Embed Size (px)

Citation preview

Legislative & Regulatory

Updates

Tuesday, July 21, 2015

Amanda V. Green, Esq.Vice President of Operations & ComplianceShapiro Kreisman & Associates, [email protected]

SESSION SPEAKERS

Kristina G. Murtha, Esq. Managing Attorney, New JerseyKivitz McKeever Lee, [email protected]

Eric RosenkoetterDirector of Government AffairsNational Association of Retail Collection Attorneys (NARCA)[email protected]

Matt Hunoval, Esq.FounderThe Hunoval Law Firm, [email protected]

You can submit them by:

• Texting 66364 and your question to 22333

• Ask questions or make comments verbally by using the microphones provided in the session room

Questions for the Panelists?

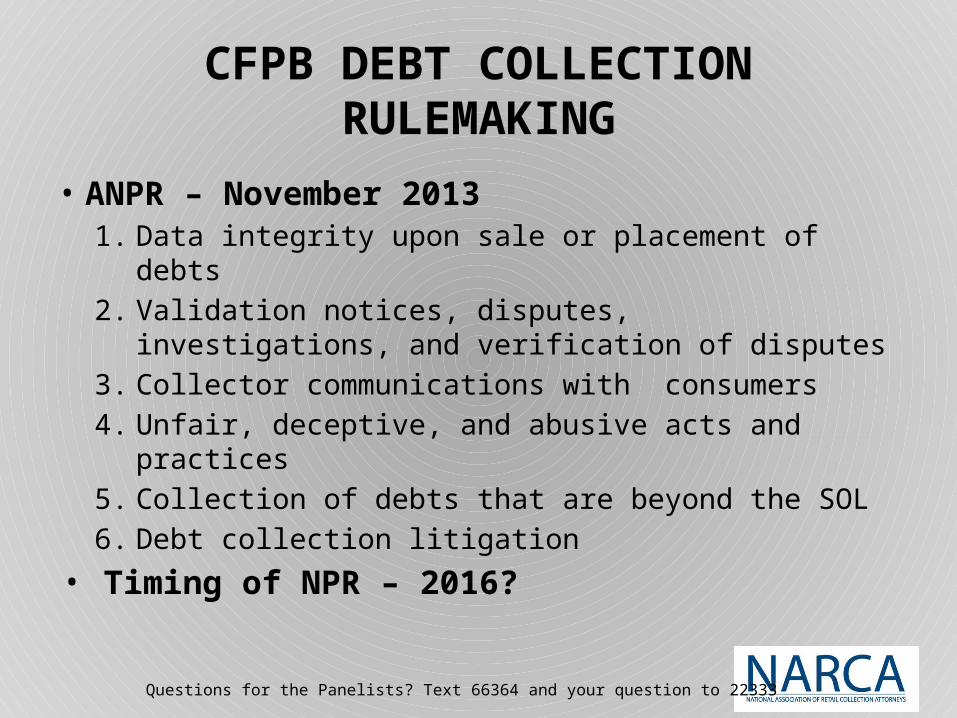

CFPB DEBT COLLECTION RULEMAKING

• ANPR – November 20131. Data integrity upon sale or placement of

debts2. Validation notices, disputes, investigations,

and verification of disputes3. Collector communications with consumers4. Unfair, deceptive, and abusive acts and

practices5. Collection of debts that are beyond the SOL6. Debt collection litigation

• Timing of NPR – 2016?Questions for the Panelists? Text 66364 and your question to 22333

