Embed Size (px)

Citation preview

March 18, 2010

ICICIdirect.com | Equity Research

Initiating Coverage

Growing strongly… Maruti Suzuki India (MSIL) maintained its leadership position with ~45% market share and its presence in the value for money segment, new launches and an extensive sales network, getting a boost from reviving domestic demand and rising export volumes. With strong export growth and an expanding domestic market, we expect MSIL’s net sales to grow at 21.9% CAGR to Rs 37,641.4 crore while net profit will grow at 35.4% CAGR to Rs 3,024.5 crore over FY09-12E. We are initiating coverage on the stock with a BUY rating. Market share and volume led growth MSIL improved its market share to 45.2% in passenger vehicles with stellar volume growth on the back of aggressive product launches, focus on rural and government employees and favourable economic conditions like improving GDP, high liquidity and lower interest rate regimes. In the 11 months of FY10, the company reported sales volume of 7.91 lakh units in the domestic market and 1.32 lakh units in the export market registering 22.1% and 30.7% growth, respectively. This is already exceeding FY09 sales by 16.5% to 9.23 lakh units. Volumes led tempo to be maintained With a strong economic outlook and revised GDP estimates of ~7.5% for FY10 and ~9% for FY11, increase in disposable income from softening of tax rate and focus on rural and government employees with buoyant export growth, we expect sales volumes to rise 1.6x FY09 to 12.6 lakh in FY12. Export growth is pegged at 2.6x FY09 while domestic volumes would grow 1.5x FY09. EBITDA margin to sustain After seeing a sharp dip in the EBITDA margin in FY09, we expect FY10 to end with an EBITDA margin of 13%. Going forward, it will sustain in the range of 12.9% to 13.3%. Rising raw material prices is a key risk to our EBITDA margin projections while a slew of launches with sustained volume growth provide an upside trigger for EBITDA margin expansion.

Valuations The company is debt free and enjoys cash and cash equivalent of Rs 222 (as per FY09 balance sheet) per share. We have valued the stock at 18x FY12E its core EPS and added Rs 222 as cash and cash equivalent to arrive at our target price of Rs 1,689 per share. On an EV/EBITDA basis, at 9x FY12E, we have arrived at Rs 1,643 per share. At the CMP of Rs 1,474, the stock is trading at 15.3x and 13.7x FY11E and FY12E EPS, respectively, and 8.7x and 7.6x FY11E and FY12E EV/EBITDA, respectively (Refer detailed valuation).

Exhibit 1: Key Financials (Rs Crore) Year end March 31 FY08 FY09 FY10E FY11E FY12ENet Sales (Rs crore) 18,227.5 20,775.6 31,684.5 34,957.7 37,641.4 EBITDA (Rs crore) 2587.5 1951.8 3968.5 4510.5 4994.8Net profit (Rs crore) 1730.9 1218.7 2418.9 2719.0 3024.5EPS (Rs) 54.2 40.3 83.7 94.1 104.7PE (x) 26.5 35.6 17.1 15.3 13.7PBV (x) 4.9 4.4 3.6 2.9 2.4EV to EBITDA (x) 16.2 20.6 10.1 8.7 7.6RoCE (%) 29.6 18.5 33.2 29.8 27.9RoNW (%) 21.7 13.3 23.1 21.0 19.3

Source: Company, ICICIdirect.com Research

Maruti Suzuki India (MARUTI) Rs 1435

Rating Matrix Rating : Buy

Target : Rs 1689

Target Period : 12 months

Potential Upside : 17.7%

YoY Growth (%) FY09 FY10E FY11E FY12E

Net sales 14.0 52.5 10.3 7.7EBITDA -24.6 110.3 9.9 10.7Adj. net profit -29.6 106.1 8.3 11.2EPS -25.7 115.8 8.3 11.2

Target Multiples (x) FY09 FY10E FY11E FY12E

Target PE 41.9 20.2 18.0 16.1EV/EBITDA 24.4 11.9 10.3 9.1Price/BV 5.2 4.2 3.4 2.9

Stock Metrics Bloomberg Code MSIL INReuters Code MRTI.BOFace value (Rs) 5Promoters Holding(%) 54.2Market Cap (Rs cr) 41471.552 week H/L (Rs) 1737 / 692Sensex 17,489Average volumes 125,497

Comparative return matrix (%) Stock returns ( 1M 3M 6M 12MMaruti Suzuki 7.6 -9.7 -2.0 116.9M&M 5.6 0.8 32.3 242.2Tata Motors 14.1 14.5 58.4 464.3

Price movement (Stock vs. Nifty)

500

700

900

1,100

1,300

1,500

1,700

1,900

Mar-10Sep-09Mar-092,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

Maruti Suzuki NIFTY

Analyst’s name

Supriya Madye (Khedkar) [email protected]

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 2

Company Background Maruti Suzuki India was incorporated in February 1981 by the Government of India and Suzuki Motor Corporation (SMC) of Japan. The company commenced commercial production in 1982 and rolled out its first car Maruti 800 (M800). SMC started the company with an initial stake of 26% and raised the same to 55% while the government completely exited in FY07. MSIL has four plants, three in Gurgaon and one in Manesar with a total plant capacity of 1 million unit – 0.7 million units in Gurgaon and 0.3 million units in the Manesar plant. The management now plans to increase the same to 1.3 million units by FY13 and 1.5 million units by FY15. However, capital expenditure (capex) is yet to be decided. MSIL’s key strength lies in its wide range of cars to suit the different needs of customers. The company has a portfolio of 14 brands, including Maruti 800, Omni, Eeco, Zen Estilo, Alto, WagonR, off-roader Gypsy, mid size Sx4, compact Swift, A-star, Ritz, sedan Dzire and Luxury SUV Grand Vitara. MSIL is planning to launch new variants to existing models to suit emission norms and plans to launch the Kizashi in FY11. Exhibit 2: Product portfolio at every price point (Rs’000)

M800 Omni Eeco AltoZen Estilo

A StarSwift Gypsy Ritz Dzire

Sx4

Kizashi

Vitara

WagonR 100

250

400

550

700

850

1000

1150

1300

1450

1600

Source: Company, ICICIdirect.com Research

Exhibit 3: Pricing range for product portfolio Segment Models Price range (Rupee lakhs)A1 M800 1.7-2.2A2 Alto, WagonR, Estilo, Swift, Astar, Ritz 2.5-5.5A3 Sx4, Dzire 5.5-8.8C Omni, Eeco 2.0-2.3MUV Gypsy 5.0 -5.45MUV Grand Vitara 16 and above

Source: Company, ICICIdirect.com Research

Shareholding pattern (Q3FY10)

% HoldingsPromoters 55.0Institutional Investors 39.1Other Investors 4.0Public 1.8 Promoter and institutional holding trend (%)

54.2 54.2 54.2 54.2

39.139.139.341.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

Q4FY09 Q1FY10 Q2FY10 Q3FY10

Promoters Institutional

Source: Company, ICICIdirect.com Research

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 3

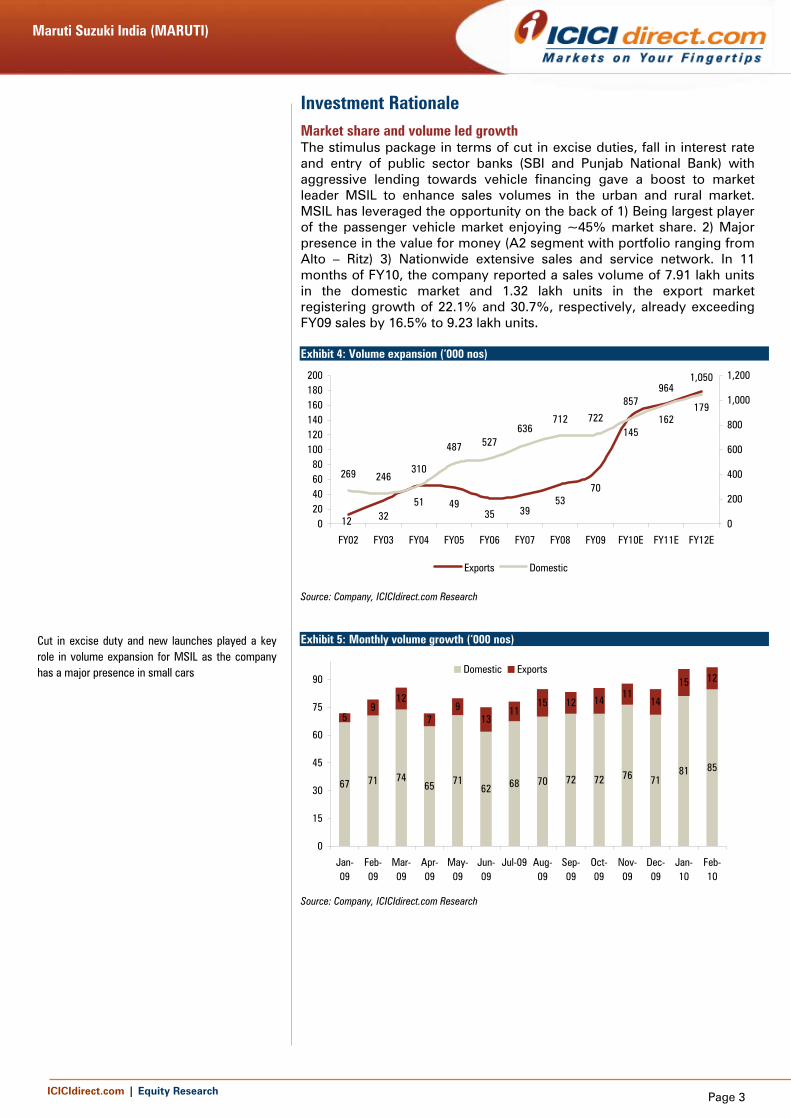

Investment Rationale Market share and volume led growth The stimulus package in terms of cut in excise duties, fall in interest rate and entry of public sector banks (SBI and Punjab National Bank) with aggressive lending towards vehicle financing gave a boost to market leader MSIL to enhance sales volumes in the urban and rural market. MSIL has leveraged the opportunity on the back of 1) Being largest player of the passenger vehicle market enjoying ~45% market share. 2) Major presence in the value for money (A2 segment with portfolio ranging from Alto – Ritz) 3) Nationwide extensive sales and service network. In 11 months of FY10, the company reported a sales volume of 7.91 lakh units in the domestic market and 1.32 lakh units in the export market registering growth of 22.1% and 30.7%, respectively, already exceeding FY09 sales by 16.5% to 9.23 lakh units. Exhibit 4: Volume expansion (‘000 nos)

3251 49

35 3953

70

145162

179

12

269 246310

487 527636

712 722

857964

1,050

020406080

100120140160180200

FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

0

200

400

600

800

1,000

1,200

Exports Domestic

Source: Company, ICICIdirect.com Research

Exhibit 5: Monthly volume growth (‘000 nos)

67 71 7465 71

62 68 70 72 72 76 7181 85

59

12

79

1311

15 12 1411

14

15 12

0

15

30

45

60

75

90

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09 Aug-09

Sep-09

Oct-09

Nov-09

Dec-09

Jan-10

Feb-10

Domestic Exports

Source: Company, ICICIdirect.com Research

Cut in excise duty and new launches played a keyrole in volume expansion for MSIL as the companyhas a major presence in small cars

