Embed Size (px)

Citation preview

Major transactions: driving

activity in Lyon

The Lyon office market 3rd quarter 2016

2222222

Editorial

Highlight

Record volume by the end of September

With 384 rental transactions recorded by the end of September, 2016 is one of the

most active years for the Lyon market. In 2006 and 2007, the number of leases

recorded over the Q1-Q3 period did go over the 400 level, although the volume of these

transactions was much lower. Now having clocked up 199,000 sq m of take-up, the

market is now 26% over the ten-year average.

There’s no doubt that 2016 is set to be a very good year. The Lyon market has now

seen strong levels of activity for the last 5 quarters and this should continue over

the next few months. There will be a series of major elections over the next few

quarters, but history dictates that the economic climate prevails over politics. Rental and

investment market analyses show no signs of any significant change over previous

market cycles (see "Are elections slowdown factors for the real estate market?", JLL

Capital Markets 2016). Activity in the Lyon market should not therefore suffer as the

political climate surrounding the French presidential elections intensifies over the coming

months.

2

4

Market update

Major transactions: driving activity in Lyon High activity levels continue in the Lyon market

Succession of excellent quarterly results. After having posted 130,600 sq m of

take-up over H1 2016, the Lyon market continued to perform well with an additional

68,300 sq m over the last three months. The overall volume therefore stands at

198,900 sq m, representing a 10% year-on-year increase. Such levels haven't been

seen since 2007, a year when many of the records for the Lyon market were set.

The rising level of major transactions has led for far higher results than normal.

With a cumulative figure of 118,450 sq m, the over 1,000 sq m segment accounted for

60% of overall take-up. The volume may be high, but so was the number of

transactions: while there were only 23 transactions in the over 1,000 sq m

segment across all submarkets by 30 September 2015, there were 37 over the

first nine months of 2016. Examples of these transactions include ORANGE with

5,500 sq m in the "Anthémis" building in Part-Dieu, CARSAT's leases of 3,900 and

4,880 sq m and NOVACAP with 3,400 sq m in Ecully.

With 384 transactions recorded over the first nine months of the year, 2016 is

one of the most active years ever recorded for the Lyon market. High-performance

years in the Lyon market have historically been due to activity from turnkey

transactions when these market "accelerators" have driven levels over the symbolic

200,000 sq m barrier. The same is true in 2016. 6 major projects, accounting for

46,000 sq m and 23% of overall take-up, were finalised . Turnkey deals are still

desirable as they allow companies to tailor a building to meet their needs. The

DANONE Group signed a forward funded lease for the future “Linux” building in

Limonest (over 11,000 sq m) where it plans to install the head offices for its

subsidiaries BLEDINA and DANONE NUTRICIA AFRICA OVERSEAS. The LDLC

Group also completed a deal for the construction of two turnkey buildings totalling

7,000 sq m for its own use as well as the creation of the LDLC School offering digital

skills training. Finally, ORANGE is to move to 26,000 sq m of dedicated office space

on Avenue Lacassagne in the Part-Dieu submarket. The building should be

completed by the end of 2019. Land reserves to meet this type of demand are still

available in the suburbs and in Inner Lyon where several projects are under

construction or consideration.

These good results are also indicative of consistent activity across all space

segments. The small and medium space segment (under 500 sq m) remains a solid

base for the market and has continued to be very active. Since the beginning of the

year, transactions in this segment have accounted for 81% (311 in total), representing

a 9% increase on the 10-year average. Examples of companies leasing small spaces

in the city include INPI at "Convergence", ARCHI GRAPHI at "Greenopolis" and ST

GOBAIN DEVELOPPEMENT at "Tour Part-Dieu".

4

Companies still favour Lyon and Villeurbanne: Inner Lyon accounted for 7 out

of every 10 sq m transacted. Following an initial delay, the completion of the

Orange lease mentioned above means that the Part-Dieu market is now back on

track. The suburbs gained ground in 2016, mainly due to good performance in the

North-West submarket, which saw strong demand over H1. This area accounted

for 17% of overall take-up due to a high number of major turnkey transactions, most

of which were completed over Q1.

