Embed Size (px)

Citation preview

KBC Group

Summer presentationJune 2005Web site: www.kbc.com

Ticker codes: KBC BB (Bloomberg) KBKBT BR (Reuters)

ISIN code: BE0003565737

2

Contact information

Investor Relations Office

Luc CoolNele KindtMarina Kanamori

Tel.: +32 2 429 49 16 investor.relations @ kbc.com

Surf to www.kbc.com for the latest update.

3

KBC Group’s financial accounts are presented according to IFRS reporting standards as of 1Q2005

As IFRS have a material impact on the way earnings are presented, this presentation is drafted to increase their visibility and to help the investment community to understand the underlying profit trends

KBC believes that this presentation is reliable, although some information may be condensed or incomplete

By receiving this presentation, each investor is deemed to represent that it possesses sufficient expertise to understand the risks involved

This presentation is provided for informational purposes only and does not constitute an offer to sell or the solicitation of an offer to buy any security

This presentation contains forward-looking statements with respect to our earnings development. By their nature, these forward-looking statements involve assumptions, uncertainties and opportunities. The risk exists that these statements may not be fulfilled and that future results differ materially.

Important information

Foto gebouw

Financial highlights - 1Q 2005

- Group performance

- Headlines per segment

FY 2005 profit outlook

Additional information on 1Q 2005 results

2004 pro forma IFRS quarterly accounts

5

Strong earnings momentum

393476

332

557

376434

365440

717

1Q04 2Q04 3Q04 4Q04 1Q04 2Q04 3Q04 4Q04 1Q05 2Q05

As published (Bel. GAAP), KBC Old Pro forma (IFRS 2004), MergCo IFRS 2005

Net profit+91% yoy

6

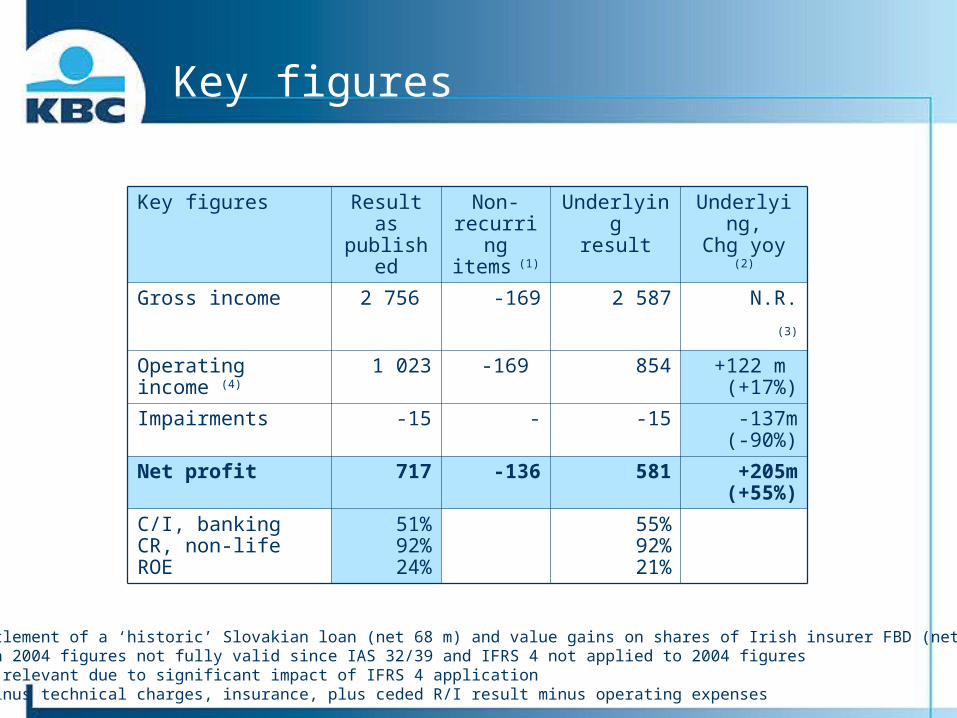

Key figures

Key figures Result as published

Non-recurring items (1)

Underlyingresult

Underlying,Chg yoy (2)

Gross income 2 756 -169 2 587 N.R.

(3)

Operating income (4) 1 023 -169 854 +122 m (+17%)

Impairments -15 - -15 -137m(-90%)

Net profit 717 -136 581 +205m(+55%)

C/I, bankingCR, non-lifeROE

51%92%24%

55%92%21%

Notes:(1) Related to settlement of a ‘historic’ Slovakian loan (net 68 m) and value gains on shares of Irish insurer FBD (net 68 m)(2) Comparison with 2004 figures not fully valid since IAS 32/39 and IFRS 4 not applied to 2004 figures(3) Comparison not relevant due to significant impact of IFRS 4 application (4) Gross income minus technical charges, insurance, plus ceded R/I result minus operating expenses

7

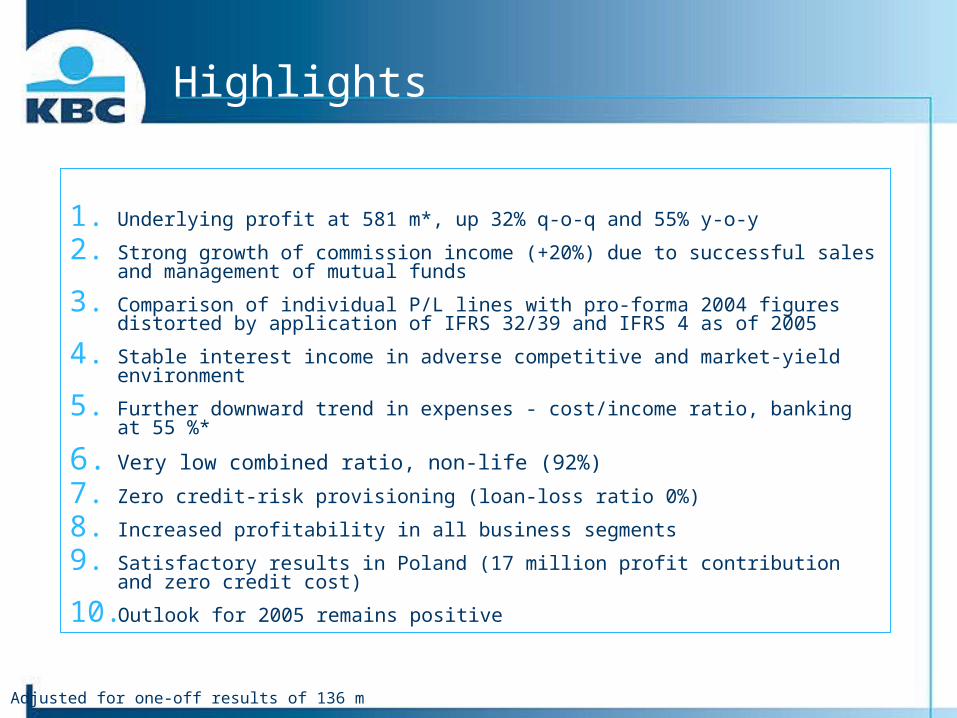

1. Underlying profit at 581 m*, up 32% q-o-q and 55% y-o-y

2. Strong growth of commission income (+20%) due to successful sales and management of mutual funds

3. Comparison of individual P/L lines with pro-forma 2004 figures distorted by application of IFRS 32/39 and IFRS 4 as of 2005

4. Stable interest income in adverse competitive and market-yield environment

5. Further downward trend in expenses - cost/income ratio, banking at 55 %*

6. Very low combined ratio, non-life (92%)

7. Zero credit-risk provisioning (loan-loss ratio 0%)

8. Increased profitability in all business segments

9. Satisfactory results in Poland (17 million profit contribution and zero credit cost)

10. Outlook for 2005 remains positive

Highlights

* Adjusted for one-off results of 136 m

8

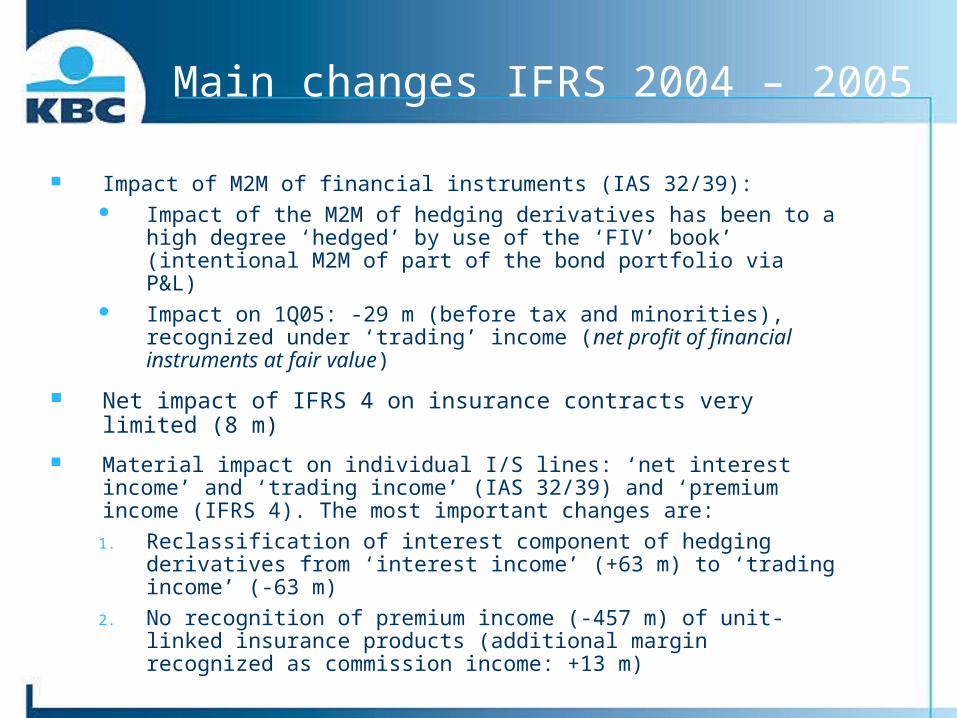

Main changes IFRS 2004 – 2005

Impact of M2M of financial instruments (IAS 32/39): Impact of the M2M of hedging derivatives has been to a high degree

‘hedged’ by use of the ‘FIV’ book’ (intentional M2M of part of the bond portfolio via P&L)

Impact on 1Q05: -29 m (before tax and minorities), recognized under ‘trading’ income (net profit of financial instruments at fair value)

Net impact of IFRS 4 on insurance contracts very limited (8 m)

Material impact on individual I/S lines: ‘net interest income’ and ‘trading income’ (IAS 32/39) and ‘premium income (IFRS 4). The most important changes are:

1. Reclassification of interest component of hedging derivatives from ‘interest income’ (+63 m) to ‘trading income’ (-63 m)

2. No recognition of premium income (-457 m) of unit-linked insurance products (additional margin recognized as commission income: +13 m)

9

Satisfactory quality of revenue

1Q04 2Q04 3Q04 4Q04 1Q05 2Q05

Pro forma IFRS 2004 IFRS 2005

3 462

2 517

3 1783 175

2 756

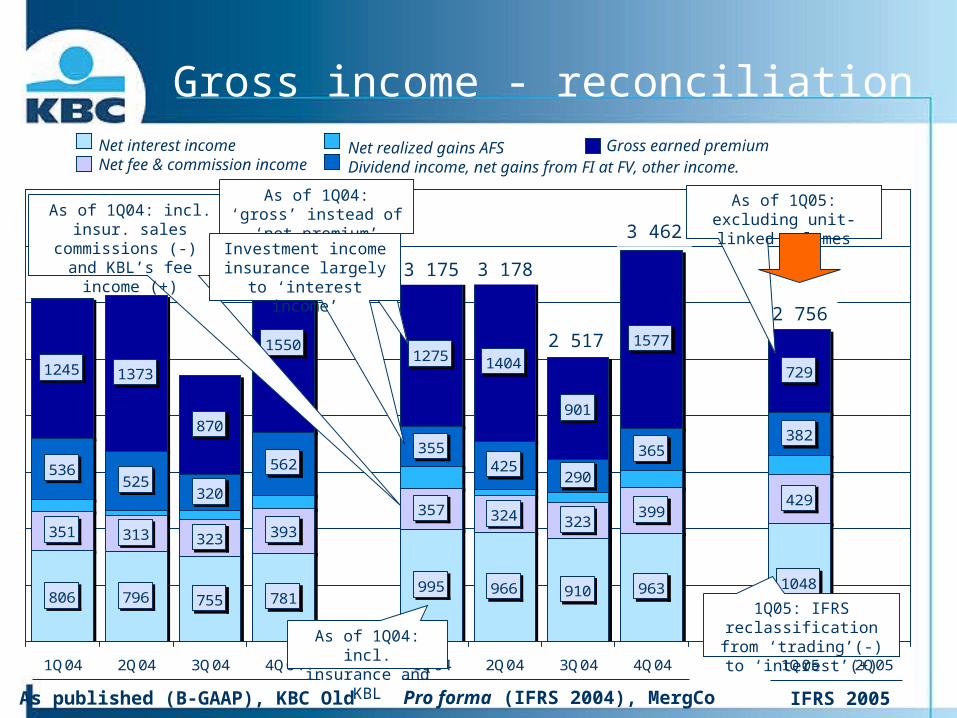

Excl. one-offs (169 m) and IFRS reclassifications, solid quality of banking income: stable interest income (in adverse interest rate environment), strong commission line (+17% y-o-y) and lower trading revenue

