Embed Size (px)

Citation preview

Copyright @ 2014 Jindal Steel & Power Limited 1 Copyright @ 2014 Jindal Steel & Power Limited 1

3QFY15 (December’ 14)

Jindal Steel and Power Ltd

Investor Presentation

Copyright @ 2014 Jindal Steel & Power Limited 2 Copyright @ 2014 Jindal Steel & Power Limited 2

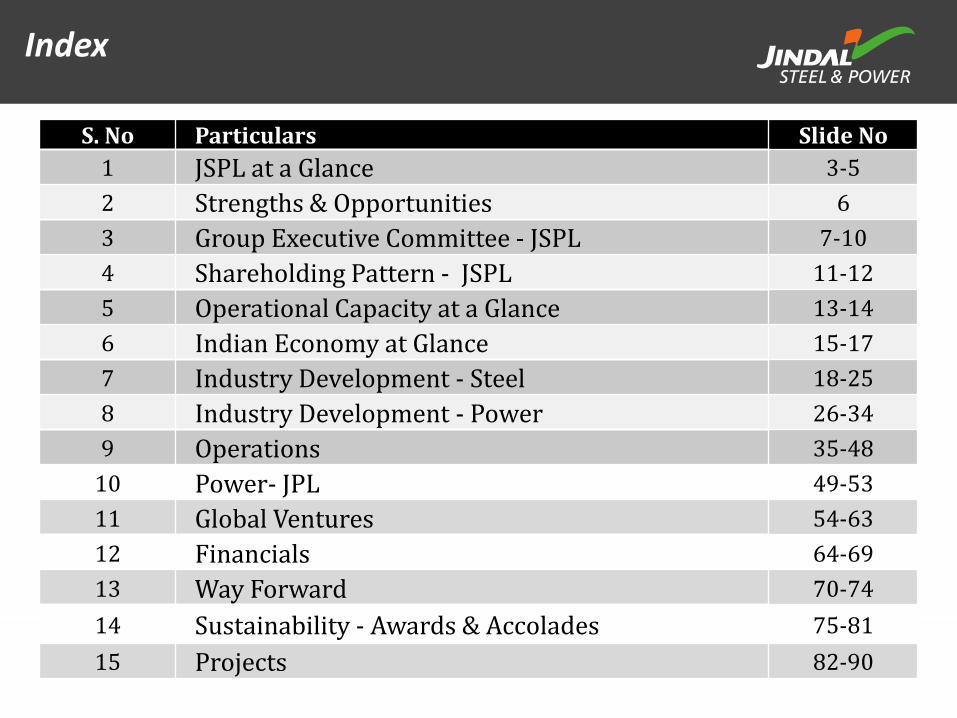

Index

S. No Particulars Slide No

1 JSPL at a Glance 3-5

2 Strengths & Opportunities 6

3 Group Executive Committee - JSPL 7-10

4 Shareholding Pattern - JSPL 11-12

5 Operational Capacity at a Glance 13-14

6 Indian Economy at Glance 15-17

7 Industry Development - Steel 18-25

8 Industry Development - Power 26-34

9 Operations 35-48

10 Power- JPL 49-53

11 Global Ventures 54-63

12 Financials 64-69

13 Way Forward 70-74

14 Sustainability - Awards & Accolades 75-81

15 Projects 82-90

Copyright @ 2014 Jindal Steel & Power Limited 3 Copyright @ 2014 Jindal Steel & Power Limited 3

Jindal Steel & Power Limited Building the Nation of Our Dreams

Aerial View of Raigarh Plant

Copyright @ 2014 Jindal Steel & Power Limited 4 Copyright @ 2014 Jindal Steel & Power Limited 4

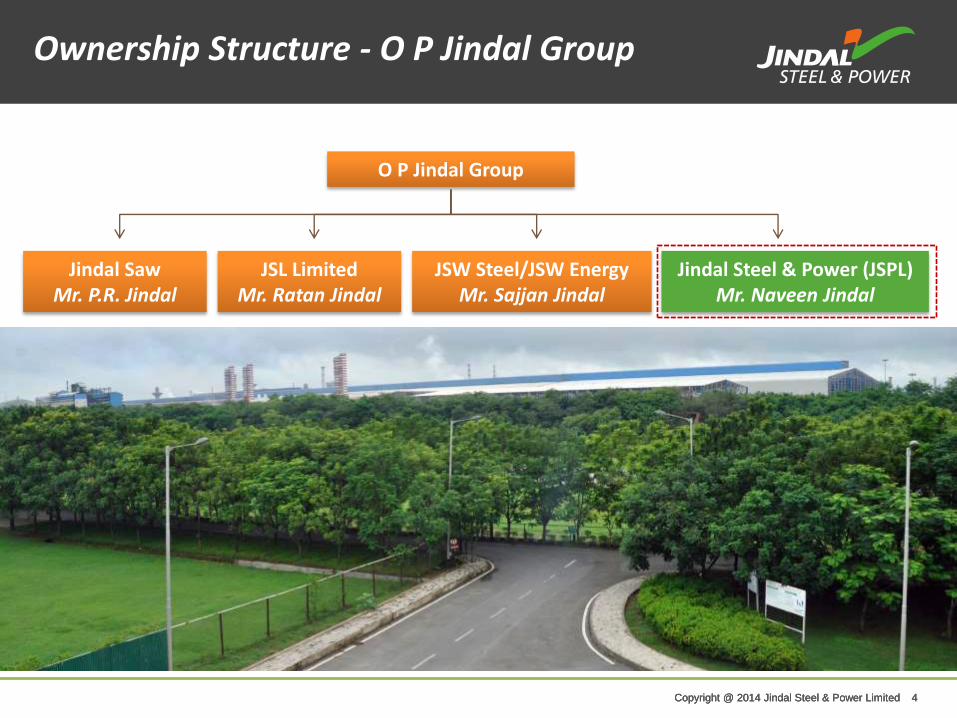

O P Jindal Group

Jindal Saw Mr. P.R. Jindal

JSL Limited Mr. Ratan Jindal

JSW Steel/JSW Energy Mr. Sajjan Jindal

Jindal Steel & Power (JSPL) Mr. Naveen Jindal

Copyright @ 2014 Jindal Steel & Power Limited 4

Ownership Structure - O P Jindal Group

Copyright @ 2014 Jindal Steel & Power Limited 5 Copyright @ 2014 Jindal Steel & Power Limited 5

Annual turnover of JSPL

US$ 3.3 bn+

Steel making capacity Mining capacity

16.56 MTPA

Power capacity

4,485 MW

Pellet making capacity

9 MTPA 29 Countries

Ensuring pan-India presence, covering 534 districts for retail

business

People strengths

16000+

Lives impacted by JSPL’s social endeavors

900,000+

Saplings planted

7.4 mn+

7.75 MTPA

Export presence

1,670 Dealers

JSPL at a Glance - Part of US$ 18 billion* OP Jindal Group

* As of 31st March’ 2014

Copyright @ 2014 Jindal Steel & Power Limited 6 Copyright @ 2014 Jindal Steel & Power Limited 6

Strengths & Opportunities

• Successful commissioning of enhanced Steel & Power Capacities :

– Steel 3 MTPA to 7.75 MTPA

– JPL Power 1000MW to 3400 MW*

– Pellets 4.5 MTPA to 9 MTPA

• Proven track record of Highest Capacity Utilization

• Expertise in Mining operations – would help in faster ramp up of production from new coal mines

• Harness higher revenues from enhanced capacities

• Intrinsic value of the company – in Steel (45K Cr) and Power (20K Cr) is not reflected in its market cap (14K Cr**).

• Increase in demand in Steel & Power sectors will lead to higher revenue generation

• Opportunity to secure raw materials in the ensuing coal block auctions

Strengths Opportunities

• Includes 600 MW which will be commissioned in FY15 • ** As on 4th Feb’2015

Copyright @ 2014 Jindal Steel & Power Limited 7 Copyright @ 2014 Jindal Steel & Power Limited 7 Copyright @ 2014 Jindal Steel & Power Limited 7

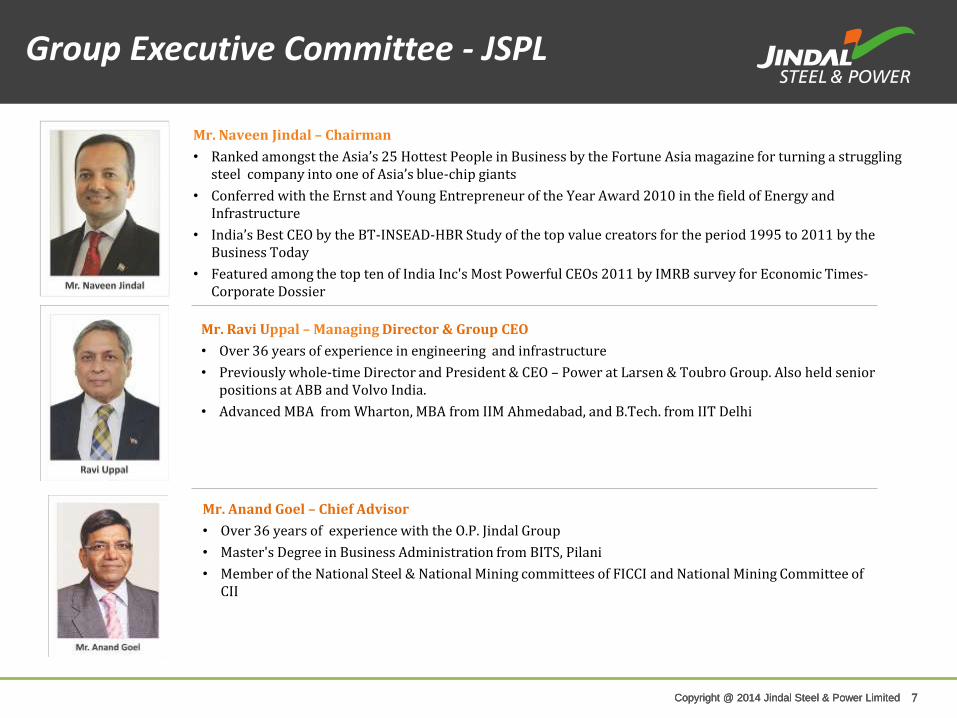

Mr. Naveen Jindal – Chairman

• Ranked amongst the Asia’s 25 Hottest People in Business by the Fortune Asia magazine for turning a struggling steel company into one of Asia’s blue-chip giants

• Conferred with the Ernst and Young Entrepreneur of the Year Award 2010 in the field of Energy and Infrastructure

• India’s Best CEO by the BT-INSEAD-HBR Study of the top value creators for the period 1995 to 2011 by the Business Today

• Featured among the top ten of India Inc's Most Powerful CEOs 2011 by IMRB survey for Economic Times-Corporate Dossier

Mr. Ravi Uppal – Managing Director & Group CEO

• Over 36 years of experience in engineering and infrastructure

• Previously whole-time Director and President & CEO – Power at Larsen & Toubro Group. Also held senior positions at ABB and Volvo India.

• Advanced MBA from Wharton, MBA from IIM Ahmedabad, and B.Tech. from IIT Delhi

Mr. Anand Goel – Chief Advisor

• Over 36 years of experience with the O.P. Jindal Group

• Master's Degree in Business Administration from BITS, Pilani

• Member of the National Steel & National Mining committees of FICCI and National Mining Committee of CII

Group Executive Committee - JSPL

Copyright @ 2014 Jindal Steel & Power Limited 8 Copyright @ 2014 Jindal Steel & Power Limited 8 Copyright @ 2014 Jindal Steel & Power Limited 8

Mr. Rajesh Bhatia – CEO Global Ventures

• Over 25 years of experience in the field of Finance, Accounts, Taxation, Administration, Commercial and Business Development.

• Played an important role in JSPL's overseas acquisitions in Australia, Indonesia, South Africa, Mozambique, Madagascar, Mongolia & Oman, apart from arranging financing from domestic and international lenders for various projects.

Group Executive Committee - JSPL

Mr. K Rajagopal – Director & Group CFO

• A Chartered Accountant by qualification, Mr. Rajagopal has extensive background into the whole gamut of Finance across organizations.

• He brings with him more than 31 years of experience out of which about 21 years has been with ABB.

• He is a strategist, a policy maker, and has strived to continuously improve the profitability through strategic and highly efficient business portfolio evaluation.

Copyright @ 2014 Jindal Steel & Power Limited 9 Copyright @ 2014 Jindal Steel & Power Limited 9

Mr. V K Mehta – ED Marketing

• Over 36 years of experience in marketing

• Previously, he was working with SAIL, Kolkata as its Executive Director,, Marketing and was also on the Board of Directors of Mjunction and SAIL-SCI Shipping Co.

Mr. Rajeev Bhadauria – Director Group HR

• More than 28 years as an HR professional across Public and Private sectors

• Previously President HR – Reliance ADA Group and Regional HR head – NTPC

• Post Graduate in Industrial Relations from the Power Management Institute, NTPC and LLB from Allahabad University

Group Executive Committee - JSPL

Copyright @ 2014 Jindal Steel & Power Limited 10 Copyright @ 2014 Jindal Steel & Power Limited 10

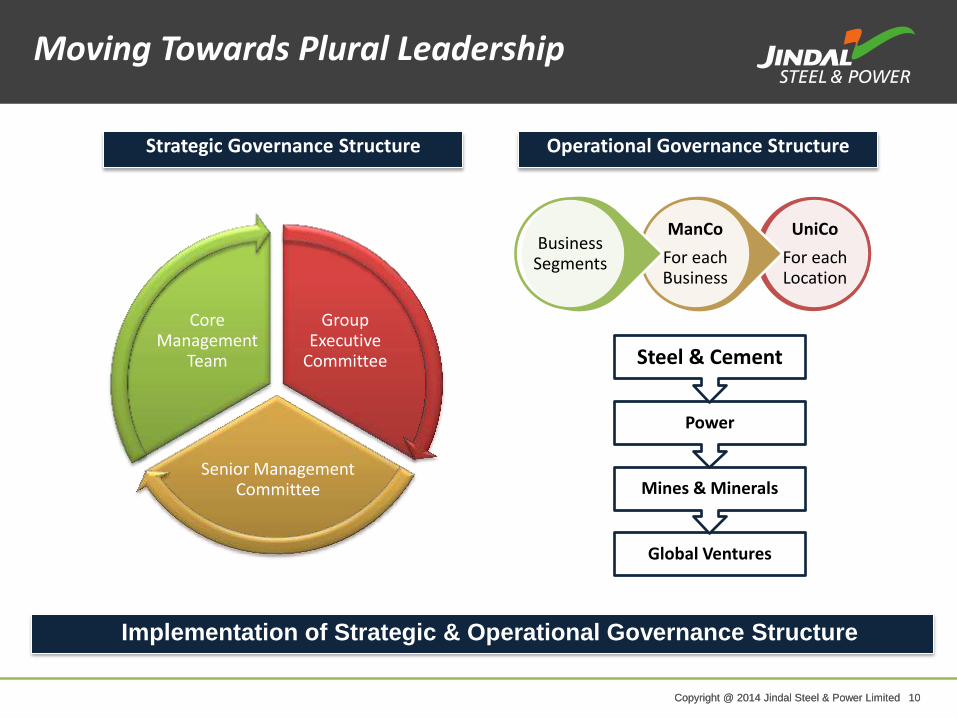

Group Executive

Committee

Senior Management Committee

Core Management

Team

UniCo

For each Location

ManCo

For each Business

Business Segments

Global Ventures

Mines & Minerals

Power

Steel & Cement

Moving Towards Plural Leadership

Strategic Governance Structure Operational Governance Structure

Implementation of Strategic & Operational Governance Structure

Copyright @ 2014 Jindal Steel & Power Limited 11 Copyright @ 2014 Jindal Steel & Power Limited 11

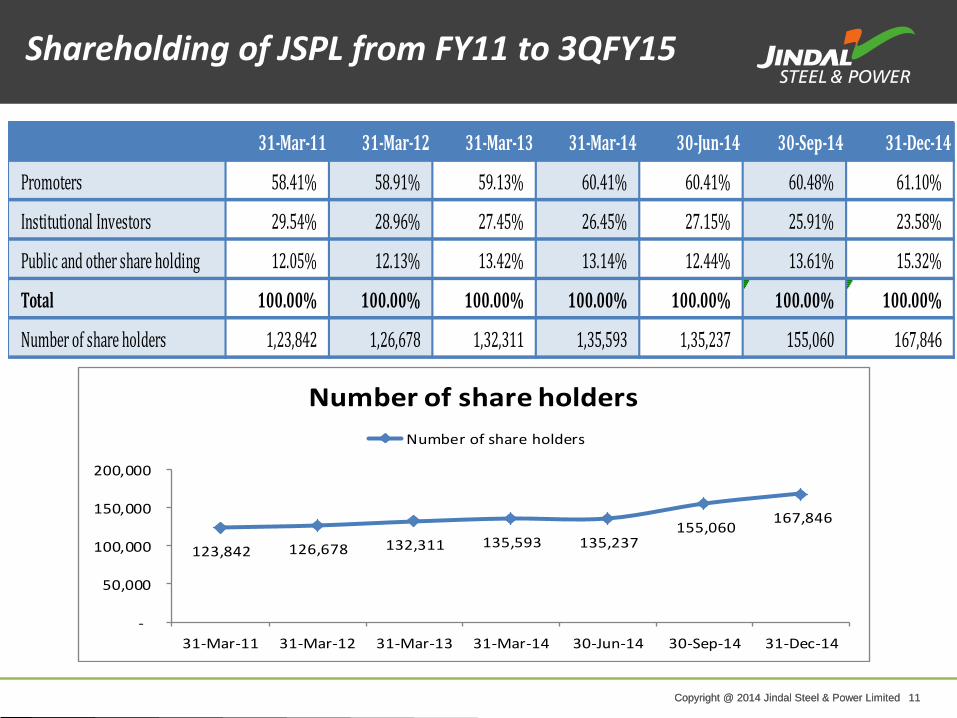

Shareholding of JSPL from FY11 to 3QFY15

Number of share holder s (Retail /HNI) increases by 15% in 2Q FY15

31-Mar-11 31-Mar-12 31-Mar-13 31-Mar-14 30-Jun-14 30-Sep-14 31-Dec-14

Promoters 58.41% 58.91% 59.13% 60.41% 60.41% 60.48% 61.10%

Institutional Investors 29.54% 28.96% 27.45% 26.45% 27.15% 25.91% 23.58%

Public and other share holding 12.05% 12.13% 13.42% 13.14% 12.44% 13.61% 15.32%

Total 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

Number of share holders 1,23,842 1,26,678 1,32,311 1,35,593 1,35,237 155,060 167,846

123,842 126,678 132,311 135,593 135,237 155,060

167,846

-

50,000

100,000

150,000

200,000

31-Mar-11 31-Mar-12 31-Mar-13 31-Mar-14 30-Jun-14 30-Sep-14 31-Dec-14

Number of share holders

Number of share holders

Copyright @ 2014 Jindal Steel & Power Limited 12 Copyright @ 2014 Jindal Steel & Power Limited 12

