Embed Size (px)

Citation preview

15/06/2011

1

Managing Debt: Lessons Learned

Bogotá, Colombia

Managing Debt: Lessons Learnedand Emerging Issues

Finance Secretary

June 2011

Outline

1. Institutional framework

2. Financing sources - Alternative schemes

3. Financing sources - Traditional schemes

4. Fiscal sustainability

Annex

Conclusions

15/06/2011 2

15/06/2011

2

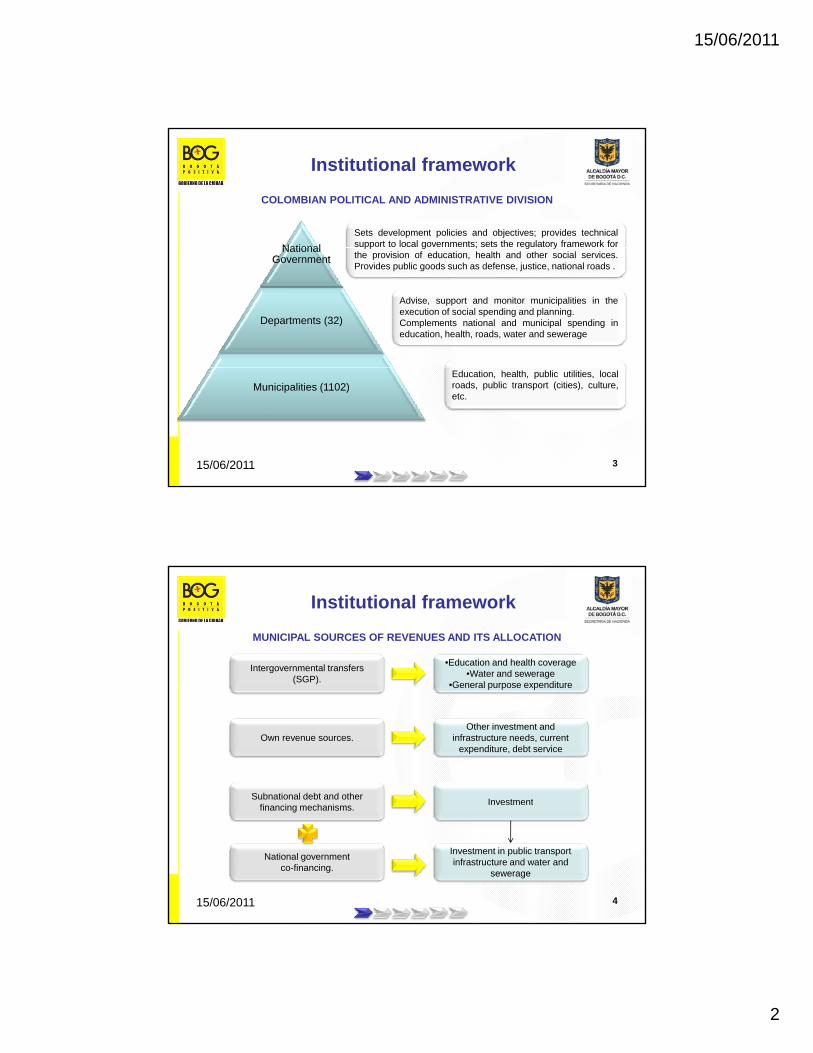

Institutional framework

COLOMBIAN POLITICAL AND ADMINISTRATIVE DIVISION

National

Sets development policies and objectives; provides technicalsupport to local governments; sets the regulatory framework forNational

Government

Departments (32)

pp g ; g ythe provision of education, health and other social services.Provides public goods such as defense, justice, national roads .

Advise, support and monitor municipalities in theexecution of social spending and planning.Complements national and municipal spending ineducation, health, roads, water and sewerage

15/06/2011 3

Municipalities (1102)Education, health, public utilities, localroads, public transport (cities), culture,etc.

Institutional framework

MUNICIPAL SOURCES OF REVENUES AND ITS ALLOCATION

•Education and health coverage•Water and sewerage

•General purpose expenditure

Intergovernmental transfers(SGP).

•General purpose expenditure

Other investment and infrastructure needs, current

expenditure, debt service

Investment

Own revenue sources.

Subnational debt and otherfi i h i

15/06/2011 4

Investment

Investment in public transportinfrastructure and water and

sewerage

financing mechanisms.

National governmentco-financing.

15/06/2011

3

Agreement to provide a specific infrastructure asset or service in

PUBLIC PRIVATE PARTNERSHIPS (PPP) - CONCESSIONS

Financing sources –Alternative schemes

Public sector Private sector

exchange of payments based on the service actually delivered.

$

Source of repayment of investment:- User charges (fares, tolls, etc)- Public budget payments if the project is not self-financed

CONTINGENT LIABILITIES

$

5

Why do governments choose PPPs?

PUBLIC PRIVATE PARTNERSHIPS (PPP) - CONCESSIONS

Financing sources –Alternative schemes

• Insufficient public funds to meet the demand for infrastructure.

• New sources of finance.

• A desire to improve the quality of a specific service.

• Transfer of certain risks to the private sector.

• Better value for public

Examples in Bogota:• Public transportation systems (Transmilenio, SITP).• Urban highways.• Landfill.• Garbage collection.• Parking lots.• Schools’ management.

Better value for public investments in infrastructure by the use of private sector skills.

• Introduction of innovation/ technology.