Over the past few months, immediate availability in the Lyon region has seen a

period of absorption and now stands at around 375,000 sq m with a vacancy

rate of 6.3%, although with some marked differences across the various

submarkets. While availability in Part-Dieu stands at 3%, the vacancy rate in Gerland

stands at over 10%.

The share of new space in supply remained stable at 38% with some significant

variations depending on the district. Given the localised lack of new supply,

occupiers are turning to development projects. The pre-let rate for buildings

under construction, which had fallen over the last few quarters, posted an

increase to 42%. Inner Lyon remains in the lead both in terms of location and pre-

lets with a slightly higher percentage (44%). Reduced levels of supply are

encouraging companies to take early positions on projects. The gap is however

narrowing with the suburbs which are attracting an increasing number of occupiers to

latest-generation buildings with competitive rents and ever-improving public transport

links.

The rate of new deliveries varies considerably in the Lyon region. One good

year for new deliveries is normally followed by a downturn. 17,400 sq m is still

under construction and should take the total amount of new space delivered by the

end of the year to 74,500 sq m. 2017 will be a major year with around 50 projects

reported including "King Charles" in Confluence, "Silex 1" in Part Dieu and "View

One" in Carré de Soie.

Rental values remained stable in most submarkets. The prime rent remained at

€300 per sq m per year excl. taxes and charges for high-rise towers in Part-Dieu

as well as the office element of the future Grand Hôtel-Dieu district. The value

for more traditional buildings in the Part-Dieu submarket also remained unchanged at

€270 per sq m per year. Incentives are still widely used, although levels vary

substantially depending on the district and the type of building. More substantial

concessions are made for prime buildings or for leases of large spaces.

4

Lyon market dominated by French investors

Following a particularly active H1 with €536 million in investments, the Lyon

investment market has slowed considerably. "Only" €51 million was invested in

Lyon over Q3, taking the overall investment volume to €587 million.

Market activity therefore appears to have slowed somewhat over the last few months;

this has mainly been due to the lack of deals for values in excess of €15 million. The

lack of prime supply on the market is clearly having an impact. 11 transactions were

recorded in Q3 alone (compared with 13 over the same period last year) only one of

which was for more than €15 million. Although lower than in 2015, performance at

the beginning of the year has allowed volumes to reach a level that is 26%

higher than the average Q3 figure for the last 5 years. Concerns therefore

remain relative and the first two quarters were highly active thanks to two large

leases. These transactions include AEW EUROPE's acquisition of the "Le Triangle"

office building in the Part-Dieu district for almost €54 million as well as PRIMONIAL's

purchase of the office building "Universaône" (12,782 sq m) which was completed in

2013 in the Lyon Vaise district for around €50 million.

However, most acquisitions were for assets under €15 million. 26 of the 38

transactions were carried out in this segment for a total of €165 million. The

average transaction value, normally around €12 million for single assets, stood at only

€4 million in Q3 2016. Examples include SHAM's acquisition of the "Fakto" office

building in Villeurbanne which has 6,186 sq m of space for close to €15 million, as

well as another by SWISS LIFE REIM for the "Récamier" office building in the 6th

district of Lyon which has 3,500 sq m of space for €13.5 million. These "small"

disposals still form a considerable and solid foundation for the Lyon market.

