Embed Size (px)

Citation preview

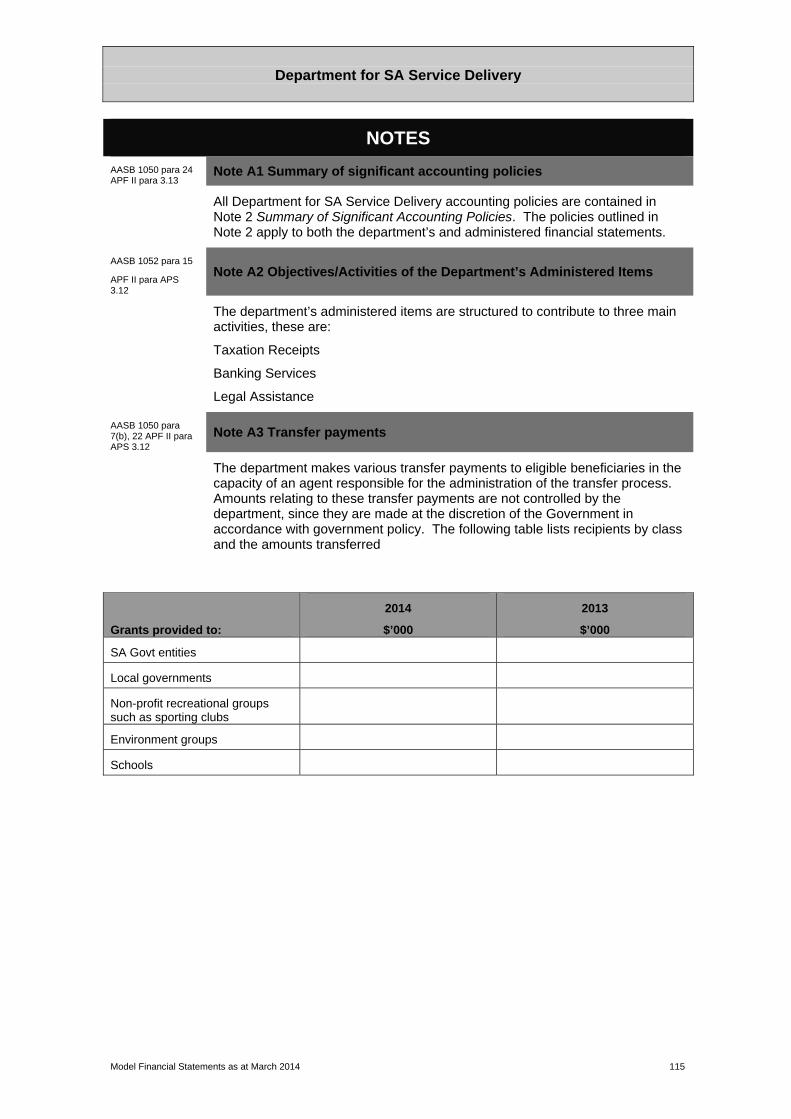

Department for SA Service Delivery

1

MODEL FINANCIAL STATEMENTS

FOR SA GOVERNMENT

NOT-FOR-PROFIT ENTITIES

For the year ended 30 June 2014

Department for SA Service Delivery

2

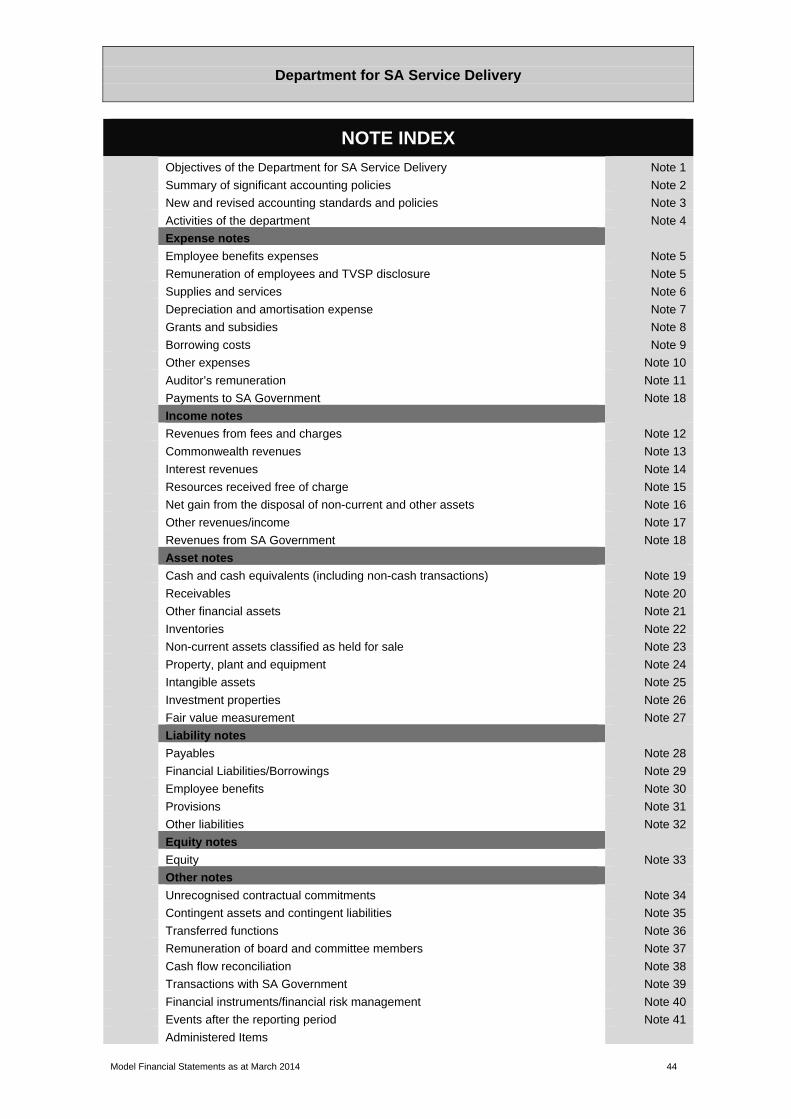

A message from the Under Treasurer ....................................................................................... 4

Acknowledgements ..................................................................................................................... 5

Financial reporting requirements .............................................................................................. 6

Summary of changes in reporting requirements ..................................................................... 9

Department for SA Service Delivery

(Model financial statements for SA Government not-for-profit entities)

Report of the Auditor-General .................................................................................................. 20

Certification of the financial statements ................................................................................. 21

Controlled items

Statement of Comprehensive Income ...................................................................... 22

Statement of Financial Position ............................................................................... 26

Statement of Changes in Equity ............................................................................. 30

Statement of Cash Flows ........................................................................................ 33

Disaggregated Disclosures - Expenses and Income ............................................................ 36

Disaggregated Disclosures - Assets and Liabilities .............................................................. 38

Notes to and forming part of the Financial Statements ......................................................... 40

Administered items

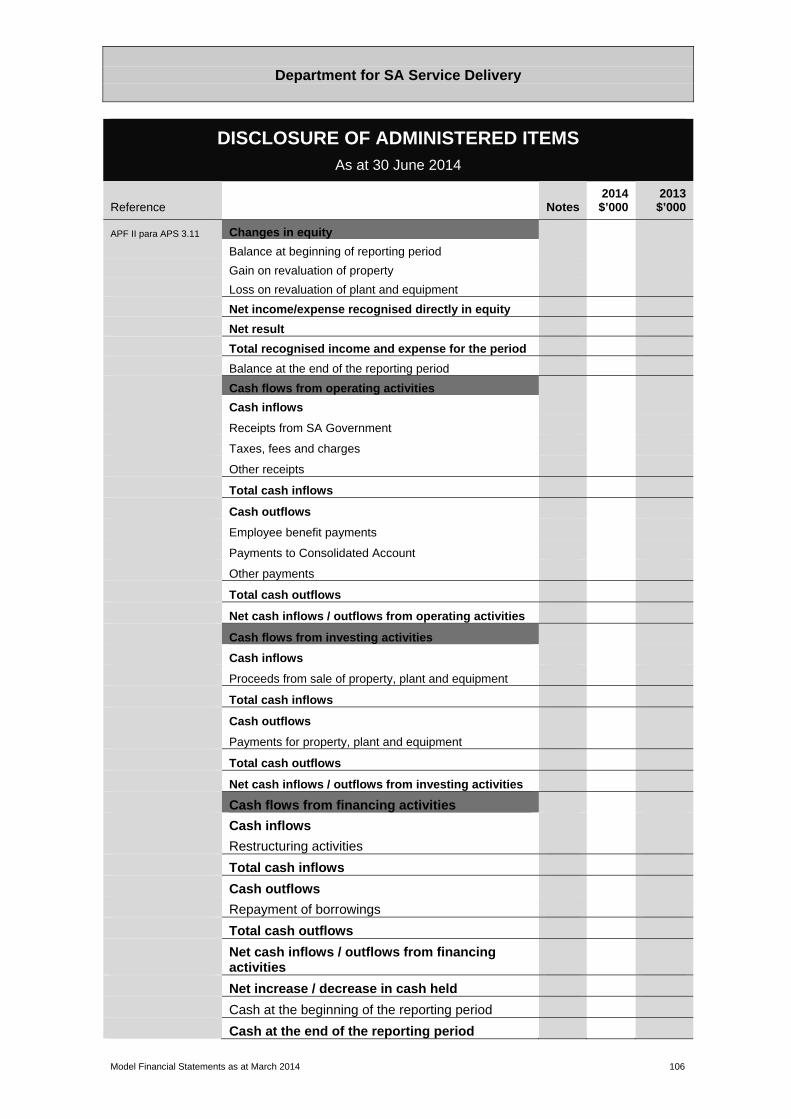

Disclosure of administered items ........................................................................... 104

Administered financial statements ......................................................................... 109

Appendix – alternate note presentation ................................................................................ 116

TABLE OF CONTENTS

Although not included in the model financial statements, appendices to the annual report may include disclosures set out in the Premier and Cabinet Circular 13 Annual Reporting Requirements and a financial review (analysis of reported financial performance and position).

Department for SA Service Delivery

3

Department of Treasury and Finance Level 6, State Administration Centre 200 Victoria Square ADELAIDE SOUTH AUSTRALIA 5000 AUSTRALIA

Financial Management Team Telephone: +618 8226 9529 Facsimile: +618 8226 3127 Website: www.treasury.sa.gov.au

Published by the Department of Treasury and Finance Issue Date: March 2014 © State of South Australia

The Department for SA Service Delivery is a fictitious department and has been used only for the purpose of illustrating the preferred reporting format for South Australian Government not-for-profit entities.

12 May

Department for SA Service Delivery

5

The Financial Management Team within the Government Accounting, Reporting and Procurement Branch of the Department of Treasury and Finance wishes to express its gratitude to the Auditor-General’s Department for their input on this 2014 edition of the Model Financial Statements for South Australian Government not-for-profit entities.

ACKNOWLEDGEMENTS

Department for SA Service Delivery

6

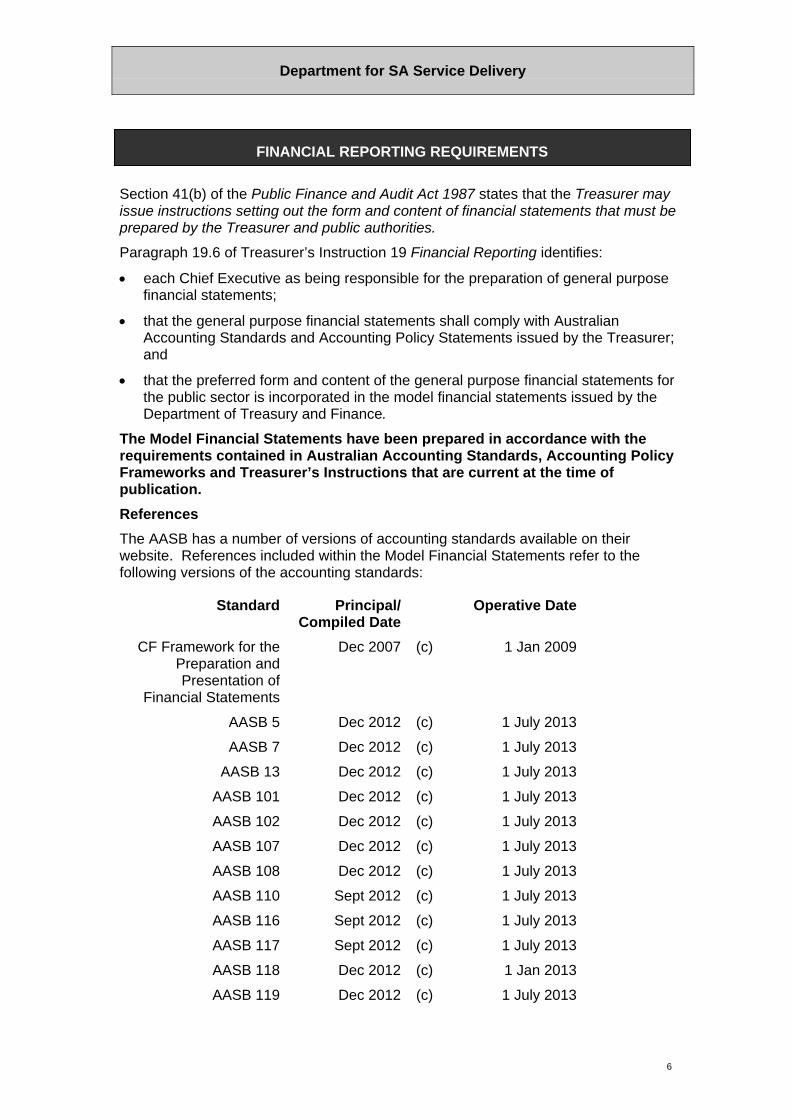

Section 41(b) of the Public Finance and Audit Act 1987 states that the Treasurer may issue instructions setting out the form and content of financial statements that must be prepared by the Treasurer and public authorities.

Paragraph 19.6 of Treasurer’s Instruction 19 Financial Reporting identifies:

each Chief Executive as being responsible for the preparation of general purpose financial statements;

that the general purpose financial statements shall comply with Australian Accounting Standards and Accounting Policy Statements issued by the Treasurer; and

that the preferred form and content of the general purpose financial statements for the public sector is incorporated in the model financial statements issued by the Department of Treasury and Finance.

The Model Financial Statements have been prepared in accordance with the requirements contained in Australian Accounting Standards, Accounting Policy Frameworks and Treasurer’s Instructions that are current at the time of publication.

References

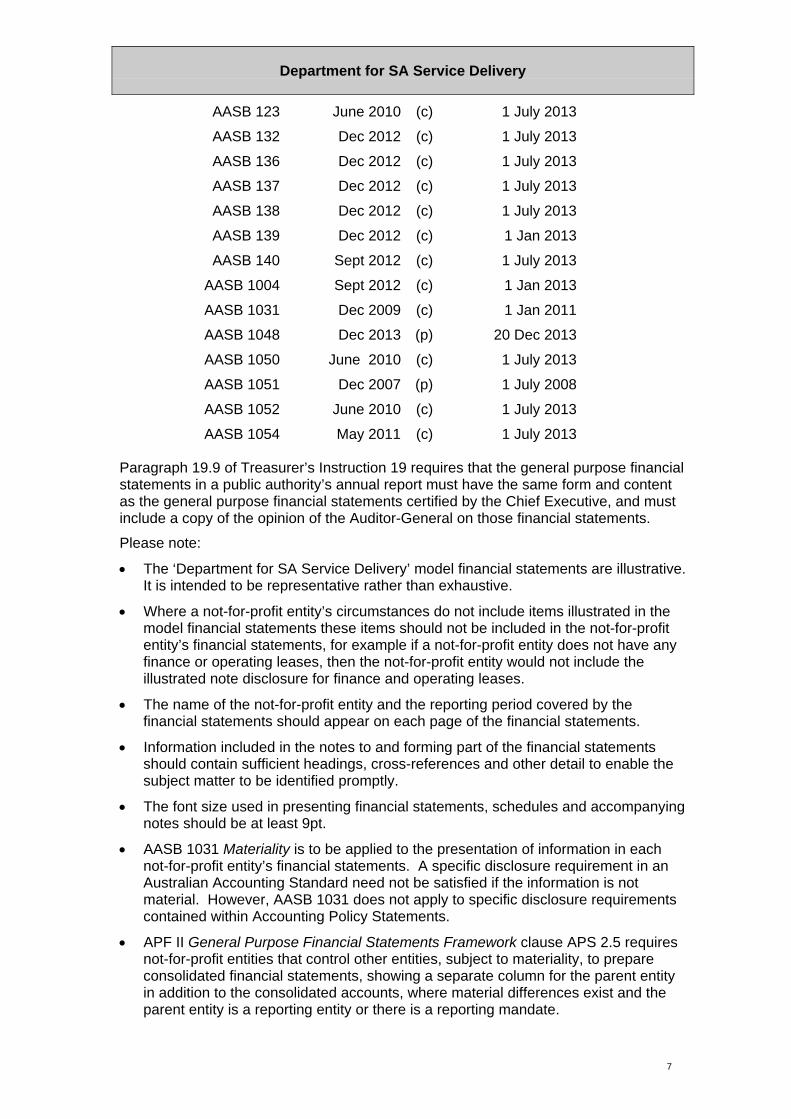

The AASB has a number of versions of accounting standards available on their website. References included within the Model Financial Statements refer to the following versions of the accounting standards:

Standard Principal/ Compiled Date

Operative Date

CF Framework for the Preparation and Presentation of

Financial Statements

Dec 2007 (c) 1 Jan 2009

AASB 5 Dec 2012 (c) 1 July 2013

AASB 7 Dec 2012 (c) 1 July 2013

AASB 13 Dec 2012 (c) 1 July 2013

AASB 101 Dec 2012 (c) 1 July 2013

AASB 102 Dec 2012 (c) 1 July 2013

AASB 107 Dec 2012 (c) 1 July 2013

AASB 108 Dec 2012 (c) 1 July 2013

AASB 110 Sept 2012 (c) 1 July 2013

AASB 116 Sept 2012 (c) 1 July 2013

AASB 117 Sept 2012 (c) 1 July 2013

AASB 118 Dec 2012 (c) 1 Jan 2013

AASB 119 Dec 2012 (c) 1 July 2013

FINANCIAL REPORTING REQUIREMENTS

Department for SA Service Delivery

7

AASB 123 June 2010 (c) 1 July 2013

AASB 132 Dec 2012 (c) 1 July 2013

AASB 136 Dec 2012 (c) 1 July 2013

AASB 137 Dec 2012 (c) 1 July 2013

AASB 138 Dec 2012 (c) 1 July 2013

AASB 139 Dec 2012 (c) 1 Jan 2013

AASB 140 Sept 2012 (c) 1 July 2013

AASB 1004 Sept 2012 (c) 1 Jan 2013

AASB 1031 Dec 2009 (c) 1 Jan 2011

AASB 1048 Dec 2013 (p) 20 Dec 2013

AASB 1050 June 2010 (c) 1 July 2013

AASB 1051 Dec 2007 (p) 1 July 2008

AASB 1052

AASB 1054

June 2010

May 2011

(c)

(c)

1 July 2013

1 July 2013

Paragraph 19.9 of Treasurer’s Instruction 19 requires that the general purpose financial statements in a public authority’s annual report must have the same form and content as the general purpose financial statements certified by the Chief Executive, and must include a copy of the opinion of the Auditor-General on those financial statements.

Please note:

The ‘Department for SA Service Delivery’ model financial statements are illustrative. It is intended to be representative rather than exhaustive.

Where a not-for-profit entity’s circumstances do not include items illustrated in the model financial statements these items should not be included in the not-for-profit entity’s financial statements, for example if a not-for-profit entity does not have any finance or operating leases, then the not-for-profit entity would not include the illustrated note disclosure for finance and operating leases.

The name of the not-for-profit entity and the reporting period covered by the financial statements should appear on each page of the financial statements.

Information included in the notes to and forming part of the financial statements should contain sufficient headings, cross-references and other detail to enable the subject matter to be identified promptly.

