Embed Size (px)

Citation preview

Monetary economicsY. AksoyEC3115

2015

Undergraduate study in Economics, Management, Finance and the Social Sciences

This is an extract from a subject guide for an undergraduate course offered as part of the University of London International Programmes in Economics, Management, Finance and the Social Sciences. Materials for these programmes are developed by academics at the London School of Economics and Political Science (LSE).

For more information, see: www.londoninternational.ac.uk

This guide was prepared for the University of London International Programmes by:

Dr Y. Aksoy, Reader in Economics, Department of Economics, Mathematics and Statistics, Birkbeck, University of London.

Some of the material in this subject guide has been adapted from the previous edition, written by:

Ryan Love, formerly of the London School of Economics and Political Science.

This is one of a series of subject guides published by the University. We regret that due to pressure of work the authors are unable to enter into any correspondence relating to, or arising from, the guide. If you have any comments on this subject guide, favourable or unfavourable, please use the form at the back of this guide.

University of London International ProgrammesPublications OfficeStewart House32 Russell Square

London WC1B 5DN

www.londoninternational.ac.uk

Published by: University of London

© University of London 2015

The University of London asserts copyright over all material in this subject guide except where otherwise indicated. All rights reserved. No part of this work may be reproduced in any form, or by any means, without permission in writing from the publisher. We make every effort to respect copyright. If you think we have inadvertently used your copyright material, please let us know.

