Embed Size (px)

DESCRIPTION

Estudio sobre el uso de servicios a través de dispositivos moviles en Latinoamerica. Brazil, Colombia, Mexico, Argentina, Chile y Venezuela

Citation preview

Executive Summary:

Latin American Mobile Content Services

Markets I & II

I: Brazil, Colombia, Mexico

II: Argentina, Chile, Venezuela

N755/ N756-63

June 2010

2N755-63

Disclaimer

Frost & Sullivan takes no responsibility for any incorrect information supplied to us by manufacturers or users.

Quantitative market information is based primarily on interviews and therefore, is subject to fluctuation.

Frost & Sullivan Research Services are limited publications containing valuable market information provided to a

select group of customers in response to orders. Our customers acknowledge, when ordering, that

Frost & Sullivan Research Services are for customers’ internal use and not for general publication or disclosure

to third parties.

No part of this Research Service may be given, lent, resold or disclosed to non-customers without writtenpermission.

Furthermore, no part may be reproduced, stored in a retrieval system, or transmitted in any form or by any

means, electronic, mechanical, photocopying, recording or otherwise, without the permission of the publisher.

For information regarding permission, write to:

Frost & Sullivan

331 E. Evelyn Avenue, Suite 100

Mountain View, CA 94041

The United States

© 2010 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan.

No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

3N755-63

Certification

We hereby certify that the views expressed in this research service accurately reflect our views based on primary

and secondary research with industry participants, industry experts, end users, regulatory organizations, financial

and investment community, and other related sources.

In addition to the above, our robust in-house forecast and benchmarking models along with the Frost & Sullivan

Decision Support Databases have been instrumental in the completion and publishing of this research service.

We also certify that no part of our analyst compensation was, is, or will be, directly or indirectly, related to the

specific recommendations or views expressed in this service.

4

Latin American Mobile Content

Services Markets I

5N755-63

Table of Contents

Executive Summary………………………………………………………………….......…

Methodology and Service Definitions…………………………………………..…….…

Brazilian Mobile Content Services Market

Market Overview…………………………………………………..……..

Market Engineering Measurements……………………………..……

Main Market Facts…………………………………………………..……

Market Sizing………………………………………………………….…..

Market Drivers……………………………………………………….……

Market Restraints…………………………………………………….…..

Market Demand Analysis……………….………………………………

Market Trends…………………………………….………………………

Market Forecasts……………………………………………………...…

Demand Analysis by Content Service……………………….…….…

Application Stores…………………………………………………….…

Competitive Structure…………………………….…………….……….

Colombian Mobile Content Services Markets

Market Overview…………………………………………………..……..

Market Engineering Measurements……………………………..……

Main Market Facts…………………………………………………..……

Market Sizing…………………………………………………….………..

Market Drivers……………………………………………………….……

Market Restraints………………………………………………………..

Market Demand Analysis………………………………………………

Market Trends……………………………………………………………

08

13

17

18

19

20

23

24

25

26

27

33

35

36

42

43

44

45

48

49

50

51

6N755-63

Table of Contents

Market Forecasts……………………………………………………...…

Demand Analysis by Content Service……………………….…….…

Application Stores…………………………………………………….…

Competitive Structure…………………………….…………….……….