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 4

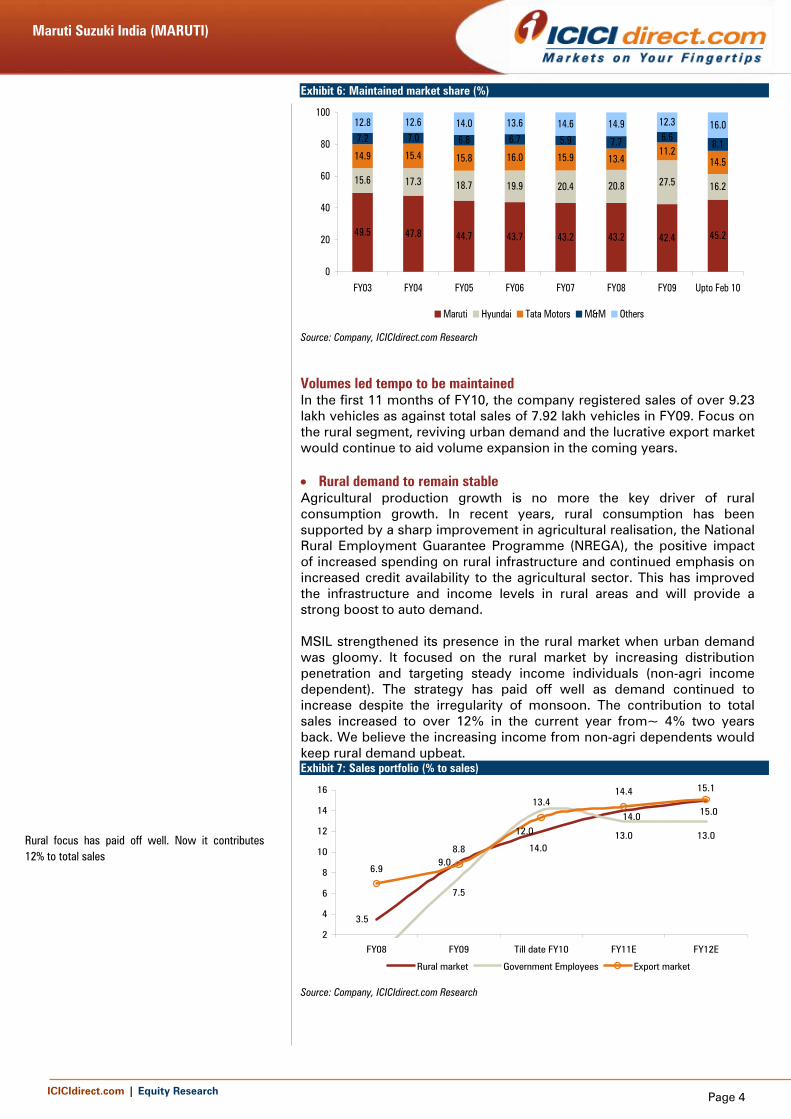

Exhibit 6: Maintained market share (%)

49.5 47.8 44.7 43.7 43.2 43.2 42.4 45.2

15.6 17.3 18.7 19.9 20.4 20.8 27.5 16.2

14.9 15.4 15.8 16.0 15.9 13.411.2

14.5

7.2 7.0 6.8 6.7 5.9 7.7 6.68.1

12.8 12.6 14.0 13.6 14.6 14.9 12.3 16.0

0

20

40

60

80

100

FY03 FY04 FY05 FY06 FY07 FY08 FY09 Upto Feb 10

Maruti Hyundai Tata Motors M&M Others

Source: Company, ICICIdirect.com Research

Volumes led tempo to be maintained In the first 11 months of FY10, the company registered sales of over 9.23 lakh vehicles as against total sales of 7.92 lakh vehicles in FY09. Focus on the rural segment, reviving urban demand and the lucrative export market would continue to aid volume expansion in the coming years. • Rural demand to remain stable Agricultural production growth is no more the key driver of rural consumption growth. In recent years, rural consumption has been supported by a sharp improvement in agricultural realisation, the National Rural Employment Guarantee Programme (NREGA), the positive impact of increased spending on rural infrastructure and continued emphasis on increased credit availability to the agricultural sector. This has improved the infrastructure and income levels in rural areas and will provide a strong boost to auto demand. MSIL strengthened its presence in the rural market when urban demand was gloomy. It focused on the rural market by increasing distribution penetration and targeting steady income individuals (non-agri income dependent). The strategy has paid off well as demand continued to increase despite the irregularity of monsoon. The contribution to total sales increased to over 12% in the current year from~ 4% two years back. We believe the increasing income from non-agri dependents would keep rural demand upbeat. Exhibit 7: Sales portfolio (% to sales)

3.5

9.0

12.0

7.5

13.0 13.0

6.9

8.8

13.414.4 15.1

14.0 15.0

14.0

2

4

6

8

10

12

14

16

FY08 FY09 Till date FY10 FY11E FY12E

Rural market Government Employees Export market

Source: Company, ICICIdirect.com Research

Rural focus has paid off well. Now it contributes12% to total sales

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 5

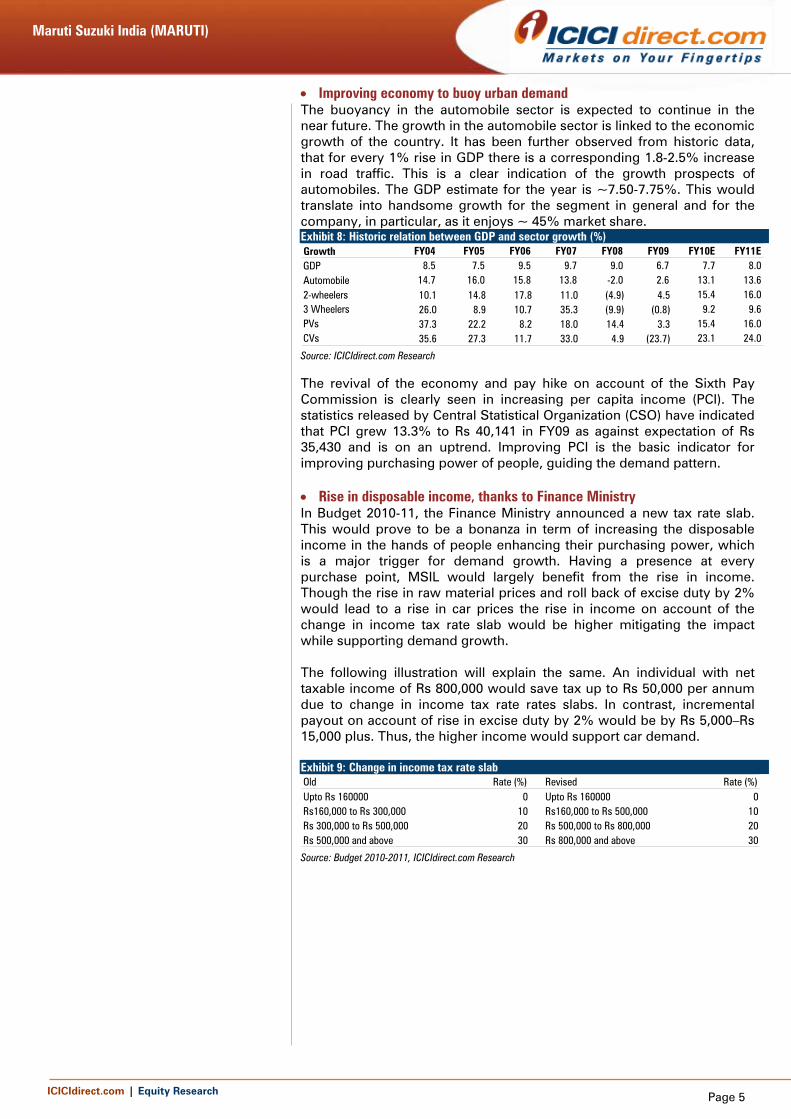

• Improving economy to buoy urban demand The buoyancy in the automobile sector is expected to continue in the near future. The growth in the automobile sector is linked to the economic growth of the country. It has been further observed from historic data, that for every 1% rise in GDP there is a corresponding 1.8-2.5% increase in road traffic. This is a clear indication of the growth prospects of automobiles. The GDP estimate for the year is ~7.50-7.75%. This would translate into handsome growth for the segment in general and for the company, in particular, as it enjoys ~ 45% market share. Exhibit 8: Historic relation between GDP and sector growth (%) Growth FY04 FY05 FY06 FY07 FY08 FY09 FY10E FY11EGDP 8.5 7.5 9.5 9.7 9.0 6.7 7.7 8.0Automobile 14.7 16.0 15.8 13.8 -2.0 2.6 13.1 13.62-wheelers 10.1 14.8 17.8 11.0 (4.9) 4.5 15.4 16.03 Wheelers 26.0 8.9 10.7 35.3 (9.9) (0.8) 9.2 9.6PVs 37.3 22.2 8.2 18.0 14.4 3.3 15.4 16.0CVs 35.6 27.3 11.7 33.0 4.9 (23.7) 23.1 24.0

Source: ICICIdirect.com Research

The revival of the economy and pay hike on account of the Sixth Pay Commission is clearly seen in increasing per capita income (PCI). The statistics released by Central Statistical Organization (CSO) have indicated that PCI grew 13.3% to Rs 40,141 in FY09 as against expectation of Rs 35,430 and is on an uptrend. Improving PCI is the basic indicator for improving purchasing power of people, guiding the demand pattern. • Rise in disposable income, thanks to Finance Ministry In Budget 2010-11, the Finance Ministry announced a new tax rate slab. This would prove to be a bonanza in term of increasing the disposable income in the hands of people enhancing their purchasing power, which is a major trigger for demand growth. Having a presence at every purchase point, MSIL would largely benefit from the rise in income. Though the rise in raw material prices and roll back of excise duty by 2% would lead to a rise in car prices the rise in income on account of the change in income tax rate slab would be higher mitigating the impact while supporting demand growth. The following illustration will explain the same. An individual with net taxable income of Rs 800,000 would save tax up to Rs 50,000 per annum due to change in income tax rate rates slabs. In contrast, incremental payout on account of rise in excise duty by 2% would be by Rs 5,000–Rs 15,000 plus. Thus, the higher income would support car demand. Exhibit 9: Change in income tax rate slab Old Rate (%) Revised Rate (%)Upto Rs 160000 0 Upto Rs 160000 0Rs160,000 to Rs 300,000 10 Rs160,000 to Rs 500,000 10Rs 300,000 to Rs 500,000 20 Rs 500,000 to Rs 800,000 20Rs 500,000 and above 30 Rs 800,000 and above 30

Source: Budget 2010-2011, ICICIdirect.com Research

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 6

Exhibit 10: Impact analysis on change in income tax rate slab and excise duty rates Particulars Amount (Rs)Effective savings from new income tax ratesTax liability as per old rates 144000Tax liability as per new rates 94000Savings on tax liability 50000Incremental payout due to rise in excise duty by 2% on car prices upto250,000 5,000350,000 7,000450,000 9,000600,000 12,000Car above Rs 750,000 15000+Additional costs due to rise in excise duty 5,000 - 15,000+

Source: ICICIdirect.com Research

• Attractive offers by financial institution The financial meltdown, increasing non performing assets (NPA) or bad loans and downturn in the automobile industry had forced financing leaders to take a step back towards the auto loan portfolio. This squeezed liquidity, which was the key concern for de-growth in auto demand from H2FY08 to FY09. This also resulted in a rise in interest rates on the vehicle loan portfolio. An increase in financial lending with easing interest rates played a major role in translating pent-up demand into actual sales in the past few months reviving the subdued performance of the sector. Exhibit 11: Interest rate vis-à-vis industry and company growth (%)

13.510.5 10.3 9.5

18.014.4

3.3

10

16.2

36.7

20.6

1.4

29.9

48.7

9.511.5

17.7

12.0

0

5

10

15

20

25

30

35

40

45

50

FY07 FY08 FY09 Q1FY10 Q2FY10 Q3FY10Av int rate (%) Industry gr (%) MSIL gr (%)

Source: Company, ICICIdirect.com Research

It has been observed that when interest rates were rising, MSIL grew lower than the industry while when interest rates eased, MSIL’s growth was faster than the industry. This also indicates that growth is highly sensitive to interest rate movements for MSIL. Going forward… Currently, most of the banks are offering auto loans at an interest rate of 8%. This augurs well for MSIL from a sales perspective. However, with the rise in excise duty coupled with higher raw material prices companies are increasing car prices. This can slow down the sales growth, going forward. Recently, private banks that had re-entered auto loans with an incentive scheme of 8-8.25% have withdrawn their schemes on March 4, 2010. They have announced interest rate hikes of 25-50 basis points. This can

Over 70% of sales are loan funded and easing normsboosted demand Interest rates are expected to rise in the near future.However, they would remain low from peak levels oflast year. Hence, there is no immediate risk