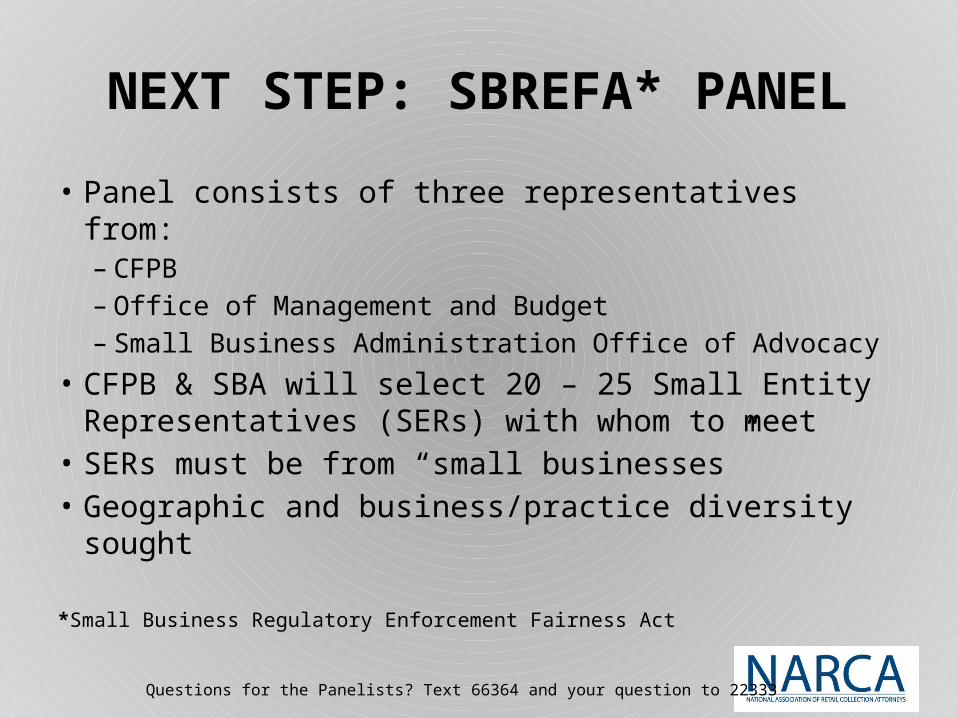

NEXT STEP: SBREFA* PANEL

• Panel consists of three representatives from:– CFPB– Office of Management and Budget– Small Business Administration Office of Advocacy

• CFPB & SBA will select 20 – 25 Small Entity Representatives (SERs) with whom to meet

• SERs must be from “small businesses”• Geographic and business/practice diversity

sought

*Small Business Regulatory Enforcement Fairness Act

Questions for the Panelists? Text 66364 and your question to 22333

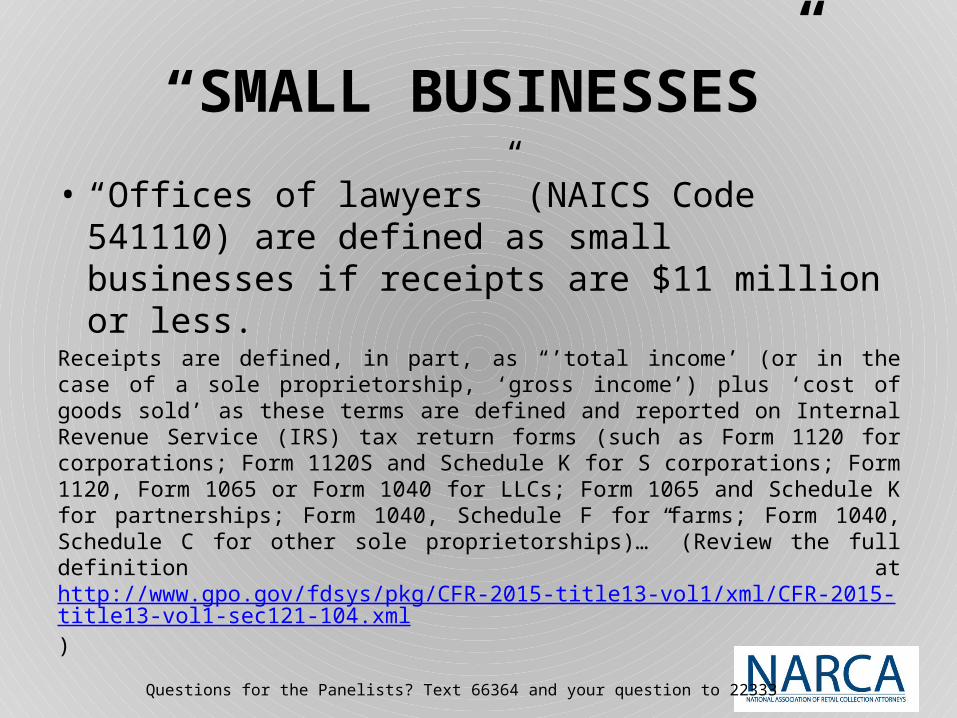

“SMALL BUSINESSES”

• “Offices of lawyers” (NAICS Code 541110) are defined as small businesses if receipts are $11 million or less.

