Embed Size (px)

Citation preview

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 1/46

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 2/46

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 3/46

• Over view• Introduction

• Emergence of Islamic banking

• Definition of Islamic banking

• Modes of finance

• Services

• Other Notes

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 4/46

• Modern banking system was introduced into

the Muslim countries at a time when they

were politically and economically at a low ebb,

in the late 19th century. The main banks in the

home countries of the imperial powers

established local branches in the capitals of

the subject countries and they catered mainlyto the import export requirements of the

foreign businesses.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 5/46

• The banks were generally confined to the capitalcities and the local population remained largelyuntouched by the banking system. The localtrading community avoided the “foreign” banks

both for nationalistic as well as religious reasons.However, as time went on it became difficult toengage in trade and other activities withoutmaking use of commercial banks. Even then many

confined their involvement to transactionactivities such as current accounts and moneytransfers.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 6/46

• Borrowing from the banks and depositing theirsavings with the bank were strictly avoided in orderto keep away from dealing in interest which isprohibited by religion.

• With the passage of time, however, and other socio-economic forces demanding more involvement innational economic and financial activities, avoidingthe interaction with the banks became impossible.Local banks were established on the same lines asthe interest-based foreign banks for want of anothersystem and they began to expand within the countrybringing the banking system to more local people.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 7/46

• As countries became independent the need toengage in banking activities became unavoidableand urgent. Governments, businesses andindividuals began to transact business with the

banks, with or without liking it. This state of affairs drew the attention and concern of Muslimintellectuals. The story of interest-free or Islamicbanking begins here. In the following paragraphs

we will trace this story to date and examine howfar and how successfully their concerns havebeen addressed

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 8/46

• Historical development

It seems that the history of interest-free

banking could be divided into two parts. First,

when it still remained an idea; second, when it

became a reality -- by private initiative in

some countries and by law in others.

We will discuss the two periods separately

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 9/46

• The last decade has seen a marked decline in

the establishment of new Islamic banks and

the established banks seem to have failed to

live up to the expectations. The literature of

the period begins with evaluations and ends

with attempts at finding ways and means of

correcting and overcoming the problemsencountered by the existing banks

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 10/46

• What is Islamic Banking?

Islamic banking is the conduct of banking

based on Shariah principles (Islamic rules on

transactions) and does not allow the paying

and receiving of interest while promoting

profit sharing.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 11/46

• It has exactly the same purpose as

conventional banking except that it operates

under the rules of Shariah, the law of Islam

that covers every aspect of life, based on the

holy Quran.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 12/46

• Islamic banks and financial institutions that

offer Islamic banking products are required to

establish a Shariah advisory committee to

advise them on the rules of the Shariah and to

ensure that they operate in accordance with

the Shariah principles

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 13/46

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 14/46

This is done in the following modes :

• A. Musharaka where a bank may join another

entity to set up a joint venture, both parties

participating in the various aspects of the projectin varying degrees. Profit and loss are shared in a

pre-arranged fashion. This is not very different

from the joint venture concept The venture is anindependent legal entity and the bank may

withdraw gradually after an initial period

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 15/46

B : Mudarabha where the bank contributes the

finance and the client provides the expertise,

management and labour. Profits are shared by

both the partners in a pre-arrangedproportion, but when a loss occurs the total

loss is borne by the bank.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 16/46

• D: Financing on the basis of an estimated rate of

return.

• Under this scheme, the bank estimates the expectedrate of return on the specific project it is asked tofinance and provides financing on the understandingthat at least that rate is payable to the bank. (Perhapsthis rate is negotiable.) If the project ends up in a profitmore than the estimated rate the excess goes to the

client. If the profit is less than the estimate the bankwill accept the lower rate. In case a loss is suffered thebank will take a share in it.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 17/46

• This is also done in several ways. The mainones are: a) Mark-up where the bank buys anitem for a client and the client agrees to repay

the bank the price and an agreed profit lateron. b) Leasing where the bank buys an itemfor a client and leases it to him for an agreedperiod and at the end of that period the

lessee pays the balance on the price agreed atthe beginning an becomes the owner of theitem. c) Hire-purchase

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 18/46

• where the bank buys an item for the client andhires it to him for an agreed rent and period, andat the end of that period the client automaticallybecomes the owner of the item. d) Sell-and-buy-

back where a client sells one of his properties tothe bank for an agreed price payable now oncondition that he will buy the property back aftercertain time for an agreed price. e) Letters of

credit where the bank guarantees the import of an item using its own funds for a client, on thebasis of sharing the profit from the sale of thisitem or on a mark-up basis.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 19/46

• Main forms of Lending are:

A) Loans with a service charge where the bank lendsmoney without interest but they cover their expensesby levying a service charge. This charge may be subjectto a maximum set by the authorities.

