Embed Size (px)

DESCRIPTION

FGFGFGHGJH

Citation preview

List of PMJDY Nodal Officers

Sub Service Area wise mapping of Micro Insurance Agents for PMJDY

LIC’s Micro Insurance Plans are not plans but opportunities that knock on your door once in a lifetime. These plans are a perfect blend of insurance, investment and a lifetime of happiness!.

LICs New Jeevan Mangal Micro - Insurance Forms LIC's Bhagya Lakshmi Plan

Special Plans - New Jeevan Mangal

Policy Document

LIC’s New JEEVAN MANGAL PLAN – MICRO INSURANCE PRODUCT (UIN: 512N287V01)

Features

1.Introduction:

LIC’s New Jeevan Mangal is a protection plan with return of premiums on maturity, where you may pay the premiums either in lump sum or regularly over the term of the policy. This plan has an in-built Accident Benefit which provides for double risk cover in case of accidental death.

Special Plans -New Jeevan Mangal

a. Maturity Benefit:

Provided the policy is inforce, on surviving to the date of maturity, “Sum Assured on Maturity” shall be payable which is equal to the total amount of premiums paid during the term of the contract (excluding the taxes and extra premium, if any)

b. Death Benefit:

Provided the policy is inforce, the death benefit shall be payable as under:-

Death due to any reason other than accident:

For regular premium policies : “Sum Assured on Death” shall be payable which is defined as highest of 10 times of annualised premium or 105% of all the premiums paid as on date of death or Sum assured on Maturity or absolute amount assured to be paid on death where absolute amount assured to be paid on death is Sum Assured.

The premiums mentioned above exclude taxes and extra premium, if any.

For single premium policies : “Sum Assured on Death” shall be payable which is defined as higher of 125% of single premium (excluding the taxes and extra premium, if any) or absolute amount assured to be paid on death where absolute amount assured to be paid on death is Sum Assured.

Death due to accident :

An additional sum equal to Sum Assured shall also be payable.

An ‘Accident’ for the purpose of this policy is defined as “An Accident is a sudden, unforeseen and involuntary event caused by external, violent and visible means.”

Micro Insurance Plans -Jeevan Mangal

1. Eligibility Conditions and Other Restrictions:

a) Minimum age at entry : 18 years (completed)

b) Maximum age at entry : 55 years (nearest birthday)

c) Maximum age at maturity : 65 years (nearest birthday)

d) Policy Term : 10 to 15 years for regular premium.

5 to 10 years for single premium.

e) Minimum Instalment Premium : Rs 60/- under Monthly Mode

For other modes, there is no specific minimum instalment premium.

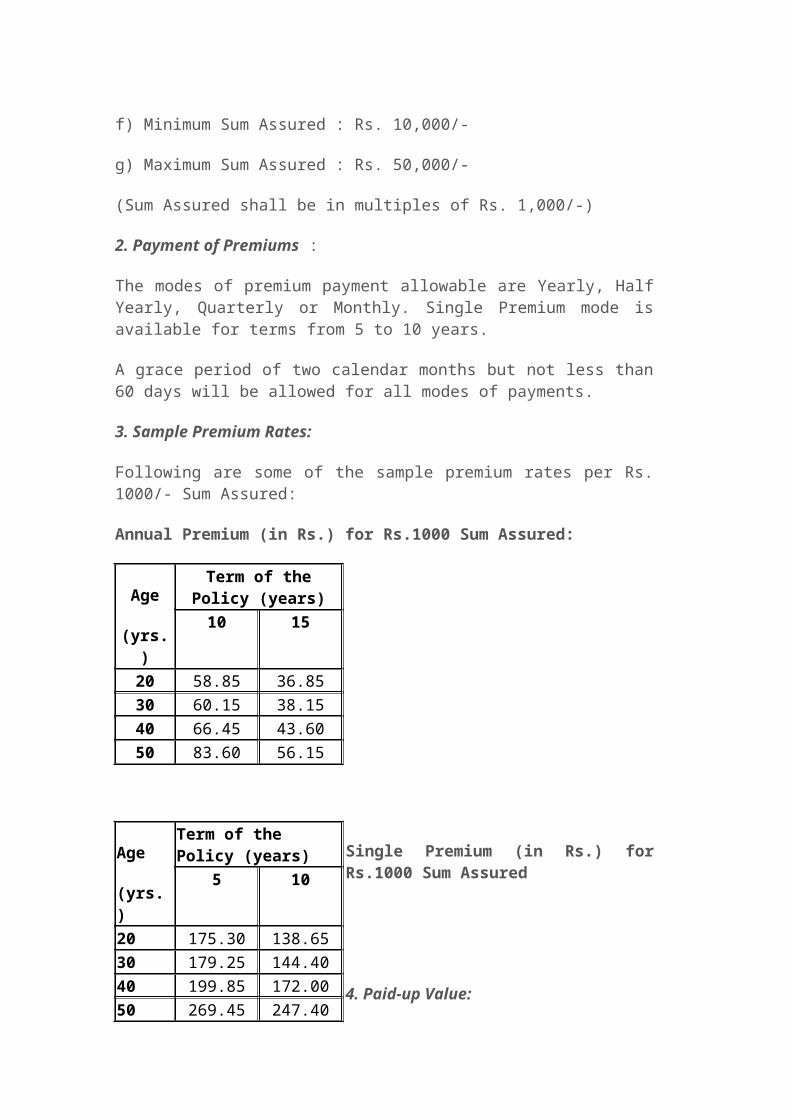

f) Minimum Sum Assured : Rs. 10,000/-

g) Maximum Sum Assured : Rs. 50,000/-

(Sum Assured shall be in multiples of Rs. 1,000/-)

2. Payment of Premiums :

The modes of premium payment allowable are Yearly, Half Yearly, Quarterly or Monthly. Single Premium mode is available for terms from 5 to 10 years.

A grace period of two calendar months but not less than 60 days will be allowed for all modes of payments.

3. Sample Premium Rates:

Following are some of the sample premium rates per Rs. 1000/- Sum Assured:

Annual Premium (in Rs.) for Rs.1000 Sum Assured:

Single Premium (in Rs.) for Rs.1000 Sum Assured

Age

(yrs.)

Term of the Policy (years)

10 15

20 58.85 36.85 30 60.15 38.15 40 66.45 43.60 50 83.60 56.15

4. Paid-up Value:

In case of regular premium policies, if after at least three full years’ premiums have been paid in respect of this policy and any subsequent premium be not duly paid, this policy shall not be wholly void, but shall subsist as a paid-up policy. The Sum Assured on Death shall be reduced to a sum, called the Death Paid-up Sum Assured. The Death Paid-Up Sum Assured shall bear the same ratio to the Sum Assured on Death as the premiums paid bears to the total number of premiums payable.

On the Life Assured’s death prior to maturity, the Death Paid-Up Sum Assured shall be payable. On Maturity, total premiums paid less taxes and extra premium, if any, shall be payable.

5. Revival:

Subject to production of satisfactory evidence of continued insurability, a lapsed policy can be revived by paying arrears of premium together with interest within a period of two years from the date of first unpaid premium but before maturity. The rate of interest applicable will be as fixed by the Corporation from time to time.

6. Surrender Value:

The Guaranteed Surrender Value available under this plan is as under:

Single Premium policies : The policy may be surrendered for cash at any time during the policy term. The Guaranteed Surrender Value shall be as under:

- Within three policy years from Date of Commencement of policy: 70% of the Single premium excluding taxes and extra premium, if any.