The Lyon market is traditionally diverse in terms of asset type. Offices continued to

be the asset of choice accounting for €448 million in investments or 76% of the

overall volume. However, other assets were not overlooked. Industrial and logistics

accounted for €121 million since the beginning of the year, representing 29% of

investments in the Lyon region. Deals of note included GOODMAN’s acquisition of a

43,000 sq m class-A warehouse in Satolas-et-Bonce for €27 million as well as

another by VAILLANCE IMMOBILIER for a group of industrial buildings (9,100 sq m)

on a site called Espaces des Portes de l'Est in Saint Priest for €6 million. Retail

assets, which had been lacking at the beginning of the year, made a comeback

with HERACLES INVESTISSEMENT's forward funding speculative acquisition of 11

retail sites at Ilot Ynfluences Square in the Lyon Confluence submarket.

Mis en forme : Anglais (États Unis)

4

« Universaône »

Source: JLL

« Universaône »

Source: JLL

4

Forward-funding sales are becoming increasingly popular. While there has

been an average of 7 per year since 2010, at the end of September there have

already been 7. Investment in this type of asset stood at €158 million representing

over a quarter of the overall volume. Occupier appetite for this type of space makes

this category a secure and liquid asset for investors. Forward funding sales (VEFA)

have seen great success in the office investment market this year and have

accounted for a third of investments. For example, UNOFI GESTION d’ACTIFS

acquired "Linux", the future headquarters for the DANONE subsidiaries BLEDINA and

NUTRICIA AFRICA, with over 11,000 sq m of space in Limonest for €52 million. In

addition, there was AEW EUROPE's speculative acquisition of the "Oxaya" building in

the North of the Gerland submarket for €23 million.

It came as no surprise that national (and local) players dominated the Lyon

market, both on the buy and sell sides: 68% of vendors and 81% of purchasers

were French. These included a private investor's turnkey acquisition of EFS

(ETABLISSEMENT FRANÇAIS DU SANG) in Décines-Charpieu for €19 million and

KEYS ASSET MANAGEMENT's acquisition of "Le Seven", a 6,270 sq m office

building in the Gerland district for €21 million.

International investors were also active and accounted for around a quarter of the

overall investment volume. Noteworthy transactions include ROCKSPRING’s

acquisition of an 18,700 sq m warehouse in St Quentin Fallavier for €8 million.

Given the lack of supply, competition for prime assets remains strong. The

prime office yield in Lyon therefore saw further compression over Q3 2016. It

now stands at a historic low of 4.50%. This compression also applies to other

asset classes as the best industrial and logistics assets are currently being

negotiated at 7.00% and 5.50% respectively.

The climate is still favourable for asset disposals as investors in the marketplace

continue to benefit from the combination of low yields and the strong level of demand

to dispose of their assets in the Lyon region. As financing terms have been relaxed,

purchasers are increasingly on the look-out for opportunities.

