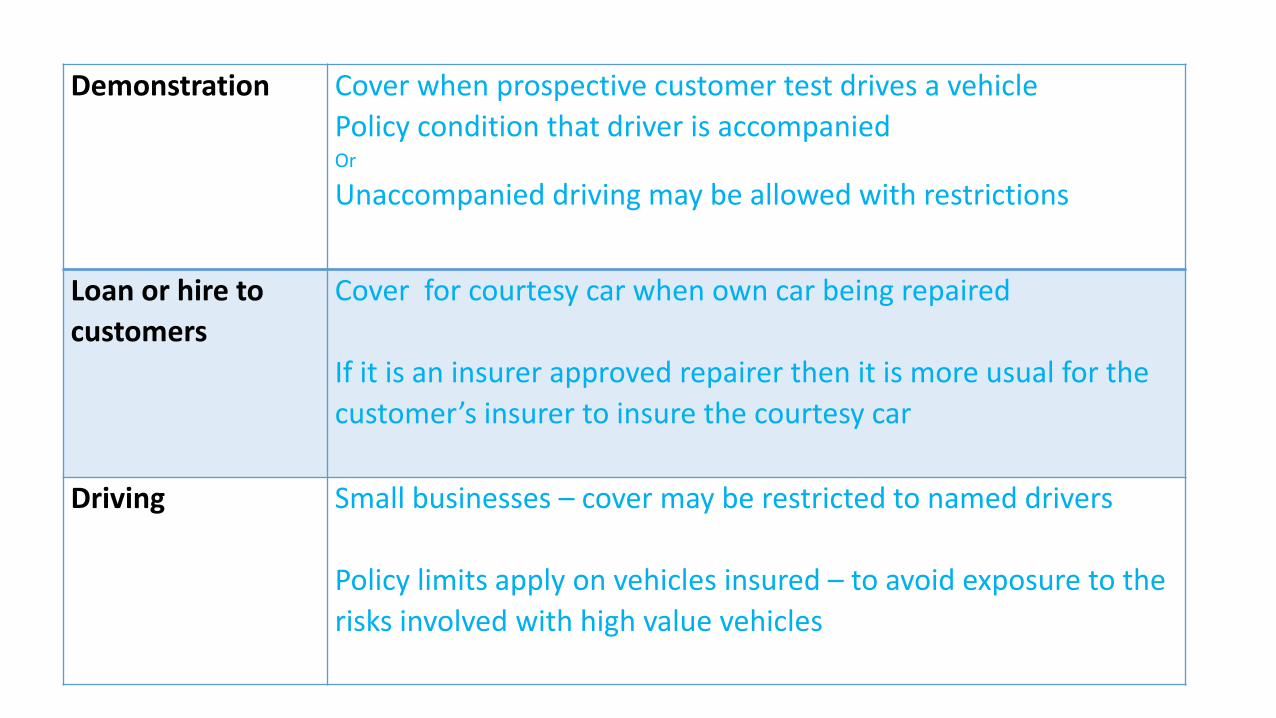

Demonstration Cover when prospective customer test drives a vehicle

Policy condition that driver is accompaniedOr

Unaccompanied driving may be allowed with restrictions

Loan or hire to

customers

Cover for courtesy car when own car being repaired

If it is an insurer approved repairer then it is more usual for the

customer’s insurer to insure the courtesy car

Driving Small businesses – cover may be restricted to named drivers

Policy limits apply on vehicles insured – to avoid exposure to the

risks involved with high value vehicles

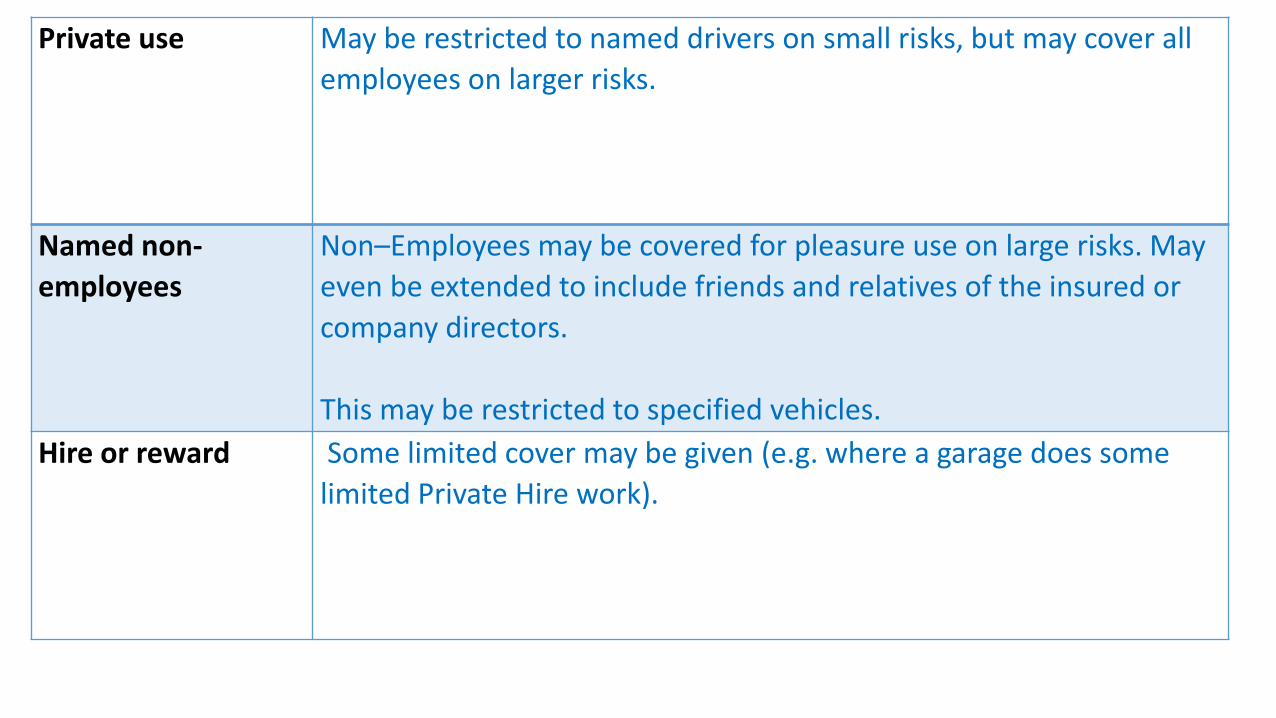

