Embed Size (px)

Citation preview

2005

Morgan Stanley Investment Management

Investment Management Journal

01 Asset-liability risks and portable alphaJohn S. Coates, Ph.D., CFA—Managing Director

Every so often, there is a development in the world of finance that results in a major paradigm shift. Currently, we find ourselves in the midst of a very unusual situation in which three such shifts are emerging simultaneously. Each can have a significant impact on the management of the investment portfolios of pensionfunds, endowments and foundations.

09 Emerging markets: All grown up? Paul Psaila, CFA—Executive Director

Emerging market equities have been among the best performing asset classes over the last few years. This has led observers to wonder whether this current bout of outperformance will again end in tears or if the emerging markets have moved on to a more mature plane. We lean toward the latter of these two scenarios, as we believe emerging markets are well into a stage we would characterize as “young adulthood.”

15 The case for a strategic allocation to global real estate securitiesTed Bigman—Managing Director Christina Chiu—Associate

Real estate has gained increased acceptance among institutional investors as a distinct asset class that deserves a permanent strategic allocation in a multi-asset classportfolio. However, only a limited number have incorporated international exposureinto their overall real estate allocations. We believe the global real estate market has evolved such that institutional investors would benefit from a strategic allocation to global real estate, particularly through the listed property markets.

35 Countdown conundrumJoseph McAlinden, CFA—Managing DirectorWarren Hatch, Ph.D., CFA—Vice President

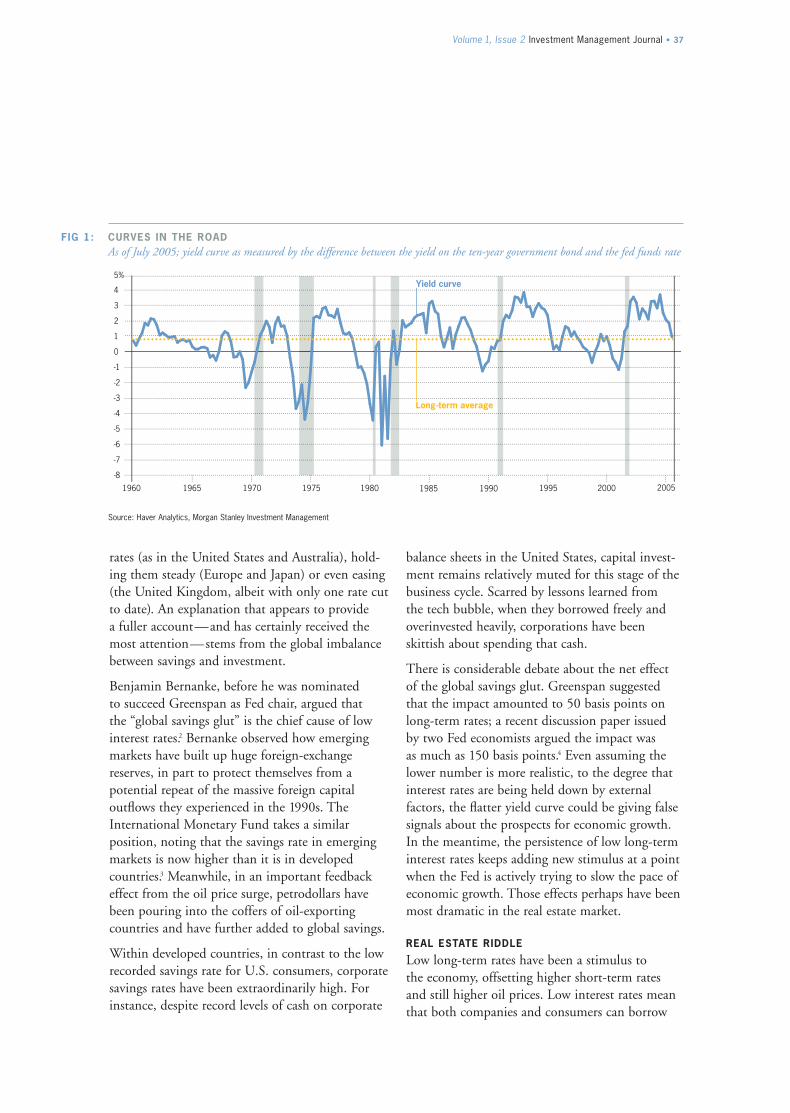

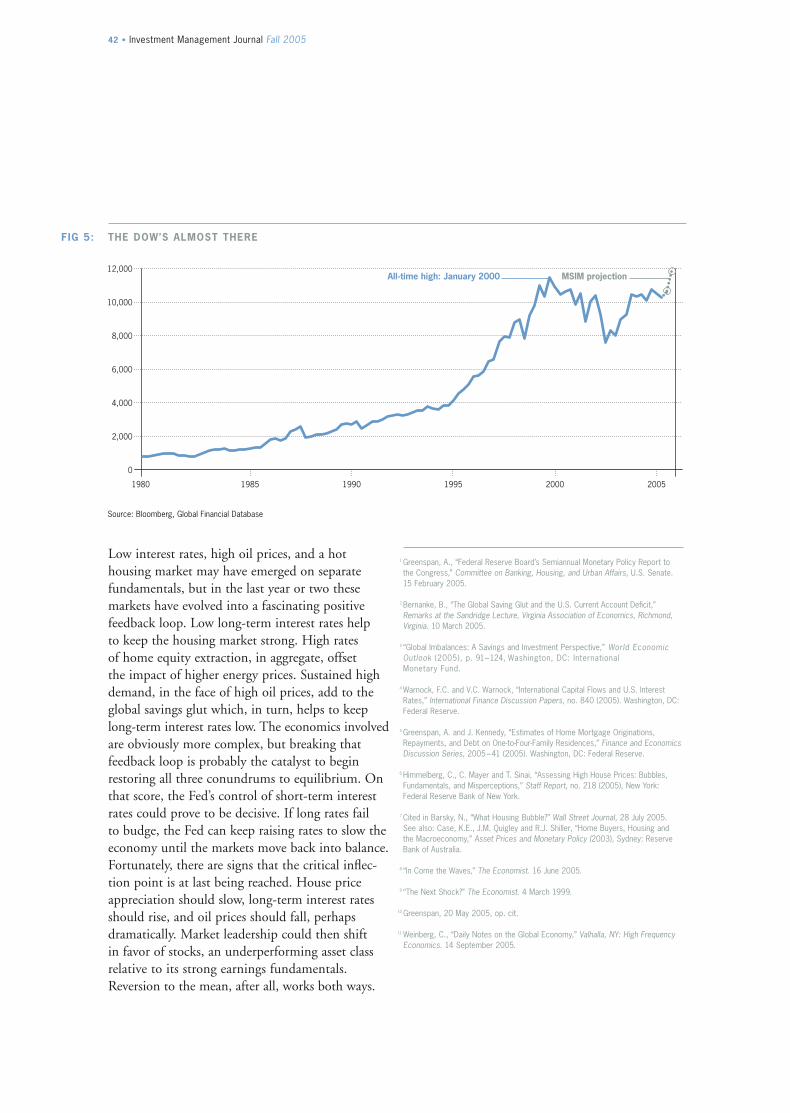

Low long-term interest rates, high oil prices and a red-hot housing market have been the dominant themes in the current business cycle for a surprisingly long time. Their return to equilibrium as the fundamentally strong economic expansionmatures could offer new opportunities for other asset classes, particularly U.S. common stocks.

Volume1

Issue 2

IS05-01016F-N11/05

© 2005 Morgan Stanley. Investments and services are offered throughMorgan Stanley DW Inc., member SIPC.

Morgan Stanley Investment Management (“MSIM”) is the asset managementdivision of Morgan Stanley. Assets are managed by teams representing differentMSIM legal entities with offices in New York, Philadelphia, Houston, Chicago,London, Amsterdam, Singapore, Tokyo and Mumbai.

LITRAK: MSIM

JRNL 12/05

CLF: 79527

Please direct any comments or questions about theMorgan Stanley Investment Management Journal to:

Daniel P. DonnellyManaging [email protected]

ABOUT THE AUTHORS

John S. Coates, Ph.D., CFA Managing DirectorJack is co-business group head of Morgan Stanley AIP.He joined Morgan Stanley AIP in 2000 and has morethan 20 years of investment experience. Jack receivedboth a bachelor’s and a master’s degree in aerospace engineering from the Georgia Institute of Technology.He received an M.B.A. as a Wharton Fellow from the University of Pennsylvania and a Ph.D. from theUniversity of Washington.

Paul Psaila, CFAExecutive DirectorPaul is a portfolio manager for the Emerging MarketsEquity portfolios, focusing on global analytics. Hejoined Morgan Stanley in 1994 and has 11 years ofinvestment experience. Paul received a B.A. in politicalscience from Brandeis University and a master’s degreein economics and Latin American studies from the School of Advanced International Studies of Johns Hopkins University.

Ted BigmanManaging DirectorTed is head of Global Real Estate Securities, the firm’sreal estate securities investment management business.He joined Morgan Stanley in 1995 and has 18 years ofinvestment experience. Ted received a B.A. in economicsfrom Brandeis University and an M.B.A. from HarvardBusiness School.

Christina Chiu AssociateChristina is a securities analyst on the Global RealEstate Securities team, responsible for research and analytical support for the firm’s real estate securitiesinvestment management business. She joined MorganStanley in 2002 and has three years of investment experience. Christina received a B.S. summa cum laudein finance and accounting from New York University’sStern School of Business.

Joseph McAlinden, CFA Managing DirectorJoe is chief investment officer, directing the daily activities of the firm’s investment department. He joinedMorgan Stanley in 1995 and has more than 30 years of investment experience. Joe received a B.A. cum laudein economics from Rutgers University.

Warren Hatch, Ph.D., CFA Vice PresidentWarren is an investment strategist and co-portfoliomanager of the Allocator Fund. He joined MorganStanley in 1999 and has six years of investment experience. Warren received a B.A. in history from the University of Utah, an M.A. in Russian and international policy studies from the Monterey Instituteof International Studies, and a Ph.D. in political science from the University of Oxford.

The forecasts and opinions in this piece are not necessarily those of Morgan Stanley InvestmentManagement and may not actually come to pass.Information in this report does not pertain to anyMorgan Stanley product and is not a solicitation for any product. The views expressed are those of the authors at the time of writing and are subject to change based on market, economic and other conditions. They should not be construed as recommendations, but as illustrations of broader economic themes. All information contained within is based on past performance and is not intended to be indicative of future results. All information is subject to change.

Morgan Stanley does not provide tax advice. The taxinformation contained herein is general and is notexhaustive by nature. It was not intended or writtento be used, and it cannot be used by any taxpayer,for the purpose of avoiding penalties that may beimposed on the taxpayer under U.S. federal tax laws.Federal and state laws are complex and constantlychanging. You should always consult your own legalor tax advisor for information concerning yourindividual situation.

Equity securities are more volatile than bonds and subject to greater risks. Small and mid-sized companystocks involve greater risks than those customarilyassociated with larger companies. Bonds are subject to interest rate, price and credit risks. Prices tend to be inversely affected by changes in interest rates.Unlike stocks and bonds, U.S. Treasury securities are guaranteed as to payment of principal and interest if held to maturity. REITs are more susceptible to the risks generally associated with investments in realestate. Note that it is not possible to invest in a market index.

THIS MATERIAL IS PREPARED FOR INSTITUTIONAL INVESTOR USE ONLY.It may not be reproduced, shown or quoted to members of the general public or used in written form as sales literature; any such use would be in violation of the NASD Conduct Rules.

PG.01

Every now and then, there is a development in the world of finance that results in a major paradigm shift. Examples include the introduction of present value as a tool in financial decision making,1 the Modigliani-Miller hypotheses regarding capital structure2 and the introduction of modern portfolio theory in investing.3

Today we are in the midst of a very unusual situation in which three paradigm shiftsare emerging simultaneously. Each can have a significant impact on the managementof the investment portfolios of pension funds, endowments and foundations.

The first of these developments is a growing focus on various types of asset-liabilityrisk. The second is the recognition that defined benefit plan and endowment orfoundation assets and liabilities are part of the capital structure of the sponsoringentity. They are thus subject to both corporate or trust financial principles and optimal portfolio theory. The third development is the use of various portable alphafinancial engineering techniques to raise investment returns, reduce financing costsand/or facilitate the reduction of various risks, such as asset-liability risks.

Jack would like to thank Charles Stucke and Scott Gregory, executive directors of MorganStanley Alternative Investment Partners, for their significant contributions to our portablealpha programs and to this article.

Asset-liability risks and portable alpha

John S. Coates, Ph.D., CFAManaging DirectorMorgan Stanley Alternative Investment Partners

2 • Investment Management Journal Fall 2005

securities that experience rising values as inflationrises. Inflation-linked bonds might not increaseyield relative to nominal bonds, but they canreduce inflation risk. Also, in a volatile interest-rateenvironment, they can have low correlations withnominal bonds and, thus, provide a risk-reducingportfolio benefit.

Changing demographics. While interest-rate and inflation risks can be quantified and mitigated by various investment strategies, the impacts ofcertain demographic factors generally cannot.Various effects such as the length of plan partici-pant employment, early retirement programs andincreases in longevity can affect defined benefit liabilities. For example, as plan beneficiaries livelonger, benefit payments will continue beyond the dates originally indicated by demographic projections. Medical and other advances cannot be easily forecasted, and this risk cannot be wellhedged (although a market for longevity risk transfer is emerging, and the risk can be offset to some extent if a pension plan is overfunded).