B) No-cost loans where each bank is expected to setaside a part of their funds to grant no-cost loans toneedy persons such as small farmers, entrepreneurs,

producers, etc. and to needy consumers. c) Overdraftsalso are to be provided, subject to a certain maximum,free of charge.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 20/46

• Wadiah (Safekeeping)In Wadiah, a bank is deemed as a keeper andtrustee of funds. You deposit your funds in thebank and the bank guarantees refund of the

whole amount or any part of the amount whenyou demand it. The bank may also reward youwith ‘hibah’ (gift) in appreciation for allowing thebank to use your deposited funds. Under

conventional banking, Wadiah is applicable toyour savings or current account while hibahwould be the interest earned on these accounts.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 21/46

• Mudharabah (Profit Sharing)Mudharabah is an agreement between you andthe bank where the bank allows you to mobilize

its funds for your business activities. If there isany profit resulting from the venture, it is sharedwith the bank while any losses are borne byyou. Under conventional banking, Mudharabah is

applicable to your savings, current or investmentaccounts as well as deposit instruments, shareand unit trust financing.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 22/46

• Musharakah (Joint Venture)

Musharakah is a joint venture agreement

between you and the bank where profits and

losses are both shared in accordance with theterms of the agreement. Under conventional

banking, it is applicable to share or unit trust

financing and letters of credit.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 23/46

According to this concept, a financier and his clientparticipate either in the joint ownership of aproperty or an equipment, or in a jointcommercial enterprise. The share of the financier

is further divided into a number of units and it isunderstood that the client will purchase the unitsof the share of the financier one by oneperiodically, thus increasing his own share till all

the units of the financier are purchased by him soas to make him the sole owner of the property, orthe commercial enterprise, as the case may be.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 24/46

• Murabahah (Cost Plus)

Murabahah is the selling of goods at an

agreed price and at an agreed profit margin

between the bank and you

• Under conventional banking, it is applicable to

a cash line facility, working capital financing,

letters of credit and accepted bills.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 25/46

• Salam is a sales contract in which the price is

paid in advance at the time of contracting

,against delivery of the purchased

goods/services at a specified future date.

• Note every commodity is suitable for a salam

contract.

• It is usually applied only to fungible

commodities

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 26/46

• Al- Istisna a contract in which a party ordersanother to manufacture and provide acommodity , the description of which ,

delivery date, price and payment date are allset in the contract .

• According to a decision of the OIC fiqhAcademy, this type of contract is of a bindingnature , and the payment of price could bedeferred.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 27/46

• Bai’ Bithaman Ajil (Deferred Payment Sale)This is the selling of goods on a deferredpayment basis at a price which includes a

profit margin agreed to by the bank andyou. Under conventional banking, Bai’Bithaman Ajil is applicable to a negotiabledebt certificate, home or property financing,

share or unit trust financing, Umrah (Muslimpilgrimage to Mecca) and visitation financing.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 28/46

• Wakalah (Agency)

Wakalah is when you appoint your bank to

undertake transactions on your behalf just as

your bank acts for you when issuing letters of credit in trade financing.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 29/46

• Qardhul Hassan (Benvolent Loan)

Qardhul Hassan is when your bank extends

you a loan based on goodwill and you are only

required to repay the amountborrowed. However, you may at your

discretion pay more to your bank as a token of

appreciation.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 30/46

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 31/46

• Ijarah Thumma Al Bai’ (Hire Purchase)

There are two contracts under this hire

purchase principle. The first is the Ijarah

contract (leasing/renting) when you enter intoan agreement with your bank to lease the car

from the bank at an agreed rental and time

frame. When the leasing period ends, the Bai’(purchase) contract takes effect which enables

you to purchase the car at an agreed price

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 32/46

• Hibah (Gift)

A token given voluntarily in return for a loan

received or benefit obtained.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 33/46

• Ujr (Fee)All other banking services are based on the Ijrprinciple which are fee-based services such asstockbroking, telegraphic transfers, travelers’checks, ATM services and telebanking.

• Islamic Banking RatesFor savings, current and deposit accounts hibah

(gift) is paid at the discretion of the banks shouldthere be any profit from utilization of yourdeposited funds

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 34/46

• Finance

• asset-backed interest-free bond in Islamic

financing, the equivalent of a bond, which

represents undivided shares in ownership of

tangible assets. Under Islamic law it cannot

earn interest.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 35/46

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 36/46

• For a new house the financing rate ranges

from about 2.8% in the first year to about

7.75% after the fifth year. For a completed

house the financing rate ranges from about3.8% in the first year to about 7.75% after the

