Embed Size (px)

Citation preview

Lithuanian Private Equity and Venture Capital Market

Market Overview: 2016

LT VCA represents virtually every major player of the private equity and

venture capital industry in Lithuania and is dedicated to promoting the

private equity and venture capital industry for the benefit of funds, entrepre-

neurs, private equity and venture capital professionals and the economy as a

whole.

VC/PE market players in Lithuania create jobs, increases economic growth,

set the standards for more transparent business environment & creates

liquidity!

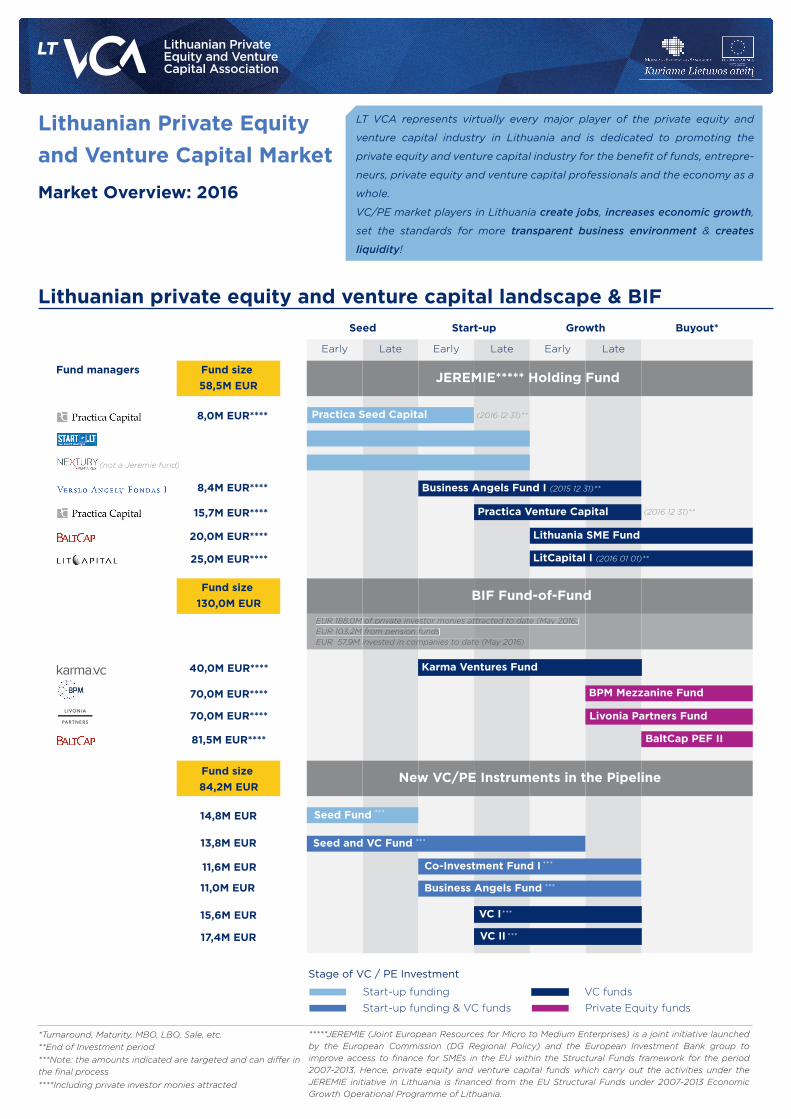

*****JEREMIE (Joint European Resources for Micro to Medium Enterprises) is a joint initiative launched by the European Commission (DG Regional Policy) and the European Investment Bank group to improve access to finance for SMEs in the EU within the Structural Funds framework for the period 2007-2013. Hence, private equity and venture capital funds which carry out the activities under the JEREMIE initiative in Lithuania is financed from the EU Structural Funds under 2007-2013 Economic Growth Operational Programme of Lithuania.

