Embed Size (px)

Citation preview

Minding your family business

Succession planning

Bob Rosone Director – Deloitte Growth Enterprise Services

Jamie Casey Tax Partner – Deloitte

Brian Raftery Trusts & Estates Partner – Herrick, Feinstein LLP

Commerce and Industry Association of New Jersey

February 6, 2014

2

“Houston, we have a problem.”

3

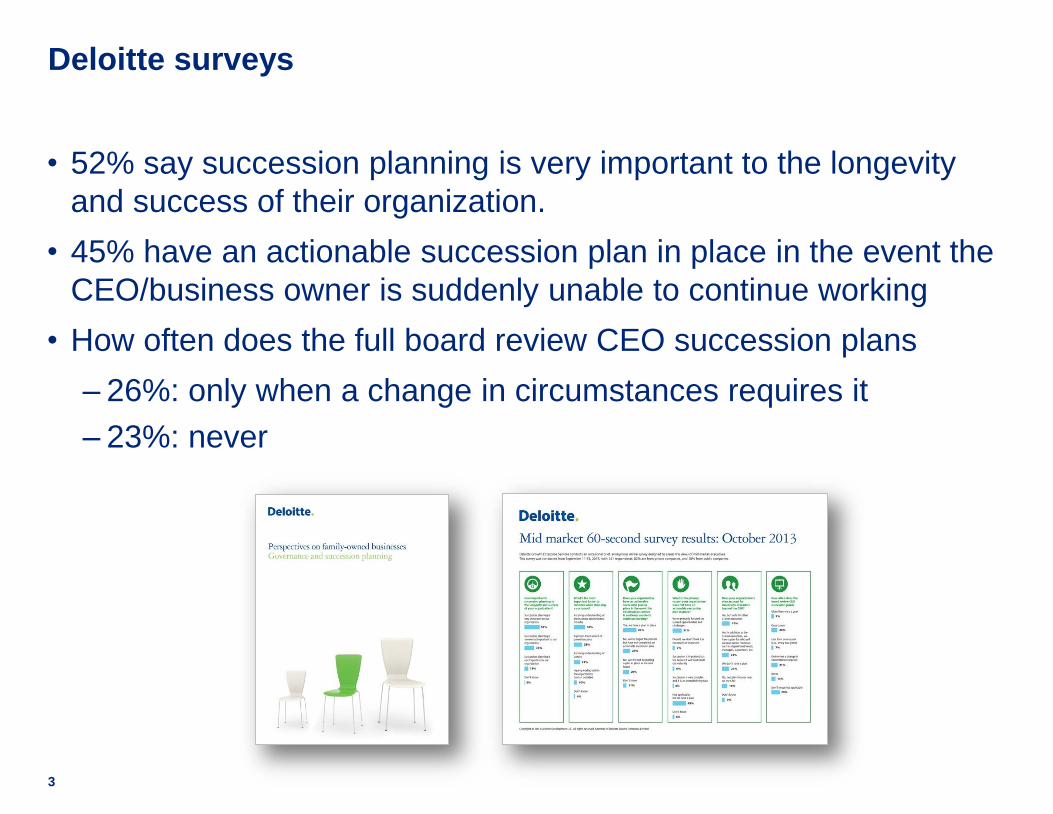

Deloitte surveys

• 52% say succession planning is very important to the longevity

and success of their organization.

• 45% have an actionable succession plan in place in the event the

CEO/business owner is suddenly unable to continue working

• How often does the full board review CEO succession plans

‒ 26%: only when a change in circumstances requires it

‒ 23%: never

4

The impact of succession planning on risk management

Succession planning

Operational

risk

Strategic

risk

Financial

risk

Reputational

risk

5

6

Areas for consideration

Determine goals and vision

Realistic current assessment

Understand additional family issues

Involve the board

It’s all about the people

Determine “ready now” and “ready later”

Communicate, communicate, communicate

Don’t stop

7

Timing is everything.

Income Tax planning

Jamie CaseyTax Partner – Deloitte

9

Succession planning – the journey

• How do we see succession planning?

‒ Orderly transition of management and ownership….

‒ A long-term process of developing successors while not being

disruptive to the business operations and value…

• A complex ongoing process involving multiple disciplines

‒ Manage complex relationships

• Family values

• Business objectives

• Personal finance

• Organizational and talent management

10

Critical areas to effective succession planning

Goal articulation

Business strategy

Management talent

Family communication

Corporate finance

Estate and gift planning

Life insurance analysis

Investment advisory

Shareholder agreements

Disability planning

Corporate structuring

Retirement planning

Business valuation

Compensation

Stock transfer techniques

Family offices

11

Succession planning

Our experience with the complex relationships

• When does the transition to a corporate establishment occur?