ASSET-LIABILITY MATCHING ON THE RISE

One of a chief financial officer’s tasks is to developan attractive overall capital structure for the firm.Experiences in difficult financial markets, coupledwith scrutiny from investors and analysts, havecaused a growing trend to view a pension programas part of the overall capital structure.

Recent and expected accounting, regulatory and rating agency changes have combined with underfunding of pension plans to cause CFOs to increasingly recognize and deal with the implications for the plan sponsor’s shareholders of the mismatch between defined benefit pensionfund assets and plan liabilities. For example, rela-tively new Securities and Exchange Commissionreporting rules require increased disclosure of pension assets and liabilities. In addition, ratingagencies are beginning to treat unfunded portionsof pension plans as debt-like and might be expected to assign an equity-like risk to significant asset-liability mismatches. The resulting higherimplied leverage puts pressure on companies’credit ratings and associated financing costs, whichalso can increase the volatility of a company’s common stock.

RISKS OF DEFINED BENEFIT PENSION PLANS

We begin with a discussion of the impacts of thesedevelopments on corporate defined benefit pensionplans. Traditionally, pension fund managers oftentended to measure risk in terms of asset portfoliovolatility and relative deviation from the averagepension fund asset mix. Many maintained a classic60/40 mix of stocks and bonds—a decision oftensupported by efficient frontier studies and advicefrom consultants.

Having a “typical” asset mix was often thought tobe a safe harbor from criticism by the Departmentof Labor, which enforces ERISA (the EmployeeRetirement Income Security Act of 1974, the federal law that governs the operation of most private benefit plans). Specifically, a typical mix was viewed as appropriate given ERISA’s prudentman rules; however, a prudent mix for one fund is not necessarily the best mix for another with a different plan liability structure. There are a number of fundamental risk factors that can raisethe unfunded liabilities, potentially increase cashcontributions from the sponsor and call for a tailored optimal asset mix. Several of the moreimportant of these factors are as follows.

Interest rates. An environment of changing interestrates can affect assets and liabilities in differentways and adversely impact a plan’s funded status.For example, falling interest rates increase the present value of liabilities, but the impact on assetvalues can vary quite a bit depending upon theasset mix and macroeconomic environment. This is a typical form of asset-liability mismatch.

Even interest-rate exposures as measured by duration of assets and liabilities can change in different ways as interest rates change because theyhave different convexities and/or key rate duration profiles. This risk can be offset significantly with ahigher allocation to fixed income or other assets inthe pension fund that have durations similar to the liabilities in terms of magnitude and characteristics.

Rising inflation. Rising inflation can also have different impacts on assets and liabilities, particu-larly to the extent a defined benefit plan has inflation-linked benefits, such as cost-of-living provisions. This impact can be mitigated with

Volume 1, Issue 2 Investment Management Journal • 3

Asset-liability mismatch can create risk that is even greater than most rising-interest-rate scenarioshave on a company’s cost of borrowing. Yet, many companies manage their interest rate exposure more carefully than their pension fund asset-liability risk.

Some pension fund managers believe that equitieshave a long duration. They also like the higherexpected long-term returns from equities. However,the duration of equities can be shorter and morevariable than one might expect. In fact, it can be negative at times. Furthermore, funding rulesdo not adequately compensate for relatively short-term (several years) variability in effectiveduration of equity portfolios. This dilemma can be magnified when low stock prices affect both the funding deficit and the company’s ability toraise equity financing.

OTHER ARGUMENTS SUPPORTING HIGHER FIXEDINCOME ALLOCATIONS

In a 1980 paper entitled “The Tax Consequencesof Long-Run Pension Policy,” Fischer Blackshowed that there would be an increase in shareholder value if a pension fund would shift to investing primarily in fixed income securitiesand the sponsoring company would issue bonds at the corporate level to buy back its own shares.5

A related argument is the Modigliani-Millerhypothesis that a company’s stock value will not be increased by actions that shareholders could dothemselves.6 For example, in the absence of taxes or bankruptcy considerations, the hypothesisimplies that the asset mix in a pension fund isirrelevant to the degree that shareholders couldadjust their stock and bond positions to offset or replicate those in the pension fund. In a worldwith taxes, however, the mix becomes important,since interest income in a U.S. pension fund isnontaxable, while individual shareholders would betaxed if they owned bonds. There is less advantageto a fund owning equities since shareholders caninvest in them on their own with low capital gainand dividend taxes.

Accounting rules are expected to evolve in the United States to become more similar to those in Europe that reduce the flexibility to smoothreturns over a period of years and that requireannual marks-to-market of both assets and liabilities. In addition, funding rules are likely to be strengthened and will require more rapidfunding of shortfalls.

We believe that these developments are causing as many as half—or perhaps even more—of U.S.defined benefit pension plan sponsors to considerat least some degree of asset-liability matching.Governments around the world are planningincreased issuance of long-maturity bonds, partlyin anticipation of future demand for the extended-duration securities that asset-liability matching will require.

THE IMPACT OF EQUITIES

Pension fund managers historically have usedmean-variance efficient frontier optimizations as guidance for setting an asset mix. However, theresults of such optimizations are extremely sensitiveto input assumptions of the expected returns,volatilities and correlations of the various assetclasses. These optimizations use asset return volatility (variance) as the measure of risk. Usingasset-liability duration and inflation mismatches as risk measures would suggest higher allocations to long-duration fixed income and inflation-linkedsecurities, with lower allocations to equity.

Not only does a typical 60% allocation to equityexacerbate the asset-liability risk of many funds,but the effective total equity exposure in institu-tional portfolios might be greater than many managers realize. For example, research by Marty Leibowitz and Anthony Bova of MorganStanley indicates that 90% or more of the volatilityof U.S. pension funds is attributable to U.S. stockbeta, even with total equity allocations much less than 90%.4 Furthermore, the effective equityexposure can become even higher in times of unusual market stress.

A number of companies are expected to follow the lead of General Motors Corporation by issuingdebt at the corporate level to help fund their pension plans as part of a tax arbitrage.7 In a particularly interesting Harvard Business Schoolcase, the U.K. company Boots Group issued bondsat the company level, where the interest wasdeductible, while investing exclusively in fixedincome in the pension fund to take advantage of the tax treatment in both the pension fund and the company. Harvard contended that this resulted in an approximate 6% increase in the market capitalization of Boots.8

WHAT ABOUT PUBLIC PENSION PLANS?

We believe public plans could also reduce the risk of interest-rate movements and inflation by shiftingto an asset-liability framework, and it would be in the interest of taxpayers to do this. In addition, the public budgeting process strongly favors predictability and stability in cost structures, including the cost of benefit payments. Therefore,an asset-liability matching model could be helpfulin the process.

However, public pension funding depends upon political factors in many cases—ERISA does notgovern public sector plans. Public plans tend tohave pressures from employees (e.g., throughunions) to raise benefits, and they have pressures to limit tax increases (e.g., through elected repre-sentatives). But the interests of future taxpayers, who must ultimately pay for any shortfalls, are underrepresented.

As a result, there tends to be excessive risk in these systems. Participants favor policies that grantbenefit improvements when a public plan is in a surplus position. Politicians favor policies that deferfunding or that reduce long-term indicated funding,in some cases via higher expected return/higher risk assets.

But when a public plan subsequently moves to adeficit, it is typically much more difficult to reducebenefits or raise taxes to fund adequately. And pub-lic pension deficits are very high on average. Theaggregate funding ratio was estimated to be 88%

4 • Investment Management Journal Fall 2005

in 2004, but the amount of underfunding would beabout twice as large if public plans used the sameaccounting rules as those used by private plans.9

WHAT ABOUT ENDOWMENTS AND FOUNDATIONS?

Endowments and foundations do not have thesame capital structure or ERISA issues as pensionplans. However, they do encounter other issueswith similar risks. Many endowments and foundations have donation goals that are somewhatpredictable and spending requirements that are relatively consistent year after year. Endowmentsand foundations with annual spending policiesdetermined by a fixed percentage of a multi-yearaverage can be forced to sell low and buy highwhen they use a high allocation to equities. Theyalso face inflation risk to the extent their spendingneeds rise over time with inflation.

For example, a college endowment might berequired to deliver a somewhat consistent flow of funds to its campus, or a foundation might have a need to maintain a particular ongoing research or charity program. Endowments and foundationsare generally interested in strategies that are likelyto generate relatively high and consistent real rates of return to maintain the ongoing funding of their programs. While equities are expected todeliver reasonable long-term real rates of return,their volatility introduces near-term risk to theendowment’s or foundation’s capital base and mightnot provide returns that will be adequately high or increase with inflation. Despite the consequencesof this volatility on the future of the institution,stakeholders are often very reluctant to acceptreductions in funding for campus, research or charity programs. Furthermore, reductions in suchfunding can have serious long-term consequencesfor the mission of the institution. Small to medium-sized endowments and foundations, or those with spending needs that are relatively inflexible and above current real interest rates, canbe particularly sensitive to near-term volatility risk.

In addition, many nonprofit organizations issue debt securities, which create additional defined liabilities. While tax law prohibits the direct

Volume 1, Issue 2 Investment Management Journal • 5

funds search for higher returns among asset classes that even further exacerbate the asset-liability mismatch. For example, they might include anallocation to certain types of difficult-to-hedgenon-U.S. securities when their liabilities aredenominated in dollars, or they might look tomicro-cap or emerging market stocks with higherexpected returns, but also with higher volatility.

INCREASED INTEREST IN PORTABLE ALPHA

This brings us to the third paradigm shift. In the last year or two there has been an incredibleincrease in interest in portable alpha as a way toadd expected return to all asset classes, includingfixed income and inflation-protected securities—the very investments that can reduce the risks thatwould otherwise exist. This can be seen from the large number of articles and conferences during 2005 on the specific topic of portablealpha. A 2005 survey indicated that 33% of the large companies surveyed are using portable alpha programs, with another 23% consideringthem—15% of the public funds surveyed areusing portable alpha, with a staggering 37% considering them.10 Many corporate pension funds,endowments and foundations have portable alpha programs; and at least one large public plan has a long history of investing in alternatives in general,and over three years of experience with a majorsuccessful portable alpha program.11

There is a growing recognition of the importanceof using a risk budget for alpha rather than beta,and tailoring the asset mix to better match liabilities. Portable alpha can help investors in their efforts to achieve the best of both worlds—a reduction in various types of asset-liability mismatch while generating high expected returns,even in a low-interest-rate environment.

We discussed the concept of portable alpha atlength in the previous issue of the Morgan StanleyInvestment Management Journal; what follows is an overview of the basics and its applicationwithin defined benefit plans, endowments and foundations.

matching of investment assets to specific tax-exempt bond issues, rating agencies, bondunderwriters and letter-of-credit providers clearlyassess the capital structure of an endowment orfoundation fund. For many private, nonprofit institutions, the strength of the institution relativeto spending needs is the primary source of creditand, consequently, access to capital.

CATCH-22

All of this fits nicely with the concept of increasing the use of long-duration fixed incomeand inflation-protected securities to reduce asset-liability risks. However, the problem is that thevery fixed income and inflation-protected securitiesthat might help institutional investors reduce these risks are not generally projected to generatereturns sufficient to meet their needs for benefit payments or other spending requirements.

This might not be a problem if one could findactive investment managers capable of generatingadequately high and consistent levels of excessreturns (i.e., alpha) to facilitate more asset-liabilitymatching. But the alpha-generating ability of most traditional managers is often limited.Typically, these managers operate in very efficientmarkets (e.g., large-cap U.S. stocks and bonds), are not willing to take positions that deviate verysignificantly from those in their evaluation bench-marks, and are long-only investors. Since they do not sell short, the most they can do to reflect a belief that a security will underperform is tounderweight it or exclude it from their portfolio.

In addition, returns among traditional managers in a given asset class tend to be highly correlated, so a portfolio of such managers offers limiteddiversification benefits. This can be particularlynotable during major negative market events.

When investors using a traditional approach cannot find active managers whose alphas over passive benchmarks are sufficient, they often seek returns and/or alpha in asset classes that arenot ideal for their objectives. As a result, many

6 • Investment Management Journal Fall 2005

The result is a superior mix of alphas, while stillachieving the desired aggregate betas. Althoughportable alpha can be difficult to implement andcan add new management requirements, there are distinct advantages compared to traditionalportfolio management:

Universe. Investors are not forced to seek alphaonly from managers within the target asset classes, opening a vast field of possible high-alphastrategies, such as certain types of hedge funds, private equity and opportunistic real estate, as wellas a few traditional strategies.

Markets. The least efficient markets typically offer the best opportunities for alpha, but theymight entail too much market risk for an investor.Portable alpha lets investors offset undesired exposures and/or capitalize on alpha from sourcesthat do not have undesired market risks.

Objectives. An investor might reduce total portfolio risk by shifting the asset mix to one better suited to its risk objectives. For example, an allocation to equities could be reduced andfixed income and inflation-linked exposuresincreased, while also increasing the expected returnto help achieve asset-liability duration matching, as well as inflation protection and a reduction in volatility.

Efficiency. Portable alpha allows selection of alpha-generating managers without regard to their assetclass. Alpha-generating managers often have lowcorrelations with each other and can be combinedinto very efficient, risk-controlled portfolios.

Risk. By separating alpha and beta decisions, onecan allocate different amounts of a risk budget toeach. For example, the alpha component can belarge or small, unrelated to the amounts of theasset classes to which the alpha is transported. Aninitial small allocation to the alpha source might be increased as cumulative alpha is generated.