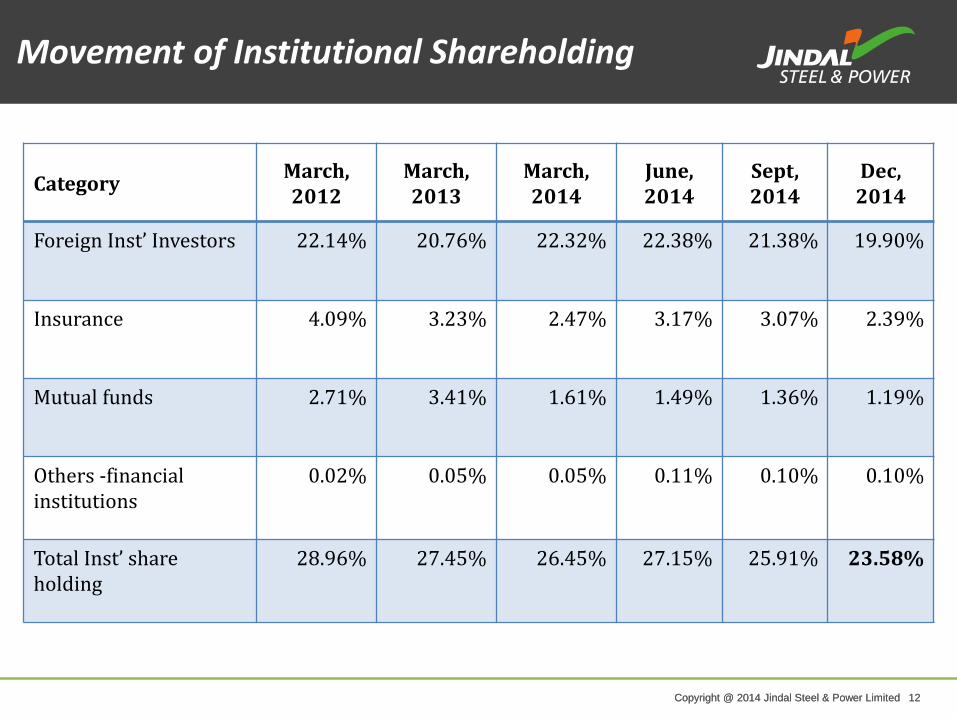

Category March, 2012

March, 2013

March, 2014

June, 2014

Sept, 2014

Dec, 2014

Foreign Inst’ Investors 22.14% 20.76% 22.32% 22.38% 21.38% 19.90%

Insurance 4.09% 3.23% 2.47% 3.17% 3.07% 2.39%

Mutual funds 2.71% 3.41% 1.61% 1.49% 1.36% 1.19%

Others -financial institutions

0.02% 0.05% 0.05% 0.11% 0.10% 0.10%

Total Inst’ share holding

28.96% 27.45% 26.45% 27.15% 25.91% 23.58%

Movement of Institutional Shareholding

Copyright @ 2014 Jindal Steel & Power Limited 13 Copyright @ 2014 Jindal Steel & Power Limited 13

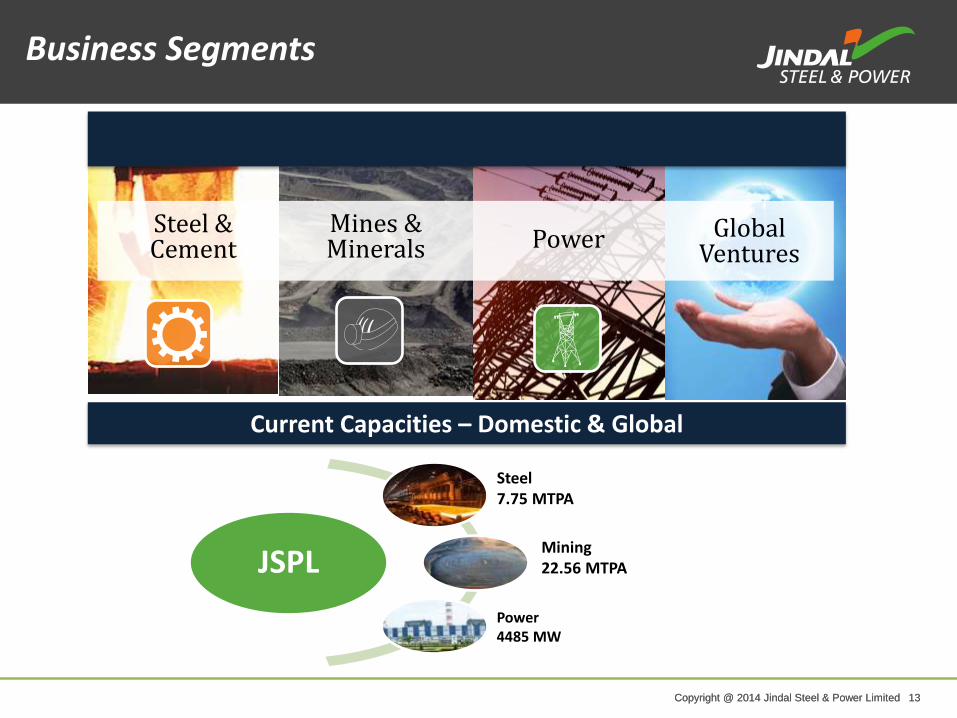

Steel & Cement Power

Mines & Minerals

Business segments

Global Ventures

JSPL

Steel 7.75 MTPA

Mining 22.56 MTPA

Power 4485 MW

Current Capacities – Domestic & Global

Business Segments

Copyright @ 2014 Jindal Steel & Power Limited 14 Copyright @ 2014 Jindal Steel & Power Limited 14

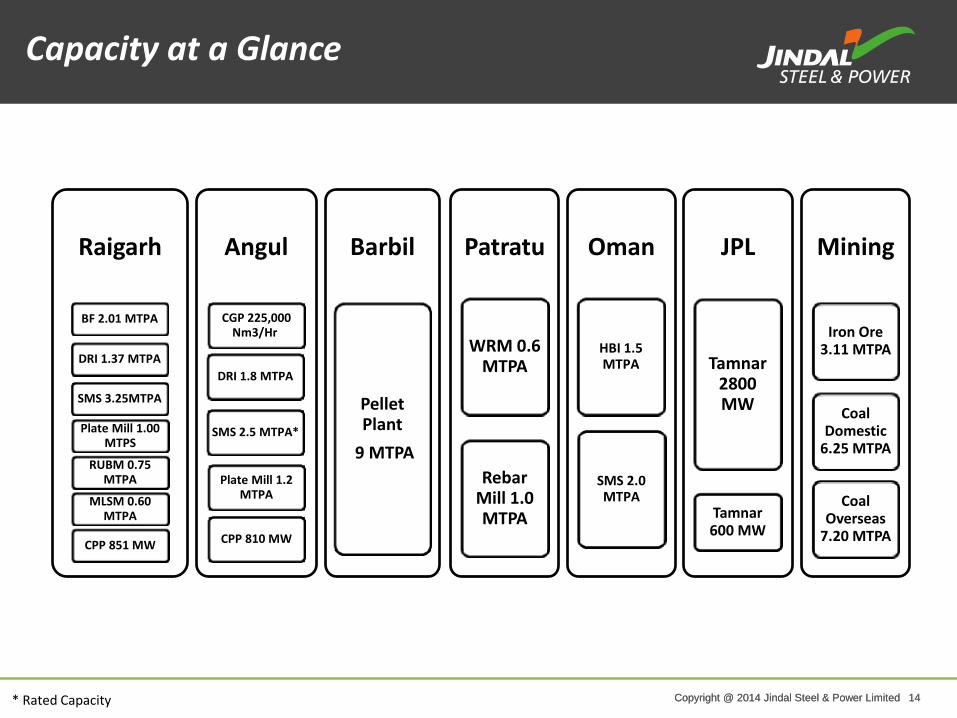

Capacity in deail

Raigarh

SMS 3.25MTPA

BF 2.01 MTPA

DRI 1.37 MTPA

Plate Mill 1.00 MTPS

RUBM 0.75 MTPA

MLSM 0.60 MTPA

CPP 851 MW

Angul

SMS 2.5 MTPA*

DRI 1.8 MTPA

CGP 225,000 Nm3/Hr

Plate Mill 1.2 MTPA

CPP 810 MW

Barbil

Pellet Plant

9 MTPA

Patratu

WRM 0.6 MTPA

Rebar Mill 1.0 MTPA

Oman

SMS 2.0 MTPA

HBI 1.5 MTPA

JPL

Tamnar 2800 MW

Tamnar 600 MW

Mining

Iron Ore 3.11 MTPA

Coal Domestic

6.25 MTPA

Coal Overseas

7.20 MTPA

Capacity at a Glance

* Rated Capacity

Copyright @ 2014 Jindal Steel & Power Limited 15 Copyright @ 2014 Jindal Steel & Power Limited 15

Copyright @ 2014 Jindal Steel & Power Limited 16 Copyright @ 2014 Jindal Steel & Power Limited 16

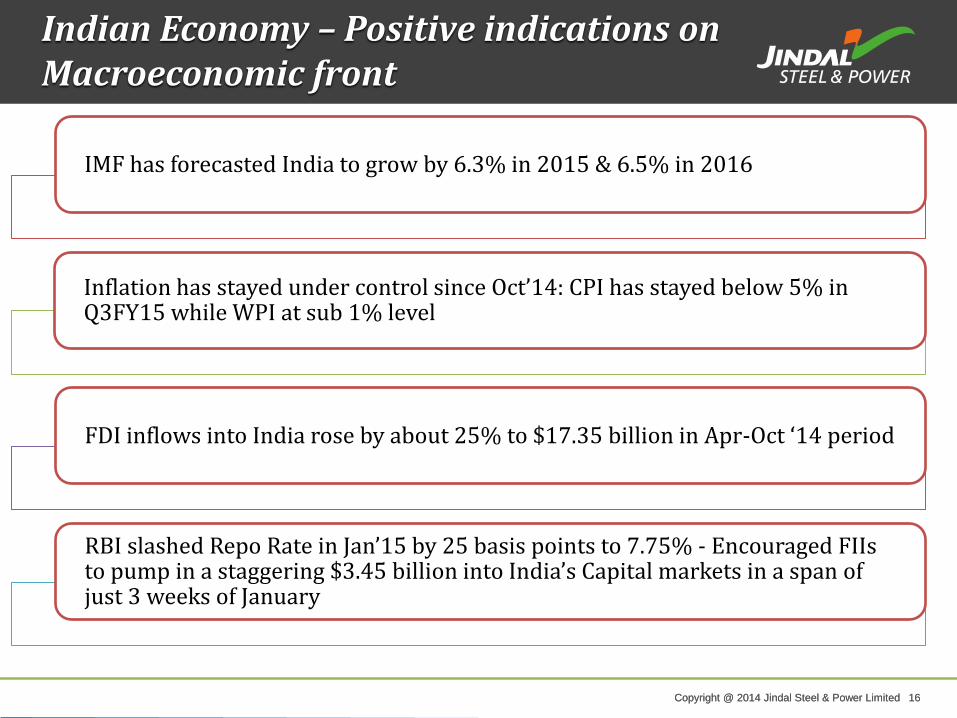

Indian Economy – Positive indications on Macroeconomic front

IMF has forecasted India to grow by 6.3% in 2015 & 6.5% in 2016

Inflation has stayed under control since Oct’14: CPI has stayed below 5% in Q3FY15 while WPI at sub 1% level

FDI inflows into India rose by about 25% to $17.35 billion in Apr-Oct ‘14 period

RBI slashed Repo Rate in Jan’15 by 25 basis points to 7.75% - Encouraged FIIs to pump in a staggering $3.45 billion into India’s Capital markets in a span of just 3 weeks of January

Copyright @ 2014 Jindal Steel & Power Limited 17 Copyright @ 2014 Jindal Steel & Power Limited 17

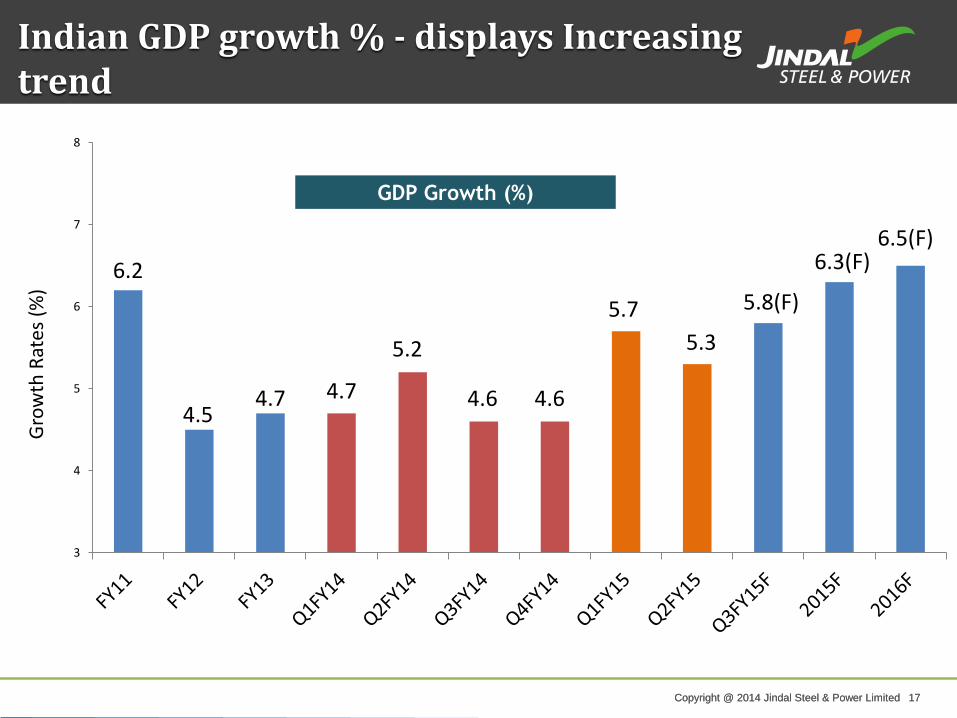

Indian GDP growth % - displays Increasing trend

6.2

4.5 4.7 4.7

5.2

4.6 4.6

5.7

5.3

5.8(F)

6.3(F) 6.5(F)

3

4

5

6

7

8

Gro

wth

Rat

es (

%)

GDP Growth (%)

Copyright @ 2014 Jindal Steel & Power Limited 18 Copyright @ 2014 Jindal Steel & Power Limited 18

Copyright @ 2014 Jindal Steel & Power Limited 19 Copyright @ 2014 Jindal Steel & Power Limited 19

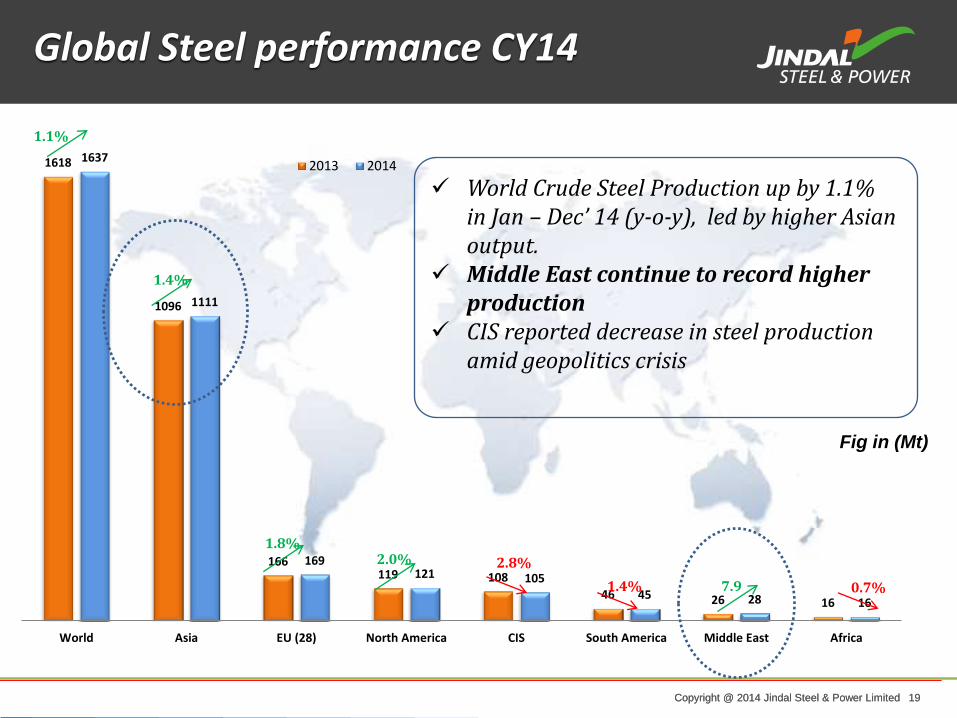

Global Steel performance CY14

1618

1096

166 119 108

46 26 16

1637

1111

169 121 105

45 28 16

World Asia EU (28) North America CIS South America Middle East Africa

2013 2014

1.1%

1.4%

1.8%

2.8%

7.9 0.7%

2.0%

1.4%

Fig in (Mt)

World Crude Steel Production up by 1.1% in Jan – Dec’ 14 (y-o-y), led by higher Asian output.

Middle East continue to record higher production

CIS reported decrease in steel production amid geopolitics crisis

Copyright @ 2014 Jindal Steel & Power Limited 20 Copyright @ 2014 Jindal Steel & Power Limited 20

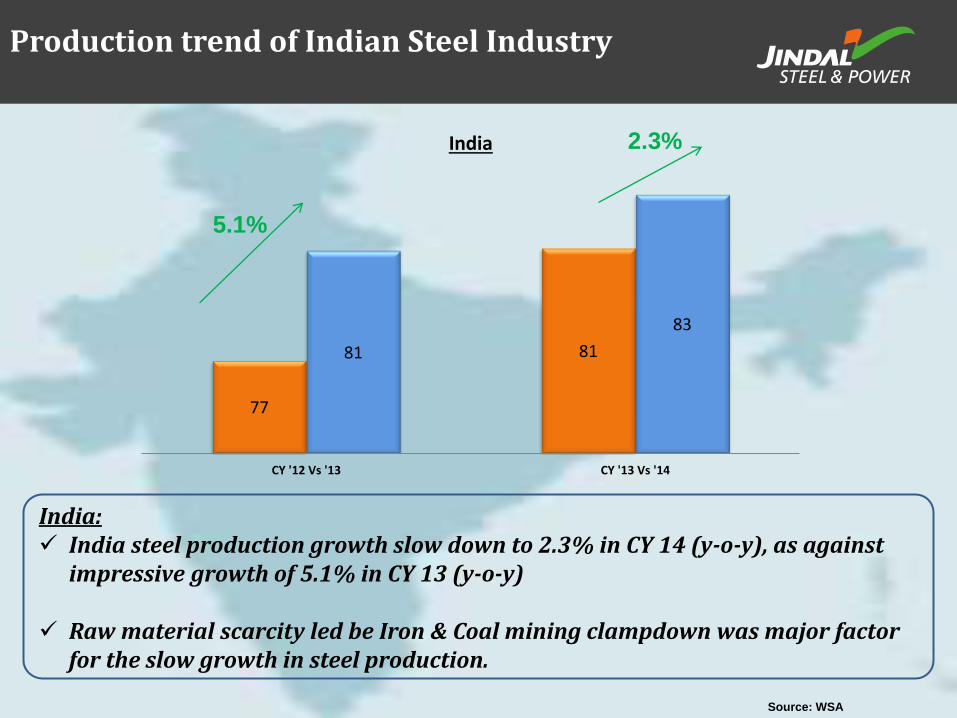

77

81 81

83

CY '12 Vs '13 CY '13 Vs '14

India 2.3%

5.1%

Production trend of Indian Steel Industry

India: India steel production growth slow down to 2.3% in CY 14 (y-o-y), as against

impressive growth of 5.1% in CY 13 (y-o-y)

Raw material scarcity led be Iron & Coal mining clampdown was major factor for the slow growth in steel production.