‒ Startup to national or global organization

• Aircraft and entertainment facilities

• Compensation and benefits arrangements

• Corporate governance

• Best practices to get started

‒ Experienced financial professionals

• CFOs play many roles

‒ Consistent family values and corporate objectives

• Community involvement

• Charity

• Personal financial objectives aren’t business drivers

12

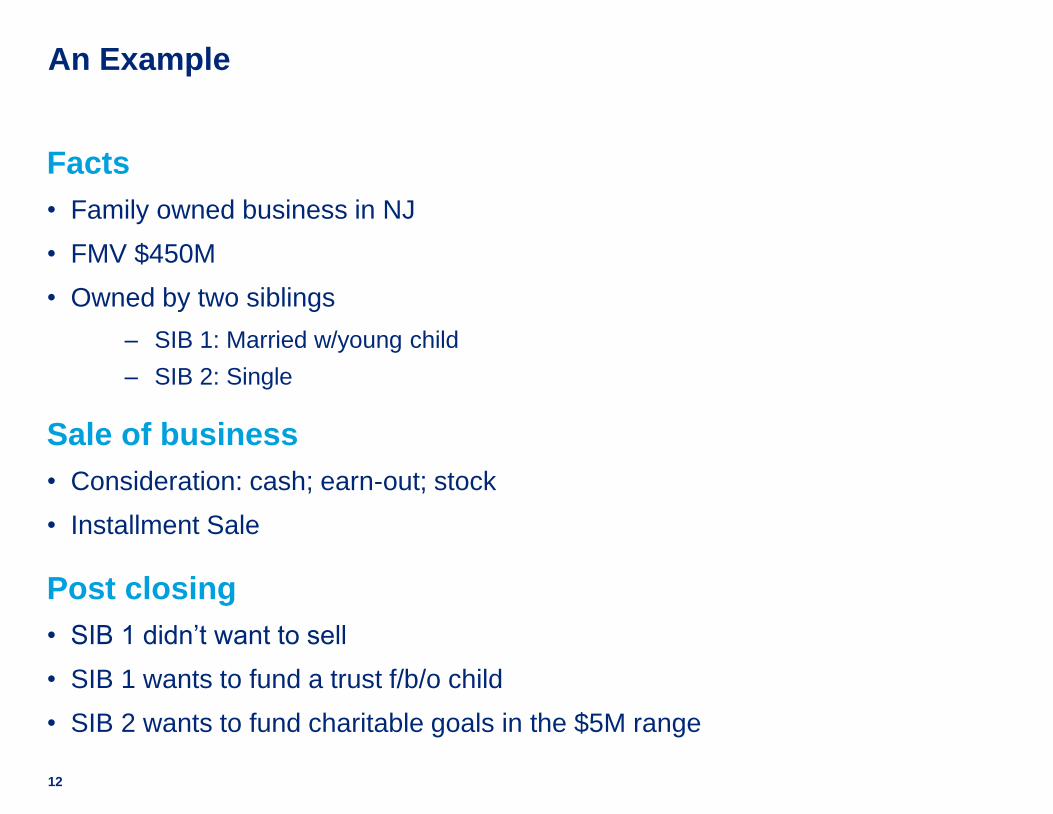

An Example

Facts

• Family owned business in NJ

• FMV $450M

• Owned by two siblings

‒ SIB 1: Married w/young child

‒ SIB 2: Single

Sale of business

• Consideration: cash; earn-out; stock

• Installment Sale

Post closing

• SIB 1 didn’t want to sell

• SIB 1 wants to fund a trust f/b/o child

• SIB 2 wants to fund charitable goals in the $5M range

13

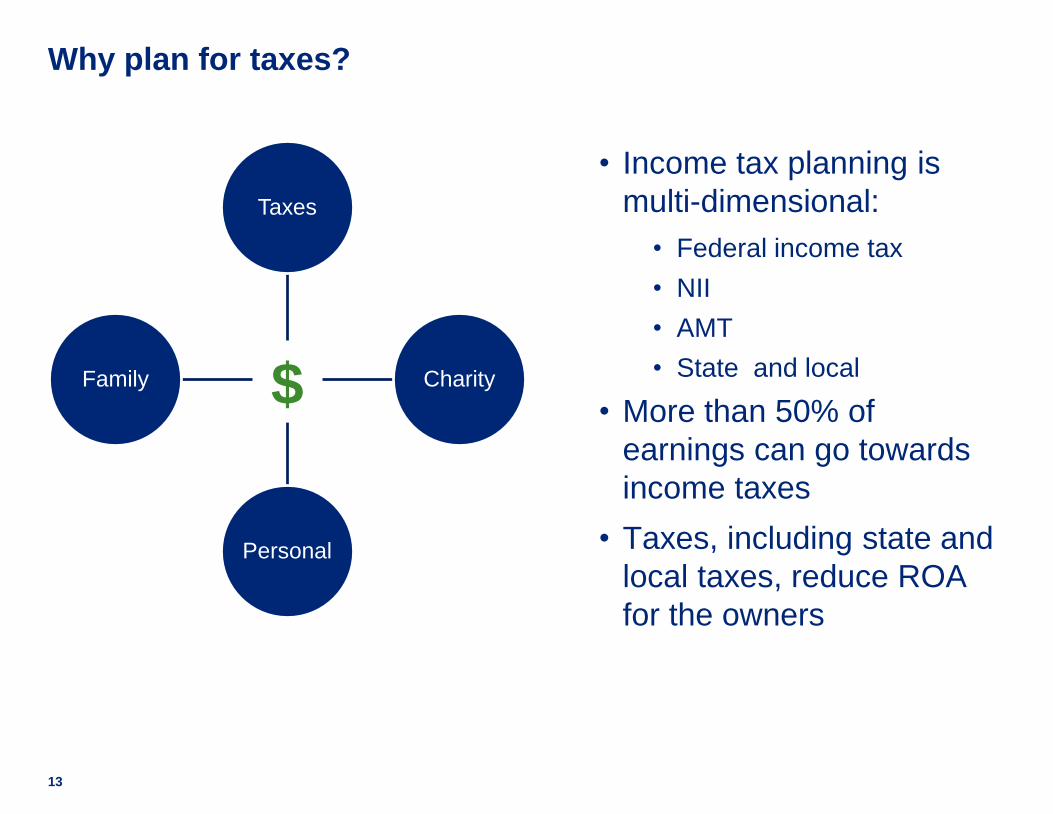

Why plan for taxes?

• Income tax planning is

multi-dimensional:

• Federal income tax

• NII

• AMT

• State and local

• More than 50% of

earnings can go towards

income taxes

• Taxes, including state and

local taxes, reduce ROA

for the owners

Taxes

Charity

Personal

Family $

14

Succession planning

The sale

39.6%

3.8%

8.97%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

=53.27%

NJ StateIncome Tax

HealthcareTax

NetInvestmentIncome TaxOrdinaryIncome

Long-TermCapital Gains

0.9%

20%

Provision 2014

Rates for ordinary income 15% - 39.6%

Top rate for long-term

capital gains

20%

Top rate for qualified

dividends

20%

AMT exception $51,900 (single filers)

$80,800 (joint filers)

Net Investment Income Tax

(NII Tax)

3.8% surtax on NII for

taxpayers with AGI over

$200,000 ($250,000 MFJ)

Additional FICA-Hospital

Insurance Tax (FICA-HI)

0.9% additional FICA tax for

taxpayers with wages or

self-employed income over

$200,000 ($250,000 MFJ)

15

When there is a sale

High level considerations when a sale is contemplated

Cash vs. stock received

• Risk/reward

• Liquidity

• Hedging

• Goals/objectives of seller

Selling Assets or Stock

• Purchase Price differential

• State taxes

• Will business assets be capital

gain property?

Installment sale

• Longer payout

• Opportunities for income tax

deferral

• Additional risk

Compensating key

stakeholders

• Are they owners of the business?

• Are there parachute agreements

in place?

• Plan early!