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 7

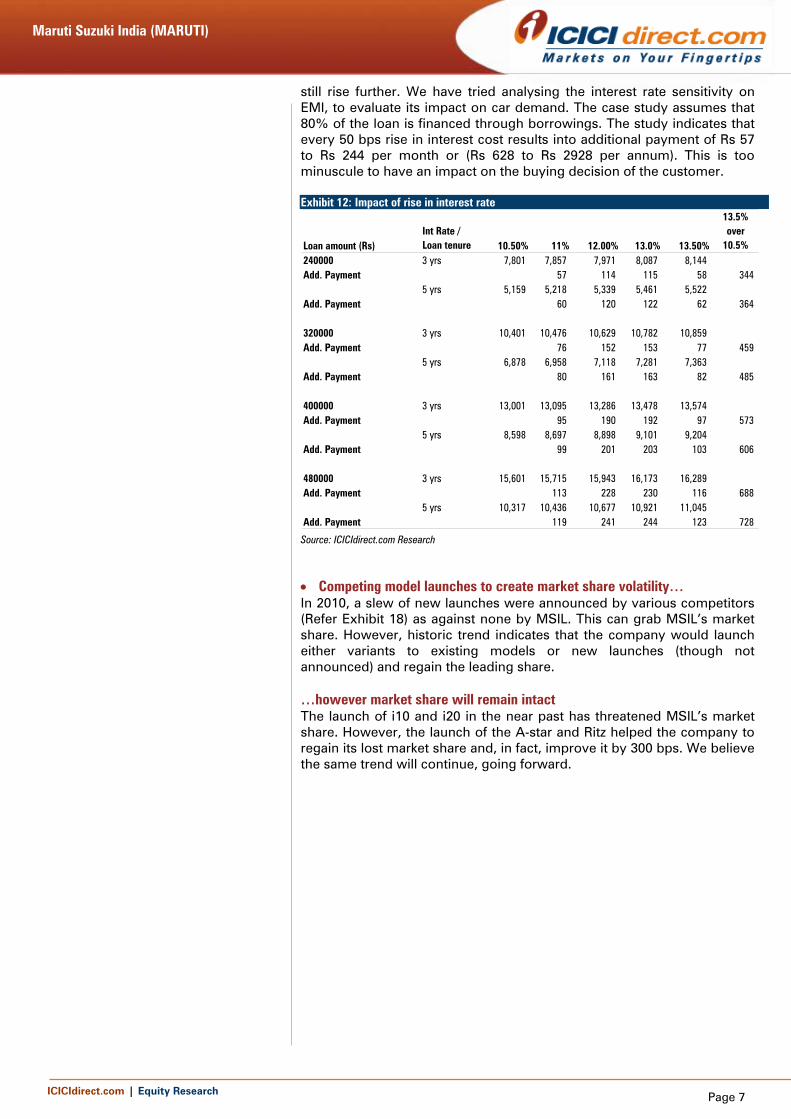

still rise further. We have tried analysing the interest rate sensitivity on EMI, to evaluate its impact on car demand. The case study assumes that 80% of the loan is financed through borrowings. The study indicates that every 50 bps rise in interest cost results into additional payment of Rs 57 to Rs 244 per month or (Rs 628 to Rs 2928 per annum). This is too minuscule to have an impact on the buying decision of the customer. Exhibit 12: Impact of rise in interest rate

Loan amount (Rs)Int Rate / Loan tenure 10.50% 11% 12.00% 13.0% 13.50%

13.5% over

10.5%240000 3 yrs 7,801 7,857 7,971 8,087 8,144Add. Payment 57 114 115 58 344

5 yrs 5,159 5,218 5,339 5,461 5,522Add. Payment 60 120 122 62 364

320000 3 yrs 10,401 10,476 10,629 10,782 10,859Add. Payment 76 152 153 77 459

5 yrs 6,878 6,958 7,118 7,281 7,363Add. Payment 80 161 163 82 485

400000 3 yrs 13,001 13,095 13,286 13,478 13,574Add. Payment 95 190 192 97 573

5 yrs 8,598 8,697 8,898 9,101 9,204Add. Payment 99 201 203 103 606

480000 3 yrs 15,601 15,715 15,943 16,173 16,289Add. Payment 113 228 230 116 688

5 yrs 10,317 10,436 10,677 10,921 11,045Add. Payment 119 241 244 123 728

Source: ICICIdirect.com Research

• Competing model launches to create market share volatility… In 2010, a slew of new launches were announced by various competitors (Refer Exhibit 18) as against none by MSIL. This can grab MSIL’s market share. However, historic trend indicates that the company would launch either variants to existing models or new launches (though not announced) and regain the leading share. …however market share will remain intact The launch of i10 and i20 in the near past has threatened MSIL’s market share. However, the launch of the A-star and Ritz helped the company to regain its lost market share and, in fact, improve it by 300 bps. We believe the same trend will continue, going forward.

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 8

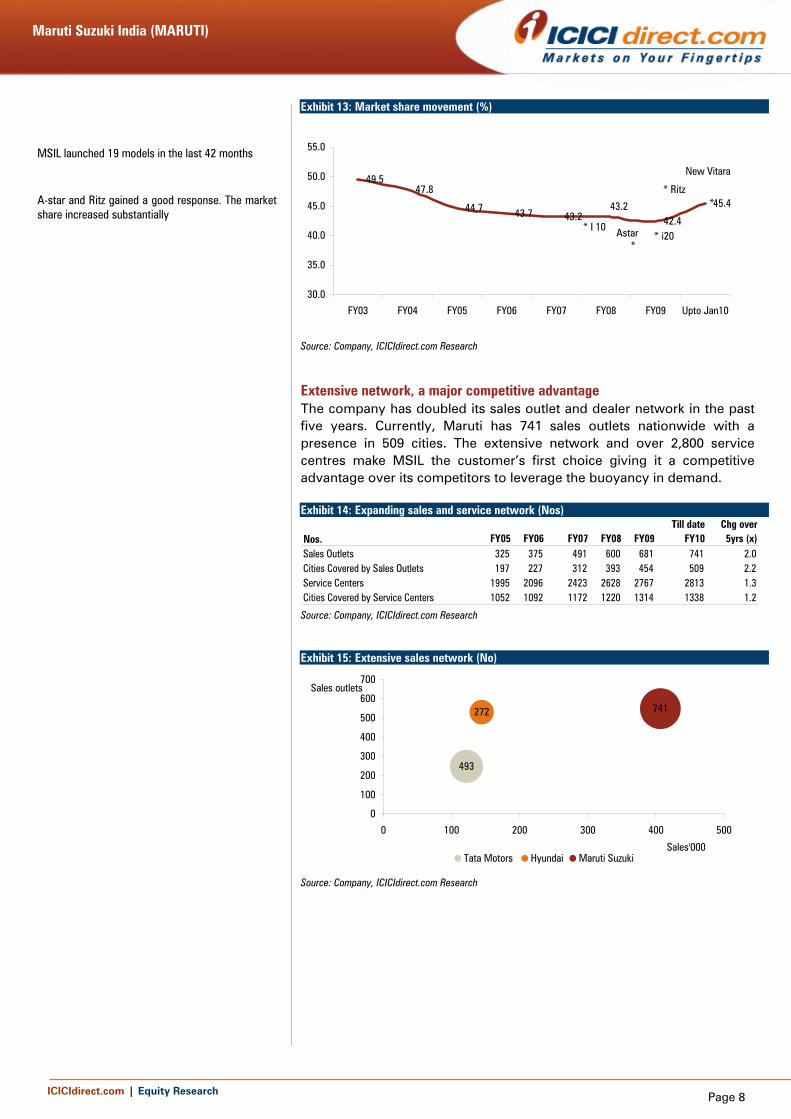

Exhibit 13: Market share movement (%)

49.547.8

44.7 43.7 43.2 42.4

45.443.2

30.0

35.0

40.0

45.0

50.0

55.0

FY03 FY04 FY05 FY06 FY07 FY08 FY09 Upto Jan10

* I 10

*

*

Astar

* Ritz

New Vitara

* i20

Source: Company, ICICIdirect.com Research

Extensive network, a major competitive advantage The company has doubled its sales outlet and dealer network in the past five years. Currently, Maruti has 741 sales outlets nationwide with a presence in 509 cities. The extensive network and over 2,800 service centres make MSIL the customer’s first choice giving it a competitive advantage over its competitors to leverage the buoyancy in demand. Exhibit 14: Expanding sales and service network (Nos)

Nos. FY05 FY06 FY07 FY08 FY09Till date

FY10Chg over

5yrs (x)Sales Outlets 325 375 491 600 681 741 2.0Cities Covered by Sales Outlets 197 227 312 393 454 509 2.2Service Centers 1995 2096 2423 2628 2767 2813 1.3Cities Covered by Service Centers 1052 1092 1172 1220 1314 1338 1.2 Source: Company, ICICIdirect.com Research

Exhibit 15: Extensive sales network (No)

493

272 741

0

100

200

300

400

500

600

700

0 100 200 300 400 500

Tata Motors Hyundai Maruti Suzuki

Sales outlets

Sales'000

Source: Company, ICICIdirect.com Research

MSIL launched 19 models in the last 42 months

A-star and Ritz gained a good response. The marketshare increased substantially

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 9

Other developments

True value initiatives The company is also gaining major market share in the used car market and gaining a very good response to its True Value initiative. Through this initiative, the company has sold 1,23,000 units in the second car market in FY09 registering growth of 23% over FY08. The rising sales through True Value would increase its sales as well as market share. Smooth logistic movement The company has commissioned a dedicated roll on roll off car terminal at Mundra Sea Port in partnership with Mundra Port and Special Economic Zone Ltd (MPSEZL) for a total investment of Rs 100 crore. MSIL’s contribution is at 40%. This would help the company to smoothen its export sales. Volkswagen buying stake in parent company Suzuki Motors German carmaker Volkswagen (VW) has announced that it will purchase a 19.9% stake in Suzuki Motors Corporation for US$2.5 billion. In turn, SMC would invest half of the money received from VW into shares of VW. Through this deal VW would have access to SMC’s expertise in manufacturing small cars and its dominant presence in emerging markets like India. SMC, in turn, would have access to VW’s efficient and environmental-friendly drive train and vehicle technologies. Implications for Maruti Suzuki The deal will not bring any immediate structural change in Maruti Suzuki’s business model. However, in the long run, it can have access to VW’s technological know-how to strengthen its presence in the global market where cost-effective and fuel efficient cars are gaining acceptance. We also see the possibility of MSIL having a deal with VW like the one it has for Nissan Motors. However, it is premature to comment on the possible future development and its impact on MSIL but they are likely to bring synergies in the long run. Capex The company will increase its gross block by ~ Rs 2,500 crore in FY10 and would spend ~ Rs 1,700 crore in FY11 to expand its capacities to 1.25 million units by FY12. We expect the company to spend around Rs 1,500–2000 crore per annum on upgradation as well as product development expenses. The company also plans to increase its total capacity to 1.5 million by FY15. However, we have accounted for capacity of 120,000 units by FY12 in our financial model.

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 10

Risks and concerns Losing status of people’s car with Nano launch With the launch of Nano by Tata Motors, the company has lost its people’s car status and is likely to face tougher competition in the segment where M800 was the only vehicle available at the entry level. We have analysed the running and maintenance cost of both cars and found the cost-benefit was more in favour of Tata’s Nano. Exhibit 16: Comparison between M800 and Tata Nano Particulars Nano M800 Diff.Assumptionsprice (Rs/ unit) 160000 175000 -15000Down payment 15% 15%Loan requirements 136000 148750 -12750Loan tenure (months) 36 36Rate of interest 10.00% 10.00%EMI 4,388 4,800 -411Petrol prices 55 55Cost analysisAv. monthly usage 1,000 km 1,000 kmAv. fuel efficiency 18.4 km/lt 12 km/lt 4km/ltFuel consumption 54.3 83.3 -29.0Total cost per month 2989 4583 -1594.2Additional monthly maintenance 500 500 0.0EMI (if financed by borrowed fund) 4388 4800 -411Total cash outflow 7877 9883 -2006Savings if switchover to NANO 2006

Source: ICICIdirect.com Research

Export volumes may be volatile Exports growth for MSIL has been splendid in FY10 with the scrappage scheme in Europe and launch of A-star in that market, where contribution to sales increased to ~14% in the year. However, the pulling off of scrappage schemes would surely impact export growth, going forward. The company received a huge response to the A-star in the European market. It is sold as Alto in Europe while it is sold as Nissan’s Pixo in the United Kingdom, Germany and Italy. It is also sold as Celerion in non-European nations. Total exports of A-star till date (since inception) have been over 1,00,000 units in the European market and as Pixo contributed ~35,200 units. In the domestic market, it sold over 25,580 units. Towards the end of February 2010, MSIL recalled 1,00,000 A-stars on account of faulty fuel gasket. A-star is the largest selling model of the company in the overseas market and the fault that occurred in the model is likely to dampen its demand in the near short-term. However, we believe the corrective actions from company will bring a spurt in demand in the long-term.