Source: Worldbank. Large project finance

15/06/2011 6

15/06/2011

4

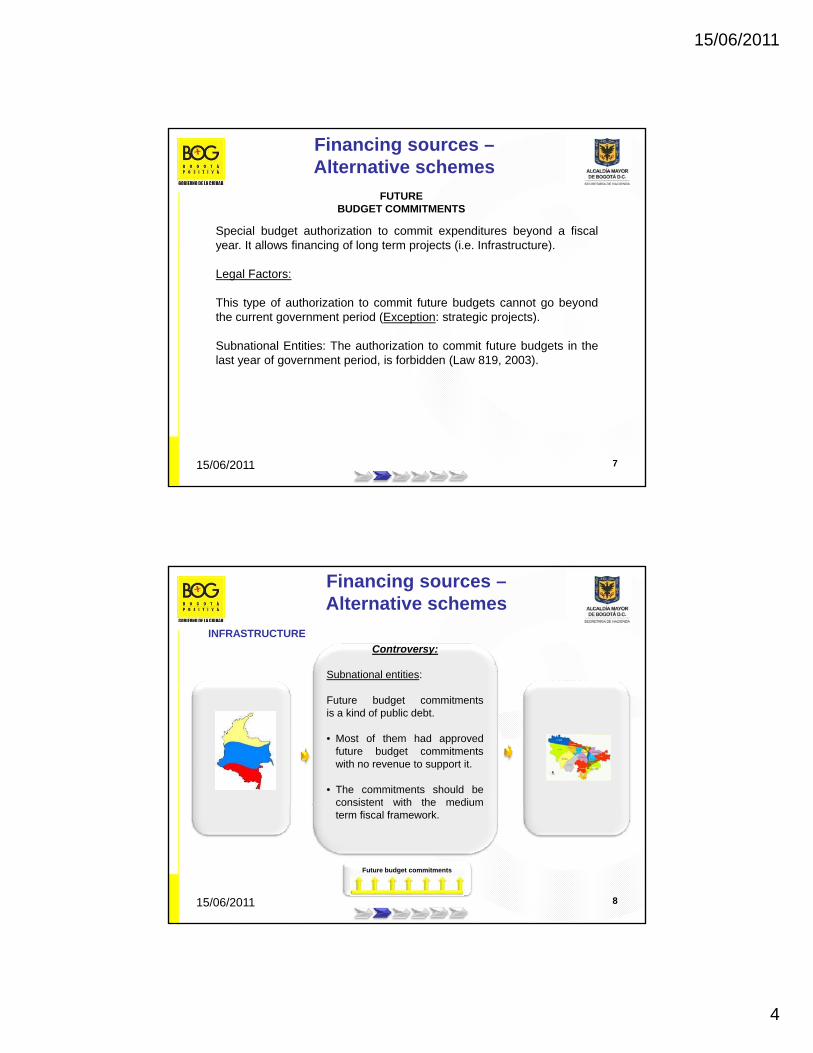

FUTURE BUDGET COMMITMENTS

Special budget authorization to commit expenditures beyond a fiscalyear It allows financing of long term projects (i e Infrastructure)

Financing sources –Alternative schemes

year. It allows financing of long term projects (i.e. Infrastructure).

Legal Factors:

This type of authorization to commit future budgets cannot go beyondthe current government period (Exception: strategic projects).

Subnational Entities: The authorization to commit future budgets in thelast year of government period, is forbidden (Law 819, 2003).

15/06/2011 7

Controversy:

Subnational entities:

INFRASTRUCTURE

Financing sources –Alternative schemes

Future budget commitmentsis a kind of public debt.

• Most of them had approvedfuture budget commitmentswith no revenue to support it.

• The commitments should beconsistent with the mediumconsistent with the mediumterm fiscal framework.

