Embed Size (px)

Citation preview

MOBILE APPS FOR WEALTH MANAGEMENT 2017HOW INNOVATION BEATS COMPLACENCY

BENCHMARKING - DATA - ANALYSIS - STRATEGY - RANKINGS

SEPTEMBER 2017

ONAWA LACEWELLSENIOR ANALYST

REPORT EXTRACT

Original report with 153 pages

Plus comprehensive data appendix

MOBILE APPS FOR WEALTH MANAGEMENT | 14

CONTENT

1.0 EXECUTIVE SUMMARY 5

2.0 2017 RANKINGS 8

3.0 METHODOLOGY 9

3.1 CASE SELECTION 9

3.2 THE EVALUATION PROCESS 10

3.3 CASE SELECTION: WEALTH MANAGERS AND MOBILE APPS 2017 16

4.0 STRATEGY: NAVIGATING THE TRANSFORMATION OF DIGITAL WEALTH MANAGEMENT 17

4.1 THE CASE FOR A STRONG MOBILE APP 17

4.2 THE STATE OF THE WEALTH MANAGEMENT ECOSYSTEM 2017 17

4.3 THE TRANSFORMATION OF MOBILE WEALTH MANAGEMENT APPS 20

4.4 NO TWO JOURNEYS ALIKE: USING PERSONALIZATION TO PROVIDE A UNIQUE AND TAILORED CLIENT EXPERIENCE 24

4.5 FUTURE (AND FUTURISTIC) INNOVATIONS THAT COULD TRANSFORM MOBILE WEALTH MANAGEMENT YET AGAIN 25

4.6 THE ESSENTIAL COMPONENTS OF A SUCCESSFUL MOBILE APP 26

5.0 TOP 15 BEST PRACTICES 28

5.1 DESIGN AND USABILITY 29

5.2 PLATFORM INTEGRATION 30

5.4 USE OF INNOVATIVE TECHNOLOGY 32

5.5 VALUE-ADDED SERVICES 33

6.0 SUMMARY OF FINDINGS 35

6.1 POSITIVE TRENDS IN MOBILE APPS FOR WEALTH MANAGEMENT 35

6.2 REMAINING SHORTCOMINGS OF MOBILE APPS FOR WEALTH MANAGEMENT 36

6.3 2017 PERFORMANCE BY CATEGORY 37

6.4 WEALTH SERVICES INDICATOR 44

MOBILE APPS FOR WEALTH MANAGEMENT | 15

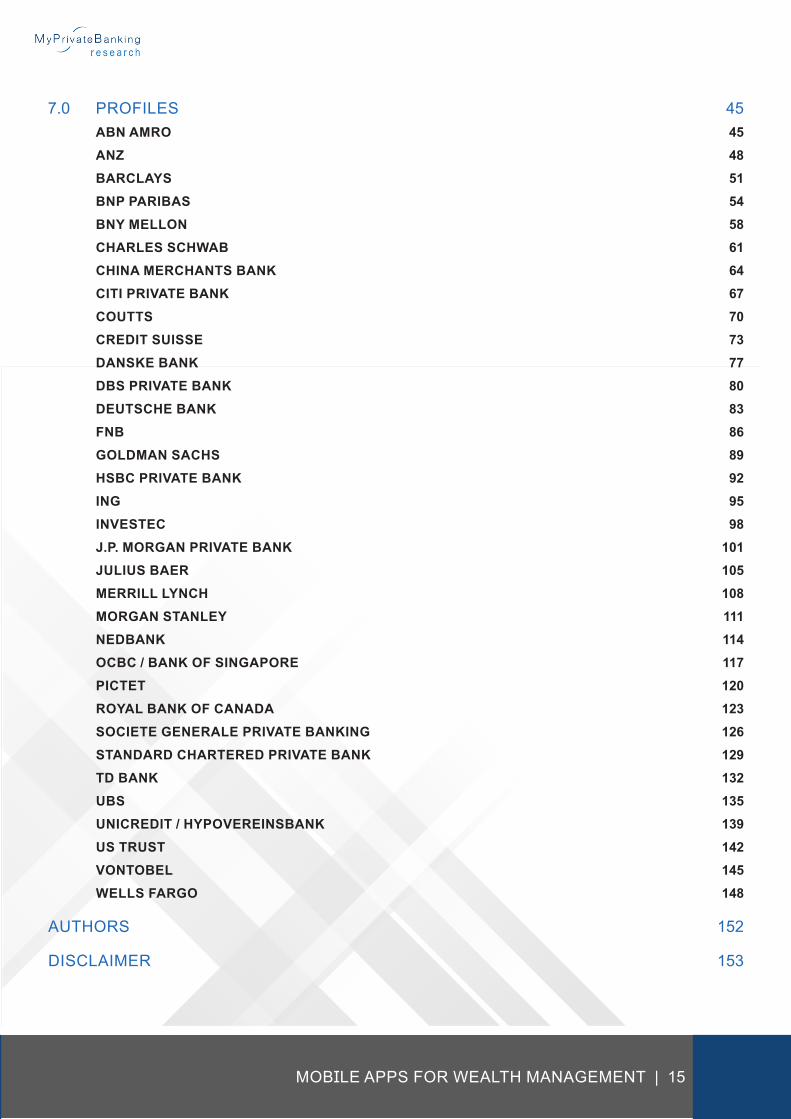

7.0 PROFILES 45 ABN AMRO 45 ANZ 48 BARCLAYS 51 BNP PARIBAS 54 BNY MELLON 58 CHARLES SCHWAB 61 CHINA MERCHANTS BANK 64 CITI PRIVATE BANK 67 COUTTS 70 CREDIT SUISSE 73 DANSKE BANK 77 DBS PRIVATE BANK 80 DEUTSCHE BANK 83 FNB 86 GOLDMAN SACHS 89 HSBC PRIVATE BANK 92 ING 95 INVESTEC 98 J.P. MORGAN PRIVATE BANK 101 JULIUS BAER 105 MERRILL LYNCH 108 MORGAN STANLEY 111 NEDBANK 114 OCBC / BANK OF SINGAPORE 117 PICTET 120 ROYAL BANK OF CANADA 123 SOCIETE GENERALE PRIVATE BANKING 126 STANDARD CHARTERED PRIVATE BANK 129 TD BANK 132 UBS 135 UNICREDIT / HYPOVEREINSBANK 139 US TRUST 142 VONTOBEL 145 WELLS FARGO 148