Source: WSA

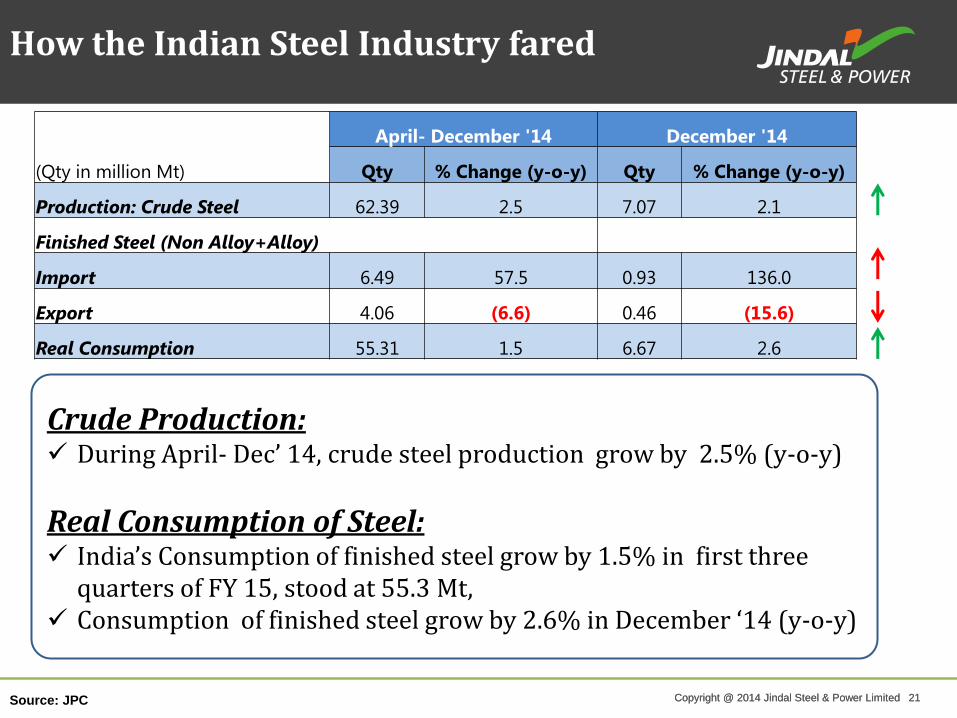

Copyright @ 2014 Jindal Steel & Power Limited 21 Copyright @ 2014 Jindal Steel & Power Limited 21

April- December '14 December '14

(Qty in million Mt) Qty % Change (y-o-y) Qty % Change (y-o-y)

Production: Crude Steel 62.39 2.5 7.07 2.1

Finished Steel (Non Alloy+Alloy)

Import 6.49 57.5 0.93 136.0

Export 4.06 (6.6) 0.46 (15.6)

Real Consumption 55.31 1.5 6.67 2.6

How the Indian Steel Industry fared

Crude Production: During April- Dec’ 14, crude steel production grow by 2.5% (y-o-y)

Real Consumption of Steel: India’s Consumption of finished steel grow by 1.5% in first three

quarters of FY 15, stood at 55.3 Mt, Consumption of finished steel grow by 2.6% in December ‘14 (y-o-y)

Source: JPC

Copyright @ 2014 Jindal Steel & Power Limited 22 Copyright @ 2014 Jindal Steel & Power Limited 22

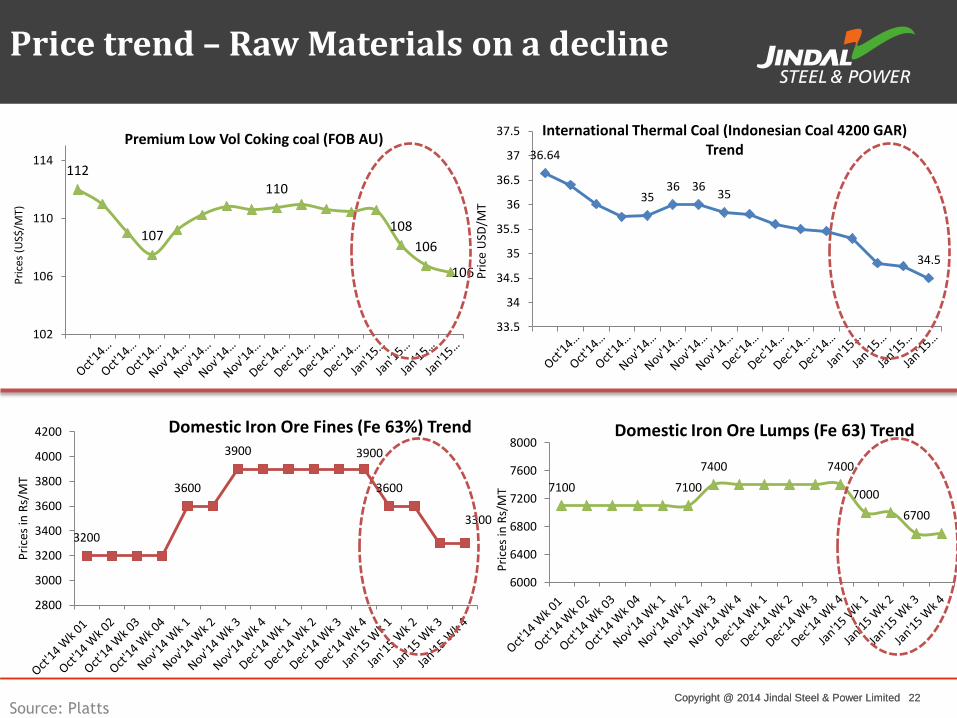

Price trend – Raw Materials on a decline

Source: Platts

112

107

110

108

106

106

102

106

110

114

Pri

ces

(US$

/MT)

Premium Low Vol Coking coal (FOB AU) 36.64

35 36 36

35

34.5

33.5

34

34.5

35

35.5

36

36.5

37

37.5

Pri

ce U

SD/M

T

International Thermal Coal (Indonesian Coal 4200 GAR) Trend

7100 7100

7400 7400

7000

6700

6000

6400

6800

7200

7600

8000

Pri

ces

in R

s/M

T

Domestic Iron Ore Lumps (Fe 63) Trend

3200

3600

3900 3900

3600

3300

2800

3000

3200

3400

3600

3800

4000

4200

Pri

ces

in R

s/M

T

Domestic Iron Ore Fines (Fe 63%) Trend

Copyright @ 2014 Jindal Steel & Power Limited 23 Copyright @ 2014 Jindal Steel & Power Limited 23

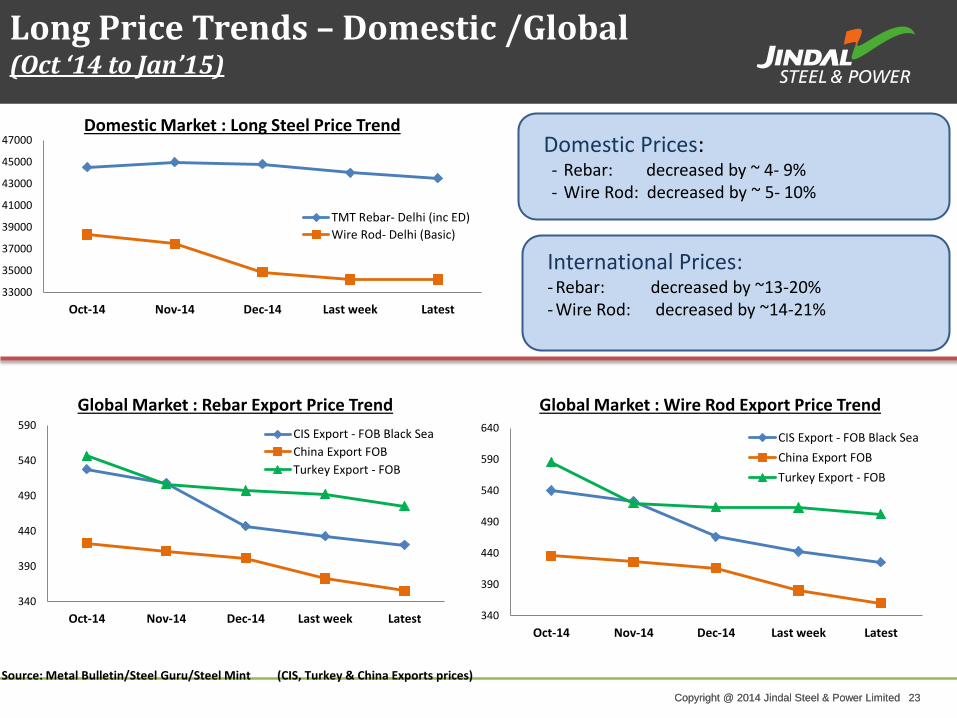

Long Price Trends – Domestic /Global (Oct ‘14 to Jan’15)

340

390

440

490

540

590

Oct-14 Nov-14 Dec-14 Last week Latest

Global Market : Rebar Export Price Trend

CIS Export - FOB Black Sea

China Export FOB

Turkey Export - FOB

340

390

440

490

540

590

640

Oct-14 Nov-14 Dec-14 Last week Latest

Global Market : Wire Rod Export Price Trend

CIS Export - FOB Black Sea

China Export FOB

Turkey Export - FOB

33000

35000

37000

39000

41000

43000

45000

47000

Oct-14 Nov-14 Dec-14 Last week Latest

Domestic Market : Long Steel Price Trend

TMT Rebar- Delhi (inc ED)

Wire Rod- Delhi (Basic)

Source: Metal Bulletin/Steel Guru/Steel Mint

International Prices: - Rebar: decreased by ~13-20% - Wire Rod: decreased by ~14-21%

Domestic Prices: - Rebar: decreased by ~ 4- 9% - Wire Rod: decreased by ~ 5- 10%

(CIS, Turkey & China Exports prices)

Copyright @ 2014 Jindal Steel & Power Limited 24 Copyright @ 2014 Jindal Steel & Power Limited 24

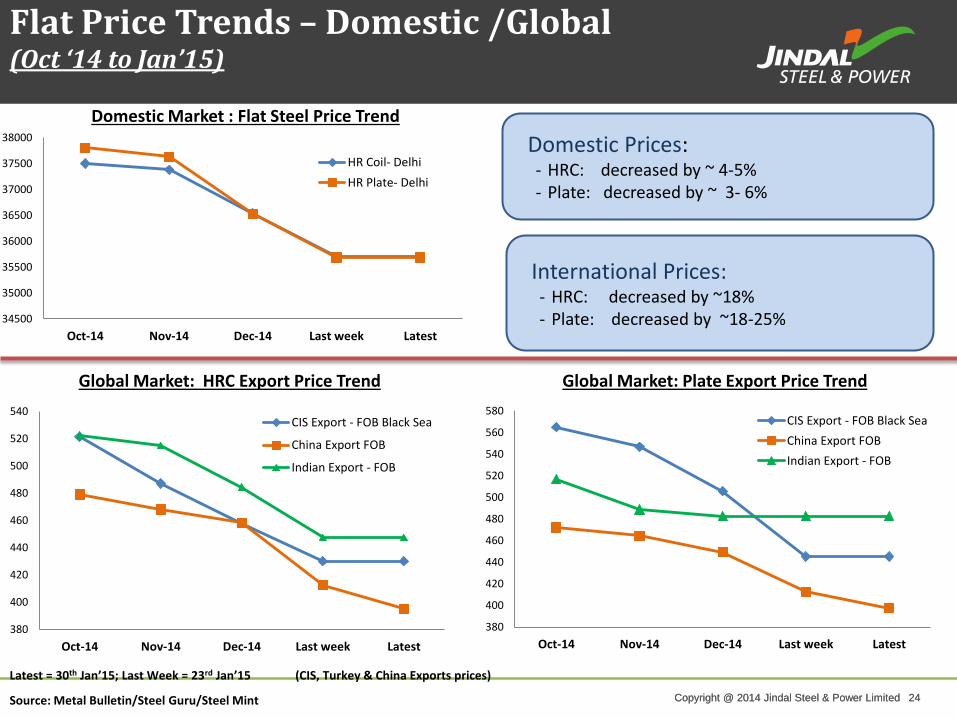

Flat Price Trends – Domestic /Global (Oct ‘14 to Jan’15)

Source: Metal Bulletin/Steel Guru/Steel Mint

International Prices: - HRC: decreased by ~18% - Plate: decreased by ~18-25%

Domestic Prices: - HRC: decreased by ~ 4-5% - Plate: decreased by ~ 3- 6%

(CIS, Turkey & China Exports prices)

380

400

420

440

460

480

500

520

540

Oct-14 Nov-14 Dec-14 Last week Latest

Global Market: HRC Export Price Trend

CIS Export - FOB Black Sea

China Export FOB

Indian Export - FOB

380

400

420

440

460

480

500

520

540

560

580

Oct-14 Nov-14 Dec-14 Last week Latest

Global Market: Plate Export Price Trend

CIS Export - FOB Black Sea

China Export FOB

Indian Export - FOB

34500

35000

35500

36000

36500

37000

37500

38000

Oct-14 Nov-14 Dec-14 Last week Latest

Domestic Market : Flat Steel Price Trend

HR Coil- Delhi

HR Plate- Delhi

Latest = 30th Jan’15; Last Week = 23rd Jan’15

Copyright @ 2014 Jindal Steel & Power Limited 25 Copyright @ 2014 Jindal Steel & Power Limited 25

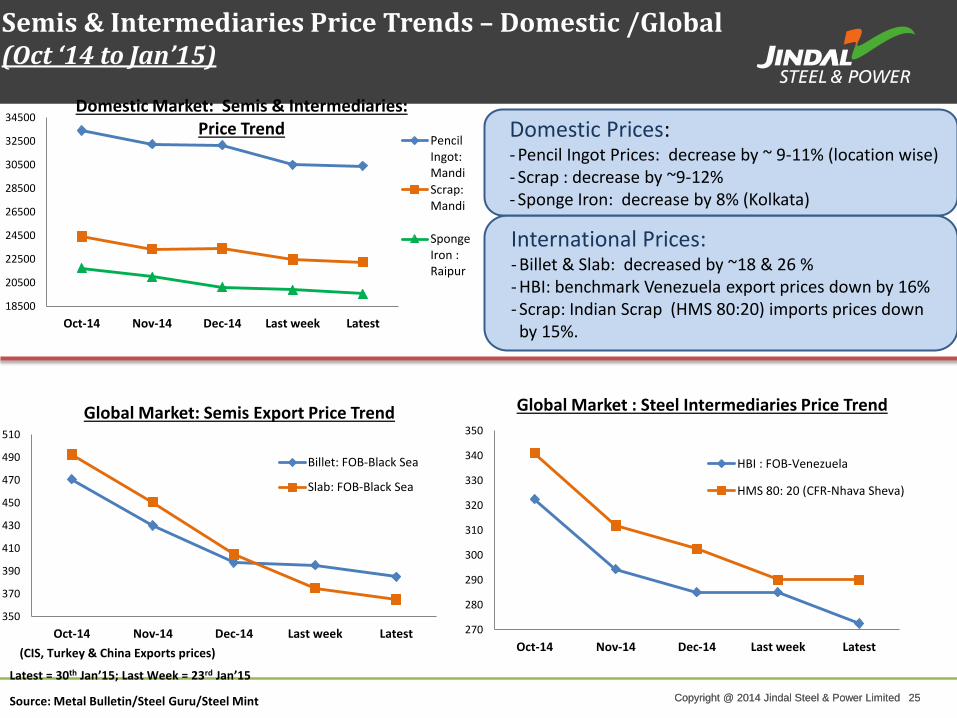

Semis & Intermediaries Price Trends – Domestic /Global (Oct ‘14 to Jan’15)

Source: Metal Bulletin/Steel Guru/Steel Mint

International Prices: - Billet & Slab: decreased by ~18 & 26 % - HBI: benchmark Venezuela export prices down by 16% - Scrap: Indian Scrap (HMS 80:20) imports prices down by 15%.

Domestic Prices: - Pencil Ingot Prices: decrease by ~ 9-11% (location wise) - Scrap : decrease by ~9-12% - Sponge Iron: decrease by 8% (Kolkata)

(CIS, Turkey & China Exports prices)

18500

20500

22500

24500

26500

28500

30500

32500

34500

Oct-14 Nov-14 Dec-14 Last week Latest

Domestic Market: Semis & Intermediaries: Price Trend

PencilIngot:Mandi

Scrap:Mandi

SpongeIron :Raipur

350

370

390

410

430

450

470

490

510

Oct-14 Nov-14 Dec-14 Last week Latest

Global Market: Semis Export Price Trend

Billet: FOB-Black Sea

Slab: FOB-Black Sea

270

280

290

300

310

320

330

340

350

Oct-14 Nov-14 Dec-14 Last week Latest

Global Market : Steel Intermediaries Price Trend

HBI : FOB-Venezuela

HMS 80: 20 (CFR-Nhava Sheva)

Latest = 30th Jan’15; Last Week = 23rd Jan’15

Copyright @ 2014 Jindal Steel & Power Limited 26 Copyright @ 2014 Jindal Steel & Power Limited 26

Copyright @ 2014 Jindal Steel & Power Limited 27 Copyright @ 2014 Jindal Steel & Power Limited 27

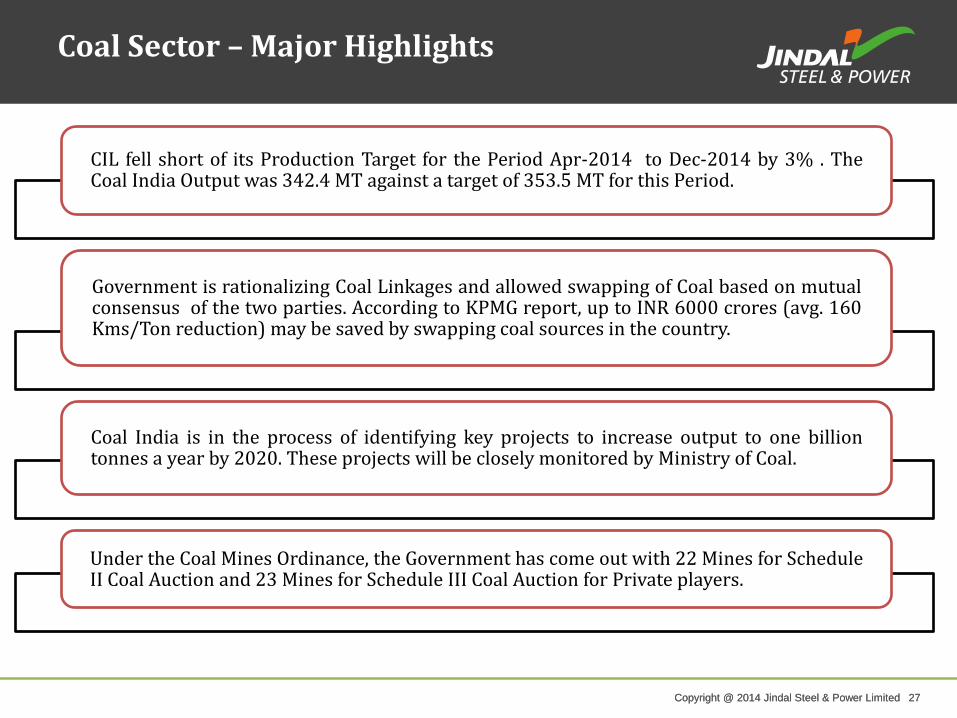

Coal Sector – Major Highlights

CIL fell short of its Production Target for the Period Apr-2014 to Dec-2014 by 3% . The Coal India Output was 342.4 MT against a target of 353.5 MT for this Period.

Government is rationalizing Coal Linkages and allowed swapping of Coal based on mutual consensus of the two parties. According to KPMG report, up to INR 6000 crores (avg. 160 Kms/Ton reduction) may be saved by swapping coal sources in the country.

Coal India is in the process of identifying key projects to increase output to one billion tonnes a year by 2020. These projects will be closely monitored by Ministry of Coal.

Under the Coal Mines Ordinance, the Government has come out with 22 Mines for Schedule II Coal Auction and 23 Mines for Schedule III Coal Auction for Private players.

