Embed Size (px)

Citation preview

Borrowing

Money Guides

There are lots of different ways to borrow money; overdrafts, personal loans, buying on credit and mortgages, are all forms of borrowing. It's a good idea to find out about the different options availableso you can choose which one is best for you and be sure you'll be able to afford the repayments. We have put together this guide to help you.

An easy, step-by-step guide to borrowing

Read straight through the Guide or jump to a particular section of interest as outlined on our contents page.

We’ve included a user-friendly glossary to help youmake sense of the jargon! You can find all red words throughout the Guide in the glossary.

LOANS ££

MR. MANAGER

Provided by

Part of www.NationwideEducation.co.uk. Independent of Nationwide products and services. © Nationwide Building Society, 2013

Check out our Money GuidesClick on the links below to view the guides for:

Savings and Investments

Handling Debt

Spending Wisely

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

Contents

Borrowing Guide Money Guides

CONTENTSBorrowing GuideClick on a Section to jump straight to that page.

Section 1: Things to think about before you borrow

Section 2: Can you afford the repayments?

Section 3: Overdrafts

Section 4: Loan providers

Section 5: How loans work

Section 6: Personal loans

Section 7: Special types of loans

Section 8: Loans for learners

Section 9: Car loans and finance

Section 10: Credit and store cards

Section 11: Other forms of credit

Section 12: Loans for home owners

Section 13: Loans to be cautious about

Section 14: Compare your choices

Section 15: Applications and credit checks

Section 16: Insurances

Section 17: If things go wrong

Section 18: Tips when borrowing

Appendix

a) What does all this jargon mean (glossary)

b) Useful contacts

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 1: page 1 of 1

Borrowing Guide Money Guides

SECTION

Do you really need to borrow?

Calculate the real cost!

What are you borrowing for, and for how long?

1 Things to think about before you borrow

Different methods of borrowing will suit different types of people at different times in their lives and which is best for you will depend on your borrowing needs and your personal circumstances. However, there are a few things you should first give consideration to.

Do you really need to borrow? First of all, it seems obvious – but could you wait until you have saved enough instead of borrowing? Or do you already have savings you could use? Could you be eligible for any of the many benefits, grants and different types of financial assistance available?

• Why not check at:www.turn2us.org.uk

Calculate the real cost! You should always take the time to calculate, as far as possible, what the real cost of the various borrowing options would be! Work out not only what you think the monthly payments will be, but also what the total cost over the time you plan to keep the loan will be. That way you will be comparing like with like! Also factor in fees or insurances.

What are you borrowing for, and for how long?Give some thought to what you need to borrow money for. Perhaps you just need to cover a cash shortfall until your next payday? Perhaps you have an unexpected bill to pay, need to buy a replacement household item, or want to fund something more expensive like a holiday, wedding or car? Your answer will help determine what type of borrowing is best for you.

If you’re borrowing for a specific item, say a washing machine or even a car, you get the benefit of using it as you pay for it! This is great news! However, if you are thinking about taking a loan out over a considerable length of time, remember to factor in the possible useful life span of the item. You may find yourself in the position of needing to replace the item, whilst still being left with an outstanding loan to repay!

Our guide will help you consider the different borrowing options available so you can choose which one is best for you.

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 2: page 1 of 3

Borrowing Guide Money Guides

Assess your current situation

If circumstances change

Budget Sheet

Can you afford the repayments?

It is vitally important that you consider carefully whether you can afford to take on any borrowing. Your goal when borrowing money should be to remain in control, making sure that you can repay the money comfortably and not overstretch yourself.

Assess your current situationTo get a better idea of how the cost of any borrowing will fit into your overall budget, take time to relook at all your finances.

Work out your income (salary, benefits and any other income) and your outgoings, both home (rent or mortgage, council tax, utilities, insurances, telephone, TV, etc.) and personal (food, drink, travel, clothes, toiletries, etc.). Remember to include everything – as the little things can add up. Use the budget sheet (overleaf) to aid you. By adding up all your monthly income and deducting your monthly outgoings, you will get a clear picture of how much you want to borrow and how much you can afford to commit to in repayments.

Be wary if you find that your outgoings are already close to, or more than your income! It may not be a good idea for you to borrow more. On the other hand, just because you find you can afford to borrow, doesn’t mean that a specific type of borrowing is right for you. Try to avoid ending up with more financial commitments than you really have to.

You also have to factor in if any of the borrowing is at variable interest rates – could you afford to meet repayments if interest rates increased.

If circumstances changeNone of us can accurately predict the future, but it’s wise to think ahead and be aware of how a change in interest rates would affect your ability to repay any loan or credit card. For example if interest rates were to rise and you were not on a fixed rate, would you struggle with repayments? What about your personal circumstances? What if you are unable to work because of a serious illness, injury, or if there’s a reduction in overtime, bonus or commission, or you are made redundant? How would you manage the repayments then? Most lenders offer insurance cover to help you to keep up repayments (see Section 16).

SECTION 2

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 2: page 2 of 3

Borrowing Guide Money Guides

Assess your current situation

If circumstances change

Budget Sheet

Can you afford the repayments?

To get a better idea of how the cost of any borrowing will fit into your overall budget, take time to re-look at all your finances.

SECTION 2: page 3 of 3

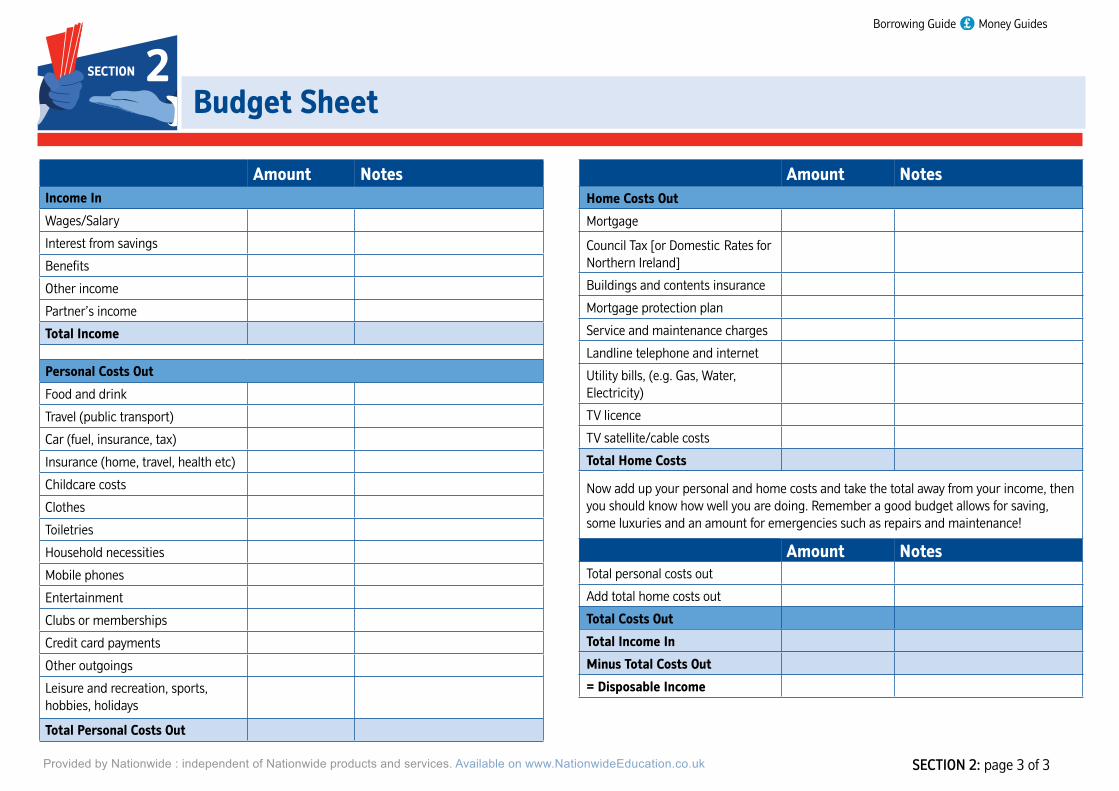

Budget Sheet

Provided by Nationwide : independent of Nationwide products and services. Available on www.NationwideEducation.co.uk

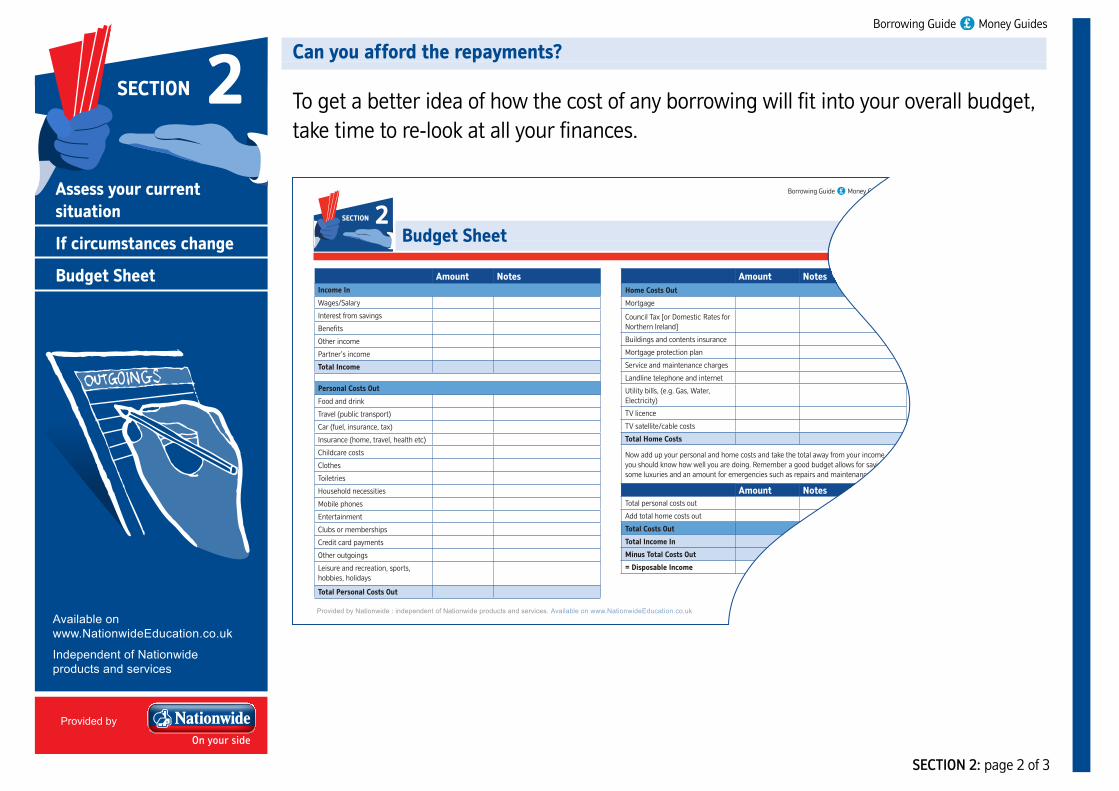

Amount NotesIncome In

Wages/Salary

Interest from savings

Benefits

Other income

Partner’s income

Total Income

Personal Costs Out

Food and drink

Travel (public transport)

Car (fuel, insurance, tax)

Insurance (home, travel, health etc)

Childcare costs

Clothes

Toiletries

Household necessities

Mobile phones

Entertainment

Clubs or memberships

Credit card payments

Other outgoings

Leisure and recreation, sports, hobbies, holidays

Total Personal Costs Out

Amount NotesHome Costs Out

Mortgage

Council Tax [or Domestic Rates for Northern Ireland]

Buildings and contents insurance

Mortgage protection plan

Service and maintenance charges

Landline telephone and internet

Utility bills, (e.g. Gas, Water, Electricity)

TV licence

TV satellite/cable costs

Total Home Costs

Now add up your personal and home costs and take the total away from your income, then you should know how well you are doing. Remember a good budget allows for saving, some luxuries and an amount for emergencies such as repairs and maintenance!

