Embed Size (px)

Citation preview

J. Barrie Shineton President & CEO

January 28, 2011

To our Shareholders, I am pleased to report our first positive earnings since 2006. Norbord generated earnings of $0.39 per share on EBITDA of $105 million in 2010, a meaningful improvement on the breakeven result of the prior year. This reflects much stronger performance from our European business, better OSB prices in North America and higher capacity utilization across all of the Company’s operations. After a slower start in the first quarter, 2010 turned out to be a much better year for Norbord. North American OSB prices improved, particularly in the second quarter when they peaked at almost $400. Panel demand was stronger allowing our North American mills to operate more of their capacity and our European mills to run flat out. Our European operations had an excellent year, generating more than double the cash flow of last year. And we continued to tightly manage working capital, finishing the year at our lowest-ever level. I believe the worst is behind us. Today, we have a strong balance sheet, we are cash flow positive and have successfully managed through the toughest downturn in our industry’s history. Our share price has recovered significantly over the last two years, but it still values Norbord’s assets well below their replacement cost. We have put in place a normal course issuer bid that allows us to buy back up to 5% of our outstanding common shares, a sound investment should our cash flow support it. Norbord’s House is in Order Our balance sheet is solid. Our efforts over the past three years to stabilize our finances are largely complete. We extended our bank lines, added a seventh lender and put in place a more flexible accounts receivable securitization program. Today, we have unutilized bank lines and cash on hand totalling $348 million, which is sufficient liquidity to support our operating initiatives and fund our capital allocation priorities. Our focus as a low-cost OSB producer is sharper. We have continued to streamline our North American operations by exiting non-core businesses. We sold our Deposit MDF mill late in 2009 and we wrote down our investment in the Cochrane hardwood plywood joint venture at year-end. Today, our North American operations consist solely of high-quality, well-located OSB facilities. Continuous improvement drives productivity and margin gains. In 2010, we implemented new resin technology across all of our North American OSB operations. We expect the full benefit of this margin improvement initiative to flow through to our 2011 results through faster line operating speeds, higher sales margins and a richer value-

1

added product mix. Initial feedback from customers suggests that these changes have been well received in the market. Diversified sales minimize exposure to cyclical new home construction. Today, almost two-thirds of Norbord’s North American OSB is directed to home improvement centres and industrial customers and away from the new home construction sector. This diversification strategy has served us well through the downturn, allowing Norbord to operate 70% of its OSB capacity in 2010, compared to the industry-wide operating rate of about 60%. The time is right to re-invest. We appropriately constrained capital investments to minimal levels for the last three years. Now, our improving cash flows and more positive near-term outlook support a modest ramp up in capital spending. A significant project to upgrade our European particleboard assets will be complete by mid-2011, enabling Norbord to reposition its product offering and compete on an equal footing with the newest generation of particleboard capacity. We are closer to our goal of world-class safety performance. Last year, Norbord achieved a best-ever safety incident rate of 0.96. This year, our days lost due to injury - an important injury severity measure - decreased by 80% to just 82 days across the entire company, another best-ever result. Our Guntown, Cordele and Nacogdoches mills achieved Safety Star certifications, a program based on OSHA’s Voluntary Protection Program (VPP). Four more of our facilities will meet this rigorous safety standard in 2011. And both our Cordele and Nacogdoches mills completed their second calendar year without a single recordable injury, an exceptional, industry-leading achievement. Proactive succession planning further strengthens our management team. In September, we promoted Peter Wijnbergen to the newly-created position of Chief Operating Officer with responsibility for our North American operations. As well, Nigel Banks joined our team in November as a successor to Bob Kinnear who will retire from his role as Senior Vice President, Corporate Services this year. Both these appointments ensure organizational continuity as we execute on our strategic priorities. Outlook for 2011 The housing market in North America is improving, but slowly. Experts are not yet predicting a sharp rebound in housing starts and more recently have adjusted their forecasts down, closer to 2010 levels. We expect that overall OSB demand in 2011 will look very similar to last year. Good working capital practices are keeping inventories low across the supply chain. Small changes in either supply or demand are likely to result in ongoing price volatility. It’s my view that the general economic news will improve and unemployment levels will fall throughout this year, leading to better new home construction activity and improving OSB demand and prices in the second half.

2

In Europe, the bull market for OSB peaked late in 2010. However, prices are holding and we expect this positive panel market dynamic to continue well into this year. A favourable exchange rate continues to support our UK-based manufacturing by limiting competing imports and providing a unique opportunity to export our panels to the Continent. We expect to run our European mills at capacity in 2011. There are some industry developments that we are watching closely. In North America, the broader economic recovery could drive higher raw material prices that may be difficult to pass on should the housing recovery lag. In Europe, government biomass energy incentive programs could put further pressure on wood fibre prices. We will continue to ‘push the envelope’ on controllable costs to mitigate this potential input cost risk. Norbord is Well-Positioned The recovery phase of this housing cycle is approaching and Norbord will enter it a stronger company. We have high-quality, low-cost facilities that are running at relatively higher operating rates. We have strong customer partnerships. We have continued to grow our sales with key customers throughout the cyclical downturn. Our European operations are providing meaningful and stable earnings. The long-term fundamentals supporting housing demand are favourable. Norbord is well-positioned to generate superior returns once the recovery takes hold. On behalf of everyone at Norbord, I thank you for your continued support. I look forward to reporting on our progress throughout the year.

This letter includes forward-looking statements, as defined by applicable securities legislation including statements related to our strategy, projects, plans, future financial or operating performance and other statements that express management’s expectations or estimates of future performance. Often, but not always, forward-looking statements can be identified by the use of words such as “believe,” “should,” “expect,” “suggest,” “likely,” “would,” or variations of such words and phrases or statements that certain actions “may,” “could,” “must,” “would,” “might,” or “will” be undertaken, occur or be achieved. Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause the actual results, performance or achievements of Norbord to be materially different from any future results, performance or achievement expressed or implied by the forward-looking statements. See the cautionary language in the Forward-Looking Statements section of the 2010 Management’s Discussion and Analysis dated January 28, 2011.

3

4

News Release NORBORD REPORTS STRONGER 2010 RESULTS; GENERATES POSITIVE EARNINGS ON IMPROVED EBITDA

Note: Financial references in US dollars unless otherwise indicated HIGHLIGHTS

• Achieved positive EBITDA of $105 million vs. break-even in 2009 • European EBITDA more than doubled from $17 million in 2009 to $36 million • Ramped up North American OSB production in improved pricing environment • North Central benchmark OSB price increased 34% vs. the prior year to levels not seen since

2006 • Indicative European OSB price increased 25% from 2009 • Employee days lost due to injury down 80%, a best-ever result TORONTO, ON (January 28, 2011) – Norbord Inc. (TSX: NBD, NBD.WT) today reported positive EBITDA of $105 million versus break-even EBITDA in 2009. The year-over-year improvement is due largely to higher North American OSB and European panel prices and higher shipment volumes. North American OSB generated a year-over-year EBITDA improvement of $90 million driven by strong second quarter results, while Norbord’s European panel operations generated a $19 million year-over-year EBITDA improvement. In the fourth quarter, Norbord recorded positive EBITDA of $13 million versus $12 million in the previous quarter and $6 million in the fourth quarter of 2009. Norbord recorded earnings of $17 million or $0.39 per share (basic) for the full year versus a loss of $58 million or $1.35 per share in 2009. The Company recorded a loss of $2 million or $0.05 per share in the fourth quarter, excluding the impact of a $6 million after-tax or $0.14 per share non-cash write-down of its investment in a non-core business. In the fourth quarter of 2009, the Company incurred a loss of $11 million or $0.25 per share. “Our 2010 results exceeded our expectations,” said Barrie Shineton, President and CEO. “In North America, our customer and product strategy enabled us to run more capacity and to benefit from a stronger pricing environment throughout the year. In Europe, our EBITDA more than doubled on the back of particularly robust OSB markets. While I’m pleased that Norbord generated positive annual earnings for our shareholders this year, we recognize that we still have a long way to go before our financial performance is back to acceptable levels.” “We expect the overall business environment in 2011 to generally mirror Norbord’s experience in the past year. We are seeing the beginnings of a slow recovery for the US housing market, which should start taking hold in the second half of the year. Norbord will be well-positioned to generate stronger results once that occurs.” Market Conditions US housing starts were 0.59 million in 2010, up modestly from 0.55 million in 2009, but significantly below the long-term annual average of 1.5 million. For the full year, the North Central benchmark OSB price averaged $219 per Msf (7⁄16-inch basis) compared to $163 per Msf in 2009. In the South East region, where approximately 55% of Norbord’s