The font size used in presenting financial statements, schedules and accompanying notes should be at least 9pt.

AASB 1031 Materiality is to be applied to the presentation of information in each not-for-profit entity’s financial statements. A specific disclosure requirement in an Australian Accounting Standard need not be satisfied if the information is not material. However, AASB 1031 does not apply to specific disclosure requirements contained within Accounting Policy Statements.

APF II General Purpose Financial Statements Framework clause APS 2.5 requires not-for-profit entities that control other entities, subject to materiality, to prepare consolidated financial statements, showing a separate column for the parent entity in addition to the consolidated accounts, where material differences exist and the parent entity is a reporting entity or there is a reporting mandate.

Department for SA Service Delivery

8

AASB 112 Income Taxes is not applicable to SA Government not-for-profit entities that are required by Treasurer’s Instruction 22 Tax Equivalent Payments to calculate income tax equivalent payments using the accounting profit model.

In accordance with APF II General Purpose Financial Statements Framework clause APS 2.7 a not-for-profit entity must seek the Department of Treasury and Finance’s approval prior to adopting a new or amended accounting standard ahead of the specified commencement date due to the effect on the whole-of-government financial statements.

Reporting period

The Model Financial Statements apply to the reporting period commencing 1 July 2013 to 30 June 2014.

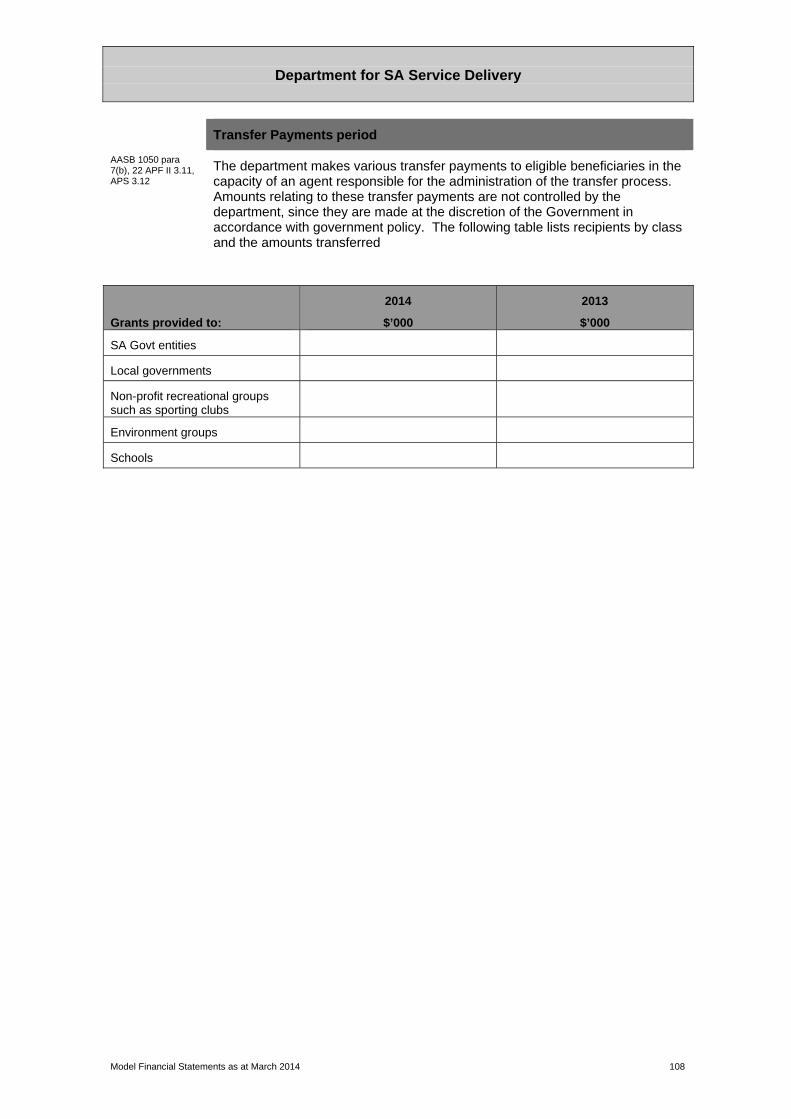

Controlled and administered items

The financial statements must distinguish between those transactions and balances that are ‘controlled’ by the entity and those that are ‘administered’ by the entity on behalf of the Government.

Controlled transactions and balances must be recognised in the financial statements.

Administered transactions and balances that are significant in relation to the not-for-profit entity’s overall financial performance or financial position must have separate ‘administered’ financial statements and notes prepared. Administered items that are insignificant to the entity’s overall financial performance and position must be disclosed in the notes to the accounts.

Administrative restructures/machinery of government changes

Pursuant to legislation or other authority, the identity and/or structure of a government reporting entity may be dismantled or restructured by the Government. The restructuring process may result in the transfer of certain employees, activities, assets and/or the assumption of liabilities to other government reporting entities.

Accounting Policy Statements contained within Accounting Policy Framework II General Purpose Financial Statements Framework specify the financial reporting requirements for administrative restructures. In addition, the Financial Management Toolkit contains guidance and checklists which may be of assistance.

Rounding

Amounts shown in the financial statements must be rounded to the nearest $1,000 and expressed in Australian currency.

Assistance

Assistance on financial reporting and related accounting issues may be directed to the Financial Management Team by e-mail or telephone:

Email: [email protected]

Phone: 8226 9529

An electronic version of the Model Financial Statements for SA Government not-for-profit entities is available at http://www.treasury.sa.gov.au

Department for SA Service Delivery

9

Treasurer’s instructions

Amendments have been made to Treasurer’s instructions since 30 June 2013, but these will not have an impact on the production of general purpose financial statements.

Accounting policy frameworks

The main amendments to the Accounting Policy Frameworks are for:

AASB 13 Fair Value Measurement – This standard has had a significant impact on APF III Asset Accounting Framework.

AASB 1053 Application of Tiers of Australian Accounting Standards – APF II General Purpose Financial Statements requires Tier 1 reporting requirements be adopted.

Minor amendments have been made to other Accounting Policy Frameworks since 30 June 2013.

Prospective Accounting policy framework changes

It is anticipated that Department of Treasury and Finance will amend in May certain rates and thresholds for employee benefits within APF IV Financial Asset and Liability Framework.

Public Finance and Audit Act 1987

Amendments have been made to the Public Finance and Audit Act 1987 since 30 June 2013, but these will not have an impact on the production of general purpose financial statements.

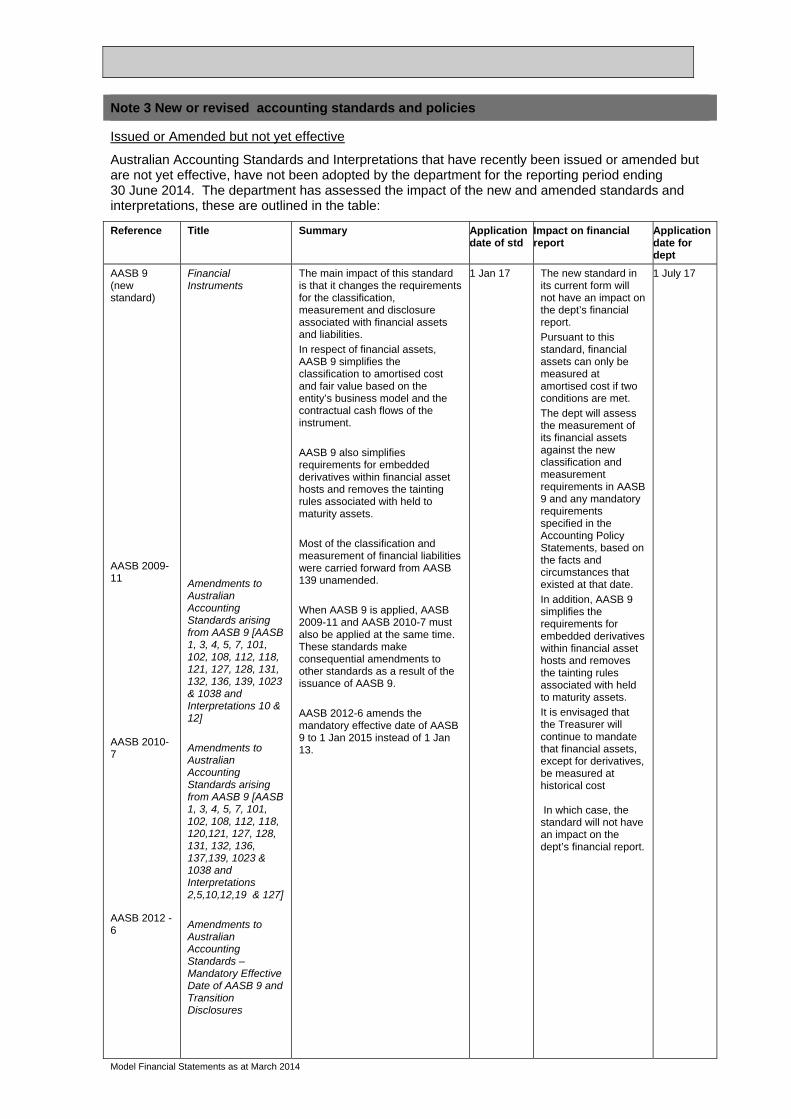

New and revised Australian accounting standards

When complying with Australian accounting standards, preparers need to comply with all applicable new and amending standards and interpretations.

Note, the AASB has released separate For-Profit (FP) and Not-For-Profit (NFP) versions of Australian Accounting Standards due to the consolidation and joint arrangement set of standards. These standards apply to not-for-profit entities for periods beginning on or after 1 January 2014 compared with 1 January 2013 for for-profit entities. All references to AASBs are the NFP version.

The AASB have released the following new/revised accounting standards:

AASB 9 Financial Instruments is operative from 1 January 2017. This standard applies to not-for-profit entities. AASB 9 includes requirements for the classification, measurement, recognition and de-recognition for financial instruments.

SUMMARY OF CHANGES IN REPORTING REQUIREMENTS

Department for SA Service Delivery

10

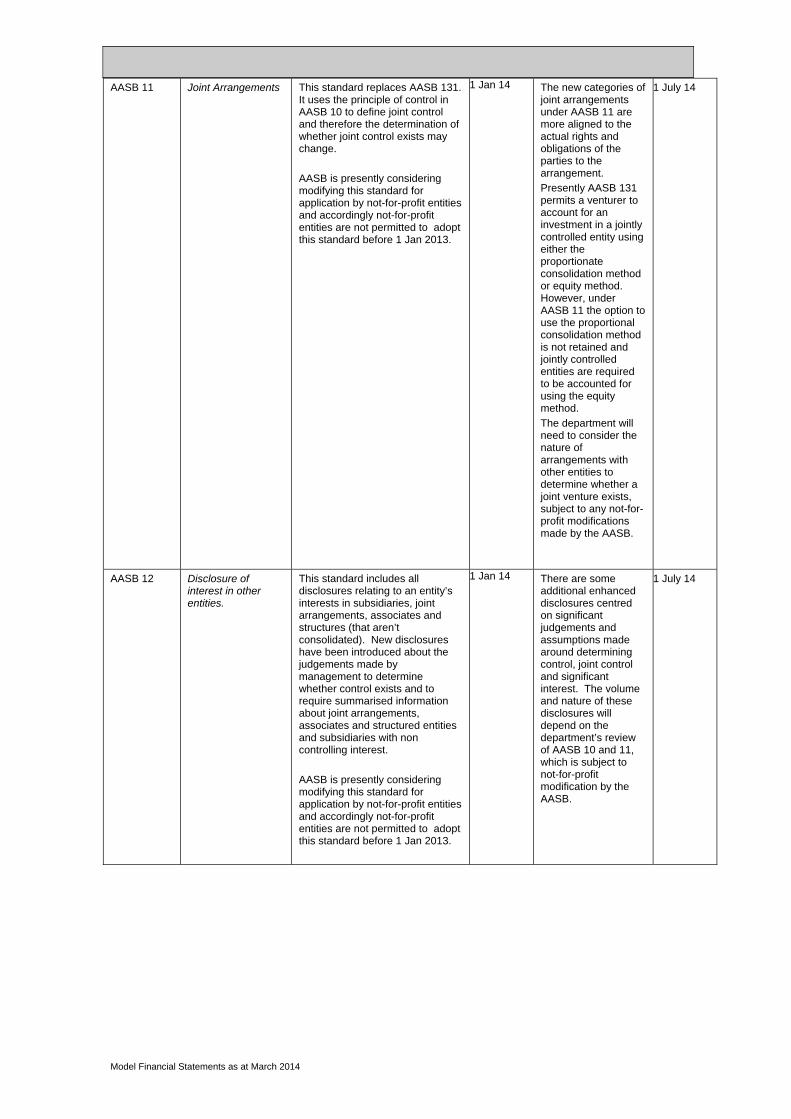

AASB 10 Consolidated Financial Statements is operative from 1 January 2014. This standard applies to not-for-profit entities, however not-for-profit entities are not permitted to apply this standard prior to 1 January 2013. AASB 10 includes principles for the presentation and preparation of consolidated financial statements when an entity controls one or more other entities.

AASB 11 Joint Arrangements is operative from 1 January 2014. This standard applies to not-for-profit entities, however not-for-profit entities are not permitted to apply this standard prior to 1 January 2013. AASB 11 includes principles for financial reporting by entities that have an interest in arrangements that are controlled jointly.

AASB 12 Disclosure of Interests in Other Entities is operative from 1 January 2014. This standard applies to not-for-profit entities, however not-for-profit entities are not permitted to apply this standard prior to 1 January 2013. AASB 12 requires entities to disclose information to enable users to evaluate the nature and risk associated with its interest in other entities and the effects of those interests on its financial position, financial performance and cash flows.

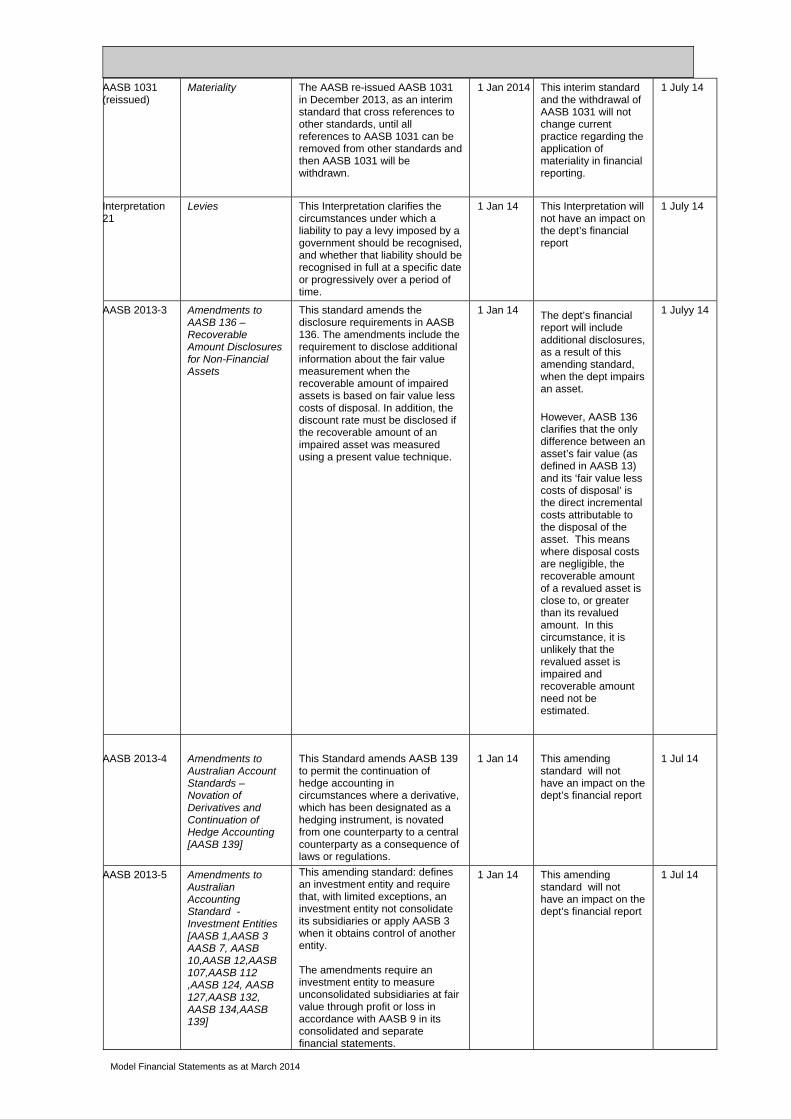

AASB 1031 Materiality is operative from 1 January 2014. The AASB re-issued AASB 1031 in December 2013 as an interim standard that cross references to other standards, until all references to AASB 1031 can be removed from other standards and then, AASB 1031 will be withdrawn. Note: it is not envisaged that the withdrawal of the standard will change current practice regarding the application of materiality in financial reporting.

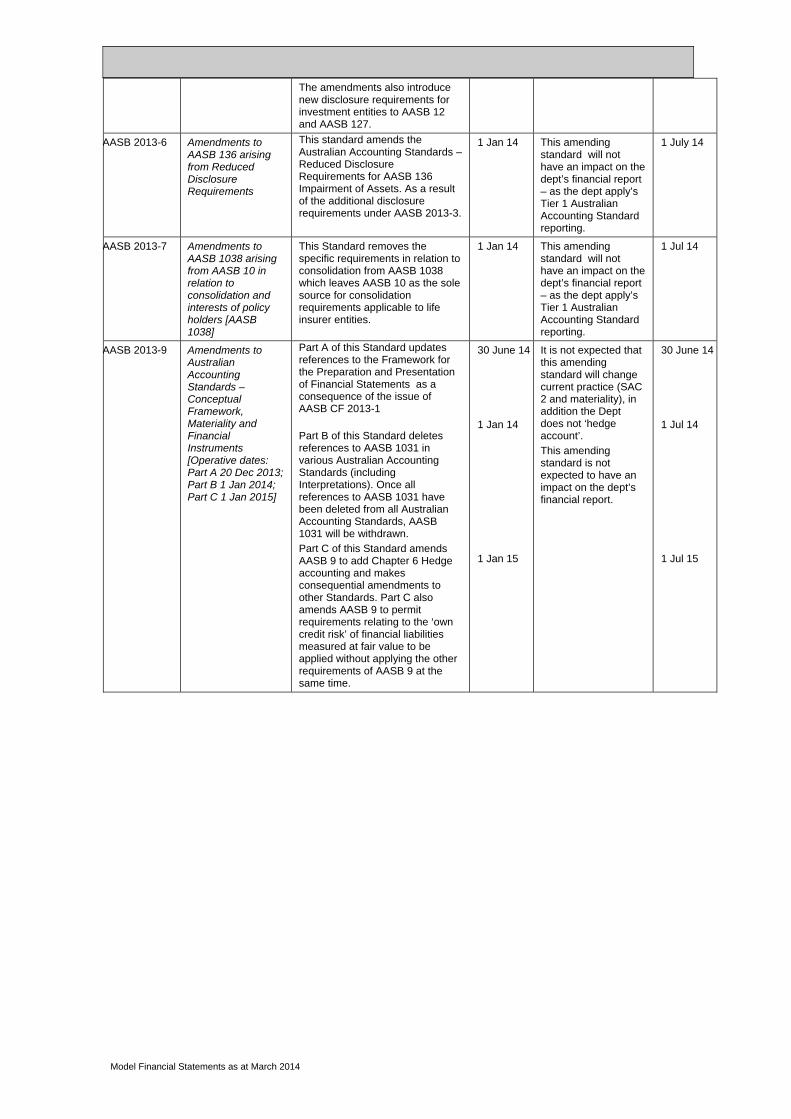

AASB 1048 Interpretation and Application of Standards is operative from 1 January 2014. This standard applies to not-for-profit entities. The main amendment is the addition of IFRIC 21.