Private use May be restricted to named drivers on small risks, but may cover all

employees on larger risks.

Named non-

employees

Non–Employees may be covered for pleasure use on large risks. May

even be extended to include friends and relatives of the insured or

company directors.

This may be restricted to specified vehicles.

Hire or reward Some limited cover may be given (e.g. where a garage does some

limited Private Hire work).

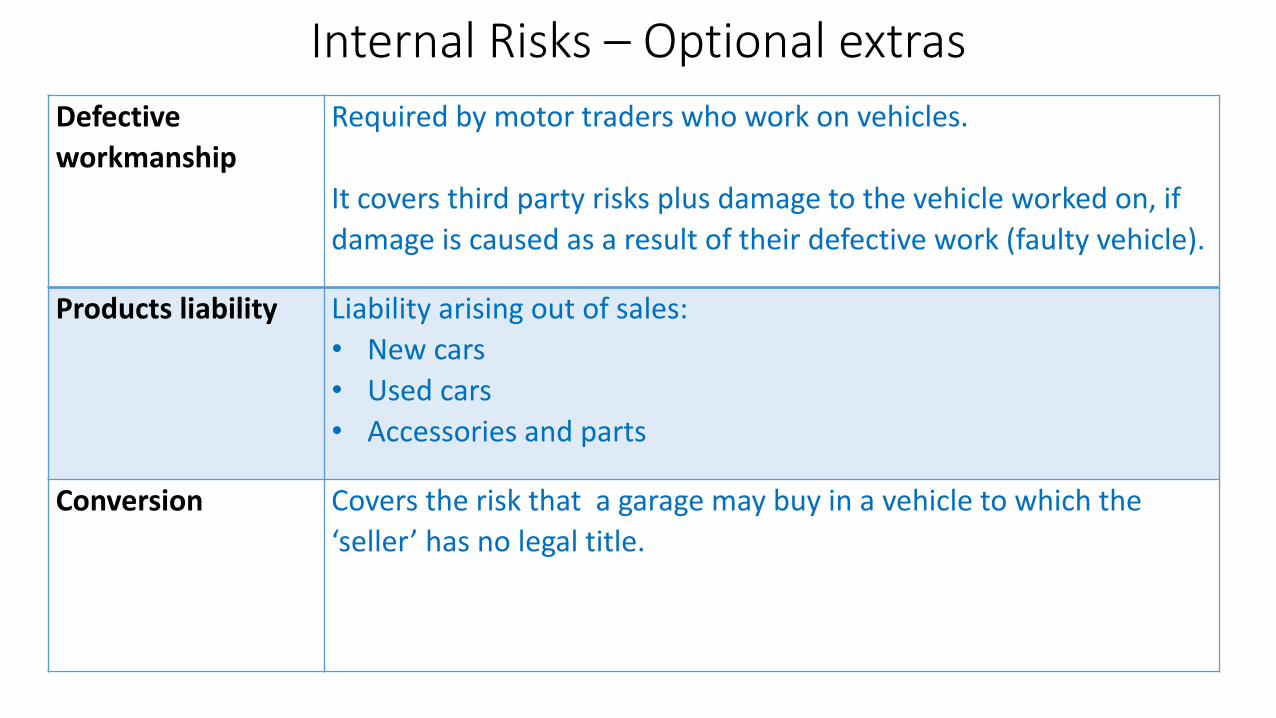

Internal Risks – Optional extras

Defective

workmanship

Required by motor traders who work on vehicles.