The traditional approach to institutional invest-ment management is epitomized by engaging a committee to set target asset classes, and thenchoosing index funds or active managers withineach class in the hope of finding those that are able to generate alphas above the passive asset classreturns. For example, to fill a target equity alloca-tion, investors would search only among equitymanagers; similarly, for a bond allocation, theywould search only among bond managers.

By focusing exclusively on managers within each class, however, investors limit the universe of strategies and managers from which to select and, hence, the opportunities to find the desiredlevels of alpha. Allocations to managers capable of generating the greatest alphas are excluded ifthey do not fit within the confines of the chosenasset classes.

Portable alpha is quite different. It is predicated upon the notion that portfolio objectives can be best achieved when asset class decisions andmanager selections are made independently. It is further based upon the separation of market-based and skill-based returns, and allocating mostof a fund’s active management risk budget to alpha sources.

A typical portable alpha strategy begins by selecting a well-diversified portfolio of the bestalpha-generating managers, regardless of the assetclasses in which they operate, with adequate consideration given to liquidity constraints. Oncean attractive mix of managers is identified, theembedded market exposures (betas) in the portfolioare assessed. The investor then creates an overlay,employing futures, options, swaps or other contractsto add or subtract exposures to particular assetclasses in order to achieve the desired total asset allocation. The objective is to set the overlayexposures so that they and the exposures embeddedin the alpha sources aggregate to the investor’s target exposures.

Volume 1, Issue 2 Investment Management Journal • 7

top-performing managers. During our more than20 years of intense focus on locating alpha—both as a plan sponsor and a fund of funds manager—we have found the most compelling sources to be various types of alternative investments, such as selected subcategories of hedge funds, private equity and opportunistic real estate.

The most attractive alternative strategies are continually changing. Further, the return disper-sion between the best and worst performing strategies and managers can be very large in thefield of the high alpha-generating alternatives, and the relative performance relationships among managers can change dramatically over long periods of time—even for “successful” managers with long track records. Therefore, multi-manager,diversified alpha engines provide key strategicadvantages in a portable alpha structure.

An investor must have access to the best managers,and thoroughly understand each strategy and conduct extensive investment, staffing, process and operational due diligence on candidate managers.Experience-based qualitative evaluations of themanager must be conducted as a complement toquantitative analyses. Managers of portfolios ofalternatives and portable alpha strategies shouldcontinually monitor existing managers and searchfor attractive new ideas and managers. Correlationsamong managers must be analyzed in order tooptimize portfolio efficiency and risk. Investorsmust also consider each manager’s capacity andevaluate the impact on returns of cash flows intothe strategy. Furthermore, fees must be carefullyevaluated relative to the projected alpha.

A fund of funds approach can be one attractiveway for many investors to achieve these multipletasks in a one-stop manner.

Fees. With portable alpha, investors typically pay higher fees only to managers with the ability to add alpha, with much lower costs for beta exposures.

Another attractive element of portable alpha is that alpha can be transported to virtually any assetclass—including cash, all types of equity and fixedincome, tactical allocation and other categories—through the sophisticated use of derivatives andother financial instruments. This is importantbecause different pension plans, endowments andfoundations will have different benefit liability and spending rule characteristics and, thus, different beta requirements for true matching.

Alpha may be transported (1) to any market indexfor which well-functioning derivatives marketsexist, (2) to any asset class that can be replicatedrelatively closely using baskets of securities or (3) to any asset class for which an active or passivemanager exists. A single, diversified portfolio of alpha-generating strategies can be transported to multiple benchmarks simultaneously, making the process of alpha generation more efficient than would be the case if alpha had to be foundseparately for each asset class.

There are many advanced forms of portable alpha.These include a mixed hedge fund/private equityalpha engine, the use of some of the alpha for principal protection, and the addition of global tactical allocation to improve the shape of thereturn distribution, to name but a few.

FINDING ALPHA

Locating, analyzing and accessing investments for an alpha-generating portfolio is very labor- andskill-intensive. The investor must have access to acontinual stream of new ideas for alpha generation,along with relationships with and access to

8 • Investment Management Journal Fall 2005

CONCLUSION

We are still in the early stages of what we expect tobe a massive shift to better asset-liability matchingby pension funds, endowments and foundations,with portable alpha as a financial engineering tool to achieve better matching while seeking to generate high levels of return. This is likely toresult in higher allocations to long-duration fixedincome and inflation-protected securities. It mightalso result in decreased borrowing costs by defined benefit sponsors, endowments and foundations.

Investors are likely to increase their search forsources of alpha, but the search is very skill- and labor-intensive. It requires a great deal of experience, extensive investment and operationsdue diligence, and access to the best strategies and managers.

Portable alpha strategies can help improve portfolioperformance, in terms of return and risk, for institutional investors of all stripes. By dissectingreturns into their underlying components—alphaand beta—and then seeking to optimize resultsfrom each component separately, investors canmeaningfully increase return potential while main-taining a level of market risk more appropriate totheir objectives.

TRANSPORTING ALPHA AND MANAGING BETAS

Once an attractive alpha-generating portfolio isconstructed, an array of tools can be used to estimate the market exposures embedded in theportfolio. Even so-called market-neutral funds havesome embedded betas that must be consideredwhen constructing an overlay. Although there aremathematical techniques to estimate embeddedbetas, the betas tend to fluctuate, can be indirectand relate to other variables, can be the result ofskill that is desirable, and/or can be the result of other nuances. A certain degree of judgment is required to determine when fluctuations are temporary noise and when they reflect a truechange in the underlying economic betas.

After assessing the amounts and typical patterns of betas embedded in an alpha portfolio, aninvestor can implement the desired amount ofadditional beta exposures using futures, options or swaps on the desired target indices. Determiningwhich instruments to use and the correct amountsrequires precise analysis of multiple factors, including pricing, basis risk, optionality and cash management of derivative settlements.

The embedded beta exposures of an alpha portfolio can change over time, and the sum of the embedded and derivative exposures will drift as markets move and alpha is generated. Ongoingmonitoring and periodic adjustments of the overlayare necessary to address such effects. The decisionof how often and by what degree to adjust theoverlay can be complicated, but it is manageable.

Swaps, futures, options and other instruments used in a portable alpha strategy can have quite different cash settlement requirements that need to be managed closely. For example, a swap into a fund of funds will usually require only quarterlyinterest payments, with the gain or loss on thefund of funds settled either at final expiration or, at the option of the investor, earlier. Futures, in contrast, require daily settlements.

1 Fisher, I., The Theory of Interest (1930), New York: Macmillan.

2 Modigliani, F. and M. Miller, “The Cost of Capital, Corporation Finance and the Theory of Investment,” American Economic Review, vol. 48, no. 3 (1958), p. 261–297.

3 Markowitz, H., “Portfolio Selection,” The Journal of Finance, vol. 7, no. 1 (1952), p. 77–91.

4 Leibowitz, M. and A. Bova, “Allocation Betas,” Financial Analysts Journal,vol. 61, no. 4 (2005), p. 70–82.

5 Black, F., “The Tax Consequences of Long-Run Pension Policy,” Financial AnalystsJournal, vol. 36 (1980), p. 21–28.

6 Modigliani, F. and M. Miller, “The Cost of Capital, Corporation Finance and the Theory of Investment,” American Economic Review, vol. 48, no. 3 (1958), p. 261–297.

7 Calio, V., “Others Expected to Hitch Ride on GM Funding Idea,” Pensions & Investments, 22 August 2005, p. 3, 28.

8 Capon, A., “Balancing Act,” Institutional Investor, July 2005, p. 42–43.

9 “Their Own Worst Enemy,” Plan Sponsor, August 2005, p. 57.

10 Chernoff, J., “Lower Returns Put Portable Alpha in Better Light,” Pensions & Investments Online (www.pionline.com), 11 July 2005.

11 “PennSERS ‘Pretty Happy’ with Program,” Pensions & Investments, 4 April 2005.

PG.09

Emerging market equities have been among the best performing asset classes overthe last few years. The MSCI Emerging Markets Index posted a 14.63% annualizedreturn over the five-year period ended October 31, 2005, versus a decline in theS&P 500 Index and flattish European markets. This outperformance has intensifiedover the past three years, with emerging market equities returning 33.59% perannum. (Data sourced from FactSet and MSCI.)

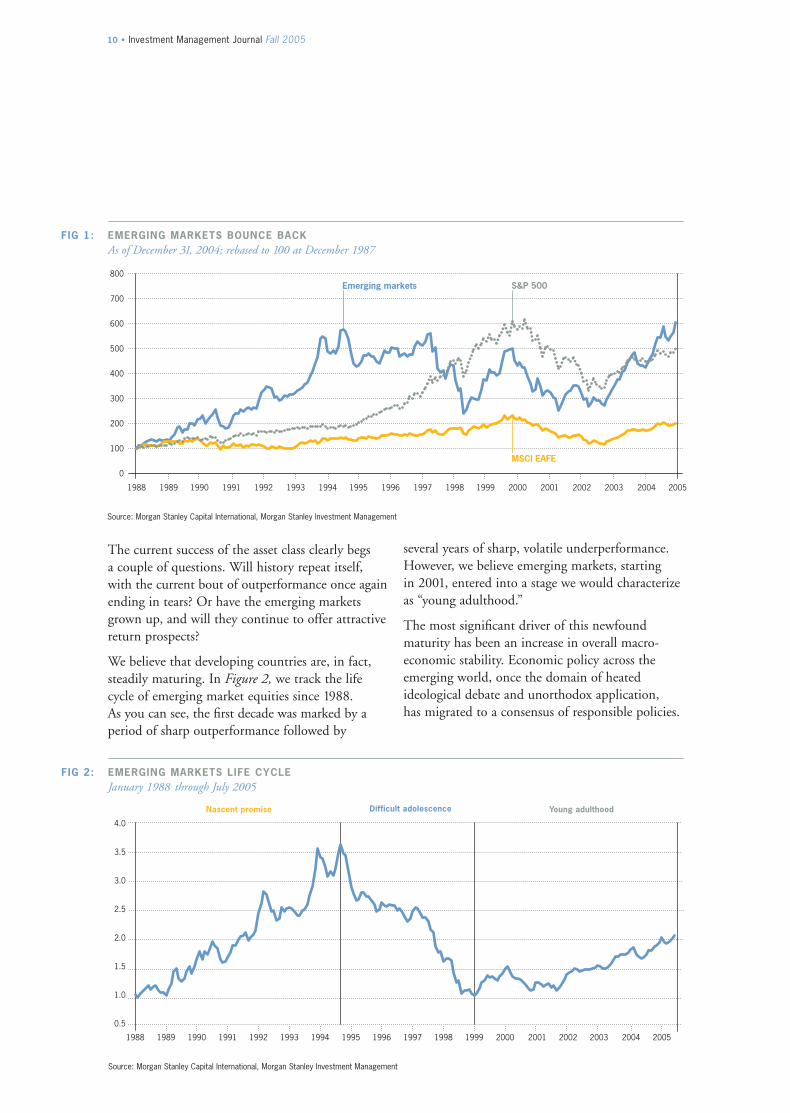

Investors have seen this before. The emerging markets posted spectacular gains from 1992 to 1997. This success, however, was short-lived; a series of crises hit the devel-oping world beginning in 1997, leading to a period of dramatic underperformance. In some cases, investors lost more than 75% (in U.S. dollar terms) of their prior market gains during this period. (See Figure 1.)

Emerging markets: All grown up?

Paul Psaila, CFAExecutive DirectorMorgan Stanley Investment Management

10 • Investment Management Journal Fall 2005

several years of sharp, volatile underperformance.However, we believe emerging markets, starting in 2001, entered into a stage we would characterize as “young adulthood.”

The most significant driver of this newfound maturity has been an increase in overall macro-economic stability. Economic policy across theemerging world, once the domain of heated ideological debate and unorthodox application, has migrated to a consensus of responsible policies.

The current success of the asset class clearly begs a couple of questions. Will history repeat itself,with the current bout of outperformance once againending in tears? Or have the emerging marketsgrown up, and will they continue to offer attractivereturn prospects?