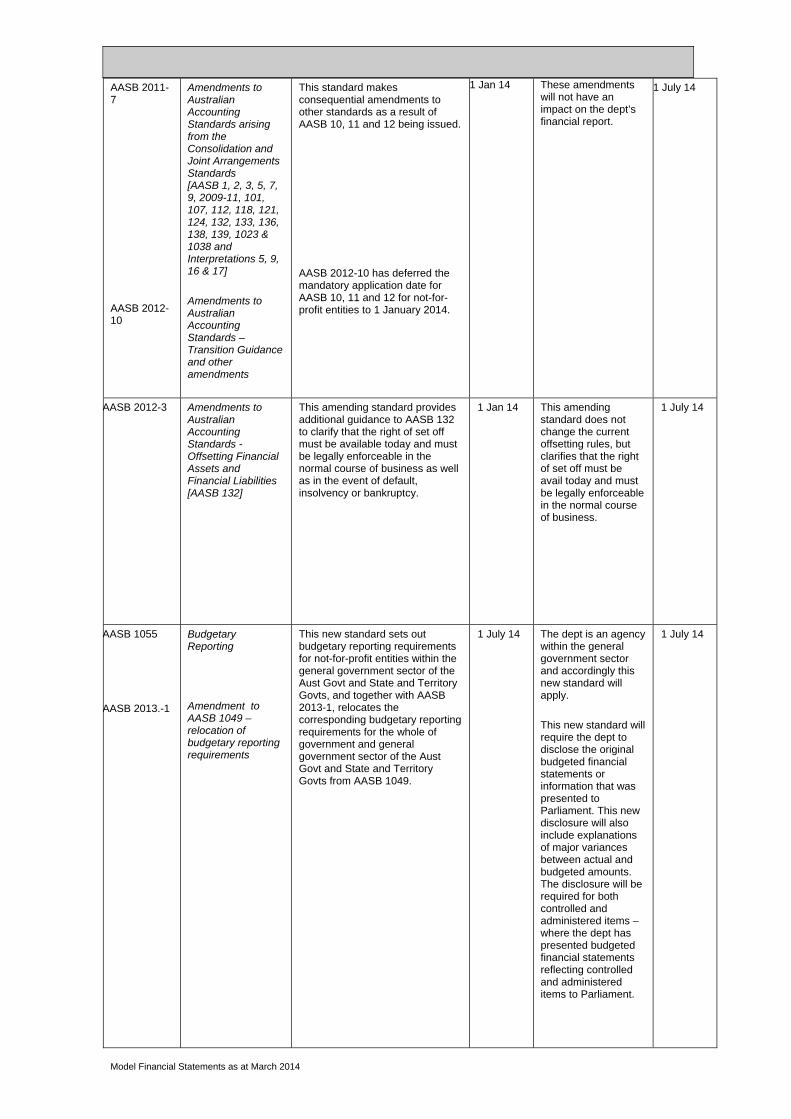

AASB 1055 Budgetary Reporting is operating from 1 July 2014. This standard requires not-for-profit entities within the general government sector of the Australian Government and State and Territory Governments; and whole of government and general government sectors of the Australian Government and State and Territory Governments to include budgetary reporting requirements in financial statements.

As at March 2014, the following new and/or revised accounting standards are applicable for the year ending 30 June 2014:

AASB 1 First-time adoption of Australian Accounting Standards (amendments arose from AASB 2010-2, AASB 2011-8, AASB 2011-10, AASB 2011-12, AASB 2012-4, AASB 2012-5, AASB 2012-10 and AASB 2012-11)

AASB 2 Share-based Payment (amendments arose from AASB 2010-2, AASB 2011-8 and AASB 2012-11)

AASB 3 Business Combinations (amendments arose from AASB 2010-2, AASB 2011-8 and AASB 2012-1)

AASB 4 Insurance Contracts (amendments arose from AASB 2011-8)

AASB 5 Non-current Assets Held for Sale and Discontinued Operations (amendments arose from AASB 2010-2, AASB 2011-8 and AASB 2012-10)

Department for SA Service Delivery

11

AASB 7 Financial Instruments: Disclosures (amendments arose from AASB 2010-2, AASB 2011-8, AASB 2012-1, AASB 2012-2, AASB 2012-7 and AASB 2012-10)

AASB 8 Operating Segments (amendments arose from AASB 2010-2, AASB 2011-10, AASB 2012-10 and AASB 2012-11)

AASB 13 Fair Value (new standard with amendments that arose from AASB 2012-1 and AASB 2012-10)

AASB 101 Presentation of Financial Statements (amendments arose from AASB 2010-2, AASB 2011-2, AASB 2011-8, AASB 2011-10, AASB 2012-5, AASB 2012-7 and AASB 2012-10)

AASB 102 Inventories (amendments arose AASB 2010-2, AASB 2011-8 and AASB 2012-10)

AASB 107 Statement of Cash Flows (amendments arose from AASB 2010-2 and AASB 2012-11)

AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors (amendments arose from AASB 2010-2, AASB 2011-8 and AASB 2012-10)

AASB 110 Events after the Reporting Period (amendments arose from AASB 2010-2 and AASB 2011-8)

AASB 111 Construction Contracts (amendments arose from AASB 2010-2)

AASB 112 Income Taxes (amendments arose from AASB 2010-2 and AASB 2012-10)

AASB 116 Property, Plant and Equipment (amendments arose from AASB 2010-2, AASB 2011-8 and AASB 2012-5)

AASB 117 Leases (amendments arose from AASB 2010-2 and AASB 2011-8)

AASB 118 Revenue (amendments arose from AASB 2011-8 and AASB 2012-10)

AASB 119 Employee Benefits (reissued standard with amendments that arose from AASB 2011-8, AASB 2011-10, AASB 2011-11 and AASB 2012-10)

AASB 120 Accounting for Government Grants and Disclosure of Government Assistance (amendments arose from AASB 2011-8)

AASB 121 The Effects of Changes in Foreign Exchange Rates (amendments arose from AASB 2010-2 and AASB 2011-8)

AASB 123 Borrowing Costs (amendments arose from AASB 2010-2)

AASB 124 Related Party Disclosures (amendments arose from AASB 2010-2, AASB 2011-4 and AASB 2011-10)

AASB 127 Consolidated and Separate Financial Statements (amendments arose from AASB 2010-2 and AASB 2011-6)

AASB 128 Investments (amendments arose from AASB 2010-2, AASB 2011-6 and AASB 2011-8)

AASB 131 Interest in Joint Ventures (amendments arose from AASB 2010-2 and AASB 2011-6 and AASB 2011-8)

Department for SA Service Delivery

12

AASB 132 Financial Instruments: Presentation (amendments arose from AASB 2011-8, AASB 2012-2, AASB 2012-5 and AASB 2012-10)

AASB 133 Earnings per Share (amendments arose from AASB 2010-2, AASB 2011-8, AASB 2012-10 and AASB 2012-11)

AASB 134 Interim Financial Reporting (amendments arose from AASB 2010-2, AASB 2011-8, AASB 2011-10, AASB 2012-5, AASB 2012-10 and AASB 2012-11)

AASB 136 Impairment of Assets (amendments arose from AASB 2010-2 and AASB 2011-8)

AASB 137 Provisions, Contingent Liabilities and Contingent Assets (amendments arose from AASB 2010-2 and AASB 2012-10)

AASB 138 Intangible Assets (amendments arose from AASB 2010-2 and AASB 2011-8)

AASB 139 Financial Instruments: Recognition and Measurement (amendments arose from AASB 2011-8)

AASB 140 Investment Property (amendments arose from AASB 2010-2, AASB 2011-8 and AASB 2012-1)

AASB 141 Agriculture (amendments arose from AASB 2010-2, AASB 2011-8 and AASB 2012-1)

AASB 1004 Contributions (amendments arose from AASB 2011-8)

AASB 1023 General Insurance Contracts (amendments arose from AASB 2011-8 and AASB 2012-10)

AASB 1038 Life Insurance Contracts (amendments arose from AASB 2011-8, AASB 2012-10 and AASB 2013-2)

AASB 1039 Concise Financial Reports (amendments arose from AASB 2012-10)

AASB 1049 Whole of Government and General Government Sector Financial Reporting (amendments arose from AASB 2011-10 and AASB 2012-10)

AASB 1050 Administered Items (amendments arose from AASB 2010-2)

AASB 1052 Disaggregated Disclosures (amendments arose from AASB 2010-2)

AASB 1053 Application of Tiers of Australian Accounting Standards (new standard)

AASB 1054 Australian Additional Disclosures (amendments arose from AASB 2011-2)

Department for SA Service Delivery

13

AASB 2010-2 Amendments to Australian Accounting Standards arising from Reduced Disclosure Requirements [AASB 1, 2, 3, 5, 7, 8, 101, 102, 107, 108, 110, 111, 112, 116, 117, 119, 121, 123, 124, 127, 128, 131, 133, 134, 136, 137, 138, 140, 141, 1050, 1052 and Interpretations 2, 4, 5, 15, 17, 127, 129 and 1052]

This standard gives effect to the new standard - AASB 1053 Reduced Disclosure Requirements via making amendments to the Australian Accounting Standards and Interpretations listed above.

These standards and interpretations have been amended for the application by certain entities to adopt the reduced disclosure requirements (ie Tier 2 reporting) in preparing general purpose financial statements.

Impact

In accordance with APF II, all not-for-profit entities that are consolidated into the whole of government financial statements must apply AASB 1053’s Tier 1 Australian Accounting Standards reporting requirements.

Consequently the amendments will not have an impact and have not been included in the Model Financial Statements for not-for-profit entities.

AASB 2010-10 Further amendments to Australian Accounting Standards – Removal of Fixed Dates for First Time Adopters [AASB 2009-11 and AASB 2010-7]

This standard amends two Amending Standards as a result of the IASB issuing Severe Hyperinflation and Removal of Fixed Dates for First Time Adopters.

Impact

Entities apply AASB 1 on first-time adoption. As public sector not-for-profit entities, have adopted Australian equivalents to International Financial Reporting Standards, the amendments will not have an impact and have not been included in the Model Financial Statements for not-for-profit entities.

AASB 2011-2 Amendments to Australian Accounting Standards arising from the Trans-Tasman Convergence Project - Reduced Disclosure Requirements [AASB 101 and AASB 1054]

This standard revises the Reduced Disclosure Requirement amendments, originally specified in AASB 2010-2 (ie the above amending standard) for AASB 101, to reflect the deletion of certain requirements from AASB 101 that are now in AASB 1054 Australian Additional Disclosures.

Impact

In accordance with APF II, all not-for-profit entities that are consolidated into the whole of government financial statements must apply AASB 1053’s Tier 1 Australian Accounting Standards reporting requirements.

Consequently the amendments will not have an impact and have not been included in the Model Financial Statements for not-for-profit entities.

Department for SA Service Delivery

14

AASB 2011-4 Amendments to Australian Accounting Standards to Remove Individual Key Management Personnel Disclosure Requirements [AASB 124]

This standard revises AASB 124 to remove the individual key management personnel disclosures from the standard on the basis that they are not part of IFRS; not included in NZ accounting standards; and are considered by the AASB to be more in the nature of governance disclosures that are better dealt with as part of the Corporations Act 2001.

Impact

AASB 124 does not apply to general purpose financial statements of not-for-profit public sector entities. Accordingly the amendments will not have an impact and have not been included in the Model Financial Statements for not-for-profit entities.

AASB 2011-6 Amendments to Australian Accounting Standards – Extending Relief from Consolidation, the Equity Method and Proportionate Consolidation -Reduced Disclosure Requirements [AASB 127, 128 and 131]

This standard extends the relief (provided by AASB 2011-5) from consolidation; the equity method; and proportionate consolidation - that is available in certain circumstances to a parent entity, investor or venturer where the ultimate or any intermediate parent entity prepares consolidated financial statements that are not compliant with IFRS as a result of applying RDR.

Impact

In accordance with APF II, all not-for-profit entities that are consolidated into the whole of government financial statements must apply AASB 1053’s Tier 1 Australian Accounting Standards reporting requirements.

Consequently the amendments will not have an impact and have not been included in the Model Financial Statements for not-for-profit entities.

AASB 2011-8 Amendments to Australian Accounting Standards arising from AASB 13 [AASB 1, 2, 3, 4, 5, 7, 9, 101, 102, 108, 110, 116, 117, 118, 119, 120, 121, 128, 131, 132, 133, 134, 136, 138, 139, 140, 141, 1004, 1023 and 1038. Interpretations 2, 4, 12, 13, 14, 17, 19, 131 and 132]

AASB 13 establishes a new definition of fair value and general requirements when measuring the fair value of assets and liabilities. This standard replaces the existing definition and fair value guidance in the Australian Accounting Standards and Interpretations listed above.

Impact

APF III requires not-for-profit entities to measure certain assets at fair value. Consequently the new requirements (AASB 13 and the amending standard) will apply to Department of SA Service Delivery’s assets that are measured at fair value.

The department has reviewed its fair value measurement methodologies (both internal estimates and independent valuation appraisal) to ensure they are consistent with the standard. In the past, the department has used either the cost approach or the market approach to measure fair value. The department will continue to measure its non-current assets using either the cost approach or market approach.

Where required, the department has liaised with Certified Practising Valuers and/or third parties to ascertain the additional information for note disclosure as required by the standard.

Department for SA Service Delivery

15

The Model Financial Statements has been amended to reflect any changes in terminology, measurement and disclosure as required by AASB 13 and any related amending standards.

AASB 2011-10 Amendments to Australian Accounting Standards arising from AASB 119 (September 2011) [AASB 1, 8, 101, 124, 134 and 1049 and Interpretation 14]

This standard amends the accounting standards listed above as a result of the AASB issuing a revised version of AASB 119. The main change as a result of the revised version of AASB 119, is the accounting for defined benefit plans. The amendment removes the option for accounting for the liability and requires that the liabilities arising from such plans are recognised in full and actuarial gains and losses being recognised in other comprehensive income. It also revises the method of calculating the return on plan assets.

In addition, the revised AASB 119 has changed the definition of ‘short term employee benefits’ and accordingly the criteria to account for these.

Impact

Defined benefit plans are accounted for, recognised and reported at a whole of government level. The department only makes super contributions to Super SA, accordingly the amendments relating to defined benefit plans from the amending standard will not have an impact on the Department for SA Service Delivery.

In relation to the change in definition of ‘short term employee benefits’ and the criteria to account for these:

Previously short-term employee benefits were defined as employee benefits (other than termination benefits) that are due to be settled within twelve months after the end of the period in which the employees render the related service.

The revised AASB 119 defines short-term employee benefits as employee benefits (other than termination benefits) that are expected to be settled wholly before twelve months after the end of the annual reporting period in which the employees render the related service.

The Commissioner for Public Sector Employment Determination 3.1: Employment Conditions – Leave and Regulation 21 of the Public Sector Regulations 2010 state that recreation leave must be applied for and granted so that the employee’s recreation leave entitlement for a service year is taken before the end of the following service year, unless the employee applies to carry over such leave and the Chief Executive or delegate approves the application. The Chief Executive or delegate may approve an application by an employee to accrue and carry forward any amount of accrued recreation leave for a maximum of 24 months after its accrual. Deferral for a longer period may only occur in the most exceptional cases.

Accordingly it is the department’s expectation that recreational leave will be settled wholly before twelve months after the end of the annual reporting period in which the employee renders the related service.

Further, in the unusual event where an employee’s recreational leave is approved to be carried forward, and:

the application of a discount calculation would be immaterial - agencies would continue to use the nominal value.

Department for SA Service Delivery

16

the agency has substantial excess leave balances that would result in the non application of a discount calculation being material – agencies would measure that part of the liability at its present value ie a long term benefit

This is consistent with current practise.

Note: It is expected that in the majority of cases, agencies will apply the nominal value and not the present value method due to the immaterial effect of discounting.

Where the amendments have had an impact, the Model Financial Statements for not-for-profit entities has been updated.

AASB 2011-11 Amendments to AASB 119 arising from the Reduced Disclosure Requirements

This standard amends the reissued AASB 119 to incorporate reduced disclosure requirements into the standard for entities applying AASB 1053’s Tier 2 reporting requirements.

Impact

In accordance with APF II, all not-for-profit entities that are consolidated into the whole of government financial statements must apply AASB 1053’s Tier 1 Australian Accounting Standards reporting requirements.

Consequently the amendments will not have an impact and have not been included in the Model Financial Statements for not-for-profit entities.

AASB 2011-12 Amendments to Australian Accounting Standards arising from Interpretation 20 [AASB 1]

This standard amends AASB 1 as a result of IFRIC Interpretation 20 Stripping Costs in the Production Phase of a Surface Mine being issued.

Impact

Entities apply AASB 1 on first-time adoption. As public sector not-for-profit entities, have adopted Australian equivalents to International Financial Reporting Standards, the amendments will not have an impact and have not been included in the Model Financial Statements for not-for-profit entities.

AASB 2012-1 Amendments to Australian Accounting Standards – Fair Value Measurement – Reduced Disclosure Requirements [AASB 3, 7, 13, 140 and 141]

This standard amends AASB 13 to incorporate reduced disclosure requirements into the standard for entities applying AASB 1053’s Tier 2 reporting requirements.

Impact

In accordance with APF II, all not-for-profit entities that are consolidated into the whole of government financial statements must apply AASB 1053’s Tier 1 Australian Accounting Standards reporting requirements.

Consequently the amendments will not have an impact and have not been included in the Model Financial Statements for not-for-profit entities.

Department for SA Service Delivery

17

AASB 2012-2 Amendments to Australian Accounting Standards – Disclosures – Offsetting Financial Assets and Financial Liabilities [AASB 7 and 132]

This standard amends the required disclosures in AASB 7 to include information that will enable users of an entity’s financial statements to evaluate the effect or potential effect of netting arrangements, including rights of set off associated with the entity’s recognised financial assets and recognised financial liabilities, on the entity’s financial position.

This standard also amends AASB 132 to refer to the additional disclosures added to AASB 7 by this standard.

Impact

Public sector not-for-profit entities would rarely enter into netting arrangements. The Department of SA Service Delivery has no such arrangements - accordingly the disclosure requirements have not been included in the Model Financial Statements for not-for-profit entities.

AASB 2012-4 Amendments to Australian Accounting Standards – Government Loans [AASB 1]

This standard amends AASB 1 to require first time adopts to apply the requirement in ASB 139 and AASB 120 prospectively to government loans existing at the date of transition to Australian Accounting Standards.

Impact

Entities apply AASB 1 on first-time adoption. As public sector not-for-profit entities, have adopted Australian equivalents to International Financial Reporting Standards, the amendments will not have an impact and have not been included in the Model Financial Statements for not-for-profit entities.

AASB 2012-5 Amendments to Australian Accounting Standards arising from Annual Improvements 2009-2011 Cycle [AASB 1, 101, 116, 132 and 134 and Interpretation 2]

This amending standard amends the Australian Accounting Standards that are equivalent to those made by the IASB under its program of annual improvements. A number of the amendments are largely technical and clarify particular terms.

AASB 1 – first time adopters can elect to apply the requirements of AASB 123 Borrowing Costs from the date of transition or from an earlier date.

AASB 101 –amendments clarity the requirements for comparative information in respective of the preceding period ie information is presented rather than disclosed.

AASB 116 – amendments clarify that spare parts, stand by equipment, and servicing equipment is capitalised when it meets the definition of an asset.

AASB 132 – amendments clarify the tax effect of distribution to owners.

AASB 134 –amendments clarify the requirements for comparative information in respect of the preceding period ie information is presented rather than disclosed.

Impact

The amendments are minor in nature and will not have an impact on the Department for SA Service Delivery. Consequently they have not been included in the Model Financial Statements for not-for-profit entities.

Department for SA Service Delivery

18

AASB 2012-7 Amendments to Australian Accounting Standards arising from Reduced Disclosure Requirements [AASB 7, 12, 101 and 127]

This standard amends the accounting standards listed above to include reduced disclosure requirements into the standard for entities applying AASB 1053’s Tier 2 requirements.

Impact

In accordance with APF II, all not-for-profit entities that are consolidated into the whole of government financial statements must apply AASB 1053’s Tier 1 Australian Accounting Standards reporting requirements.

