Embed Size (px)

Citation preview

NATIONAL MANAGEMENT COLLEGE102nd NATIONAL MANAGEMENT COURSE

IRP – PRESENTATION

WILL LNG IMPORT SUBSTITUTE PIPED GAS IMPORT?

2

ASAD MAHMOOD QAZIEx-Cadre (IB&NH)

Faculty Advisor: Rai Ijaz Ali Zaigham

24th June, 2015

Sequence

• Introduction

• Statement of the Problem

• Research Question

• Research Methodology

• Significance and Scope

• Natural Gas

• Benefits & Uses

• Benefits of Gas in Pakistan

Sequence

• Trans-border Gas Import Pipeline Projects• IP & TAPI

• Liquefied Natural Gas (LNG)

• Need for LNG

• LNG a Value Chain

• LNG Import in Pakistan

• Analysis – LNG Import Vs. Piped Gas Import

• Conclusion

• Recommendations

Sources Consulted

• 22nd World Gas Conference, Tokyo 2003 - Report

• Internal Documents of M/o Petroleum and Natural Resources, Islamabad (Total Gas Demand on System, 2013)

• Inter-State Gas Services Limited –MPNR

• Earnest and Young (2013), Global LNG: Will New Demand and New Supply Means New Pricing

• International Gas Union – World LNG Report, 2014

• Pakistan’s Gas Pipeline Projects, Energy Charter Treaty Meeting on Transit and Trade, October, 2006.

Sources Consulted

• TAPI – Conflict Resolution Mechanism – Express Tribune, March, 4, 2015

• Greening Natural Gas Delivery – LNG Vs. Pipelines• Overseas Investors Chamber of Commerce and

Investments (OICCI) Pakistan, Energy Sub-Committee, NEPRA’s State of Industry Report, 2013

• Article By Zafar Bhutta, The Express Tribune, February 20, 2015 – 21b LNG Import Deal

• Iran-Lybia Sanctions Act, 50 USC 1701• Certain Websites on LNG & Piped Gas Imports

Sources Consulted

• Officials & Departments consulted

– Mr. Irshad Ahmed Kaleemi – Ex-Joint Secretary (Development) MPNR, Islamabad, Ex-MD GHPL, Ex-Director, PPL

–M/o Petroleum and Natural Resources, Islamabad– OGDC, Islamabad– SGNPL, Lahore– Hydro Carbon Development Institute of Pakistan,

Islamabad (HDIP)

INTRODUCTION

Introduction

ENABLE AS MANY PEOPLE AS POSSIBLE TO ACCESS ENERGY

Gas will be the energy of the 21st century. 10-Year

Demand forecast @ 2.5% per annum, ranking it second

in the global energy mix in 2030

Total Says: Already a top-tier global producer of

liquefied natural gas (LNG), we continue to expand our

positions through a policy of strategic partnerships

Introduction

• Acute and lingering energy crisis – Pakistan

• Effects – Severe Socio-Economic and Industrial

• Reasons – Mismanagement, Feeble Regulatory and

Pricing Mechanisms

• Supply and Demand Gap

• 44% Primary Energy Needs through Natural Gas

Source: Total Gas Demand on System, 2013 – M/o Petroleum & Natural Resources, Islamabad

Introduction • Decreasing Natural Gas Reserves• Slow pace of New Discoveries • Fill in the gap, Country needs to import to supplement• Natural Gas Imports – Principally Piped Gas & LNG• Piped Gas Import Projects – IP & TAPI• LNG Import – Quick in Mitigating the Shortage• Natural gas converted into liquefied state by

compression– Negative 260F (160C)– Reduces volume of gas 600 times

Source: www.slideshare.net/kellylng.deepwaters

Introduction

– LNG is converted into gaseous form at import

facility (i.e. platform, ship, onshore facility)

– Transported to end user via main trunk pipeline

• Japan, Korea and China included LNG – as a

replacement to RFO as power plant fuel

• Pipeline Projects – remain in limbo

• What options Left – Importing LNG or Piped Gas?

Source: Business Recorder – March, 2014 – LNG Replaced Residual Furnace Oil (RFO)

Statement of the Problem

Owing to the geopolitical constraints, internal security

issues and shortage of domestic natural piped gas for

local consumption, it seems improbable that piped-gas

import will materialize and sustain in foreseeable

future. The piped gas projects – IP and TAPI seem to

remain in limbo due to Afghan security, American

influence and financial constraints. LNG import can be

a fast track option than the piped-gas import

Research Question

Which option to be exercised – trans border

piped gas import or LNG import?