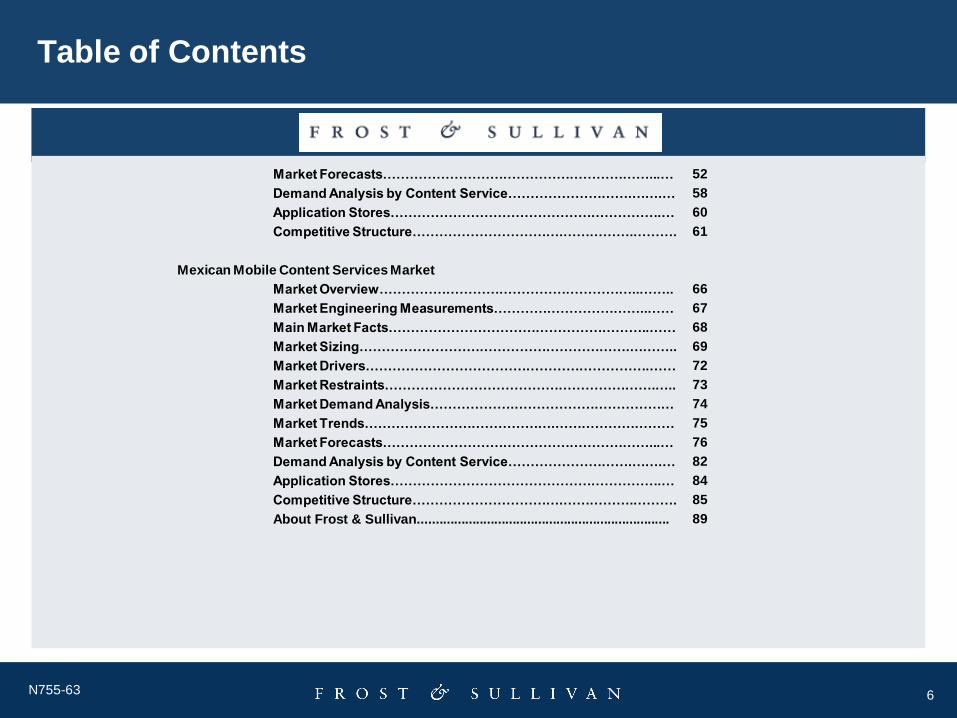

Mexican Mobile Content Services Market

Market Overview…………………………………………………..……..

Market Engineering Measurements……………………………..……

Main Market Facts…………………………………………………..……

Market Sizing…………………………………………………….………..

Market Drivers……………………………………………………….……

Market Restraints…………………………………………………….…..

Market Demand Analysis……………….………………………………

Market Trends…………………………………….………………………

Market Forecasts……………………………………………………...…

Demand Analysis by Content Service……………………….…….…

Application Stores…………………………………………………….…

Competitive Structure…………………………….…………….……….

About Frost & Sullivan.....................................................................

52

58

60

61

66

67

68

69

72

73

74

75

76

82

84

85

89

7N755-63

List of Figures

Brazilian Mobile Content Services Market

Mobile Content Services Market: Fact Sheet (Brazil), 2009.................................................................... ...........

Mobile Content Services Market: Market Drivers Ranked in Order of Impact (Brazil), 2010-2014…………..

Mobile Content Services Market: Market Restraints Ranked in Order of Impact (Brazil), 2010-2014...........

Mobile Content Services Market: User Base and Penetration Rates (Brazil), 2009-2014...............................

Mobile Content Services Market: Revenues and User Base (Brazil), 2009-2014.............................................

Mobile Content Services Market: Revenues by Service Type (Brazil), 2009-2014..........................................

Colombian Mobile Content Services Market

Mobile Content Services Market: Fact Sheet (Colombia), 2009.................................................................. ......

Mobile Content Services Market: Market Drivers Ranked in Order of Impact (Colombia), 2010-2014…...…

Mobile Content Services Market: Market Restraints Ranked in Order of Impact (Colombia), 2010-2014….

Mobile Content Services Market: User Base and Penetration Rates (Colombia), 2009-2014………..………

Mobile Content Services Market: Revenues and User Base (Colombia), 2009-2014…………………..………

Mobile Content Services Market: Revenues by Service Type (Colombia), 2009-2014……………..…………

Mexican Mobile Content Services Market

Mobile Content Services Market: Fact Sheet (Mexico), 2009............................................................................

Mobile Content Services Market: Market Drivers Ranked in Order of Impact (Mexican), 2010-2014…….…

Mobile Content Services Market: Market Restraints Ranked in Order of Impact (Mexican), 2010-2014……

Mobile Content Services Market: User Base and Penetration Rates (Mexican), 2009-2014…………...….….