Contents

Contents

1 Introduction to the subject guide 7

1.1 The structure of the guide . . . . . . . . . . . . . . . . . . . . . . . . . . 7

1.2 The subject guide and the syllabus . . . . . . . . . . . . . . . . . . . . . 7

1.3 Specifics of the syllabus . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

1.4 Aims . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

1.5 Learning outcomes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

1.6 Subject chapters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

1.7 Reading advice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

1.8 Essential reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

1.9 Further reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

1.10 Online study resources . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

1.11 How to use this subject guide . . . . . . . . . . . . . . . . . . . . . . . . 14

1.12 The examination . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

1.13 Use of mathematics and statistics . . . . . . . . . . . . . . . . . . . . . . 16

2 The nature of money 17

2.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

2.2 Aims . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

2.3 Learning outcomes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

2.4 Reading advice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

2.5 Essential reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

2.6 Further reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

2.7 What is money? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

2.8 The functions of money . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

2.9 Why do we have money? . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

2.10 Types of money . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

2.11 Properties of money . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

2.12 A reminder of your learning outcomes . . . . . . . . . . . . . . . . . . . . 26

2.13 Sample examination questions . . . . . . . . . . . . . . . . . . . . . . . . 27

2.14 Feedback to Sample examination questions . . . . . . . . . . . . . . . . . 27

1

Contents

3 The demand for money 29

3.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

3.2 Aims . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

3.3 Learning outcomes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

3.4 Reading advice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

3.5 Essential reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

3.6 Further reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

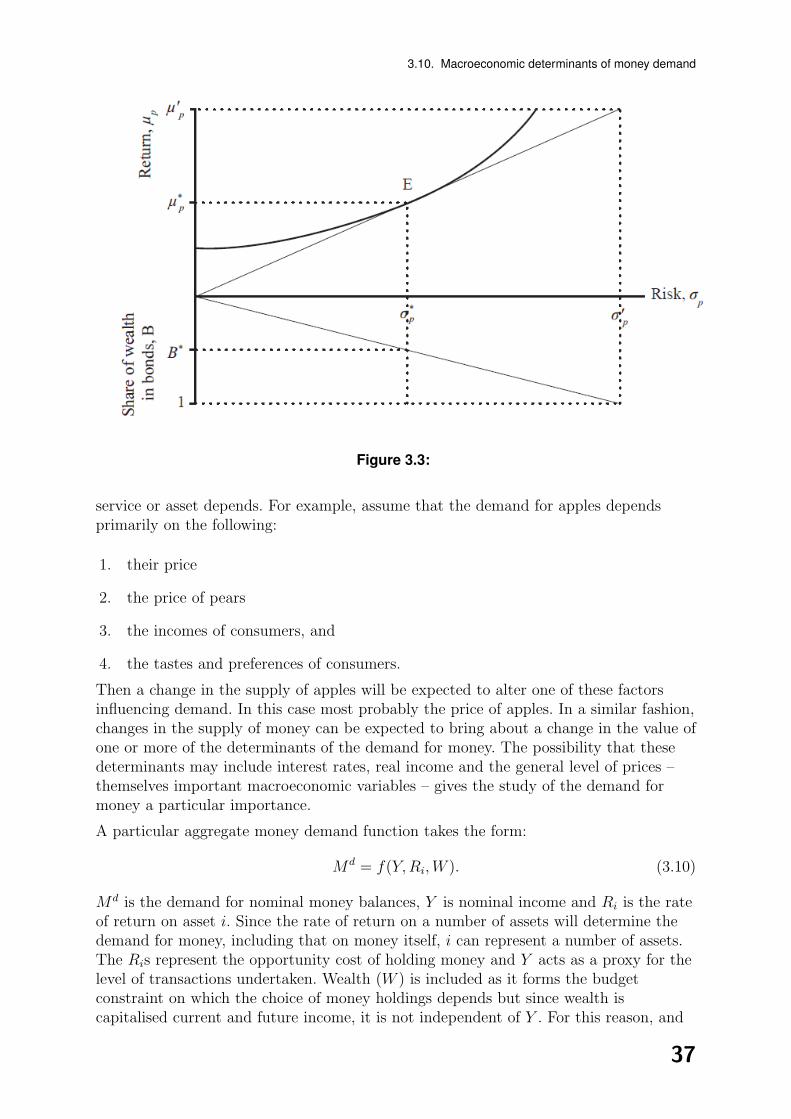

3.7 Microeconomic determinants of the demand for money . . . . . . . . . . 31

3.8 Baumol–Tobin transactions demand for money . . . . . . . . . . . . . . . 33

3.9 Tobin’s model of portfolio selection . . . . . . . . . . . . . . . . . . . . . 35

3.10 Macroeconomic determinants of money demand . . . . . . . . . . . . . . 36

3.11 The stability of the money demand function . . . . . . . . . . . . . . . . 38

3.12 Reasons for the breakdown of the money demand functions . . . . . . . . 39

3.13 A reminder of your learning outcomes . . . . . . . . . . . . . . . . . . . . 39

3.14 Sample examination questions . . . . . . . . . . . . . . . . . . . . . . . . 40

3.15 Feedback to Activity 3.1 . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

3.16 Feedback to Sample examination questions . . . . . . . . . . . . . . . . . 41

4 The supply of money 43

4.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

4.2 Aims . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

4.3 Learning outcomes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

4.4 Reading advice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

4.5 Essential reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

4.6 Further reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

4.7 Financial intermediaries . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

4.8 The money multiplier and base money . . . . . . . . . . . . . . . . . . . 46

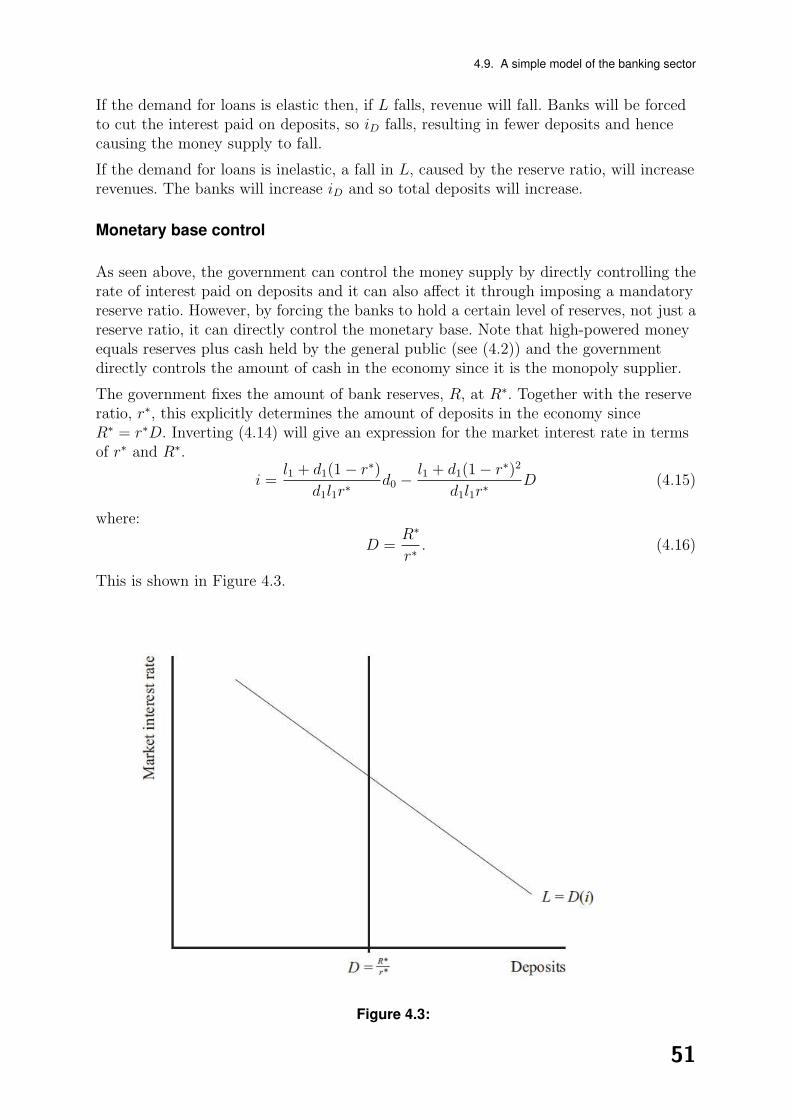

4.9 A simple model of the banking sector . . . . . . . . . . . . . . . . . . . . 47

4.10 A reminder of your learning outcomes . . . . . . . . . . . . . . . . . . . . 52

4.11 Sample examination questions . . . . . . . . . . . . . . . . . . . . . . . . 53

4.12 Feedback to Activity 4.5 . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

4.13 Feedback to Sample examination questions . . . . . . . . . . . . . . . . . 55

5 Classical theory 57

5.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

5.2 Aims . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

2

Contents

5.3 Learning outcomes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

5.4 Reading advice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

5.5 Essential reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

5.6 Further reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

5.7 The quantity theory of money . . . . . . . . . . . . . . . . . . . . . . . . 58

5.8 A simple general equilibrium framework . . . . . . . . . . . . . . . . . . 63

5.9 A reminder of your learning outcomes . . . . . . . . . . . . . . . . . . . . 65

5.10 Sample examination questions . . . . . . . . . . . . . . . . . . . . . . . . 65

5.11 Feedback to Sample examination questions . . . . . . . . . . . . . . . . . 66

6 Stylised facts 69

6.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

6.2 Aims . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

6.3 Learning outcomes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

6.4 Reading advice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

6.5 Essential reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

6.6 Further reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

6.7 Trends and business cycles . . . . . . . . . . . . . . . . . . . . . . . . . . 71

6.8 Moments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

6.9 Cross country business cycle evidence . . . . . . . . . . . . . . . . . . . . 78

6.10 Key macroeconomic relationships . . . . . . . . . . . . . . . . . . . . . . 79

6.10.1 Relationship between monetary aggregates and inflation . . . . . 79

6.11 Relationship between monetary instruments and macroeconomy . . . . . 80

6.12 Price level stickiness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82

6.13 A reminder of your learning outcomes . . . . . . . . . . . . . . . . . . . . 82

6.14 Sample examination questions . . . . . . . . . . . . . . . . . . . . . . . . 83

6.15 Feedback to Sample examination questions . . . . . . . . . . . . . . . . . 83

7 Money, inflation and welfare 85

7.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

7.2 Aims . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

7.3 Learning outcomes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

7.4 Reading advice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

7.5 Essential reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

7.6 Further reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

7.7 Inflation as taxation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

3

Contents

7.8 A reminder of your learning outcomes . . . . . . . . . . . . . . . . . . . . 96

7.9 Sample examination questions . . . . . . . . . . . . . . . . . . . . . . . . 97

7.10 Feedback to Activity 7.5 . . . . . . . . . . . . . . . . . . . . . . . . . . . 98

7.11 Feedback to Sample examination questions . . . . . . . . . . . . . . . . . 99

8 Classical models and monetary policy 101

8.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

8.2 Aims . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

8.3 Learning outcomes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

8.4 Reading advice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102

8.5 Essential reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102

8.6 Further reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102

8.7 The classical model revisited . . . . . . . . . . . . . . . . . . . . . . . . . 103

8.8 The effect of monetary policy . . . . . . . . . . . . . . . . . . . . . . . . 103

8.9 Real business cycle theory . . . . . . . . . . . . . . . . . . . . . . . . . . 106

8.10 Business cycle facts and RBC theory . . . . . . . . . . . . . . . . . . . . 106

8.11 Classical models with real effects of money . . . . . . . . . . . . . . . . . 107

8.12 A reminder of your learning outcomes . . . . . . . . . . . . . . . . . . . . 109

8.13 Sample examination questions . . . . . . . . . . . . . . . . . . . . . . . . 109

8.14 Feedback to Sample examination questions . . . . . . . . . . . . . . . . . 110

8.15 Appendix to Chapter 8: a ‘simple’ RBC model . . . . . . . . . . . . . . . 111

9 Keynesian models with money supply as a policy instrument 119

9.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 119

9.2 Aims . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 119

9.3 Learning outcomes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 119

9.4 Reading advice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 120

9.5 Essential reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 120

9.6 Further reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 120

9.7 Keynesian aggregate supply function . . . . . . . . . . . . . . . . . . . . 121

9.8 Predictable and unpredictable components of the money supply . . . . . 130

9.9 A reminder of your learning outcomes . . . . . . . . . . . . . . . . . . . . 133

9.10 Sample examination questions . . . . . . . . . . . . . . . . . . . . . . . . 133

9.11 Feedback to Sample examination questions . . . . . . . . . . . . . . . . . 134

10 New Keynesian models of monetary policy 137

10.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 137

4

Contents

10.2 Aims . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 137

10.3 Learning outcomes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 137

10.4 Reading advice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 138

10.5 Essential reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 138

10.6 Further reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 138

10.7 IS-PC-MR model of new Keynesian economics . . . . . . . . . . . . . . . 139

10.8 Analysing demand shocks . . . . . . . . . . . . . . . . . . . . . . . . . . 141

10.9 Analysing supply shocks . . . . . . . . . . . . . . . . . . . . . . . . . . . 143

10.10 Financial accelerator models . . . . . . . . . . . . . . . . . . . . . . . . 145

10.11 Simple monetary policy rules . . . . . . . . . . . . . . . . . . . . . . . . 147

10.12 A reminder of your learning outcomes . . . . . . . . . . . . . . . . . . . 149

10.13 Sample examination questions . . . . . . . . . . . . . . . . . . . . . . . 150

10.14 Feedback to Sample examination questions . . . . . . . . . . . . . . . . 150

11 Time inconsistency and inflation bias 151

11.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 151

11.2 Aims . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 151

11.3 Learning outcomes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 151

11.4 Reading advice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152

11.5 Essential reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152

11.6 Further reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152

11.7 Time inconsistency and inflation bias . . . . . . . . . . . . . . . . . . . . 153

11.8 Inflation aversion, steepness of the Phillips curve and interest rates . . . 155

11.9 Ways inflation bias can be reduced . . . . . . . . . . . . . . . . . . . . . 156

11.9.1 Delegation of monetary policy to a conservative central bank: centralbank independence . . . . . . . . . . . . . . . . . . . . . . . . . . 156

11.9.2 Inflation contract for the central bank . . . . . . . . . . . . . . . . 156

11.9.3 Reputation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 157

11.10 A reminder of your learning outcomes . . . . . . . . . . . . . . . . . . . 157

11.11 Sample examination questions . . . . . . . . . . . . . . . . . . . . . . . 158

11.12 Feedback to Sample examination questions . . . . . . . . . . . . . . . . 158

12 Monetary policy and data/parameter uncertainties 161

12.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 161

12.2 Aims . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 162

12.3 Learning outcomes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 162

12.4 Reading advice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 162

5

Contents

12.5 Essential reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 162

12.6 Further reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 162

12.7 Data uncertainty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 163

12.8 Parameter (or multiplicative) uncertainty . . . . . . . . . . . . . . . . . . 165

12.8.1 The New Keynesian model and parameter uncertainty . . . . . . 167

12.8.2 Graphical exposition . . . . . . . . . . . . . . . . . . . . . . . . . 170

12.9 Interest rate smoothing . . . . . . . . . . . . . . . . . . . . . . . . . . . . 171

12.10 A reminder of your learning outcomes . . . . . . . . . . . . . . . . . . . 172

12.11 Sample examination questions . . . . . . . . . . . . . . . . . . . . . . . 172

12.12 Feedback to Sample examination questions . . . . . . . . . . . . . . . . 173

13 The term structure of interest rates 175

13.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 175

13.2 Aims . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 175

13.3 Learning outcomes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 175

13.4 Reading advice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 176

13.5 Essential reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 176

13.6 Further reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 176

13.7 The yield curve . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 177

13.8 Why is the yield curve of importance to policy-makers? . . . . . . . . . . 177

13.9 Bond prices and the rate of return . . . . . . . . . . . . . . . . . . . . . . 178

13.10 Empirical regularities of the term structure . . . . . . . . . . . . . . . . 179

13.11 The expectations hypothesis . . . . . . . . . . . . . . . . . . . . . . . . 179

13.12 The segmentation hypothesis . . . . . . . . . . . . . . . . . . . . . . . . 180

13.13 Preferred habitat theory . . . . . . . . . . . . . . . . . . . . . . . . . . 181

13.14 A reminder of your learning outcomes . . . . . . . . . . . . . . . . . . . 182

13.15 Sample examination questions . . . . . . . . . . . . . . . . . . . . . . . 182

13.16 Feedback to Sample examination questions . . . . . . . . . . . . . . . . 183

A Sample examination paper 185

B Examiners’ commentary to Sample examination paper 189

6

Chapter 1

Introduction to the subject guide

1.1 The structure of the guide

The subject guide broadly mirrors the syllabus, which is split into three sections.