The company will make ~1,00,000 units for Suzuki Corporation and ~30,000 units for Nissan Motors. Gradually, the numbers will grow as A-star is gaining a good response. We expect export volumes to grow 2.6x FY09 to 1.8 lakh units in the next three years.

M800 sales, however, accounted for only 6% of totalsales. The impact may be marginal

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 11

Exhibit 17: Export growth trend

35 3953

70

145162

179

-20406080

100120140160180200

FY06 FY07 FY08 FY09 FY10E FY11E FY12E

Thou

sand

s

-40

-20

0

20

40

60

80

100

120

Exports nos (LHS) YoY growtb % RHS

Source: Company Research, ICICIdirect.com Research

Royalty payments The company makes royalty payments to parent company Suzuki Corporation and the same is paid at 3% on old models and 5% on new models for 10 years. This would increase the royalty payment as the company has launched a slew of new models in the past few months and proposes to launch the Kizashi in the projected period. However, some vehicles are getting free from royalty payment due to completion of the royalty period of 10 years. The current year is the last year for payment of royalty for Alto. This would save cost of 3% on every Alto sold and the benefits may not be necessarily passed on to end customers keeping realisation intact. MSIL sells ~20,000 units of Alto per month. This would bring savings of ~Rs 120–150 crore per year contributing to the EBITDA. New model launches to intensify competition in small car segment Though the company enjoys a leadership position with ~50% market share in the passenger car segment, the new launches and price wars from competitors continue to threaten its leadership position as well as loss of market share. After the launch of the Hyundai i10 and i20, the company has lost market share in the segment while with the launch of Tata Nano, it has already lost its people’s car status. The company continues to face competition from General Motors’ Spark, Nissan’s future launch of Micra, Tata Motors’ Punto and many more; a threat to maintaining market share, going forward. Exhibit 18: Exhibit 18: New launches in 2010 Company Car Model Price Range (Rs Lakh)Ford Figo Rs 3.5 - 5 Nissan Micra Rs 4 - 5Mahindra Renault Sandero Rs 4 - 5Volkwagen Polo Rs 4 - 6 Toyota Avanza Rs 6 - 8Tata Indica Vista Electric NAHyundai i30 NAHyundai i10 Electric NA

Source: SIAM, ICICIdirect.com Research

No new launches in the value for money categoryhave been announced by MSIL. Hence, the proposedlaunches from competitors is a major concern inmaintaining market share, going forward

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 12

Higher commodity costs to pressurise margins Steel is the main raw material for the company and prices touched the peak during Q3FY09. From here, it had started smoothening and was Rs 28,000 per tonne during Q4FY09. Peak steel prices had a significant impact on the EBITDA margin and the correction has added to EBITDA margin expansion during the period. Steel prices have started rising and are currently ruling around Rs 30,000 per tonne. Rising steel prices would continue to pressurise the EBITDA margin. Exhibit 19: Steel prices movement (Rs /Tonne)

31,57434,532

27,661

65,519

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Apr-07

Jun-0

7

Aug-07

Oct-07

Dec-07

Feb-0

8Apr-

08

Jun-0

8

Aug-08

Oct-08

Dec-08

Feb-0

9Apr-

09

Jun-0

9

Aug-09

Oct-09

Source: ICICIdirect.com Research, Reuters

We have done a sensitivity analysis to evaluate the impact of the rise in steel prices on the EBITDA margin and, thereby, on the EPS. We have observed that a 2% movement on either side brings ~ Rs 1.7 and ~ Rs 3 volatility in the EPS for FY11E and FY12E, respectively. We have assumed three scenarios of

• Base Case - where we have assumed a price hike in steel representing the current scenario

• A 2% rise above our expectation in the base case • A 2% fall from our expectation in the base case

Exhibit 20: Steel prices sensitivity on earnings

FY10E FY11E FY12EBase case EBITDA margins (%) 12.95 12.9 13.3

EPS(Rs) 86.9 94.1 104.7

2 % rise above our expectation EBITDA margins (%) 12.9 12.7 12.9EPS(Rs) 86.2 92.3 101.5

2 % fall from our expectation EBITDA margins (%) 13.04 13.1 13.6EPS(Rs) 87.6 95.8 107.7

Source: ICICIdirect.com Research

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 13

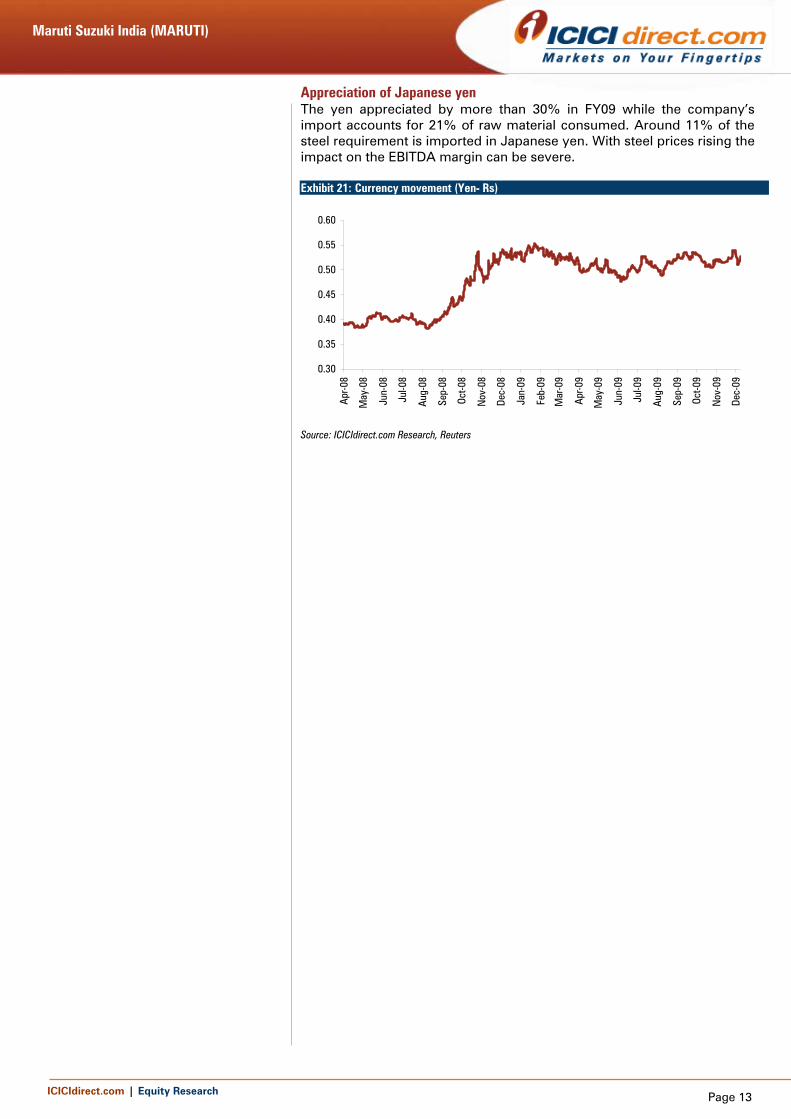

Appreciation of Japanese yen The yen appreciated by more than 30% in FY09 while the company’s import accounts for 21% of raw material consumed. Around 11% of the steel requirement is imported in Japanese yen. With steel prices rising the impact on the EBITDA margin can be severe. Exhibit 21: Currency movement (Yen- Rs)

0.30

0.35

0.40

0.45

0.50

0.55

0.60

Apr-0

8

May

-08

Jun-

08

Jul-0

8

Aug-

08

Sep-

08

Oct-0

8

Nov

-08

Dec-

08

Jan-

09

Feb-

09

Mar

-09

Apr-0

9

May

-09

Jun-

09

Jul-0

9

Aug-

09

Sep-

09

Oct-0

9

Nov

-09

Dec-

09

Source: ICICIdirect.com Research, Reuters

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 14

Financials Sales to grow at CAGR of 21.9%

FY09 hit by downturn… The year FY09 was severely impacted by the downturn in demand on account of financing scarcity, higher raw material prices and higher interest costs. This restricted volume growth to 3.6% while realisation was higher by only 5.4%.

…FY10 a turnaround

With easing financial norms, fall in interest rates and the stimulus package of reduction in excise duties by 4% to 8% on small cars, the pent-up demand has actually materialised and in the first 10 months FY10. MSIL reported sales growth of 22.3% to 7.06 lakh units in the domestic market. Export incentives like scrappage schemes in the European market further added fuel to growth while exports volume grew 141.9% to 1.2 lakh units.

Going forward

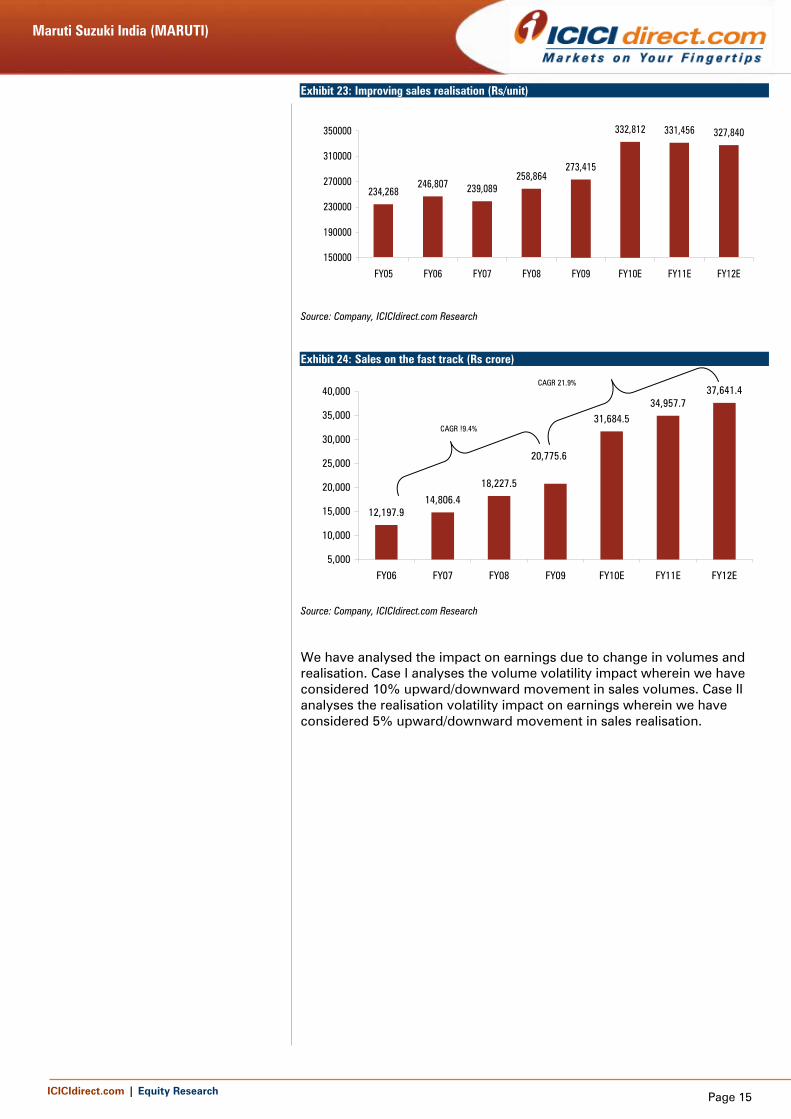

We expect the sales volumes to grow by 1.6x FY09. This would bring 21.9% growth in sales revenue over FY09-FY12E. The addition of A-star and Ritz high value, high margin models to its portfolio would increase its sales realisation from over Rs 2.7 lakh per unit to over Rs 3.32 lakh per unit, a growth of 21.6%. Since the company has not announced any new model launch other than the Kizashi in FY11, we expect the realisation to be maintained at this level. Exhibit 22: Sales volume on the rise (Nos)

536,301 561,819

674,924764,842

1,002,300

1,126,682

1,228,914

792,167

400000500000600000700000800000900000

1000000110000012000001300000

FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

Source: Company, ICICIdirect.com Research

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 15

Exhibit 23: Improving sales realisation (Rs/unit)

234,268246,807 239,089

258,864273,415

332,812 331,456 327,840

150000

190000

230000

270000

310000

350000

FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

Source: Company, ICICIdirect.com Research

Exhibit 24: Sales on the fast track (Rs crore)

