Embed Size (px)

Citation preview

1

Investor MeetingsAugust 2009

Content

St t i FStrategic Focus

Business Updates

Market Review and Outlook

Going Forward

2

2

STRATEGIC FOCUS

3

Focus on Two Core Businesses

Two Core Businesses

Fee based income from

Property

Development

Property

Fund

SINGAPORE

Commercial developments mainly in New Downtown and CBDResidential developments including lifestyle waterfront projects

OVERSEAS Fee‐based income from fund management with greater AUM

K‐REIT Asia to recycle capital

for Sale Management Residential developments including townships, sustainable developments and integrated lifestyle projects

Commercial developments selectively

4

3

BUSINESS UPDATES

5

SINGAPORE

6

4

Improvement in sentiments :

• Park Infinia at Wee Nam and The Tresor almost fully sold

Singapore Residential

• Good response to previews :

– Madison Residences (46% of 56 units sold)

– Caribbean Residences (45% of 31 launched units sold)

• The Promont : Preparing for launch

7Madison Residences The Promont Caribbean Residences

Singapore Commercial

Marina Bay Financial Centre Ocean Financial Centre

Capitalising on flight to quality with leasing enquiries picking up

NLA : 2.9m sfStrong overall pre‐commitment : 61%

‐ Phase 1 : 66% ‐ Phase 2 : 55%

Expected completion : ‐ Phase 1 : 2010‐ Phase 2 : 2012

NLA : 850,000 sf

4th generation building to rise at former Ocean Building site

Awarded BCA Platinum Green Mark Award

Commenced pre‐lease negotiations

Expected completion : 2011

T2

y

Marina Bay Financial Centre

MBR

T3T2

T1

MBS

Ocean Financial Centre

8

5

Singapore Commercial ‐ K‐REIT Asia

Healthy • Aggregate leverage maintained at 27.6%

Quality portfolio provides stable rental income

Stable Portfolio of Five Quality Office Assets with AUM of $2.1bn

yBalance Sheet

Continued Income Growth

gg g g• Debt maturing only in 2011

• 1H 2009 distributable income up 29.6% y‐o‐y to $33.2m• Distribution per unit for 1H 2009 : 5 cents

• 94.9% committed occupancy as at end‐June 2009• Average portfolio gross rental of $8.13 psf per month• 28.2% of portfolio’s NLA accounted by long lease terms