AUTHORS 152

DISCLAIMER 153

MOBILE APPS FOR WEALTH MANAGEMENT | 16

TABLE OF CHARTS

Mobile app performance 2014 - 2017 7

2017 Performance rankings 9

Use cases for mobile apps 11

Case selection 2017 17

The XXX app provides a social network for U/HNWIs, relationship managers, and family officers 19

Client of a well-known wealth manager who spoke with MPB Research 20

CircleBlack targets U/HNWIs with a sleek wealth management app with advanced features. 21

XXX’s app provides direct contact and collaboration between clients and advisors 22

The transformation of digital wealth management means redefining the digital advisor journey 23

The XXX app provides value-added services in the form of philanthropy 24

The essential components of a successful mobile strategy 28

The XXX app has a faster and better user interface thanks to gesture recognition 30

One of XXX’s payment options lets clients share payment requests through SMS 31

Clients can chat from their XXX smartwatch app 31

XXX lets clients stream video reports on financial and market issues from CNBC 32

A view of XXX’s Relationship Manager feature 32

XXX’s portal provides a wide range of information to clients 32

XXX’s facial recognition feature makes large transfers quicker 33

Partners of XXX’s program are superimposed on the smartphone screen 33

XXX’s clients can get advice and notifications and act on these in app 33

XXX’s platform gives clients an easy opportunity to find and donate to causes they care about 34

XXX’s feature is a clever solution to address wealth clients’ non-financial assets 34