Mobile Content Services Market: Revenues and User Base (Mexican), 2009-2014……………………...……

Mobile Content Services Market: Revenues by Service Type (Mexican), 2009-2014………………….…….…

17

23

24

28

30

32

42

48

49

53

55

57

66

72

73

77

79

81

8N755-63

List of Charts

Brazilian Mobile Content Services Market

Mobile Content Services Market: Market Engineering Measurements (Brazil), 2009……………………

Mobile Content Services Market: Percent of Revenues by Service Type (Brazil), 2009…………………

Mobile Content Services Market: Percent of Subscribers by Mobile Operator (Brazil), 2009…….……

Mobile Content Services Market: Percent of Revenues by Mobile Operator (Brazil), 2009……….……

Mobile Content Services Market: User Base and Penetration Rates (Brazil), 2009-2014………….……

Mobile Content Services Market: Revenues and User Base (Brazil), 2009-2014……………………..….

Mobile Content Services Market: Revenues by Service Type (Brazil), 2009-2014……………………….

Mobile Content Services Market: Competitive Structure (Brazil), 2009……………………………………

Colombian Mobile Content Services Market

Mobile Content Services Market: Market Engineering Measurements (Colombia), 2009………………

Mobile Content Services Market: Percent of Revenues by Service Type (Colombia), 2009……………

Mobile Content Services Market: Percent of Subscribers by Service Type (Colombia), 2009…………

Mobile Content Services Market: Percent of Revenues by Service Type (Colombia), 2009……………

Mobile Content Services Market: User Base and Penetration Rates (Colombia), 2009-2014………..…

Mobile Content Services Market: Revenues and User Base (Colombia), 2009-2014…………………....

Mobile Content Services Market: Revenues by Service Type (Colombia), 2009-2014………………..…

Mobile Content Services Market: Competitive Structure (Colombia), 2009…………………….…………

Mexican Mobile Content Services Market

Mobile Content Services Market: Market Engineering Measurements (Mexico), 2009………….………

Mobile Content Services Market: Percent of Revenues by Service Type (Mexico), 2009………………

Mobile Content Services Market: Percent of Subscribers by Service Type (Mexico), 2009……………

Mobile Content Services Market: Percent of Revenues by Service Type (Mexico), 2009………………

Mobile Content Services Market: User Base and Penetration Rates (Mexico), 2009-2014…………..…

Mobile Content Services Market: Revenues and User Base (Mexico), 2009-2014……………………….

Mobile Content Services Market: Revenues by Service Type (Mexico), 2009-2014……..………………

Mobile Content Services Market: Competitive Structure (Mexico), 2009………………………….………

18

20

21

22

27

29

31

36

43

45

46

47

52

54

56

61

67

69

70

71

76

78

80

85

9N755-63

Executive Summary

Economic Downturn - Despite the economic downturn from the last quarter of 2008 to 2009, the total Latin

American mobile content services markets maintained its growth trend. Brazil and Mexico witnessed growth by

a rate of 15.8 and 6.7 percent, respectively, while Colombia declined by a rate of 0.9 percent.

The Total Latin American Mobile Content Services Markets - The total mobile content market in Latin

America is nearing saturation with a considerable number of subscribers. In Brazil, Colombia, and Mexico, the

mobile penetration rates were 92.2, 84.3, and 77.2 percent, respectively. Nevertheless, mobile content users’

penetration rates in these countries were 10.2, 15.1, and 22.4 percent, respectively.

Main Facts in Latin America - In Brazil, Vivo’s launch of an open platform for application developers and Tim’s

announcement of an application store in partnership with QUALCOMM Incorporated Incorporated were among

the main facts for the mobile content market. Meanwhile, Comcel and Nokia announced their alliance to open

Ovi store in the Colombian market, and in Mexico, Televisa Group bought 30 percent stake on NII Holdings,

which enables the former to provide wireless and broadband data services to its existing portfolio of pay TV

offerings.

Market Drivers and Restraints - The mobile content market is expected to grow by a double-digit rate in

Brazil, Colombia, and Mexico. Penetration of feature-rich and capable handsets that enable advanced contents

and increase in the adoption of mobile broadband are among the main drivers for the market growth. However,

the high price for data plans in Latin America, coupled with a common perception of mobile data as a high-cost

service, inhibit the demand for advanced contents.