Amount NotesTotal personal costs out

Add total home costs out

Total Costs Out

Total Income In

Minus Total Costs Out

= Disposable Income

Borrowing Guide Money Guides

SECTION 2

SECTION 2

SECTION 2: page 3 of 3

Budget Sheet

Provided by Nationwide : independent of Nationwide products and services. Available on www.NationwideEducation.co.uk

Amount NotesIncome In

Wages/Salary

Interest from savings

Benefits

Other income

Partner’s income

Total Income

Personal Costs Out

Food and drink

Travel (public transport)

Car (fuel, insurance, tax)

Insurance (home, travel, health etc)

Childcare costs

Clothes

Toiletries

Household necessities

Mobile phones

Entertainment

Clubs or memberships

Credit card payments

Other outgoings

Leisure and recreation, sports, hobbies, holidays

Total Personal Costs Out

Amount NotesHome Costs Out

Mortgage

Council Tax [or Domestic Rates for Northern Ireland]

Buildings and contents insurance

Mortgage protection plan

Service and maintenance charges

Landline telephone and internet

Utility bills, (e.g. Gas, Water, Electricity)

TV licence

TV satellite/cable costs

Total Home Costs

Now add up your personal and home costs and take the total away from your income, then you should know how well you are doing. Remember a good budget allows for saving, some luxuries and an amount for emergencies such as repairs and maintenance!

Amount NotesTotal personal costs out

Add total home costs out

Total Costs Out

Total Income In

Minus Total Costs Out

= Disposable Income

Borrowing Guide Money Guides

SECTION 2

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 3: page 1 of 1

Borrowing Guide Money Guides

Overdraft uses

Finding out what’s what

Overdrafts

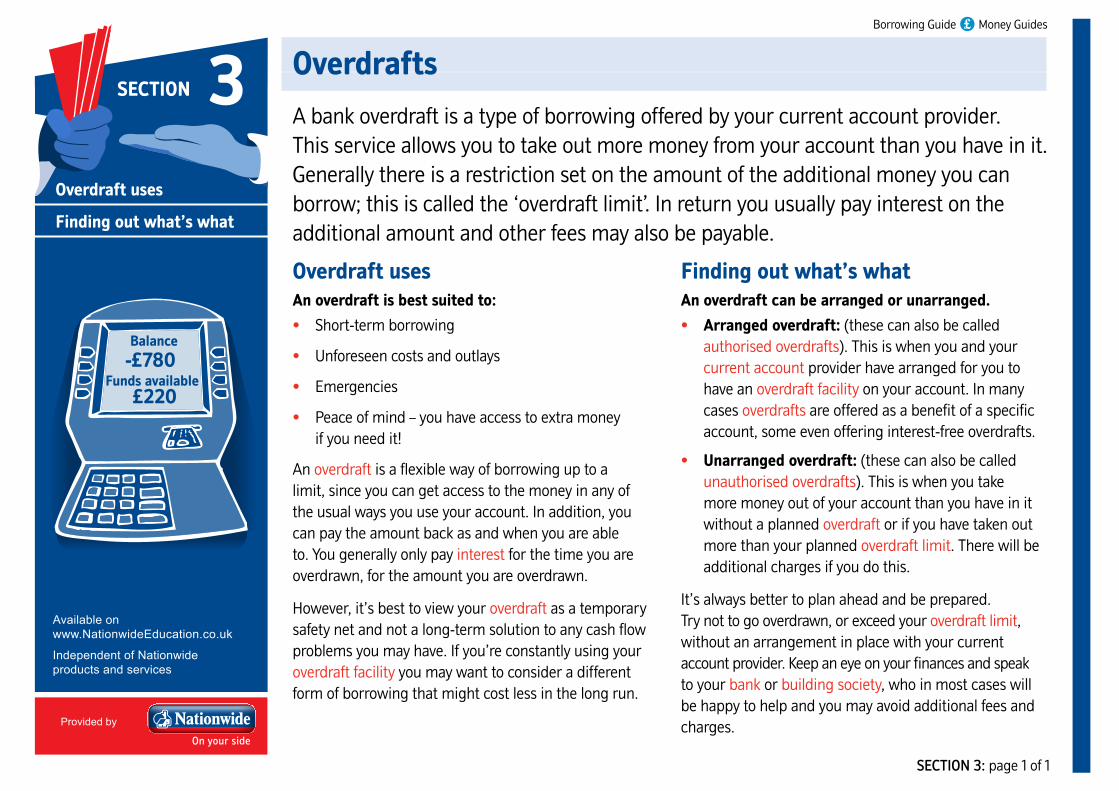

A bank overdraft is a type of borrowing offered by your current account provider. This service allows you to take out more money from your account than you have in it. Generally there is a restriction set on the amount of the additional money you can borrow; this is called the ‘overdraft limit’. In return you usually pay interest on the additional amount and other fees may also be payable.

Overdraft usesAn overdraft is best suited to:

• Short-term borrowing

• Unforeseen costs and outlays

• Emergencies

• Peace of mind – you have access to extra money if you need it!

An overdraft is a flexible way of borrowing up to a limit, since you can get access to the money in any of the usual ways you use your account. In addition, you can pay the amount back as and when you are able to. You generally only pay interest for the time you are overdrawn, for the amount you are overdrawn.

However, it’s best to view your overdraft as a temporary safety net and not a long-term solution to any cash flow problems you may have. If you’re constantly using your overdraft facility you may want to consider a different form of borrowing that might cost less in the long run.

Finding out what’s whatAn overdraft can be arranged or unarranged.

• Arranged overdraft: (these can also be called authorised overdrafts). This is when you and your current account provider have arranged for you to have an overdraft facility on your account. In many cases overdrafts are offered as a benefit of a specific account, some even offering interest-free overdrafts.

• Unarranged overdraft: (these can also be called unauthorised overdrafts). This is when you take more money out of your account than you have in it without a planned overdraft or if you have taken out more than your planned overdraft limit. There will be additional charges if you do this.

It’s always better to plan ahead and be prepared. Try not to go overdrawn, or exceed your overdraft limit, without an arrangement in place with your current account provider. Keep an eye on your finances and speak to your bank or building society, who in most cases will be happy to help and you may avoid additional fees and charges.

SECTION 3

-£780Balance

Funds available£220

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 4: page 1 of 2

Borrowing Guide Money Guides

Finding the right one for you

What lenders look at

Loan providers

There are so many different organisations willing to lend you money, in a vast array of different ways. Walk down the high street, turn on the TV, open a newspaper or search the internet and you will be spoilt for choice! Or you can simply just wait for the offers to pop through your letterbox or into your inbox! But the key is finding the best type of borrowing for what you need it for, from the right type of responsible lender!

Finding the right one for youIt’s very important to check the lender is licensed with the Office of Fair Trading (OFT) or regulated by the Financial Conduct Authority or the Prudential Regulation Authority.

Be very wary with certain forms of borrowing such as Payday loans, Logbook loans and other types of short-term cash loans. Frequently these loans can charge high interest rates – some even as high as 4,000% APR!

Be especially cautious of Doorstep loans, where you borrow money and the lender calls at your home to collect the repayments. They may be offered by illegal lenders (loan sharks). (See Section 13 ‘Loans to be cautious about’)

Responsible lenders are committed to helping you make financial decisions that best suit your circumstances. They want to ensure that you only take on borrowing which you can afford to repay. They pledge to be open and honest in their dealings with you and to treat you fairly. So take time to find the right lender!

The main places that you can borrow from are:

• Building societies and banks

• Insurance companies

• Credit card providers

• Catalogue companies

• Specialist loan companies or finance houses

• Loan brokers

• Credit unions

• Community Development Finance Institutions

• Motor manufacturers and dealerships for car loans

• Student Loan Company for student loans

• Specialist mortgage companies for mortgages and other home loans

SECTION 4

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 4: page 2 of 2

Borrowing Guide Money Guides

Finding the right one for you

What lenders look at

Loan providers

What lenders look at!Remember there are lots of things that lenders look at when you apply

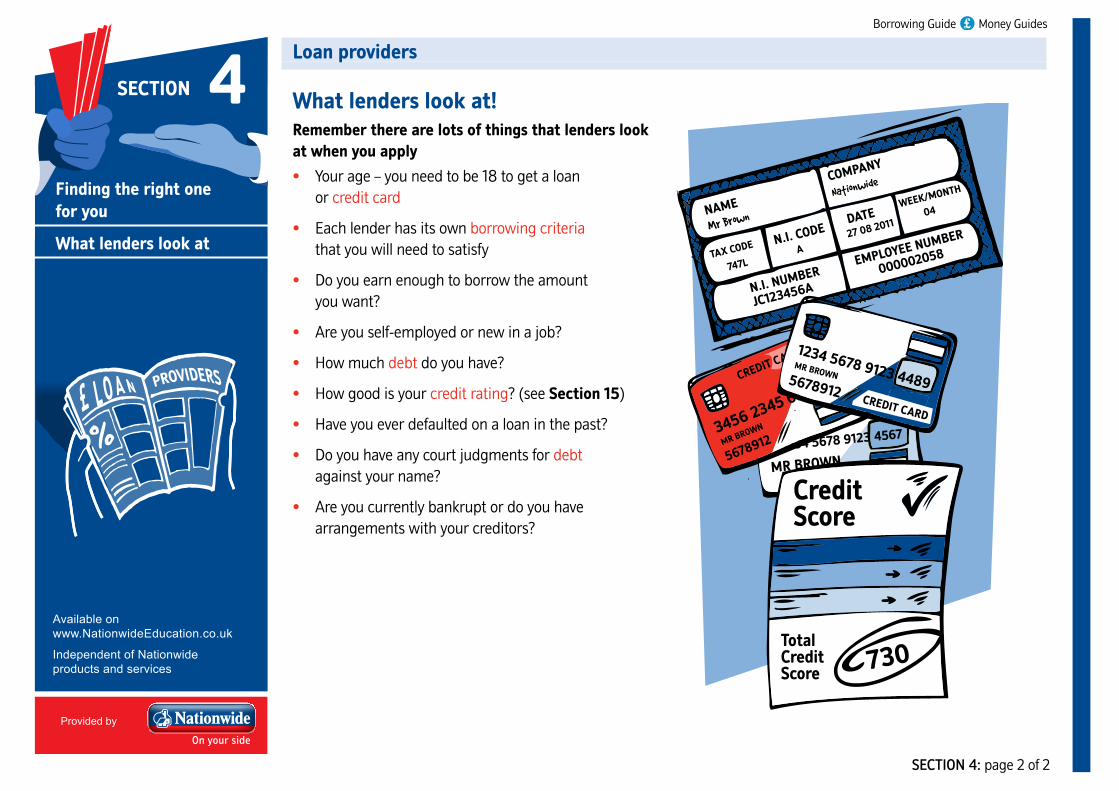

• Your age – you need to be 18 to get a loan or credit card

• Each lender has its own borrowing criteria that you will need to satisfy

• Do you earn enough to borrow the amount you want?

