Embed Size (px)

DESCRIPTION

Citation preview

December 13, 2012

Investor Day

Mike Waites, President and CEO

Strategic Overview

Executive Team

2

Andy Fraser President

Finning Canada

Dave Smith EVP and CFO

Finning International

Neil Dickinson Managing Director

Finning UK & Ireland

Rebecca Schalm SVP, Human Resources

Finning International

Marcello Marchese President

Finning South America

Juan Carlos Villegas EVP and COO

Finning International

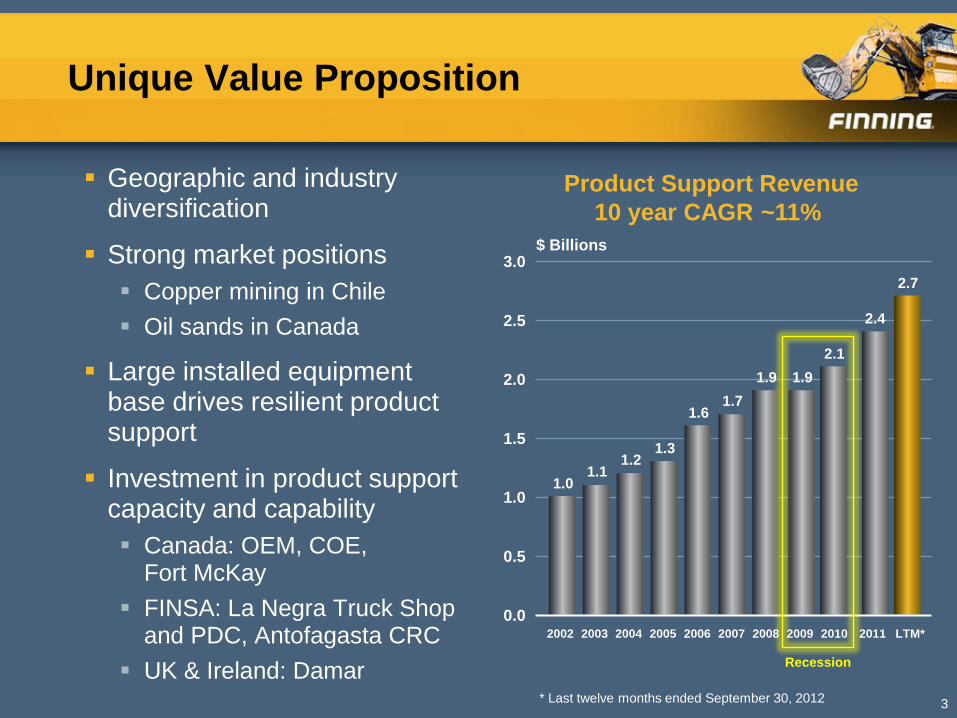

Unique Value Proposition

Geographic and industry diversification

Strong market positions

Copper mining in Chile

Oil sands in Canada

Large installed equipment base drives resilient product support

Investment in product support capacity and capability

Canada: OEM, COE, Fort McKay

FINSA: La Negra Truck Shop and PDC, Antofagasta CRC

UK & Ireland: Damar

3

$ Billions

* Last twelve months ended September 30, 2012

Recession

1.0 1.1

1.2 1.3

1.6 1.7

1.9 1.9

2.1

2.4

2.7

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 LTM*

Product Support Revenue

10 year CAGR ~11%

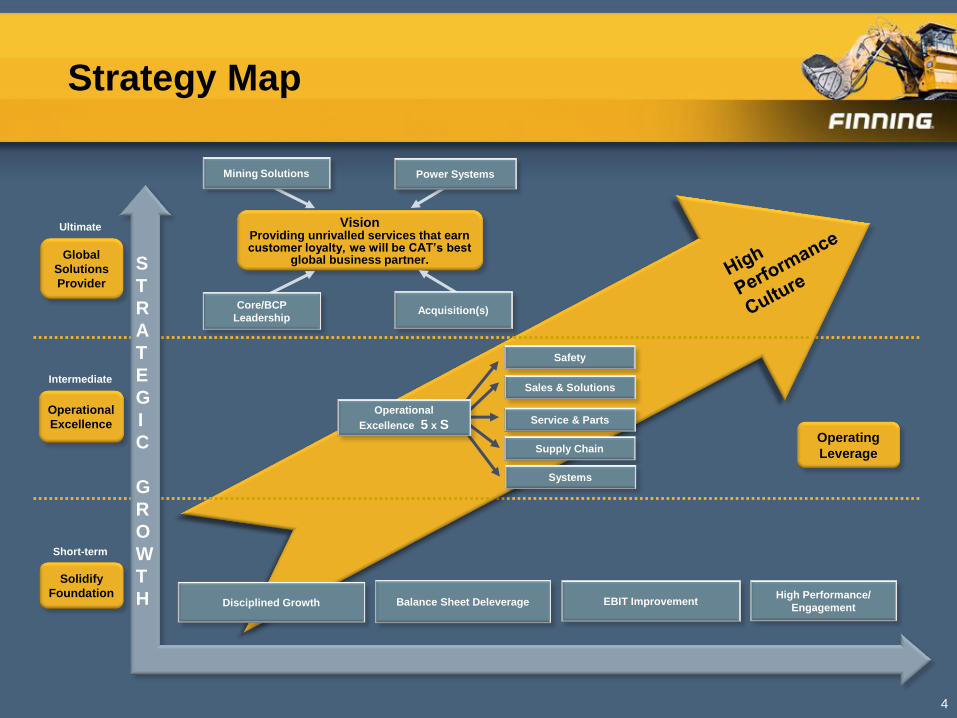

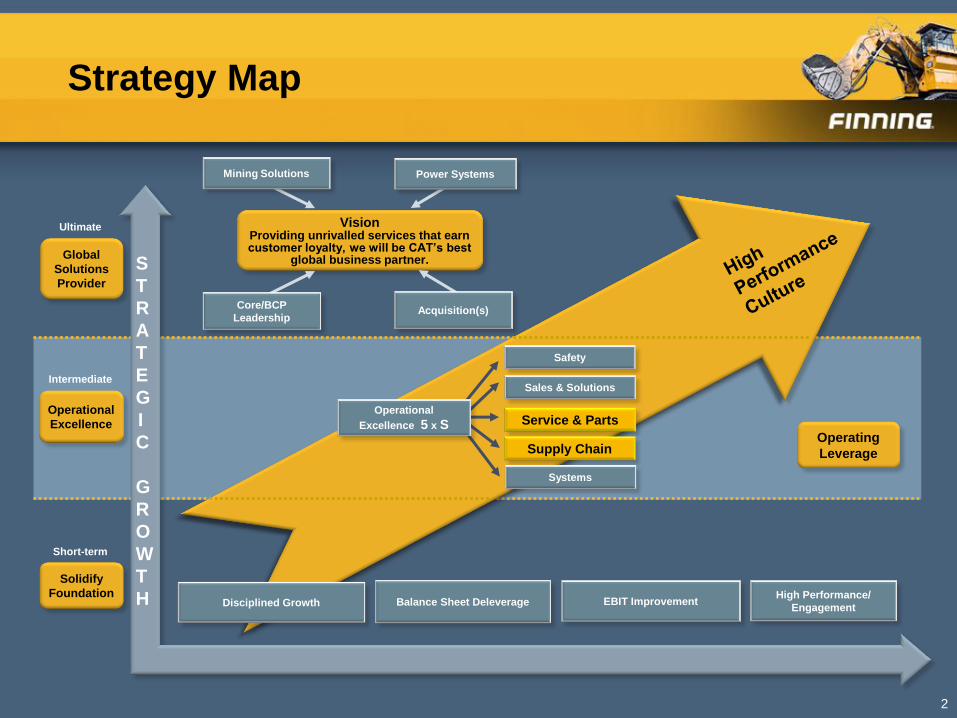

Strategy Map

4

Global

Solutions

Provider

Operational

Excellence

Solidify

Foundation

S

T

R

A

T

E

G

I

C

G

R

O

W

T

H

Vision Providing unrivalled services that earn customer loyalty, we will be CAT’s best

global business partner.

Acquisition(s)

