Embed Size (px)

Citation preview

Richard Laudy

Head of Global Infrastructure

Key Global Infrastructure Disruptors

Impact on European

International Contractors

Large projects typically take 20 percent

longer to finish than scheduled and are

up to 80 percent over budget.

Construction productivity has actually

declined in some markets since the

1990s. Financial returns for contractors

are often relatively low – and volatile.

McKinsey & Company – Imagining construction’s

digital future, June 2016

Today’s Agenda

1. China – Striking a Deal with Europe on

BRI

2. Technology – Integrating Technology and

Infrastructure

3. Off-Site Manufacturing – Driving a Step-

Change in Productivity

4. New Generations – Driving Change

China – Striking a Deal

with Europe on BRI

Annual value of completed

Chinese FDI in EU-28

2.1

7.9

10.2

6.7

14.7

20.7

37.2

29.1

17.3

20.0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019F

Annual values (€bn) in current prices

Note – Q1

2019

estimate of

pending

transactions

Source: Chinese FDI in Europe: 2018 trends and Impact of New Screening Policies

Rhodium Group and Merics – Mar 2019 and Pinsent Masons analysis

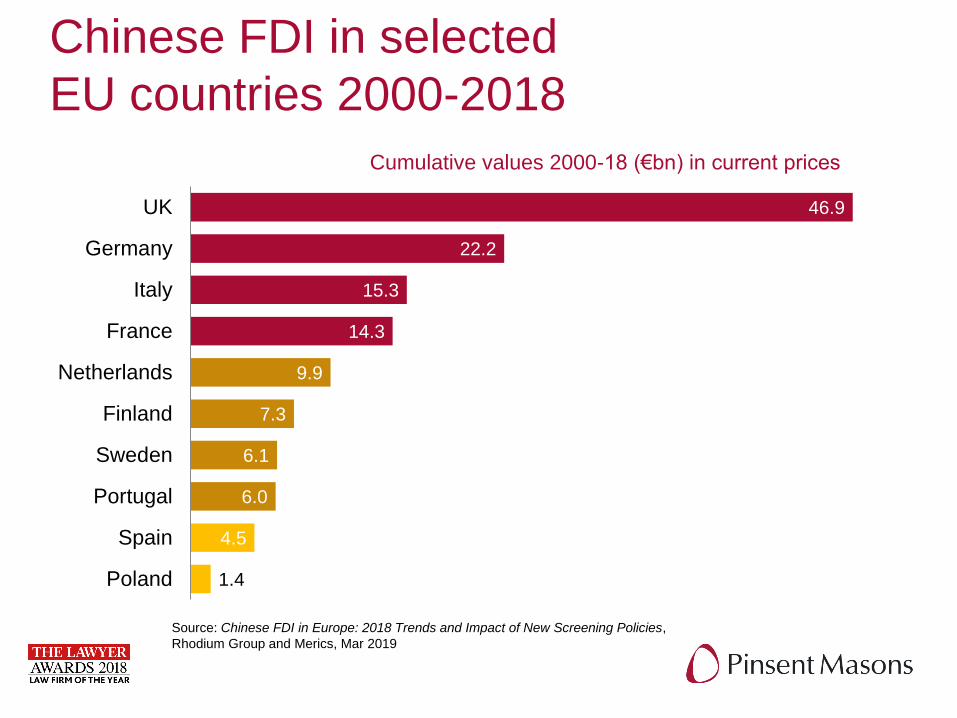

Chinese FDI in selected

EU countries 2000-2018

46.9

22.2

15.3

14.3

9.9

7.3

6.1

6.0

4.5

1.4

UK

Germany

Italy

France

Netherlands

Finland

Sweden

Portugal

Spain

Poland

Cumulative values 2000-18 (€bn) in current prices

Source: Chinese FDI in Europe: 2018 Trends and Impact of New Screening Policies,

Rhodium Group and Merics, Mar 2019

Accumulated £105 billion of Chinese

investment to flow into UK infrastructure

between 2014 and 2025

Source: China Invests West, Pinsent Masons, November 2014

Investment from China into UK infrastructure, cumulative values, 2014-25 current GBP billions