• Are you self-employed or new in a job?

• How much debt do you have?

• How good is your credit rating? (see Section 15)

• Have you ever defaulted on a loan in the past?

• Do you have any court judgments for debt against your name?

• Are you currently bankrupt or do you have arrangements with your creditors?

1234 5678 9123 4567

MR BROWN

CREDIT CARD

NAME

747LA

27 08 201104

TAX CODE N.I. CODE

N.I. NUMBEREMPLOYEE NUMBER

000002058

JC123456A

DATEWEEK/MONTH

COMPANY

3456 2345 6789

5678912MR BROWN

CREDIT CARD1234 5678 9123 44895678912

MR BROWN

CREDIT CARD

730

Credit Score

Total Credit Score

SECTION 4

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 5: page 1 of 2

Borrowing Guide Money Guides

How much will you pay?

APR

Compare ‘like for like’

How loans work

It’s important to know about all of the extra costs involved when you apply for a loan.

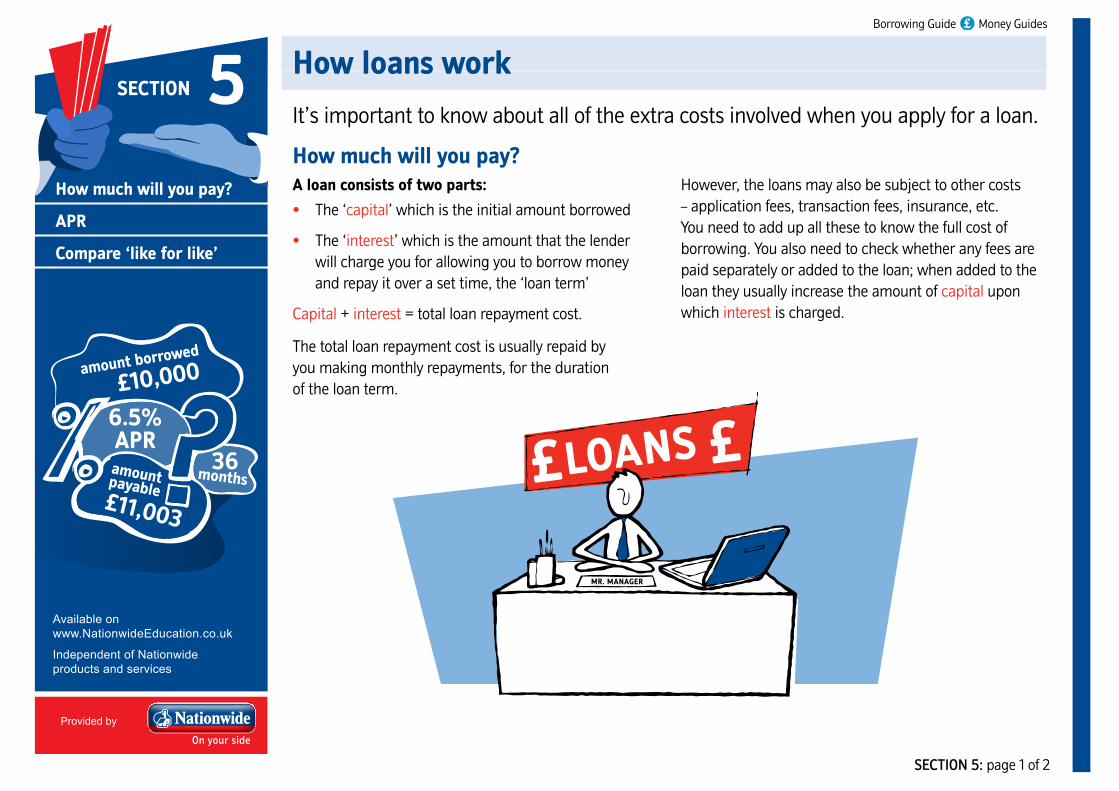

How much will you pay?A loan consists of two parts:

• The ‘capital’ which is the initial amount borrowed

• The ‘interest’ which is the amount that the lender will charge you for allowing you to borrow money and repay it over a set time, the ‘loan term’

Capital + interest = total loan repayment cost.

The total loan repayment cost is usually repaid by you making monthly repayments, for the duration of the loan term.

However, the loans may also be subject to other costs – application fees, transaction fees, insurance, etc. You need to add up all these to know the full cost of borrowing. You also need to check whether any fees are paid separately or added to the loan; when added to the loan they usually increase the amount of capital upon which interest is charged.

LOANS ££

MR. MANAGER

SECTION 5

APR

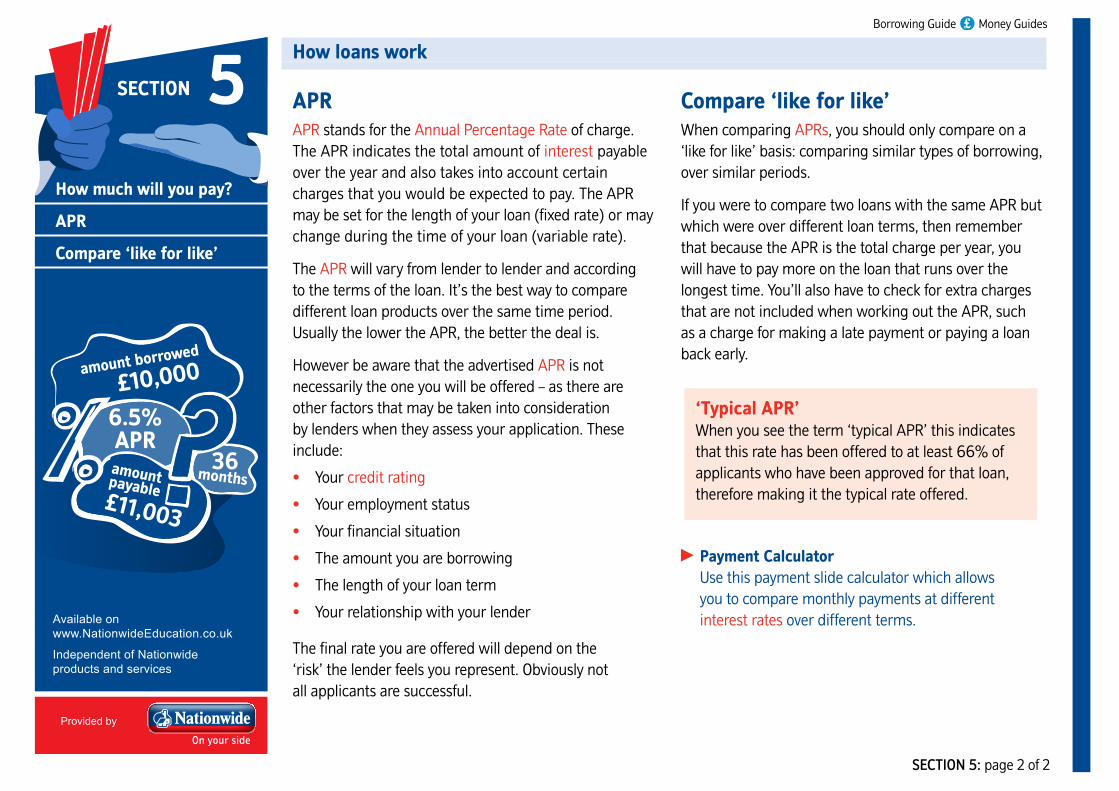

£10,000amount borrowed

months

£11,003

36

6.5%

amountpayable

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 5: page 2 of 2

Borrowing Guide Money Guides

How much will you pay?

APR

Compare ‘like for like’

How loans work

APRAPR stands for the Annual Percentage Rate of charge. The APR indicates the total amount of interest payable over the year and also takes into account certain charges that you would be expected to pay. The APR may be set for the length of your loan (fixed rate) or may change during the time of your loan (variable rate).

The APR will vary from lender to lender and according to the terms of the loan. It’s the best way to compare different loan products over the same time period. Usually the lower the APR, the better the deal is.

However be aware that the advertised APR is not necessarily the one you will be offered – as there are other factors that may be taken into consideration by lenders when they assess your application. These include:

• Your credit rating

• Your employment status

• Your financial situation

• The amount you are borrowing

• The length of your loan term

• Your relationship with your lender

The final rate you are offered will depend on the ‘risk’ the lender feels you represent. Obviously not all applicants are successful.

Compare ‘like for like’When comparing APRs, you should only compare on a ‘like for like’ basis: comparing similar types of borrowing, over similar periods.

If you were to compare two loans with the same APR but which were over different loan terms, then remember that because the APR is the total charge per year, you will have to pay more on the loan that runs over the longest time. You’ll also have to check for extra charges that are not included when working out the APR, such as a charge for making a late payment or paying a loan back early.

Payment CalculatorUse this payment slide calculator which allows you to compare monthly payments at different interest rates over different terms.

‘Typical APR’When you see the term ‘typical APR’ this indicates that this rate has been offered to at least 66% of applicants who have been approved for that loan, therefore making it the typical rate offered.

SECTION 5

APR

£10,000amount borrowed

months

£11,003

36

6.5%

amountpayable

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 6: page 1 of 1

Borrowing Guide Money Guides

Secured loans

Unsecured loans

Personal loans

Loans can either be secured or unsecured. A loan is a way of borrowing a lump sum of money, which you usually repay in fixed instalments over a set period of time (the term). The interest you pay is usually fixed and additionally there will be fees to pay. You can use the APR (Annual Percentage Rate of charge) to compare deals (see Section 5).

Secured loansWith these you have to have something of value as security (an asset), such as a property or car, against which the loan can be ‘secured’. It’s like a guarantee so that, if you’re unable to repay the loan, the lender can take and sell your asset to get its money back. Usually a secured loan allows you to borrow a larger amount of money and may allow you a longer time to pay it back. The most common form of secured loan is a mortgage, and is made against your home (with any value in your home as the security.) Additional borrowing secured against your home with the same lender may be called a further advance or further loan, while additional secured borrowing from a different lender is a second (or subsequent) charge. (See Section 12). As secured loans are less risky for the lender the interest rates are more favourable. However, remember you could be putting your home at risk.

Secured Loans are best for borrowing large amounts of money over the medium/long-term.

Unsecured loansWith these the lender relies on your promise to repay the loan and they are therefore more risky for them. You are legally bound to repay the loan and the lender can take court action against you if you are unable to repay it. Interest rates for unsecured loans tend to be higher because of the increased risk involved. They are usually most suitable if you want a short-term loan and for lower amounts.

Loans are most commonly available from banks, building societies and other financial organisations.

BANK

SECTION 6

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 7: page 1 of 1

Borrowing Guide Money Guides

Credit unions

Community Development Finance Institutions (CDFIs)

Special types of loans

Here are a couple of different lenders who may offer loans suitable to your circumstances.

Credit unionsCredit unions are mutual financial organisations – which are owned and run by their members for their members. They offer loans to their members but you usually have to prove to them that you can save regularly. The APR on their loans is capped by law at 26.8%, but many offer lower rates. Credit union members have a common bond, such as living in the same area, working in the same industry or belonging to the same organisation, church, Housing Association, trade union, etc.