Future budget commitments

15/06/2011 8

15/06/2011

5

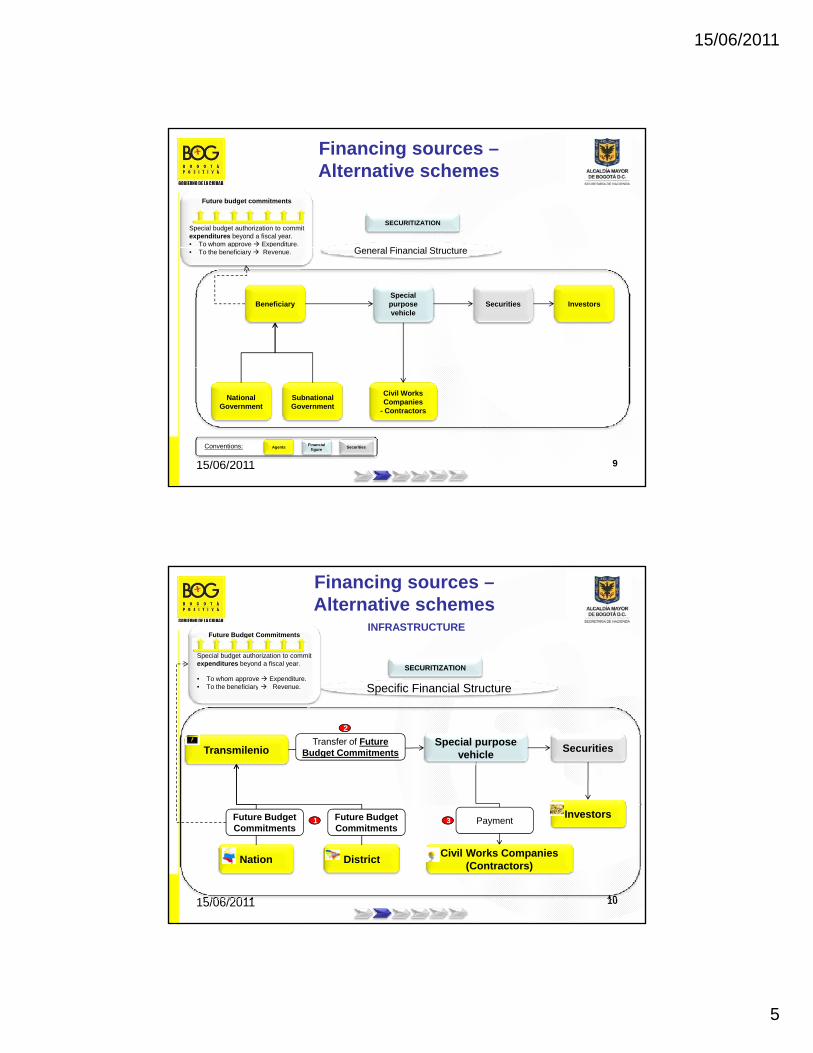

INFRASTRUCTURE

SECURITIZATION

G l Fi i l St t

Financing sources –Alternative schemes

Future budget commitments

Special budget authorization to commitexpenditures beyond a fiscal year.• To whom approve Expenditure.

General Financial Structure

BeneficiarySpecialpurposevehicle

Securities Investors

• To the beneficiary Revenue.

15/06/2011 9

NationalGovernment

SubnationalGovernment

Civil Works Companies

- Contractors

AgentsConventions: Financial figure

Securities

INFRASTRUCTURE

SECURITIZATION

S ifi Fi i l St t

Future Budget Commitments

Special budget authorization to commitexpenditures beyond a fiscal year.

• To whom approve Expenditure.T th b fi i R

Financing sources –Alternative schemes

TransmilenioSpecial purpose

vehicleSecurities

Transfer of FutureBudget Commitments

2

Specific Financial Structure• To the beneficiary Revenue.

15/06/2011 10

Nation DistrictCivil Works Companies

(Contractors)

InvestorsPayment1 3Future Budget

CommitmentsFuture BudgetCommitments

15/06/2011

6

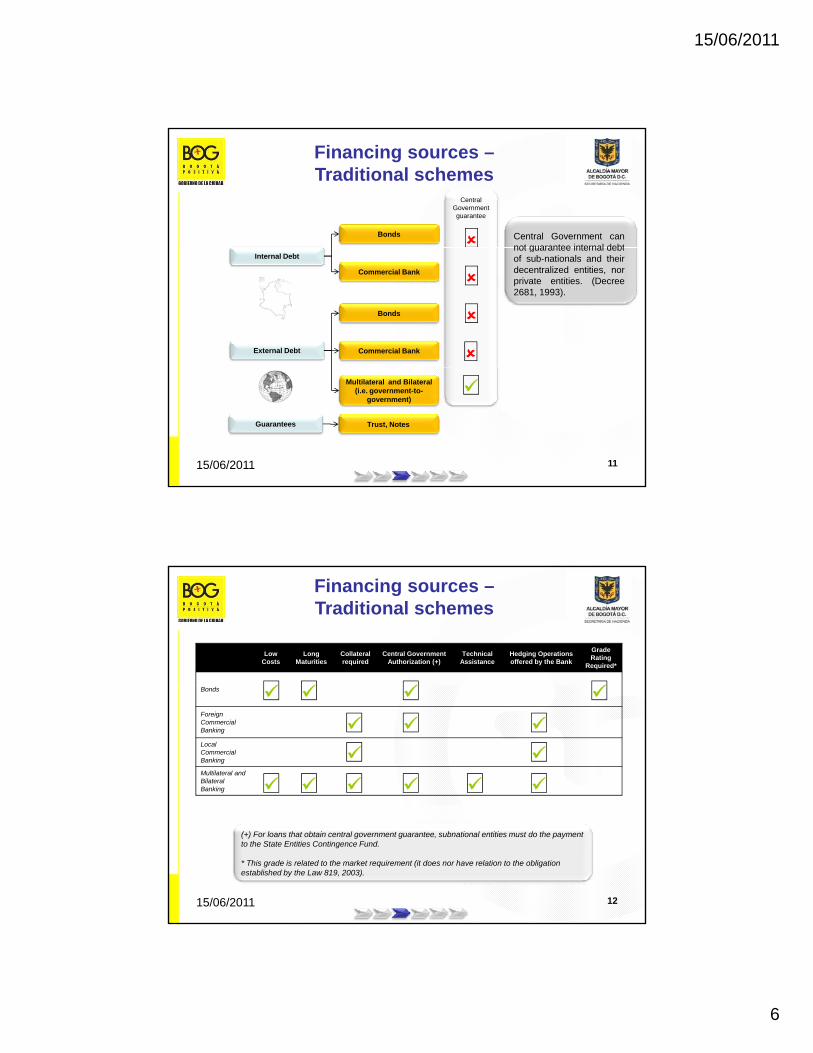

Central Governmentguarantee

Bonds Central Government cannot guarantee internal debt

Financing sources –Traditional schemes

Internal Debt

External Debt

Commercial Bank

Bonds

Commercial Bank

not guarantee internal debtof sub-nationals and theirdecentralized entities, norprivate entities. (Decree2681, 1993).

