Embed Size (px)

Citation preview

1

WTO Schedules of Concessions

and Renegotiation of Concessions ESTIMATED TIME: 4 hours

OBJECTIVES OF MODULE 4

To explain the WTO Schedules of concessions on goods and the main disciplines

applicable to them, particularly Article II of the GATT 1994.

To explain the rules and procedures regarding the modification of the Schedule of

concessions through renegotiations, with a focus on Article XXVIII of the

GATT 1994.

To introduce the Integrated Data Base (IDB) and the Consolidated Tariff Schedule

(CTS).

MODULE

4

2

MODULE 4 TO SCHEDULES OF CONCESSIONS AND RENEGOTIATION OF CONCESSIONS .............. 1

I. INTRODUCTION ............................................................................................................ 3

II. WTO SCHEDULES OF TARIFF CONCESSIONS .................................................................... 4

II.A. STRUCTURE OF WTO GOODS SCHEDULES ........................................................... 4

II.B. CONSOLIDATED LOOSE-LEAF SCHEDULES ........................................................ 10

II.C. AMENDMENTS TO WTO SCHEDULES ................................................................ 11

III. ARTICLE II OF THE GATT 1994 ..................................................................................... 15

III.A. APPLICATION AND INTERPRETATION OF ARTICLE II:1(A) OF THE GATT 1994 ........ 17

III.B. APPLICATION AND INTERPRETATION OF ARTICLE II:1(B), OF THE GATT 1994, FIRST

SENTENCE ..................................................................................................... 18

III.C. OTHER DISCIPLINES AIMED AT PRESERVING THE VALUE OF TARIFF CONCESSIONS

CONTAINED IN ARTICLE II OF THE GATT 1994 .................................................. 21

III.D. TAXES AND CHARGES NOT SUBJECT TO THE RULES ON TARIFF CONCESSIONS ..... 23

IV. MODIFICATION OF THE SCHEDULES OF CONCESSIONS .................................................. 27

IV.A. MODIFICATION OF SCHEDULES UNDER ARTICLE XXVIII OF THE GATT 1994 ......... 28

IV.B. RENEGOTIATIONS OF CONCESSIONS UNDER OTHER GATT PROVISIONS .............. 37

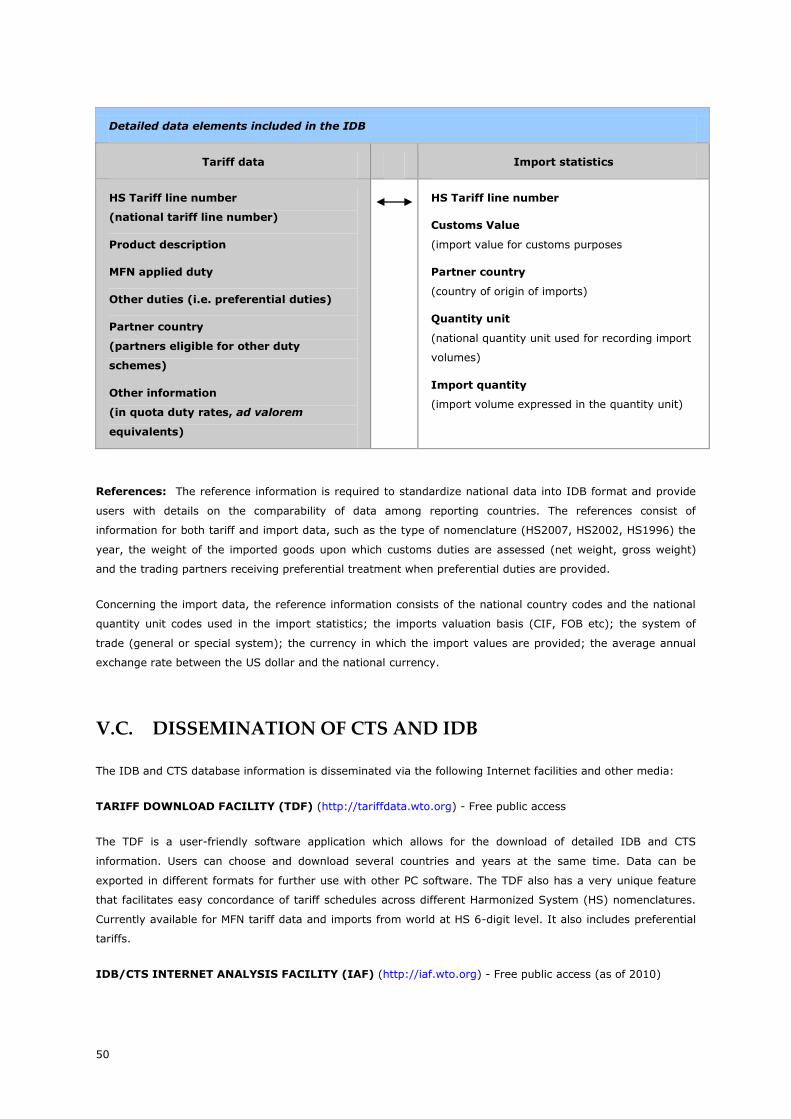

V. INFORMATION ON TARIFFS AND IMPORT FLOWS ........................................................... 47

V.A. CONSOLIDATED TARIFF SCHEDULE (CTS) DATABASE ......................................... 47

V.B. INTEGRATED DATA BASE (IDB)........................................................................ 49

V.C. DISSEMINATION OF CTS AND IDB.................................................................... 50

VI. SUMMARY .................................................................................................................. 52

3

I. INTRODUCTION

In Module 3, we have studied tariffs as the most visible barrier to market access for goods. We have also

introduced the eight rounds of GATT multilateral trade negotiations, which have resulted in substantial

reductions of tariffs and a wide coverage of bound tariff lines.

The outcome of the negotiations on tariffs (most importantly the tariff concessions) have been incorporated in

legal documents called ''Schedules of Concessions'', which record WTO Members' specific commitments on

tariffs and other concessions. By doing so, the Schedules of concessions provide security and predictability of

market access for goods. In this Module, we will explain Members' WTO Schedules of concessions on goods

and the disciplines applicable thereto, particularly Article II of the GATT 1994.

Tariff concessions may become too onerous to maintain over time due to changing circumstances. In such

cases, Members are allowed to modify their tariff concessions through negotiations with Members holding

special rights, subject to certain requirements. In this regard, Article XXVIII of the GATT 1994, which is the

main provision ruling the modification of the Schedules of concessions, will be also explained in this Module.

An overview of the databases containing information regarding Members' tariffs and import flows, administered

by the WTO Secretariat, will be provided at the end of this Module.

4

II. WTO SCHEDULES OF TARIFF CONCESSIONS

IN BRIEF

The WTO Schedule of concessions on goods record, specific tariff and non-tariff concessions given by each

Member on an MFN basis, as well as domestic support and export subsidy commitments on agricultural

products. The Schedules of concessions form part of the binding commitments made by WTO Members and

are an integral part of the WTO Agreements.

Each Member has its own Schedule of concessions, except for Members that are part of a customs union

(e.g. the European Union and Switzerland/Liechtenstein), who have a single common Schedule that covers

all its Members. Members' tariff bindings are recorded in their Schedules of concessions on goods, which are

annexed to the GATT 1994 and are considered an integral part of that Agreement. 1 In the case of Members

that acceded to the WTO after its establishment, their Schedules are part of their Protocols of Accession.

The Schedules also record the results of bilateral or plurilateral negotiations (e.g. plurilateral negations

under the auspices of the Information Technology Agreement "ITA").

Determining a Member's concession for a specific tariff line could involve, in some cases, the examination of

several different legal instruments (e.g. pre- Uruguay Schedules, 2 Uruguay Round Schedules, accession

Schedules, ITA Schedules). In order to consolidate all tariff information, the Council for Trade in Goods has

established Consolidated Loose-leaf Schedules on Goods. Although the process of consolidation remains

pending for most Members, in practice, the information has been consolidated on an informal basis through

the Consolidated Tariff Schedules Database (CTS).

Article II of the GATT 1994 is the main provision dealing with the WTO Schedules of concessions in goods. It

requires Members, among others, to refrain from imposing ordinary customs duties in excess of those

provided in their Schedules of concessions.

II.A. STRUCTURE OF WTO GOODS SCHEDULES

In the WTO, tariffs are regarded as the most visible barriers to trade in goods and are subject to negotiations,

which have led to their successive reduction. However, the value of such tariff reductions would not guarantee

enhanced and predictable market access conditions if Members could freely increase them after the

negotiations. Thus, Members agree to bind their tariffs at specific levels and to record such tariff bindings in

their WTO Schedules of concessions, which represent their legal commitments in the WTO in respect of those

products and levels. The Appellate Body clarified in EC – Computer Equipment that concessions provided for in

1 See Article II:7 of the GATT 1994.

2 It should be noted that the Schedules of concessions pre-dating the Uruguay Round are also part of the GATT

1994. It is worth noting however, that the Uruguay Round negotiations introduced changes to most, but not

all, of the concessions granted previously.

5

Members' Schedules are part of the GATT 1994, which constitutes an integral part of the WTO Agreement

pursuant to Article II:2 of the WTO Agreement (EC – Computer Equipment, Appellate Body Report, para. 84).

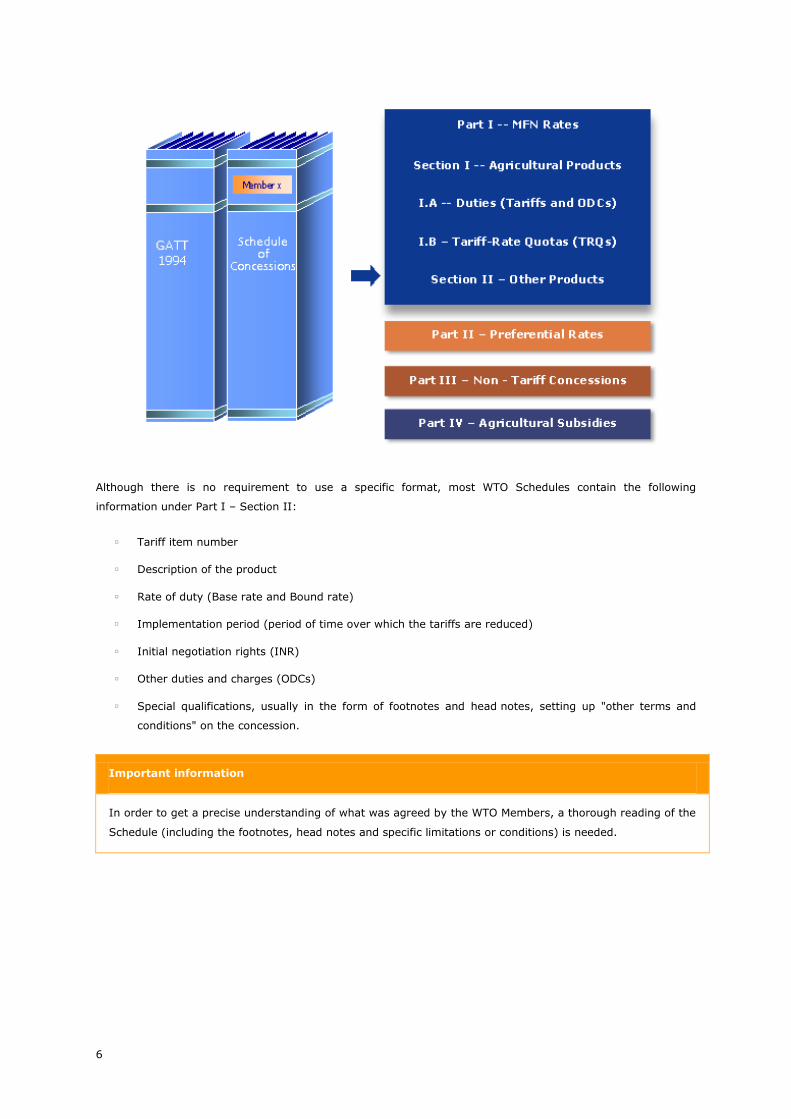

A WTO Member's goods Schedule consists of four parts:

Part I - Most Favoured Nation (MFN) tariffs: i.e. records the maximum tariff levels that can be

imposed on goods originating from other WTO Members. Part I is further divided into:

Section I: A — Agricultural products - Tariffs;

Section I: B — Agricultural products – Tariff quotas;

Section II — Other products (which are referred to as "non-agricultural" products in the context of

the Doha negotiations);

Part II – Preferential Tariffs: records (historical) preferential tariff arrangements listed in Article I of

the GATT 1994;

Part III – Non-Tariff Concessions: enumerates concessions made relating to non-tariff measures;

and,

Part IV – Agricultural Products - Commitments Limiting Subsidization: records specific

commitments on domestic support and export subsidies on agricultural products.

Important note

For the purpose of this Course, we only examine the MFN tariffs on other products (non-agricultural

products), that is, Part I: Section II of the goods Schedule.

RECALL:

Non-agricultural products or "other products" refer to all products which are NOT covered by the

Agreement on Agriculture (see Module 2). Agricultural products are defined in Annex 1A of the

Agreement on Agriculture. In practice, non-agricultural products cover a wide range of goods, including

manufactured products, fuels and mining products, fish and fish products, as well as forestry products.

These were referred to as "other products" in the context of the Uruguay Round and are sometimes called

"industrial" products.

6

Although there is no requirement to use a specific format, most WTO Schedules contain the following

information under Part I – Section II:

Tariff item number

Description of the product

Rate of duty (Base rate and Bound rate)

Implementation period (period of time over which the tariffs are reduced)

Initial negotiation rights (INR)

Other duties and charges (ODCs)

Special qualifications, usually in the form of footnotes and head notes, setting up "other terms and

conditions" on the concession.