108

8

9

Outlook

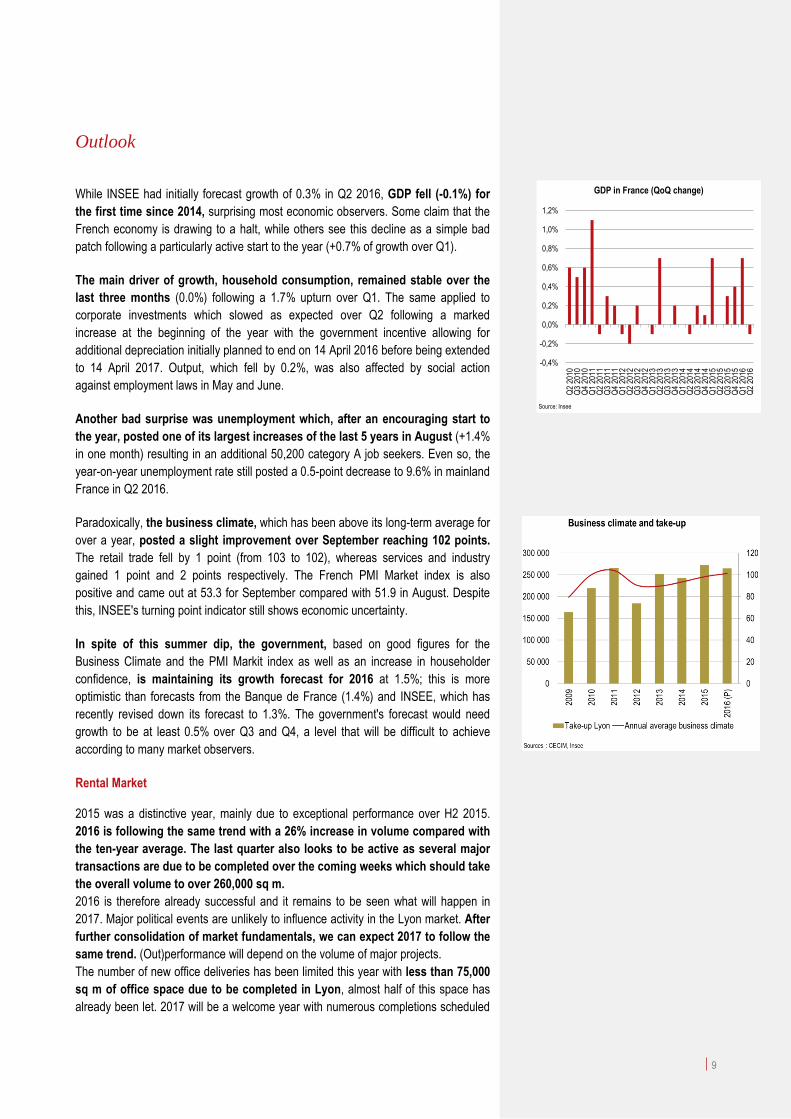

While INSEE had initially forecast growth of 0.3% in Q2 2016, GDP fell (-0.1%) for

the first time since 2014, surprising most economic observers. Some claim that the

French economy is drawing to a halt, while others see this decline as a simple bad

patch following a particularly active start to the year (+0.7% of growth over Q1).

The main driver of growth, household consumption, remained stable over the

last three months (0.0%) following a 1.7% upturn over Q1. The same applied to

corporate investments which slowed as expected over Q2 following a marked

increase at the beginning of the year with the government incentive allowing for

additional depreciation initially planned to end on 14 April 2016 before being extended

to 14 April 2017. Output, which fell by 0.2%, was also affected by social action

against employment laws in May and June.

Another bad surprise was unemployment which, after an encouraging start to

the year, posted one of its largest increases of the last 5 years in August (+1.4%

in one month) resulting in an additional 50,200 category A job seekers. Even so, the

year-on-year unemployment rate still posted a 0.5-point decrease to 9.6% in mainland

France in Q2 2016.

Paradoxically, the business climate, which has been above its long-term average for

over a year, posted a slight improvement over September reaching 102 points.

The retail trade fell by 1 point (from 103 to 102), whereas services and industry

gained 1 point and 2 points respectively. The French PMI Market index is also

positive and came out at 53.3 for September compared with 51.9 in August. Despite

this, INSEE's turning point indicator still shows economic uncertainty.

In spite of this summer dip, the government, based on good figures for the

Business Climate and the PMI Markit index as well as an increase in householder

confidence, is maintaining its growth forecast for 2016 at 1.5%; this is more

optimistic than forecasts from the Banque de France (1.4%) and INSEE, which has

recently revised down its forecast to 1.3%. The government's forecast would need

growth to be at least 0.5% over Q3 and Q4, a level that will be difficult to achieve

according to many market observers.

Rental Market

2015 was a distinctive year, mainly due to exceptional performance over H2 2015.

2016 is following the same trend with a 26% increase in volume compared with

the ten-year average. The last quarter also looks to be active as several major

transactions are due to be completed over the coming weeks which should take

the overall volume to over 260,000 sq m.

2016 is therefore already successful and it remains to be seen what will happen in

2017. Major political events are unlikely to influence activity in the Lyon market. After

further consolidation of market fundamentals, we can expect 2017 to follow the

same trend. (Out)performance will depend on the volume of major projects.