15/06/2011 11

Multilateral and Bilateral (i.e. government-to-

government)

Guarantees Trust, Notes

Financing sources –Traditional schemes

LowCosts

Long Maturities

Collateralrequired

Central GovernmentAuthorization (+)

TechnicalAssistance

Hedging Operationsoffered by the Bank

GradeRating

Required*

Bonds

ForeignCommercialBanking

Local CommercialBanking

Multilateral and Bilateral Banking

15/06/2011 12

(+) For loans that obtain central government guarantee, subnational entities must do the paymentto the State Entities Contingence Fund.

* This grade is related to the market requirement (it does nor have relation to the obligationestablished by the Law 819, 2003).

15/06/2011

7

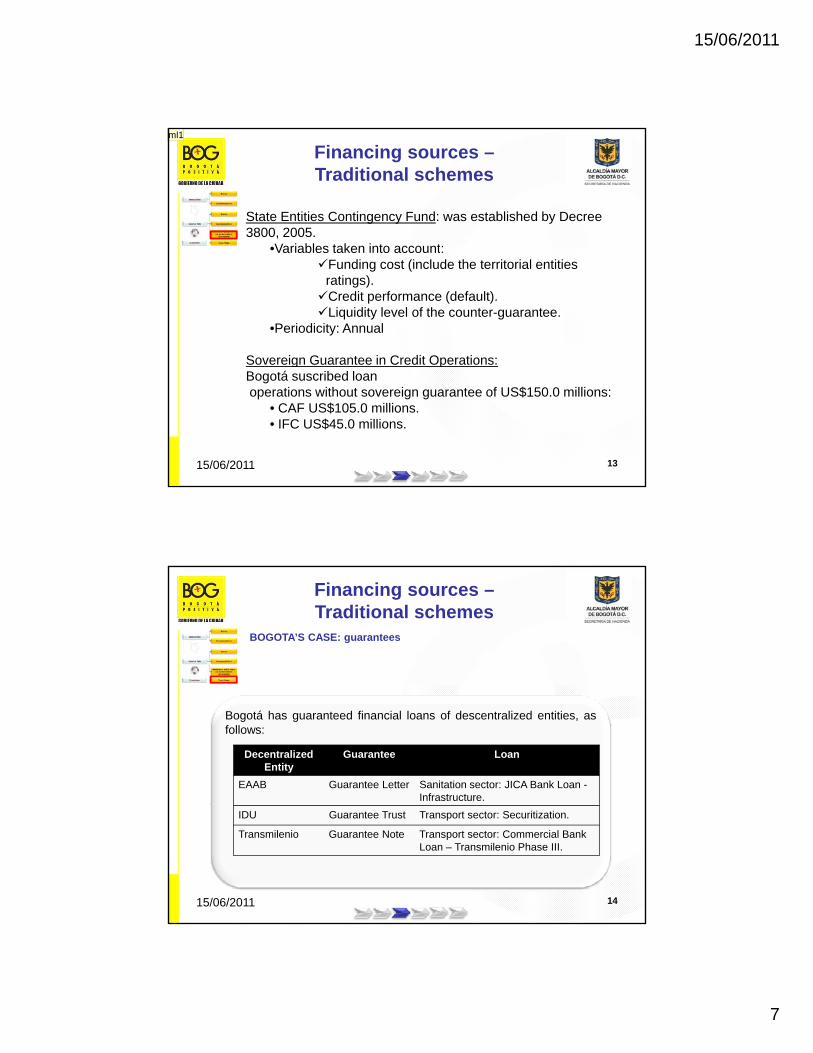

State Entities Contingency Fund: was established by Decree3800, 2005.

•Variables taken into account:

Financing sources –Traditional schemes

•Variables taken into account: Funding cost (include the territorial entities

ratings).Credit performance (default). Liquidity level of the counter-guarantee.

•Periodicity: Annual

Sovereign Guarantee in Credit Operations:

15/06/2011 13

gBogotá suscribed loanoperations without sovereign guarantee of US$150.0 millions:

• CAF US$105.0 millions.• IFC US$45.0 millions.

ml1

Financing sources –Traditional schemes

BOGOTA’S CASE: guarantees

Bogotá has guaranteed financial loans of descentralized entities, asfollows:

DecentralizedEntity

Guarantee Loan

EAAB Guarantee Letter Sanitation sector: JICA Bank Loan -Infrastructure.

15/06/2011 14

IDU Guarantee Trust Transport sector: Securitization.

Transmilenio Guarantee Note Transport sector: Commercial Bank Loan – Transmilenio Phase III.

Slide 13

ml1 La palabra contragarantía está de esa forma (counterguarantee) en el Prospecto de Emisión del Bono Externo (Offering Memorandum). No obstante, consideramos que también se puede colocar con guion intermedio (counter-guarantee).mlparra, 6/2/2011

15/06/2011

8

• Colombia has made big improvements in the regulatory

Financing sources in the context of fiscal sustainability

Colombia has made big improvements in the regulatoryframework to increase fiscal discipline in order tocontrol debt levels of subnational governments and tomitigate the associated risks (contingent liabilities).

• This has also done in order to avoid incur in backingfrom the central goverment to the subnationals and

15/06/2011 15

gconsequently.