Important information

In order to get a precise understanding of what was agreed by the WTO Members, a thorough reading of the

Schedule (including the footnotes, head notes and specific limitations or conditions) is needed.

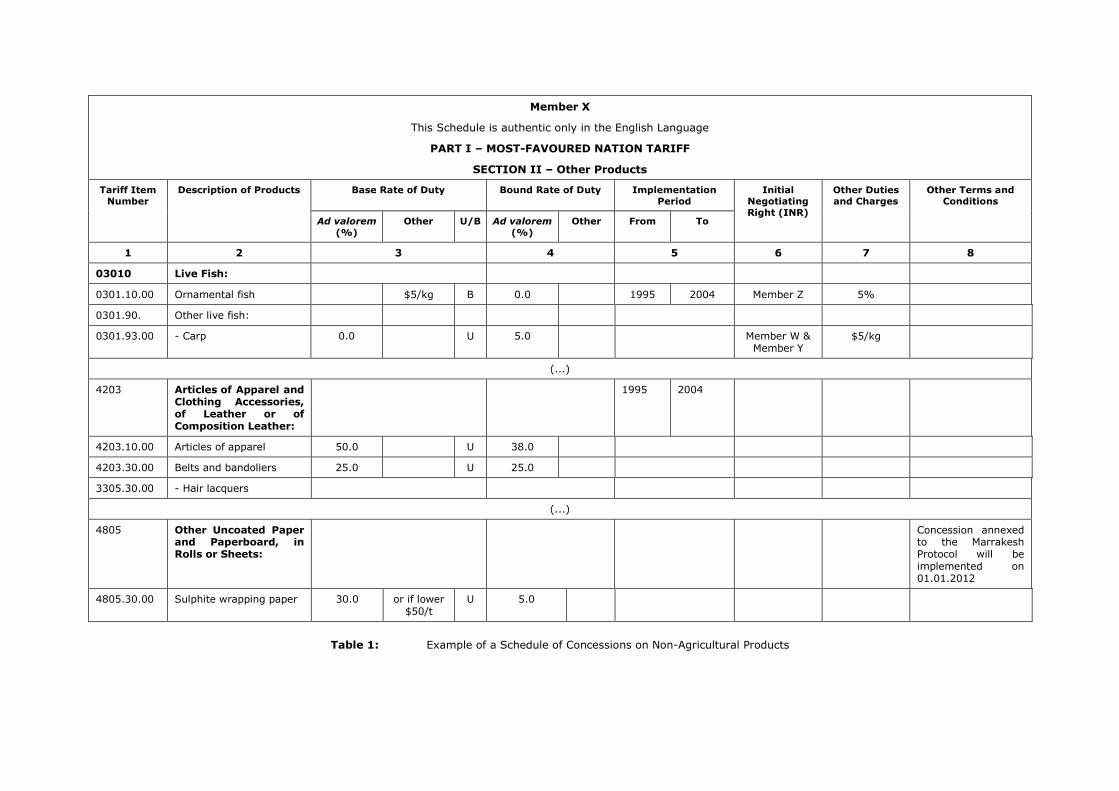

Member X

This Schedule is authentic only in the English Language

PART I – MOST-FAVOURED NATION TARIFF

SECTION II – Other Products

Tariff Item

Number

Description of Products Base Rate of Duty Bound Rate of Duty Implementation

Period

Initial

Negotiating

Right (INR)

Other Duties

and Charges

Other Terms and

Conditions

Ad valorem

(%)

Other U/B Ad valorem

(%)

Other From To

1 2 3 4 5 6 7 8

03010 Live Fish:

0301.10.00 Ornamental fish $5/kg B 0.0 1995 2004 Member Z 5%

0301.90. Other live fish:

0301.93.00 - Carp 0.0 U 5.0 Member W & Member Y

$5/kg

(...)

4203 Articles of Apparel and Clothing Accessories, of Leather or of Composition Leather:

1995 2004

4203.10.00 Articles of apparel 50.0 U 38.0

4203.30.00 Belts and bandoliers 25.0 U 25.0

3305.30.00 - Hair lacquers

(...)

4805 Other Uncoated Paper and Paperboard, in Rolls or Sheets:

Concession annexed to the Marrakesh Protocol will be implemented on 01.01.2012

4805.30.00 Sulphite wrapping paper 30.0 or if lower $50/t

U 5.0

Table 1: Example of a Schedule of Concessions on Non-Agricultural Products

EXPLANATION:

Column 1 (Tariff Item Number) and Column 2 (Description of Products): reflect the tariff code and

product description used by the Member. Although there is no formal requirement to use a specific tariff

nomenclature, they often refer to the Harmonized System (HS) Nomenclature up to the six-digit level.

Members are free under the HS and the WTO to introduce national distinctions beyond those six-digit codes

(often referred to as "breakouts") for various purposes (see Module 3 - The Harmonized System).

Column 3 (Base Rate of Duty): records the base rate of duty to which the tariff cutting techniques/formulae

should be applied during trade negotiations. The base rates can be bound (B) or unbound (U) initially. During

the Uruguay Round Members defined the base rates for "other products" as follows: for those tariff lines

already bound, the base rates were defined as the existing bound MFN rates; for unbound tariff lines, the base

rates were defined as the MFN applied tariff rates during a reference period of time as agreed by the Members.

Column 4 (Bound Rate of Duty): records what is probably the most important outcome of tariff

negotiations. That is, the final bound tariff rates to be achieved at the end of the implementation period. The

Marrakesh Protocol to the GATT 1994 (paragraph 2) provided that the reductions agreed upon by each Member

in the Uruguay Round shall be implemented in five equal rate reductions, except as otherwise specified in a

Member's Schedule (see below – Column 5). According to the Marrakesh Protocol, the first such reduction had

to be made effective on the date of entry into force of the Agreement Establishing the WTO (1st January 1995)

and each successive reduction made effective on 1st January of each of the following years. The final rate had

to become effective no later than the date four years after the date of entry into force of the WTO Agreement

Establishing the WTO, except as was otherwise specified in that Member's Schedule.

Column 5 (Implementation Period): Members requiring a transitional period to implement the committed

tariff reductions normally indicate so in their Schedules of concessions. For Member X, Column 5 specifies the

year "from" and "to" in which the tariff reduction will take place (it refers to 1st January of the year

concerned). The tariff concession on "ornamental fish" made by Member X will be implemented in 10 equal

reductions, starting from the date of entry into force of the Agreement Establishing the WTO (1st January

1995). After the end of the designated implementation period (i.e. 1st January 2004), tariffs are not allowed

to be applied on "ornamental fish" beyond the levels specified in Column 4. The Schedules of some Members

replace this column by headnotes or footnotes which describe the implementation in more general terms.

Column 6 (Initial Negotiating Rights): indicates the Members holding initial negotiating rights (INRs). The

INRs are generally the result of bilateral negotiations between Members, but are sometimes not reflected in

Members' Schedules. Members holding INRs are entitled to participate in renegotiations with a Member

requesting for modification of its tariff concessions (i.e. increasing the bound tariff rates). In our example,

Country Z holds INRs with Country X on ''ornamental fish'', while Country W and Country Y hold INRs with

Country X on ''carp''. If Country X requests to modify the concessions made on "ornamental fish", it would be

required to engage in renegotiations with the Member(s) holding INRs on ornamental fish (in this case Country

Z) in accordance with Article XXVIII of the GATT 1994 (explained below).

Column 7 (Other Duties and Charges): specifies other duties or charges (ODCs) inscribed according to

Article II:1(b), second sentence, of the GATT 1994 and the "Understanding on the Interpretation of

Article II:1(b) of the GATT 1994". Other duties and charges may be imposed in addition to the ''ordinary

customs duty''. Other duties and charges levied and not recorded in Member's Schedules are inconsistent with

Article II:1(b) of the GATT 1994. In the example, Country X may apply an ODC up to 5% ad valorem on

''ornamental fish''. Country X is also allowed to impose a specific duty up to $5/kg on ''carp''.

10

Column 8 (Other Terms and Conditions): wherever necessary, clarifications or comments regarding the

scope of the concessions shall be included in the Schedule. Like in the case of the implementation period, the

Schedules of certain Members have recorded terms and conditions that apply on the concession through

footnotes and headnotes rather than through comments in a separate column.

Note

The Schedules of concessions resulting from the Doha Round of negotiations will use the Uruguay Round

formats although, the Doha Round Schedules will probably differ from the Uruguay Round Schedules. The

Uruguay Round formats required the same information, but used a smaller number of columns, leaving the

final details of the structure of some tables to each Member. For more information on Doha Schedules on

Goods, please refer to the document "(Draft) Doha Schedules on Goods: Guidelines for Preparation and

Procedures for Submissions prepared by the Secretariat" (JOB(06)/99/Rev.1). It should be noted that the

modalities regarding Doha Schedules of Concessions are still under negotiation.

Information on WTO Members' Schedules is available on each WTO Member country’s information page on

the WTO website. To have access to a Member's Schedule, go to the list of Members and click a country’s

name. http://www.wto.org/english/thewto_e/whatis_e/tif_e/org6_e.htm

II.B. CONSOLIDATED LOOSE-LEAF SCHEDULES

The practice since the GATT 1947 was that the changes in the Schedules resulting from rounds of negotiations

or from renegotiations was attached to protocols or other legal instruments. Thus, information on concessions

made by a GATT Contracting Party was spread out throughout several different legal instruments. Following

the conclusion of the Tokyo Round in 1979, it was decided that a single document should replace all earlier

Schedules and negotiating records with respect to each Contracting Party. 3 It was also decided that such

consolidated Schedules should be in a "loose-leaf" format, i.e. a flexible system which allows to keep the

Schedules updated as and when necessary through loose papers which are replaced as changes are introduced.

In 1996 a further decision regarding the establishment of consolidated loose-leaf Schedules was adopted in

order to provide the legal framework for such Schedules. 4

The 1996 Decision provides that the consolidated Schedules shall be binding instruments, replacing all previous

Schedules for all purposes relating to a Member's rights and obligations under the WTO, except with respect to

historical Initial Negotiating Rights (INRs). The consolidated Schedules therefore, shall contain all necessary

information in order to reflect the exact situation in respect of each tariff concession and commitment. These

Schedules mainly include the following:

WTO Member;

Schedule Number;

Pre-Uruguay Round Schedule;

3 GATT BISD 27S/22.

4 G/L/138.

11

Schedules annexed to the Marrakesh Protocol, Schedules annexed to Protocols of Accession (PA);

HS96 changes – recording the status of implementation of HS changes;

Rectifications/Modifications to schedules, if any;

Comments – mainly record the procedures used for the implementation of HS changes.

Although the 1996 Decision has not worked as originally envisaged (i.e. only a limited number of Members

submitted a loose-leave schedule), transparency has been considerably improved by the Consolidated Tariff

Schedule Database (CTS), which is maintained by the WTO Secretariat on an informal basis, without

implications as to the legal status of the information therein.

TO KNOW MORE...:

Secretariat keeps track of the different modifications to the Schedules in a document entitled "Situation of

Schedules of WTO Members" which is periodically updated and circulated under the G/MA/W/23/Rev

document symbol. This document is available in WTO Documents on-line: http://docsonline.wto.org.

See also: IDB/CTS Internet Analysis Facility: http://iaf.wto.org

II.C. AMENDMENTS TO WTO SCHEDULES 5

Schedules of concessions change from time to time for several reasons, the most important of which are:

the introduction of the Harmonized System and its subsequent amendments (explained below);

rectifications and modifications introduced to the Schedules for various reasons, including

modifications resulting from tariff renegotiations under Article XXVIII of the GATT 1994 (explained in

the next section of this Module).

II.C.1. HARMONIZED SYSTEM AND THE GATT/WTO SCHEDULES OF

CONCESSIONS 6

RECALL (MODULE 3):

Most tariff Schedules are based on the Harmonized System (HS) which is an international product

nomenclature for the description, classification and coding of goods developed by the World Customs

Organization (WCO). The HS was established through the "International Convention on the Harmonized

5 For more information, please refer to:

http://www.wto.org/english/tratop_e/schedules_e/goods_schedules_table_e.htm

6 See also: Yu, Dayong, The Harmonized System – Amendments and their Impact on WTO Members

Schedules, WTO Staff Working Paper ESRD-2008-02.

12

Commodity Description and Coding System" (hereinafter the HS Convention), which entered into force on

1 January 1988.

There is no obligation under the WTO for Members to adopt the HS or to implement subsequent changes

in their Schedules of concessions. However, as of January 2009, there were 118 WTO Members which

were contracting parties to the HS Convention and, in practice, most WTO Members have used the HS to

describe the concessions in their corresponding Schedule. The HS has also been referred to in

multilateral agreements (such as the Agreement on Agriculture and the Agreement on Textiles and

Clothing) and in plurilateral agreements (Agreement on Trade in Civil Aircraft, the Information Technology

Agreement, etc.).

The HS is administered by the WCO and is subject to periodic review by the HS Committee of the WCO.

As of 2009, it has been amended four times - in 1992, 1996, 2002 and 2007, respectively. The purpose

for the periodical review and amendments is to take into account changes in technology and patterns in

international trade.

As explained in Module 3, GATT Contracting Parties used different nomenclatures to schedule their concessions

before the introduction of the HS, such as the Brussels Tariff Nomenclature (BTN) and later the Customs

Cooperation Council Nomenclature (CCCN). The lack of consistency in product classifications posed difficulties

for conducting tariff negotiations and monitoring the implementation of concessions.

