Embed Size (px)

Citation preview

U T R E C H T U N I V E R S I T Y

Faculty of Law, Economics and Governance

International Economics and Business

International Management

MASTER THESIS

Marek Cech

Logit Model Analysis:

Does the Merger-Related Legislation in the Nation of the M&A Target

Company Affect the Probability of the Pre-Merger Deal Failure?

July 31, 2016

Abstract The paper examines the relationship between the nation of an M&A transaction’s

target company and the probability of deal completion/ pre-merger failure based on a sample of

transactions proposed by Dutch bidders during the period ranging from 2003 to 2015 with other

Dutch companies; British (UK); or American (US) targets. By the logistic regression analysis, the

US-targeted deals were found to be associated with higher probabilities of pre-merger failure

which is aimed to be explained by applying a mediation analysis of several country-specific

indicators potentially affecting the deal completion. This way, four factors which are addressed in

the theoretical part of the paper (including the restrictiveness of the merger control mechanisms,

effectiveness of corporate-related legislation and the time and complexity of contract

enforcement) were found to be the mediators of the relationship between the target nation and

pre-merger failure. Additionally, according to the regression results, transactions conducted

during the end of a merger wave are expected to be less likely completed than the ones

negotiated in the earlier or later stages, regardless of the target nation.

Keywords merger control, deal completion

JEL Classifications K21, M21

Acknowledgements Comments, remarks and advices by the supervisor of this thesis, dhr. drs.

Erik Dirksen, are gratefully acknowledged.

