Embed Size (px)

Citation preview

8/12/2019 Mena - Eapayment Booz - Leaving_Cash_Behind

http://slidepdf.com/reader/full/mena-eapayment-booz-leavingcashbehind 1/12

Perspective Ramez Shehadi

Lut Zakhour

Charles Habak

Leaving Cash BehindThe Rise of Electronic

Payments in theMENA Region

8/12/2019 Mena - Eapayment Booz - Leaving_Cash_Behind

http://slidepdf.com/reader/full/mena-eapayment-booz-leavingcashbehind 2/12

Booz & Company

Contact Information

Abu Dhabi

Lutf ZakhourSenior Associate

+971-2-699-2400

Beirut

Ramez Shehadi

Partner

+961-1-985-655

Dubai

Charles Habak

Associate

+971-4-390-0260

8/12/2019 Mena - Eapayment Booz - Leaving_Cash_Behind

http://slidepdf.com/reader/full/mena-eapayment-booz-leavingcashbehind 3/12

Booz & Company

EXECUTIVESUMMARY

For too long, governments and businesses in the Middle East

and North Africa (MENA) region have relied on cash to pay

their employees, make or receive payments, and fulll othernancial obligations. As a result, their economies have been

slowed by the negative side effects of needing cash on hand—

long lines and wait times, instances of delayed or missed

payments, and paper-based record-keeping, to name a few.

In recent years, though, some MENA countries have started

to turn to electronic payments to alleviate these constraints

and boost the efciency and transparency of their operations.

Governments have beneted by enhancing their liquidity

and opening the nancial system to a larger portion of their population. Businesses have lowered their costs of doing

business, while creating more secure and reliable means of

conducting transactions. Consumers have gained greater insigh

into their nances, along with reclaiming some of their lost time

As governments and businesses in MENA countries seek to

replicate the success of e-payments’ early adopters, how well

they fare will depend on the extent to which they are able to

spread the benets to these diverse stakeholders, account for

their specic needs, and actively involve them in the design

and implementation of e-payments systems.