Heatmap: Content for customer retention of high/low ranked WMs 37

Graphic: Categorical performance overview 38

Graphic: availability of mobile apps 38

Graphic: Provision of core features 39

Heatmap: Core features provided by high/low ranked WMs 39

Graphic: Security and privacy features 40

Graphic: Content for customer retention and marketing 41

Graphic: Key changes in customer retention features 41

Graphic: Contact features 42

Graphic: A closer look at client-advisor relationship building 2016/2017 42

Graphic: Technical features and support 43

Graphic: Innovative mobile app features 43

Graphic: A closer look at account aggregation 44

Graphic: Platform integration 44

Wealth services indicator rankings 2017 45

MOBILE APPS FOR WEALTH MANAGEMENT | 1

SUMMARY

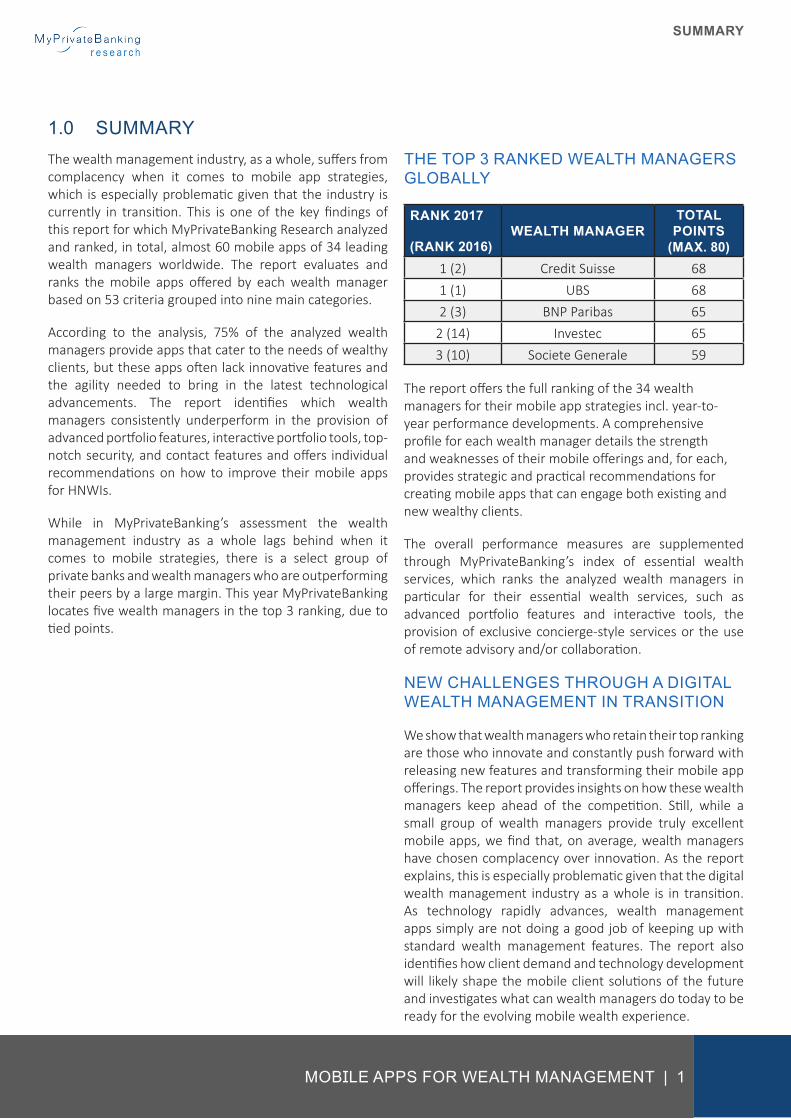

The wealth management industry, as a whole, suffers from complacency when it comes to mobile app strategies, which is especially problematic given that the industry is currently in transition. This is one of the key findings of this report for which MyPrivateBanking Research analyzed and ranked, in total, almost 60 mobile apps of 34 leading wealth managers worldwide. The report evaluates and ranks the mobile apps offered by each wealth manager based on 53 criteria grouped into nine main categories.

According to the analysis, 75% of the analyzed wealth managers provide apps that cater to the needs of wealthy clients, but these apps often lack innovative features and the agility needed to bring in the latest technological advancements. The report identifies which wealth managers consistently underperform in the provision of advanced portfolio features, interactive portfolio tools, top-notch security, and contact features and offers individual recommendations on how to improve their mobile apps for HNWIs.

While in MyPrivateBanking’s assessment the wealth management industry as a whole lags behind when it comes to mobile strategies, there is a select group of private banks and wealth managers who are outperforming their peers by a large margin. This year MyPrivateBanking locates five wealth managers in the top 3 ranking, due to tied points.

THE TOP 3 RANKED WEALTH MANAGERS GLOBALLY

RANK 2017

(RANK 2016)WEALTH MANAGER

TOTAL POINTS

(MAX. 80)1 (2) Credit Suisse 681 (1) UBS 682 (3) BNP Paribas 65

2 (14) Investec 653 (10) Societe Generale 59

The report offers the full ranking of the 34 wealth managers for their mobile app strategies incl. year-to-year performance developments. A comprehensive profile for each wealth manager details the strength and weaknesses of their mobile offerings and, for each, provides strategic and practical recommendations for creating mobile apps that can engage both existing and new wealthy clients.

The overall performance measures are supplemented through MyPrivateBanking’s index of essential wealth services, which ranks the analyzed wealth managers in particular for their essential wealth services, such as advanced portfolio features and interactive tools, the provision of exclusive concierge-style services or the use of remote advisory and/or collaboration.

