Embed Size (px)

Citation preview

Member Information Session – March 2014

WELCOMETomo Matesic – Board Chair

Objectives• To provide members with information

on the partnership discussions between Mainstreet and Lambton Financial Credit Unions

• To discuss the potential benefits of a combined credit union

• Take your questions and receive your feedback

AMALGAMATION OVERVIEW

Janet Grantham – President and CEO

AmalgamationThe Boards of Directors of

Mainstreet Credit Union and Lambton Financial Credit Union have

entered in to an agreement to amalgamate our credit unions as of

May 31, 2014

Guiding Principles• Merger must create tangible value

and benefit to our members• Staff will be our champions and must

see the benefits for the members, the credit union and themselves

• We will retain our skilled and valued staff

• Build a future credit union based on mutual gains – creation not a negotiation

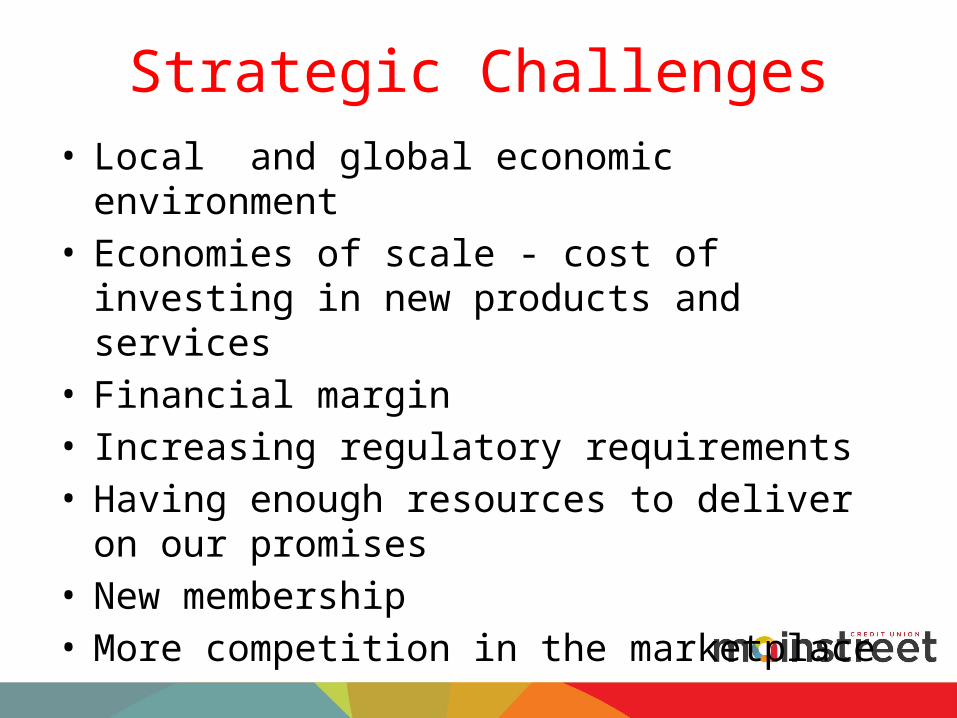

Strategic Challenges• Local and global economic environment• Economies of scale - cost of investing in

new products and services• Financial margin• Increasing regulatory requirements• Having enough resources to deliver on our

promises• New membership• More competition in the marketplace

Ontario Credit Union System

• 164 credit unions in 2008• 105 credit unions in 2013 • 6 mergers have already been announced

in 2014• Mainstreet is 19th largest in Ontario• New Mainstreet will be 15th largest in

Ontario

Rationale The merger will create new economies

of scale that will drive enhanced profitability and the ability to invest in expanded services that all credit unions require, such as: • data management• banking systems• enhanced products and services• networks• compliance oversight• aligns with our current strategic plan

Overview of Lambton Financial• 5 branches – all in the Sarnia area

• 60 employees• $210 million in assets• $30 million commercial loan portfolio• $60 million mutual fund portfolio• More liquid than Mainstreet