8/12/2019 Mena - Eapayment Booz - Leaving_Cash_Behind

http://slidepdf.com/reader/full/mena-eapayment-booz-leavingcashbehind 4/12

Booz & Company22

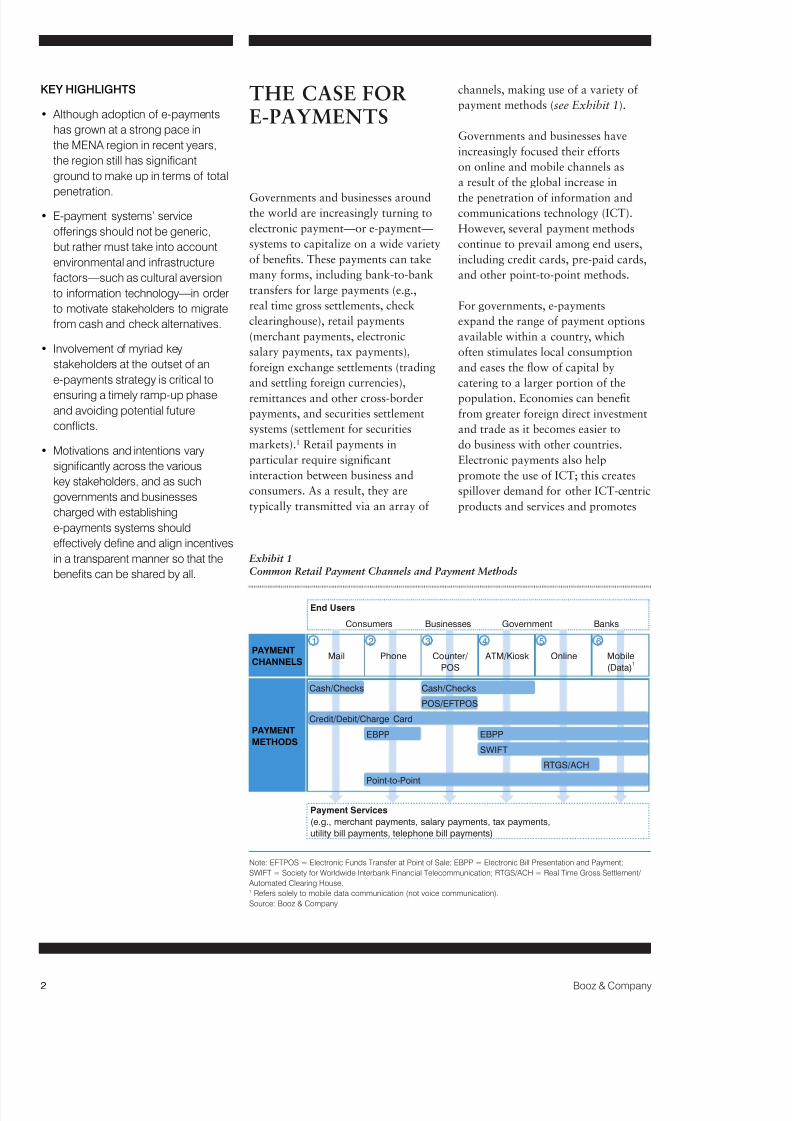

channels, making use of a variety of

payment methods (see Exhibit 1).

Governments and businesses have

increasingly focused their efforts

on online and mobile channels as

a result of the global increase in

the penetration of information andcommunications technology (ICT).

However, several payment methods

continue to prevail among end users,

including credit cards, pre-paid cards,

and other point-to-point methods.

For governments, e-payments

expand the range of payment options

available within a country, which

often stimulates local consumption

and eases the ow of capital by

catering to a larger portion of the

population. Economies can benet

from greater foreign direct investment

and trade as it becomes easier to

do business with other countries.

Electronic payments also help

promote the use of ICT; this creates

spillover demand for other ICT-centric

products and services and promotes

Governments and businesses aroundthe world are increasingly turning to

electronic payment—or e-payment—

systems to capitalize on a wide variety

of benets. These payments can take

many forms, including bank-to-bank

transfers for large payments (e.g.,

real time gross settlements, check

clearinghouse), retail payments

(merchant payments, electronic

salary payments, tax payments),

foreign exchange settlements (trading

and settling foreign currencies),

remittances and other cross-border

payments, and securities settlement

systems (settlement for securities

markets).1 Retail payments in

particular require signicant

interaction between business and

consumers. As a result, they are

typically transmitted via an array of

THE CASE FORE-PAYMENTS

KEY HIGHLIGHTS

• Although adoption of e-payments

has grown at a strong pace in

the MENA region in recent years,

the region still has signicant

ground to make up in terms of total

penetration.

• E-payment systems’ service

offerings should not be generic,

but rather must take into account

environmental and infrastructure

factors—such as cultural aversion

to information technology—in order

to motivate stakeholders to migrate

from cash and check alternatives.

• Involvement of myriad key

stakeholders at the outset of an

e-payments strategy is critical to

ensuring a timely ramp-up phaseand avoiding potential future

conicts.

• Motivations and intentions vary

signicantly across the various

key stakeholders, and as such

governments and businesses

charged with establishing

e-payments systems should

effectively dene and align incentives

in a transparent manner so that the

benets can be shared by all.

Note: EFTPOS = Electronic Funds Transfer at Point of Sale; EBPP = Electronic Bill Presentation and Payment;

SWIFT = Society for Worldwide Interbank Financial Telecommunication; RTGS/ACH = Real Time Gross Settlement/

Automated Clearing House. 1 Refers solely to mobile data communication (not voice communication).