NEW CHALLENGES THROUGH A DIGITAL WEALTH MANAGEMENT IN TRANSITION

We show that wealth managers who retain their top ranking are those who innovate and constantly push forward with releasing new features and transforming their mobile app offerings. The report provides insights on how these wealth managers keep ahead of the competition. Still, while a small group of wealth managers provide truly excellent mobile apps, we find that, on average, wealth managers have chosen complacency over innovation. As the report explains, this is especially problematic given that the digital wealth management industry as a whole is in transition. As technology rapidly advances, wealth management apps simply are not doing a good job of keeping up with standard wealth management features. The report also identifies how client demand and technology development will likely shape the mobile client solutions of the future and investigates what can wealth managers do today to be ready for the evolving mobile wealth experience.

1.0 SUMMARY

MOBILE APPS FOR WEALTH MANAGEMENT | 2

SUMMARY

WEALTH MANAGERS NEED TO STRIVE FOR AGILITY AND INNOVATION

In MyPrivateBanking’s view, several points are particularly important to this transition period and the report identifies the areas where wealth managers must push forward and how to best achieve this. Failure to respond to these developments will quickly lead to wealth managers’ mobile apps becoming outdated and, as a result, clients, walking out of the door. The report also explores how traditional wealth managers can develop a mobile strategy that counters the threat of new FinTechs that have set their sights on the wealth management industry.

Based on our in-depth benchmarking and a detailed strategic analysis of current and future the client needs and technological developments, the report provides a series of recommendations for developing an innovative, top-performing app. These recommendations are illustrated by plenty of examples of best practices in areas such as design and usability, platform integration, use of innovative technology and value-added services.

The report includes more than 50 visuals including graphs, screenshots and charts, and it comes with a comprehensive data-appendix containing content analytical data of each firm’s mobile app(s) according to 53 detailed criteria.

To order the full report, please click here

MOBILE APPS FOR WEALTH MANAGEMENT | 3

SUMMARY

2.0 2017 RANKINGS

MOBILE APPS FOR WEALTH MANAGEMENT | 4

SUMMARY

3.0 METHODOLOGY

3.1 CASE SELECTIONThis study examines the mobile apps offered by 34 different banks and wealth managers specifically for wealth clients. Naturally, we only considered banks with strong mobile offerings in our initial pool of contenders. From these, we chose a sample of banks based on their fulfillment of one of two criteria: high assets under management (AuM) or geographical dominance. Often, the banks fulfilled both criteria but sometimes we chose to include cases with lower AuM if the bank fulfilled a key role in its region’s wealth management and private banking sphere. For AuM, we based the selection on totals from the end of 2016. Choosing banks according to these two criteria allows us to include the most important wealth managers globally as well as ensure broad and balanced geographical coverage.

For all wealth managers, we include apps that are available for either Apple, Android, or both. Additionally, the app must have some sort of wealth-specific features. Such features include, for example, a separate design for U/HNWIs, a wealth-specific e-magazine, personalization of features based on account type, or similar.

Apps that target institutional or commercial clients are excluded. Also excluded are apps that are solely for retail clients. However, if a bank uses a retail app for both retail and wealth management clients then, depending on the circumstances, this app is included. Finally, we excluded apps that are solely for investor relations, such as an “Events” app.

These selection criteria mean that apps are included in the study if:

■ They are available to wealth clients. The apps must be promoted as wealth management apps either on the website of the bank or in the app description in the app store. For instance, a banking app that is targeted at all clients, retail and wealth management alike, but that is promoted on the private banking sub-site, is included.

■ They are available in the home market. For all private banks and wealth managers, we evaluate apps based on their availability in the home market and in the home language. We do so with the belief that the home market/language app will offer the most possible features. We do not, however, restrict the sample in terms of additional markets served.

■ The app targets international wealth clients. Sometimes banks offer specific apps for international wealth clients—for example, Danske Bank’s Luxembourg-based app is specifically for use by international wealth clients. Such apps are also allowed in the study.

Based on the above specifications, we were able to narrow our case selection down to 34 different banks and wealth managers. This is four more cases than the 2016 report, but there is still quite a bit of overlap in the cases included this year and last year—allowing us to maintain continuity and allow for some minor trend analysis. The full list of cases included in our final survey is shown in the table at the end of this chapter.

MOBILE APPS FOR WEALTH MANAGEMENT | 5

SUMMARY

Use cases for mobile apps

3.2 THE EVALUATION PROCESS

USE CASE OBJECTIVES

Portfolio Check Overview of investment portfolio and portfolio analysis capabilities.