Consequently the amendments will not have an impact and have not been included in the Model Financial Statements for not-for-profit entities.

AASB 2012-9 Amendments to AASB 1048 arising from the withdrawal of Australian Interpretation 1039

This standard amends AASB 1048 Interpretation of Standards as a consequence of the withdrawal of Interpretation 1039 Substantive Enactment of Major Tax Bills in Australia.

Impact

This amending standard will not have an impact on the Department for SA Service Delivery and has not been included in the Model Financial Statements for not-for-profit entities.

AASB 2012-10 Amendments to Australian Accounting Standards – Transition Guidance and other amendments [AASB 1, 5, 7, 8 ,10, 11, 12, 13, 101, 102, 108, 112, 118, 119, 127, 128, 132, 133, 134, 137, 1023, 1038, 1039 and 1049 and Interpretation 12]

This standard amends those accounting standards and interpretations listed above. The amendments arise from:

The release of IFRS Consolidated Financial Statements, Joint Arrangements and Disclosure of Interest in Other Entities;

The decision by the AASB to defer the mandatory application of AASB 10 Consolidated Financial Statements and related standards to not-for-profit entities until annual reporting periods beginning on or after 1 Jan 2014;

Editorial corrections made by the IASB to its standards and interpretations and AASB to its pronouncements.

Impact

The amendments are minor in nature and will not have an impact on the Department for SA Service Delivery and have not been included in the Model Financial Statements for not-for-profit entities.

Department for SA Service Delivery

19

AASB 2012-11 Amendments to Australian Accounting Standards - Reduced Disclosure Requirements and other amendments [AASB 1, 2, 8, 10, 107, 128, 133 and 134]

This standard makes various editorial corrections to Australian Accounting Standards – Reduced Disclosure Requirements (Tier 2). In addition these amendments provide relief from consolidation and the equity method when the parent, investor or joint venture: is an entity complying with Tier 2 requirements; has an ultimate or intermediate parent that prepares consolidated financial statements; and meets certain criteria specified in ASB 10 and AASB 128.

Impact

In accordance with APF II, all not-for-profit entities that are consolidated into the whole of government financial statements must apply AASB 1053’s Tier 1 Australian Accounting Standards reporting requirements.

Consequently the amendments will not have an impact and have not been included in the Model Financial Statements for not-for-profit entities.

AASB 2013-2 Amendments to AASB 1038 – Regulatory Capital

This standard amends AASB 1038 as a consequence of changes in the APRA reporting requirements relating to life insurers.

Impact

AASB 1038 does not apply to general purpose financial statements of not-for-profit public sector entities. Accordingly the amendments will not have an impact and have not been included in the Model Financial Statements for not-for-profit entities.

AASB CF 2013-1 Amendments to the Australian Conceptual Framework

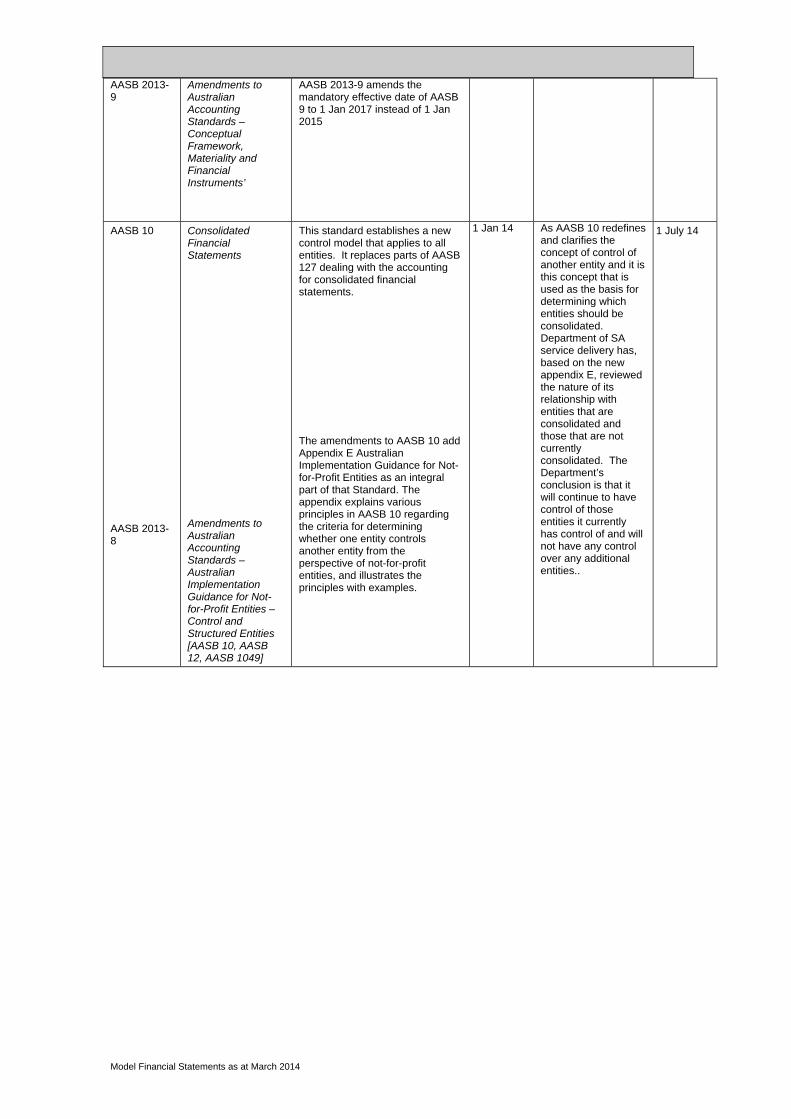

This amending standard revises guidance including a restatement of the objective of general purpose financial reporting, and reconsideration of the qualitative characteristics that identify useful financial information. Consequential amendments to Accounting Standards (including Interpretations) arising from these revisions are made in Accounting Standard AASB 2013-9 Amendments to Australian Accounting Standards – Conceptual Framework, Materiality and Financial Instruments.

Consequently the previous guidance on the objective and the qualitative characteristics of financial statements available in Statement of Accounting Concepts SAC 2 Objective of General Purpose Financial Reporting is now superseded.

Impact

The amendments are minor in nature and will not have an impact on the Department for SA Service Delivery and have not been included in the Model Financial Statements for not-for-profit entities.

Department for SA Service Delivery

20

Independent Auditor’s Report To the Chief Executive

(Insert Auditor’s Opinion)

S O’Neill AUDITOR-GENERAL August 2014

REPORT OF THE AUDITOR-GENERAL

Section 23(1) of the Public Finance and Audit Act 1987 requires each public authority, within 42 days after the end of the financial year of the public authority, to deliver to the Auditor-General financial statements relating to that financial year that comply with the Treasurer’s Instructions.

Department for SA Service Delivery

21

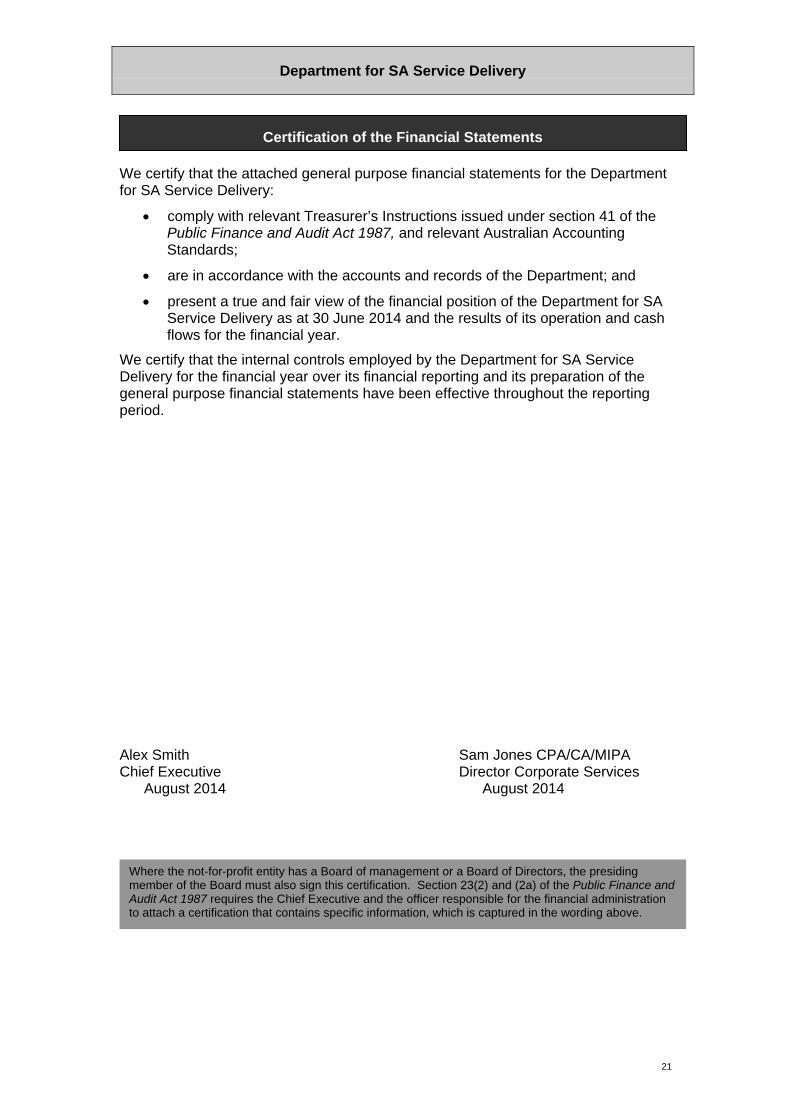

We certify that the attached general purpose financial statements for the Department for SA Service Delivery:

comply with relevant Treasurer’s Instructions issued under section 41 of the Public Finance and Audit Act 1987, and relevant Australian Accounting Standards;

are in accordance with the accounts and records of the Department; and

present a true and fair view of the financial position of the Department for SA Service Delivery as at 30 June 2014 and the results of its operation and cash flows for the financial year.

We certify that the internal controls employed by the Department for SA Service Delivery for the financial year over its financial reporting and its preparation of the general purpose financial statements have been effective throughout the reporting period.

Alex Smith Sam Jones CPA/CA/MIPA Chief Executive Director Corporate Services August 2014 August 2014

Certification of the Financial Statements

Where the not-for-profit entity has a Board of management or a Board of Directors, the presiding member of the Board must also sign this certification. Section 23(2) and (2a) of the Public Finance and Audit Act 1987 requires the Chief Executive and the officer responsible for the financial administration to attach a certification that contains specific information, which is captured in the wording above.

Department for SA Service Delivery

22

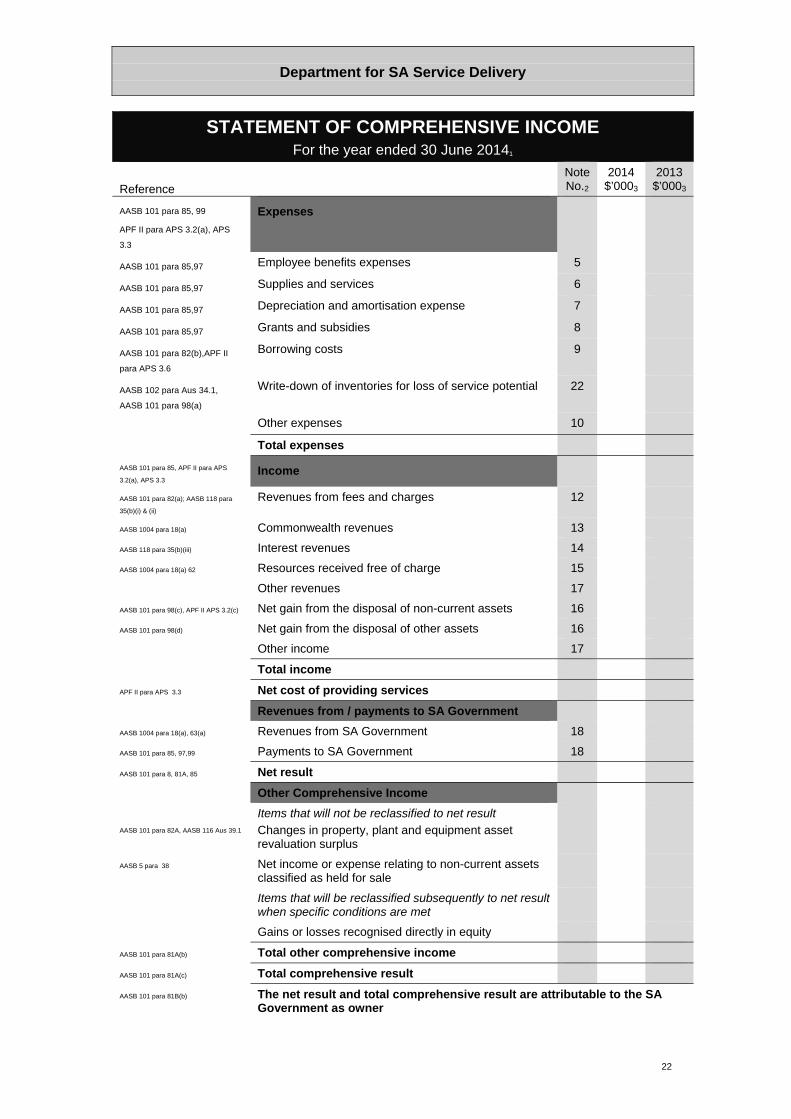

STATEMENT OF COMPREHENSIVE INCOME For the year ended 30 June 20141

Reference Note No.2

2014 $’0003

2013$’0003

AASB 101 para 85, 99

APF II para APS 3.2(a), APS

3.3

Expenses

AASB 101 para 85,97 Employee benefits expenses 5

AASB 101 para 85,97 Supplies and services 6

AASB 101 para 85,97 Depreciation and amortisation expense 7

AASB 101 para 85,97 Grants and subsidies 8

AASB 101 para 82(b),APF II

para APS 3.6

Borrowing costs 9

AASB 102 para Aus 34.1,

AASB 101 para 98(a)

Write-down of inventories for loss of service potential 22

Other expenses 10

Total expenses

AASB 101 para 85, APF II para APS

3.2(a), APS 3.3 Income

AASB 101 para 82(a); AASB 118 para

35(b)(i) & (ii)

Revenues from fees and charges 12

AASB 1004 para 18(a) Commonwealth revenues 13

AASB 118 para 35(b)(iii) Interest revenues 14

AASB 1004 para 18(a) 62 Resources received free of charge 15

Other revenues 17

AASB 101 para 98(c), APF II APS 3.2(c) Net gain from the disposal of non-current assets 16

AASB 101 para 98(d) Net gain from the disposal of other assets 16

Other income 17

Total income

APF II para APS 3.3 Net cost of providing services

Revenues from / payments to SA Government

AASB 1004 para 18(a), 63(a) Revenues from SA Government 18

AASB 101 para 85, 97,99 Payments to SA Government 18

AASB 101 para 8, 81A, 85 Net result

Other Comprehensive Income

AASB 101 para 82A, AASB 116 Aus 39.1

Items that will not be reclassified to net result

Changes in property, plant and equipment asset revaluation surplus

AASB 5 para 38 Net income or expense relating to non-current assets classified as held for sale

Items that will be reclassified subsequently to net result when specific conditions are met

Gains or losses recognised directly in equity

AASB 101 para 81A(b) Total other comprehensive income

AASB 101 para 81A(c) Total comprehensive result

AASB 101 para 81B(b) The net result and total comprehensive result are attributable to the SA Government as owner

Department for SA Service Delivery

23

The above statement should be read in conjunction with the accompanying notes.

Note that if a not-for-profit entity has no amounts applicable to any individual item, these items should not be included in the statement.

1. The name of the entity and reporting date must be identified, required by AASB 101, paragraph 51(a) and (c).

2. AASB 101, paragraph 113 requires notes to be presented systematically and each item to be cross-referenced to any related information in the notes.

3. The rounding used in the financial report must be identified, required by AASB 101, paragraph 51(e).

Department for SA Service Delivery

24

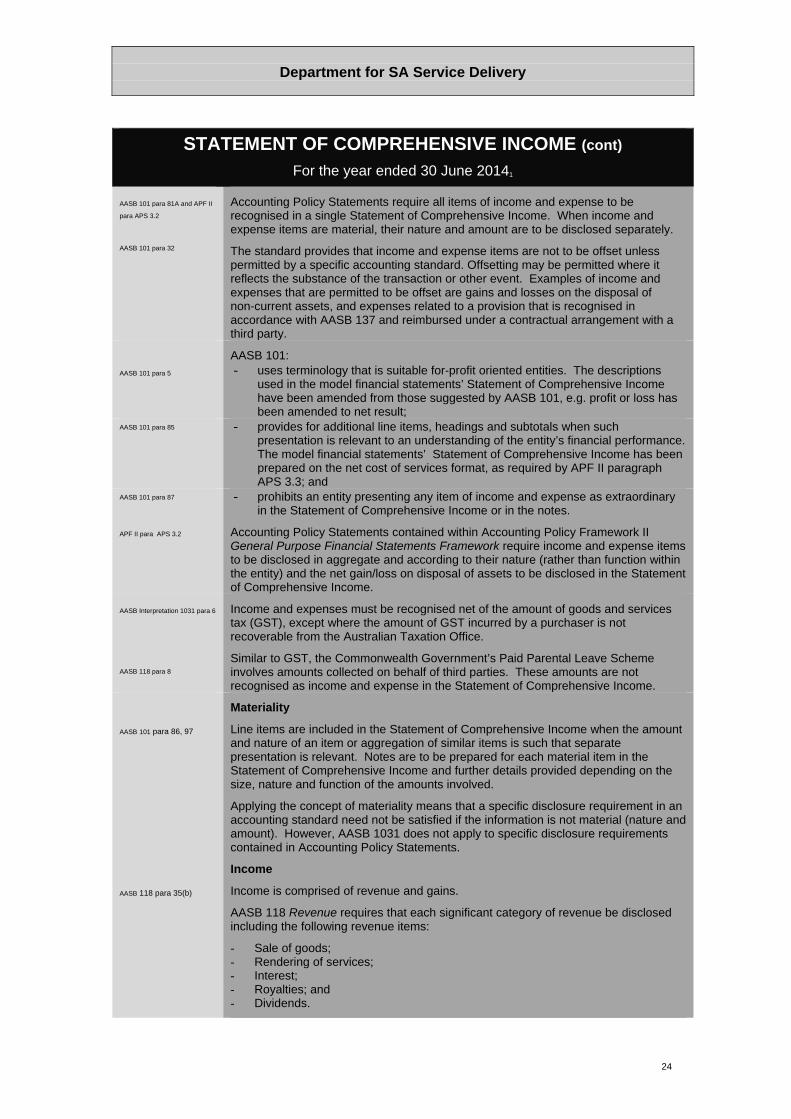

STATEMENT OF COMPREHENSIVE INCOME (cont) For the year ended 30 June 20141

AASB 101 para 81A and APF II

para APS 3.2 Accounting Policy Statements require all items of income and expense to be recognised in a single Statement of Comprehensive Income. When income and expense items are material, their nature and amount are to be disclosed separately.

AASB 101 para 32 The standard provides that income and expense items are not to be offset unless permitted by a specific accounting standard. Offsetting may be permitted where it reflects the substance of the transaction or other event. Examples of income and expenses that are permitted to be offset are gains and losses on the disposal of non-current assets, and expenses related to a provision that is recognised in accordance with AASB 137 and reimbursed under a contractual arrangement with a third party.

AASB 101 para 5

AASB 101: - uses terminology that is suitable for-profit oriented entities. The descriptions

used in the model financial statements’ Statement of Comprehensive Income have been amended from those suggested by AASB 101, e.g. profit or loss has been amended to net result;

AASB 101 para 85 - provides for additional line items, headings and subtotals when such presentation is relevant to an understanding of the entity’s financial performance. The model financial statements’ Statement of Comprehensive Income has been prepared on the net cost of services format, as required by APF II paragraph APS 3.3; and

AASB 101 para 87 - prohibits an entity presenting any item of income and expense as extraordinary in the Statement of Comprehensive Income or in the notes.