Research Methodology

• Descriptive and analytical approaches

• Discussions

• Library-Books, Journals, Magazines etc.

• Internet

• Interviews

• News Reports

Significance and Scope

• Immediate attention of NMC researchers, research

groups, NGOs, media, etc.

• Nature of topic in policy perspective & current

• Complex security situation and enormous challenges

• Focus of research on practicality & implementation

• Service to nation - knowledge base and background

• Sensitizing coming generation

• Prioritizing national interests & purpose

NATURAL GAS

18

Natural Gas

It refers to natural gases that occur in mother nature

underground deposits. The gas is exploited and compressed to

convert it into LNG which is mainly methane-CH4

19

Natural Gas

Benefits

• 1993 to 2011 – Global Energy Market demand for

Natural Gas expanded 650 mtoe to 1380 mtoe

• Minimal per unit power generation cost

- natural gas plant: $650/kw

- coal-fired plant: $1,300/kw

- fuel-oil fired plant: $1,000/kw

Source: www.slideshare.net/Iran-Pakistan/Pipelines

20

Natural Gas

Benefits• Higher Thermal Efficiency Translated into cost as

well

- natural gas plant: 45 - 50 % efficient - coal fired plant: 30 - 35 % efficient - fuel-oil fired plant: 30 - 35 % efficient

•Shorter Project Gestation

- natural gas plant: 2 - 3 years - coal fired plant: 5 years - fuel-oil fired plant: 4 years

Source: www.slideshare.net/Iran-Pakistan/Pipelines

21

Natural Gas

UsesCabinet of Pakistan has decided following priority users of Natural Gas

Domestic (Home)

Commercial

Fertilizer

Power Generation

Transportation (CNG)

Source: www.slideshare.net/Iran-Pakistan/Pipelines & MPNR

22

Benefits of Gas in Pakistan

• Cost Efficient – ($4.2 per mmcfd)

• Safe and Clean

• Development of far flung areas of BLN, Sindh &

KPK from where the gas is exploited.

• Local investor & local industry development

• Agricultural development due to domestic fertilizer

production & saving of FOREX reserves of Pakistan

Source: M/o Petroleum and Natural Resources, Islamabad

PAKISTAN’S TRANS BORDER PIPED GAS IMPORT

PROJECTS

Pakistan’s Trans Border Piped Gas Import Projects

• Iran – Pakistan (IP)• Turkmenistan-Afghanistan-Pakistan-

India (TAPI)

25

Route

26Iran Pakistan Pipeline

Iran – Pakistan (IP)

In mid 1950s, a young Pakistani civil engineer Malik

Aftab Ahmed Khan proposed the idea of Iran-Pakistan-

India gas pipeline – IPI or Peace pipeline proposed to

deliver natural gas from Iran to Pakistan and India

Pakistan’s Trans Border Piped Gas Import Projects

Iran – Pakistan (IP)

• Negotiations started in 1994 - Iran and Pakistan– A preliminary agreement was signed in 1995– Construction of a pipeline from South Paras gas

field to Karachi, Pakistan– Later Iran proposed to extend the pipeline from

Pakistan to India– In February 1999 a preliminary agreement between

Iran and India was signed– 2009 India withdrew over security and pricing issues

Pakistan’s Trans Border Piped Gas Import Projects

29

Iran – Pakistan (IP)

• Total length of Pakistani portion of IP is 784 km i.e.

from Asaluyeh to Multan, where the Irani gas will be

injected in to Pakistani Trunk

• Route – Asaluyeh – Bandar Abbas – Khuzdar –

Multan.