Nominal amount dropped, mainly due to a) non-recognition under IFRS 2005 of 464 m new unit-linked premium volume, b) M2M of financial instruments (IAS 32/39) and c) lower guaranteed life insurance (-667 m q-o-q and –95 m y-o-y)

Gross income (m)

10

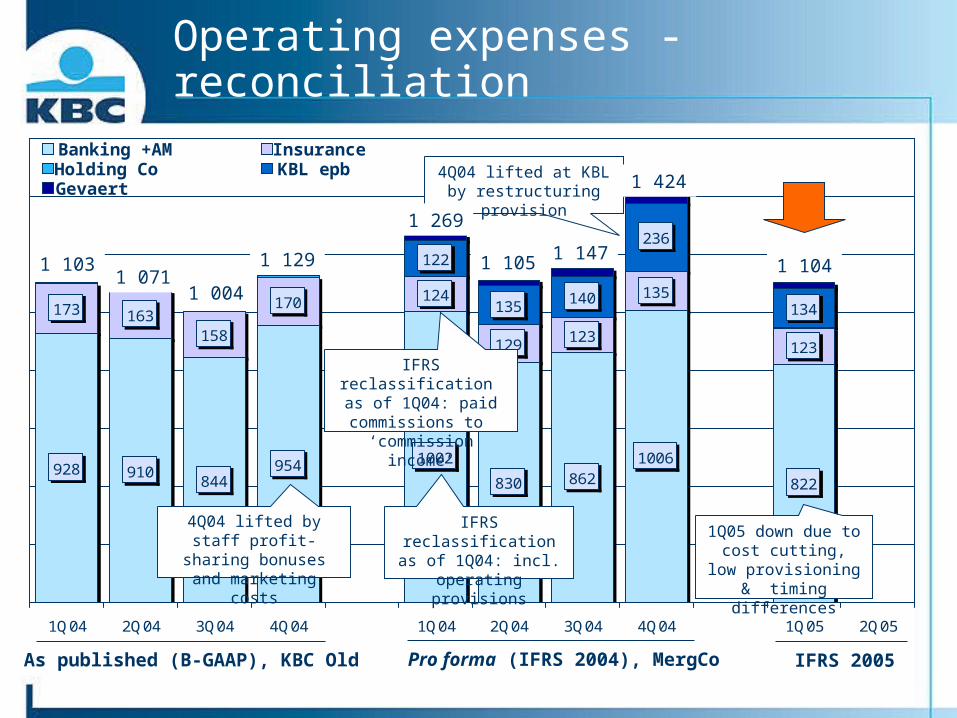

Operating expenses at low level

1Q04 2Q04 3Q04 4Q04 1Q05 2Q05

4Q04 lifted by staff profit-sharing bonuses, marketing costs, litigation provision (KBC Bank) and restructuring provision (KBL epb)

Pro forma IFRS 2004 IFRS 2005

1 424

1 1471 105

1 269

1 104

* C/I of 55% excl. non-recurring income

1Q05 down 13% y-o-y due to cost cutting, no provisioning for future operating expenses & timing differences (y-o-y trend not to be extrapolated to Q2)

Cost/income of banking and asset management at 51%*

Operating expenses (m)

11

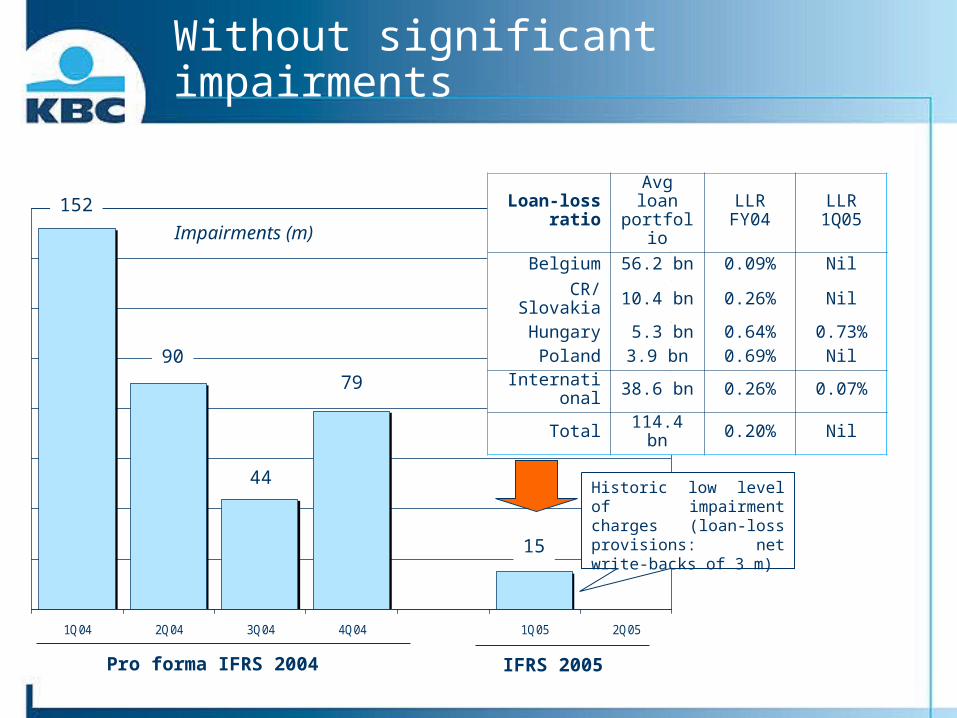

Without significant impairments

1Q04 2Q04 3Q04 4Q04 1Q05 2Q05

Pro forma IFRS 2004 IFRS 2005

15

152

90

44

79

Loan-loss ratio

Avg loan portfolio

LLRFY04

LLR1Q05

Belgium 56.2 bn 0.09% Nil

CR/Slovakia 10.4 bn 0.26% NilHungary 5.3 bn 0.64% 0.73%

Poland 3.9 bn 0.69% Nil

International 38.6 bn 0.26% 0.07%

Total 114.4 bn 0.20% Nil

Historic low level of impairment charges (loan-loss provisions: net write-backs of 3 m)

Impairments (m)

12

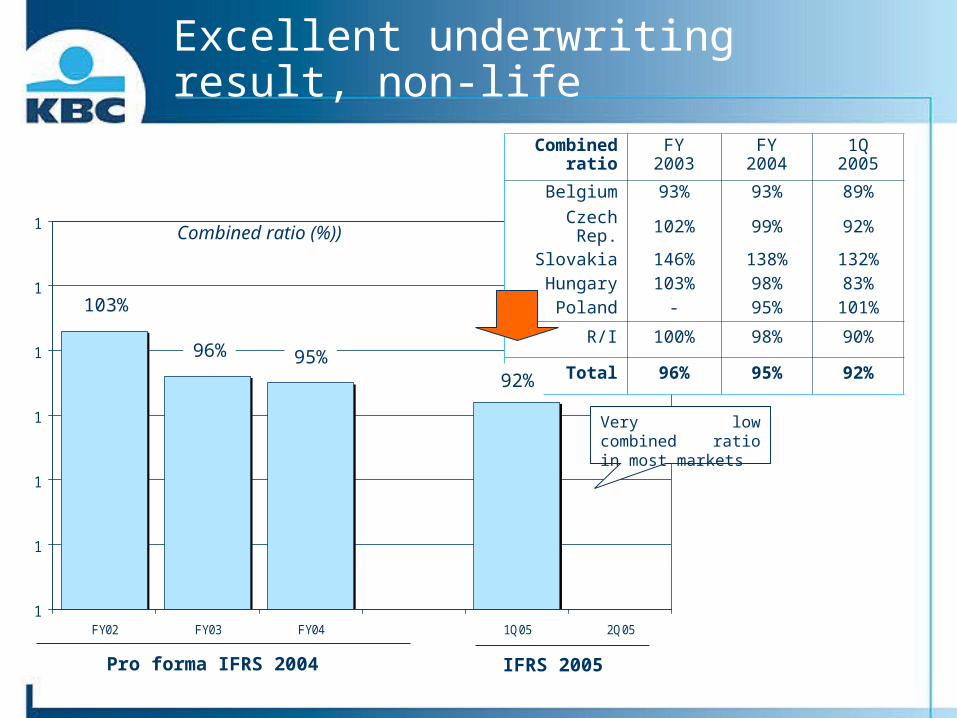

Excellent underwriting result, non-life

1

1

1

1

1

1

1

FY02 FY03 FY04 1Q05 2Q05

Pro forma IFRS 2004 IFRS 2005

103%

96% 95%

Combined ratio

FY2003

FY2004

1Q2005

Belgium 93% 93% 89%

Czech Rep. 102% 99% 92%Slovakia 146% 138% 132%Hungary 103% 98% 83%

Poland - 95% 101%

R/I 100% 98% 90%

Total 96% 95% 92%

Very low combined ratio in most markets

Combined ratio (%))

92%

13

Asset growth

Customer loans (1)

o/w mortgages

Customer deposits (1)

‘Life deposits’

AUM(off-balance)

108.4 bn 29.0 bn 166.4 bn 13.9 bn 150.7 bn

Total %, Ytd (1) +2% +4% +4% +3% +7%

Belgium +2% +4% +5% +3% +9%

CEE- CR/Slovakia- Hungary- Poland

0%+1%+1%-4%

+6%+6%+8%+2%

+10%+14%+ 4%+ 2%

+7%+8%

+15%-7%

+7%+12%+35%-14%

Rest of the world +4% +6% +2% -5% +5%

Note:(1) Growth excl. (reverse) repo’s

Foto gebouw

Financial highlights - 1Q 2005

- Group performance

- Headlines per segment

FY 2005 profit outlook

Additional information on 1Q 2005 results

2004 pro forma IFRS accounts

15

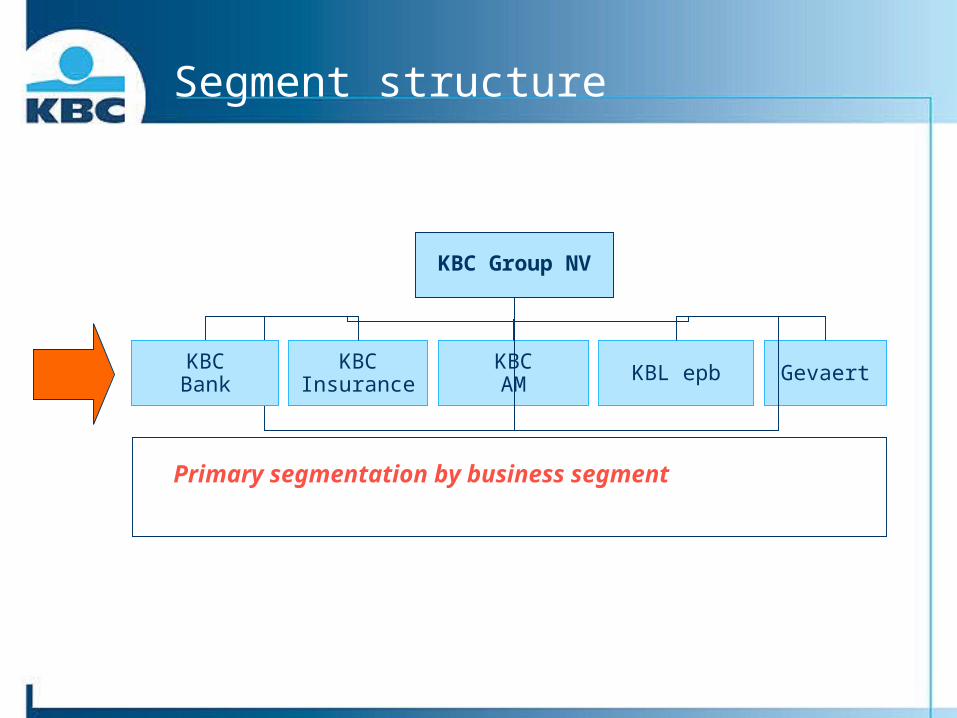

Segment structure

KBC Group NV

KBCInsurance

KBCAM KBL epb GevaertKBC

Bank

Primary segmentation by business segment

16

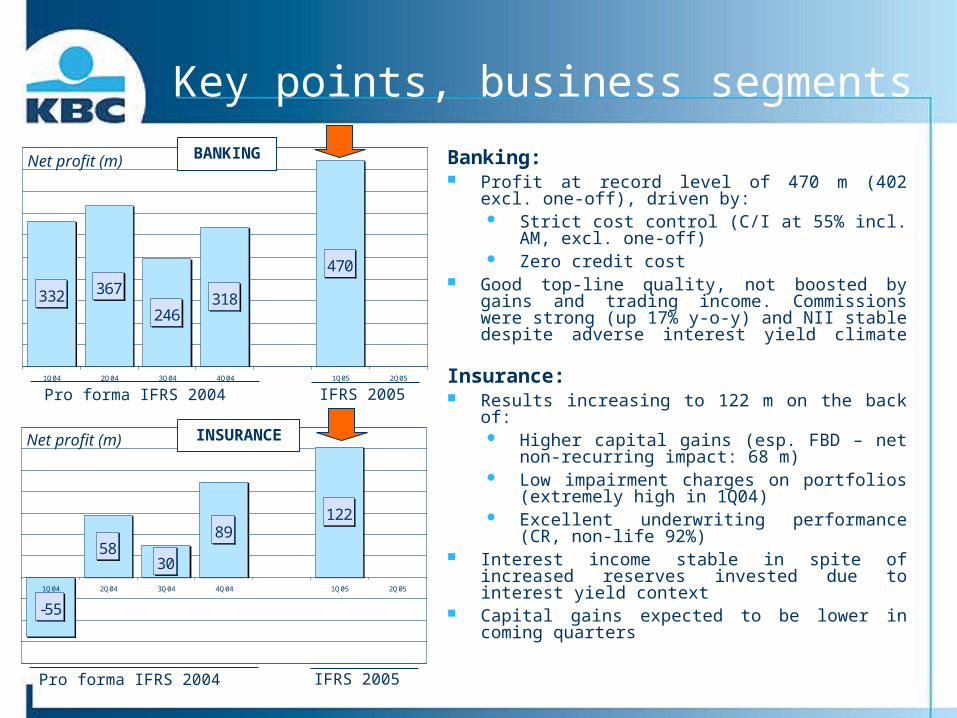

Key points, business segments

-55

5830

89122

1Q04 2Q04 3Q04 4Q04 1Q05 2Q05

Pro forma IFRS 2004 IFRS 2005

Net profit (m)