Receipts are defined, in part, as “’total income’ (or in the case of a sole proprietorship, ‘gross income’) plus ‘cost of goods sold’ as these terms are defined and reported on Internal Revenue Service (IRS) tax return forms (such as Form 1120 for corporations; Form 1120S and Schedule K for S corporations; Form 1120, Form 1065 or Form 1040 for LLCs; Form 1065 and Schedule K for partnerships; Form 1040, Schedule F for farms; Form 1040, Schedule C for other sole proprietorships)…” (Review the full definition at http://www.gpo.gov/fdsys/pkg/CFR-2015-title13-vol1/xml/CFR-2015-title13-vol1-sec121-104.xml)

Questions for the Panelists? Text 66364 and your question to 22333

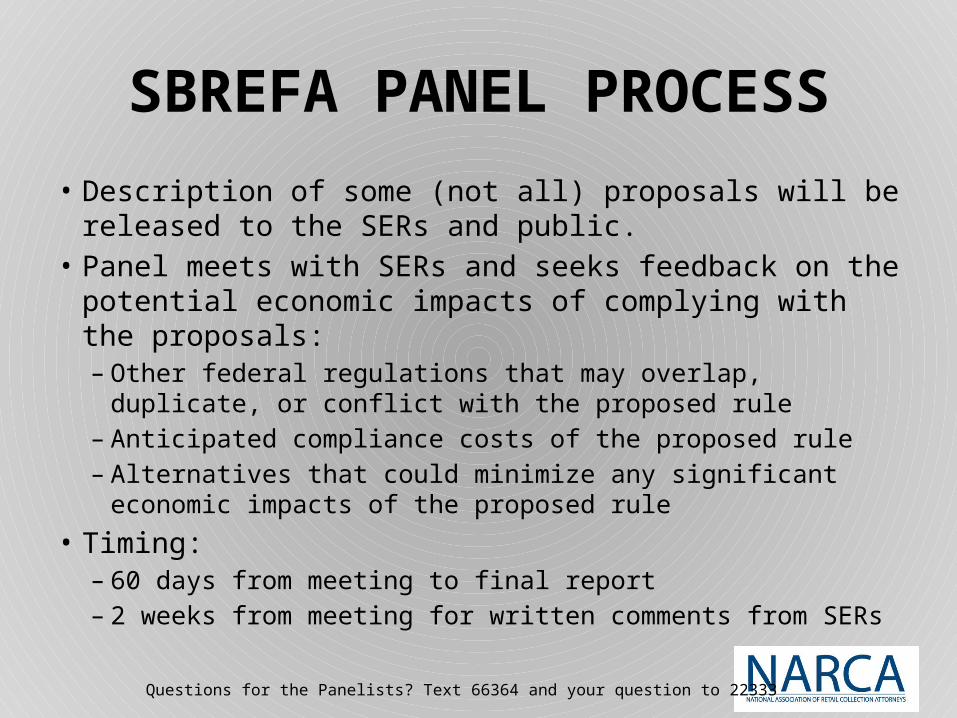

SBREFA PANEL PROCESS

• Description of some (not all) proposals will be released to the SERs and public.

• Panel meets with SERs and seeks feedback on the potential economic impacts of complying with the proposals:– Other federal regulations that may overlap, duplicate, or

conflict with the proposed rule– Anticipated compliance costs of the proposed rule– Alternatives that could minimize any significant economic

impacts of the proposed rule

• Timing:– 60 days from meeting to final report– 2 weeks from meeting for written comments from SERs

Questions for the Panelists? Text 66364 and your question to 22333

SBREFA PANEL CONSIDERATIONS

• Provides an early look at the proposals under consideration

• Opportunity for companies, small and large, to develop and present metrics (usually through their respective trade associations)

