Embed Size (px)

Citation preview

MAJOR CINEPLEX GROUP PLC.

LIFESTYLEentertainment

Major Cineplex Group PLC.Analyst Meeting, Paragon Cineplex: May 13rd, 2013

Quarterly Briefing 1Q13

1Q13 QUATERLY BRIEFINGLIFESTYLEentertainment

2

contents

The Bottom Line

1Q13 Financial ReviewReview of Revenue, Net profit B/S snapshot

Growth Potentials

LIFESTYLEentertainment

1Q13 QUATERLY BRIEFINGLIFESTYLEentertainment

Highlight Results

“Major contribution are coming from cinema and advertising”

Operation

Expansion &

Investment

Lotus Maesod (4 Screens)Big C Roi Et (5 Screens)Lotus Nakornsawan (4 Screens)

Successful transformation to 268 digital screens

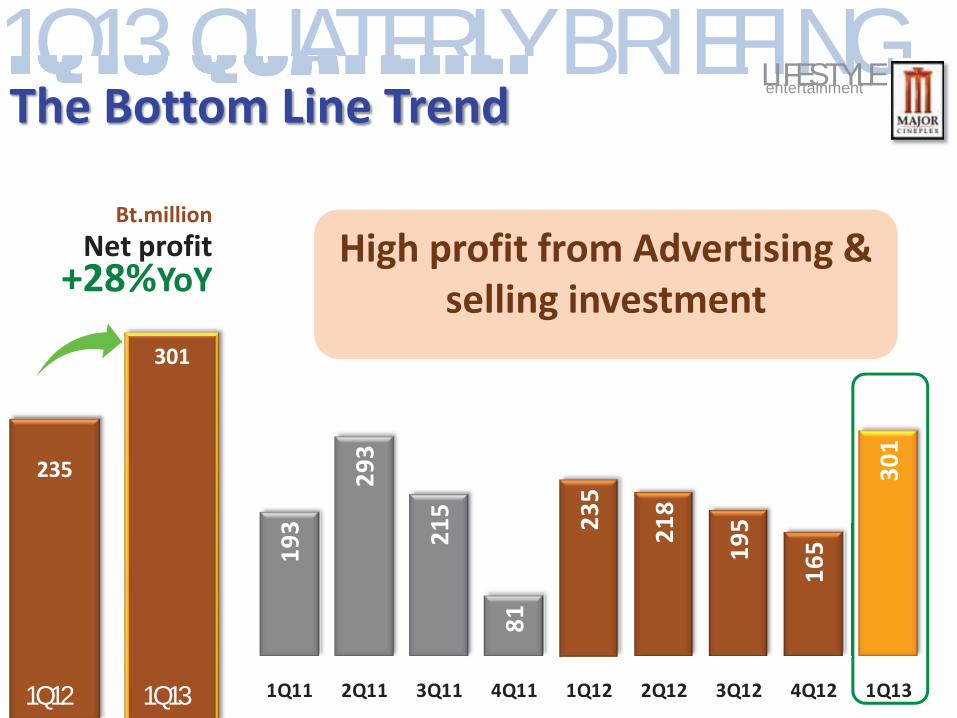

1Q13 QUATERLY BRIEFINGLIFESTYLEentertainmentThe Bottom Line Trend

Bt.millionNet profit

+28%YoYHigh profit from Advertising &

selling investment

235

301

193

293

215

81

235

218

195

165

301

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q131Q12 1Q13

1Q13 QUATERLY BRIEFINGLIFESTYLEentertainmentLThe Revenue Review breakdown

Bt.millionRevenue+0.3%YoY

Cinema, Concession and Advertising drove core revenue

Cinema+3.8%

Concession+20.6%

Advertising+37.8%

Bowling group-5.1%

Retails-4.8%

Film Distribution

-44.7%

1,66

7

1,67

1

1Q12

101

96

1Q12 1Q13

804 83

4

1Q12 1Q13

196

237

1Q12 1Q13

169

233

1Q12 1Q13

129

123

1Q12 1Q13

44

267

148

1Q12 1Q131Q13

1Q13 QUATERLY BRIEFINGLIFESTYLEentertainmentThe Revenue Review : CinemaBt.million