2

Table of contents

List of Tables ………………………………………………………………………………….. 4

List of Figures ………………………………………………………………………………… 5

List of Acronyms ……………………………………………………………………………… 6

1 Introduction ……………………………………………………………………………….. 7

2 Literature Review …………………………………………………………………………. 10

3 Merger Regulation ………………………………………………………………………… 13

3.1 Antitrust Laws in the USA ……………………………………………………………. 13

3.1.1 The Sherman Act ………………………………………………………………… 13

3.1.2 The Federal Trade Commission Act ……………………………………………... 15

3.1.3 The Clayton Act …………………………………………………………………. 15

3.1.4 Federal Trade Commission Cases and Proceedings ……………………………… 16

3.2 Merger Regulation in the EU …………………………………………………………. 19

3.2.1 Criteria for the EU Merger Regulation to Apply …………………………………. 19

3.2.2 The EU Merger Regulation Notification, Investigation and Penalties ……………. 20

3.2.3 The EU Merger Regulation Statistics …………………………………………….. 22

3.3 Comparison of the EU and US Merger Control Mechanisms …………………………. 24

4 Takeover Defense Tactics ………………………………………………………………… 26

4.1 Dual-class Shares ……………………………………………………………………… 26

4.2 ESOP …………………………………………………………………………………. 27

4.3 Poison Pills …………………………………………………………………………… 27

4.4 Golden Parachute ……………………………………………………………………... 28

4.5 Staggered Board Amendments ………………………………………………………... 28

4.6 Greenmail …………………………………………………………………………….. 29

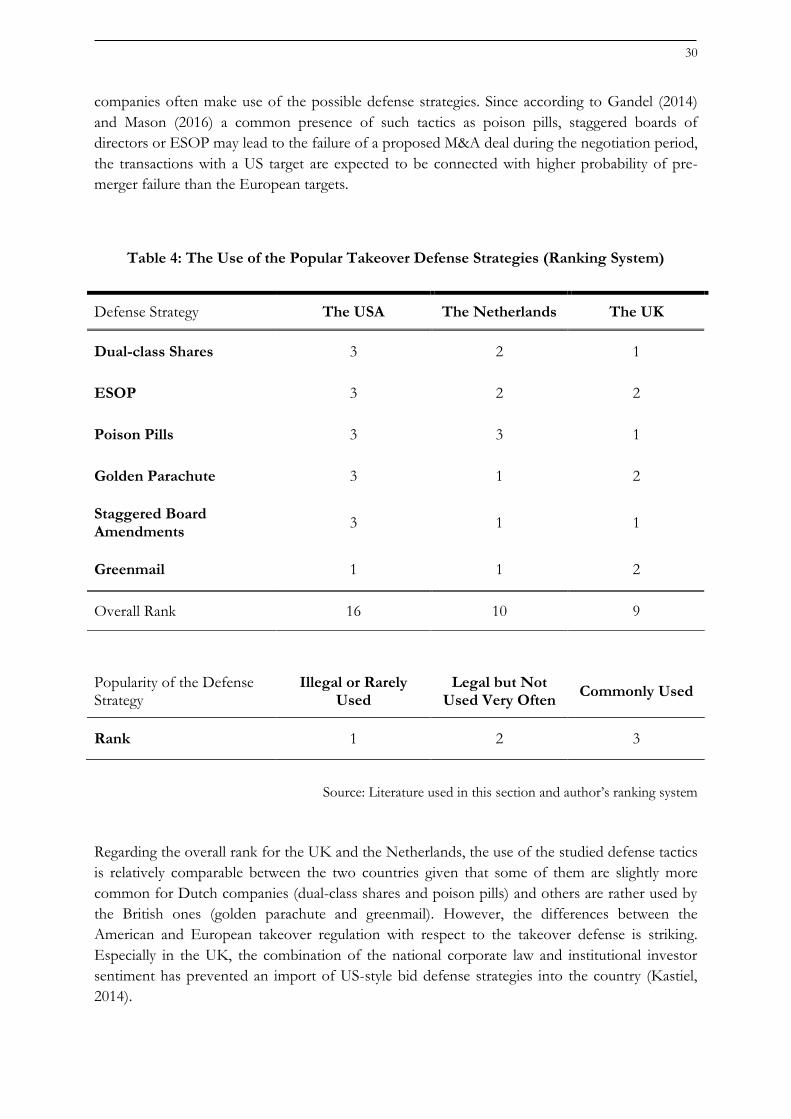

4.7 Comparison of the US, UK and Dutch Defense Tactics ……………………………… 29

3

5 Hypotheses Formulation …………………………………………………………………. 31

6 Logit Model Analysis …………………………………………………………………….... 32

6.1 Methodology ………………………………………………………………………….. 32

6.1.1 Basic Assumptions of the Logit Model …………………………………………... 33

6.2 Data Structure and Model Variables …………………………………………………... 33

6.2.1 The Dependent and Independent Variables …………………………………….... 34

6.2.2 The Mediator Variables ………………………………………………………….. 35

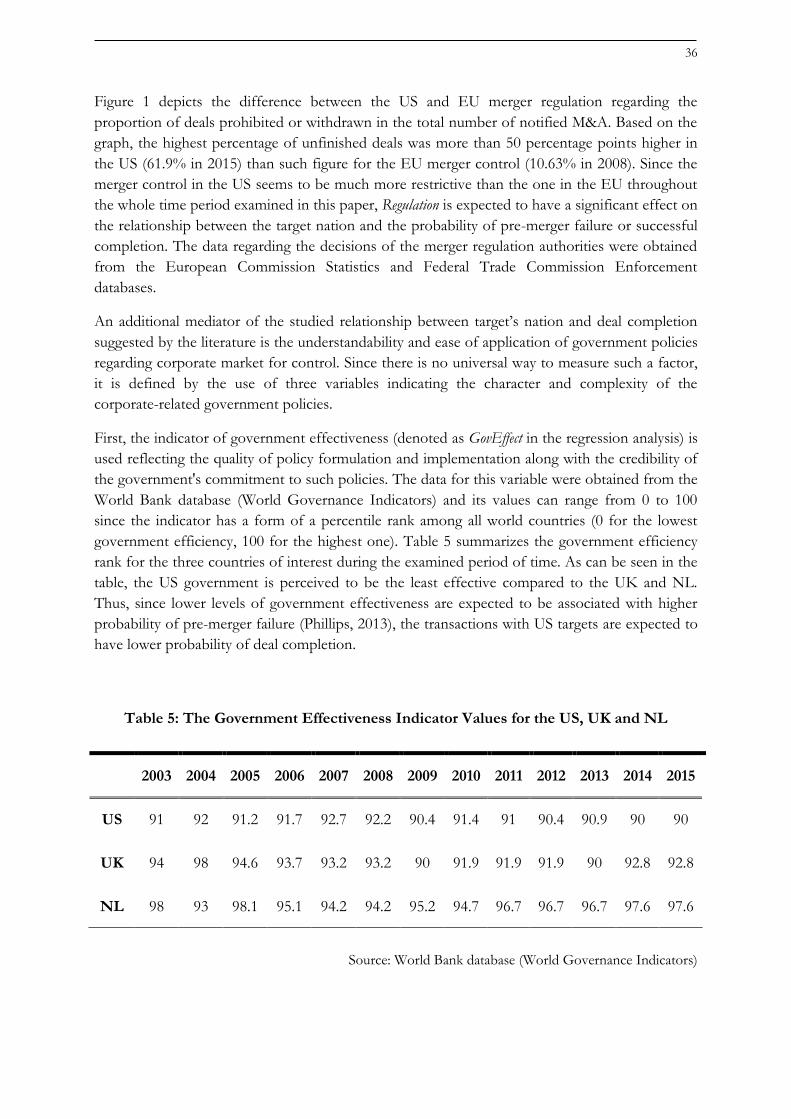

6.2.3 The Moderator Variable …………………………………………………………. 37

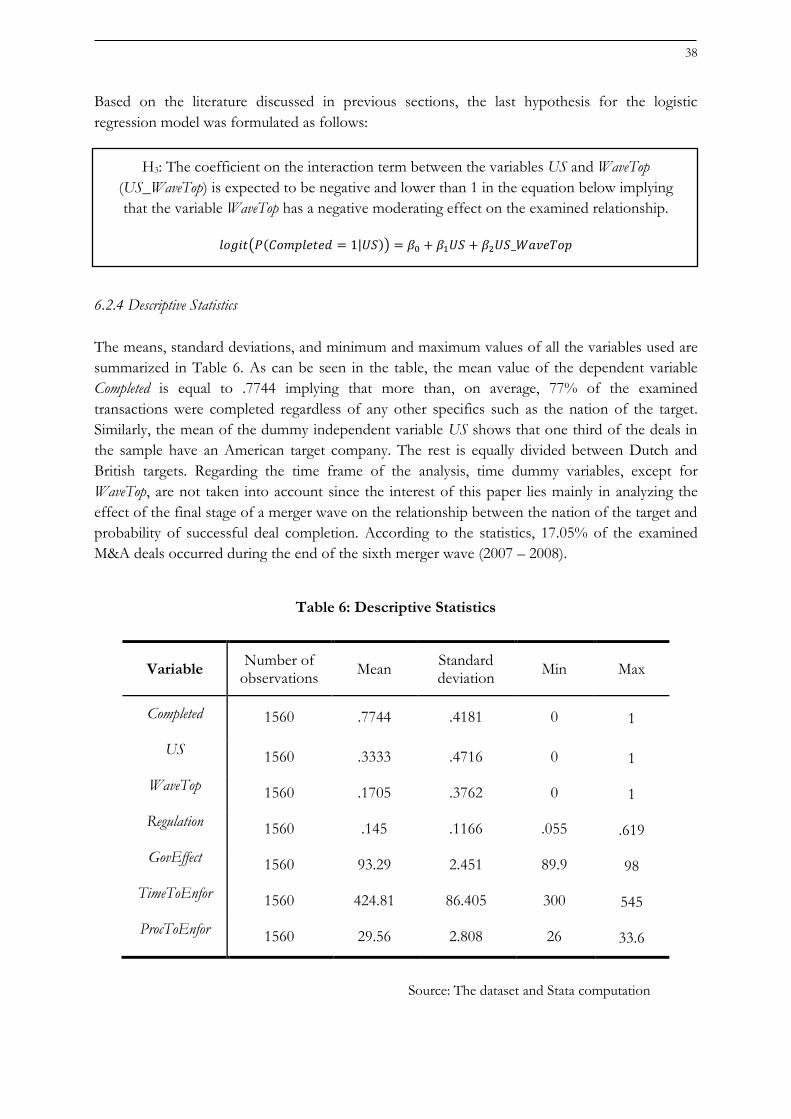

6.2.4 Descriptive Statistics ……………………………………………………………... 38

6.3 Logistic Regression Analysis …………………………………………………………... 39

6.3.1 Hypothesis Testing ………………………………………………………………. 40

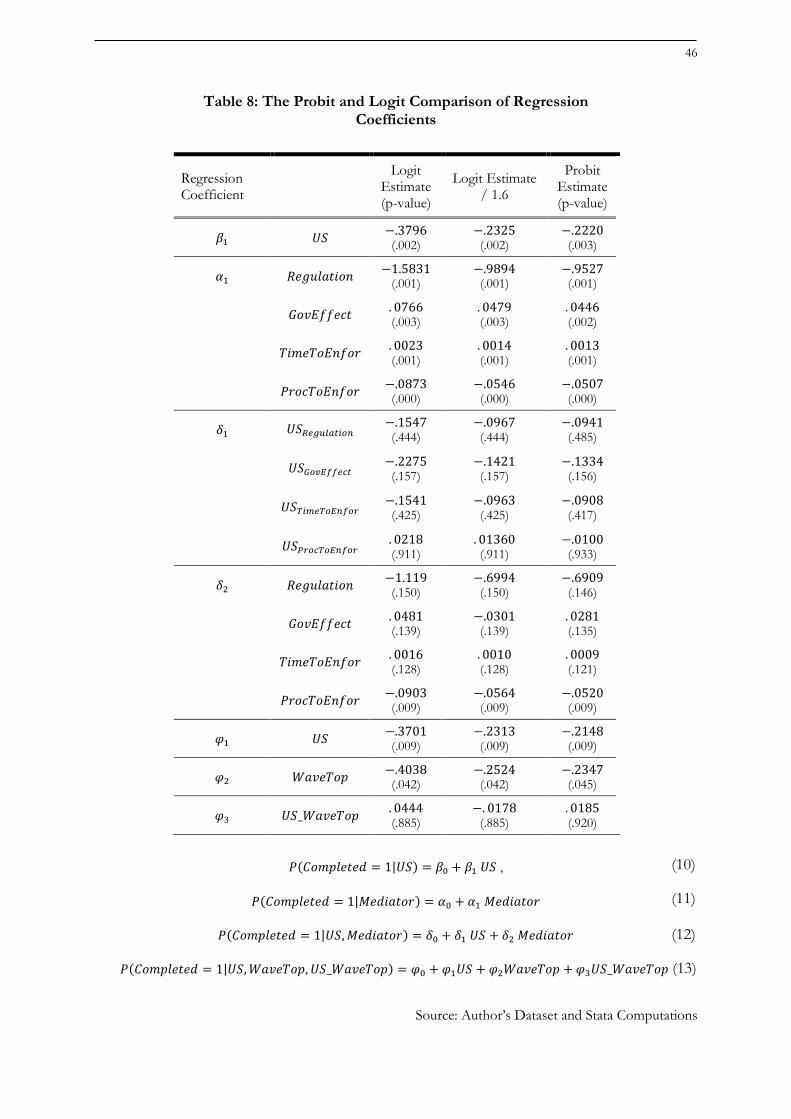

7 Robustness Test: Probit Model Analysis ………………………………………………….. 45

8 Conclusion and Discussion ……………………………………………………………….. 48

Bibliography …………………………………………………………………………………. 51

Appendix A: EU Merger Regulation Thresholds ……………………………………………... 55

4

List of Tables

Table 1: The Main Provisions of the US Antitrust Laws …………………………………….... 14

Table 2: The Summary of Federal Trade Commission Law Enforcement Cases …………….... 17

Table 3: The Summary of EU Merger Regulation Decisions …………………………………. 23

Table 4: The Use of the Popular Takeover Defense Strategies (Ranking System) …………….. 30

Table 5: The Government Effectiveness Indicator Values for the US, UK and NL ………….. 35

Table 6: Descriptive Statistics ……………………………………………………………….... 37

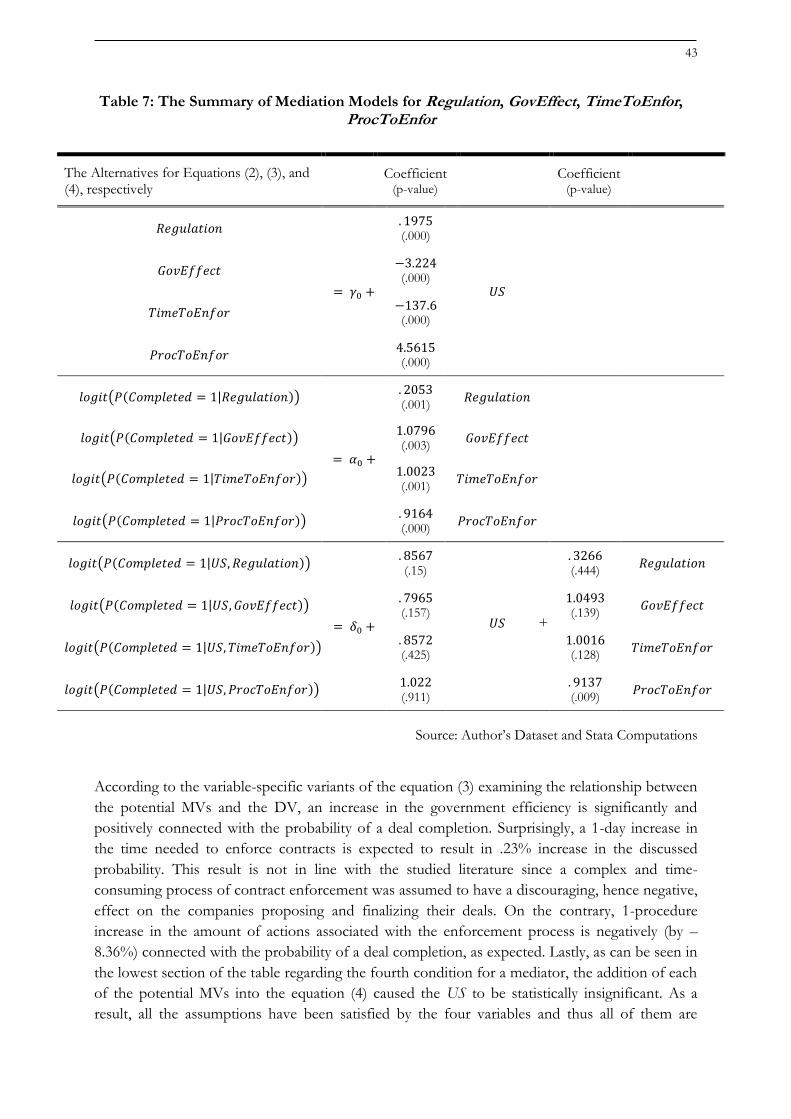

Table 7: The Summary of Mediation Models ………………………………………………… 42

Table 8: The Probit – Logit Comparison of Regression Coefficients ………………………… 45

5

List of Figures

Figure 1: Comparison of the US and the EU Merger Regulation Restrictiveness ……………. 34

Figure 2: Necessary Conditions for a Variable to be a Mediator ……………………………… 40

6

List of Acronyms

DV / Dependent Variable

ESOP / Employee Share Ownership Plan

IV / Independent Variable

M&A / Mergers and Acquisitions

MV / Mediator Variable

NCA / National Competition Authority

NYSE / New York Stock Exchange

SEC / Securities and Exchange Commission

7

1 Introduction

Companies engaging in mergers and acquisitions (M&A) spent more than USD 3.8 trillion on

their deals in 2015, exceeding the previous record amount of money invested in such activities set

in 2007. Currently, high numbers of firms worldwide seem to be more confident and optimistic

about pursuing M&A than they were in the last few years following the financial crisis of 2008.

This trend resembles the six merger waves that occurred over the last 120 years (Baigorri, 2016).

Porzio (2015) has suggested that favorable conditions for M&A transactions are nowadays

present almost in the whole US economy, regardless of sector or industry, and that they have

occurred as a combination of high consumer and management confidence, and low interest rates.