• Coordination of SERs on main themes is valuable prior to the meeting

• Metrics are essential, and the sooner the better

Questions for the Panelists? Text 66364 and your question to 22333

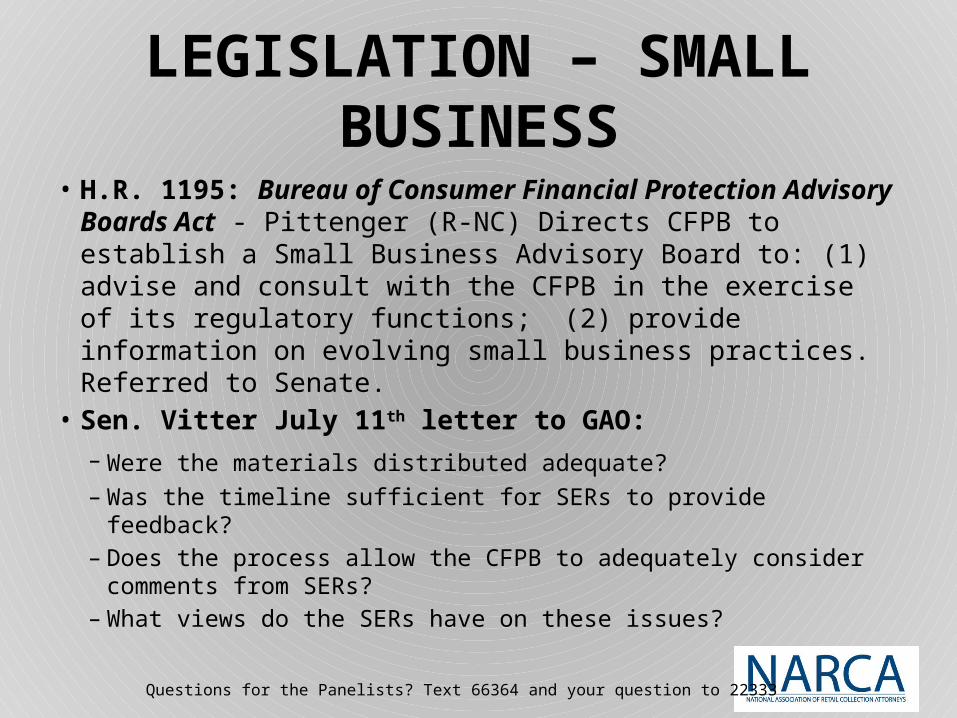

LEGISLATION – SMALL BUSINESS

• H.R. 1195: Bureau of Consumer Financial Protection Advisory Boards Act - Pittenger (R-NC) Directs CFPB to establish a Small Business Advisory Board to: (1) advise and consult with the CFPB in the exercise of its regulatory functions; (2) provide information on evolving small business practices. Referred to Senate.

• Sen. Vitter July 11th letter to GAO: – Were the materials distributed adequate?– Was the timeline sufficient for SERs to provide feedback?– Does the process allow the CFPB to adequately consider

comments from SERs?– What views do the SERs have on these issues?

Questions for the Panelists? Text 66364 and your question to 22333

SBREFA PANEL PROCESS

• Description of some (not all) proposals will be released to the SERs and public.

• Panel meets with SERs and seeks feedback on the potential economic impacts of complying with the proposals:– Other federal regulations that may overlap, duplicate, or

conflict with the proposed rule– Anticipated compliance costs of the proposed rule– Alternatives that could minimize any significant economic

impacts of the proposed rule

• Timing:– 60 days from meeting to final report– 2 weeks from meeting for written comments from SERs

Questions for the Panelists? Text 66364 and your question to 22333

SBREFA PANEL CONSIDERATIONS

• Provides an early look at the proposals under consideration

• Opportunity for companies, small and large, to develop and present metrics (usually through their respective trade associations)

• Coordination of SERs on main themes is valuable prior to the meeting

• Metrics are essential, and the sooner the better

Questions for the Panelists? Text 66364 and your question to 22333

LEGISLATION – SMALL BUSINESS

• H.R. 1195: Bureau of Consumer Financial Protection Advisory Boards Act - Pittenger (R-NC) Directs CFPB to establish a Small Business Advisory Board to: (1) advise and consult with the CFPB in the exercise of its regulatory functions; (2) provide information on evolving small business practices. Referred to Senate.

• Sen. Vitter July 11th letter to GAO: – Were the materials distributed adequate?– Was the timeline sufficient for SERs to provide feedback?– Does the process allow the CFPB to adequately consider

comments from SERs?– What views do the SERs have on these issues?