ComparisonAs at December 31, 2013

Mainstreet Lambton

Members 13,300 8,000

Residential Mortgages 54.68% 53.55%

Commercial and Agriculture Loans

25.82% 14.93%

Mutual Funds $22.5 Million $60 Million

Registered Deposits 35.93% 23.62%

Retained earnings 4.33% 7.62%

Capital 6.71% 8.22%

Return on assets* .19% .46%

Delinquency .77% .39%

Efficiency ratio 91.75% 88.31%

Liquidity 9.04% 14.29%*.29% before merger costs for Mainstreet

Branch Locations

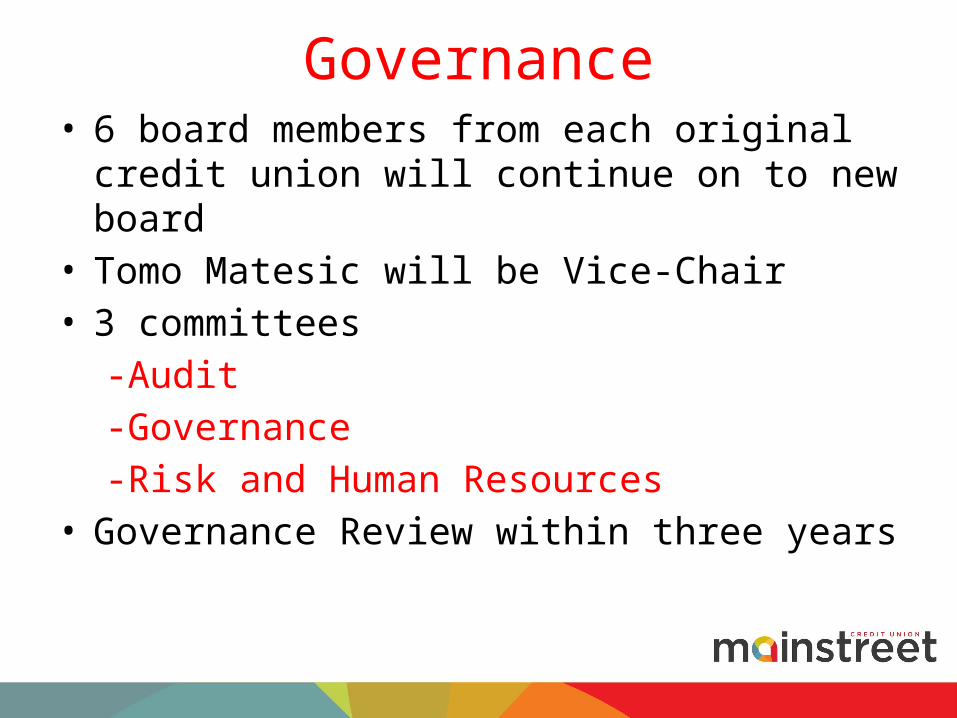

Governance• 6 board members from each original credit

union will continue on to new board• Tomo Matesic will be Vice-Chair• 3 committees

-Audit-Governance-Risk and Human Resources

• Governance Review within three years

Leadership

Janet Grantham President and Chief Executive Officer

Bob FerrisExecutive Vice President - Strategy &

Operations

Shawn Bustin Executive Vice President - Sales &

Member Service

Benefits to Members• Increased lending limits• Access to more branches – 13 versus 8• Better able to…

- Manage the risks in an increasingly competitive and complex market

- Provide enhanced levels of specialized expertise by reallocating resources

- Deliver more responsive advisory services- Provide greater returns to members and

our communities

Financial Benefits for Members

Projected Mainstreet

Projected New Mainstreet

Return on Assets .46 .51

Capital 7.05 7.40

Efficiency 78.76 77.68

New Mainstreet Projections

2013 Yearend Combined

2018 Yearend Combined

Increase or Decrease

Assets $542,675,000 $688,759,000 26.92%

Capital 7.18% 7.40% 0.22%

Efficiency Ratio 89.26% 77.68% -11.58%

Return on Assets

0.26% 0.51% 0.25%

Incremental Financial Benefit Annually

$1,400,000 $1.4 million annually

Benefits for Staff• No jobs will be lost • No branch closures• Increased opportunities for employees• Minimal change at Senior Management

level• Will benefit from what we learned this

past year• No banking system conversion

VisionThe new Mainstreet will…

• Have strong relationships with our members

• Retain a strong local presence in each of our communities

• Be nimble and responsive to local needs

• Employ and retain exceptional staff who are committed to investing in our members and our communities

Annual General andSpecial Member Meetings

April 28 @ 7:00pmMount Brydges

Community Center

QUESTIONS?

For more information or further questions www.cupartnership.ca

THANK YOU