5

North American OSB capacity is located, prices were somewhat lower than in the North Central region, averaging $198 per Msf, compared to $148 per Msf last year. In the fourth quarter, North Central benchmark OSB prices averaged $191, up $11 from the third quarter and up $19 from the fourth quarter of 2009. South East prices averaged $165 in the quarter, up $9 from the third quarter and up $11 from the fourth quarter of 2009. In 2010, the US housing market remained challenging while OSB demand and prices continued to be volatile. The first half of the year saw surging North Central benchmark OSB prices that peaked at $395 per Msf in May before retreating to more sustainable levels in the second half of the year. The first-half price run-up was largely influenced by several unique factors that resulted in overall demand outstripping the ability of both producers and distributors to respond in a timely manner. Second-half housing activity was softer as the May expiry of the US first-time home buyer tax credit pulled home buying demand forward into the first half of the year. In the UK, where the majority of Norbord’s European assets are located, housing starts increased by 30% over 2009 as house builders replenished their inventories of new homes. The European OSB market was particularly robust in 2010, building on the recovery that began at the end of 2009. The 25% year-over-year increase in average indicative OSB prices was driven by firmer end-use demand, inventory re-stocking and substitution for plywood. Particleboard and MDF prices also strengthened during the year, increasing a more modest 5% and 6%, respectively, reflecting the recovery of higher input costs. MDF exports to Continental Europe increased by 46%. Although the Euro weakened somewhat during the year versus the Pound Sterling, the currency remained in a range that continued to benefit Norbord’s UK-based operations. Performance Norbord’s operating North American OSB mills ran at approximately 90% of their capacity in 2010 compared to 80% in 2009. Including the indefinitely closed mills, North American operations ran at 70% of capacity in 2010, compared to 60% in 2009. In Europe, mills operated at approximately 95% of capacity in 2010, up 15% from the previous year. For the full year, Norbord’s North American per unit OSB cash production costs increased 8% over the prior year. The benefit of higher production volume was offset by higher resin and fibre prices, higher supplies and maintenance costs as a result of running more production in 2010, employee profit share payouts, and the foreign exchange impact of the strengthening Canadian dollar. In the fourth quarter, North American per unit OSB cash production costs decreased by 1% over the third quarter of 2010 due to higher production volume and lower key input prices and usages. OSB cash production costs increased by 3% over the fourth quarter of 2009 as improved key input usages and higher production volume were offset by higher resin and fibre prices, supplies and maintenance costs. Resin, fibre and energy, which account for approximately 65% of Norbord’s cash production costs, increased sharply over the five-year period preceding 2009. Margin Improvement Program gains of $16 million in 2010 limited the impact that higher raw material prices had on earnings. At year-end, Norbord had unutilized liquidity of $348 million, comprising $235 million in undrawn revolving bank lines and $113 million in cash and cash equivalents. The Company’s tangible net worth was $352 million and net debt to total capitalization on a book basis was 49%.

6

Capital investments were constrained to essential capital projects totaling $16 million in 2010. Norbord’s 2011 capital investments are planned at $25 million, which includes an infrastructure investment at the Cowie, Scotland particleboard mill that is expected to increase production capacity and reduce manufacturing costs. Developments In January 2011, True North Hardwood Plywood Inc. announced the winding-down of its hardwood plywood operation in Cochrane, Ontario. In the fourth quarter, Norbord recorded a $6 million after-tax ($0.14 per share) non-cash provision for its 50% investment in this business. Additional Information Norbord’s year-end 2010 letter to shareholders, news release, management’s discussion & analysis, annual consolidated audited financial statements and notes to the financial statements have been filed on SEDAR (www.sedar.com) and are available in the investor section of the Company’s website at www.norbord.com. Shareholders are encouraged to read this material. Conference Call Norbord will hold a conference call for analysts and institutional investors on Friday, January 28, 2011 at 11:00 a.m. ET. The call will be broadcast live over the Internet via www.norbord.com and www.newswire.ca. A replay number will be available approximately one hour after completion of the call and will be accessible until February 28, 2011 by dialing 1-888-203-1112 or 647-436-0148. The passcode is 6532094. Audio playback and a written transcript will be available on the Norbord website. Norbord Profile Norbord Inc. is an international producer of wood-based panels with assets of $1.0 billion, employing approximately 2,030 people at 13 plant locations in the United States, Europe and Canada. Norbord is one of the world’s largest producers of oriented strand board (OSB). In addition to OSB, Norbord manufactures particleboard, medium density fibreboard (MDF) and related value-added products. Norbord is a publicly traded company listed on the Toronto Stock Exchange under the symbols NBD and NBD.WT.

-end- Contact: Robin Lampard Senior Vice President & Chief Financial Officer Tel. (416) 365-0705 [email protected]

This news release contains forward-looking statements, as defined in applicable legislation, including statements related to our strategy, projects, plans, future financial or operating performance and other statements that express management’s expectations or estimates of future performance. Often, but not always, words such as “expect,” “should,” “will,” “will not,” “forecasts,” “suggest,” “expects,” “may,” and other expressions which are predictions of or indicate future events, trends or prospects and which do not relate to historical matters identify forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Norbord to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Although Norbord believes it has a reasonable basis for making these forward-looking statements, readers are cautioned not to place undue reliance on such forward-looking information. By its nature, forward-looking information involves numerous assumptions, inherent risks and uncertainties, both general and specific, which contribute to the possibility that the predictions, forecasts and other forward-looking statements will not occur. Factors that could cause actual results to differ materially from those contemplated or implied by forward-looking statements include: general economic conditions; risks inherent with product concentration; effects of competition and product pricing pressures; risks inherent with customer dependence; effects of variations in the price and availability of manufacturing inputs; risks inherent with a capital intensive industry; and other risks and factors described from time to time in filings with Canadian securities regulatory authorities.

7

Except as required by applicable laws, Norbord does not undertake to update any forward-looking statements, whether as a result of new information, future events or otherwise, or to publicly update or revise the above list of factors affecting this information. See the “Caution Regarding Forward-Looking Information” statement in the March 1, 2010 Annual Information Form and the cautionary statement contained in the “Forward-Looking Statements” section of the 2010 Management’s Discussion and Analysis dated January 28, 2011.

Some of the statements included in this MD&A constitute forward-looking statements that are based on various assumptions and are subject to various risks. See the cautionary statement contained in the Forward-Looking Statements section.

8

JANUARY 28, 2011

Management’s Discussion and Analysis

INTRODUCTION This Management’s Discussion and Analysis (MD&A) provides a review of the significant developments that impacted Norbord’s performance during 2010 relative to 2009. The information in this section should be read in conjunction with the audited financial statements, which follow this MD&A.

In this MD&A, “Norbord” means Norbord Inc. and all of its consolidated subsidiaries and affiliates, and “Company” means Norbord Inc. as a separate corporation, unless the context implies otherwise. “Brookfield” means Brookfield Asset Management Inc. or any of its consolidated subsidiaries and affiliates, a related party, by virtue of a controlling equity interest in the Company.

Additional information on Norbord, including documents publicly filed by the Company, is available on the Company’s web site at www.norbord.com or the System for Electronic Document Analysis and Retrieval (SEDAR) at www.sedar.com.

Some of the statements included or incorporated by reference in this MD&A constitute forward-looking statements within the meaning of applicable securities legislation. Forward-looking statements are based on various assumptions and are subject to various risks. See the cautionary statement contained in the Forward-Looking Statements section.

To enhance shareholders’ understanding, certain five-year historical financial and statistical information is presented. Norbord’s significant accounting policies and other financial disclosures are contained in the audited financial statements and accompanying notes, which follow this MD&A. All financial references in the MD&A are stated in US dollars unless otherwise noted.

Earnings before interest, taxes, depreciation and amortization (EBITDA), EBITDA margin, operating working capital, total working capital, capital employed, return on capital employed (ROCE), return on common equity (ROE), net debt, net debt to capitalization on a book basis, and net debt to capitalization on a market basis are non-GAAP financial measures described in the Non-GAAP Financial Measures section. Non-GAAP financial measures do not have any standardized meaning prescribed by Canadian generally accepted accounting principles (GAAP) and are therefore unlikely to be comparable to similar measures presented by other companies. Where appropriate, a quantitative reconciliation of the non-GAAP financial measure to the most directly comparable GAAP measure is also provided.

Some of the statements included in this MD&A constitute forward-looking statements that are based on various assumptions and are subject to various risks. See the cautionary statement contained in the Forward-Looking Statements section.

9

BUSINESS OVERVIEW Norbord is an international producer of wood-based panels with 13 plant locations in North America and Europe.

Norbord is one of the world’s largest producers of oriented strand board (OSB) with an annual capacity of 5 billion square feet (Bsf) (3⁄8-inch basis). The majority of Norbord’s OSB business is located in the South East region of the US. The Company is also a significant producer of wood-based panels in the UK. Norbord does not own any timberlands. Wood fibre is purchased from third parties that include private landowners and government-owned and -managed timberlands. Norbord employed approximately 2,030 people at December 31, 2010.

Operations include 11 OSB mills, 2 particleboard mills, 1 medium density fibreboard (MDF) mill and 1 furniture plant. The Company reports all operations as a single operating segment – wood-based panels.

STRATEGY Norbord’s business strategy is focused entirely on the wood panels sector – in particular OSB – in North America and Europe. Pricing and demand for Norbord’s principal product – OSB – continued to be significantly affected by challenging housing markets. This environment, while not altering the long-term strategy of the business, required management to focus on certain short-term objectives starting in 2008.

In this regard, Norbord accomplished the following in 2010:

Short-Term Strategic Priority

2010 Performance

1. Generate cash. • Achieved EBITDA of $105 million versus break-even EBITDA in 2009.

• Returned North American operations to positive EBITDA of $82 million versus a loss of $8 million in 2009.

• Generated positive EBITDA of $36 million at European operations versus $17 million in 2009.

• Ramped up the Company’s North American and European production capacity by 10% and 15%, respectively, benefitting from higher prices during the year.

• Ongoing minimal investment in operating working capital, achieving lowest-ever year-end levels.

2. Strengthen the balance sheet.

• Added a seventh lender to revolving bank group, increasing committed bank lines to $245 million, and extended term to May 2013.

• Improved bank covenant headroom through generation of $130 million in operating cash flow.

• Replaced existing accounts receivable securitization program with new $85 million evergreen program, containing no financial covenants and subject to a minimum credit-rating requirement of single B(mid).