• Pipeline Diameter 56” (1,422 mm)

Pakistan’s Trans Border Piped Gas Import Projects

Source: www.slideshare.net/Iran-Pakistan/Pipelines & MPNR

30

Iran – Pakistan (IP)• Initial capacity was 8.7 billion cubic meter - now

raised to 40 billion cubic meter - meeting increased gap

• Expected completion cost + $8 billion

• Pakistani segment completion of pipeline: 30.01. 2013

• President Zardari inaugurated on 11.03.2013

• PM Nawaz Sharif assured to complete

• Penalty clause on delay in implementation

Pakistan’s Trans Border Piped Gas Import Projects

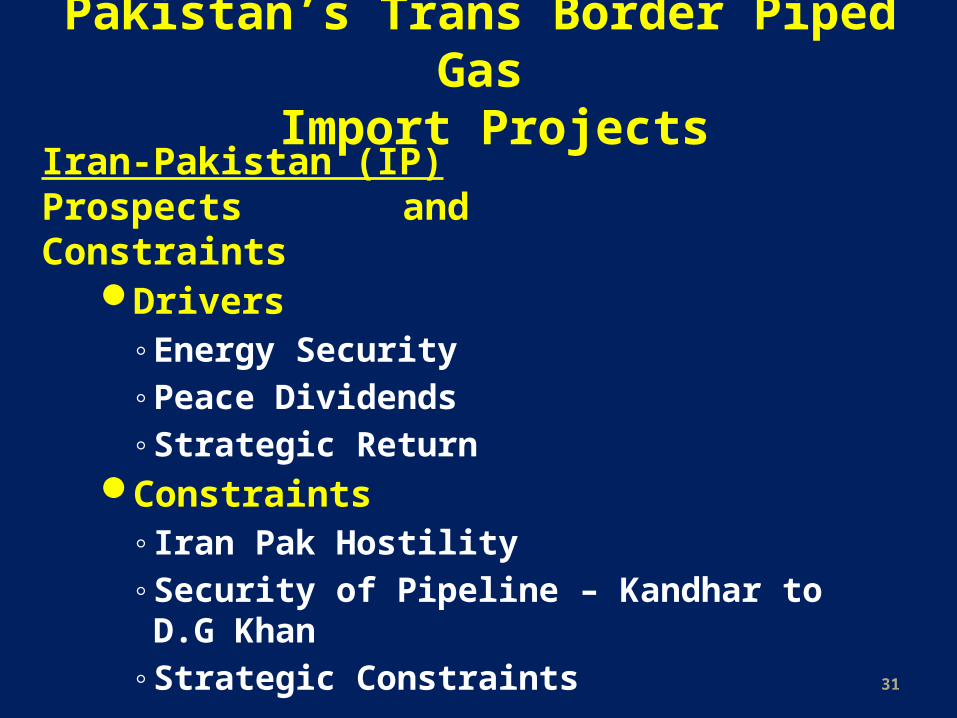

Prospects and Constraints

Drivers◦Energy Security◦Peace Dividends◦Strategic Return

Constraints◦Iran Pak Hostility◦Security of Pipeline – Kandhar to D.G Khan◦Strategic Constraints 31

Pakistan’s Trans Border Piped Gas Import Projects

Iran-Pakistan (IP)

32

TAPI PIPED GAS PROJECT

33

TAPI Turkmenistan-Afghanistan-Pakistan- India Pipeline

34

Pakistan’s Trans Border Piped Gas Import Projects

Turkmenistan-Afghanistan-Pakistan-India (TAPI)

• South Asian countries’ Cooperation in energy – Crucial• Bringing peace in the region – Main concern• SAs leading countries (India and Pakistan)• Potential to pave the way for a compromise and a

balanced bargain• Long time at stake (since 1990s)• 2 Consortium BRIDAS and UNOCAL• US support for UNOCAL, 1997 negotiations with

Taliban

35

Pakistan’s Trans Border Piped Gas Import Projects

Turkmenistan-Afghanistan-Pakistan-India (TAPI)

• In 2001 negotiation broke down• Afghan new government resumed negotiations • 2003 ADB started the technical studies• India was proposed to participate – TAP to TAPI

(India is heading the Steering Committee)• 2008 all participants signed (India did not convene the meeting

for 2.5 years) • Supposed to start supply of gas by 2015• Yet pipeline & construction preliminaries have not been