Following the adoption of the HS by the Customs Co-operation Council in June 1983, Contracting Parties to the

GATT decided to introduce the HS in the Schedules of concessions of those Contracting Parties to the GATT

which were also contracting parties to the HS Convention. It was understood that the adoption of the HS

would ensure greater ability for countries to monitor and protect the value of tariff concessions. A Decision

adopted by the Contracting Parties in July 1983 laid down the main principles and procedures in connection

with the introduction of the HS in national tariffs and Schedules of concessions, where the main principle to be

observed was that the existing GATT bindings should be maintained unchanged. 7 Renegotiations under

Article XXVIII of the GATT 1994 were envisaged for those cases where, as a result of the introduction of the

HS, Members had to change their tariff bindings. 8

Following the entry into force of the HS on 1 January 1988, a certain number of pre-UR Schedules were

transposed following the above mentioned procedures. Some Contracting Parties undertook to negotiate their

Schedules in connection with the implementation of the HS. 9

II.C.2. INTRODUCTION OF THE HS AMENDMENTS INTO THE SCHEDULES

OF CONCESSIONS

Following the introduction of the HS into their Schedules of concessions, the GATT Contracting Parties and later

the WTO Members have taken actions to reflect each HS amendment into their Schedules with a view to

7 See L/5470/Rev.1.

8 Yu, Dayong, (see footnote 2), pages 8-9.

9 Yu, Dayong, (see footnote 2), pages 8-9.

13

keeping the authentic texts of their Schedules of tariff concessions up–to-date and in conformity with their

national tariffs. This is important because it would otherwise be very difficult for traders and other Members to

compare the duty being charged by the Member in practice with the corresponding concession in its WTO

Schedule.

For this purpose, the Committee on Tariff Concessions of the GATT adopted a simplified procedure to

implement the HS1992 amendment and any future changes relating to the HS. 10

Eleven GATT Contracting

Parties followed these procedures and submitted the required documentation. 11

Members made use of the same procedures for introducing modifications resulting from HS1996 amendments.

A total of 49 Members submitted HS1996 documentation, out of which 29 were full loose-leaf Schedules, 12

19

included only the HS1996 changes and 1 included information on a preliminary basis. 13

Since a large number

of Schedules had not being transposed, the General Council adopted in 2009 procedures for the verification

and certification of HS1996 changes relating to the Schedules of 64 developing country Members which, at the

time of the adoption of such procedures, had not initiated the introduction of HS1996 amendments. 14

In 2001, the WTO General Council established new procedures for the introduction of HS2002 amendments in

the Schedule of concessions. 15

Although the HS2002 is being currently applied by most WTO Members, only

some of them submitted the documentation required by these procedures. 16

Since the "do-it-yourself"

approach was not delivering results in a timely and efficient manner, Members decided to amend the HS2002

procedures by asking the Secretariat to undertake most of the technical work. These procedures will be

explained in detail in the following section.

II.C.3. NEW PROCEDURES FOR THE TRANSPOSITION OF THE HS2002 AND

HS2007 AMENDMENTS 17

The General Council adopted on 15 February 2005 amendments to the procedures in which the CTS database

(explained below) would be used as a working tool to introduce the changes in the Schedules resulting from

the HS2002 amendments. Furthermore, the WTO Secretariat was instructed to transpose the Schedules of

10 Decision of 8 October 1991, Annex to L/6905

11 GATT docs. Let/1793, TAR/M/34 and 35.

12 Decision of 29 November 1996, G/L/138.

13 G/MA/TAR/2/REV.37.

14 WT/L/756.

15 WT/L/407

16 G/MA/TAR/4/REV.8.

17 ''Yu, Dayong, ''The Harmonized System – Amendments and Their Impact on WTO Members' Schedules'',

WTO Staff Working Paper ESRD-2008-02''.

14

concessions of all developing countries, in consultation with the respective Member, 18

which represented a

significant departure from the previous approach, where Members prepared and reviewed the documentation

by themselves.

According to the new procedures, the Secretariat would transpose Members' commitments included in the CTS

database to the HS2002 nomenclature following a standard methodology. The Members concerned are given a

certain period of time to review the Secretariat's work and to provide comments. The files, including possible

modifications by the Members, are then submitted to a process of multilateral review by all other Members.

Developed Members are expected to prepare their own HS2002 files, which are also reviewed by the

Secretariat before they are presented for multilateral review. If there are no objections to the files with the

draft changes at the multilateral review sessions, then the files are considered approved and the HS2002

changes are circulated under the 1980 Procedures for Modification and Rectification of Schedules. 19

These

amendments are formally certified by the Director-General if no reservations are raised by other Members after

a three-month period of time. 20

The new procedure has proved to be very effective, in particular in ensuring that the concessions of all

Members are transposed in a timely and efficient manner. In light of the success of the new procedure for

HS2002, the General Council adopted very similar procedures for the transposition of the HS2007 related

amendments. 21

The Secretariat prepares periodically a report which provides the status of the HS2002 files.

22 As of March 2009, 115 Schedules have been transposed by the WTO Secretariat and 29 of them have been

certified. 23

EXERCISES:

1. What is a WTO Member's Schedule of tariff concessions?

2. List the main information contained in a Schedule.

3. Why is the transposition of concessions to reflect HS amendments important? Explain briefly this

procedure.

18 Decision of 15 February 2005, WT/L/605.

19 G/MA/TAR/RS/ document symbol series.

20 Yu, Dayong, (see footnote 2), pages 9-11.

21 WT/L/673.

22 See JOB(06)/8/ document symbol.

23 As of March 2009, the transposition of 3 Members was pending. It is worth noting that no transposition was

required for seven Members whose Schedules were already in HS2002 nomenclature.

15

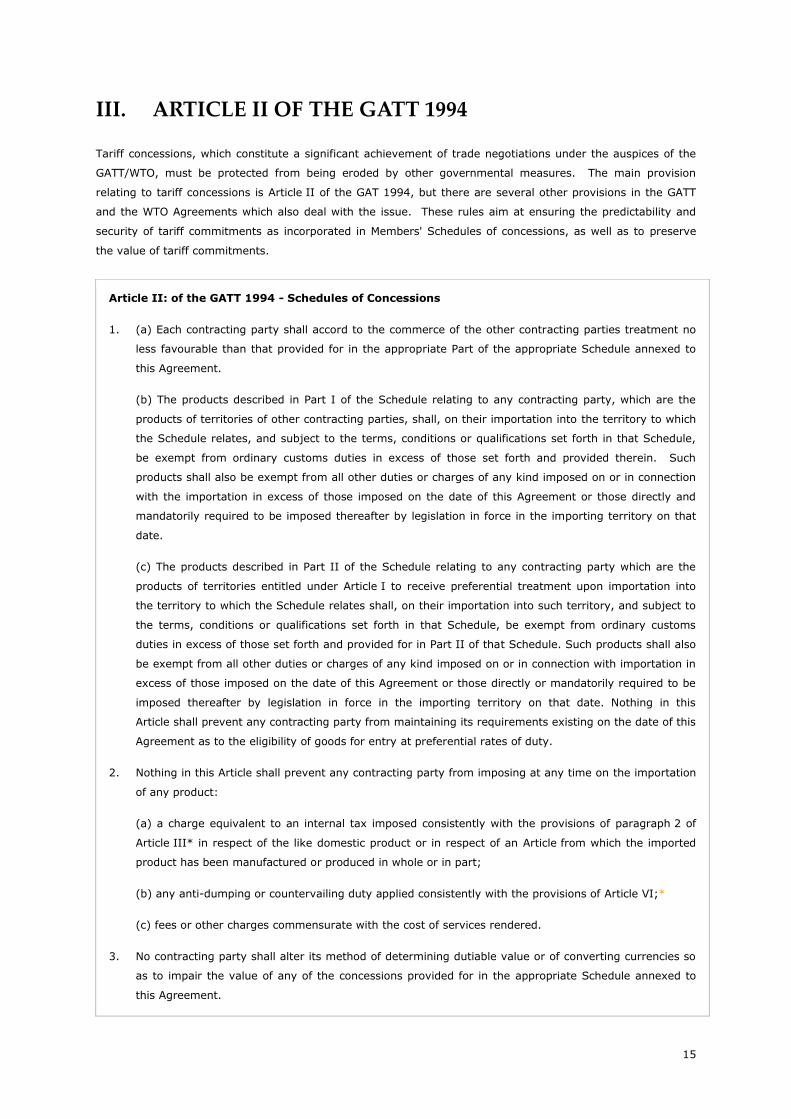

III. ARTICLE II OF THE GATT 1994

Tariff concessions, which constitute a significant achievement of trade negotiations under the auspices of the

GATT/WTO, must be protected from being eroded by other governmental measures. The main provision

relating to tariff concessions is Article II of the GAT 1994, but there are several other provisions in the GATT

and the WTO Agreements which also deal with the issue. These rules aim at ensuring the predictability and

security of tariff commitments as incorporated in Members' Schedules of concessions, as well as to preserve

the value of tariff commitments.

Article II: of the GATT 1994 - Schedules of Concessions

1. (a) Each contracting party shall accord to the commerce of the other contracting parties treatment no

less favourable than that provided for in the appropriate Part of the appropriate Schedule annexed to

this Agreement.

(b) The products described in Part I of the Schedule relating to any contracting party, which are the

products of territories of other contracting parties, shall, on their importation into the territory to which

the Schedule relates, and subject to the terms, conditions or qualifications set forth in that Schedule,

be exempt from ordinary customs duties in excess of those set forth and provided therein. Such

products shall also be exempt from all other duties or charges of any kind imposed on or in connection

with the importation in excess of those imposed on the date of this Agreement or those directly and

mandatorily required to be imposed thereafter by legislation in force in the importing territory on that

date.

(c) The products described in Part II of the Schedule relating to any contracting party which are the

products of territories entitled under Article I to receive preferential treatment upon importation into

the territory to which the Schedule relates shall, on their importation into such territory, and subject to

the terms, conditions or qualifications set forth in that Schedule, be exempt from ordinary customs

duties in excess of those set forth and provided for in Part II of that Schedule. Such products shall also

be exempt from all other duties or charges of any kind imposed on or in connection with importation in

excess of those imposed on the date of this Agreement or those directly or mandatorily required to be

imposed thereafter by legislation in force in the importing territory on that date. Nothing in this

Article shall prevent any contracting party from maintaining its requirements existing on the date of this

Agreement as to the eligibility of goods for entry at preferential rates of duty.

2. Nothing in this Article shall prevent any contracting party from imposing at any time on the importation

of any product:

(a) a charge equivalent to an internal tax imposed consistently with the provisions of paragraph 2 of

Article III* in respect of the like domestic product or in respect of an Article from which the imported

product has been manufactured or produced in whole or in part;

(b) any anti-dumping or countervailing duty applied consistently with the provisions of Article VI;*

(c) fees or other charges commensurate with the cost of services rendered.

3. No contracting party shall alter its method of determining dutiable value or of converting currencies so

as to impair the value of any of the concessions provided for in the appropriate Schedule annexed to

this Agreement.

16

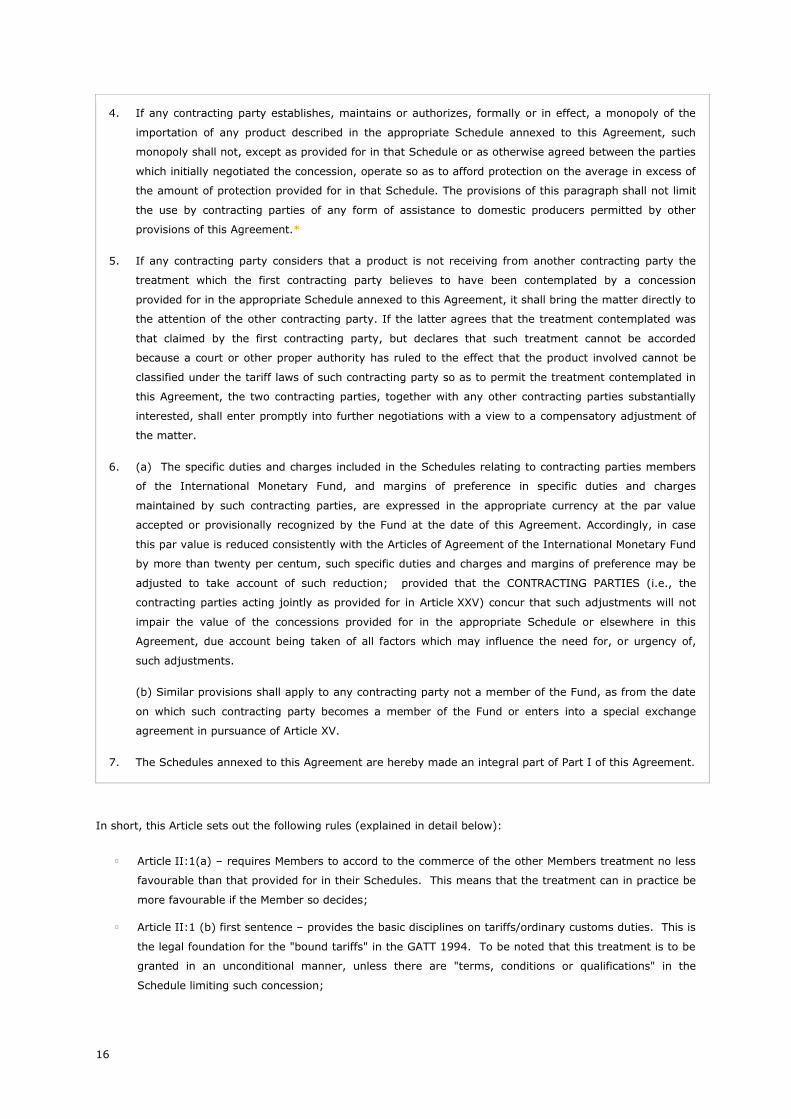

4. If any contracting party establishes, maintains or authorizes, formally or in effect, a monopoly of the

importation of any product described in the appropriate Schedule annexed to this Agreement, such

monopoly shall not, except as provided for in that Schedule or as otherwise agreed between the parties

which initially negotiated the concession, operate so as to afford protection on the average in excess of

the amount of protection provided for in that Schedule. The provisions of this paragraph shall not limit

the use by contracting parties of any form of assistance to domestic producers permitted by other

provisions of this Agreement.*

5. If any contracting party considers that a product is not receiving from another contracting party the

treatment which the first contracting party believes to have been contemplated by a concession

provided for in the appropriate Schedule annexed to this Agreement, it shall bring the matter directly to

the attention of the other contracting party. If the latter agrees that the treatment contemplated was

that claimed by the first contracting party, but declares that such treatment cannot be accorded

because a court or other proper authority has ruled to the effect that the product involved cannot be

classified under the tariff laws of such contracting party so as to permit the treatment contemplated in

this Agreement, the two contracting parties, together with any other contracting parties substantially

interested, shall enter promptly into further negotiations with a view to a compensatory adjustment of

the matter.