- Thereafter: 90% of the Single premium excluding taxes and extra premium, if any.

Regular Premium policies : The policy may be surrendered for cash provided the premiums have been paid for atleast three consecutive years. The Guaranteed Surrender Value shall be equal to Guaranteed Surrender Value factor multiplied by total premiums paid (excluding taxes and extras, if any). The Guaranteed Surrender Value factor will depend on the policy term and policy year in which the policy is surrendered and is as under:

Age

(yrs.)

Term of the Policy (years)

5 10

20 175.30 138.65 30 179.25 144.40 40 199.85 172.00 50 269.45 247.40

Policy Year Policy Term

10 11 12 13 14 15 1 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 2 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 3 30.00% 30.00% 30.00% 30.00% 30.00% 30.00% 4 50.00% 50.00% 50.00% 50.00% 50.00% 50.00% 5 50.00% 50.00% 50.00% 50.00% 50.00% 50.00% 6 50.00% 50.00% 50.00% 50.00% 50.00% 50.00% 7 50.00% 50.00% 50.00% 50.00% 50.00% 50.00% 8 65.00% 60.00% 57.50% 56.00% 55.00% 54.29% 9 80.00% 70.00% 65.00% 62.00% 60.00% 58.57% 10 80.00% 80.00% 72.50% 68.00% 65.00% 62.86% 11 80.00% 80.00% 74.00% 70.00% 67.14% 12 80.00% 80.00% 75.00% 71.43% 13 80.00% 80.00% 75.71% 14 80.00% 80.00% 15 80.00%

Corporation may, however, pay special surrender value if it is more favourable to the policyholders.

7. Loan:

No loan facility will be available under this plan.

8. Taxes:

Taxes including Service Tax, if any, shall be as per the Tax laws and the rate of tax shall be as applicable from time to time.

The amount of tax as per the prevailing rates shall be payable by the policyholder on the premiums including extra premiums, if any. The amount of Tax paid shall not be considered for the calculation of benefits payable under the plan.

9. Cooling-off period:

If the policyholder is not satisfied with the “Terms and Conditions” of the policy, the policy may be returned to the Corporation within 15 days from the date of receipt of the policy stating the reason of objections. On receipt of the same the Corporation shall cancel the policy and return the amount of premium deposited after deducting the proportionate risk premium for the period on cover and charges for stamp duty.

10. Exclusions:

a) Suicide :

Under Single Premium policies :

The policy shall be void if the Life Assured (whether sane or insane) commits

suicide at any time within 12 months from the date of commencement of risk and the Corporation will not entertain any claim under this policy except to the extent of 90% of the single premium paid excluding taxes and any extra premium paid.

Under Regular Premium policies :

This policy shall be void

i. If the Life Assured (whether sane or insane) commits suicide at any time within 12 months from the date of commencement of risk and the Corporation will not entertain any claim under this policy except to the extent of 80% of the premiums paid excluding any taxes and extra premiums, if any, provided the policy is In-force.

ii. If the Life Assured (whether sane or insane) commits suicide within 12 months from date of revival, an amount which is higher of 80% of the premiums paid till the date of death (excluding any taxes and extra premiums, if any) or the surrender value, provided the policy is inforce, shall be payable. The Corporation will not entertain any other claim under this policy.

b) Accident Benefit:

The Corporation will not be liable to pay the additional sum referred if the death of the Life Assured shall:

(i) be caused by intentional self injury, attempted suicide, insanity or immorality or whilst the Life Assured is under the influence or consumption of intoxicating liquor, drug or narcotic; or

(ii) be caused by injuries resulting from taking any part in riots, civil commotion, rebellion, war (whether war be declared or not), invasion, hunting, mountaineering, steeple chasing, racing of any kind, paragliding or parachuting, taking part in adventurous sports; or

(iii) result from the Life Assured committing any breach of law with criminal intent; or

(iv) occur after 180 days from the date of accident of the Life Assured.

Section 45 of the Insurance Act, 1938:

No policy of life insurance shall after the expiry of two years from the date on which it was effected, be called in question by an insurer on the ground that a statement made in the proposal for insurance or in any report of a medical officer, or referee, or friend of the insured, or in any other document leading to the issue of the policy, was inaccurate or false, unless the insurer shows that such statement was on a material matter or suppressed facts which it was material to disclose and that it was fraudulently made by the policyholder and that the policyholder knew at the time of making it that the statement was false or that it suppressed facts which it

was material to disclose.

Provided that nothing in this section shall prevent the insurer from calling for proof of age at any time if he is entitled to do so, and no policy shall be deemed to be called in question merely because the terms of the policy are adjusted on subsequent proof that the age of the life assured was incorrectly stated in the proposal.

Section 41 of the Insurance Act, 1938:

No person shall allow or offer to allow, either directly or indirectly, as an inducement to any person to take out or renew or continue an insurance in respect of any kind of risk relating to lives or property in India, any rebate of the whole or part of the commission payable or any rebate of the premium shown on the policy, nor shall any person taking out or renewing or continuing a policy accept any rebate, except such rebate as may be allowed in accordance with the published prospectuses or tables of the insurer : provided that acceptance by an insurance agent of commission in connection with a policy of life insurance taken out by himself on his own life shall not be deemed to be acceptance of a rebate of premium within the meaning of this sub-section if at the time of such acceptance the insurance agent satisfies the prescribed conditions establishing that he is a bonafide insurance agent employed by the insurer.

Any person making default in complying with the provisions of this Section shall be punishable with a fine which may extend to Rs.500 / -

Note: “Conditions apply” for which please refer to the Policy document or contact our nearest Branch Office.

“Insurance is the subject matter of solicitation”

Registered Office:

Life Insurance Corporation of India

Central Office, Yogakshema,

Jeevan Bima Marg,

Mumbai - 400021.

Website: www.licindia.in

Registration Number : 512

2

Micro Insurance Plans - LIC's Bhagya Lakshmi (UIN: 512N292V01)

Policy Document

LIC's Bhagya Lakshmi - Salient Features

LIC's Bhagya Lakshmi - Premium Rates

LIC's Bhagya Lakshmi - Proposal Form

1. Introduction:

LIC’s Bhagya Lakshmi is a non-par limited payment protection oriented plan with return of 110% of total amount of premiums payable on maturity where the premium paying term is 2 years lesser than the policy term.

Micro Insurance Plans -LIC's Bhagya Lakshmi (UIN: 512N292V01)

1. Benefits :

a. Maturity Benefit:

Provided the policy is inforce, on surviving to the date of maturity, “Sum Assured on Maturity” shall be payable which is equal to 110% of total amount of premiums payable during the term of the contract (excluding taxes and extra premium, if any)

b. Death Benefit:

On Life Assured's death before the stipulated Date of Maturity, provided the policy is in full force by paying up-to-date premiums, “Sum Assured on Death” equal to Sum Assured under the policy shall be payable.

Micro Insurance Plans -LIC's Bhagya Lakshmi (UIN: 512N292V01)

Eligibility Conditions and Other Restrictions: Minimum Sum Assured : Rs. 20,000/-

Maximum Sum Assured : Rs. 50,000/-

(The Sum Assured shall be in multiples of Rs. 1,000/-)

Minimum age at entry : 18 years (completed) Maximum age at entry : 55 years (nearest birthday) Minimum Premium Paying Term : 5 years Maximum Premium Paying Term : 13 years Policy Term : Premium Paying Term + 2 years Maximum age at maturity : 65 years (nearest birthday)

Payment of Premiums:

The modes of premium payment allowable are yearly, half-yearly, quarterly, monthly or through salary deductions.