Questions for the Panelists? Text 66364 and your question to 22333

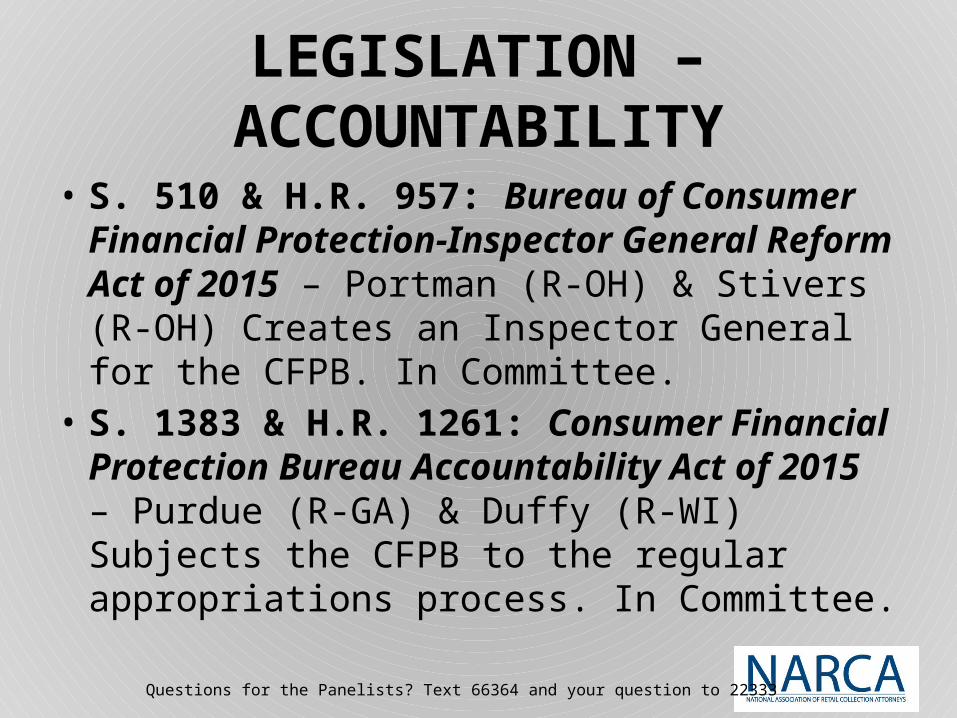

LEGISLATION – ACCOUNTABILITY

• S. 510 & H.R. 957: Bureau of Consumer Financial Protection-Inspector General Reform Act of 2015 – Portman (R-OH) & Stivers (R-OH) Creates an Inspector General for the CFPB. In Committee.

• S. 1383 & H.R. 1261: Consumer Financial Protection Bureau Accountability Act of 2015 – Purdue (R-GA) & Duffy (R-WI) Subjects the CFPB to the regular appropriations process. In Committee.

Questions for the Panelists? Text 66364 and your question to 22333

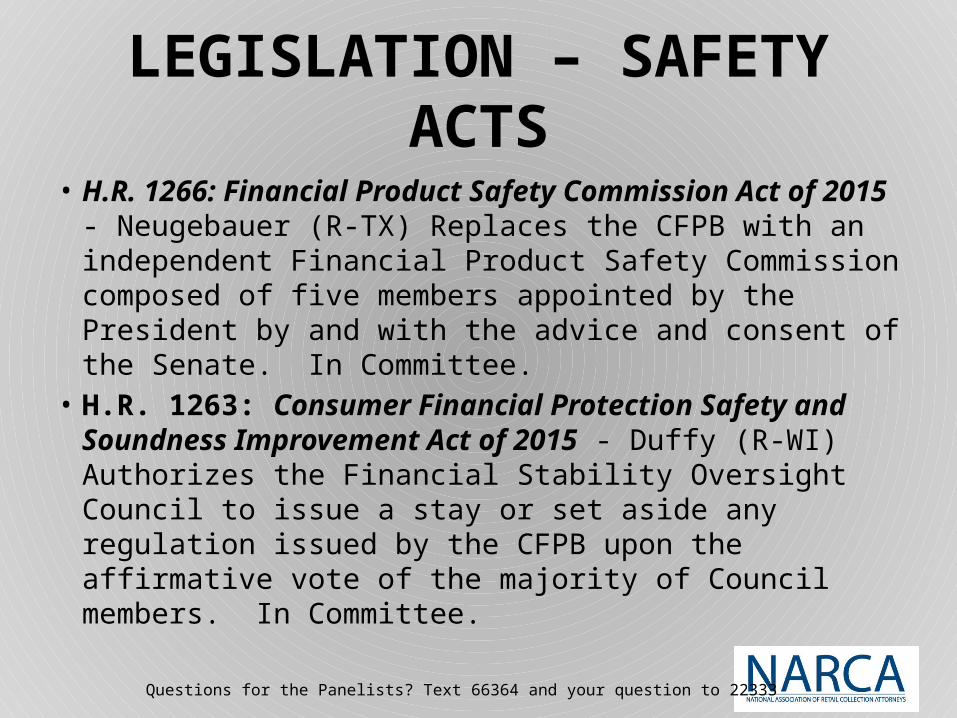

LEGISLATION – SAFETY ACTS

• H.R. 1266: Financial Product Safety Commission Act of 2015 - Neugebauer (R-TX) Replaces the CFPB with an independent Financial Product Safety Commission composed of five members appointed by the President by and with the advice and consent of the Senate. In Committee.