Estate planning

Brian RafteryTrusts & Estates Partner – Herrick, Feinstein LLP

17

Reasons for advanced estate planning

1. Federal Estate Tax

2. New Jersey Estate Tax

3. Federal Gift Tax

4. Generation-Skipping Transfer Tax (“GSTT”)

5. New Jersey Inheritance Tax

6. CREDITOR PROTECTION / DIVORCE PROTECTION /

ESTATE TAX PROTECTION FOR CHILDREN

18

Basic estate planning documents everyone needs

1. Last Will and Testament

2. Durable Power of Attorney

3. Health Care Proxy

4. Living Will

19

Estate tax issues

1. The federal estate tax applies to the date-of-death value of a U.S. citizen’s (and U.S. resident’s) worldwide property – not just property within the United States

2. The federal estate tax on $30,000,000 worth of property for a person who dies in 2014 would be about $14,000,000 or about 40%

• How would this tax be paid? Is the liquidity there?

• What can be done to reduce this tax?

3. There is a “step-up” in basis for inherited property which may ultimately reduce income taxes on the sale of such property

20

Gift tax issues

1. The U.S. has a “transfer tax” system which may tax property transferred on death OR property which is gifted during life

2. If “too much” property is gifted by Mr. Jones during his lifetime, then he may have to pay gift taxes

3. If property in excess of the “Annual Exclusion” (currently $14,000) is gifted by Mr. Jones to any one person in any one year, he begins to use-up his $5,340,000 lifetime gift tax exemption which, correspondingly, decreases his estate tax exemption

4. The same rates of tax apply for gift tax as for the estate tax

5. No “step-up” for gifts

21

Generation-skipping transfer tax issues

1. The “GSTT” is a separate tax which is in addition to the estate tax and gift tax

2. The GSTT applies to transfers, outright or in trust, during life or at death, to beneficiaries who are two or more generations below the transferor's generation. Such beneficiaries (for example, grandchildren) are called "skip persons”

• Types of “skips” include “direct skips”, “taxable distributions” and “taxable terminations”

3. The GSTT tax rate is equal to the highest estate tax rate –currently 40%

22

New Jersey inheritance tax issues

1. The New Jersey Inheritance Tax is a separate NJ state tax that is owed by the person receiving inherited property upon someone’s death