6. (a) The specific duties and charges included in the Schedules relating to contracting parties members

of the International Monetary Fund, and margins of preference in specific duties and charges

maintained by such contracting parties, are expressed in the appropriate currency at the par value

accepted or provisionally recognized by the Fund at the date of this Agreement. Accordingly, in case

this par value is reduced consistently with the Articles of Agreement of the International Monetary Fund

by more than twenty per centum, such specific duties and charges and margins of preference may be

adjusted to take account of such reduction; provided that the CONTRACTING PARTIES (i.e., the

contracting parties acting jointly as provided for in Article XXV) concur that such adjustments will not

impair the value of the concessions provided for in the appropriate Schedule or elsewhere in this

Agreement, due account being taken of all factors which may influence the need for, or urgency of,

such adjustments.

(b) Similar provisions shall apply to any contracting party not a member of the Fund, as from the date

on which such contracting party becomes a member of the Fund or enters into a special exchange

agreement in pursuance of Article XV.

7. The Schedules annexed to this Agreement are hereby made an integral part of Part I of this Agreement.

In short, this Article sets out the following rules (explained in detail below):

Article II:1(a) – requires Members to accord to the commerce of the other Members treatment no less

favourable than that provided for in their Schedules. This means that the treatment can in practice be

more favourable if the Member so decides;

Article II:1 (b) first sentence – provides the basic disciplines on tariffs/ordinary customs duties. This is

the legal foundation for the "bound tariffs" in the GATT 1994. To be noted that this treatment is to be

granted in an unconditional manner, unless there are "terms, conditions or qualifications" in the

Schedule limiting such concession;

17

Article II:1 (b) second sentence – sets forth the basic disciplines on "other duties or charges" (ODCs) -

see also Module 3;

Article II:1 (c) –sets forth the rules applicable to products entitled to preferential treatment as provided

in Members' Schedules. This historical provision is not applicable anymore to the extent that

practically all Members have discontinued their historical Part II preferences;

Article II:2 – lists the charges and duties that are not covered by the disciplines in Article II and which

may be applied to products in excess of those provided in the Schedules (as long as the relevant

provisions are respected);

Article II:3 – prohibits Members from altering their methods of determining dutiable value or methods

of converting currencies so as to impair the value of tariff concessions. To be noted that the

determination of value for customs purposes is regulated by Article VII of GATT and the Agreement on

Customs Valuation;

Article II:4 – establishes disciplines for those cases in which imports into a certain Members are to take

place under a monopoly;

Article II:5 – lays down procedures to address a situation in which a member believes that the

treatment contemplated in a concession by another Member is not being provided;

Article II:6 – provides that currency revaluations should not undermine the value of tariff concessions

expressed in terms of specific duties, for which it makes reference to the rules of the International

Monetary Fund, which at the time were based on the "gold standard"; and,

Article II:7 - specifies the legal status of a Schedule as an integral part of the GATT 1994. Since the

GATT 1994 is an integral part of the WTO Agreement, it means that Schedules of concessions are also

an integral part of the WTO Agreement.

Besides Article II of the GATT 1994, the value of tariff concessions is also protected through other GATT

provisions and WTO Agreements regulating different "non-tariff" governmental measures on trade in goods.

These measures will be explained in detail in Module 5.

III.A. APPLICATION AND INTERPRETATION OF ARTICLE II:1(A)

OF THE GATT 1994

Article II:1(a) of the GATT 1994 requires Members to accord to the commerce of the other Members treatment

no less favourable than that provided for in their Schedules of concessions, i.e. to respect the commitments

they have assumed in their Schedules.

In Argentina-Textiles and Apparel, the Appellate Body stated that paragraph (a) of Article II:1 contains a

general prohibition against according treatment less favourable to imports than that provided for in a Member's

Schedule. Article II:1(b) refers to specific measures which could lead to the provision of less favourable

treatment. Therefore, according to the Appellate Body, any measure inconsistent with Article II:1(b) is

necessarily inconsistent with Article II:1(a) (Argentina-Textiles and Apparel, Appellate Body Report, para. 45).

18

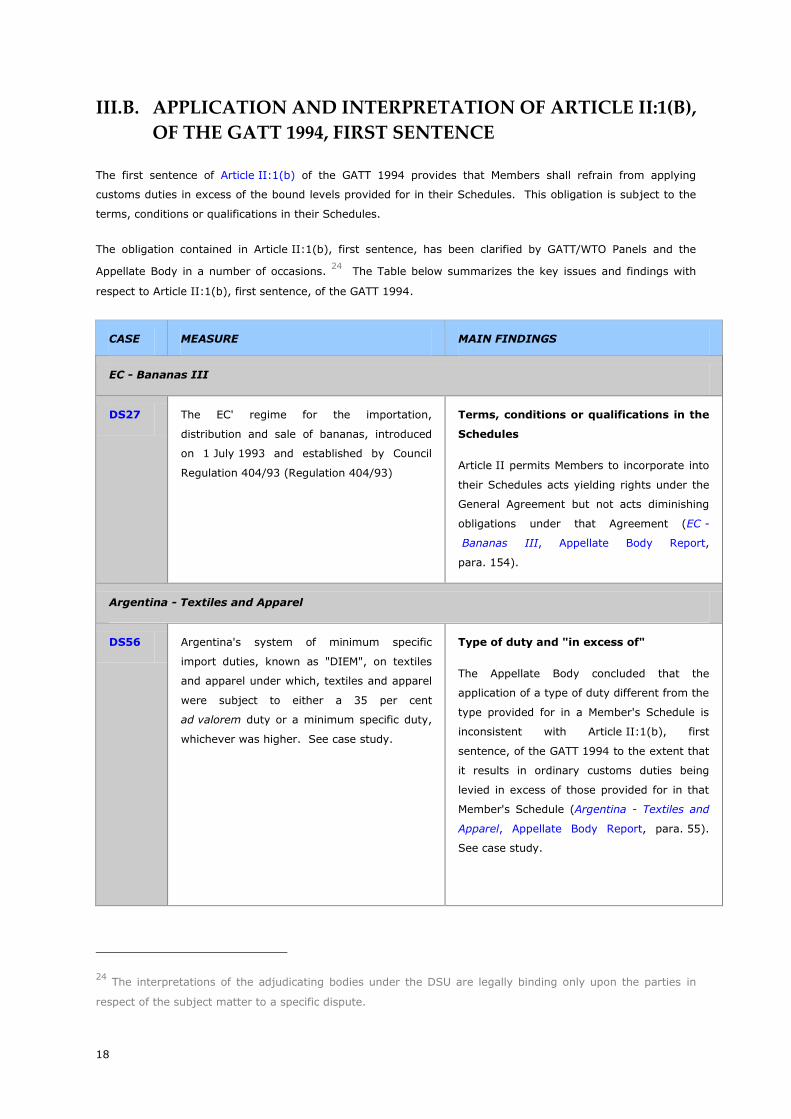

III.B. APPLICATION AND INTERPRETATION OF ARTICLE II:1(B),

OF THE GATT 1994, FIRST SENTENCE

The first sentence of Article II:1(b) of the GATT 1994 provides that Members shall refrain from applying

customs duties in excess of the bound levels provided for in their Schedules. This obligation is subject to the

terms, conditions or qualifications in their Schedules.

The obligation contained in Article II:1(b), first sentence, has been clarified by GATT/WTO Panels and the

Appellate Body in a number of occasions. 24

The Table below summarizes the key issues and findings with

respect to Article II:1(b), first sentence, of the GATT 1994.

CASE MEASURE MAIN FINDINGS

EC - Bananas III

DS27 The EC' regime for the importation,

distribution and sale of bananas, introduced

on 1 July 1993 and established by Council

Regulation 404/93 (Regulation 404/93)

Terms, conditions or qualifications in the

Schedules

Article II permits Members to incorporate into

their Schedules acts yielding rights under the

General Agreement but not acts diminishing

obligations under that Agreement (EC -

Bananas III, Appellate Body Report,

para. 154).

Argentina - Textiles and Apparel

DS56 Argentina's system of minimum specific

import duties, known as "DIEM", on textiles

and apparel under which, textiles and apparel

were subject to either a 35 per cent

ad valorem duty or a minimum specific duty,

whichever was higher. See case study.

Type of duty and "in excess of"

The Appellate Body concluded that the

application of a type of duty different from the

type provided for in a Member's Schedule is

inconsistent with Article II:1(b), first

sentence, of the GATT 1994 to the extent that

it results in ordinary customs duties being

levied in excess of those provided for in that

Member's Schedule (Argentina - Textiles and

Apparel, Appellate Body Report, para. 55).

See case study.

24 The interpretations of the adjudicating bodies under the DSU are legally binding only upon the parties in

respect of the subject matter to a specific dispute.

19

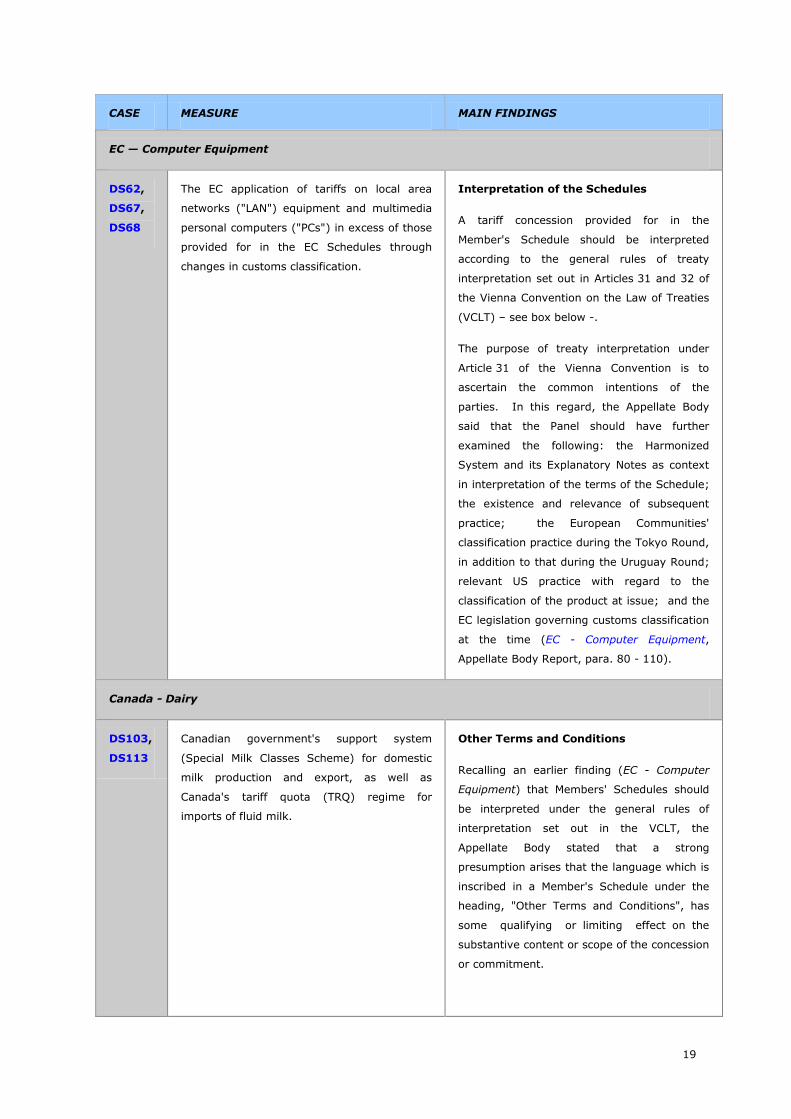

CASE MEASURE MAIN FINDINGS

EC — Computer Equipment

DS62,

DS67,

DS68

The EC application of tariffs on local area

networks ("LAN") equipment and multimedia

personal computers ("PCs") in excess of those

provided for in the EC Schedules through

changes in customs classification.

Interpretation of the Schedules

A tariff concession provided for in the

Member's Schedule should be interpreted

according to the general rules of treaty

interpretation set out in Articles 31 and 32 of

the Vienna Convention on the Law of Treaties

(VCLT) – see box below -.