Copyright @ 2014 Jindal Steel & Power Limited 28 Copyright @ 2014 Jindal Steel & Power Limited 28

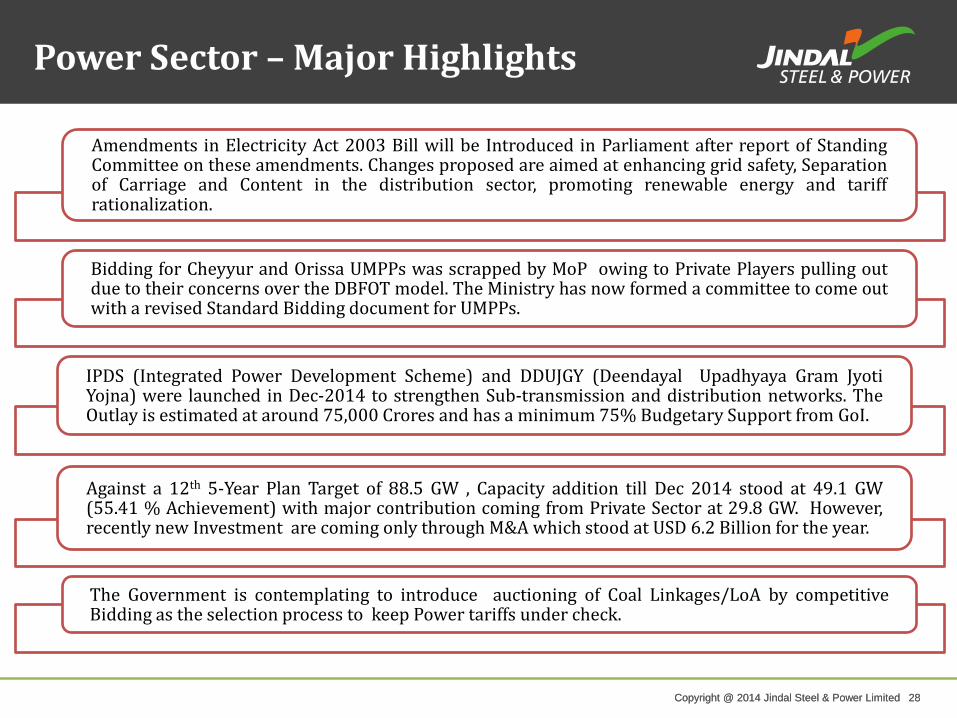

Power Sector – Major Highlights

Amendments in Electricity Act 2003 Bill will be Introduced in Parliament after report of Standing Committee on these amendments. Changes proposed are aimed at enhancing grid safety, Separation of Carriage and Content in the distribution sector, promoting renewable energy and tariff rationalization.

Bidding for Cheyyur and Orissa UMPPs was scrapped by MoP owing to Private Players pulling out due to their concerns over the DBFOT model. The Ministry has now formed a committee to come out with a revised Standard Bidding document for UMPPs.

IPDS (Integrated Power Development Scheme) and DDUJGY (Deendayal Upadhyaya Gram Jyoti Yojna) were launched in Dec-2014 to strengthen Sub-transmission and distribution networks. The Outlay is estimated at around 75,000 Crores and has a minimum 75% Budgetary Support from GoI.

Against a 12th 5-Year Plan Target of 88.5 GW , Capacity addition till Dec 2014 stood at 49.1 GW (55.41 % Achievement) with major contribution coming from Private Sector at 29.8 GW. However, recently new Investment are coming only through M&A which stood at USD 6.2 Billion for the year.

The Government is contemplating to introduce auctioning of Coal Linkages/LoA by competitive Bidding as the selection process to keep Power tariffs under check.

Copyright @ 2014 Jindal Steel & Power Limited 29 Copyright @ 2014 Jindal Steel & Power Limited 29

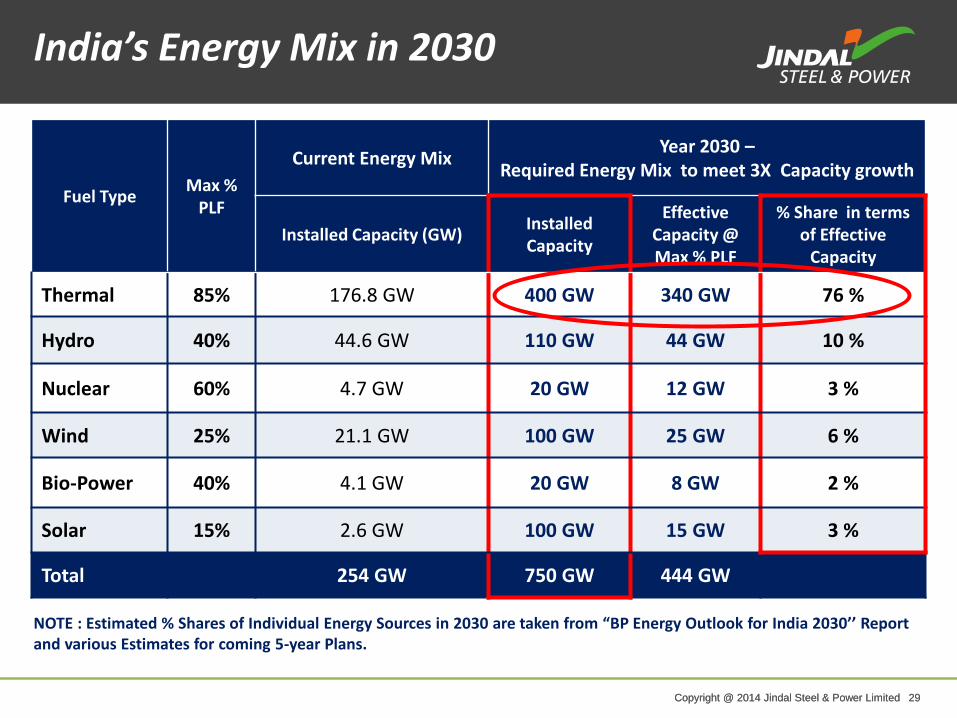

India’s Energy Mix in 2030

Fuel Type Max %

PLF

Current Energy Mix Year 2030 –

Required Energy Mix to meet 3X Capacity growth

Installed Capacity (GW) Installed Capacity

Effective Capacity @ Max % PLF

% Share in terms of Effective

Capacity

Thermal 85% 176.8 GW 400 GW 340 GW 76 %

Hydro 40% 44.6 GW 110 GW 44 GW 10 %

Nuclear 60% 4.7 GW 20 GW 12 GW 3 %

Wind 25% 21.1 GW 100 GW 25 GW 6 %

Bio-Power 40% 4.1 GW 20 GW 8 GW 2 %

Solar 15% 2.6 GW 100 GW 15 GW 3 %

Total 254 GW 750 GW 444 GW

NOTE : Estimated % Shares of Individual Energy Sources in 2030 are taken from “BP Energy Outlook for India 2030’’ Report and various Estimates for coming 5-year Plans.

Copyright @ 2014 Jindal Steel & Power Limited 30 Copyright @ 2014 Jindal Steel & Power Limited 30

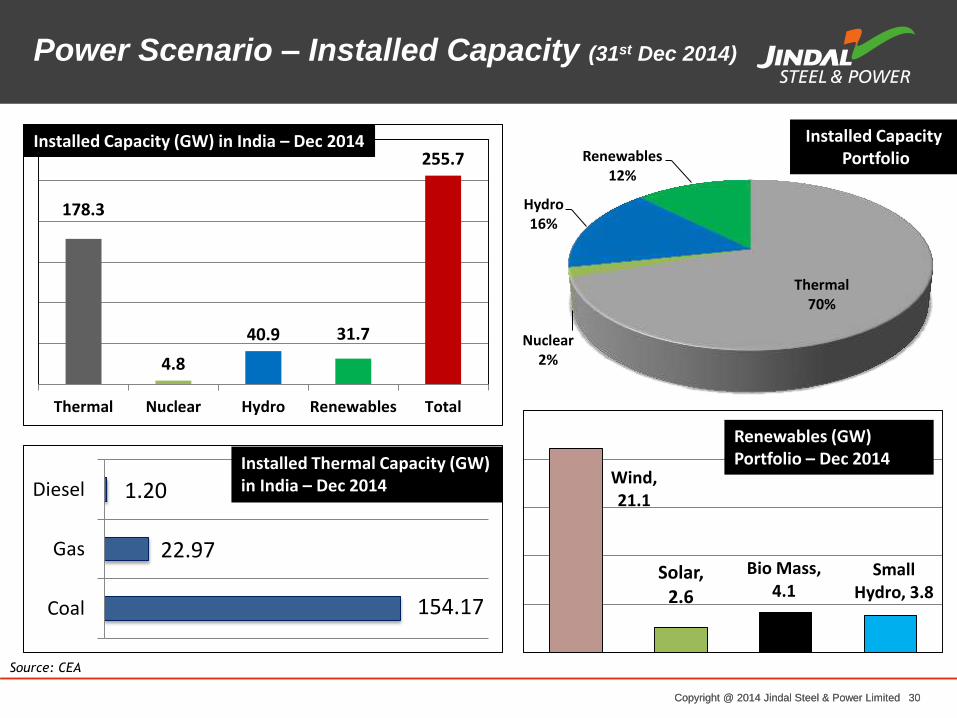

Power Scenario – Installed Capacity (31st Dec 2014)

Source: CEA

178.3

4.8

40.9 31.7

255.7

Thermal Nuclear Hydro Renewables Total

Installed Capacity (GW) in India – Dec 2014

Thermal 70%

Nuclear 2%

Hydro 16%

Renewables 12%

Wind, 21.1

Solar, 2.6

Bio Mass, 4.1

Small Hydro, 3.8

154.17

22.97

1.20

Coal

Gas

Diesel

Installed Thermal Capacity (GW) in India – Dec 2014

Renewables (GW) Portfolio – Dec 2014

Installed Capacity Portfolio

Copyright @ 2014 Jindal Steel & Power Limited 31 Copyright @ 2014 Jindal Steel & Power Limited 31

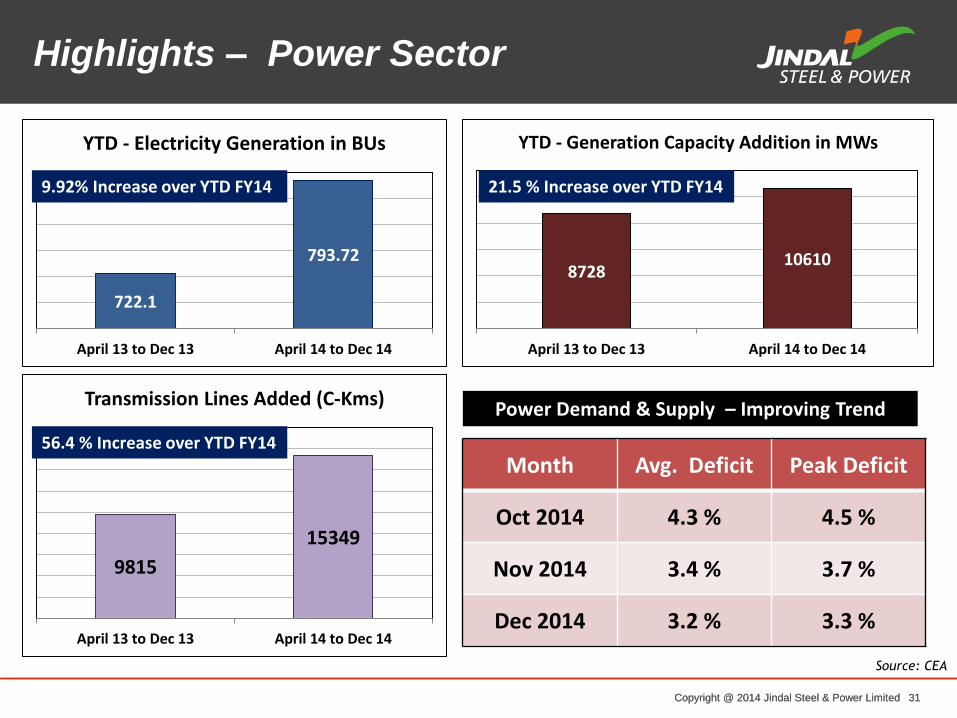

Highlights – Power Sector

Source: CEA

722.1

793.72

April 13 to Dec 13 April 14 to Dec 14

YTD - Electricity Generation in BUs

8728 10610

April 13 to Dec 13 April 14 to Dec 14

YTD - Generation Capacity Addition in MWs

9815

15349

April 13 to Dec 13 April 14 to Dec 14

Transmission Lines Added (C-Kms)

Month Avg. Deficit Peak Deficit

Oct 2014 4.3 % 4.5 %

Nov 2014 3.4 % 3.7 %

Dec 2014 3.2 % 3.3 %

Power Demand & Supply – Improving Trend

9.92% Increase over YTD FY14 21.5 % Increase over YTD FY14

56.4 % Increase over YTD FY14

Copyright @ 2014 Jindal Steel & Power Limited 32 Copyright @ 2014 Jindal Steel & Power Limited 32

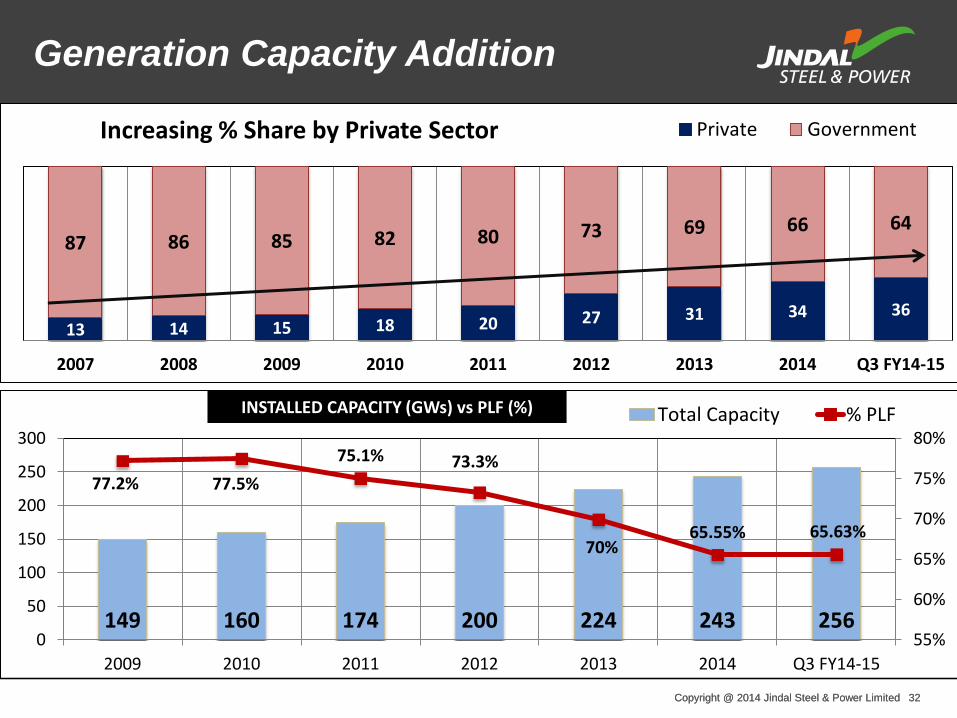

Generation Capacity Addition

13 14 15 18 20 27 31 34 36

87 86 85 82 80 73 69 66 64

2007 2008 2009 2010 2011 2012 2013 2014 Q3 FY14-15

Increasing % Share by Private Sector Private Government

149 160 174 200 224 243 256

77.2% 77.5%

75.1% 73.3%

70% 65.55% 65.63%

55%

60%

65%

70%

75%

80%

0

50

100

150

200

250

300

2009 2010 2011 2012 2013 2014 Q3 FY14-15

Total Capacity % PLFINSTALLED CAPACITY (GWs) vs PLF (%)

Copyright @ 2014 Jindal Steel & Power Limited 33 Copyright @ 2014 Jindal Steel & Power Limited 33

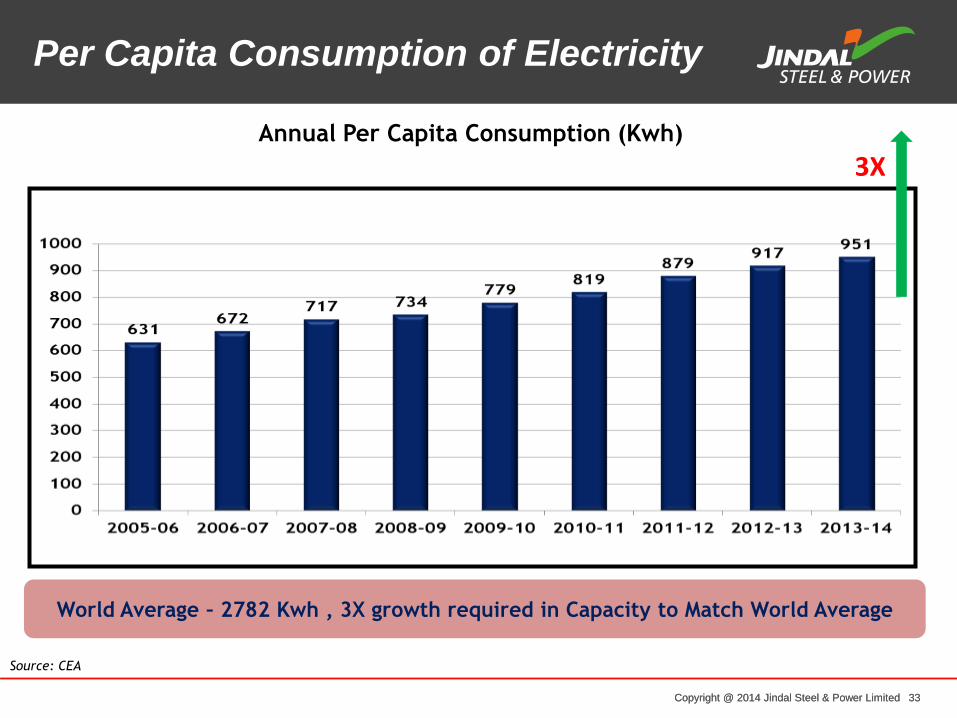

Per Capita Consumption of Electricity

Source: CEA

World Average – 2782 Kwh , 3X growth required in Capacity to Match World Average

Annual Per Capita Consumption (Kwh)

3X

Copyright @ 2014 Jindal Steel & Power Limited 34 Copyright @ 2014 Jindal Steel & Power Limited 34

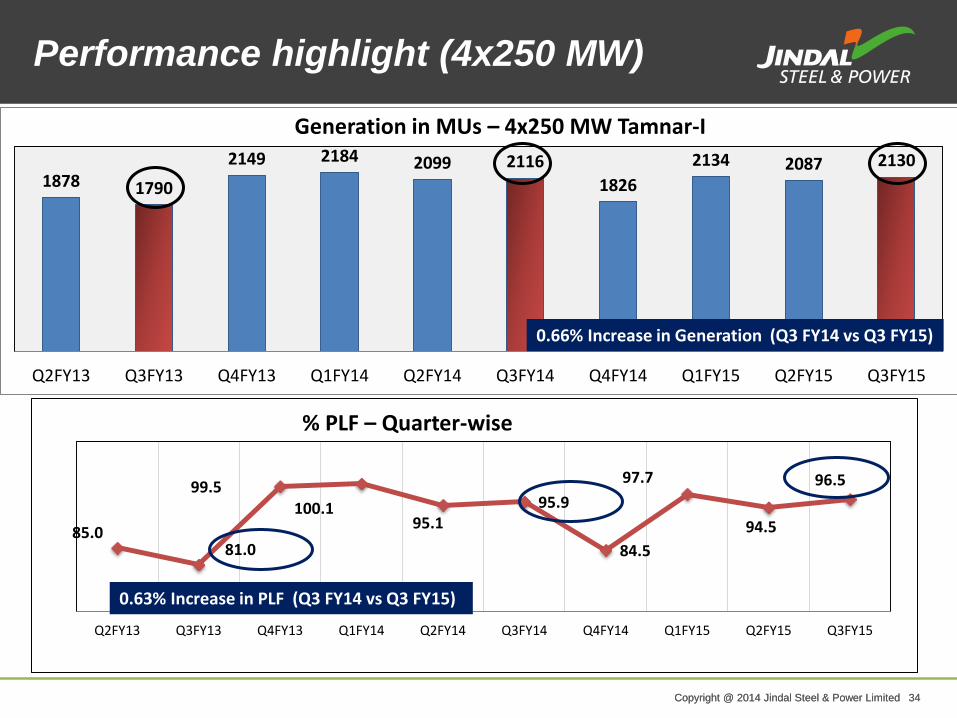

Performance highlight (4x250 MW)