What is this going to mean for

European infrastructure sector?If the potential investment from China is realised

then this would help unlock growth for the UK

economy. The Challenge for Government and

the private sector is to come together to make

this happenMartin Gilbert

Co-founder and Chief Executive Officer

Aberdeen Asset Management

The key difference is China’s ability to take a

much longer-term view of risk than the UKSir John Armitt CBE

Chairman

National Infrastructure Commission

The real estate and infrastructure sectors are

the two most important markets for investment

from China into the UKZhen Yang

Investment Department

Citic Construction Co Ltd

Technology –

Integrating Technology

and Infrastructure

The evolution of Infratech – How

technology is shaping the future of

infrastructure

Infratech – the integration of

digital technologies with

physical infrastructure to

deliver efficient, connected,

resilient and agile assets.

Pinsent Masons – The evolution of

Infratech – How technology is

shaping the future of infrastructure,

October 2017

Technology and Off-Site Manufacturing

– Driving a Step-Change in Productivity

94%

35%

24%

33%

13%

98%

53%

53%

43%

14%

Sub-Contractor

JV Partner

In-House

PPP

PrimeContractor

How will Infrastructure engage with Technology

Past Three Years

Next Three Years

Source: The evolution of Infratech – How technology is shaping the future

of infrastructure, Pinsent Masons, October 2017

Technology and Off-Site Manufacturing

– Driving a Step-Change in Productivity

58%

18%

36%

53%

35%

87%

58%

36%

14%

5%

Transport

DigitalCommunications

Energy

SocialInfrastructure

Water andSanitation

Which areas of Infrastructure will Technology impact

Past Three Years

Next Three Years

Source: The evolution of Infratech – How technology is shaping the future

of infrastructure, Pinsent Masons, October 2017

Off-Site Manufacturing

– Driving a Step-

Change in Productivity

Construction Productivity

Stagnant for Decades

1.0

2.7

3.6

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Construction Total Economy Manufacturing

Annual % change 1995-2014

Source: Reinventing Construction, McKinsey Global Institute

Technology and Off-Site Manufacturing

– Driving a Step-Change in Productivity

• Lack of skills and labour shortages driving Off-Site

Manufacturing globally.

• China emerging as a market leader e.g. Broad Group.

• Off-Site Manufacturing will drive significant productivity

improvement (50% improvement is needed in UK).

• Contractors will need tighter control over workflow and

improved supply-chain management.

• Significant rise in the number of contractors investing in

Off-Site Manufacturing facilities.

• Major Tech players such as Amazon, Google and IBM

see construction as a sector ripe for disruption.

Global Construction Markets 2018-30Cumulative Volumes US$ trillions in 2017 prices and exchange rates

30.6

30.5

18.9

14.0

12.7

78.3

28.9

10.6

4.5

0.0 10.0 20.0 30.0 40.0 50.0 60.0 70.0 80.0 90.0

Western Europe

North America

Asia Pacific(Developed)

Eastern Europe

Latin America

Emerging Asia

Emerging Asia (Excl.China)

MENA

Sub-Saharan Africa

Source: Global Construction Perspectives and Oxford Economics

www.globalconstruction2030.com

New Generations –

Driving Change

Change in Age Structure of EU-28

Population, 2017-2050

15.6 15.5 14.9 14.7 14.8

65.0 64.2 61.2 58.3 56.7

19.5 20.4 23.9 27.0 28.5

2017 2020 2030 2040 2050

% of total population EU-28

Age 0-14 Age 15-64 Age 65 and over

Source: Eurostat, Mar 2019

Population Change in Germany 2018-2060

82.8 83.8 84.6 84.1 82.7 80.8

54.5 54.350.9 48.8 47.6

44.9

2018 2020 2030 2040 2050 2060

Population in Germany (millions)

Population Working Age Population

Source: Eurostat, Mar 2019

Richard Laudy

Head of Global Infrastructure

Key Global Infrastructure Disruptors

Impact on European

International Contractors