Power Systems

Core/BCP

Leadership

Disciplined Growth EBIT Improvement Balance Sheet Deleverage High Performance/

Engagement

Sales & Solutions

Service & Parts

Supply Chain

Safety

Systems

Mining Solutions

Operating

Leverage

Ultimate

Intermediate

Short-term

Operational

Excellence 5 x S

Meeting our Commitments

5

7.8% in Q3 2012

From (0.3%) in Q3 2011 to 7.8% in Q3 2012

Expect modest net usage of cash in FY12

Expect above target range in 2012

Targets

EBIT margin expansion

9-10% in 2013

Free Cash Flow

Essentially break-even

Net Debt to Total Capital

35 - 45%

Canada business recovery

EBIT margin improvement

Revenue growth

12-15% including Bucyrus Up 19% YTD ending Sep 30, 2012

Ach

ievem

en

ts

Return on Equity

>18% 21.9% LTM ended Sep 30, 2012

Bucyrus

Acquisition and transition Successful; accretive to EPS

Rele

ntl

ess F

ocu

s

Progress

Outlook

Expect constructive business conditions in key markets

Mining to remain active supported by relatively strong oil and copper prices

Uncertain outlook for equipment sales

Customers becoming more cautious, delaying some purchasing decisions

Expect continued strong demand for product support

Large and aging equipment population

Robust level of equipment utilization

6

Revenue Drivers

Product support growth

New products and services

Bucyrus - full suite of mining products

CAT 795 electric drive truck

UK & Ireland Power Systems - Damar, Komptech

Chile - truck dump bodies

New technologies

Remote condition monitoring

C175 engine

Gas fuel substitution

Grow market share as equipment availability has improved

7

Driving Value

Operational excellence focus

Supply chain management

Service productivity and profitability

SG&A improvements

Priorities

Operating leverage

Sequential EBIT margin expansion

Committed to 9-10%

Sustain strong ROE

Drive return on investments made

Strengthen balance sheet

8

Summary

Sustainable competitive advantage

Continued focus on operational excellence

Operating with caution

Driving value in slow growth environment

9

December 13, 2012

Investor Day

Dave Smith, EVP and CFO

Financial Outlook

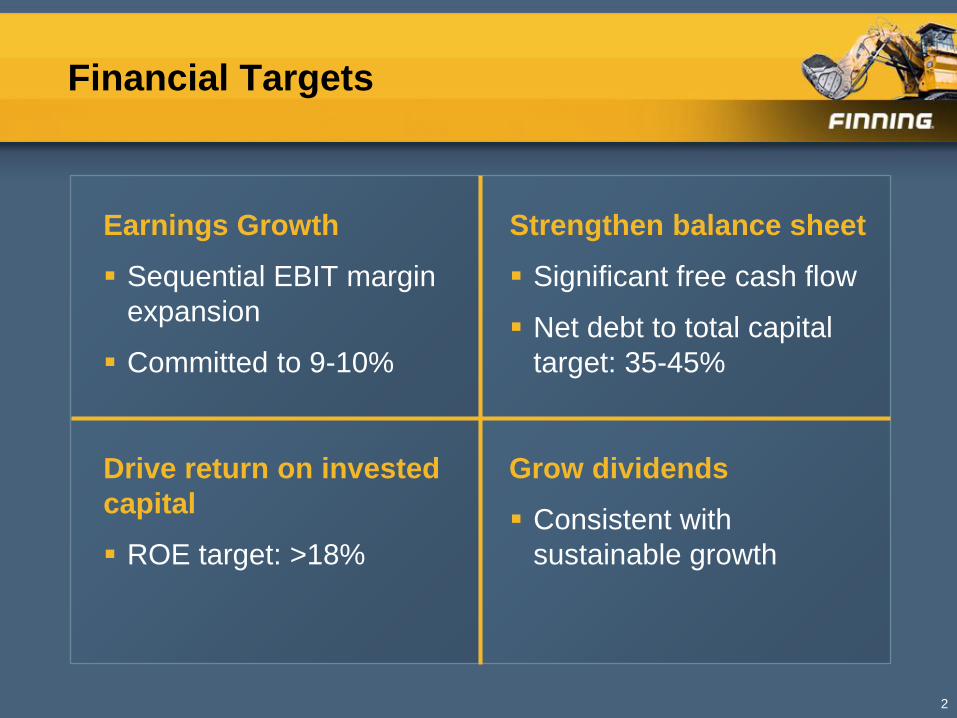

Financial Targets

Earnings Growth

Sequential EBIT margin

expansion

Committed to 9-10%

2

Strengthen balance sheet

Significant free cash flow

Net debt to total capital

target: 35-45%

Drive return on invested

capital

ROE target: >18%

Grow dividends

Consistent with

sustainable growth

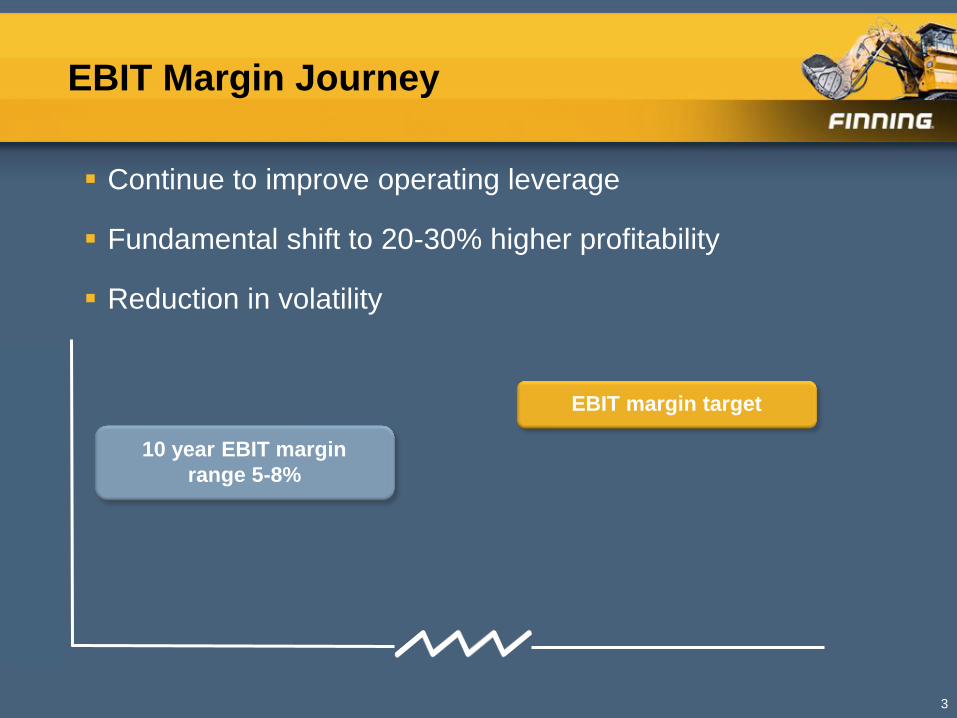

EBIT Margin Journey

Continue to improve operating leverage

Fundamental shift to 20-30% higher profitability

Reduction in volatility

3