The purpose of treaty interpretation under

Article 31 of the Vienna Convention is to

ascertain the common intentions of the

parties. In this regard, the Appellate Body

said that the Panel should have further

examined the following: the Harmonized

System and its Explanatory Notes as context

in interpretation of the terms of the Schedule;

the existence and relevance of subsequent

practice; the European Communities'

classification practice during the Tokyo Round,

in addition to that during the Uruguay Round;

relevant US practice with regard to the

classification of the product at issue; and the

EC legislation governing customs classification

at the time (EC - Computer Equipment,

Appellate Body Report, para. 80 - 110).

Canada - Dairy

DS103,

DS113

Canadian government's support system

(Special Milk Classes Scheme) for domestic

milk production and export, as well as

Canada's tariff quota (TRQ) regime for

imports of fluid milk.

Other Terms and Conditions

Recalling an earlier finding (EC - Computer

Equipment) that Members' Schedules should

be interpreted under the general rules of

interpretation set out in the VCLT, the

Appellate Body stated that a strong

presumption arises that the language which is

inscribed in a Member's Schedule under the

heading, "Other Terms and Conditions", has

some qualifying or limiting effect on the

substantive content or scope of the concession

or commitment.

20

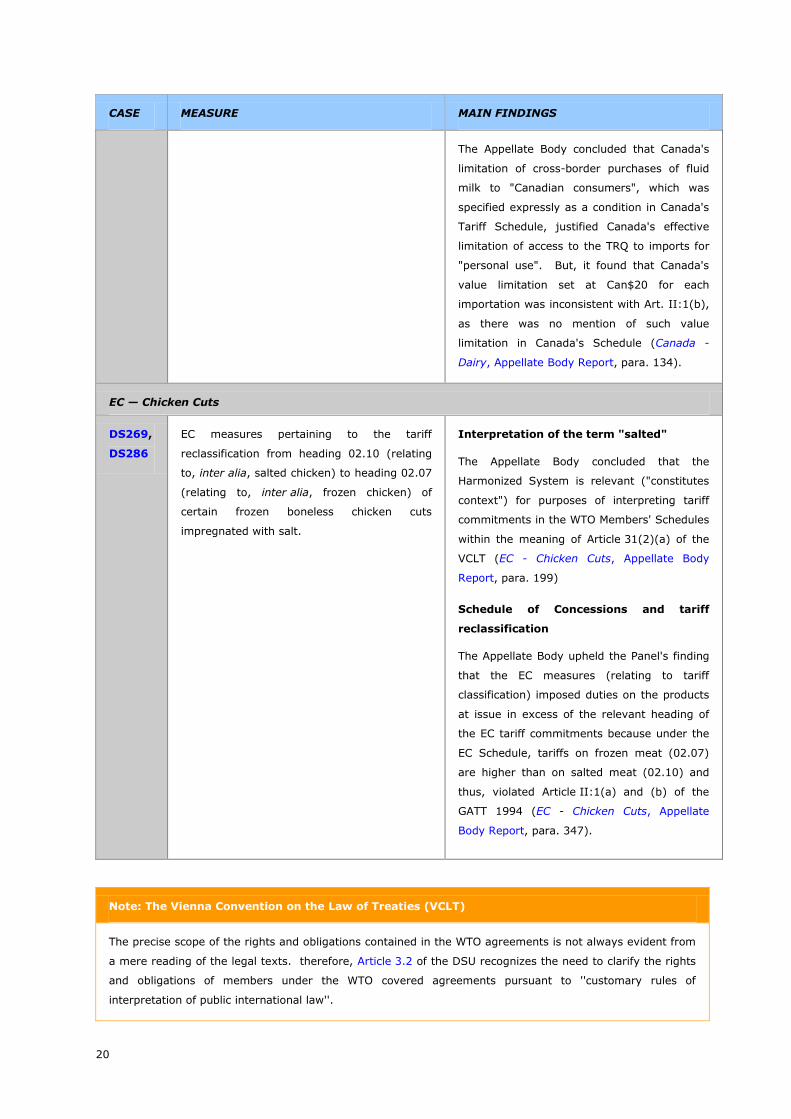

CASE MEASURE MAIN FINDINGS

The Appellate Body concluded that Canada's

limitation of cross-border purchases of fluid

milk to "Canadian consumers", which was

specified expressly as a condition in Canada's

Tariff Schedule, justified Canada's effective

limitation of access to the TRQ to imports for

"personal use". But, it found that Canada's

value limitation set at Can$20 for each

importation was inconsistent with Art. II:1(b),

as there was no mention of such value

limitation in Canada's Schedule (Canada -

Dairy, Appellate Body Report, para. 134).

EC — Chicken Cuts

DS269,

DS286

EC measures pertaining to the tariff

reclassification from heading 02.10 (relating

to, inter alia, salted chicken) to heading 02.07

(relating to, inter alia, frozen chicken) of

certain frozen boneless chicken cuts

impregnated with salt.

Interpretation of the term "salted"

The Appellate Body concluded that the

Harmonized System is relevant ("constitutes

context") for purposes of interpreting tariff

commitments in the WTO Members' Schedules

within the meaning of Article 31(2)(a) of the

VCLT (EC - Chicken Cuts, Appellate Body

Report, para. 199)

Schedule of Concessions and tariff

reclassification

The Appellate Body upheld the Panel's finding

that the EC measures (relating to tariff

classification) imposed duties on the products

at issue in excess of the relevant heading of

the EC tariff commitments because under the

EC Schedule, tariffs on frozen meat (02.07)

are higher than on salted meat (02.10) and

thus, violated Article II:1(a) and (b) of the

GATT 1994 (EC - Chicken Cuts, Appellate

Body Report, para. 347).

Note: The Vienna Convention on the Law of Treaties (VCLT)

The precise scope of the rights and obligations contained in the WTO agreements is not always evident from

a mere reading of the legal texts. therefore, Article 3.2 of the DSU recognizes the need to clarify the rights

and obligations of members under the WTO covered agreements pursuant to ''customary rules of

interpretation of public international law''.

21

Note: The Vienna Convention on the Law of Treaties (VCLT)

While customary international law is normally unwritten, the Vienna convention on the law of treaties (VCLT)

has codified in articles 31 and 32 some of these customary rules of treaty interpretation. although Article 3.2

of the DSU does not refer directly to such provisions, the appellate body has recognized their status of "rule

of customary or general international law" (US - Gasoline, p. 17; Japan - Alcoholic beverages II, pages 10-

12). WTO adjudicating bodies make frequent reference to these rules when interpreting provisions contained

in the covered agreements. these legal interpretations are legally binding only on the parties and in respect

of the subject matter of a specific dispute.

The text of the VCLT can be found at:

http://untreaty.un.org/ilc/texts/instruments/english/conventions/1_1_1969.pdf

TO KNOW MORE...

A more detailed description of the legal findings concerning the different provisions under Article II of the

GATT 1994 can be found in:

http://www.wto.org/english/res_e/booksp_e/analytic_index_e/gatt1994_02_e.htm#article2

III.C. OTHER DISCIPLINES AIMED AT PRESERVING THE VALUE

OF TARIFF CONCESSIONS CONTAINED IN ARTICLE II OF

THE GATT 1994

There are other provisions contained in Article II aimed at preserving the value of tariff concessions. For

example, Article II:1(b) second sentence allows Members to apply other duties and charges, in addition to

ordinary customs duties, subject to certain requirements. Article II:3 prohibits Members from altering their

methods of determining dutiable value or methods of converting currencies so as to impair the value of tariff

concessions, while Article II:6 provides that currency revaluations should not undermine the value of such

concessions.

III.C.1. OTHER DUTIES AND CHARGES (ODCS)

As has been explained before, the "bound rate" of duty in a Schedule of concessions represents the maximum

customs duty that WTO Members have committed to levy on imports from other Members. However, "ODCs"

may be imposed in addition to the "ordinary customs duty" if provided and within the levels indicated in a

Member's Schedule.

ODCs are regulated by the second sentence of Article II:1(b) and the Understanding on the Interpretation of

Article II.1(b). Some examples of ODCs include "temporary import surcharges", "revenue taxes" and charges

imposed by import monopolies (see also Article II:4 below). Article II:1(b) second sentence stipulates that

imported products shall be exempt from "all other duties or charges of any kind" that are imposed "on or in

connection with" importation, to the extent that such duties or charges exceed amounts imposed on the date

22

of entry into force of the GATT 1994 (or which are directly and mandatorily required to be imposed by

legislation in force on that date), as recorded and bound in the Schedules of concessions annexed to the GATT

1994. In this way, the second sentence of Article II:1(b) helps to prevent tariff concessions from being

circumvented.

However, unlike tariffs, there were no legal instruments which recorded ODCs that a Contracting Party to the

GATT 1947 was allowed to apply before the Uruguay Round. This led to a lack of transparency and difficulties

in retrieving data. The Understanding on the Interpretation of Article II:1 (b) of GATT 1994, negotiated during

the Uruguay Round, is aimed at obtaining greater transparency in the use of ODCs. This Understanding, which

is legally part of the GATT 1994, provides that the date as of which "other duties or charges" are bound, for the

purpose of Article II, shall be 5 April 1994. "Other duties or charges" had to be recorded in the Schedule at the

levels applicable on that date. In case of renegotiation of a concession or negotiation of new concessions, the

applicable date for the tariff item in question shall become the date of the incorporation of the new or revised

concessions into the Schedule. If ODCs were not recorded in a Member's Schedule but are nevertheless levied,

they are inconsistent with Article II:1 (b).

Members had three years – until 15 April 1997 – originally, and then three years after any subsequent

renegotiation, to challenge the level of ODCs recorded against any tariff item if they considered that the level

was greater than applied at the date of first incorporation in the WTO Schedules. The recording of an ODC in a

Member's Schedule is without prejudice to its consistency with the rights and obligations of the Members under

the GATT 1994. All Members retain the right to challenge, at any time, the consistency of other ODC with such

obligations (Understanding on the Interpretation of Article II:1 (b) of GATT 1994, paragraph 5).

III.C.2. OTHER PROVISIONS AIMED AT PRESERVING THE VALUE OF

TARIFF CONCESSIONS CONTAINED IN ARTICLE II OF THE GATT

1994 (BESIDES ODCS)

As mentioned above, there are some other provisions under Article II of the GATT 1994 aimed at protecting

the value of tariff concessions by targeting other governmental measures. These include:

Article II:3 of the GATT 1994 – prevents Members from altering their method of determining dutiable

value or converting currencies so as to impair the value of any of the concessions provided for in the

Schedule. For import tariffs calculated on an ad valorem basis, the customs values of imports are

crucial, as they determine the final applicable tariff rates. The benefit of binding could otherwise be

eliminated or circumvented by an arbitrary of unfair valuation. Customs procedures applied to

determine the customs value of imported goods are normally referred to as ''customs valuation''.

Under the WTO, customs valuation is regulated by Article VII of the GATT 1994 and the Agreement on

Customs Valuation, which will be studied in Module 5.

Article II:4 of the GATT 1994 – prevents the operation of import monopolies from frustrating the

Scheduled tariff concessions. This provision relates to Article XVII on State Trading Enterprises (STEs)

–i.e. governmental and non-governmental enterprises which have been granted exclusive or special

rights or privileges in the exercise of which they influence through their purchases or sales the level or

23

direction of imports or exports. 25

State-designated trading enterprises that are given import

monopoly powers may affect the value of a binding in a number of ways, particularly by adding a

"mark-up" to import prices. Article II:4 applies to import monopolies whether or not they are STEs.

Article II:5 of the GATT 1994 – reclassification of goods within a tariff may effectively remove the

benefit of a tariff binding. In this regard, Article II:5 provides for compensatory adjustment between

Members in situations where a Member's rights are affected by another Member's reclassification of

bound duties; and,

Article II:6 of the GATT 1994 – is a provision on exchange rates for the calculation of specific duties. It

was aimed at protecting tariff concessions from being undermined by currency revaluation. This

provision relates to the regime of fixed exchange rates that existed during the first three decades of the

GATT 1947. 26

III.D. TAXES AND CHARGES NOT SUBJECT TO THE RULES ON

TARIFF CONCESSIONS

At the same time that Article II of the GATT 1994 provides disciplines on tariffs and ODCs, it explicitly

enumerates a number of levies on imports which are not subject to the rules on tariff bindings. In this respect,

Article II:2 of the GATT 1994 provides that nothing therein shall prevent any Member from imposing at any

time on the importation of any product the following charges:

Internal taxes imposed consistently with Article III:2 of the GATT 1994 - tariffs are different from

internal taxes or charges. An internal tax may however, be applied at the border on imported goods

(see Ad note to Article III). They are subject to the national treatment embodied in Article III of the

GATT which prohibits a Member from utilising internal regulations to favour its domestic products over

the imported products of other WTO Members;

Anti-dumping or countervailing duties applied consistently with Article VI of the GATT 1994 – anti-

dumping and countervailing measures take the form of customs duties, which may be levied in excess

of the bound tariff rates provided in the Schedule of concessions of the Member applying the measure.

They are permitted under the WTO provided that their application meets the conditions laid down in

Article VI of the GATT and the Agreement on Anti-Dumping or the Agreement on Subsidies and

Countervailing Measures, depending on the case. These measures are applied as a deviation from the

general rules on bound concessions (See Module 2);

''Fees'' or ''charges'' commensurate with the cost of services rendered - ''fees'' or ''charges'' associated

with an import service may be applied to imports, subject to certain conditions. Although they are not

tariffs or ODCs, such ''fees'' or ''charges'', if applied arbitrarily and unjustifiably, may increase the costs

of transactions for importers and exporters and consequently, impede market access in the form of

non-tariff barriers. Thus, Article VIII of the GATT 1994 requires them to be limited in amount to the

25 See paragraph 2 of the "Understanding on the Interpretation of Article XVII of GATT 1994". It is worth

noting that an enterprise need not to be owned by the state to be designed as a STE.