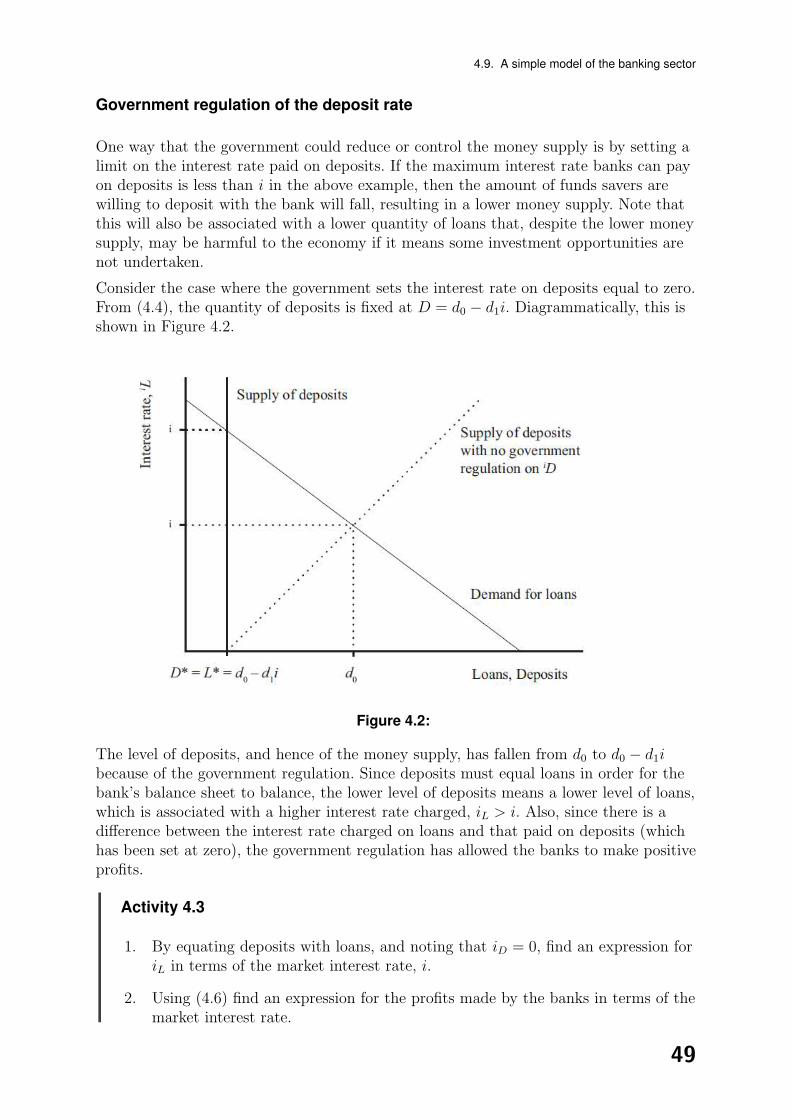

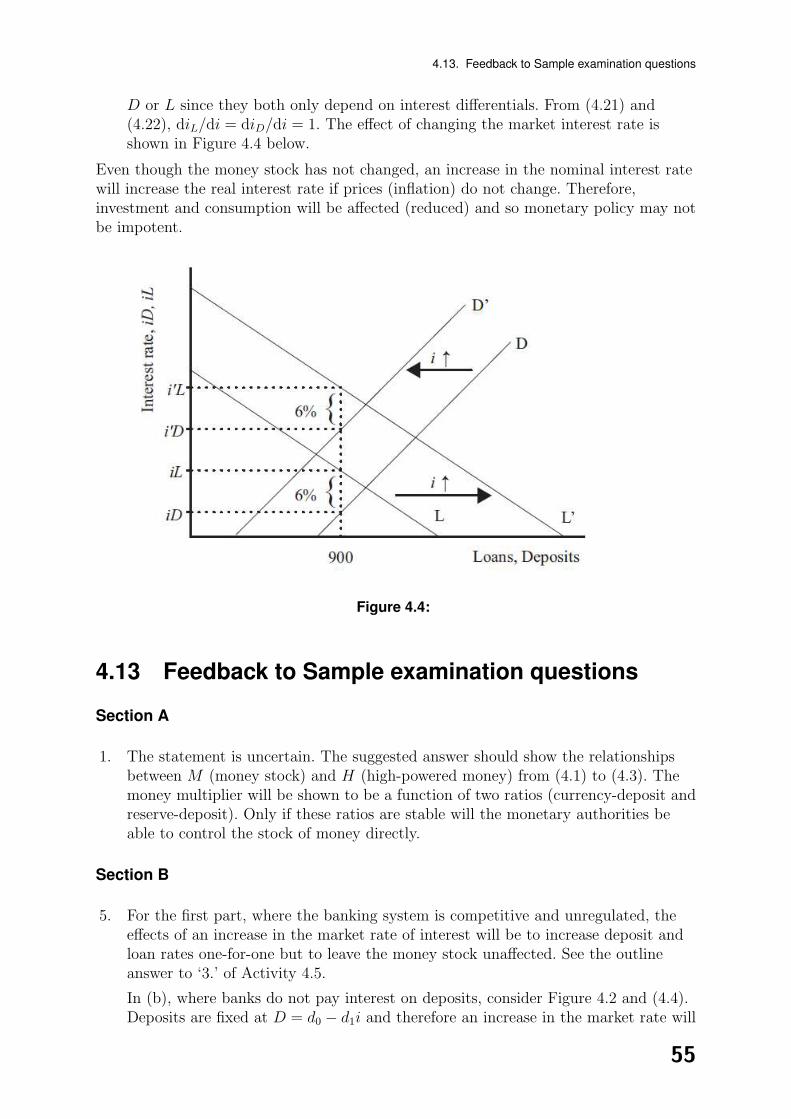

The first section of the guide (Chapters 2–5) introduces the concept of money;what it is, why we use it and how it is created. The role of banks and the bankingsector will be analysed in this section only, leaving the rest of the guide to focus onpolicy issues.

The second section (Chapters 6–10) examines monetary policy in a closed economy,considering a number of models that allow real effects of monetary policy, rangingfrom new-Classical to new-Keynesian. Specific models will be introduced andsolved, allowing you to see exactly how these models work and what differentiatesone from another.

The third section of the guide considers important issues in the design of monetarypolicymaking. Topics include i) time inconsistency in monetary policy design, ii)monetary policy in an uncertain environment such as data and parameteruncertainties that monetary policy makers face and how policy makers canalleviate problems associated with these uncertainties and iii) term structure ofinterest rates.

Please see the syllabus at the end of this ‘Introduction’.

1.2 The subject guide and the syllabus

The aim of the guide is to enable you to interpret fully the published syllabus for theEC3115 Monetary economics course. It does so by identifying what you areexpected to know within each area of the syllabus, and suggesting the reading that willbe most helpful in acquiring an understanding of the material concerned. It cannot beemphasised strongly enough that the guide is not a substitute for reading textbooks andother references.

1.3 Specifics of the syllabus

Important: the information given in the following section is based on the syllabus atthe time this guide was written. However, you should refer to the Programme handbookfor the latest version of the syllabus and any additional information.

7

1. Introduction to the subject guide

Section 1: Introduction to money and monetary economics

The nature of money:

What constitutes money. Why people hold money; introduction to cash in advance(CIA) and money in the utility (MIU) functions.

Money demand and supply:

Microeconomic determinants of the demand for money and macroeconomic moneydemand functions. Financial intermediaries, banks and money creation.

The Classical school, neutrality of money and the quantity theory:

The Classical dichotomy, Walras’ and Say’s laws, introduction to money in ageneral equilibrium setting.

Section 2: Monetary policy

Stylised facts and monetary policy:

Trends and business cycles. Means, volatility, cyclicality and persistence inmacroeconomic time series. Money and macroeconomic variables in the short andlong-run. Empirical evidence for Phillips curves.

The welfare effects of inflation and monetary policy:

Neutrality and superneutrality of money, welfare costs, seigniorage and theinflation tax.

The Classical model, flexible price economies and monetary policy:

Rational expectations, representative agents and real business cycle theory. MIU,CIA, Lucas supply functions and the effects of monetary policy.

The Keynesian approach to monetary policy – nominal rigidities:

Multi-period pricing and the persistence of monetary policy shocks. The Lucascritique.

The new Keynesian approach to monetary policy – nominal rigidities:

New Keynesian Phillips curve, IS Curve, Taylor rules, financial accelerator models.

Section 3: Topics in monetary economics

Time inconsistency in monetary policy:

Inflation bias, the central bank independence. Monetary policy rules: interest ratetargeting and monetary targeting. (rules versus discretion).

8

1.4. Aims

Uncertainties in the monetary policy design:

News versus noise in data revisions. Brainard conservatism, certainty equivalence,interest rate smoothing.

Term structure of interest rates:

Explanation of the yield curve: expectations hypothesis and the segmentationhypothesis.

1.4 Aims

The aims of the course are to:

develop understanding of the theories that relate to the existence of money,explaining why it is demanded by individuals and used in the trading process

develop an understanding of the monetary transmission mechanism, wherebydecisions made by the monetary authorities concerning money supplies or interestrates can have real effects on the economy

develop a number of macroeconomic models through which monetary policy can beevaluated. Such models will include Classical, Keynesian and new Keynesianschools of thought and will consider why monetary policy matters and whenmonetary policy decisions may be impotent

develop understanding of the uncertainties policy-makers face and how policymakers may deal with these.

1.5 Learning outcomes

At the end of this course and having completed the essential reading and activitiesstudents should be able to:

explain and discuss why people hold money and why it is used in the tradingprocess

solve macroeconomic models and assess the role and efficacy of monetary policy forvarious types of models in both the Classical and Keynesian set-ups

describe and explain the main channels of the monetary transmission mechanism,through which monetary policy can have real effects on the economy

discuss the merits and disadvantages of different monetary policies used by CentralBanks

introduce the concepts of data and parameter uncertainties and discuss policyunder uncertainty.

9

1. Introduction to the subject guide

1.6 Subject chapters

A different chapter is devoted to each major section of the syllabus, and the chapterorder follows very closely, though not identically, the order of the topics as they appearin the syllabus. This order will not concur with that in any one of the recommendedtextbooks and the fact that the order varies between the textbooks themselves reflectsthe view that there is no obvious sequence of topics because of the interrelationshipsbetween them. It is most important to appreciate that the ‘topics’ in the syllabus arenot self-contained and mutually exclusive, and neither therefore are the chapters of thisguide. Instead there is considerable overlap between many of the ‘topics’ and betweenthe chapters. For example, the chapter on ‘the demand for money’ explains the linkbetween the level of real money balances an economy wishes to hold and the nominalinterest rate. This is essential for understanding how monetary policy influences the realeconomy in later chapters. Similarly, an understanding of how, and to what extent,changes in the supply of money affect the macroeconomy will require an understandingof the subject matter of several chapters.

Consequently, you must expect the examination to include questions that require anunderstanding of several different parts of this subject, in other words you cannot ‘pickand choose’ what to study from the guide.

Each chapter begins with a checklist of learning outcomes; what you should know afterhaving completed the chapter and done the essential reading and activities. Thenfollows some reading advice and a list of the most helpful books and articles for thatparticular chapter. Following the main text, each chapter concludes with a list ofSample examination questions. Occasionally these questions will overlap with materialcovered in one or more of the other chapters.