Prudential Tower Keppel Towers GE Tower Bugis Junction Towers One Raffles Quay 9

OVERSEAS

10

6

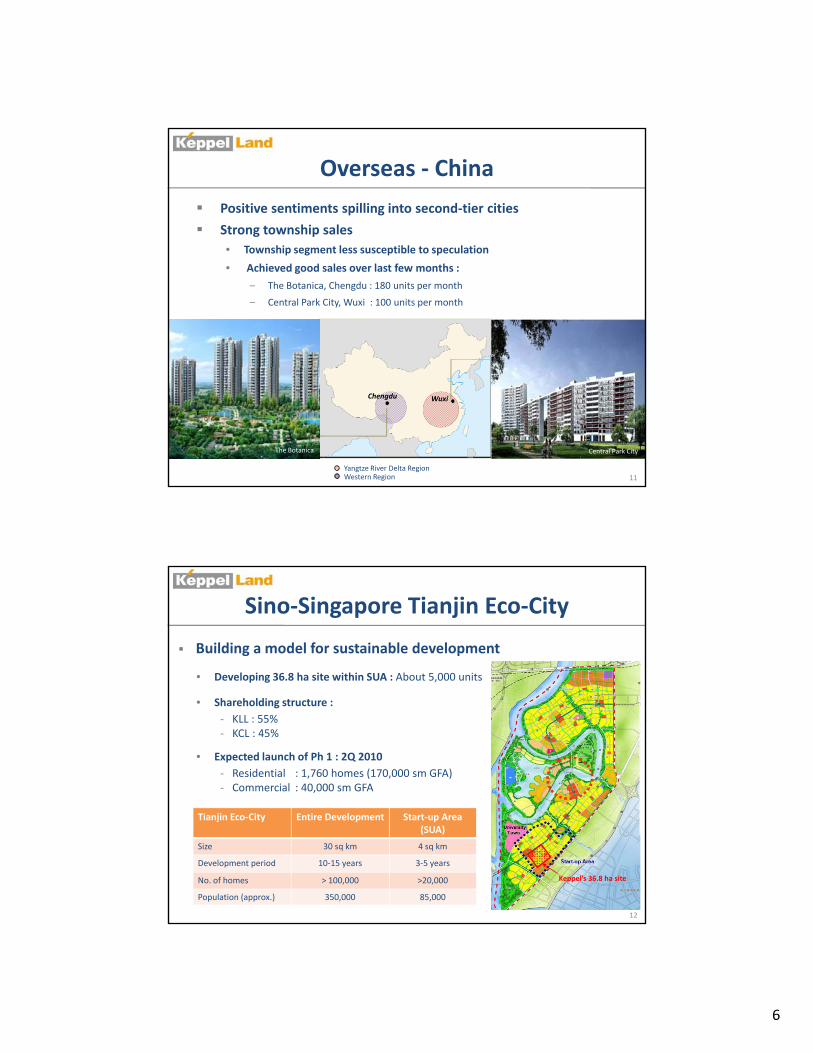

Positive sentiments spilling into second‐tier cities

Strong township sales• To nship segment less s sceptible to spec lation

Overseas ‐ China

• Township segment less susceptible to speculation

• Achieved good sales over last few months :

– The Botanica, Chengdu : 180 units per month

– Central Park City, Wuxi : 100 units per month

Yangtze River Delta RegionWestern Region

WuxiChengdu

The Botanica Central Park City

Villa Riviera

11

Building a model for sustainable development

• Developing 36.8 ha site within SUA : About 5,000 units

Sino‐Singapore Tianjin Eco‐City

• Shareholding structure :‐ KLL : 55%‐ KCL : 45%

• Expected launch of Ph 1 : 2Q 2010‐ Residential : 1,760 homes (170,000 sm GFA)‐ Commercial : 40,000 sm GFA

Tianjin Eco‐City Entire Development Start‐up Area (SUA)

Size 30 sq km 4 sq km

Development period 10‐15 years 3‐5 years

No. of homes > 100,000 >20,000

Population (approx.) 350,000 85,000

Keppel’s 36.8 ha site

12

7

Overseas – Vietnam

Resumed sales at The Estella, Ho Chi Minh City

• Maintained selling price : US$2,000 – US$2,200 psm

• Sales since May 2009 : 52 units sold

• Sales since launch in April 2008 : 346 units sold

13

FUND MANAGEMENT

14

8

K REIT A i

Fund Management

K‐REIT Asia and Alpha looking at asset acquisitions in Asia Total AUM: $9.8 bn (1)

• K‐REIT Asia

– Portfolio value : $2.1 bn

– Explore opportunities for pan‐Asian acquisitions

• Alpha Investment Partners

– AUM : $7.7 bn (1)

– Alpha Asia Macro Trends Fund

Funds under Alpha

Committed Equity

% Invested

No. of Countries Invested in

Asia No. 1

Property Fund$400m 100% 6

Alpha Core Plus $720m 100% 4

$

15

Acquired a retail property in Tokyo

Strong financial position to seek acquisitions in Asia :

About 11% of $1.7bn invested

(1) When fully leveraged and fully invested As at 1H 2009

Real Estate Fund

AIB Alpha Japan

Fund$259m 46% 1

Alpha Asia Marco

Trends Fund$1.7bn 11% 4

MARKET REVIEW AND OUTLOOK

16

9

Singapore Residential

Strong take‐up of 7,250 units in 1H 09 : 70% higher than FY 2008

Improved Market Sentiments with Stabilising Economy

• Prices are firming and momentum gathering pace

• Good take‐up at recently launched mid‐ and higher‐end projects

Supply fear mitigated with significant amount pre‐sold

• 6,209 units due to be completed in 2H 2009 : 90% already sold

• 5,394 units due to be completed in 2010 : 77% already sold

17

Healthy Fundamentals to Sustain Demand

Pent‐up demand from owner‐occupiers and HDB upgraders

Population growth

Low mortgage rates

IRs to elevate Singapore’s profile and attract more foreign buyers

Singapore Commercial

Market

Office demand likely to be subdued in 2009

However, there are signs of stabilisation :