Such environment is not expected to change rapidly in the near future and hence the amount of

M&A deals involving US companies is assumed to continue growing. Similarly, positive

macroeconomic, financial and investment conditions encouraging M&A activity can be observed

in the EU. According to Corte and Horbach (2015), the confidence of European companies has

been resumed after the economic crisis due to the combined effect of improved methods of

financing, high levels of cash reserves on corporate financial statements, rising levels of

investment returns, and strong equity market performance allowing publicly listed bidders to pay

in stock for their takeovers and thus benefit from using such payment method. Based on these

factors, M&A activity is expected to remain important for the global economic development in

the upcoming years (Yoon, 2015).

Generally, companies have various reasons for conducting mergers and acquisitions. To mention

some of them, Sudarsanam (2003) finds that firms are mostly motivated by potential benefits

resulting from the transaction in a form of financial gains (acquiring an undervalued or poorly

managed company which can be restructured, healed and then resold with a premium), strategic

market advantage (increasing market share and power, or taking control over firms attractive for

competitors), diversification, and internal pressures from management and corporate executives

either being concerned about the company’s reputation leading them to follow the others’ M&A

decisions (“following the crowd”), or being self-interested and overconfidently aiming to leave a

legacy or boost their own egos with a specific deal. Other authors see the drivers of M&A

transactions in the globalization and the increased competition in both domestic and international

markets linked to it (Zuhairy et al., 2015), or in the access to new technologies, know-how or

scarce resources (Motis, 2007). Since all of these motives currently lead an increasing amount of

companies that engage in M&A activities (instead of using some other market entry modes),

interact with others internationally and spend billions of US dollars in mutual deals, this field

seems to be highly relevant for the current global economy and thus worth studying within the

scope of this paper.

Regardless of the motives behind M&A, the companies conducting such transactions usually

share one common objective which is delivering positive value to shareholders. However,

according to the current literature, between 70% and 90% of the deals actually fail to create

expected synergies and shareholder value (McMorris, 2015). According to the literature reviewed

on this topic, the reasons why the companies do not succeed in reaching their merger-related

goals often include differences between the involved parties regarding e.g. corporate culture,

8

management structure and habits, business strategy or long-term objectives. This in turn leads to

an unsuccessful post-merger integration of the firms. While there are plenty of papers and

publications analyzing the success or failure of M&A deals from the post-merger perspective and

focusing on the ability of the companies to create and deliver value to their shareholders along

with achieving the expected synergies, there is little amount of literature studying the topic from

the pre-merger point of view. Despite the record figure for the volume of M&A deals completed

recently, in 2015, there has been more than 25% of the total number of proposed transactions

that failed during the pre-merger period, i.e. before they were even finalized (Zephyr and World

Bank, 2016). Since such incompletion (withdrawal or prohibition) of a proposed deal is usually

accompanied by high fees and losses for the bidder harming the company and its shareholders,

this study aims to examine some of the factors assumed to affect the pre-merger M&A failure in

detail and help the companies avoid the costly pre-merger deal incompletion.

Thus, the main purpose of the present paper is to uncover and empirically analyze some of the

reasons why some mergers or acquisitions fail to be completed and others do not. Based on the

literature reviewed on this topic, the most commonly discussed factors have been the legislative,

administrative and business environments linked to the nation of the M&A target company.

While several country-specific factors were addressed by the authors (such as merger regulation

mechanisms, popularity and legality of various takeover defense strategies, complexity of

governmental corporate-related legislation or time-demand of contract administration and

enforcement), the proposed relationship between specific target nations and the pre-merger

failure rate has not been tested empirically by any of them. This paper combines the theoretical

description of the relevant country-specific characteristics of the merger-related legislation

present in the target nation with an econometric logit model analysis designed to test whether the

relationships assumed by the studied literature hold after application of the real-life data.

More specifically, M&A deals proposed by Dutch companies with their most common deal

partners or targets, namely British, American, or other Dutch firms are examined. Another

reason for choosing these nations for the analysis is that they represent the 3 most important

players in the global M&A activity based on the amount and volume of transactions made, and

hence there is also enough data available regarding the deals and their completion/ pre-merger

failure. The time period examined by the analysis spans from 2003 to 2015 in order to cover

three groups of data: (1) the sixth merger wave (2003 – 2008) which is expected to affect the pre-

merger deal failure according to the studied literature, (2) the most recent M&A activity (2014 –

2015) which is considered to be an upward-sloping part of a potential seventh merger wave, and

(3) the years between these two periods as a reference period of time when deal-making is not

affected by any merger wave. In order to find an answer to the primary research question stated

as “Does the merger-related legislation in the nation of the M&A target company affect

the probability of the pre-merger deal failure?”, each target nation in the sample of this paper

is described by variables corresponding to the restrictiveness of the merger regulation (percentage

of penalized or rejected deals in the total amount of deals), effectiveness of the government

legislation and time and number of procedures needed for companies to finalize and inforce

contracts. Additionally, testing the relationship between the fact that a transaction is being

negotiated during the end of a merger wave (when there is a high amount of deterrent examples

9

of deals failed during the earlier stages of the wave) and the probability of successful completion

of such a deal is also part of the empirical analysis.

Since the importance and amount of money involved in the field of M&A seem to be on their

continuous increase, an empirical analysis of the factors, more specifically the regulation-related

characteristics of the target nation, affecting the probability of a deal’s pre-merger failure can

represent a valuable contribution to the field. This paper aims not only to extend the current

literature on this topic (which is mainly focused on post-merger failures) but also provide

companies that consider engaging in M&A transactions with an empirical study suggesting what

kind of country-specific factors are estimated to positively or negatively influence the likelihood

of the deal completion. Such factors are then important to be inspected while choosing a suitable

target company for an M&A activity. Since the present paper is based on the analysis of the

transactions proposed by Dutch bidders, it is expected to be relevant especially for companies

operating in the Netherlands which have been investing the world highest amount of money in

M&A deals relative to the country’s GDP over the last few years (Zephyr, 2016). In addition, as

some authors claim that the global economy is moving towards the top of a seventh merger wave

(Lam, 2016), it is found relevant to examine the effect of the later stage of a merger wave (using

the data from the sixth wave) on the probability of a deal completion that might be applicable on

the current deal-making. This is also one of the unique features of this study by which it aims to

contribute to the existing research and literature.

In the following section, a literature review regarding the main factors expected to affect the pre-

merger M&A deal failure is provided. In Section 3, the focus is put on the most commonly

discussed one, the merger control and regulation mechanisms in the EU and the US. In that part

of the paper the two legislations are summarized and compared according to the levels of

restrictiveness later used for the empirical analysis. An in-depth explanation and comparison of

the two merger regulation systems is provided in order to help the reader understand the

differences between the two regulatory regimes and the reasons why they can influence the

probability of pre-merger M&A deal failure. Section 4 provides an overview of the popularity and

use of the takeover defense strategies as a part of the country-specific merger control

mechanisms since the literature review suggested that countries with higher legal allowance of

such tactics are expected to experience significantly higher pre-merger failure rate. In Section 5,

the hypotheses for the empirical analysis of this paper are stated. Sections 6 and 7 are then related

to the logit model analysis of the proposed hypotheses and the robustness test in a form of a

probit regression. Finally, Section 8 summarized the results and conclusions drawn from the

empirical part of the paper and suggests potential areas of further research.

10

2 Literature Review

In the literature studied on the topic of the pre-merger M&A completion, a few major reasons

for the transactions to fail in this stage of the deal-making process were discussed. Reis et al.

(2013) addressed cross-border deals and found that cultural differences in corporate and social

behavior and habits may make the pre-completion stage of negotiation and deal finalization

difficult or even impossible. Manchin (2004) suggests that the level of M&A deal completion

between the European and US companies is lower than in the case of transactions conducted

within the EU. The author claims that this fact may be affected by various macroeconomic,

legislative and institutional aspects characteristic for each of the involved countries. Such factors

include e.g. the regulatory environment, contract enforcement mechanisms, market for corporate

control, or quality and efficiency of the governmental institutions.

The purpose of this paper is to analyze how the nationality of the target company and the

legislative system linked to it affect the probability that the deal will fail during the pre-merger

stage. In order to do so, a few aspects characterizing the target nation (and being expected to

have an effect on the deal completion) are identified. First, the level of merger control in a nation

of the target has been discussed as an important factor. Although only few deals have been

prohibited as a result of the merger regulation in the EU or the USA compared to the total

amount of deals completed, the potential restrictions or compliance requirements set by the

regulatory authorities can still deter significant amount of companies from proceeding with the

proposed M&A transactions. Phillips (2013) has addressed the fact that strict rules passed by the

US Federal Trade Commission requiring pharmaceutical companies to notify antitrust authorities

when they aim to conduct any kind of M&A, or e.g. just acquire an exclusive patent license, are

observed to result in a relatively high amount of deal withdrawals among drug and biotech

companies. According to De Loecker et al. (2008) and Tsang (2015), similar deterrent effects of

the merger regulation requirements can be also noticed in industries including tobacco, petroleum

products or transportation (specifically railroads or airspace) in the USA. In addition, companies

sometimes back out of their planned M&A activities during the pre-merger stage because of two

factors: (1) the severity and nature (criminal or civil) of the penalties issued to them in case they

would fail to comply with an order received from the regulatory authority, and (2) the extent of

the potential remedial actions required to proceed with the deal. It has been observed that a

threat of criminal penalties discourages more anticompetitive transactions from their completion

than civil penalties (Peitz and Spiegel, 2014). The logit model analysis in Section 6 aims to

estimate the effect of the restrictiveness of merger regulation in the three key players in the world

M&A deals (the USA, the United Kingdom and the Netherlands) on the probability of pre-

merger transaction failure taking into account the number of deals penalized and prohibited by

each of the regulatory legislations.

Also connected to the merger control legislation, the success or failure of an M&A deal

finalization process is assumed to be affected by the legality and popularity of takeover defense

strategies used in the nation of the target company since these practices are designed to prevent

unwanted takeovers and mergers from being completed (Pearce and Robinson, 2004). Gandel

(2014) claims that the tactics, such as poison pills or staggered board membership, have been

11

highly relevant and key defense tools used by target companies to block offers during the pre-

merger negotiation stage of the deal-making process. According to Mason (2016), the popularity

of takeover defense strategies (including golden parachutes, dual-class stock structure, employee

share ownership plans or greenmailing) has significantly increased during the last 20 years and

even though they are allowed by the government and regulatory authorities in an effort to help

companies safeguard the rights and interests of their shareholders in case of a hostile takeover

threat, such tactics are often used by the target’s management for purely self-motivated reasons

to block all kinds of deals, even those potentially beneficial for the shareholders. As stressed by

Sundaramurthy (2000), the defense strategies seem not only to raise barriers to finalization of

transactions that are already being negotiated (leading to the pre-merger M&A deal failure) but

also to deter potential acquirers from initiating a bid. The theoretical part of the paper addresses

primarily the potential effects of the use of the takeover defense tactics on the deal completion,

and compares the popularity and legality of such strategies within the studied countries.