Community Development Finance Institutions (CDFIs) These organisations help people who struggle to get finance from banks, building societies or loan companies. They aim to help deprived communities by offering loans and support at an affordable rate. Some are part-funded by government departments or supported by charities. No membership is needed to get a loan from a CDFI. These loans are usually more expensive than borrowing from a credit union.

SECTION 7

Credit union

CDFIs

I’ll find out if

there’s a Credit

Union locally.

CRISIS

CDFIs

CREDITUNIONS

BUDGETING

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 8: page 1 of 1

Borrowing Guide Money Guides

Student loans

Professional and career development loans

Loans for learners

Here are a couple of different lenders who may offer loans suitable to your circumstances.

Student loansThese are available to students in higher education to help them with study costs, including tuition fees and living expenses.

If you’re a full-time student you can apply for a:

• Tuition Fee Loan to cover tuition fees

• Maintenance Loan to help with living costs

Part -time students can only apply for Tuition Fee Loans.

These are low interest loans. The Maintenance Loan is partly means tested. However, you only start to repay them once you have finished your studies and are earning above a certain amount. The loans are run by the Student Loans Company, but you start by contacting your Local Education Authority (LEA).

Professional and career development loansThis is a loan provided by a participating bank to help you develop your career through education and/or training. You have to be over 18 to qualify and it can be used to fund both tuition fees and living expenses. You can borrow anything between £300 and £10,000 to help you fund up to two years of learning (or three if your course includes work experience). Interest is charged but is paid for by the government during the qualifying period, after which you will be expected to pay it. Interest rates depend on the bank you apply to but are usually quite competitive.

SECTION 8

MaybeI can geta loan.

I want totrain to be anaccountant.

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 9: page 1 of 1

Borrowing Guide Money Guides

A car loan

Car finance

Credit card

Car loans and finance

So what are your options if you want to buy a car?

A car loanThis is a personal loan (see Section 6). The advantage is that you legally own the car.

Car financeThis is where you have an agreement, usually with a car finance company, directly or through a car dealership or manufacturer. With some of these agreements you do not own the car but only have the use of it, subject to certain conditions. There are three main types:

• Hire Purchase (HP): through monthly repayments you repay the purchase price of the car and the agreed interest. A deposit is usually required. The car belongs to the lender until the end of the contract period.

• Personal Contract Purchase (PCP): with this method, you pay an initial deposit, followed by monthly payments over an agreed term and then have the option to pay a final payment, called a Guaranteed Future Value (GFV). If you choose not to make this payment you can return the car with nothing extra to pay. This way of financing a car allows for lower monthly payments, but in order to own the car you will need to make the GFV, which in many cases can be a substantial amount.

• Lease Purchase (LP): this type of financing is similar to a PCP in that you need to make a final payment which is deferred to the end of the agreement, and which must be settled to gain outright ownership. This payment is called the Residual Value. However there is no option to return the car at the end of the contract.

Credit cardDepending on the credit card deal you have and the cost of the car, this may be a viable option for financing your purchase. (See Section 10)

598 0

SECTION 9

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 10: page 1 of 4

Borrowing Guide Money Guides

Credit cards

How they work

How to get a credit card

Charges

How to use one

Store cards

Card hints and tips

Credit and store cards

These are very useful cards to have when you don’t have any cash on you, but what exactly do they offer and is it right for you?

Credit cardsCredit cards are useful in many ways.

• They allow you to pay for goods or services without using cash.

• They offer an easy way of borrowing in the short-term.

• They are flexible, allowing you to spend up to an agreed credit limit and then repay what you have borrowed by making a minimum payment, or to clear your entire balance, or to pay a fixed amount each month.

• Credit cards can also offer you better legal protection when buying goods worth over £100.

• They are useful for buying online or by telephone.

• They may offer a variety of features including promotional offers, air miles, cashback, charity giving and loyalty schemes.

• They offer interest-free credit – can be up to 60 days!

• You can also use most credit cards to withdraw cash, either in the UK or when abroad (but please be aware that this can be an expensive way to get cash).

• It’s possible to transfer debt you have in other places over to your credit card.

• You can take advantage of introductory offers when you first take one out, in some cases allowing you interest-free purchasing for several months.

• You can usually have the option to manage your credit card account online, by phone, or in person at a branch.

PROTECTION

NO NEED FOR CASH

UP TO 60DAYS INTEREST

FREE

FLEXIBLE

EASY

LOYALTY SCHEMES

1234 5678 9123 44895678912

MR BROWN

CREDIT CARD

SECTION10

CREDIT

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 10: page 2 of 4

Borrowing Guide Money Guides

Credit cards

How they work

How to get a credit card

Charges

How to use one

Store cards

Card hints and tips

Credit and store cards

How they workA credit card allows you to use money you don’t have by borrowing money that is supplied by the card provider, to pay for goods or services and then pay this amount back over a period of time.

When you open a credit card account your card provider will provide you with a set credit limit. This is the amount that you are allowed to borrow using your credit card. Care should be taken not to exceed your set credit limit. You may incur charges if you do exceed your set credit limit.

You will be sent a statement each month detailing the amount you owe (the balance). If you can pay off this balance by the date they tell you it’s due, you will not usually pay any interest. Although if any of the balance is from a cash advance, you will normally be charged interest from the next day after withdrawal. In addition there may be some fees or charges e.g. for currency conversions. If you do not pay the total due, you need to at least make a set minimum payment. Interest will then be charged on each of the transactions shown on your statement.

Balance transfer and purchases savings calculator Use this balance transfer and purchases savings calculator to see which credit card offer is best for you. You may have some balances to transfer, a purchase in mind or both. This calculator will show you which offer could save you the most compared to your current credit card.

CREDITCARD

CREDIT

CARD

CASH CARD

PAY HERE

SECTION10

CREDIT

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 10: page 3 of 4

Borrowing Guide Money Guides

Credit cards

How they work

How to get a credit card

Charges

How to use one

Store cards

Card hints and tips

Credit and store cards

How to get a credit cardIf you are over 18, you can apply for one to banks and building societies by filling in an application online, by phone, or in person. If you are successful you will be sent a card which will bear the name and logo of the issuer. It will also identify which international payment scheme it uses; the main ones are Visa and Mastercard. When you see these signs displayed anywhere, including shops, restaurants, garages, and when internet shopping, you can use your credit card to pay.

ChargesWhen you first apply for a credit card you may be able to get a good ‘introductory offer’ which may mean you pay no or less interest for a set initial period of time. However, normally you will be charged a pre-stated rate of interest on your outstanding balance.

If you use your credit card to take money out you will probably start paying interest immediately. Be aware that issuers also charge fees for certain services such as cash withdrawals or balance transfers. You may also face charges if you miss payments or go over your set credit limit.

How to use oneIf you’re there in person, you put your card into the payment machine, and enter your four digit Personal Identification Number (PIN) when the cashier tells you. A microchip inside the card which holds secure data verifies your identity.

The previous method of giving your card to the shop assistant to swipe it through an electronic card reader is still widely used abroad.

You can also use your card to pay for things online or over the phone. You will be asked to give your credit card number, your name as it is written on the card, the expiry date of your card and sometimes the three digit security code on the back of the card.

Payment calculator Use this payment calculator to see how much you would need to pay each month to clear your balance over a set period of time, or how long it would take to clear your balance if you paid off a set amount each month.

SECTION10

CREDIT

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 10: page 4 of 4

Borrowing Guide Money Guides

Credit cards

How they work

How to get a credit card

Charges

How to use one

Store cards

Card hints and tips

Credit and Store cards

Store cardsThese are a form of credit card. However you can usually only use them in a specific store or group of stores. You will be required to fill in an application form and are given a spending limit based on your credit worthiness. You often get special deals or offers related to the store that are not available to other customers. However, they may charge higher interest rates than other credit cards.

Card hints and tips• Consider whether a credit or store card is right

for your circumstances or if a personal loan may be cheaper.

• When you’re choosing a credit card deal, try and make sure you are comparing similar products.

• Make sure you understand the costs and charges of each option and how they work.

• Check the small print on any offers and choose a card that will suit your needs.

• Look beyond any initial promotional rate to understand what interest rate you will be paying on your card, once the promotional period has ended.

• Choose a card with the special feature most useful to you – these may include free insurance, promotional offers, air miles, cashback, charity giving or loyalty schemes.

• Only take on credit that you can realistically afford to repay.

• Always have a plan in place to pay off your credit or store card.

• Set up a Direct Debit to pay off the minimum payment each month, so you avoid missing a payment.

• Remember, if you only make the minimum payment, you will be paying a lot in interest over a long time.

• Only withdraw cash using your credit card as a last resort.

Look out for ‘contactless’ cards!More and more debit, credit and pre-payment cards with ‘contactless’ technology are becoming available. You can use them to make low value payments (currently £20 or less) without having to insert your card into the chip & PIN machine and typing in a PIN. You simply hold it to the reader to pay.

SECTION10

CREDIT

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 11: page 1 of 1

Borrowing Guide Money Guides

Other forms of credit

If you don’t have or want to use a credit card you can apply for other forms of credit, such as:

• In-store finance: deals offered in stores may be tempting to help you pay for expensive purchases and are convenient, as you do not have to shop around for an alternative way to get the funds. However, you may find that overall it can be more expensive than other ways of borrowing.

• Hire Purchase (HP): with Hire Purchase you make monthly payments to repay the purchase price of the item and the agreed interest. You don’t own the item until you’ve paid back all the money you owe, until then it actually belongs to the lender. You are essentially ‘hiring it’, until you pay off the whole amount.

• ‘Buy now, pay later’: this type of offer is often made in stores or in mail order catalogues. You get your goods now and put off payments until a later time. You will eventually pay back the cost in instalments, usually with a high interest rate. This may be convenient, but the initial purchase price is often higher than you may have been able to get elsewhere.

IN-STOREFINANCE

AVAILABLE!£1,800

£1,200

SALE

BUY NOWPAY LATER

SECTION11

BUY NOWPAY LATER!

IN-STOREFINANCEAVAILABLE!

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 12: page 1 of 1

Borrowing Guide Money Guides

Mortgage

Remortgage

Secured loans/further advances

Loans for home owners

Whether you are a first time buyer, seeking to move home, remortgage or take out a further advance, you will usually be making one of the most long-term loan commitments of your life.

MortgageA mortgage is a type of loan secured against your home. If you then want to take out further loans, or borrow for other things, you may, as a home owner, have more options available to you.

RemortgagePeople may choose to remortgage to obtain better terms and conditions (usually the rate of interest), or to borrow more money for many reasons. If your home has increased in value during the period of your mortgage, you could borrow more by ‘raising capital’ using the equity in your home. (Equity = the current value of your home – the total amount outstanding on all mortgages and loans secured against the property).

If you have enough equity in your property and can afford the new payments this is an option that might be attractive to you particularly if you are also able to obtain a lower interest rate. However, remember this is a secured, long-term loan and weigh up the pros and cons.

Further advances/secured loansA further advance is a loan secured by the existing mortgage deed on your property and adds an additional claim against your home in the event that you fail to keep up your repayments.

If you are a home owner it may be possible to borrow money by getting a secured loan and use your home as the security. This loan could be with any lender you choose or you may decide to get an additional loan from your current mortgage provider. There will be various deals on offer, both fixed and variable.