10N755-63

Executive Summary (Contd…)

Mobile Content Services - Subscription services are the most common and used in Latin America due to their

low prices. However, TV/video services are expected to witness the highest growth in the next few years,

stimulated by the penetration of capable handsets and the FIFA World Cup. Music and games are likely to

witness similar growth, with huge opportunities in the countries analyzed. Apart from the general analysis, some

services witness excellent growth in specific markets, for instance, penetration of TV/video in Mexico,

stimulated by higher penetration of feature-rich handsets and smartphones with lower prices in this country, and

the success of ring-back tones in Colombia, which was driven by an innovative billing model of a local operator

and a cultural predisposition to adopt music services.

Application Stores - After the launch of manufacturers’ application stores in Latin America, mobile operators

are expected to launch their own application stores in each country by 2010. In Brazil, Vivo was the first to

launch an application store with an open platform, while Tim, Claro, and Oi are expected to launch their own

stores before the end of 2010. A similar trend is expected in Colombia, where Comcel and Movistar are trying to

open their application stores in 2010, while Tigo plans the launch of a music store in the same year. In Mexico,

the three main operators are planning to provide their application stores by 2010. Despite the plans to open

their own application stores, Telcel and Comcel, America Movil companies, partner with Nokia to provide Ovi

store in their countries.

11N755-63

Executive Summary (Contd…)

Competitive Structure - The Brazilian mobile content market is one of the most competitive in

Latin America, with four nationwide participants. Vivo holds the market leadership position in

terms of mobile content revenues and subscribers. The operator focuses on a wide variety of

content offers, especially music, and was the first to launch an application store.

Tim holds the second position, focusing on low price for content acquisition and simple layout.

Claro is the third-largest operator and focuses on investment in partnerships with content

providers to develop attractive contents. The operator also has great offering of video at

competitive prices.

Oi is the fourth-largest mobile content operator. It stimulates the development of regional

contents and focuses on music contents to attract youngsters.

Nextel invested in partnership with the main content developers to create attractive services for

its high-income consumer base; however, it needs 3G technology to improve advanced contents.

In Colombia, the market is highly concentrated on a single operator that has national coverage

and competitive prices for mobile content services, Comcel. With a wide variety of mobile

content offerings, the operator competes in this market with low prices and strong promotional

activities to stimulate data traffic.

In 2009, Movistar, the second-largest mobile operator in this market, invested in the expansion of

coverage with its GSM and 3G networks. It focuses on high-quality content and a wide variety

of services.

12N755-63

Executive Summary (Contd…)

Tigo, the third-largest operator in the Colombian market, grew in importance by providing low-price services

to attract consumers that cannot afford premium services. It also invested in promotions, innovative

contents, packages of minutes, and an innovative billing model for ring-back tones.

Similar to Colombia, the mobile content market in Mexico is also highly concentrated on a single operator with

national coverage and competitive prices, Telcel. The operator sets strategic partnerships with companies

such as Nokia, ESPN, and Disney among others to attract consumers that have interest in premium services

with low prices. It also has a complete structure to provide TV/video, music, and subscriptions contents.

Movistar, the second-largest mobile operator in Mexico, creates a more segmented and focused proposal

oriented to all the consumer segments, from children to adults. It also invested in its loyalty program, Movistar

Club to attract and retain consumers that are willing to pay less for mobile services.

Tigo, the third-largest mobile content operator, invested in new business models such as video on demand

for mobile TV focused on specific clients segments. It also invests in quality and focuses on contents that

consumers are more willing to acquire.

Nextel is the fourth-largest operator in this market. It provides basic content services such as SMS,

subscription services, and alarms.

13

Latin American Mobile Content Services

Markets II

14N755-63

Table of Contents

Executive Summary………………………………………………………………….......…

Methodology and Service Definitions…………………………………………..…….…

Argentinean Mobile Content Services Market

Market Overview…………………………………………………..……..

Market Engineering Measurements……………………………..……

Main Market Facts…………………………………………………..……

Market Sizing………………………………………………………….…..

Market Drivers……………………………………………………….……

Market Restraints…………………………………………………….…..

Market Demand Analysis……………….………………………………

Market Trends…………………………………….………………………

Market Forecasts……………………………………………………...…

Demand Analysis by Content Service……………………….…….…

Application Stores…………………………………………………….…

Competitive Structure…………………………….…………….……….