APF II para APS 3.2 Accounting Policy Statements contained within Accounting Policy Framework II General Purpose Financial Statements Framework require income and expense items to be disclosed in aggregate and according to their nature (rather than function within the entity) and the net gain/loss on disposal of assets to be disclosed in the Statement of Comprehensive Income.

AASB Interpretation 1031 para 6

AASB 118 para 8

Income and expenses must be recognised net of the amount of goods and services tax (GST), except where the amount of GST incurred by a purchaser is not recoverable from the Australian Taxation Office.

Similar to GST, the Commonwealth Government’s Paid Parental Leave Scheme involves amounts collected on behalf of third parties. These amounts are not recognised as income and expense in the Statement of Comprehensive Income.

AASB 101 para 86, 97

Materiality

Line items are included in the Statement of Comprehensive Income when the amount and nature of an item or aggregation of similar items is such that separate presentation is relevant. Notes are to be prepared for each material item in the Statement of Comprehensive Income and further details provided depending on the size, nature and function of the amounts involved.

Applying the concept of materiality means that a specific disclosure requirement in an accounting standard need not be satisfied if the information is not material (nature and amount). However, AASB 1031 does not apply to specific disclosure requirements contained in Accounting Policy Statements.

AASB 118 para 35(b)

Income

Income is comprised of revenue and gains.

AASB 118 Revenue requires that each significant category of revenue be disclosed including the following revenue items:

- Sale of goods; - Rendering of services; - Interest; - Royalties; and - Dividends.

Department for SA Service Delivery

25

STATEMENT OF COMPREHENSIVE INCOME (cont) For the year ended 30 June 20141

AASB 1004 Contributions requires asset contributions, forgiveness of liabilities, appropriations, liabilities assumed, goods and services received free of charge to be disclosed.

Note: the line item ‘other revenue’ should not exceed 10% of the total value of revenues.

Gains are displayed separately to revenue in the Statement of Comprehensive Income. Generally gains are reported net of related expenses e.g. gain on sale of property, plant and equipment; gain on contributed assets; gain on investment. The line item ‘other income’ will be used where a specific standard prohibits the item being classified as revenue (e.g. AASB 138, paragraph 113 de-recognition of an intangible asset), the amount is immaterial and does not warrant an additional descriptive line item in the Statement of Comprehensive Income.

AASB 101 para 100

Expenses

AASB 101 encourages entities to disclose expenses aggregated in the Statement of Comprehensive Income with further detail in the notes. Accounting standards require borrowing costs to be disclosed separately.

It is considered best practice that income and expenses disclosed in the Statement of Comprehensive Income are reconciled to the detailed categorisations of income and expenses contained in the notes unless these disclosures are presented in the Statement of Comprehensive Income.

‘Payments to government’ may include the return of surplus cash pursuant to the cash alignment policy, income tax equivalent payments, or other payments made directly to the Consolidated Account. It is unlikely that not-for-profit entities will pay a dividend to the Treasurer as dividends are payments from profit. Not-for-profit entities generally do not make a profit but rather receive appropriation or earn income to cover the cost of providing services. However, if a ‘dividend’ was made, it would be included here.

Note: the line item ‘other expenses’ should not exceed 10% of the total value of expenses.

Other information

The reference column in the Statement of Comprehensive Income is for information only and should not be replicated in not-for-profit entities’ financial statements.

Paragraph 19.7 of Treasurer’s Instruction 19 Financial Reporting provides that in the event of any inconsistency between an accounting policy statement issued by the Treasurer pursuant to that instruction and an Australian accounting standard, the requirements of the accounting policy statement will prevail.

Department for SA Service Delivery

26

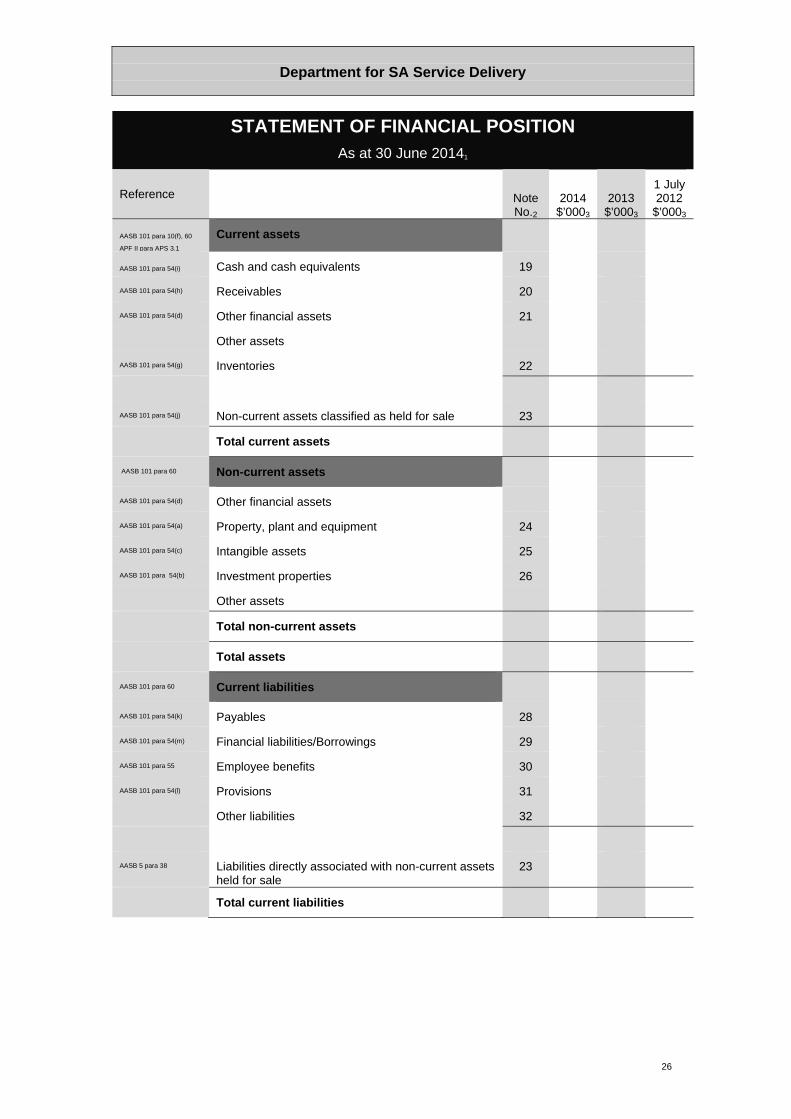

STATEMENT OF FINANCIAL POSITION As at 30 June 20141

Reference

NoteNo.2

2014 $’0003

2013 $’0003

1 July 2012

$’0003

AASB 101 para 10(f), 60

APF II para APS 3.1 Current assets

AASB 101 para 54(i) Cash and cash equivalents 19 AASB 101 para 54(h) Receivables 20 AASB 101 para 54(d) Other financial assets 21 Other assets AASB 101 para 54(g) Inventories 22 AASB 101 para 54(j) Non-current assets classified as held for sale 23 Total current assets

AASB 101 para 60 Non-current assets

AASB 101 para 54(d) Other financial assets AASB 101 para 54(a) Property, plant and equipment 24 AASB 101 para 54(c) Intangible assets 25 AASB 101 para 54(b) Investment properties 26

Other assets

Total non-current assets

Total assets

AASB 101 para 60 Current liabilities

AASB 101 para 54(k) Payables 28 AASB 101 para 54(m) Financial liabilities/Borrowings 29 AASB 101 para 55 Employee benefits 30 AASB 101 para 54(l) Provisions 31 Other liabilities 32

AASB 5 para 38 Liabilities directly associated with non-current assets

held for sale 23

Total current liabilities

Department for SA Service Delivery

27

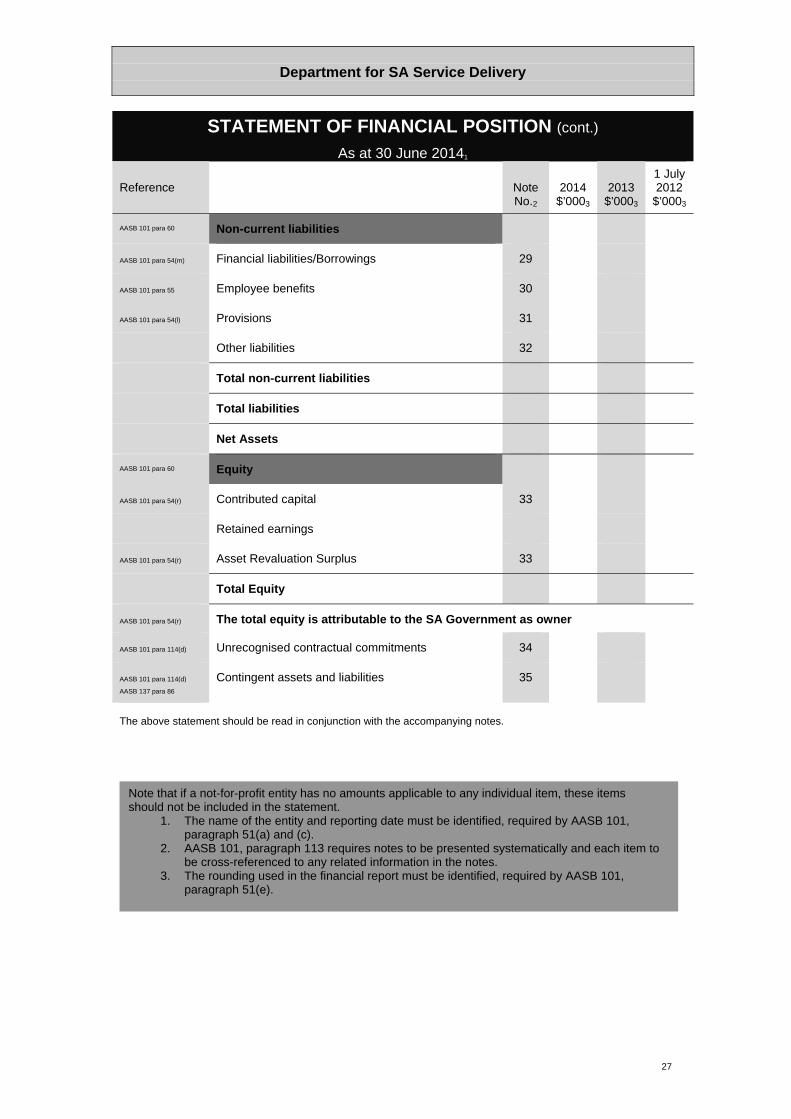

The above statement should be read in conjunction with the accompanying notes.

STATEMENT OF FINANCIAL POSITION (cont.) As at 30 June 20141

Reference

NoteNo.2

2014 $’0003

2013 $’0003

1 July 2012

$’0003

AASB 101 para 60 Non-current liabilities

AASB 101 para 54(m) Financial liabilities/Borrowings 29

AASB 101 para 55 Employee benefits 30

AASB 101 para 54(l) Provisions 31

Other liabilities 32

Total non-current liabilities

Total liabilities

Net Assets

AASB 101 para 60 Equity

AASB 101 para 54(r) Contributed capital 33

Retained earnings

AASB 101 para 54(r) Asset Revaluation Surplus 33

Total Equity

AASB 101 para 54(r) The total equity is attributable to the SA Government as owner

AASB 101 para 114(d) Unrecognised contractual commitments 34

AASB 101 para 114(d)

AASB 137 para 86

Contingent assets and liabilities 35

Note that if a not-for-profit entity has no amounts applicable to any individual item, these items should not be included in the statement.

1. The name of the entity and reporting date must be identified, required by AASB 101, paragraph 51(a) and (c).

2. AASB 101, paragraph 113 requires notes to be presented systematically and each item to be cross-referenced to any related information in the notes.

3. The rounding used in the financial report must be identified, required by AASB 101, paragraph 51(e).

Department for SA Service Delivery

28

STATEMENT OF FINANCIAL POSITION (cont.) As at 30 June 20141

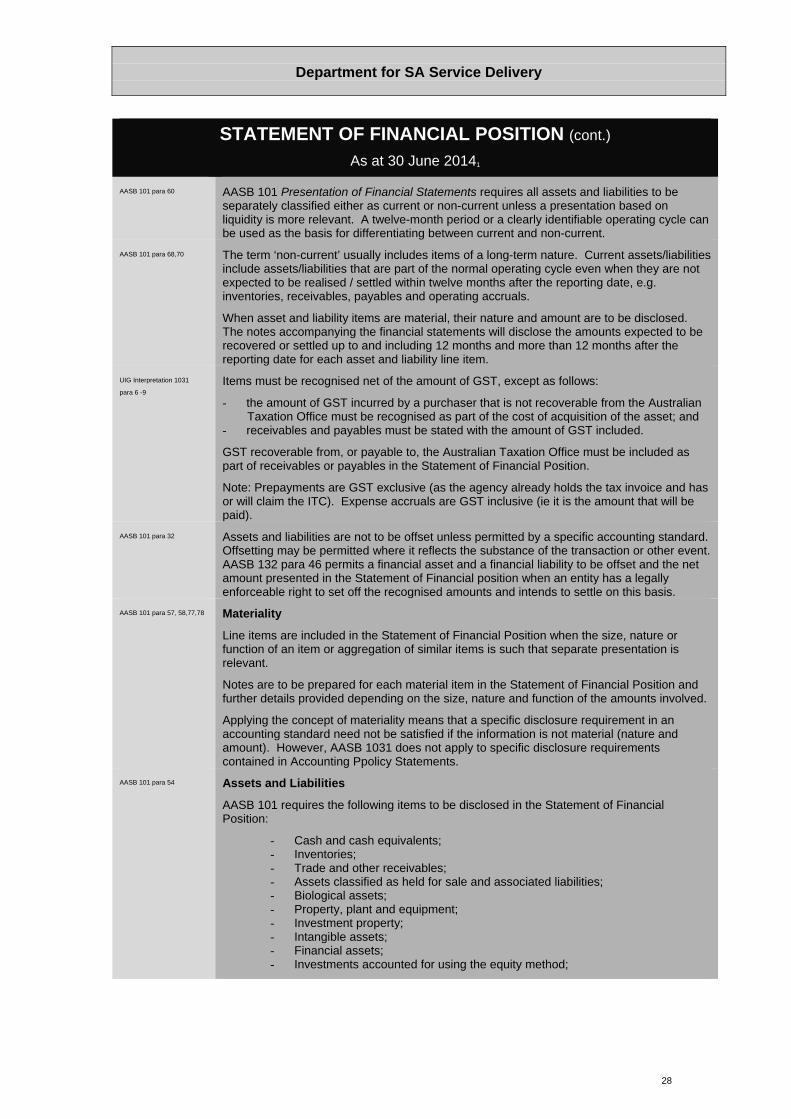

AASB 101 para 60 AASB 101 Presentation of Financial Statements requires all assets and liabilities to be separately classified either as current or non-current unless a presentation based on liquidity is more relevant. A twelve-month period or a clearly identifiable operating cycle can be used as the basis for differentiating between current and non-current.

AASB 101 para 68,70 The term ‘non-current’ usually includes items of a long-term nature. Current assets/liabilities include assets/liabilities that are part of the normal operating cycle even when they are not expected to be realised / settled within twelve months after the reporting date, e.g. inventories, receivables, payables and operating accruals.

When asset and liability items are material, their nature and amount are to be disclosed. The notes accompanying the financial statements will disclose the amounts expected to be recovered or settled up to and including 12 months and more than 12 months after the reporting date for each asset and liability line item.

UIG Interpretation 1031

para 6 -9

Items must be recognised net of the amount of GST, except as follows:

- the amount of GST incurred by a purchaser that is not recoverable from the Australian Taxation Office must be recognised as part of the cost of acquisition of the asset; and

- receivables and payables must be stated with the amount of GST included.

GST recoverable from, or payable to, the Australian Taxation Office must be included as part of receivables or payables in the Statement of Financial Position.

Note: Prepayments are GST exclusive (as the agency already holds the tax invoice and has or will claim the ITC). Expense accruals are GST inclusive (ie it is the amount that will be paid).

AASB 101 para 32 Assets and liabilities are not to be offset unless permitted by a specific accounting standard. Offsetting may be permitted where it reflects the substance of the transaction or other event. AASB 132 para 46 permits a financial asset and a financial liability to be offset and the net amount presented in the Statement of Financial position when an entity has a legally enforceable right to set off the recognised amounts and intends to settle on this basis.

AASB 101 para 57, 58,77,78 Materiality

Line items are included in the Statement of Financial Position when the size, nature or function of an item or aggregation of similar items is such that separate presentation is relevant.

Notes are to be prepared for each material item in the Statement of Financial Position and further details provided depending on the size, nature and function of the amounts involved.

Applying the concept of materiality means that a specific disclosure requirement in an accounting standard need not be satisfied if the information is not material (nature and amount). However, AASB 1031 does not apply to specific disclosure requirements contained in Accounting Ppolicy Statements.

AASB 101 para 54 Assets and Liabilities

AASB 101 requires the following items to be disclosed in the Statement of Financial Position:

- Cash and cash equivalents; - Inventories; - Trade and other receivables; - Assets classified as held for sale and associated liabilities; - Biological assets; - Property, plant and equipment; - Investment property; - Intangible assets; - Financial assets; - Investments accounted for using the equity method;

Department for SA Service Delivery

29

STATEMENT OF FINANCIAL POSITION (cont.) As at 30 June 20141

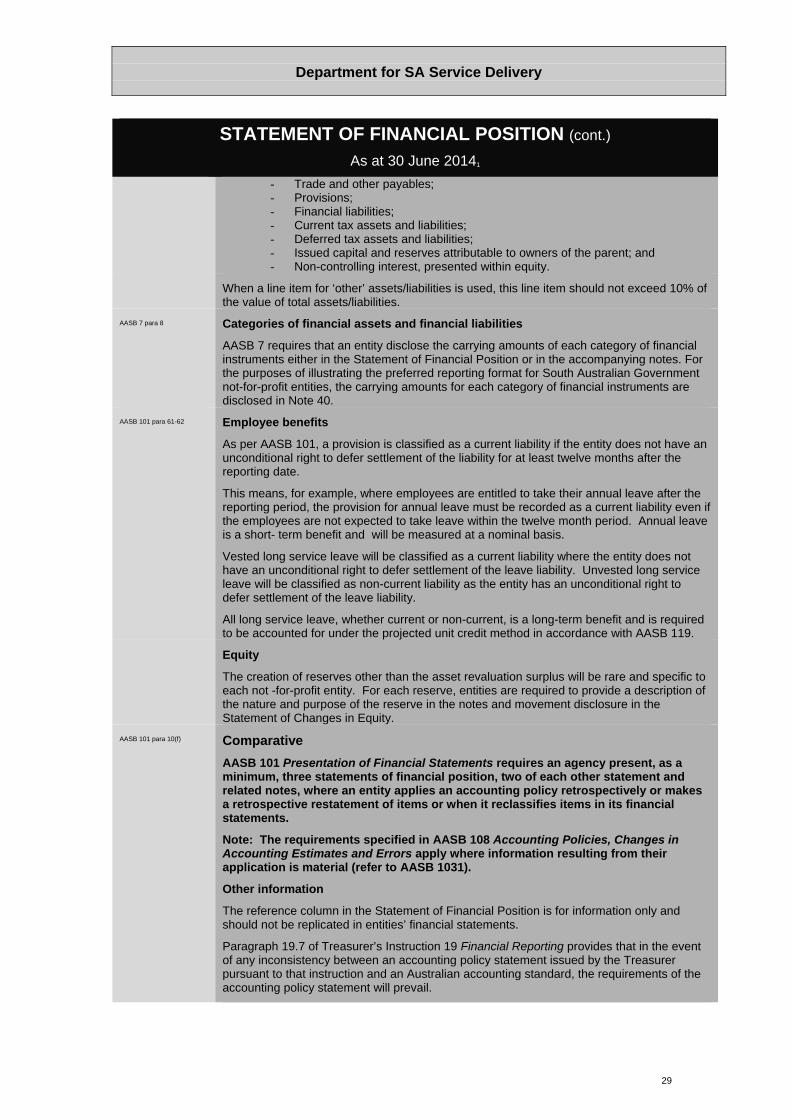

- Trade and other payables; - Provisions; - Financial liabilities; - Current tax assets and liabilities; - Deferred tax assets and liabilities; - Issued capital and reserves attributable to owners of the parent; and - Non-controlling interest, presented within equity.