finalized

Source: www.slideshare.net/tapi/Pipelines/politicalstudies/southaisa/ & MPNR

36

Pakistan’s Trans Border Piped Gas Import Projects

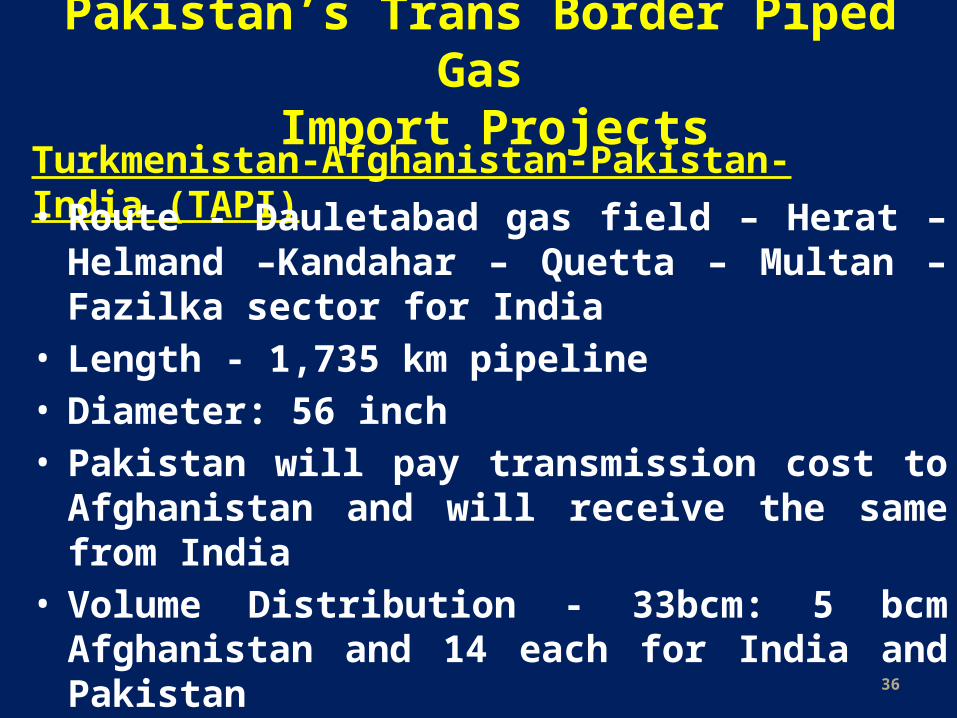

Turkmenistan-Afghanistan-Pakistan-India (TAPI)

• Route - Dauletabad gas field – Herat – Helmand –Kandahar – Quetta – Multan – Fazilka sector for India

• Length - 1,735 km pipeline • Diameter: 56 inch• Pakistan will pay transmission cost to Afghanistan and

will receive the same from India• Volume Distribution - 33bcm: 5 bcm Afghanistan and

14 each for India and Pakistan• Estimated cost $3.3bn & increased $7.6 bn• Financed by the Asian Development Bank