fifth year.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 37/46

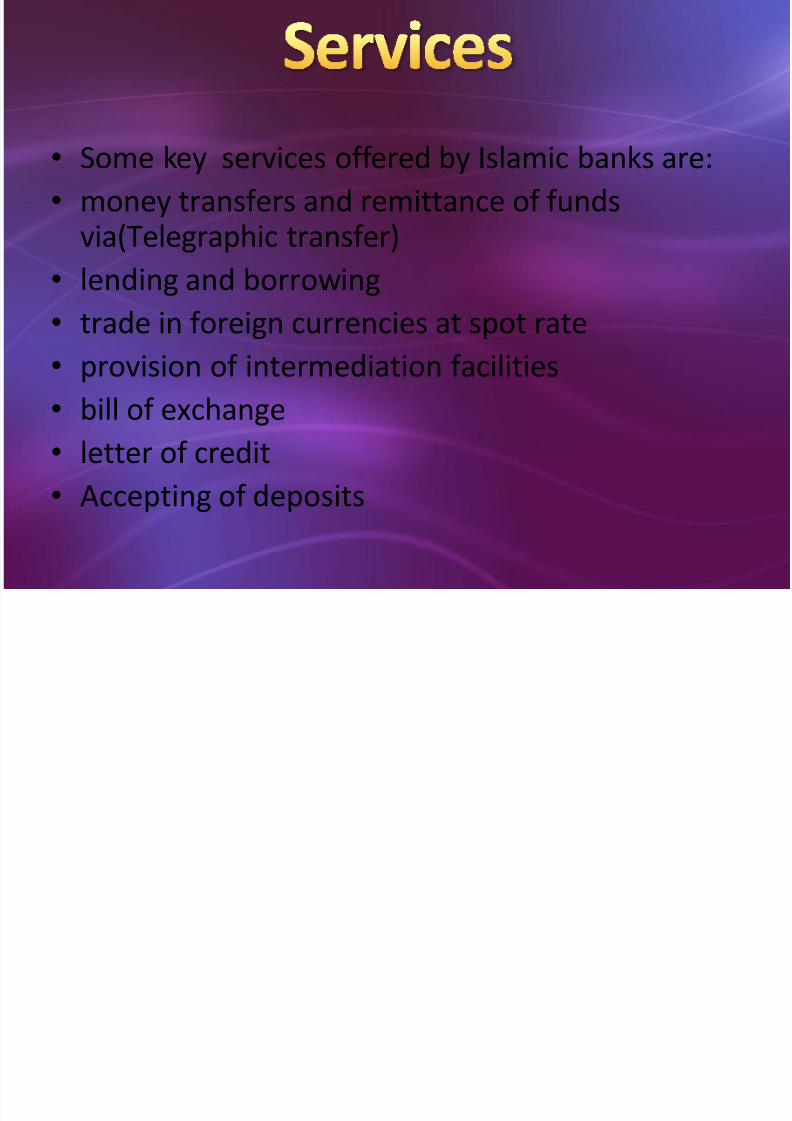

• Some key services offered by Islamic banks are:

• money transfers and remittance of fundsvia(Telegraphic transfer)

• lending and borrowing• trade in foreign currencies at spot rate

• provision of intermediation facilities

•

bill of exchange• letter of credit

• Accepting of deposits

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 38/46

• Issuance of credit and debit cards

• Issuance of guarantees, securities etc.

• Issuance of cheques or travel cheques

• ATM(Aatomated Teller Machine)• Provision of researches, sustainability studies,

consultations and advices

•

Mail• Telephone banking

• Online banking

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 39/46

• Mobile banking

• Video banking

• Safekeeping of documents and other items in

safe deposit boxes.

where the bank’s own money is not involved are

provided on a commission or charges basis.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 40/46

• In the previous section we listed the current

practices under three categories: deposits,

modes of financing (or acquiring assets) and

services. There seems to be no problems asfar as banking services are concerned

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 41/46

• Islamic banks are able to provide nearly all the

services that are available in the conventional

banks. The only exception seems to be in the

case of letters of credit where there is apossibility for interest involvement. However

some solutions have been found for this

problem -- mainly by having excess liquiditywith the foreign bank.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 42/46

• On the deposit side, judging by the volume of

deposits both in the countries where both

systems are available and in countries where

law prohibits any dealing in interest, the non-payment of interest on deposit accounts

seems to be no serious problem. Customers

still seem to deposit their money withinterest-free banks.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 43/46

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 44/46

• That leaves us with investment financing and

trade financing. Islamic banks are expected to

engage in these activities only on a profit and

loss sharing (PLS) basis. This is where thebanks’ main income is to come from and this

is also from where the investment account

holders are expected to derive their profitsfrom.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 45/46

• And the latter is supposed to be the incentive

for people to deposit their money with the

Islamic banks. And it is precisely in this PLS

scheme that the main problems of the Islamicbanks lie. Therefore we will look at this system

more carefully in the following section.

8/2/2019 Islamic Banking Services

http://slidepdf.com/reader/full/islamic-banking-services 46/46

• This body (AAOIFI )was established after an agreementsigned by various Islamic financial institutions on 26February 1990 and was registered in Bahrain as aninternational autonomous non-profit making corporatebody on 27 March 1991. At that time local countryaccounting standards were not well established in theMiddle East and a need was clearly felt for theestablishment of accounting standards for Islamicfinancial institutions that would be harmonized across

countries. AAOIFI has also established a Shariah Boardwhich is highly respected, and is probably the leadingglobal setter of Islamic finance Shariah standards.However the organization's name clearly indicates