It covers third party risks plus damage to the vehicle worked on, if

damage is caused as a result of their defective work (faulty vehicle).

Products liability Liability arising out of sales:

• New cars

• Used cars

• Accessories and parts

Conversion Covers the risk that a garage may buy in a vehicle to which the

‘seller’ has no legal title.

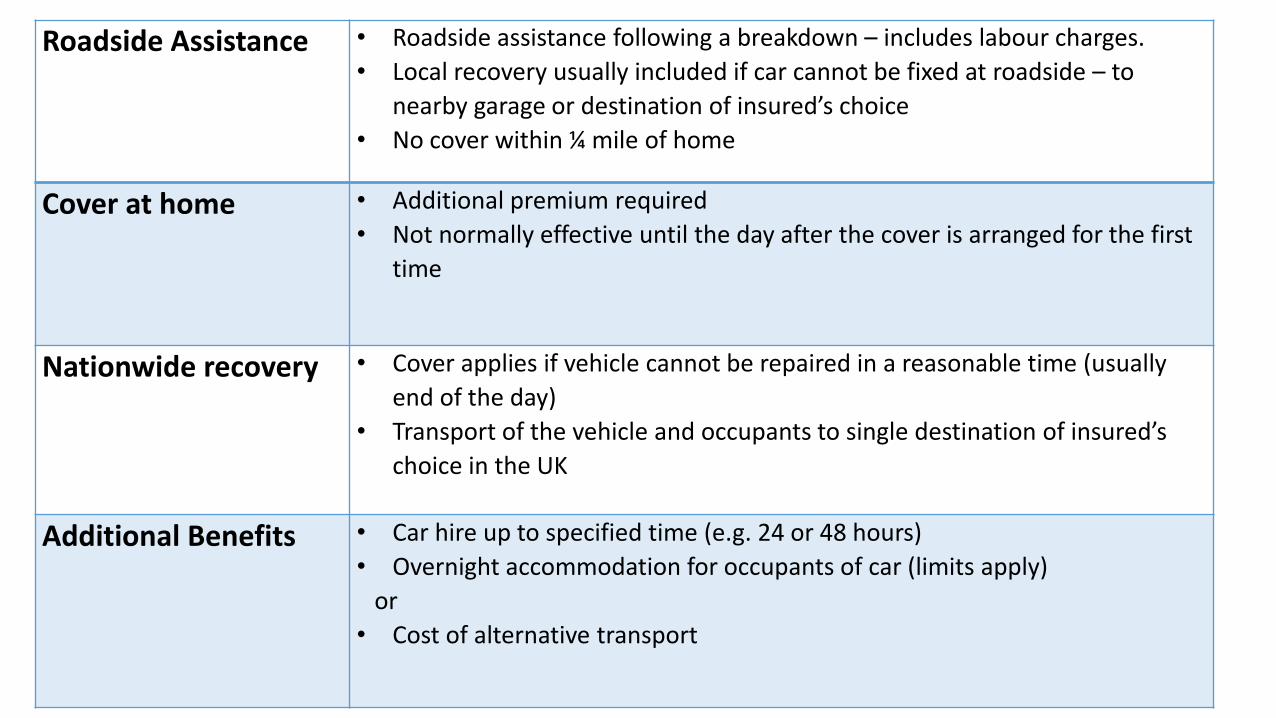

Roadside Assistance • Roadside assistance following a breakdown – includes labour charges.

• Local recovery usually included if car cannot be fixed at roadside – to

nearby garage or destination of insured’s choice

• No cover within ¼ mile of home

Cover at home • Additional premium required

• Not normally effective until the day after the cover is arranged for the first

time

Nationwide recovery • Cover applies if vehicle cannot be repaired in a reasonable time (usually

end of the day)

• Transport of the vehicle and occupants to single destination of insured’s

choice in the UK

Additional Benefits • Car hire up to specified time (e.g. 24 or 48 hours)

• Overnight accommodation for occupants of car (limits apply)

or

• Cost of alternative transport

Breakdown – Main Exclusions

• Replacement Parts

• Labour – not at the roadside

• Unroadworthy vehicle

• Supplying spare wheel

• Locksmith, body glass or tyre specialist

• Ferry crossing or toll charges

• Stranded - beach, bog, ditch, etc.