332 367

246318

470

1Q04 2Q04 3Q04 4Q04 1Q05 2Q05

Pro forma IFRS 2004 IFRS 2005

Net profit (m)

INSURANCE

BANKING Banking: Profit at record level of 470 m (402 excl. one-off),

driven by: Strict cost control (C/I at 55% incl. AM, excl.

one-off) Zero credit cost

Good top-line quality, not boosted by gains and trading income. Commissions were strong (up 17% y-o-y) and NII stable despite adverse interest yield climate

Insurance: Results increasing to 122 m on the back of:

Higher capital gains (esp. FBD – net non-recurring impact: 68 m)

Low impairment charges on portfolios (extremely high in 1Q04)

Excellent underwriting performance (CR, non-life 92%)

Interest income stable in spite of increased reserves invested due to interest yield context

Capital gains expected to be lower in coming quarters

17

Key points, business segments

43

2338

-30

53

1Q04 2Q04 3Q04 4Q04 1Q05 2Q05

Pro forma IFRS 2004 IFRS 2005

Net profit (m)

5158 53

6658

1Q04 2Q04 3Q04 4Q04 1Q05 2Q05

Pro forma IFRS 2004 IFRS 2005

Net profit (m)

EUROPEAN PRIVATE BANKING

ASSET MANAGEMENT Asset management: AUM in 1Q05 up 8% to 85.2 bn on the back of new

money entries Profit contribution at 58 m, +7 m y-o-y (driven by

increased AUM), down 8 m q-o-q (exceptionally high dividend income in Q4)

Note: total 3rd assets of the group: 150.7 bn Asset management segment: 72.3 bn (3rd party)

+ 12.9 bn (group assets) Banking segment: 28.7 bn (mostly private and

HNWI assets in Belgium and CEE) European private banking segment: 49.7 bn (o/w

46.0 bn of private customers via epb network)

European private banking: Profit contribution at 53 m, up 10 m y-o-y and up 83

m q-o-q (Q4 heavily depressed by one-off restructuring provisions)

Top-line at high level (partly due to M2M of financial instruments) with sustained growth trend of commission income

Private banking AUM in 1Q05 up 6% to 49.7 bn Cost/income at 63% No relevant impairment charges

18

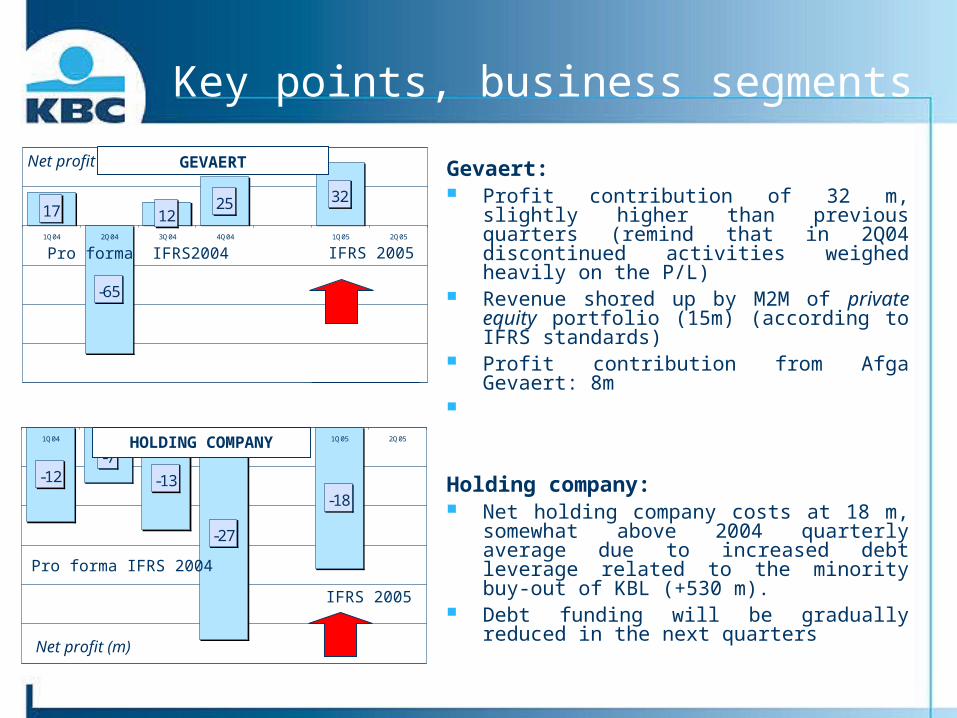

17

-65

1225 32

1Q04 2Q04 3Q04 4Q04 1Q05 2Q05

Pro forma IFRS2004

Key points, business segments

-12-7

-13

-27

-18

1Q04 2Q04 3Q04 4Q04 1Q05 2Q05

Pro forma IFRS 2004

IFRS 2005

Net profit (m)

IFRS 2005

Net profit (m)

HOLDING COMPANY

GEVAERT Gevaert: Profit contribution of 32 m, slightly higher than

previous quarters (remind that in 2Q04 discontinued activities weighed heavily on the P/L)

Revenue shored up by M2M of private equity portfolio (15m) (according to IFRS standards)

Profit contribution from Afga Gevaert: 8m

Holding company: Net holding company costs at 18 m, somewhat

above 2004 quarterly average due to increased debt leverage related to the minority buy-out of KBL (+530 m).

Debt funding will be gradually reduced in the next quarters

19

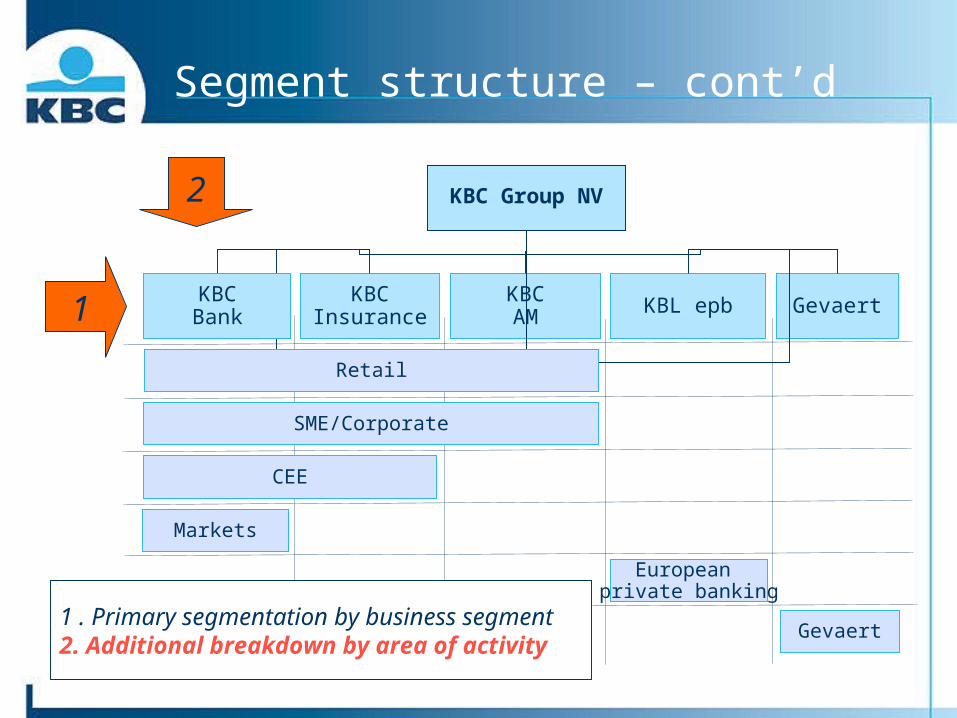

Segment structure – cont’d

KBC Group NV

KBCInsurance

KBCAM KBL epb GevaertKBC

Bank

CEE

Markets

European private banking

Gevaert

Retail

SME/Corporate

1

2

1 . Primary segmentation by business segment2. Additional breakdown by area of activity

20

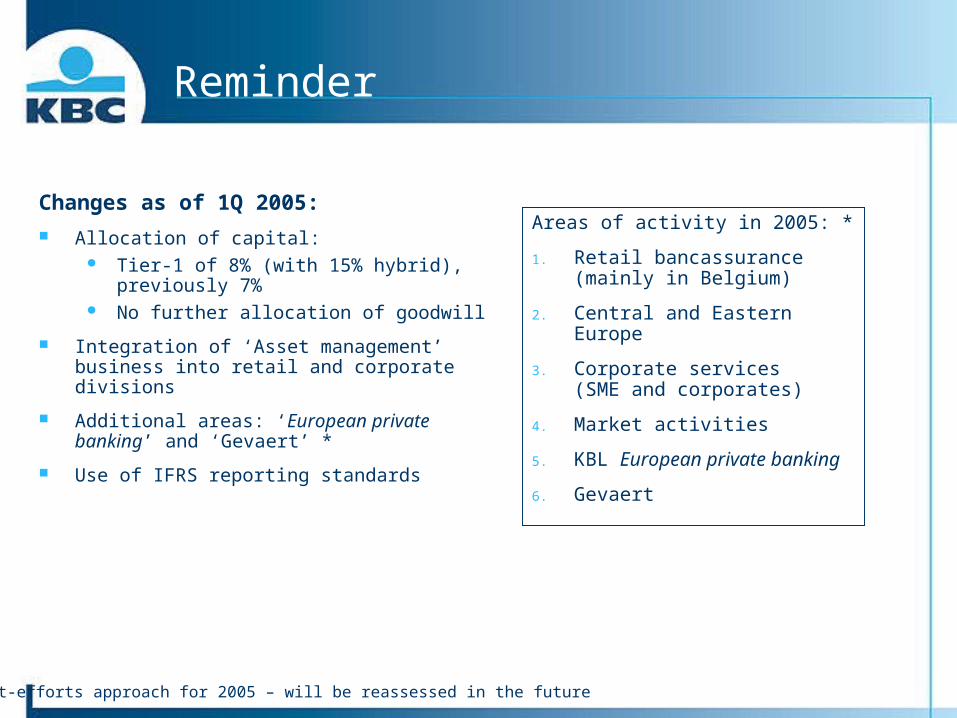

Reminder

Changes as of 1Q 2005:

Allocation of capital: Tier-1 of 8% (with 15% hybrid), previously 7% No further allocation of goodwill