• Preserve the macroeconomic stability.

• 1968 – 1993: Legal framework that guaranteed income for

BACKGROUND

Fiscal sustainability

subnational governments, without controlling the use ofthese resources.

• The Constitution of 1991 deepened the decentralizationprocess and increased the amount of transfers from theNational Government to local governments.

15/06/2011 16

• These transfers were used as a guarantee of paymentand increased the supply of credit to subnationalgovernments.

15/06/2011

9

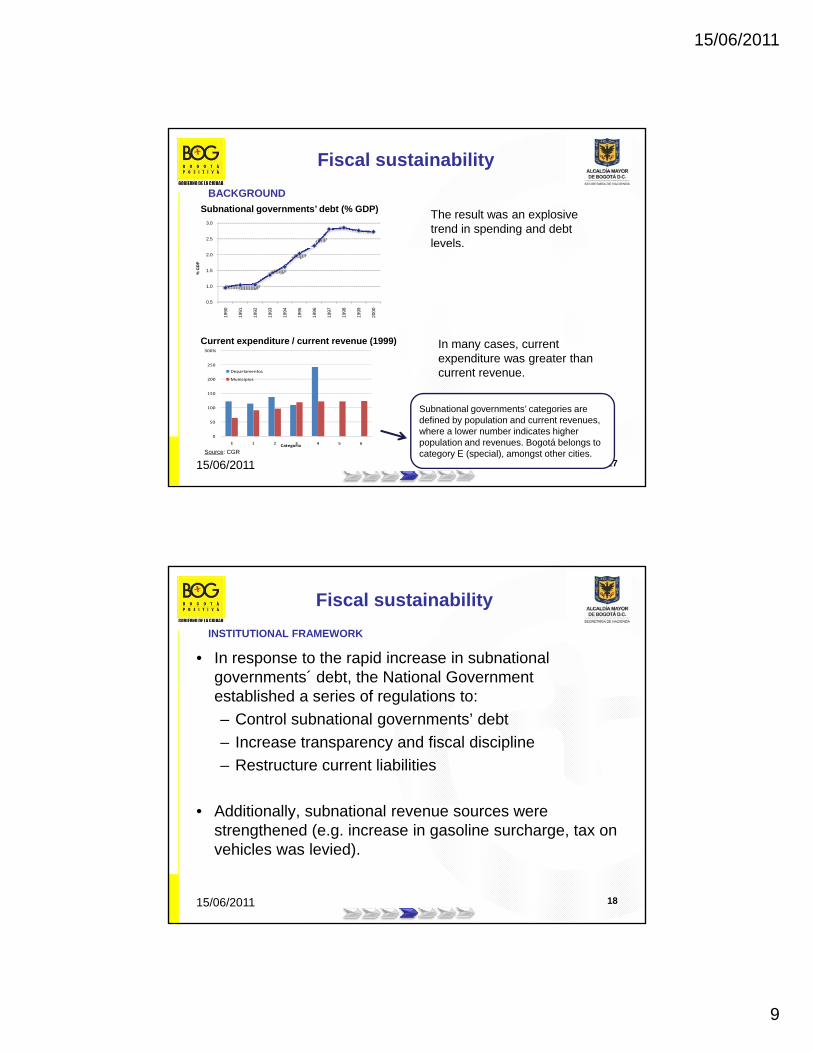

Subnational governments’ debt (% GDP)

2.5

3.0The result was an explosivetrend in spending and debtlevels.

Fiscal sustainability

BACKGROUND

250

300%

Current expenditure / current revenue (1999)

0.5

1.0

1.5

2.0

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

% G

DP

In many cases, currentexpenditure was greater than

15/06/2011 17

0

50

100

150

200

E 1 2 3 4 5 6Categoria

Departamentos

Municipios

Source: CGR

Subnational governments’ categories are defined by population and current revenues, where a lower number indicates higherpopulation and revenues. Bogotá belongs tocategory E (special), amongst other cities.

current revenue.

• In response to the rapid increase in subnationalgovernments´ debt, the National Government

Fiscal sustainability

INSTITUTIONAL FRAMEWORK

gestablished a series of regulations to:

– Control subnational governments’ debt

– Increase transparency and fiscal discipline

– Restructure current liabilities

15/06/2011 18

• Additionally, subnational revenue sources werestrengthened (e.g. increase in gasoline surcharge, tax onvehicles was levied).