Some of the statements included in this MD&A constitute forward-looking statements that are based on various assumptions and are subject to various risks. See the cautionary statement contained in the Forward-Looking Statements section.

10

The actions taken by Norbord over the past three years to recapitalize, increase liquidity, reduce losses and conserve cash have stabilized the Company’s balance sheet, which is an important element of Norbord’s ongoing financial strategy.

At the end of the year, the Company had unutilized liquidity of $348 million, net debt to capitalization on a book basis of 49%, and tangible net worth of $352 million. Management believes that its record of superior operational performance and prudent balance sheet management should enable it to access public and private capital markets, subject to financial market conditions. Norbord’s long-term strategic priorities remain unchanged from prior years, and the following table provides updates on the Company’s 2010 achievements in each area:

Long-Term Strategic Priority

2010 Performance

1. Develop a world class safety culture.

• Maintained an industry-leading safety performance with an Occupational Safety and Health Administration (OSHA) recordable rate of 1.43 and a lowest-ever lost-time injury rate of 82 days.

• Completed second OSHA recordable injury-free year at the Cordele, Georgia, and Nacogdoches, Texas, mills.

• Achieved Norbord Safety Star certification at the Cordele, Nacogdoches and Guntown mills.

2. Pursue growth in OSB. • Monitored opportunities to grow OSB business through acquisition.

• Improved operating efficiency at the Genk, Belgium, mill, lowering manufacturing costs and increasing production volume by almost 40%.

3. Own high-quality assets with low-cost positions.

• Implemented new resin technology across North American OSB mills.

• Exited joint venture investment in non-core hardwood plywood business in Cochrane, Ontario.

4. Maintain a margin-focused operating culture.

• Generated margin improvements of $16 million in spite of limited production volume increases.

• Appointed Chief Operating Officer with the mandate to advance the implementation of cost-reduction technologies.

5. Focus on growth customers.

• Increased sales volume to key North American pro-dealer customers by 30%.

• Increased North American value-added product sales volume by 40%.

• Increased UK MDF exports by over 45%.

• Limited exposure to new home construction segment through end-use diversity.

6. Allocate capital with discipline.

• Limited capital investments to essential projects totalling $16 million.

• Put normal course issuer bid in place, enabling Norbord to purchase up to 5% of its outstanding Common Shares.

Some of the statements included in this MD&A constitute forward-looking statements that are based on various assumptions and are subject to various risks. See the cautionary statement contained in the Forward-Looking Statements section.

11

SUMMARY

(US $ millions, except per share information, unless otherwise noted) 2010 2009 2008 2007 2006

KEY PERFORMANCE METRICS

Return on capital employed (ROCE) 13% 0% (6)% 4% 25% Return on equity (ROE) 5% (19)% (37)% (11)% 20% Cash provided by (used for) operating activities 130 (35) (13) 15 191 Cash provided by (used for) operating activities per share 3.00 (0.82) (0.86) 1.03 13.36

NET SALES AND EARNINGS Net sales 892 718 943 1,104 1,252 EBITDA 105 0 (60) 42 247 Earnings 17 (58) (115) (45) 97

PER COMMON SHARE EARNINGS

Basic 0.39 (1.35) (7.62) (3.10) 6.76 Diluted 0.38 (1.35) (7.62) (3.10) 6.74 Common dividends 0 0 3.68 3.80 12.47

Total assets 1,062 1,043 1,044 1,404 1,299 Long-term debt 443 471 542 480 480 Net debt 337 454 477 547 460 Net debt to capitalization, market basis 35% 48% 32% 30% 27%Net debt to capitalization, book basis 49% 58% 61% 60% 51%

Shipments (MMsf–3⁄8") North America 2,989 2,780 3,624 3,947 3,932 Europe(1) 1,298 1,158 1,348 1,712 1,603 Indicative OSB pricing Average OSB price

North Central ($/Msf–7⁄16") 219 163 172 161 217 South East ($/Msf–7⁄16") 198 148 143 143 219

Europe (€/m3) 210 168 203 240 208 (1) Excludes product consumed internally (108 MMsf, 127 MMsf, 114 MMsf, 138 MMsf, 178 MMsf for each period, respectively).

Markets remained challenging as high unemployment and limited mortgage availability continued to delay a meaningful recovery in both US and UK housing demand in 2010. Notwithstanding this environment of continued low demand, prices for the Company’s products were firmer in both North America and Europe, and Norbord generated significantly improved financial results this year.

Fluctuation in North American structural panel demand and OSB prices are significant variables affecting Norbord’s results. North American OSB prices were very volatile during the year, ranging from $160 to $395 per thousand square feet (Msf) (North Central 7⁄16-inch basis), averaging $219 per Msf compared to $163 per Msf in the prior year. Norbord benefited from these higher prices by running more of its capacity during the year, operating at 70% of capacity compared to 60% in 2009.

Norbord achieved EBITDA of $105 million in 2010 versus break-even EBITDA in 2009. EBITDA margins for 2010 were 12%, compared to 0% for the prior year. 2010 earnings were $17 million or $0.39 per share (basic) versus a loss of $58 million or $1.35 per share in 2009. Pre-tax ROCE averaged 13% compared to 0% in the prior year. ROCE is a measurement of financial performance, focusing on cash generation and the efficient use of

Some of the statements included in this MD&A constitute forward-looking statements that are based on various assumptions and are subject to various risks. See the cautionary statement contained in the Forward-Looking Statements section.

12

capital. As Norbord operates in a cyclical commodity business, it interprets ROCE over the cycle as a useful means of comparing businesses in terms of efficiency of management and viability of products. Through this five-year cyclical trough, Norbord has generated an average annual ROCE of 7%.

Higher product prices and sales volume in both North America and Europe were the key drivers of the EBITDA improvement in 2010. Norbord’s North American OSB operations achieved six consecutive quarters of positive EBITDA, with the second quarter posting the strongest result since 2006. Norbord’s European operations generated more than double the prior year’s EBITDA, which resulted from particularly robust OSB prices this year.

Over the past five years, $288 million in cash has been generated from operating activities and $200 million in cash has been generated from recapitalization activities. This cash has been used to reshape the Company from its historic role as a diversified Canadian forest products company into an internationally recognized leader in the structural panel industry. During this time, Norbord invested $253 million in capital expenditures primarily focused on growing the business, and paid out approximately $232 million in cash dividends, including special dividends, to shareholders.

Markets are expected to remain volatile in 2011 as global economies reposition for recovery. The past three years have seen the worst housing downturn in several generations, and the Company focused on preserving cash and stabilizing its balance sheet. This year, Norbord generated significant positive operating cash flow and strengthened its balance sheet. The Company is well positioned to benefit from recovering housing markets. Over the long term, the underlying demographics will continue to support robust demand for new homes. Further, management believes that Norbord’s North American and European operations provide meaningful market and geographic diversification over the cycle, while capitalizing on Norbord’s strength as a panel producer.

OUTLOOK FOR 2011 Norbord operates in extremely volatile markets and expects the overall business environment in 2011 to generally mirror that of 2010. Housing markets are expected to begin showing meaningful signs of improvement in the second half of 2011 as the structural impediments to recovery are worked through.

High unemployment and competition from foreclosures remain the biggest structural hurdles to a recovery in the US housing market. While the market works through these issues, significant OSB industry supply remains curtailed through indefinite mill closures. Norbord’s two indefinitely closed mills, in Texas and Alabama, will not operate until signs of a sustainable recovery in housing starts are visible. Industry experts are forecasting 2011 US housing starts of around 0.68 million. On the positive side, new home inventories remain very low, and affordability is at generational highs. Norbord is of the view that, once the economy finds its footing and the foreclosure overhang subsides, new household formation trends will ultimately support a return to the long-term annual average of 1.5 million housing starts.

In the UK, the government is implementing the most significant public sector spending cuts since the World War II. While the impact on European panel markets is not yet clear, Norbord believes its European business outlook remains relatively buoyant. Pent-up demand for new homes continues to grow, and Norbord expects the Pound Sterling, relative to the Euro, to remain in a range that is supportive of its UK-based manufacturing. This currency advantage limits UK imports and provides further export opportunities on the Continent.

On the input cost side, global commodity prices that troughed in 2009 recovered in 2010. Unlike previous economic cycles, the overall economy appears likely to lead a housing sector recovery in this cycle. Improving demand for global commodities could put upward pressure on resin and wax prices that panel producers may not be able to pass on to customers. In addition, western European government incentives for biomass energy expansion are putting upward pressure on European fibre prices. Norbord continues to pursue Margin Improvement Program (MIP) initiatives to mitigate potentially higher uncontrollable costs.

Some of the statements included in this MD&A constitute forward-looking statements that are based on various assumptions and are subject to various risks. See the cautionary statement contained in the Forward-Looking Statements section.

13

After constraining capital expenditures at minimal levels for the past three years, Norbord expects to modestly increase capital investments to $25 million in 2011. Projects that improve Norbord’s product offerings and cost position will be prioritized. Norbord has strong financial liquidity, and no debt maturities in 2011. Combined with the Company’s solid customer partnerships and favourable European market dynamics, Norbord is well positioned for the recovery in housing markets and will benefit from stronger OSB demand in the years ahead.