Trading and Brokerage Check price information and perform trades.Financial Content Making informed trading decisions; market data, financial news, watch-lists.

Interactive Portfolio Analysis Benchmarking, hypothetical portfolios, personalized product and investment advice.

Expertise Content Expert commentary, customer magazines, blogs, educational content.

Contact Features General contact (phone, email), advanced contact (call back, live chat), direct contact to advisor, video and chat support features.

Generally, we evaluate two types of app: core apps and supplementary apps. Core apps are primary apps—meaning that they allow clients to do general and advanced banking tasks such as checking investment portfolios, buying and selling securities, making payments (including bill pay) and sending/receiving transfers. These apps allow users to actively manage their daily finances. Supplementary apps, on the other hand, are apps dedicated to a specific service. For instance, the provision of educational material intended to support wealth clients in making sound investment decisions. As in our 2016 report, we only include supplementary apps that are intended to be used by wealth clients or which meet the needs of U/HNWIs.

We approached the evaluation process in a stepwise manner. First, we did an initial sweep of the mobile offerings of each bank or wealth manager included in the study. Then, after compiling a full list of mobile offerings, we narrowed the list down to those that targeted wealth clients in some way. Next, we threw out any client services apps. Finally, we designated each remaining app as a core app or a supplementary app (where available).

Once we had narrowed down the list of core apps and supplementary apps for each wealth manager, we began the evaluation with the core app. Then, in a second step, we repeated the evaluation for the next app—often a supplementary app. Where the primary app did not receive the maximum number of points, these points could be assigned to the second evaluated app. However, if the first app received the maximum number of points for an evaluation criteria, the second app would not be awarded these points.

In this way, other apps could contribute to the bank’s overall score, up to the maximum of 80 points, but no single case (bank or wealth manager) could earn more than 80 points. However, some criteria that were considered as critical could not earn any additional points if they were not present in the core app. For example, if a core app had technical errors this could not be compensated for by an error-free supplementary app.

GENERAL MOBILE STRATEGY

It was important for our evaluation that we considered the bank or wealth manager’s overall app strategy. Before starting our evaluation, we contacted each bank and wealth manager on our list and requested access to their mobile app or offered them the chance of a personal interview to discuss app strategy. Some banks provide a public demo (sample) account within their app so that non-clients can test drive their functions. In some cases, it was not possible for our analysts to test the full set of functions of an app, as there was no response to our request for log-in credentials from the banks in question. In these cases, we evaluated the features and functions based on the app description, user feedback in the various app stores, screenshots of the app from various sources, and media coverage of the app and its functions.

USE CASES AS A GUIDELINE

The evaluation criteria are derived from use cases defined based on years of research in this field, including, for example, regular in-depth interviews with wealth managers and comprehensive surveys aimed at profiling today’s digital use patterns of high-net-worth clients. Grouping the representative user profiles to reflect user preferences and concerns plays an important role in the weighting of the criteria. The use cases and objectives are listed in the table below.

MOBILE APPS FOR WEALTH MANAGEMENT | 6

SUMMARY

EVALUATION PROCEDURE

The evaluations were carried out by two analysts, working independently, within a four-week period. This helped minimize the possibility of subjective bias and technical problems such as network failures. Given the sheer quantity of information analyzed, it is not possible to rule out that some information was not found. However, an intensive feedback process for each evaluation by a separate analyst minimizes this risk as much as possible. The evaluation included 53 separate criteria that were distributed across nine different categories. Care was taken to keep the definition and allocation of points as free as possible from all subjective influences, thus ensuring a high level of objectivity in the benchmarking process.

In addition to the apps themselves, other sources of information were also included in the analysis: user feedback and ratings as well as screenshots from the major app stores (iTunes, Google Play), information from the banks’ websites (often the banks displayed additional information about their apps on their websites such as the privacy policy, FAQs or a video tutorial), and occasionally other sources such as Twitter feeds, blogs, newspaper coverage, etc. If specific questions arose during the evaluation procedure that could not be answered via these sources, the analyst would contact customer service via the support line or using social media.

EVALUATION CRITERIA

In this study, the main evaluation criterion for the apps was the extent to which they fulfill the use cases described above. In contrast to last year’s report, we loosened the restriction on wrapper features (i.e., features that are not native to an app but rather open a link to the mobile website via the phone’s browser). While wrapper features are, as a whole, sub-optimal in terms of user design, we decided that for some types of information wrapper features are understandable. For example, we allowed wrapper features for FAQs and Help Menu information as well as for information about product and service offerings of a bank. When determining whether a wrapper feature received full points, we always asked the question “how much does the wrapper impede usability?”