• H.R. 1263: Consumer Financial Protection Safety and Soundness Improvement Act of 2015 - Duffy (R-WI) Authorizes the Financial Stability Oversight Council to issue a stay or set aside any regulation issued by the CFPB upon the affirmative vote of the majority of Council members. In Committee.

Questions for the Panelists? Text 66364 and your question to 22333

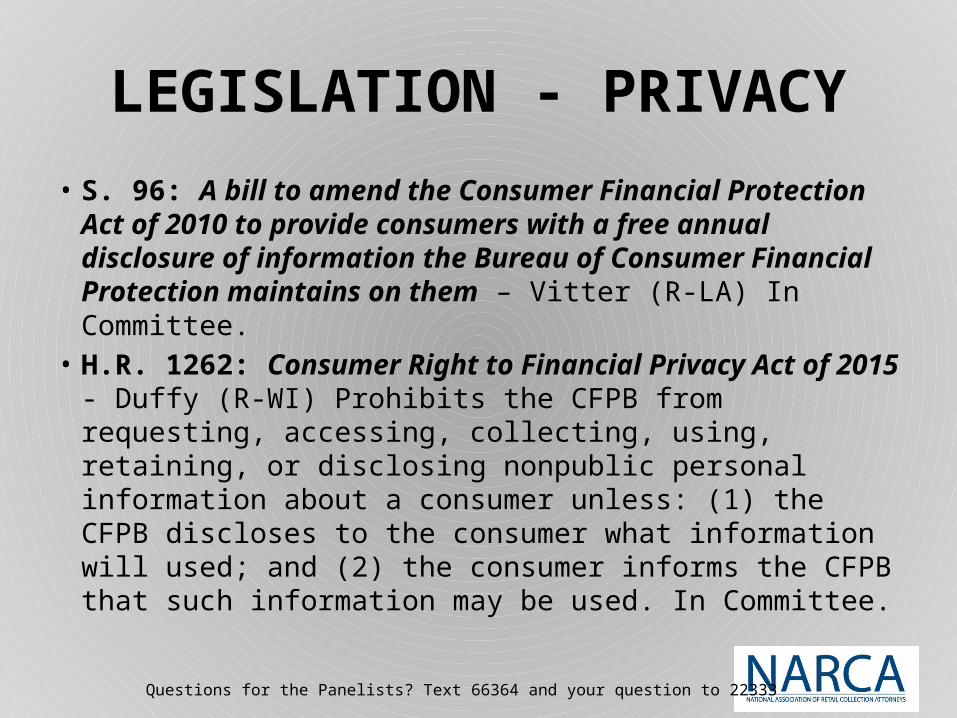

LEGISLATION - PRIVACY

• S. 96: A bill to amend the Consumer Financial Protection Act of 2010 to provide consumers with a free annual disclosure of information the Bureau of Consumer Financial Protection maintains on them – Vitter (R-LA) In Committee.

• H.R. 1262: Consumer Right to Financial Privacy Act of 2015 - Duffy (R-WI) Prohibits the CFPB from requesting, accessing, collecting, using, retaining, or disclosing nonpublic personal information about a consumer unless: (1) the CFPB discloses to the consumer what information will used; and (2) the consumer informs the CFPB that such information may be used. In Committee.

Questions for the Panelists? Text 66364 and your question to 22333

CFPB 2015 Proposed Amendments

A.Background

B. Proposed changes reviewed in this session:

1. successors in interest; and 2. loan modifications for files

that are service transferred, also called “in flight” modifications.