RESULTS OF OPERATIONS

(US $ millions) 2010 2009 2008 2007 2006

Net sales $892 $718 $943 $1,104 $1,252 EBITDA 105 0 (60) 42 247 EBITDA margin 12% 0% (6)% 4% 20% Depreciation 45 48 68 88 94 Investment in property, plant and equipment 16 14 27 36 160

Shipments (MMsf–3⁄8")(1) 4,287 3,938 4,972 5,659 5,535 Indicative OSB pricing Average OSB price

North Central ($/Msf–7⁄16") 219 163 172 161 217 South East ($/Msf–7⁄16") 198 148 143 143 219 Europe (€/m3) 210 168 203 240 208

(1) Excludes product consumed internally (108 MMsf, 127 MMsf, 114 MMsf, 138 MMsf, 178 MMsf for each period, respectively).

Markets North America is the principal market destination for Norbord’s products. North American OSB comprises 70% of Norbord’s panel shipments by volume. Therefore, results of operations are most affected by volatility in North American OSB prices. European panel prices are less volatile than North American prices, and Europe comprises just 30% of Norbord’s shipments by volume, affecting Norbord’s results to a lesser degree.

Shipments (MMsf–3⁄8") 2010 2009 2008 2007 2006

North America 2,989 2,780 3,624 3,947 3,932 Europe(1) 1,298 1,158 1,348 1,712 1,603 Total 4,287 3,938 4,972 5,659 5,535

(1) Excludes product consumed internally (108 MMsf, 127 MMsf, 114 MMsf, 138 MMsf, 178 MMsf for each period, respectively).

North America The US housing market remained challenging, with periods of price volatility during 2010. The first half of the year saw surging North Central benchmark OSB prices that peaked at $395 per Msf (7⁄16-inch basis) in May before retreating to more sustainable levels in the second half of the year. The first-half price run-up was largely influenced by several unique factors that resulted in overall demand outstripping the ability of both producers and distributors to increase supply. Second-half housing markets were softer as the expiry of the US first-time home buyer tax credit in May pulled home buying demand forward into the early part of the year.

The North Central benchmark OSB price averaged $219 per Msf (7⁄16-inch basis) in 2010 compared to $163 per Msf in 2009. In the South East region, where approximately 55% of Norbord’s North American OSB capacity is located, prices were somewhat lower than in the North Central region, averaging $198 per Msf, compared to $148 per Msf last year.

Some of the statements included in this MD&A constitute forward-looking statements that are based on various assumptions and are subject to various risks. See the cautionary statement contained in the Forward-Looking Statements section.

14

New home construction is still the primary end use for OSB in North America, accounting for approximately 50% of OSB demand in 2010. US housing starts were 0.59 million in 2010, up modestly from 0.55 million in 2009, but still significantly below the long-term annual average of 1.5 million. To put the decline into context, 100,000 housing starts represent approximately 1 Bsf (⅜-inch basis) of OSB demand. It is important to note that approximately 40% of Norbord’s OSB sales volume goes directly into the new home construction sector, while the other 60% goes into repair and remodelling, light commercial construction and industrial applications. Management believes that this limits the Company’s relative exposure to the new home construction segment and provides meaningful distribution channel benefits.

According to APA – The Engineered Wood Association, North American OSB demand was modestly higher in 2010, at approximately 15.3 Bsf (⅜-inch basis) versus 14.1 Bsf in 2009, representing almost 60% of total North American structural panel demand and 57% of industry OSB production capacity. Against this backdrop of modestly improved demand, Norbord’s North American OSB mills operated at approximately 70% of capacity in 2010, compared to 60% in 2009.

Europe European panel markets showed increasing strength throughout 2010 as housing construction activity picked up and repair and remodelling demand remained robust. In the UK, where the majority of Norbord’s European assets are located, housing starts increased by 30% over 2009 despite eroding consumer confidence throughout the year. In Germany, Norbord’s largest Continental market, housing starts were up a more modest 8% over 2009, while consumer confidence rose to its highest level in a decade. In this firmer-demand environment, Norbord’s European mills operated at 95% of capacity throughout the year, compared to 80% in 2009, with the two OSB mills running at full capacity.

The European OSB market was particularly robust in 2010, building on the recovery started at the end of 2009 and supporting a 25% year-over-year increase in indicative OSB prices (denominated in Euros). OSB market strength was driven by firmer end-use demand, inventory re-stocking and substitution for plywood. Particleboard and MDF prices also recovered during the year, increasing a more modest 5% and 6%, respectively, reflecting the recovery of higher input costs.

Although the Euro weakened somewhat during the year versus the Pound Sterling, the currency remained in a range that continued to benefit Norbord’s primarily UK-based operations. Particularly noteworthy was a 46% increase in MDF exports to the Continent.

Net Sales

(US $ millions) 2010 2009 2008 2007 2006

North America $541 $406 $538 $593 $823 Europe 351 312 405 511 429 Total $892 $718 $943 $1,104 $1,252

Consolidated net sales rose by $174 million or 24% in 2010 compared to 2009. North American sales increased by 33%, and European panel sales increased by 13%. In North America, the sales increase was driven by higher OSB prices in the first and second quarters of 2010 combined with a 12% increase in OSB shipment volume. Average North Central and South East OSB benchmark prices per Msf (7⁄16-inch basis) increased by $56 and $50, respectively, in 2010, which is an increase of 34% compared to 2009. In Europe, the sales increase was driven by higher panel prices and shipment volumes across all products. European panel shipment volumes increased by 13% for OSB, 7% for particleboard and 8% for MDF.

Some of the statements included in this MD&A constitute forward-looking statements that are based on various assumptions and are subject to various risks. See the cautionary statement contained in the Forward-Looking Statements section.

15

Production

(MMsf–3⁄8") 2010 2009 2008 2007 2006

North America 2,993 2,785 3,645 4,268 3,987 Europe 1,437 1,266 1,332 1,704 1,738 Total 4,430 4,051 4,977 5,972 5,725

Norbord continued to curtail production in 2010 to maximize earnings and manage inventory levels. Notwithstanding, total production volume increased by 9% or 379 MMsf (⅜-inch basis). North America North American production volume increased by 7% or 208 MMsf (⅜-inch basis) in 2010, driven by an 11% increase in OSB production volume compared to 2009. Norbord’s newest OSB line in Cordele, constructed in 2006, established a company-wide production record in the year, with volume exceeding design expectations.

In 2009, OSB production volume decreased by approximately 25% in North America compared to 2008. In January 2009, Norbord announced that indefinite shutdowns would take place at its OSB mills in Huguley, Alabama, and Jefferson, Texas. These two mills represent approximately 20% of Norbord’s annual OSB production capacity in North America. Subject to market conditions, Norbord does not expect to restart these two mills in the near term. In June 2009, Norbord reduced production schedules at the original line in Cordele and at Guntown. In total, approximately 270 employees were affected by these decisions. In March 2010, Norbord returned the Guntown mill to a full production schedule. From March to August 2010, Norbord returned the Cordele line to a full production schedule and then ran the mill at a reduced work week for the rest of the year. Weak market conditions and reduced demand were the primary drivers for these decisions, which were made out of a necessity to contain costs and manage operating working capital.

Norbord’s operating North American OSB mills ran at approximately 90% of their capacity in 2010, compared to 80% in 2009. Including the indefinitely closed mills, Norbord’s North American OSB mills operated at approximately 70% of capacity in 2010, compared to 60% in 2009.

In 2010, production at the hardwood plywood joint-venture operation in Cochrane ceased, and in 2009, the Company sold its MDF mill in Deposit, New York (see Investments and Divestitures). Together, these two non-core North American operations represented, on average, less than 5% of Norbord’s North American production volume in each respective year prior.

In 2007, North American OSB production included the ramp-up of the new OSB line in Cordele. Europe European panel production volume increased by 14% or 171 MMsf (⅜-inch basis) in 2010. Production volume increased by 24% for OSB, 13% for MDF and 1% for particleboard. Norbord’s OSB mill in Genk ran on a full production schedule in 2010, which, when combined with significantly improved production efficiency, increased production volume by approximately 40% year-over-year.

In 2009, European panel production volume decreased by 5% or 66 MMsf (⅜-inch basis) compared to 2008. Production volume decreased by 3% for OSB, 12% for MDF and 5% for particleboard. In March 2008, a particleboard line at Genk was closed permanently. The particleboard line was considered non-core as the Genk site was acquired to expand Norbord’s OSB presence in Europe.

In Europe, mills operated at approximately 95% of capacity in 2010, compared to 80% in 2009.

Some of the statements included in this MD&A constitute forward-looking statements that are based on various assumptions and are subject to various risks. See the cautionary statement contained in the Forward-Looking Statements section.