Remember though that your home may be at risk if you do not keep up payments on a mortgage or any other loan secured on it. Check out our Home Guides below:

First Time Buyers’ Guide

Home Buyers’ Guide

Remortgaging Guide

Selling Guide

SECTION12

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 13: page 1 of 2

Borrowing Guide Money Guides

Payday loans

Logbook loans

Pawnbrokers

Doorstep loans

Loan sharks

Loans to be cautious about

It is very important to check that any lender you are considering is licensed with the Office of Fair Trading (OFT) or regulated by the Financial Conduct Authority or the Prudential Regulation Authority.

Payday loansThese are a form of short-term cash loan where you borrow money to last you until you next get paid; it’s a way of getting cash quickly. However, it’s important to be aware of the high interest rates that can be charged – some even as high as 4,000% APR! They should only ever be used for the shortest time necessary and only if you have no alternative.

Logbook loansThis is another form of short-term cash loan where borrowing is arranged against the value of your car. Cash can be obtained quickly. Usually the car needs to be less than eight years old, road worthy and of sufficient value for you to qualify. You keep your car and use it as normal, but the lender will hold the log book for the duration of the loan. Be aware though that interest rates may be high and you risk your car being sold without even going to court if you miss a payment!

PawnbrokersPawnbroking has long been a way to get hold of cash in a hurry. Through a pawnbroker you can get a short-term cash loan but you must leave some item of value as security in return for the loan. At the end of the agreed term, typically six months, you repay the loan and the interest and get back your item. But if you cannot repay the loan in full, the pawnbroker may keep or sell your item. Interest rates can be high.

SECTION13

%

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 13: page 2 of 2

Borrowing Guide Money Guides

Payday loans

Logbook loans

Pawnbrokers

Doorstep loans

Loan sharks

Loans to be cautious about

Doorstep loansAlso known as Home Credit Loans, these are where you borrow money and the lender calls at your home to collect the repayments. This is usually a very expensive way to borrow money as you will be charged a high rate of interest as well as collection charges. You should be very clear about how much you are borrowing, the interest rate, what payments will be, over how long and the total amount you will have to pay in the end.

Loan sharks Report any illegal lenders (often called loan sharks) that approach you to the police and the trading standards team at your local council. Also inform the special government taskforces:

In EnglandTel: 0300 555 2222 (Available 24 hours) Text: LOAN SHARK and the lender’s details to 60003

In WalesTel: 0300 123 3311 (Available 24 hours) Text: LOAN SHARK and the lender’s details to 60003

In ScotlandTel: 0141 2876 655

In Northern IrelandTel: 0300 123 6262

Or visit: www.gov.uk/report-loan-shark

SECTION13

%

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 14: page 1 of 2

Borrowing Guide Money Guides

Online comparison tools

The press

Online, by phone or in person

Professional advice

Compare ‘like for like’

Check early repayment charges

Be vigilant!

Compare your choices

There is a huge range of different ways to borrow available to you. Hopefully this guide helps you gain some knowledge and understanding of which way is best for you. You should then compare your choices. Here are some useful ways to do this.

Online comparison tools Online comparison tools are easy to use. By simply inputting a few basic details about your personal circumstance and preferences, you will be provided with a list of suitable deals to consider. They usually allow you to compare loans by various criteria including: loan type, minimum and maximum loan amounts, rate type, monthly repayments and total payable. For credit cards you can usually compare such criteria as APR, balance transfer rate, new purchase rate and rewards.

Think of the time you can save accessing these details all in the one place. They often also allow you to click through to the lender’s website and actually begin the application process.

The pressCheck out the best buys in newspapers and specialist magazines. You should also keep an eye out for news stories about new loans or credit card offers that are available.

Online, by phone or in personAlternatively you can visit your preferred lenders’ websites, give their loan departments a call or if they have a local branch, pop in and speak with them.

Professional adviceIf you feel a bit overwhelmed, then speak to a professional. Do check that whoever you choose is regulated by the Financial Conduct Authority (FCA) or the Prudential Regulation Authority (PRA) – this means they are obliged to meet certain standards and treat you fairly. Be sure you understand their level of independence (whether or not they are committed to certain lenders), the extent of the service they will provide and if and what they will be charging you. Ask at the outset!

Useful comparison websites • Money Supermarket

www.moneysupermarket.com/loans

www.moneysupermarket.com/credit-cards

• Compare the Market

www.comparethemarket.com/loans

www.comparethemarket.com/credit-cards

• uSwitchwww.uswitch.com

• Which?www.which.co.uk/money/credit-cards-and-loans

SECTION14

LIKELIKE

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 14: page 2 of 2

Borrowing Guide Money Guides

Online comparison tools

The press

Online, by phone or in person

Professional advice

Compare ‘like for like’

Check early repayment charges

Be vigilant!

Compare your choices

Before deciding remember to...

Compare ‘like for like’• The same type of borrowing

• The same loan amount

• Over the same term

• Rate type

• APR

• Number of repayments

• Total payable

• Special features

• Fees and charges

• Small print – check out the terms and conditions.

Be aware that some firms that advertise loans are really only brokers who arrange loans for you with other providers. Usually these brokers charge fees, which may still be payable even if the provider they pass you to subsequently rejects your application.

You should always check the terms and conditions along with any charges that a broker may make very carefully.

Check early repayment chargesIf you think there may be a possibility that you could repay your loan early, before the end of its term, then you should check which loans will make a charge and which won’t. While many lenders do not make this charge and others make minimal charges, it’s something to factor in before you decide which loan is right for you.

Be vigilant!Be extremely cautious of companies you have never heard of, particularly when looking for a loan, and always do some research to make sure they are reputable. Before proceeding check they are registered with the Financial Conduct Authority or the Prudential Regulation Authority or licensed with the Office of Fair Trading. Be wary when applying online or if you receive emails offering financial products. Do not give out personal details unless you are convinced they are genuine.

One common scam is when an upfront fee to cover insurance for the loan is requested, before the loan can be released. Then the victim does not hear from the company again.

Be aware that identity fraud is on the increase, with Experian revealing that last year 20 in every 10,000 applications for credit or other financial products were found to be fraudulent. So protect your identity.

SECTION14

LIKELIKE

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 15: page 1 of 3

Borrowing Guide Money Guides

Getting started

Paperwork that may be needed

Credit checks

Improve your rating

Decision time

Applications and credit checks

Once you have decided on the type of borrowing best for you and chosen your preferred lender, it’s time to make your application. You’re usually able to do this online, over the phone, by post or in person at a branch of your lender.

Getting started• How much?: before you start, you’ll need to have

decided how much you will be borrowing.

• Be prepared: make sure you have everything to hand before you start (see over page). There is nothing more frustrating than having to go back and forth looking for details you could have found earlier.

• Be thorough: when completing any forms, fill out every single little box, no matter how trivial you may find it. Don’t leave anything blank, as this will avoid having to go back and redo your whole application again.

• Just ask: if you are stuck for answers and are not sure how to fill in the application, just ask your advisor or lender to help you. Application forms aren’t a test; they are there to help you get the right loan for you.

Most lenders will fill out the application form with you, so don’t worry you will not be on your own!

Fill everybox!

Have I got all the

info?

Ask if Ineed help!

How muchdo I need to

borrow?

SECTION15

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 15: page 2 of 3

Borrowing Guide Money Guides

Getting started

Paperwork that may be needed

Credit checks

Improve your rating

Decision time

Applications and credit checks

Paperwork that may be needed Proof of your...ID

• Passport and your National Insurance number

• Driving licence or other document with your photograph

Address

• Proof of your address/es for last three years such as utility or council tax bills

Employment

• Employer and contact number

Financial situation

• Your income i.e. payslips, P45, accounts if self-employed

• Your outgoings – debts, loans, etc., and your last few bank statements

• Detailed breakdown of assets such as other accounts, properties, investments, etc.

If you are applying for a mortgage or secured loan you will also need to know:

• The current value of your property

• The amount still outstanding on your mortgage

• The total amount of any other debts

• The agreement of any joint owner and adult occupier

Credit checks and credit ratingsWhen you apply for a loan or credit card, lenders will want to make sure that your credit rating is adequate. They use the information you give in your application, but they also rely heavily on data supplied by credit reference agencies. Your ‘credit worthiness’ is based on your history of borrowing and repayment in the UK. If you have no debts, have lived overseas, or your borrowing is in your partner’s sole name, then you may have no track record and receive a low score.

Their assessment also takes into account any other financial assets or liabilities you might have. From all this information, a ‘credit score’ is generated. If you have a low rating you will be considered a greater risk and may be offered a less favourable interest rate or be offered a lower credit limit on a credit card. Your application may even be rejected.

If you are turned down, you can ask the lender if your credit rating was the reason. In addition you have the right to check your rating and can do this for a small fee online, via the credit reference agencies, Experian, Equifax and CallCredit. (See Appendix b – Useful contacts).

Online loan applicationCheck out an example of an online loan application

SECTION15

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 15: page 3 of 3

Borrowing Guide Money Guides

Getting started

Paperwork that may be needed

Credit checks

Improve your rating

Decision time

Applications and credit checks

Improve your rating There are some ways that you can improve your credit rating, such as:

• Check the information on your credit report is accurate and flag up any errors – the information may not be up to date or your circumstances may have changed, for example if you’ve separated or divorced, your partner’s rating may be linked to yours if you had any joint financial dealings.

• Check you are registered to vote at your current address.

• Pay bills on time and try not to miss any payments.

• Stay within the limits of any current credit arrangements you have.

• Close any accounts and cancel any contracts you no longer use.

• If you have any savings use these to pay off any existing debts.

• Build up a credit profile – you want lenders to see you have a good track record of managing credit wisely. A good way of doing this is by getting a credit card and using it wisely. (See Section 10)

• Beware of fraud – protect your ID

• Do not make too many applications for credit at the same time.

Decision timeThe time it takes for a decision on your application may vary greatly. For a secured loan it usually takes longer and may be several weeks before you receive the money. For an unsecured loan you may be able to get an immediate decision. This is particularly so if you choose a lender you already have an account with.

Often an ‘agreement in principle’ decision (provisional approval) is given until a full assessment of your application is complete. Remember it is in your interest for lenders to be responsible and carry out the necessary checks so that you are both happy with the agreement.

You will usually be asked to sign a loan agreement, although sometimes this can be done online if this is how you originally applied. You should always check carefully and make sure you fully understand all of the terms and conditions. If you have applied online or by phone, the loan agreement will be sent to you for signing, (or you will have to download and sign the forms,) and you may need to supply documents to confirm your identity, your income or other details. You are usually entitled to a ‘cooling off’ period.

TIPYour credit rating is about you – not your address! So don’t worry that the financial circumstances of any previous occupiers may have a bearing on you!

SECTION15

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 16: page 1 of 1

Borrowing Guide Money Guides

Payment Protection Insurance (PPI)

Card protection

Insurances

After choosing the right loan for you, you may want to consider taking out insurance to help you if something unexpected were to happen.

Payment Protection Insurance (PPI)Many lenders offer insurance cover to help you to keep up repayments if, for example, you are unable to work because of a serious illness, injury or if you are made redundant. This will provide you with the confidence that you will be able to meet your repayments, should your personal circumstances change. The range of benefits offered and their terms can vary, so you should always very carefully check to ensure you understand what is covered. You should also very carefully consider whether you actually need this insurance or not; you may have this cover elsewhere or may be self-employed, unemployed, retired or have a pre-existing illness, in which case it may not offer relevant cover for you or may not pay out in your circumstances.