85.0 81.0

99.5 100.1

95.1 95.9

84.5

97.7

94.5

96.5

Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14 Q4FY14 Q1FY15 Q2FY15 Q3FY15

% PLF – Quarter-wise

1878 1790

2149 2184 2099 2116

1826

2134 2087 2130

Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14 Q4FY14 Q1FY15 Q2FY15 Q3FY15

Generation in MUs – 4x250 MW Tamnar-I

0.66% Increase in Generation (Q3 FY14 vs Q3 FY15)

0.63% Increase in PLF (Q3 FY14 vs Q3 FY15)

Copyright @ 2014 Jindal Steel & Power Limited 35 Copyright @ 2014 Jindal Steel & Power Limited 35

Copyright @ 2014 Jindal Steel & Power Limited 36 Copyright @ 2014 Jindal Steel & Power Limited 36

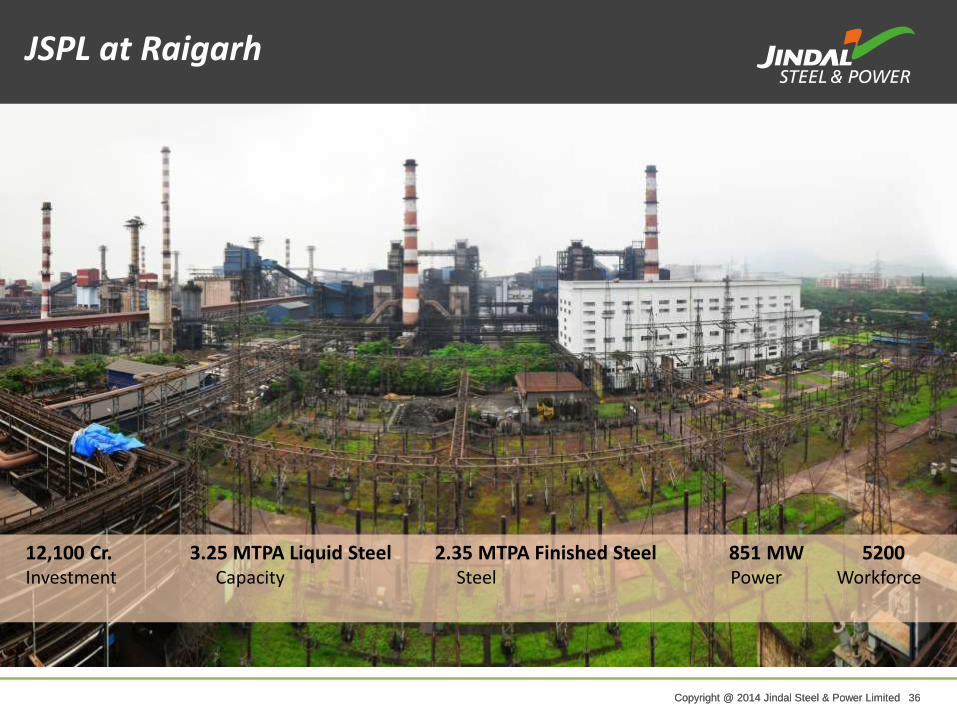

12,100 Cr. 3.25 MTPA Liquid Steel 2.35 MTPA Finished Steel 851 MW 5200 Investment Capacity Steel Power Workforce

JSPL at Raigarh

Copyright @ 2014 Jindal Steel & Power Limited 37 Copyright @ 2014 Jindal Steel & Power Limited 37

Plant Installed

Capacity (Ton)

Covered area (Sq. Mts)

Angul (Odisa)

84,000 32,000

Plant Installed

Capacity (Ton)

Covered area (Sq. Mts)

Punjipatra (Raigarh)

1,20,000 60,000

Structural Steel Division

Copyright @ 2014 Jindal Steel & Power Limited 38 Copyright @ 2014 Jindal Steel & Power Limited 38

18500 Cr. + 2.5 MTPA Steel 1.2 MTPA Finished Steel 810 MW 2723 Investment Capacity Capacity Power Workforce

JSPL at Angul

Copyright @ 2014 Jindal Steel & Power Limited 39 Copyright @ 2014 Jindal Steel & Power Limited 39

Key Features of DRI & CGP at Angul

1) The DRI - Coal Gasification route is being used

for the first time in the world and has the

advantage of using high ash coal.

2) The technology of Coal Gasification Plant has

been taken from Lurgi( South Africa and Germany)

for producing syn gas from coal using a process

known as - Fixed bed dry bottom coal gasification

process.

3) The DRI plant is the first ( Technology - Midrex

USA) in the world to produce cold/hot DRI using

synthesis gas.

Copyright @ 2014 Jindal Steel & Power Limited 40 Copyright @ 2014 Jindal Steel & Power Limited 40

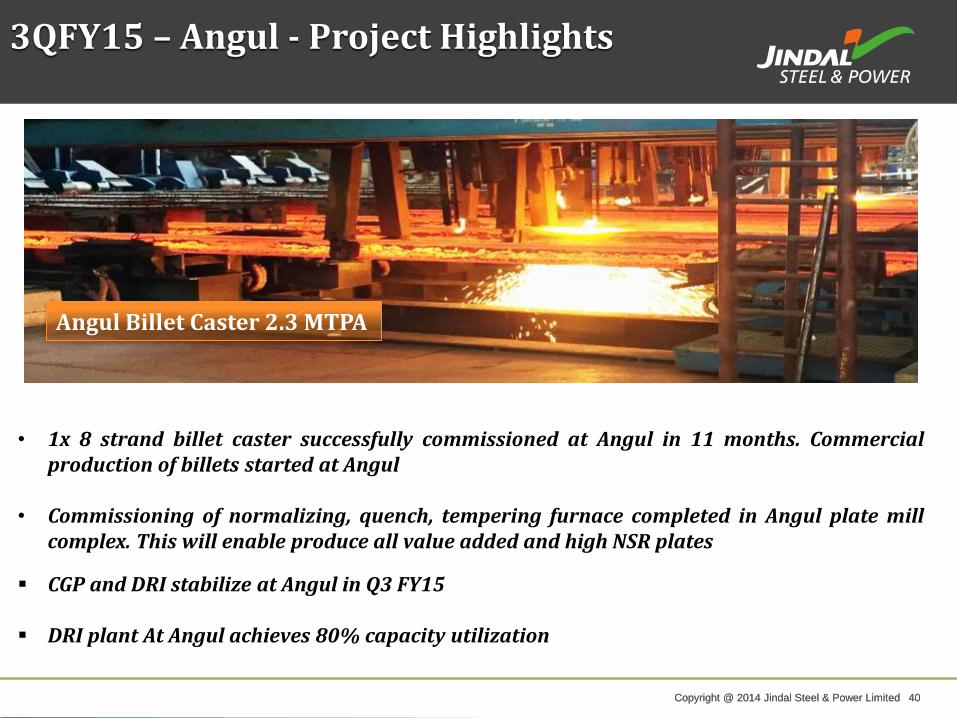

3QFY15 – Angul - Project Highlights

• 1x 8 strand billet caster successfully commissioned at Angul in 11 months. Commercial production of billets started at Angul

• Commissioning of normalizing, quench, tempering furnace completed in Angul plate mill complex. This will enable produce all value added and high NSR plates

CGP and DRI stabilize at Angul in Q3 FY15

DRI plant At Angul achieves 80% capacity utilization

Angul Billet Caster 2.3 MTPA

Copyright @ 2014 Jindal Steel & Power Limited 41 Copyright @ 2014 Jindal Steel & Power Limited 41

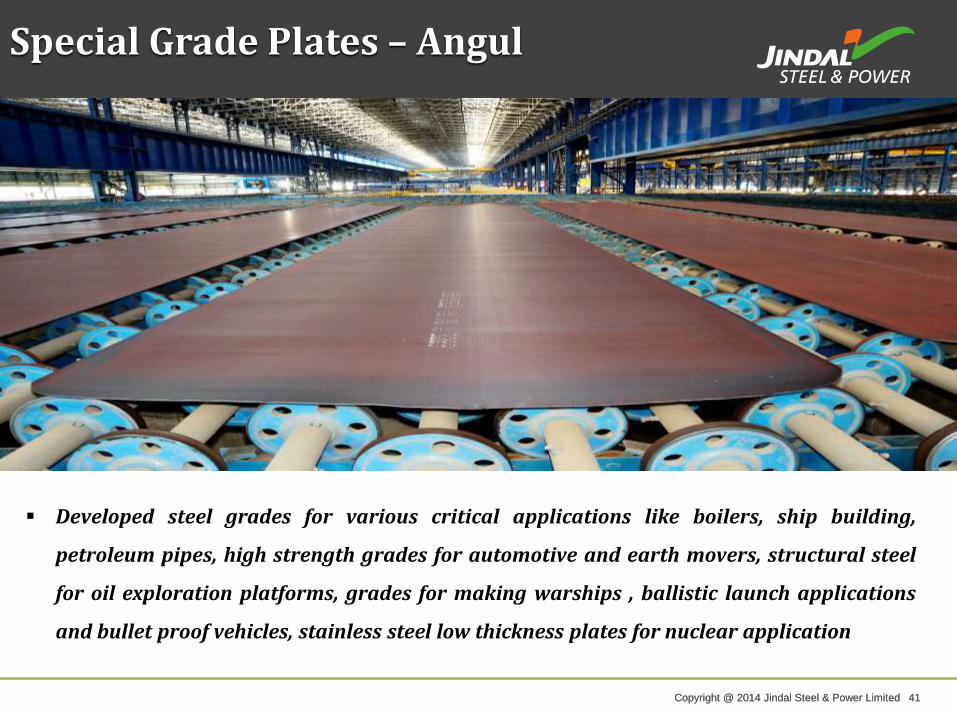

Special Grade Plates – Angul

Developed steel grades for various critical applications like boilers, ship building,

petroleum pipes, high strength grades for automotive and earth movers, structural steel

for oil exploration platforms, grades for making warships , ballistic launch applications

and bullet proof vehicles, stainless steel low thickness plates for nuclear application

Copyright @ 2014 Jindal Steel & Power Limited 42 Copyright @ 2014 Jindal Steel & Power Limited 42

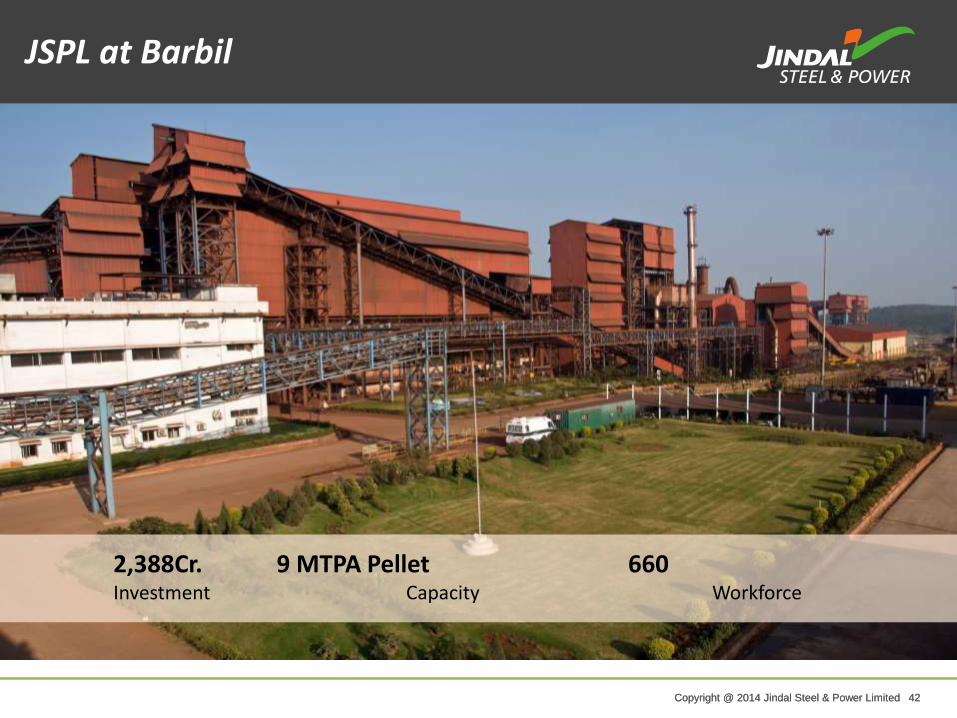

2,388Cr. 9 MTPA Pellet 660 Investment Capacity Workforce

JSPL at Barbil

Copyright @ 2014 Jindal Steel & Power Limited 43 Copyright @ 2014 Jindal Steel & Power Limited 43

1,764 Cr. 1.6 MTPA Finished Steel 1,373 Investment Capacity Workforce

JSPL at Patratu

Copyright @ 2014 Jindal Steel & Power Limited 44 Copyright @ 2014 Jindal Steel & Power Limited 44

S. No. Plant/

Location

Capacity Infrastructure-

Rail track length

in Km

1 Raigarh Inward :14MT; Outward : 4MT 44

2 Angul Inward : 4 MT being enhanced to 10 M T

Outward : 1 MT being enhanced to 2 MT by July’15

20

3 Patratu Inward : 1.5 MT ; Outward: 1.5 MT 12

4 Barbil Outward: 6.6 MT will increase to 8MT (March’15) and

12 MT (August’15)

11

All Plants are well connected by rail and road to ports like Vizag, Paradip, Gangavaram and Haldia.

Logistics - Efficient Rail Handling Capacity

Robust Inwards (Raw Material) & Outwards (Finished goods) connectivity

Copyright @ 2014 Jindal Steel & Power Limited 45 Copyright @ 2014 Jindal Steel & Power Limited 45

Fabricated Structures Hot Rolled Plates

and Coils Parallel Flange Beams

Wire Rods Power

Angles and Channels

TMT Rebars Rails

JSPL Product Range

Copyright @ 2014 Jindal Steel & Power Limited 46 Copyright @ 2014 Jindal Steel & Power Limited 46

Key Customers

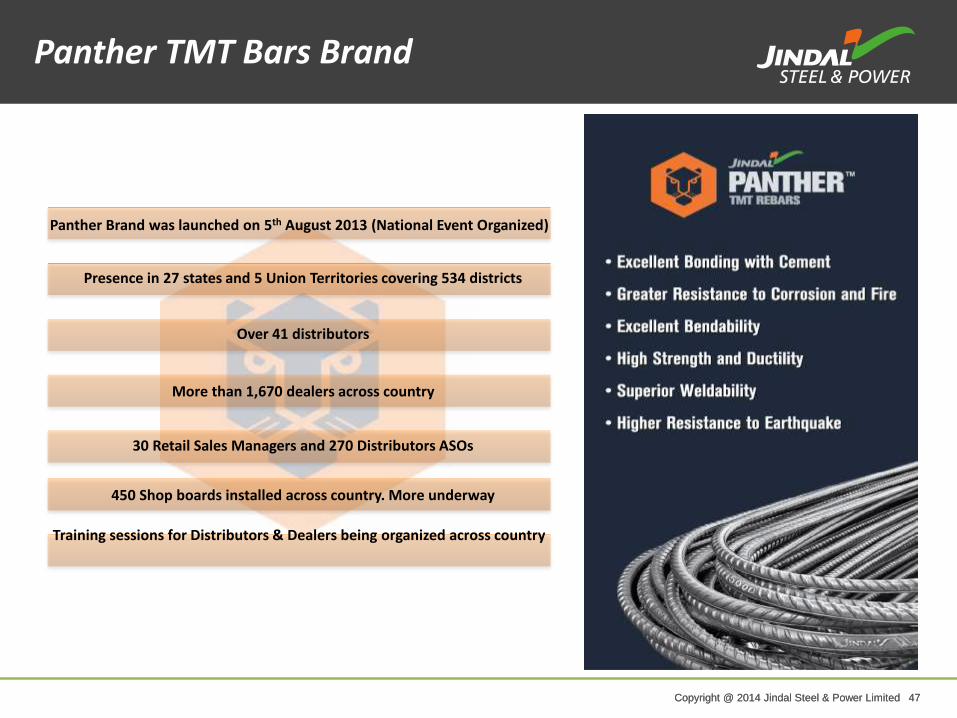

Copyright @ 2014 Jindal Steel & Power Limited 47 Copyright @ 2014 Jindal Steel & Power Limited 47

Presence in 27 states and 5 Union Territories covering 534 districts

Over 41 distributors

More than 1,670 dealers across country

30 Retail Sales Managers and 270 Distributors ASOs

450 Shop boards installed across country. More underway

Panther Brand was launched on 5th August 2013 (National Event Organized)

Training sessions for Distributors & Dealers being organized across country

Panther TMT Bars Brand

Copyright @ 2014 Jindal Steel & Power Limited 48 Copyright @ 2014 Jindal Steel & Power Limited 48

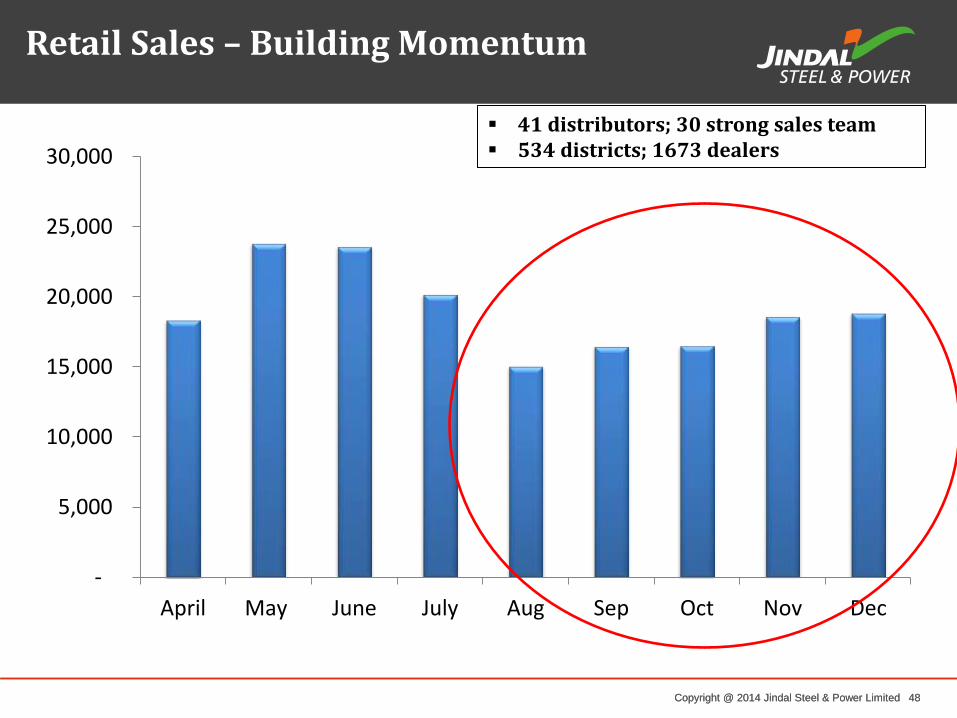

Retail Sales – Building Momentum

-

5,000

10,000

15,000

20,000

25,000

30,000

April May June July Aug Sep Oct Nov Dec

41 distributors; 30 strong sales team 534 districts; 1673 dealers

Copyright @ 2014 Jindal Steel & Power Limited 49 Copyright @ 2014 Jindal Steel & Power Limited 49 Power Plant at Tamnar

POWER

Copyright @ 2014 Jindal Steel & Power Limited 50 Copyright @ 2014 Jindal Steel & Power Limited 50

96.43% subsidiary of JSPL

Existing Units Phase I - 1000MW (4 X 250) Phase II - 1800MW (3 X 600)

Under Implementation 600MW (1 X 600)

JINDAL POWER LIMITED

Copyright @ 2014 Jindal Steel & Power Limited 51 Copyright @ 2014 Jindal Steel & Power Limited 51

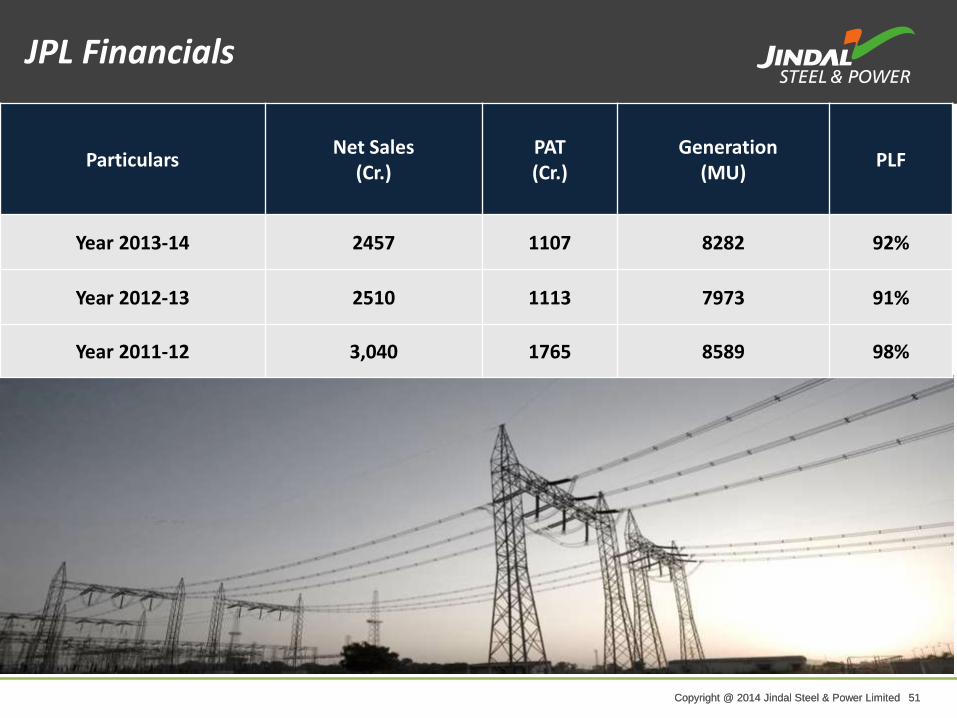

Particulars Net Sales

(Cr.) PAT (Cr.)