37

TAPI Significance

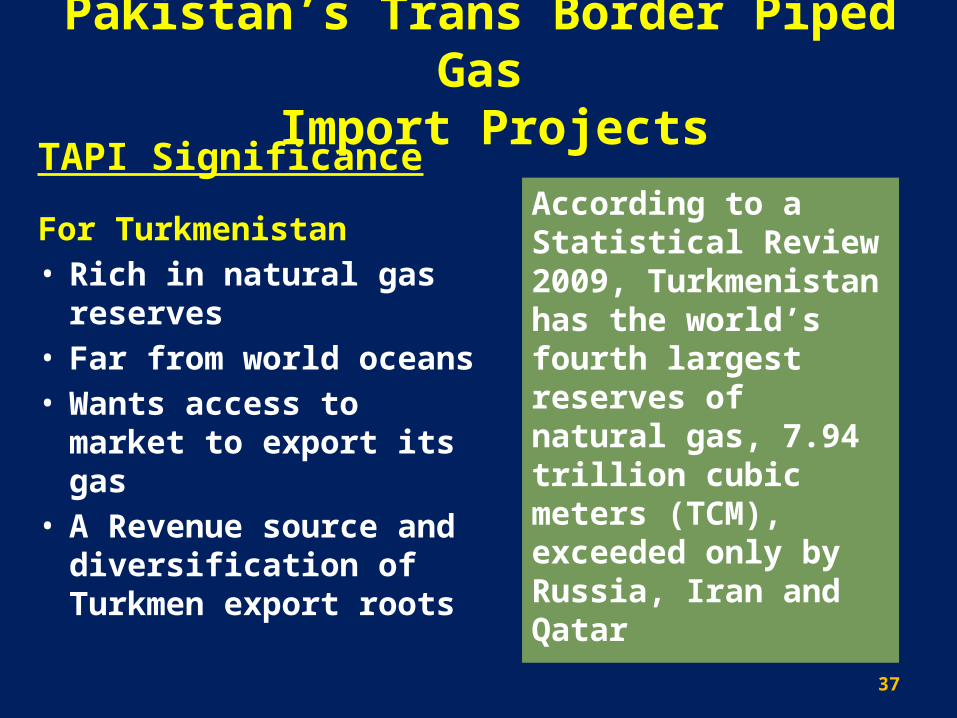

For Turkmenistan• Rich in natural gas

reserves• Far from world oceans• Wants access to market

to export its gas• A Revenue source and

diversification of Turkmen export roots

According to a Statistical Review 2009, Turkmenistan has the world’s fourth largest reserves of natural gas, 7.94 trillion cubic meters (TCM), exceeded only by Russia, Iran and Qatar

Pakistan’s Trans Border Piped Gas Import Projects

38

Afghanistan is an

important bridge

between South and

Central Asia

For Afghanistan TAPI could mean around five

billion cubic meters of gas for internal needs

$300 million of transit fee leading to certain employment and source-of-income opportunities

TAPI Significance

Pakistan’s Trans Border Piped Gas Import Projects

Source: www.slideshare.net/tapi/Pipelines/politicalstudies/southaisa/ & MPNR

39

For India• To acquire additional sources

of energy supplies • Strategic benefit of equating

China in getting a foothold in Central Asia

Annual India’s gas demand = 57.32

bcm 45.58 bcm are provided

domestically Balance is imported as LNG including 5

bcm from Qatar

This will be an addition to India’s

demand

For Pakistan also it means a source to fill in its energy gap, earn the transit fee, employment and other industrial benefits etc.

TAPI Significance

Pakistan’s Trans Border Piped Gas Import Projects

40

• Russia interested in TAPI

• Renewal of Moscow’s strategic influence in the region

• Reduce the EU source of available gas field

• US want to connect South Central Asia to extend its influence from South to Central Asia. (New Great Game)

• Check on Russia, counter China and influence central Asia

• Alternative to IP for India & to weaken the Iran trade in gas.

TAPI Significance

Pakistan’s Trans Border Piped Gas Import Projects

For Russia

For US

LIQUEFIED NATURAL GAS (LNG)

42

43

What is LNG?

• Natural gas (methane-CH4) - converted temporarily by compression to liquid form

• LNG takes up to 1/600th volume of natural gas in the liquefied state

• Colorless, non-toxic and non-corrosive

• Highly Flame-able, then HSE poorer than Piped Gas

• Energy density of LNG is %60 that of diesel fuel

Liquefied Natural Gas (LNG)

44

• Reduction in volume – cost efficient to transport over long distances

• Purified by removal of condensates such as water,

mud, oil, other gases like CO2 , H2S & solids like

mercurry

• Transported through designed cryogenic sea vessels (LNG carriers)

• Re-gasified into Natural Gas & injected in Main Trunk

Liquefied Natural Gas (LNG)

What is LNG?

45

Liquefied Natural Gas (LNG)

Process of LNG

46

Liquefied Natural Gas (LNG)

Compositions

Source: Energy Economic Research, Bureau of Economic Geology, University of Texas Austin

47

Liquefied Natural Gas (LNG)

Need for LNG

Source: Why Pakistan Needs LNG Now – Article by Razi Syed – Daily Times, 26.3.2014

• Pakistan is currently passing through the most

difficult phase of its economic history due to acute

energy shortage

• Our energy requirements are outstripping supply

• LNG import is the fastest short-term solution to

crippling economic needs

48

Liquefied Natural Gas (LNG)

Need for LNG

Source: Energy Economic Research, Bureau of Economic Geology, University of Texas Austin

• IP & TAPI piped gas projects though being very safe and cost efficient but are in the doldrums

• Hydel expansions at Tarbela Costs $840 million – 2018 (1410 MW generation)

• Nuclear Expansion Project at Karachi – 2019 cost $4.8 bn (1100 MW)

• Next 3 to 4 years – no solutions to ongoing energy crises except LNG import or Fast Track implementation of trans border pipelines.