Source: Booz & Company

Exhibit 1Common Retail Payment Channels and Payment Methods

PAYMENT

METHODS

End Users

Consumers Businesses Government Banks

PAYMENT

CHANNELSOnline

1 2 3 4 5

PhoneMail Counter/

POS

ATM/Kiosk

6

Mobile

(Data)1

Payment Services

(e.g., merchant payments, salary payments, tax payments,

utility bill payments, telephone bill payments)

Credit/Debit/Charge Card

Cash/Checks

RTGS/ACH

Point-to-Point

SWIFT

Cash/Checks

POS/EFTPOS

EBPPEBPP

8/12/2019 Mena - Eapayment Booz - Leaving_Cash_Behind

http://slidepdf.com/reader/full/mena-eapayment-booz-leavingcashbehind 5/12

Booz & Company

the growth of e-government services

and electronic services in general.

Businesses benet from e-payments

through lower costs by providing

secure, reliable, and efcient

alternatives to paper-based cash or

check payments. They can streamlinetheir collections processes and shorten

the time required to collect, resulting

in better working capital management

and greater visibility into provisioning

for bad debt. Businesses also enjoy

increased opportunities to better

target their sales and marketing, as

e-payments give them instant access

to data on customer segmentation.

E-payments enable nancial institu-

tions to better manage their loan

portfolios by giving them greater

insight into borrowing and spending

patterns. Furthermore, by encourag-

ing consumers to migrate to banking

services and channels, these institu-

tions increase their potential for

cross-selling or up-selling their prod-

ucts and services to new customers.

Finally, consumers enjoy greater con-

venience through multiple payment

channels, such as the Internet and

automated teller machines (ATMs).

These touch points give consumers

ready access to their account history

and fund transfers, and they reduce

the amount of cash consumers need

to keep on hand on a daily basis.

Such benets could substantially

change the way businesses and

governments operate in the Middle

East and North Africa (MENA)

region. MENA countries’ historical

reliance on paper-based nancial

systems has left them vulnerable to

a number of related inefciencies:

substantial numbers of employees

standing in line at month’s end

to receive their salaries in cash,

contractors issuing checks to pay their

suppliers, and residents traveling to

collection centers to pay their utility

bills through cash or check.