However, because of the lack of data regarding the use of takeover defense in each of the

countries and each year of the examined time period, this factor is not included in the empirical

analysis.

In addition to the country-specific merger regulation and control mechanisms discussed above,

Phillips (2013) argues that a complex government policy regarding corporate activities that is

difficult to understand and apply can also deter companies engaging in M&A deals from

finalizing the transactions. Using the example of unclear changes in rules passed by the Federal

Trade Commission of the USA with respect to the notification requirements applicable for

pharmaceutical companies in 2013, the author claims that vague interpretation of regulatory

policies along with their excessive complexity can have a negative effect on the completion of the

deals being negotiated. Regarding the policy complexity, Smith (2003) has claimed that for some

companies, a short time needed to finalize contract with another firm and receive decision, such

as unconditional clearance or conditions required for clearance, from the regulatory authority is

very important, especially in cases when the deal has to be completed as soon as possible in order

to achieve proposed strategic objectives with time-limited validity. In this sense, a complicated

merger and competition law and contract enforcement can delay takeovers so much that they are

withdrawn during the pre-merger period since the opportunity costs of the companies waiting for

the regulatory decision are higher than expected benefits from the merger (UKSA, 2016).

Lastly, a few authors have addressed the relationship between the occurrence of merger waves

and pre-merger deal withdrawals. Gaugham (2015) has stated that these waves, short periods of

very intense merger activity, start when there is a high amount of potentially attractive target

companies in the market and they usually end with a burst of an economic bubble which led to

such abundance of M&A deals in the first place. Thus, at the top of the merger wave, more deals

are expected to fail during the pre-merger deal-making period since a noticeable number of

companies back out of the deals once they see a lot of unsuccessful deals that were completed at

the beginning of the wave but did not manage to achieve expected synergies and shareholder

value creation. This trend has been observed mainly in the USA. According to Galli and

Pelkmans (2000), towards the end of the merger wave, not only companies observe the deterrent

examples of deals completed at an earlier stage of the wave (eventually with an undesirable

outcome) but also the merger control and antitrust authorities learn their lesson from these cases

12

in a form of stricter merger regulation enforcement that in turn results in more deals penalized or

prohibited increasing the probability of the pre-merger M&A failure.

Besides the above listed factors (namely the level of restrictiveness of the merger control, the use

of takeover defense strategies, understandable and effective government policies, and fast and

uncomplicated enforcement of contracts), there are many other reasons why M&A deals fail

before they are even finalized, e.g. the executive management’s hubris, over-confidence or over-

optimism which leads them to proceed with their bid despite the fact that the merger regulation

or the allowed takeover defense tactics might make the deal impossible to finish. Such companies

are often even willing to take the risk of paying high penalties if the deal is not completed

(Sudarsanam, 2003). However, such factors are hardly observable and measurable and thus, for

the purpose of this paper, they are not included in the empirical model.

The next two sections describe the merger regulation legislation and mechanisms effective in the

USA and the EU along with the legality and use of the takeover defense strategies most

commonly discussed in the examined literature. This way the reader is aimed to be provided with

a sufficient in-depth overview of the topic of merger control for an easier understanding of the

relationships tested by the empirical analysis.

13

3 Merger Regulation

3.1 Antitrust Laws in the USA

Since 1890, the United States Congress has passed three antitrust laws, namely the Sherman Act,

the Federal Trade Commission Act, and the Clayton Act. After some revisions and amendments,

all of them are currently still in effect. The main purpose of the US antitrust laws is to prohibit

unlawful mergers, acquisitions and business practices in general. In order to spot and inspect

such transactions, the laws have set fundamental rules and benchmarks for fair competition

within firms whose activities and operations are in any way affecting the US economy. Since the

antitrust laws define unlawful M&A and business practices in relatively general terms, the

authorized courts then have to decide which of the transactions and activities are illegal based on

the specific characteristics of each case. Yet, the basic objective of the law does not change.

Every antitrust legal proceeding aims to protect competition in the relevant market for the

customers’ benefit, making sure that businesses have strong incentives to operate efficiently and

keep quality of their products up without increasing their prices (Federal Trade Commission,

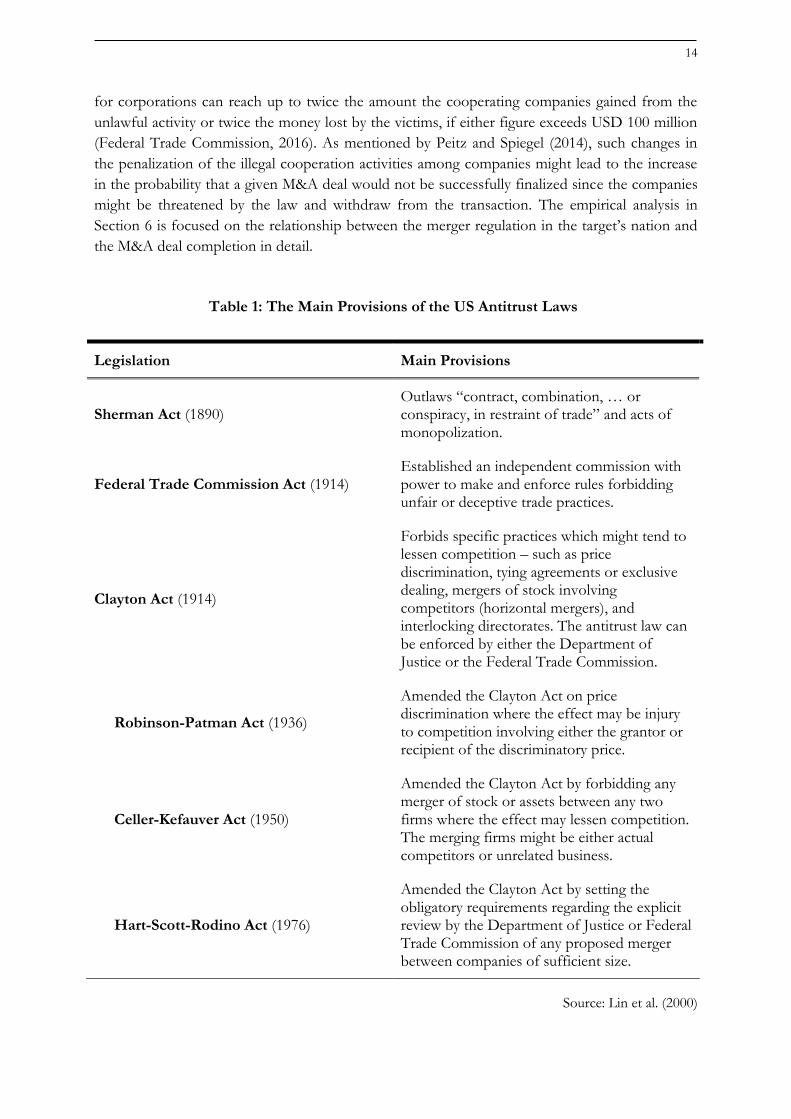

2016). Table 1 summarizes the most important provisions of the three antitrust laws and their

amendments. All of them are described below more in detail.

3.1.1 The Sherman Act

This antitrust law states that “every contract, combination in the form of trust or otherwise, or

conspiracy, in restraint of trade or commerce among the United States, or with foreign nations, is

declared to be illegal” as well as an “attempt to monopolize, combine or conspire with any other

person or persons [corporations or associations by the laws of the United States or any foreign

country] to monopolize any part of the trade or commerce among the United States, or with

foreign nations” (Legal Information Institute, 2016). Although the interpretation of the law by

the courts might differ (potentially leading to declaring agreements lawful even if they restrain

trade), certain acts are perceived to harm competition so seriously that they are declared illegal in

vast majority of cases. Such acts include, among others, intentional bid rigging (promising a

commercial contract to one party even though several other parties present a bid as well), market

division within a few major players, or plain arrangements between competing businesses to fix

prices.

The violation of the Sherman Act is usually penalized financially but can also result in

imprisonment as the Act is the only US antitrust statute which carries criminal penalties because

it is both civil and criminal law. The size of the criminal penalties for intentional and clear

violations of the law (such as bid rigging or price fixing) is one of the few changes that have been

made since its implementation in 1890. As amended in the original version of the Act, the

unlawful activities restraining or monopolizing trade “shall be punished by fine not exceeding

USD 10 million if a corporation, or USD 350 thousand if any other person, or by imprisonment

not exceeding three years” (Legal Information Institute, 2016). In June 22, 2004, the maximum

fines for corporations increased to USD 100 million and for individuals to USD 1 million, along

with up to 10 years in prison. In addition, under federal law, the maximum level of the penalty

14

for corporations can reach up to twice the amount the cooperating companies gained from the

unlawful activity or twice the money lost by the victims, if either figure exceeds USD 100 million

(Federal Trade Commission, 2016). As mentioned by Peitz and Spiegel (2014), such changes in

the penalization of the illegal cooperation activities among companies might lead to the increase

in the probability that a given M&A deal would not be successfully finalized since the companies

might be threatened by the law and withdraw from the transaction. The empirical analysis in

Section 6 is focused on the relationship between the merger regulation in the target’s nation and

the M&A deal completion in detail.

Table 1: The Main Provisions of the US Antitrust Laws

Legislation Main Provisions

Sherman Act (1890) Outlaws “contract, combination, … or conspiracy, in restraint of trade” and acts of monopolization.

Federal Trade Commission Act (1914) Established an independent commission with power to make and enforce rules forbidding unfair or deceptive trade practices.

Clayton Act (1914)

Forbids specific practices which might tend to lessen competition – such as price discrimination, tying agreements or exclusive dealing, mergers of stock involving competitors (horizontal mergers), and interlocking directorates. The antitrust law can be enforced by either the Department of Justice or the Federal Trade Commission.