Generation (MU)

PLF

Year 2013-14 2457 1107 8282 92%

Year 2012-13 2510 1113 7973 91%

Year 2011-12 3,040 1765 8589 98%

JPL Financials

Copyright @ 2014 Jindal Steel & Power Limited 52 Copyright @ 2014 Jindal Steel & Power Limited 52

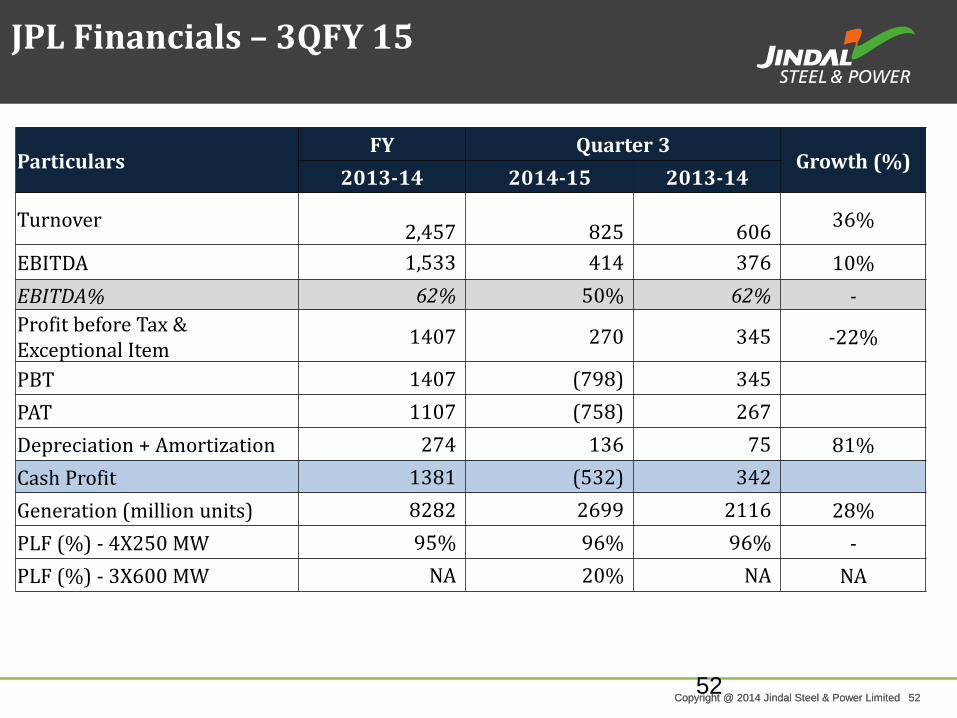

JPL Financials – 3QFY 15

Particulars FY Quarter 3

Growth (%) 2013-14 2014-15 2013-14

Turnover

2,457

825

606 36%

EBITDA 1,533 414 376 10%

EBITDA% 62% 50% 62% -

Profit before Tax & Exceptional Item

1407 270 345 -22%

PBT 1407 (798) 345

PAT 1107 (758) 267

Depreciation + Amortization 274 136 75 81%

Cash Profit 1381 (532) 342

Generation (million units) 8282 2699 2116 28%

PLF (%) - 4X250 MW 95% 96% 96% -

PLF (%) - 3X600 MW NA 20% NA NA

52

Copyright @ 2014 Jindal Steel & Power Limited 53 Copyright @ 2014 Jindal Steel & Power Limited 53

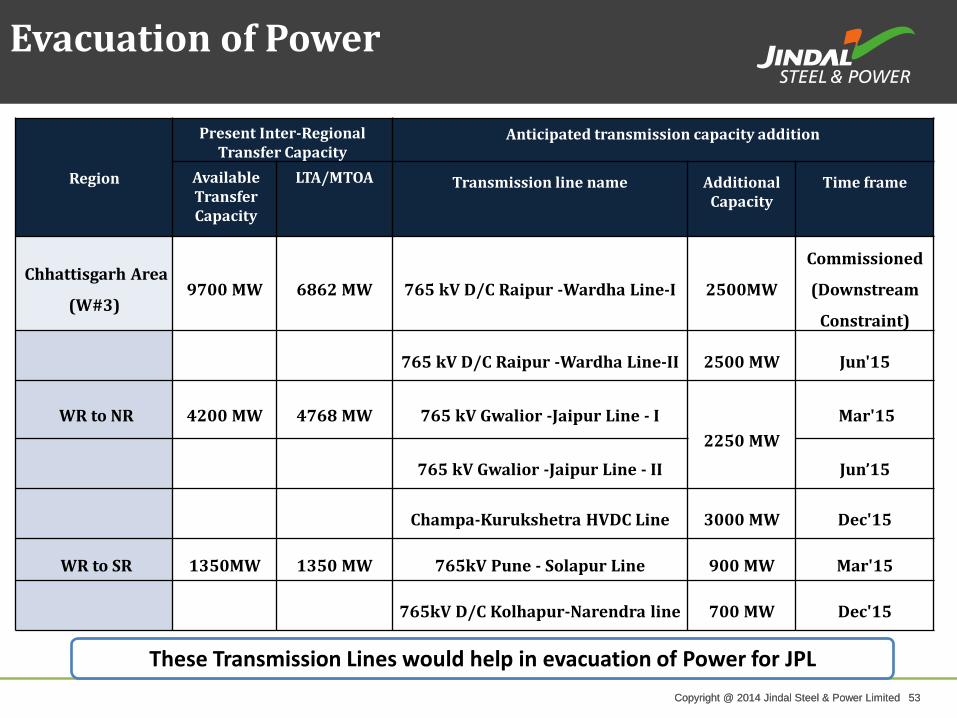

Evacuation of Power

These Transmission Lines would help in evacuation of Power for JPL

Region

Present Inter-Regional Transfer Capacity

Anticipated transmission capacity addition

Available Transfer Capacity

LTA/MTOA Transmission line name Additional Capacity

Time frame

Chhattisgarh Area

(W#3) 9700 MW 6862 MW 765 kV D/C Raipur -Wardha Line-I 2500MW

Commissioned

(Downstream

Constraint)

765 kV D/C Raipur -Wardha Line-II 2500 MW Jun'15

WR to NR 4200 MW 4768 MW 765 kV Gwalior -Jaipur Line - I

2250 MW

Mar'15

765 kV Gwalior -Jaipur Line - II Jun’15

Champa-Kurukshetra HVDC Line 3000 MW Dec'15

WR to SR 1350MW 1350 MW 765kV Pune - Solapur Line 900 MW Mar'15

765kV D/C Kolhapur-Narendra line 700 MW Dec'15

Copyright @ 2014 Jindal Steel & Power Limited 54 Copyright @ 2014 Jindal Steel & Power Limited 54 Corporate Office, Jindal Africa

Copyright @ 2014 Jindal Steel & Power Limited 55 Copyright @ 2014 Jindal Steel & Power Limited 55

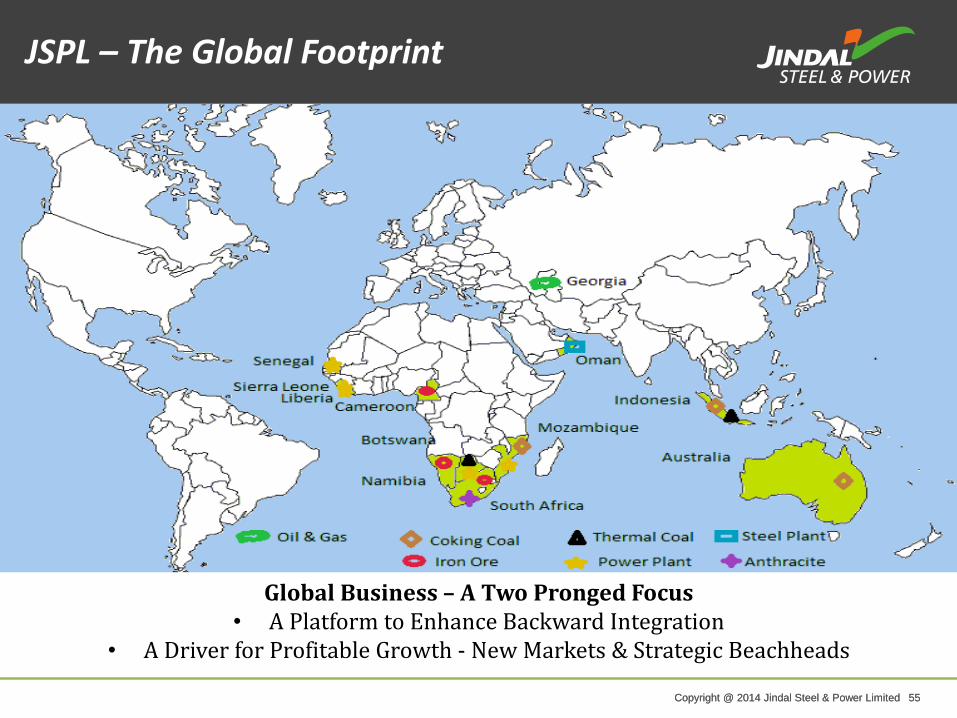

Global Business – A Two Pronged Focus • A Platform to Enhance Backward Integration

• A Driver for Profitable Growth - New Markets & Strategic Beachheads

JSPL – The Global Footprint

Copyright @ 2014 Jindal Steel & Power Limited 56 Copyright @ 2014 Jindal Steel & Power Limited 56

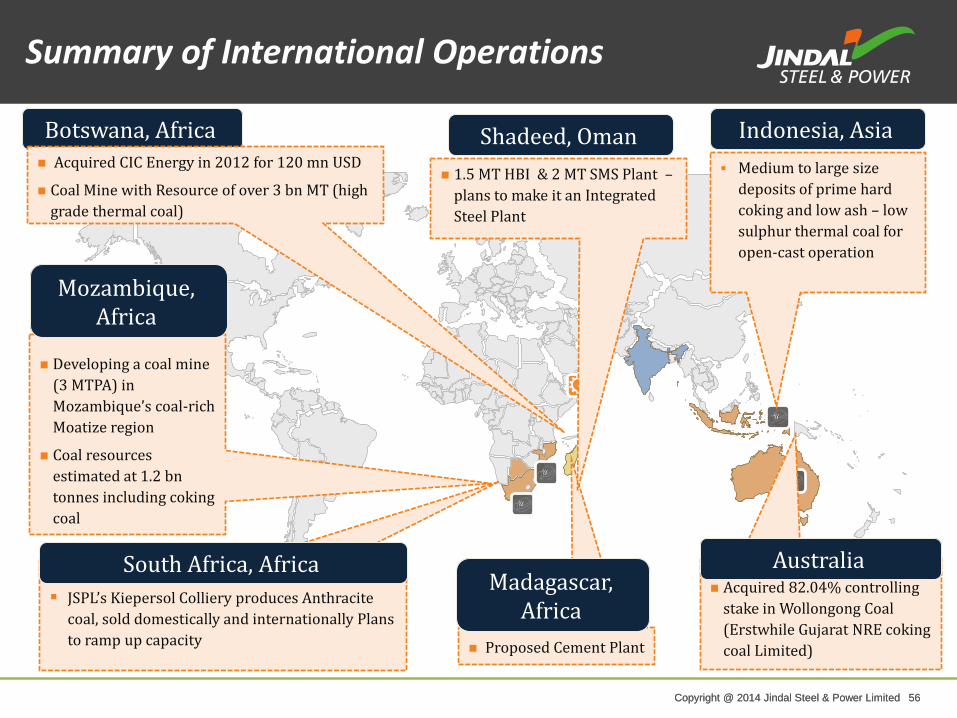

Developing a coal mine

(3 MTPA) in

Mozambique’s coal-rich

Moatize region

Coal resources

estimated at 1.2 bn

tonnes including coking

coal

Mozambique, Africa

JSPL’s Kiepersol Colliery produces Anthracite

coal, sold domestically and internationally Plans

to ramp up capacity

South Africa, Africa

Botswana, Africa Acquired CIC Energy in 2012 for 120 mn USD

Coal Mine with Resource of over 3 bn MT (high

grade thermal coal)

Proposed Cement Plant

Madagascar, Africa

Acquired 82.04% controlling

stake in Wollongong Coal

(Erstwhile Gujarat NRE coking

coal Limited)

Australia

1.5 MT HBI & 2 MT SMS Plant –

plans to make it an Integrated

Steel Plant

Shadeed, Oman Medium to large size

deposits of prime hard

coking and low ash – low

sulphur thermal coal for

open-cast operation

Indonesia, Asia

Summary of International Operations

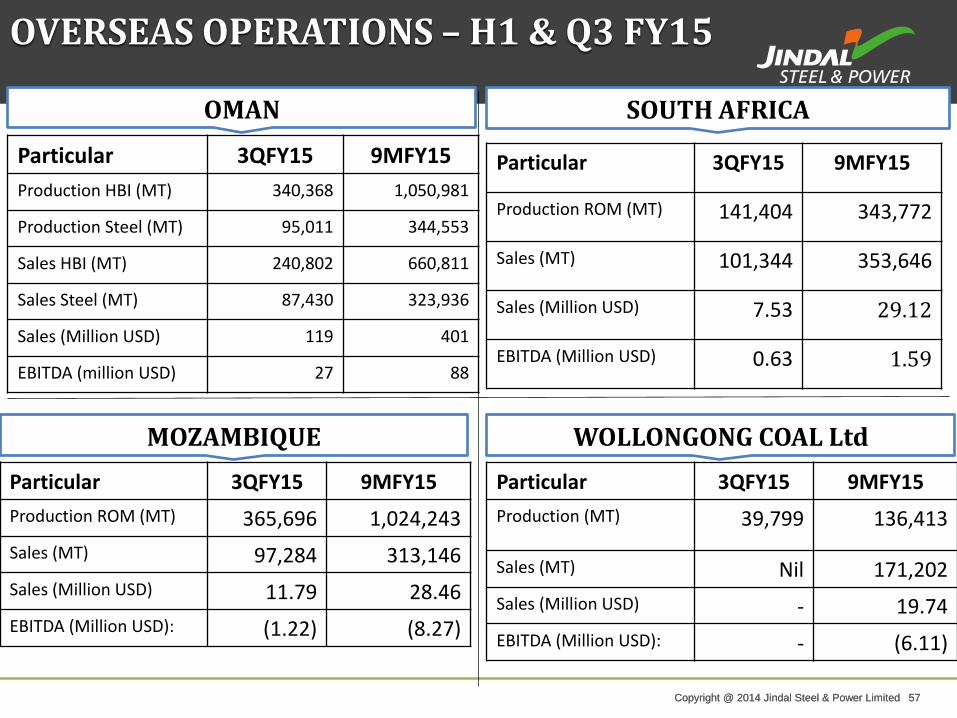

Copyright @ 2014 Jindal Steel & Power Limited 57 Copyright @ 2014 Jindal Steel & Power Limited 57

OMAN

OVERSEAS OPERATIONS – H1 & Q3 FY15

Particular 3QFY15 9MFY15

Production HBI (MT) 340,368 1,050,981

Production Steel (MT) 95,011 344,553

Sales HBI (MT) 240,802 660,811

Sales Steel (MT) 87,430 323,936

Sales (Million USD) 119 401

EBITDA (million USD) 27 88

Particular 3QFY15 9MFY15

Production ROM (MT) 141,404 343,772

Sales (MT) 101,344 353,646

Sales (Million USD) 7.53 29.12

EBITDA (Million USD) 0.63 1.59

SOUTH AFRICA

Particular 3QFY15 9MFY15

Production ROM (MT) 365,696 1,024,243

Sales (MT) 97,284 313,146

Sales (Million USD) 11.79 28.46

EBITDA (Million USD): (1.22) (8.27)

MOZAMBIQUE

Particular 3QFY15 9MFY15

Production (MT) 39,799 136,413

Sales (MT) Nil 171,202

Sales (Million USD) - 19.74

EBITDA (Million USD): - (6.11)

WOLLONGONG COAL Ltd

Copyright @ 2014 Jindal Steel & Power Limited 58 Copyright @ 2014 Jindal Steel & Power Limited 58

In July 2010, JSPL acquired Shadeed Iron & Steel Co. LLC, a company incorporated under the laws of the Sultanate of Oman

• Gas-based 1.5 MTPA HBI plant at Sohar Industrial Port commenced production in January 2011

• Commissioned steelmaking facility of 2 MTPA in CY14

Investment

Jindal Shadeed – Oman

Copyright @ 2014 Jindal Steel & Power Limited 59 Copyright @ 2014 Jindal Steel & Power Limited 59 59

• DRI Plant has achieved maximum operating hours of 8,629 in the calendar year 2014 since commissioning of the plant. Worldwide, no other DRI plant has achieved this target. The operating efficiency of 98.5% is the best for a plant of this size running on the same technology.

• EBIDTA in Q3 has increased by 3.8 % as compared to previous year Q3 (Oct13-Dec 13).

• Round Billets were cast successfully after commissioning and dispatched 2200 Tons through see route in November 2014 to JESCO, Saudi Arabia.

• Oman Chamber of Commerce & Industry (OCCI) felicitated JSIS for its contribution to the development of Small & Medium Enterprises (SMEs).

• Various management initiatives like TPM, Safe workplace activities, maintenance of quality standards have been implemented in the entire plant.