2. Applies to transfers for a brother or sister, niece or nephew – but not to a child, grandchild or spouse

3. Only a $500 exemption

4. Tax rates from 11% to 16% for a brother or sister

23

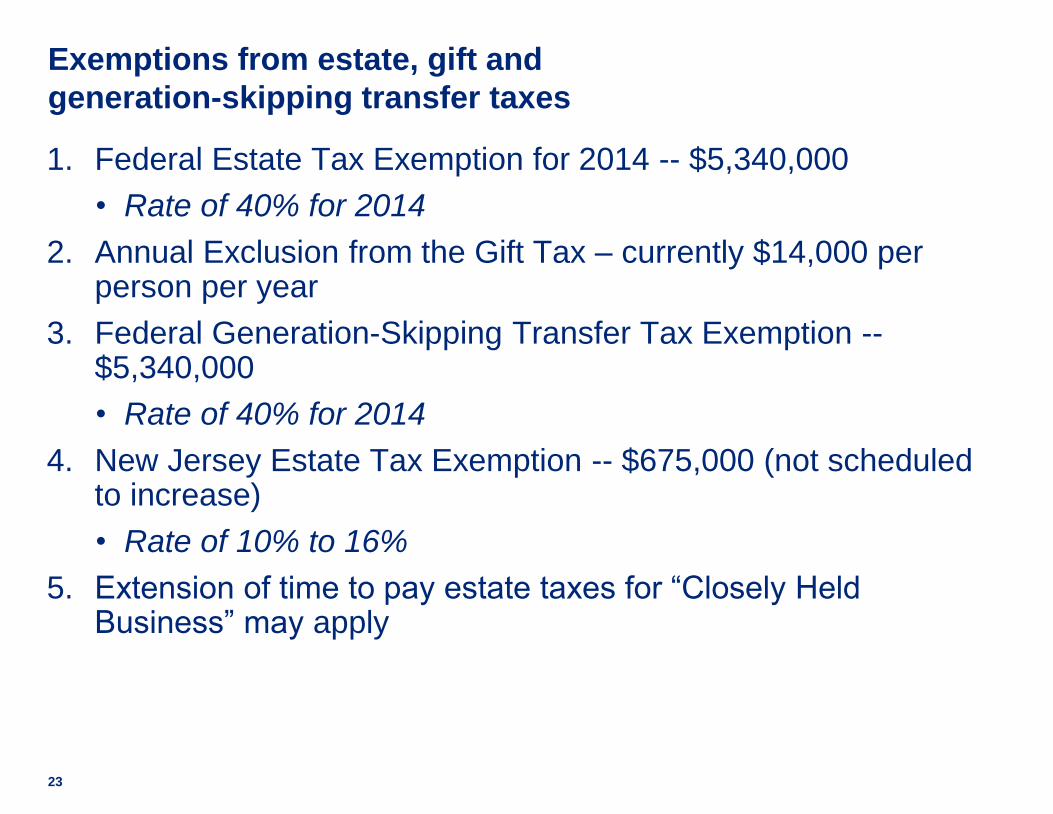

Exemptions from estate, gift and

generation-skipping transfer taxes

1. Federal Estate Tax Exemption for 2014 -- $5,340,000

• Rate of 40% for 2014

2. Annual Exclusion from the Gift Tax – currently $14,000 per person per year

3. Federal Generation-Skipping Transfer Tax Exemption --$5,340,000

• Rate of 40% for 2014

4. New Jersey Estate Tax Exemption -- $675,000 (not scheduled to increase)

• Rate of 10% to 16%

5. Extension of time to pay estate taxes for “Closely Held Business” may apply

24

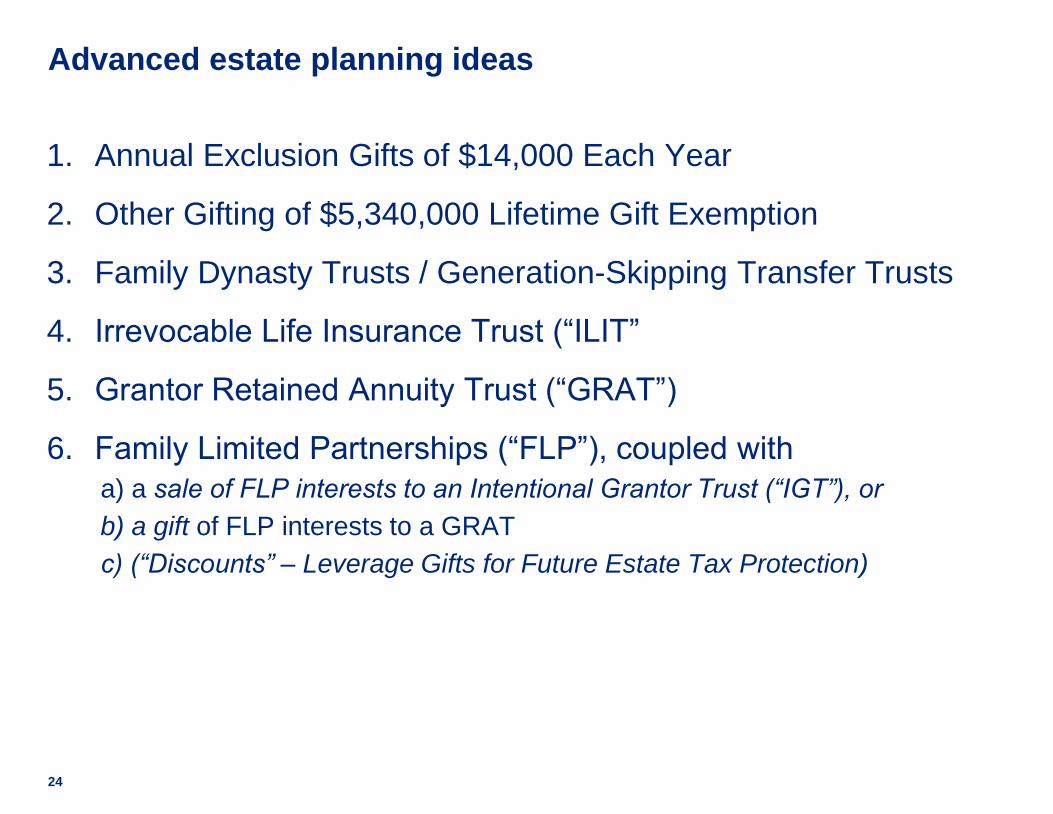

Advanced estate planning ideas

1. Annual Exclusion Gifts of $14,000 Each Year

2. Other Gifting of $5,340,000 Lifetime Gift Exemption

3. Family Dynasty Trusts / Generation-Skipping Transfer Trusts

4. Irrevocable Life Insurance Trust (“ILIT”

5. Grantor Retained Annuity Trust (“GRAT”)

6. Family Limited Partnerships (“FLP”), coupled with

a) a sale of FLP interests to an Intentional Grantor Trust (“IGT”), or

b) a gift of FLP interests to a GRAT

c) (“Discounts” – Leverage Gifts for Future Estate Tax Protection)