However, a grace period of two calendar months but not less than 60 days will be allowed for all modes of payments.

Sample Premium Rates:

Following are some of the sample annual tabular premium rates (exclusive of service tax) per Rs. 1000/- Sum Assured:

AGEIn years

TERM (PPT) in years7(5) 10(8) 15(13)

20 127.45 64.35 37.2030 129.30 65.80 38.5540 138.30 72.80 44.2550 164.10 91.40 57.1555 179.90 103.05 -

Mode and High Sum Assured Rebates:

Mode Rebate:Yearly mode - 2% of Tabular PremiumHalf-yearly mode - 1% of Tabular premiumOther modes - NIL

High Sum Assured Rebate: Nil

Paid-up Value:

For policies with premium paying term less than 10 years if after at least two full years' premiums have been paid and for policies with premium paying term 10 years or more if after at least three full years' premiums have been paid and any

subsequent premium be not duly paid, this policy shall not be wholly void, but shall subsist as a paid-up policy.

The amount payable on death under a paid-up policy shall be reduced to such a Sum, called Death Paid-up Sum Assured and shall bear the same ratio to the Sum Assured on Death as the number of premiums paid bears to the total number of premiums payable i.e. Death Paid-up Sum Assured = Sum Assured on Death * (number of premiums paid/number of premiums payable during the policy term).

The amount payable at Maturity under a paid-up policy shall be reduced to such a Sum, called Maturity Paid-up Sum Assured and shall bear the same ratio to the Sum Assured on Maturity as the number of premiums paid bears to the total number of premiums payable i.e. Maturity Paid-up Sum Assured = Sum Assured on Maturity * (number of premiums paid/number of premiums payable during the policy term).

The policy so reduced shall thereafter be free from all liabilities for payment of the within mentioned premium.

Revival:

If premiums are not paid within the grace period then the policy will lapse. A lapsed policy can be revived within a period of two consecutive years from the date of first unpaid premium but before the date of maturity, as the case may be, on submission of proof of continued insurability as per “Board approved underwriting policy” and the payment of all the arrears of premium together with interest (compounding half-yearly) at such rate as fixed by the Corporation from time to time.

The Corporation reserves the right to accept at original terms, accept with modified terms or decline the revival of a discontinued policy as per “Board approved underwriting policy”. The revival of a discontinued policy shall take effect only after the same is approved by the Corporation and is specifically communicated in writing to the Life Assured.

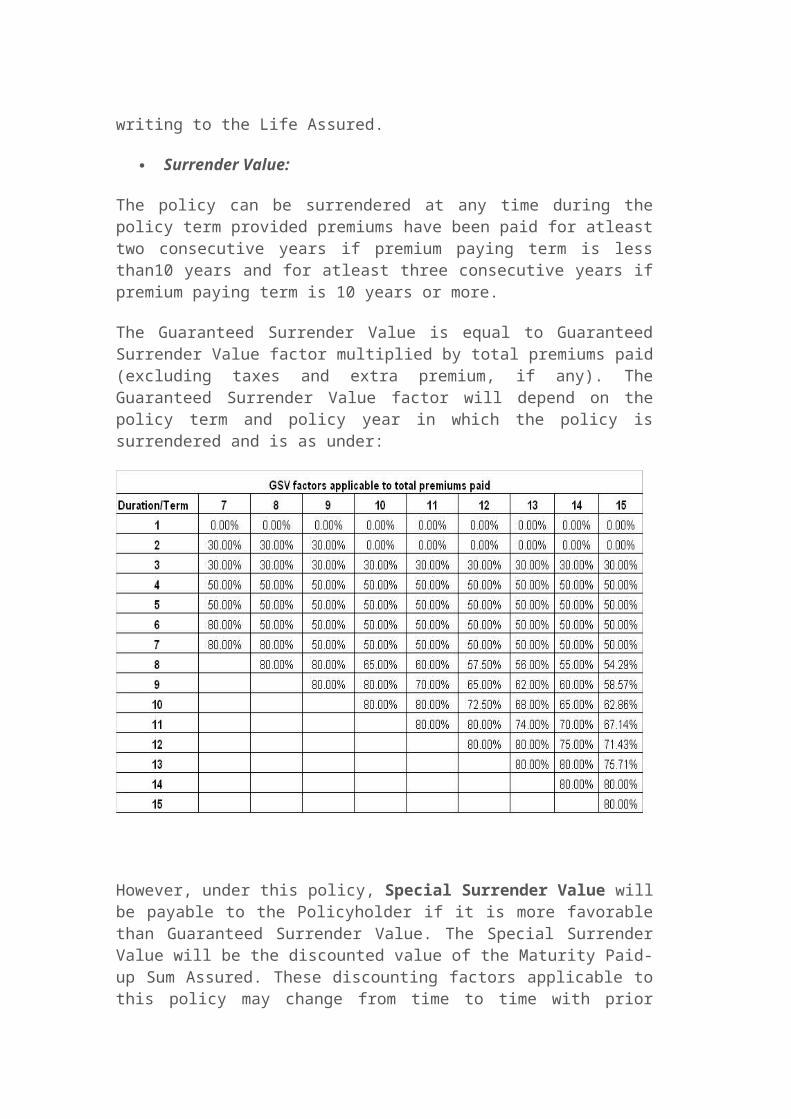

Surrender Value:

The policy can be surrendered at any time during the policy term provided premiums have been paid for atleast two consecutive years if premium paying term is less than10 years and for atleast three consecutive years if premium paying term is 10 years or more.

The Guaranteed Surrender Value is equal to Guaranteed Surrender Value factor multiplied by total premiums paid (excluding taxes and extra premium, if any). The Guaranteed Surrender Value factor will depend on the policy term and policy year in which the policy is surrendered and is as under:

However, under this policy, Special Surrender Value will be payable to the Policyholder if it is more favorable than Guaranteed Surrender Value. The Special Surrender Value will be the discounted value of the Maturity Paid-up Sum Assured. These discounting factors applicable to this policy may change from time to time with prior approval of IRDA.

Loan:

No loan facility will be available under this plan.

Taxes:

Taxes including service tax, if any, shall be as per the Tax laws and the rate of tax shall be as applicable from time to time.

The amount of tax as per the prevailing rates shall be payable by the policyholder on the premium including extra premium and rider premium, if any. The amount of Tax paid shall not be considered for the calculation of benefits payable under the plan.

Free Look period:

If the policyholder is not satisfied with the “Terms and Conditions” of the policy, the policy may be returned to the Corporation within 15 days from the date of receipt of the policy stating the reason of objections. On receipt of the same the

Corporation shall cancel the policy and return the amount of premium deposited after deducting the proportionate risk premium for the period on cover and charges for stamp duty.

Exclusions: Suicide :

This policy shall be void

If the Life Assured (whether sane or insane) commits suicide at any time within 12 months from the date of commencement of risk and the Corporation will not entertain any claim under this policy except to the extent of 80% of the premiums paid excluding any taxes and extra premium, if any, provided the policy is inforce.

If the Life Assured (whether sane or insane) commits suicide within 12 months from date of revival, an amount which is higher of 80% of the premiums paid till the date of death (excluding any taxes and extra premium, if any) or the surrender value, shall be payable. The Corporation will not entertain any other claim under this policy.