26 In this regard, it should be noted that the WTO does not deal with issues relating to monetary policies and

exchange rates.

24

approximate cost of services rendered and not to represent an indirect protection to domestic products

or a taxation of imports or exports for fiscal purposes. You will study customs fees and formalities in

Module 5, which explains NTMs.

EXERCISES:

4. According to Article II:1, first sentence, of the GATT 1994, what are the basic disciplines on tariffs

concessions under the WTO?

5. What does Article II:1(b) second sentence provides with respect to "other duties and charges" (ODCs)?

6. Are all border charges imposed on imports subject to the disciplines on bound concessions?

25

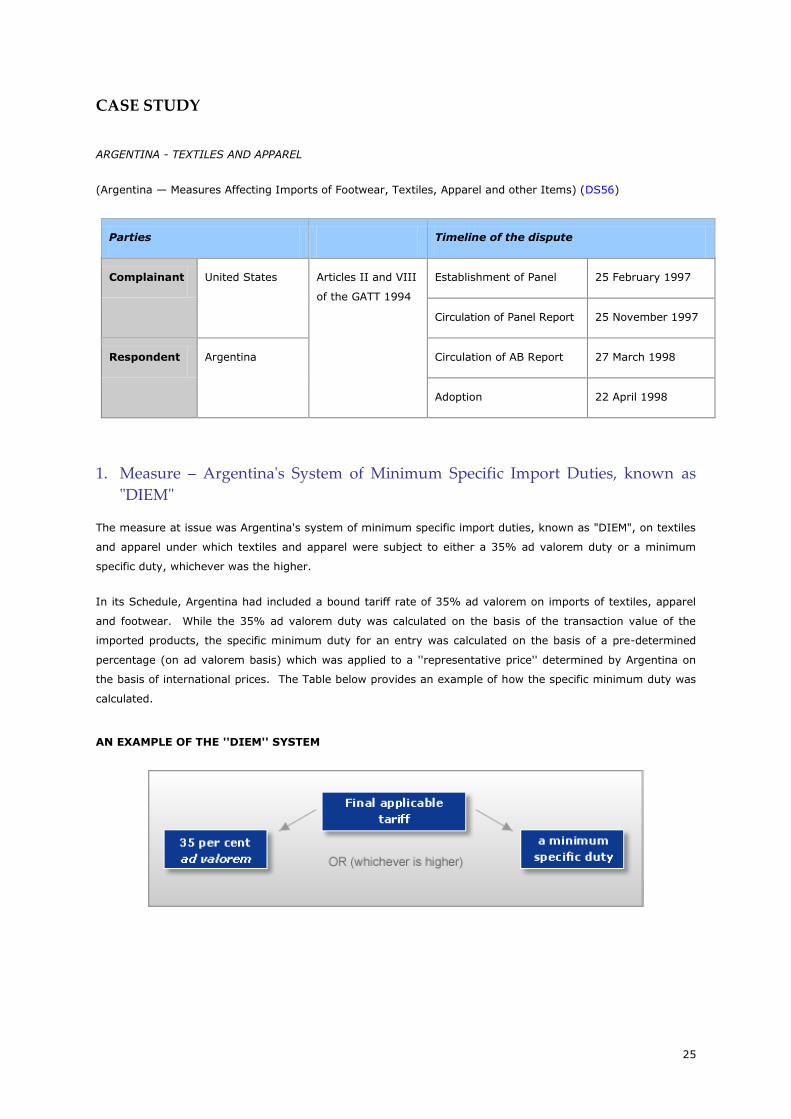

CASE STUDY

ARGENTINA - TEXTILES AND APPAREL

(Argentina — Measures Affecting Imports of Footwear, Textiles, Apparel and other Items) (DS56)

Parties Timeline of the dispute

Complainant United States Articles II and VIII

of the GATT 1994

Establishment of Panel 25 February 1997

Circulation of Panel Report 25 November 1997

Respondent Argentina Circulation of AB Report 27 March 1998

Adoption 22 April 1998

1. Measure – Argentina's System of Minimum Specific Import Duties, known as

"DIEM"

The measure at issue was Argentina's system of minimum specific import duties, known as "DIEM", on textiles

and apparel under which textiles and apparel were subject to either a 35% ad valorem duty or a minimum

specific duty, whichever was the higher.

In its Schedule, Argentina had included a bound tariff rate of 35% ad valorem on imports of textiles, apparel

and footwear. While the 35% ad valorem duty was calculated on the basis of the transaction value of the

imported products, the specific minimum duty for an entry was calculated on the basis of a pre-determined

percentage (on ad valorem basis) which was applied to a ''representative price'' determined by Argentina on

the basis of international prices. The Table below provides an example of how the specific minimum duty was

calculated.

AN EXAMPLE OF THE ''DIEM'' SYSTEM

26

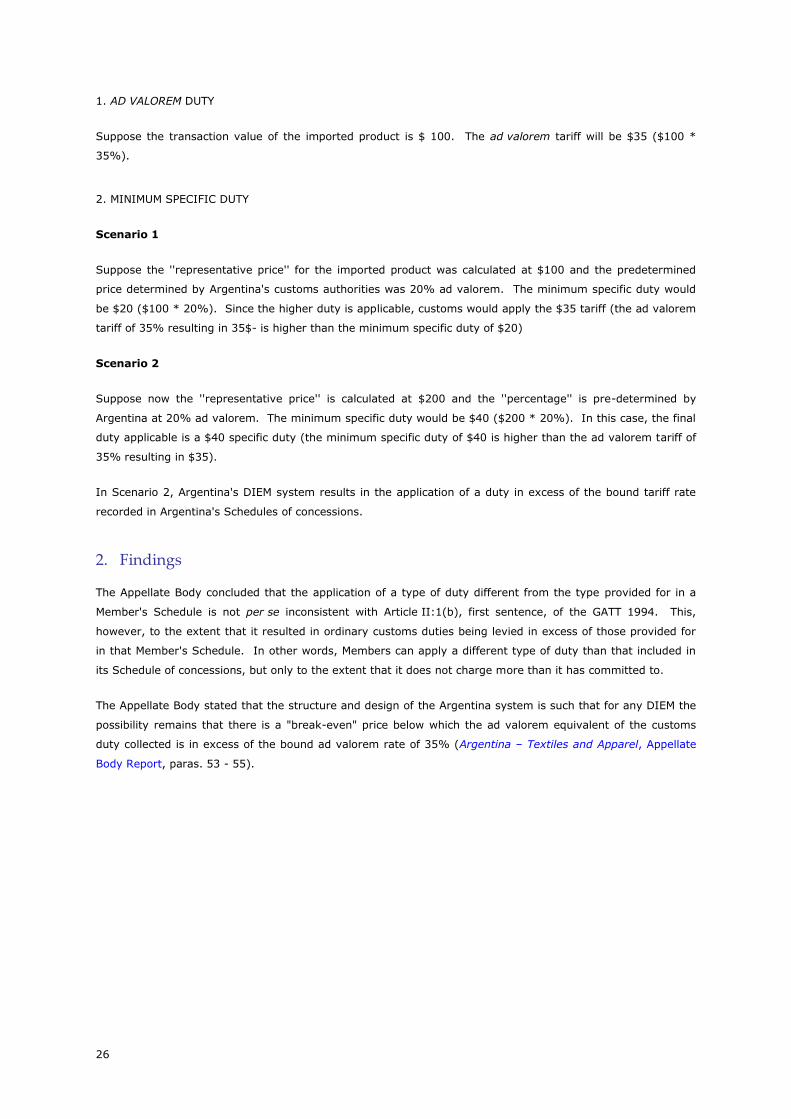

1. AD VALOREM DUTY

Suppose the transaction value of the imported product is $ 100. The ad valorem tariff will be $35 ($100 *

35%).

2. MINIMUM SPECIFIC DUTY

Scenario 1

Suppose the ''representative price'' for the imported product was calculated at $100 and the predetermined

price determined by Argentina's customs authorities was 20% ad valorem. The minimum specific duty would

be $20 ($100 * 20%). Since the higher duty is applicable, customs would apply the $35 tariff (the ad valorem

tariff of 35% resulting in 35$- is higher than the minimum specific duty of $20)

Scenario 2

Suppose now the ''representative price'' is calculated at $200 and the ''percentage'' is pre-determined by

Argentina at 20% ad valorem. The minimum specific duty would be $40 ($200 * 20%). In this case, the final

duty applicable is a $40 specific duty (the minimum specific duty of $40 is higher than the ad valorem tariff of

35% resulting in $35).

In Scenario 2, Argentina's DIEM system results in the application of a duty in excess of the bound tariff rate

recorded in Argentina's Schedules of concessions.

2. Findings

The Appellate Body concluded that the application of a type of duty different from the type provided for in a

Member's Schedule is not per se inconsistent with Article II:1(b), first sentence, of the GATT 1994. This,

however, to the extent that it resulted in ordinary customs duties being levied in excess of those provided for

in that Member's Schedule. In other words, Members can apply a different type of duty than that included in

its Schedule of concessions, but only to the extent that it does not charge more than it has committed to.

The Appellate Body stated that the structure and design of the Argentina system is such that for any DIEM the

possibility remains that there is a "break-even" price below which the ad valorem equivalent of the customs

duty collected is in excess of the bound ad valorem rate of 35% (Argentina – Textiles and Apparel, Appellate

Body Report, paras. 53 - 55).

27

IV. MODIFICATION OF THE SCHEDULES OF

CONCESSIONS

IN BRIEF

As studied in Module 3, modifications of tariff concessions usually take place during multilateral rounds of

trade negotiations (e.g. the Doha Round). Despite the fundamental importance of recording tariff

concessions resulting from such negotiations in a transparent and predictable manner, WTO Members are

allowed to modify or withdraw their tariff concessions subject to certain conditions. The possibility of

allowing for such modifications stems from the consideration that a negotiated tariff binding may become too

cumbersome to maintain at times due to changing circumstances. Thus, the possibility of having tariff

renegotiations introduce flexibility into the WTO system to allow Members to seek a lasting rebalancing of

concessions in such circumstances.

There are different provisions dealing with the modification or withdrawal of tariff concessions and other

concessions included in the Schedules. Many of these provisions allow a Member to renegotiate in order to

modify or withdraw tariff and non-tariff concessions on a permanent basis subject to stipulated

requirements, including compensation. The main provision in this respect is Article XXVIII of the GATT

1994, which allows a Member to enter into renegotiations in three different situations: 1) before the

initiation of a three-year period; 2) in "special circumstances", subject to the authorization of other

Members; or, 3) if the Member has reserved its right to do so before the initiation of the triennial period.

Other relevant provisions include Article XXIV:6 of the GATT 1994, which provides for the renegotiation of

tariff concessions in the context of the formation of a customs union, and Article XVIII:7 of the GATT 1994

which provides for renegotiations of concessions by developing countries for purposes of promoting the

establishment of a particular industry. In addition, Article XXVII of the GATT 1994 allows a Member to

withhold or withdraw a concession made during multilateral rounds of trade negotiations if the government

with which the concession was negotiated does not become or has ceased to be a WTO Member.

While the provisions mentioned above allow the permanent modification or withdrawal of a concession, a

Member can also suspend a tariff concession on a temporary basis, for instance, by requesting a waiver

under Article IX:3 of the Agreement Establishing the WTO –explained in Module 2.

Last but not least, one should distinguish the process of "modification" of tariff Schedules explained above

from the procedure of "rectification" of the Schedule (see box below). The latter is limited to changes of a

purely formal character that do not alter the scope of the concessions contained therein.

This section will focus on tariff renegotiations held under Article XXVIII of the GATT 1994.