When a line item for ‘other’ assets/liabilities is used, this line item should not exceed 10% of the value of total assets/liabilities.

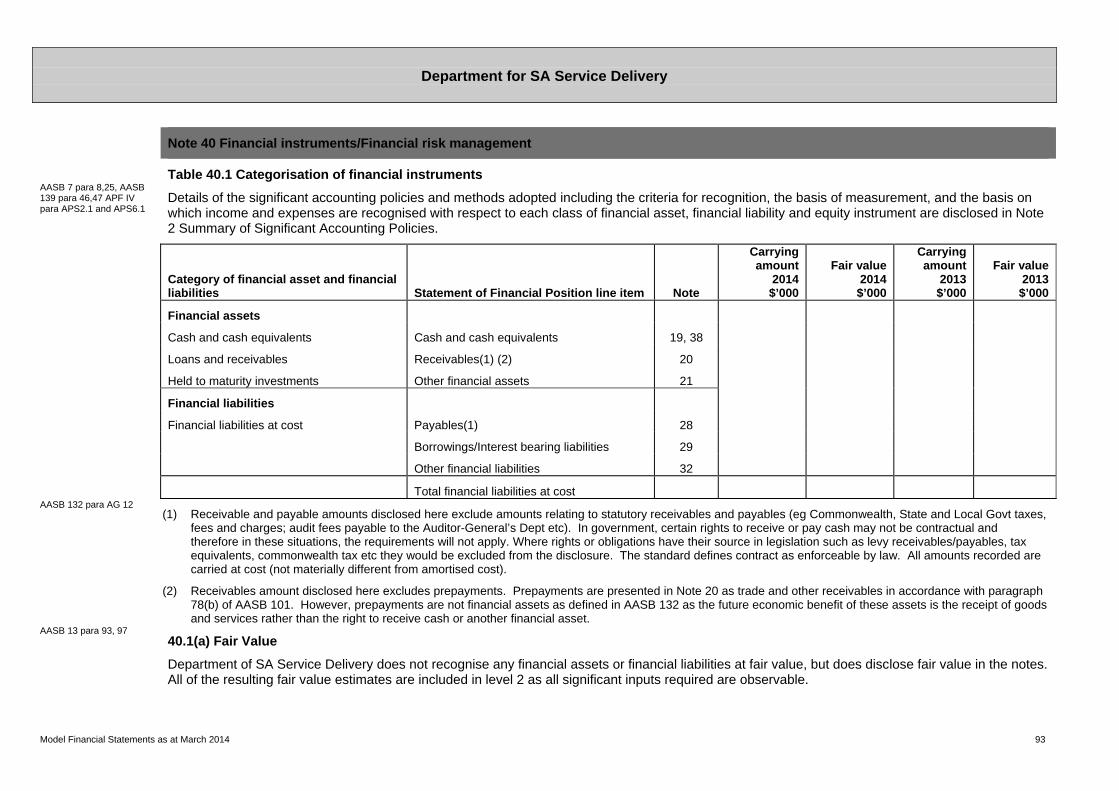

AASB 7 para 8 Categories of financial assets and financial liabilities

AASB 7 requires that an entity disclose the carrying amounts of each category of financial instruments either in the Statement of Financial Position or in the accompanying notes. For the purposes of illustrating the preferred reporting format for South Australian Government not-for-profit entities, the carrying amounts for each category of financial instruments are disclosed in Note 40.

AASB 101 para 61-62 Employee benefits

As per AASB 101, a provision is classified as a current liability if the entity does not have an unconditional right to defer settlement of the liability for at least twelve months after the reporting date.

This means, for example, where employees are entitled to take their annual leave after the reporting period, the provision for annual leave must be recorded as a current liability even if the employees are not expected to take leave within the twelve month period. Annual leave is a short- term benefit and will be measured at a nominal basis.

Vested long service leave will be classified as a current liability where the entity does not have an unconditional right to defer settlement of the leave liability. Unvested long service leave will be classified as non-current liability as the entity has an unconditional right to defer settlement of the leave liability.

All long service leave, whether current or non-current, is a long-term benefit and is required to be accounted for under the projected unit credit method in accordance with AASB 119.

Equity

The creation of reserves other than the asset revaluation surplus will be rare and specific to each not -for-profit entity. For each reserve, entities are required to provide a description of the nature and purpose of the reserve in the notes and movement disclosure in the Statement of Changes in Equity.

AASB 101 para 10(f) Comparative

AASB 101 Presentation of Financial Statements requires an agency present, as a minimum, three statements of financial position, two of each other statement and related notes, where an entity applies an accounting policy retrospectively or makes a retrospective restatement of items or when it reclassifies items in its financial statements.

Note: The requirements specified in AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors apply where information resulting from their application is material (refer to AASB 1031).

Other information

The reference column in the Statement of Financial Position is for information only and should not be replicated in entities’ financial statements.

Paragraph 19.7 of Treasurer’s Instruction 19 Financial Reporting provides that in the event of any inconsistency between an accounting policy statement issued by the Treasurer pursuant to that instruction and an Australian accounting standard, the requirements of the accounting policy statement will prevail.

Department for SA Service Delivery

30

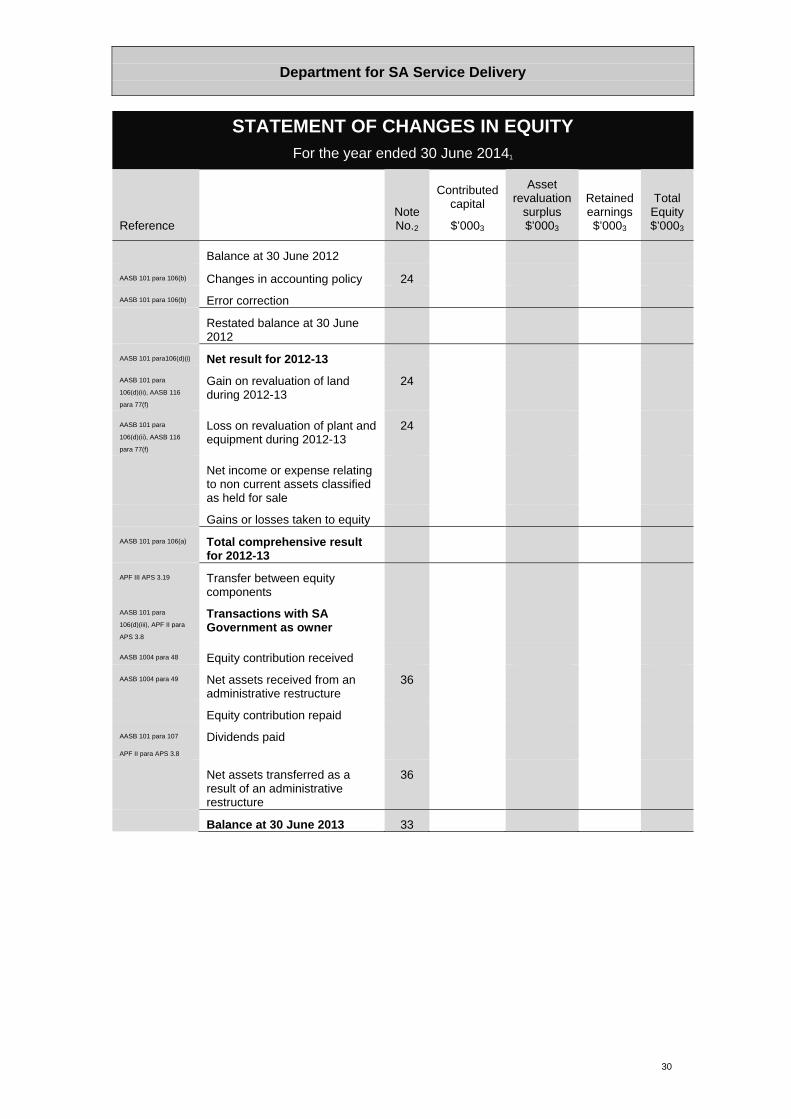

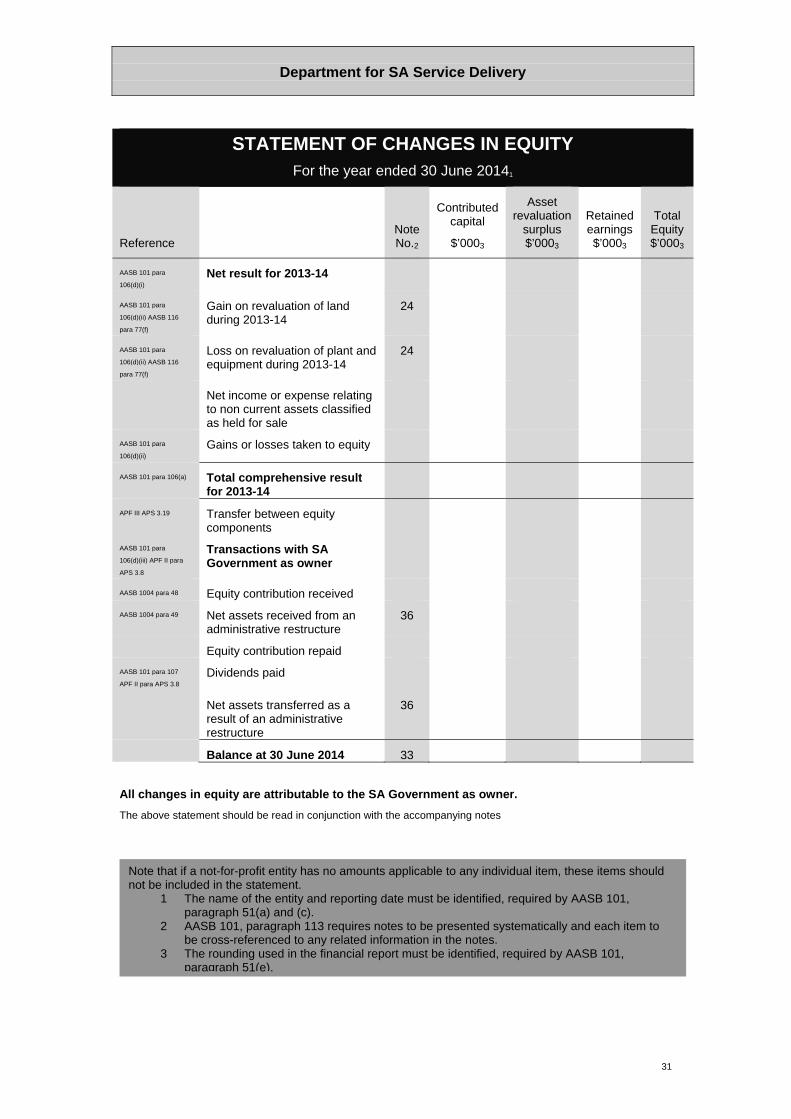

STATEMENT OF CHANGES IN EQUITY For the year ended 30 June 20141

Reference NoteNo.2

Contributed capital

$’0003

Asset revaluation

surplus $’0003

Retained earnings $’0003

Total Equity$’0003

Balance at 30 June 2012

AASB 101 para 106(b) Changes in accounting policy 24

AASB 101 para 106(b) Error correction

Restated balance at 30 June 2012

AASB 101 para106(d)(i) Net result for 2012-13

AASB 101 para

106(d)(ii), AASB 116

para 77(f)

Gain on revaluation of land during 2012-13

24

AASB 101 para

106(d)(ii), AASB 116

para 77(f)

Loss on revaluation of plant and equipment during 2012-13

24

Net income or expense relating to non current assets classified as held for sale

Gains or losses taken to equity

AASB 101 para 106(a) Total comprehensive result for 2012-13

APF III APS 3.19

AASB 101 para

106(d)(iii), APF II para

APS 3.8

Transfer between equity components

Transactions with SA Government as owner

AASB 1004 para 48 Equity contribution received

AASB 1004 para 49 Net assets received from an administrative restructure

36

Equity contribution repaid

AASB 101 para 107

APF II para APS 3.8

Dividends paid

Net assets transferred as a result of an administrative restructure

36

Balance at 30 June 2013 33

Department for SA Service Delivery

31

STATEMENT OF CHANGES IN EQUITY For the year ended 30 June 20141

Reference NoteNo.2

Contributed capital

$’0003

Asset revaluation

surplus $’0003

Retained earnings $’0003

Total Equity$’0003

AASB 101 para

106(d)(i)

Net result for 2013-14

AASB 101 para

106(d)(ii) AASB 116

para 77(f)

Gain on revaluation of land during 2013-14

24

AASB 101 para

106(d)(ii) AASB 116

para 77(f)

Loss on revaluation of plant and equipment during 2013-14

24

Net income or expense relating to non current assets classified as held for sale

AASB 101 para

106(d)(ii)

Gains or losses taken to equity

AASB 101 para 106(a) Total comprehensive result for 2013-14

APF III APS 3.19

AASB 101 para

106(d)(iii) APF II para

APS 3.8

Transfer between equity components

Transactions with SA Government as owner

AASB 1004 para 48 Equity contribution received

AASB 1004 para 49 Net assets received from an administrative restructure

36

Equity contribution repaid

AASB 101 para 107

APF II para APS 3.8

Dividends paid

Net assets transferred as a result of an administrative restructure

36

Balance at 30 June 2014 33

All changes in equity are attributable to the SA Government as owner.

The above statement should be read in conjunction with the accompanying notes

Note that if a not-for-profit entity has no amounts applicable to any individual item, these items should not be included in the statement.

1 The name of the entity and reporting date must be identified, required by AASB 101, paragraph 51(a) and (c).

2 AASB 101, paragraph 113 requires notes to be presented systematically and each item to be cross-referenced to any related information in the notes.

3 The rounding used in the financial report must be identified, required by AASB 101, paragraph 51(e).

Department for SA Service Delivery

32

STATEMENT OF CHANGES IN EQUITY (cont.) For the year ended 30 June 20141

AASB 101 para 106-110

In accordance with AASB 101 Presentation of Financial Statements an entity is required to disclose in the Statement of Changes in Equity:

- Total comprehensive result for the period, showing separately total amounts attributable to owners and non-controlling interests;

- For each component of equity, the effects of retrospective application or retrospective restatements recognised;

- The amounts of transactions with owners in their capacity as owners, showing separately contributions by and distributions to owners; and

- For each component of equity, reconciliation between the carrying amount at the beginning and the end of the period, separately disclosing each change.

The APF II APS 3.8 requires analysis of other comprehensive income by item and transactions with the State Government as owner, including dividends to be presented in the Statement of Changes in Equity rather than the notes.

In accordance with the revised AASB 1004 Contributions restructure of administrative arrangements are in the nature of transactions with owners in their capacity as owners and accordingly are presented in the Statement of Changes in Equity rather than recognised as a net revenue or expense through profit and loss.

The reference column in the Statement of Changes in Equity is for information only and should not be replicated in not-for-profit entities’ financial statements.

Separate line items shown in the Statement of Changes in Equity need not be included unless they are material and relevant to the circumstances of the entity.

Paragraph 19.7 of Treasurer’s Instruction 19 Financial Reporting provides that in the event of any inconsistency between an accounting policy statement issued by the Treasurer pursuant to that instruction and an Australian accounting standard, the requirements of the Accounting Policy Statement will prevail.

Department for SA Service Delivery

33

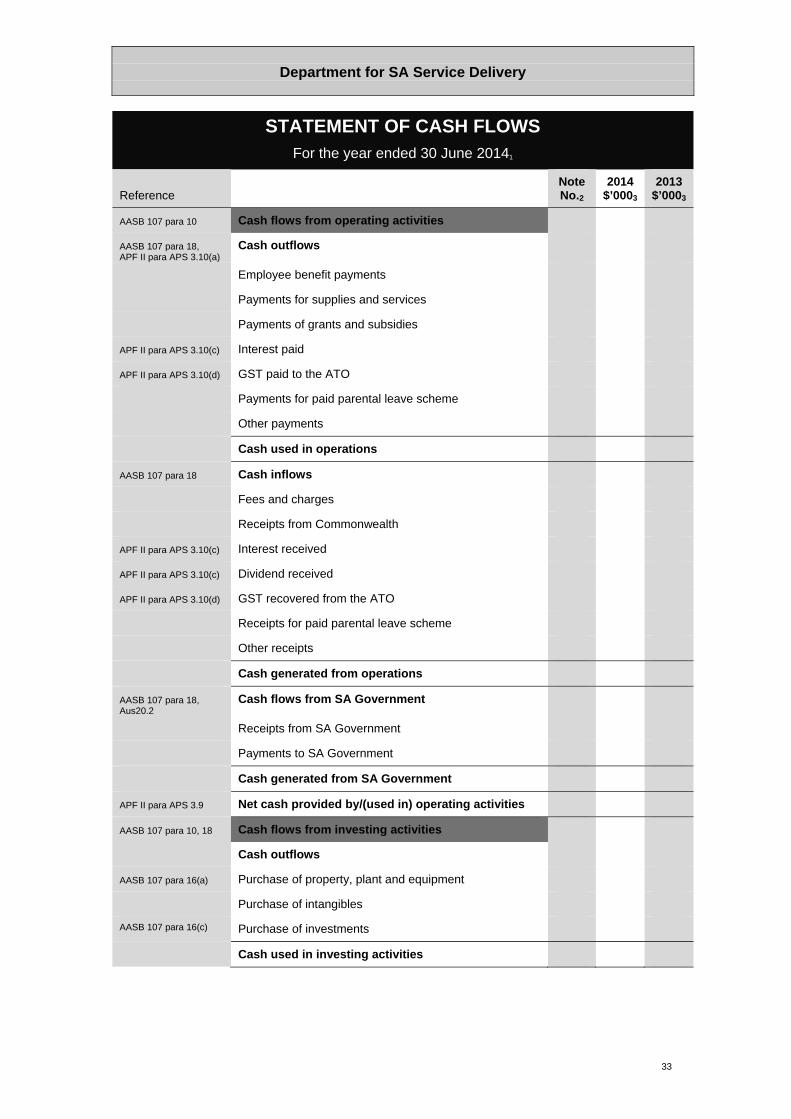

STATEMENT OF CASH FLOWS For the year ended 30 June 20141

Reference Note No.2

2014 $’0003

2013$’0003

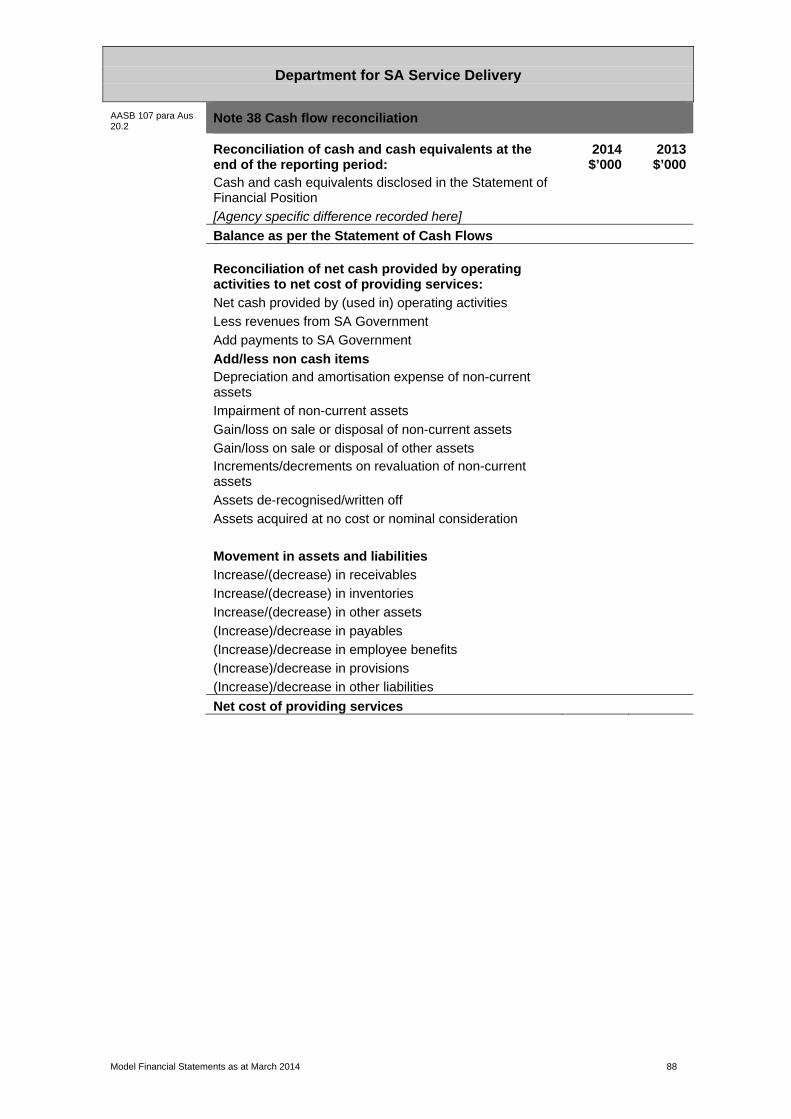

AASB 107 para 10 Cash flows from operating activities AASB 107 para 18, APF II para APS 3.10(a)

Cash outflows

Employee benefit payments Payments for supplies and services Payments of grants and subsidies APF II para APS 3.10(c) Interest paid APF II para APS 3.10(d) GST paid to the ATO Payments for paid parental leave scheme Other payments

Cash used in operations

AASB 107 para 18 Cash inflows Fees and charges Receipts from Commonwealth APF II para APS 3.10(c) Interest received APF II para APS 3.10(c) Dividend received APF II para APS 3.10(d) GST recovered from the ATO Receipts for paid parental leave scheme Other receipts

Cash generated from operations

AASB 107 para 18, Aus20.2

Cash flows from SA Government

Receipts from SA Government Payments to SA Government

Cash generated from SA Government

APF II para APS 3.9 Net cash provided by/(used in) operating activities

AASB 107 para 10, 18 Cash flows from investing activities Cash outflows AASB 107 para 16(a) Purchase of property, plant and equipment Purchase of intangibles AASB 107 para 16(c) Purchase of investments Cash used in investing activities

Department for SA Service Delivery

34

The above statement should be read in conjunction with the accompanying notes.