1.7 Reading advice

Unfortunately no single textbook adequately covers the whole of the EC3115Monetary economics syllabus. Indeed, using several different textbooks may still notprove adequate. Sometimes it will be necessary to consult a ‘specialist’ book, or perhapsan article in a journal in order to get a good grasp of the subject matter concerned.Consequently, the reading suggested at the beginning of each chapter might include notonly references to one or more textbooks, but also references for wider reading. In somechapters, it might be useful to study the recommended reading before you move on tothe material presented in the subject guide. Where this is the case, the introductoryparagraph will let you know what you should read before you work through the chapter.For each chapter, the reading list is split into two sections: Essential reading andFurther reading. As the name suggests, Essential reading is required reading in orderfor you to fully understand the concepts introduced in the particular chapter. Again, itmust be stressed that this subject guide is not a substitute for reading textbooks. Theitems listed under Further reading will give you greater insight into the topics coveredin the chapter and will certainly help you understand any areas with which you still feeluncomfortable.

10

1.8. Essential reading

1.8 Essential reading

For Sections 1 and 2, you are encouraged to buy:

either

Lewis, M.K. and P.D. Mizen Monetary Economics. (Oxford; New York: OxfordUniversity Press, 2000) [ISBN 9780198290629]

or

Carlin,W. and D. Soskice Macroeconomics: Imperfections, Institutions and Policies.(Oxford: Oxford University Press, 2006).

For Sections 1 and 2 the Carlin and Soskice and Lewis and Mizen books are veryhelpful. Carlin and Soskice book provides an excellent account of new Keynesian modelsin particular, while Lewis and Mizen is easier to read. For Section 3, there is no singlebook that is adequately covering issues addressed in the guide. We indicate relevantliterature in academic journals.

Throughout this guide, there are references in both the Essential and Further readingsections to articles in The New Palgrave Dictionary of Money and Finance. Thisincludes essays and articles on most aspects of money, contributed by authors who areinternationally recognised authorities on the subject matter of their particular entry. Ineach chapter you will be directed to the relevant entries in this book in either theEssential or Further reading categories. Other books are particularly useful on specifictopics (such as money demand). Where such books (and indeed articles as well) arerecommended, page references or chapter numbers are given.

Detailed reading references in this subject guide refer to the editions of the settextbooks listed above. New editions of one or more of these textbooks may have beenpublished by the time you study this course. You can use a more recent edition of anyof the books; use the detailed chapter and section headings and the index to identifyrelevant readings. Also check the virtual learning environment (VLE) regularly forupdated guidance on readings.

The Essential reading for all chapters in this subject guide is taken from the twotextbooks above but also includes the following:

Books

Cagan, P. ‘The monetary dynamics of hyperinflation’, in Friedman, M. (ed.)Studies in the Quantity Theory of Money. (Chicago: University of Chicago Press,2000) [ISBN 9780226264042].

Gali, J. Monetary Policy, Inflation, and the Business Cycle: An Introduction to theNew Keynesian Framework. (Princeton: Princeton University Press, 2008) [ISBN:9781400829347].

Goodhart, C.A.E. Money, Information and Uncertainty. (London: Macmillan,1989) second edition [ISBN 9780262570756].

11

1. Introduction to the subject guide

Gordon, R.J., ‘A century of evidence on wage and price stickiness in the US, theUK and Japan’, in Tobin, J. (ed.) Macroeconomics, Prices and Quantities. (Oxford:Blackwell, 1983) [ISBN 9780815784852].

Jones, C.I. Macroeconomics. (W. W. Norton Company, 2013) third edition [ISBN9780393923902].

Laidler, D.E.W. The Demand for Money: Theories, Evidence and Problems. (NewYork: Harper Collins, 1997) fourth edition [ISBN 9780065010985].

Lucas, R.E. ‘Econometric policy evaluation: a critique’, in Brunner, K. and A.H.Meltzer (eds) The Phillips Curve and Labor Markets. (Amsterdam; Oxford:North-Holland, 1976) [ISBN 9780444110077].

Mankiw, N.G. Macroeconomics. (New York: Worth Publishers, 2012) eighth edition[ISBN 9781429240024].

McCallum, B. Monetary Economics. (New York: Macmillan; London: CollierMacmillan, 1989) [ISBN 9780023784712].

Mishkin, F.S. The Economics of Money, Banking and Financial Markets. (Boston,Mass.; London: Prentice Hall, 2012) tenth edition [ISBN 9780132770248].

Newman, P., M. Milgate and J. Eatwell (eds) The New Palgrave Dictionary ofMoney and Finance. (London: Macmillan, 1994) [ISBN 9780333527221].

Williamson, S. Macroeconomics. (New Jersey: Prentice Hall, 2013) fifth edition[ISBN 978-0132991339].

Journal articles

Aksoy, Y. and T. Piskorski, ‘US domestic money, inflation and output’, Journal ofMonetary Economics, 53, 2006, pp.183–197.

Bernanke, B. , Gertler, M., and S. Gilchrist (1999) ‘The financial accelerator in aquantitative business cycle framework’, Chapter 21, in Handbook ofMacroeconomics, Volume 1, Edited by J.B. Taylor and M. Woodford, Elsevier.Brainard, W., ‘Uncertainty and effectiveness of policy’, American Economic Review(papers and proceedings), 57 (2), 1967, pp.411–425.

Carlin, W. and D. Soskice ‘The 3-equation New Keynesian model – A graphicalexposition’, BE Journals in Macroeconomics: Contributions, 5(1) 2005, pp.1–38.

Clarida, R., Gal, J. and Gertler, M., ‘The science of monetary policy: a newKeynesian perspective’, Journal of Economic Literature, 37(4), 1999, pp.1661–1707.

Kydland, F.E. and E.C. Prescott, ‘Rules rather than discretion: the inconsistencyof optimal plans’, Journal of Political Economy 85(3), 1977, pp.473–492.

Long, J. and C. Plosser, ‘Real business cycles’, Journal of Political Economy 91(1),1983, pp.39–69.

12

1.9. Further reading

Lucas, R., ‘Some international evidence on output-inflation trade-offs’, AmericanEconomic Review, 63, 1973, pp.326–334.

Plosser, C., ‘Understanding real business cycles’, Journal of Economic Perspectives3(3) 1989, pp.51–77.

Taylor, J.B., ‘An historical analysis of monetary policy rules’, NBER workingpaper, w6768, (1998).

1.9 Further reading

Please note that as long as you read the Essential reading you are then free to readaround the subject area in any text, paper or online resource. You will need to supportyour learning by reading as widely as possible and by thinking about how theseprinciples apply in the real world. To help you read extensively, you have free access tothe VLE and University of London Online Library (see below).

1.10 Online study resources

In addition to the subject guide and the Essential reading, it is crucial that you takeadvantage of the study resources that are available online for this course, including theVLE and the Online Library.

You can access the VLE, the Online Library and your University of London emailaccount via the Student Portal at: http://my.londoninternational.ac.uk

You should have received your login details for the Student Portal with your officialoffer, which was emailed to the address that you gave on your application form. Youhave probably already logged in to the Student Portal in order to register! As soon asyou registered, you will automatically have been granted access to the VLE, OnlineLibrary and your fully functional University of London email account.

If you forget your login details, please click on the ‘Forgotten your password’ link on thelogin page.

The VLE

The VLE, which complements this subject guide, has been designed to enhance yourlearning experience, providing additional support and a sense of community. It forms animportant part of your study experience with the University of London and you shouldaccess it regularly.

The VLE provides a range of resources for EMFSS courses:

Self-testing activities: Doing these allows you to test your own understanding ofsubject material.

Electronic study materials: The printed materials that you receive from theUniversity of London are available to download, including updated reading listsand references.

13

1. Introduction to the subject guide

Past examination papers and Examiners’ commentaries : These provide advice onhow each examination question might best be answered.

A student discussion forum: This is an open space for you to discuss interests andexperiences, seek support from your peers, work collaboratively to solve problemsand discuss subject material.

Videos: There are recorded academic introductions to the subject, interviews anddebates and, for some courses, audio-visual tutorials and conclusions.

Recorded lectures: For some courses, where appropriate, the sessions from previousyears’ Study Weekends have been recorded and made available.

Study skills: Expert advice on preparing for examinations and developing yourdigital literacy skills.

Feedback forms.

Some of these resources are available for certain courses only, but we are expanding ourprovision all the time and you should check the VLE regularly for updates.

Making use of the Online Library

The Online Library contains a huge array of journal articles and other resources to helpyou read widely and extensively.

To access the majority of resources via the Online Library you will either need to useyour University of London Student Portal login details, or you will be required toregister and use an Athens login: http://tinyurl.com/ollathens

The easiest way to locate relevant content and journal articles in the Online Library isto use the Summon search engine.

If you are having trouble finding an article listed in a reading list, try removing anypunctuation from the title, such as single quotation marks, question marks and colons.

For further advice, please see the online help pages:www.external.shl.lon.ac.uk/summon/about.php

1.11 How to use this subject guide

At the start of most chapters you are advised on how to approach the material andwhich readings to consult as well as when to consult them. In general though, for eachtopic in the syllabus you should read through the whole of the chapter in the guide soas to get an overview of the material to be covered. Then try to read as much of thesuggested reading as you can. This is important as you will often find that things youhave difficulty understanding in one book are made perfectly clear in another. Athorough understanding of the material covered in recommended passages is essential ifyou are to maximise the benefits you derive from this subject.

Use the checklist and Sample questions as a way of testing your understanding of thematerial covered. The textbooks will also include exercises and questions, and youwould be well advised to attempt as many of these as you can. The real test of whether

14

1.12. The examination

you understand something is not whether you have followed the explanation, butwhether you can apply that understanding to answering questions.

A number of chapters include a substantial activity. This is a longer question, whichyou should be able to work through after having consulted the relevant readings.Although an outline of the solution is included at the end of the chapter, you arestrongly encouraged to use this only to check your answers or to get hints as to how tostart your answer.

You should allocate approximately two weeks to study each chapter. Chapters 1 and 2contain relatively little mathematical material, therefore can easily be dealt with in oneweek.