In recent years, though, the govern-

ment ofcials, business executives,

and consumers in these “cash and

check” environments have increas-

ingly been exposed to online paymen

channels, payment kiosks, and other

such e-payment options. As a result,

these countries are picking up the

pace of their e-payments investment

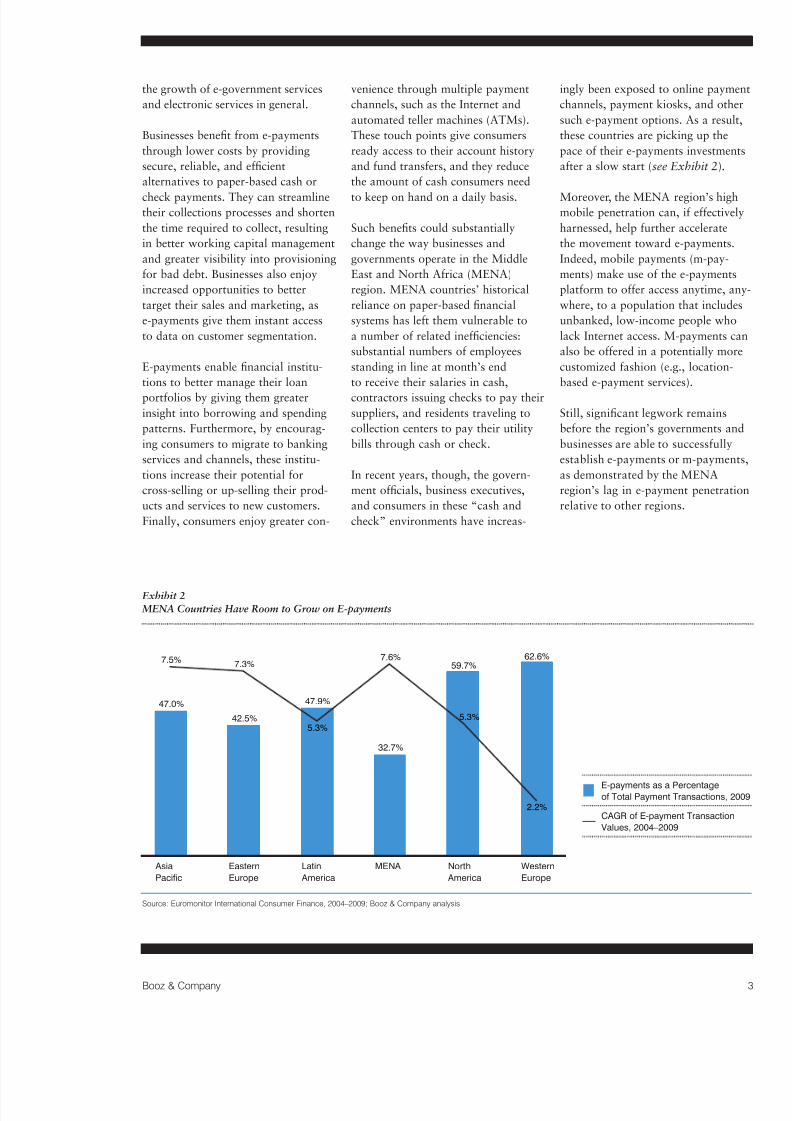

after a slow start (see Exhibit 2).

Moreover, the MENA region’s highmobile penetration can, if effectively

harnessed, help further accelerate

the movement toward e-payments.

Indeed, mobile payments (m-pay-

ments) make use of the e-payments

platform to offer access anytime, an

where, to a population that includes

unbanked, low-income people who

lack Internet access. M-payments ca

also be offered in a potentially more

customized fashion (e.g., location-

based e-payment services).

Still, signicant legwork remains

before the region’s governments and

businesses are able to successfully

establish e-payments or m-payment

as demonstrated by the MENA

region’s lag in e-payment penetratio

relative to other regions.

Source: Euromonitor International Consumer Finance, 2004–2009; Booz & Company analysis

Exhibit 2 MENA Countries Have Room to Grow on E-payments

E-payments as a Percentageof Total Payment Transactions, 20

CAGR of E-payment Transaction

Values, 2004–2009

7.3%7.5%

42.5%

47.0%

62.6%59.7%

32.7%

47.9%

2.2%

5.3%

7.6%

5.3%

Asia

Pacific

Eastern

Europe

Latin

America

MENA North

America

Western

Europe

8/12/2019 Mena - Eapayment Booz - Leaving_Cash_Behind

http://slidepdf.com/reader/full/mena-eapayment-booz-leavingcashbehind 6/12

Booz & Company4

No single formula exists to establish

and sustain a healthy e-payments

ecosystem within any given country,

sector, or community. Ultimately, such

an ecosystem’s success depends on the

degree to which it caters to end users

and accommodates country-specic

factors. The optimal e-payments

ecosystem incorporates all of the

relevant players and considerations at

the various layers of engagement

(see Exhibit 3).

The outer layer represents the

end users—the beneciaries of

e-payments. Meeting users’ needs

is essential in e-payments, with

end users primarily consisting of

government entities, businesses,

consumers (e.g., citizens or residents),

THE E-PAYMENTSECOSYSTEM

Exhibit 3The E-payments Ecosystem

Source: Booz & Company

E-payment

Stakeholder

Partnership

Model

E-payment

Service

Offering

E-payment

Internal

Operating

Model

B u s i n e s s e s

Go vernme n t

C u l t u r a l / So c i a l T r a i t s

I C T I n

f r a

s t r u c t u

r e

L e g a l

F r a m

e w

o r k

C o nsume r s

End Users

Environment and Infrastructure

Business Model

F i n a n c

i a l

I

n s t

i t

u t i o

n s

8/12/2019 Mena - Eapayment Booz - Leaving_Cash_Behind

http://slidepdf.com/reader/full/mena-eapayment-booz-leavingcashbehind 7/12

Booz & Company

or nancial institutions that serve as

either recipients or payers.