JSPL – Oman – 3QFY15 Highlights

Copyright @ 2014 Jindal Steel & Power Limited 60 Copyright @ 2014 Jindal Steel & Power Limited 60

• Potential Resource: 2 bn MT

• Grade: Semi Hard coking coal , High Grade Thermal Coal

• Current Mining @ 3 MTPA run rate

• 3 MTPA Coal Washery commissioned

Mozambique, Africa

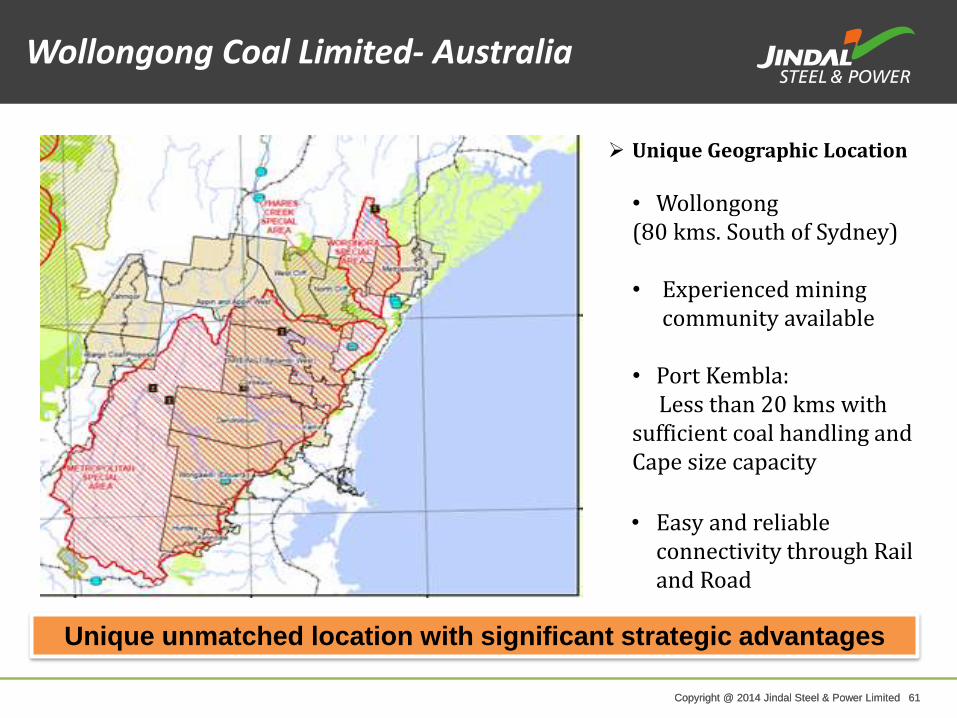

Copyright @ 2014 Jindal Steel & Power Limited 61 Copyright @ 2014 Jindal Steel & Power Limited 61

Unique unmatched location with significant strategic advantages

Unique Geographic Location

• Wollongong (80 kms. South of Sydney) • Experienced mining

community available

• Port Kembla: Less than 20 kms with sufficient coal handling and Cape size capacity

• Easy and reliable

connectivity through Rail and Road

Wollongong Coal Limited- Australia

Copyright @ 2014 Jindal Steel & Power Limited 62 Copyright @ 2014 Jindal Steel & Power Limited 62

• Southern Africa head office is based in Johannesburg, South Africa

• Operations include Kiepersol Colliery outside the town of Piet Retief in Mpumalanga province

• The mine produces high-quality anthracite coal, sold nationally and internationally

• Underground mining with 1.2 MTPA capacity annually

South Africa, Africa

Copyright @ 2014 Jindal Steel & Power Limited 63 Copyright @ 2014 Jindal Steel & Power Limited 63

Thermal Coal Asset

• Large size deposit of low ash – low sulphur thermal coal for open cast operation

• Coal mining license obtained in 2009 for 10 years till March 2018 for over 35.9 square Kilometres

• Permit received from the Ministry of Forest for the entire concession area

• MoU signed with Bupati Barito to develop road for coal hauling

• 139 hectares acquired for the first phase of mining

• Acquired 17.7 hectares for the development of captive coal terminal for coal handling and

barge loading at Barito River

Coking Coal Asset

Exploration License over 100 square kilometre in Central Kalimantan

Medium to large size deposits of prime hard coking and thermal coal for open-cast operation Pit Sampling

Indonesia, Asia

Copyright @ 2014 Jindal Steel & Power Limited 64 Copyright @ 2014 Jindal Steel & Power Limited 64

Copyright @ 2014 Jindal Steel & Power Limited 65 Copyright @ 2014 Jindal Steel & Power Limited 65

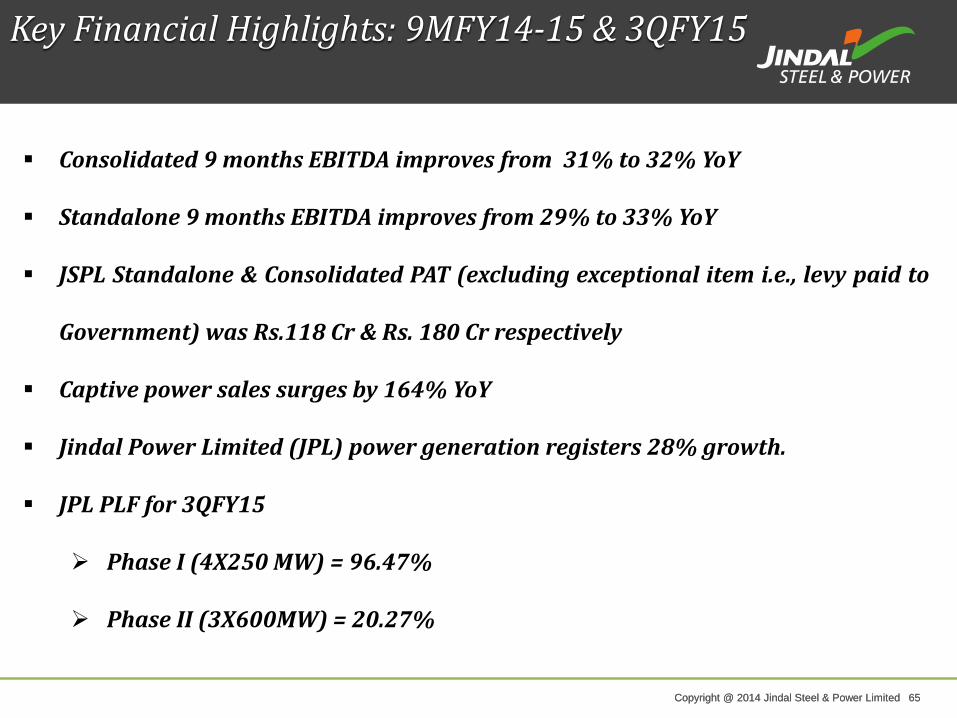

Key Financial Highlights: 9MFY14-15 & 3QFY15

Consolidated 9 months EBITDA improves from 31% to 32% YoY

Standalone 9 months EBITDA improves from 29% to 33% YoY

JSPL Standalone & Consolidated PAT (excluding exceptional item i.e., levy paid to

Government) was Rs.118 Cr & Rs. 180 Cr respectively

Captive power sales surges by 164% YoY

Jindal Power Limited (JPL) power generation registers 28% growth.

JPL PLF for 3QFY15

Phase I (4X250 MW) = 96.47%

Phase II (3X600MW) = 20.27%

Copyright @ 2014 Jindal Steel & Power Limited 66 Copyright @ 2014 Jindal Steel & Power Limited 66

Consolidated Financials at a Glance

FY08 FY09 FY10 FY11 FY12 FY13 FY14 9M FY 15

INCOME STATEMENT

Revenue 5,539 10,913 11,152 13,194 18,351 19,807 19,286 14,875

EBITDA 2,253 5,908 5,232 6,398 6,935 6,669 5,776 4,694

PAT* 1,251 3,007 3,635 3,804 4,002 2,912 1,894 982

Cash Profit* 1,810 4,194 4,760 5,115 5,575 4,593 3,876 3,403

BALANCE SHEET

Gross Block 10,680 14,928 21,109 29,317 35,802 45,912 63,056 69,262

Net Worth 3,824 7,021 10,387 14,088 17,931 21,150 21,191 20,097

Borrowings 6,996 8,113 8,605 13,987 17,058 24,618 36,368 44,222

Net Debt 6,225 7,091 8,436 12,854 15,616 24,430 35,419 41,934

SIGNIFICANT RATIOS

EBITDA Margin (%) 41 54 47 48 38 34 30 32

Net Profit to Sales (%) 23% 28% 33% 29% 22% 15% 10% 7%

Return on Net Worth (%) 34% 43% 35% 27% 22% 14% 9% 10%

Long Term Debt Equity

Ratio1.74 1.03 0.59 0.7 0.61 0.77 1.29 1.62

EPS (INR/Share) (a) (b) 13.54 32.44 39.05 40.75 42.42 31.13 20.53 11.37

* Before Exceptional Item

Copyright @ 2014 Jindal Steel & Power Limited 67 Copyright @ 2014 Jindal Steel & Power Limited 67

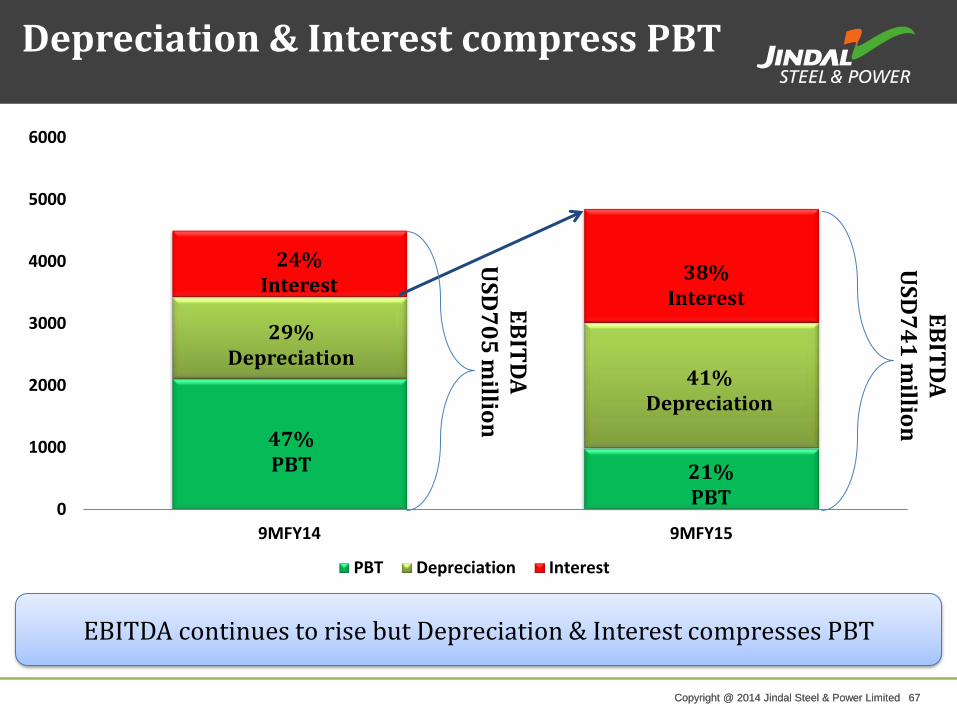

0

1000

2000

3000

4000

5000

6000

9MFY14 9MFY15

PBT Depreciation Interest

EBITDA continues to rise but Depreciation & Interest compresses PBT

38% Interest

21% PBT

Depreciation & Interest compress PBT

24% Interest

47% PBT

EB

ITD

A

US

D7

05

millio

n

29% Depreciation

41% Depreciation

EB

ITD

A

US

D7

41

millio

n

Copyright @ 2014 Jindal Steel & Power Limited 68 Copyright @ 2014 Jindal Steel & Power Limited 68

Financial Results – Standalone 9M FY15

Particulars (Rupees in Crores) For 9M ending %

31.12.2014 31.12.2013 Y ON Y

Turnover-Total 10,062 10,344 -2.7%

EBITDA 3,321 3,041

EBITDA % 33% 29%

Depreciation 1,319 906 45.6%

Finance costs 1,430 932 53.5%

Profit before tax & exceptional item 627 1,216 -48.4%

Exceptional item 787 -

Profit before Tax (160) 1,216

Profit after Tax (PAT) (76) 861

Profit after Tax (PAT) before exceptional items 711 861

Cash Profit before exceptional item 2,212 1,867

Cash Profit after exceptional item 1,425 1,867 -23.7%

CAPEX 2,442 4,413 -44.7%

Inspite of subdued steel demand, EBITDA margin grew 4% YoY

Copyright @ 2014 Jindal Steel & Power Limited 69 Copyright @ 2014 Jindal Steel & Power Limited 69

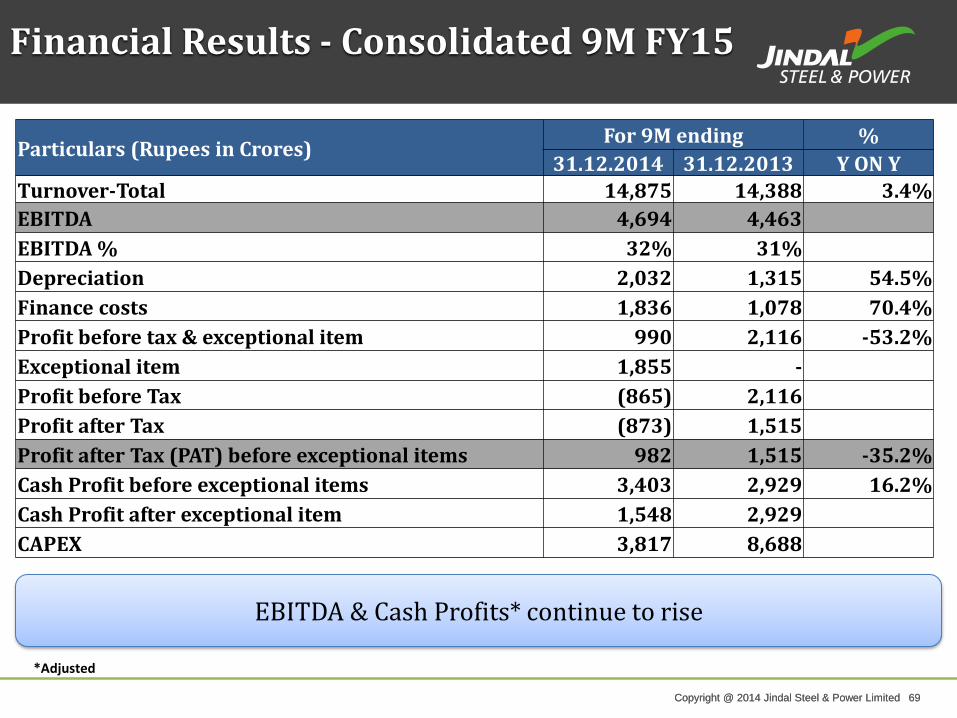

Financial Results - Consolidated 9M FY15

Particulars (Rupees in Crores) For 9M ending %

31.12.2014 31.12.2013 Y ON Y

Turnover-Total 14,875 14,388 3.4%

EBITDA 4,694 4,463

EBITDA % 32% 31%

Depreciation 2,032 1,315 54.5%

Finance costs 1,836 1,078 70.4%

Profit before tax & exceptional item 990 2,116 -53.2%

Exceptional item 1,855 -

Profit before Tax (865) 2,116

Profit after Tax (873) 1,515

Profit after Tax (PAT) before exceptional items 982 1,515 -35.2%

Cash Profit before exceptional items 3,403 2,929 16.2%

Cash Profit after exceptional item 1,548 2,929

CAPEX 3,817 8,688

EBITDA & Cash Profits* continue to rise

*Adjusted

Copyright @ 2014 Jindal Steel & Power Limited 70 Copyright @ 2014 Jindal Steel & Power Limited 70

Way Forward

Copyright @ 2014 Jindal Steel & Power Limited 71 Copyright @ 2014 Jindal Steel & Power Limited 71

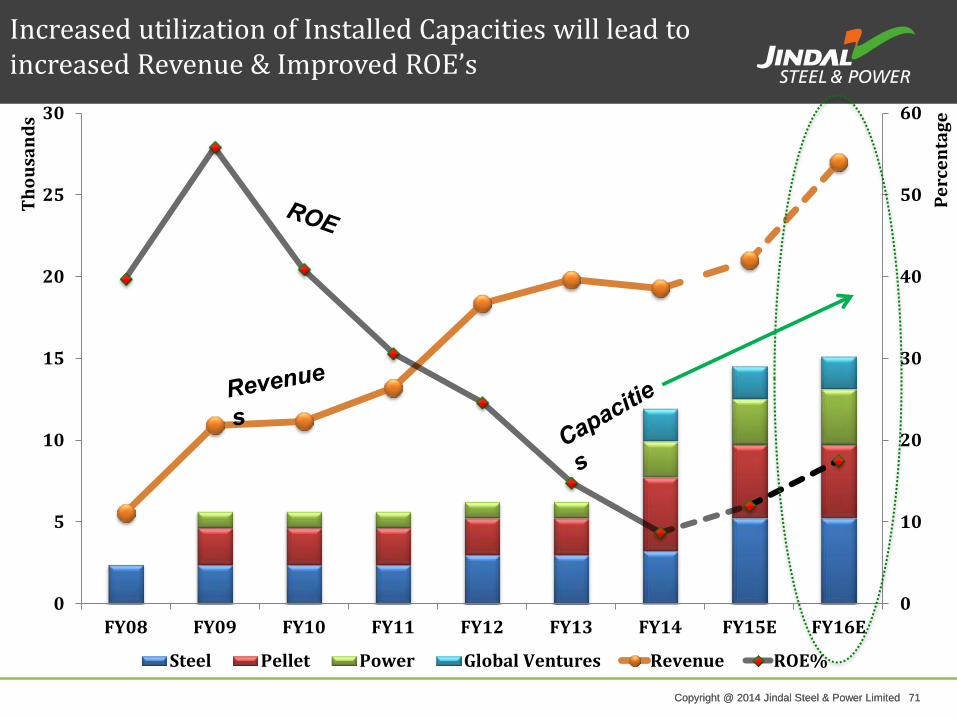

0

10

20

30

40

50

60

0

5

10

15

20

25

30

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E

Pe

rce

nta

ge

Th

ou

san

ds

Steel Pellet Power Global Ventures Revenue ROE%

Increased utilization of Installed Capacities will lead to increased Revenue & Improved ROE’s

Copyright @ 2014 Jindal Steel & Power Limited 72 Copyright @ 2014 Jindal Steel & Power Limited 72

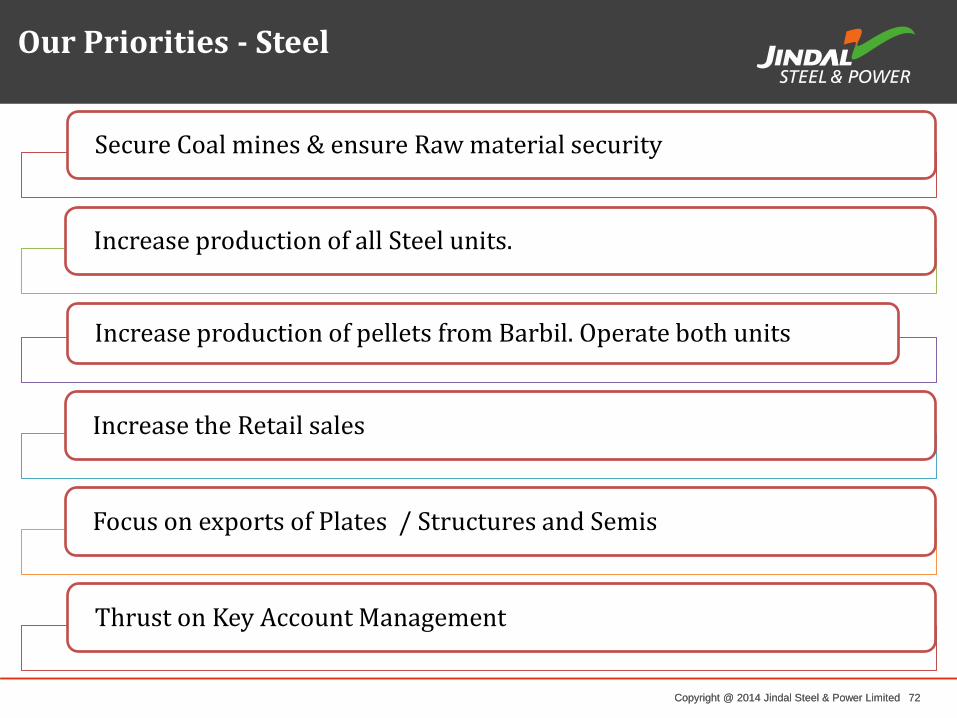

Our Priorities - Steel

Secure Coal mines & ensure Raw material security

Increase production of all Steel units.