Integration of ‘Asset management’ business into retail and corporate divisions

Additional areas: ‘European private banking’ and ‘Gevaert’ *

Use of IFRS reporting standards

Areas of activity in 2005: *

1. Retail bancassurance (mainly in Belgium)

2. Central and Eastern Europe

3. Corporate services (SME and corporates)

4. Market activities

5. KBL European private banking

6. Gevaert

* Best-efforts approach for 2005 – will be reassessed in the future

21

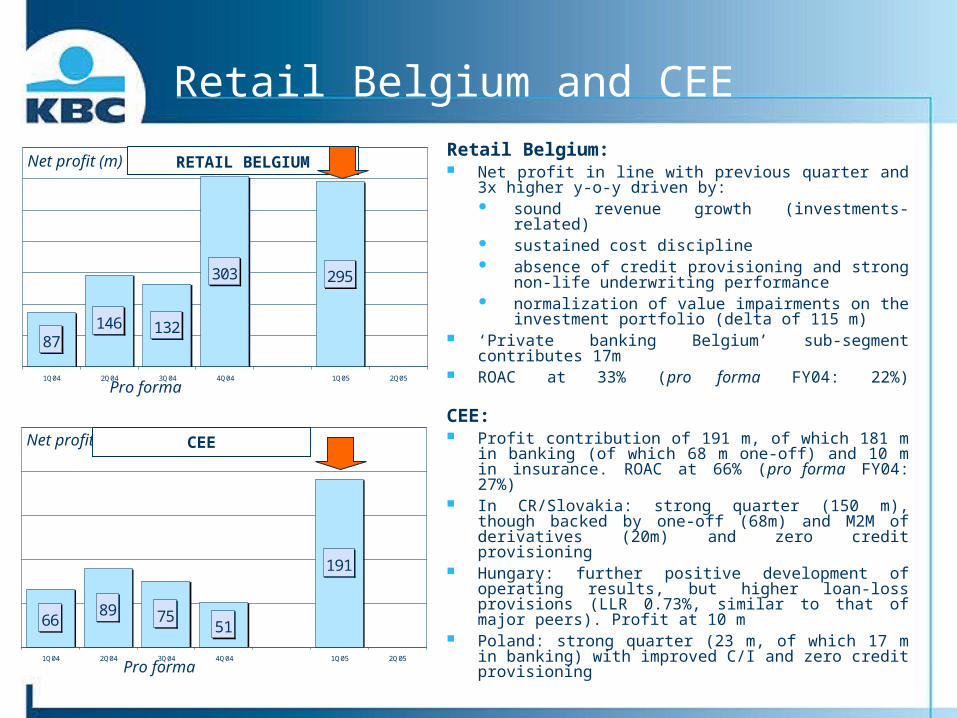

Retail Belgium and CEE

6689 75

51

191

1Q04 2Q04 3Q04 4Q04 1Q05 2Q05

Pro forma

Net profit (m)

87146 132

303 295

1Q04 2Q04 3Q04 4Q04 1Q05 2Q05

Pro forma

Net profit (m)

CEE

RETAIL BELGIUMRetail Belgium: Net profit in line with previous quarter and 3x

higher y-o-y driven by: sound revenue growth (investments-related) sustained cost discipline absence of credit provisioning and strong non-

life underwriting performance normalization of value impairments on the

investment portfolio (delta of 115 m) ‘Private banking Belgium’ sub-segment contributes

17m ROAC at 33% (pro forma FY04: 22%)

CEE: Profit contribution of 191 m, of which 181 m in

banking (of which 68 m one-off) and 10 m in insurance. ROAC at 66% (pro forma FY04: 27%)

In CR/Slovakia: strong quarter (150 m), though backed by one-off (68m) and M2M of derivatives (20m) and zero credit provisioning

Hungary: further positive development of operating results, but higher loan-loss provisions (LLR 0.73%, similar to that of major peers). Profit at 10 m

Poland: strong quarter (23 m, of which 17 m in banking) with improved C/I and zero credit provisioning

22

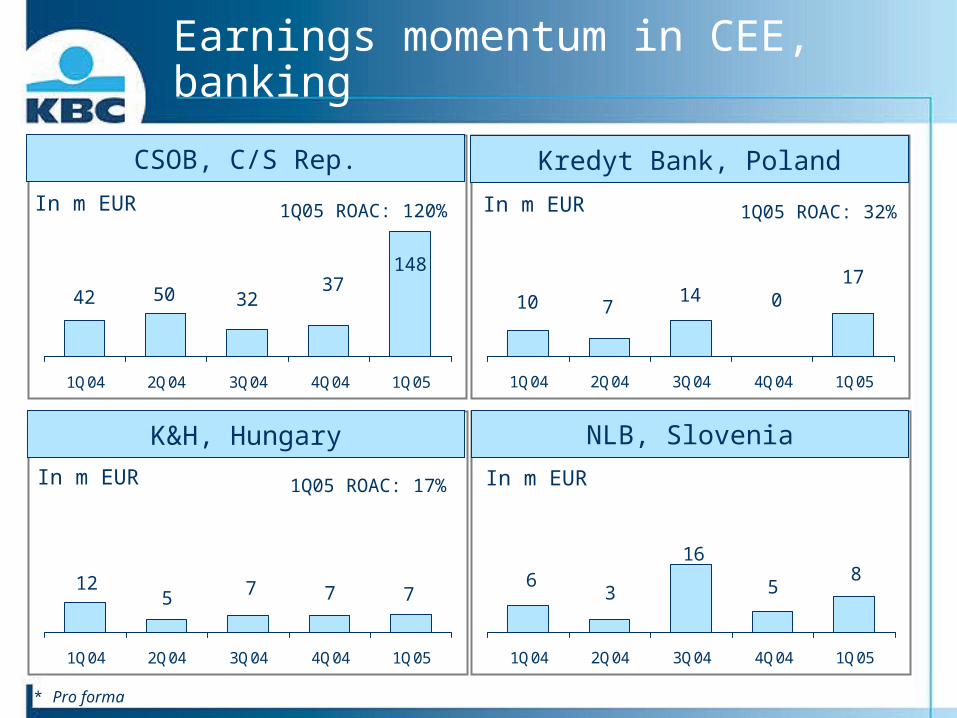

Earnings momentum in CEE, banking

* Pro forma

3250 3742

148

1Q04 2Q04 3Q04 4Q04 1Q05

CSOB, C/S Rep.

In m EUR 1Q05 ROAC: 120%

712 75 7

1Q04 2Q04 3Q04 4Q04 1Q05

K&H, Hungary

In m EUR 1Q05 ROAC: 17%

1710 07

14

1Q04 2Q04 3Q04 4Q04 1Q05

Kredyt Bank, Poland

In m EUR 1Q05 ROAC: 32%

86 53

16

1Q04 2Q04 3Q04 4Q04 1Q05

NLB, Slovenia

In m EUR

23

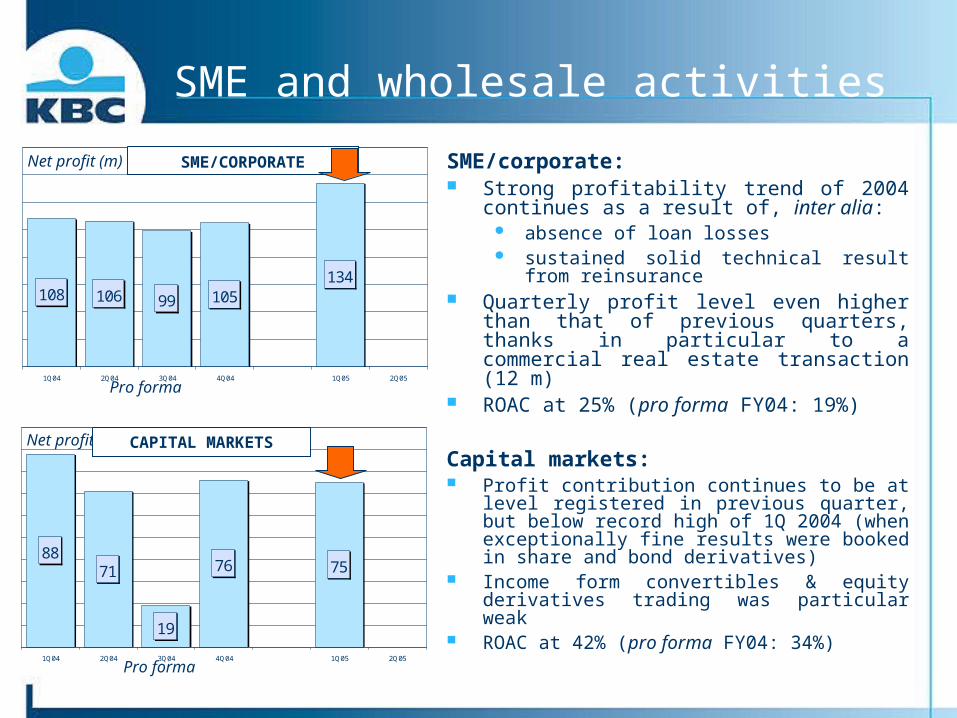

SME and wholesale activities

8871

19

76 75

1Q04 2Q04 3Q04 4Q04 1Q05 2Q05

Pro forma

Net profit (m)

108 106 99 105134

1Q04 2Q04 3Q04 4Q04 1Q05 2Q05

Pro forma

Net profit (m)

CAPITAL MARKETS

SME/CORPORATE SME/corporate: Strong profitability trend of 2004 continues as a

result of, inter alia: absence of loan losses sustained solid technical result from

reinsurance Quarterly profit level even higher than that of

previous quarters, thanks in particular to a commercial real estate transaction (12 m)

ROAC at 25% (pro forma FY04: 19%)

Capital markets: Profit contribution continues to be at level

registered in previous quarter, but below record high of 1Q 2004 (when exceptionally fine results were booked in share and bond derivatives)

Income form convertibles & equity derivatives trading was particular weak

ROAC at 42% (pro forma FY04: 34%)

24

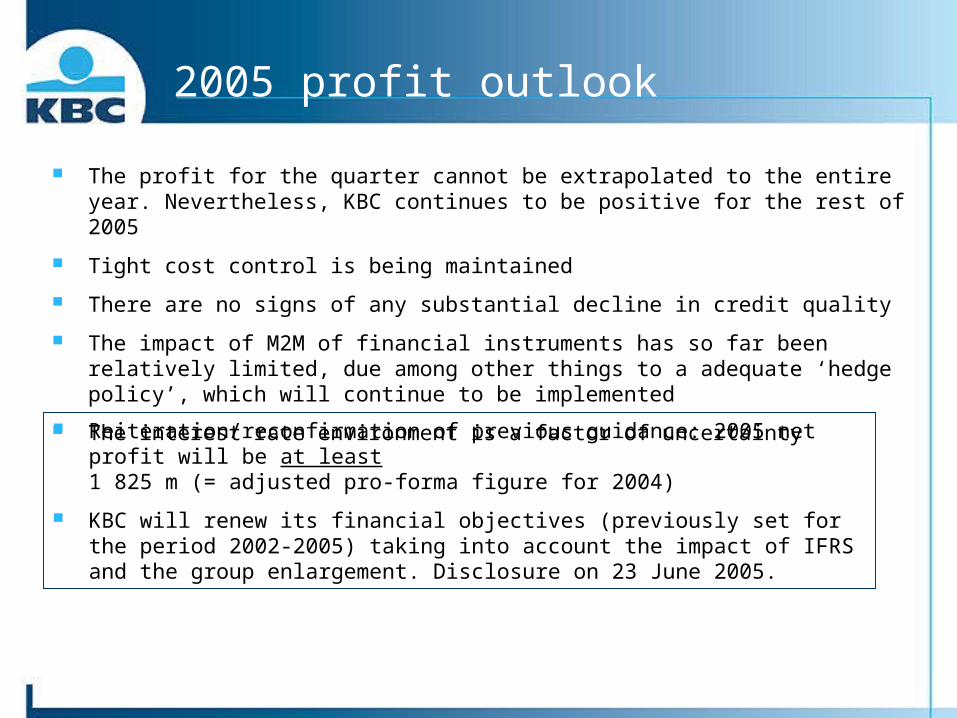

2005 profit outlook

The profit for the quarter cannot be extrapolated to the entire year. Nevertheless, KBC continues to be positive for the rest of 2005

Tight cost control is being maintained

There are no signs of any substantial decline in credit quality

The impact of M2M of financial instruments has so far been relatively limited, due among other things to a adequate ‘hedge policy’, which will continue to be implemented

The interest rate environment is a factor of uncertainty

Reiteration/reconfirmation of previous guidance: 2005 net profit will be at least 1 825 m (= adjusted pro-forma figure for 2004)

KBC will renew its financial objectives (previously set for the period 2002-2005) taking into account the impact of IFRS and the group enlargement. Disclosure on 23 June 2005.