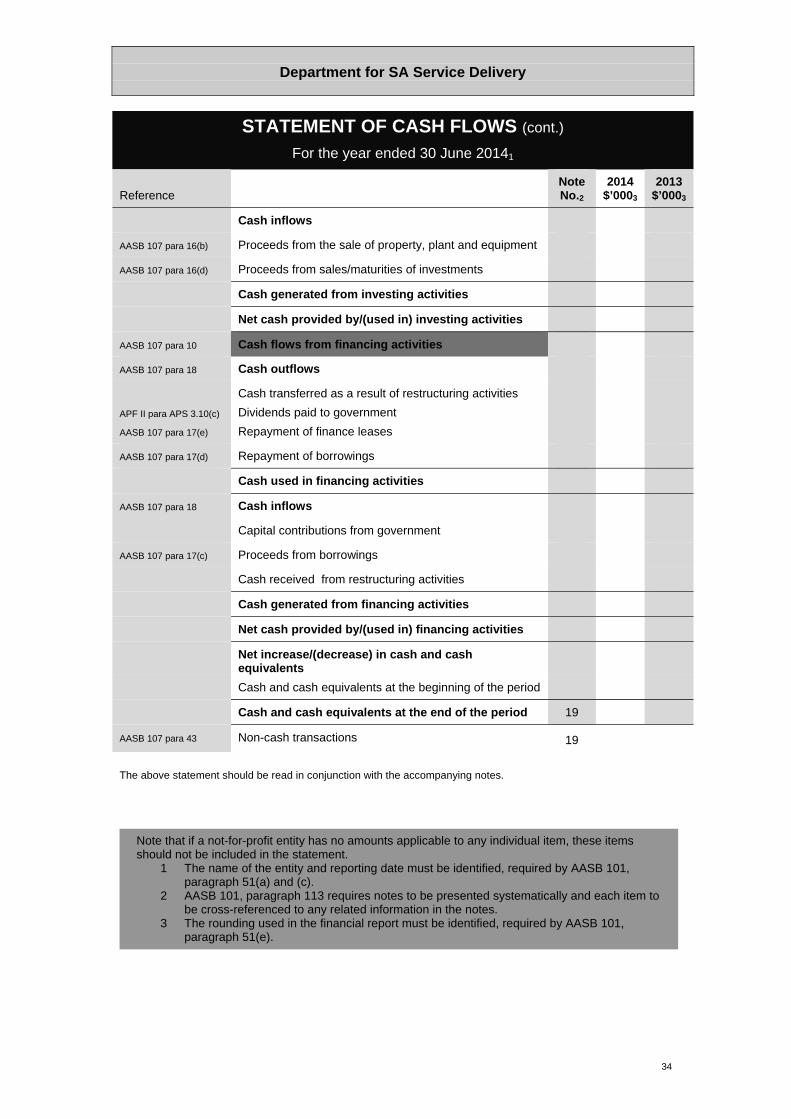

STATEMENT OF CASH FLOWS (cont.) For the year ended 30 June 20141

Reference Note No.2

2014 $’0003

2013$’0003

Cash inflows

AASB 107 para 16(b) Proceeds from the sale of property, plant and equipment

AASB 107 para 16(d) Proceeds from sales/maturities of investments

Cash generated from investing activities

Net cash provided by/(used in) investing activities

AASB 107 para 10 Cash flows from financing activities

AASB 107 para 18 Cash outflows

APF II para APS 3.10(c)

Cash transferred as a result of restructuring activities

Dividends paid to government

AASB 107 para 17(e) Repayment of finance leases

AASB 107 para 17(d) Repayment of borrowings

Cash used in financing activities

AASB 107 para 18 Cash inflows

Capital contributions from government

AASB 107 para 17(c) Proceeds from borrowings

Cash received from restructuring activities

Cash generated from financing activities

Net cash provided by/(used in) financing activities

Net increase/(decrease) in cash and cash equivalents

Cash and cash equivalents at the beginning of the period

Cash and cash equivalents at the end of the period 19

AASB 107 para 43 Non-cash transactions 19

Note that if a not-for-profit entity has no amounts applicable to any individual item, these items should not be included in the statement.

1 The name of the entity and reporting date must be identified, required by AASB 101, paragraph 51(a) and (c).

2 AASB 101, paragraph 113 requires notes to be presented systematically and each item to be cross-referenced to any related information in the notes.

3 The rounding used in the financial report must be identified, required by AASB 101, paragraph 51(e).

Department for SA Service Delivery

35

STATEMENT OF CASH FLOWS (cont.) For the year ended 30 June 20141

AASB 107 Statement of Cash Flows requires a Statement of Cash Flows to report cash flows during the period. Cash flows will be classified as operating, investing or financing activities.

AASB 107 allows cash flows arising from operating activities to be reported in the statement using either the direct or indirect method. APS 3.10 in APF II mandates the use of the direct method, whereby major classes of gross cash receipts and cash payments are disclosed.

The Statement of Cash Flows has been prepared on the net cost of services format consistent with the requirement outlined in APS 3.9 within APF II and as permitted by AASB 107, ‘Aus’ paragraph 20.2.

The following cash flows must be separately disclosed and classified in a consistent manner from period to period as either operating, investing or financing activities:

- interest received, dividends received and interest paid (classified as operating flows); and - dividends paid (classified as financing flows).

It is unlikely that not-for-profit entities will pay a dividend to the Treasurer as dividends are payments from profit and not-for-profit entities generally do not make a profit but rather receive appropriation or earn income to cover the cost of providing services.

Cash flows are to be included in the Statement of Cash Flows on a gross basis, subject to AASB Interpretation 1031, paragraphs 6 to 11 and AASB 107.

When accounting for the GST cash flows, the ‘2 line method’ is preferred, i.e. a separate line for GST recovered and paid to the Australian Taxation Office. The GST arising from investing and financing activities which is recoverable from, or payable to, the Australian Taxation Office must be classified as operating cash flows.

At the UIG meeting in September 2000, UIG members noted that although GST amounts are not required to be disclosed in cash flow statements, an entity could choose to make specific GST disclosures in the statement itself or in notes to the statement.

When accounting for the Commonwealth Government’s Paid Parental Leave Scheme, agencies are acting as a conduit through which the payment to eligible employees are made on behalf of the Family Assistance Office – consistent with the treatment of GST, the 2 line method is preferred.

The line item for ‘other’ receipts/payments should not exceed 10% of the total value of receipts/payments.

Materiality

Each material class of similar items shall be presented separately in the statement. If a line item is not individually material, it is aggregated with other items in the statement or in the notes. An item that is not sufficiently material to warrant separate presentation in the Statement of Cash Flows may be sufficiently material for it to be presented separately in the notes.

Notes are to be prepared for each material item in the Statement of Cash Flows. Applying the concept of materiality means that a specific disclosure requirement in an accounting standard need not be satisfied if the information is not material. However, AASB 1031 does not apply to specific disclosure requirements contained in accounting policy statements.

The reference column in the Statement of Cash Flows is for information only and should not be replicated in not-for-profit entities’ financial statements. Separate line items shown in the statement need not be included unless they are material and relevant to the circumstances of the entity.

Non-cash transactions

AASB 107 paragraph 43 requires investing and financing activities that do not require the use of cash to be disclosed in a way that provides all the relevant information about these activities.

Other disclosures

AASB 107 paragraphs 48 and 50 require an entity to disclose, together with commentary by management, the amounts of cash and cash equivalent balances held by the entity that are not available for use by the entity. This disclosure is applicable to the Department for SA Service Delivery and has been illustrated at Note 19 Cash and cash equivalents.

Department for SA Service Delivery

Model Financial Statements as at March 2014 36

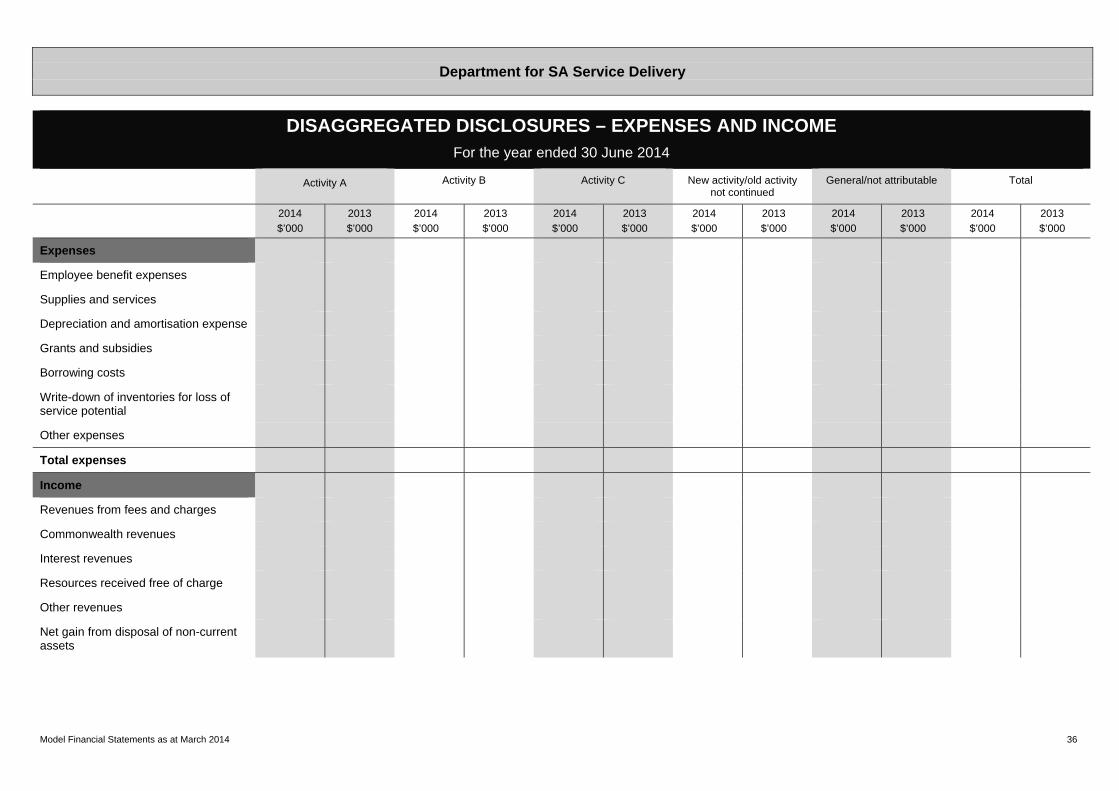

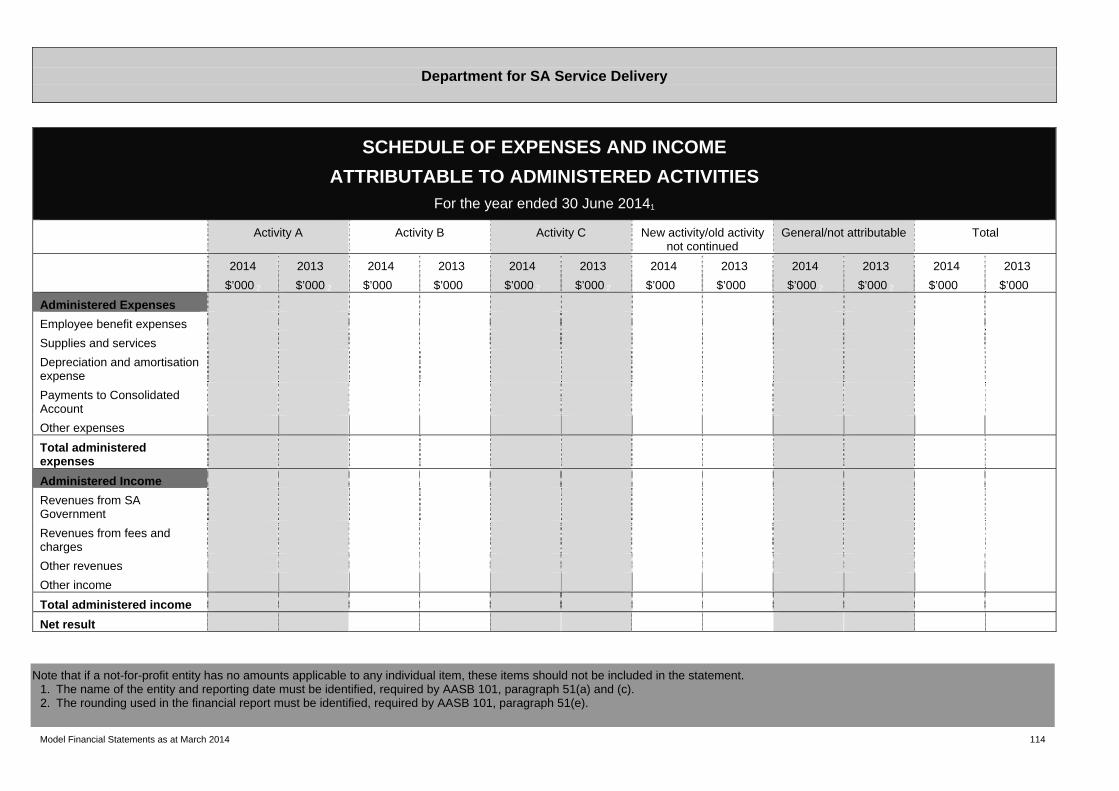

DISAGGREGATED DISCLOSURES – EXPENSES AND INCOME For the year ended 30 June 2014

Activity A Activity B Activity C New activity/old activity not continued

General/not attributable Total

2014

$’000

2013

$’000

2014

$’000

2013

$’000

2014

$’000

2013

$’000

2014

$’000

2013

$’000

2014

$’000

2013

$’000

2014

$’000

2013

$’000

Expenses

Employee benefit expenses

Supplies and services

Depreciation and amortisation expense

Grants and subsidies

Borrowing costs

Write-down of inventories for loss of service potential

Other expenses

Total expenses

Income

Revenues from fees and charges

Commonwealth revenues

Interest revenues

Resources received free of charge

Other revenues

Net gain from disposal of non-current assets

Department for SA Service Delivery

Model Financial Statements as at March 2014 37

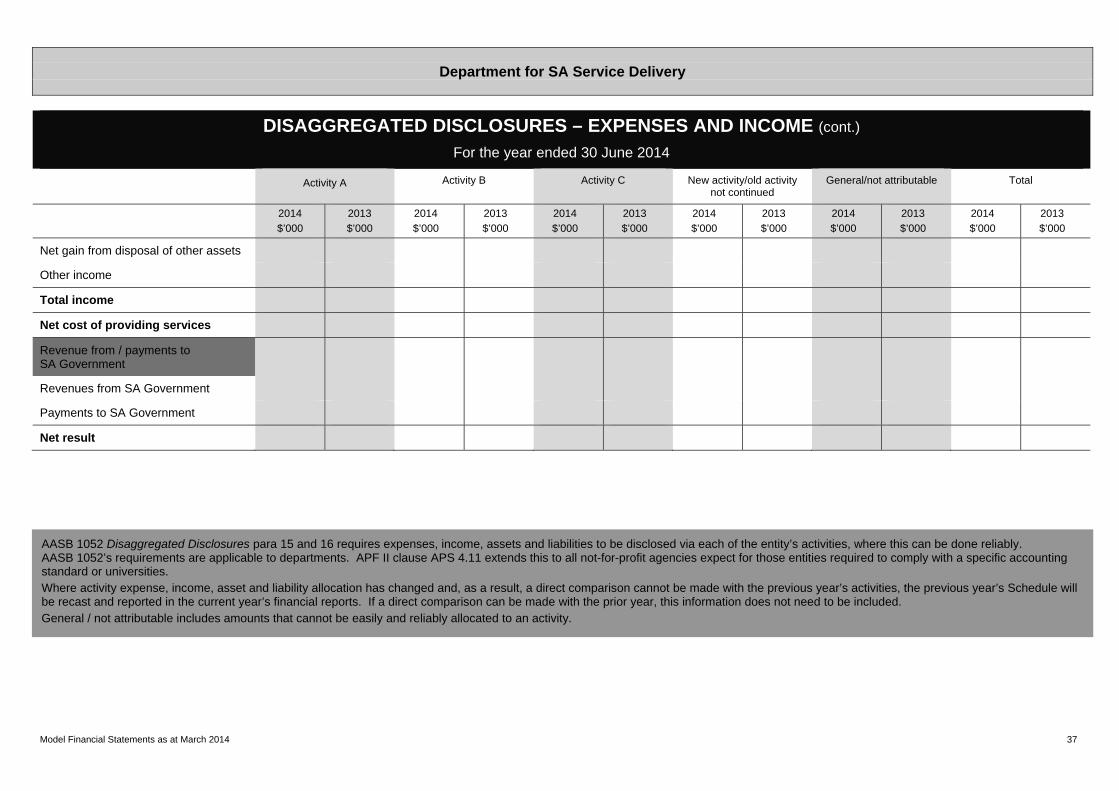

DISAGGREGATED DISCLOSURES – EXPENSES AND INCOME (cont.)