The number of new office deliveries has been limited this year with less than 75,000

sq m of office space due to be completed in Lyon, almost half of this space has

already been let. 2017 will be a welcome year with numerous completions scheduled

-0,4%

-0,2%

0,0%

0,2%

0,4%

0,6%

0,8%

1,0%

1,2%

Q2

2010

Q3

2010

Q4

2010

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

Q1

2016

Q2

2016

Source: Insee

GDP in France (QoQ change)

108

8

9

which will boost the Lyon office stock to over 6,000,000 sq m.

Prime rental values remain broadly stable with adjustments applied in some areas.

Market conditions remain balanced. Leeway in negotiations remains a key lever,

although with strong variations depending on the district and the building type. Rents

are not expected to increase over the near future or until additional prime supply

comes onto the market; this type of space is currently at the project stage.

Investment market

In the national context, the Lyon market stands out as an active and attractive

area in terms of economics which, combined with a favourable investment

climate, has enabled the Lyon market to remain a market of choice as

recognised by investors.

The market may remain active with a rising number of transactions recorded, but

volumes are clearly falling and should reach €800 million by the end of the year.

Performance or any decline will largely depend on whether the best quality assets

across all product types come onto the market. Demand remains strong and all the

market now needs is for landlords to make the decision to sell.

Several new projects have already submitted applications for building permits and

should attract investor interest. The City of Lyon remains a recognised and liquid

market for national and international purchasers, even though the latter have been

discreet since the beginning of the year. On a positive note, as the vast majority of

activity in this market is attributable to domestic players, the Lyon market has

relatively little exposure to any fall in demand linked to Brexit.

Finally, the lack of so-called “classic” product will keep yields under pressure.

108

8

11 10

Note pad

Navly: the driverless shuttle to ‘reconnect ' workers in

Confluence

Since 5 November and for a one-year trial period, two electric driverless and completely

autonomous shuttle buses will operate along a 1,350 metre stretch alongside the Saône in

the Confluence eco-district, an iconic site in the city of Lyon.

This is a world first for this type of system.

These NAVLY shuttle buses, which can accommodate up to 15 passengers, stop at 5

stations between the Confluence shopping centre and the far south of the district up to the

head office of GL EVENTS. Free of charge, the service runs on weekdays from 7.30 am to

7 pm and at 10-minute intervals during peak times.

This service is a response to the challenges and needs of future urban mobility and

is complementary to existing traditional transport services (bus, tram, métro, ...). It

offers a successful, innovative and intelligent alternative to operate for the "last

kilometre" of the commute. These shuttle buses aim to reconnect employees working

along the banks of Confluence.

The project came about as the result of a collaboration between the City of Lyon, Sytral

(the body responsible for organising mobility in the city), NAVYA (company specialising in

the development of innovative mobility solutions) and the KEOLIS GROUP which runs the

public transport network in Lyon, TCL. This initiative is a public/private collaboration which

aims to encourage the creation of new services and the emergence of innovative

companies with a focus on sustainable development. The project is also supported by

ADEME (French Environment and Energy Management Agency).

Authorised by the MINISTRY OF ECOLOGY, SUSTAINABLE DEVELOPMENT AND

ENERGY, the NAVLY service meets all the security and capacity regulations required for

these autonomous shuttles to run on the public highway.

Source: KEOLIS

8

11

Markets holding up to political and economic

uncertainty

The main markets around the world have so far fared relatively well through this

period of instability seen since the beginning of 2016. Despite rising concerns,

investment volumes should remain high in 2016, while rental market fundamentals

and corporate demand remain robust in the United States and Europe. At this stage,

the main areas of concern are the consequences of Brexit as well as the slowdown in

the Chinese economy.