25

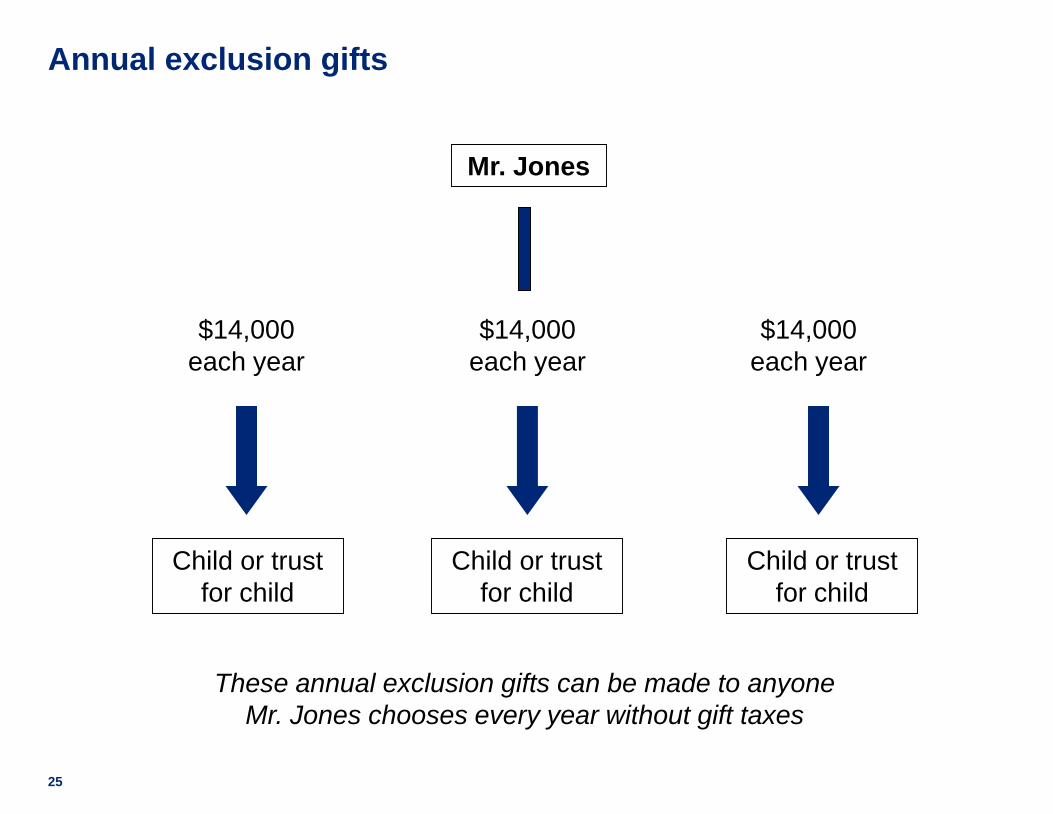

Mr. Jones

$14,000

each year

Child or trust

for child

These annual exclusion gifts can be made to anyone

Mr. Jones chooses every year without gift taxes

Annual exclusion gifts

$14,000

each year

$14,000

each year

Child or trust

for child

Child or trust

for child

26

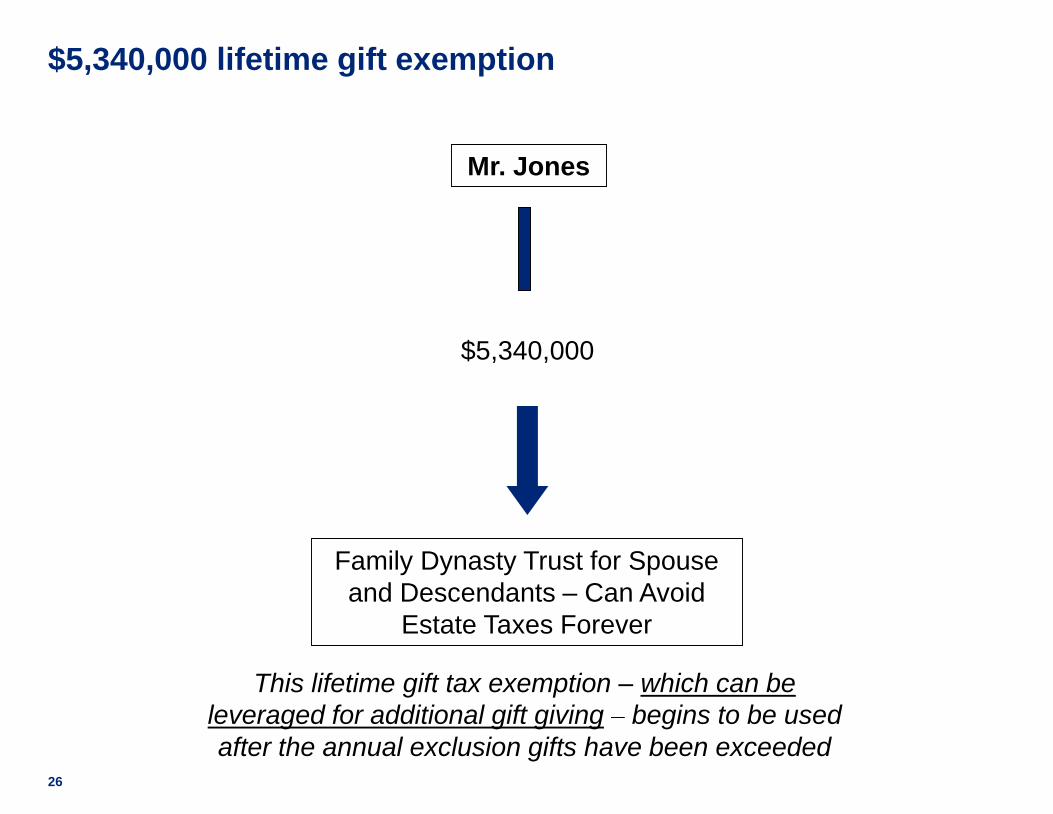

$5,340,000 lifetime gift exemption

Mr. Jones

This lifetime gift tax exemption – which can be

leveraged for additional gift giving – begins to be used

after the annual exclusion gifts have been exceeded

$5,340,000

Family Dynasty Trust for Spouse

and Descendants – Can Avoid

Estate Taxes Forever

27

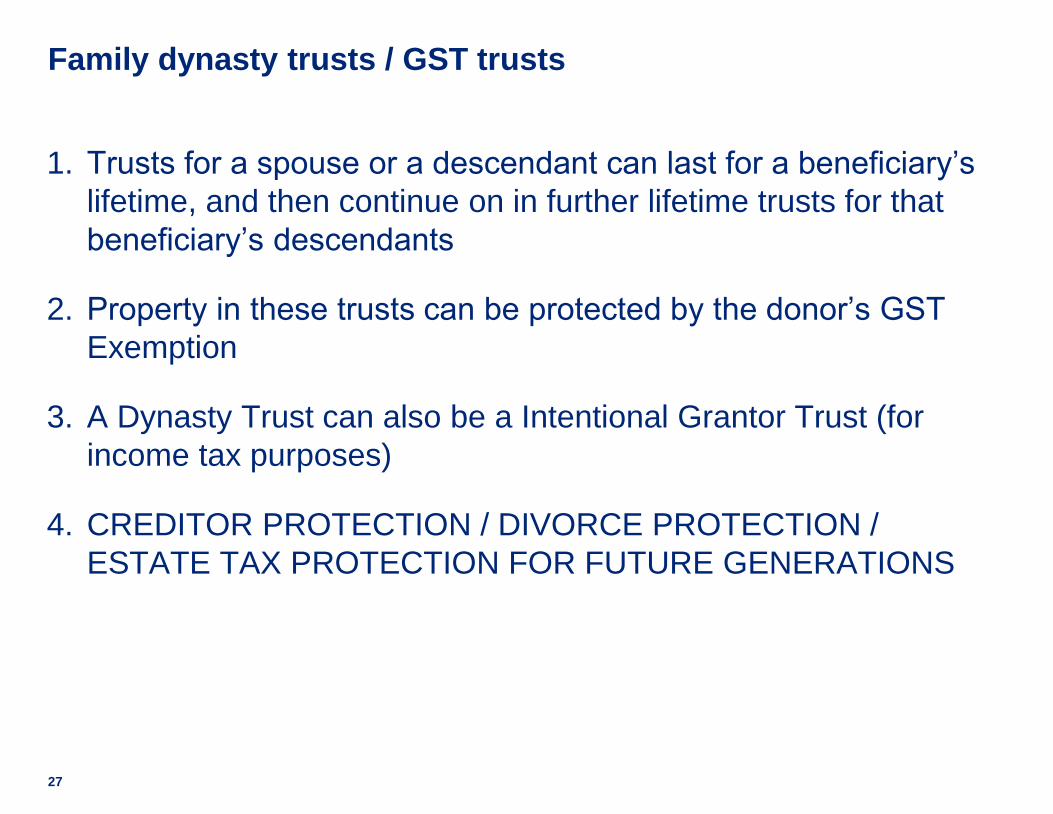

Family dynasty trusts / GST trusts

1. Trusts for a spouse or a descendant can last for a beneficiary’s

lifetime, and then continue on in further lifetime trusts for that

beneficiary’s descendants

2. Property in these trusts can be protected by the donor’s GST

Exemption

3. A Dynasty Trust can also be a Intentional Grantor Trust (for

income tax purposes)