15/06/2011

10

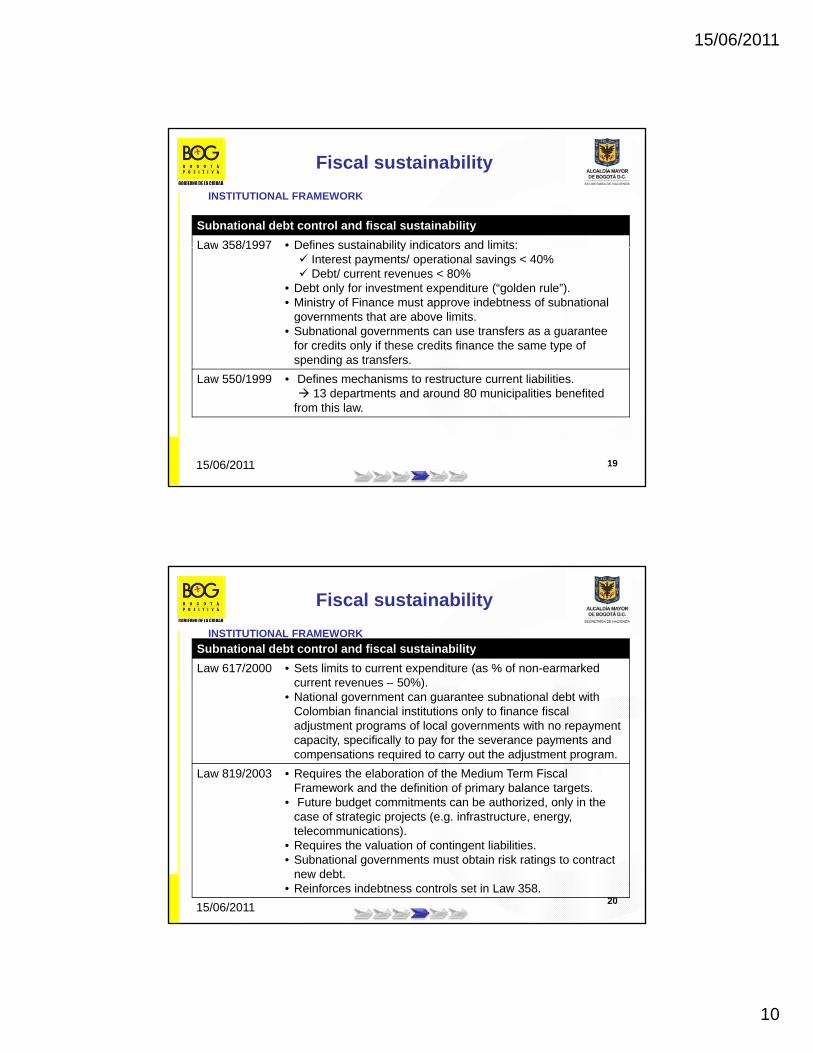

Subnational debt control and fiscal sustainability

Law 358/1997 • Defines sustainability indicators and limits:

INSTITUTIONAL FRAMEWORK

Fiscal sustainability

Law 358/1997 Defines sustainability indicators and limits: Interest payments/ operational savings < 40% Debt/ current revenues < 80%

• Debt only for investment expenditure (“golden rule”).• Ministry of Finance must approve indebtness of subnational

governments that are above limits.• Subnational governments can use transfers as a guarantee

for credits only if these credits finance the same type of spending as transfers.

15/06/2011 19

Law 550/1999 • Defines mechanisms to restructure current liabilities. 13 departments and around 80 municipalities benefited

from this law.

Subnational debt control and fiscal sustainability

Law 617/2000 • Sets limits to current expenditure (as % of non-earmarkedcurrent revenues – 50%)

INSTITUTIONAL FRAMEWORK

Fiscal sustainability

current revenues 50%).• National government can guarantee subnational debt with

Colombian financial institutions only to finance fiscal adjustment programs of local governments with no repaymentcapacity, specifically to pay for the severance payments and compensations required to carry out the adjustment program.

Law 819/2003 • Requires the elaboration of the Medium Term Fiscal Framework and the definition of primary balance targets.

• Future budget commitments can be authorized only in the

15/06/201120

Future budget commitments can be authorized, only in thecase of strategic projects (e.g. infrastructure, energy, telecommunications).

• Requires the valuation of contingent liabilities.• Subnational governments must obtain risk ratings to contract

new debt.• Reinforces indebtness controls set in Law 358.