At the end of H1 2016, the investment market posted a volume of $292 billion

(€263 bn), representing a 10% decrease compared with 2015. Due to the rise in

political uncertainty and greater investor prudence, the investment market could see a

10 to 15% decrease in activity in 2016. However, even with a reduction to around

$600 billion (€540 bn), this is one of the highest ever levels. In Europe, investment

volume at the half-year point reached $109 billion (€98 bn) and is only 5% down on

2015; this is due to sustained activity in continental Europe which has virtually offset

the reduction in activity seen in Great Britain. Yields continued to fall in some markets

but the overall trend is stabilisation.

As corporates are adopting a more prudent stance, the position for rental markets

is more mixed. Activity is holding well in the United States, most European countries

and in Japan; of the main markets, only Great Britain and China have seen reductions

in activity. Given the context of uncertainty, the rental market could see a slight

reduction of around 5% in 2016 compared with the 2015 record of 41 million sq m.

Supply has continued to fall and reached 12.1% at the half-year. Levels are not

expected to change considerably by the end of the year, with Europe and the United

States posting a fall while Asia could see a slight increase in vacancy rates. Because

of tightening levels of supply, rents are on an upward trend with a 5% year-on-year

increase. However, the rate of increase should slow to 3% towards the end of the

year.

12

Part-Dieu: roof of Halles car park to become a terrace

It's the oldest car park in the city of Lyon, managed by LPA (Lyon Parc Auto). Developed

in 1969, the Halles car park, located along Rue Garibaldi, is soon to be completely

transformed.

Until now, the building had been blocked between a petrol station and a walkway and was

also hidden by the Halles market on one side and the stairwell onto Rue Garibaldi on the

other. But since redevelopment work in the district, the building is once more

visible for all to see.

And it is now being offered a new opportunity. Car drivers and tenants of the adjacent

“Incity” tower will be able to continue to park in the building, but the roof, which is 25m

high and currently inaccessible, is to be converted into a 360-degree rooftop garden

terrace. This will create a new 1,800 sq m space. Visitors will be able to stroll around,

have a drink at the refreshment stand, enjoy an ice cream at the tables provided or have a

picnic in the gardens.

There will also be a restaurant on the ground floor and there is an electric scooter station

which opened at the beginning of summer. "The aim of the project is to provide a space

for non-car owners and create a tourist destination" adds Louis Pelaez, president of LPA.

To complete the ecological image, the site also has the first electric scooter hire station in

Lyon, as well as a new urban logistics service in a 380 sq m unit in the basement

which has been created in partnership with Oxipio which is also setting up in Lyon.

This will be an off-site storage site offering a delivery service for shops and

restaurants which will operate from the building using electric tricycles.

Work is due to start towards the end of the year with completion planned for autumn

2017.

Project roof of Halles car park

Source: WW Architecture / Menghi Zheng

13

Work becomes lifestyle as generations Y and Z reinvent

offices

According to a JLL report1, 49% of employees aged under 35 believe that they

would be more committed to their company if it were to introduce a democratic

model based on shared decision making and responsibilities.

The report reveals that young people dream of involvement and responsibility,

recognition from management, flexible working practices and involvement in important

projects. More than freedom, they dream of belonging to a community that

embodies the values in which they believe. They dream of fluidity, of a world without

silos, without dress codes, with no distinction between professional and personal and

no longer want the environment to be imposed.

As part of the report, the young people interviewed devised 15 new forms of

workspace with a range of complementary uses.

By 2030, the office will of course remain a place where we go to work, but in addition

the workplace will sometimes:

be hyper productive, working in PERFORMANCE TUBES, or be highly

collaborative, within PROJECT SPACES, FABLABS which allow

experimentation, or using PITCH THEATRES for idea creation.

be a place of inspiration, which would allow one to withdraw to a HIDEAWAY

or to experience art installations in a DISRUPTIVE space, designed like a

curiosity cabinet.

allow for the formation of new relationships in a RECEPTION LOUNGE,

completely open to all, to work at a POP-UP DESK in an unexpected location,

or to stroll through an AGORA dedicated to connections and the organisation of

meet-ups within the company.