Lithuanian private equity and venture capital landscape & BIF

70,0M EUR****

70,0M EUR****

40,0M EUR****

Early Late Early Late Early Late

Seed Start-up Growth Buyout*

Stage of VC / PE Investment

Fund managers

**End of Investment period*Turnaround, Maturity, MBO, LBO, Sale, etc.

***Note: the amounts indicated are targeted and can di�er in the final process****Including private investor monies attracted

Lithuania SME Fund

LitCapital I (2016 01 01)**25,0M EUR****

20,0M EUR****

Start-up funding

Private Equity funds

VC funds

Start-up funding & VC funds

8,0M EUR**** Practica Seed Capital (2016 12 31)**

(not a Jeremie fund)

Karma Ventures Fund

Livonia Partners Fund

BPM Mezzanine Fund

VC I15,6M EUR

17,4M EUR

13,8M EUR

14,8M EUR

11,6M EUR Co-Investment Fund I

11,0M EUR Business Angels Fund

***

VC II ***

Seed Fund ***

***

***

Seed and VC Fund ***

Fund size 58,5M EUR

JEREMIE***** Holding Fund

Fund size 130,0M EUR

BIF Fund-of-Fund

Fund size 84,2M EUR

New VC/PE Instruments in the Pipeline

Business Angels Fund I (2015 12 31)**8,4M EUR****

Practica Venture Capital (2016 12 31)**

EUR 188,0M of private investor monies attracted to date (May 2016)EUR 188,0M of private investor monies attracted to date (May 2016)EUR 188,0M of private investor monies attracted to date (May 2016)EUR 188,0M of private investor monies attracted to date (May 2016)EUR 188,0M of private investor monies attracted to date (May 2016)EUR 188,0M of private investor monies attracted to date (May 2016)EUR 188,0M of private investor monies attracted to date (May 2016)EUR 188,0M of private investor monies attracted to date (May 2016)EUR 103,2M from pension fundsEUR 103,2M from pension fundsEUR 103,2M from pension fundsEUR 103,2M from pension fundsEUR 103,2M from pension fundsEUR 57,9M invested in companies to date (May 2016)EUR 57,9M invested in companies to date (May 2016)EUR 57,9M invested in companies to date (May 2016)EUR 57,9M invested in companies to date (May 2016)EUR 57,9M invested in companies to date (May 2016)EUR 57,9M invested in companies to date (May 2016)EUR 57,9M invested in companies to date (May 2016)

15,7M EUR****

81,5M EUR**** BaltCap PEF II

Fundraising

VC/PE funds performance of Jeremie Holding Fund

Fundraising of VCA members, EUR M Cumulative fundraising Capital attracted GPs commitment

47,7

0,41 0,70

22,86

1,906,95

1,400,03 0,86 0,14 0,10

48,1 48,8

72,5 74,681,6 83,0

2010 2011 2012 2013 2014 2015

Lithuanian VC fundraising activity commenced in 2010, fuelled by EU structural funds and steered by EIF.

The funds have completed general fundraising rounds, with most capital raised in 2010 and 2012.

VCA member funds includedin this report and main year

BaltCapLitCapitalBusiness Angels Fund I Practica Capital

(2010)(2010)(2010)(2012)Investment

Funds invested, EUR M Cumulative investment Capital invested

0,20

6,39 8,55 9,89

14,68

9,36

0,20

6,59

15,12

25,01

39,69

49,05

2010 2011 2012 2013 2014 2015

34M EUR (40%) is still to be invested, subject to funds allocated to cover operational expenses

As funds are nearing the end of their investment cycles, investment activity is declining, after reaching peak of 14.7M EUR in 2014.

Accounts for almost 60% of total committed capital.