16

Operating Results

EBITDA (US $ millions) 2010 2009

North America $82 $(8)Europe 36 17Unallocated (13) (9)Total $105 $0

Norbord achieved EBITDA of $105 million in 2010, compared to break-even EBITDA in 2009. North American OSB generated EBITDA of $84 million, compared to negative $6 million in the prior year, marking a year-over-year improvement of $90 million. Other North American products generated EBITDA of negative $2 million in 2010 and 2009. Norbord’s European panel operations generated EBITDA of $36 million, which is a year-over-year improvement of $19 million. Unallocated costs were $13 million in 2010 compared to $9 million in 2009, an increase of $4 million primarily due to the foreign exchange impact of the strengthening Canadian dollar. North America Norbord’s North American OSB operations delivered positive EBITDA results in each quarter of 2010. The EBITDA improvement of $90 million in 2010 was driven by strong second quarter results. EBITDA generated in the second quarter of 2010 was $64 million compared to negative $6 million in the second quarter of 2009, which represents a year-over-year improvement of $70 million that can be attributed primarily to higher prices. North Central OSB benchmark prices peaked at $395 per Msf (7⁄16-inch basis) in the second quarter, a price level not experienced since 2005. The upward momentum commenced in the first quarter of 2010. Prices rose against the backdrop of cold and wet weather conditions in the Southern US, which affected log availability and impacted operating schedules. Demand was seasonally firmer in the second quarter, and the expiry of the US first-time home buyer tax credit in May generated a pull-forward effect on demand earlier in 2010. During the year, OSB price volatility was extreme as prices climbed quickly in the second quarter and then declined dramatically during the remainder of 2010. On the cost side, higher raw material prices impacted operating costs. Resin and fibre prices, which were at cycle-bottom levels in 2009, climbed in the first half of 2010 and then leveled off for the remainder of the year. Europe Norbord’s European operations experienced stronger results in each quarter of 2010 compared to 2009. EBITDA results more than doubled from $17 million in 2009 to $36 million in 2010. Higher European panel prices and higher shipment volumes contributed to the improved year-over-year results, despite the continuing input cost pressures, particularly related to fibre. In Europe, the average indicative OSB price (denominated in Euros) increased by 25%, and particleboard and MDF prices increased by 5% and 6%, respectively. European panel shipment volumes increased by 13% for OSB, 7% for particleboard and 8% for MDF. European OSB markets continued to show increasing strength throughout the year in response to some short-term recovery in new home construction, resilient repair and remodelling demand, substitution for scarce plywood and inventory re-stocking. In addition, OSB supply was constrained by curtailments early in the year as a result of weather-related wood shortages, particularly in Continental Europe. The weak Pound Sterling relative to the Euro continued to be advantageous for Norbord, as it improved sales opportunities within the UK and slowed the flow of Continental European imports. This currency trend also supported Norbord’s export program to the Continent.

Some of the statements included in this MD&A constitute forward-looking statements that are based on various assumptions and are subject to various risks. See the cautionary statement contained in the Forward-Looking Statements section.

17

The components of the EBITDA change are summarized in the variance table below.

EBITDA Variance (US $ millions) 2010 vs. 2009

EBITDA – current period $105EBITDA – comparative period 0

Variance $105

Mill nets(1) $151Volume(2) 19 Key input prices(3) (34) Key input usage(3) (2) Other(4) (35) Production curtailment, net(5) 6 Total $105

(1) The mill nets variance represents the change in realized pricing across all products. Mill nets are calculated as net sales divided by shipment volume.

(2) The volume variance represents the impact of shipment volume changes across all products. (3) The key inputs include fibre, resin and energy. (4) The other category covers all remaining variances including labour and benefits, supplies and maintenance, and the impact of foreign exchange. (5) The production curtailment, net, represents the net EBITDA variance impact related to the indefinite curtailment of North American OSB mills in

Jefferson and Huguley.

Higher North American OSB and European panel prices improved Norbord’s results by $151 million in 2010. In addition, higher shipment volumes in both North America and Europe added $19 million to EBITDA in 2010. Housing market activity, particularly in the US, influences OSB demand and pricing. Fluctuation in North American OSB demand and prices significantly affects Norbord’s results. US housing starts modestly improved by 7% year-over-year, from 0.55 million starts in 2009 to 0.59 million in 2010. Higher mill nets in 2010 reflected the benefits of diversified distribution channels, low inventories in the supply chain, slightly firmer demand as a result of the US stimulus tax incentive which ended in May, and extremely wet weather conditions in the Southern US at the beginning of the year. In the UK, government stimulus programs generated an improvement in construction activity that supported stronger panel pricing, particularly for OSB. Overall, Norbord’s European operations benefited from underlying robust demand dynamics resulting from the weak Pound Sterling and limited imports.

On the cost side, the benefit of lower global commodity prices was experienced for most of 2009, resulting in cycle-bottom prices. Resin and energy prices increased in the first half of 2010 and then leveled off for the remainder of the year. The direct impact on operating costs of rising energy prices continues to be limited since all of Norbord’s heat energy for OSB operations is generated from biomass. Norbord’s reduced reliance on fossil fuels has generated significant energy-cost savings in both North America and Europe. Further, the ability of Norbord’s European mills to comply with Kyoto Protocol energy-efficiency targets has resulted in a surplus of carbon credits, which have been monetized on environmental exchanges.

Fibre prices in both North America and Europe increased in 2010 compared to 2009. In the first quarter of 2010, extremely cold and wet weather conditions affected fibre availability and prices. North American fibre prices moderated slowly throughout the rest of the year. European fibre prices remained under pressure due to the impact of government biomass energy incentives. Norbord does not own any timberlands; therefore, it purchases timber, wood chips and fibre as well as other wood recycled materials on the open market, in competition with other users of such resources, where prices are influenced by factors beyond Norbord’s control.

Resin, fibre and energy, which account for approximately 65% of Norbord’s cash production costs, increased sharply over the five-year period preceding 2009. MIP gains of $16 million in 2010, measured relative to 2009 at

Some of the statements included in this MD&A constitute forward-looking statements that are based on various assumptions and are subject to various risks. See the cautionary statement contained in the Forward-Looking Statements section.

18

constant prices and exchange rates, limited the impact that higher raw material prices had on earnings in 2010. Contributions to MIP included an added-value product mix, improved production efficiencies and key input usage reduction initiatives. In addition, cost-reduction initiatives undertaken on controllable and discretionary expenses resulted in lower overhead costs over the past two years, despite running more production capacity in 2010.

In 2010, Norbord’s North American per unit OSB production costs increased 8% over the prior year. The benefit of higher production volume was offset by the negative impact of higher resin and fibre prices (which were at cycle-bottom lows in 2009), higher supplies and maintenance costs as a result of running more production in 2010, higher employee profit share costs, and the foreign exchange impact of the strengthening Canadian dollar. Norbord’s European operations are disproportionately impacted by rising resin and global energy prices because the products are more resin and energy intensive. A number of initiatives have been undertaken to address these cost pressures, including the permanent closure of a particleboard line at the Genk site in 2008, and the installation of biomass heat energy systems at Genk OSB and Cowie, Scotland, MDF in 2007.

INTEREST, DEPRECIATION AND INCOME TAX

(US $ millions) 2010 2009 2008 2007 2006

Interest and other income $– $– $3 $5 $3 Interest expense (34) (36) (49) (49) (29) Depreciation (45) (48) (68) (88) (94) Income tax recovery (expense) (3) 33 95 45 (17)

Interest In 2007, the Company had higher average cash balances arising principally from the $200 million issue of senior notes completed in 2007 to pre-fund the 2008 debenture maturity.

Interest expense was $2 million lower in 2010 compared to 2009 due to lower average drawings on revolving bank lines. Interest expense was $13 million lower in 2009 compared to 2008 due to three main factors. First, Norbord paid down borrowings under the Company’s committed revolving bank lines and Brookfield debt facility with proceeds from the Rights Offering completed in the first quarter of 2009. Second, average interest rates in 2009 were lower than 2008 due to low US Federal Reserve rates. And third, interest was higher in 2008 due to the 8⅛% debentures repurchased in the first quarter of 2008.

The effective interest rate on Norbord’s debt-related obligations, including the impact of interest rate swaps, was 6.2% as at December 31, 2010, compared to 6.1% as at prior year-end. Approximately 1% of Norbord’s net debt was subject to floating interest rates during the year, compared to 32% in the prior year, because of the significant cash balances accumulated during 2010.

From time to time, the Company can recoupon its portfolio of interest rate swaps to more efficiently manage cash flow and credit exposure. Any gains or losses realized are deferred and amortized over the remaining term of the debt against which the swaps were designated as hedges. As at December 31, 2010, $3 million in gains were deferred and included in the carrying value of long-term debt in the consolidated balance sheet. Amortization of $3 million in 2010, and $2 million in 2009, was included in interest expense.

Depreciation Depreciation expense in 2010 was lower than 2009 due to the prospective change in estimate in the depreciation of production equipment from the straight-line to units of production methodology, effective March 29, 2009 (see Significant Accounting Policies and Estimates). The units of production depreciation methodology provides a more rational and systematic cost allocation, as the fluctuation in depreciation expense reflects changes in mill production levels. The impact of this change in estimate resulted in a reduction in depreciation expense of $12

Some of the statements included in this MD&A constitute forward-looking statements that are based on various assumptions and are subject to various risks. See the cautionary statement contained in the Forward-Looking Statements section.

19

million in 2009. Continued fluctuating production volumes and the indefinite closure of the Jefferson and Huguley OSB mills triggered this change.