By 2030, the office will have finally become a regenerative space:

It will offer disconnection COCOONS, playgrounds to let off steam,

ASSOCIATIONS to fulfil the need for civic engagement.

It will be a community space: parties and FLASH MOBS will form part of the

daily routine and workers will meet at COMMUNAL KITCHEN GARDENS where

they can cultivate tomatoes alongside interpersonal relationships.

In light of these rising expectations, some companies in the digital economy

have already made the first steps. BlaBlaCar, Deezer and Allo Resto are already

experimenting with tribal working, games rooms and disconnection areas. Their

spaces have been jointly designed with the employees and create an experience that

workers deem to be unique - and which brings them closer to the company. This

longed-for managerial vision should soon become reality and offices will, without a

doubt, have a decisive role to play.

1 Quantitative survey of 200 young people, carried out by the CSA institute - and qualitative with 3 focus

groups comprised of high-school pupils, students and young start-up owners.

14

ICC, ILAT and ILC: all indicators are positive

After posting a downturn last quarter, the ICC recovered over Q2 2016. With a 0.5%

increase in the index, it now stands at 1,622 points compared with 1,615 last quarter.

In parallel, the ILAT still saw annual growth post a moderate increase with a 0.5%

year-on-year increase. The index stood at 108.41 in Q2 2016, compared with 107.86

over the same period last year.

In conclusion for commercial leases, the ILC index remained stable and positive

over Q2 2016. Its value remained unchanged quarter on quarter: 108.40 points,

representing a slight 0.02% year-on-year increase. The retail rents index has

remained relatively stable for over three years, fluctuating in a range from 108.32 to

108.53.

-6%

-4%

-2%

0%

2%

4%

6%

8%

Q4

2009

Q1

2010

Q2

2010

Q3

2010

Q4

2010

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

Q1

2016

Q2

2016

Source: INSEE

Comparison of ICC, ILAT and ILC changes

ICC annual change ILAT annual change ILC annual change

Virginie Houzé MRICS

Head of Research France

Research department – Paris

T : +33 1 40 55 15 94

Delphine Mahé

Research manager

Research department – Paris

T : +33 1 40 55 15 91

Magali Pousson

Consultant

Research department – Lyon

T : +33 4 78 17 13 13

www.jll.fr

COPYRIGHT © JONES LANG LASALLE IP, inc. 2016 - This publication is the sole property of Jones Lang LaSalle IP, Inc. and must not be copied, reproduced or transmitted in any form or by any means,

either in whole or in part, without the prior written consent of Jones Lang LaSalle IP, Inc. The information contained in this publication has been obtained from Source generally regarded to be reliable.

However, no representation is made, or warranty given, in respect of the accuracy of this information. We would like to be informed of any inaccuracies so that we may correct them. Jones Lang LaSalle IP,

Inc does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.

Paris

40-42, rue La Boétie

75008 Paris

T : +33 (0)1 40 55 15 15

F : +33 (0)1 46 22 28 28

Le Plessis-Robinson

« La Boursidière » - BP 171

92357 Le Plessis-Robinson

T : +33 (0)1 40 55 15 15

F : +33 (0)1 46 22 28 28

Lyon

55, avenue Foch

69006 Lyon

T : +33 (0)4 78 89 26 26

F : +33 (0)4 78 89 04 76

La Défense

« Cœur Défense »

100-110, esplanade Charles de Gaulle

92932 Paris La Défense Cedex

T : +33 (0)1 40 55 15 15

F : +33 (0)1 49 00 32 59

Saint-Denis

3, rue Jesse Owens

93210 Saint-Denis

T : +33 (0)1 40 55 15 15

F : +33 (0)1 48 22 52 83

Marseille

21, rue de la République

13002 Marseille

T : +33 (0)4 95 09 13 13

F : +33 (0)4 95 09 13 00