Each of the 53 evaluation criterion falls into one of nine categories:

Availability of mobile apps

■ Core functions for clients

■ Security and privacy

■ Content and features for customer retention and marketing

■ Contact features

■ Technical features and support

■ Innovative in-app features

■ Platform integration

■ Best practices

In the following, the parameters for each criterion are described in detail, including the maximum achievable points. In comparison to last year’s report, there have been some changes in our rating scheme. These changes, along with several minor adjustments (e.g. in the weighting for the criteria), reflect current developments and future trends in the interface of wealth management and the digital world. Newly added criteria reflect changes in the overall environment and the constant development of technical features that can be realized in mobile apps. For example, this year’s evaluation reflects the on-going trend towards more interactivity and remote advisory within the wealth management industry.

One of the bigger changes that we made to this year’s evaluation grid was the inclusion of a ninth category, “Innovative in-app features.” For this year’s evaluation we decided to create a separate category that included four criteria: chatbots, account aggregation, voice control/hands-free technology, and contextuality (the use of a smartphone’s data-gathering features to tailor a user’s app experience). These four innovations reflect current trends in digital wealth management. Chatbots have been one of the biggest trends of the past year in wealth management technology and we specifically wanted to discover, with this criterion, whether wealth managers were also targeting U/HNWI clients with chatbot technology or whether this trend is more retail-based.

Below, we provide an overview of all criteria included in the evaluation.

(...more in full report pages 12-16)