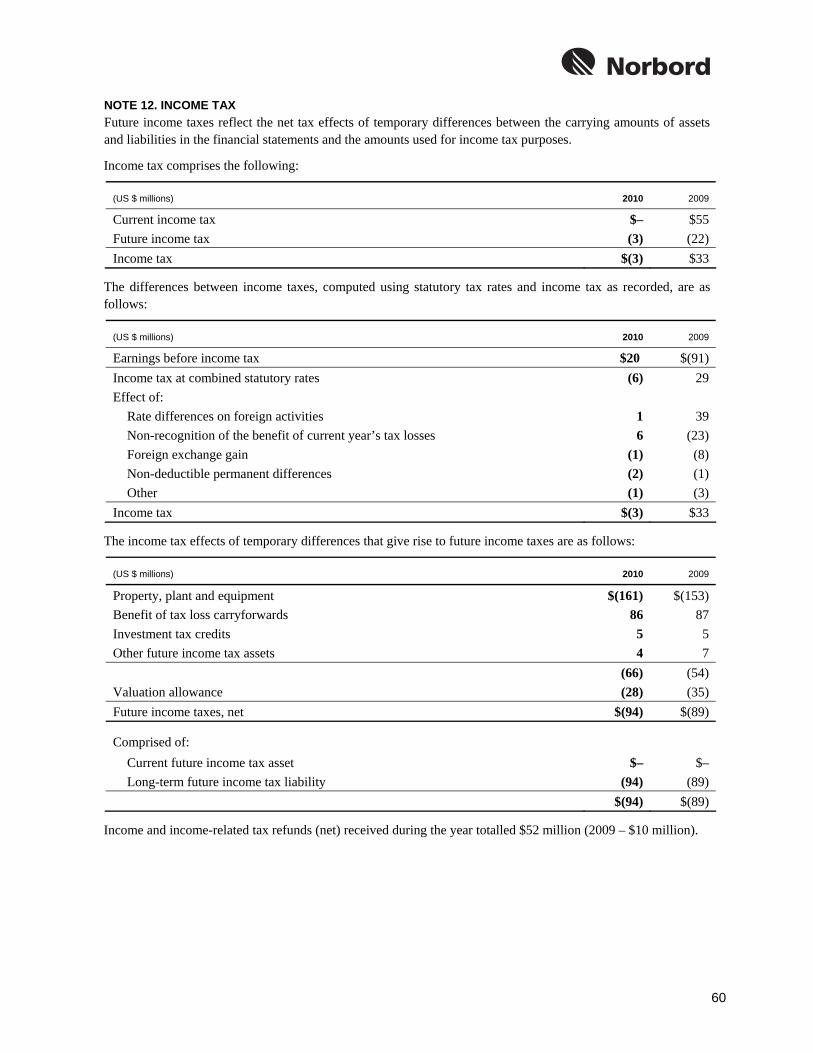

Income Tax A tax expense of $3 million was recorded in 2010 on pre-tax income of $20 million. The effective tax rate of 15% is lower than the statutory rate due principally to rate differences on foreign activities and fluctuations in relative currency values. In 2009, the Company recorded an income tax recovery of $8 million ($0.19 per share) related to the recognition of a future income tax asset previously charged to retained earnings in the fourth quarter of 2008, due to Brookfield’s acquisition of control.

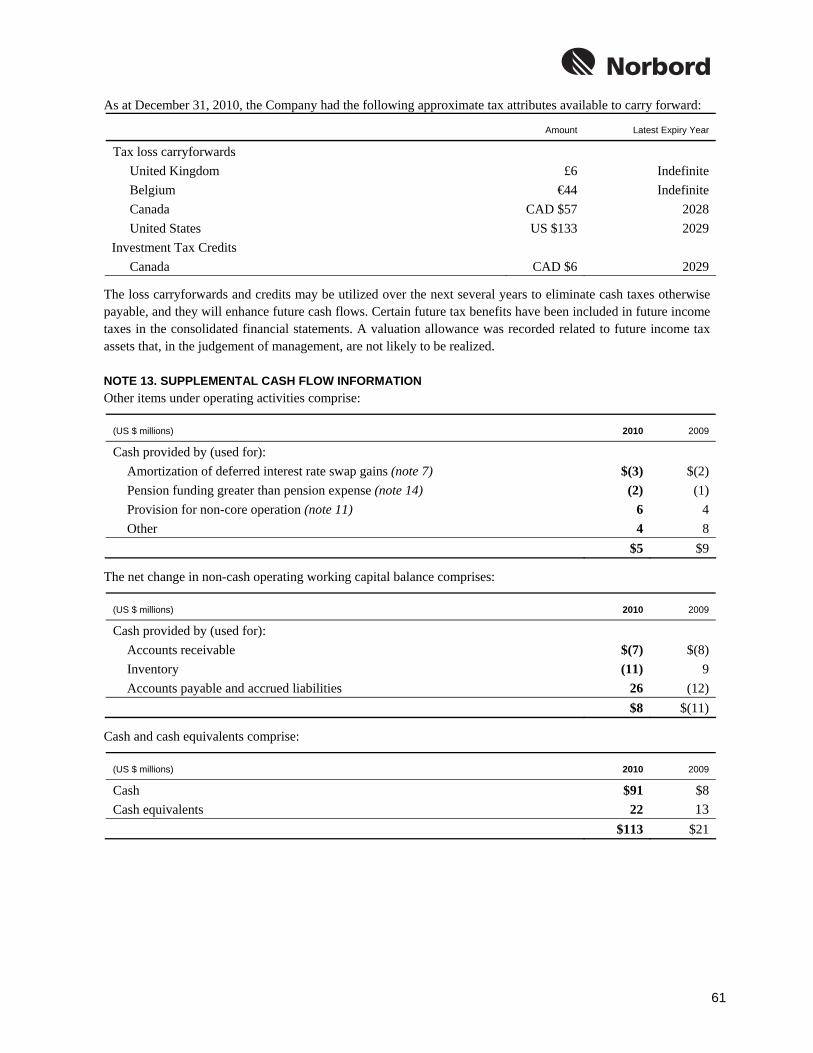

From 2004 to 2006, Norbord paid $234 million in income and income-related taxes, principally in North America. In 2010, 2009, 2008 and 2007, the Company received tax refunds of $52 million, $10 million, $85 million and $33 million, respectively, related to losses carried back and over installments.

At December 31, 2010, the Company had tax operating loss carryforwards of approximately £6 million and €44 million from operations in the UK and Belgium, respectively. These losses can be carried forward indefinitely to offset future taxable income. The Company has tax operating losses of CAD $57 million and US $133 million from operations in Canada and the US, respectively, which expire between 2028 and 2029. The Company also has approximately CAD $6 million worth of Investment Tax Credits (ITCs) available to reduce future Canadian tax liabilities. The ITCs expire between 2021 and 2029. The loss carryforwards and credits may be utilized over the next several years to eliminate cash taxes otherwise payable, and will enhance future cash flows. Certain future tax benefits have been included in future income taxes in the consolidated financial statements. A valuation allowance was recorded related to future income tax assets that, in the judgement of management, are not likely to be realized.

LIQUIDITY AND CAPITAL RESOURCES

(US $ millions, except per share information, unless otherwise noted) 2010 2009 2008 2007 2006

Cash provided by (used for) operating activities $130 $(35) $(13) $15 $191Cash provided by (used for) operating activities per share 3.00 (0.82) (0.86) 1.03 13.36

Operating working capital (57) (42) (53) 23 –Total working capital 62 36 (20) 240 53 Investment in property, plant and equipment 16 14 27 36 160Net debt to capitalization, market basis 35% 48% 32% 30% 27%Net debt to capitalization, book basis 49% 58% 61% 60% 51%

At year-end, the Company had unutilized liquidity of $348 million, comprising $235 million in revolving bank lines and $113 million in cash and cash equivalents. Norbord has no investments in, or other direct exposure to, US sub-prime mortgages, US auction rate securities or Canadian asset-backed commercial paper.

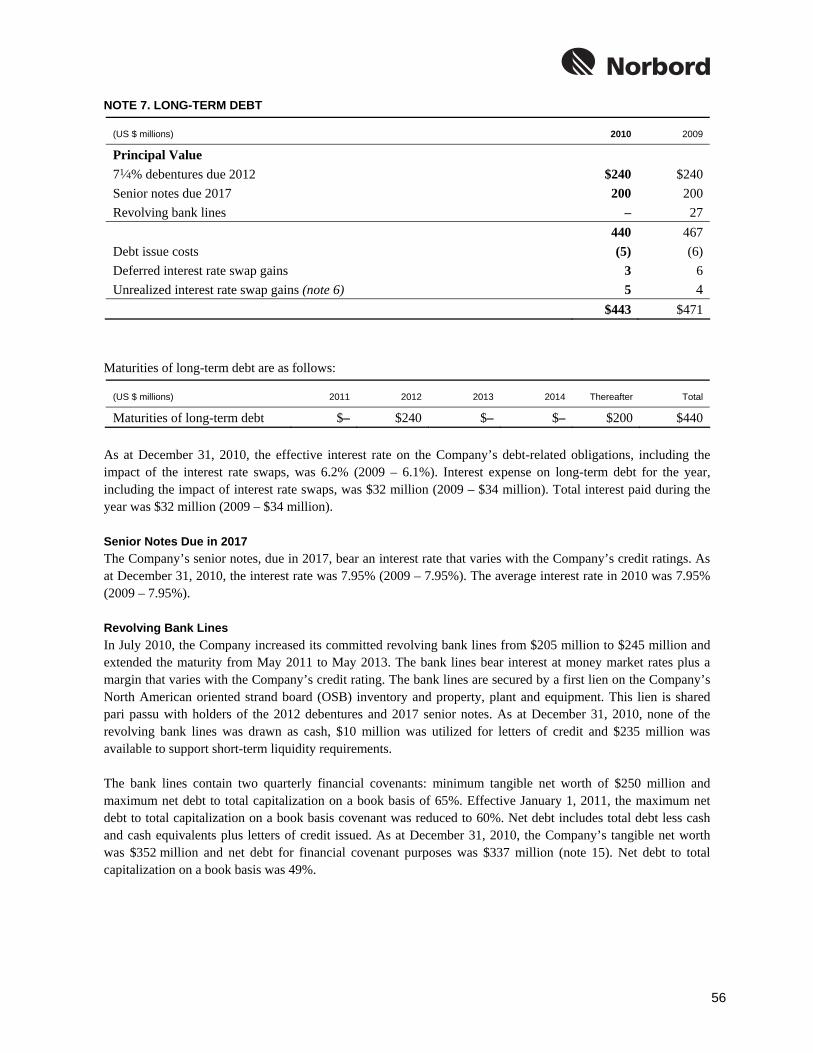

The Company’s outstanding long-term debt has a weighted average term of 3.6 years. Norbord’s net debt for financial covenant purposes stood at $337 million at December 31, 2010, which includes long-term debt of $440 million less cash and cash equivalents of $113 million plus letters of credit of $10 million.