The “environment and infrastructure”

layer reects the underlying

elements that either stimulate or

limit the adoption of e-payments.

These elements include the legal

framework governing the provision

and use of e-payments, cultural and

social traits that help to drive the

preferred e-payment channels, and

the ICT infrastructure for delivering

e-payments in a cost-effective manner.

Finally, the core represents the

e-payment business model, which

takes the other two layers into account

in building the e-payments foundation

through three primary means:

• E-payment service offering—i.e.,

services to be offered, payment

channels available to transmit

the payment (e.g., online, mobile

network, ATM switch, etc.), and

payment methods available for end

users to perform the payment (e.g.,

credit card, charge card, pre-paid,

or point-to-point)

• Stakeholder partnership model—

i.e., stakeholders to involve in

the provision of services, type of

partnership structures to select, and

fee structure

• E-payment service providers’

internal operating model required

to best provision the services

Governments and businesses seeking

to replicate this business model must

work to ensure that the e-payment

service offering fully aligns with

market demand, as well as environ-

ment and infrastructure factors.

MENA consumers’ lack of trust

in technology or limited access to

nancial institutions may signicantly

reduce their use of e-payment services

if those services are offered through

bank accounts, online channels, and

other delivery means that are simply

borrowed from more developed

regions, without any consideration

for local context.

Unlike typical business-to-business o

business-to-consumer services that ar

provided through common enterpris

applications or e-commerce solu-

tions—such as sales, order status, or

customer prole updates—the provi-

sioning of e-payments involves myria

stakeholders with differing incentive

and agendas. This complexity natu-

rally renders the level of engagement

and partnership across stakeholders a

one of the most sensitive and crucial

elements in the sustained success of

e-payments.

Key stakeholders generally consist

of a combination of governments,

businesses, service providers, and

consumers.

Government players typically include

central banks, departments of nanc

8/12/2019 Mena - Eapayment Booz - Leaving_Cash_Behind

http://slidepdf.com/reader/full/mena-eapayment-booz-leavingcashbehind 8/12

Booz & Company6

and/or other government entities seek-

ing to streamline payments. Often,

these entities play the dual role of

collector and payer, making the use of

e-payments systems ideal for collecting

taxes and customs charges, transfer-

ring budgets, and paying suppliers.

These stakeholders are willing to

invest to move their customers to

e-payment channels, but they require

signicant increases in internal efcien-

cies to offset the up-front investment

in the e-payment systems and ongoing

transaction costs to various service

providers (e.g., nancial institutions).

Businesses use e-payments to pay

salaries and suppliers, and to col-

lect payments from end-customers

and downstream partners. Like their

government counterparts, busi-

nesses often have high expectations

for savings derived from e-payments

investments, and they face the same

challenges in recouping their costs.

Service providers such as nancial

institutions often play an enabling

role by offering consumers bank

accounts, which serve as the plat-

form to receive and send e-payments.

Telecom operators or stand-alone

e-payment providers support the

ecosystem by enabling transactions to

take place. Service providers normally

use e-payments to generate direct and

indirect revenues from transaction

fees or cross-selling opportunities.

Complicating matters further in

the MENA region is the fact that

electronic payment services com-

panies can be privately or publicly

owned—or a combination of the two.

In Egypt, for example, the e-payment

company was created through a

public–private partnership, though

it is was recently nationalized by the

government.

Finally, consumers turn to e-payments

to facilitate a variety of transactions,

ranging from retail purchases to util-

ity bill payments. The most important

factors for consumers are ease of use

and reasonably low transaction costs.

Businesses have high expectationsfor savings derived from e-payments

investments.