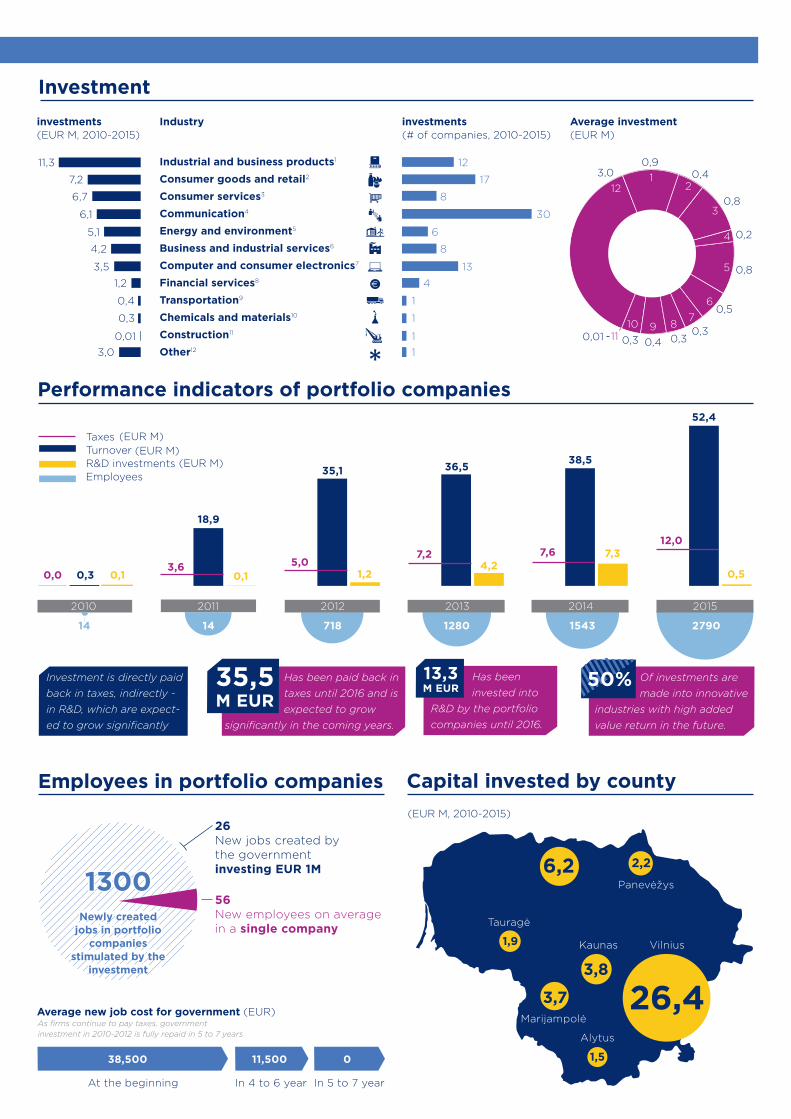

Investment

1,7

38

57%(27,6)

Value of investments (EUR m and % of total) # Of investment Average investment (EUR M)

0,2

0,2

0,6

17

7

19

12%(5,8)

28%(13,3)

3%

Seed Start-up Growth Turnaround

The average investment value for all stages is at 0.9M EUR. Lithuanian funds are limiting their maximum investment into one company at 3M EUR, as is imperative by structural funding requirements by EU.

Lithuanian funds are allocating most of its funds into companies that already have an estab-lished revenue and client bases. Investments in seed stage companies are frequent, yet significantly smaller (average invest-ment of 0.2M EUR).

High number of investments into seed stage companies can be explained by the recent boom in start-up culture in Lithuania.

(1,3)

14 14 718 1280 1543 2790

12

3

4

5

67

891011

12

0,90,4

0,8

0,2

0,8

0,5

0,30,30,40,30,01

3,0

As firms continue to pay taxes, government investment in 2010-2012 is fully repaid in 5 to 7 years

Investment

Industrial and business products1

Consumer goods and retail2

Consumer services3

Communication4

Energy and environment5

Business and industrial services6

Computer and consumer electronics7

Financial services8

Transportation9

Chemicals and materials10

Construction11

Other12

investments(EUR M, 2010-2015)

Industry investments(# of companies, 2010-2015)

11,3

7,2

6,7

6,1

5,1

4,2

3,5

1,2

0,4

0,3

0,013,0

12

17

8

30

6

8

13

4

1

1

11

Average investment (EUR M)

(EUR M)(EUR M)

(EUR M)

Capital invested by county

2,26,2

26,43,8

3,7

1,5

1,9

Panevėžys

VilniusKaunas

Tauragė

Marijampolė

Alytus

Performance indicators of portfolio companies

(EUR M, 2010-2015)

Taxes Turnover R&D investments Employees

0,3 0,10,0

18,9

0,13,6

35,1

1,25,0

36,5

4,27,2

52,4

0,5

12,0

38,5

7,37,6

2010 2011 2012 2013 20152014

Of investments are made into innovative

industries with high added value return in the future.

50%Investment is directly paid back in taxes, indirectly - in R&D, which are expect-ed to grow significantly

Employees in portfolio companies

1300

26New jobs created bythe governmentinvesting EUR 1M

56New employees on average in a single company

38,500 11,500 0

In 5 to 7 yearIn 4 to 6 yearAt the beginning

Average new job cost for government (EUR)

Has been invested into

R&D by the portfolio companies until 2016.

13,3M EUR

Has been paid back in taxes until 2016 and is expected to grow

significantly in the coming years.