SECTION 45 OF INSURANCE ACT, 1938:

No policy of life insurance shall after the expiry of two years from the date on which it was effected, be called in question by an insurer on the ground that a statement made in the proposal for insurance or in any report of a medical officer, or referee, or friend of the insured, or in any other document leading to the issue of the policy, was inaccurate or false, unless the insurer shows that such statement was on a material matter or suppressed facts which it was material to disclose and that it was fraudulently made by the policyholder and that the policyholder knew at the time of making it that the statement was false or that it suppressed facts which it was material to disclose.

Provided that nothing in this section shall prevent the insurer from calling for proof of age at any time if he is entitled to do so, and no policy shall be deemed to be called in question merely because the terms of the policy are adjusted on subsequent proof that the age of the life assured was incorrectly stated in the proposal.

PROHIBITION OF REBATES (SECTION 41 OF INSURANCE ACT, 1938):(1) No person shall allow or offer to allow, either directly or indirectly, as an inducement to any person to take out or renew or continue an insurance in respect of any kind of risk relating to lives or property in India, any rebate of the whole or part of the commission payable or any rebate of the premium shown on the policy, nor shall any person taking out or renewing or continuing a policy accept any

rebate, except such rebate as may be allowed in accordance with the published prospectuses or tables of the insurer: provided that acceptance by an insurance agent of commission in connection with a policy of life insurance taken out by himself on his own life shall not be deemed to be acceptance of a rebate of premium within the meaning of this sub-section if at the time of such acceptance the insurance agent satisfies the prescribed conditions establishing that he is a bona fide insurance agent employed by the insurer.

(2) Any person making default in complying with the provisions of this section shall be punishable with fine which may extend to five hundred rupees.

Note: “Conditions apply” for which please refer to the Policy document or contact our nearest Branch Office.

BEWARE OF SPURIOUS PHONE CALLS AND FICTITIOUS/FRAUDULENT OFFERS

IRDA clarifies to public that

IRDA or its officials do not involve in activities like sale of any kind of insurance or financial products nor invest premiums.

IRDA does not announce any bonus.

Public receiving such phone calls are requested to lodge a police compliant along with details of phone call, number.

��

“Insurance is the subject matter of solicitation”

Registered Office:Life Insurance Corporation of IndiaCentral Office, Yogakshema,Jeevan Bima Marg,Mumbai - 400021.Website: www.licindia.in

Registration Number : 512

Insurance Plans - LIC's e-Term (UIN: 512N288V01)

Policy Document

LIC’s e-TERM PLAN

Key Features :

1. Available through Online mode (www.licindia.in) 2. Pure Term plan 3. Differential premium rates for Smoker/Non-Smoker lives 4. Proposal on own life ONLY will be considered

Key Benefits :

o Death Benefit – Sum Assured payable on death o Maturity Benefit – Not available

Eligibility conditions :

o Minimum Sum Assured : Rs.25,00,000 for Aggregate category Rs.50,00,000 for Non-smoker category

Maximum Sum Assured : No limit Minimum age at entry : 18 years (completed) Maximum age at entry : 60 years (nearest

birthday) Maximum cover : 75 years (nearest

birthday) ceasing age Minimum policy term : 10 years Maximum policy term : 35 years Mode of payment : Yearly

Insurance Plans - LIC's e-Term (UIN: 512N288V01)

LIC’s e-Term is a regular premium non-participating “on-line term assurance policy” which provides financial protection to the insured’s family in case of his/her unfortunate demise. This plan will be available through on-line application process only and no intermediaries will be involved. To purchase this plan please log on to our website www.licindia.in.

Under this plan, there are two categories of premium rates namely (1) Aggregate lives & (2) Non-smoker lives. For Sum Assured upto Rs. 49 lacs Aggregate category rates only would apply. For Sum Assured Rs. 50 lacs and above there is an option to choose differential premium rate for Non-smoker category. However, the application of Non-smoker rates shall be based on the findings of the Urinary Cotinine test. In all other cases the Aggregate premium rates shall be applicable.

Benefits:

Death Benefit: In case of unfortunate death of the Life Assured during the policy term Sum Assured shall be payable.

Maturity Benefit: On survival to the end of the policy term, nothing shall be payable.

Insurance Plans - LIC's e-Term (UIN: 512N288V01)

1. Eligibility Conditions and Other Restriction: Minimum Sum Assured : Rs. 25,00,000 for

Aggregate category

Rs. 50,00,000 for Non-smoker category

Maximum Sum Assured : No limit

(The Sum Assured shall be in multiples of Rs. 1, 00,000/-)

Minimum age at entry : 18 years (completed) Maximum age at entry : 60 years (nearest

birthday)

Maximum cover ceasing age : 75 years (nearest birthday)

Minimum policy term : 10 years Maximum policy term : 35 years Proposal on own life only will be considered. Key Man

Insurance (KMI)/Partnership/EE Cover will not be allowed.

Payment of Premiums:

Premium need to be paid annually during the policy term.

A grace period of one month but not less than 30 days from due date of premium will be allowed for payment of premiums.

Sample Premium Rates:

The sample premium rates (exclusive of taxes) are as under:

For Aggregate category

Annualised premium rates per Rs. 1000 Sum Assured

Age(yrs.)

Term of the Policy (years)10 15 20 25 30

20 0.92 0.92 0.93 1.00 1.1130 1.10 1.20 1.39 1.66 1.9740 2.02 2.48 3.00 3.56 4.1950 4.86 5.72 6.73 7.90 -

For Non-smoker category

Annualised premium rates per Rs. 1000 Sum Assured

Age(yrs.)

Term of the Policy (years)10 15 20 25 30

20 0.63 0.63 0.65 0.70 0.7930 0.77 0.85 1.00 1.21 1.4640 1.48 1.84 2.25 2.69 3.1850 3.67 4.34 5.13 6.06 -

Revival:

If premiums are not paid within the grace period then the policy will lapse. A lapsed policy can be revived within a

period of 2 consecutive years from the date of first unpaid premium but before the expiry of policy term, by paying all the arrears of premium together with interest (compounding half-yearly) at such rate as may be prevailing at the time of the payment, subject to submission of satisfactory evidence of continued insurability.

The cost of the medical reports, including special reports, if any, required for the purposes of revival of the policy, shall be borne by the Life Assured.

The Corporation reserves the right to accept at original terms, accept at revised terms or decline the revival of a discontinued policy. The revival of discontinued policy shall take effect only after the same is approved by the Corporation and is specifically communicated to the Policyholder.

Paid-up Value:

The policy shall not acquire any paid-up value.

Surrender Value:

No Surrender Value will be available under this plan.

Taxes:

Taxes including Service Tax, if any, shall be as per the Tax laws and the rate of tax shall be as applicable from time to time.

The amount of tax as per the prevailing rates shall be payable by the Policyholder on Instalment premiums including extra premiums, if any.

Cooling-off period:

If the Policyholder is not satisfied with the “Terms and Conditions” of the policy, the policy may be returned to us within 30 days from the date of receipt of the policy bond stating the reason of objections. On receipt of the same the Corporation shall cancel the policy and return the amount of premium deposited after deducting the proportionate risk premium for the period on cover, stamp duty charges, expenses for medical examination and special reports, if any.

Exclusion:

Suicide: This policy shall be void if the Life Assured (whether sane or insane) commits suicide at any time within 12 months from the date of commencement of risk or within 12 months from the date of revival and the Corporation will not entertain any claim under this policy except to the extent of 80% of the premiums paid till the date of death excluding any taxes, extra premium, if any, provided the policy is inforce.