8/12/2019 Mena - Eapayment Booz - Leaving_Cash_Behind

http://slidepdf.com/reader/full/mena-eapayment-booz-leavingcashbehind 9/12

Booz & Company

pensioners to withdraw their pensions

through ATMs would create social

discontent due to their low levels of

technology familiarity, as well as the

limited availability of ATMs.

Rather, the Ministry chose to develop

a “halfway solution” whereby eachpensioner was issued a banking card

to withdraw pensions from manned

point-of-sales terminals. Pensioners

can visit any pension outlet, swipe

their card, and punch in their four-

digit code to view their balance

and withdraw funds. All the while,

the teller is there to support them,

answering any questions or simply

providing elderly pensioners with the

human interaction to which they had

grown accustomed.

Although ATMs are being deployed

with the hopes of slowly migrating

pensioners to purely electronic

channels, the near-term solution has

already reduced waiting times from

hours to minutes.

Actively Involve Key Stakeholders

Creating and maintaining an

e-payments system encompasses a

number of diverse stakeholders, andthe level of involvement of each can be

a sticking point if potential conicts

aren’t addressed at the outset.

One proven strategy is to formally

include key stakeholders in the

governance of the e-payments

provider, be it through shared

ownership (e.g., transaction or equit

based) or through participation as

members of the board or steering

committee. Stakeholders are often

disinterested at the outset of an

e-payments investment because it is

perceived as just another IT initiativEarly participation helps identify th

full scope of e-payments activities a

their benets up front, rather than

at an inconvenient point later in the

process. Areas that are often missed

include potential earnings from

cross-selling opportunities, as well a

the level of control that e-payments

systems allow, particularly when it

comes to collecting taxes and other

payments.

Involving stakeholders on the front

end also helps to ensure that the

benets of an e-payments system

reach the largest audience possible.

The government of Abu Dhabi’s

approach to modernizing customs

payments is a case in point. Abu

Dhabi, like many governments

in the MENA region, historically

mandated that customs payments b

made by cash or check. As a result,

importers had to carry large sums

of cash on hand, and either enduresignicant delays in withdrawing

cash onsite or perform payments at

a later date. This process resulted in

long delays before the government’s

customs or nance departments

received payments, while bad debt

accumulated on their books.

Creating an e-payments system that

incorporates country-specic factors

and appeals to diverse end users can

be a difcult task, but select cases

from the MENA region illustrate

how governments and businesses

can achieve this necessary balance.

These examples illustrate three best

practices: rationalize service offerings,

actively involve key stakeholders, and

align stakeholder incentives.

Rationalize Service Offerings

The design of e-payments service

offerings must account for the

country’s specic supply and demand

landscapes; failure to do so often leads

to the creation of new services that go

largely unused.

For example, until recently, up to 7million people in Egypt received their

pensions in cash on a monthly basis.

This process involved withdrawing

large bundles of cash, paper-based

record keeping, and long lines. The

Egyptian government, via the Ministry

of Finance, realized that forcing

BESTPRACTICES INIMPLEMENTINGE-PAYMENTS

8/12/2019 Mena - Eapayment Booz - Leaving_Cash_Behind

http://slidepdf.com/reader/full/mena-eapayment-booz-leavingcashbehind 10/12

Booz & Company8

Rather than tackle the customs

payment issue alone, the government

of Abu Dhabi in 2007 launched

a government-wide e-payments

platform in partnership with a local

telecom operator, Etisalat. The

Department of Finance dened the

business needs that the e-payment

system would have to meet, thus

helping to determine the platform’s

service offerings; Etisalat designed,

implemented, and hosted the

platform; and the overall strategy for

the e-payment platform was aligned

with the larger e-government agenda.

The government involved its partners

early in the planning process in orderto ensure that problems would be

avoided or addressed quickly rather

than cropping up in later stages.

The customs department was the rst

government entity to use the system,

which quickly extended to other

areas of the government’s operations.