Foto gebouw

Financial highlights - 1Q 2005

- Group performance

- Headlines per segment

FY 2005 profit outlook

Additional information on 1Q 2005 results

2004 pro forma IFRS quarterly accounts

26

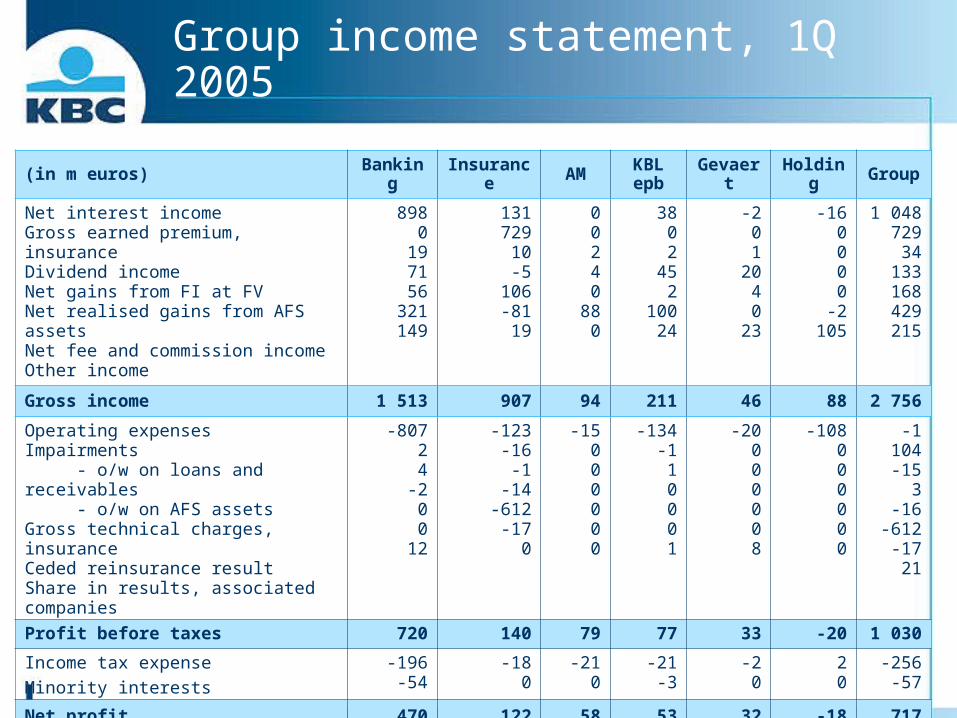

Group income statement, 1Q 2005

(in m euros) Banking Insurance AM KBLepb Gevaert Holding Group

Net interest incomeGross earned premium, insuranceDividend incomeNet gains from FI at FV Net realised gains from AFS assetsNet fee and commission incomeOther income

8980

197156

321149

13172910-5

106-8119

00240

880

3802

452

10024

-201

2040

23

-160000

-2105

1 04872934

133168429215

Gross income 1 513 907 94 211 46 88 2 756

Operating expensesImpairments - o/w on loans and receivables - o/w on AFS assetsGross technical charges, insuranceCeded reinsurance resultShare in results, associated companies

-80724

-200

12

-123-16-1

-14-612-17

0

-15000000

-134-110001

-20000008

-108000000

-1 104-15

3-16

-612-1721

Profit before taxes 720 140 79 77 33 -20 1 030

Income tax expense

Minority interests

-196-54

-180

-210

-21-3

-20

20

-256-57

Net profit 470 122 58 53 32 -18 717

27

Gross income - reconciliation

806 796 755 781995 966 910 963 1048

351 313 323 393

357 324 323399

429

536525

320

562355

425290

365382

1245 1373

870

15501275 1404

901

1577

729

1Q04 2Q04 3Q04 4Q04 1Q04 2Q04 3Q04 4Q04 1Q05 2Q05

As of 1Q04: incl. insurance and KBL

1Q05: IFRS reclassification from

‘trading’(-) to ‘interest’(+)

As published (B-GAAP), KBC Old Pro forma (IFRS 2004), MergCo IFRS 2005

3 462

2 517

3 1783 175

2 756

As of 1Q04: incl. insur. sales commissions (-)

and KBL’s fee income (+)

As of 1Q05: excluding unit-linked volumes

As of 1Q04: ‘gross’ instead of ‘net premium’

Investment income insurance largely to

‘interest income’

Net interest incomeNet fee & commission income

Net realized gains AFSDividend income, net gains from FI at FV, other income.

Gross earned premium

28

Operating expenses - reconciliation

928 910844

954 1002

830 8621006

822

173 163158

170 124

129123

135

123

122

135140

236

134

1Q04 2Q04 3Q04 4Q04 1Q04 2Q04 3Q04 4Q04 1Q05 2Q05

IFRS reclassification as of 1Q04: incl. operating

provisions

4Q04 lifted by staff profit-sharing bonuses and marketing costs

1Q05 down due to cost cutting, low

provisioning & timing differences

4Q04 lifted at KBL by restructuring provision

As published (B-GAAP), KBC Old Pro forma (IFRS 2004), MergCo IFRS 2005

1 1031 071

1 004

1 424

1 1471 105

1 269

1 1041 129

IFRS reclassification as of 1Q04: paid commissions to

‘commission income’

Banking +AM InsuranceHolding Co KBL epbGevaert

29

Impairments - reconciliation

43

77

14

65

33

74

15

7627

119

12

18

16

11

11

123

31

1Q04 2Q04 3Q04 4Q04 1Q04 2Q04 3Q04 4Q04 1Q05 2Q05

1Q04: high equity impairments (under

IFRS, impact not compensated by write-

back of dedicated provisioning, as was the

case under B-GAAP)

As published (B-GAAP), KBC Old Pro forma (IFRS 2004), MergCo IFRS 2005

15

152

90

44

79

Under IFRS, no further amortization of

goodwill (avg. 10m/Q)

KBL’s 10 m write-back explains delta with B-GAAP

Zero credit-loss provisioning

11 m real-estate impairments

KBL’s 10 m provisioning explains delta with B-GAAP

KBL/Gevaert’s 18 m write-back explains delta with B-GAAP

30

Areas of activity overview, 1Q 2005 (1)

(in m euros and % y-o-y)

Retail CEE SME/Corp.

Markets KBLepb Gevaert Total

Banking and AM

Gross incomeOperating expensesAssociatesIncome tax expenseMinority interestsNet profit – group share

659 (+13%)- 371 (-2%)

0 (-) - 87 (58%)

0 (-)213 (47%)

522 (+47%)-253 (6%)

1 (-)- 59 (79%)-25(-233%)181 (157%)

258(+13%)-94 (15%)

0 (-)- 44 (15%)

0 (-)123 (19%)

207 (-28%)-93 (-38%)

0 (-)- 40 (15%)

0 (-)75 (19%)

211 (13%)-134 (10%)

-1 (-)- 21 (-)

-3 (-)53 (22%)

1 608 (+1%)-822 (-18%)

12 +20%)- 218 (+59%)

-54 (+23%)528 (+38%)

Insurance

Gross incomeOperating expensesAssociatesIncome tax expenseMinority interestsNet profit – group share

618 (-45%)- 74 (-4%)

0 (-)- 11 (-91%)

0 (-)82 (-241%)

203 (13%)- 41 (0%)

0 (-)- 6 (-326%)- 2 (-259%)10 (-241%)

79 (-)- 8 (-)

0 (-)- 1 (-)

0 (-)12 (-102%)

907 (+34%) - 123 (-1%)

0 (-)- 18 (64%)

0 (-)122 (-)

Holding Co

Net profit – group share 32 - 18

Group total

Net profit – Group shareShare in group resultROAC

295 (238%)41%33%

191(191%)27%66%

134 (24%)19%25%

75 (-15%)10%41%

53 (+22%) 7%

18%

32 (84%)4%13%

717 (91%)

24%

(1) excl. Non-allocated

31

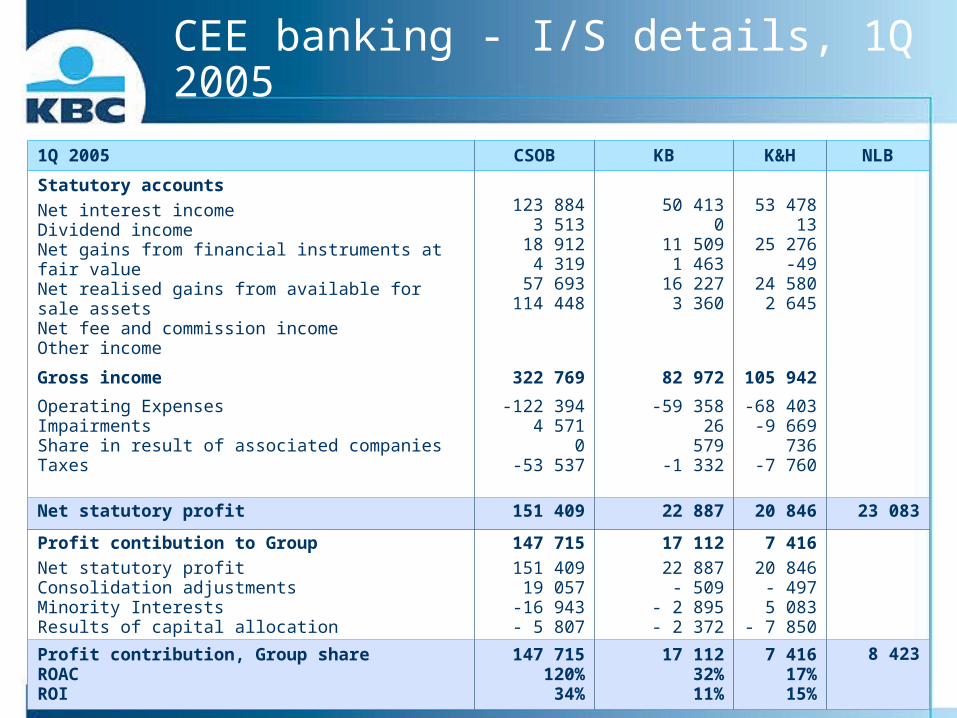

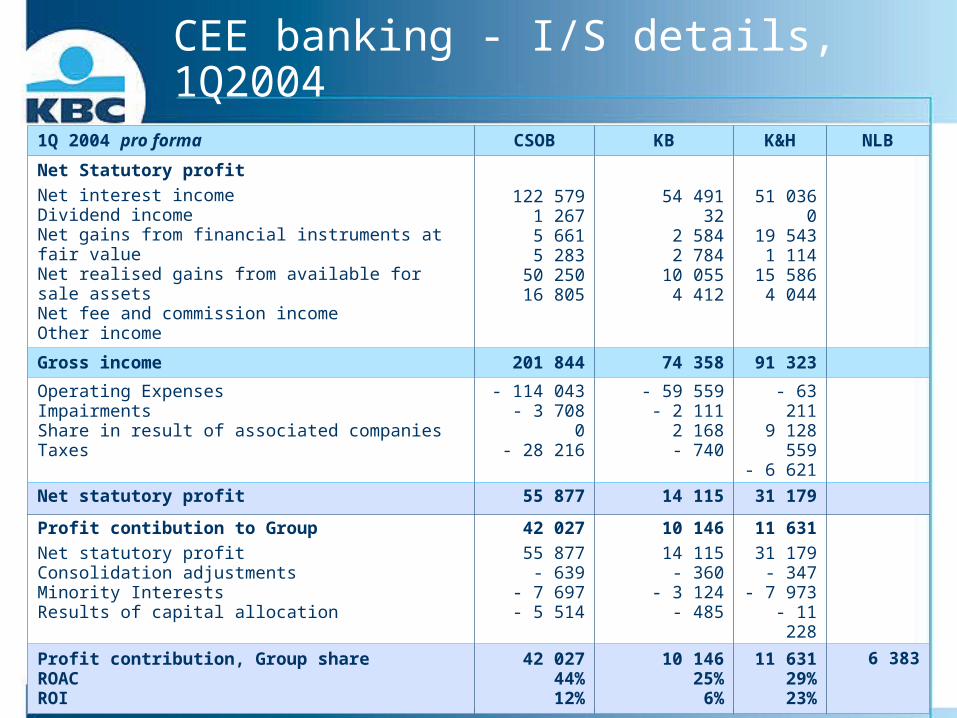

CEE banking - I/S details, 1Q 2005

1Q 2005 CSOB KB K&H NLB

Statutory accounts

Net interest incomeDividend incomeNet gains from financial instruments at fair valueNet realised gains from available for sale assetsNet fee and commission incomeOther income

123 8843 513

18 9124 319

57 693114 448

50 4130

11 5091 463

16 2273 360

53 47813

25 276-49

24 5802 645

Gross income 322 769 82 972 105 942

Operating ExpensesImpairmentsShare in result of associated companiesTaxes

-122 3944 571

0-53 537

-59 35826

579-1 332

-68 403-9 669

736-7 760

Net statutory profit 151 409 22 887 20 846 23 083

Profit contibution to Group

Net statutory profitConsolidation adjustmentsMinority InterestsResults of capital allocation

147 715

151 40919 057

-16 943- 5 807

17 112

22 887- 509

- 2 895- 2 372

7 416

20 846- 497

5 083- 7 850

Profit contribution, Group shareROACROI

147 715120%34%

17 11232%11%

7 41617%15%

8 423

32

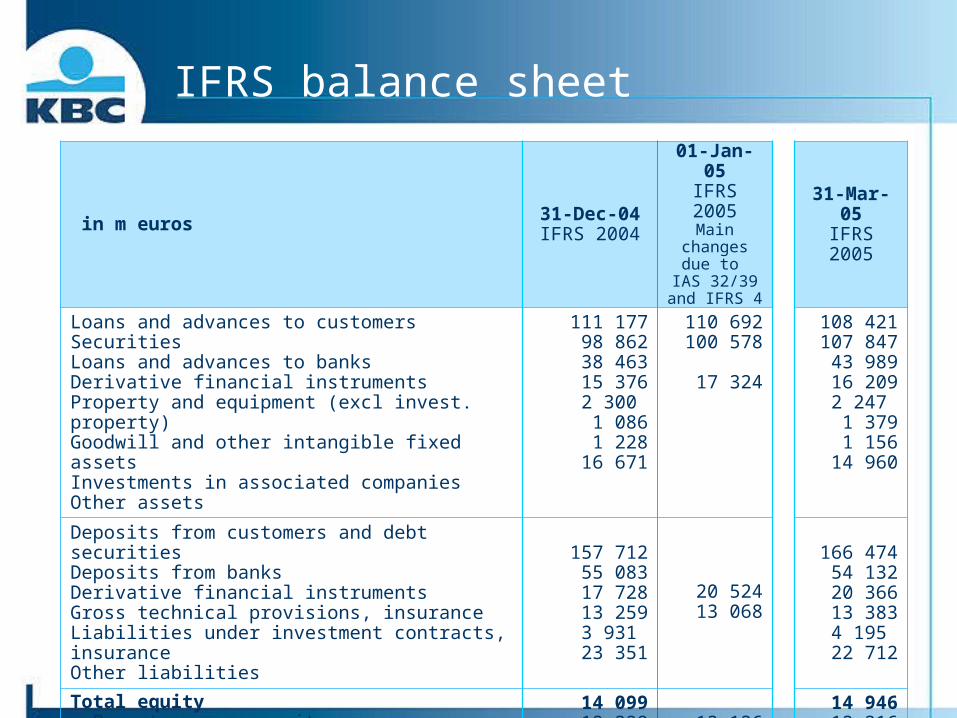

IFRS balance sheet

in m euros 31-Dec-04IFRS 2004

01-Jan-05IFRS 2005

Main changes due

to IAS 32/39

and IFRS 4

31-Mar-05IFRS 2005

Loans and advances to customersSecuritiesLoans and advances to banksDerivative financial instrumentsProperty and equipment (excl invest. property) Goodwill and other intangible fixed assetsInvestments in associated companiesOther assets

