Embed Size (px)

DESCRIPTION

Lecture 1: Money, Banking & Financial Markets Why Study Financial Markets? 1.Channel funds from savers to investors, thereby promoting economic efficiency 2.Affect personal wealth and behavior of business firms Bond Market - where corporations and governments borrow funds - PowerPoint PPT Presentation

Citation preview

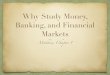

Number of Bank Failures Per Year

411

3 4 0 3

25

140

157

92

51

00

25

50

75

100

125

150

175

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Source: FDIC

Lecture 1: Money, Banking & Financial Markets

Why Study Financial Markets?

1. Channel funds from savers to investors, thereby promoting economic efficiency

2. Affect personal wealth and behavior of business firms

Bond Market

- where corporations and governments borrow funds

- where interest rates are determined

- affects consumers willingness to spend & save

- affects business spending decisions

Stock Market

- affects personal wealth

- affects business investment decisions

Foreign Exchange Market

- used for transfer of funds between countries

- affects costs of imports & exports for domestic and foreign consumers

- affects competitiveness of domestic versus foreign businesses

The Circular Flow Diagram

Financial SystemFlow of Funds

Lenders/Savers•Firms•Households•Government•Foreigners

Financial Intermediaries•Banks•S&Ls•CUs

Financial Markets•Stock Market•Bond Market•FX Market

Borrowers/Spenders•Firms•Households•Government•Foreigners

$$

$$

Deposits

Securities

Securities

Securities

$$

$$

Direct Finance

Indirect Finance

Profit search is to moneywhat gravity is to water

The Heart Vs Bank AnalogyHow the Heart Works: Blood Flow DiagramHow Blood Flows Through a Healthy Heart.

Interest Rates and Recessions 1988-2013

0

1

2

3

4

5

6

7

8

9

10

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

0

1

2

3

4

5

6

7

8

9

10

Recession Baa Fed Funds 10-yr Treas

S&P 500 Stock Index(monthly average)

0

100

200

300

400

500

600

700

800

900

1000

1100

1200

1300

1400

1500

1600

1700

1800

1900

2000

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 140

1

2

3

4

5

6

7

8

9

10

Nominal Index Recession

Fed Funds Rate (RHS) Real Index

U.S. Dollar Versus Euro Exchange Rate

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

$1.10

$1.20

$1.30

$1.40

$1.50

$1.60

$1.70

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

Euro/$

Euro/$$/Euro

$/Euro

Quarterly % Change in U.S. Economic Output(Real GDP - Chainweighted 2005$)

2.7%2.6%3.0%

3.3%

4.2%

3.2%

2.1%

5.1%

1.6%

0.1%

2.7%

0.5%

3.6%

3.0%

1.7%

-1.8%

1.3%

-2.0%

-8.3%

-5.4%

-0.4%

1.3%

3.9%

1.6%

3.9%

2.8%2.8%

-1.3%

3.2%

1.4%

4.9%

3.7%

1.2%

2.8%

0.1%

1.1%

2.5%2.5%2.5%

3.5%3.5%3.5%3.5%

1.8%

-10%

-9%

-8%

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

04:1 05:1 06:1 07:1 08:1 09:1 10:1 11:01 12:01 13:01 14:01

Source: Department of Commerce.

Recession Factors:•Loose monetary policy•Poor regulation•Lax bank supervision•Opaque derivatives•Shadow banking system•Lax investor diligence•Poor governance•Misaligned incentives•fraud

2.5% Target

Consumer Price Index 1970 to Present

5.6

3.33.4

8.7

12.3

6.9

4.9

6.7

9.0

12.5

8.9

3.83.84.04.44.44.7

6.1

3.12.92.72.72.5

3.3

1.71.6

2.6

3.4

1.6

2.41.9

3.33.5

2.5

4.1

-0.1

2.8

1.4

3.0

1.71.8

3.8

1.1

13.3

-1

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12

Federal Reserve Balance Sheet (January 2010 vs July 2009 vs July 2008) ($ Billions, H.4.1 Release, Table 10)

Assets Liabilities + Capital

T-Bills (18/18/22) Federal Reserve Notes (879/870/793)T-Notes/Bonds (708/618/402) TIPS (47/48/40)

Depository Institution Deposits (1,135/809/23)Federal Agency Debt (161/102/0)Mortgage-Backed Securities (969/526/0)

Repurchase Agreements (0/0/117) Reverse Repurchase Agreements (64/66/43)

Term Auction Credit (76/274/150) U.S. Treasury, General Account (124/65/4) Primary Credit (18/34/14) U.S. Treasury, Supplementary Financing (5/200/0)Secondary Credit (1/0/0)Seasonal Credit (0/1/1)

Asset-backed CP MMMF Liquidity Facility (0/8/0)AIG Credit (25/43/0)Term Asset-back Security loan Facility ((298/26/0) Foreign Official Deposits (3/2/2)

Commercial Paper Funding LLC (14/111/0)Money Market Investor Funding (0/0/0)

Maiden Lane I, II, III LLC (64/60/29) Capital Paid In (26/25/5) Surplus (25/21/3)

Central Bank Liquidity Swaps (6/112/62) Other Capital (1/4/1)