• Singapore GDP forecast upgraded to between ‐6% and ‐4% for 2009Market Sentiments Have Improved

• Investment sales and leasing activities picking up

• Negative take‐up for 2Q 2009 easing from last two quarters

• Pace of decline for office rents eased in 2Q 09

Delays in construction of some office projects have reduced supply

• New office supply from 2Q 2009 – 2012 lowered to 5.9m sf (1)

Growth into a global cosmopolitan city and multi‐hub business destination

Financial sector in Singapore selectively re hiring

18

Singapore Remains Key Business Destination in Longer Term

Financial sector in Singapore selectively re‐hiring

Colliers’ Asia‐Pacific Grade A office rents ranking in 2Q 09

• Increased competitive edge with Singapore’s rents below Ho Chi Minh City

Ranked 4th in recent Forbes ranking of Best Countries to do Business

Ranked 15th in CBRE’s 2009 May Global Occupancy Costs Survey

• Behind Asian cities like Tokyo, Hong Kong, Mumbai and New Delhi

(1) Excluding pre‐committed space of about 2.4 million sf as estimated by CBRE

10

OverseasAsia : Signs of market stabilisation• Stimulus packages yielding positive effects

• Favourable government policies support marketsFavourable government policies support markets

• Increased buying confidence as affordability improves e.g. lower mortgage rates

• Long‐term growth trend backed by firm fundamentals

HOME OWNERSHIP ASPIRATIONS

19

China Better‐than‐expected sales volume in first‐ and second‐tier cities

Vietnam Demand expected to increase with change in Housing Laws

India Affordability improving with lower mortgage rates and prices

Economic Growth

Favourable Demographics

Rising Affluence

Urbanisation Trends

Growing Middle Class

GOING FORWARD

20

11

Accelerating projects for sale in tandem with market recovery

Going Forward

recovery

Seeking acquisitions in Singapore and overseas and capitalising on opportunities from impact of downturn

Continuing to focus on developing quality residential,office, township and sustainable developments

21

office, township and sustainable developments

K‐REIT Asia and Alpha seeking acquisitions of quality assets

Monitor market for opportune time to launch :

• Reflections at Keppel Bay (30% stake) : 382 units

Singapore Residential

• Marina Bay Suites (33.3% stake) : 221 units

22Reflections at Keppel Bay Marina Bay Suites

12

Overseas Residential

Vietnam : Expect to launch Riviera Cove in 2H 2009

23

Riviera Cove, District 9, HCMCVillasTotal units : 96 villas

Riviera Point, District 7, HCMCCondominium development Total units : 2,400 Expected launch : 2010

THANK YOU

24

13

ADDITIONAL SLIDES

25

Financial Highlights 2Q 09 vs 1Q 09

2Q 2009 1Q 2009 % Chg

Turnover ($m) 249.9 145.7 71.5

EBITDA ($m) 47.5 34.3 38.5

Operating Profit ($m) 45.1 31.9 41.4

Pre tax Profit ($m) 83 5 55 7 49 9Pre‐tax Profit ($m) 83.5 55.7 49.9

PATMI ($m) 58.2 36.9 57.7

26

14

Financial Highlights 2Q 09 vs 2Q 08

2Q 2009 2Q 2008 % Chg

Turnover ($m) 249.9 185.9 34.4

EBITDA ($m) 47.5 62.8 (24.4)

Operating Profit ($m) 45.1 61.0 (26.1)

Pre tax Profit ($m) 83 5 75 9 9 9Pre‐tax Profit ($m) 83.5 75.9 9.9

PATMI ($m) 58.2 52.7 10.4

27

Financial Highlights 1H 09 vs 1H 08

1H 2009 1H 2008 % Chg

Turnover ($m) 395.6 459 (13.8)

EBITDA ($m) 81.8 135.6 (39.7)

Operating Profit ($m) 77 132.1 (41.7)

Pre tax Profit ($m) 139 1 158 9 (1) (12 5)Pre‐tax Profit ($m) 139.1 158.9 ( ) (12.5)

PATMI ($m) 95.1 113 (1) (15.8)

(1) Includes a gain of $7.3m arising from acquisition of additional interest in K‐REIT Asia