Questions for the Panelists? Text 66364 and your question to 22333

CFPB 2015 Proposed Amendments

C. Successors in Interest 1. Current Rules 2. Proposed 2015 amendments

i. Who qualifies ii. Communication with a

Potential SII iii. Protections that Apply to

a Confirmed SII

Questions for the Panelists? Text 66364 and your question to 22333

CFPB 2015 Proposed Amendments

D. Mortgage Servicing Transfers 1. Current Rules 2. Proposed Amendments re:

Servicing Transfers and Loss Mitigation

i. Timeframes ii. Exceptions iii. Goal

Questions for the Panelists? Text 66364 and your question to 22333

PPTFA

A. Background

B. Proposed legislation: PPTFA

C. Alternatives to PPTFA

D. Website: http://nhlp.org/node/1341

Questions for the Panelists? Text 66364 and your question to 22333

TRID

A. Background

B. Amendment

C. Documents a. Loan Estimate (three days after

loan application) b. Closing Disclosure (three days

before closing)

Questions for the Panelists? Text 66364 and your question to 22333

TRID

D. Issues with implementation a. Scope of business affected b. Operational changes required c. Systems changes required

E. Timing a. Effective date: August 1, 2015 b. Delayed effective date: October 3, 2015

F. Resources

Questions for the Panelists? Text 66364 and your question to 22333

Legislation We’re Watching:Financial Regulatory Improvement Act of 2015 (S. 1418)

A broad, legislative package aimed at providing commonsense fixes to Dodd Frank, including:

• Extending the examination cycle for community banks• Helping rural consumers get mortgages• Safe harbor for mortgages held in a bank’s portfolio• Reduces unnecessary costs from stress testing

community banks• Establishes a process for federal regulators to evaluate

institutions to determine whether to designate them as systemically important

• Sponsor: Shelby/AL (R)

Questions for the Panelists? Text 66364 and your question to 22333

Legislation We’re Watching:Mortgage Servicing Asset Capital Requirements Act of 2015 (H.R. 1408)

Bill would allow regulators will have six months to study and report back to Congress on many outstanding questions about the mortgage servicing industry including:

• How the assets performed during the financial crisis• The ability to establish a value and liquidity for MSAs• The ability of regulated banks to service mortgages they

originate

• Sponsor: Perlmutter/CO-7 (D)• Co-Sponsor(s): Luetkemeyer/MO-3 (R)

Hill/AR-2 (R)

Questions for the Panelists? Text 66364 and your question to 22333

Legislation We’re Watching:Bureau of Consumer Financial Protection-Inspector General Reform

Act of 2015 (S. 510) Bureau of Consumer Financial Protection-Inspector General Reform Act of 2015 (H.R. 958)

• Under current law, the CFPB has to share an IG with the

Federal Reserve.• Unlike most major agency IGs, the Federal Reserve IG is a

“designated federal entity IG” hired by the Fed Chairman, rather than appointed by the President with the advice and consent of the Senate.

• Sponsor: Stivers/OH-15 (R)• Co-Sponsor(s): Luetkemeyer/MO-3 (R)

Hill/AR-2 (R) Royce/CA-39 (R) Walz/MN-1 (D) Wagner/MO-2 (R) Trott/MI-11 (R) Rothfus/PA-12 (R)

Bills would create the position of an independent Inspector General for CFPB:

Questions for the Panelists? Text 66364 and your question to 22333

Legislation We’re Watching:Illinois HB 2814

• The Illinois Appellate Court ruled in March 2014 that a mortgage is void if the originating lender was not licensed (or exempt) under the Illinois Residential Mortgage Licensing Act of 1987 at the time the loan originated. See. First Mortgage Company, LLC v. Gratzielda Dina, 2014 IL App (2d) 130567. This case has created a new line of mortgage foreclosure defense strategy.

• Recently, Judge Otto in Cook County expanded the holding of Dina to say that if any lender in the chain of title was not properly registered, then the mortgage is declared void.

• The Illinois Department of Financial & Professional Regulation has a website that can be searched to ensure the originating lender was licensed if they are not an exempt entity.– www.idfpr.com

• HB 2814 is proposed legislation that would override the holding in Dina by amending the Residential Mortgage License Act of 1987 to provide that a mortgage loan brokered, funded, originated, serviced, or purchased by a party who is not licensed shall not be held to be invalid solely on the basis of specified violations of the Act.

• The bill passed both the House and Senate and is currently with the Governor awaiting signature. It is unclear at this time whether this law will be enacted.

Legislation We’re Watching:Ohio HB134

Vacant and Abandoned Properties – Summary Foreclosure Actions

• HB134 (which is in committee) –Introduced 3/25/2015 and referred to the Financial Institutions Housing and Urban Development Committee on 4/14/2015

• This bill makes changes to judicial foreclosure actions in Ohio. It permits the holder of a mortgage note to bring a summary foreclosure action against residential property that appears to be “vacant and abandoned”.

• The bill modifies the procedures that generally apply to the judicial sale of property.

• The bill creates a pilot program for “unoccupied, blighted” property, under which a municipal corporation may seek an order for remediation against the owner of the property.