This type of protection can be offered by your lender or it can be bought independently. You should not feel you have to take out PPI it’s entirely up to you whether you feel you need it and can afford it.

Card protectionYou may want to consider taking out cover against your cards being stolen. A card protection policy enables you to cancel all your credit, debit and store cards and order replacements immediately, with just one phone call. You usually also get help to access cash in an emergency. Some policies offer cover for all the members of your household. Check first that you do not have this cover already, perhaps as a benefit of a bank account or as part of your home insurance cover.

I’ve lost mywallet, can I

cancel ALL mycards please.

SECTION16

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 17: page 1 of 1

Borrowing Guide Money Guides

Getting behind with repayments

How to complain

If things go wrong

It’s good practice to know what to do if you get behind in your payments. This section will help you to maintain a good credit rating whilst getting back on track.

Getting behind with repaymentsOne of the worst things you can do if you find yourself in difficulty with repayments is to bury your head and try to ignore things, thinking they’ll go away – they won’t, they will only get worse! The moment you realise you cannot make a loan payment, act!

Go to your lender first. They may be able to:

• Help you manage your account to avoid/ minimise fees and charges

• Consider giving you a payment holiday

• Accept reduced payments from you in the short term

• Rearrange your loan over a longer period to reduce payments

If you are unable to reach a payment agreement with your lender, or you have multiple debts with a number of lenders, then you should get help. Many national advice agencies and charities provide free debt counselling services. Do not put your head in the sand and hope the debt will go away. It won’t. The longer you delay dealing with it, the bigger and more difficult it will become.

Remember that missed payments will show up on your credit report and may have an adverse effect on your credit rating, making getting credit in the future more difficult.

If you’re missing payments it’s probably a sign that your finances are in trouble, so take it as a warning and reassess your situation now!

Handling Debt Guide

How to complainIt’s always best to give your lender or credit card provider the opportunity to put the matter right before lodging a complaint. Use the contact details on your paperwork. Tell your lender what you feel is wrong, and give the lender the opportunity to explain. Remember, to keep a record of who you speak to and when, also what was said and any action agreed.

If you feel you’re making no progress then put in a formal complaint. Make sure that you head up your email or letter as a ‘Complaint’ as financial providers are obliged to deal with any complaints within eight weeks. If there is still no resolution, you should use the Financial Ombudsman Service (FOS), which aims to settle disputes as fairly and as quickly as possible.

SECTION17

OVERDUEMORTGAGE

Provided by

Available on www.NationwideEducation.co.uk

Independent of Nationwide products and services

SECTION 18: page 1 of 1

Borrowing Guide Money Guides

Top tips

Top ten tips

Top tips when borrowing • There are lots of ways to borrow money. Do your

own research to see which option is best for you, according to what you want the money for.

• Don’t borrow more than you need to – carefully work out how much you actually need.

• When borrowing money, your goal should be to remain in control; work out a budget and make sure that you can repay the money comfortably and not overstretch yourself.

• Calculate the real cost of any borrowing – the total over the whole term.

• Only deal with lenders who are properly regulated, and who are committed to helping you make financial decisions that best suit your circumstances.

• Be aware that the advertised rate is not necessarily the one you will be offered. It will depend on the ‘risk’ the lender feels you represent.

• Don’t sign anything until you have considered all your options and avoid lenders that charge exceptionally high APRs.

• If you think you may go overdrawn, it is always best to have a ‘planned’ overdraft to avoid unnecessary charges.

• Check your credit rating and consider ways to improve it, if needed.

• Stay committed to repaying the money you have borrowed.

BORROWED

TO PAY

£

£

SECTION18

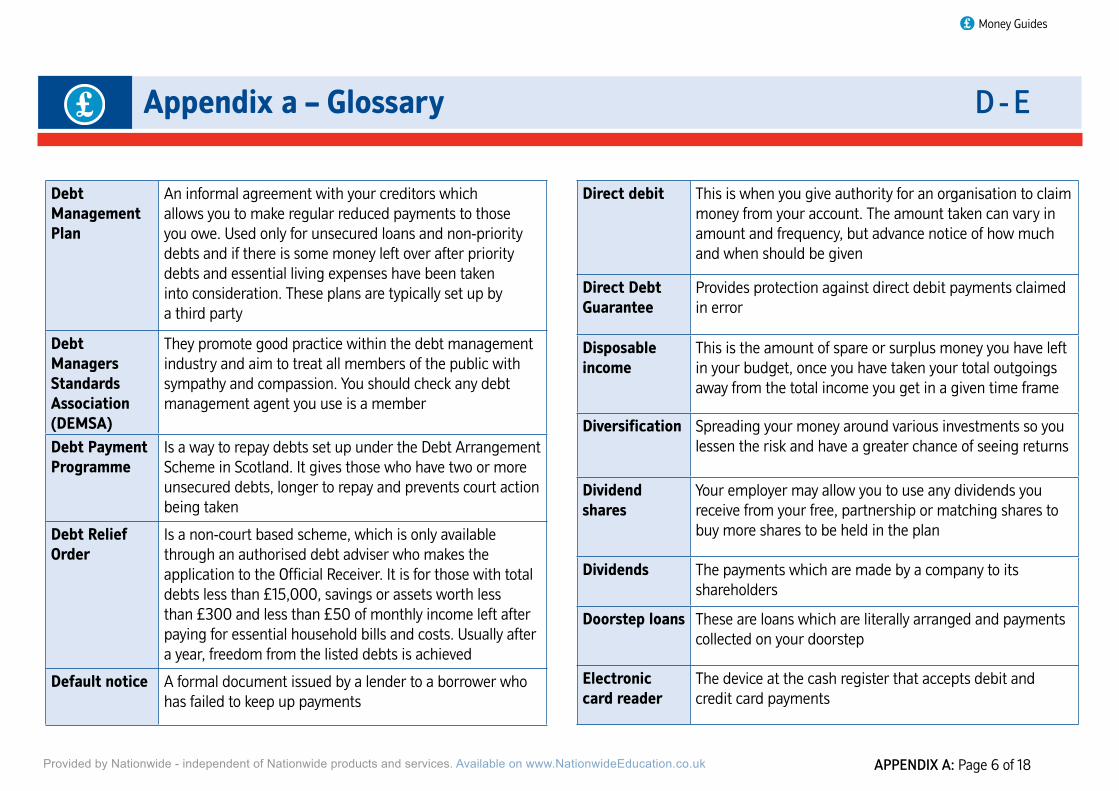

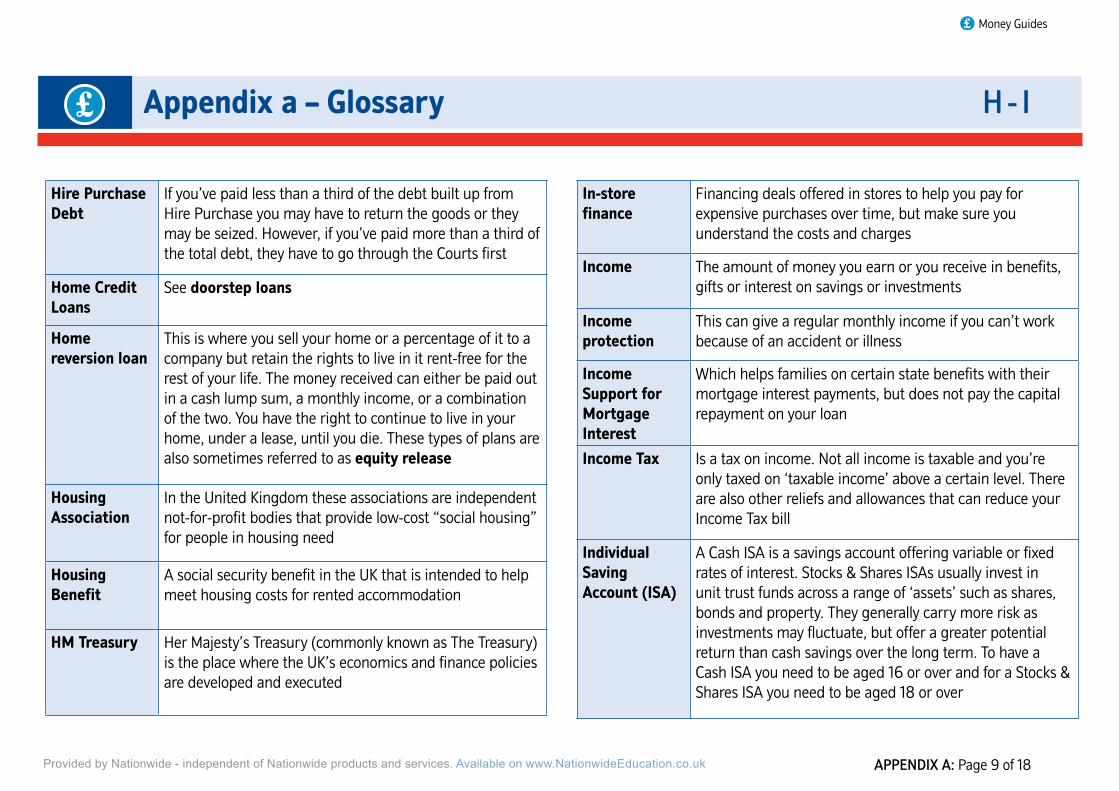

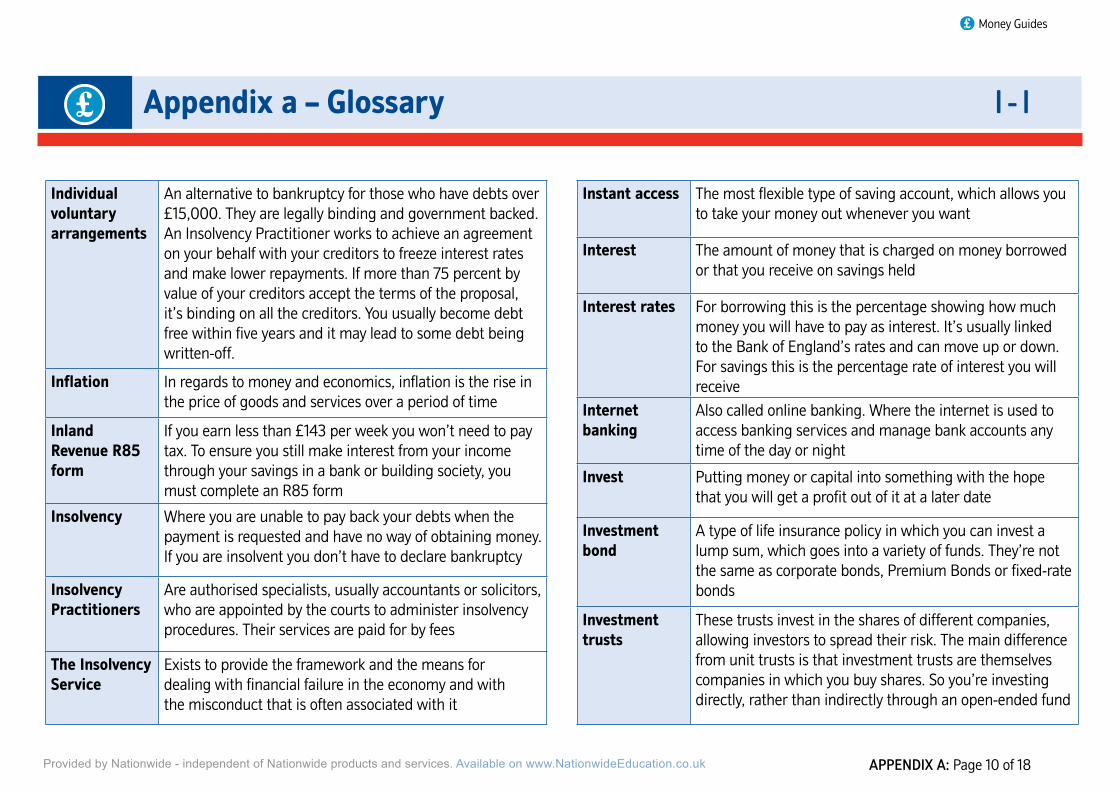

Appendix a – Glossary

Provided by Nationwide - independent of Nationwide products and services. Available on www.NationwideEducation.co.uk APPENDIX A: Page 1 of 18