EBIT margin target

10 year EBIT margin

range 5-8%

0

10

20

30

40

50

60

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Sep

Net Debt to Total Capital Ratio %

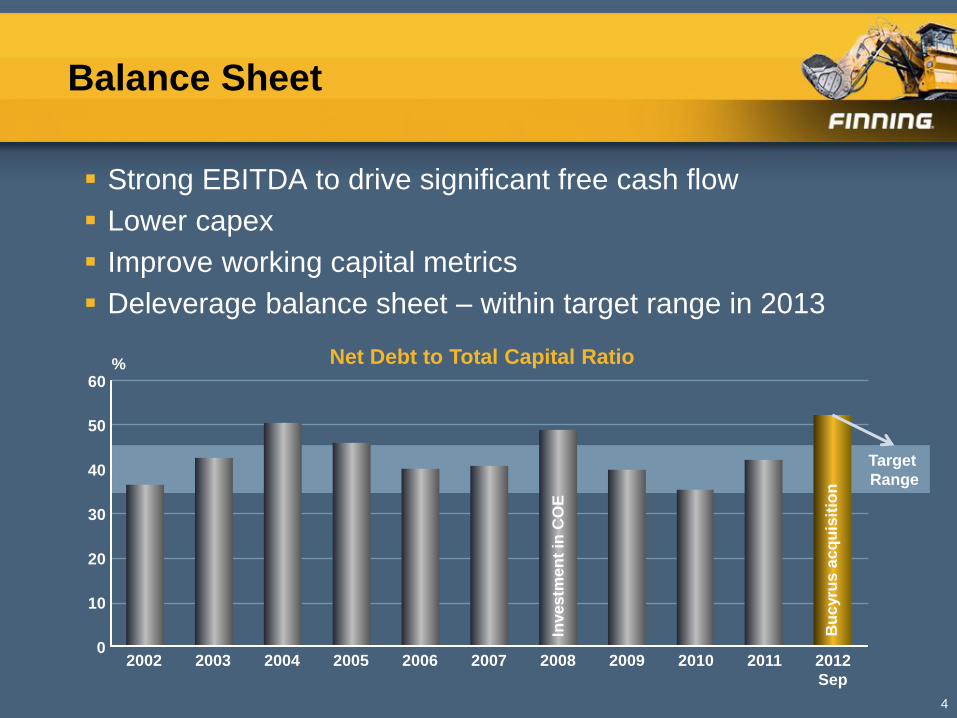

Balance Sheet

Strong EBITDA to drive significant free cash flow

Lower capex

Improve working capital metrics

Deleverage balance sheet – within target range in 2013

4

Target

Range

Bu

cyru

s a

cq

uis

itio

n

Inve

stm

en

t in

CO

E

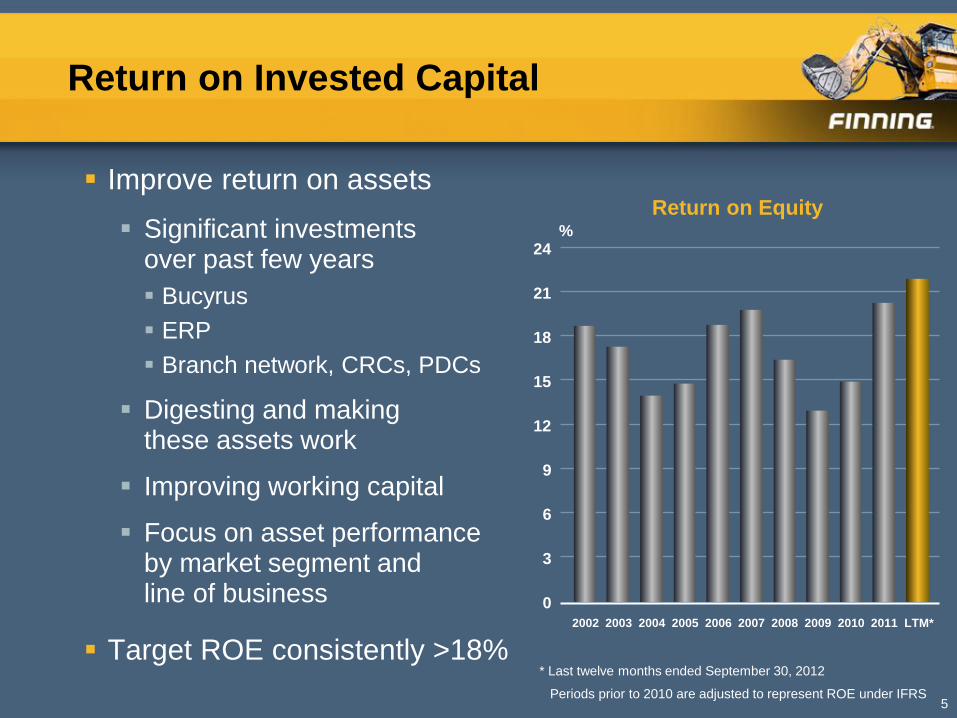

Return on Invested Capital

Improve return on assets

Significant investments over past few years

Bucyrus

ERP

Branch network, CRCs, PDCs

Digesting and making these assets work

Improving working capital

Focus on asset performance by market segment and line of business

Target ROE consistently >18%

5

* Last twelve months ended September 30, 2012

0

3

6

9

12

15

18

21

24

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 LTM*

Return on Equity %

Periods prior to 2010 are adjusted to represent ROE under IFRS

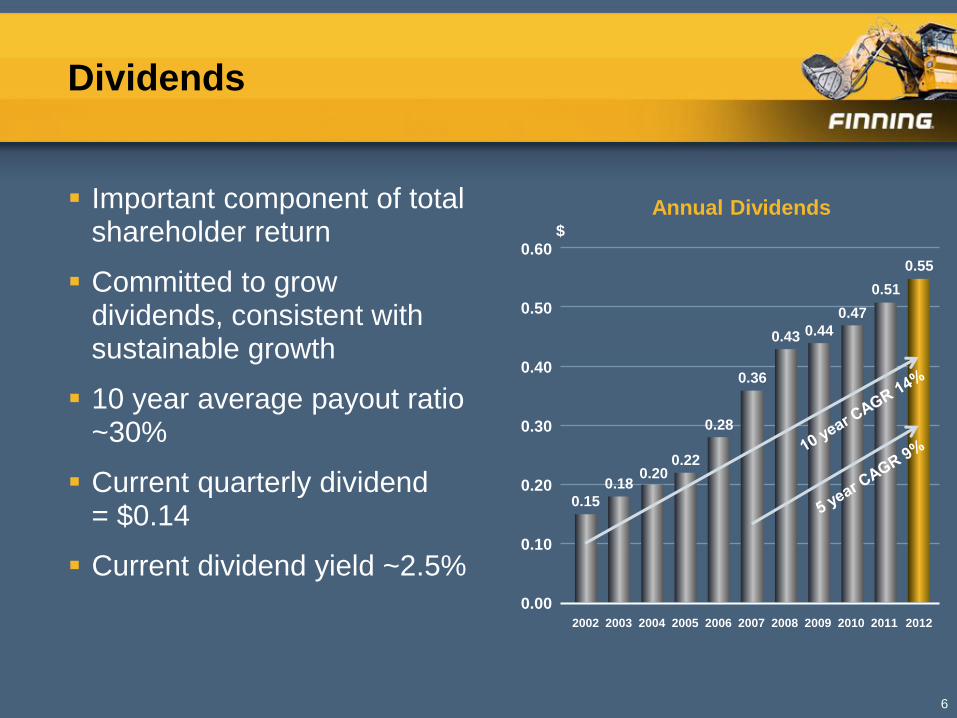

Dividends

Important component of total shareholder return

Committed to grow dividends, consistent with sustainable growth

10 year average payout ratio ~30%

Current quarterly dividend = $0.14

Current dividend yield ~2.5%

6

0.00

0.10

0.20

0.30

0.40

0.50

0.60

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Annual Dividends $

0.15

0.18 0.20

0.22

0.28

0.36

0.43 0.44

0.47

0.51

0.55

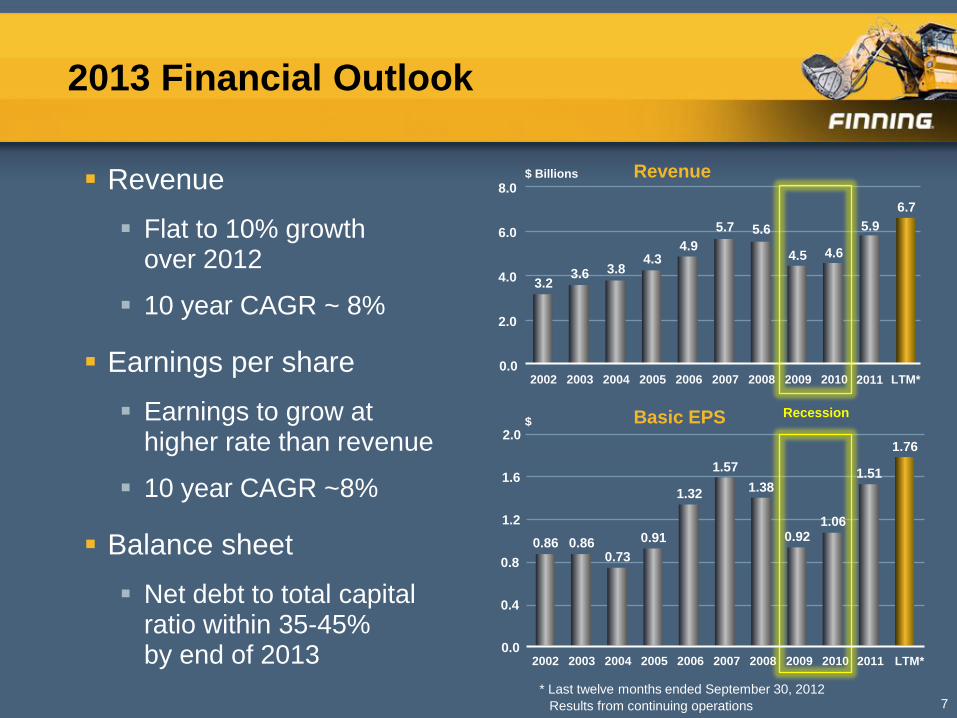

2013 Financial Outlook

Revenue

Flat to 10% growth over 2012

10 year CAGR ~ 8%

Earnings per share

Earnings to grow at higher rate than revenue

10 year CAGR ~8%

Balance sheet

Net debt to total capital ratio within 35-45% by end of 2013

7

$ Billions

* Last twelve months ended September 30, 2012

Revenue

Basic EPS

0.0

2.0

4.0

6.0

8.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 LTM* 2011

0.0

0.4

0.8

1.2

1.6

2002 2003 2004 2005 2006 2007 2008 2009 2010 LTM* 2011

2.0 $

3.2 3.6 3.8

4.3 4.9

5.7 5.6

4.5 4.6

5.9

6.7

0.86 0.86 0.73

0.91

1.32

1.57

1.38

0.92 1.06

1.51

1.76

Recession

Results from continuing operations

Key Financial Focus Areas

Improve earnings growth and quality

Drive return on invested capital

Deleverage balance sheet

Grow dividends

8

December 13, 2012

Investor Day

Juan Carlos Villegas, EVP and COO

Operational Excellence

Strategy Map

2

Global

Solutions

Provider

Operational

Excellence

Solidify

Foundation

S

T

R

A

T

E

G

I

C

G

R

O

W

T

H

Vision Providing unrivalled services that earn customer loyalty, we will be CAT’s best

global business partner.

Acquisition(s)