• The bill also expands the jurisdiction of the Toledo Municipal Court over certain real property actions and expands the responsibilities of the clerk of common please related to the filing of a judgment of foreclosure.

Questions for the Panelists? Text 66364 and your question to 22333

Legislation Update:Ohio HB9

• HB9 (Enacted)- To amend sections 317.08, 2333.22, 2715.21, 2735.01, 2735.02, 2735.04, and 5301.09 of the Ohio Revised Code to add to and clarify the powers of a receiver, to provide a procedure for a receiver's sale of property, to specify that a lease of natural gas and petroleum is an interest in real estate, and to establish a Study Committee on Receivership Laws to study matters related to receiverships and payment of public utility services

Questions for the Panelists? Text 66364 and your question to 22333

Legislation Update:Indiana SB-415

Vacant and Abandoned Housing (SB-415):

Establishes that the State of Indiana is the sole regulator of the mortgage foreclosure process. This law preempts all other regulation(s) of the mortgage foreclosure process by a political subdivision (municipal corporation or special taxing district). A political subdivision cannot create ordinances imposing reporting requirements or any other obligations upon mortgage lenders/servicers regarding vacant and abandoned properties.

This bill was signed by the governor, and became law on May 6, 2015. This law is effective July 1, 2015.

Questions for the Panelists? Text 66364 and your question to 22333

Legislation Update:MINNESOTA STATUTE § 580.033

WHERE NOTICE PUBLISHED

• The Minnesota State Legislature added this statute providing that the qualified newspaper where the Notice of Sale is published must have its known office of issue either:– Where the mortgaged premises is located;– Where part of the mortgaged premises is located; or– In an adjoining county with circulation in the County where the mortgaged premises is located.

• Known Office of Issue is defined in Minn. Stat. 331A.01, subdivision 2 to mean the newspaper’s principal office devoted primarily to business related to the newspaper. A newspaper may only have one (1) known office of issue.

• Qualified newspaper is defined in Minn. Stat. 331A.01, subdivision 8, as a newspaper which complies with the requirements of 331A.02. [These specific statutes may be provided upon request.]

• The statute also requires that the Affidavit of Publication list where the known office of issue is located and that the newspaper complies with the provisions in the statute.

• This statute is effective July 1, 2015 and applies to foreclosures where the Notice of Pendency is recorded on or after that date.

Legislation Update:MINNESOTA STATUTE § 582.25 –

MORTGAGES; VALIDATING FORECLOSURE SALES

• This statute is commonly known within the state as the “curative” statute. It provides that certain defects in the foreclosure process will cure if an action alleging the defect is not commenced by the mortgagor within the specified time frame.

• The legislature added subdivision 24 relating to Minn. Stat. 580.033. If the publication of the notice of sale does not comply with Minn. Stat. 580.033 the borrower will have until 1 year following the expiration of the redemption period to bring a claim. If they fail to do so, this issue is considered cured and no longer an issue.

• This statute was also revised to add a subdivision allowing a curative provision if the notice of postponement of the sheriff’s sale was not timely or properly mailed or published.

• This statute is effective July 1, 2015 and applies to foreclosures where the Notice of Pendency is recorded on or after that date.

Legislation Update:MINNESOTA STATUTE § 580.07, Subd. 2

POSTPONEMENT BY MORTGAGOR OR OWNER

• This statute was revised to include subdivision 2 (2)(c) which clarifies that the mortgagor’s redemption period is reduced only for the foreclosure action where the Affidavit was filed. For any subsequent foreclosure actions the reduction period reverts back to the full time period. The exception is for circumstances where a bankruptcy is filed after the Affidavit of Postponement is filed invoking the automatic stay,

• This section is effective May 2, 2015 and applies to mortgages executed before, on or after that date.

Legislation Update:MINNESOTA STATUTE § 580.30

REINSTATEMENT

• This statute was revised to add requirements on when a reinstatement quote must be sent. The mortgagee is to provide the reinstatement quote to the borrower within three days of the request for figures. If the reinstatement quote is not mailed within three days of receipt of the request it will not invalidate the foreclosure sale and there will not be any liability assessed to the party foreclosing or its attorney. Further, the party foreclosing does not have an obligation to postpone the foreclosure sale in order to comply, if they request is made less than 3 days prior to sale. The reinstatement amount is effective for seven days after the quote is provided or until the date of the foreclosure sale, whichever occupies first.