Increase production of pellets from Barbil. Operate both units

Increase the Retail sales

Focus on exports of Plates / Structures and Semis

Thrust on Key Account Management

Copyright @ 2014 Jindal Steel & Power Limited 73 Copyright @ 2014 Jindal Steel & Power Limited 73

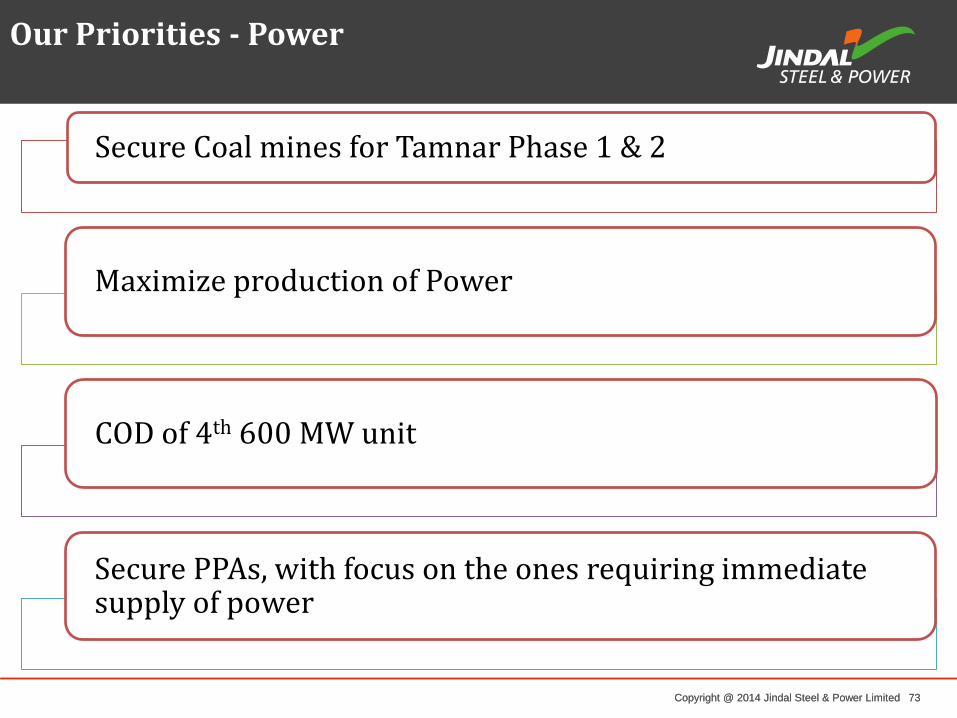

Our Priorities - Power

Secure Coal mines for Tamnar Phase 1 & 2

Maximize production of Power

COD of 4th 600 MW unit

Secure PPAs, with focus on the ones requiring immediate supply of power

Copyright @ 2014 Jindal Steel & Power Limited 74 Copyright @ 2014 Jindal Steel & Power Limited 74

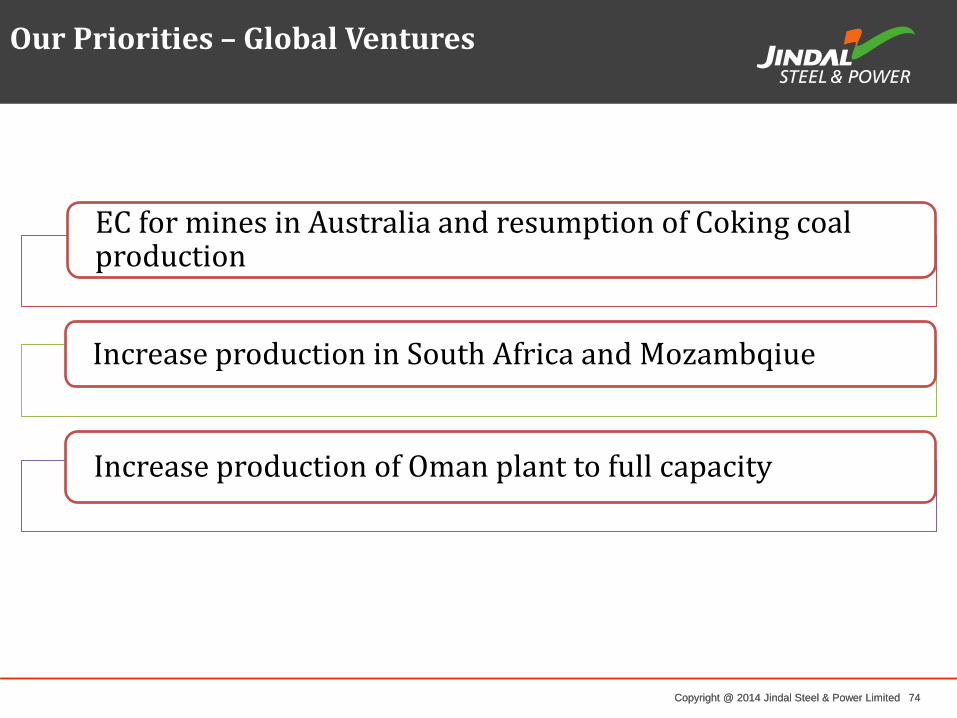

Our Priorities – Global Ventures

EC for mines in Australia and resumption of Coking coal production

Increase production in South Africa and Mozambqiue

Increase production of Oman plant to full capacity

Copyright @ 2014 Jindal Steel & Power Limited 75 Copyright @ 2014 Jindal Steel & Power Limited 75

Making Sustainability a Focus Priority

Copyright @ 2014 Jindal Steel & Power Limited 76 Copyright @ 2014 Jindal Steel & Power Limited 76

9 PILLARS OF CSR

A Responsible Corporate Citizen

Copyright @ 2014 Jindal Steel & Power Limited 77 Copyright @ 2014 Jindal Steel & Power Limited 77

A Responsible Corporate Citizen

Copyright @ 2014 Jindal Steel & Power Limited 78 Copyright @ 2014 Jindal Steel & Power Limited 78

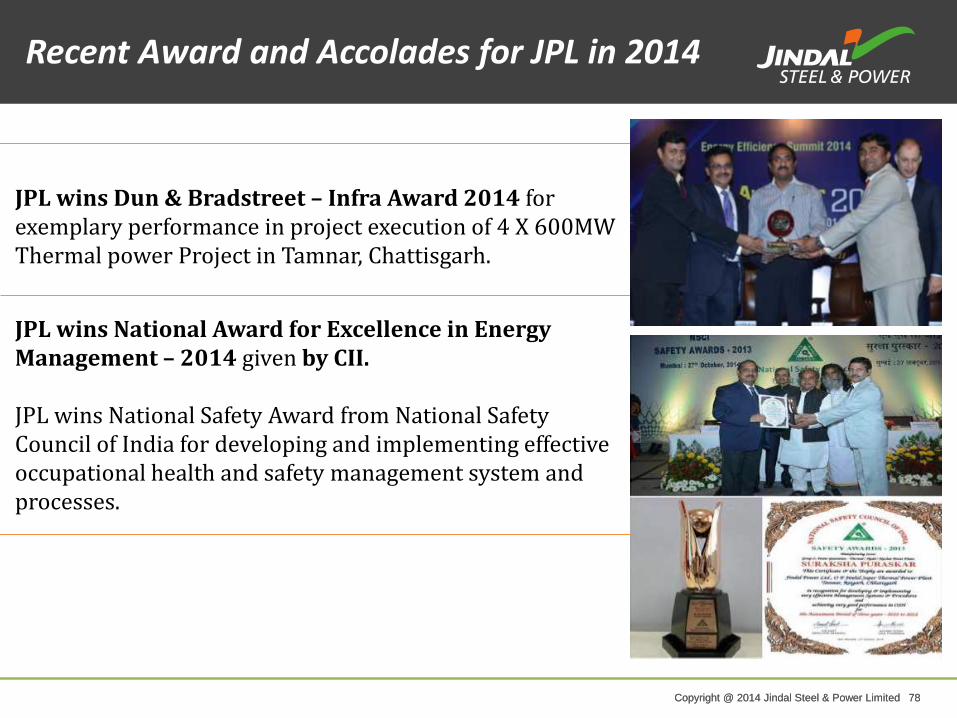

JPL wins Dun & Bradstreet – Infra Award 2014 for exemplary performance in project execution of 4 X 600MW Thermal power Project in Tamnar, Chattisgarh.

JPL wins National Award for Excellence in Energy Management – 2014 given by CII. JPL wins National Safety Award from National Safety Council of India for developing and implementing effective occupational health and safety management system and processes.

Recent Award and Accolades for JPL in 2014

Copyright @ 2014 Jindal Steel & Power Limited 79 Copyright @ 2014 Jindal Steel & Power Limited 79

2014 Shrishti Global Award -2014 Global HR Excellence Award-2014

2013 International Safety Award with merit 2014 by British Safety Council, UK. World CSR Congress Award 2013 Greentech CSR Award 2013

2012 Golden Peacock National CSR Award 2012

2011

Ranked No.1 as Wealth Creator in India over a 10- year period (Business World)

Awarded the Dun & Bradstreet- Rolta Corporate Awards 2011

Ranked 3rd in the Metals Category of Business World’s India’s Most Respected Companies Survey

Received the Forbes Asia’s ‘Fabulous 50’ International Award

Golden Peacock Innovation Management Awards

Greentech Award for 1st Position in Metal & Mining Industries

World HRD Congress CSR Award on women empowerment

2010

Rated the World’s 2nd Largest Value Creator by Boston Consulting Group (BCG), based on Total Shareholder Return from 2005-2009, and the largest Value Creator in Mining and Materials category

Received the Forbes Asia’s ‘Fabulous 50’ International Award

Golden Peacock Innovation Management Awards

CSR Excellence Award 2010 by ASSOCHAM for promoting and propagating Corporate Social Responsibility initiatives

2009

Received the CNBC’s Most Promising Entrant into the Big League at IBLA

National Energy Conservation Award

Golden Peacock Innovation Award 2009

Winner of ‘Shrishti Green Cube Award 2009

SAIL HR Excellence Award 2009

Other Award and Accolades

Copyright @ 2014 Jindal Steel & Power Limited 80 Copyright @ 2014 Jindal Steel & Power Limited 80

SAFETY INDUCTION ON-THE-JOB SAFETY TRAINING

SAFETY REVIEWS SAFETY AUDITS / INSPECTIONS

Health & Safety Best Practices

Copyright @ 2014 Jindal Steel & Power Limited 81 Copyright @ 2014 Jindal Steel & Power Limited 81

TOOL BOX MEETINGS SAFETY AWARDS/REWARDS

MEDICAL EXAMINATIONS/ WORLD CLASS PPEs MOCK DRILLS

Health & Safety Best Practices

Copyright @ 2014 Jindal Steel & Power Limited 82 Copyright @ 2014 Jindal Steel & Power Limited 82

Copyright @ 2014 Jindal Steel & Power Limited 83 Copyright @ 2014 Jindal Steel & Power Limited 83

RMHS - Angul

Jindal Steel & Power Limited

Copyright @ 2014 Jindal Steel & Power Limited 84 Copyright @ 2014 Jindal Steel & Power Limited 84

Railway Siding- Angul

Copyright @ 2014 Jindal Steel & Power Limited 85 Copyright @ 2014 Jindal Steel & Power Limited 85

Oxygen Plant- Angul

Copyright @ 2014 Jindal Steel & Power Limited 86 Copyright @ 2014 Jindal Steel & Power Limited 86

Jindal Shadeed, Oman – Rolling Mill under Construction

Copyright @ 2014 Jindal Steel & Power Limited 87 Copyright @ 2014 Jindal Steel & Power Limited 87

Jindal Shadeed, Oman -Rolling Mill under Construction

Copyright @ 2014 Jindal Steel & Power Limited 88 Copyright @ 2014 Jindal Steel & Power Limited 88

JPL – 4x600 MW

Copyright @ 2014 Jindal Steel & Power Limited 89 Copyright @ 2014 Jindal Steel & Power Limited 89

JPL – 4x600 MW

Copyright @ 2014 Jindal Steel & Power Limited 90 Copyright @ 2014 Jindal Steel & Power Limited 90

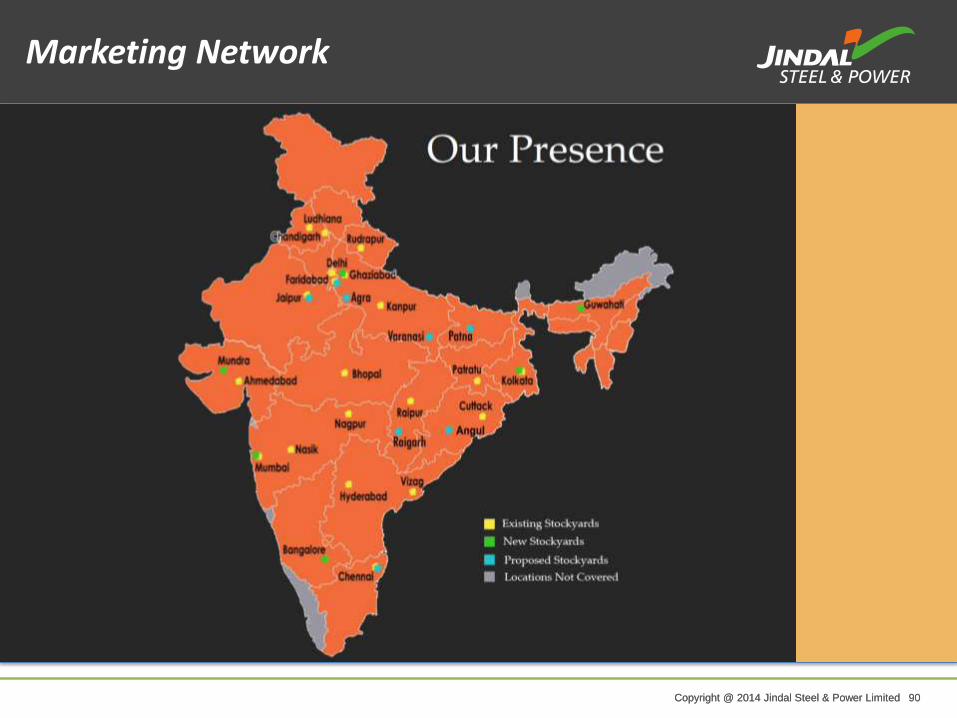

Marketing Network

Copyright @ 2014 Jindal Steel & Power Limited 91 Copyright @ 2014 Jindal Steel & Power Limited 91

Mr. D.Balasubramanyam Head of Investor Relations Tel: 011-26739109, Mobile: 8130755166 Email: [email protected]

Ms. Pallavi Kumari Investor Relations Tel: 011-26739165, Mobile: 8800094171 Email: [email protected]

For any information please contact : -

Mr. Nishant Baranwal Investor Relations Tel: 011-26739178, Mobile: 8800690255 Email: [email protected]

Copyright @ 2014 Jindal Steel & Power Limited 92 Copyright @ 2014 Jindal Steel & Power Limited 92

Thank You

Copyright @ 2014 Jindal Steel & Power Limited 93 Copyright @ 2014 Jindal Steel & Power Limited 93

Annexures

Copyright @ 2014 Jindal Steel & Power Limited 94 Copyright @ 2014 Jindal Steel & Power Limited 94

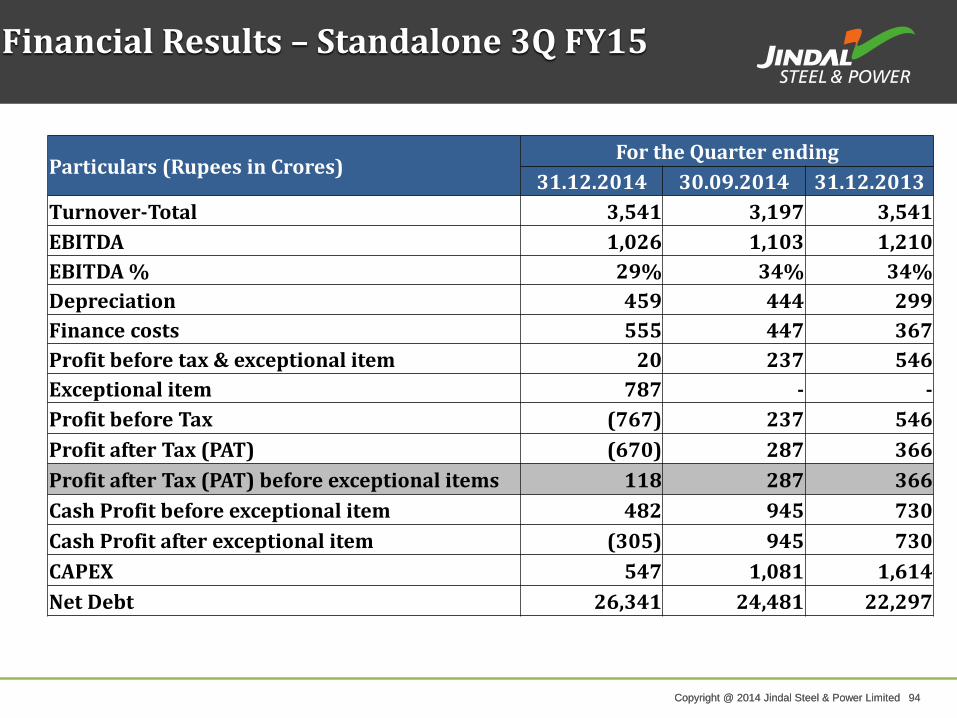

Financial Results – Standalone 3Q FY15

Particulars (Rupees in Crores) For the Quarter ending

31.12.2014 30.09.2014 31.12.2013

Turnover-Total 3,541 3,197 3,541

EBITDA 1,026 1,103 1,210

EBITDA % 29% 34% 34%

Depreciation 459 444 299

Finance costs 555 447 367

Profit before tax & exceptional item 20 237 546

Exceptional item 787 - -

Profit before Tax (767) 237 546

Profit after Tax (PAT) (670) 287 366

Profit after Tax (PAT) before exceptional items 118 287 366

Cash Profit before exceptional item 482 945 730

Cash Profit after exceptional item (305) 945 730

CAPEX 547 1,081 1,614

Net Debt 26,341 24,481 22,297

Copyright @ 2014 Jindal Steel & Power Limited 95 Copyright @ 2014 Jindal Steel & Power Limited 95

Financial Results - Consolidated Q3 FY15

Particulars (Rupees in Crores) For the Quarter ending

31.12.2014 30.09.2014 31.12.2013

Turnover-Total 5,045 5,143 5,142

EBITDA 1,425 1,640 1,701

EBITDA % 28% 32% 33%

Depreciation 715 650 460

Finance costs 702 599 430

Profit before tax & exceptional item 42 431 819

Exceptional item 1,855 - -

Profit before Tax (1,813) 431 819

Profit after Tax (1,675) 400 559

Profit after Tax (PAT) before exceptional items 180 400 559

Cash Profit before exceptional item 946 1,308 1,093

Cash Profit after exceptional item (909) 1,308 1,093

CAPEX 820 1,182 2,548

Net Debt 41,934 37,682 34,127