• Breakdown on motor trade premises

• Transportation of animals

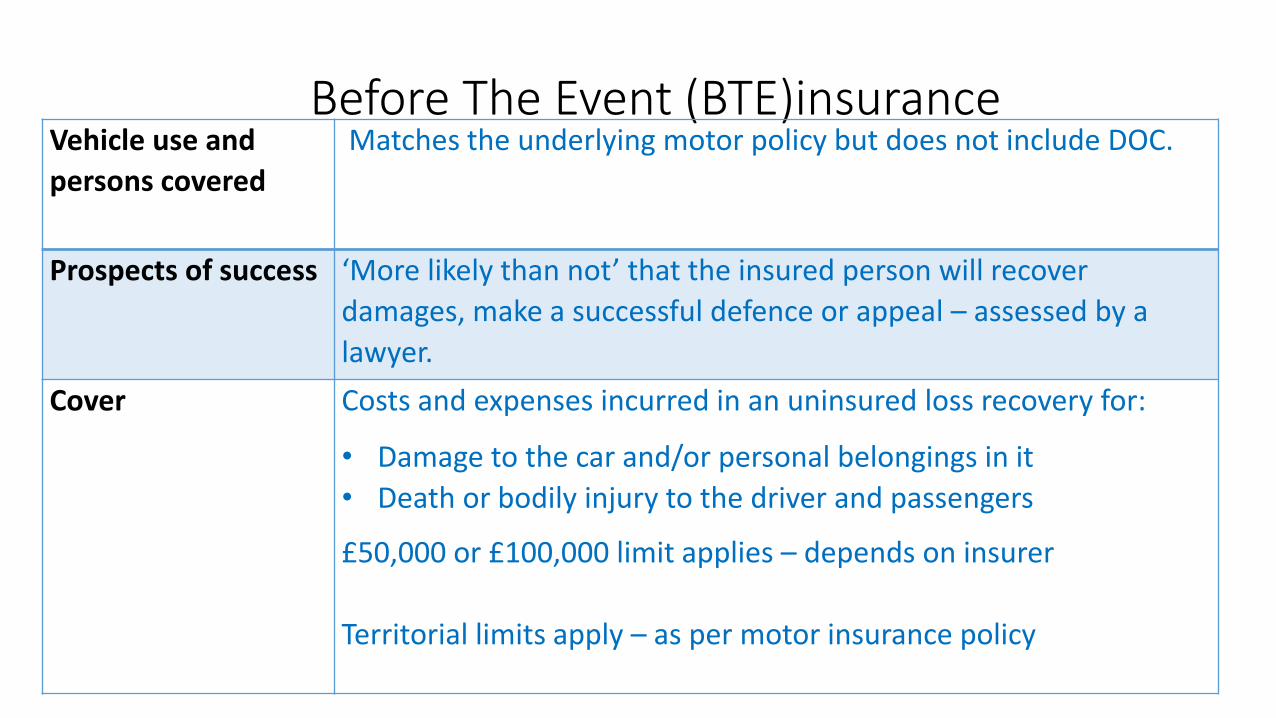

Before The Event (BTE)insuranceVehicle use and

persons covered

Matches the underlying motor policy but does not include DOC.

Prospects of success ‘More likely than not’ that the insured person will recover

damages, make a successful defence or appeal – assessed by a

lawyer.

Cover Costs and expenses incurred in an uninsured loss recovery for:

• Damage to the car and/or personal belongings in it

• Death or bodily injury to the driver and passengers

£50,000 or £100,000 limit applies – depends on insurer

Territorial limits apply – as per motor insurance policy

BTE Exclusions

• Deliberate or intentionally caused claims by insured

• Costs and expenses not agreed to by insurer

• Legal action the insurer has not agreed to

• Fines, penalties, compensation, damages

• Prosecutions for dishonesty

• Applications for judicial review

• General exclusions matching the main motor policy

BTE Conditions

• Appeal or defence of an appeal must be reported to the insurer within 10 days of the court deadline

• Insured persons must keep to the terms of the policy

• Contracts (Rights of Third Parties) Act 1999 does not apply

• Incidents must be reported as soon as possible and an absolute time limit of 180 days – from date of knowledge of an insured event

More BTE Conditions

• Insurer appoints solicitor –relevant law society to choose if insured and insurer cannot agree

• Co-operation with solicitor plus requirement to keep insurer informed – fail to do so leads to withdrawal of cover

Conditional Fee Arrangement (CFA’s)

• No win/no fee

• Solicitor does not charge unless he/she wins the case

• Loser still responsible for winners costs

• CFA’s normally linked to After the Event Insurance – most of us could not afford to pay winner’s costs