Power Systems

Core/BCP

Leadership

Disciplined Growth EBIT Improvement Balance Sheet Deleverage High Performance/

Engagement

Sales & Solutions

Service & Parts

Supply Chain

Safety

Systems

Operational

Excellence 5 x S

Mining Solutions

Operating

Leverage

Ultimate

Intermediate

Short-term

Operational Excellence

Maintain local customer focus

Align organizational structure to strategy

Consistently apply leading practices which add value

Leverage expertise of Finning’s regions

Share learning across organization

Focus on margin expansion

3

Customer Centric

Culture

Operational Discipline

and Efficiency

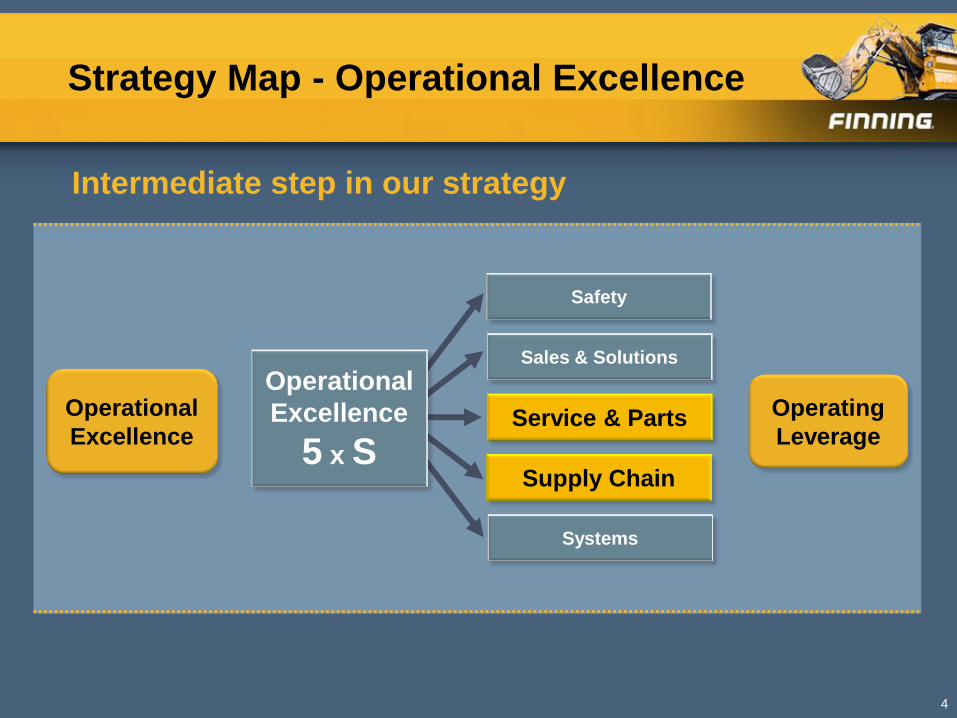

Strategy Map - Operational Excellence

Intermediate step in our strategy

4

Operational

Excellence

Sales & Solutions

Service & Parts

Supply Chain

Safety

Systems

Operational

Excellence

5 x S

Operating

Leverage

Safety

Strong safety performance = solid culture and competitive advantage

Employee opinion on safety scores – top 10% of global organizations

Good example of cultural change and best practices sharing

Embedded process and standardization

5

Lost Time Injuries (LTI) per 200,000 work hours

0

0.5

1.0

1.5

2.0

2.5

02 03 04 05 06 07 08 09 10 12 11

Sales and Solutions

Enhanced focus on market segmentation and analysis

Leveraging power systems leadership globally

New businesses and solutions

Bucyrus

Truck dump bodies

Damar

Komptech

Technology services

Fintech

Finsight

Remote condition monitoring 6

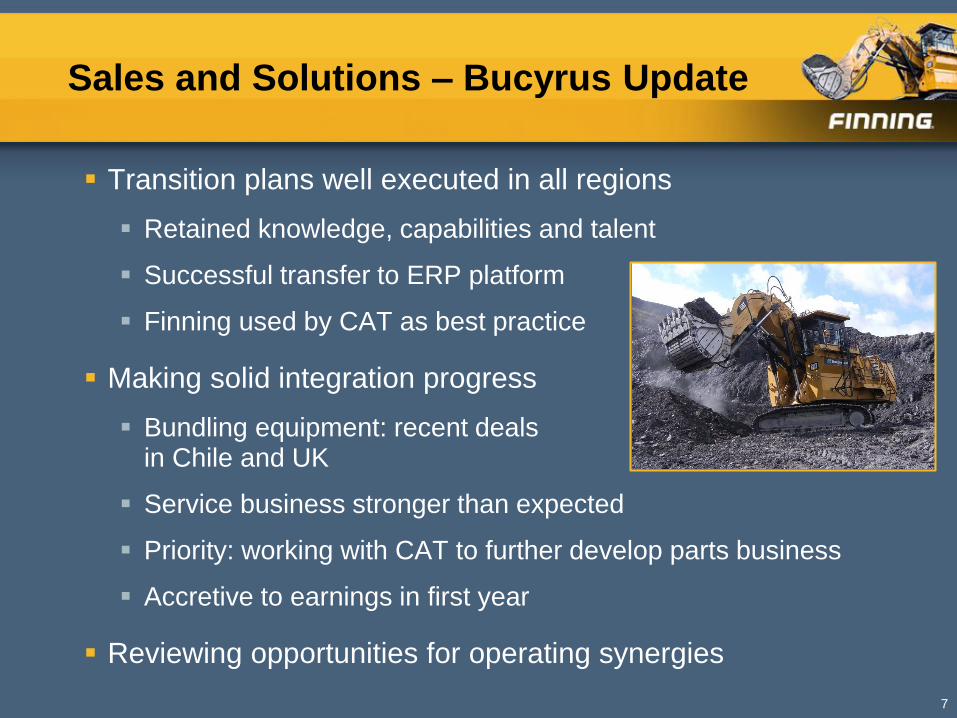

Sales and Solutions – Bucyrus Update

Transition plans well executed in all regions

Retained knowledge, capabilities and talent

Successful transfer to ERP platform

Finning used by CAT as best practice

Making solid integration progress

Bundling equipment: recent deals in Chile and UK

Service business stronger than expected

Priority: working with CAT to further develop parts business

Accretive to earnings in first year

Reviewing opportunities for operating synergies

7

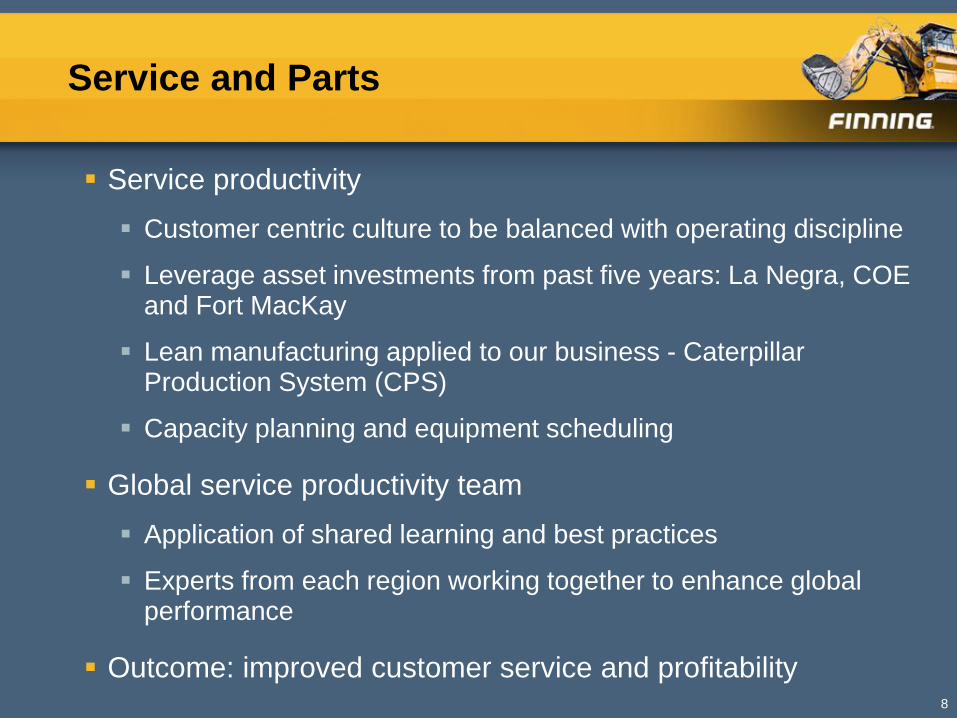

Service and Parts

Service productivity

Customer centric culture to be balanced with operating discipline

Leverage asset investments from past five years: La Negra, COE and Fort MacKay

Lean manufacturing applied to our business - Caterpillar Production System (CPS)

Capacity planning and equipment scheduling

Global service productivity team

Application of shared learning and best practices

Experts from each region working together to enhance global performance

Outcome: improved customer service and profitability 8

Supply Chain

Building sustainable, efficient and consistent supply chain

Standardized, rigorous processes with common metrics

Sharing leading practices across the regions

Regional leads are Global Supply Chain Council members

End-to-end processes include Caterpillar

Improving inventory planning process

Sustainable benefits

Faster inventory turns while maintaining service levels

Shorter cash-to-cash cycle

Reduced working capital levels over business cycle

Improved asset utilization

Improving customer service and satisfaction

9

Systems

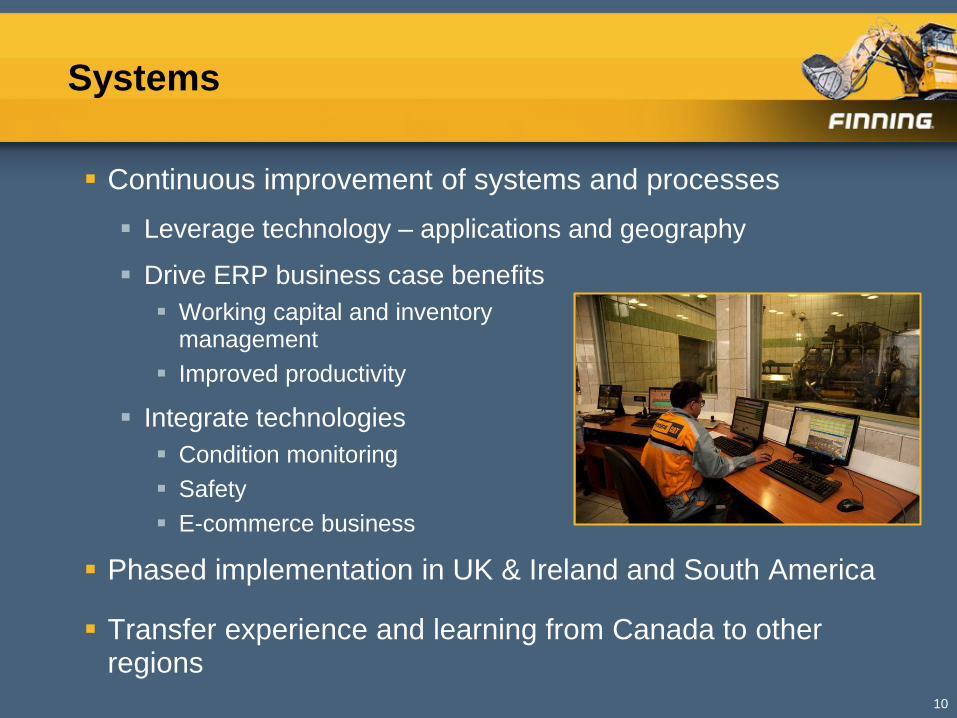

Continuous improvement of systems and processes

Leverage technology – applications and geography

Drive ERP business case benefits

Working capital and inventory management

Improved productivity

Integrate technologies

Condition monitoring

Safety

E-commerce business

Phased implementation in UK & Ireland and South America

Transfer experience and learning from Canada to other regions

10

Summary

Operational excellence across all regions - key driver of sustainable improvement in operating profitability and customer loyalty

Consistent processes transferable and scalable

Focus on largest margin impacts

Supply chain

Service productivity

SG&A improvements

Sharing best practices

Bucyrus integration

Global Supply Chain Council

Global Power Systems 11

December 13, 2012

Investor Day

Andy Fraser, President, Finning Canada

Finning Canada

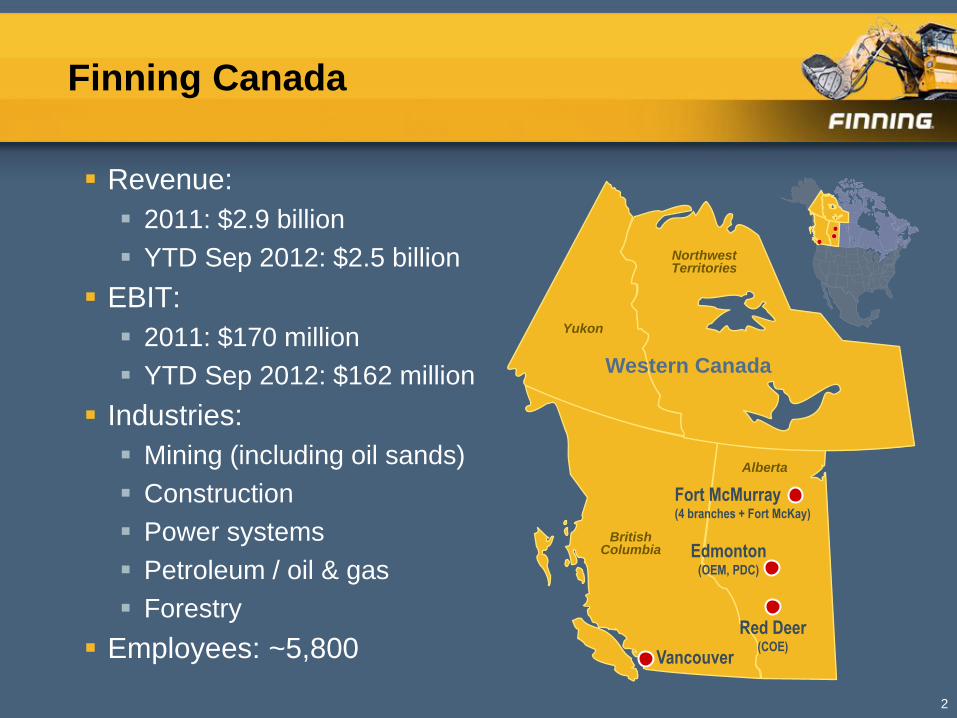

Revenue:

2011: $2.9 billion

YTD Sep 2012: $2.5 billion

EBIT:

2011: $170 million

YTD Sep 2012: $162 million

Industries:

Mining (including oil sands)

Construction

Power systems

Petroleum / oil & gas

Forestry

Employees: ~5,800

2

Vancouver

Edmonton (OEM, PDC)

Fort McMurray (4 branches + Fort McKay)

Western Canada

Red Deer (COE)