111 17798 86238 46315 3762 300 1 0861 228

16 671

110 692100 578

17 324

108 421107 847

43 98916 2092 247 1 3791 156

14 960

Deposits from customers and debt securitiesDeposits from banksDerivative financial instrumentsGross technical provisions, insuranceLiabilities under investment contracts, insuranceOther liabilities

157 71255 08317 72813 2593 931 23 351

20 52413 068

166 47454 13220 36613 3834 195 22 712

Total equity- Parent company equity- Minorities

14 09912 328

1 77113 136

14 94613 316

1 630

Balance sheet total 285 163 296 208

33

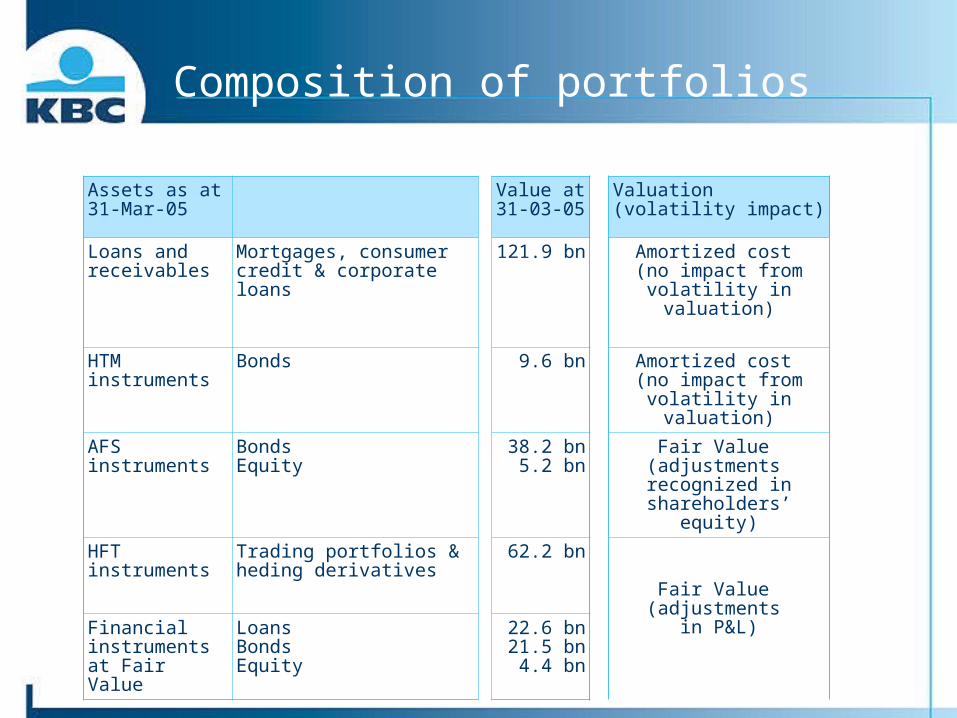

Composition of portfolios

Assets as at31-Mar-05

Value at 31-03-05

Valuation (volatility impact)

Loans and receivables

Mortgages, consumer credit & corporate loans

121.9 bn Amortized cost (no impact from volatility

in valuation)

HTMinstruments

Bonds 9.6 bn Amortized cost (no impact from volatility

in valuation)

AFS instruments

BondsEquity

38.2 bn5.2 bn

Fair Value (adjustments recognized in

shareholders’ equity)

HFT instruments Trading portfolios & heding derivatives

62.2 bn

Fair Value (adjustments

in P&L)Financial instruments at Fair Value

LoansBondsEquity

22.6 bn21.5 bn

4.4 bn

34

Number of shares

BASIC NUMBER OF SHARES (in millions)

Ordinary shares

Mandatory convertibles

Treasury shares

Basic No.of shares

Avg. quarter

Average Ytd

31/12/03 367.7 2. 6 -11.0 359. 4 - -

31/03/04 367.0 2. 6 -10.1 359.6 359.5 359.5

30/06/04 366.3 2. 6 -9.7 359.2 359.4 359.5

30/09/04 366.3 2. 6 -9.5 359.4 359.3 359.4

31/12/04 366.4 2. 6 -9. 6 359.5 359.5 359.4

31/03/05 366. 4 2. 6 -12.6 356.5 358. 0 358.0

DILUTIVE NUMBER OF SHARES (in millions)

Basic No. of shares

Stock options

Convertible bonds

Dilutive No. of shares

Avg. quarter

Average Ytd

31/12/03 359.4 6.1 5.2 370.7 - -

31/03/04 359.6 6.1 5.2 370.9 370.8 370.8

30/06/04 359.2 6.0 5.2 370.5 370.7 370.8

30/09/04 359.5 5.8 5.2 370.5 370.5 370.7

31/12/04 359.5 5.0 5.2 369.7 370.1 370.5

31/03/05 356.5 5.0 5.2 366.7 368.2 368.2

Net profit (in m EUR)

717

Basic number of shares

357 990 384

Diluted number of shares

368 187 859

Basic EPS (euros)

2.00

Diluted EPS (euros)

1.96

Foto gebouw

Financial highlights - 1Q 2005

- Group performance

- Headlines per segment

FY 2005 profit outlook

Additional information on 1Q 2005 results

2004 pro forma IFRS quarterly accounts

36

Important information

Pro forma figures 2004 are drafted according to the European IFRS. It is important to highlight that the impact of IFRS 32/39 on the valuation of financial instruments and of IFRS 4 on insurance contracts is therefore not included. As a result, the 2005 figures (which include the impact of the stated valuation rules) are not fully comparable with 2004 pro forma figures.

37

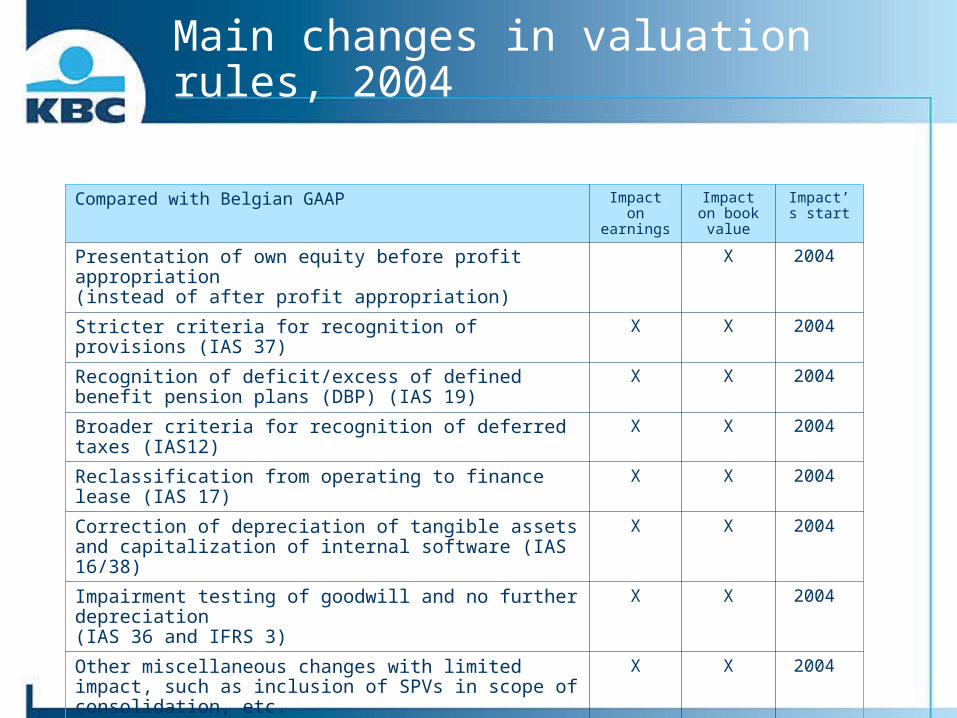

Main changes in valuation rules, 2004

Compared with Belgian GAAP Impact on earnings

Impact on book value

Impact’s start

Presentation of own equity before profit appropriation (instead of after profit appropriation)

X 2004

Stricter criteria for recognition of provisions (IAS 37) X X 2004

Recognition of deficit/excess of defined benefit pension plans (DBP) (IAS 19)

X X 2004

Broader criteria for recognition of deferred taxes (IAS12) X X 2004

Reclassification from operating to finance lease (IAS 17) X X 2004

Correction of depreciation of tangible assets and capitalization of internal software (IAS 16/38)

X X 2004

Impairment testing of goodwill and no further depreciation (IAS 36 and IFRS 3)

X X 2004

Other miscellaneous changes with limited impact, such as inclusion of SPVs in scope of consolidation, etc.

X X 2004

38

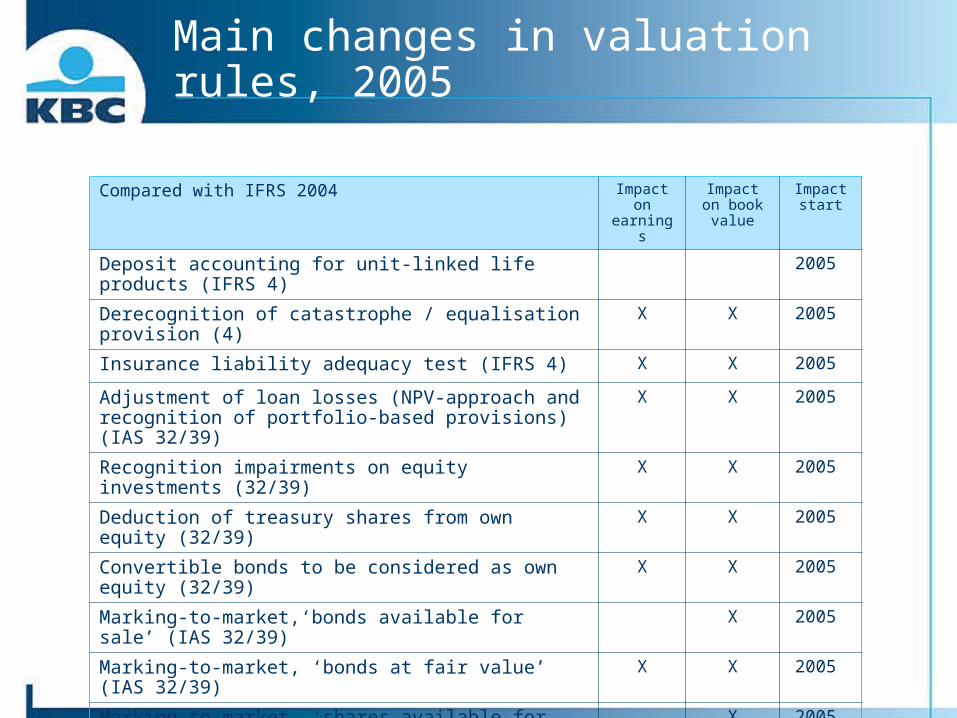

Main changes in valuation rules, 2005

Compared with IFRS 2004 Impact on earnings

Impact on book value

Impact start

Deposit accounting for unit-linked life products (IFRS 4) 2005

Derecognition of catastrophe / equalisation provision (4) X X 2005

Insurance liability adequacy test (IFRS 4) X X 2005

Adjustment of loan losses (NPV-approach and recognition of portfolio-based provisions) (IAS 32/39)