Chilean Mobile Content Services Markets

Market Overview…………………………………………………..……..

Market Engineering Measurements……………………………..……

Main Market Facts…………………………………………………..……

Market Sizing…………………………………………………….………..

Market Drivers……………………………………………………….……

Market Restraints………………………………………………………..

Market Demand Analysis………………………………………………

Market Trends……………………………………………………………

08

13

17

18

19

20

23

24

25

26

27

33

35

36

42

43

44

45

48

49

50

51

15N755-63

Table of Contents

Market Forecasts……………………………………………………...…

Demand Analysis by Content Service……………………….…….…

Application Stores…………………………………………………….…

Competitive Structure…………………………….…………….……….

Venezuelean Mobile Content Services Market

Market Overview…………………………………………………..……..

Market Engineering Measurements……………………………..……

Main Market Facts…………………………………………………..……

Market Sizing…………………………………………………….………..

Market Drivers……………………………………………………….……

Market Restraints…………………………………………………….…..

Market Demand Analysis……………….………………………………

Market Trends…………………………………….………………………

Market Forecasts……………………………………………………...…

Demand Analysis by Content Service……………………….…….…

Application Stores…………………………………………………….…

Competitive Structure…………………………….…………….……….

About Frost & Sullivan.....................................................................

52

58

60

61

66

67

68

69

72

73

74

75

76

82

84

85

89

16N755-63

List of Figures

Argentinean Mobile Content Services Market

Mobile Content Services Market: Fact Sheet (Argentina), 2009........................................................................

Mobile Content Services Market: Market Drivers Ranked in Order of Impact (Argentina), 2010-2014…..…

Mobile Content Services Market: Market Restraints Ranked in Order of Impact (Argentina), 2010-2014....

Mobile Content Services Market: User Base and Penetration Rates (Argentina), 2009-2014........................

Mobile Content Services Market: Revenues and User Base (Argentina), 2009-2014......................................

Mobile Content Services Market: Revenues by Service Type (Argentina), 2009-2014...................................

Chilean Mobile Content Services Market

Mobile Content Services Market: Fact Sheet (Chile), 2009..................................................................... ... …..

Mobile Content Services Market: Market Drivers Ranked in Order of Impact (Chile), 2010-2014…...……..

Mobile Content Services Market: Market Restraints Ranked in Order of Impact (Chile), 2010-2014………

Mobile Content Services Market: User Base and Penetration Rates (Chile), 2009-2014………..……………

Mobile Content Services Market: Revenues and User Base (Chile), 2009-2014…………………..…………..

Mobile Content Services Market: Revenues by Service Type (Chile), 2009-2014……………..………………

Venezuelean Mobile Content Services Market

Mobile Content Services Market: Fact Sheet (Venezuela), 2009................................................................. ......

Mobile Content Services Market: Market Drivers Ranked in Order of Impact (Venezuela), 2010-2014…….

Mobile Content Services Market: Market Restraints Ranked in Order of Impact (Venezuela), 2010-2014…

Mobile Content Services Market: User Base and Penetration Rates (Venezuela), 2009-2014…………...….

Mobile Content Services Market: Revenues and User Base (Venezuela), 2009-2014……………………....…

Mobile Content Services Market: Revenues by Service Type (Venezuela), 2009-2014………………….…….

17

23

24

28

30

32

42

48

49

53

55

57

66

72

73

77

79

81

17N755-63

List of Charts

Argentinean Mobile Content Services Market

Mobile Content Services Market: Market Engineering Measurements (Argentina), 2009………………

Mobile Content Services Market: Percent of Revenues by Service Type (Argentina), 2009……………

Mobile Content Services Market: Percent of Subscribers by Mobile Operator (Argentina), 2009…….

Mobile Content Services Market: Percent of Revenues by Mobile Operator (Argentina), 2009……….

Mobile Content Services Market: User Base and Penetration Rates (Argentina), 2009-2014……….….

Mobile Content Services Market: Revenues and User Base (Argentina), 2009-2014…………………….