15/06/2011

11

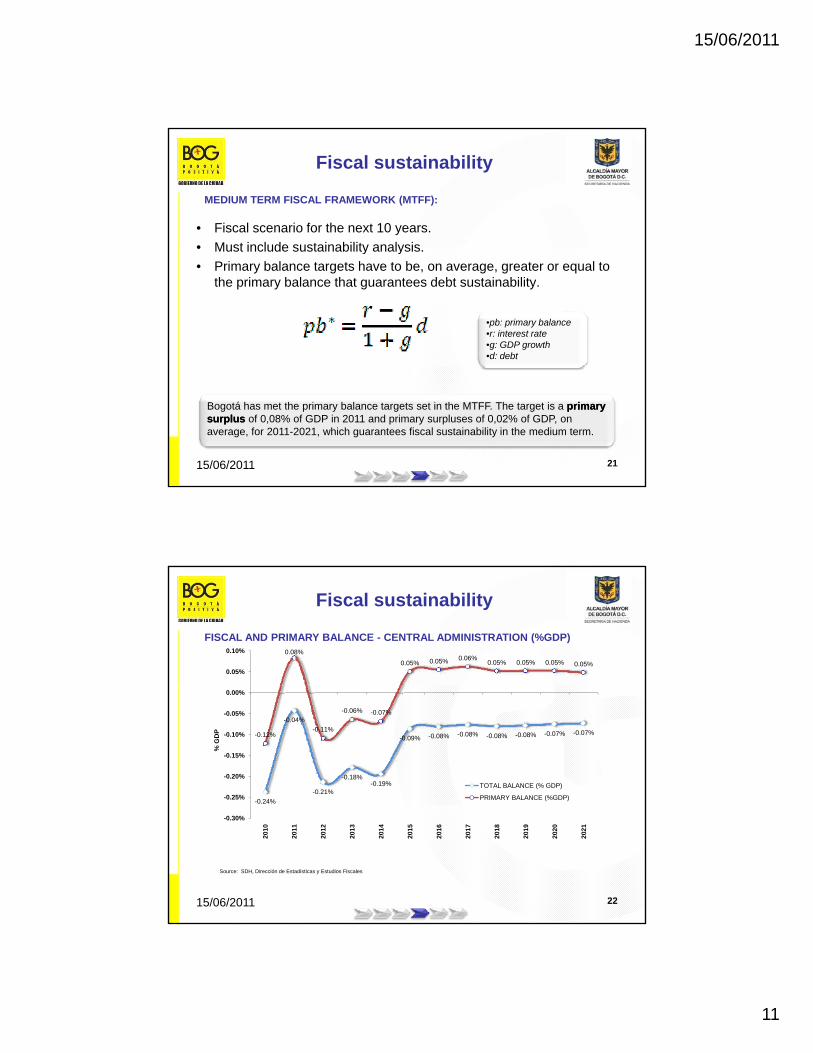

• Fiscal scenario for the next 10 years.

• Must include sustainability analysis

MEDIUM TERM FISCAL FRAMEWORK (MTFF):

Fiscal sustainability

• Must include sustainability analysis.

• Primary balance targets have to be, on average, greater or equal tothe primary balance that guarantees debt sustainability.

•pb: primary balance•r: interest rate•g: GDP growth•d: debt

15/06/2011 21

Bogotá has met the primary balance targets set in the MTFF. The target is a primaryprimarysurplus surplus of 0,08% of GDP in 2011 and primary surpluses of 0,02% of GDP, onaverage, for 2011-2021, which guarantees fiscal sustainability in the medium term.

FISCAL AND PRIMARY BALANCE - CENTRAL ADMINISTRATION (%GDP)

Fiscal sustainability

0.08%

0.05% 0.05% 0.06%0.05% 0.05% 0.05% 0.05%

0.05%

0.10%

-0.24%

-0.04%

-0.21%

-0.18%-0.19%

-0.09% -0.08% -0.08% -0.08% -0.08% -0.07% -0.07%-0.12%-0.11%

-0.06% -0.07%

-0.25%

-0.20%

-0.15%

-0.10%

-0.05%

0.00%

% G

DP

TOTAL BALANCE (% GDP)

PRIMARY BALANCE (%GDP)

Source: SDH, Dirección de Estadísticas y Estudios Fiscales

15/06/2011 22

-0.30%

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

15/06/2011

12

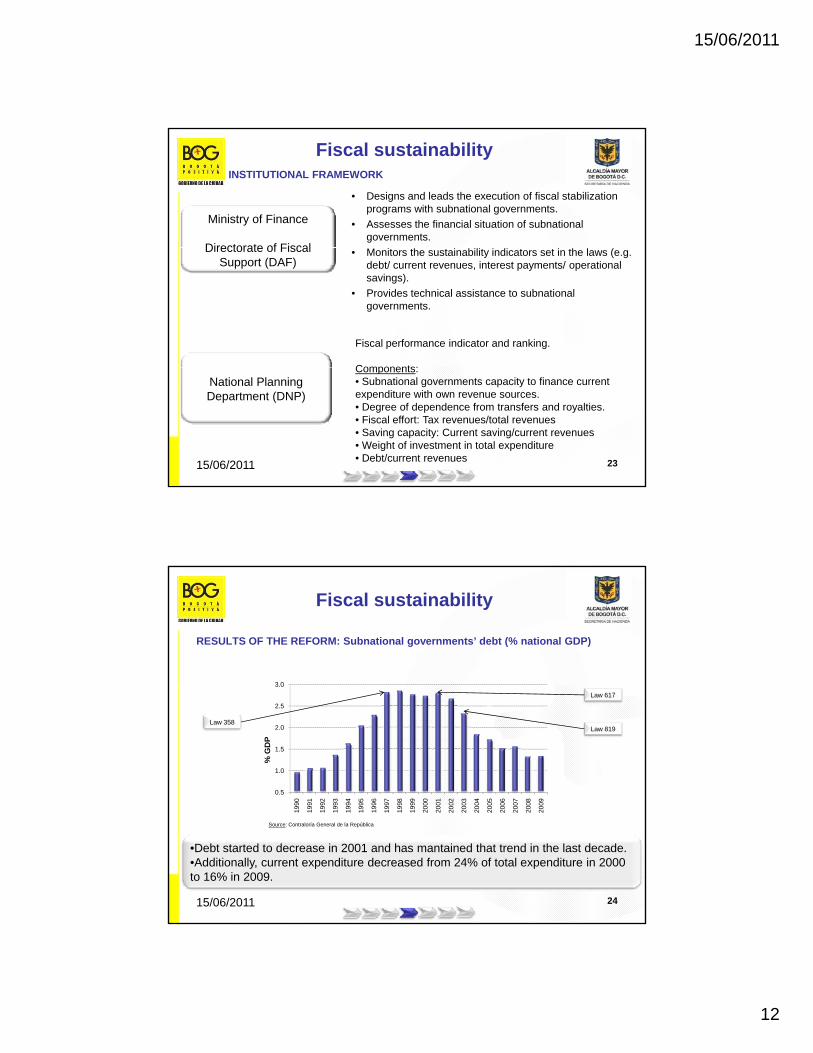

• Designs and leads the execution of fiscal stabilizationprograms with subnational governments.

• Assesses the financial situation of subnationalgovernments.