Cinema Group+7.1%YoY

Strong film line-up and concession variety built margin

804 83

4

196 23

7

1Q12 1Q13

Concession

+20.6%

GBO

+3.8%

1,0001,071

28%

31%

% Gross Margin

1Q12 1Q13

5.946.08

141

144

1Q12 1Q13

ATP & Guest count(Net Complementary)

196

237

24%

28%

1Q12 1Q13

Concession Rev. & % con-to-box

1Q13 QUATERLY BRIEFINGLIFESTYLEentertainmentLenteLIFLIFThe Revenue Review : Advertising

Bt.millionAdvertising+37.8%YoY

More advertising revenue from confident sponsors i.e. Toyota and Pepsi

152

22687%

90%

152

226

TalentOne

MPIC

CineAd

233

169

1Q12 1Q13

1Q12 1Q13

Core Advertising revenue & % Gross margin

1Q13 QUATERLY BRIEFINGLIFESTYLEentertainment

B/S SnapshotBt.million Dec 31, 12 Mar 31, 13 %chg

Assets 11,392 11,659 2%Liabilities 5,354 5,388 1%Equity 6,038 6,270 4%

6,038 6,270

5,354 5,38811,392 11,659

Dec 31,12 Mar 31,13

ASSE

TS

ASSE

TS

EQUI

TY

EQUI

TY

LIAB

ILIT

IES

LIAB

ILIT

IES

Net interest-bearing debts Equity Net D/E

0.600.51

0.42 0.39 0.37

YE09 YE10 YE11 YE12 End of 1Q13

1Q13 QUATERLY BRIEFINGLIFESTYLEentertainmentInvestments Portfoliovs. Interest-bearing debts

• Investment portfolio as of May 10,2013:• 20% in Siam Future Development Plc. (SF) • 74% in M Pictures Entertainment Plc. (MPIC)• 33% in Major Cineplex Lifestyle

Leasehold Property Fund (MJLF)• 40% in ThaiTicketMajor Co., Ltd.• 45% in Major Kantana Broadcasting Co., Ltd.• 8.8% in PVR Limited (PVRL)• 49% in PVR blu-O Entertainment Limited• 80% in Talent One Co.,ltd.• 50% in K-Arena

6,270

5,38811,659

Mar 31,13

ASSE

TS

EQUI

TYLI

ABIL

ITIE

S

Bt.million

Interest-bearing debts 1Q13

Bank OD & ST loans 842

CP of LT borrowings 886

LT borrowings 174

Debentures 1,000

Total 2,901

Bt.million

Investments %ShareCost per

ShareMarket value*

Major's Cost

Gain(Loss)

MJLF 33% 10.00 1,525 1,089 436

Siam Future 20% 2.64 2,551 623 1,929

MPIC 74% 1.61 1,173 768 405

PVRL 8.8% 89.69 527 229 298

Total 5,776 2,709 3,067 *Closing price on May 9,2013

LIFESTYLEentertainment

Quarterly Briefing1Q13GROWTH POTENTIALS

1Q13 QUATERLY BRIEFINGLIFESTYLEentertainmentGROWTH POTENTIALSLIFESTYLEentertainment

11

FY13 Strategic Focus

• Complete transformation into 100% Digital Format.

• Shift Media Selling Strategy to high gear.

• Utilize M-Generation database to maximize online revenue.

1Q13 QUATERLY BRIEFINGLIFESTYLEentertainmentGROWTH POTENTIALSFY13 Blockbuster Highlight LIFESTYLEE

*Movie line up will be add in movie line up around 3 months before showing

1Q13Hollywood MoviesJack the Giant Slayer G.I.Joe 2A Good Day to Die HardOz: The Great and PowerfulHansel and Gretel : Witch HuntersThai MoviesPee Mak Phrakhanong - 27 MarKhun nai Ho(M39)

2Q13Hollywood MoviesOBLIVIONIRON MAN 3STAR TREK INTO THE DARKNESSTHE GREAT GATSBYFAST SIX (FAST & FURIOUS 6)AFTER EARTHSUPERMAN: MAN OF STEELWORLD WAR ZThai MoviesPee Mak PhrakhanongSunset / คูกรรม (M39)