28

15

5‐Year Financial Profile

FY2008 FY2007 FY2006 FY2005 FY2004

T ($ ) 842 2 1407 9 948 0 586 4 476 2Turnover ($m) 842.2 1407.9 948.0 586.4 476.2

Operating Profit ($m) 231.7 312.3 204.1 146.6 111.1

Pre‐tax Profit ($m) 314.0 988.7 263.4 184.6 139.9

PATMI ($m) 227.7 * 779.7 * 200.3 155.7 132.7

Overseas Earnings (% of PATMI) 29.5 39.7 63.6 59.0 43.3

EPS (¢) 31 6 108 3 27 9 21 8 18 7EPS (¢) 31.6 108.3 27.9 21.8 18.7

NTA/Share ($) 3.39 3.18 2.21 2.35 2.26

Net Debt/Equity Ratio (x) 0.52 0.41 1.04 1.14 0.96

* Includes gain on acquisition of additional interest in K‐REIT Asia and net gain on revaluation of investment properties

^ Includes corporate restructuring surplus from sale of ORQ and net gain on revaluation of investment properties less impairment provision

29

Post Rights Issue

Financial Ratios

1H 2009 1H 2008 % Chg

Net Debt/Equity Ratio (x) 0.23 0.54 (57.4)

EPS (cents) 8.2 11.1(1) (26.1)

NTA/Share ($) 2.29 3.13 (26.8)

Annualised ROE (%) 7 9 8 (28 6)

30

(1) Restated to include the effect of the rights issue in accordance with FRS 33

Annualised ROE (%) 7 9.8 (28.6)

16

Active Capital Management

1H 2009 1H 2008

Net Debt ($b) 0.84 1.42

Avg Interest Rate of Borrowings (%) 2.3 2.7

Fixed Rate Debt (%) 23 14

Avg Debt Maturity (Yr) 1.24 1.46

Interest Cover Ratio (X)* 8.08 9.65

* Interest Cover Ratio = Profit Before Interest and Tax

Net Interest Cost Expensed and Capitalised

31

Healthy cash balances of $1.2bn

Unutilised credit facilities of $1.6bn

• MTN programme : $0.7bn

• Bank facilities : $0.9bn

Asset Breakdown – Geographical Location

Asset Breakdown ‐ Geographical Location

Singapore64%China

16%

Vietnam8%

Others*12%

g p(30 June 2009)

32

* Others include Indonesia, India, Thailand and Philippines

17

Rights Issue and Dividend Reinvestment Scheme

Strengthened Balance Sheet and

Well‐positioned to capitalise on attractive acquisition opportunities

47% oversubscribed

Raised gross proceeds of approx. $707.6m

649.2m rights shares issued

i id d i h ( )

Strengthened Balance Sheet and Enhanced Financial Flexibility

Higher cash position : $1.2 bn(1)

Lower gearing : 0.23x(1)

Rights Issue

Dividend Reinvestment Scheme (DRS)

Strong shareholder participation

34.3m new shares issued

Enlarged share base : 1.4 bn(1) shares

Larger market capitalisation : $3.8 bn(2)

(1) As at 30 Jun 2009(2) As at 13 Aug 2009

33

Singapore Residential Landbank

A ib bl A ib bl T lP j L i KLL' T Attributable AttributableLand Area GFA

(%) (sf) (sf)

Reflections at Keppel Bay (1) Keppel Bay 30% 99‐yr 269,930 624,521 1,129Marina Bay Suites Marina Bay 33.3% 99‐yr 19,015 156,462 221The Promont Cairnhill Circle 100% Freehold 11,183 31,310 15Keppel Bay Plot 3 Keppel Bay 30% 99‐yr 125,366 152,999 307Keppel Bay Plot 4 Keppel Bay 11.7% 99‐yr 36,114 40,300 234Keppel Bay Plot 6 Keppel Bay 30% 99‐yr 141,429 67,813 94Total 603,037 1,073,405 2,000