Robinson-Patman Act (1936)

Amended the Clayton Act on price discrimination where the effect may be injury to competition involving either the grantor or recipient of the discriminatory price.

Celler-Kefauver Act (1950)

Amended the Clayton Act by forbidding any merger of stock or assets between any two firms where the effect may lessen competition. The merging firms might be either actual competitors or unrelated business.

Hart-Scott-Rodino Act (1976)

Amended the Clayton Act by setting the obligatory requirements regarding the explicit review by the Department of Justice or Federal Trade Commission of any proposed merger between companies of sufficient size.

Source: Lin et al. (2000)

15

With regard to the cross-border M&A, a “strict territorial interpretation” was originally used by

courts when applying the Sherman Act to foreign conduct, i.e. they were looking exclusively at

the laws of the locality where the anticompetitive activity occurred. This approach was, however,

replaced by an “effect test” in 1945 which stated that “any state may impose liabilities … for

conduct outside its borders that has consequences within its borders which the state reprehends”

(Becker and Kirtland, 2003). Thus since then, the American merger regulations apply directly not

only to the companies operating in the USA making deals among each other, but also to the

firms based outside the USA entering the American market, strengthening their positions there or

affecting the nature and competitiveness of the market (including import and export) in any other

way.

3.1.2 The Federal Trade Commission Act

All violations of the Sherman Act are according to the Supreme Court of the United States also

outside the law stated in the Federal Trade Commission Act which aims to define and ban unfair

methods of competition and deceptive acts or business practices. Under the Act from 1914, the

Commission is empowered to seek monetary compensation or any other relief for activities

detrimental to customers and market competition; introduce trade regulation rules specifically

defining unfair and deceptive practices along with establishing clear requirements to prevent such

activities; conduct investigations related to the entities suspected of the unlawful practices; and

make public releases and legislative recommendations to the Congress to improve the antitrust

law system. In addition to covering majority of the activities that already violate the Sherman Act,

the Federal Trade Commission Act also reaches some other practices (harming fair competition)

which do not clearly fit into the rules of conduct formally prohibited by the Sherman Act, thus

the legislation addresses and inspects wider range of transactions affecting the American market

(Federal Trade Commission, 2016).

3.1.3 The Clayton Act

Together with its amendments (Robinson-Patman Act, Celler-Kefauver Act and Hart-Scott-

Rodino Act), the Clayton Act defines and forbids such activities as price discrimination (including

rebates and discounts), specific mergers and interlocking directorates (when the same person

makes decisions for competing companies), tying arrangements (when the seller conditions the

sale of one product on the buyer’s agreement to purchase a separate product from the seller), and

exclusive dealing or boycotts. The three amendments to the Clayton Act have noticeably affected

the scope and nature of the US antitrust law. In 1936, the Robinson-Patman Act banned certain

discriminatory price settings and allowances in dealings between companies. However, the effect

of this amendment has diminished since both the Department of Justice and the Federal Trade

Commission have rarely enforced the Act since it became effective (Lin et al., 2000).

In 1950, Section 7 of the Clayton Act was amended by the Celler-Kefauver Antimerger Act

prohibiting M&A which might result in substantial lessening of the competition or tend to create

a monopoly. Prior to this amendment, many firms were able to get around the original version of

the Clayton Act by making use of the fact that asset transactions among competitors were not

16

illegal even though stock deals were. This way the Celler-Kefauver Act aimed to capture more

M&A activities that would lead to explicit or tacit collusion (caused by increased market

concentration) making the US antimerger law stricter than it had been before (Federal Trade

Commission, 2016).

In 1976, the Hart-Scott-Rodino Antitrust Improvements Act brought new obligatory requirements for

companies planning large M&A to notify the government in advance about the purpose,

expected execution and impact of their plans. Since either the Department of Justice or the

Federal Trade Commission acquired the responsibility to formally review the potential mergers,

the role of these institutions became significantly more important with respect to the antitrust law

enforcement affecting the chance that a company‘s proposed merger would not be approved (Lin

et al., 2000). Additionally, the agencies’ role in the US antitrust policy changed from the one

based on law enforcement to one based on regulation. As a result, the importance of their Joint

Merger Guidelines outlining the principal analytical techniques, practices and enforcement policy

with respect to both horizontal and non-horizontal (vertical and conglomerate) M&A naturally

increased as well (Coate and Kleit, 1996). As suggested by the US General Accounting Office

(1990), the new law after the Hart-Scott-Rodino amendment had a significant impact on the

process how specific cases attracted attention of the two enforcement bodies. Since until 1978,

the Antitrust Division of the Office was notified about potentially unlawful mergers through

complaints of attorneys, citizen information, or trade press reports, it was relatively difficult for

them to investigate proposed mergers completely before they were finalized. However, the

“premerger notification program” becoming effective in 1978 as part of the Hart-Scott-Rodino

Act led to a noticeable increase in the number of cases investigated by the regulatory bodies (Lin

et al., 2000).

3.1.4 Federal Trade Commission Cases and Proceedings

As discussed above, one of the Commission’s fundamental missions is to promote fair

competition in the American market. In order to do so, the authority enforces federal antitrust

laws that prohibit anticompetitive M&A and other business practices potentially leading to higher

prices, narrower variety of products, or less innovation (Federal Trade Commission, 2016). Even

though the Commission also enforces federal consumer protection laws that aim to prevent

fraud, deception and unfair practices of companies with respect to the customer welfare, this

section of the paper deals exclusively with the enforcement mechanisms linked to the cases

addressing antitrust issues. These cases are the most relevant for the empirical analysis presented

in Section 6 since they reflect (un)fair competition between market participants responding to

their mutual transactions and cooperation in form of M&A. The effects of these cases’

enforcement proceedings (orders and penalties issued by the Commission) on the probability of

M&A’s failure during the pre-merger stage are tested by the logit model analysis. In this part of

the paper, the Commission’s enforcement practices are briefly summarized and described.

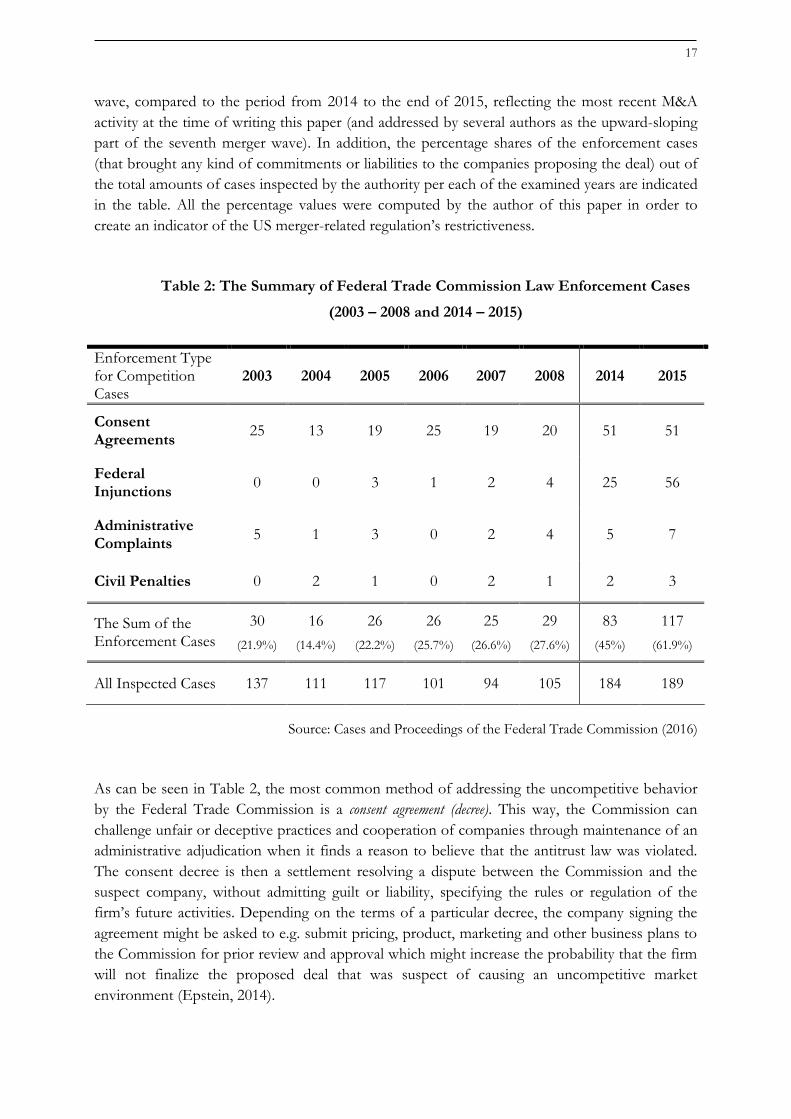

Table 2 contains the amounts of cases that were subject to one of the Commission’s types of the

antitrust law enforcements. These are sorted into four main categories – namely the consent

agreements, federal injunctions, administrative complaints, and civil penalties. The table includes

data for the years spanning from 2003 to the end of 2008, corresponding to the sixth merger

17

wave, compared to the period from 2014 to the end of 2015, reflecting the most recent M&A

activity at the time of writing this paper (and addressed by several authors as the upward-sloping

part of the seventh merger wave). In addition, the percentage shares of the enforcement cases

(that brought any kind of commitments or liabilities to the companies proposing the deal) out of

the total amounts of cases inspected by the authority per each of the examined years are indicated

in the table. All the percentage values were computed by the author of this paper in order to

create an indicator of the US merger-related regulation’s restrictiveness.

Table 2: The Summary of Federal Trade Commission Law Enforcement Cases

(2003 – 2008 and 2014 – 2015)

Enforcement Type for Competition Cases

2003 2004 2005 2006 2007 2008 2014 2015

Consent Agreements

25 13 19 25 19 20 51 51

Federal Injunctions

0 0 3 1 2 4 25 56

Administrative Complaints

5 1 3 0 2 4 5 7

Civil Penalties 0 2 1 0 2 1 2 3

The Sum of the Enforcement Cases

30

(21.9%)

16

(14.4%)

26

(22.2%)

26

(25.7%)

25

(26.6%)

29

(27.6%)

83

(45%)

117

(61.9%)

All Inspected Cases 137 111 117 101 94 105 184 189

Source: Cases and Proceedings of the Federal Trade Commission (2016)

As can be seen in Table 2, the most common method of addressing the uncompetitive behavior

by the Federal Trade Commission is a consent agreement (decree). This way, the Commission can

challenge unfair or deceptive practices and cooperation of companies through maintenance of an

administrative adjudication when it finds a reason to believe that the antitrust law was violated.