MOBILE APPS FOR WEALTH MANAGEMENT | 7

SUMMARY

4.0 STRATEGY: NAVIGATING THE TRANSFORMATION OF DIGITAL WEALTH MANAGEMENT

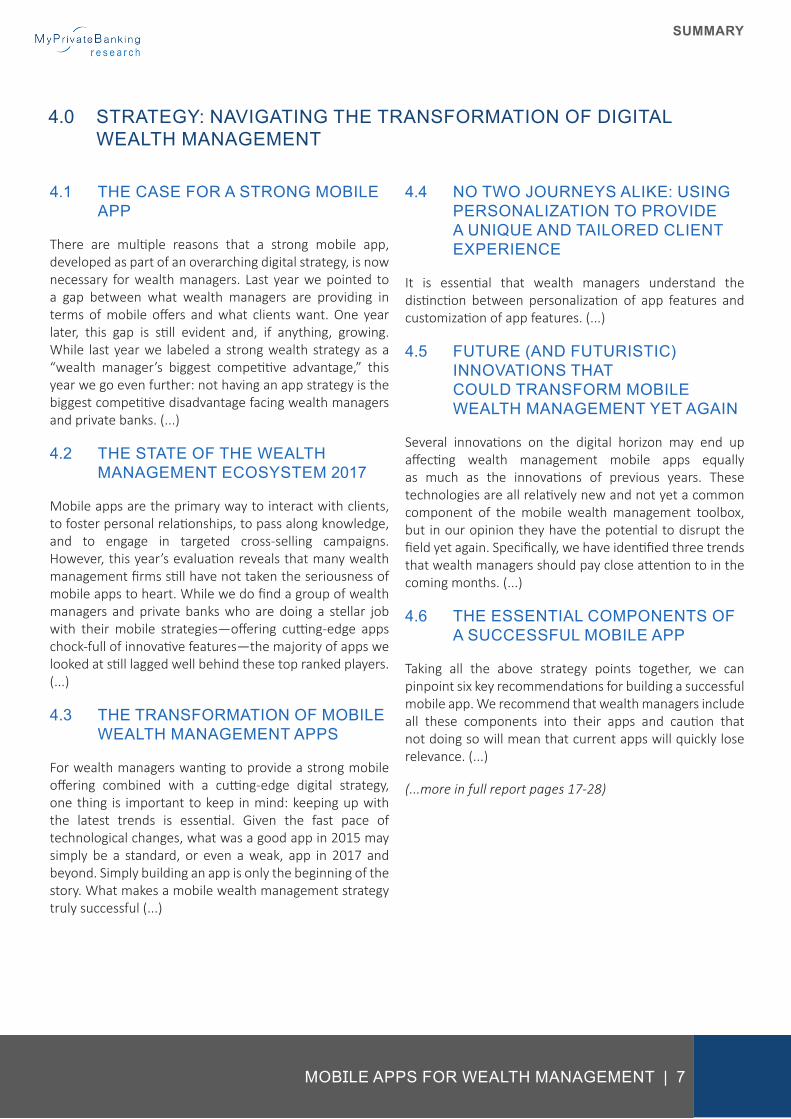

4.1 THE CASE FOR A STRONG MOBILE APP

There are multiple reasons that a strong mobile app, developed as part of an overarching digital strategy, is now necessary for wealth managers. Last year we pointed to a gap between what wealth managers are providing in terms of mobile offers and what clients want. One year later, this gap is still evident and, if anything, growing. While last year we labeled a strong wealth strategy as a “wealth manager’s biggest competitive advantage,” this year we go even further: not having an app strategy is the biggest competitive disadvantage facing wealth managers and private banks. (...)

4.2 THE STATE OF THE WEALTH MANAGEMENT ECOSYSTEM 2017

Mobile apps are the primary way to interact with clients, to foster personal relationships, to pass along knowledge, and to engage in targeted cross-selling campaigns. However, this year’s evaluation reveals that many wealth management firms still have not taken the seriousness of mobile apps to heart. While we do find a group of wealth managers and private banks who are doing a stellar job with their mobile strategies—offering cutting-edge apps chock-full of innovative features—the majority of apps we looked at still lagged well behind these top ranked players. (...)

4.3 THE TRANSFORMATION OF MOBILE WEALTH MANAGEMENT APPS

For wealth managers wanting to provide a strong mobile offering combined with a cutting-edge digital strategy, one thing is important to keep in mind: keeping up with the latest trends is essential. Given the fast pace of technological changes, what was a good app in 2015 may simply be a standard, or even a weak, app in 2017 and beyond. Simply building an app is only the beginning of the story. What makes a mobile wealth management strategy truly successful (...)

4.4 NO TWO JOURNEYS ALIKE: USING PERSONALIZATION TO PROVIDE A UNIQUE AND TAILORED CLIENT EXPERIENCE

It is essential that wealth managers understand the distinction between personalization of app features and customization of app features. (...)

4.5 FUTURE (AND FUTURISTIC) INNOVATIONS THAT COULD TRANSFORM MOBILE WEALTH MANAGEMENT YET AGAIN

Several innovations on the digital horizon may end up affecting wealth management mobile apps equally as much as the innovations of previous years. These technologies are all relatively new and not yet a common component of the mobile wealth management toolbox, but in our opinion they have the potential to disrupt the field yet again. Specifically, we have identified three trends that wealth managers should pay close attention to in the coming months. (...)

4.6 THE ESSENTIAL COMPONENTS OF A SUCCESSFUL MOBILE APP

Taking all the above strategy points together, we can pinpoint six key recommendations for building a successful mobile app. We recommend that wealth managers include all these components into their apps and caution that not doing so will mean that current apps will quickly lose relevance. (...)

(...more in full report pages 17-28)

MOBILE APPS FOR WEALTH MANAGEMENT | 8

SUMMARY

These 15 best practices highlight firms that are pioneering new ways of banking and engaging with their clients. We are heartened to see signs that private banks and wealth management companies are warming to cutting edge technologies, even if these are not yet common features in mobile wealth management apps. Furthermore, some even more envelope-pushing features, such as artificial intelligence, augmented reality, and gesture recognition, have begun to show up in mobile apps. Some companies cited in this chapter are also way ahead of their counterparts when it comes to understanding how digital technology changes and influences their clients’ daily lives. The integration of payment systems as well as offers of new products and services through mobile devices is an acknowledgment of this changing consumer behavior and banking landscape.

In this report, the best practices we highlight cover the following general themes:

■ Design and usability: features that make it easy for clients to access and use the app.

■ Platform integration: features that integrate the bank’s offline and online services and products via mobile devices.

■ Tools for wealth management: features that help to manage clients’ wealth.

■ Use of innovative technology: features that are supported by digital innovations such as AI, machine learning, augmented reality, etc.

■ Value-added services: features and content that bring about enhanced client interaction with the bank.

(... more in full report pages 29-34)

5.0 TOP 15 BEST PRACTICES

MOBILE APPS FOR WEALTH MANAGEMENT | 9

SUMMARY

This year we cover the mobile app offerings of 34 wealth managers worldwide. This group represents the cream of the crop of wealth managers and private banks. While we see some clear improvements when it comes to the mobile apps of some of the wealth managers in our evaluation, we find that there is a serious and problematic complacency in the wealth management industry as a whole when it comes to developing innovative, envelope-pushing mobile strategies. In particular, we identify four key trends for 2017: two positive developments and two trends that we see as problematic for the wealth management industry as a whole. (...)