Ministry of Finance

Directorate of Fiscal

Fiscal sustainabilityINSTITUTIONAL FRAMEWORK

• Monitors the sustainability indicators set in the laws (e.g.debt/ current revenues, interest payments/ operationalsavings).

• Provides technical assistance to subnationalgovernments.

Directorate of Fiscal Support (DAF)

Fiscal performance indicator and ranking.

Components:

15/06/2011 23

National PlanningDepartment (DNP)

Components:• Subnational governments capacity to finance currentexpenditure with own revenue sources.• Degree of dependence from transfers and royalties.• Fiscal effort: Tax revenues/total revenues• Saving capacity: Current saving/current revenues• Weight of investment in total expenditure• Debt/current revenues

RESULTS OF THE REFORM: Subnational governments’ debt (% national GDP)

3 0

Fiscal sustainability

0.5

1.0

1.5

2.0

2.5

3.0

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

% G

DP

Law 819

Law 617

Law 358

15/06/2011 24

199

199

199

199

199

199

199

199

199

199

200

200

200

200

200

200

200

200

200

200

Source: Contraloría General de la República

•Debt started to decrease in 2001 and has mantained that trend in the last decade.•Additionally, current expenditure decreased from 24% of total expenditure in 2000 to 16% in 2009.

15/06/2011

13

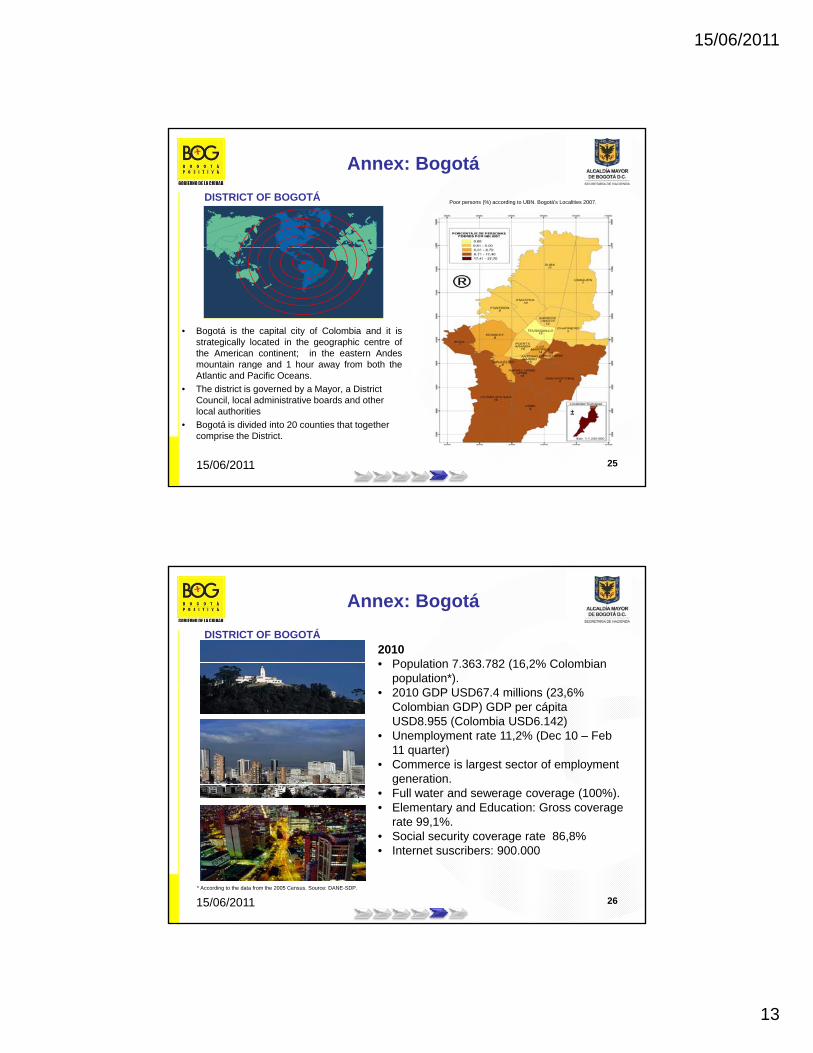

Annex: Bogotá

DISTRICT OF BOGOTÁPoor persons (%) according to UBN. Bogotá's Localities 2007.

• Bogotá is the capital city of Colombia and it isstrategically located in the geographic centre ofthe American continent; in the eastern Andesmountain range and 1 hour away from both the

15/06/2011 25

mountain range and 1 hour away from both theAtlantic and Pacific Oceans.

• The district is governed by a Mayor, a District Council, local administrative boards and other local authorities

• Bogotá is divided into 20 counties that together comprise the District.

DISTRICT OF BOGOTÁ

2010 • Population 7.363.782 (16,2% Colombian

population*).

Annex: Bogotá

• 2010 GDP USD67.4 millions (23,6% Colombian GDP) GDP per cápita USD8.955 (Colombia USD6.142)

• Unemployment rate 11,2% (Dec 10 – Feb11 quarter)

• Commerce is largest sector of employmentgeneration.

• Full water and sewerage coverage (100%).El t d Ed ti G

15/06/2011 26

• Elementary and Education: Gross coveragerate 99,1%.

• Social security coverage rate 86,8%• Internet suscribers: 900.000

* According to the data from the 2005 Census. Source: DANE-SDP.

15/06/2011

14

ThankThank youyou