Total Units

Project Location KLL's Stake

Tenure

Total 603,037 1,073,405 2,000

(1) Includes units sold

34

18

China Residential Launches

Units to Launch 2009 2010 2011

8 Park Avenue, Shanghai (1) ‐ 90 277

Villa Riviera, Shanghai (1) 20 50 ‐

The Botanica, Chengdu (1) 234 892 1,070

The Arcadia, Tianjin (1) 68 50

Central Park City, Wuxi (1) 169 877 900

Shenyang Township (2) ‐ 560 675

Residential Development, Nanhui, Shanghai (2) ‐ 265 300

Integrated Marina Lifestyle Development Zhongshan (2) ‐ ‐ 343

35

Integrated Marina Lifestyle Development, Zhongshan 343

Stamford City, Jiangyin (1) 22 80 80

Summer Ville, Changzhou (1) 54 ‐ ‐

Serenity Cove, Tianjin (1) 28 100 100

Total 595 2,964 3,745

(1) Balance units ; (2) New launches

Other Overseas Residential LaunchesProject 2009 2010 2011

VietnamThe Estella, Dist. 2, HCMC (1) 60 200 525 (3)

Waterfront Condo, Binh Thanh Dist., HCMC (2) ‐ ‐ 350(2)Riviera Point, Dist. 7, HCMC (2) ‐ 200 300

Prime Condo, Dist. 2, HCMC (2) ‐ ‐ 350Prime Condo, Dist. 9, HCMC (2) ‐ ‐ ‐Riviera Cove (Villa Devt.), Dist. 9, HCMC (2) 20 76 ‐Villa Devt., Dist. 9, HCMC (2) ‐ ‐ 76Saigon Sports City, HCMC (2) ‐ ‐ 355Dong Nai Waterfront City (2) ‐ ‐ 100

ThailandVilla Arcadia at Srinakarin, Bangkok (1) 45 50 50Villa Arcadia at Watcharapol, Bangkok (1) 27 30 30

India

36

Elita Promenade, Bangalore (1) 208 116 ‐Elita Horizon, Bangalore (2) ‐ ‐ 187Elita Garden Vista, Kolkata (1) 316 390 200

IndonesiaJakarta Garden City (1) 308 366 107

Middle EastWaterfront Apartment Devt., Jeddah, Saudi Arabia (2) 300 300 300

Total 1,283 1,728 2,930

(1) Balance units ; (2) New launches; (3) Includes SoHo units

19

China Residential Landbank

Site Location Total TotalLand Area GFA

(%) (sm) (sm)

Remaining Units for

Sale

KLL's Stake

Remaining Area for Sale

(sm)

8 Park Avenue Shanghai 99% 33,432 133,393 65,424 394Park Avenue Central Shanghai 99% 28,488 99,708 99,708 708Villa Riviera Shanghai 99% 153,726 53,796 20,558 70The Arcadia Tianjin 100% 127,970 74,826 52,785 118Central Park City Wuxi 49.7% 352,534 670,510 (2) 437,442 (1) 3,676The Botanica Chengdu 44.1% 419,775 1,042,846 470,488 (1) 5,168Stamford City Jiangyin 76.8% 82,987 301,338 (2) 259,824 (2) 979Shenyang Township Shenyang 100% 338,287 743,847 (2) 705,463 (1) 6,256Residential Devt., Nanhui Shanghai 99% 264,090 332,906 (2) 320,222 (1) 2,676Integrated Marina Lifestyle Devt. Zhongshan 80% 827,641 408,274 402,774 2,855Integrated Marina Lifestyle Devt. Zhongshan 80% 827,641 408,274 402,774 2,855Summerville Changzhou 85.4% 46,108 64,890 7,374 54Serenity Cove (Ph 1 & Ph 2) Tianjin 85.4% 195,170 66,910 8,024 28Total 2,870,208 3,993,244 2,850,086 22,982

(1) Excludes commercial area(2) Includes commercial area

37

Other Overseas Residential LandbankKLL's Total Land Total GFA Remaining Area RemainingStake Area (sm) (sm) for Sale (sm) Units for Sale

India Elita Promenade 51% 96,618 193,237 49,139 324

Elita Horizon 51% 79,177 150,680 150,680 1,138

Elita Garden Vista 37.7% 93,998 195,355 143,978 906Sub‐total 269,793 539,272 343,797 2,368

Country Project

Indonesia Jakarta Garden City, Jarkata ‐ Phase 1 51% 144,510 173,412 113,063 781

Jakarta Garden City ‐ Remaining Phases 758,428 1,283,874 1,052,941 8,117Sub‐total 902,938 1,457,286 1,166,004 8,898