28

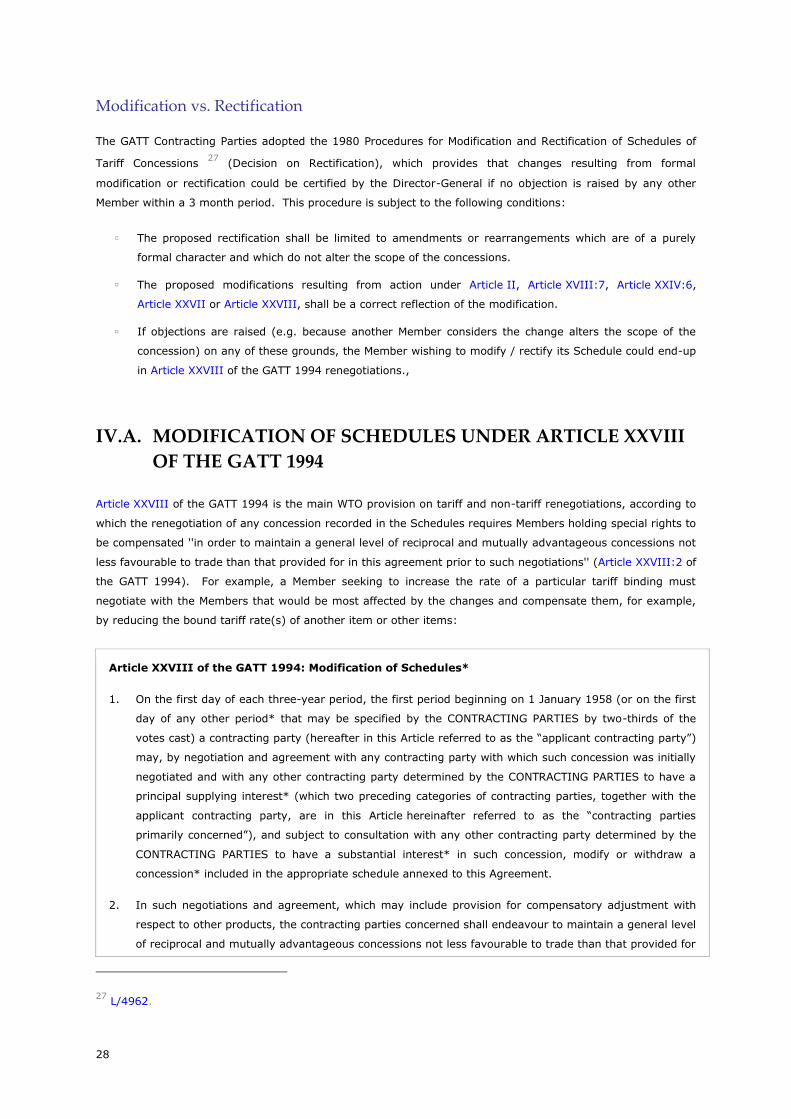

Modification vs. Rectification

The GATT Contracting Parties adopted the 1980 Procedures for Modification and Rectification of Schedules of

Tariff Concessions 27

(Decision on Rectification), which provides that changes resulting from formal

modification or rectification could be certified by the Director-General if no objection is raised by any other

Member within a 3 month period. This procedure is subject to the following conditions:

The proposed rectification shall be limited to amendments or rearrangements which are of a purely

formal character and which do not alter the scope of the concessions.

The proposed modifications resulting from action under Article II, Article XVIII:7, Article XXIV:6,

Article XXVII or Article XXVIII, shall be a correct reflection of the modification.

If objections are raised (e.g. because another Member considers the change alters the scope of the

concession) on any of these grounds, the Member wishing to modify / rectify its Schedule could end-up

in Article XXVIII of the GATT 1994 renegotiations.,

IV.A. MODIFICATION OF SCHEDULES UNDER ARTICLE XXVIII

OF THE GATT 1994

Article XXVIII of the GATT 1994 is the main WTO provision on tariff and non-tariff renegotiations, according to

which the renegotiation of any concession recorded in the Schedules requires Members holding special rights to

be compensated ''in order to maintain a general level of reciprocal and mutually advantageous concessions not

less favourable to trade than that provided for in this agreement prior to such negotiations'' (Article XXVIII:2 of

the GATT 1994). For example, a Member seeking to increase the rate of a particular tariff binding must

negotiate with the Members that would be most affected by the changes and compensate them, for example,

by reducing the bound tariff rate(s) of another item or other items:

Article XXVIII of the GATT 1994: Modification of Schedules*

1. On the first day of each three-year period, the first period beginning on 1 January 1958 (or on the first

day of any other period* that may be specified by the CONTRACTING PARTIES by two-thirds of the

votes cast) a contracting party (hereafter in this Article referred to as the ―applicant contracting party‖)

may, by negotiation and agreement with any contracting party with which such concession was initially

negotiated and with any other contracting party determined by the CONTRACTING PARTIES to have a

principal supplying interest* (which two preceding categories of contracting parties, together with the

applicant contracting party, are in this Article hereinafter referred to as the ―contracting parties

primarily concerned‖), and subject to consultation with any other contracting party determined by the

CONTRACTING PARTIES to have a substantial interest* in such concession, modify or withdraw a

concession* included in the appropriate schedule annexed to this Agreement.

2. In such negotiations and agreement, which may include provision for compensatory adjustment with

respect to other products, the contracting parties concerned shall endeavour to maintain a general level

of reciprocal and mutually advantageous concessions not less favourable to trade than that provided for

27 L/4962.

29

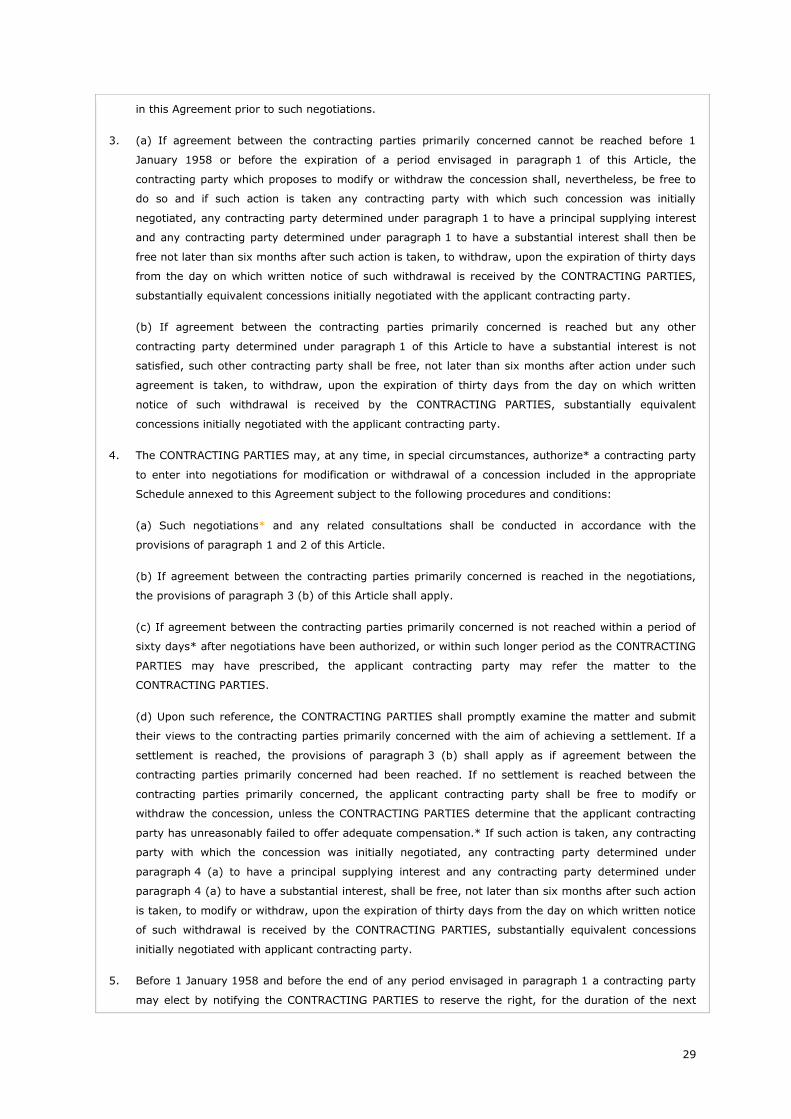

in this Agreement prior to such negotiations.

3. (a) If agreement between the contracting parties primarily concerned cannot be reached before 1

January 1958 or before the expiration of a period envisaged in paragraph 1 of this Article, the

contracting party which proposes to modify or withdraw the concession shall, nevertheless, be free to

do so and if such action is taken any contracting party with which such concession was initially

negotiated, any contracting party determined under paragraph 1 to have a principal supplying interest

and any contracting party determined under paragraph 1 to have a substantial interest shall then be

free not later than six months after such action is taken, to withdraw, upon the expiration of thirty days

from the day on which written notice of such withdrawal is received by the CONTRACTING PARTIES,

substantially equivalent concessions initially negotiated with the applicant contracting party.

(b) If agreement between the contracting parties primarily concerned is reached but any other

contracting party determined under paragraph 1 of this Article to have a substantial interest is not

satisfied, such other contracting party shall be free, not later than six months after action under such

agreement is taken, to withdraw, upon the expiration of thirty days from the day on which written

notice of such withdrawal is received by the CONTRACTING PARTIES, substantially equivalent

concessions initially negotiated with the applicant contracting party.

4. The CONTRACTING PARTIES may, at any time, in special circumstances, authorize* a contracting party

to enter into negotiations for modification or withdrawal of a concession included in the appropriate

Schedule annexed to this Agreement subject to the following procedures and conditions:

(a) Such negotiations* and any related consultations shall be conducted in accordance with the

provisions of paragraph 1 and 2 of this Article.

(b) If agreement between the contracting parties primarily concerned is reached in the negotiations,

the provisions of paragraph 3 (b) of this Article shall apply.

(c) If agreement between the contracting parties primarily concerned is not reached within a period of

sixty days* after negotiations have been authorized, or within such longer period as the CONTRACTING

PARTIES may have prescribed, the applicant contracting party may refer the matter to the

CONTRACTING PARTIES.

(d) Upon such reference, the CONTRACTING PARTIES shall promptly examine the matter and submit

their views to the contracting parties primarily concerned with the aim of achieving a settlement. If a

settlement is reached, the provisions of paragraph 3 (b) shall apply as if agreement between the

contracting parties primarily concerned had been reached. If no settlement is reached between the

contracting parties primarily concerned, the applicant contracting party shall be free to modify or

withdraw the concession, unless the CONTRACTING PARTIES determine that the applicant contracting

party has unreasonably failed to offer adequate compensation.* If such action is taken, any contracting

party with which the concession was initially negotiated, any contracting party determined under

paragraph 4 (a) to have a principal supplying interest and any contracting party determined under

paragraph 4 (a) to have a substantial interest, shall be free, not later than six months after such action

is taken, to modify or withdraw, upon the expiration of thirty days from the day on which written notice

of such withdrawal is received by the CONTRACTING PARTIES, substantially equivalent concessions

initially negotiated with applicant contracting party.

5. Before 1 January 1958 and before the end of any period envisaged in paragraph 1 a contracting party

may elect by notifying the CONTRACTING PARTIES to reserve the right, for the duration of the next

30

period, to modify the appropriate Schedule in accordance with the procedures of paragraph 1 to 3. If a

contracting party so elects, other contracting parties shall have the right, during the same period, to

modify or withdraw, in accordance with the same procedures, concessions initially negotiated with that

contracting party.

(*) See also Ad note to Article XXVIII of the GATT 1994.

Other WTO legal instruments applicable to renegotiations under Article XXVIII of the GATT 1994 include the

following:

Understanding on the Interpretation of Article XXVIII of the GATT 1994;

Procedures for Modification and Rectification of Schedules of Tariff, Decision adopted on 26 March 1980 28

; and,

Procedures for Negotiations under Article XXVIII, Guidelines adopted on 10- November 1980. 29

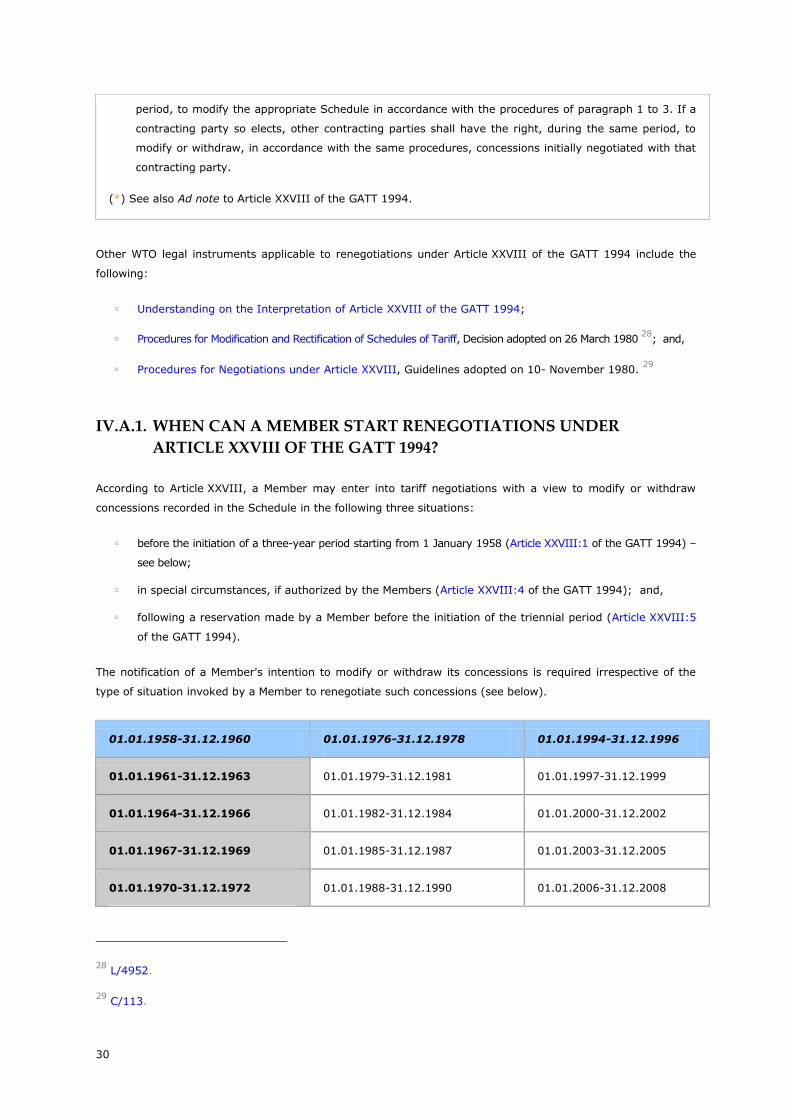

IV.A.1. WHEN CAN A MEMBER START RENEGOTIATIONS UNDER

ARTICLE XXVIII OF THE GATT 1994?