How to purchase LIC’s e-Term

Step-by-step process to buy LIC’s e-TERM Online:

Log-on to our website (www.licindia.in) for buying this online product. Click on ‘Buy Online’. Select e-Term.

Choose your desired Sum Assured and the Policy Term (the period for which you want the cover). The Sum Assured will be paid to the nominee on the unfortunate event of the death of the policy-holder.

Enter Basic details - Name, Age, Gender, Qualification, etc in the form displayed on your screen.

After filling in the details, a premium calculator will calculate the premium for the chosen parameters. The Premium will depend on the age, gender, term, sum-assured, health and tobacco-usage. Lower premium rates are applied to non-tobacco users for Sum Assured more than 50 Lakhs.

Premium payment mode – Annual. Complete the form online with these details and pay

premium online – at www.licindia.in.

Section 45 of Insurance Act, 1938:No policy of life insurance shall after the expiry of two years from the date on which it was effected, be called in question by an insurer on the ground that a statement made in the proposal for insurance or in any report of a medical officer, or referee, or friend of the insured, or in any other document leading to the issue of the policy, was inaccurate or false, unless the insurer shows that such statement was on a material matter or suppressed facts which it was material to disclose and that it was fraudulently made by the policyholder and that the policyholder knew at the time of making it that the statement was false or that it suppressed facts which it was

material to disclose.

Provided that nothing in this section shall prevent the insurer from calling for proof of age at any time if he is entitled to do so, and no policy shall be deemed to be called in question merely because the terms of the policy are adjusted on subsequent proof that the age of the life assured was incorrectly stated in the proposal.

Prohibition of Rebates (Section 41 of INSURANCE ACT, 1938) :(1) No person shall allow or offer to allow, either directly or indirectly, as an inducement to any person to take out or renew or continue an insurance in respect of any kind of risk relating to lives or property in India, any rebate of the whole or part of the commission payable or any rebate of the premium shown on the policy nor shall any person taking out or renewing or continuing a policy accept any rebate except such rebates as may be allowed in accordance with the published prospectuses or tables of the insurer provided that acceptance by an insurance agent of commission in connection with a policy of life insurance taking out by himself on his own life shall not be deemed to be acceptance of a rebate of premium within the meaning of this sub-section if at the time of such acceptance the insurance agent satisfies the prescribed conditions establishing that he is a bona fide insurance agent employed by the insurer.

(2) Any person making default in complying with the provision of this Section shall be punishable with a fine, which may extend to 500 rupees.

LIC’s new term plans 2014-Anmol Jeevan-II and Amulya Jeevan-II

Today LIC launched new versions of it’s existing Term Insurance policies. Let see how they are beneficial to you and what changes are done to the prior plans. From initial findings it looks that they are cheaper. But I need to validate with the data which may take some time.

Latest News (17th May 2014) !!!

LIC launched it’s first online term plan. Review will be available here “LIC’s online Term Plan e-Term-Review and Benefit“

1) Anmol Jeevan-II

Minimum Sum Assured raised from Rs.5,00,000 to Rs.6,00,000. Maximum Sum Assured Rs.24,00,000. Minimum Age at entry is 18 years and maximum age is 55 years. Maximum cover ceasing age is 65 years. Minimum Policy Term- 5 Years and Maximum Policy Term-25 years. Premium paying term-Yearly and Half Yearly only. Revival-A lapsed policy can be revived within 2 years from the first unpaid premium

but before the expiry of policy term. Medical report cost should be borne by Life Assured.

Death Benefit-Policy Sum Assured will be payable to nominee. Maturity Benefit-Nothing will be payable on survival of life assured till the end of

policy term. If the death of Life Assured occurs within the grace period but before the payment of

premium due then, policy will still be considered as valid and benefit will be payable to nominee (but after deducting the due premium+unpaid premiums due before the next policy anniversary).

2% of tabular annual premium will be add for half yearly premium. Agents Commission-

1. For term of 5-9 years-1st Year 10%, 2nd and 3rd Years-5% and subsequent years-5%.2. For term of 10 to 14 years-1st Year 15%, 2nd and 3rd Years-7.5% and subsequent

years-5%.3. For term of 15 years and above-1st Year 25%, 2nd and 3rd Years-7.5% and subsequent

years-5%

Bonus commission will be 40% of 1st year commission.

No loan, paid up value or surrender value. Policy will be considered as void if life assured commits suicide within 12 months

from the date of commencement of risk or from the date of revival. An amount equal to 80% of premiums paid till date of death (excluding taxes and extra premiums) will be payable if policy is in force.

2) Amulya Jeevan-II

Minimum Sum Assured Rs.25,00,000. Maximum Sum Assured-No limit. Minimum Age at entry-18 years and maximum age 60 years. Maximum maturity age-70 Years. Minimum policy term-5 years and maximum term-35 years.

Premium paying term-Yearly and Half Yearly only. Revival-A lapsed policy can be revived within 2 years from the first unpaid premium

but before the expiry of policy term. Medical report cost should be borne by Life Assured.

Death Benefit-Policy Sum Assured will be payable to nominee. Maturity Benefit-Nothing will be payable on survival of life assured till the end of

policy term. If the death of Life Assured occurs within the grace period but before the payment of

premium due then, policy will still be considered as valid and benefit will be payable to nominee (but after deducting the due premium+unpaid premiums due before the next policy anniversary).

2% of tabular annual premium will be add for half yearly premium. Agents Commission-

1. For term of 5-9 years-1st Year 10%, 2nd and 3rd Years-5% and subsequent years-5%.2. For term of 10 to 14 years-1st Year 20%, 2nd and 3rd Years-7.5% and subsequent

years-5%.3. For term of 15 years and above-1st Year 25%, 2nd and 3rd Years-7.5% and subsequent

years-5%

Bonus commission will be 40% of 1st year commission.

No loan, paid up value or surrender value. Policy will be considered as void if life assured commits suicide within 12 months

from the date of commencement of risk or from the date of revival. An amount equal to 80% of premiums paid till date of death (excluding taxes and extra premiums) will be payable if policy is in force.

Normal Requirements for claim-Claim form as prescribed by LIC with original policy bond, NEFT mandate form to directly transfer the amount to nominee bank, proof of title, proof of death, medical treatment prior to death and if age is not submitted during the time of policy buying then age of life assured should be furnished.

Whether to buy LIC’s term plans or not?

Major drawback why lot of people stayed away from LIC term plans are their pricing. They are costly when you compare with online or offline term plans available with other insurers in India. But few still tried to buy term plans with LIC because of their faith in it and to diversify their risk among insurers. Currently I don’t have valid table to compare. But when I considered the available resources I found that these new plans are cheaper than the older (this is my assumption and will update on it shortly).

For example for the aged 30 years and SA Rs.1,00,00,000 and term 25 years was previously cost us Rs.29,200 yearly. But now it is costing us Rs.22,028 (claiming to be inclusive of tax).

Image courtesy of [Stuart Miles] / FreeDigitalPhotos.net

Pension Plans are Individual Plans that gaze into your future and foresee financial stability during your old age. These policies are most suited for senior citizens and those planning a secure future, so that you never give up on the best things in life.