35,5M EUR

Newly created jobs in portfolio

companies stimulated by the

investment

1 3

46

2

5

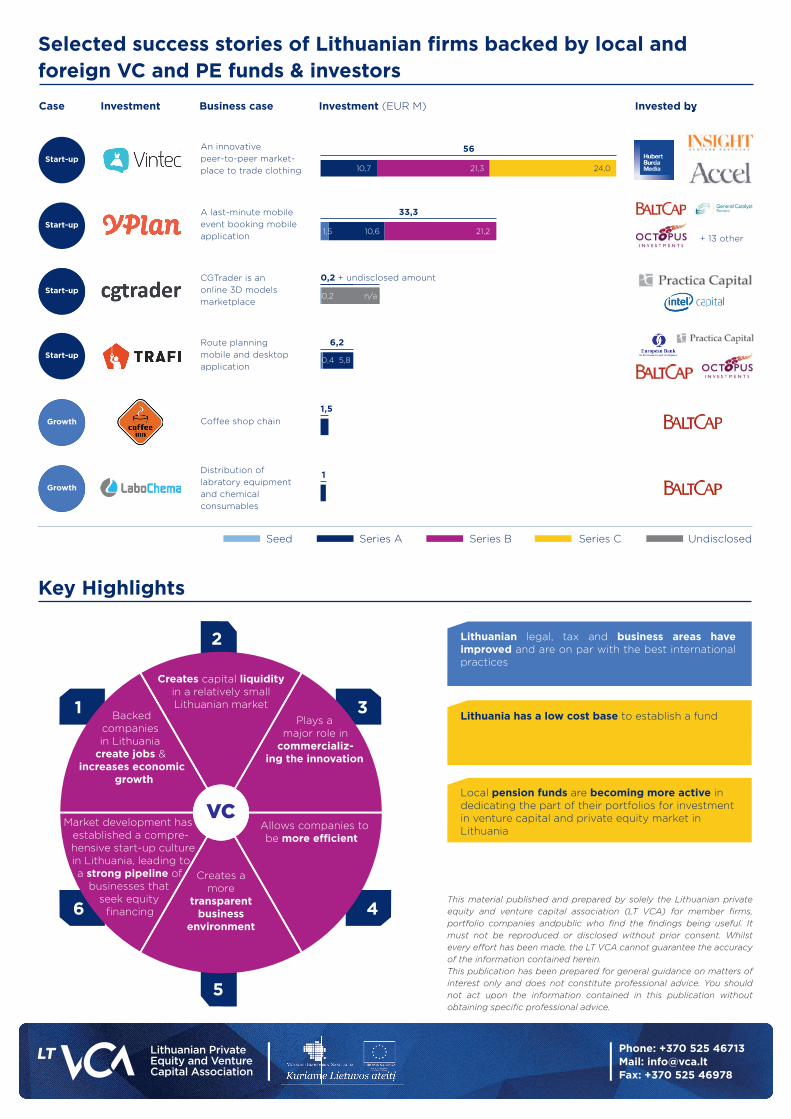

Selected success stories of Lithuanian firms backed by local and foreign VC and PE funds & investors

Phone: +370 525 46713Mail: [email protected]: +370 525 46978

Case Investment Business case Investment (EUR M) Invested byInvested by

An innovative peer-to-peer market-place to trade clothing

Start-up56

A last-minute mobile event booking mobile application

Start-up33,3

+ 13 other

CGTrader is an online 3D models marketplace

Start-up0,2 + undisclosed amount

Start-up

Route planning mobile and desktop application

Start-up6,2

Co�ee shop chainStart-up1,5

Growth

Distribution of labratory equipment and chemical consumables

Start-up1

Growth

10,7 21,3 24,0

1,5 10,6 21,2

0,2 n/a

0,4 5,8

Seed Series A Series B Series C Undisclosed

Key Highlights

This material published and prepared by solely the Lithuanian private equity and venture capital association (LT VCA) for member firms, portfolio companies andpublic who find the findings being useful. It must not be reproduced or disclosed without prior consent. Whilst every e�ort has been made, the LT VCA cannot guarantee the accuracy of the information contained herein.This publication has been prepared for general guidance on matters of interest only and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice.

VC

Lithuanian legal, tax and business areas have improved and are on par with the best international practices

Lithuania has a low cost base to establish a fund

Local pension funds are becoming more active in dedicating the part of their portfolios for investment in venture capital and private equity market in Lithuania

Market development has established a compre-hensive start-up culture in Lithuania, leading to a strong pipeline of

businesses that seek equity

financing

Creates capital liquidity in a relatively small Lithuanian market

Creates a more

transparent business

environment

Backed companies in Lithuania

create jobs & increases economic

growth

Plays a major role in

commercializ-ing the innovation

Allows companies to be more e�cient