Mobile Content Services Market: Revenues by Service Type (Argentina), 2009-2014……………..……

Mobile Content Services Market: Competitive Structure (Argentina), 2009…………………………….…

Chilean Mobile Content Services Market

Mobile Content Services Market: Market Engineering Measurements (Chile), 2009…………………….

Mobile Content Services Market: Percent of Revenues by Service Type (Chile), 2009…………………

Mobile Content Services Market: Percent of Subscribers by Service Type (Chile), 2009………………

Mobile Content Services Market: Percent of Revenues by Service Type (Chile), 2009…………………

Mobile Content Services Market: User Base and Penetration Rates (Chile), 2009-2014………..………

Mobile Content Services Market: Revenues and User Base (Chile), 2009-2014……………………….....

Mobile Content Services Market: Revenues by Service Type (Chile), 2009-2014………………..………

Mobile Content Services Market: Competitive Structure (Chile), 2009…………………….………………

Venezuelean Mobile Content Services Market

Mobile Content Services Market: Market Engineering Measurements (Venezuela), 2009………..….…

Mobile Content Services Market: Percent of Revenues by Service Type (Venezuela), 2009…………..

Mobile Content Services Market: Percent of Subscribers by Service Type (Venezuela), 2009…….….

Mobile Content Services Market: Percent of Revenues by Service Type (Venezuela), 2009……..……

Mobile Content Services Market: User Base and Penetration Rates (Venezuela), 2009-2014………….

Mobile Content Services Market: Revenues and User Base (Venezuela), 2009-2014……………………

Mobile Content Services Market: Revenues by Service Type (Venezuela), 2009-2014……..……………

Mobile Content Services Market: Competitive Structure (Venezuela), 2009………………………….……

18

20

21

22

27

29

31

36

43

45

46

47

52

54

56

61

67

69

70

71

76

78

80

85

18N755-63

Executive Summary

Economic Downturn – Despite the global economic downturn that was witnessed between the last quarter of

2008 and whole of 2009, the mobile market witnessed growth in most of the Latin American countries. It grew

by 4.4 percent and 23.7 percent in Argentina and Venezuela, respectively, and declined by 4.5 percent in Chile.

The Total Latin American Mobile Content Services Markets – The mobile market in Latin America is nearing

saturation in terms of the number of subscribers. In Argentina, Chile, and Venezuela, mobile penetration

reached 121.3 percent, 103.5 percent, and 105.7 percent, respectively, in 2009. Nevertheless, mobile content

penetration in these countries reached 14.8 percent, 12.1 percent, and 9.5 percent, respectively.

Main Facts in Latin America – In Argentina, the launch of a music store by Personal and an application store

by Movistar were among the main events in the mobile content market in 2009. Meanwhile, Claro and Nokia

initiated negotiations to open Ovi Store in the Chilean market; in Venezuela, Movilnet launched the Vergatario,

which is the first handset made in the country, and the Government centralized the national purchase of

handsets, thereby restraining operators’ revenues.

Market Drivers and Restraints – The mobile content market is expected to witness double-digit growth rates

in Argentina, Chile, and Venezuela. Improvement in mobile content quality and applications, penetration of

feature-rich handsets that enable advanced content downloads, and increase in mobile broadband adoption are

some of the main drivers for the Latin American mobile content markets. However, high price of data plans in

Latin America results in the common perception of mobile data being a high-cost service; this inhibits the

demand for advanced content.

19N755-63

Executive Summary (Contd…)

Mobile Content Services – Subscription services are the most commonly used ones in Latin America because

of their low price. However, TV/video are expected to witness high growth in the next few years, stimulated by

the penetration of capable handsets and FIFA World Cup in 2010. Music has already achieved high penetration

rates, and gaming is likely to witness higher growth rate and present many opportunities in Latin America.

Some services are in different stages of lifecycle in various countries, for instance, in Argentina, operators are

still waiting for final regulations to develop mobile TV.

Application Stores – After the launch of manufacturers’ application (APP) stores in Latin America, mobile

operators are expected to launch their own APP stores in each country by 2010. In Argentina, Movistar was the

first to launch an APP store with an open platform, while Personal and Claro are expected to launch their own

stores before the end of 2010. The same trend is expected in Chile, where Entel offers applications through

Kool Tools, and other operators are planning for their future store launches. Claro is expected to launch Claro

Widgets, a service based on the Mobile Internet application developed by Qualcomm Plaza that will allow 190

million customers in Latin America to download new applications, in 2010.