Revolving Bank Lines In July 2010, the Company completed amendments to its committed revolving bank lines. Under the amended terms, the aggregate commitment was increased from $205 million to $245 million, and the maturity was extended from May 2011 to May 2013. The bank lines bear interest at money market rates plus a margin that varies with the Company’s credit rating. The bank lines are secured by a first lien on the Company’s North

Some of the statements included in this MD&A constitute forward-looking statements that are based on various assumptions and are subject to various risks. See the cautionary statement contained in the Forward-Looking Statements section.

20

American OSB inventory and property, plant and equipment. This lien is shared pari passu with holders of the 2012 debentures and 2017 senior notes.

The bank lines contain two quarterly financial covenants: minimum tangible net worth of $250 million and maximum net debt to total capitalization on a book basis of 65%. Effective January 1, 2011, the maximum net debt to total capitalization on a book basis covenant was reduced to 60%. Net debt includes total debt less cash and cash equivalents plus letters of credit issued. As at December 31, 2010, the Company’s tangible net worth was $352 million and net debt for financial covenant purposes was $337 million. Net debt to total capitalization on a book basis was 49%.

As at December 31, 2010, none of the revolving bank lines was drawn as cash, $10 million was utilized for letters of credit and $235 million was available to support short-term liquidity requirements.

Brookfield Debt Facility Concurrent with the amendments made to the revolving bank lines described above, the Company cancelled the $50 million Brookfield debt facility, which was undrawn. The facility bore interest equal to the greater of 8% or US base rate plus ½%, and was subordinated to the revolving bank lines. Any drawings under the facility were treated as tangible net worth for financial covenant purposes. The standby fee on the facility was less than $1 million in 2010 (2009 – less than $1 million).

Other Liquidity and Capital Resources Operating working capital, consisting of accounts receivable and inventory less accounts payable and accrued liabilities, decreased by $15 million during the year to negative $57 million at year-end, compared to negative $42 million at December 31, 2009. Operating working capital decreased due to higher accounts payable, partially offset by higher inventory and accounts receivable. The overall decrease is attributed to fewer production curtailments taken towards the end of 2010 compared to the prior year. The Company aims to minimize the amount of capital held as operating working capital and continued to manage it at minimal levels throughout the year.

The 2010 and 2009 accounts receivable balances are net of $60 million and $62 million, respectively, of accounts receivable sold under a securitization facility (see Off Balance Sheet Arrangements). The $85 million facility, with a third-party trust sponsored by a highly rated Canadian financial institution, commenced in June 2010 and replaced an existing program. Despite the challenging economic environment, Norbord’s accounts receivable performance metrics remain in line with prior periods.

Total working capital, which includes operating working capital plus cash and cash equivalents and income tax receivable, was $62 million as at December 31, 2010, compared to $36 million in the prior year. The increase is attributed to a higher cash balance generated from operations and the collection of $52 million in cash tax refunds, partially offset by lower operating working capital.

Operating activities provided $130 million in cash or $3.00 per share in 2010, compared to the consumption of $35 million or $0.82 per share in 2009. In 2010, positive EBITDA from operations, the reduction of operating working capital and the receipt of $52 million in cash tax refunds more than offset the interest paid on debt. In 2009, interest expense and an increase in operating working capital were partially offset by $10 million in cash tax refunds.

On November 10, 2008, the Company announced the suspension of quarterly dividend payments on its common shares until further notice. No dividends were paid in 2009 or 2010.

The Company realized a gain of $6 million on its matured net investment hedges in 2010, compared to a loss of $2 million in 2009. The realized gain and loss were offset by an unrealized loss and gain on the net investments being hedged.

Some of the statements included in this MD&A constitute forward-looking statements that are based on various assumptions and are subject to various risks. See the cautionary statement contained in the Forward-Looking Statements section.

21

The following table summarizes the aggregate amount of future cash outflows for contractual obligations:

Payments Due by Period

Contractual Obligations (US $ millions) Total Less than One Year

One to Three Years

Four to Five Years

After Five Years

Long-term debt, including interest $576 $32 $288 $32 $224 Purchase obligations 147 58 66 10 13 Operating leases 10 3 4 2 1 Total $733 $93 $358 $44 $238

Note: The above table does not include pension and post-retirement benefits plan obligations, which are discussed in the Significant Accounting Policies and Estimates – Defined Benefit Pension Plans section.

INVESTMENTS AND DIVESTITURES Investment in Property, Plant and Equipment

(US $ millions) 2010 2009 2008 2007 2006

Increased productivity $7 $4 $3 $20 $32Environmental 4 6 13 2 6Maintenance of business 5 4 11 11 18Greenfield and major expansion – – – – 97Capitalized interest – – – 3 7Total $16 $14 $27 $36 $160

Investment in property, plant and equipment in 2010 was constrained to $16 million, representing approximately 35% of depreciation. In the fourth quarter, Norbord commenced an infrastructure investment program at its particleboard mill in Cowie. The investment is expected to increase production capacity and reduce manufacturing costs.

Due to market conditions, investment in property, plant and equipment was limited in the past few years to essential projects. In 2006, investment in property, plant and equipment was high as the Company took advantage of strong earnings to expand capacity at the Cordele mill, to accelerate higher-return capital projects focused primarily on energy reduction and production enhancement, and to meet Maximum Achievable Control Technology (MACT) requirements. The second OSB line at Cordele, which was completed on time and on budget in December 2006, is one of the largest and most efficient OSB manufacturing facilities in the world. The expansion added approximately 550 Msf (3⁄8-inch basis) of production capacity at a capital cost of $135 million and increased Norbord’s North American OSB production capacity by 15%.

Norbord’s 2011 investment in property, plant and equipment is expected to be constrained to $25 million for essential capital projects and will be funded with cash on hand, cash generated from operations and, if necessary, drawings under the Company’s committed revolving bank lines.

Divestitures In January 2011, True North Hardwood Plywood Inc. announced the winding down of its hardwood plywood operation in Cochrane. Norbord held a 50% joint-venture interest in this non-core business, which represented less than 1% of total assets. Approximately 200 employees were affected by this decision. In 2010, the Company recorded a $6 million non-cash provision for the write-down of its investment in the joint venture.

Some of the statements included in this MD&A constitute forward-looking statements that are based on various assumptions and are subject to various risks. See the cautionary statement contained in the Forward-Looking Statements section.

22

In November 2009, Norbord sold its non-core MDF mill in Deposit to a third party for proceeds of $2 million. Approximately 90 employees were affected by this decision. In 2009, the Company recorded a $4 million provision, primarily for the write-down of certain property, plant and equipment and inventory to net realizable value.

CAPITALIZATION

Common Share Information as at December 31 2010 2009 2008 2007 2006

Shares outstanding (millions) 43.5 43.2 26.9 14.7 14.4 Dividends (US $ millions) $ 0 $ 0 $ 56 $ 55 $ 178Market price at year-end (CAD $) $ 14.64 $ 14.66 $ 7.00 $ 79.60 $ 89.10

At January 28, 2011, there were 43.5 million common shares outstanding. In 2010, the total return on Norbord shares was negative 1%, compared to 109% in 2009. The average daily volume traded during 2010 was approximately 170,000 shares, compared to approximately 55,000 shares in 2009.

In 2010, Norbord applied to the Toronto Stock Exchange (TSX) and received approval to conduct a normal course issuer bid in accordance with TSX rules. Under the bid, the Company may purchase up to 2,176,198 of its common shares, representing approximately 5% of the 43.5 million issued and outstanding common shares as at January 28, 2011. Purchases under the bid will terminate on the earlier of September 16, 2011, the date Norbord completes its purchases pursuant to the notice of intention to make a normal course issuer bid filed with the TSX, or the date Norbord provides notice of termination of the bid.

Secondary Offering In March 2010, Brookfield and the Company entered into an agreement with a syndicate of investment dealers to complete a secondary offering of Norbord’s common shares. Under the agreement, the syndicate purchased 9 million common shares at a price of CAD $16.70 per common share, for gross proceeds of CAD $150 million, on March 30, 2010. Brookfield offered 8.7 million shares and the Company’s senior management offered 0.3 million shares. Upon completion of the secondary offering, Brookfield’s ownership decreased from approximately 73% to 52% of common shares outstanding. Norbord did not receive any proceeds from the offering.