6.1 POSITIVE TRENDS IN MOBILE APPS FOR WEALTH MANAGEMENT

(...)

6.2 REMAINING SHORTCOMINGS OF MOBILE APPS FOR WEALTH MANAGEMENT

(...)

6.3 2017 PERFORMANCE BY CATEGORY

(...)

6.4 WEALTH SERVICES INDICATOR

In 2016 we debuted a new measure of wealth-specific mobile app services. Wealth-specific features are important as they ensure that the user experience is tailored to wealth clients and that the app provides some sort of extended or additional services specifically targeting this wealth segment. These services include advanced portfolio features and interactive tools, personalization of content, investment strategies, or similar, the provision of exclusive concierge-style services within the app, a document vault, and the use of remote advisory and/or collaboration features, among others. This year we once again include this important measure of wealth focus in our evaluation. As such, our WSI narrows the focus to the most relevant and important features that wealth managers should provide their U/HNWI clients. (...)

(...more in full report pages 36-44)

6.0 SUMMARY OF FINDINGS

MOBILE APPS FOR WEALTH MANAGEMENT | 10

SUMMARY

7.0 PROFILES PAGES 45-151

■ ABN AMRO

■ ANZ

■ Barclays

■ BNP Paribas

■ BNY Mellon

■ Charles Schwab

■ Citi Private Bank

■ China Merchants Bank

■ Coutts

■ Credit Suisse

■ Danske Bank

■ DBS

■ Deutsche Bank

■ FNB

■ Goldman Sachs

■ HSBC Private Bank

■ ING

■ Investec

■ J.P. Morgan

■ Julius Baer

■ Merrill Lynch

■ Morgan Stanley

■ Nedbank

■ OCBC / Bank of Singapore

■ Pictet

■ RBC

■ Societe Generale

■ Standard Chartered

■ TD Bank

■ UBS

■ Unicredit/HVB

■ US Trust

■ Vontobel

■ Wells Fargo

The full report contains detailed profiles and evaluations fo the mobile app portfolios offered by the following 34 wealth managers:

MOBILE APPS FOR WEALTH MANAGEMENT | 11

AUTHORS

AUTHORS

Onawa Promise Lacewell, Senior Analyst, has a research focus on the impact of disruptive technologies on the financial services sector as well as on consumer behavior and global regulation. A particular focus in her work is the rise of automated investments services and breakthrough technologies such as augmented reality. Previously she worked as a Senior Researcher for the WZB Berlin Social Science Center. She holds a PhD in Political Science with specializations in comparative politics and quantitative research methods and a Bachelor’s degree in Political Science with a secondary focus in English.

Kay Luiz Alave, Junior Analyst, has a research focus that includes the digital strategies and online presence of private banks and wealth management. Previously, she worked as a business and trade journalist in Manila, Philippines and then as a research analyst for a SaaS company in Berlin. She holds a Master of Science in Global Change Management from Hochschule fuer nachhaltige Entwicklung (University for Sustainable Development) in Eberswalde.

MOBILE APPS FOR WEALTH MANAGEMENT | 12

DISCLAIMER

DISCLAIMER

IMPORTANT NOTICE AND DISCLAIMERS:

NO INVESTMENT ADVICE

This report is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. This report is distributed for informational purposes only and should not be construed as investment advice or a recommendation to sell or buy any security or other investment, or undertake any investment strategy. It does not constitute a general or personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. The price and value of securities referred to in this report will fluctuate. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of all of the original capital invested in a security discussed in this report may occur. Certain transactions, including those involving futures, options, and other derivatives, give rise to substantial risk and are not suitable for all investors.

DISCLAIMERS

There are no warranties, expressed or implied, as to the accuracy, completeness, or results obtained from any information set forth in this report. MyPrivateBanking GmbH will not be liable to you or anyone else for any loss or injury resulting directly or indirectly from the use of the information contained in this report, caused in whole or in part by its negligence in compiling, interpreting, reporting or delivering the content in this report.

COPYRIGHT

MyPrivateBanking GmbH’s Products are the property of MyPrivateBanking GmbH, Switzerland, and are protected by Swiss and international copyright law and other intellectual property laws. Customers are prohibited to copy, forward or store MyPrivateBanking Products outside of the legal entity that has made the purchase.

MyPrivateBanking GmbH Hafenstrasse 50B CH-8280 Kreuzlingen, Switzerland Tel. +41 71 566 10 05

For our latest reports please check: http://www.myprivatebanking.com/Category/reports