49

Liquefied Natural Gas (LNG)

LNG – A Value Chain

Source: http://www.singaporegas.com.sg/resources/end-users/

• LNG value chain - main stages

- Discovery, Transportation, liquefaction, storage and delivery

50

LNG Chain

Source: http://www.slideshare.net/basicsforlng2011

51

Liquefied Natural Gas (LNG)

LNG Import to Pakistan

Source: www.wapda.gov.pk

• GoP devised short/long terms strategies – Energy crises

• Short term – LNG import & overcoming line losses

• Long term – Change in energy mix

• More shares for generation through coal and nuclear sources

• Renewable sources – Hydro, Solar & Wind

• IP & TAPI piped gas imports

• Building new dams – Diamir Bhasha, Munda etc.

52

Liquefied Natural Gas (LNG)

Source: http://www.engro.com/our-business/elengy-terminal-pakistan/

• LNG import terminal at Port Qasim – 600 MMCFD

• Constructed by Engro Elengy Private Ltd.

• Elengy Terminal Pakistan is 100% owned subsidiary of the company

• Handling, regasification, storage, treatment and processing of LNG, RLNG, LPG etc.

• Total cost of the project is $145 m

LNG Import to Pakistan

53

Liquefied Natural Gas (LNG)

Source: http://www.engro.com/our-business/elengy-terminal-pakistan/

• Pakistan currently producing NG - 4200 mmcfd

• Demand is around 6000 mmcfd

• Import of 5000 mmcfd is likely to bridge the gap

• But won’t eliminate the problem completely

• LNG import shipments arrived from Qatar’s open market on Spot Basis or OTC basis without any G to G agreement, future trading market

• LNG injected to the SSGCL distribution network

LNG Import to Pakistan

54

Liquefied Natural Gas (LNG)

Energy Mix Comparison

Source: www.wapda.gov.pk

Pakistan’s energy mix is around 36% which amounts to approximately $15.8 billion

ANALYSIS

56

Analysis

• In presence of IP Pipeline Project – Committing any quantity of gas what’s the need of TAPI?

IP Length - Asaluyeh to Multan 784 km

TAPI - Dauletabad to Quetta 1735 km

• Means Increased – operational & security costs

• Paying Ransom and Transit Fee Both to: Rasheed Dostam in Northwest Afghanistan, Kabul Government & to Taliban etc. while Crossing through Central Afghanistan, Kandhar, Balochistan

• Above two factors – Road blockers for TAPI

Why TAPI?

57

Analysis

• Initially Dauletabad & now South Yolotan/Osman Gas fields – tremendous volumes

• An Embassy of Pakistan in Central Europe – got 3rd Party Evaluation/Volume Confirmation of suppliable Turkmen Gas

• Turkmenistan Govt. highly willing to supply

• SSGCL & SNGPL of Pak. – world renowned GCs having par excellence in laying the pipeline in shortest possible time with a great cost efficiency

Positivities of TAPI

Sources: Development Wing of MPNR & Interstate Gas Systems Pvt. Ltd.

58

Analysis

• LNG is +$16 mmcfd Costlier than Domestic Piped Gas and + $ 8 mmcfd than the Imported piped gas

• Presently Pakistan buying LNG from open market on spot basis – always expensive

• Qatar has committed all of its LNG to other buyers for next 50 years – no official LNG for Pakistan

• What Qatar does? Asks any of future committed buyer to give ex-quota from their volume to any friendly buyer

LNG Import Vs. Trans-border Piped Gas Import

Sources: Development Wing of MPNR & Interstate Gas Systems Pvt. Ltd.