Money Guides

A - A

Accident, Sickness, and Unemployment insurance (ASU)

An insurance policy that pays out in the event that you are unable to work due to recovering from an accident; prolonged illness; or due to involuntary unemployment. It may be linked to your mortgage or can been taken separately

Administration Order

Is a way to pay off your debts in monthly instalments and can help stop calls from your creditors. It is delegated by the county court for total non-priority debts amounting to less than £5,000. The court then pays the creditors on a pro-rata basis

Allowance A set amount of money or capital which you are allowed within a specified time frame

Annual Percentage Rate (APR)

This is the interest rate you would pay over a year period and helps you to compare the ‘cost’ of borrowing between lenders. It takes into account interest to be paid, length of the repayment term and any other charges

Annuity Is a financial product bought from an insurance company with your pension or a lump sum which then provides a regular income, payable for life after retirement. The payout depends on the scheme in which the money is invested

Anti-virus and Anti-spyware

This software searches your hard drive for any known or potentially malicious programmes or viruses that can cause damage to your computer

Apparent insolvency

This happens when you don’t have enough funds to repay your debts and the creditors are making legal threats

Arranged overdraft

(These can also be called authorised overdrafts.) This is when you and your current account provider have arranged for you to have an overdraft facility on your account. In many cases overdrafts are offered as a benefit of a specific account, some even offering interest free overdrafts

Asset Any item of economic value owned by an individual or corporation, especially that which could be converted to cash

Assured shorthold tenancy agreement

Is a type of tenancy which offers the landlord a guaranteed right to repossess his property at the end of the term

Attachment of earnings

Is when your employer may have to make deductions from your earnings and pay them to the court

Automated phone answering system

An automated answering system that uses prompts to direct callers to the correct department or extension

Authorised overdraft

See arranged overdraft

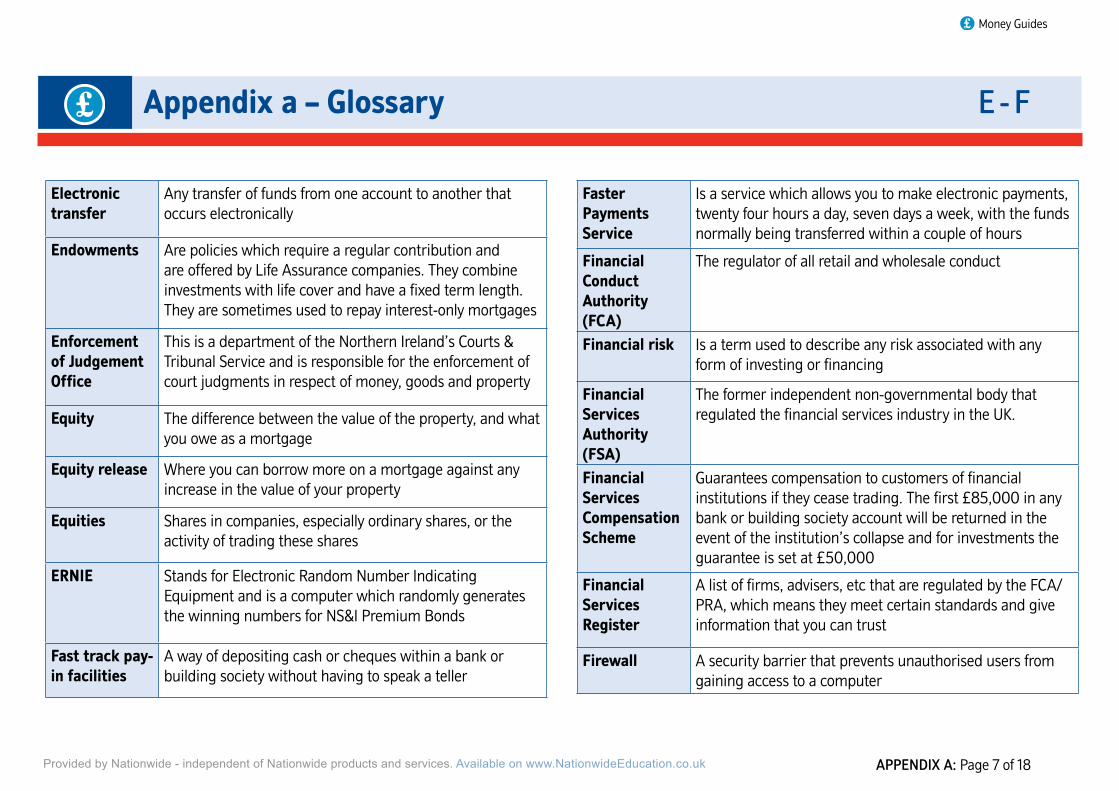

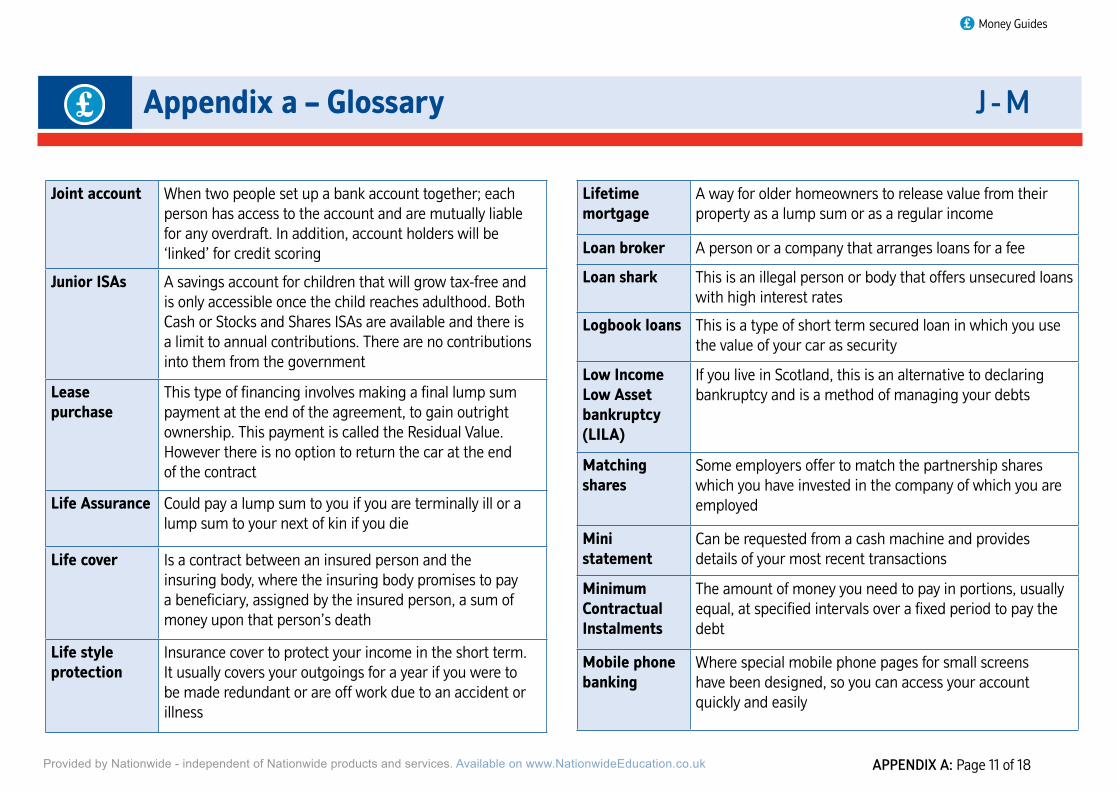

Appendix a – Glossary

Provided by Nationwide - independent of Nationwide products and services. Available on www.NationwideEducation.co.uk APPENDIX A: Page 2 of 18

Money Guides

B - B

Bankruptcy A legal procedure which begins with a petition to the courts when outstanding debts cannot be repaid. It results in any assets, other than basic household goods, being sold off and any bank accounts frozen. Normally after a year you are freed from the bankruptcy

Bankruptcy discharge

When you are freed from your bankruptcy after a year and released from your debts

Bare trust This is a trust in its simplest form and is sometimes called a ‘simple trust’ if you set up a bare trust the assets (such as money, land or buildings) which you have set aside will go directly to the people or organisations that you have initially agreed

Basic bank account

Is one that allows you to receive money and pay bills. A cash card is normally provided, but no overdraft facility, debit card or cheque book is provided

Bonds A debt investment in which you loan money to an entity (corporate or governmental) that borrows the funds for a defined period of time at a fixed interest rate. Bonds are used by companies and also governments to finance a variety of projects and activities

Borrowing Criteria

What a lender uses to decide if they are willing to lend you money, may include passing their own credit scoring system and having an adequate salary

Bacs Direct Credit

Is a simple, secure and reliable way for organisations to make payments direct into your bank or building society account. Funds paid this way can be used by you on the day they arrive into your account

Bailiffs Are officers of the court who work to collect debt. There are several types of bailiffs who act differently according to the type of debt being collected

Bank An organisation that offers a range of services such as current and savings accounts, loans and mortgages

Bank of England

Is the central bank for the United Kingdom and is responsible for setting interest rates, issuing bank notes and maintaining a stable financial economy

Bank statement

Is a record of your bank account transactions for a given time period

Banker’s drafts

Are cheques drawn directly on the account of a bank rather than the account of a customer. They are considered a safer option for some transactions as they are unlikely to be returned unpaid due to lack of funds

Banking online See internet banking

Appendix a – Glossary

Provided by Nationwide - independent of Nationwide products and services. Available on www.NationwideEducation.co.uk APPENDIX A: Page 3 of 18

Money Guides

B - C

Cash point machine

A computerised device in to which you insert your cash card and key in your Personal Identification Number (PIN) to get cash out or get account information

Cashback Where you can ask for additional money when you are using your debit card to pay for purchases at certain retailers. The total amount of your purchases and the cashback are taken from your account right away

CHAPS (Clearing House Automated Payments System)

Is a secure, same-day guaranteed method of sending high-value payments, for which a charge is usually made

Charging order

Is an order obtained from a court or judge by a creditor, by which they gain an interest in any property, land, stocks or funds you own, in order to recover the debt owned

Cheque Are written orders from account holders instructing their banks or building societies to pay a specific sum of money to another person, company or organisation

Cheque book The book containing detachable blank cheques; which is issued by a bank or building society to account holders

Cleared When a deposit into your account has been processed and is available to you