Jeevan Akshay-VILIC's New Jeevan Nidhi

What is Pension Plan?All of us are worried about our income when we retire. Pension Plans, also called Retirement Plans are one of the safest and surest ways of a trouble-free retirement life. Invest small amounts today while you are earning and receive fixed annual payouts during your retirement years. You build your kitty by investing small amounts regularly in your earning days and then use that kitty to buy an Annuity on retirement. The annuity will ensure the regular payouts during your golden years of retirement.

It is best to start planning for your retirement as early as possible because these small amounts contributed today will become a large sum of money over the years.

Pension Plans are flexible and can be used effectively if planned out well. On attaining the retirement age, the policy holder can withdraw 33% of the maturity amount for some immediate financial needs. The balance amount is used to purchase an annuity which gives a regular monthly/annual income

Pension Plans - Jeevan Akshay VI ( UIN - 512N234V04 )

Introduction: Policy Document

It is an Immediate Annuity plan, which can be purchased by paying a lump sum amount. The plan provides for annuity payments of a stated amount throughout the life time of the annuitant. Various options are available for the type and mode of payment of annuities.

Options Available:

The following options are available under the plan

Type of Annuity: o Annuity payable for life at a uniform rate. o Annuity payable for 5, 10, 15 or 20 years certain and thereafter as

long as the annuitant is alive. o Annuity for life with return of purchase price on death of the

annuitant. o Annuity payable for life increasing at a simple rate of 3% p.a. o Annuity for life with a provision of 50% of the annuity payable to

spouse during his/her lifetime on death of the annuitant. o Annuity for life with a provision of 100% of the annuity payable to

spouse during his/her lifetime on death of the annuitant. o Annuity for life with a provision of 100% of the annuity payable to

spouse during his/ her life time on death of annuitant. The purchase price will be returned on the death of last survivor.

You may choose any one. Once chosen, the option cannot be altered.

Mode:

Annuity may be paid either at monthly, quarterly, half yearly or yearly intervals. You may opt any mode of payment of Annuity..

Salient features:

Premium is to be paid in a lump sum. Minimum purchase price :

Rs.100,000/- for all distribution channels except online.

Rs.150,000/- for on line sale. No medical examination is required under the plan. No maximum limits for purchase price, annuity etc. Minimum allowed age at entry is 30 years (completed) and

Maximum allowed age at entry is 85 years (completed). Age proof necessary.

Annuity Rate:

Amount of annuity payable at yearly intervals which can be purchased for Rs. 1 lakh under different options is as under:

Age last birthday

Yearly annuity amount under option( i ) ( ii ) (15 years

certain) ( iii ) ( iv ) ( v ) ( vi ) (vii)

30 7190 7160 6890 5250 7080 6970 686040 7510 7440 6930 5610 7310 7120 689050 8140 7950 7000 6280 7760 7420 693060 9350 8790 7110 7530 8640 8030 701070 12080 9830 7260 10220 10560 9370 713080 17880 10440 7480 15890 14600 12340 7290

Incentives for high purchase price:

If your purchase price is Rs. 2.50 lakh or more, you will receive higher amount of annuity due to available incentives. In addition of this, for policies sold online, a rebate of 1% by way of increase in the annuity rate shall also be available.

Service Tax:

Service tax, if any, shall be as per the Service Tax Laws and at the rate of service tax as applicable from time to time. The amount of service tax as per the prevailing rates shall be payable by the policyholder along with the purchase price.

Paid-up value:

The policy does not acquire any paid-up value.

Surrender Value:

No surrender value will be available under the policy.

Loan:

No loan will be available under the policy.

Cooling-off period:

If you are not satisfied with the ?Terms and Conditions? of the policy, you may return the policy to us within 15 days from the date of receipt of the Policy Bond. On receipt of the policy we shall cancel the same and the amount of premium deposited by you shall be refunded to you after deducting the charges for stamp duty.

Section 45 Of Insurance Act 1938:

o No policy of life insurance shall after the expiry of two years from the date on which it was effected, be called in question by an insurer on the ground that a statement made in the proposal for insurance or in any report of a medical officer, or referee, or friend of the insured, or in any other document leading to the issue of the policy, was inaccurate or false, unless the insurer shows that such statement was on a material matter or suppressed facts which it was material to disclose and that it was fraudulently made by the policyholder and that the policyholder knew at the time of making it that the statement was false or that it suppressed facts which it was material to disclose.

o Provided that nothing in this section shall prevent the insurer from calling for proof of age at any time if he is entitled to do so, and no policy shall be deemed to be called in question merely because the terms of the policy are adjusted on subsequent proof that the age of the life assured was incorrectly stated in the proposal.

Section 41 of Insurance Act 1938:

o No person shall allow or offer to allow, either directly or indirectly, as an inducement to any person to take out or renew or continue an insurance in respect of any kind of risk relating to lives or property in India, any rebate of the whole or part of the commission payable or any rebate of the premium shown on the policy, nor shall any person taking out or renewing or continuing a policy accept any rebate, except such rebate as may be allowed in accordance with the published prospectuses or tables of the insurer: provided that acceptance by an insurance agent of commission in connection with a policy of life insurance taken out by himself on his own life shall not be deemed to be acceptance of a rebate of premium within the meaning of this sub-section if at the time of such acceptance the insurance agent satisfies the prescribed conditions establishing that he is a bona fide insurance agent employed by the insurer.

o Provided that nothing in this section shall prevent the insurer from calling for proof of age at any time if he is entitled to do so, and no policy shall be deemed to be called in question merely because the terms of the policy are adjusted on subsequent proof that the age of the life assured was incorrectly stated in the proposal.

Pension Plans - Jeevan Akshay VI ( UIN - 512N234V04 )

The amount of annuity is assured throughout life of the annuitant.

What happens if the annuitant dies?

If the annuitant dies :

1. Under option (i) annuity ceases. 2. Under option (ii)

On death during the guaranteed period - annuity is paid to the nominee till the end of the guaranteed period after which the same ceases. On death after the guaranteed period - annuity ceases.

3. Under option (iii) annuity ceases and the purchase price is paid to the nominee.

4. Under option (iv) annuity ceases. 5. Under option (v) annuity ceases and 50% of the annuity is payable to the

surviving named spouse during his/her life time. If the spouse predeceases the annuitant, the annuity ceases.

6. Under option (vi) annuity ceases and full annuity is payable to the surviving named spouse during his/her life time. If the spouse predeceases the annuitant, the annuity ceases.

7. Under option (vii) annuity ceases. Full annuity is payable to the surviving named spouse during his/ her life time and purchase price is paid to the nominee after the death of the spouse. If the spouse predeceases the annuitant, the annuity ceases and purchase price will be paid to the nominee.

When first installment of annuity payable:

First installment of annuity is payable after one month, three months, six months or one year from the date of purchase of annuity depending on the mode chosen is monthly, quarterly, half yearly or yearly respectively.

Pension Plans - New Jeevan Nidhi (UIN:512N271V01)

LIC's New Jeevan Nidhi Plan is a conventional with profits pension plan which provides for death cover during the deferment period and offers annuity on survival to the date of vesting.

1. Eligibility Conditions and Other Restrictions (For Basic Plan):

a) Minimum Basic Sum Assured : Rs.1,00,000 under Regular Premium policies

Rs.1, 50,000 under Single Premium policies

b) Maximum Basic Sum Assured : No Limit

(The Sum Assured shall be in multiples of Rs.5000/-)

c) Minimum Entry Age : 20 years (nearest Birthday)

d) Maximum Entry Age : 60 years (nearest birthday)

e) Policy Term : 5 to 35 years

f) Minimum Vesting Age : 55 years (nearest birthday)

g) Maximum Vesting Age : 65 years (nearest Birthday)

2. Payment of Premiums:

Premiums can be paid regularly at yearly, half-yearly, quarterly or monthly (through ECS only) or through SSS mode over the term of policy. Alternatively, a single premium can be paid.