4. CREDITOR PROTECTION / DIVORCE PROTECTION /

ESTATE TAX PROTECTION FOR FUTURE GENERATIONS

28

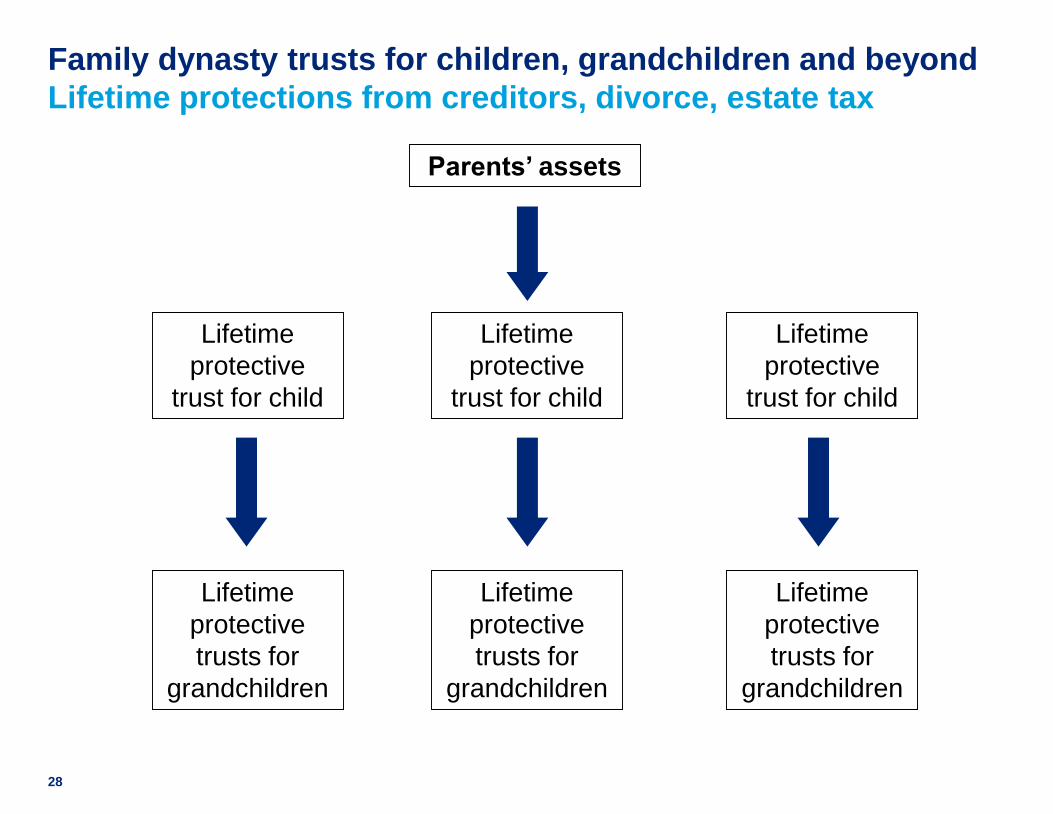

Family dynasty trusts for children, grandchildren and beyond

Lifetime protections from creditors, divorce, estate tax

Parents’ assets

Lifetime

protective

trusts for

grandchildren

Lifetime

protective

trusts for

grandchildren

Lifetime

protective

trusts for

grandchildren

Lifetime

protective

trust for child

Lifetime

protective

trust for child

Lifetime

protective

trust for child

29

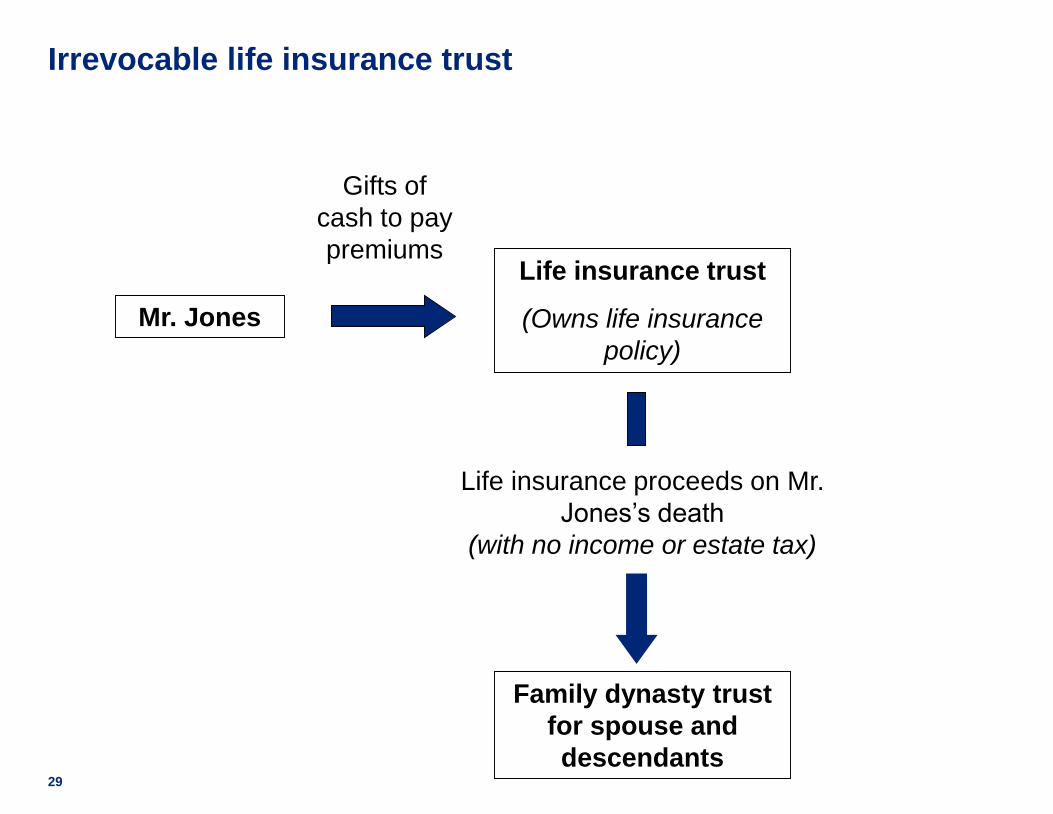

Mr. Jones

Life insurance trust

(Owns life insurance

policy)

Family dynasty trust

for spouse and

descendants

Life insurance proceeds on Mr.