X X 2005

Recognition impairments on equity investments (32/39) X X 2005

Deduction of treasury shares from own equity (32/39) X X 2005

Convertible bonds to be considered as own equity (32/39) X X 2005

Marking-to-market,‘bonds available for sale’ (IAS 32/39) X 2005

Marking-to-market, ‘bonds at fair value’ (IAS 32/39) X X 2005

Marking-to-market, ‘shares available for sale’ (IAS 32/39) X 2005

Marking-to-market, ‘shares at fair value’ (IAS 32/39) X X 2005

Marking-to-market, derivatives not held for trading (32/39) X X 2005

39

11

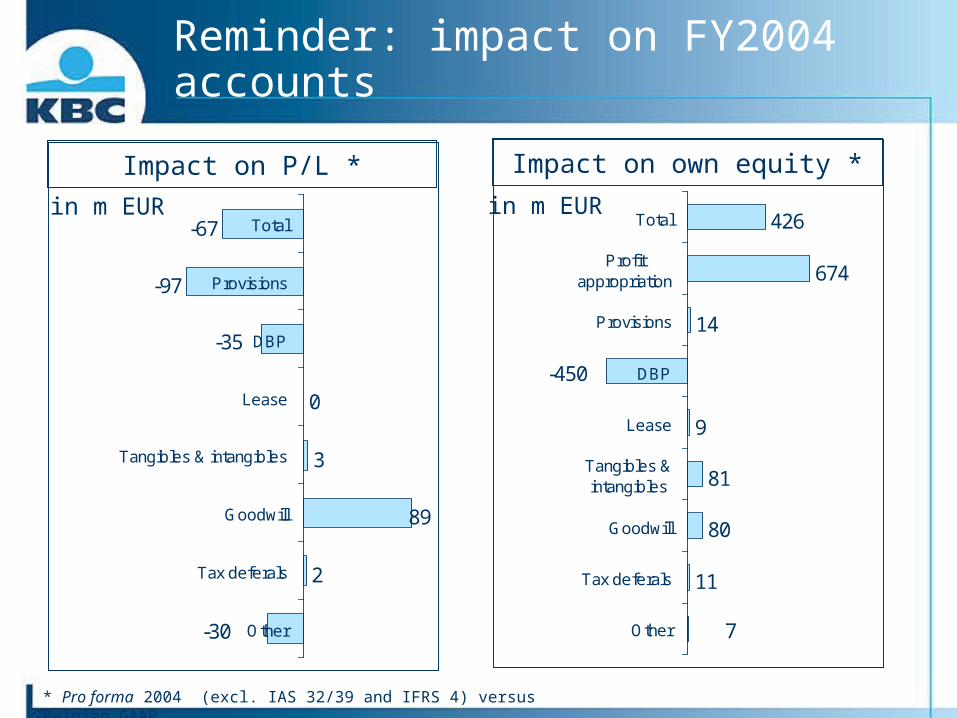

80

81

9

14

674

426

-450

7Other

Tax deferals

Goodwill

Tangibles &intangibles

Lease

DBP

Provisions

Profitappropriation

Total

2

89

3

0

-97

-67

-35

-30 Other

Tax deferals

Goodwill

Tangibles & intangibles

Lease

DBP

Provisions

Total

Reminder: impact on FY2004 accounts

Impact on own equity *Impact on P/L *

in m EUR in m EUR

* Pro forma 2004 (excl. IAS 32/39 and IFRS 4) versus Belgian GAAP

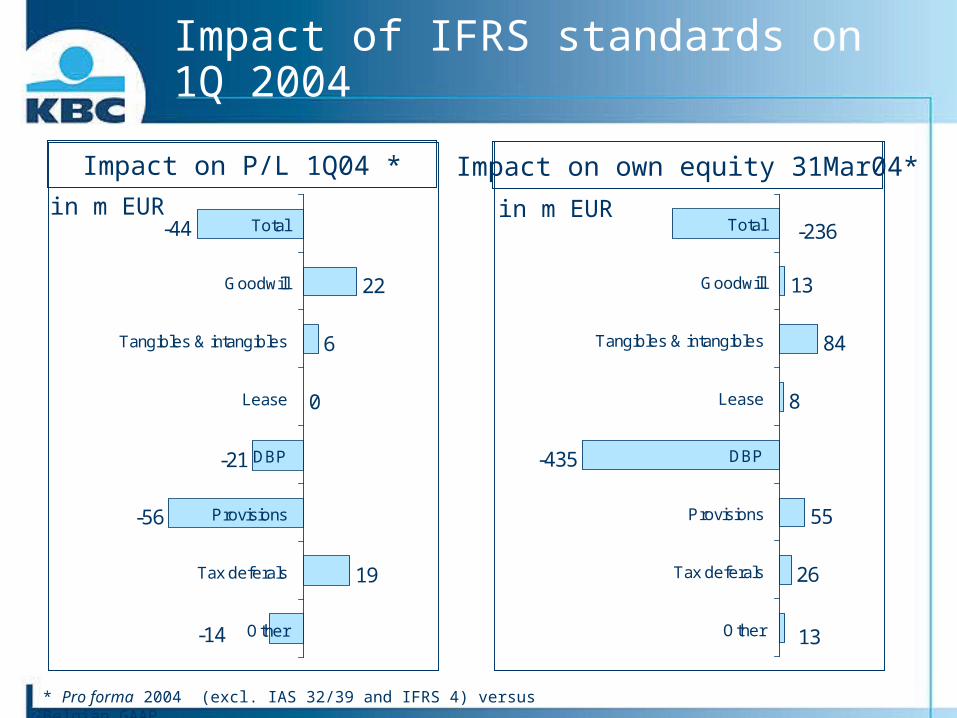

40

26

55

-435

8

84

13

-236

13Other

Tax deferals

Provisions

DBP

Lease

Tangibles & intangibles

Goodwill

Total

19

-56

-21

0

6

22

-44

-14 Other

Tax deferals

Provisions

DBP

Lease

Tangibles & intangibles

Goodwill

Total

Impact of IFRS standards on 1Q 2004

Impact on own equity 31Mar04*Impact on P/L 1Q04 *

in m EUR in m EUR

* Pro forma 2004 (excl. IAS 32/39 and IFRS 4) versus Belgian GAAP

41

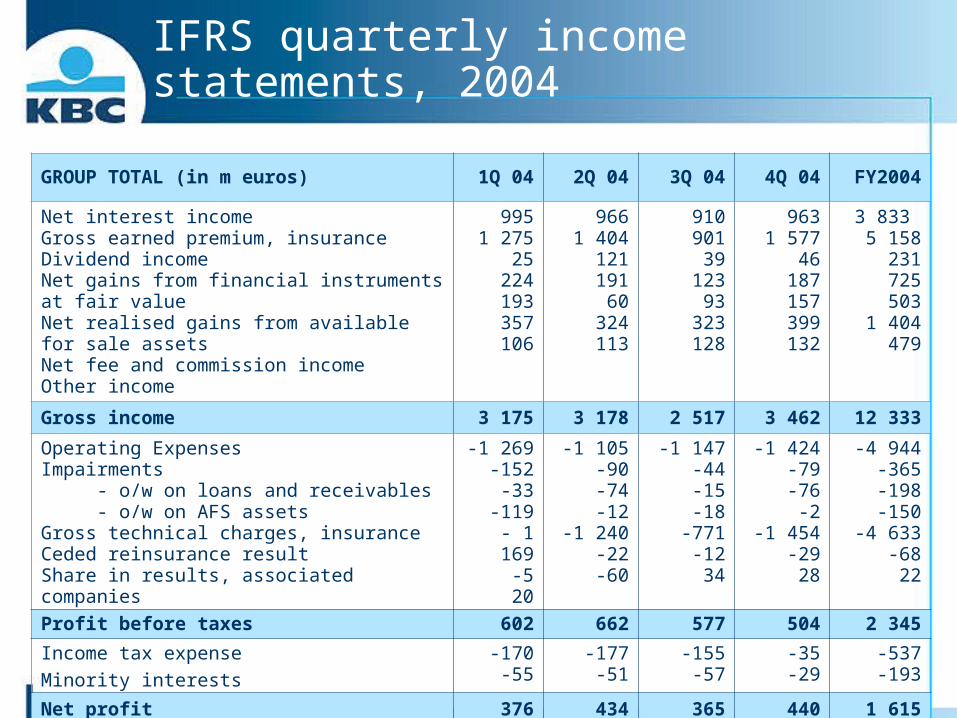

IFRS quarterly income statements, 2004

GROUP TOTAL (in m euros) 1Q 04 2Q 04 3Q 04 4Q 04 FY2004

Net interest incomeGross earned premium, insuranceDividend incomeNet gains from financial instruments at fair valueNet realised gains from available for sale assetsNet fee and commission incomeOther income

9951 275

25224193357106

9661 404

121191

60324113

910901

39123

93323128

9631 577

46187157399132

3 833 5 158

231725503

1 404479

Gross income 3 175 3 178 2 517 3 462 12 333

Operating ExpensesImpairments - o/w on loans and receivables - o/w on AFS assetsGross technical charges, insuranceCeded reinsurance resultShare in results, associated companies

-1 269-152

-33-119

- 1 169-520

-1 105-90-74-12

-1 240-22-60

-1 147-44-15-18

-771-1234

-1 424-79-76

-2-1 454

-2928

-4 944-365-198-150

-4 633-6822

Profit before taxes 602 662 577 504 2 345

Income tax expense

Minority interests

-170-55

-177-51

-155-57

-35-29

-537-193

Net profit 376 434 365 440 1 615

42

Banking - I/S details, 2004

BANKING SEGMENT (in m euros) 1Q 04 2Q 04 3Q 04 4Q 04 FY2004

Net interest incomeGross earned premium, insuranceDividend incomeNet gains from financial instruments at fair valueNet realised gains from available for sale assetsNet fee and commission incomeOther income

8360

13220116274

52

8250

41177

60226

71

7870

258556

23752

8050

23150

76305

68

3 253 0

103632307

1 042243

Gross income 1 511 1 400 1 241 1 428 5 581

Operating ExpensesImpairments - o/w on loans and receivables - o/w on AFS assetsGross technical charges, insuranceCeded reinsurance resultShare in results, associated companies

-989-39-42

300

10

-816-72-77

5003

-848-28-14

000

19

-993-80-65-15

003

-3 646-220-199

-700

35

Profit before taxes 493 516 383 358 1 750

Income tax expense

Minority interests

-117-44

-108-41

-93-45

-3-38

-320-167

Net profit 332 367 246 318 1 263

43

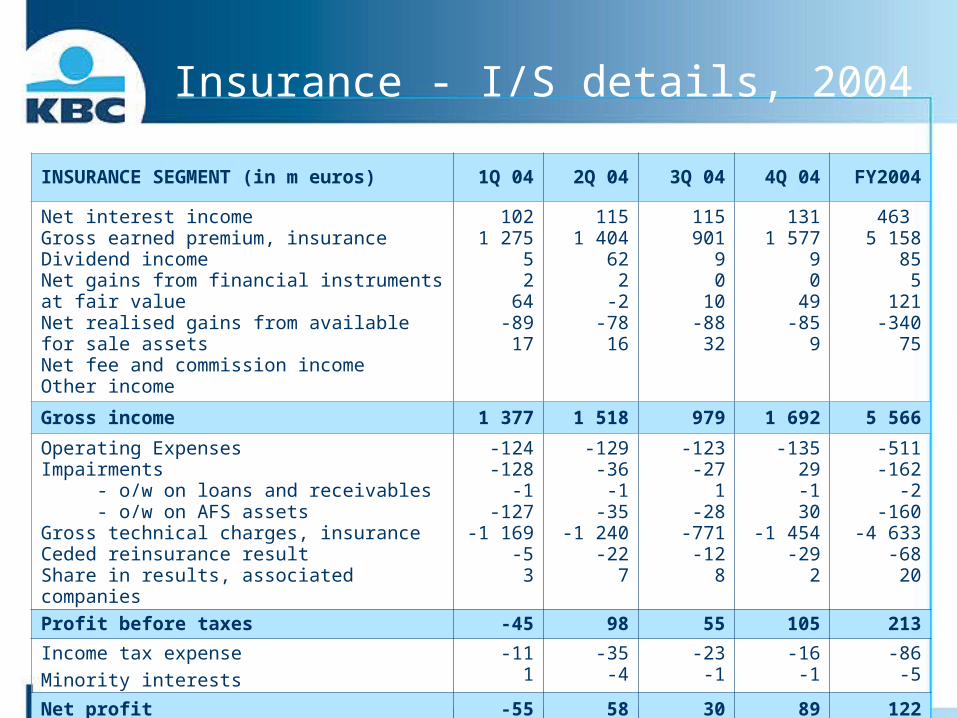

Insurance - I/S details, 2004

INSURANCE SEGMENT (in m euros) 1Q 04 2Q 04 3Q 04 4Q 04 FY2004

Net interest incomeGross earned premium, insuranceDividend incomeNet gains from financial instruments at fair valueNet realised gains from available for sale assetsNet fee and commission incomeOther income

1021 275

52

64-8917

1151 404

622

-2-7816

115901

90

10-8832

1311 577

90

49-85

9

463 5 158

855

121-340

75

Gross income 1 377 1 518 979 1 692 5 566

Operating ExpensesImpairments - o/w on loans and receivables - o/w on AFS assetsGross technical charges, insuranceCeded reinsurance resultShare in results, associated companies