A grace period of one calendar month but not less than 30 days will be allowed for payment of yearly or half-yearly or quarterly premiums and 15 days for monthly premiums.

3. Sample Premium Rates:

Following are some of the sample premium rates (exclusive of service tax) per Rs. 1000/- S.A.:

4. Mode and High S.A. Rebates:

Mode Rebate:

Yearly - 2% of tabular premium

Half-Yearly - 1% of tabular premium

Quarterly - Nil

Sum Assured Rebate:

For Regular Premium policies:

Sum Assured Rebate

1, 00,000 to 2, 95,000 Nil3, 00,000 and above 2%o S.A.

For Single Premium Policies:

Sum Assured Rebate

1, 50,000 to 2, 95,000 Nil3, 00,000 and above 5%o S.A.

5. Revival:

If premiums are not paid within the grace period then the policy will lapse. A lapsed policy can be revived from the date of first unpaid premium and before the date of vesting by paying all the arrears of premium together with interest within a period of five years, subject to submission of satisfactory evidence of

Single PremiumsAge at entry Policy term

10 20 3025 - - 435.8035 - 612.00 456.1545 852.55 632.80 -

Annual PremiumsAge at entry Policy term

10 20 3025 - - 32.7535 - 53.60 34.8045 115.25 57.15 -

continued insurability.

The Corporation reserves the right to accept at original terms, accept at revised terms or decline the revival of a discontinued policy. The revival of discontinued policy shall take effect only after the same is approved by the Corporation and is specifically communicated to the life assured. Accident Benefit Rider, if opted for, shall be revived along with the basic plan and not in isolation.

6. Policy Loan:

No loan facility will be available under this plan.

7. Service Tax:

Service tax, if any, shall be as per the Service Tax laws and the rate of service tax as applicable from time to time.

The amount of service tax as per the prevailing rates shall be payable by the policyholder on premium(s) as and when the premiums are paid.

8. Cooling-off period:

If the Life Assured is not satisfied with the 'Terms and Conditions' of the policy, he/she may return the policy to the Corporation within 15 days from the date of receipt of the policy stating the reason of objections. On receipt of the same the Corporation shall cancel the policy and return the amount of premium deposited after deducting the risk premium, expenses incurred on medical examination and stamp duty.

9. Exclusion:

Suicide: This policy shall be void if the Life Assured commits suicide (whether sane or insane at that time) at any time within one year from the date of commencement of risk and the Corporation will not entertain any other claim by virtue of this policy except to the extent of a maximum of 90% of single premium paid excluding any extra premium (in case of single premium policies).

LIC New Jeevan Nidhi Plan

27,087 Views

27,087 Views

LIC New Jeevan Nidhi Plan

LIC New Jeevan Nidhi Plan is a deferred annuity plan with bonus. This is a non unit-linked insurance pension plan. This plan is purchased to cover the risk of living too long and hence has multiple pension options to cover that risk. The corpus that is created to provide pension for old age is the Sum Assured + Accrued Guaranteed Additions + Simple Reversionary Bonus + Terminal Bonus. The age where pension is payable is called Vesting Age and the date when pension starts is called Vesting Date.

Key Features of LIC New Jeevan Nidhi Plan

Deferred annuity plan with bonus facility Guaranteed Additions available for the first 5 years Offers Bonus from the 6th year onwards Optional cover of Accidental Death and Disability Benefit rider available Large sum assured rebate

Benefits you get from LIC New Jeevan Nidhi Plan

Death Benefit – In case of death of the Life Insured before the vesting date, but

Within the first 5 years of the policy: provided all premiums have been paid, the nominee will be provided the Basic Sum Assured + accrued Guaranteed Additions which can be paid in a lumpsum or as annuity or a combination of the two.

After the first 5 years of the policy: provided all premiums have been paid, the nominee will be provided the Basic Sum Assured + accrued Guaranteed Additions + Simple Reversionary + Final Additional Bonus, if any, which can be paid in a lumpsum or as annuity or a combination of the two.

In case of death of the Life Insured after the vesting date, it entirely depends upon pension option chosen.

Vesting Benefit – At the time of vesting, there are 3 choices

Withdraw 1/3rd of the entire corpus tax free and then purchase an Immediate Annuity Plan from the remaining amount at the prevailing annuity rates

Buy an Immediate Annuity Plan from the entire amount at the prevailing annuity rates

Buy a Single Premium Deferred Annuity Plan

Immediate Annuity Plan can be purchased only from LIC of India and the vesting option can be chosen from the available options at that time and it cannot be ascertained now.

Income Tax Benefit – Premiums paid under life insurance policy are exempted from tax under Section 80 C and 1/3rd of the maturity proceeds are exempted from tax under Section 10(10A). Pension amount will be taxable.

Eligibility conditions and other restrictions in LIC New Jeevan Nidhi Plan

Minimum Maximum

Basic Sum Assured (in Rs.)1,00,000 for Regular

Premium and 1,50,000 for Single Premium

No Limit

Deferment Period (in years)7 for Regular Premium

5 for Single Premium35

Premium Payment Term (in years) Single Regular

Entry Age (in years) 2058 for Regular Premium

and 60 for Single Premium

Age at Vesting (in years) 55 65

Premium (in Rs.)10,000 for Single

3000 for RegularNo Limit

Payment modes Single, Yearly, Half-yearly, Quarterly, Monthly and SSS

Sample illustration of LIC New Jeevan Nidhi Plan

The below illustration is for a healthy Male of 35 years (non-tobacco user) opting for Sum Assured of Rs 1,00,000 and Deferment Period of 20 and 30 years respectively.

Additional Features and Benefits of LIC New Jeevan Nidhi Plan

Riders - There is 1 additional rider available:

Accidental Death and Disability Benefit rider

What happens if?

You stop paying the premium –If the premiums are not paid within the grace period, the policy lapses and all benefits cease. However, there the policy can be revived within 2 years from the date of first unpaid premium.

You want to surrender the policy – There is a Guaranteed Surrender Value in this plan

Single Premium Policies: The policy can be surrendered at any time during the deferment period and the Guaranteed Surrender Value would be:

Within 3 policy years would be 70% of the Single Premium Paid excluding taxes and extra premium, if any and

After 3 policy years would be 90% of the Single Premium Paid excluding taxes and extra premium, if any

Regular Premium Policies:

For deferment period less than 10 years: The policy can be surrendered provided the premiums have been paid for at least two consecutive years.

For deferment period 10 years or more: The policy can be surrendered provided the premiums have been paid for at least three consecutive years.

The Guaranteed Surrender Value is a percentage of total premiums paid excluding taxes, extra premiums, if any and rider premium and it depends on the deferment period and the policy year in which the policy is surrendered.

You want a loan against your policy – Loan facility is not available under this policy

Alternate deferred annuity plans from different insurance companies

Aviva Next Innings Pension Plan

Future Generali Pension Guarantee

HDFC Life Personal Pension Plus

Other annuity plans from Life Insurance Corporation of India

LIC Jeevan Akshay VI Plan

Leave a Comment

Show Comments

Pension Plans - New Jeevan Nidhi (UIN:512N271V01)

LIC's New Jeevan Nidhi Plan is a conventional with profits pension plan which provides for death cover during the deferment period and offers annuity on survival to the date of vesting.