1.12 The examination

Important: the information and advice given here are based on the examinationstructure used at the time this guide was written. Please note that subject guides maybe used for several years. Because of this we strongly advise you to always check boththe current Regulations for relevant information about the examination, and the VLEwhere you should be advised of any forthcoming changes. You should also carefullycheck the rubric/instructions on the paper you actually sit and follow those instructions.

Examination questions will require short essays, demonstrating understanding of thesubject material and critical ability.

The three-hour unseen examination consists of two sections:

Section A (40 marks) contains eight statements, which are true, false or uncertain.You will be asked to answer all of these, also explaining your answer in a shortparagraph. A typical ‘true, false or uncertain’ question will appear at the end ofeach chapter and in the first half of the guide a suggested answer is also included,in order to give you an idea as to how detailed the explanation should be.

Section B is worth 60 marks. You must answer three out of five questions. Thesewill typically involve discussing and solving some of the models covered in theguide. These may also involve interpretation of data in the light of specifiedmacro-monetary theories.

To give you an idea as to how the examination will be structured, an example isincluded in the Appendix. In addition to the Sample examination paper, the questionsat the end of each chapter will also give you an insight into the examination. The ‘true,false or uncertain’ question in each chapter is representative of the questions you will beasked in Section A and the remaining questions are similar to those found in Section B.The longer activities, found in a number of chapters, are exactly the type of questionyou should expect to find in Section B of the examination.

To give you an idea as to how you should structure your answers in the examination,feedback to some of the Sample examination questions is given at the end of eachchapter. However, as is the case for the feedback to the longer activities, you shouldonly use this to check your answers, or to get hints as to how to start.

15

1. Introduction to the subject guide

Remember, it is important to check the VLE for:

up-to-date information on examination and assessment arrangements for this course

where available, past examination papers and Examiners’ commentaries for thecourse which give advice on how each question might best be answered.

1.13 Use of mathematics and statistics

Economics is becoming an increasingly technical subject and, as such, in this subjectyou will be required to employ mathematics in order to solve simple optimisationproblems. However, what is most important is the intuition behind the models, whichcan often be demonstrated easily using diagrams. Any mathematics that is used in thissubject is limited to simple calculus (differentiation), algebra and basic statistics (thedefinition and calculation of means and variances). The most technically demandingchapters are from Chapter 7 to Chapter 12 but in order to help you work through this,the mathematics is presented so as to allow you to see how the models are solved,step-by-step. Some of the passages in some of the recommended books and articles docontain more complicated or lengthy mathematics/statistics but almost invariably itsmeaning is clarified in the written text.

Model-based approach of the guide

This subject guide follows a more model-based approach to monetary economics thanthe previous guide. Each chapter introduces one or more models that, when solved, willshow you the linkages between monetary variables (money supply or interest rates, forexample) and other variables such as output. As such, for the examination you will beexpected to solve and work through mathematical models but these will be no morecomplicated than what is presented in this subject guide. However, what is just asimportant is that you demonstrate that you understand what is going on. To do this,you must explain your answer using words, and possibly also diagrams. Even though allyou need to know to succeed in your study of monetary economics is presented in theessential and further reading sections of each chapter, for those of you who require morehelp with this model-based approach, you can consult Walsh, C. Monetary Theory andPolicy (2010) third edition and Gali, J. Monetary Policy, Inflation and the BusinessCycle (2008). It should be stressed, however, that you should read the items in therecommended reading sections first, before you consider reading these moreadvanced/technical textbooks. Hopefully you will find your study of monetaryeconomics interesting and enjoyable.

Good luck.

Dr. Yunus Aksoy (Birkbeck, University of London)

16

Chapter 2

The nature of money

2.1 Introduction

Fiat money is indispensable in modern economic systems, although it has been part ofdaily life as far back as 9000 BC, when grain and cattle were used in Anatolia andMesopotamia for exchange purposes. While we take the usage of some form of money asgranted, we need to understand why it exists, its functions and properties. In particular,we need to solve the double coincidence of wants problem associated with barter and toresolve the lack of trust between the payer and the payee in a transaction.

2.2 Aims

The aim of the chapter is to introduce the main ingredients of a monetary economy. Wewill introduce money for exchange purposes of goods and services. We will describe itsfunctions, why money is useful in trade, its types and properties.

2.3 Learning outcomes

By the end of this chapter, and having completed the Essential reading and activities,you should be able to:

discuss the nature and shortcomings of a barter economy

list and describe the general functions performed by money

describe the Wicksell problem and demonstrate how indirect barter can lead to theemergence of a commodity money

describe the differences between transactions using credit cards and bank debitcards

list and describe what the different types of money are.

2.4 Reading advice

You will certainly find it easiest, and probably most useful, to read the appropriatesections on the nature of money in one or more of the basic textbooks before you move

17

2. The nature of money

on to the material in this chapter.1 All textbooks on money and banking will have asection covering the material here. However the best, although most difficult, is that ofGoodhart (1989a) Chapter 2 – see below under ‘Essential reading’. You may find ithelpful to read Goodhart (1989b) first – see below under ‘Further reading’.

2.5 Essential reading

Goodhart, C.A.E. Money, Information and Uncertainty. (London: Macmillan, 1989a)Chapter 2.

Lewis, M.K. and P.D. Mizen Monetary Economics. (Oxford; New York: OxfordUniversity Press, 2000) Chapters 1 and 2.

2.6 Further reading

Clower, R.W. ‘Introduction’ in Clower, R.W. (ed.) Monetary Theory: Selected readings.(Harmondsworth: Penguin, 1969).

Goodhart, C.A.E. ‘The Development of Monetary Theory’ in Llewellyn, D.T. (ed.)Reflections on Money. (Basingstoke: Macmillan, 1989b).

Harris, L. Monetary Theory. (New York; London: McGraw-Hill, 1985) Chapter 1.

Kiyotaki, N. and J.H. Moore ‘Evil is the Root of all Money’. Clarendon Lecture series,Lecture 1 (2001).

Kiyotaki, N. and R. Wright ‘Acceptability, Means of Payment, and Media of Exchange’,Federal Reserve Bank of Minneapolis Quarterly Review, Summer 1992. Also in Newman,P., M. Milgate and J. Eatwell (eds) The New Palgrave Dictionary of Money andFinance. (London: Macmillan, 1994).

McCallum, B. Monetary Economics. (New York; Macmillan; London: CollierMacmillan, 1989).

Newlyn, W.T. and R.P. Bootle Theory of Money. (Oxford: Clarendon Press, 1978)Chapter 1.

2.7 What is money?

Money is defined by its function rather than the form in which it takes. In this sense,money is defined as ‘anything which is in general use, and generally accepted, as ameans of payment.’ In the past, money has taken the form of corn, rice, cattle, shells,various precious metals and more recently, pieces of paper issued by governments. In allcases though, money was and is used as a means of payment in exchange. The payer ina transaction (he or she who is purchasing a good or service) hands over money to thevalue of the item bought and at this point the payee (the seller of the good or service)

1See for example, Harris, and Newlyn and Bootle.

18

2.8. The functions of money

accepts that the payment is complete. The payee neither holds any further claims onthe payer, nor on any third party who may have produced or issued the money.

In this chapter we will discuss and explain the important functions, properties anddifferent types of money. We will also explain why we use money and compare thealternative trading strategies, both with and without money.

2.8 The functions of money

Below, we will discuss the three main functions of money, although, arguably, someauthors will expand these into four.2

Money as a means of payment

As suggested above, the most important function of money is its use as a means ofpayment – money being used to pay for items purchased or to settle any debts. Arelated role of money is that as a medium of exchange, which Wicksell defined as anobject which is taken in exchange, not on its own account. . . not to be consumed by thereceiver or to be employed in technical production, but to be exchanged for somethingelse within a longer or shorter period of time.’3 In this sense, a means of payment canalso be a medium of exchange. A gold coin for example, used to buy a piece of land, willbe a means of payment (the seller of the land will not hold a claim on the payee whohas just handed over the gold) but it will also be a medium of exchange. The receiver ofthe gold coin will not use it for decorative purposes or to ‘make’ any other goods orservices, but will use it as a medium of exchange when he or she wishes to purchase agood or service some time in the future.

However, the converse is not necessarily true.4 That which may act as a medium ofexchange may not act simultaneously as a means of payment. For example, if I wish topay for a television set using a credit card, the seller may accept this as a medium ofexchange.

Although the television shop’s account may be credited effectively immediately, it maynot be a means of payment since I, the payer, still have a debt outstanding, namely thatto the credit card company. I have merely replaced a debt to the television shop with adebt to the credit card issuer. The purchase of the television set with the credit card isthen not a means of payment. For this reason we will not include credit cards, tradecredit between firms, or any other line of credit such as unused overdraft facilities, inour definition of money.

2The fourth function of money commonly quoted, is that of a standard for deferred payment. Thissimply means that if something is bought today although payment for it does not have to be made untilsome later date, then the amount due for deferred payment can be measured in terms of money.

3Wicksell, 1906, quoted by Kiyotaki and Wright, (1992).4For an excellent analysis of the differences between ‘means of payment’ and ‘medium of exchange’

see Goodhart (1989a) Chapter 2, Section 4.

19

2. The nature of money

Money as a unit of account

This function is also described as money acting as a measure of exchange value, moneyacting as a standard of value, or money as a numeraire. The essential point about thisfunction is that money is acting as a common denominator, in terms of which the valuein exchange of all goods and services can be expressed. Money is simply acting as a unitof measurement in the same way that metres measure length and kilograms measureweight. Money in this sense is being used to measure the value of goods, services andassets relative to other goods, services and assets. If it is convenient to trade allcommodities in exchange for a single commodity, so it is convenient to measure theprices of all commodities in terms of a single unit, rather than record the relative priceof every good in terms of every other good. If there is to be a single unit of account, it isagain clearly convenient (though not necessary) that the unit of account be the mediumof exchange, given that goods actually exchange against the medium of exchange.