20N755-63

Executive Summary (Contd…)

Competitive Structure –The mobile content markets in Argentina, Chile, and Venezuela are the

most competitive ones in Latin America, with four nationwide participants. Movistar is the leader in

the Argentinean market in terms of revenues. The operator focuses on a wide variety of content

and was the first to launch an APP store.

Claro was ranked second; it focuses on low price and simple layout.

Personal was ranked third; it focuses on offering mobile content in music stores and developing

attractive and innovative content.

Nextel was the fourth major mobile operator. Though it is the newest participant in this market, it

has witnessed high downloads of its content, as most of its clients are from the corporate sector.

In Chile, the market is highly dominated by two operators that have nationwide coverage and

aggressive prices for mobile services - Movistar and Entel PCS. With a similar wide variety of

content offers, both operators compete in this market in terms of prices and promotions aimed at

stimulating data traffic .

Claro, the third participant in this market, planned to expand its coverage and invested in 3G

networks in 2009, covering almost 85 percent of the population.

21N755-63

Executive Summary (Contd…)

In Venezuela, the mobile content market is dominated by one operator that has nationwide coverage and

aggressive prices - Movistar. It focuses on customer retention and clients segmentation. In 2009, Movistar

offered more plans at reasonable prices, which resulted in increased revenues for it.

CANTV leads the mobile content market in Venezuela in terms of number of users; in 2009, the company

implemented a successful strategy, launching a new tariff scheme with prices reduced by about 20 percent.

Digitel is the third-largest participant in the Venezuelan mobile content market and the last operator to enter the

mobile market in the country. Its investments are focused on technology upgrades and enhancement of network

efficiency. The company improved the competition and it accounted for 21.0 percent of the total mobile content

users in Venezuela in 2009. Its strategy focuses on 3G network improvement and positioning itself as an

innovative company.

22

Graphics

23N755-63

Market Sizing – Latin America

15%

2%

16%

65%

2%

Subscription Services Music Games TV/Video Others

Mobile Content Services Market: Percent of Revenues by

Service Type (Latin America), 2009

Mobile Content Revenues 2009 = US$2,409.6 Million

Note: Others include image and graphic services (wallpapers, pictures, and so on)

Note: All figures are rounded; the base year is 2009.

Source: Frost & Sullivan

24N755-63

Market Sizing – Latin America

11%12%

38%

31%

3%

5%

Mexico Brazil Colombia

Argentina Venezuela Chile

Mobile Content Subscribers 2009 = 63.2 Million

Note: Others includes local participants such as CTBC Celular, Sercomtel and Aeiou

Mobile Content Services Market: Percent of Subscribers

by Mobile Operator (Latin America), 2009

Note: All figures are rounded; the base year is 2009.

Source: Frost & Sullivan

25N755-63

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

2009 2010 2011 2012 2013 2014

Year

Users

(M

illio

n)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Penetr

ati

on (

%)

Users (Million) Penetration (%)

Market Forecasts – Latin America

Mobile Content Services Market: Users Base and

Penetration Rates in Latin America Population

(Latin America), 2009-2014

Note: All figures are rounded; the base year is 2009.

Source: Frost & Sullivan

26

Methodology and Service Definitions

27N755-63

Methodology

Revenues - This study presents the net revenues obtained either directly from service providers’ financial

reports or through the primary interviews conducted.

Exchange Rates - The U.S. dollar is the official currency used in this study to measure revenues. The

exchange rates of certain countries for 2009 are given below:

1US$ = AR$ 3.80 1US$ = R$ 1.75 1US$ = CLP$ 634.25

1US$ = CP$ 2,064.63 1US$ = MXP$ 13.04 1US$ = Bs.F$ 2.15

Forecasts - This study presents a six-year forecast for revenues, from 2009 to 2014. The US Dollar projection

uses year-base exchange rate frozen throughout the whole period.