1. Benefits:

a. Benefit on Vesting : On vesting an amount equal to the Basic Sum Assured along with accrued Guaranteed Additions, vested Simple Reversionary bonuses and Final Additional bonus, if any, shall be made available to the Life Assured.

The following options shall be available to the Life Assured for utilization of the benefit amount.

1. To purchase an immediate annuity

The Life Assured shall have a choice to commute the amount available

on vesting to the extent allowed under Income Tax Act. The entire

amount available on vesting or the balance amount after commutation,

as the case may be, shall be utilized to purchase immediate annuity at

the then prevailing annuity rates. Commutation shall only be allowed

provided the balance amount is sufficient to purchase a minimum

amount of annuity as per the provisions of section 4 of Insurance Act,

1938.

In case the total benefit amount is insufficient to purchase the

minimum amount of annuity, then the said amount shall be paid as a

lump sum to the Life assured.

The annuity shall only be purchased from Life Insurance Corporation

of India.

or

2. To purchase a new Single Premium deferred pension product

from Life Insurance Corporation of India

Under this option the entire proceeds available on vesting shall be

utilized to purchase a single premium deferred pension product

provided the policyholder satisfies the eligibility criteria for purchasing

single premium deferred pension product.

The Life Assured will have to intimate his / her intention to go for a particular option available on the date of vesting atleast six months prior to

the date of vesting.

b. Death Benefit :

Death during first five policy years: Basic Sum Assured along with accrued Guaranteed Addition shall be paid as lump sum or in the form of an annuity or partly in lump sum and balance in the form of an annuity to the nominee.

Death after first five policy years: Basic Sum Assured along with accrued Guaranteed Addition, Simple Reversionary and Final Additional Bonus, if any, shall be paid as lump sum or in the form of an annuity or partly in lump sum and balance in the form of an annuity to the nominee.

The amount of annuity will depend on the payable lump sum and the then prevailing immediate annuity rates.

c. Guaranteed Additions : The policy provides for Guaranteed Additions @ Rs.50/- per thousand Sum assured for each completed year, for the first five years.

d. Participation in profits : The policy shall participate in profits of the Corporation from the 6th year onwards and shall be entitled to receive Simple Reversionary bonuses declared as per the experience of the Corporation, provided the policy is in full force.

Final Additional Bonus may also be declared in addition.

2. Optional Benefit:

Accident Benefit Rider: Accident Benefit Rider is available as an optional rider by payment of additional premium under regular premium policies. In

case of accidental death, the Accident Benefit Rider Sum Assured will be payable as lumpsum along with the death benefit under the basic plan. In case of accidental disability arising due to accident (within 180 days from the date of accident), an amount equal to the Accident Benefit Sum Assured will be paid in monthly instalments spread over 10 years and future premiums shall be waived. If the policy becomes a claim either by way of death or the policy vests before the expiry of the said period of 10 years, the disability benefit instalments which have not fallen due will be paid in lump sum.

The Accident Benefit Sum Assured may be opted for an amount upto the Basic Sum Assured subject to minimum of Rs. 25,000 and maximum of Rs. 50 lakh (including all policies with LIC of India and other insurers). This benefit will be available only till the age nearer birthday of the Life assured is 65 yrs or till the vesting age, whichever is earlier.

3. Paid-up Value:

Under regular premium policies, if after atleast three full year's premiums have been paid and any subsequent premium be not duly paid, this Policy shall not be wholly void but the Sum Assured under basic plan shall be reduced to such a sum, called the paid-up sum assured, as shall bear the same ratio to the full Sum Assured as the number of premiums actually paid shall bear to the total number of premiums originally stipulated for in the Policy. The policy so reduced shall thereafter be free from all liability for payment of the within-mentioned premium but shall not be entitled to guaranteed additions and any bonuses in future. The accrued guaranteed additions and vested bonus additions, if any, will remain attached to the reduced paid-up policy.

This paid-up sum assured alongwith the accrued Guaranteed Additions and vested Simple Reversionary Bonuses, if any, is payable on the date of vesting or on Life Assured's prior death.

On the death of the Life Assured, the nominee shall have an option to take the proceeds as lump sum or in the form of an annuity or partly in lump sum and balance in the form of an annuity.

On vesting the proceeds shall be payable as per one of the options as specified

against para 1.a. above.

Accident Benefit rider do not acquire any paid-up value.

4. Surrender Value:

The policy can be surrendered at any time after completion of at least 3 policy

years but before the date on which annuity vests.

The Guaranteed Surrender Value will be as under:

i) Single Premium Policies: The Guaranteed Surrender value is equal to 90% of the premium paid excluding extras, if any.

ii) Regular Premium Policies: The Guaranteed Surrender Value will be available provided atleast three full years' premiums have been paid and is equal to 30% of the premiums paid excluding the premium paid for the first year and all premiums in respect of optional rider and extras, if any.

The surrender value shall be the guaranteed surrender value along with cash value of any accrued Guaranteed Additions and vested simple reversionary bonuses, if any.

Corporation may, however, pay Special Surrender value, as the discounted value of the paid-up sum assured (as specified in para 8), accrued Guaranteed Additions and vested Simple Reversionary Bonuses, if any, as applicable on date of surrender, provided the same is higher than Guaranteed Surrender value.

The following options shall be available to the Life Assured for utilization of the

Surrender proceeds:

1. To purchase an immediate annuity

The Life Assured shall have a choice to commute the amount available

on surrender to the extent allowed under Income Tax Act. The entire

amount available on surrender or the balance amount after

commutation, as the case may be, shall be utilized to purchase

immediate annuity at the then prevailing annuity rates. Commutation

shall only be allowed provided the balance amount is sufficient to

purchase a minimum amount of annuity as per the provisions of

section 4 of Insurance Act, 1938.

In case the total benefit amount is insufficient to purchase the

minimum amount of annuity, then the said amount shall be paid as a

lump sum to the Life assured.

The annuity shall only be purchased from Life Insurance Corporation

of India.

or

2. To purchase a new Single Premium deferred pension product

from Life Insurance Corporation of India

Under this option the entire proceeds available on surrender may be utilized to purchase a single premium deferred pension product provided the policyholder satisfies the eligibility criteria for purchasing single premium deferred pension product

What is Child Insurance Plans?Child Insurance Plans are the best way for investing in your child's future. From a very early age of the child, the parent can invest fixed amounts every year which can be timed to mature when the child attains a certain age, say 18 years. Major events in the child's life, like marriage or higher studies can be planned and financed by Child Insurance Policies if the parent takes adequate plans at the right time. Plans can be purchased as soon as the Child is born.

In certain Child Plans there are built-in flexibilities which keep the policy active and waive off the premium even after the death of the parents. These options are extremely useful as no other financial instrument offers such flexible options. Most plans come with built-in riders or add-on covers such as Waiver of Premium benefit.

Types of Child Insurance Plans?Child Insurance Plans come in 2 variants:

Traditional Plans

Traditional plans in which the amount of payout is guaranteed. Here the investments are usually made in safe and low yielding products. The returns will not be great but they will be stable and predictable.

ULIPs

ULIPs - here the investments are more into equity markets and the chances of returns over a longer period of time are much higher. The policyholder can even choose to invest in debt instruments, in which case it becomes similar to the traditional plans investments. The flexibility is completely in the hands of the investor and one can switch between the types of funds also.