The consent decree is then a settlement resolving a dispute between the Commission and the

suspect company, without admitting guilt or liability, specifying the rules or regulation of the

firm’s future activities. Depending on the terms of a particular decree, the company signing the

agreement might be asked to e.g. submit pricing, product, marketing and other business plans to

the Commission for prior review and approval which might increase the probability that the firm

will not finalize the proposed deal that was suspect of causing an uncompetitive market

environment (Epstein, 2014).

18

If the suspect does not agree with the decision and charges issued by the Commission, the

company can make a formal administrative complaint. The Federal Trade Commission’s Complaint

Counsel then conducts the prosecution of the antitrust matter and with its decision it

recommends either entry of an order to cease or dismissal of the complaint. In Table 2, the

figures corresponding to the administrative complaints represent the amount of cases when the

Commission enforced their charges after the complaint trial proceeding.

When the Commission has a reason to believe that some companies or their combination are

violating a provision of the antitrust law, it may issue a preliminary or permanent injunctions not

only barring unlawful practices but also imposing various kinds of monetary remedies (such as

the refund of overcharges attributable to collusive price fixing) to redress past violations and

deter other companies from similar activities. As can be seen in Table 2, the amount of deals

subject to the federal injunction orders has recently increased compared to the cases examined

during the sixth merger wave (Federal Trade Commission, 2016).

Lastly, if any companies fail to comply with the provisions of the antitrust laws described above

(such as merging without observing the requirements of the Clayton Act), the Commission may

seek civil penalties which can be as high as USD 10,000 for each day during which the company

violated the law. Since civil penalties are usually also linked to some other enforcement methods

of the Commission (e.g. federal injunctions), the numbers presented in Table 2 for the civil

penalties represent the cases when the Commission ordered the violator to only pay certain

penalty without any further restrictions. If the respondent violates the final order, it is liable to

pay another fine up to USD 16,000 for each violation (Federal Trade Commission Act, Section

5(1), 15 U.S.C. Sec. 45(1)).

To summarize the previous paragraphs, it can be seen that the total amount of deals subject to

the Federal Trade Commission regulation and orders has recently noticeably increased as

compared to the figures for the last merger wave. In addition, by observing the data from 2003 to

2008, it can be noticed that towards the end of the sixth merger wave, there was a gradual

increase in the percentage of deals with further liabilities or requirements set by the US antitrust

authorities before the transaction could be finalized. This suggests that at the top of the wave,

more M&A deals are penalized or prohibited which is in line with Galli and Pelkmans (2000) who

claim that in the later stages of a merger wave, regulatory bodies tend to enforce the merger

control mechanisms more strictly because they learn their lesson from deterrent examples of

deals allowed at an earlier stage of the merger wave with an undesirable eventual outcome. Even

more significant growth trend can be noticed in the data for 2014 to 2015 with their peak at more

than 60% of all deals examined by the Commission being subject to orders and penalties issued

by the authority. This can be seen as a sign of the economy currently moving towards the top of

a potential seventh merger wave (Lam, 2016).

19

3.2 Merger Regulation in the EU

The original version of the European Merger Regulation came into force in September 1990,

introducing the first legal framework for the systematic review of M&A and other forms of

concentration into the EU Competition Law. After a series of amendments and wide-ranging

consultation exercise initiated in 2001, the EU Merger Regulation was replaced by the current

revised version (Council Regulation (EC) No 139/2004) which has been effective since May

2004. The new EU Merger Regulation has become the fundamental EU legislation for the

control of proposed M&A transactions and for its interpretation, notices and guidelines released

by the European Commission play an important role. The main purpose of the regulation is to

prohibit M&A deals which would significantly reduce competition in the EU market by e.g.

creating or strengthening dominant players that would likely harm consumers by raising prices

and deter competitors with less market power (European Commission, 2016).

3.2.1 Criteria for the EU Merger Regulation to Apply

In general, the EU Merger Regulation applies to any concentration (referring to mergers,

acquisitions of control and creation of full-functioning joint ventures) having, or being assumed

to have in the future, a so called EU dimension. For an M&A deal to have such dimension, it has

to reach certain thresholds which are in their nature purely jurisdictional. Since the thresholds are

applied to transactions regardless any specific competition issues, the nationality of the bidder or

the target, the country where the transaction takes place or the law applicable to the transaction,

the EU Merger Regulation can in fact apply in some cases to deals with little connection to the

EU (Slaughter and May, 2015).

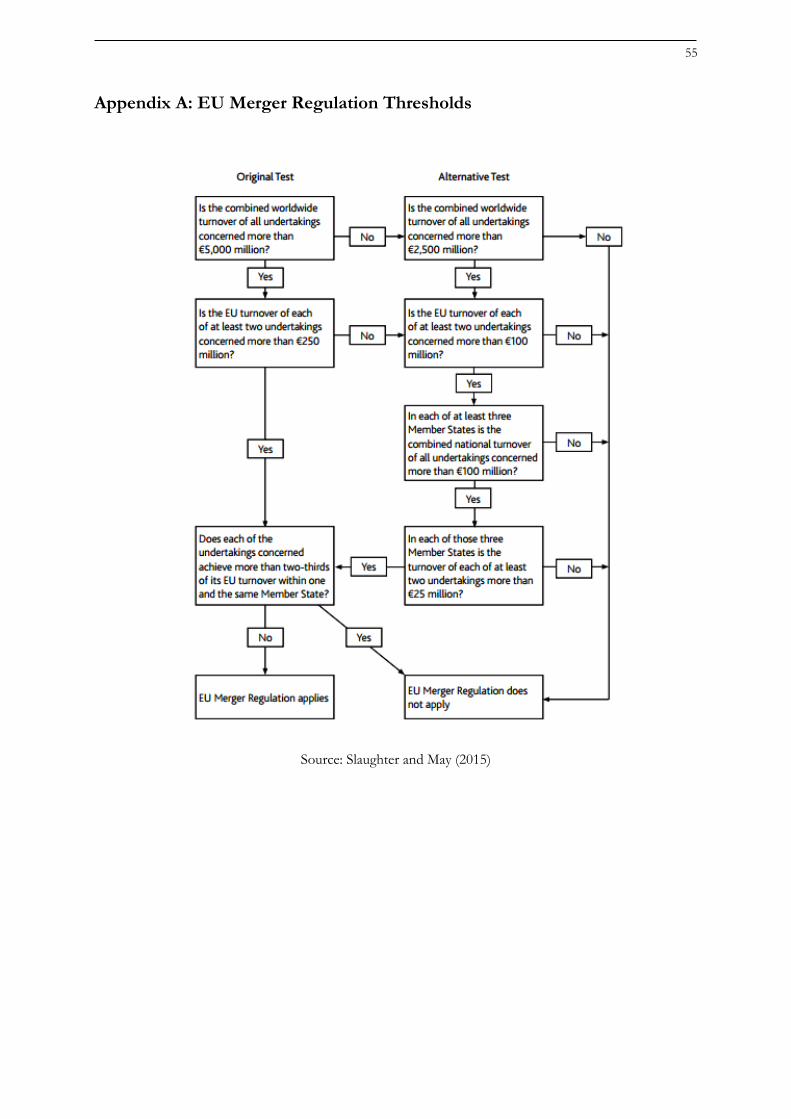

There are two sets of criteria that to a certain point limit the EU Merger Regulation since at least

one of these has to be fulfilled for the deal to be found relevant and thus inspected by the

European Commission under the terms of the EU merger control. First, the original thresholds for

EU dimension (dating back to 1990 and still remaining in force) define three tests that have to be

met by the potentially examined deals:

(1) worldwide turnover test

(2) EU-wide turnover test

(3) two-thirds rule

From the worldwide perspective, the combined turnover of all companies involved in the

concentration has to be more than EUR 5,000 million while with respect to the EU market, each

of at least two of the companies concerned has to have an EU-wide turnover of more than EUR

250 million. Additionally, the deal is considered to have the EU dimension only if each of the

companies participating in the transaction achieved more than two thirds of its EU-wide turnover

in one and the same EU member country.

Second, deals that do not fulfill some of the original thresholds can still be assigned the EU

dimension status (and thus be inspected by the Commission) if they meet all of the alternative

thresholds for EU dimension created to extend the European Commission’s list of reviewed mergers.

This extension covers mainly the deals that would otherwise be subject to the merger control by

20

at least three National Competition Authorities (NCAs) in the EU. Thus, the alternative

thresholds consist of modified and additional tests as compared to the original ones. The criteria

needed to be met by the transactions are as follows:

(1) lower worldwide turnover test

(2) lower EU-wide turnover test

(3) additional three member states test

(4) two-thirds rule

In the case of the alternative thresholds, the requirement regarding the combined worldwide

turnover of all companies concerned is lowered to EUR 2,500 million and the minimum EU-

wide turnover of each of the parties has to be EUR 100 million. The two-third rule for EU

dimension stays the same for both the original and alternative thresholds. Regarding the “three

member states” test, two additional conditions have to be met for the deal to become subject to

the EU Merger Regulation. First, the combined national turnover of all companies involved in

the concentration has to be more than EUR 100 million in each of at least three EU member

countries, and second, each of at least two of the companies has to have national turnover higher

than EUR 25 million. The turnover of the companies considered in the criteria, regardless of the

set of thresholds used, is calculated from the sales of products and the provision of services

(according to the geographical location of the customer) after sales rebates, value added tax and

other taxes related directly to the turnover (Slaughter and May, 2015).

As the primary European legislation with respect to merger control, the EU Merger Regulation

sets conditions necessary for either the European Commission or the NCAs to have jurisdiction

over the proposed concentrations. In the vast majority of cases, the Commission investigates

larger deals having the EU dimension status while the NCAs are assigned to screen and examine

(in accordance with their national merger control rules) those smaller transactions not fulfilling

some of the criteria defined by either the original or alternative thresholds. However, there are

several procedures under which the involved companies can apply for reallocation of the

jurisdiction between the Commission and the NCAs under the terms of a pre- or post-

notification agreement with the authorities giving the companies, under certain limited

circumstances, the opportunity to choose the most appropriate authority and legislation applied

in their cases (European Commission, 2016).