Budget sheet A record showing all income and outgoings, prepared to work out how you are doing financially

Budgeting Loans

A social fund loan for those on a low income and getting certain benefits, up to £1,500 can be borrowed to help spread the cost of certain important expenses over a longer period, for example, furniture, household goods, clothing, and travel expenses

Building society

A financial company that offers similar services to a bank (e.g. letting you save or borrow money) but is owned by its members (customers)

Buy-to-let A property that people buy as an investment, which they then let to tenants

Call centre A central office where customer service assistants help callers with their telephone banking

Capital The amount of money you have actually borrowed, still owe on your loan (not including interest or other charges)

Card Protection Policy

Insurance cover against your cards being stolen. It usually enables you to cancel all your credit, debit and store cards and order replacements immediately, with just one phone call. You usually also get help to access cash in an emergency

Cash card Any card that you can insert into an ATM or other cash dispenser

Appendix a – Glossary

Provided by Nationwide - independent of Nationwide products and services. Available on www.NationwideEducation.co.uk APPENDIX A: Page 4 of 18

Money Guides

C - C

Corporate bonds

These bonds are issued by companies as a way of raising money to invest in their business. They are bought and sold on the stock market and their price can fluctuate

County Court Judgement (known as a decree in Scotland)

Is where a court makes a decision over an outstanding debt and orders that payment must be made, usually in monthly instalments

Credit agreement

A formal agreement between someone borrowing money and the bank or building society lending the money

Credit card A plastic card which you use to buy products and services on credit, which is usually issued by a bank or building society. The issuer of the card will collect payment later or you can choose to defer payment and interest will be charged

Credit rating This is decided on information in your credit report, that lenders use to assess the credit risk you pose. Your ability to repay debts is ‘rated’

Credit reference agency

They evaluate your ‘credit worthiness’ based on your history of borrowing and repayment; they also take into account any other financial assets or liabilities you might have. From all this information, a ‘credit score’ is generated. The main credit reference agencies are Experian, Equifax and CallCredit

Commission The money a salesman makes for services or products which they have supplied

Community Development Finance Institutions (CDFIs)

Organisations that help people who struggle to get finance from banks, building societies or loan companies. They aim to help deprived communities by offering loans and support at an affordable rate

Composition order

Is when a court agrees that you only pay part of the total debt you owe that is subject to an Administration Order

Contactless payment

This typically takes the form of a chip in a credit card, which is simply placed on or very near a reader device to initiate a transaction. You can use them to make low value payments without having to use a chip & PIN machine

Continuous Payment Authority

May also be called a ‘recurring transaction’. When you give your credit or debit card details to a company and authorise them to take regular payments from your account. Unlike Direct Debits, they do not offer the same guarantee if the amount or date of the payment changes

Cooling off period

An agreed length of time during which you can decide not to buy something, or continue with something, you have previously agreed to

Appendix a – Glossary

Provided by Nationwide - independent of Nationwide products and services. Available on www.NationwideEducation.co.uk APPENDIX A: Page 5 of 18

Money Guides

C - D

Debt Money which is owed to a bank, building society or other lending organisation

Debt Arrangement Scheme

A Scottish government backed scheme designed to allow the repayment of multiple unsecured debts over an extended period of time at an affordable amount each month. An approved money adviser works to set up a Debt Payment Programme (DPP) with the creditors. You are protected from court action during the scheme

Debt Collection Agency

Is a business that collects unpaid, overdue debts for other businesses

Debt consolidation

This is where debts are combined together so instead of paying lots of different creditors, only one single payment is made that covers all debts

Debt consolidation loan

Is a new loan that is taken out to repay several existing debts, usually with a more competitive interest rate, so that only one single payment is required

Debt management companies

Will, for a fee, negotiate with your creditors to agree the payments you make to them. They may even be able to get your creditors to freeze the interest and charges on your account or offer you a lower interest rate

Credit report The report provided by the credit reference agency detailing their assessment of your credit risk

Credit score This is a number, calculated based on information in your credit report, that lenders use to assess the credit risk you pose

Credit union Are mutual financial organisations, which are owned and run by their members for their members

Credit worthiness

Your eligibility to borrow money based on the credit risk you pose

Creditors Are those that you owe money to

Crisis loans A social fund loan provided by the government, which provides £1,500 to help in an emergency or following a disaster for those who qualify

Critical illness cover

A form of protection insurance that can be taken to provide funds if you were to ever suffer from a critical illness

Current account

The most common type of bank account usually with the benefit of an overdraft facility, a debit card and a cheque book. You can also set up Direct Debits and Standing Orders to be paid out

Debit card Are used to withdraw cash, buy goods or pay for services and the amount is taken from your bank account straight away

Appendix a – Glossary

Provided by Nationwide - independent of Nationwide products and services. Available on www.NationwideEducation.co.uk APPENDIX A: Page 6 of 18

Money Guides

D - E

Direct debit This is when you give authority for an organisation to claim money from your account. The amount taken can vary in amount and frequency, but advance notice of how much and when should be given

Direct Debt Guarantee

Provides protection against direct debit payments claimed in error

Disposable income

This is the amount of spare or surplus money you have left in your budget, once you have taken your total outgoings away from the total income you get in a given time frame

Diversification Spreading your money around various investments so you lessen the risk and have a greater chance of seeing returns

Dividend shares

Your employer may allow you to use any dividends you receive from your free, partnership or matching shares to buy more shares to be held in the plan

Dividends The payments which are made by a company to its shareholders

Doorstep loans These are loans which are literally arranged and payments collected on your doorstep

Electronic card reader

The device at the cash register that accepts debit and credit card payments

Debt Management Plan

An informal agreement with your creditors which allows you to make regular reduced payments to those you owe. Used only for unsecured loans and non-priority debts and if there is some money left over after priority debts and essential living expenses have been taken into consideration. These plans are typically set up by a third party

Debt Managers Standards Association (DEMSA)

They promote good practice within the debt management industry and aim to treat all members of the public with sympathy and compassion. You should check any debt management agent you use is a member

Debt Payment Programme

Is a way to repay debts set up under the Debt Arrangement Scheme in Scotland. It gives those who have two or more unsecured debts, longer to repay and prevents court action being taken

Debt Relief Order

Is a non-court based scheme, which is only available through an authorised debt adviser who makes the application to the Official Receiver. It is for those with total debts less than £15,000, savings or assets worth less than £300 and less than £50 of monthly income left after paying for essential household bills and costs. Usually after a year, freedom from the listed debts is achieved

Default notice A formal document issued by a lender to a borrower who has failed to keep up payments

Appendix a – Glossary

Provided by Nationwide - independent of Nationwide products and services. Available on www.NationwideEducation.co.uk APPENDIX A: Page 7 of 18

Money Guides

E - F

Faster Payments Service

Is a service which allows you to make electronic payments, twenty four hours a day, seven days a week, with the funds normally being transferred within a couple of hours

Financial Conduct Authority (FCA)

The regulator of all retail and wholesale conduct

Financial risk Is a term used to describe any risk associated with any form of investing or financing

Financial Services Authority (FSA)

The former independent non-governmental body that regulated the financial services industry in the UK.

Financial Services Compensation Scheme

Guarantees compensation to customers of financial institutions if they cease trading. The first £85,000 in any bank or building society account will be returned in the event of the institution’s collapse and for investments the guarantee is set at £50,000

Financial Services Register

A list of firms, advisers, etc that are regulated by the FCA/PRA, which means they meet certain standards and give information that you can trust

Firewall A security barrier that prevents unauthorised users from gaining access to a computer

Electronic transfer

Any transfer of funds from one account to another that occurs electronically

Endowments Are policies which require a regular contribution and are offered by Life Assurance companies. They combine investments with life cover and have a fixed term length. They are sometimes used to repay interest-only mortgages

Enforcement of Judgement Office

This is a department of the Northern Ireland’s Courts & Tribunal Service and is responsible for the enforcement of court judgments in respect of money, goods and property

Equity The difference between the value of the property, and what you owe as a mortgage

Equity release Where you can borrow more on a mortgage against any increase in the value of your property

Equities Shares in companies, especially ordinary shares, or the activity of trading these shares

ERNIE Stands for Electronic Random Number Indicating Equipment and is a computer which randomly generates the winning numbers for NS&I Premium Bonds

Fast track pay-in facilities

A way of depositing cash or cheques within a bank or building society without having to speak a teller

Appendix a – Glossary

Provided by Nationwide - independent of Nationwide products and services. Available on www.NationwideEducation.co.uk APPENDIX A: Page 8 of 18

Money Guides

F - H

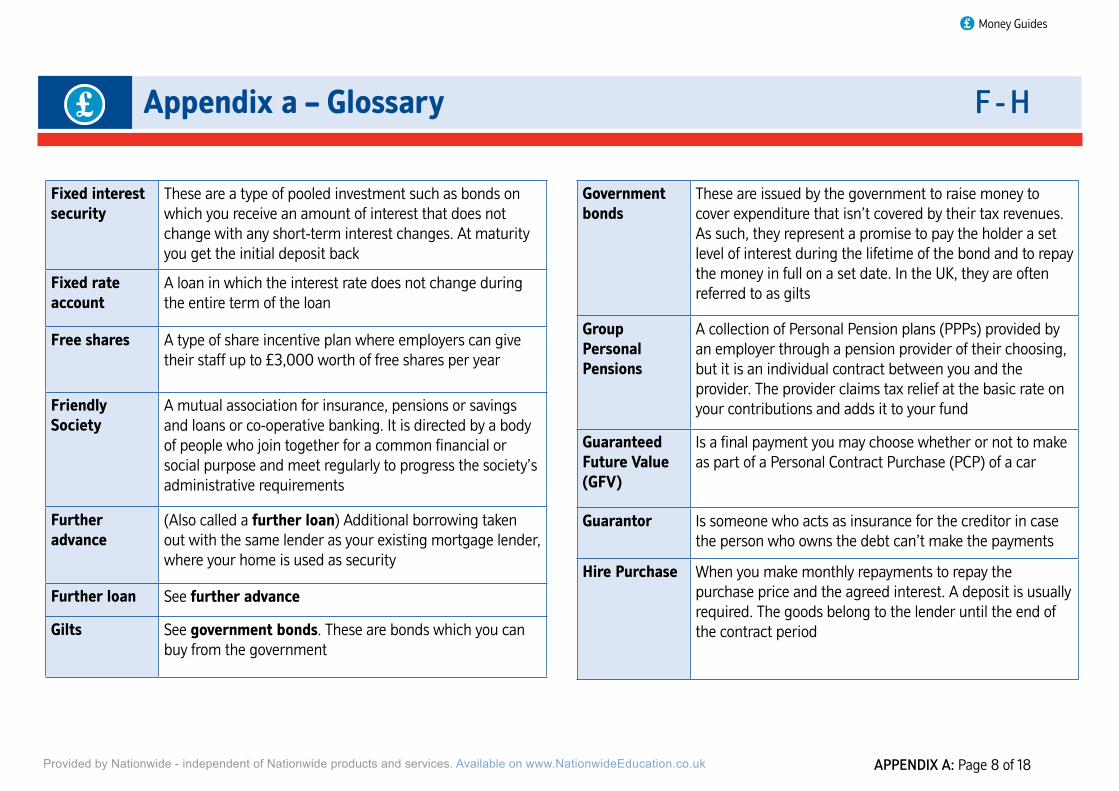

Government bonds