According to Article XXVIII, a Member may enter into tariff negotiations with a view to modify or withdraw

concessions recorded in the Schedule in the following three situations:

before the initiation of a three-year period starting from 1 January 1958 (Article XXVIII:1 of the GATT 1994) –

see below;

in special circumstances, if authorized by the Members (Article XXVIII:4 of the GATT 1994); and,

following a reservation made by a Member before the initiation of the triennial period (Article XXVIII:5

of the GATT 1994).

The notification of a Member's intention to modify or withdraw its concessions is required irrespective of the

type of situation invoked by a Member to renegotiate such concessions (see below).

01.01.1958-31.12.1960 01.01.1976-31.12.1978 01.01.1994-31.12.1996

01.01.1961-31.12.1963 01.01.1979-31.12.1981 01.01.1997-31.12.1999

01.01.1964-31.12.1966 01.01.1982-31.12.1984 01.01.2000-31.12.2002

01.01.1967-31.12.1969 01.01.1985-31.12.1987 01.01.2003-31.12.2005

01.01.1970-31.12.1972 01.01.1988-31.12.1990 01.01.2006-31.12.2008

28 L/4952.

29 C/113.

31

01.01.1973-31.12.1975 01.01.1991-31.12.1993 01.01.2009-31.12.2011

Table 2: Art.XXVIII Triennial-Period

When can a Member start Renegotiations under Article XXVIII of the GATT 1994?

Renegotiations before a

three-year period (para. 1)

Request for authorization: between 3 and 6 months before the

beginning of the triennial period. The Member shall notify the

intention of modification or withdrawal of tariff concessions*. The

negotiations shall be completed before the commencement of the

successive three-year period.

For example, for the three-year period commencing on 1 January

2009, the Member wishing to modify or withdraw any concession

should have notified other Members to this effect between 1 July 2008

and 30 September 2008. Negotiations should have been completed

by 31 December 2008 and the effect of the modification should take

place on 1 January 2009 (Ad Article XXVIII:1.3).

Renegotiations in special

circumstances (para. 4)

Request for authorization: at any time. The Member concerned shall

request the authorization from other Members by sending a

notification of its intention of modification or withdrawal of tariff

concessions*.

The renegotiation shall be completed within a 60-day period if such

negotiations involve only a single item or a very small group of items.

A longer period of time may be granted by Members if such

negotiations involve a larger number of items (Ad Article XXVIII: 4.3).

Renegotiations following a

reservation Member (para. 5)

Reservation of rights to modify tariffs: before the end of any three-

year period. The Member concerned shall reserve the rights for

renegotiation at any time before the end of any triennial period

through a notification*.

Negotiations may be completed at any time. In practice,

Article XXVIII:5 has gradually become the most frequently-invoked

provision for tariff renegotiations.

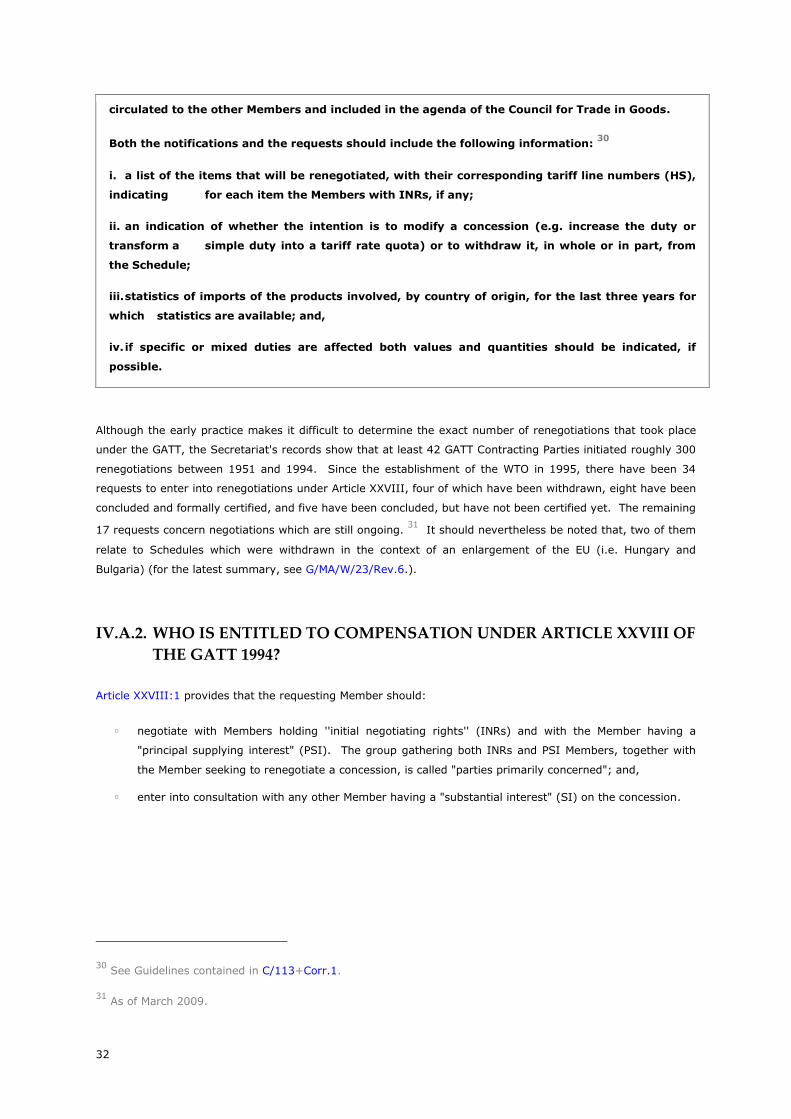

*Notification Requirements for Starting Tariff Renegotiations under Paragraphs 1, 4 and 5

Although the procedures for starting renegotiations under Article XXVIII differ according to the

paragraph under which they are undertaken, the three of them apply the same definitions and

are subject to the same substantive requirements. In terms of the procedures for starting

renegotiations under Article XXVIII, a Member entering into a renegotiation under paragraphs 1

or 5 of Article XXVIII must submit a notification, which will thereafter be circulated to all other

Members. A Member requesting permission to enter into a renegotiation under paragraph 4

must, on the other hand, submit a "request for authority to enter into negotiations" which is also

32

circulated to the other Members and included in the agenda of the Council for Trade in Goods.

Both the notifications and the requests should include the following information: 30

i. a list of the items that will be renegotiated, with their corresponding tariff line numbers (HS),

indicating for each item the Members with INRs, if any;

ii. an indication of whether the intention is to modify a concession (e.g. increase the duty or

transform a simple duty into a tariff rate quota) or to withdraw it, in whole or in part, from

the Schedule;

iii. statistics of imports of the products involved, by country of origin, for the last three years for

which statistics are available; and,

iv. if specific or mixed duties are affected both values and quantities should be indicated, if

possible.

Although the early practice makes it difficult to determine the exact number of renegotiations that took place

under the GATT, the Secretariat's records show that at least 42 GATT Contracting Parties initiated roughly 300

renegotiations between 1951 and 1994. Since the establishment of the WTO in 1995, there have been 34

requests to enter into renegotiations under Article XXVIII, four of which have been withdrawn, eight have been

concluded and formally certified, and five have been concluded, but have not been certified yet. The remaining

17 requests concern negotiations which are still ongoing. 31

It should nevertheless be noted that, two of them

relate to Schedules which were withdrawn in the context of an enlargement of the EU (i.e. Hungary and

Bulgaria) (for the latest summary, see G/MA/W/23/Rev.6.).

IV.A.2. WHO IS ENTITLED TO COMPENSATION UNDER ARTICLE XXVIII OF

THE GATT 1994?

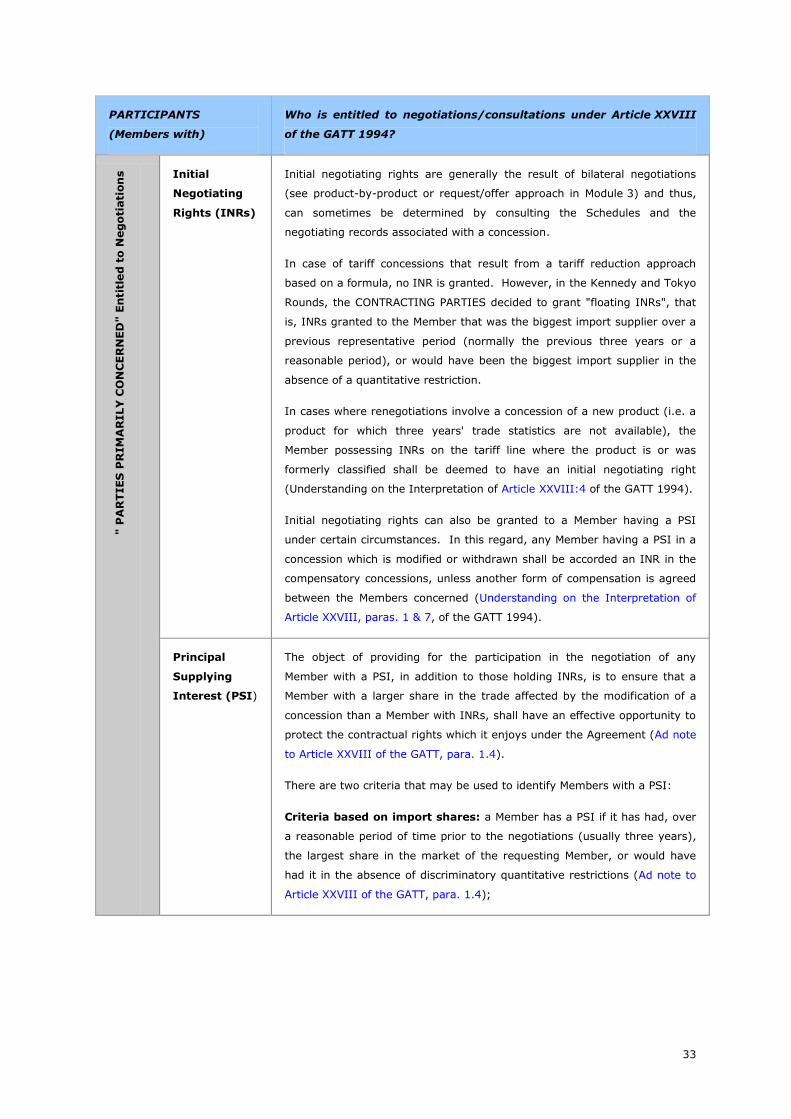

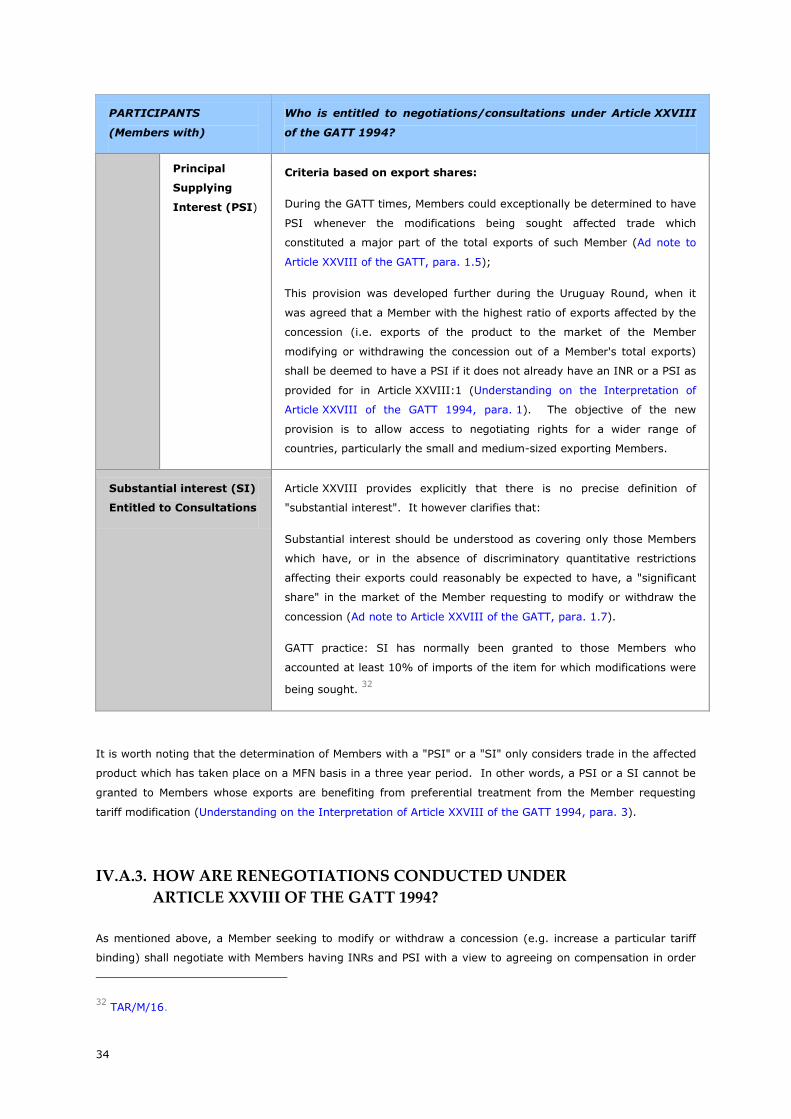

Article XXVIII:1 provides that the requesting Member should:

negotiate with Members holding ''initial negotiating rights'' (INRs) and with the Member having a

"principal supplying interest" (PSI). The group gathering both INRs and PSI Members, together with

the Member seeking to renegotiate a concession, is called "parties primarily concerned"; and,

enter into consultation with any other Member having a "substantial interest" (SI) on the concession.