12,197.914,806.4

18,227.5

31,684.534,957.7

37,641.4

20,775.6

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

FY06 FY07 FY08 FY09 FY10E FY11E FY12E

CAGR 21.9%

CAGR !9.4%

Source: Company, ICICIdirect.com Research

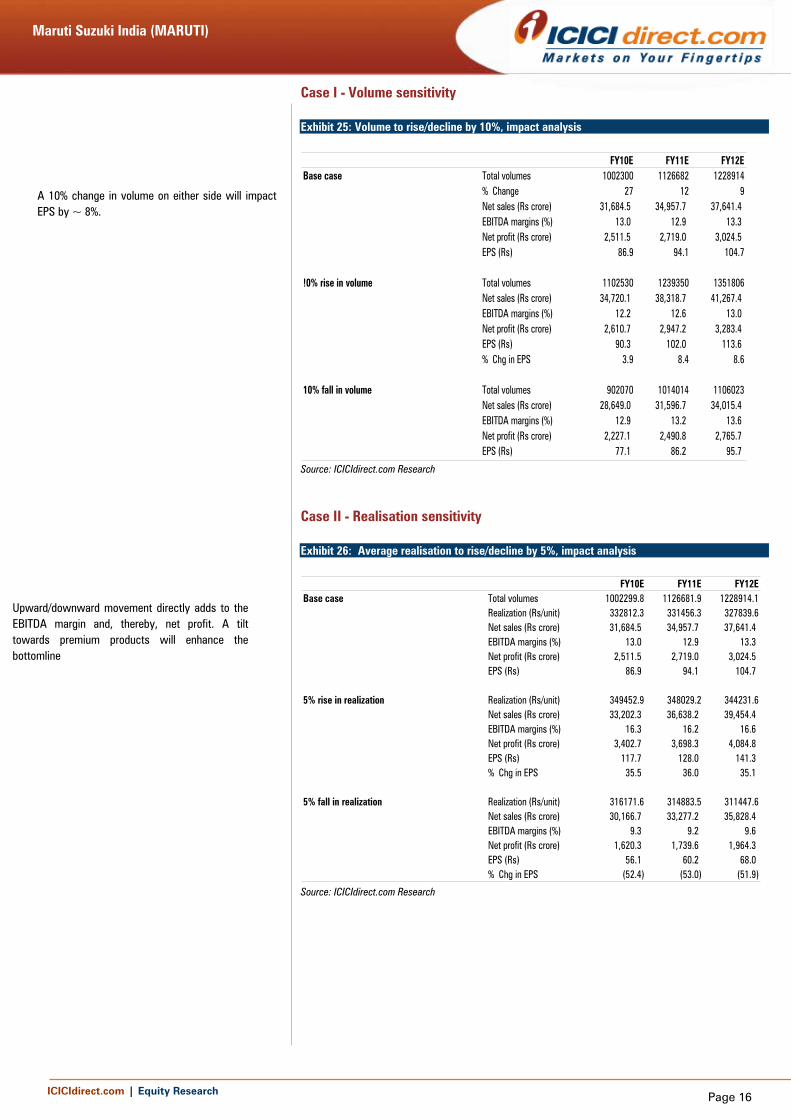

We have analysed the impact on earnings due to change in volumes and realisation. Case I analyses the volume volatility impact wherein we have considered 10% upward/downward movement in sales volumes. Case II analyses the realisation volatility impact on earnings wherein we have considered 5% upward/downward movement in sales realisation.

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 16

Case I - Volume sensitivity

Exhibit 25: Volume to rise/decline by 10%, impact analysis

FY10E FY11E FY12EBase case Total volumes 1002300 1126682 1228914

% Change 27 12 9Net sales (Rs crore) 31,684.5 34,957.7 37,641.4 EBITDA margins (%) 13.0 12.9 13.3 Net profit (Rs crore) 2,511.5 2,719.0 3,024.5 EPS (Rs) 86.9 94.1 104.7

!0% rise in volume Total volumes 1102530 1239350 1351806Net sales (Rs crore) 34,720.1 38,318.7 41,267.4 EBITDA margins (%) 12.2 12.6 13.0 Net profit (Rs crore) 2,610.7 2,947.2 3,283.4 EPS (Rs) 90.3 102.0 113.6 % Chg in EPS 3.9 8.4 8.6

10% fall in volume Total volumes 902070 1014014 1106023Net sales (Rs crore) 28,649.0 31,596.7 34,015.4 EBITDA margins (%) 12.9 13.2 13.6 Net profit (Rs crore) 2,227.1 2,490.8 2,765.7 EPS (Rs) 77.1 86.2 95.7

Source: ICICIdirect.com Research

Case II - Realisation sensitivity

Exhibit 26: Average realisation to rise/decline by 5%, impact analysis

FY10E FY11E FY12EBase case Total volumes 1002299.8 1126681.9 1228914.1

Realization (Rs/unit) 332812.3 331456.3 327839.6Net sales (Rs crore) 31,684.5 34,957.7 37,641.4 EBITDA margins (%) 13.0 12.9 13.3 Net profit (Rs crore) 2,511.5 2,719.0 3,024.5 EPS (Rs) 86.9 94.1 104.7

5% rise in realization Realization (Rs/unit) 349452.9 348029.2 344231.6Net sales (Rs crore) 33,202.3 36,638.2 39,454.4 EBITDA margins (%) 16.3 16.2 16.6 Net profit (Rs crore) 3,402.7 3,698.3 4,084.8 EPS (Rs) 117.7 128.0 141.3 % Chg in EPS 35.5 36.0 35.1

5% fall in realization Realization (Rs/unit) 316171.6 314883.5 311447.6Net sales (Rs crore) 30,166.7 33,277.2 35,828.4 EBITDA margins (%) 9.3 9.2 9.6 Net profit (Rs crore) 1,620.3 1,739.6 1,964.3 EPS (Rs) 56.1 60.2 68.0 % Chg in EPS (52.4) (53.0) (51.9)

Source: ICICIdirect.com Research

A 10% change in volume on either side will impactEPS by ~ 8%.

Upward/downward movement directly adds to theEBITDA margin and, thereby, net profit. A tilttowards premium products will enhance thebottomline

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 17

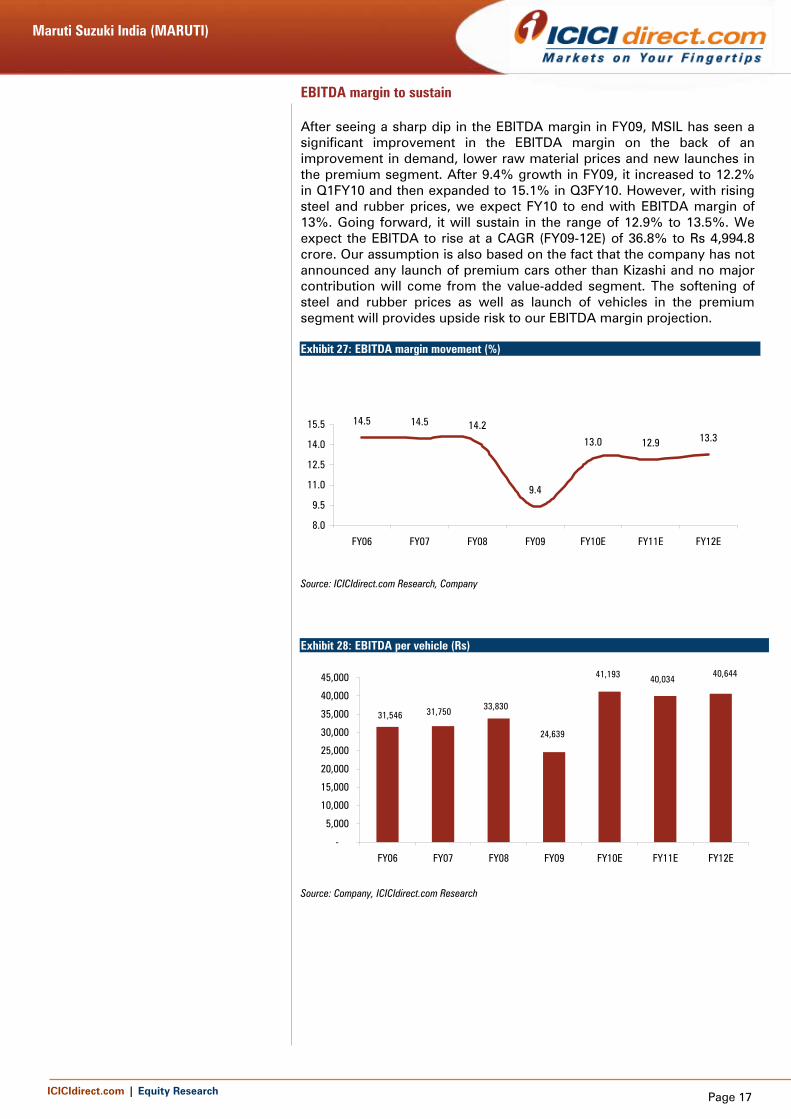

EBITDA margin to sustain After seeing a sharp dip in the EBITDA margin in FY09, MSIL has seen a significant improvement in the EBITDA margin on the back of an improvement in demand, lower raw material prices and new launches in the premium segment. After 9.4% growth in FY09, it increased to 12.2% in Q1FY10 and then expanded to 15.1% in Q3FY10. However, with rising steel and rubber prices, we expect FY10 to end with EBITDA margin of 13%. Going forward, it will sustain in the range of 12.9% to 13.5%. We expect the EBITDA to rise at a CAGR (FY09-12E) of 36.8% to Rs 4,994.8 crore. Our assumption is also based on the fact that the company has not announced any launch of premium cars other than Kizashi and no major contribution will come from the value-added segment. The softening of steel and rubber prices as well as launch of vehicles in the premium segment will provides upside risk to our EBITDA margin projection. Exhibit 27: EBITDA margin movement (%)

14.5 14.5 14.2

9.4

13.0 12.9 13.3

8.0

9.5

11.0

12.5

14.0

15.5

FY06 FY07 FY08 FY09 FY10E FY11E FY12E

Source: ICICIdirect.com Research, Company

Exhibit 28: EBITDA per vehicle (Rs)

40,64440,03441,193

24,639

33,83031,75031,546

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

FY06 FY07 FY08 FY09 FY10E FY11E FY12E

Source: Company, ICICIdirect.com Research

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 18

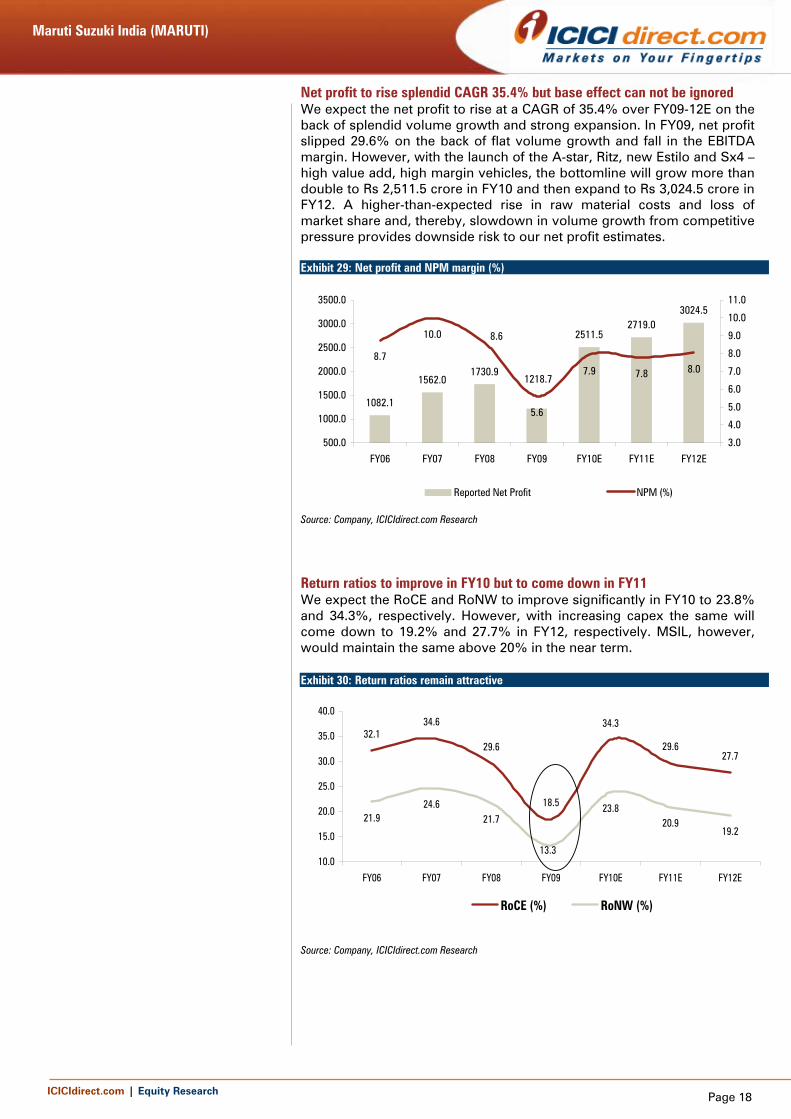

Net profit to rise splendid CAGR 35.4% but base effect can not be ignored We expect the net profit to rise at a CAGR of 35.4% over FY09-12E on the back of splendid volume growth and strong expansion. In FY09, net profit slipped 29.6% on the back of flat volume growth and fall in the EBITDA margin. However, with the launch of the A-star, Ritz, new Estilo and Sx4 – high value add, high margin vehicles, the bottomline will grow more than double to Rs 2,511.5 crore in FY10 and then expand to Rs 3,024.5 crore in FY12. A higher-than-expected rise in raw material costs and loss of market share and, thereby, slowdown in volume growth from competitive pressure provides downside risk to our net profit estimates. Exhibit 29: Net profit and NPM margin (%)

1082.1

1562.01730.9

2511.52719.0

3024.5

1218.7

8.7

10.0

5.6

7.9 7.8 8.0

8.6

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

3500.0

FY06 FY07 FY08 FY09 FY10E FY11E FY12E

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

Reported Net Profit NPM (%)

Source: Company, ICICIdirect.com Research

Return ratios to improve in FY10 but to come down in FY11 We expect the RoCE and RoNW to improve significantly in FY10 to 23.8% and 34.3%, respectively. However, with increasing capex the same will come down to 19.2% and 27.7% in FY12, respectively. MSIL, however, would maintain the same above 20% in the near term. Exhibit 30: Return ratios remain attractive

32.134.6

29.6

18.5

34.3

29.627.7

21.924.6

21.723.8

20.919.2

13.310.0

15.0

20.0

25.0

30.0

35.0

40.0

FY06 FY07 FY08 FY09 FY10E FY11E FY12E

RoCE (%) RoNW (%)

Source: Company, ICICIdirect.com Research

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 19

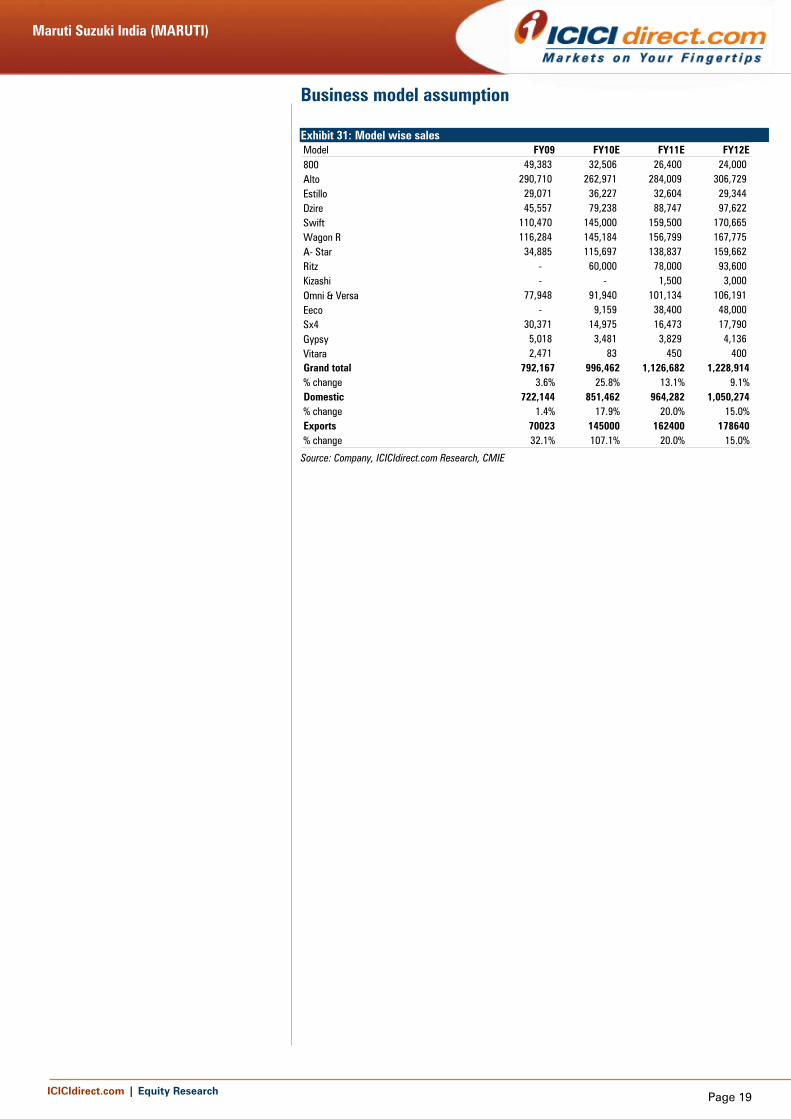

Business model assumption Exhibit 31: Model wise sales Model FY09 FY10E FY11E FY12E800 49,383 32,506 26,400 24,000 Alto 290,710 262,971 284,009 306,729 Estillo 29,071 36,227 32,604 29,344 Dzire 45,557 79,238 88,747 97,622 Swift 110,470 145,000 159,500 170,665 Wagon R 116,284 145,184 156,799 167,775 A- Star 34,885 115,697 138,837 159,662 Ritz - 60,000 78,000 93,600 Kizashi - - 1,500 3,000 Omni & Versa 77,948 91,940 101,134 106,191 Eeco - 9,159 38,400 48,000 Sx4 30,371 14,975 16,473 17,790 Gypsy 5,018 3,481 3,829 4,136 Vitara 2,471 83 450 400 Grand total 792,167 996,462 1,126,682 1,228,914% change 3.6% 25.8% 13.1% 9.1%Domestic 722,144 851,462 964,282 1,050,274% change 1.4% 17.9% 20.0% 15.0%Exports 70023 145000 162400 178640% change 32.1% 107.1% 20.0% 15.0%

Source: Company, ICICIdirect.com Research, CMIE

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 20

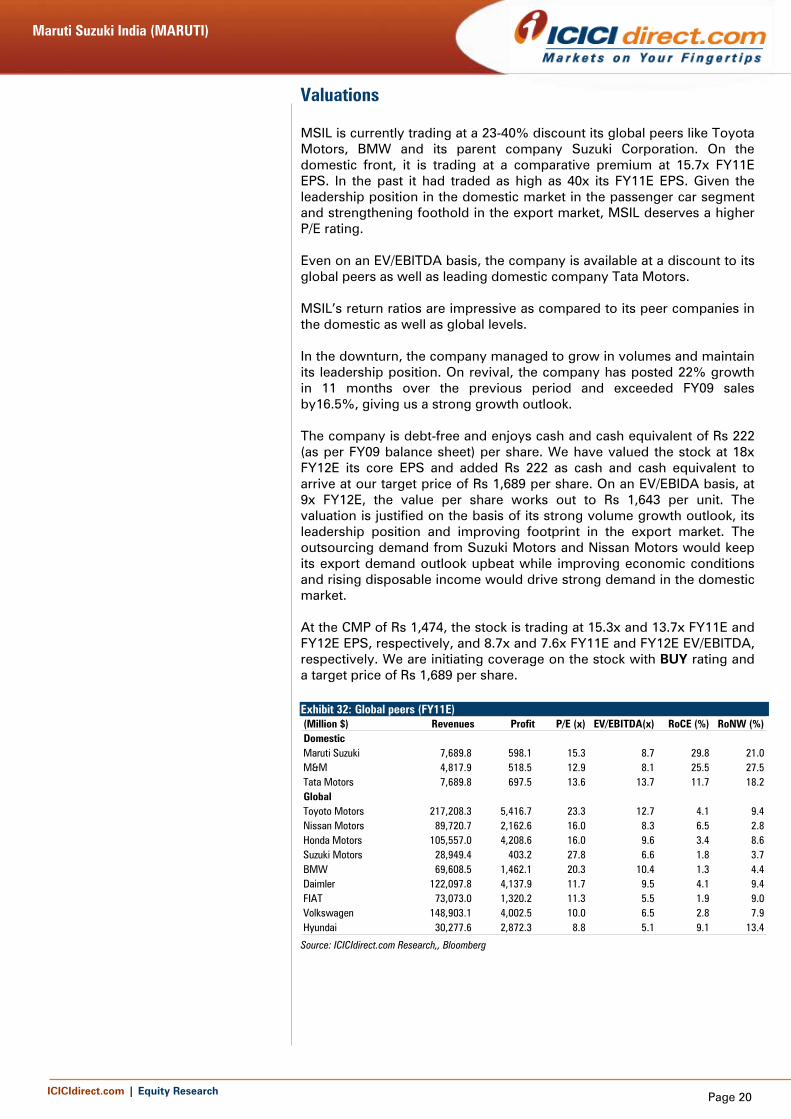

Valuations MSIL is currently trading at a 23-40% discount its global peers like Toyota Motors, BMW and its parent company Suzuki Corporation. On the domestic front, it is trading at a comparative premium at 15.7x FY11E EPS. In the past it had traded as high as 40x its FY11E EPS. Given the leadership position in the domestic market in the passenger car segment and strengthening foothold in the export market, MSIL deserves a higher P/E rating. Even on an EV/EBITDA basis, the company is available at a discount to its global peers as well as leading domestic company Tata Motors. MSIL’s return ratios are impressive as compared to its peer companies in the domestic as well as global levels. In the downturn, the company managed to grow in volumes and maintain its leadership position. On revival, the company has posted 22% growth in 11 months over the previous period and exceeded FY09 sales by16.5%, giving us a strong growth outlook. The company is debt-free and enjoys cash and cash equivalent of Rs 222 (as per FY09 balance sheet) per share. We have valued the stock at 18x FY12E its core EPS and added Rs 222 as cash and cash equivalent to arrive at our target price of Rs 1,689 per share. On an EV/EBIDA basis, at 9x FY12E, the value per share works out to Rs 1,643 per unit. The valuation is justified on the basis of its strong volume growth outlook, its leadership position and improving footprint in the export market. The outsourcing demand from Suzuki Motors and Nissan Motors would keep its export demand outlook upbeat while improving economic conditions and rising disposable income would drive strong demand in the domestic market. At the CMP of Rs 1,474, the stock is trading at 15.3x and 13.7x FY11E and FY12E EPS, respectively, and 8.7x and 7.6x FY11E and FY12E EV/EBITDA, respectively. We are initiating coverage on the stock with BUY rating and a target price of Rs 1,689 per share. Exhibit 32: Global peers (FY11E) (Million $) Revenues Profit P/E (x) EV/EBITDA(x) RoCE (%) RoNW (%)DomesticMaruti Suzuki 7,689.8 598.1 15.3 8.7 29.8 21.0M&M 4,817.9 518.5 12.9 8.1 25.5 27.5Tata Motors 7,689.8 697.5 13.6 13.7 11.7 18.2GlobalToyoto Motors 217,208.3 5,416.7 23.3 12.7 4.1 9.4Nissan Motors 89,720.7 2,162.6 16.0 8.3 6.5 2.8Honda Motors 105,557.0 4,208.6 16.0 9.6 3.4 8.6Suzuki Motors 28,949.4 403.2 27.8 6.6 1.8 3.7BMW 69,608.5 1,462.1 20.3 10.4 1.3 4.4Daimler 122,097.8 4,137.9 11.7 9.5 4.1 9.4FIAT 73,073.0 1,320.2 11.3 5.5 1.9 9.0Volkswagen 148,903.1 4,002.5 10.0 6.5 2.8 7.9Hyundai 30,277.6 2,872.3 8.8 5.1 9.1 13.4

Source: ICICIdirect.com Research,, Bloomberg

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 21

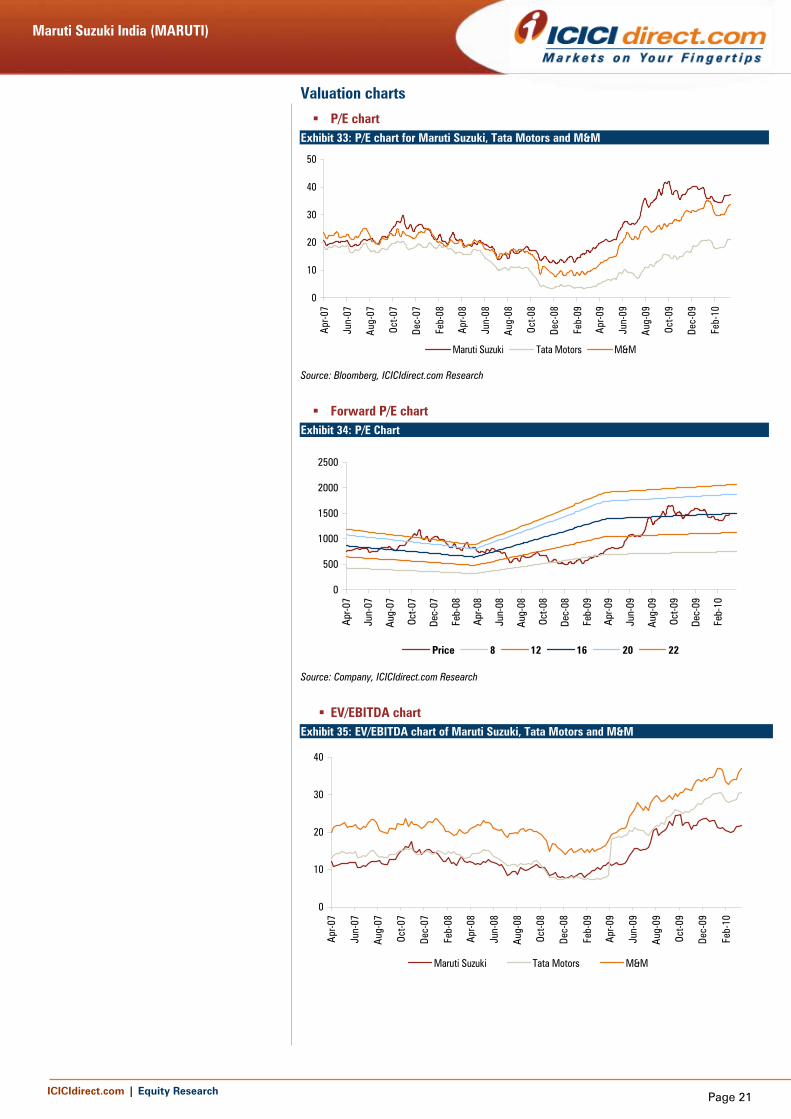

Valuation charts

P/E chart Exhibit 33: P/E chart for Maruti Suzuki, Tata Motors and M&M

0

10

20

30

40

50

Apr-0

7

Jun-

07

Aug-

07

Oct-0

7

Dec-

07

Feb-

08

Apr-0

8

Jun-

08

Aug-

08

Oct-0

8

Dec-

08

Feb-

09

Apr-0

9

Jun-

09

Aug-

09

Oct-0

9

Dec-

09

Feb-

10

Maruti Suzuki Tata Motors M&M

Source: Bloomberg, ICICIdirect.com Research

Forward P/E chart Exhibit 34: P/E Chart

0

500

1000

1500

2000

2500

Apr-0

7

Jun-

07

Aug-

07

Oct-0

7

Dec-

07

Feb-

08

Apr-0

8

Jun-

08

Aug-

08

Oct-0

8

Dec-

08

Feb-

09

Apr-0

9

Jun-

09

Aug-

09

Oct-0

9

Dec-

09

Feb-

10

Price 8 12 16 20 22

Source: Company, ICICIdirect.com Research

EV/EBITDA chart Exhibit 35: EV/EBITDA chart of Maruti Suzuki, Tata Motors and M&M

0

10

20

30

40

Apr-0

7

Jun-

07

Aug-

07

Oct-0

7

Dec-

07

Feb-

08

Apr-0

8

Jun-

08

Aug-

08

Oct-0

8

Dec-

08

Feb-

09

Apr-0

9

Jun-

09

Aug-

09

Oct-0

9

Dec-

09

Feb-

10

Maruti Suzuki Tata Motors M&M

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 22

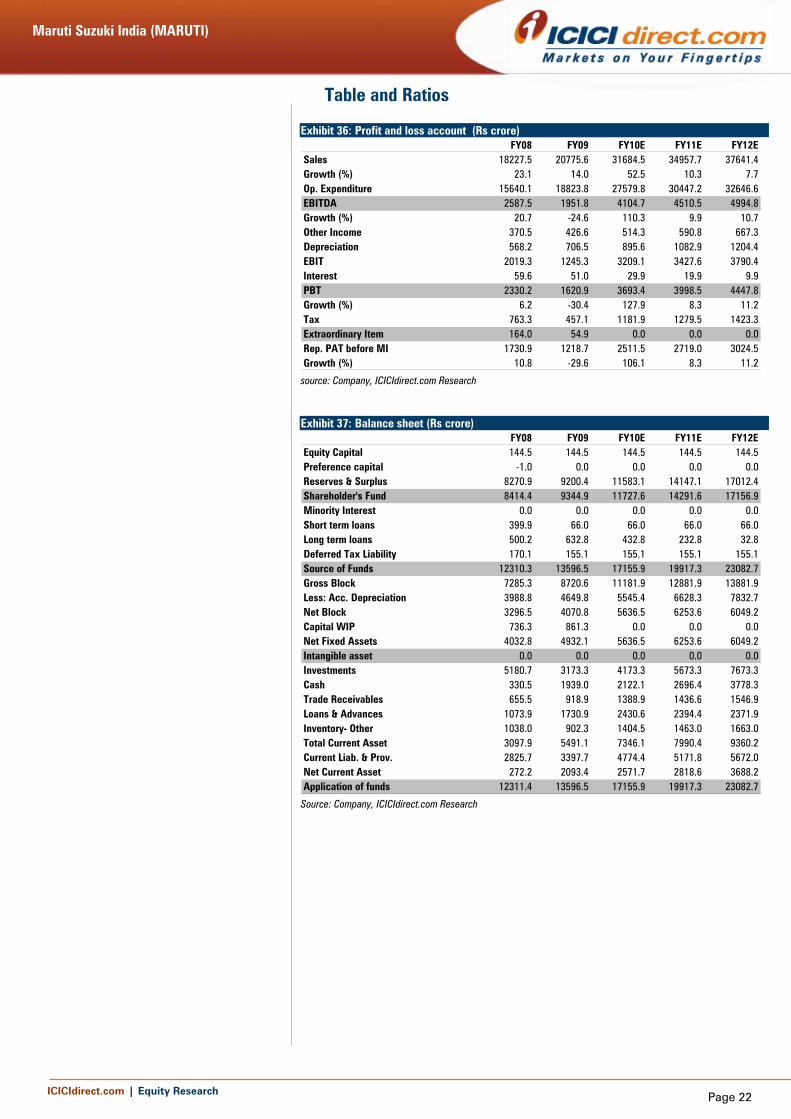

Table and Ratios Exhibit 36: Profit and loss account (Rs crore)

FY08 FY09 FY10E FY11E FY12ESales 18227.5 20775.6 31684.5 34957.7 37641.4Growth (%) 23.1 14.0 52.5 10.3 7.7Op. Expenditure 15640.1 18823.8 27579.8 30447.2 32646.6EBITDA 2587.5 1951.8 4104.7 4510.5 4994.8Growth (%) 20.7 -24.6 110.3 9.9 10.7Other Income 370.5 426.6 514.3 590.8 667.3Depreciation 568.2 706.5 895.6 1082.9 1204.4EBIT 2019.3 1245.3 3209.1 3427.6 3790.4Interest 59.6 51.0 29.9 19.9 9.9PBT 2330.2 1620.9 3693.4 3998.5 4447.8Growth (%) 6.2 -30.4 127.9 8.3 11.2Tax 763.3 457.1 1181.9 1279.5 1423.3Extraordinary Item 164.0 54.9 0.0 0.0 0.0Rep. PAT before MI 1730.9 1218.7 2511.5 2719.0 3024.5Growth (%) 10.8 -29.6 106.1 8.3 11.2

source: Company, ICICIdirect.com Research

Exhibit 37: Balance sheet (Rs crore)

FY08 FY09 FY10E FY11E FY12EEquity Capital 144.5 144.5 144.5 144.5 144.5Preference capital -1.0 0.0 0.0 0.0 0.0Reserves & Surplus 8270.9 9200.4 11583.1 14147.1 17012.4Shareholder's Fund 8414.4 9344.9 11727.6 14291.6 17156.9Minority Interest 0.0 0.0 0.0 0.0 0.0Short term loans 399.9 66.0 66.0 66.0 66.0Long term loans 500.2 632.8 432.8 232.8 32.8Deferred Tax Liability 170.1 155.1 155.1 155.1 155.1Source of Funds 12310.3 13596.5 17155.9 19917.3 23082.7Gross Block 7285.3 8720.6 11181.9 12881.9 13881.9Less: Acc. Depreciation 3988.8 4649.8 5545.4 6628.3 7832.7Net Block 3296.5 4070.8 5636.5 6253.6 6049.2Capital WIP 736.3 861.3 0.0 0.0 0.0Net Fixed Assets 4032.8 4932.1 5636.5 6253.6 6049.2Intangible asset 0.0 0.0 0.0 0.0 0.0Investments 5180.7 3173.3 4173.3 5673.3 7673.3Cash 330.5 1939.0 2122.1 2696.4 3778.3Trade Receivables 655.5 918.9 1388.9 1436.6 1546.9Loans & Advances 1073.9 1730.9 2430.6 2394.4 2371.9Inventory- Other 1038.0 902.3 1404.5 1463.0 1663.0Total Current Asset 3097.9 5491.1 7346.1 7990.4 9360.2Current Liab. & Prov. 2825.7 3397.7 4774.4 5171.8 5672.0Net Current Asset 272.2 2093.4 2571.7 2818.6 3688.2Application of funds 12311.4 13596.5 17155.9 19917.3 23082.7

Source: Company, ICICIdirect.com Research

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 23

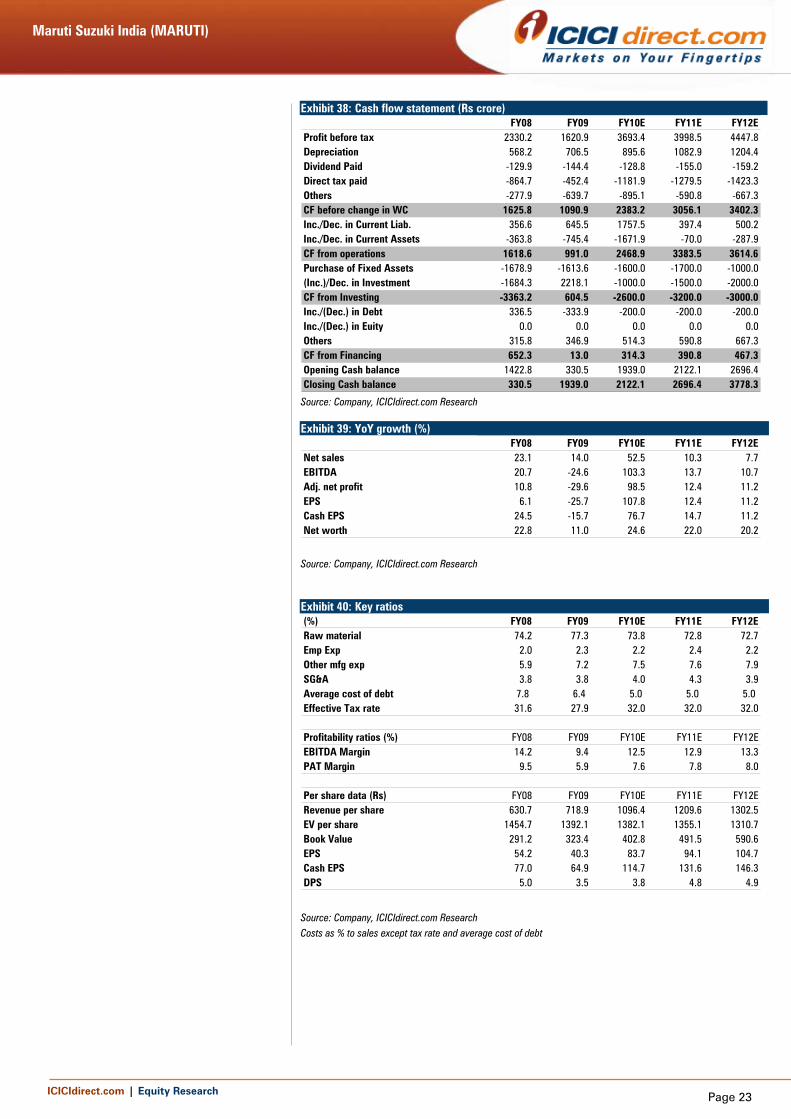

Exhibit 38: Cash flow statement (Rs crore)

FY08 FY09 FY10E FY11E FY12EProfit before tax 2330.2 1620.9 3693.4 3998.5 4447.8Depreciation 568.2 706.5 895.6 1082.9 1204.4Dividend Paid -129.9 -144.4 -128.8 -155.0 -159.2Direct tax paid -864.7 -452.4 -1181.9 -1279.5 -1423.3Others -277.9 -639.7 -895.1 -590.8 -667.3CF before change in WC 1625.8 1090.9 2383.2 3056.1 3402.3Inc./Dec. in Current Liab. 356.6 645.5 1757.5 397.4 500.2Inc./Dec. in Current Assets -363.8 -745.4 -1671.9 -70.0 -287.9CF from operations 1618.6 991.0 2468.9 3383.5 3614.6Purchase of Fixed Assets -1678.9 -1613.6 -1600.0 -1700.0 -1000.0(Inc.)/Dec. in Investment -1684.3 2218.1 -1000.0 -1500.0 -2000.0CF from Investing -3363.2 604.5 -2600.0 -3200.0 -3000.0Inc./(Dec.) in Debt 336.5 -333.9 -200.0 -200.0 -200.0Inc./(Dec.) in Euity 0.0 0.0 0.0 0.0 0.0Others 315.8 346.9 514.3 590.8 667.3CF from Financing 652.3 13.0 314.3 390.8 467.3Opening Cash balance 1422.8 330.5 1939.0 2122.1 2696.4Closing Cash balance 330.5 1939.0 2122.1 2696.4 3778.3

Source: Company, ICICIdirect.com Research

Exhibit 39: YoY growth (%) FY08 FY09 FY10E FY11E FY12E

Net sales 23.1 14.0 52.5 10.3 7.7EBITDA 20.7 -24.6 103.3 13.7 10.7Adj. net profit 10.8 -29.6 98.5 12.4 11.2EPS 6.1 -25.7 107.8 12.4 11.2Cash EPS 24.5 -15.7 76.7 14.7 11.2Net worth 22.8 11.0 24.6 22.0 20.2 Source: Company, ICICIdirect.com Research

Exhibit 40: Key ratios (%) FY08 FY09 FY10E FY11E FY12ERaw material 74.2 77.3 73.8 72.8 72.7Emp Exp 2.0 2.3 2.2 2.4 2.2Other mfg exp 5.9 7.2 7.5 7.6 7.9SG&A 3.8 3.8 4.0 4.3 3.9Average cost of debt 7.8 6.4 5.0 5.0 5.0 Effective Tax rate 31.6 27.9 32.0 32.0 32.0

Profitability ratios (%) FY08 FY09 FY10E FY11E FY12EEBITDA Margin 14.2 9.4 12.5 12.9 13.3PAT Margin 9.5 5.9 7.6 7.8 8.0

Per share data (Rs) FY08 FY09 FY10E FY11E FY12ERevenue per share 630.7 718.9 1096.4 1209.6 1302.5EV per share 1454.7 1392.1 1382.1 1355.1 1310.7Book Value 291.2 323.4 402.8 491.5 590.6EPS 54.2 40.3 83.7 94.1 104.7Cash EPS 77.0 64.9 114.7 131.6 146.3DPS 5.0 3.5 3.8 4.8 4.9 Source: Company, ICICIdirect.com Research Costs as % to sales except tax rate and average cost of debt

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 24

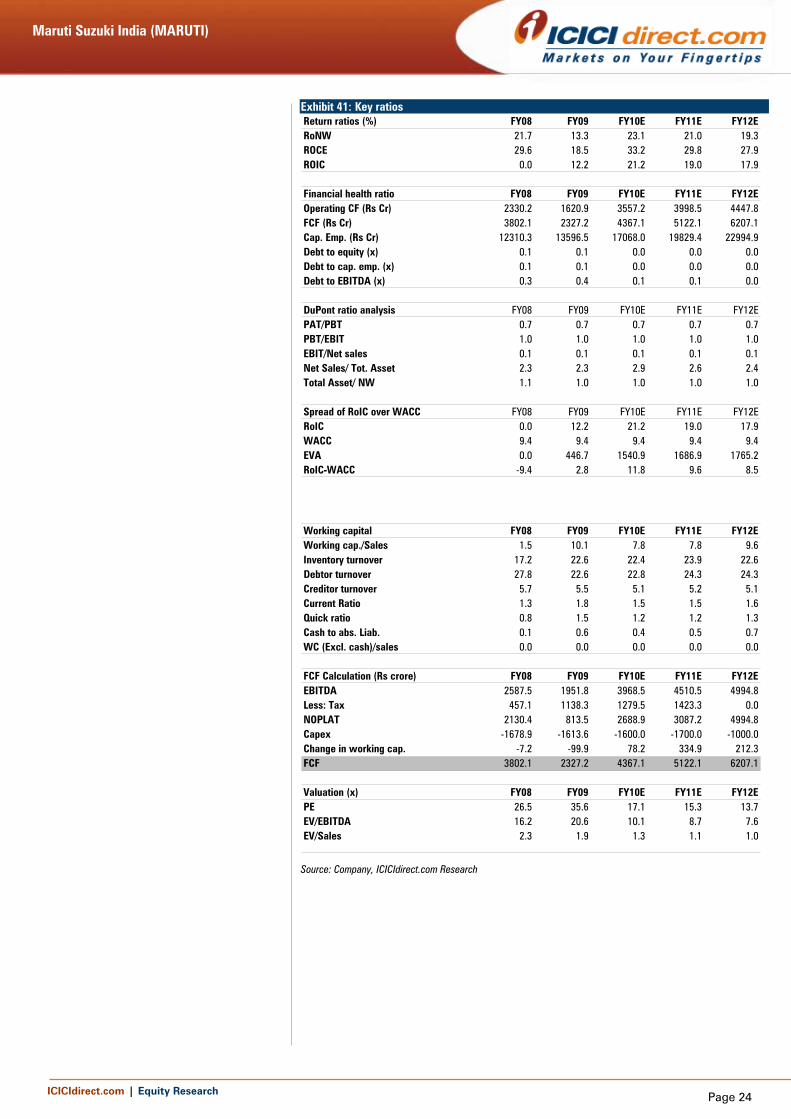

Exhibit 41: Key ratios Return ratios (%) FY08 FY09 FY10E FY11E FY12ERoNW 21.7 13.3 23.1 21.0 19.3ROCE 29.6 18.5 33.2 29.8 27.9ROIC 0.0 12.2 21.2 19.0 17.9

Financial health ratio FY08 FY09 FY10E FY11E FY12EOperating CF (Rs Cr) 2330.2 1620.9 3557.2 3998.5 4447.8FCF (Rs Cr) 3802.1 2327.2 4367.1 5122.1 6207.1Cap. Emp. (Rs Cr) 12310.3 13596.5 17068.0 19829.4 22994.9Debt to equity (x) 0.1 0.1 0.0 0.0 0.0Debt to cap. emp. (x) 0.1 0.1 0.0 0.0 0.0Debt to EBITDA (x) 0.3 0.4 0.1 0.1 0.0

DuPont ratio analysis FY08 FY09 FY10E FY11E FY12EPAT/PBT 0.7 0.7 0.7 0.7 0.7PBT/EBIT 1.0 1.0 1.0 1.0 1.0EBIT/Net sales 0.1 0.1 0.1 0.1 0.1Net Sales/ Tot. Asset 2.3 2.3 2.9 2.6 2.4Total Asset/ NW 1.1 1.0 1.0 1.0 1.0

Spread of RoIC over WACC FY08 FY09 FY10E FY11E FY12ERoIC 0.0 12.2 21.2 19.0 17.9WACC 9.4 9.4 9.4 9.4 9.4EVA 0.0 446.7 1540.9 1686.9 1765.2RoIC-WACC -9.4 2.8 11.8 9.6 8.5

Working capital FY08 FY09 FY10E FY11E FY12EWorking cap./Sales 1.5 10.1 7.8 7.8 9.6Inventory turnover 17.2 22.6 22.4 23.9 22.6Debtor turnover 27.8 22.6 22.8 24.3 24.3Creditor turnover 5.7 5.5 5.1 5.2 5.1Current Ratio 1.3 1.8 1.5 1.5 1.6Quick ratio 0.8 1.5 1.2 1.2 1.3Cash to abs. Liab. 0.1 0.6 0.4 0.5 0.7WC (Excl. cash)/sales 0.0 0.0 0.0 0.0 0.0

FCF Calculation (Rs crore) FY08 FY09 FY10E FY11E FY12EEBITDA 2587.5 1951.8 3968.5 4510.5 4994.8Less: Tax 457.1 1138.3 1279.5 1423.3 0.0NOPLAT 2130.4 813.5 2688.9 3087.2 4994.8Capex -1678.9 -1613.6 -1600.0 -1700.0 -1000.0Change in working cap. -7.2 -99.9 78.2 334.9 212.3FCF 3802.1 2327.2 4367.1 5122.1 6207.1

Valuation (x) FY08 FY09 FY10E FY11E FY12EPE 26.5 35.6 17.1 15.3 13.7EV/EBITDA 16.2 20.6 10.1 8.7 7.6EV/Sales 2.3 1.9 1.3 1.1 1.0 Source: Company, ICICIdirect.com Research

Maruti Suzuki India (MARUTI)

ICICIdirect.com | Equity Research Page 25

RATING RATIONALE ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns ratings to its stocks according to their notional target price vs. current market price and then categorises them as Strong Buy, Buy, Add, Reduce, and Sell. The performance horizon is two years unless specified and the notional target price is defined as the analysts' valuation for a stock. Strong Buy: 20% or more; Buy: Between 10% and 20%; Add: Up to 10%; Reduce: Up to -10% Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk, ICICI Securities Limited, 7th Floor, Akruti Centre Point, MIDC Main Road, Marol Naka, Andheri (East) Mumbai – 400 093

ANALYST CERTIFICATION We /I, Supriya Madye (Khedkar)PGDBM (FINANCE); research analyst, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our personal views about any and all of the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. Analysts aren't registered as research analysts by FINRA and might not be an associated person of the ICICI Securities Inc.

Disclosures: ICICI Securities Limited (ICICI Securities) and its affiliates are a full-service, integrated investment banking, investment management and brokerage and financing group. We along with affiliates are leading underwriter of securities and participate in virtually all securities trading markets in India. We and our affiliates have investment banking and other business relationship with a significant percentage of companies covered by our Investment Research Department. Our research professionals provide important input into our investment banking and other business selection processes. ICICI Securities generally prohibits its analysts, persons reporting to analysts and their dependent family members from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would endeavour to update the information herein on reasonable basis, ICICI Securities, its subsidiaries and associated companies, their directors and employees (“ICICI Securities and affiliates”) are under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities is acting in an advisory capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein is solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks. The value and return of investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities and affiliates accept no liabilities for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities and its affiliates might have managed or co-managed a public offering for the subject company in the preceding twelve months. ICICI Securities and affiliates might have received compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of public offerings, corporate finance, investment banking or other advisory services in a merger or specific transaction. ICICI Securities and affiliates expect to receive compensation from the companies mentioned in the report within a period of three months following the date of publication of the research report for services in respect of public offerings, corporate finance, investment banking or other advisory services in a merger or specific transaction. It is confirmed that Supriya Madye (Khedkar) Supriya Madye (Khedkar)PGDBM (FINANCE) research analyst and the authors of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months. Our research professionals are paid in part based on the profitability of ICICI Securities, which include earnings from Investment Banking and other business.

ICICI Securities or its subsidiaries collectively do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of the research report.

It is confirmed that Supriya Madye (Khedkar)Supriya Madye (Khedkar)PGDBM (FINANCE) research analyst and the authors of this report or any of their family members does not serve as an officer, director or advisory board member of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. ICICI Securities and affiliates may act upon or make use of information contained in the report prior to the publication thereof.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.