For example, the e-payments system

paved the way in 2008 for the

government to launch its gold card

program, which provides importers

and exporters with more convenienttracking and enhanced security of

their shipments.

The Abu Dhabi government is

also exploring future payments

through mobile, bill aggregators,

and additional counter-channels

to further leverage its single,

centralized e-payments platform.

Align Stakeholder Incentives

E-payments systems rarely succeed

when they are structured in such a way

that only a minority of stakeholders

sees the benets. Governments and

businesses charged with establishing an

e-payments platform should therefore

consider what motivates each stake-

holder and structure the system so that

the benets can be shared by all. This

can be done by quantifying the value

of e-payments and developing a fee

structure or revenue-sharing split in a

transparent and win-win fashion. But

it can also be accomplished by ensur-

ing that each stakeholder shares in thevalue proposition of participating in

an e-payments network.

When the Saudi government, via the

central bank (Saudi Arabian Monetary

Agency, or SAMA), was developing

the value proposition for SADAD, its

e-payment platform, it used stakehold-

ers’ current transaction costs to deter-

mine its pricing. By consulting with

billers (i.e., utility providers, telecom

operators, and insurance companies)

and banks about what it would costto implement payment systems and

services, SAMA was able to reach out

to these critical participants and assure

them that adopting the e-payment

platform would actually reduce their

overall transactions costs. It would

also offer the network scale advantages

of a national payment platform

accessible to all.

Governments and businesses in the

MENA region are increasingly turn-

ing to e-payments to better manage

their working capital and operate

more efciently. In due course, the

shortcomings of cash-based socie-

ties—long lines, missed payments,

and lost time—will be replaced by the

efciencies and increased transpar-ency of the digital age.

For e-payments systems to truly

gain traction, however, the benets

must extend beyond those making

the investment. Service providers,

nancial intermediaries, government

agencies, and consumers all have

something to gain as long as an e-pay-

ments platform actively involves them

from the start. The region has already

seen its fair share of e-payment con-

versions. With a continued focus on

serving the needs of key stakeholders

and customizing e-payments offerings

to local conditions, these stories will

be the rule, and not the exception.

CONCLUSION

8/12/2019 Mena - Eapayment Booz - Leaving_Cash_Behind

http://slidepdf.com/reader/full/mena-eapayment-booz-leavingcashbehind 11/12

Booz & Company

About the Authors

Ramez Shehadi is a partner

with Booz & Company inBeirut. He leads the information

technology practice in the

Middle East. He specializes

in e-government, e-business,

and IT-enabled transformation,

helping private corporations

and government organizations

leverage technology, achieve

operational efciencies, and

improve governance.

Lutf Zakhour is a senior asso-

ciate with Booz & Company in

Abu Dhabi. He specializes in

e-payment strategy and imple-

mentation, IT services strategy,

and technology-enabled trans-

formation for governments and

enterprises.

Charles Habak is an associate

with Booz & Company inDubai. He specializes in sector

development strategy, public–

private partnership launch

strategy, and technology-

enabled transformation for

governments and enterprises.

Endnotes

1 The World Bank Group, “Payment Systems Worldwide:

Outcomes of the Global Payment Systems Survey 2008.”

8/12/2019 Mena - Eapayment Booz - Leaving_Cash_Behind

http://slidepdf.com/reader/full/mena-eapayment-booz-leavingcashbehind 12/12

![Zorgbehoeftenonderzoek [BOOZ]t](https://img.dokumen.tips/doc/110x75/557807f9d8b42aa5488b4e2b/zorgbehoeftenonderzoek-boozt.jpg)

![Omgevingsanalyse [BOOZ]t](https://img.dokumen.tips/doc/110x75/557807f7d8b42aa5488b4e29/omgevingsanalyse-boozt.jpg)

![Ouderenbehoeftenonderzoek [BOOZ]t](https://img.dokumen.tips/doc/110x75/557807fdd8b42aa5488b4e2d/ouderenbehoeftenonderzoek-boozt.jpg)