3Q13Hollywood MoviesTHE LONE RANGER PACIFIC RIM R.I.P.D. THE WOLVERINE 300: RISE OF AN EMPIREPERCY JACKSON : SEA OF MONSTERS WHITE HOUSE DOWNRIDDICK 3ELYSIUMThai MoviesTOOM YUM KUNG / ตมยํากุง*The rest will be announced later

4Q13Hollywood MoviesTHOR : THE DARK WORLD THE HUNGER GAMES : CATCHING FIRETHE HOBBIT 2 : THE DESOLATION OF SMAUG 47 RONIN CAPTAIN PHILLIPSThai Movies*The rest will be announced later

1Q13 QUATERLY BRIEFINGLIFESTYLEentertainmentGROWTH POTENTIALS

Capacities LIFESTYLEentertainment

Expand more screens into high growth potential areas especially provincial.As of Apr 2013

FY10 FY11 FY12 FY13Screens 361 383 289 119

BKK & Vicinity 252 259 284 Bangyai 5IKEA : 15 Emporium 2 8

Bangkae : 10 TBA 5

Provincial 109 124 Udonthanee 1 Maesod 4 Additional screens Roi-Et 5Nakornsritham 4 Nakornsawan2 4

Ubonratchathani 2 7Nongbualumphu 4Ampo Mall Ayutthaya 4Suratthani 7Satoon 5Sakonnakhon 4Prachinburi 4Suphanburi 4Songkla 5Suratthani 2 5Klaeng 4Hadyai 10Chiangmai 2 11Samui 5

TBA 9

Lanes 504 506 180 94 BKK & Vicinity 386 386 IKEA 24

Provincial 94 94 Hadyai 16

International 24 Vasant Kunj 26 Bangalore 60 TBA 78Pune 36Mumbai 12Raja Garden� 22Chandigarh� 26

1Q13 QUATERLY BRIEFINGLIFESTYLEentertainmentMajor Cineplex’s Expansion Trend

Major has presented in only 31 out of 77 provinces.

Major continues to expand more especially in provincial area which is high potential growth.

2010 2011 2012 ~2013 ~2015 ~2020

Location

No. of Screens / Locations

5356

Screens expansion supporting cinema’s revenue growth

~1,000

361 383

~510 ~600

70% 68% 69% 54% 52% 51%

30% 32% 31% 46% 48% 49%

2010 2011 2012 ~2013 ~2014 ~2015

Urbanization is a high potential growth. BKKUPCExpansion plan compare with BKK and UPC (as%)

50 410

1Q13 QUATERLY BRIEFINGLIFESTYLEentertainmentCurrent Asia Market Trend

15Density: Population per Screen

High

Low

Cinema is blooming in Asia especially in China.

Asia becomes the world’s second largest regional for movie theaters.

SingaporePop: 5.3MScreen: 20026,300 ppl/Screen

MalaysiaPop: 30MScreen : 71841,000 ppl/Screen

TaiwanPop: 24MScreen : 58040,200 ppl/Screen

PhilipinesPop: 96MScreen : 700137,800 ppl/Screen

IndonesiaPop: 245MScreen : 726337,000 ppl/Screen

ThailandPop: 70MScreen : 84683,000 ppl/Screen

South KoreaPop: 49MScreen : 2,00024,500 ppl/Screen

IndiaPop: 1.26BScreen : 11,029114,000 ppl/Screen

ChinaPop: 1.35BScreen : 14,50095,000 ppl/ScreenThailand can reached to 2,500 – 3,000 Screens in the

future due Thailand is still under screened and penetration is still low.

1Q13 QUATERLY BRIEFINGLIFESTYLEentertainmentGROWTH POTENTIALSLIFESTYLE

entertainment

16

Total 1,945,078 members (As of Apr’13) Ratio M Gen Card : Regular & Student

We are the only movie theaters in the world which collected customer database. Also adding value by using social media such as Online E-ticketing, Facebook, Twitter, Line, Mobile application, etc.

44.6%55.4% 444444...6%%%%%444444 66%%%%%%%%4444444444 66

Regular

5555555555 4444%%%%%

Student

LIFESTYLEentertainment

Quarterly Briefing1Q13Thank you