For the year ended 30 June 2014

Activity A Activity B Activity C New activity/old activity not continued

General/not attributable Total

2014

$’000

2013

$’000

2014

$’000

2013

$’000

2014

$’000

2013

$’000

2014

$’000

2013

$’000

2014

$’000

2013

$’000

2014

$’000

2013

$’000

Net gain from disposal of other assets

Other income

Total income

Net cost of providing services

Revenue from / payments to SA Government

Revenues from SA Government

Payments to SA Government

Net result

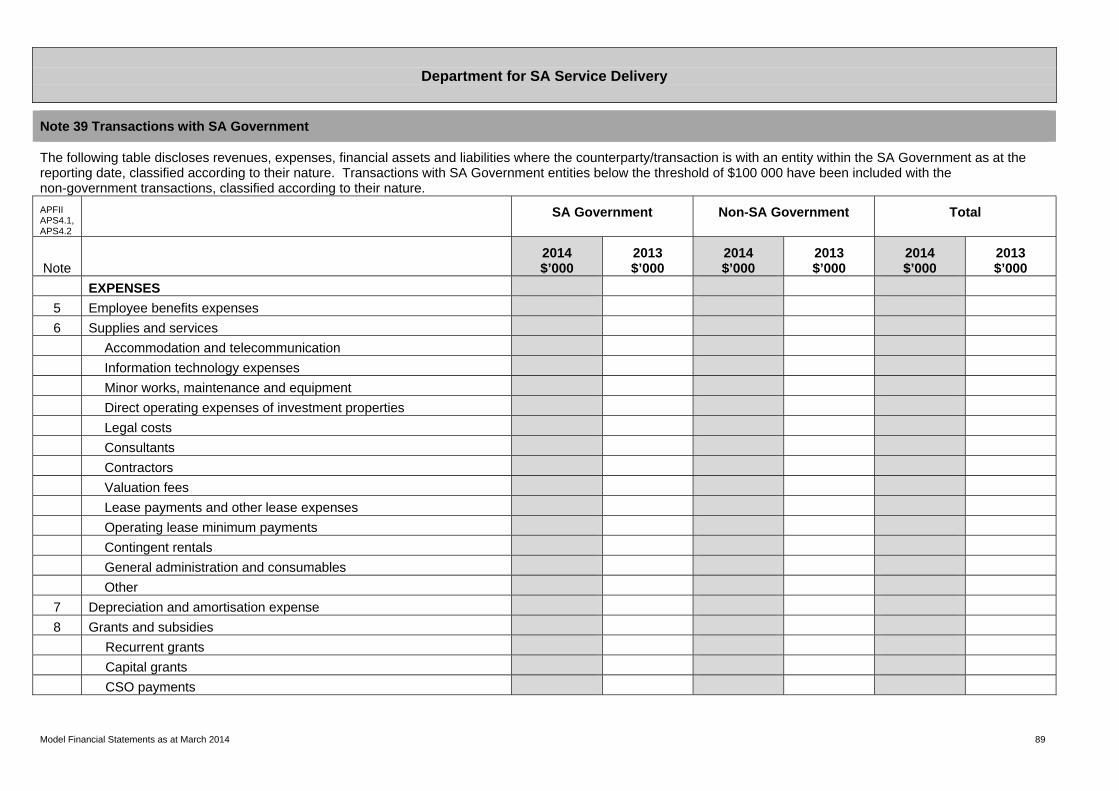

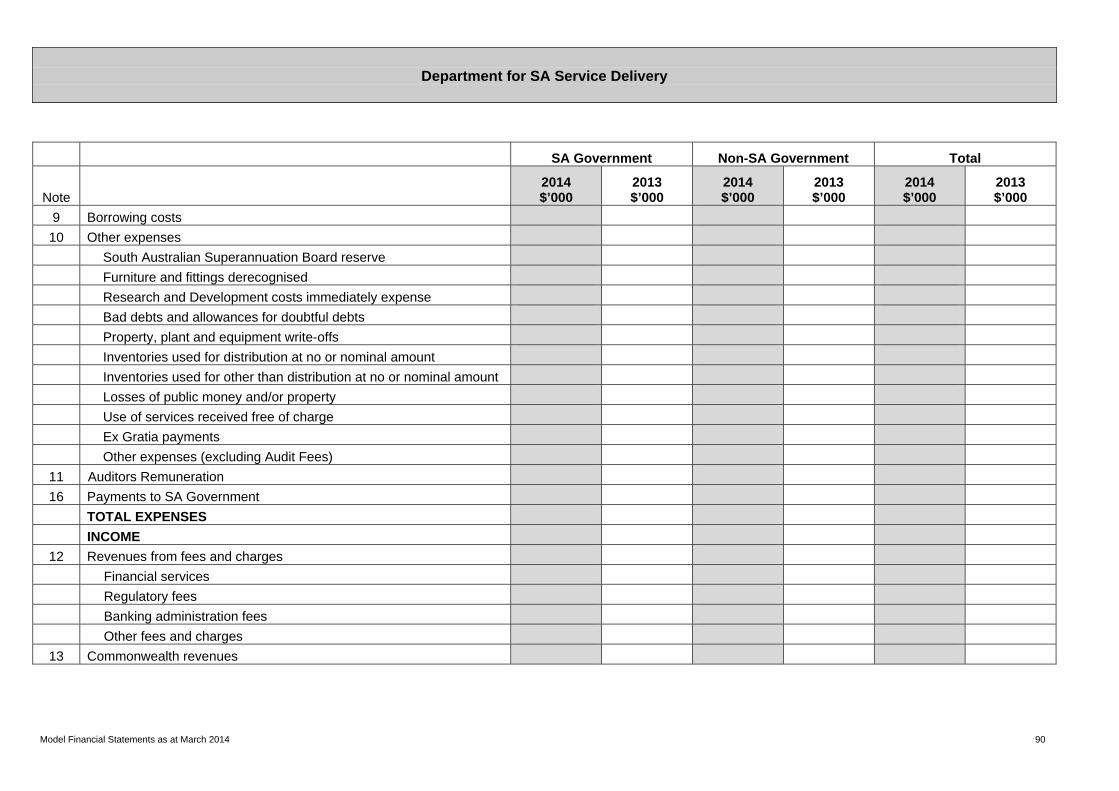

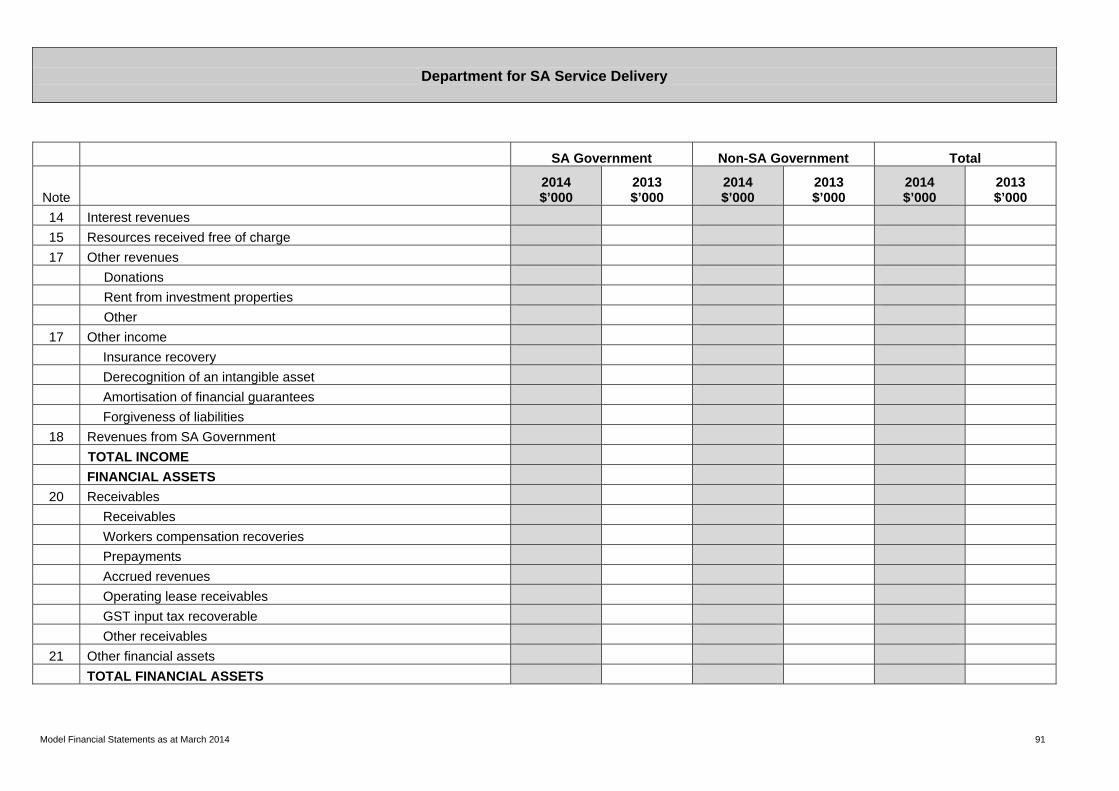

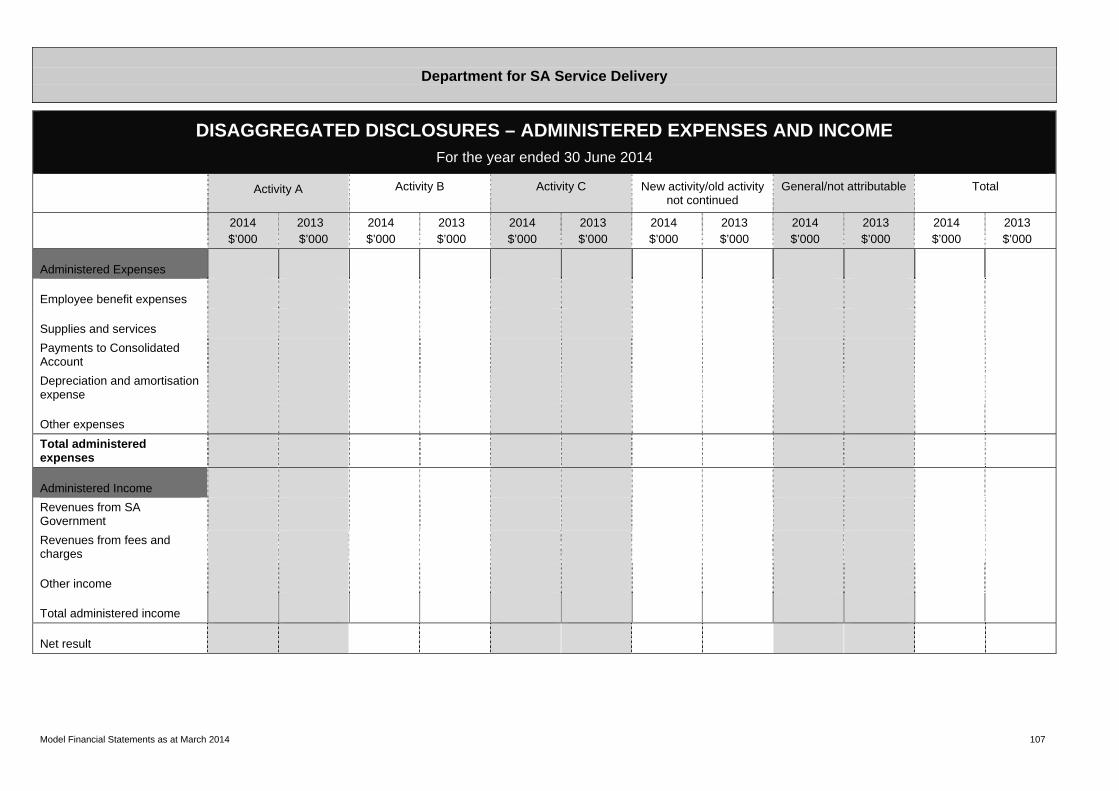

AASB 1052 Disaggregated Disclosures para 15 and 16 requires expenses, income, assets and liabilities to be disclosed via each of the entity’s activities, where this can be done reliably. AASB 1052’s requirements are applicable to departments. APF II clause APS 4.11 extends this to all not-for-profit agencies expect for those entities required to comply with a specific accounting standard or universities. Where activity expense, income, asset and liability allocation has changed and, as a result, a direct comparison cannot be made with the previous year’s activities, the previous year’s Schedule will be recast and reported in the current year’s financial reports. If a direct comparison can be made with the prior year, this information does not need to be included. General / not attributable includes amounts that cannot be easily and reliably allocated to an activity.

Department for SA Service Delivery

Model Financial Statements as at March 2014 38

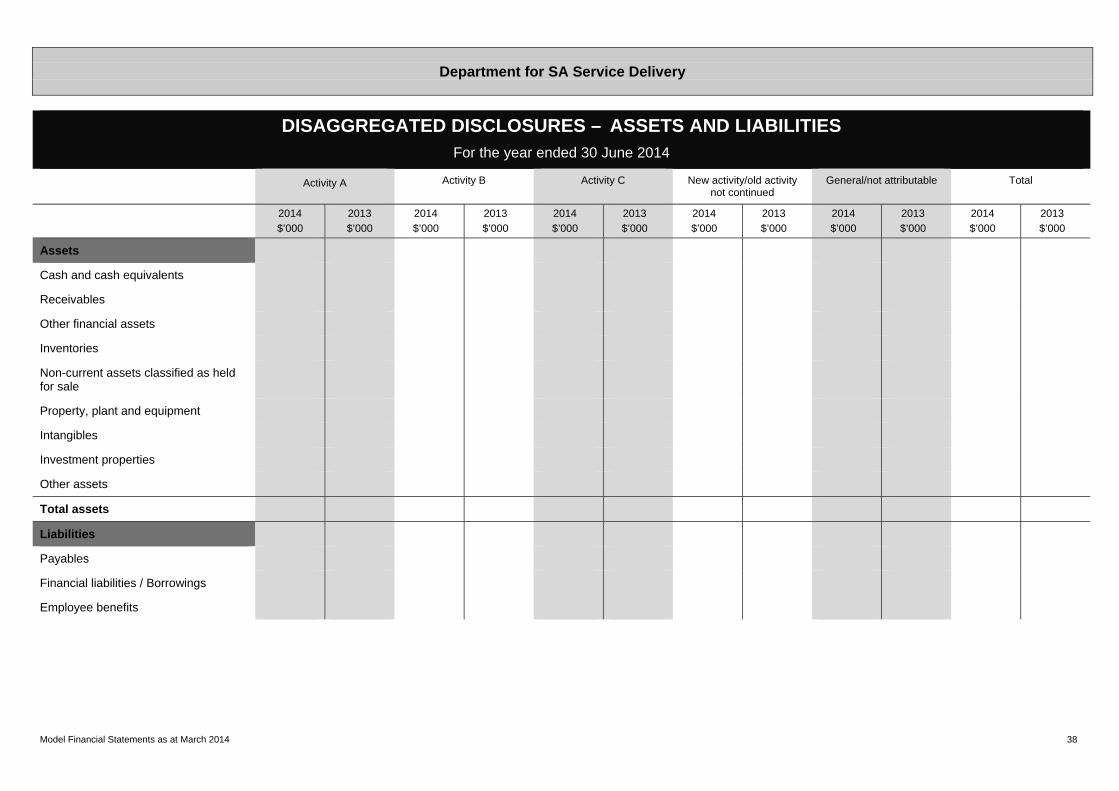

DISAGGREGATED DISCLOSURES – ASSETS AND LIABILITIES

For the year ended 30 June 2014

Activity A Activity B Activity C New activity/old activity not continued

General/not attributable Total

2014

$’000

2013

$’000

2014

$’000

2013

$’000

2014

$’000

2013

$’000

2014

$’000

2013

$’000

2014

$’000

2013

$’000

2014

$’000

2013

$’000

Assets

Cash and cash equivalents

Receivables

Other financial assets

Inventories

Non-current assets classified as held for sale

Property, plant and equipment

Intangibles

Investment properties

Other assets

Total assets

Liabilities

Payables

Financial liabilities / Borrowings

Employee benefits

Department for SA Service Delivery

Model Financial Statements as at March 2014 39

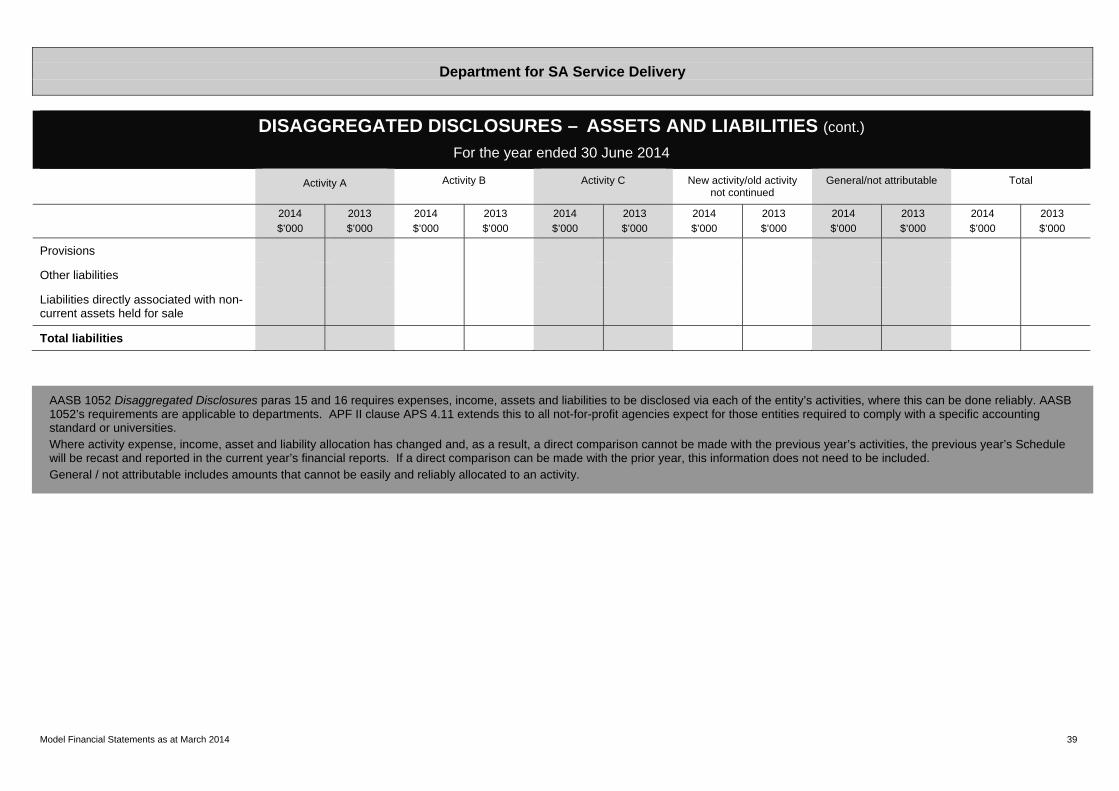

DISAGGREGATED DISCLOSURES – ASSETS AND LIABILITIES (cont.)

For the year ended 30 June 2014

Activity A Activity B Activity C New activity/old activity not continued

General/not attributable Total

2014

$’000

2013

$’000

2014

$’000

2013

$’000

2014

$’000

2013

$’000

2014

$’000

2013

$’000

2014

$’000

2013

$’000

2014

$’000

2013

$’000

Provisions

Other liabilities

Liabilities directly associated with non- current assets held for sale

Total liabilities

AASB 1052 Disaggregated Disclosures paras 15 and 16 requires expenses, income, assets and liabilities to be disclosed via each of the entity’s activities, where this can be done reliably. AASB 1052’s requirements are applicable to departments. APF II clause APS 4.11 extends this to all not-for-profit agencies expect for those entities required to comply with a specific accounting standard or universities. Where activity expense, income, asset and liability allocation has changed and, as a result, a direct comparison cannot be made with the previous year’s activities, the previous year’s Schedule will be recast and reported in the current year’s financial reports. If a direct comparison can be made with the prior year, this information does not need to be included. General / not attributable includes amounts that cannot be easily and reliably allocated to an activity.

Department for SA Service Delivery

Model Financial Statements as at March 2014 40

NOTES TO &

FORMING PART OF

THE FINANCIAL

STATEMENTS

Department for SA Service Delivery

Model Financial Statements as at March 2014 41

Commentary - Contents

Reference Contents page

A contents page/note index will assist users of the financial report.

Presentation of notes