Jones’s death

(with no income or estate tax)

Gifts of

cash to pay

premiums

Irrevocable life insurance trust

30

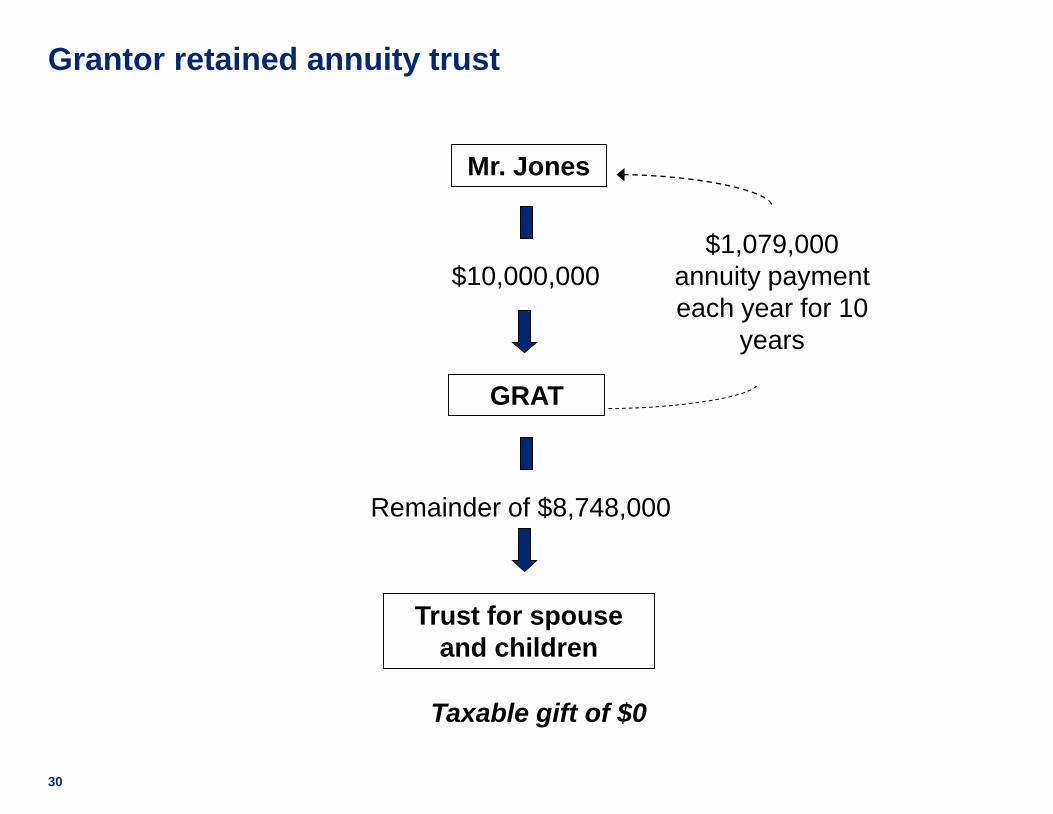

GRAT

Trust for spouse

and children

$10,000,000

Remainder of $8,748,000

$1,079,000

annuity payment

each year for 10

years

Taxable gift of $0

Grantor retained annuity trust

Mr. Jones

31

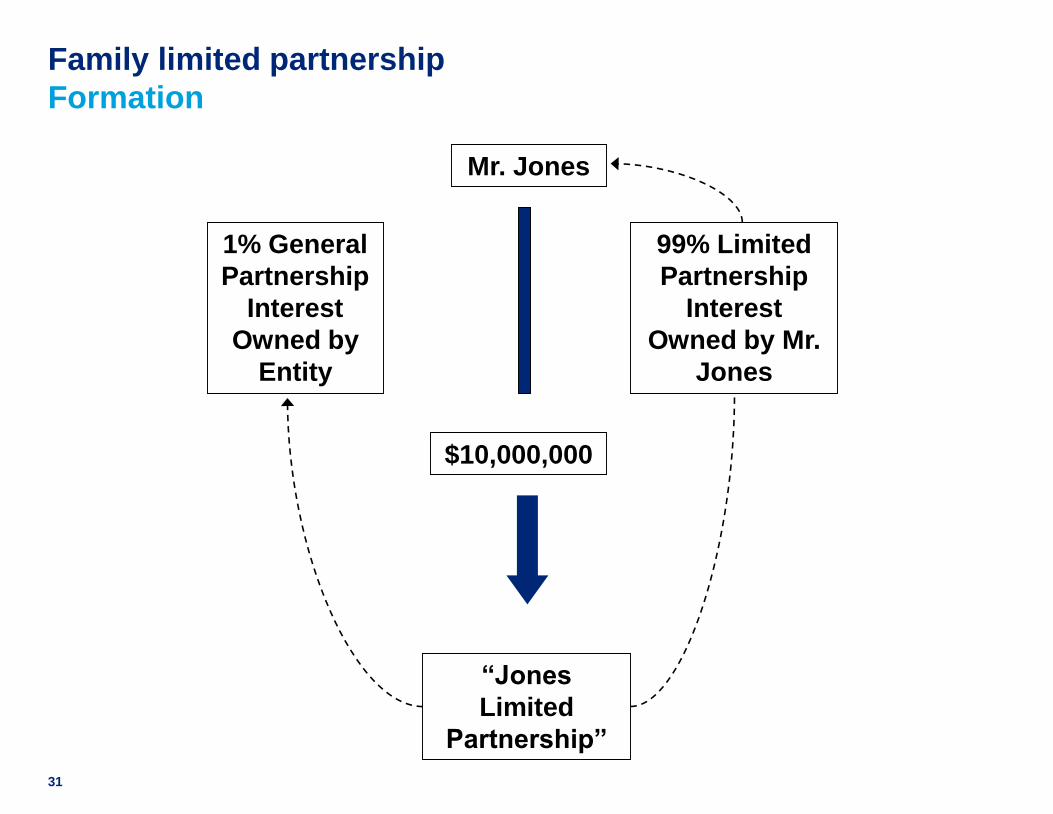

1% General

Partnership

Interest

Owned by

Entity

“Jones

Limited

Partnership”

99% Limited

Partnership

Interest

Owned by Mr.