A clear advantage of having a single unit of account is that it greatly reduces thenumber of exchange ratios between goods and services. With four goods (A, B, C andD), in order to facilitate exchange, exchange ratios of each good in terms of all theothers must be available (i.e. the six ratios A:B, A:C, A:D, B:C, B:D and C:D must beavailable). In fact with n goods, there are n(n− 1) = 2 relative prices. However, if weintroduce a fifth good, ‘money’ that acts as a unit of account then there only need to befour prices. With n goods and money being the n+ 1-th commodity acting as a unit ofaccount, we only need n prices. For example, with 1,000 goods and no unit of account,the economy needs 499,500 relative prices of one good in terms of another. Introducingmoney as a unit of account dramatically reduces this to only 1,000. Thus, having moneyas a unit of account can encourage trade by making it easier for individuals to knowhow much one good is worth in terms of another.

Money as a store of value

The exchange attributes of money, in particular that it is durable and can readily beused in the purchase of goods, also mean that people may wish to hold it as an asset,that is as part of their stock of wealth. In this sense, money serves as a store of value: itis permitting the separation in time of the act of sale from the act of purchase. Theexistence of a means of payment enables a person to sell a good without simultaneouslyhaving to buy another good in exchange. Receiving a means of payment in exchange forthe good sold allows the seller to hold on to it until such time as it is needed to beexchanged for the goods and services he or she requires.

Money is not unique as a store of value: any asset, such as equities, bonds, real estate,antiques and works of art can all act as stores of value. Money itself is sometimes a poorstore of value. This will occur when the relative price of money falls as a result of themoney prices of other goods and services rising, that is, during periods of inflation.

2.9 Why do we have money?

The use of money helps facilitate trade since in the absence of money, trade has toproceed through barter, that is the direct exchange of one good for another.

20

2.9. Why do we have money?

Barter

Barter tends to be associated with primitive economies in which individual householdsoperate in an isolated manner, and in particular have no sophisticated informationsystems concerning what is going on in the rest of the economy. For various reasonshouseholds may wish to consume a different bundle of goods from those they produce,so that there are gains from trade. The problem is how to achieve these potential gains,given that trade is a voluntary activity and can proceed only when it is to the benefit ofboth parties.

In barter, there has to be what is known as a ‘double coincidence of wants’. If I growcorn but want to consume apples, not only do I have to find someone willing to tradeapples but they must also want what I have to offer, namely corn. In other words fortrade to be mutually beneficial, it is necessary not only that trader A has what trader Bwants but also that trader B has something to offer in exchange which trader A wants.It is quite possible that no trade will occur, especially in cases where the goods desiredare so specialised that the probability of a double coincidence of wants occurring is solow that the cost of finding a match (for example in terms of advertising, transport, andso on) becomes very large and outweighs the increased utility derived from trade. Evenif the goods offered for trade are readily available, it may still be the case that no tradeoccurs. This is the subject of the Wicksell problem in which it is impossible to securegains from trade through bilateral exchange.

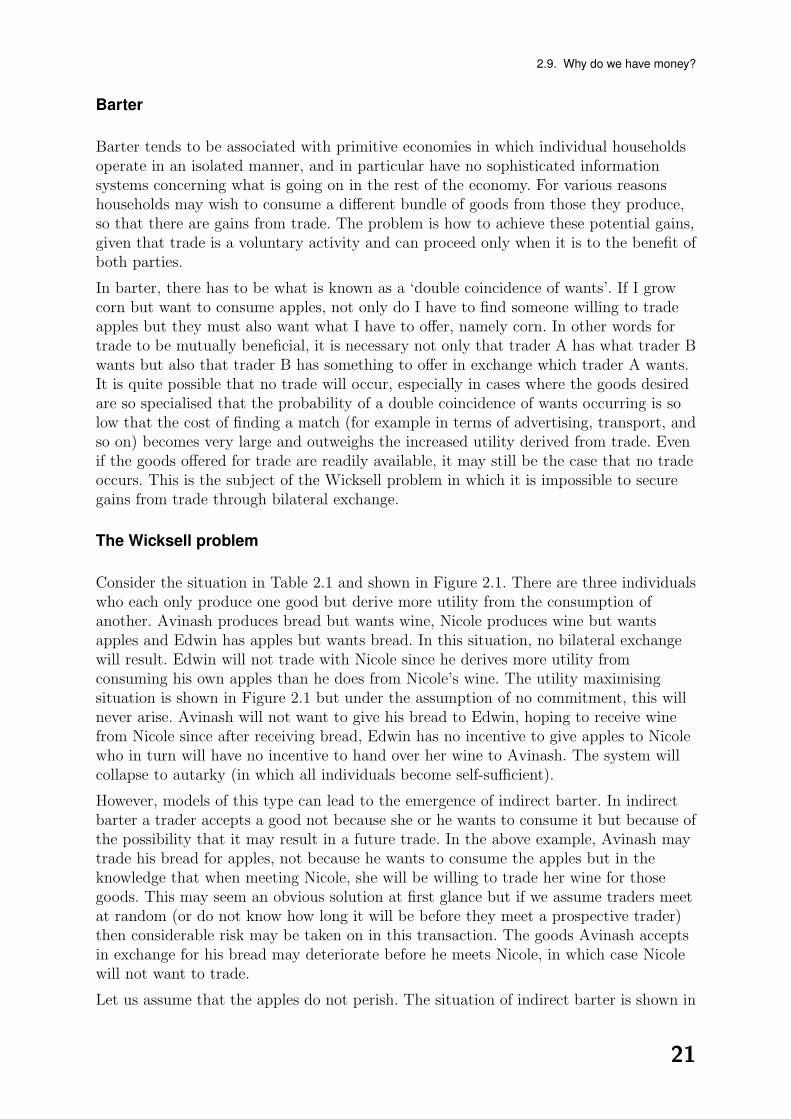

The Wicksell problem

Consider the situation in Table 2.1 and shown in Figure 2.1. There are three individualswho each only produce one good but derive more utility from the consumption ofanother. Avinash produces bread but wants wine, Nicole produces wine but wantsapples and Edwin has apples but wants bread. In this situation, no bilateral exchangewill result. Edwin will not trade with Nicole since he derives more utility fromconsuming his own apples than he does from Nicole’s wine. The utility maximisingsituation is shown in Figure 2.1 but under the assumption of no commitment, this willnever arise. Avinash will not want to give his bread to Edwin, hoping to receive winefrom Nicole since after receiving bread, Edwin has no incentive to give apples to Nicolewho in turn will have no incentive to hand over her wine to Avinash. The system willcollapse to autarky (in which all individuals become self-sufficient).

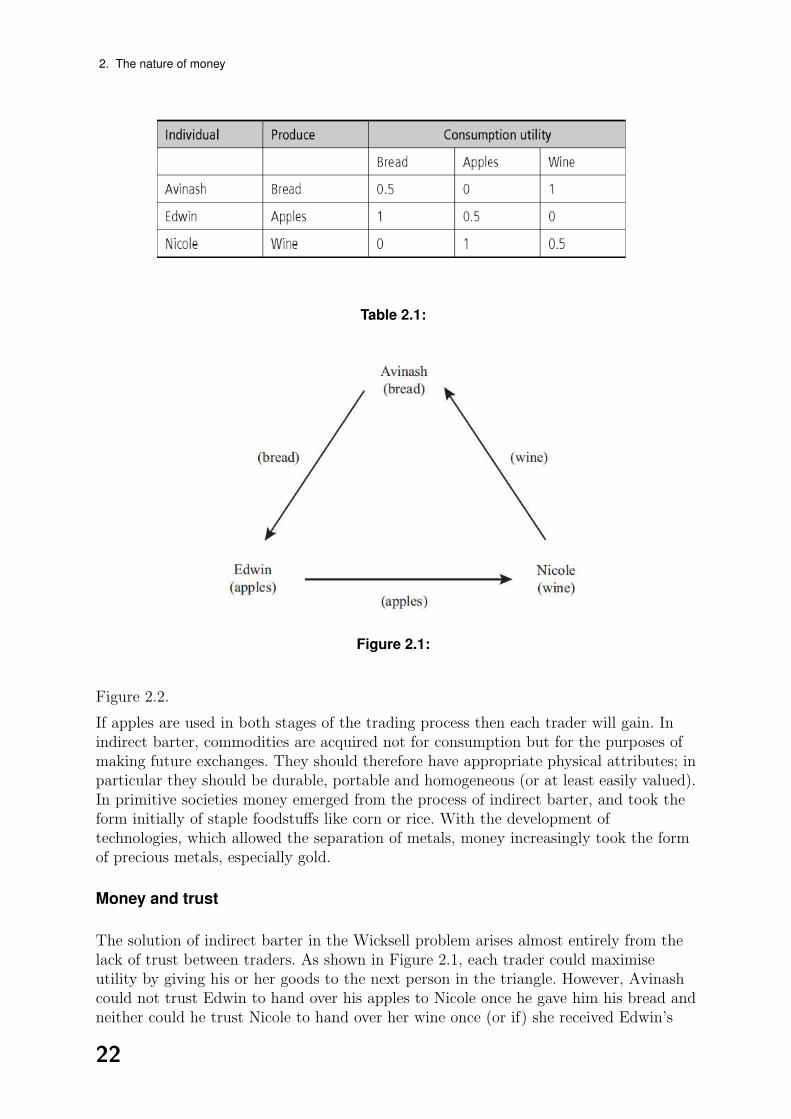

However, models of this type can lead to the emergence of indirect barter. In indirectbarter a trader accepts a good not because she or he wants to consume it but because ofthe possibility that it may result in a future trade. In the above example, Avinash maytrade his bread for apples, not because he wants to consume the apples but in theknowledge that when meeting Nicole, she will be willing to trade her wine for thosegoods. This may seem an obvious solution at first glance but if we assume traders meetat random (or do not know how long it will be before they meet a prospective trader)then considerable risk may be taken on in this transaction. The goods Avinash acceptsin exchange for his bread may deteriorate before he meets Nicole, in which case Nicolewill not want to trade.

Let us assume that the apples do not perish. The situation of indirect barter is shown in

21

2. The nature of money

Table 2.1:

Figure 2.1:

Figure 2.2.