We believe that developing countries are, in fact,steadily maturing. In Figure 2, we track the lifecycle of emerging market equities since 1988. As you can see, the first decade was marked by a period of sharp outperformance followed by

0

100

200

300

400

500

600

700

800Emerging markets S&P 500

MSCI EAFE

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

FIG 1: EMERGING MARKETS BOUNCE BACKAs of December 31, 2004; rebased to 100 at December 1987

Source: Morgan Stanley Capital International, Morgan Stanley Investment Management

4.0

3.5

3.0

2.5

2.0

1.5

1.0

0.5

Nascent promise Young adulthoodDifficult adolescence

200520042003200220012000199919981997199619951994199319921991199019891988

FIG 2: EMERGING MARKETS LIFE CYCLEJanuary 1988 through July 2005

Source: Morgan Stanley Capital International, Morgan Stanley Investment Management

Volume 1, Issue 2 Investment Management Journal • 11

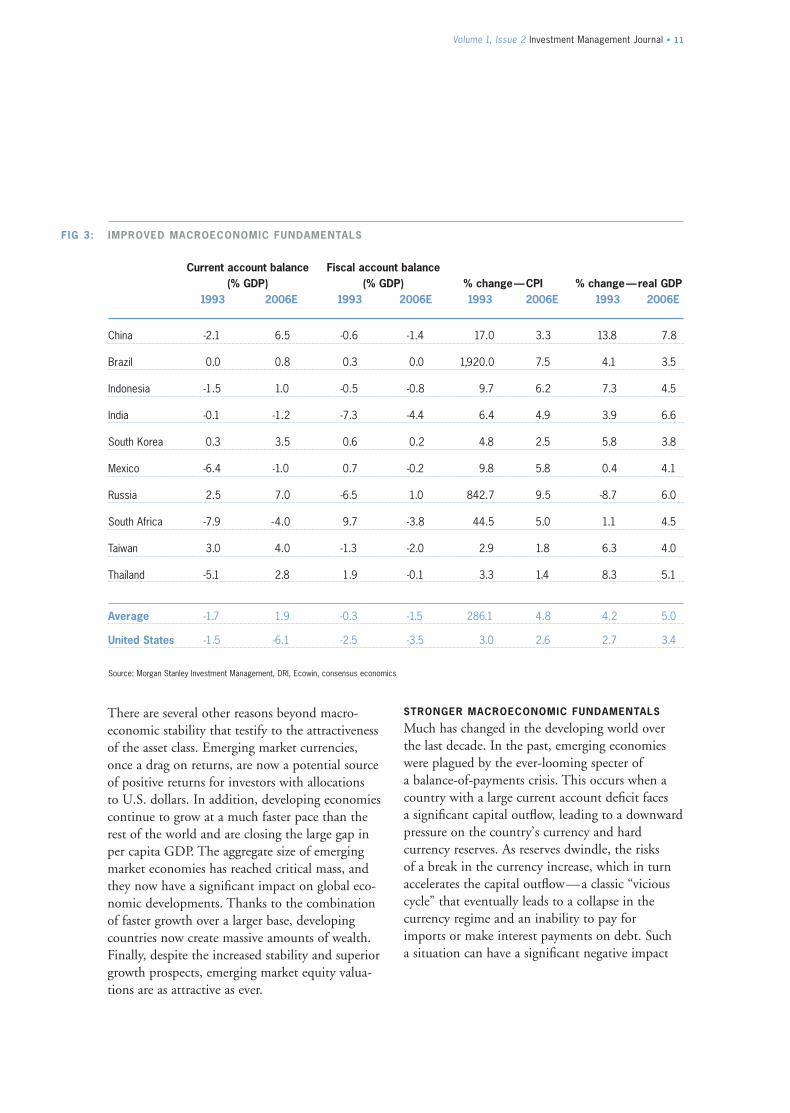

STRONGER MACROECONOMIC FUNDAMENTALS

Much has changed in the developing world overthe last decade. In the past, emerging economieswere plagued by the ever-looming specter of a balance-of-payments crisis. This occurs when acountry with a large current account deficit faces a significant capital outflow, leading to a downwardpressure on the country’s currency and hard currency reserves. As reserves dwindle, the risks of a break in the currency increase, which in turnaccelerates the capital outflow—a classic “viciouscycle” that eventually leads to a collapse in the currency regime and an inability to pay for imports or make interest payments on debt. Such a situation can have a significant negative impact

There are several other reasons beyond macro-economic stability that testify to the attractiveness of the asset class. Emerging market currencies, once a drag on returns, are now a potential sourceof positive returns for investors with allocations to U.S. dollars. In addition, developing economiescontinue to grow at a much faster pace than therest of the world and are closing the large gap inper capita GDP. The aggregate size of emergingmarket economies has reached critical mass, andthey now have a significant impact on global eco-nomic developments. Thanks to the combinationof faster growth over a larger base, developingcountries now create massive amounts of wealth.Finally, despite the increased stability and superiorgrowth prospects, emerging market equity valua-tions are as attractive as ever.

FIG 3: IMPROVED MACROECONOMIC FUNDAMENTALS

Current account balance Fiscal account balance(% GDP) (% GDP) % change—CPI % change—real GDP

1993 2006E 1993 2006E 1993 2006E 1993 2006E

China -2.1 6.5 -0.6 -1.4 17.0 3.3 13.8 7.8

Brazil 0.0 0.8 0.3 0.0 1,920.0 7.5 4.1 3.5

Indonesia -1.5 1.0 -0.5 -0.8 9.7 6.2 7.3 4.5

India -0.1 -1.2 -7.3 -4.4 6.4 4.9 3.9 6.6

South Korea 0.3 3.5 0.6 0.2 4.8 2.5 5.8 3.8

Mexico -6.4 -1.0 0.7 -0.2 9.8 5.8 0.4 4.1

Russia 2.5 7.0 -6.5 1.0 842.7 9.5 -8.7 6.0

South Africa -7.9 -4.0 9.7 -3.8 44.5 5.0 1.1 4.5

Taiwan 3.0 4.0 -1.3 -2.0 2.9 1.8 6.3 4.0

Thailand -5.1 2.8 1.9 -0.1 3.3 1.4 8.3 5.1

Average -1.7 1.9 -0.3 -1.5 286.1 4.8 4.2 5.0

United States -1.5 -6.1 -2.5 -3.5 3.0 2.6 2.7 3.4

Source: Morgan Stanley Investment Management, DRI, Ecowin, consensus economics

12 • Investment Management Journal Fall 2005

rating agencies represent more than 50% of the J.P. Morgan Emerging Markets Bond Index(EMBI); ten years ago, that number stood at less than 5%. While developing economies are still more likely to run into trouble than their developed counterparts, systemic risk hasclearly declined.

POTENTIAL FOR CURRENCY APPRECIATION

In the past, U.S. dollar-based investors typically lost significant value due to adverse currency movements in the emerging markets. However, the fundamentals of emerging market currencieshave improved dramatically in recent years. In the period before the currency crises, many emerging markets ran large current accountdeficits, a common precursor to a balance of payments crisis. Today, in aggregate, the emergingmarkets are running significant current accountsurpluses and are net creditors to the rest of theworld. The growth in developing-country currentaccount surpluses is the diametric opposite of the deterioration in the U.S. current account. Inaddition, foreign direct investment continues toflow into the developing world, attracted by higherreturn potential; these long-term capital inflowsshould continue to support positive currencyreturns. Given these factors, we think U.S. dollar-based investors are in a position to benefit frommovements in emerging market currencies.

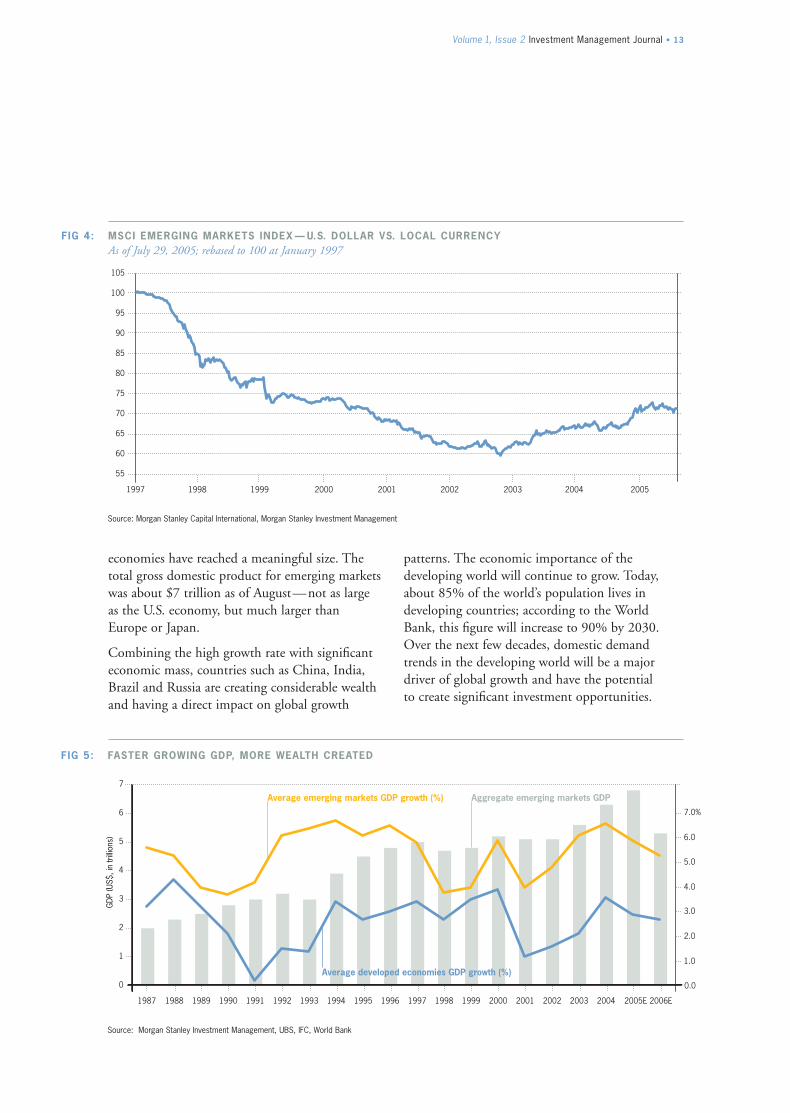

SUPERIOR ECONOMIC GROWTH RATES

Since the end of World War II, developing countries have been growing at a much faster ratethan those in the developed world; IMF data pegs the average annual growth rates in the emergingmarkets at double that of developed markets overthe last two decades. Even during periods of recession, such as the 1991 global slowdown, thisgrowth premium persisted. As the result of this strong and consistent expansion, developing

on a variety of macroeconomic measures. The 1997run on the Thai baht, which eventually spread to other economies and became known as the “Asian flu,” is one recent example of such a crisis.

Since that difficult period, the majority of developing economies have adopted floating currency regimes, which help to absorb externalshocks and to prevent a crisis in a single countryfrom spreading. In 2001, for example, Turkey’sfixed exchange rate system collapsed under theweight of capital outflows, leading to an 8% dropin GDP and a spike in inflation to 75%. However,few investors outside the country can recall theevent. The crisis did not spread, and Turkey hasrecovered to become one of the best performingmarkets in the world since then.

Having learned their lessons the hard way, mostgovernments are implementing conservative fiscalpolicy and independent monetary policy. Largebudget deficits and hyperinflation have beenreplaced by stable growth and price stability. In the 1980s, for example, developing countries ranlarge budget deficits; the International MonetaryFund (IMF) estimates the average budget deficitwas over 6%, which led to high levels of inflation.Average inflation, however, has fallen from around30% in 1995 to only 7% today, resulting in lowerinterest rates in virtually every developing country.

Emerging market debt spreads, one indicator of the overall macroeconomic health of the asset class, have tightened to unprecedented levels. As of August, average spreads were only 270 basis points above U.S. Treasuries. While some of thistightening may be due to such external factors asabundant global liquidity, developing countries in general have improved their credit ratings.According to Fitch, 75% of emerging market countries have positive liquid ratios—i.e., theirtotal hard currency debt outstanding is less thantheir export receipts. Countries whose sovereigndebt is ranked investment grade by the major

Volume 1, Issue 2 Investment Management Journal • 13

Source: Morgan Stanley Capital International, Morgan Stanley Investment Management

105

100

95

90

85

80

75

70

65

60

55

1997 1998 1999 2000 2001 2002 2003 2004 2005

FIG 4: MSCI EMERGING MARKETS INDEX — U.S. DOLLAR VS. LOCAL CURRENCYAs of July 29, 2005; rebased to 100 at January 1997

patterns. The economic importance of the developing world will continue to grow. Today,about 85% of the world’s population lives in developing countries; according to the WorldBank, this figure will increase to 90% by 2030.Over the next few decades, domestic demandtrends in the developing world will be a majordriver of global growth and have the potential to create significant investment opportunities.

economies have reached a meaningful size. Thetotal gross domestic product for emerging marketswas about $7 trillion as of August—not as large as the U.S. economy, but much larger than Europe or Japan.

Combining the high growth rate with significanteconomic mass, countries such as China, India,Brazil and Russia are creating considerable wealthand having a direct impact on global growth

Source: Morgan Stanley Investment Management, UBS, IFC, World Bank

2005E 2006E2004

0.0

20032002200120001999199819971996199519941993199219911990198919881987

Average emerging markets GDP growth (%) Aggregate emerging markets GDP

Average developed economies GDP growth (%)0

1

2

3

4

5

6

7

GDP

(US$

, in

trilli

ons)

7.0%

6.0

5.0

4.0

3.0

2.0

1.0

FIG 5: FASTER GROWING GDP, MORE WEALTH CREATED

14 • Investment Management Journal Fall 2005

ALL GROWN UP? MAYBE NOT, BUT GETTING THERE

While the emerging markets asset class may not be fully grown quite yet, we believe that it has certainly made great strides over the past couple of decades. The emerging markets asset class offersboth value and growth, an unusual combination in today’s financial world. Furthermore, the disconnect between the fundamentals of improvedmacroeconomic stability—as evidenced by record-low debt spreads—and the deep discount at whichthe asset class trades relative to developed marketsindicates an attractive investment opportunity.

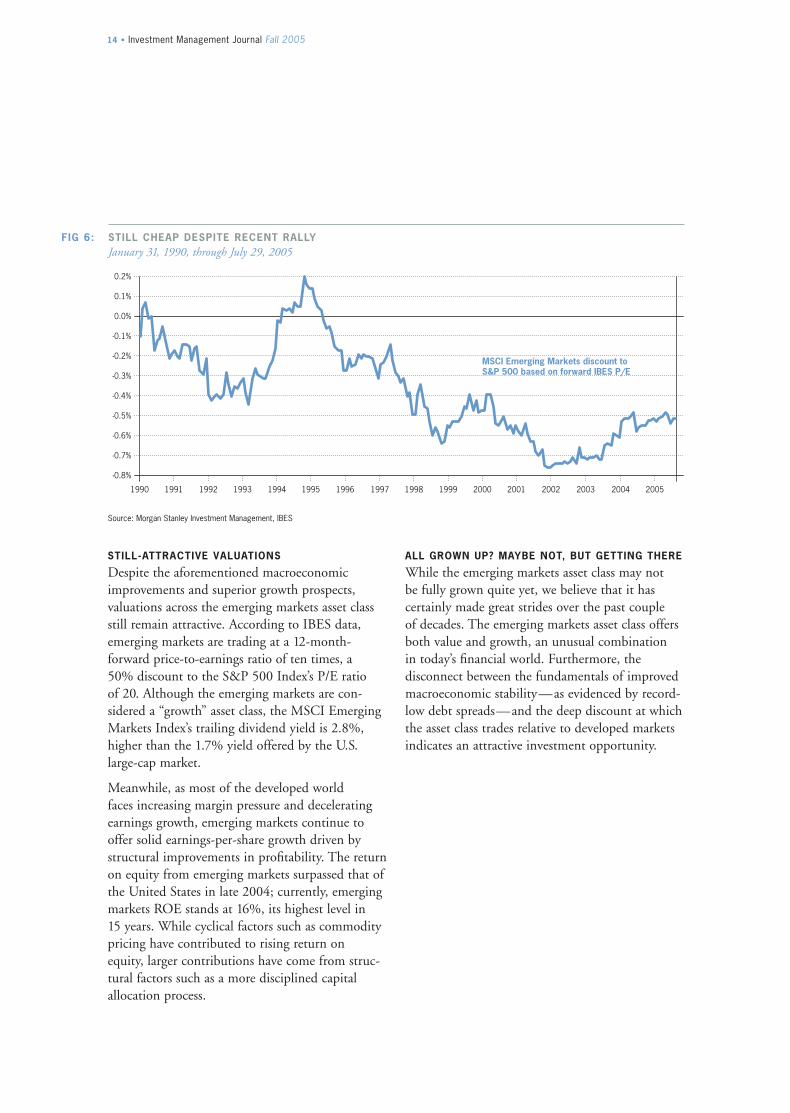

STILL-ATTRACTIVE VALUATIONS

Despite the aforementioned macroeconomicimprovements and superior growth prospects, valuations across the emerging markets asset classstill remain attractive. According to IBES data, emerging markets are trading at a 12-month-forward price-to-earnings ratio of ten times, a 50% discount to the S&P 500 Index’s P/E ratio of 20. Although the emerging markets are con-sidered a “growth” asset class, the MSCI EmergingMarkets Index’s trailing dividend yield is 2.8%,higher than the 1.7% yield offered by the U.S.large-cap market.

Meanwhile, as most of the developed world faces increasing margin pressure and decelerating earnings growth, emerging markets continue tooffer solid earnings-per-share growth driven bystructural improvements in profitability. The returnon equity from emerging markets surpassed that ofthe United States in late 2004; currently, emergingmarkets ROE stands at 16%, its highest level in 15 years. While cyclical factors such as commoditypricing have contributed to rising return on equity, larger contributions have come from struc-tural factors such as a more disciplined capital allocation process.

Source: Morgan Stanley Investment Management, IBES

-0.8%

-0.7%

-0.6%

-0.5%

-0.4%

-0.3%

-0.2%

-0.1%

0.0%

0.1%

0.2%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

MSCI Emerging Markets discount to S&P 500 based on forward IBES P/E

FIG 6: STILL CHEAP DESPITE RECENT RALLYJanuary 31, 1990, through July 29, 2005

Christina ChiuAssociateMorgan Stanley Investment Management

Ted BigmanManaging DirectorMorgan Stanley Investment Management

In recent years, real estate has received a heightened level of interest from institutional investors due to various reasons, including its attractive risk-adjustedreturns, the diversification benefits from its low correlation with other investmentclasses, and the modest expected returns for the broader equity and fixed incomemarkets. As a result, real estate has gained increased acceptance as a distinct assetclass that deserves a permanent strategic allocation in a multi-asset class portfolio.

The case for a strategic allocation to global real estate securities

PG.15

16 • Investment Management Journal Fall 2005

Source: Ibbotson Associates. Large stocks based on S&P 500 Index; small stocks represented by the fifth capitalization quintile of stocks on the New York Stock Exchange from 1926 to 1981 and the performance of the Dimensional Fund Advisors U.S. Micro Cap Portfolio thereafter; bonds based on 20-year U.S. government bond;REITs based on the National Association of Real Estate Investment Trusts (NAREIT) Equity REIT Index.

20042000199619921988198419801976

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0vs. small stocks

vs. large stocks

vs. bonds

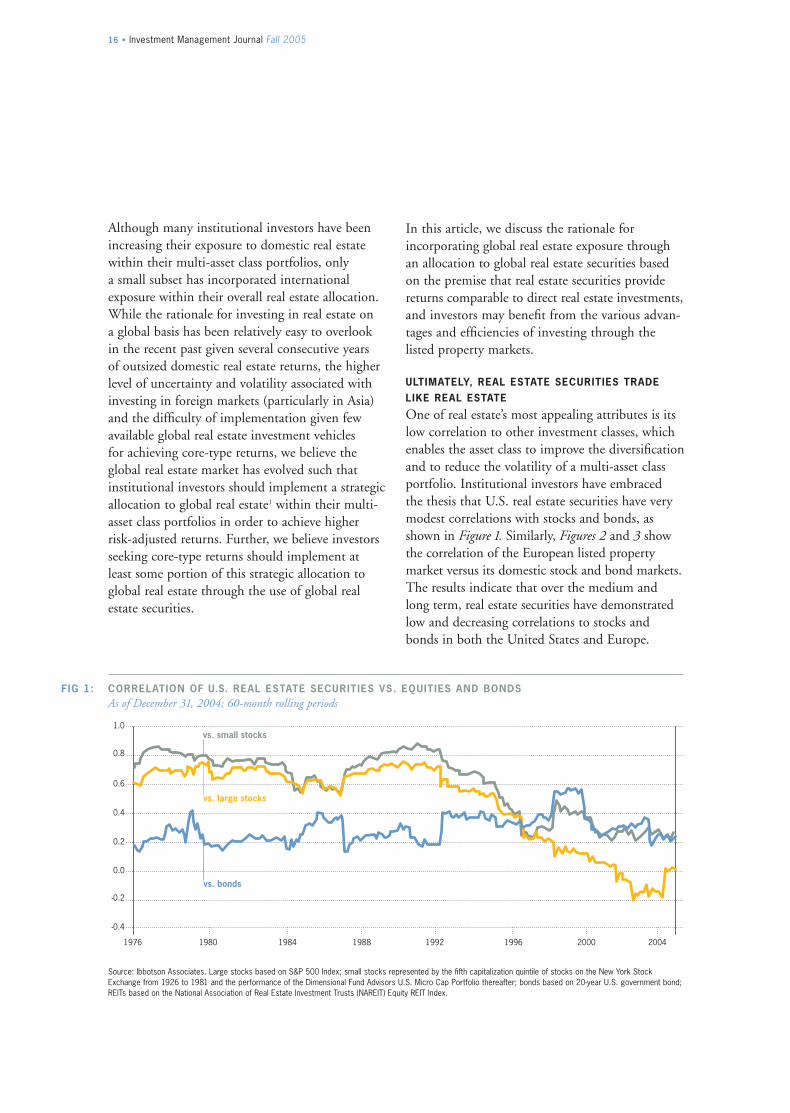

FIG 1: CORRELATION OF U.S. REAL ESTATE SECURITIES VS. EQUITIES AND BONDS As of December 31, 2004; 60-month rolling periods

In this article, we discuss the rationale for incorporating global real estate exposure throughan allocation to global real estate securities basedon the premise that real estate securities providereturns comparable to direct real estate investments,and investors may benefit from the various advan-tages and efficiencies of investing through the listed property markets.

ULTIMATELY, REAL ESTATE SECURITIES TRADELIKE REAL ESTATE

One of real estate’s most appealing attributes is itslow correlation to other investment classes, whichenables the asset class to improve the diversificationand to reduce the volatility of a multi-asset classportfolio. Institutional investors have embraced the thesis that U.S. real estate securities have very modest correlations with stocks and bonds, asshown in Figure 1. Similarly, Figures 2 and 3 showthe correlation of the European listed property market versus its domestic stock and bond markets.The results indicate that over the medium andlong term, real estate securities have demonstratedlow and decreasing correlations to stocks andbonds in both the United States and Europe.

Although many institutional investors have beenincreasing their exposure to domestic real estatewithin their multi-asset class portfolios, only a small subset has incorporated international exposure within their overall real estate allocation.While the rationale for investing in real estate on a global basis has been relatively easy to overlook in the recent past given several consecutive years of outsized domestic real estate returns, the higherlevel of uncertainty and volatility associated withinvesting in foreign markets (particularly in Asia)and the difficulty of implementation given fewavailable global real estate investment vehicles for achieving core-type returns, we believe theglobal real estate market has evolved such thatinstitutional investors should implement a strategicallocation to global real estate1 within their multi-asset class portfolios in order to achieve higher risk-adjusted returns. Further, we believe investorsseeking core-type returns should implement at least some portion of this strategic allocation toglobal real estate through the use of global realestate securities.

Volume 1, Issue 2 Investment Management Journal • 17

Source: Global Property Research, Datastream

20042003200119991997199519931991 200520022000199819961992 19941990

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

Three-year total return correlation

Five-year total return correlation

FIG 3: CORRELATION OF EUROPEAN REAL ESTATE SECURITIES VS. BONDSProperty shares vs. JP Morgan European Bond Index; as of September 30, 2005

Source: Global Property Research, MSCI, Morgan Stanley

20052004200320022001200019991998

0.4

0.5

0.6

0.7

0.8

Ten-year total return correlation

FIG 2: CORRELATION OF EUROPEAN REAL ESTATE SECURITIES VS. EQUITIES Property shares vs. MSCI European Equity Index; as of September 30, 2005

18 • Investment Management Journal Fall 2005

Source: Global Property Research, Investment Property Databank

20051999199519911985 1987 1989 1993 1997 2001 20031983

100

300

500

700

900

1,100

IPD U.K. Property Index (direct)

GPR U.K. Index (indirect)

FIG 5: EUROPEAN DIRECT AND INDIRECT REAL ESTATE RETURNSAs of September 30, 2005; values rebased to 100

Source: National Associated of Real Estate Investment Trusts (NAREIT), National Council of Real Estate Investment Fiduciaries (NCREIF), Property & Portfolio Research

1999199719951993 1994 1996 1998 2000 2001 2002 2003 2004 20051992

0

100

200

300

400

500

600

700

100

200

300

400

50

150

250

350

NAREIT Index level

NCREIF Index level

NAR

EIT N

CREIF

FIG 4: U.S. DIRECT AND INDIRECT REAL ESTATE RETURNSAs of September 30, 2005; values rebased to 100

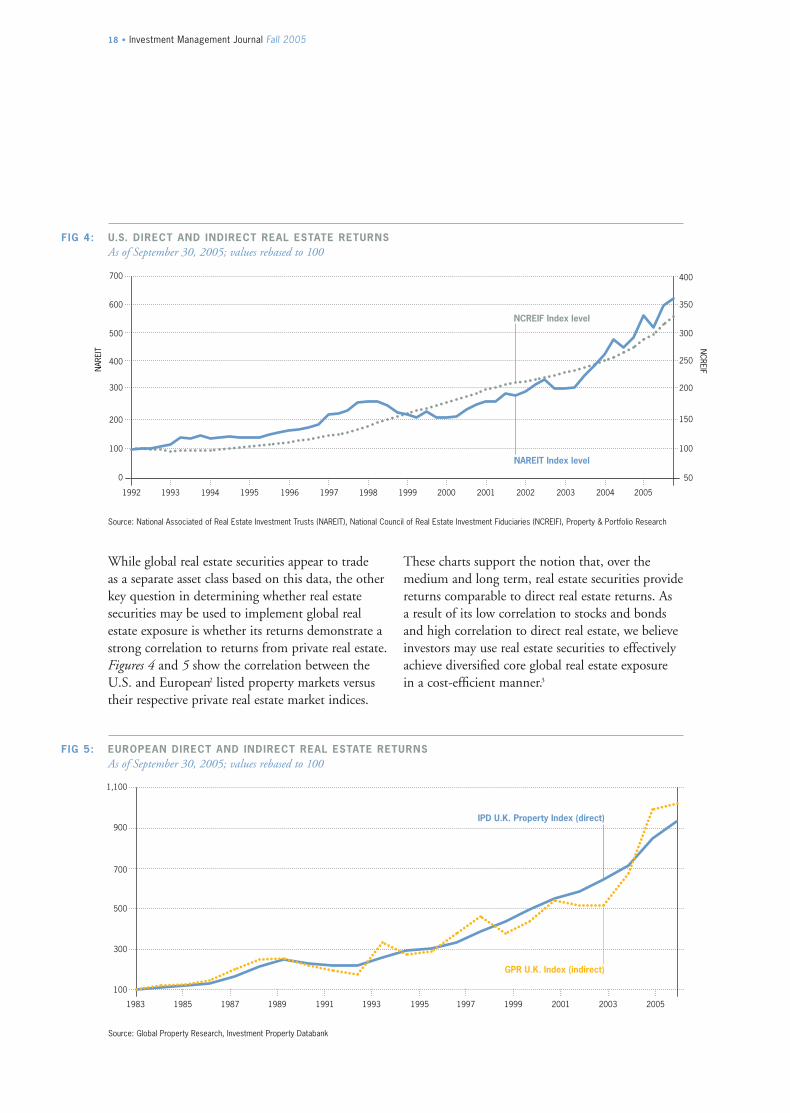

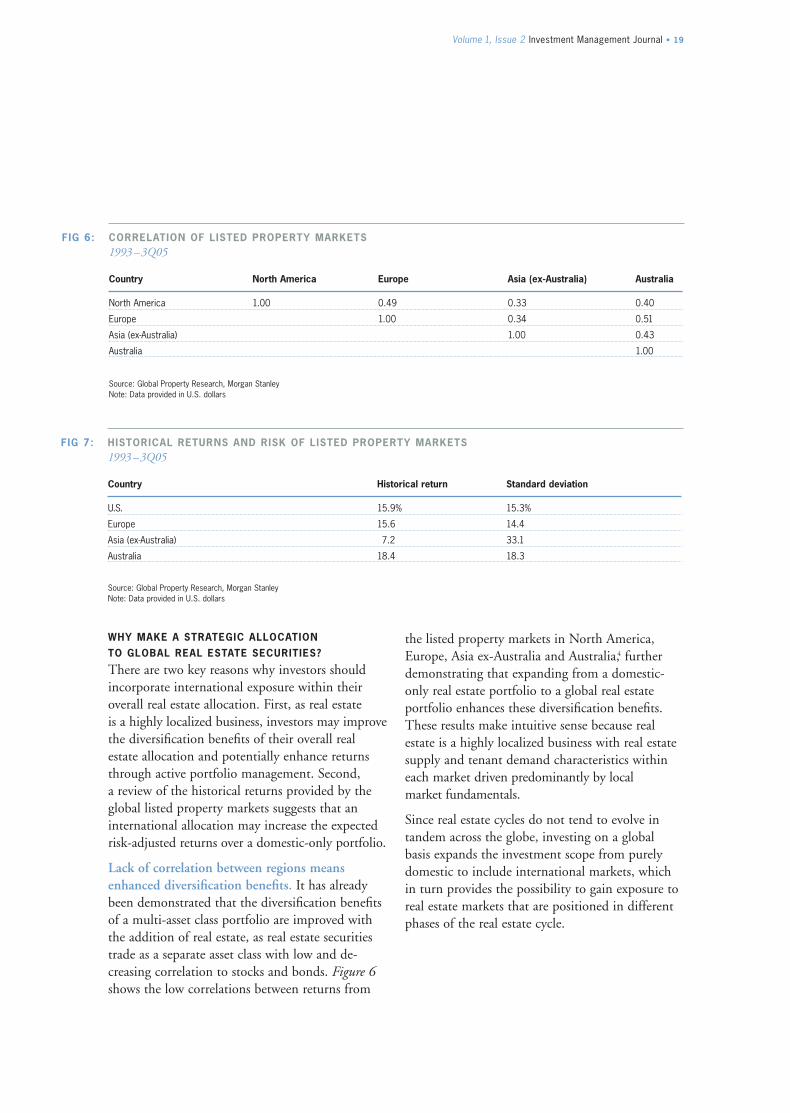

These charts support the notion that, over themedium and long term, real estate securities providereturns comparable to direct real estate returns. As a result of its low correlation to stocks and bondsand high correlation to direct real estate, we believeinvestors may use real estate securities to effectivelyachieve diversified core global real estate exposure in a cost-efficient manner.3

While global real estate securities appear to trade as a separate asset class based on this data, the otherkey question in determining whether real estatesecurities may be used to implement global realestate exposure is whether its returns demonstrate astrong correlation to returns from private real estate.Figures 4 and 5 show the correlation between theU.S. and European2 listed property markets versustheir respective private real estate market indices.

Volume 1, Issue 2 Investment Management Journal • 19

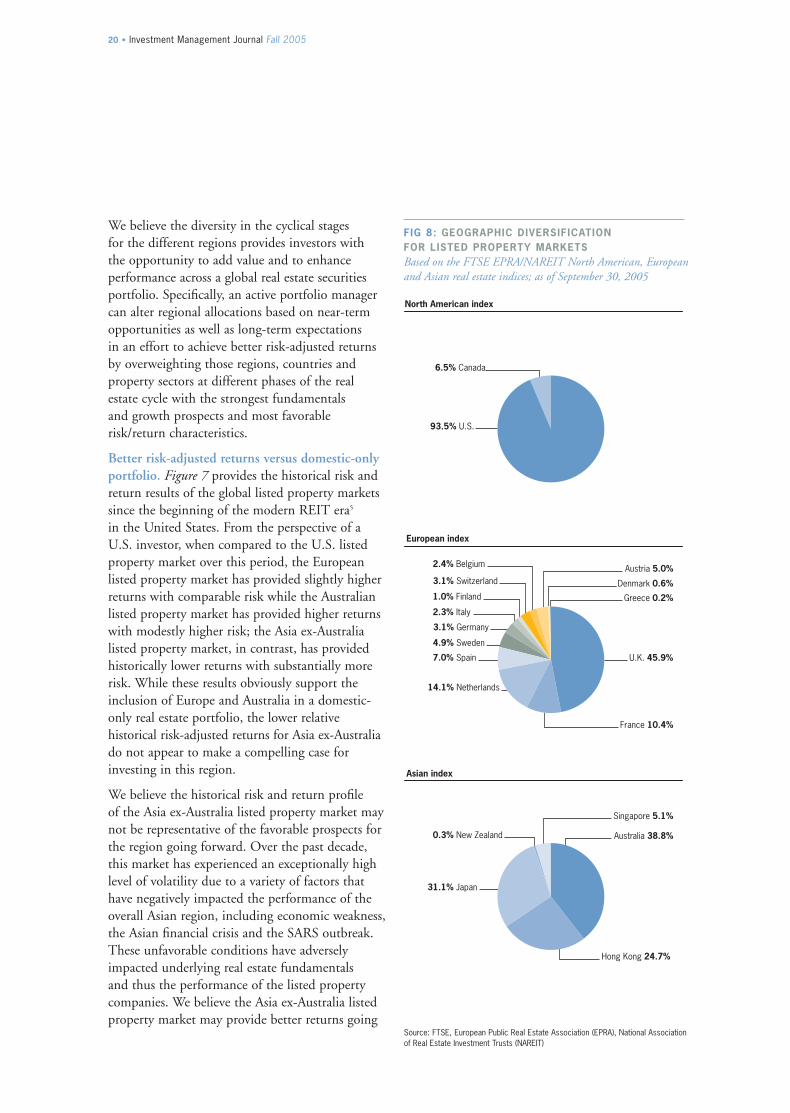

FIG 6: CORRELATION OF LISTED PROPERTY MARKETS1993 –3Q05

Country North America Europe Asia (ex-Australia) Australia

North America 1.00 0.49 0.33 0.40

Europe 1.00 0.34 0.51

Asia (ex-Australia) 1.00 0.43

Australia 1.00

Source: Global Property Research, Morgan StanleyNote: Data provided in U.S. dollars

FIG 7: HISTORICAL RETURNS AND RISK OF LISTED PROPERTY MARKETS1993 –3Q05

Country Historical return Standard deviation

U.S. 15.9% 15.3%

Europe 15.6 14.4

Asia (ex-Australia) 7.2 33.1

Australia 18.4 18.3

Source: Global Property Research, Morgan StanleyNote: Data provided in U.S. dollars

the listed property markets in North America,Europe, Asia ex-Australia and Australia,4 furtherdemonstrating that expanding from a domestic-only real estate portfolio to a global real estateportfolio enhances these diversification benefits.These results make intuitive sense because realestate is a highly localized business with real estatesupply and tenant demand characteristics withineach market driven predominantly by local market fundamentals.

Since real estate cycles do not tend to evolve intandem across the globe, investing on a global basis expands the investment scope from purelydomestic to include international markets, whichin turn provides the possibility to gain exposure toreal estate markets that are positioned in differentphases of the real estate cycle.

WHY MAKE A STRATEGIC ALLOCATION TO GLOBAL REAL ESTATE SECURITIES?

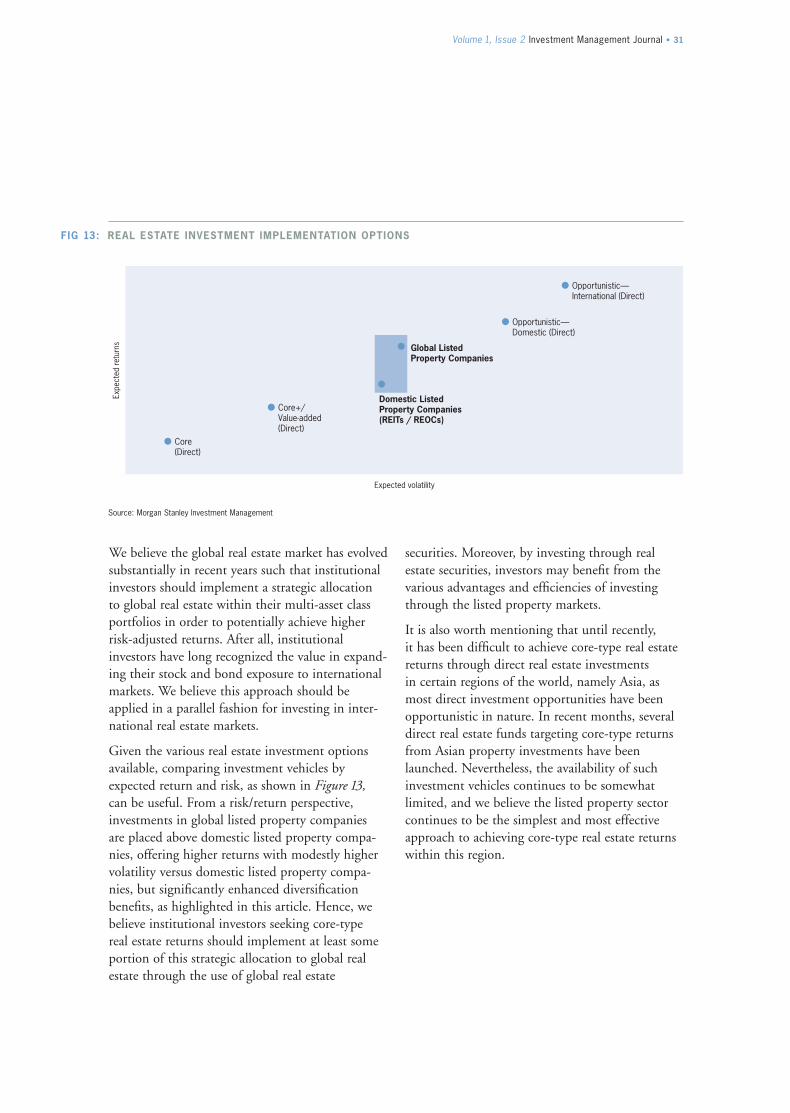

There are two key reasons why investors shouldincorporate international exposure within theiroverall real estate allocation. First, as real estate is a highly localized business, investors may improvethe diversification benefits of their overall realestate allocation and potentially enhance returnsthrough active portfolio management. Second, a review of the historical returns provided by theglobal listed property markets suggests that aninternational allocation may increase the expectedrisk-adjusted returns over a domestic-only portfolio.

Lack of correlation between regions meansenhanced diversification benefits. It has alreadybeen demonstrated that the diversification benefitsof a multi-asset class portfolio are improved withthe addition of real estate, as real estate securitiestrade as a separate asset class with low and de-creasing correlation to stocks and bonds. Figure 6shows the low correlations between returns from

We believe the diversity in the cyclical stages for the different regions provides investors with the opportunity to add value and to enhance performance across a global real estate securitiesportfolio. Specifically, an active portfolio managercan alter regional allocations based on near-termopportunities as well as long-term expectations in an effort to achieve better risk-adjusted returnsby overweighting those regions, countries andproperty sectors at different phases of the real estate cycle with the strongest fundamentals and growth prospects and most favorablerisk/return characteristics.

Better risk-adjusted returns versus domestic-onlyportfolio. Figure 7 provides the historical risk andreturn results of the global listed property marketssince the beginning of the modern REIT era5

in the United States. From the perspective of aU.S. investor, when compared to the U.S. listedproperty market over this period, the Europeanlisted property market has provided slightly higherreturns with comparable risk while the Australianlisted property market has provided higher returnswith modestly higher risk; the Asia ex-Australialisted property market, in contrast, has providedhistorically lower returns with substantially morerisk. While these results obviously support theinclusion of Europe and Australia in a domestic-only real estate portfolio, the lower relative historical risk-adjusted returns for Asia ex-Australiado not appear to make a compelling case forinvesting in this region.

We believe the historical risk and return profile of the Asia ex-Australia listed property market maynot be representative of the favorable prospects forthe region going forward. Over the past decade, this market has experienced an exceptionally highlevel of volatility due to a variety of factors thathave negatively impacted the performance of theoverall Asian region, including economic weakness,the Asian financial crisis and the SARS outbreak.These unfavorable conditions have adverselyimpacted underlying real estate fundamentals and thus the performance of the listed propertycompanies. We believe the Asia ex-Australia listedproperty market may provide better returns going

20 • Investment Management Journal Fall 2005

Singapore 5.1%

Australia 38.8%

31.1% Japan

0.3% New Zealand

Hong Kong 24.7%

Greece 0.2%

U.K. 45.9%

4.9% Sweden

7.0% Spain

2.4% Belgium

3.1% Switzerland

1.0% Finland

2.3% Italy

3.1% Germany

Denmark 0.6%

Austria 5.0%

6.5% Canada

France 10.4%

93.5% U.S.

14.1% Netherlands

North American index

European index

Asian index

FIG 8: GEOGRAPHIC DIVERSIFICATION FOR LISTED PROPERTY MARKETS Based on the FTSE EPRA/NAREIT North American, Europeanand Asian real estate indices; as of September 30, 2005

Source: FTSE, European Public Real Estate Association (EPRA), National Associationof Real Estate Investment Trusts (NAREIT)

Volume 1, Issue 2 Investment Management Journal • 21

forward with lower volatility than experienced overthe past decade due to improved real estate funda-mentals and an improved investment universe.

A LOOK AT THE GLOBAL REAL ESTATE SECURITIES INVESTMENT UNIVERSE

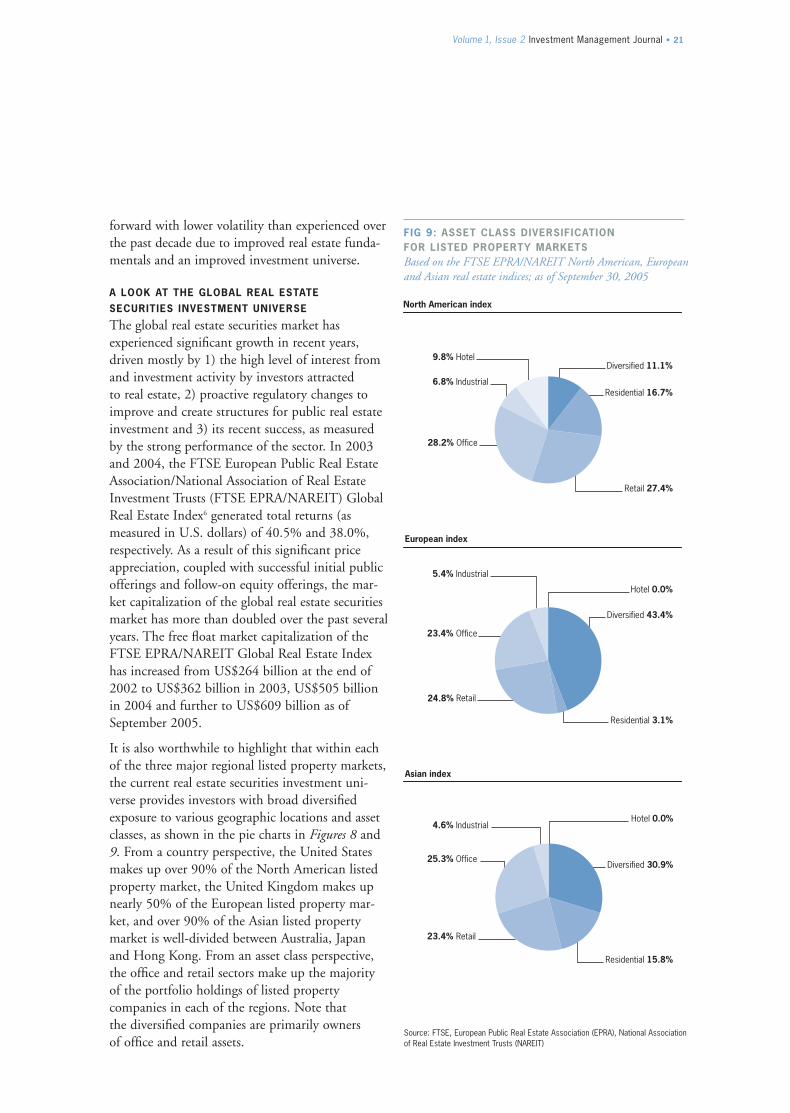

The global real estate securities market has experienced significant growth in recent years,driven mostly by 1) the high level of interest fromand investment activity by investors attracted to real estate, 2) proactive regulatory changes toimprove and create structures for public real estateinvestment and 3) its recent success, as measuredby the strong performance of the sector. In 2003and 2004, the FTSE European Public Real EstateAssociation/National Association of Real EstateInvestment Trusts (FTSE EPRA/NAREIT) GlobalReal Estate Index6 generated total returns (as measured in U.S. dollars) of 40.5% and 38.0%,respectively. As a result of this significant priceappreciation, coupled with successful initial publicofferings and follow-on equity offerings, the mar-ket capitalization of the global real estate securitiesmarket has more than doubled over the past severalyears. The free float market capitalization of theFTSE EPRA/NAREIT Global Real Estate Indexhas increased from US$264 billion at the end of2002 to US$362 billion in 2003, US$505 billionin 2004 and further to US$609 billion as ofSeptember 2005.

It is also worthwhile to highlight that within eachof the three major regional listed property markets,the current real estate securities investment uni-verse provides investors with broad diversifiedexposure to various geographic locations and assetclasses, as shown in the pie charts in Figures 8 and9. From a country perspective, the United Statesmakes up over 90% of the North American listedproperty market, the United Kingdom makes upnearly 50% of the European listed property mar-ket, and over 90% of the Asian listed propertymarket is well-divided between Australia, Japanand Hong Kong. From an asset class perspective,the office and retail sectors make up the majorityof the portfolio holdings of listed property companies in each of the regions. Note that the diversified companies are primarily owners of office and retail assets.

Hotel 0.0%

Diversified 30.9%25.3% Office

4.6% Industrial

Residential 15.8%

Diversified 43.4%

Hotel 0.0%

23.4% Office

Residential 3.1%

5.4% Industrial

9.8% HotelDiversified 11.1%

Residential 16.7%6.8% Industrial

28.2% Office

24.8% Retail

23.4% Retail

Retail 27.4%

North American index

European index

Asian index

FIG 9: ASSET CLASS DIVERSIFICATION FOR LISTED PROPERTY MARKETS Based on the FTSE EPRA/NAREIT North American, Europeanand Asian real estate indices; as of September 30, 2005

Source: FTSE, European Public Real Estate Association (EPRA), National Associationof Real Estate Investment Trusts (NAREIT)

22 • Investment Management Journal Fall 2005

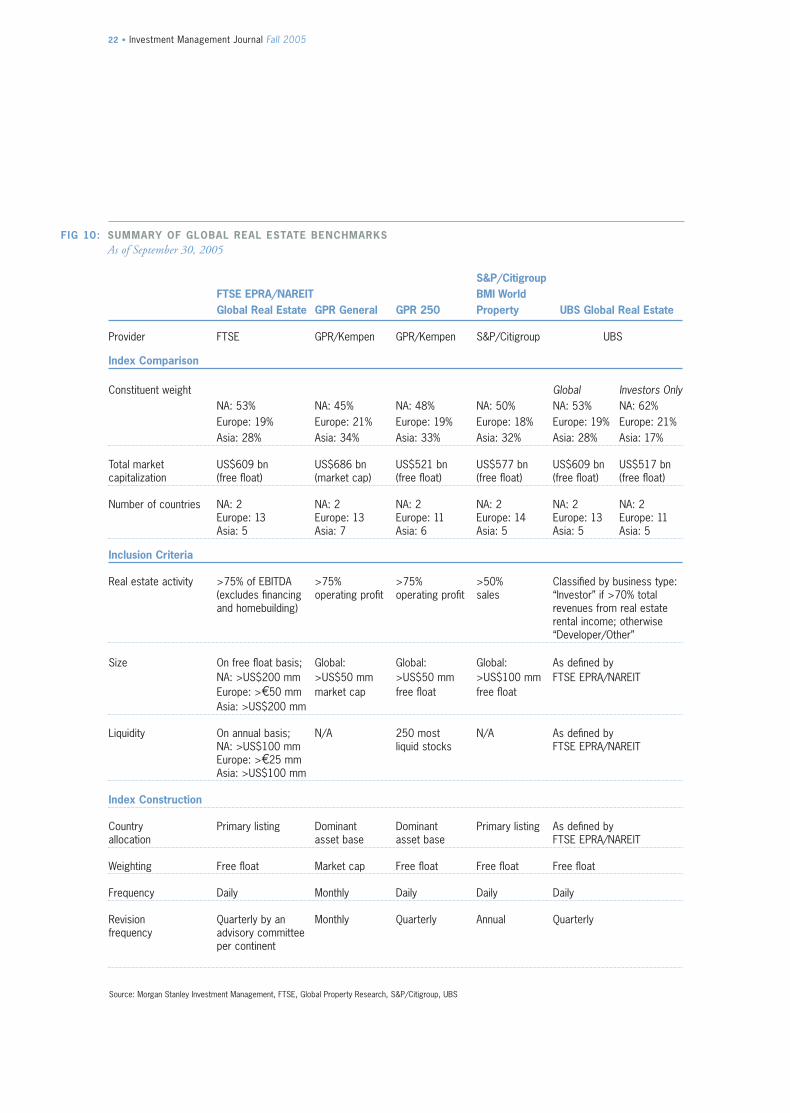

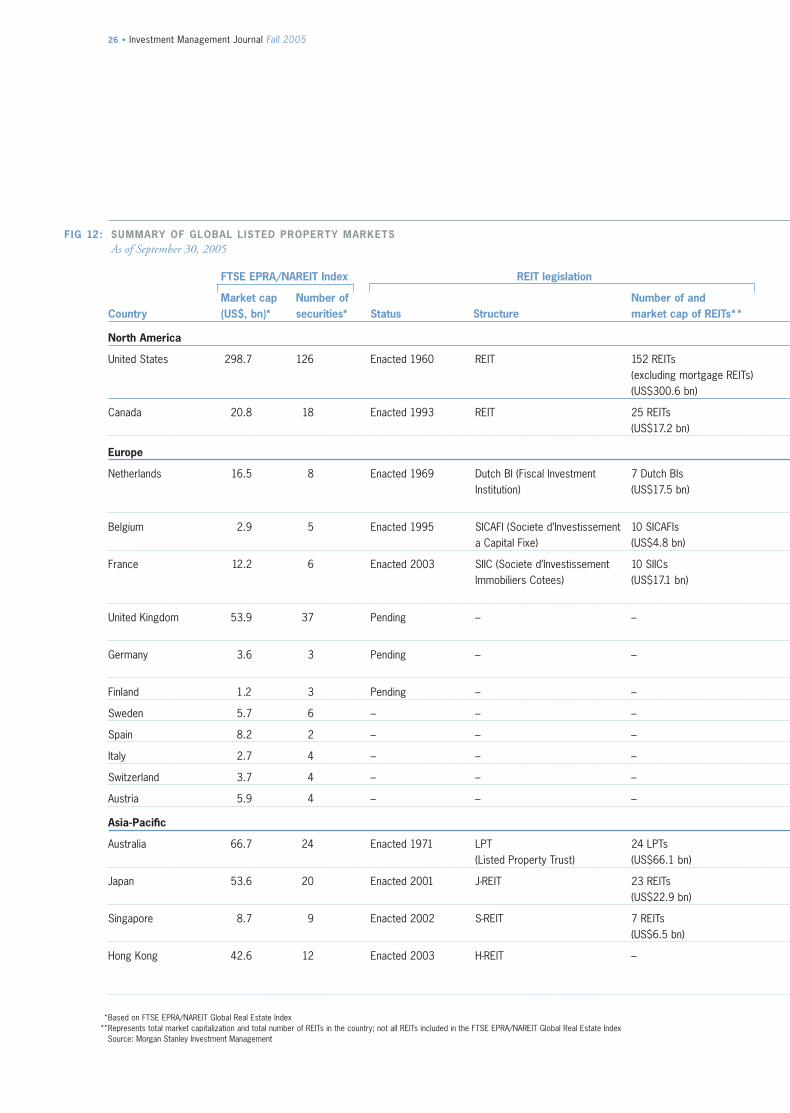

FIG 10: SUMMARY OF GLOBAL REAL ESTATE BENCHMARKSAs of September 30, 2005

S&P/CitigroupFTSE EPRA/NAREIT BMI WorldGlobal Real Estate GPR General GPR 250 Property UBS Global Real Estate

Provider FTSE GPR/Kempen GPR/Kempen S&P/Citigroup UBS

Index Comparison

Constituent weight Global Investors OnlyNA: 53% NA: 45% NA: 48% NA: 50% NA: 53% NA: 62%Europe: 19% Europe: 21% Europe: 19% Europe: 18% Europe: 19% Europe: 21%Asia: 28% Asia: 34% Asia: 33% Asia: 32% Asia: 28% Asia: 17%

Total market US$609 bn US$686 bn US$521 bn US$577 bn US$609 bn US$517 bncapitalization (free float) (market cap) (free float) (free float) (free float) (free float)

Number of countries NA: 2 NA: 2 NA: 2 NA: 2 NA: 2 NA: 2Europe: 13 Europe: 13 Europe: 11 Europe: 14 Europe: 13 Europe: 11Asia: 5 Asia: 7 Asia: 6 Asia: 5 Asia: 5 Asia: 5

Inclusion Criteria

Real estate activity >75% of EBITDA >75% >75% >50% Classified by business type:(excludes financing operating profit operating profit sales “Investor” if >70% total and homebuilding) revenues from real estate

rental income; otherwise“Developer/Other”

Size On free float basis; Global: Global: Global: As defined byNA: >US$200 mm >US$50 mm >US$50 mm >US$100 mm FTSE EPRA/NAREITEurope: >€50 mm market cap free float free floatAsia: >US$200 mm

Liquidity On annual basis; N/A 250 most N/A As defined by NA: >US$100 mm liquid stocks FTSE EPRA/NAREITEurope: >€25 mmAsia: >US$100 mm

Index Construction

Country Primary listing Dominant Dominant Primary listing As defined by allocation asset base asset base FTSE EPRA/NAREIT

Weighting Free float Market cap Free float Free float Free float

Frequency Daily Monthly Daily Daily Daily

Revision Quarterly by an Monthly Quarterly Annual Quarterlyfrequency advisory committee

per continent

Source: Morgan Stanley Investment Management, FTSE, Global Property Research, S&P/Citigroup, UBS

Volume 1, Issue 2 Investment Management Journal • 23

INVESTMENT UNIVERSE POISED TO CONTINUE TO ALLOW FOR SIGNIFICANT GROWTH

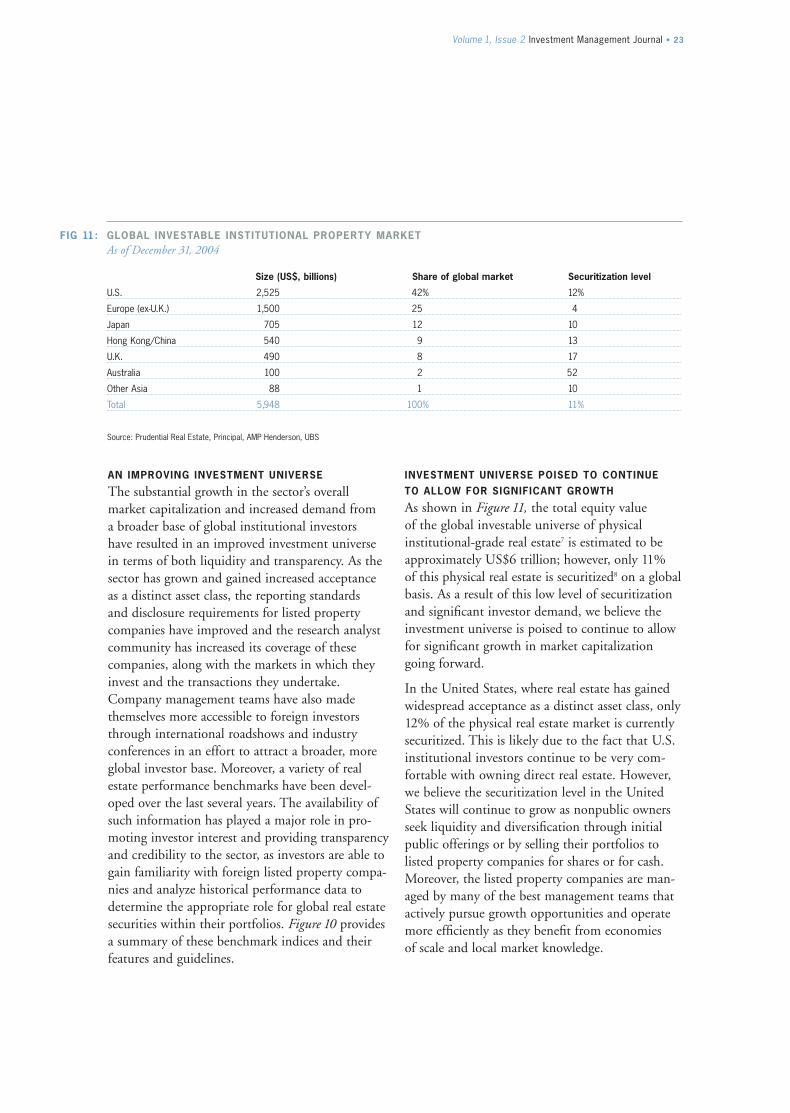

As shown in Figure 11, the total equity value of the global investable universe of physical institutional-grade real estate7 is estimated to beapproximately US$6 trillion; however, only 11% of this physical real estate is securitized8 on a globalbasis. As a result of this low level of securitizationand significant investor demand, we believe theinvestment universe is poised to continue to allowfor significant growth in market capitalizationgoing forward.

In the United States, where real estate has gainedwidespread acceptance as a distinct asset class, only12% of the physical real estate market is currentlysecuritized. This is likely due to the fact that U.S.institutional investors continue to be very com-fortable with owning direct real estate. However,we believe the securitization level in the UnitedStates will continue to grow as nonpublic ownersseek liquidity and diversification through initialpublic offerings or by selling their portfolios to listed property companies for shares or for cash.Moreover, the listed property companies are man-aged by many of the best management teams thatactively pursue growth opportunities and operatemore efficiently as they benefit from economies of scale and local market knowledge.

AN IMPROVING INVESTMENT UNIVERSE

The substantial growth in the sector’s overall market capitalization and increased demand from a broader base of global institutional investors have resulted in an improved investment universe in terms of both liquidity and transparency. As thesector has grown and gained increased acceptanceas a distinct asset class, the reporting standards and disclosure requirements for listed propertycompanies have improved and the research analystcommunity has increased its coverage of these companies, along with the markets in which theyinvest and the transactions they undertake.Company management teams have also madethemselves more accessible to foreign investorsthrough international roadshows and industry conferences in an effort to attract a broader, moreglobal investor base. Moreover, a variety of realestate performance benchmarks have been devel-oped over the last several years. The availability ofsuch information has played a major role in pro-moting investor interest and providing transparencyand credibility to the sector, as investors are able togain familiarity with foreign listed property compa-nies and analyze historical performance data todetermine the appropriate role for global real estatesecurities within their portfolios. Figure 10 providesa summary of these benchmark indices and theirfeatures and guidelines.

FIG 11: GLOBAL INVESTABLE INSTITUTIONAL PROPERTY MARKETAs of December 31, 2004

Size (US$, billions) Share of global market Securitization level

U.S. 2,525 42% 12%

Europe (ex-U.K.) 1,500 25 4

Japan 705 12 10

Hong Kong/China 540 9 13

U.K. 490 8 17

Australia 100 2 52

Other Asia 88 1 10

Total 5,948 100% 11%

Source: Prudential Real Estate, Principal, AMP Henderson, UBS

24 • Investment Management Journal Fall 2005

Introduction and development of REIT marketswill be a major catalyst for growth. One of themajor catalysts for the securitization of real estateover the last decade and in recent years has beenthe proliferation of tax-efficient real estate owner-ship structures in countries around the world. Atpresent, the three most established public REIT9

markets are in the United States, which first intro-duced real estate investment trusts in 1960, eventhough the modern REIT era did not begin untilthe early 1990s; Australia, which created listedproperty trusts, known as LPTs, in 1972; and theNetherlands, which introduced fiscal investmentinstitutions, known as Dutch BIs, in 1969. As a result of the success of these markets and in an effort to promote institutional real estate investment and remain competitive in the global financial markets, a number of countries through-out Europe and Asia have adopted or are planningto adopt legislation authorizing the creation ofREIT structures. Since 2001, France, Japan,Singapore and Hong Kong have enacted REIT legislation. In addition, the United Kingdom andGermany are actively considering the introductionof these vehicles.

CATEGORIES OF LISTED PROPERTY MARKETS IN CURRENT GLOBAL INVESTMENT UNIVERSE

In order to summarize the various types of listedproperty markets in the current global investmentuniverse, we have identified five categories of markets, with key differentiating factors beingwhether these markets are developed10 versus undeveloped, whether tax-efficient REIT owner-ship structures have been introduced, and whetherthe companies within these markets are internallyor externally managed. Figure 12 on pages 26 and 27 provides a summary of the global listedproperty markets, including the size of the variouslisted property markets, as well as which countrieshave enacted REIT legislation.

The very low level of securitization in continentalEurope is primarily due to an under-securitizedGerman listed property market. Germany is thelargest real estate market in continental Europe, but real estate is predominantly owned by Germancorporations and open-end property funds, ratherthan by listed property companies. This securitiza-tion level may increase substantially if the Germangovernment successfully introduces a tax-efficientREIT structure and provides tax incentives both for open-end funds to convert to REITs and forcorporations to sell their assets to REITs for shares.In the United Kingdom, the long-awaited intro-duction of a tax-efficient REIT structure shouldresult in a higher level of securitization, as realestate owners would be able to access tax-efficientliquidity through the U.K. REIT market ratherthan through property funds registered in the tax-efficient U.K. offshore real estate markets.

In Asia ex-Australia, the securitization of real estatehas increased significantly in recent years, primarilydue to the rapid development of REIT markets inthis region. There continues to be proactive regula-tory changes to promote the further growth of thelisted property sector. There is also a trend towardthe privatization of government-owned assets andcorporate restructurings involving the disposition of real estate assets, which should fuel the externalgrowth prospects of the listed property sector.

At the other end of the spectrum, over 50% of theAustralian physical real estate market is securitized,as real estate securities have long been accepted as a distinct asset class by Australian institutionalinvestors; in fact, the listed property sector makesup approximately 10% of its broader equity market. While the securitization of real estate inAustralia is not likely to increase substantially goingforward, we believe this high level of securitizationdemonstrates the market growth potential for theglobal listed property markets. As a result, we are optimistic with our expectations for continuedgrowth of the investable universe of global realestate securities.

Volume 1, Issue 2 Investment Management Journal • 25

to the very strong demand from domestic yield-oriented investors given Japan’s very low bondyields. More recently, the beginning of a long-awaited property market recovery has fueled thegrowth of the sector. In Singapore, there are sevenS-REITs at present, and the market capitalizationhas increased from US$260 million in 2002 toUS$7 billion as of September 2005. The rapidgrowth of the S-REIT market has been supportedby favorable government measures, including taxexemption on S-REIT distributions to individuals,the reduction of the withholding tax rate on S-REIT distributions from 20% to 10% for a five-year period, the waiver of stamp tax dutieson properties transferred into S-REITs for a five-year period and the recent increase in theleverage limit from 30% to 60% of total assets.

Despite the significant growth of the REIT markets in Japan and Singapore, however, the listed property market continues to be dominatedby REOCs.11 This is actually unsurprising given the REITs in these markets are externally managedand are therefore limited to the ownership of realestate properties. In contrast, REOCs are internally managed, are often the external managers for theseREITs, and tend to sell their more mature, stabi-lized assets into these REITs to generate proceedsto pursue higher-return opportunities. As a result,the organic growth prospects for the internallymanaged REOCs are generally far superior to that of the externally managed REITs.

The market capitalization of the Hong Kong listed property sector totaled US$43 billion as of September 2005.12 Despite enacting REIT legis-lation in 2003, however, there are currently no listed REITs due to the structure’s previously overlyrestrictive limitations on geography and leverage. Infact, the sponsor of Fortune REIT, a Hong Kongbased company that owns assets in Hong Kong,opted to list this retail REIT in Singapore ratherthan in Hong Kong due to its relatively more flexi-ble guidelines. Subsequently, in an effort to make

Developed listed property markets that offer tax-efficient structures. The first category is developed listed property markets that offer tax-efficient structures with internally managedproperty companies. This category includes thethree most established public REIT markets atpresent: the U.S. REIT market, the Australian LPT market and the Dutch BI market. The listedproperty companies within each of these marketsare internally managed, which means they are not solely ownership vehicles that pay management fees to third-party entities. Rather, these companieshave internal management teams in place to create value through internal and external growthopportunities. It is noteworthy that prior to 2004, the Australian LPTs were predominantlyexternally managed companies; however, LPTs have recently shifted towards an internally man-aged structure similar to the U.S. REIT model,whereby the externally managed trust and theexternal management entity have merged to forman internally managed trust.

Developed listed property markets that have recently introduced externally managed tax-efficient structures. The second category is developed listed property markets that haverecently introduced tax-efficient structures withexternally managed property companies, but arestill dominated by the traditional non-REIT listedproperty companies (i.e., real estate operating com-panies, or REOCs). This category includes Japan, which introduced the Japanese REIT (J-REIT) structure in 2001; Singapore, which introduced the Singapore REIT (S-REIT) structure in 2002; and Hong Kong, which introduced theHong Kong REIT (H-REIT) structure in 2003.

The market capitalization of the REIT sectors inboth Japan and Singapore has grown very rapidlysince their introduction. At present, there are 23 J-REITs in the sector, and the market capitaliza-tion has increased from US$260 million in 2001 to US$23 billion as of September 2005. The success of the J-REIT market may be attributed

26 • Investment Management Journal Fall 2005

FIG 12: SUMMARY OF GLOBAL LISTED PROPERTY MARKETSAs of September 30, 2005

FTSE EPRA/NAREIT Index REIT legislation

Market cap Number of Number of and Country (US$, bn)* securities* Status Structure market cap of REITs**

North America

United States 298.7 126 Enacted 1960 REIT 152 REITs (excluding mortgage REITs) (US$300.6 bn)

Canada 20.8 18 Enacted 1993 REIT 25 REITs (US$17.2 bn)

Europe

Netherlands 16.5 8 Enacted 1969 Dutch BI (Fiscal Investment 7 Dutch BIsInstitution) (US$17.5 bn)

Belgium 2.9 5 Enacted 1995 SICAFI (Societe d’Investissement 10 SICAFIsa Capital Fixe) (US$4.8 bn)

France 12.2 6 Enacted 2003 SIIC (Societe d’Investissement 10 SIICsImmobiliers Cotees) (US$17.1 bn)

United Kingdom 53.9 37 Pending – –

Germany 3.6 3 Pending – –

Finland 1.2 3 Pending – –

Sweden 5.7 6 – – –

Spain 8.2 2 – – –

Italy 2.7 4 – – –

Switzerland 3.7 4 – – –

Austria 5.9 4 – – –

Asia-Pacific

Australia 66.7 24 Enacted 1971 LPT 24 LPTs(Listed Property Trust) (US$66.1 bn)

Japan 53.6 20 Enacted 2001 J-REIT 23 REITs(US$22.9 bn)

Singapore 8.7 9 Enacted 2002 S-REIT 7 REITs(US$6.5 bn)

Hong Kong 42.6 12 Enacted 2003 H-REIT –