A flowchart summarizing all the thresholds and criteria needed to be satisfied for the EU Merger

Regulation to apply can be found in Appendix A.

3.2.2 The EU Merger Regulation Notification, Investigation and Penalties

In principle, all companies are obliged to notify transactions falling under the EU Merger

Regulation to the Commission which has to approve the deal and declare that it is compatible

with the relevant market before it is allowed to be finalized and implemented. To make the

process easier and less time consuming for the companies, all the necessary requirements,

guidelines, prepared templates and forms needed to be completed while notifying a deal (based

on its complexity) are included in a single document, the Implementing Regulation, which is

publicly available on the European Commission websites along with a number of Notices

21

explaining the mechanisms and application of the Merger Regulation regime by the Commission.

In addition, all significant Merger Regulation notifications and decisions are published, in

conformity with the EU transparency objectives, providing valuable insights into the

Commission’s past decisions and enabling third parties to comment on the content (Slaughter

and May, 2015).

For the proposed M&A transactions of companies not operating in the same or related markets

or not exceeding certain market share thresholds, both the notification and the review of the deal

is usually done by a simplified procedure. The market share thresholds relevant for the EU

Merger Regulation state that the companies with combined market shares lower than 15% on the

market where they both compete (horizontally related) or with market share of less than 25% on

vertically related markets can make use of the simplified inquiry process. In the case of deals

between companies with combined market share above the mentioned thresholds, the

Commission runs full investigation which can consist in two phases. Historically, more than 90%

of all examined cases have been resolved during the Phase 1 investigation which gives the

Commission 25 days to properly analyze the transaction. Although generally the deals are cleared

without any remedies, some conditions or requests can be included in the Phase I review. These

are usually based on e.g. asking the companies to provide some additional information, or

clarifying the relevant market position and role of the companies involved in the proposed M&A.

If the Commission finds any competition concerns during their Phase I merger analysis, the

dealing companies can offer remedies, usually in a form of proposing certain modifications to the

proposed deal that would guarantee fair competition on the market. If the remedies are accepted

by the Commission, the merger is approved but the companies are obliged to comply with the

stated conditions (European Commission, 2016).

In addition to the remedies proposal and approval, there are two main conclusions of the Phase I

investigation, namely an unconditional clearance (if no impediment is found to an effective

competition potentially caused by the deal) or opening of a Phase II investigation. During the

Phase II analysis of the merger’s effects on competition and consumers, the Commission aims to

gather more extensive information (including companies’ internal documents and reports,

detailed questionnaires to market participants etc.) and further analyze the claimed efficiencies

potentially achieved by the companies after the deal would be finalized. If the merging parties can

prove that the efficiencies are merger specific (cannot be achieved by other means than by a

merger), verifiable (can be materialize and substantial enough) and passed-on to consumers, the

Commission may decide to clear the merger unconditionally. If, on the other hand, the

Commission concludes that the planned transaction would likely impede competition, it informs

the companies about its conclusions in a statement of objections which can result in either

conditional clearance (setting remedies necessary to be satisfied to correct the likely competition-

distortion effect of the deal before it is implemented) or final prohibition of the transaction if no

adequate remedies to the competition concerns are offered by the involved companies (European

Commission, 2016).

According to the wording of Article 14 of the EU Merger Regulation (2004), the parties

concerned in a proposed M&A deal may be charged a fine up to 1% of the aggregate turnover of

the companies if they intentionally or negligently supply incorrect, incomplete or misleading

information during the mandatory notification process or in response to any Commission’s

22

request. The same penalty applies for companies providing the requested records and other

documents in an incomplete form during the inspection and investigation conducted by the

Commission. In more severe cases, with respect to the EU Merger Regulation legislation, fines

not exceeding 10% of the overall turnover of the involved companies may be imposed – more

specifically, when the parties implement the proposed concentration without prior mandatory

notification (unless they are expressly authorized to do so) or in breach of the EU law; proceed

with a deal declared incompatible with the common market; or fail to comply with any measure,

condition or obligation ordered by the Commission’s decision. However, the size of the fine may

defer between cases regarding the nature, gravity and duration of the infringement. Based on the

Article 15 of the EU Merger Regulation (2004), additional penalty payments of up to 5% of the

average daily aggregate turnover of the companies concerned can be enforced by the

Commission for each day of delay mainly in order to compel them to provide complete and

correct information already requested by the authority, or comply any measure or obligation

imposed by the Commission’s decision.

3.2.3 The EU Merger Regulation Statistics

Since the implementation of the initial version of the EU Merger Regulation in 1990 until the end

of April 2016, the Commission has been notified about 6,163 transactions potentially harmful to

the relevant market competition and customer welfare. According to the European Commission

statistics (2016), only 127 of those deals (2.1%) were withdrawn by the companies concerned

after the Phase 1 investigation procedures run by the European Commission and 39 after the

Phase 2 (.6%). Regarding the number of conditional clearance cases, 376 proposed M&A

transactions (6.1%) have been allowed but subject to post-merger commitments, of which 259

were conditionally cleared after the first stage of the European Commission’s investigation and

117 based on the decision made after the further analysis during the Phase 2 procedure. Finally,

as little as 24 deals (.4%) have been prohibited over the more than 25 years of the EU Merger

Regulation being in force.

In Table 3, the data regarding the Commission’s decisions with respect to the merger control and

the EU common market competition objectives are summarized for the period of the sixth

merger wave compared to the current period of time (similarly to Table 2 for the US merger

regulation). For each year, the total amount of cases conditionally cleared by the authority (after

either Phase 1 or Phase 2 inspections) is provided as an indicator of the level of restrictiveness

applied by the EU Merger Regulation with respect to the corporate M&A activities. After such

clearance, the parties may proceed with the proposed deals but at the same time have to comply

with certain conditions (such as divesture of specific businesses after the merger completion or

committing to certain post-merger rules of their corporate behavior) which might limit their

future activities or go against their business strategy to such an extent that they would rather

withdraw the notification of the proposed concentration leading them to back out of the deal

(Slaughter and May, 2015).

Next, the sum of the M&A transactions not completed after the investigation run by the

European Commission is included in the table reflecting the effect of the EU regulation on the

pre-merger failure of certain deals. The reasons why the cases were not finalized consist of the

23

M&A notification withdrawal by the companies themselves (in reaction to the Phase 1 or Phase 2

Commission decision) and the concentration prohibition by the Commission because of the

competition disruption concerns connected to the deal. The amounts of cases with such

decisions can be found in Table 3 along with the total number of M&A cases notified by the

European Commission per each of the examined years. Additionally, the table contains the

percentage representation of each of the decision types within the total number of examined

deals.

Table 3: The Summary of the EU Merger Regulation Decisions

(2003 – 2008 and 2014 – 2015)

The Amount of Cases According to the Type of the EU Decision

2003 2004 2005 2006 2007 2008 2014 2015

Deal Conditional Clearance after Phase 1 or Phase 2 Investigation

17

(8.1%)

16

(6.5%)

18

(5.7%)

19

(5.5%)

22

(5.3%)

24

(6.9%)

17

(5.6%)

20

(5.9%)

Deal Withdrawal after Phase 1 or Phase 2 Investigation

0 6

(2.4%)

9

(2.8%)

9

(2.5%)

7

(1.7%)

13

(3.7%)

6

(2%)

8

(2.4%)

Deal Prohibited after Phase 1 or Phase 2 Investigation

0 1

(.4%) 0 0

1

(.2%) 0 0 0

Sum of the Deals Not Completed after the EU Investigation

0 7

(2.8%)

9

(2.8%)

9

(2.5%)

8

(1.9%)

13

(3.7%)

6

(2%)

8

(2.4%)

Sum of the Deals Penalized or Not Completed

17

(8.1%)

23

(9.3%)

27

(8.5%)

28

(8%)

30

(7.2%)

37

(10.6%)

23

(7.6%)

28

(8.3%)

All Notified Deals 211 247 318 356 402 348 303 337

Note: All the percentage values were .computed by the author.

Source: EU Merger Regulation Statistics of the European Commission (2016)

As can be seen in the summary of the EU Merger Regulation decisions, lower percentage of the

notified M&A deals were approved with additional commitments (certain post-merger rules of

24

the firms’ corporate behavior) towards the top of the sixth merger wave in Europe. While at the

beginning of the wave (in 2003) 8.1% of all the notified deals received such decision after the

Commission’s investigation, in the middle of the wave (in 2005 and 2006) the figure dropped to

5.6% on average. However, at the top of the sixth merger wave (in 2008), the number went up

again. Specifically, 6.9% of the total amount of deals were penalized or subject to compliance

with special requirements stated in a conditional clearance provision issued by the EU Merger

Regulation authorities. The data for the deals not completed (the sum of the deals withdrawn or

prohibited) in response to the EU investigation procedures exhibit a similar trend towards the

end of the sixth merger wave, ranging from 2.8% of the examined deals being not finalized in

2004 and 2005 to 3.7% in 2008. This implies that towards the top of a merger wave, more M&A

deals are further disciplined by the regulation authorities, as suggested by Galli and Pelkmans

(2000) and the US Federal Trade Commission’s merger control decisions.

3.3 Comparison of the EU and US Merger Control Mechanisms

This section of the paper serves as a summary of the key differences and similarities of the EU

Merger Regulation and the US antitrust laws applied to the merger control issues relevant for this

paper. Since the empirical analysis in Section 6 studies how the probability of pre-merger failure

of a deal is affected by the level of restrictiveness and nature of the M&A regulation along with

the changes in its enforcement corresponding to the course of a merger wave, the following

paragraphs are focused mainly on those differences between the two legislations which are

relevant for the econometric model.

First, comparing the US Federal Trade Commission and the European Commission decisions

concerning the antitrust and competition laws linked to the merger control, an opposite trend in

the regulation of the proposed deals during the global sixth merger wave can be observed in

Table 2 and Table 3. While in the EU, the percentage of the penalized or prohibited deals

decreased every year towards the top of the wave, in the US the figure increased annually.