-124-128

-1-127

-1 169-53

-129-36

-1-35

-1 240-22

7

-123-27

1-28

-771-12

8

-13529-130

-1 454-29

2

-511-162

-2-160

-4 633-6820

Profit before taxes -45 98 55 105 213

Income tax expense

Minority interests

-111

-35-4

-23-1

-16-1

-86-5

Net profit -55 58 30 89 122

44

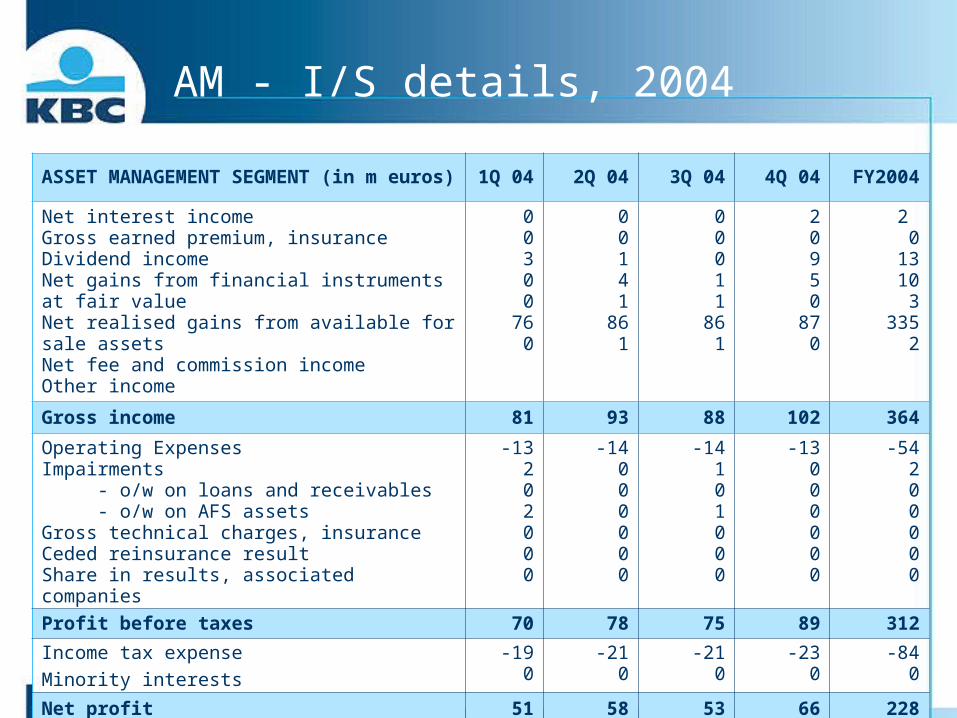

AM - I/S details, 2004

ASSET MANAGEMENT SEGMENT (in m euros) 1Q 04 2Q 04 3Q 04 4Q 04 FY2004

Net interest incomeGross earned premium, insuranceDividend incomeNet gains from financial instruments at fair valueNet realised gains from available for sale assetsNet fee and commission incomeOther income

00300

760

00141

861

00011

861

20950

870

2 0

1310

3335

2

Gross income 81 93 88 102 364

Operating ExpensesImpairments - o/w on loans and receivables - o/w on AFS assetsGross technical charges, insuranceCeded reinsurance resultShare in results, associated companies

-13202000

-14000000

-14101000

-13000000

-54200000

Profit before taxes 70 78 75 89 312

Income tax expense

Minority interests

-190

-210

-210

-230

-840

Net profit 51 58 53 66 228

45

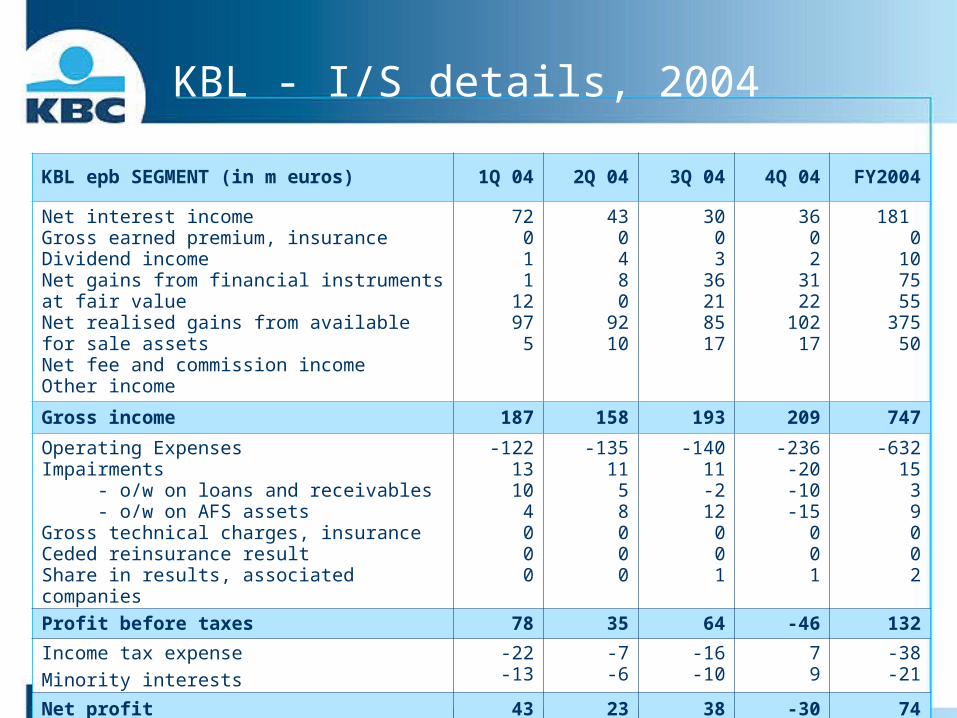

KBL - I/S details, 2004

KBL epb SEGMENT (in m euros) 1Q 04 2Q 04 3Q 04 4Q 04 FY2004

Net interest incomeGross earned premium, insuranceDividend incomeNet gains from financial instruments at fair valueNet realised gains from available for sale assetsNet fee and commission incomeOther income

72011

1297

5

430480

9210

3003

36218517

3602

3122

10217

181 0

107555

37550

Gross income 187 158 193 209 747

Operating ExpensesImpairments - o/w on loans and receivables - o/w on AFS assetsGross technical charges, insuranceCeded reinsurance resultShare in results, associated companies

-1221310

4000

-13511

58000

-14011-212

001

-236-20-10-15

001

-63215

39002

Profit before taxes 78 35 64 -46 132

Income tax expense

Minority interests

-22-13

-7-6

-16-10

79

-38-21

Net profit 43 23 38 -30 74

46

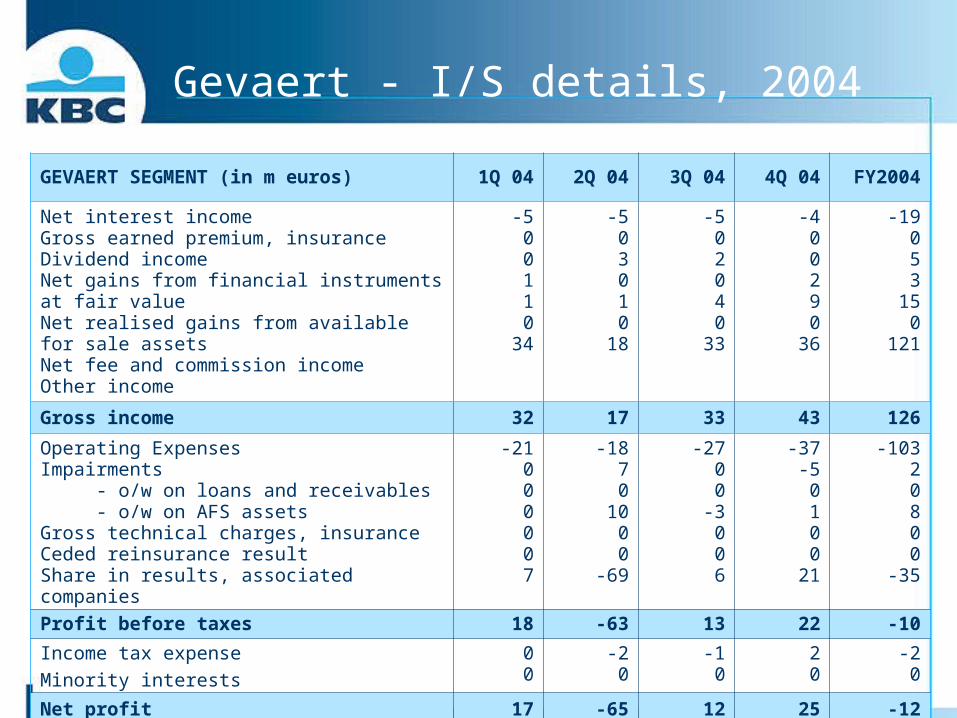

Gevaert - I/S details, 2004

GEVAERT SEGMENT (in m euros) 1Q 04 2Q 04 3Q 04 4Q 04 FY2004

Net interest incomeGross earned premium, insuranceDividend incomeNet gains from financial instruments at fair valueNet realised gains from available for sale assetsNet fee and commission incomeOther income

-500110

34

-503010

18

-502040

33

-400290

36

-19053

150

121

Gross income 32 17 33 43 126

Operating ExpensesImpairments - o/w on loans and receivables - o/w on AFS assetsGross technical charges, insuranceCeded reinsurance resultShare in results, associated companies

-21000007

-1870

1000

-69

-2700

-3006

-37-50100

21

-10320800

-35

Profit before taxes 18 -63 13 22 -10

Income tax expense

Minority interests

00

-20

-10

20

-20

Net profit 17 -65 12 25 -12

47

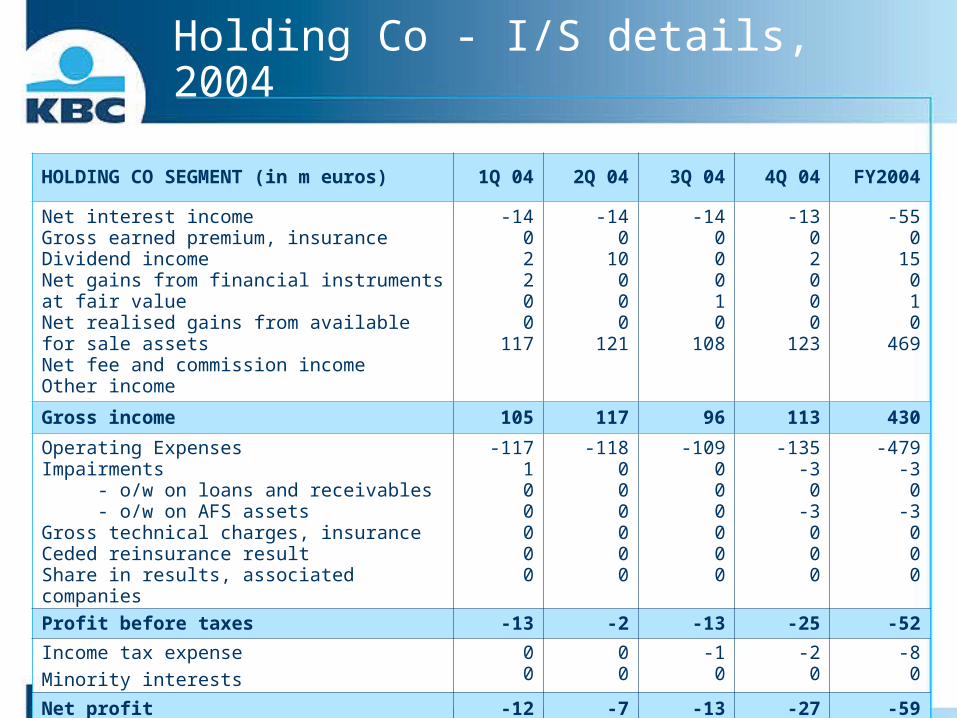

Holding Co - I/S details, 2004

HOLDING CO SEGMENT (in m euros) 1Q 04 2Q 04 3Q 04 4Q 04 FY2004

Net interest incomeGross earned premium, insuranceDividend incomeNet gains from financial instruments at fair valueNet realised gains from available for sale assetsNet fee and commission incomeOther income

-1402200

117

-140

10000

121

-1400010

108

-1302000

123

-550

15010

469

Gross income 105 117 96 113 430

Operating ExpensesImpairments - o/w on loans and receivables - o/w on AFS assetsGross technical charges, insuranceCeded reinsurance resultShare in results, associated companies

-117100000

-118000000

-109000000

-135-30

-3000

-479-30

-3000

Profit before taxes -13 -2 -13 -25 -52

Income tax expense

Minority interests

00

00

-10

-20

-80

Net profit -12 -7 -13 -27 -59

48

CEE banking - I/S details, 1Q20041Q 2004 pro forma CSOB KB K&H NLB

Net Statutory profit

Net interest incomeDividend incomeNet gains from financial instruments at fair valueNet realised gains from available for sale assetsNet fee and commission incomeOther income

122 5791 2675 6615 283

50 25016 805

54 49132

2 5842 784

10 0554 412

51 0360

19 5431 114

15 5864 044

Gross income 201 844 74 358 91 323

Operating ExpensesImpairmentsShare in result of associated companiesTaxes

- 114 043- 3 708

0- 28 216

- 59 559- 2 111

2 168- 740

- 63 2119 128

559- 6 621

Net statutory profit 55 877 14 115 31 179

Profit contibution to Group

Net statutory profitConsolidation adjustmentsMinority InterestsResults of capital allocation

42 027

55 877- 639

- 7 697- 5 514

10 146

14 115- 360

- 3 124- 485

11 631

31 179- 347

- 7 973- 11 228

Profit contribution, Group shareROACROI

42 02744%12%

10 14625%6%

11 63129%23%

6 383