Thailand Villa Arcadia at Srinakarin 45.5% 159,706 84,440 72,564 229

Villa Arcadia at Watcharapol 66.7% 124,912 68,314 81,227 258Sub‐total 284,618 152,754 153,791 487

Vietnam Saigon Sports City, HCMC 90% 640,477 713,222 (1) 290,100 (2) 2,318

The Estella, Dist. 2, HCMC 55% 47,906 279,851 158,917 1,047

Waterfront Condo, Binh Thanh Dist., HCMC 60% 17,428 87,140 74,069 549

Riviera Point, Dist. 7, HCMC 75% 85,118 340,472 289,401 2,394 Dong Nai Waterfront City 50% 3,667,127 1,979,727 (2) 1,576,190 (1) 10,155

Prime Condo, Dist. 2, HCMC 60% 51,000 244,800 166,464 1,500 Villa Devt., Dist. 9, HCMC 55% 135,142 55,746 74,328 177

Prime Condo, Dist. 9, HCMC 55% 62,727 250,908 213,272 1,777

Riviera Cove (Villa Devt.), Dist. 9, HCMC 60% 97,000 35,190 49,492 96 Sub‐total 4,803,925 3,987,056 2,892,233 20,013

Middle East 51% 36,236 253,652 253,652 993 Sub‐total 36,236 253,652 253,652 993

Philippines Palmdale Heights(Ph2), Manila 30.9% 15,976 62,751 62,751 1,264

SM‐KL Residential Devt. Manila 24.2% 7,068 56,000 56,000 430 Sub‐total 23,044 118,751 118,751 1,694

Total 6,320,554 6,508,771 4,928,228 34,453

Waterfront Apartment Devt., Jeddah, Saudi Arabia

(1) Excludes commercial area; (2) Includes commercial area 38

20

Singapore Commercial – K‐REIT AsiaTenant Business Sector by Net Lettable Area as at 30 Jun 2009

Accounting & consultancyShipping & marine

111 tenants in total

Accounting & consultancy services4.0%

Banking, insurance & financial services

35.4%Pharmaceuticals & healthcare

Real estate & property services8.2%

Services9.3%

Shipping & marine services7.4%

Conglomerate8.7%

Government agency7.3%

Hospitality & leisure3.0%

IT services & consultancy5.7%

Others6.6%

4.4%

39

Singapore Residential Developments to benefit from new Downtown Line (DTL)

– Values of properties nearby expected to rise (JLL)

KLL’s Development

Location DTL Station

The Tresor Duchess Road Tan Kah Kee

Madison Bukit Timah Stevens/

( )

Source: LTA as at 13 July 2009DTL 1 & DTL 2 : Its schematic profile, alpha‐numeric codes and end destination numbers are subjected to confirmation

Madison Residences

Bukit TimahRoad

Stevens/BotanicGardens

Interchange

Park Infinia Wee Nam Road

NewtonInterchange

40

21

Strategically located in the Tianjin Binhai New Area

Benefit from the economic vibrancy of the region

Sino‐Singapore Tianjin Eco‐City

41

AwardsBest Annual Report (Gold) at Singapore Corporate Awards

‐Market capitalisation of $1 bn and above

Governance and Transparency Index(1)

R k d 8th t f 677 i‐ Ranked 8th out of 677 companies‐ Only property company placed in Top 10

Five new BCA Green Mark Awards ‐MBFC Ph 2 (Commercial) – Gold Plus ‐Marina Bay Suites – Gold ‐Madison Residences – Gold ‐ The Promont – Gold ‐ One Raffles Quay – Gold (First building to achieve a Green Mark Award under new guidelines for existing developments)

Won six awards at the Asia Pac Property Awards‐Best High‐Rise Development, Residential : Reflections at Keppel Bay ‐ Best Development, Residential : 8 Park Avenue‐ Best Property, Residential : The Arcadia, Tianjin‐ Best Development, Residential : Villa Riviera ‐ Best Mixed‐Use Development, Commercial : Saigon Centre‐ Best Development, Residential : Elita Promenade

(1) Replaced Business Times Corporate Transparency Index42

22

This release may contain statements which are subject to risks and uncertainties that could cause actual results to differ materially from such statements. You are

cautioned not to place undue reliance on such statements, which are based on the current views of Management on future developments and events.

43