British Columbia

Alberta

Yukon

Northwest Territories

Finning Canada Revenue Profile

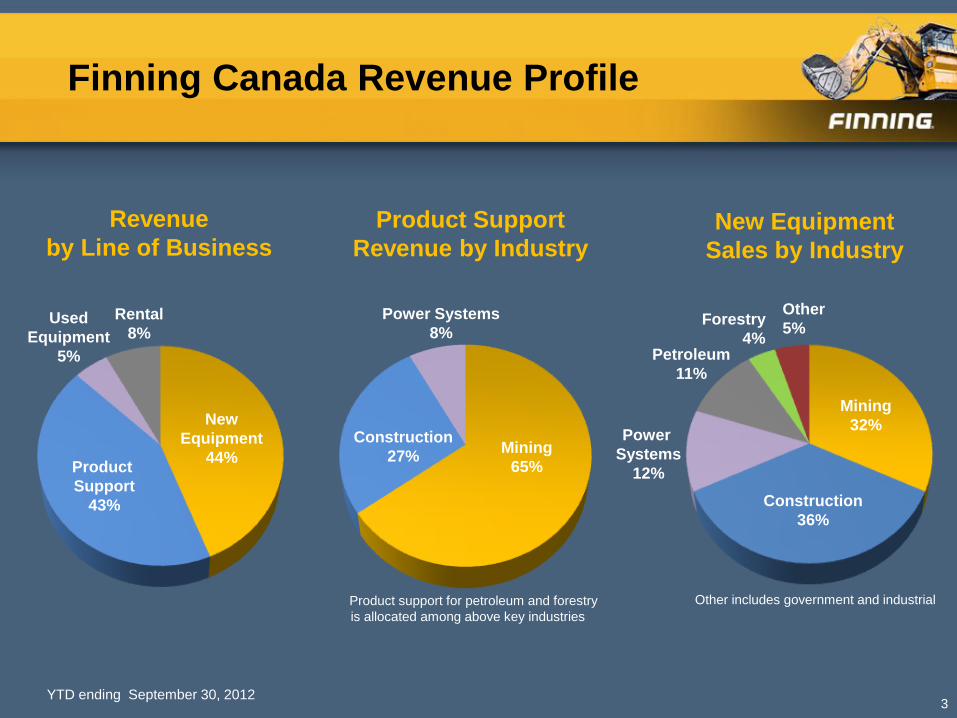

3

Mining

32% Power

Systems

12%

Construction

36%

Mining

65%

Power Systems

8%

Construction

27%

Product Support

Revenue by Industry New Equipment

Sales by Industry

Forestry

4%

Other

5%

Petroleum

11%

Revenue

by Line of Business

New

Equipment

44% Product

Support

43%

Used

Equipment

5%

Rental

8%

Other includes government and industrial Product support for petroleum and forestry

is allocated among above key industries

YTD ending September 30, 2012

Operational Excellence

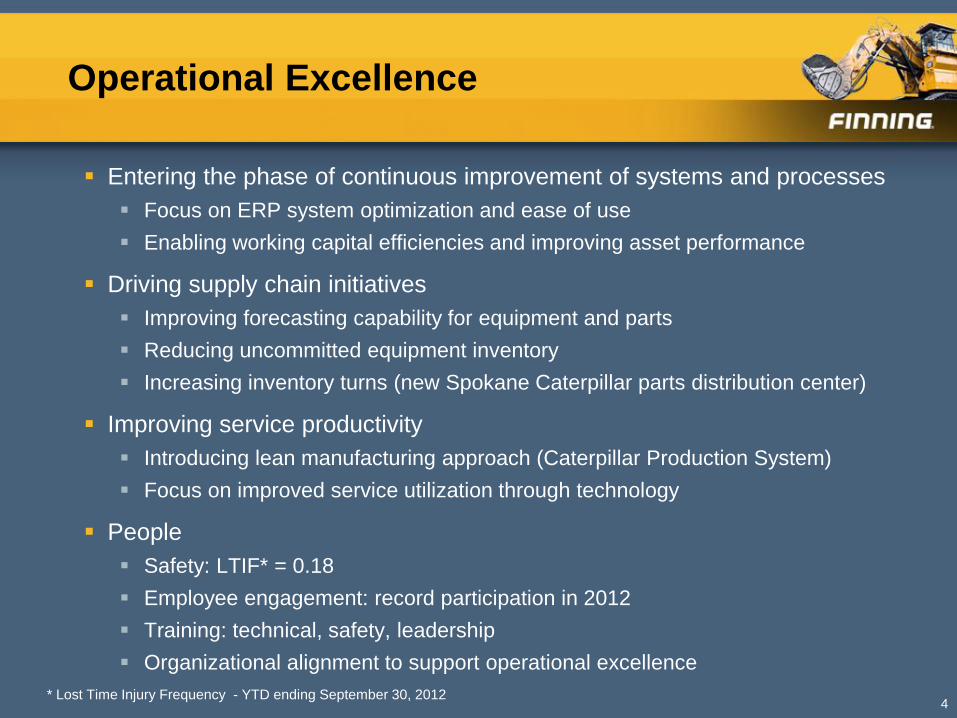

Entering the phase of continuous improvement of systems and processes

Focus on ERP system optimization and ease of use

Enabling working capital efficiencies and improving asset performance

Driving supply chain initiatives

Improving forecasting capability for equipment and parts

Reducing uncommitted equipment inventory

Increasing inventory turns (new Spokane Caterpillar parts distribution center)

Improving service productivity

Introducing lean manufacturing approach (Caterpillar Production System)

Focus on improved service utilization through technology

People

Safety: LTIF* = 0.18

Employee engagement: record participation in 2012

Training: technical, safety, leadership

Organizational alignment to support operational excellence

4 * Lost Time Injury Frequency - YTD ending September 30, 2012

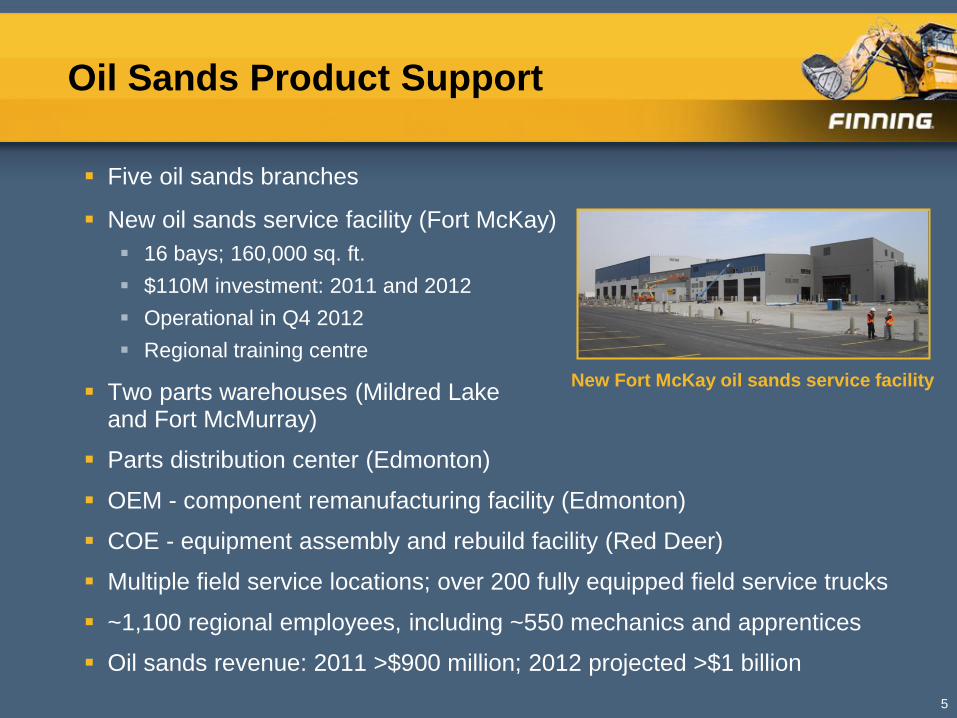

Oil Sands Product Support

Five oil sands branches

New oil sands service facility (Fort McKay)

16 bays; 160,000 sq. ft.

$110M investment: 2011 and 2012

Operational in Q4 2012

Regional training centre

Two parts warehouses (Mildred Lake and Fort McMurray)

Parts distribution center (Edmonton)

OEM - component remanufacturing facility (Edmonton)

COE - equipment assembly and rebuild facility (Red Deer)

Multiple field service locations; over 200 fully equipped field service trucks

~1,100 regional employees, including ~550 mechanics and apprentices

Oil sands revenue: 2011 >$900 million; 2012 projected >$1 billion

5

New Fort McKay oil sands service facility

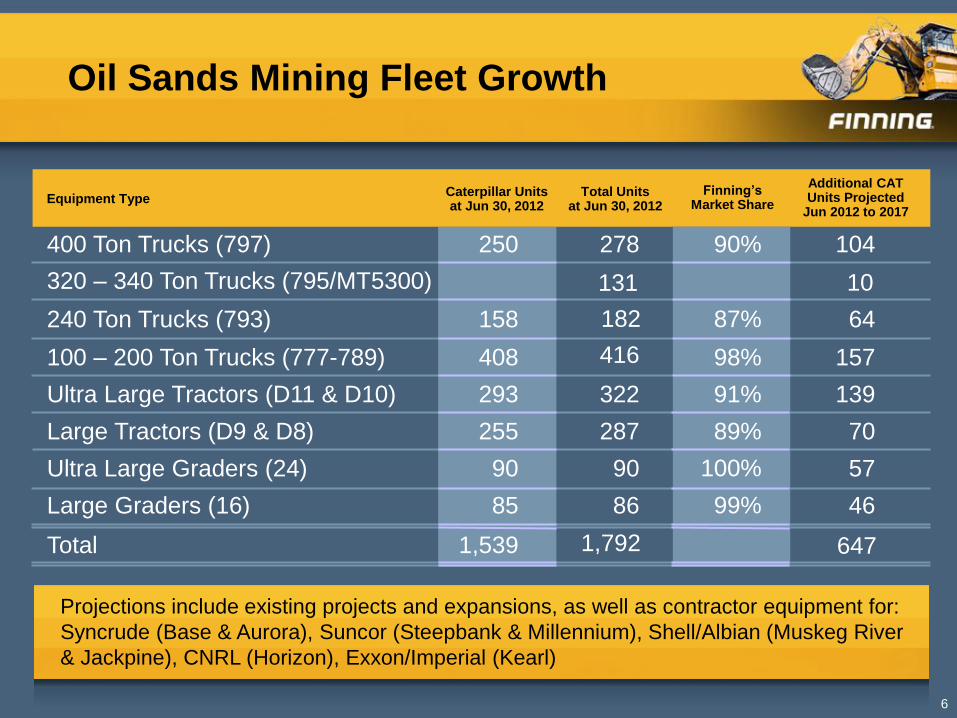

Oil Sands Mining Fleet Growth

6

99%

100%

89%

91%

98%

87%

90%

1,539

85

90

255

293

408

158

250

320 – 340 Ton Trucks (795/MT5300)

Total

Large Graders (16)