If apples are used in both stages of the trading process then each trader will gain. Inindirect barter, commodities are acquired not for consumption but for the purposes ofmaking future exchanges. They should therefore have appropriate physical attributes; inparticular they should be durable, portable and homogeneous (or at least easily valued).In primitive societies money emerged from the process of indirect barter, and took theform initially of staple foodstuffs like corn or rice. With the development oftechnologies, which allowed the separation of metals, money increasingly took the formof precious metals, especially gold.

Money and trust

The solution of indirect barter in the Wicksell problem arises almost entirely from thelack of trust between traders. As shown in Figure 2.1, each trader could maximiseutility by giving his or her goods to the next person in the triangle. However, Avinashcould not trust Edwin to hand over his apples to Nicole once he gave him his bread andneither could he trust Nicole to hand over her wine once (or if) she received Edwin’s

22

2.9. Why do we have money?

Figure 2.2:

apples.

Let us consider another situation. Suppose I visit my dentist and I pay for his servicesusing a bank debit card.5 The bank will debit my account and credit that of the dentist.I have effectively given an IOU6 to the bank and the bank has given the dentist one ofits IOUs. But why did I not just hand over one of my IOUs directly to the dentist?Perhaps it may be that my dentist does not trust me to repay once he tries to redeemmy IOU. More realistically, he cannot use my IOU to make purchases with anyone elseand the likelihood that he will ever want to redeem the IOU from me, by receiving aneconomics lesson, may be so small that he would never have agreed to spend his timefixing my teeth. If the dentist went to the grocers the following day trying to buyprovisions with an IOU from an economics teacher, of whom the grocer had neverheard, it is highly unlikely that the trade would be completed. On the other hand, if hetried to pay using the bank’s IOU, the grocer should happily agree to the sale, purelybecause everyone knows and trusts the bank.

The difference between my IOU and that of the bank is that the bank’s IOU is liquid

5This example is taken directly from ‘Evil is the Root of all Money’ by Kiyotaki and Moore (2001).The model presented in this paper is not necessary for this subject but the ideas discussed therein willgreatly improve the reader’s intuition as to what is money and why we hold it.

6‘IOU’ is short for ‘I owe you’ and is merely a written statement acknowledging that a debt has beencreated, to be repaid sometime in the future.

23

2. The nature of money

and functionally equivalent to cash. My IOU, on the other hand, is not liquid andcannot flow around the economy facilitating trades. As we will discuss later in thischapter, it is ‘credit’ money but serves the same purpose as the commodity moneyderived in the indirect barter problem, without having to use or lock up any goods inthe payment process.

Activity 2.1 Consider the problem in Figure 2.1. How could you introduce a bankand a system of IOUs to resolve the problem without having to use any commodityto act as a medium of exchange?

The idea of trust and uncertainty are important ones when explaining the existence ofmoney.7 If you do not know, or have any way of obtaining information as to thecreditworthiness of, a prospective customer, there is a high risk that he or she maydefault on that debt. The risk is, however, minimised if the payer hands over an item ofworth, such as commodity money or another store of value, or an IOU redeemable froma third party on which the payee has sufficient information, such as a bank. In this wayit may be essential to hold money beforehand in order to make purchases. This is thewhole idea behind ‘cash in advance’ (CIA) models that we will consider in a moremacroeconomic setting in later chapters. People have to hold money in order toalleviate the problem of trust (or lack of trust) when transactions are made.

2.10 Types of money

Up to now we have considered only two types of money: commodity money in thesolution to the Wicksell problem, and credit money as the solution to the lack of trust inthe issuance of private IOUs. Traditionally, however, money is divided into three types:

commodity money

fiat money

credit money.

Commodity money

Commodity money derives from the use of commodities as exchange intermediaries inindirect barter. Commodity money has taken many forms, such as cattle, corn, seashellsand suchlike, but in most societies, it has evolved towards the precious metals, copper,silver and, above all, gold. Such commodities are accepted in exchange because of theirintrinsic value, even though the trader intends to use them in further exchange ratherthan for their own consumption. Commodity money is inefficient, in part because thecommodities being used may not have ideal properties as exchange intermediaries butmore fundamentally because it is unnecessary to use goods which have intrinsic valuefor a purpose which does not make use of that value. For example, using gold as acommodity money does not make use of the fact that gold does have some alternativeutility-yielding use and could be used in more satisfying ways, such as through jewelleryor ornaments.

7On this issue, see Goodhart (1989a), Chapter 2, Section 2.

24

2.10. Types of money

Fiat money

Fiat money, whose archetype is the government-issued bank note or metal coin, ismoney that has physical substance but no intrinsic value. It is used because its use isestablished by custom and practice. People accept fiat money that they know to beintrinsically worthless because they know others will accept it in payment for goods andservices. The value of fiat money is reinforced in society by the attribute of being ‘legaltender’, that is making it illegal for anyone to refuse payment in fiat money insettlement of a debt. In fact it is this legal ‘stamp’ and recognised power of the issuer,usually governments, which gives fiat money its unquestionable acceptance as a meansof payment.

Since fiat money is essentially worthless, there is a difference between the value of thegoods such money can purchase and the smaller cost of printing this money. Thedifference is known as seigniorage and is effectively the profit made by the issuingauthority when it produces currency.

Credit money

Whereas fiat money is not a claim on any commodity or individual, credit money is; itis the debt of a private person or institution. In the dentist example above, I gave anIOU to the bank, which in turn hands this debt over to the dentist. If he can pass thisclaim on to another individual, the grocer, in exchange for goods, then this debt isbeing used as a means of payment and so constitutes money. However, the asset thatthe grocer now has, the claim on the bank, is matched one-for-one with the bank’sclaim on me. What the bank owes to the grocer (the bank’s liability) must be matchedby what I owe the bank (the bank’s asset) in order for the bank’s balance sheet tobalance. The limitation of credit money is that it can only function if both individuals,the dentist and me in the example, have complete confidence in the willingness andability of the intermediary to honour the debt. If the bank fails then both my dentistand I would lose out since the dentist would still have a claim on me and I may nothave the funds to honour that claim if the bank has been forced to close. Since thereexists a private liability perfectly offsetting the asset acting as a means of payment (i.e.the money is generated inside the private system) credit money is also known as ‘insidemoney’. Fiat money, which cannot be matched against private sector claims (and isgenerated outside the private sector) is in a similar fashion, known as ‘outside money’.In the UK today, inside money is quantitatively much larger than outside money. At thetime of writing, the nominal value of inside money is approximately 30 times the valueof outside money, notes and coins.

There may appear to be a contradiction at this point when we compare the definition ofcredit money to the discussion in the section ‘money as a means of payment’ where weargued that all forms of credit should not be included in our definition of money. In theabove example, although I have replaced a debt to my dentist with a debt to my bank,this is commonly accepted as a means of payment since a transfer of credit to a currentaccount has advantages such as safe-keeping and making use of book-keeping services atthe bank. Only when all parties concerned are entirely confident the bank will not fail,will such transfers be a means of payment. Once the bank hears of my purchase at thedentist (via the swiping of the debit card), the bank debits my account and credits that

25

2. The nature of money

of the payee, the dentist. Nothing further needs to be done since the payment iscomplete. If a purchase is made by credit card, however, a debt is still outstanding andhas to be repaid. Similarly, if I paid by my bank debit card but went overdrawn, a debtwould remain outstanding which I would later have to pay off. For this reason, overdraftfacilities are not a means of payment.

2.11 Properties of money

When discussing the appropriate properties of commodity money, we mentioneddurability, portability and that it should be homogeneous. Other necessary propertiesare divisibility and recognisability. In fact all money should possess these properties:electronic transfers when purchases are made by bank debit card are themselvesdurable, if not in a physical sense, in that $1 credited to your account does notdeteriorate over time. Another property that is just as important is that ofacceptability, the probability that it will be accepted as a means of payment. Kiyotakiand Wright (1992) emphasise this property and argue that acceptability is not aproperty of the money per se. An equilibrium can be reached where one individual usesone money purely because they believe everyone else will use it:

‘When an object is more readily acceptable to other people in the economy, itis more likely that each individual will desire it and accept it as a medium ofexchange. The implication is that the property of acceptability can have aself-reinforcing nature. . . (This) lead(s) to the conclusion that acceptabilitymay not actually be a property of an object as much as it is a property ofsocial convention.’

Kiyotaki and Wright, 1992, p.19.

2.12 A reminder of your learning outcomes

By the end of this chapter, and having completed the Essential reading and activities,you should be able to:

discuss the nature and shortcomings of a barter economy

list and describe the general functions performed by money

describe the Wicksell problem and demonstrate how indirect barter can lead to theemergence of a commodity money

describe the differences between transactions using credit cards and bank debitcards

list and describe what the different types of money are.

26

2.13. Sample examination questions

2.13 Sample examination questions

Section A

Specify whether the following statement is true, false or uncertain. Explain your answerin a short paragraph.

1. ‘The evolution of commodity money from indirect barter, as the solution to theWicksell problem, arises because of a lack of trust between the relevant parties.’

Section B

2. In a monetary economy, money usually performs the three roles of medium ofexchange, unit of account and store of value. Why are these three roles typicallycombined in one entity? Is it possible to conceive of an economy in which they areperformed by three separate entities?

3. What is money and why do we use it? Outline the three different types of moneyand explain what is different between them.

4. ‘Money should essentially be perceived as an instrument that allows an increasinglywidespread and anonymous economic society to deal with the inevitable resultingshortcomings in information and trust of each of the members on the others.’(Goodhart) Explain and discuss.

5. Explain why some economists argue that payment by cheque is the same as givingtrade credit. If this is the case and considering that cheques are drawn on bankcurrent accounts (as are payments by bank debit cards), do cheque payments countas money?

2.14 Feedback to Sample examination questions

Section A

Specify whether the following statement is true, false or uncertain. Explain your answerin a short paragraph.