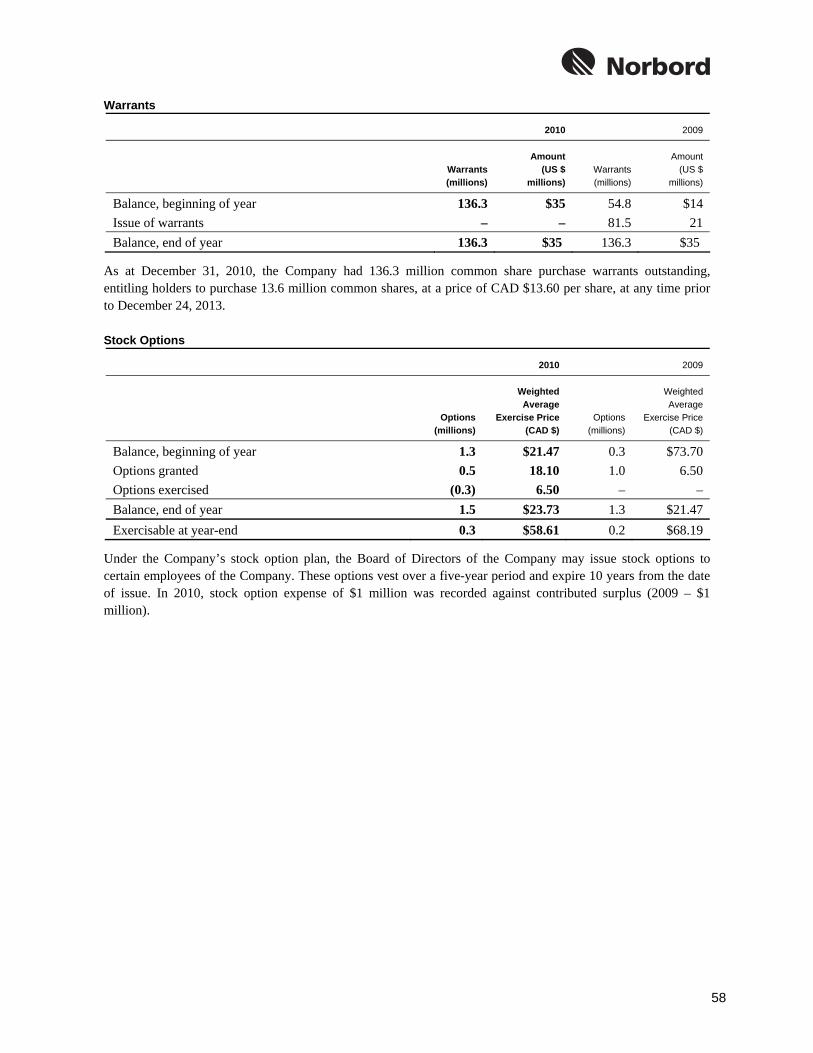

Warrants As at December 31, 2010, there were 136.3 million warrants outstanding, entitling the holders to purchase 13.6 million common shares. Ten whole warrants entitle the holder to purchase one common share at a price of CAD $13.60 at any time prior to December 24, 2013.

Stock Options As at December 31, 2010, options on 1.5 million common shares were outstanding, with 17% vested. The exercise prices for the outstanding options range from CAD $0.10 to CAD $111.30, with expiry on various dates up to 2020. In 2010, approximately 0.3 million common shares were issued under the Company’s stock option plan, generating proceeds of $2 million.

Some of the statements included in this MD&A constitute forward-looking statements that are based on various assumptions and are subject to various risks. See the cautionary statement contained in the Forward-Looking Statements section.

23

SELECTED QUARTERLY INFORMATION

2010 2009

(US $ millions, except per share information, unless otherwise noted) 4th Qtr 3rd Qtr 2nd Qtr 1st Qtr 4th Qtr 3rd Qtr 2nd Qtr 1st Qtr

KEY PERFORMANCE METRICS

Return on capital employed (ROCE) 7% 6% 33% 4% 3% 5% (1)% (7)%Return on equity (ROE) (8)% (8)% 44% (6)% (12)% (8)% (19)% (29)%

Cash provided by (used for) operating activities 50 3 75 2 16 15 39 (105)

Cash provided by (used for) operating activities per share 1.16 0.07 1.72 0.05 0.37 0.35 0.90 (2.49)

NET SALES AND EARNINGS Net sales 219 211 278 184 196 192 174 156 EBITDA 13 12 71 9 6 10 (2) (14) Earnings (8) (7) 37 (5) (11) (7) (18) (22)

PER COMMON SHARE

Earnings Basic (0.18) (0.16) 0.85 (0.12) (0.25) (0.16) (0.42) (0.52) Diluted (0.18) (0.16) 0.81 (0.12) (0.25) (0.16) (0.42) (0.52)

KEY STATISTICS

Shipments (MMsf–3⁄8") North America 768 757 834 630 726 750 717 587 Europe(1) 326 335 345 292 302 291 277 288 Indicative OSB pricing Average OSB price

North Central ($/Msf–7⁄16") 191 180 295 212 172 178 146 154 South East ($/Msf–7⁄16") 165 156 277 197 154 157 140 139 Europe (€/m3) 229 224 206 180 168 163 163 183

(1) Excludes product consumed internally (29 MMsf, 24 MMsf, 26 MMsf, 29 MMsf, 37 MMsf, 28 MMsf, 31 MMsf, 31 MMsf for each period, respectively).

Quarterly results are impacted by seasonal factors such as weather and building activity. Market demand varies seasonally, as homebuilding activity and repair and renovation work – the principal end uses of Norbord’s products – are generally stronger in the spring and summer months. Adverse weather can also limit access to logging areas, which can affect the supply of fibre to Norbord’s operations. Shipment volumes and commodity prices are affected by these factors as well as by global supply and demand conditions.

Operating working capital is typically built up in the first quarter of the year due primarily to log inventory purchases in the Northern regions of North America and Europe. Logs are generally consumed in the spring and summer months. Operating working capital also fluctuates based on the timing of bond coupon payments in the first and third quarters.

The price of and demand for OSB in North America are significant variables affecting the comparability of Norbord’s results over the past eight quarters. Fluctuations in earnings during that time mirror fluctuations in the price of and demand for OSB in North America. The Company estimates that the annualized impact of a $10 per

Some of the statements included in this MD&A constitute forward-looking statements that are based on various assumptions and are subject to various risks. See the cautionary statement contained in the Forward-Looking Statements section.

24

Msf (7⁄16-inch basis) change in the North American OSB price on EBITDA, when operating at capacity, is approximately $36 million or $0.83 per share. Regional pricing variations, particularly in the Southern US, make the North Central benchmark price a useful, albeit imperfect, proxy for overall North American OSB pricing. Further, competition premiums obtained on value-added products, the pricing lag effect of maintaining an order file, and volume and trade discounts cause realized prices to differ from the benchmark.

High global commodity prices caused upward pressure on the prices of key input costs, primarily resin, wax, energy and fibre, for most of 2008. Downward trends in global energy prices provided significant input cost relief in the first half of 2009, with prices on the bottom during the second half of 2009. In 2010, commodity prices increased in the first half of the year and then leveled off for the remainder of the year. Management believes that commodity prices may trend up moderately in 2011, although they are not expected to return to the peak levels experienced at the end of 2008.

Norbord has relatively low exposure to the Canadian dollar due to a comparatively small manufacturing base in Canada, which comprises 13% of its panel production capacity. The Company estimates that the unfavourable impact of a one-cent (US) increase in the value of the Canadian dollar would negatively impact annual EBITDA by approximately $1 million, when Norbord’s Canadian OSB mills operate at capacity.

Items not related to ongoing business operations that had a significant impact on quarterly results include:

Provision for non-core operation − In the fourth quarter of 2010, the Company recorded a provision of $6 million pre-tax ($0.14 per share) related to its 50% interest in a non-core hardwood plywood joint-venture operation. In the third and fourth quarters of 2009, the Company recorded a provision of $3 million pre-tax ($0.04 per share) and $1 million pre-tax ($0.02 per share), respectively, related to the sale of its non-core MDF mill in Deposit (see Investments and Divestitures).

Depreciation expense − In the second quarter of 2009, the Company changed to the units of production depreciation method for its production assets, resulting in a $4 million pre-tax ($0.06 per share) reduction in depreciation expense for the second, third and fourth quarters of 2009 (see Significant Accounting Policies and Estimates).

Income tax recovery − In the first quarter of 2009, the Company recorded an income tax recovery of $8 million ($0.19 per share) related to the recognition of a future income tax asset previously charged to retained earnings in the fourth quarter of 2008, due to Brookfield’s acquisition of control (see Interest, Depreciation and Income Tax).

Foreign exchange loss − In the first quarter of 2009, the Company incurred a foreign exchange loss of $3 million pre-tax ($0.05 per share) from the locked-in foreign exchange rate for Canadian proceeds received upon completion of Brookfield’s standby commitment in January 2009, related to a Rights Offering.

FOURTH QUARTER RESULTS Norbord achieved a sixth consecutive quarter of positive EBITDA results and positive operating cash flow from both its North American and European operations. Under normal market conditions, a seasonal slowdown is experienced in the fourth quarter in North America. The seasonal slowdown was less evident in 2010 as prices held up due to wet weather conditions in the Southern US (which affected log availability and supply), low OSB inventories and firmer OSB demand. In the UK, extreme cold and snowy weather conditions were experienced in the latter part of the year. Nevertheless, European panel prices and shipment volumes continued to move in a positive direction as improved do-it-yourself and housing activity continued during the quarter.

In the quarter, North Central benchmark OSB prices averaged $191 per Msf (7⁄16-inch basis), up $11 per Msf from the third quarter and $19 from the fourth quarter of 2009. In the South East region, where approximately 55% of Norbord’s North American OSB capacity is located, prices averaged $165 in the quarter, up $9 from the third quarter and $11 from the fourth quarter of 2009. Indicative European OSB prices (denominated in Euros) and MDF prices increased by 2% and 3%, respectively, relative to the third quarter of 2010, while particleboard

Some of the statements included in this MD&A constitute forward-looking statements that are based on various assumptions and are subject to various risks. See the cautionary statement contained in the Forward-Looking Statements section.

25