59

Analysis

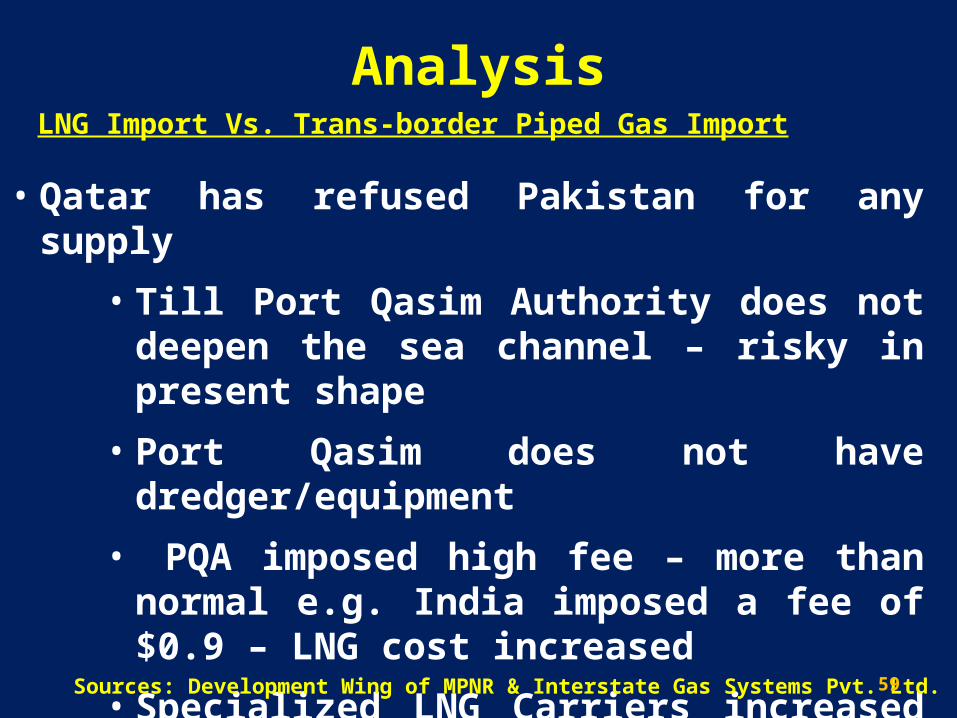

• Qatar has refused Pakistan for any supply

• Till Port Qasim Authority does not deepen the sea channel – risky in present shape

• Port Qasim does not have dredger/equipment

• PQA imposed high fee – more than normal e.g. India imposed a fee of $0.9 – LNG cost increased

• Specialized LNG Carriers increased fee

• Insurance fee of LNG Carrier Marine Vessels - increased

LNG Import Vs. Trans-border Piped Gas Import

Sources: Development Wing of MPNR & Interstate Gas Systems Pvt. Ltd.

60

Analysis

• All the global standards of Health Security & Emergency – LNG a deadly commodity in comparison to piped gas

• Rural area development factor, development of local industry & friendly geo-political relations – exporting countries will be compromised

• Thus LNG import, due to above factors, cannot substitute trans-border piped gas import

LNG Import Vs. Trans-border Piped Gas Import

Sources: Development Wing of MPNR, Interstate Gas Systems Pvt. Ltd., HSE, Hydro Carbon Development Institute, Islamabad,

61

CONCLUSION

62

Conclusion

• Both imports – LNG & Piped gas – varied prospects & consequences

• Both Capital intensive – massive investments required

• LNG – value chain needs heavy investment

• Piped Gas – exploration & transportation – heavy investment required alongwith security issues

• Transporting cost of both does not provide clarity – Whether LNG or Piped gas?

63

Conclusion• Transit security and maintenance risks of long

distance trans-border pipelines – difficult to evaluate – geopolitical landscape – changing

• Trading facility of LNG – inter-regional gas trade – major advantage over piped gas trade

• LNG a good way to diversify gas supply for regions

• Pipeline – a dominant mode of supply for large volumes of gas

• New gas resources farther away from markets & smaller in size – LNG import will increase disproportionately

64

Conclusion

• Eventually –

• Short term measures – LNG is the preferred option

• Long term measures – Piped gas import be focused

• End – LNG import cannot substitute Piped gas

import

65

Recommendations

• Both imports between government to government agreements – LNG not from open markets on spot basis

• Intermediary service providers or the companies of

exporting and importing countries shall have the sovereign guaranty

• Dispute resolution shall be governed by International

Law and not of the law of land of exporting and importing countries

66

Recommendations• Price revision mechanism shall have considerable

calendar years i.e. after a minimum of three years

• Medical experts shall evaluate the human health impact of LNG and piped gas before taking the decision of importing either of the two

• HSE (Health Security and Efficiency) measures shall be worked out before resorting any of the two

• Duties and tax regime, fees, financial structures, etc. be worked out minutely

67

Recommendations

• Gas import through trans-border pipeline, the geo-politics a key element relating to Afghanistan & Baluchistan security risks – experts be taken onboard

• Security cost must be added in the overall cost of the

import of piped gas

• Futuristic energy requirements, especially of gas for almost 25 years be worked out as per quantity to be imported

68

Recommendations

• A group of private and public sector professionals on

energy sector, especially on gas, be formulated to

have an open debate on the media towards taking the

educated decision by taking the public on board

69

70