1. The statement is true. Suggested answers may include Figure 2.1 and anexplanation as to why each person cannot trust the others to pass their goodsalong the chain. In the example of Figure 2.1, Avinash could not trust Edwin tohand over his apples to Nicole once he gave him his bread and neither could hetrust Nicole to hand over her wine once (if) she received Edwin’s apples. By using acommodity money, such as wine, the problem can be solved. Edwin trades hisapples for Nicole’s wine, not because he wants to consume the wine, but because hecan trade it with Avinash for his bread. Wine is thus being used as a commoditymoney.

27

2. The nature of money

Section B

3. Money is anything which is in general use, and generally accepted, as a means ofpayment. Although money has a number of functions, including unit of accountand store of value, it is its use as a means of payment that defines it. The mainreason why money is used is to avoid the problems associated with barter, namelythe double coincidence of wants. You could discuss the origins of a commoditymoney here, from the Wicksell problem, and also explain how money solves thelack of trust problem in a world of largely anonymous individuals. The three typesof money are: commodity money, fiat money and credit money. All these aredescribed near the end of this chapter.

28

Chapter 3

The demand for money

3.1 Introduction

In Chapter 2 we saw why there was a need for money:

to solve the double coincidence of wants problem associated with barter

to obviate the lack of trust between the payer and the payee in a transaction.

However, what determines the quantity of money that individuals and economiesdemand is a separate question. It is the aim of this chapter to explain what determinesthe quantity of money we demand and also to present a number of models (or theories)of the demand for money. The chapter is split into two main sections. The first partconsiders the demand for money from individuals or institutions/firms themicroeconomic determinants of money demand. The second part examines the demandfor money at the macroeconomic level gives a brief history of money demand, focusingon the breakdown of the macroeconomic demand for money function.

3.2 Aims

The aim of the chapter is to study the money demand as one of the building blocks ofthe money market equilibrium.

3.3 Learning outcomes

By the end of this chapter, and having completed the Essential reading and activities,you should be able to:

explain why it is important to study the demand for money

describe the four main microeconomic determinants of money demand

outline the inventory theoretic model of Baumol–Tobin and the portfolio selectionmodel of Tobin

discuss why Tobin’s model solves the ‘plunger’ problem of the demand for moneymodel of Keynes

describe the general set-up of macroeconomic money demand equations

29

3. The demand for money

discuss empirical evidence on money demand functions, especially on income andinterest elasticities

describe what happened and what is meant by ‘the case of the missing money’ andgive reasons for the breakdown of the estimated money demand equations.

3.4 Reading advice

Before embarking on this chapter, and before consulting any of the recommendedreading, you should review your understanding of ‘the demand for money’ from yourstudies in EC2065 Macroeconomics. A very useful text on the demand for money isLaidler (1993), which is both readable and comprehensive, and should be consulted oneverything covered in this chapter. Goodhart (1989) is also essential reading and shouldbe read while you work through the chapter.

3.5 Essential reading

Goodhart, C.A.E. Money, Information and Uncertainty. (London: Macmillan, 1989)Chapters 3 and 4.

Laidler, D.E.W. The demand for money: Theories, evidence and problems. (New York:Harper Collins, 1993) Section II.

Lewis, M.K. and P.D. Mizen Monetary Economics. (Oxford; New York: OxfordUniversity Press, 2000) Chapters 5, 6, 11 and 12.

3.6 Further reading

Books

Friedman, M. ‘The quantity theory of money: a restatement’, in Friedman, M. (ed.)Studies in the quantity theory of money. (University of Chicago Press, 1956).

Goldfeld, S.M. ‘Demand for money: empirical studies’, in Newman, P., M. Milgate andJ. Eatwell (eds) The New Palgrave Dictionary of Money and Finance. (London:Macmillan, 1994).

Goldfeld, S.M. and D.E. Sichel ‘The demand for money’, in Friedman, B. and F. Hahn(eds) Handbook of monetary economics. (Amsterdam: North-Holland, 1990).

Harris, L. Monetary Theory. (New York; London: McGraw-Hill, 1985) Chapters 9 and10.

Journal articles

Baumol, W. ‘The transactions demand for cash: an inventory theoretic approach’,Journal of Econometrics (1952) 66, November, pp.545–56.

30

3.7. Microeconomic determinants of the demand for money

Judd, J. and J. Scadding ‘The search for a stable money demand function: a survey ofthe post-1973 literature’, Journal of Economic Literature 20(2) 1982, pp.993–1023.

Miller, M. and D. Orr ‘A model of the demand for money by firms’, Quarterly Journalof Economics 80(3) 1966, pp.413–35.

Sprenkle, C. ‘The uselessness of transactions demand models’, Journal of Finance 24(5)1969, pp.835–47.

Tobin, J. ‘The interest elasticity of transactions demand for cash’, The Review ofEconomics and Statistics 38(3) 1956, pp.241–47.

Tobin, J. ‘Liquidity preference as behaviour towards risk’, Review of Economic Studies25(1) 1958, pp.65–86.

3.7 Microeconomic determinants of the demand formoney

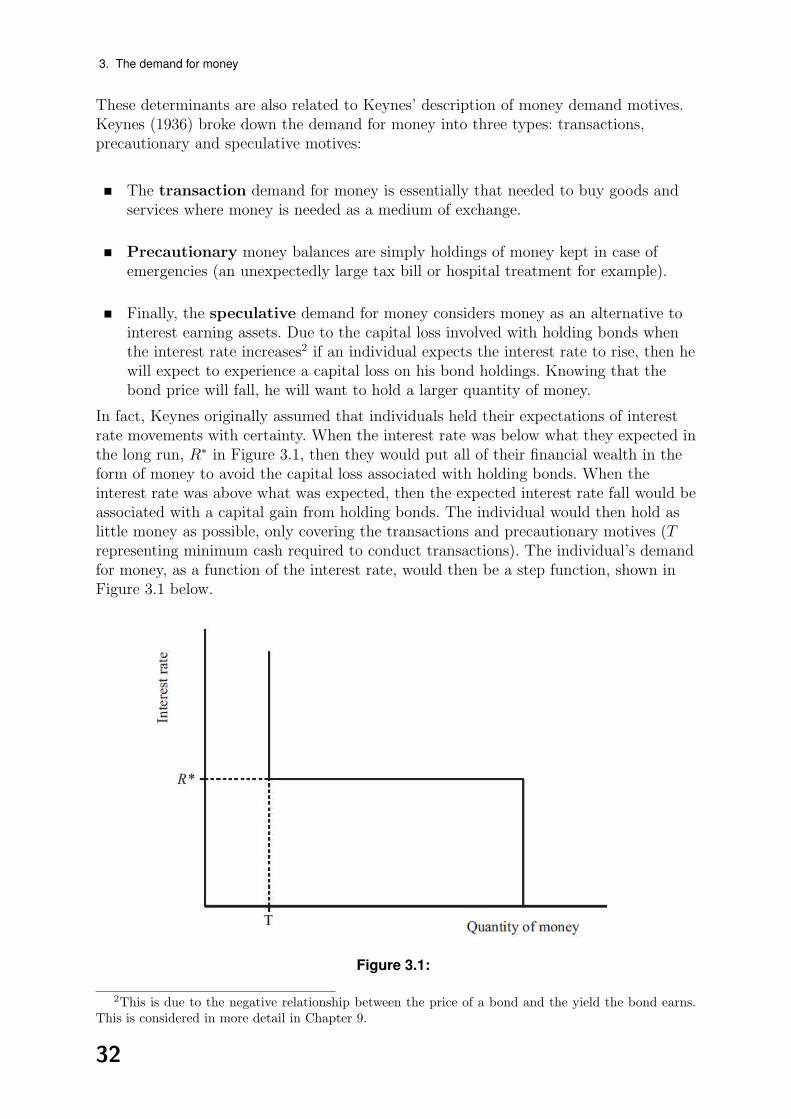

There are essentially four main determinants of money demand at the individual level.These are

1. interest differentials: the difference between the yield on money, commonlyassumed in the literature to be zero,1 and the rate of return on other assets. Thegreater the rate of return on assets other than money, the greater the opportunitycost of holding money, and so the fewer money balances will be demanded.

2. cost of transfers: the costs associated with transferring between higher interestearning assets and money, needed to purchase goods and services. If the cost oftransfers, known as brokerage fees, are high then it is unlikely that we will put ourwealth into the higher interest earning assets as to do so will involve substantialcosts. Demand for money will then be a positive function of these transfer costs.

3. price uncertainty of assets: there is inevitably risk involved in holding assets.Even though there exists a risk in holding money as a store of value, since we donot know for certain how many goods a given quantity of money can buy in thefuture due to inflation, the risk associated with holding other, interest earning,assets is generally considered to be greater. If the price of assets is likely to varyover time then, by the time we want to sell those assets in order to obtain moneyto undertake transactions, we may face considerable capital loss. If we arerisk-averse then our demand for money will therefore be a positive function of theriskiness or price uncertainty of alternative assets.

4. the expected pattern of expenditures and receipts: if individuals were paidtheir wages in lump sums weekly then average cash balances would be less than ifwages were paid monthly. If the pattern of payments and receipts was uncertainthen cash balances would be likely to be higher; it may be unwise to face thebrokerage fees and transfer cash to bonds if there is a possibility that you will needto make a large cash payment in the near future.

1In practice the interest paid on sight deposit accounts is positive.

31

3. The demand for money

These determinants are also related to Keynes’ description of money demand motives.Keynes (1936) broke down the demand for money into three types: transactions,precautionary and speculative motives:

The transaction demand for money is essentially that needed to buy goods andservices where money is needed as a medium of exchange.

Precautionary money balances are simply holdings of money kept in case ofemergencies (an unexpectedly large tax bill or hospital treatment for example).

Finally, the speculative demand for money considers money as an alternative tointerest earning assets. Due to the capital loss involved with holding bonds whenthe interest rate increases2 if an individual expects the interest rate to rise, then hewill expect to experience a capital loss on his bond holdings. Knowing that thebond price will fall, he will want to hold a larger quantity of money.