Research Methodology - Frost & Sullivan conducted primary interviews with the key executives (managers

and directors) from different areas (marketing, strategic planning, market intelligence, and product and content

services) within the most important service providers in the six countries on the scope of this study. Extensive

secondary research was conducted for two months throughout Frost & Sullivan’s internal database and other

public information sources such as financial reports, industry associations, statistic agencies, and the Internet.

28N755-63

Service Definitions

Content - Mobile content comprises all the download services such as music, games, video/TV and images,

and subscription services through SMS (excluding contests, operator promotions, and televoting services)

provided by the mobile operator.

Music - Music contents comprise the download of MP3-format music, ring tones, ring-back tones, and all

the services related to music files downloaded from operators’ music stores and other services, such as

SMS or MMS.

Games - Games comprises all the games downloaded from operators’ Web sites or provided though

other services such as SMS or MMS.

Subscription Services - These comprise all the information services acquired through subscription and

provided by the operator through SMS/MMS or WAP services such as travel, weather, horoscope,

sports, and economy among other information subscription services.

TV/Video - This comprises all the paid mobile video and TV services provided by mobile operators such

as video download, video streaming, video on demand, analog TV, and digital TV.

Others - These comprise wallpapers, pictures, and graphics among other picture-based downloads from

operators’ Web site or received through SMS services.

Note: Interactive SMS services (such as operators’ contests and promotions) as well as application services or

contents downloaded from manufacturers’ Web site are not included.

29

About Frost & Sullivan

30N755-63

Who is Frost & Sullivan

The Growth Consulting Company

• Founded in 1961, Frost & Sullivan has over 45 years of assisting clients with their decision-making

and growth issues

• Over 1,700 Growth Consultants and Industry Analysts across 32 global locations

• Over 10,000 clients worldwide - emerging companies, the global 1000 and the investment community

• Developers of the Growth Excellence Matrix – industry leading growth positioning tool for corporate

executives

• Developers of T.E.A.M. Methodology, proprietary process to ensure that clients receive a 360o

perspective of technology, markets and growth opportunities

• Three core services: Growth Partnership Services, Growth Consulting and Career Best Practices

31N755-63

What Makes Us Unique

Exclusively Focused on Growth

Global thought leader exclusively focused on

addressing client growth strategies and plans –

Team actively engaged in researching and

developing of growth models that enable clients to

achieve aggressive growth objectives.

Industry Breadth

Cover the broad spectrum of industries and

technologies to provide clients with the ability to

look outside the box and discover new and

innovative ideas.

Global Perspective

32 global offices ensure that clients receive a

global coverage/perspective based on regional

expertise.

360o

Perspective

Proprietary T.E.A.M.TM

Methodology integrates all

6 critical research methodologies to significantly

enhance the accuracy of decision making and

lower the risk of implementing growth strategies.

Growth Monitoring

Continuously monitor changing technology,

markets and economics and proactively address

clients growth initiatives and position.

Trusted Partner

Working closely with client Growth Teams –

helping them generate new growth initiatives and

leverage all of Frost & Sullivan assets to

accelerate their growth.

32N755-63

T.E.A.M. Methodology

Frost & Sullivan’s proprietary T.E.A.M. methodology, ensures that clients have complete “360 Degree

Perspective” from which to drive decision-making. Technical, Econometric, Application, and Market information

ensures that clients have a comprehensive view of industries, markets, and technology.

Technical Real-time intelligence on technology, including emerging technologies, new R&D

breakthroughs, technology forecasting, impact analysis, groundbreaking research, and

licensing opportunities.

Econometric In-depth qualitative and quantitative research focused on timely and critical global,

regional, and country specific trends, including the political, demographic, and

socioeconomic landscapes.

Application Insightful strategies, networking opportunities, and best practices that can be applied for

enhanced market growth; interactions between the client, peers, and Frost & Sullivan

representatives that result in added value and effectiveness.

Market Global and regional market analysis, including drivers and restraints, market trends,

regulatory changes, competitive insights, growth forecasts, industry challenges,

strategic recommendations, and end-user perspectives.

33N755-63

Global Perspective

1,700 staff across every major market worldwide

Over 10,000 clients worldwide from emerging to global 1000 companies