Jones

$10,000,000

Family limited partnership

Formation

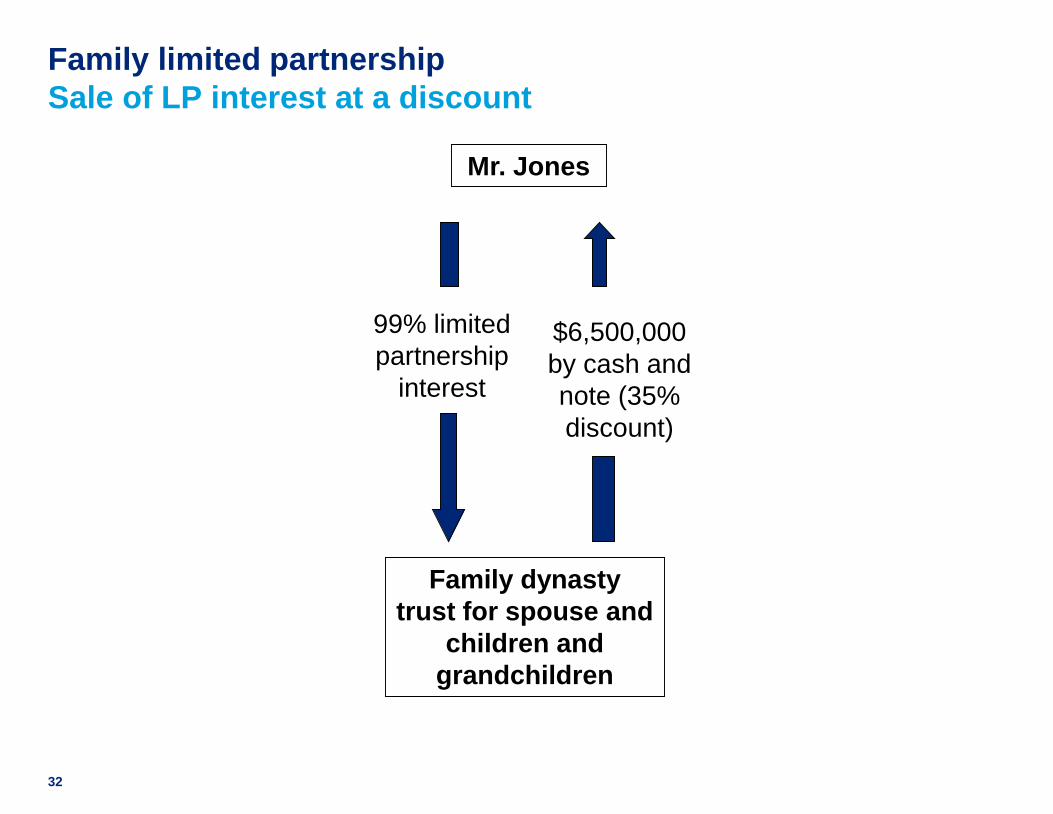

Mr. Jones

32

Family dynasty

trust for spouse and

children and

grandchildren

99% limited

partnership

interest

$6,500,000

by cash and

note (35%

discount)

Family limited partnership

Sale of LP interest at a discount

Mr. Jones

33

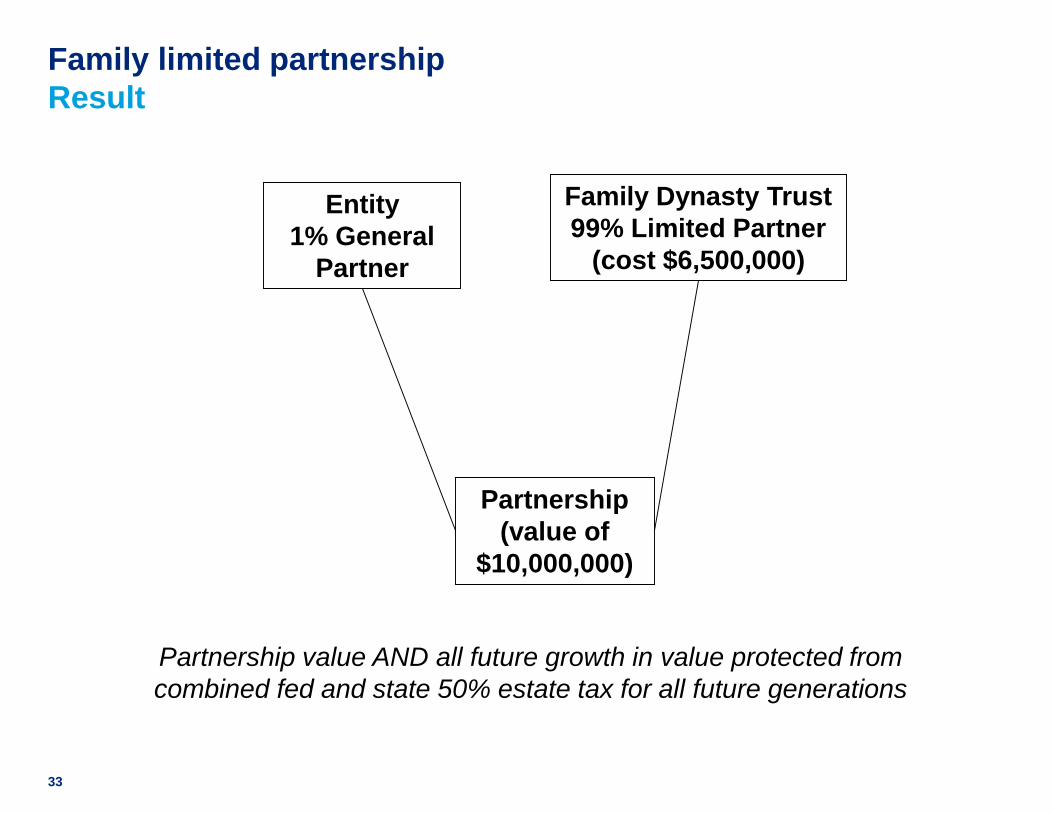

Entity

1% General

Partner

Family Dynasty Trust

99% Limited Partner

(cost $6,500,000)

Partnership

(value of

$10,000,000)

Partnership value AND all future growth in value protected from

combined fed and state 50% estate tax for all future generations

Family limited partnership

Result

For more information

Bob Rosone

Director, Deloitte Growth Enterprise Services

(973) 602-4370

Jamie Casey

Tax Partner – Deloitte

(973) 602-6013

Brian Raftery, Esq.

Trusts & Estates Partner – Herrick, Feinstein LLP

(973) 274-2022 / (212) 592-1508

About Deloitte

As used in this document, “Deloitte” means Deloitte & Touche LLP, Deloitte Tax LLP, Deloitte Consulting LLP, and Deloitte Financial Advisory Services LP, which are

separate subsidiaries of Deloitte LLP. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries.

Copyright © 2014 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited