Embed Size (px)

Citation preview

Managing The Risks of Climate Legislation

Bruce Braine, Vice PresidentJune 3, 2008

MACRUC ConferenceWilliamsburg, Virginia

Mountaineer Plant - New Haven, WV Northeastern Plant - Oologah, OK

2

Overview

Background Managing Climate Risks

Legislative and Regulatory Risks Market and Compliance Risks Technology Risks

3

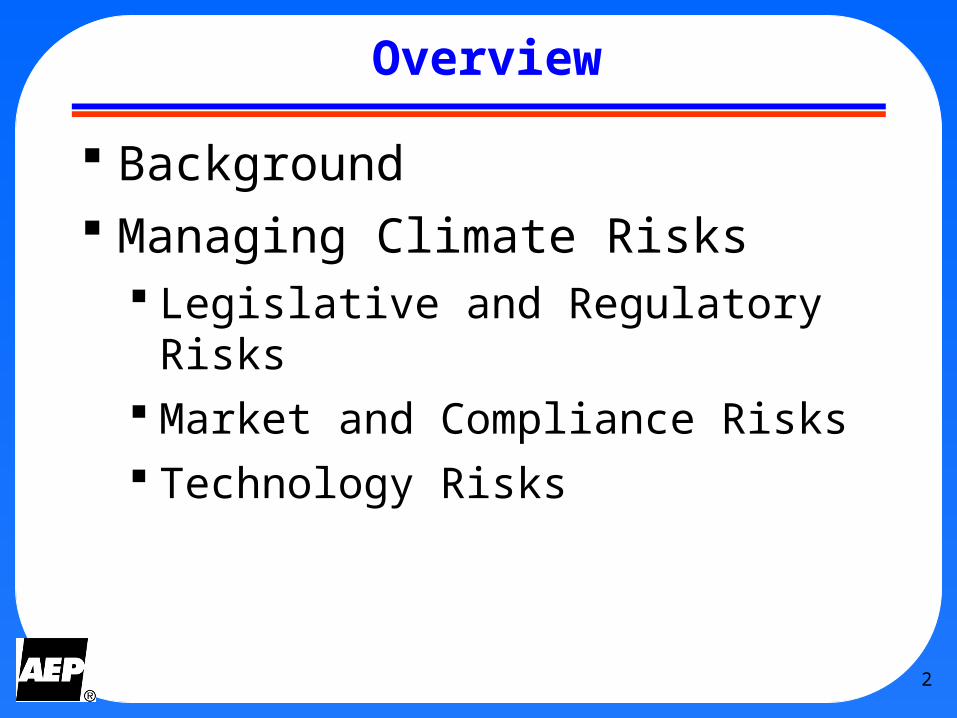

Coal/Lignite

67%

Nat. Gas/Oil

24%

Nuclear

6%Pumped Storage/

Hydro/Wind

3%AEP’s Generation

Fleet

38,388 MW Capacity

Company Overview

5.1 million customers in 11 statesIndustry-leading size and scale of assets:

Asset SizeIndustry

RankDomestic Generation ~38,300 MW # 2Transmission ~39,000 miles # 1Distribution ~208,000 miles # 1

4

AEP’s Climate Strategy

Being proactive and engaged in the development of climate policy

Investing in science/technology R&D

Taking Voluntary action now, making real reductions thru CCX (2003-07: 40 MM Tons reductions); 2011 Voluntary Commitment (additional 5 MM Tons/year reductions).

Investing in long term technology (e.g., IGCC, Ultra-supercritical PC and Carbon Capture and Storage)

AEP must be a leader in addressing climate change

5

AEP Position: A “Reasonable” Approach to Climate Legislation

• Reductions and Timing--Moderate with Adequate Lead Times

• Scope of Program-- Economy Wide

• Flexibility of the Program—Trading, Banking, Unrestricted Offsets, Early Action Credits

• Allowance Allocation And Other Cost Issues—Emissions Based and ”Low” auctions

• Technology Development/Deployment—Bonus allowances for carbon capture and storage

• International Linkage—e.g. AEP-IBEW ProposalAEP Supports Reasonable Legislation on GHG: Bingaman-

Specter “Low Carbon Economy Act of 2007”

6

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctri

c S

ecto

rC

O2 E

mis

sio

ns

(mill

ion

met

ric

ton

s)

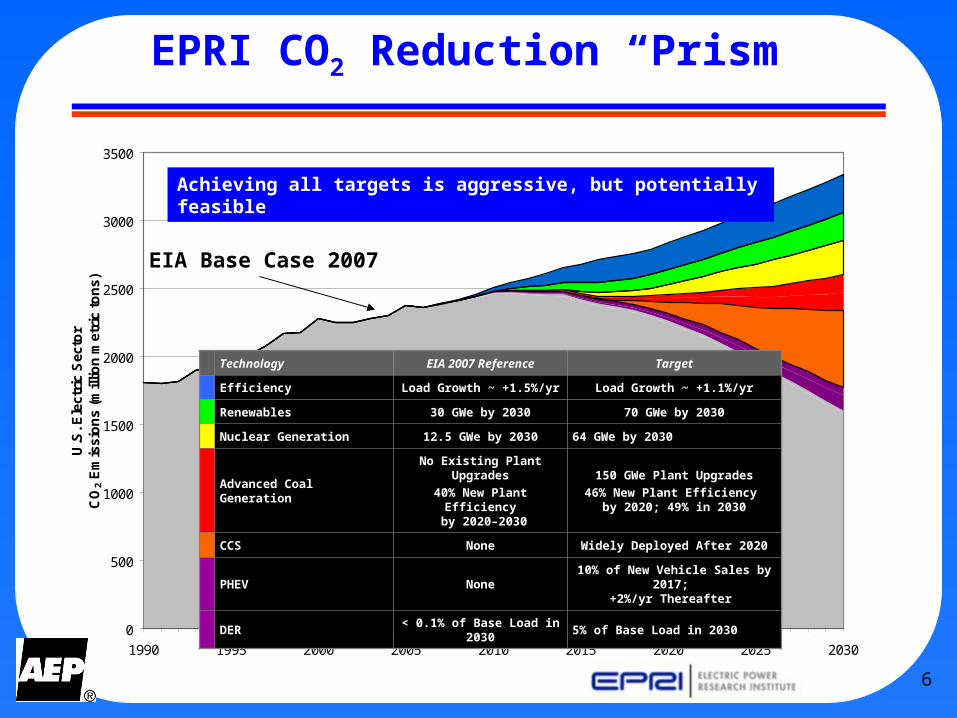

EIA Base Case 2007

EPRI CO2 Reduction “Prism”

Technology EIA 2007 Reference Target

EfficiencyLoad Growth ~

+1.5%/yrLoad Growth ~ +1.1%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear Generation 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal Generation

No Existing Plant Upgrades

40% New Plant Efficiency

by 2020–2030

150 GWe Plant Upgrades46% New Plant Efficiency

by 2020; 49% in 2030

CCS None Widely Deployed After 2020

PHEV None10% of New Vehicle Sales by

2017; +2%/yr Thereafter

DER< 0.1% of Base Load in

20305% of Base Load in 2030

Achieving all targets is aggressive, but potentially feasible

7

WA

OR

CA

NV

ID

MT

WY

UT

AZ

CO

NM

TX

ND

SD

NE

KS

OK

MN

IA

MO

AR

LA

MSAL

GA

FL

WI

OHINIL

KY

TNNC

SC

WV

MIPA

NY

VA

MEVTNH

MARI

CTNJ

DEMD

Cost-Regulated

Unbundled/ Deregulated

WA

OR

CA

NV

ID

MT

WY

UT

AZ

CO

NM

TX

ND

SD

NE

KS

OK

MN

IA

MO

AR

LA

MSAL

GA

FL

WI

OHINIL

KY

TNNC

SC

WV

MIPA

NY

VA

MEVTNH

MARI

CTNJ

DEMD

Cost-Regulated

Unbundled/ Deregulated

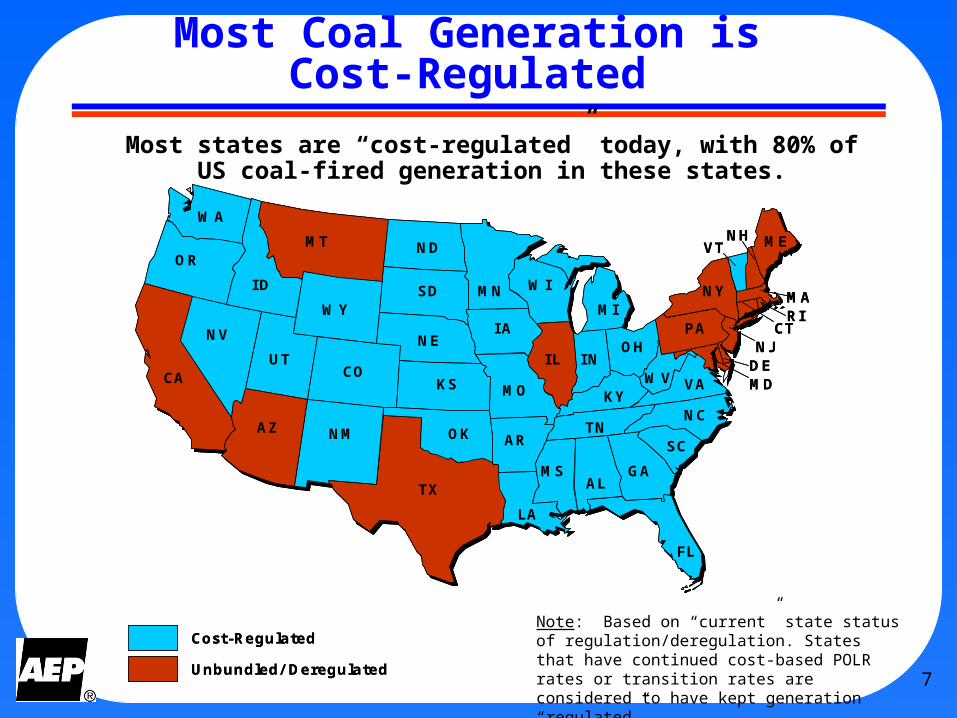

Most states are “cost-regulated” today, with 80% of US coal-fired generation in these states.

Note: Based on “current” state status of regulation/deregulation. States that have continued cost-based POLR rates or transition rates are considered to have kept generation “regulated”.

Most Coal Generation isCost-Regulated

8

$-

$10

$20

$30

$40

$50

$60

$70

$80

100% Allocation 100% Auction

$/M

Wh

Fuel, O&M, Emissions ex. CO2 CO2 Compliance Costs* Auction Costs*

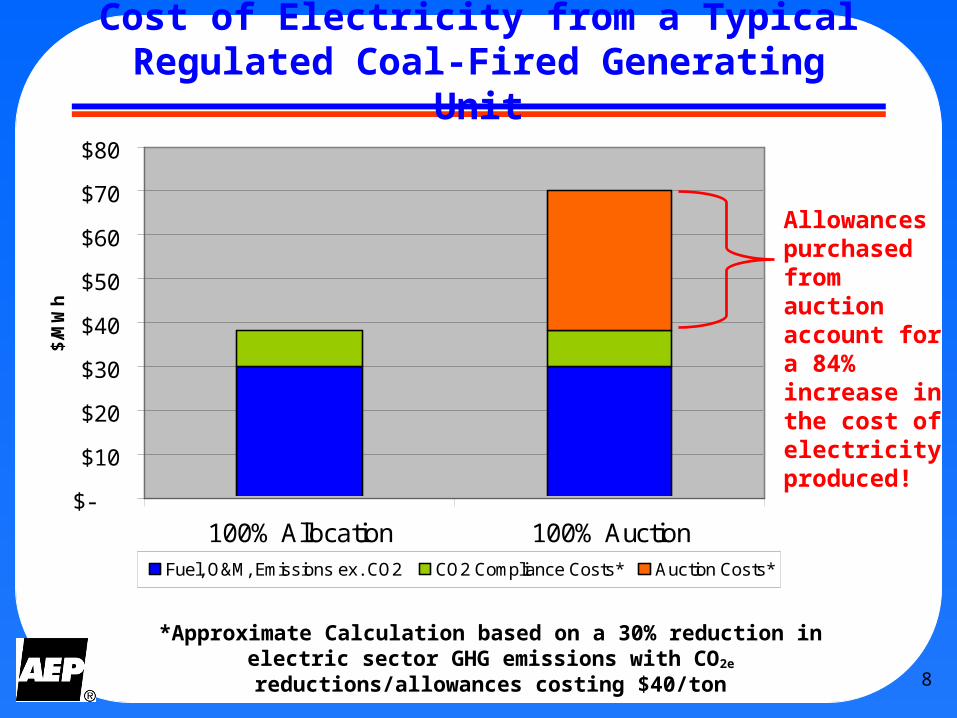

Cost of Electricity from a Typical Regulated Coal-Fired Generating Unit

Allowances purchased from auction account for a 84% increase in the cost of electricity produced!

*Approximate Calculation based on a 30% reduction in electric sector GHG emissions with CO2e reductions/allowances costing $40/ton

9

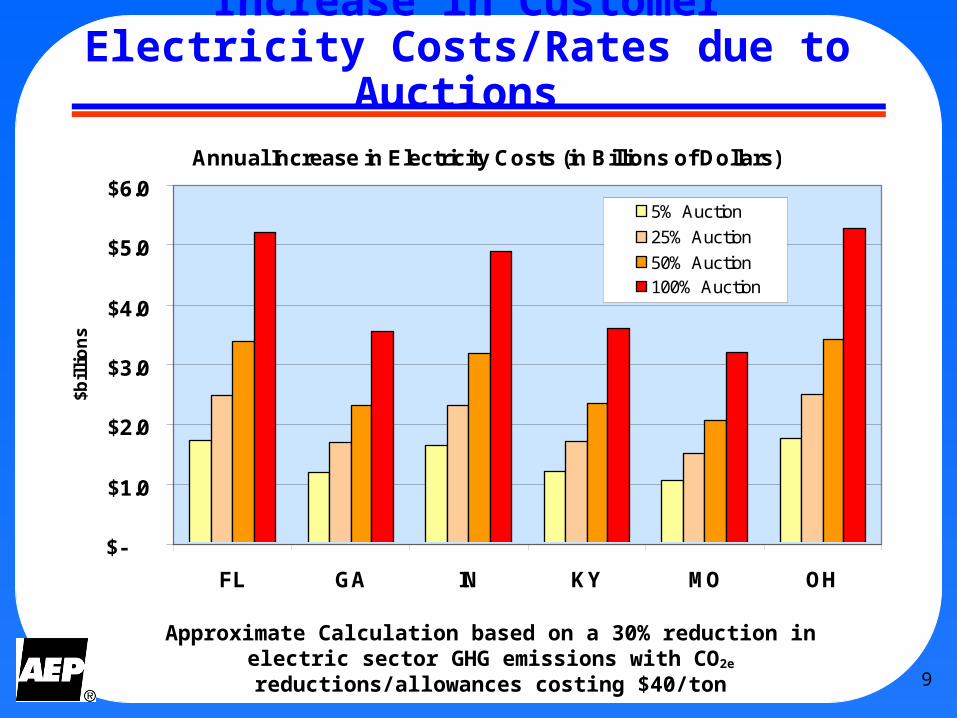

Increase in Customer Electricity Costs/Rates due to Auctions

Approximate Calculation based on a 30% reduction in electric sector GHG emissions with CO2e reductions/allowances costing $40/ton

Annual Increase in Electricity Costs (in Billions of Dollars)

$-

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

FL GA IN KY MO OH

$bil

lio

ns

5% Auction

25% Auction

50% Auction100% Auction

10

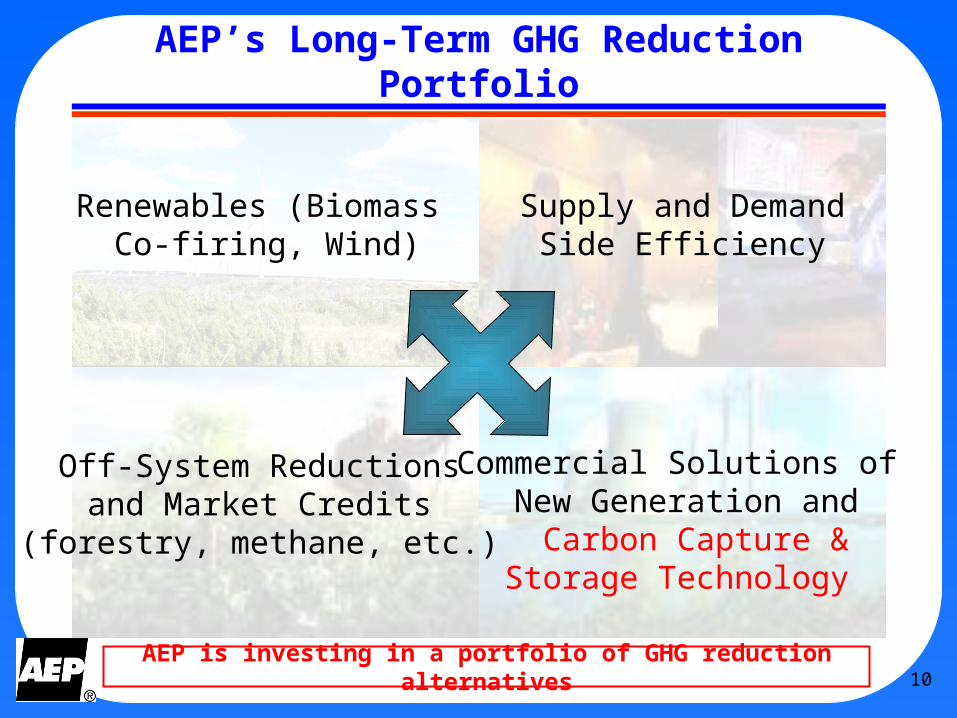

AEP’s Long-Term GHG Reduction Portfolio

Renewables (Biomass Co-firing, Wind)

Off-System Reductionsand Market Credits

(forestry, methane, etc.)

Commercial Solutions of New Generation and Carbon Capture &

Storage Technology

Supply and DemandSide Efficiency

AEP is investing in a portfolio of GHG reduction alternatives

11

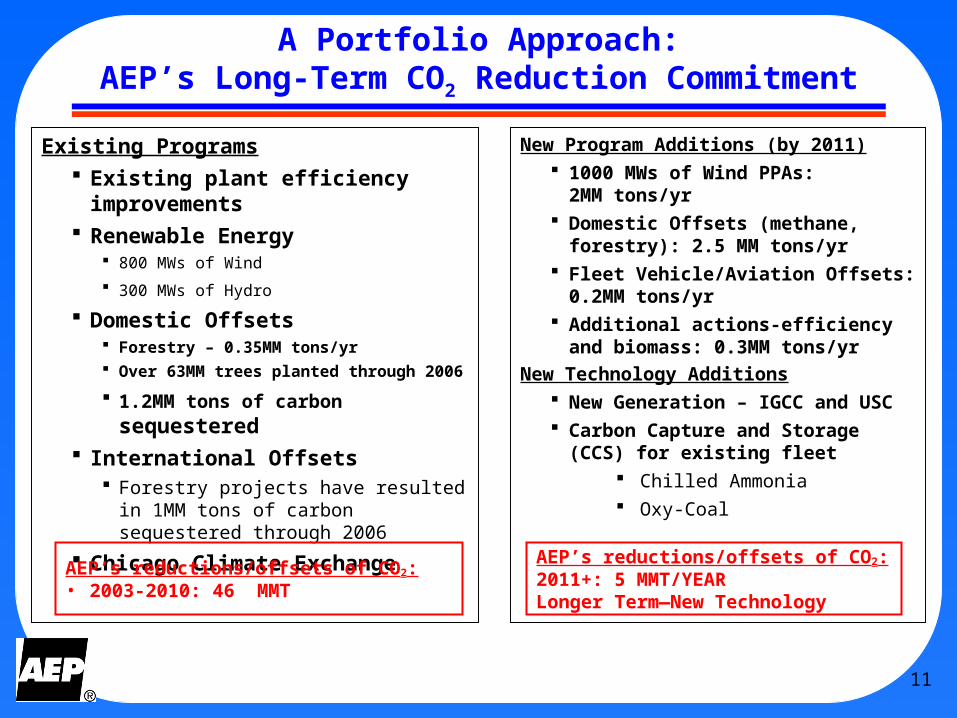

A Portfolio Approach:AEP’s Long-Term CO2 Reduction Commitment

Existing Programs Existing plant efficiency

improvements Renewable Energy

800 MWs of Wind

300 MWs of Hydro

Domestic Offsets Forestry – 0.35MM tons/yr Over 63MM trees planted through

2006

1.2MM tons of carbon sequestered

International Offsets Forestry projects have resulted in

1MM tons of carbon sequestered through 2006

Chicago Climate ExchangeAEP’s reductions/offsets of CO2:• 2003-2010: 46 MMT

New Program Additions (by 2011) 1000 MWs of Wind PPAs:

2MM tons/yr Domestic Offsets (methane,

forestry): 2.5 MM tons/yr Fleet Vehicle/Aviation Offsets:

0.2MM tons/yr Additional actions-efficiency and

biomass: 0.3MM tons/yrNew Technology Additions

New Generation – IGCC and USC Carbon Capture and Storage

(CCS) for existing fleet Chilled Ammonia Oxy-Coal

AEP’s reductions/offsets of CO2:2011+: 5 MMT/YEARLonger Term—New Technology

12

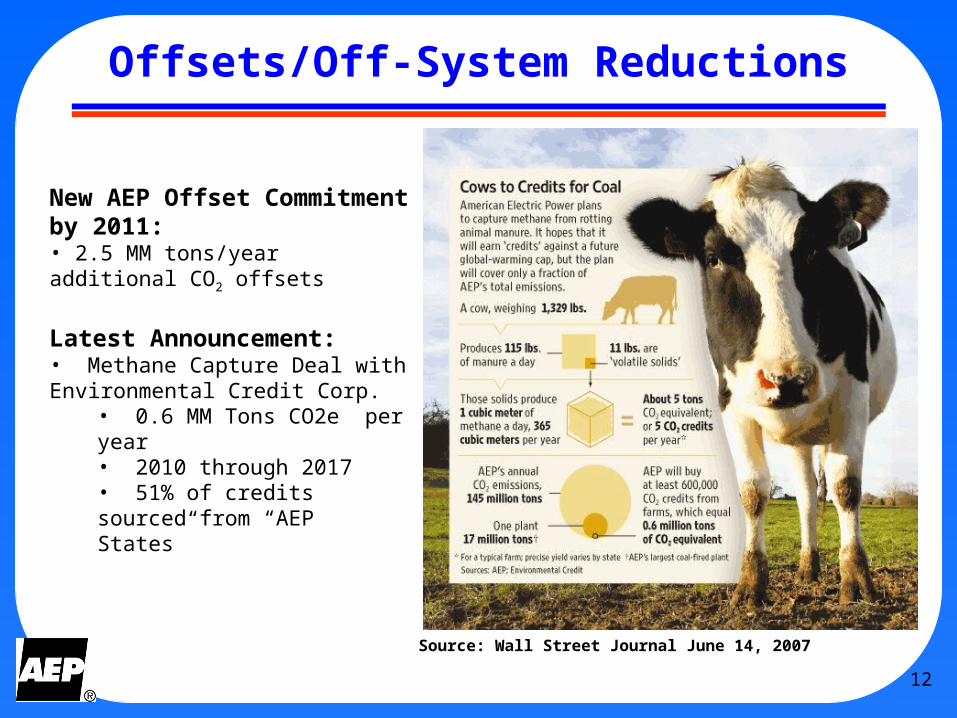

Offsets/Off-System Reductions

New AEP Offset Commitment by 2011:• 2.5 MM tons/year additional CO2 offsets

Latest Announcement:• Methane Capture Deal with Environmental Credit Corp.

• 0.6 MM Tons CO2e per year• 2010 through 2017• 51% of credits sourced from “AEP States”

Source: Wall Street Journal June 14, 2007

13

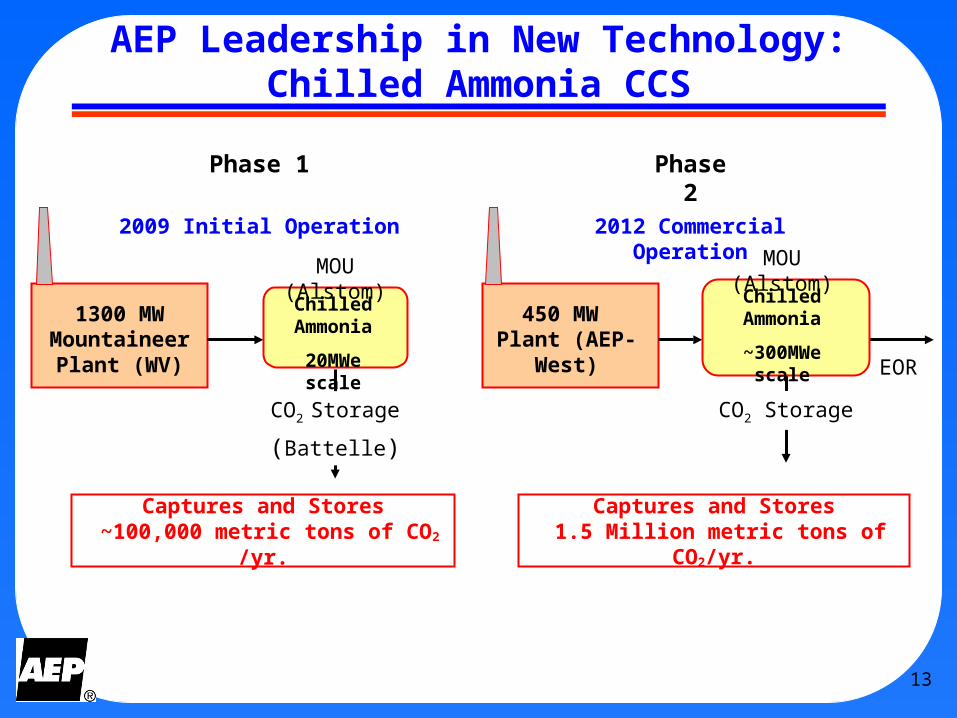

AEP Leadership in New Technology:Chilled Ammonia CCS

1300 MW Mountaineer Plant (WV)

450 MW Plant (AEP-

West)

2009 Initial Operation 2012 Commercial Operation

Chilled Ammonia

20MWe scale

Chilled Ammonia

~300MWe scale

CO2 Storage

(Battelle)

MOU (Alstom) MOU (Alstom)

EOR

CO2 Storage

Captures and Stores 1.5 Million metric tons of

CO2/yr.

Phase 1 Phase 2

Captures and Stores ~100,000 metric tons of

CO2 /yr.

14

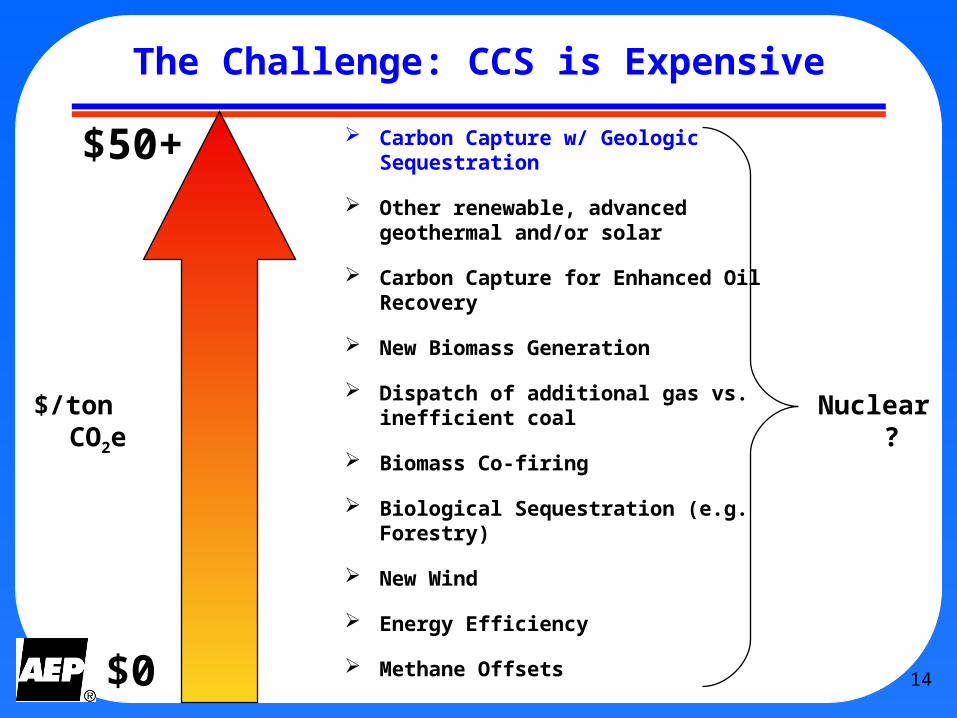

The Challenge: CCS is Expensive

Carbon Capture w/ Geologic Sequestration

Other renewable, advanced geothermal and/or solar

Carbon Capture for Enhanced Oil Recovery

New Biomass Generation

Dispatch of additional gas vs. inefficient coal

Biomass Co-firing

Biological Sequestration (e.g. Forestry)

New Wind

Energy Efficiency

Methane Offsets

$/ton CO2e

$0

$50+

Nuclear?