Ultra Large Graders (24)

Large Tractors (D9 & D8)

Ultra Large Tractors (D11 & D10)

100 – 200 Ton Trucks (777-789)

240 Ton Trucks (793)

400 Ton Trucks (797)

46

57

70

139

157

64

104

86

90

287

322

416

278

Finning’s Market Share

Caterpillar Units at Jun 30, 2012

Equipment Type Total Units

at Jun 30, 2012

Additional CAT Units Projected

Jun 2012 to 2017

647

131

182

1,792

Projections include existing projects and expansions, as well as contractor equipment for:

Syncrude (Base & Aurora), Suncor (Steepbank & Millennium), Shell/Albian (Muskeg River

& Jackpine), CNRL (Horizon), Exxon/Imperial (Kearl)

10

Construction and Power Systems

Heavy construction

Continued investment in infrastructure

Alberta – ring roads, airports, LRT in Calgary and Edmonton

British Columbia – Evergreen Line Rapid Transit, Coquitlam to Vancouver; Interior to Lower Mainland (ILM) Transmission Project, Nicola to Coquitlam

Numerous pipeline projects in Western Canada through 2020

Forestry

US housing starts improving

Diversified markets

Power systems

Petroleum / oil & gas

Slower activity due to lower well fracturing and servicing

EPG and rental power

Solid demand, particularly in mining

Strong customer value proposition with integrated product offering

7

Opportunities

Sustainable product support growth

Large and aging equipment population

Strong demand for component remanufacturing and machine rebuilds

Fort McKay oil sands facility to support producers and contractors

Oil sands remain active

Mining equipment population for existing projects expected to grow by ~40% over next 5 years

Drills, Shovels & Mining Systems*

Complete mining product offering

Significant product support opportunity

Solid demand from heavy construction and power systems

Gaining market share with improved equipment availability

8 * Former Bucyrus business

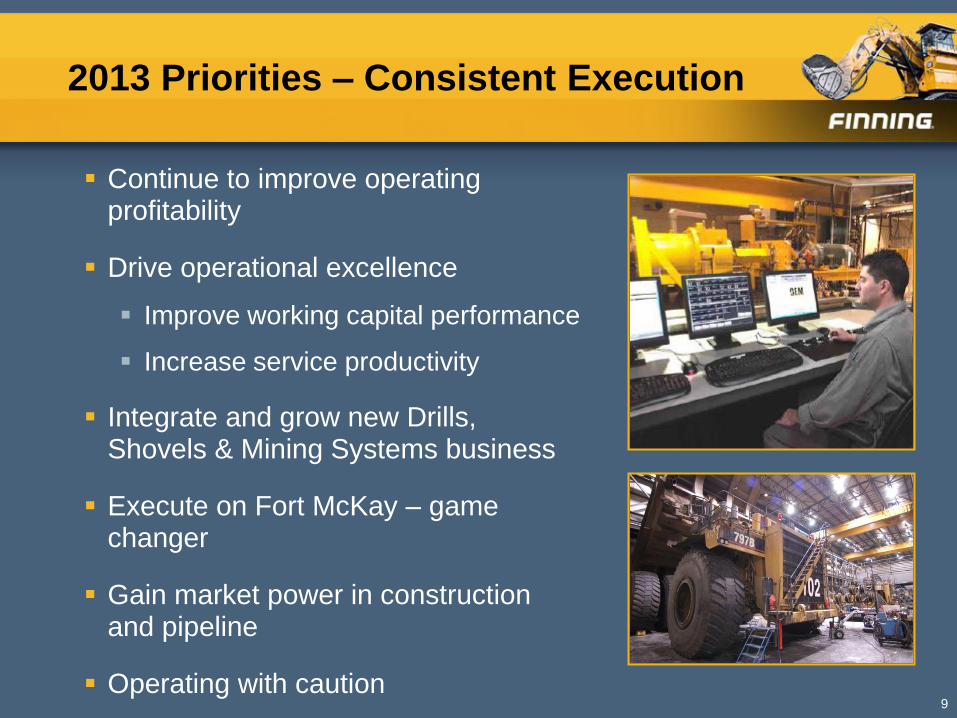

2013 Priorities – Consistent Execution

Continue to improve operating profitability

Drive operational excellence

Improve working capital performance

Increase service productivity

Integrate and grow new Drills, Shovels & Mining Systems business

Execute on Fort McKay – game changer

Gain market power in construction and pipeline

Operating with caution 9

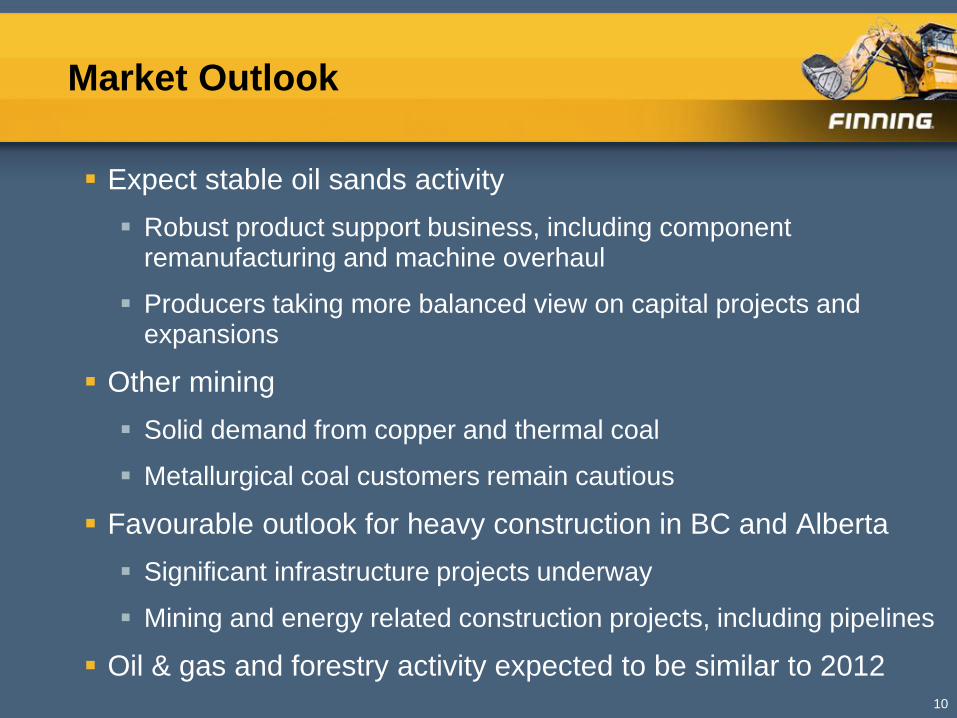

Market Outlook

Expect stable oil sands activity

Robust product support business, including component remanufacturing and machine overhaul

Producers taking more balanced view on capital projects and expansions

Other mining

Solid demand from copper and thermal coal

Metallurgical coal customers remain cautious

Favourable outlook for heavy construction in BC and Alberta

Significant infrastructure projects underway

Mining and energy related construction projects, including pipelines

Oil & gas and forestry activity expected to be similar to 2012 10

Summary

Key markets remain constructive

Capturing revenue opportunities in slow growth environment

Monitoring customer activity closely

Managing business with more conservatism

Leveraging investments to deliver customer value

Growing parts and service business for Drills, Shovels & Mining Systems

Developing and training people

Focus on rigorous and consistent execution

Driving operational excellence

Improving EBIT margin performance

11

December 13, 2012

Investor Day

Marcello Marchese, President, Finning South America

Finning South America

Revenue:

2011: US$2.1 billion

YTD Sep 2012: US$1.7 billion

Chile – 76%, Argentina – 18%,

Bolivia – 4%, Uruguay – 2%

EBIT:

2011: US$195 million

YTD Sep 2012: US$161 million

Industries:

Mining (copper, gold)

Construction / general machinery

Power systems

Employees: ~7,500

2

Revenue

EBIT

282 407

671 832 890

1,240 1,398

1,305

1,622

2,141

0

400

800

1,200

1,600

2,000

2,400

2002 2003 2004 2005 2006 2007 2008 2009 2010 LTM* 2011

2,245

29 43

65 77

96

118

139 134 145

195

0

20

40

60

80

100

120

140

160

180

200

2002 2003 2004 2005 2006 2007 2008 2009 2010 LTM* 2011

216 220

* Last twelve months ended September 30, 2012

US$ Millions

US$ Millions

FINSA Revenue Profile

3

Mining

39%

Power

Systems

13%

Construction

45%

Mining

81%

Power Systems

6% Construction

13%

Product Support

Revenue by Industry New Equipment

Sales by Industry

Other

3%

Revenue

by Line of Business

New

Equipment

44% Product

Support

51%

Used

Equipment

2%

Rental

3%

Other incudes forestry, industrial,

government

YTD ending September 30, 2012

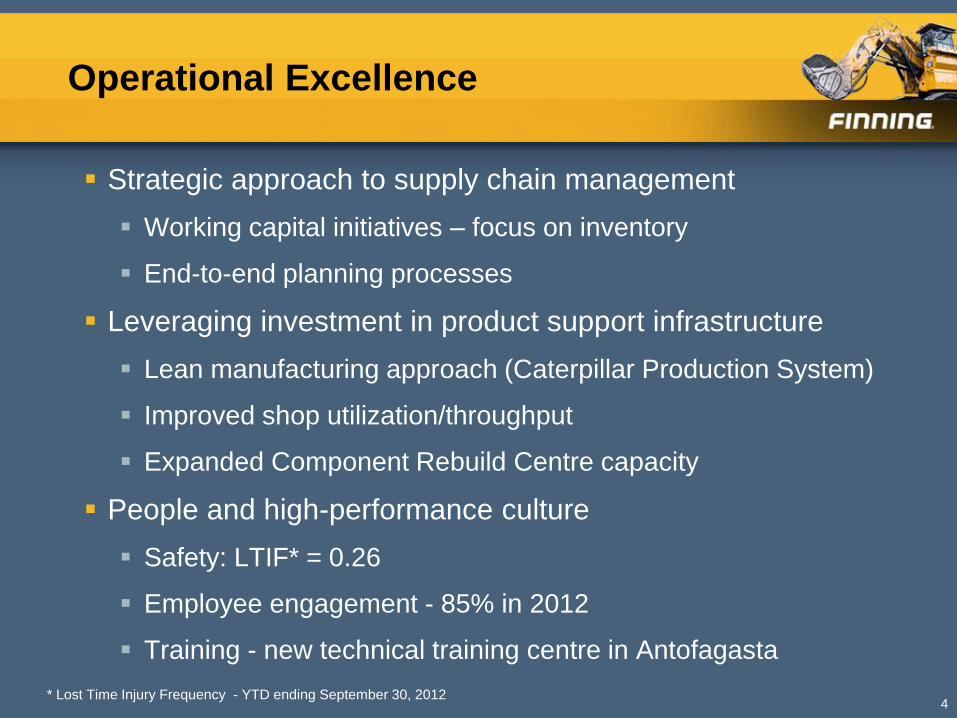

Operational Excellence

Strategic approach to supply chain management

Working capital initiatives – focus on inventory

End-to-end planning processes

Leveraging investment in product support infrastructure

Lean manufacturing approach (Caterpillar Production System)

Improved shop utilization/throughput

Expanded Component Rebuild Centre capacity

People and high-performance culture

Safety: LTIF* = 0.26

Employee engagement - 85% in 2012

Training - new technical training centre in Antofagasta

4 * Lost Time Injury Frequency - YTD ending September 30, 2012

Chilean Mining

Chilean mining investment projected at ~US$ 70 billion over next 5 years*

Strong mining outlook balanced by industry growth challenges:

Shortages of skilled people

Environmental considerations (e.g. fresh water consumption)

Energy requirements

Strong and growing product support business

19 MARC and LPP contracts covering 60-70% of equipment population

Mining product support market share ~90%

Robust mining projects portfolio

Large and expanding machine population

Mining equipment market share 50-60%

5 * Source: Cochilco

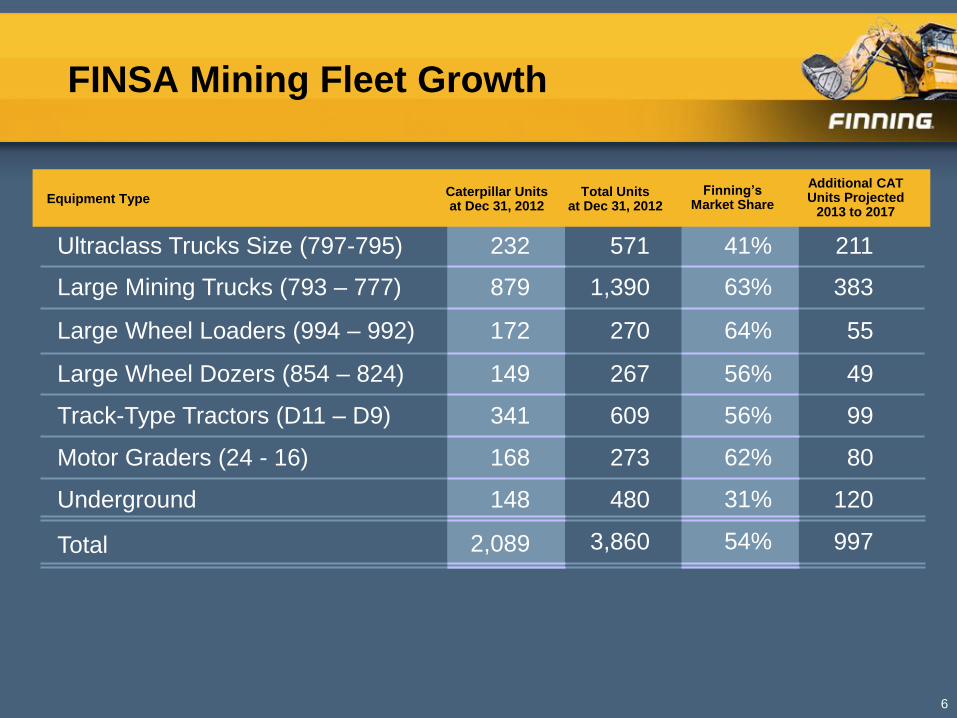

FINSA Mining Fleet Growth

54%

31%

62%

56%

56%

64%

63%

41%

879

149

172

232

Large Mining Trucks (793 – 777)

Total

Underground

Motor Graders (24 - 16)

Track-Type Tractors (D11 – D9)

Large Wheel Dozers (854 – 824)

Large Wheel Loaders (994 – 992)

Ultraclass Trucks Size (797-795)

383

997

120

80

99

49

55

211

1,390

3,860

480

273

609

267

270

571

6

Finning’s Market Share

Caterpillar Units at Dec 31, 2012

Equipment Type Total Units

at Dec 31, 2012

Additional CAT Units Projected

2013 to 2017

2,089

148

168

341

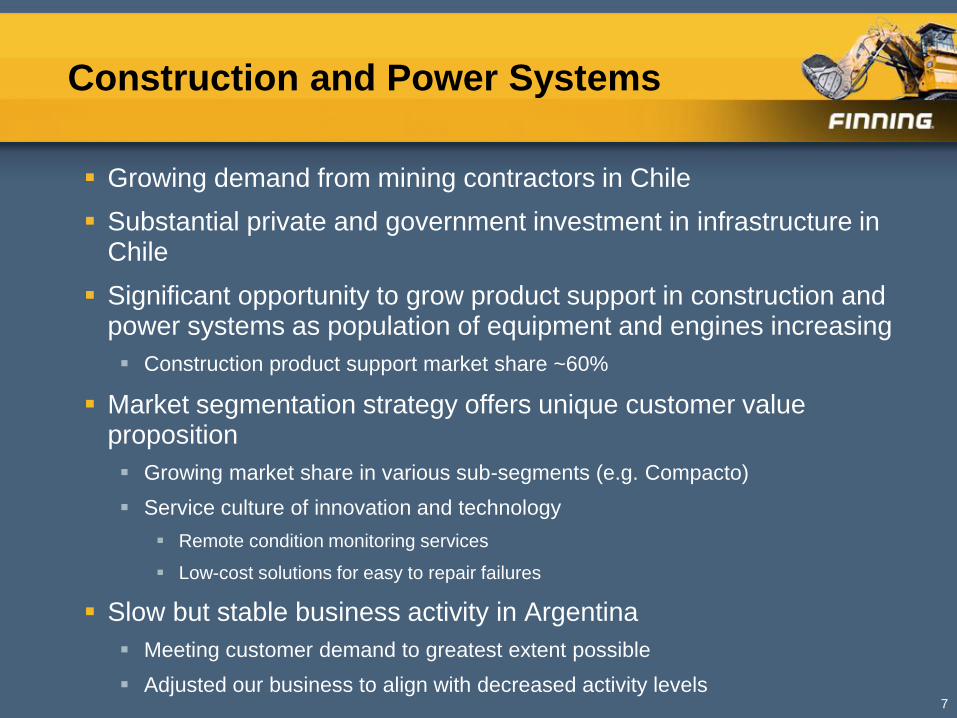

Construction and Power Systems

Growing demand from mining contractors in Chile

Substantial private and government investment in infrastructure in Chile

Significant opportunity to grow product support in construction and power systems as population of equipment and engines increasing

Construction product support market share ~60%

Market segmentation strategy offers unique customer value proposition

Growing market share in various sub-segments (e.g. Compacto)

Service culture of innovation and technology

Remote condition monitoring services

Low-cost solutions for easy to repair failures

Slow but stable business activity in Argentina

Meeting customer demand to greatest extent possible

Adjusted our business to align with decreased activity levels

7

Opportunities

Mining growth supported by healthy copper prices

Mining equipment population expected to increase significantly over next 5 years

Continued strong demand for product support

Bucyrus

Unique opportunity to offer complete mining solution

Significant product support opportunity

New products and businesses

795 electric drive truck

Fabrication of truck bodies

METSO mobile crushers

Technology products and services

Solid demand from construction and power systems customers in Chile

8

2013 Priorities – Consistent Execution

Drive operational excellence

Supply chain end-to-end integration

Grow Bucyrus business

Balance product support growth with efficiencies

Manage the business with caution in light of macro-economic uncertainty

9

Market Outlook

Positive long-term fundamentals as copper prices remain high by historical standards

Expect Chilean mining to continue to be very active

Solid activity in existing operations

Continued strong demand for product support

Caution on new projects and expansions

Positive outlook for construction and power systems in Chile, Bolivia and Uruguay

2013 – election year in Chile

Economic environment in Argentina expected to remain largely unchanged

10

Summary

Strong outlook for Chile

Mining investment presents big opportunities

Solid order intake and strong demand for product support

Infrastructure spend to support construction and power systems business

Capturing growth opportunities with Bucyrus and 795 electric drive truck

Driving operational excellence

Focus on supply chain

Leveraging product support capabilities

Improving EBIT margin performance

11

December 13, 2012

Investor Day

Neil Dickinson, Managing Director, Finning UK & Ireland

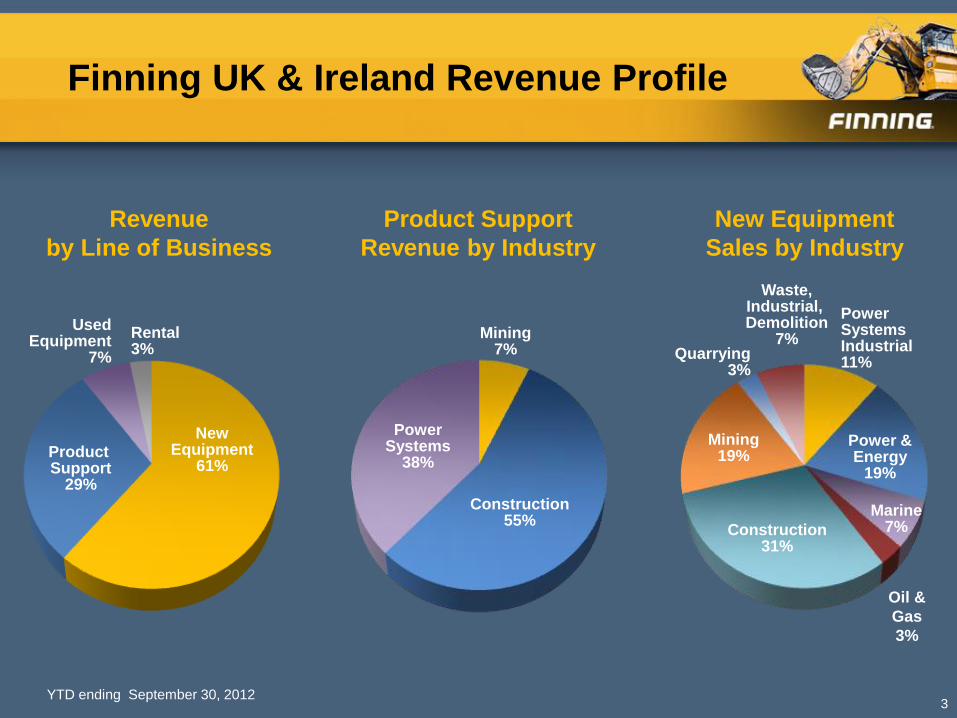

Finning UK & Ireland

Revenue:

2011: $831 million

YTD Sep 2012: $684 million

EBIT:

2011: $52 million

YTD Sep 2012: $40 million

Segmented approach

Equipment Solutions

Power Systems

Employees: ~1,800

2

Finning Cat

Cat Compact Dealers

Ag Dealers

Finning UK & Ireland Revenue Profile

3

Power Systems

38%

Construction 55%

Product Support

Revenue by Industry

New Equipment

Sales by Industry

Mining 7%

Revenue

by Line of Business

New Equipment

61% Product Support

29%

Used Equipment

7%

Rental 3%

Power Systems Industrial 11%

Power & Energy

19%

Marine 7%

Oil &

Gas

3%

Construction 31%

Mining 19%

Quarrying 3%

Waste, Industrial, Demolition

7%

YTD ending September 30, 2012

Clear Strategic Roadmap Trusted by Experts

4

Solutions

Provider

Operational

Excellence +

Profitable

Growth

Solidify

Foundation

Specialised

Engineering &

Technology Dominate Mining,

Power & Core

Product Support

Growth Beyond Core

Expand Into

Growing Markets

Sitech + Finning

Technologies

Grow & Develop

Power Systems

Scope

Product Support +

Reman Growth

Supply Chain +

Procurement

Bucyrus

MWM

Leadership

Programme

Implemented

Rollo Acquired

Panorama &

Operational

Excellence

Safety Simplified

New Finning UK

‘Trusted’ Strategy

UK Business Model

EBIT% Improvement

All Makes Managed

Services

BCP & Core

Agreements

#1 for Service &

Loyalty

C

A

T

S

T

R

A

T

E

G

I

C

CPS* & OPERATIONAL EXCELLENCE

* Caterpillar Production System

Execution on Strategy in 2012

Acquired Damar - specialised engineering

business; completed £7m anaerobic

digestion plant

Acquired Bucyrus – 6 shovels sold in year 1

Acquired distribution rights to Komptech

products – total solution for recycling sector

Established “Managed Services “ capability

Caterpillar Gas (MWM) products added and

Finning recognised as Perkins Gas Centre

of Excellence for Western Europe and

Scandinavia

Finsight launched

Recognised as leader in safety

Continue to focus on higher margin / added

value opportunities

5

Operational Excellence Strategic Focus

Driving supply chain initiatives

Outsourced national distribution centre

Revised ordering processes - Lane 1

Focused on EBIT margin improvement

Focus on SG&A

Review procurement contracts

Defined benefit pension plan closed

Headcount rationalisation

Utility costs

Caterpillar Production System (CPS) – eliminating waste

6

Operational Excellence Strategic Focus

People and high-performance culture

Safety – national award winners

Employee engagement - 82% in 2012

Training

“Developing Great Leaders” course

Finning Academy in top 100 UK schemes

Market segmentation

Customer loyalty / service productivity

Top 2 for Customer Loyalty in Caterpillar

Awarded Gold Service Excellence from Caterpillar

Finsight / Managed Services

7

Market Outlook 2013

Equipment Solutions – market size down 10%

Mining impacted by weak coal prices

Limited investment in quarry and aggregates

Government investment – rail and energy, possibly housing

Industrials slowing

Small machines – niche markets

Power Systems – mixed growth

Oil & Gas

Increased product range in Gas Electric Power

Marine

Renewables / clean power

8

UK & Ireland Opportunities Equipment Solutions

Mining and energy

Underground via Bucyrus

Legacy products

Tungsten mine

Quarrying and industrial

Managed Services

Market share gains

Machine age increasing

Waste and recycling

Komptech complementary products

Growth in Materials Recovery Facilities

Plant hire and agriculture

Developing dealer network

Market share gains – 20,000 unit market

9

UK & Ireland Opportunities Power Systems

Power and energy

Mission critical diesel – hospitals, data centres

Water treatment industry

Expanded capability and products

Oil & Gas

North Sea resurgence

Flameproof technology

Managed services contracts - BP

Marine

International opportunity

Offshore wind farms

Pleasure craft

Industrial and Perkins

Center of Excellence for Perkins Gas

60% market share rock crushers – 1,500 engines 10

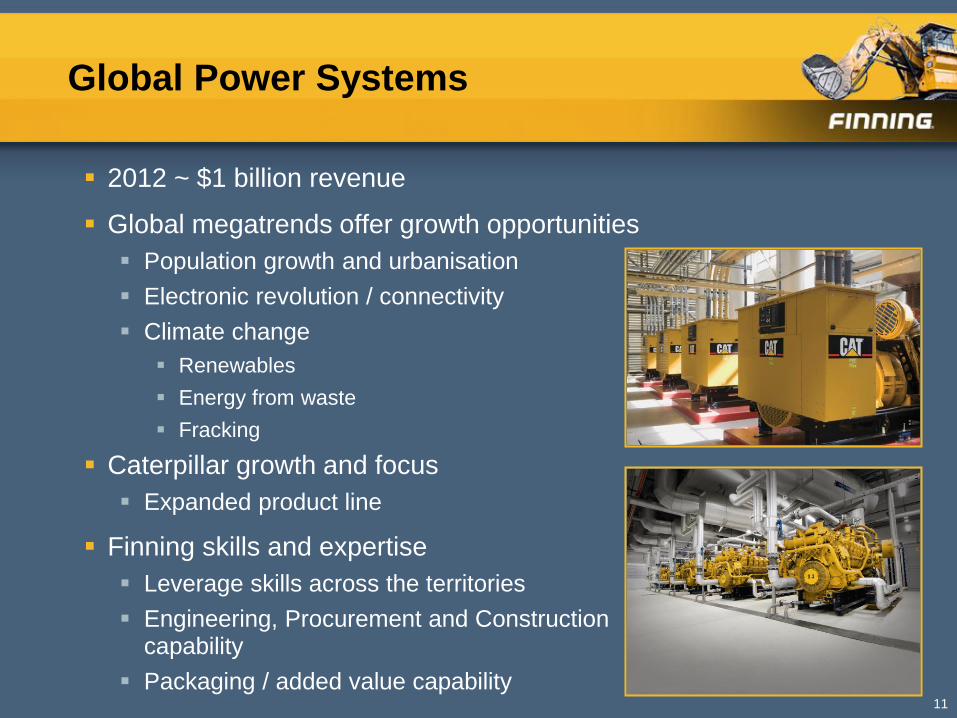

Global Power Systems

2012 ~ $1 billion revenue

Global megatrends offer growth opportunities

Population growth and urbanisation

Electronic revolution / connectivity

Climate change

Renewables

Energy from waste

Fracking

Caterpillar growth and focus

Expanded product line

Finning skills and expertise

Leverage skills across the territories

Engineering, Procurement and Construction capability

Packaging / added value capability 11

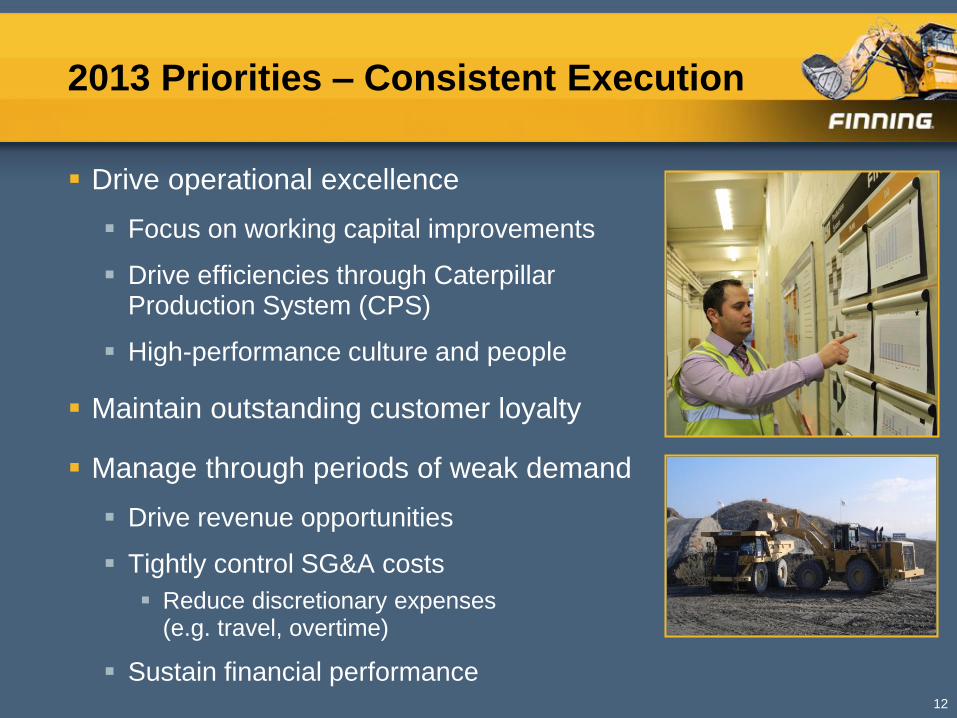

2013 Priorities – Consistent Execution

Drive operational excellence

Focus on working capital improvements

Drive efficiencies through Caterpillar Production System (CPS)

High-performance culture and people

Maintain outstanding customer loyalty

Manage through periods of weak demand

Drive revenue opportunities

Tightly control SG&A costs

Reduce discretionary expenses (e.g. travel, overtime)

Sustain financial performance 12

Summary

Drive maximum value from the strategic acquisitions

Total focus on operational excellence

Deliver financial performance

Build talent and high performance culture

Stick to the strategy - Trusted by Experts

Focus on added value growth

Power Systems and product support growth

Diversified business

13

December 13, 2012

Investor Day

Mike Waites, President and CEO

Summary

Business Conditions

Market conditions and customer confidence vary by region

Canada – stable activity levels; uncertain outlook

South America – positive long-term fundamentals; solid outlook

UK & Ireland – challenging economic landscape; some pockets of

strength

Operating with caution

Monitoring business activity closely

Taking prudent steps to manage business with more conservatism

Reducing uncommitted inventory

Carefully managing new orders

Controlling SG&A expenses

2

2013 Priorities – Consistent Execution

3

Drive revenue in slow growth environment

Focus on operational excellence

Supply chain management

Service productivity

SG&A improvements

Improve operating profitability and return on invested capital

EBIT margin - sequential expansion

Leverage latest investments

Lower capex and disciplined net rental additions

Strengthen balance sheet