However, the restrictiveness of the EU regulation (defined as the percentage of deals penalized

and prohibited) suddenly increased and reached its peak in 2008, the very top of the sixth merger

wave. Thus, the observations for both the US and EU transactions are in line with the studied

literature since Galli and Pelkmans (2000) claimed that towards the end of a merger wave, the

M&A regulation is expected to become stricter.

Second, it is important to note that, in contrast to the US antitrust laws, none of the decisions

and penalties enforced by the European Commission under the merger control mechanisms are

of a criminal law nature. Hence, they might be less deterrent for the companies planning an M&A

and lead to a lower amount of pre-merger deal withdrawals (Levy, 2004), and thus to a lower

probability of pre-merger failure analyzed in this paper.

Last but not least, as can be seen in Table 2 and Table 3, the percentage shares of penalized or

prohibited deals in all notified and examined cases are significantly different in the EU and the

USA within the whole studied period of time. More specifically, the highest share of such cases

exceeds 60% in the USA whereas in the EU it peaks at 10.6%. In addition, the fact that only 24

out of 6,163 notified deals were forbidden over the 25 years of the EU Merger Regulation can

25

make companies less concerned about the potential impact of the European Commission’s

investigation decision on the future of the proposed transaction. According to Phillips (2013), a

higher number of deterrent examples of prosecution and penalization related to the M&A

regulation may increase the amount of pre-merger deal withdrawals. Thus, according to the data

available, it is expected that the deals with a US target have a higher probability of pre-merger

failure than the European ones. In Section 6, the logit model analysis will examine this

relationship in detail.

26

4 Takeover Defense Tactics

The variety of legal takeover defense strategies available for companies’ managements to prevent

unwanted mergers or acquisitions differs between the American and European corporate culture

and governance systems. In this part of the paper, the basic characteristics and impacts of the six

most commonly used defense tactics are described. These include tools such as dual-class shares,

employee share ownership plans (ESOP), shareholder rights plans (poison pills), golden

parachute, staggered board of directors and greenmailing.

4.1 Dual-class Shares

A dual-class stock structure of a company’s shares refers to the issuance of two (or more) types

of shares differing in the voting rights and priority dividend payments connected to them. The

companies making use of such a stock structure usually distinguish between one class of shares

which is available publicly to all investors and the other share class that is offered to the company

founders, executive managers and other large stakeholders. The stock offered to general public

(usually called class A shares) has then fewer voting rights than the other one (usually referred to

as class B shares). Such a move can provide more power to certain individuals within the

company to keep the majority control over the firm helping them protect it from takeovers or

similar unwanted M&A activities of others (Magnan and Khalil, 2007).

As an example of the use of such a defense strategy in practice, it is argued by Smith et al. (2013)

that licensed firms have great incentives to protect themselves by the dual-class stock issuance. In

the industries highly regulated by the government license provisions, such as broadcasting and

cable industries, takeover of an existing company is often the only possible way to enter the

market. Thus, there is a relatively high amount of proposed M&A deals in these industries that

fail during the negotiation period due to the fact that the potential acquirers were not able to

obtain enough shares to gain control over the target company.

In the USA, the popularity of dual-class shares has noticeably increased within the last 15 years

after such activities were largely banned by the New York Stock Exchange (NYSE) from 1940

until 1980s and allowed again in 1988 when a lot of companies sought to shield themselves

during the hostile takeover era. Even though the Securities and Exchange Commission (SEC) has

adopted a rule prohibiting already listed companies to convert their single-class shares to the

dual-class ones, newly listed companies are allowed to freely use this defense tactics and they

commonly make use of this opportunity (Teen, 2015). On the contrary, the European corporate

governance and culture is rather not in favor of such a stock structure mostly because it is seen as

an unfair practice (with respect to public shareholders) which overly empowers the company’s

executives owning the privileged shares. In the Netherlands and other continental European

countries, the defense strategy has been legal but not used as often as in the USA. In the UK, the

tactics has been discouraged by institutional investors’ opposition almost to the point of total

disappearance (Smith et al., 2013).

27

4.2 ESOP (Employee Share Ownership Plans)

Employee share ownership plans are arrangements between a company’s managers and

employees based on trust. In case of a hostile takeover threat, the company’s managers can use

ESOP to allocate a certain amount of shares to the employees, who are considered to be a

friendly party, and thus prevent the company to be taken over. Often, the company’s stock

ownership is provided to the employees as part of their remuneration for work performance and

held in an ESOP trust until the employee retires or leaves the company. This way the company is

able to keep control over the certain number of shares provided to the employees and make it

more difficult for other parties to acquire sufficiently large stake in the firm (NCEO, 2016).

In the USA, ESOP has been by far the most popular form of corporate employee ownership. By

2014, more than 7 000 companies applied ESOP covering around 13.5 million employees

(NCEO, 2016). In the UK, employee share ownership has been promoted by the government

over the last 5 years and the popularity of this corporate ownership structure is currently

increasing (The Guardian, 2012). In the Netherlands, the number of companies providing their

employees with share ownership has grown as well over the last decade. For example, in 2007,

62.5% of companies listed on the Amsterdam stock exchange offered such programs as ESOP or

various kinds of employee financial participation schemes. The popularity of this defense strategy

in Europe is, however, not as high as in the USA (Wilke, 2014).

4.3 Poison Pills

Another practice adopted by managements of companies concerned about hostile takeover by

other firms is a shareholder rights plan, or so called poison pills, that represent wide range of

activities aiming to make it more difficult for a hostile bid to be successful. Such activities include

e.g. providing the existing target shareholders with a right to either subscribe at a heavy discount

to additional shares of the target or purchase shares of the acquirer at a discount after the merger;

and adding terms in the corporate directives that delay or set another barriers to the voting

process needed for change in management and corporate ownership structure (Sudarsanam,

2003).

In the UK, the use of poison pills as a defense strategy is not very popular and is constrained by a

number of factors. Especially an issuance of company’s shares or options to buy them at a

discount to impede unwanted M&A activities of other firms would not be regarded as a proper

use of corporate powers in the UK (Kastiel, 2014). Nevertheless, this is not the case in the

continental Europe (especially in the Netherlands) and the USA since such tactics are commonly

used in both of the regions. In the USA, poison pills occur mainly in the form of granting current

target shareholders an option to acquire preferred stock during the pre-merger period either at

the target (decreasing the amount of stock available for the bidder) or at the acquirer (diluting the

equity interest of existing acquirer shareholders who are not permitted to participate). However,

the inner mechanism of the Dutch type of poison pill is fundamentally different from the

American one. In the Netherlands, a Dutch foundation (stichting) is granted the option to

subscribe for preferred stock (at the price far below the market value) that typically holds the

voting power equivalent to the one of all target’s ordinary shares outstanding. Thus, the Dutch

28

poison pill usually leads to the failure of hostile bids “not by threatening them [the bidders] with

economic dilution, but by preventing them from acquiring voting control or electing allies to the

board” (UKSA, 2016).

4.4 Golden Parachute

This takeover defense strategy involves a large payment or any other financial compensation

guaranteed usually to a company’s executive if he or she should be dismissed as a result of a

merger or takeover. Thus, the tactics is used in order to make the acquisition of the target

company less attractive for the bidders once they find out that they would be obliged to pay

massive bonuses to the executive managers in order to achieve the desired post-takeover change

in control of the bought company (Sudarsanam, 2003). While in the USA, golden parachutes are

very common and generous (with respect to the executives and the amount of money paid to

them if their contract is terminated after the target company is taken over), the continental

European corporate culture has not adopted this kind of takeover defense in a large extent yet. In

the UK, several cases of merger-related windfalls for executives can be found but they are much

less popular than within the American companies (Bryant and Massoudi, 2015).

4.5 Staggered Board Amendments

Especially in the USA, staggered board amendments are a prominent practice in the corporate

law governing the leadership structure of a company. They refer to the situations when the terms

of the board of directors are set so that only a small part (usually one third), or at least less than

one half, of the directors may be elected during a period of one year. In practice, there are usually

several groups of directors which are each elected at a different time making it impossible for a

potential acquirer to change the whole board of directors within a short period time right after

the takeover (Sudarsanam, 2003). Once the majority of the company’s shareholders approve such

a rule affecting the dynamics of changes in the corporate structure and management, the

amendment can be implemented in the corporate bylaws and potentially used as a defense tactics

against undesirable takeover attempts by other companies.

As opposed to the American corporate structure, under the Dutch corporate law, it is common

to provide directors with four-year terms (in contrast to the one-year period typical for the US

companies) and unlike the US-style staggered boards, the directors of Dutch companies can be

removed by shareholder at any time for any reason within their term of office (Chazen and

Werdmuller, 2015). Similarly, company laws and corporate governance guidelines in the UK have

been preventing the occurrence of any type of staggered boards. Under the British guidelines, all

company directors must be reelected annually and fixing the composition of the board is not

possible in any way. Thus, the target board of directors has usually limited responsibilities in the

UK, performing mainly an advisory role, in contrast to the US-based gatekeeper role with respect

to any external M&A offers (Kastiel, 2014).

29

4.6 Greenmail

The last strategy discussed is a greenmail. This term stands for a defense against a hostile

takeover threat by an unfriendly party that holds a large stock in the target company. In such a

situation, the target is forced to repurchase its company’s shares from the so called corporate

raider (a company or an individual who owns the majority share in the target) in order to keep

control over its own company and halt the takeover bid. This repurchase is made at a substantial

premium (the greenmail payment) benefiting the threatening bidder. The target company can also

decide by itself to pursue the greenmail defense – to buy back a large amount of stock acquired

by a potential raider – in order to prevent any future takeover attempt. Ordinarily, the greenmail

payment is connected with an agreement that the raider will not initiate or continue in bidding for

control of the target (Sudarsanam, 2003).

In the USA, this tactics has been effectively reduced over the last two decades, mostly due to the

amendment to the US Internal Revenue Code which sets 50% tax on greenmail profits as a form

of punishment of such corporate behavior. The main reason for restriction of greenmail

payments was the fact that due to the high premium paid for the shares over the initial purchase

price, the target shareholders often lost out even if a hostile takeover was avoided (Huntsley,

2012). Regarding the UK corporate practice, the greenmail measure is still currently used by some