Total Assets (2,295/2,074/913) Total Liabilities & Capital (2,295/2,074/913)

Italicized accounts represent new policy tools

M1, Monetary Base and Money Multiplier

0200400600800

1,0001,2001,4001,6001,8002,0002,2002,4002,6002,8003,0003,200

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

$ B

illi

on

0

1

2

3

4

Mo

ney

Mu

ltip

lier

MB Multiplier M1

Money Multiplier = M1/MB = 1 + c = 1+0.83 = 0.84 r + e + c 0.1+1.25+0.83

Money Supply Growth, M1&M2 (% change year ago)

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

Recession M2 M1

M/M + V/V = P/P + Y/YM/M + 0 = P/P + 3.0%

CurrencyCheckingSavingsMMAMMMFCD

Federal Government Surplus/Deficit(Billions of Dollars)

-74-79-128

-208-185-221

-150-155-153

-221-269-290

-255-203

-164-107

-22

69126

236

128

-158

-378-413

-318

-248

-161

-459

-1,400

-1,294-1,296

-1,079

-585

-345

-269-302

-220-196-258-280-279

-339

-212

-$1,500

-$1,250

-$1,000

-$750

-$500

-$250

$0

$250

$500

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 22

Source: Congressional Budget Office.

•Bank stock purchases (TARP)•Stimulus plan•Mortgage bailout plan•Income-support programs•Recession-induced falling revenues

Function of Financial IntermediariesFinancial Intermediaries

1. Engage in process of indirect finance

• borrow funds from savers, then lend funds to borrowers

• issue liabilities, then acquire assets

• take deposits, then make loans

2. More important source of finance than securities markets

3. Needed because of

• risk sharing

• asymmetric information

• transactions costs

UWCU Balance SheetAssets Liabilities + NW Cash (7.5%) Deposits (88%)

Share Draft (15%)Investments (6%) Regular Share (15%)

MMA (29%)Loans (82%) CDs (25%)Consumer (20%) IRAs (4%)Mortgage (46%)

Student (16%) Borrowings (2.5%) Building (4.5%) Net Worth (9.5%)

YOA - COF = NIM + Fee/Other Income

- Operating Expense- PLL

= Net Income

*Required ROA = Asset Growth Rate x Capital Ratio (dependent variable) (choice variable) (current)

Treasury Yield Curves

0

1

2

3

4

5

6

1 2 3 5 10 15 20 25 30Years to Maturity

Yie

ld t

o M

atu

rity

0

1

2

3

4

5

6June 2007 August 2011 May 2013

Yield Curve & the 3 Components of NIM

6

4

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

1 year 2 3 4 5 year 6

Years to Maturity

Perc

ent

FundingSpread

Interest RateRisk Spread

Credit Spread

1-year CD @ 3.0%

5-year loan@ 7.5%

Asymmetric Information: A situation where one party lacks sufficient information about the other party to make accurate decisions

Adverse Selection

1. Asymmetric information before transaction occurs

2. Potential borrowers most likely to produce adverse outcomes are ones most likely to seek loans and be selected

3. Adverse Selection => bankers willingness to lend

Moral Hazard

1. Asymmetric information after transaction occurs

2. Hazard that borrower has incentives to engage in undesirable (immoral) activities making it more likely that won’t pay loan back

3. Moral hazard => bankers willingness to lend

4. Reputation: Declining social stigma regarding bankruptcy => M.H.

Asymmetric Information

Adverse Selection Moral Hazard

Stopping “bad credit risks” from becoming borrowers

Stopping borrowers frombecoming “bad credit risks”

Screening process Monitoring process

Loan applicants

Approve

DenyLoan signingdate

Performing

Non-performing

A situation where 1 partyhas more info

than the other party

Loan department Collections department

potential bad credit risks are the ones who most actively seek out loans

the lender runs the risk that the borrowerwill engage in risky activities that makeit less likely that the loan will be paid back

“The business of bankingis the business of collecting information”Good C.R.

Bad C.R.

2 types

Financial Intermediaries make s by Transactions costs

1. Experts on loan contracts

2. Experts with screening process

3. Experts with monitoring borrowers

4. Develop high level of lending expertise

5. Take advantage of economies of scale (lower average costs)

• number of transactions

(reduce average costs by spreading fixed costs over many transactions)

• scale of transactions

(make a few large loans instead of many small loans => variable costs)

• scope of operations

(offering many products and services => variable costs)

Regulation of the Financial SystemTwo Main Reasons for Regulation

1. Increase information to investors Decreases adverse selection and moral hazard problems SEC forces corporations to disclose information SEC prohibits insider trading

2. Ensuring the soundness of financial intermediaries Prevents financial panics Six types of regulation:

1. Chartering – restrictions on entry

2. reporting requirements – disclosure of appropriate financial statements

3. restrictions on assets and activities

4. deposit insurance – up to $250,000 per person

5. anti-competitive measures – limits on branching (abolished by 1994 legislation)

6. Restrictions on interest rates

Econ 330

Homework 1Due Friday, September 13

Chapter 2, pages 49-50.

Questions 2, 4, 7, 12, 17, 22